report rep 540 investors in initial public offeringsdownload.asic.gov.au/media/4431775/rep540... ·...

TRANSCRIPT

REPORT 540

Investors in initial public offerings

August 2017

About this report

This report contains our analysis of the findings from:

our inquiries with institutional investors about their approach to investing in an initial public offering (IPO), and with lead managers about the IPO process; and

qualitative research on the factors and information that retail investors rely on when investing in an IPO. This market research was conducted by Whereto Research, whose full report is attached to this document.

This report explains how we will use the findings from this project to enhance our regulation of IPOs. It explains how companies, their advisers and other market participants can help investors in IPOs.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 2

About ASIC regulatory documents

In administering legislation ASIC issues the following types of regulatory documents.

Consultation papers: seek feedback from stakeholders on matters ASIC is considering, such as proposed relief or proposed regulatory guidance.

Regulatory guides: give guidance to regulated entities by: explaining when and how ASIC will exercise specific powers under

legislation (primarily the Corporations Act) explaining how ASIC interprets the law describing the principles underlying ASIC’s approach giving practical guidance (e.g. describing the steps of a process such

as applying for a licence or giving practical examples of how regulated entities may decide to meet their obligations).

Information sheets: provide concise guidance on a specific process or compliance issue or an overview of detailed guidance.

Reports: describe ASIC compliance or relief activity or the results of a research project.

Disclaimer

This report does not constitute legal advice. We encourage you to seek your own professional advice to find out how the Corporations Act and other applicable laws apply to you, as it is your responsibility to determine your obligations.

Examples in this report are purely for illustration; they are not exhaustive and are not intended to impose or imply particular rules or requirements.

Acknowledgements

ASIC acknowledges Whereto Research’s significant contribution to our understanding of retail IPO investors. We would like to thank the many individual retail investors who agreed to be screened for participation in the market research, and the 52 retail investors and the institutional investors who gave up their time for interviews.

We also thank the Australian Shareholders’ Association and OnMarket Bookbuilds for promoting participation in the market research to retail investors.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 3

Contents Executive summary ....................................................................................... 4 A Commercial and legal context of IPOs ................................................ 9

Australia’s IPO market ............................................................................. 9 Legal framework ....................................................................................10 ASIC’s role in IPOs ................................................................................12

B Our inquiries—How institutional investors make decisions about IPOs ............................................................................................16 Background to our interviews ................................................................16 Assessment of IPO investment opportunities ........................................17 Information that is important to institutional investors ...........................22

C Market research—How retail investors make decisions about IPOs .......................................................................................................26 Background to the market research ......................................................26 Summary of the market research findings .............................................28 Types and sources of information .........................................................30

D Our analysis—How behavioural factors can affect retail investors’ decisions about IPOs ........................................................37 A brief introduction to behavioural economics .......................................37 Behavioural analysis in the market research .........................................37 How behavioural biases affect investment decisions ............................38 Potential behavioural factors identified in the market research .............38

E Impact of findings on ASIC’s approach to IPOs ...............................44 Summary of our key findings and proposed approach to IPOs .............44

Appendix: Accessible versions of figures ................................................52 Key terms .....................................................................................................53 Related information .....................................................................................56

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 4

Executive summary

Key points

Institutional investors rely heavily on prospectuses when assessing an IPO. Market research showed that retail investors are influenced by a broader range of sources, including analysis provided by financial commentators.

The findings from this project will influence how ASIC regulates IPOs in the future.

1 Initial public offerings (IPOs) are an important part of Australia’s capital markets. Investors need to be able to make informed decisions about IPOs to ensure that capital is invested efficiently. For companies to continue raising capital efficiently, it is important that investors have confidence in the regulation of IPOs. IPO disclosure also plays an important role in ensuring that informed secondary trading occurs once the company is listed.

2 ASIC aims to support confidence in our capital markets by closely regulating IPOs. We review a significant proportion of prospectuses and often obtain corrective disclosure if the prospectus appears to be deficient: see Section A. We also provide extensive guidance for companies and their advisers on how IPOs should be conducted.

3 We can improve our regulation of IPOs if we have an understanding of the current factors and types of information that investors rely on when investing in IPOs. The project discussed in this report looked at the information and factors that influence institutional investors and retail investors in IPOs.

How institutional investors make decisions about IPOs

4 In late 2016, we conducted several interviews with large institutional investors and other financial intermediaries that play a significant role in Australian IPOs. Institutional investors comprise the bulk of IPO investment and often help determine the pricing. Many retail investors have an indirect exposure to IPOs through institutional investors, including through their superannuation.

5 Our inquiries were intended to give us an overview of the IPO process from the perspective of institutional investors, and to gain insights into how they make their investment decisions.

6 Institutional investors said they valued the prospectus because it was the main source of information on an IPO, and it was a regulated document for which directors and others involved in the offer had liability. They felt this added weight to the credibility and reliability of the document. Institutional

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 5

investors involved in the preparation of prospectuses said ASIC’s close regulation of prospectuses improved the quality of disclosure.

7 Access to the IPO issuer’s management and the institution’s own technical analysis of the offer were also very influential.

8 The results of our inquiries with institutional investors are explained in more detail in Section B.

How retail investors make decisions about IPOs

9 We also commissioned qualitative research on the information and factors that influence retail investors when assessing an IPO. This research complements our study in 2016 of the ways in which IPOs were marketed to investors: see Report 494 Marketing practices in initial public offerings of securities (REP 494).

10 Whereto Research conducted qualitative research over a three-month period from late 2016 to early 2017. The market research involved interviews and group discussions with 52 retail investors located in Sydney, Melbourne, Brisbane and Perth who had recently considered or invested in an IPO.

11 Qualitative research of this type provides depth of understanding but, because of the limited sample size, the findings may not be representative of the total IPO population: see paragraph 131.

Note: See paragraphs 125–126 for an explanation of our classification of ‘retail investor’ for the purposes of the market research. See also the ‘Key terms’ for the meaning of ‘retail investor’, ‘sophisticated investor’, ‘professional investor’ and ‘institutional investor’ in this report.

12 Whereto Research examined the relative importance that retail investors said they placed on the prospectus, compared with the role of financial intermediaries (e.g. brokers) and other sources of investment information (e.g. social media). In general, retail investors valued information that they perceived to be independent and easy to understand, and that had been prepared by someone they perceived as having a high level of expertise.

13 The financial media, including mainstream media and subscription services, were influential in both alerting retail investors to potential IPOs and in influencing the decision-making process. The prospectus was seen as a key source of information, although many retail investors said the document was hard to read and could not be relied on to tell the whole truth about an IPO (given that it was perceived to be a marketing document).

14 The findings from the market research are discussed in more detail in Section C.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 6

How behavioural factors affect retail investors’ investment decisions

15 We conducted our own behavioural analysis of Whereto Research’s qualitative market research findings.

Note: In this report, we use the term ‘market research’ to refer to the third-party qualitative research conducted by Whereto Research.

16 Behavioural economics describes how and why people think and behave in certain ways. It draws from research across a number of social sciences, including economics, psychology, and decision science.

17 Our analysis shows that the market research identified a number of potential behavioural factors that may influence a retail investor’s IPO investment decision. Section D details our behavioural analysis.

Impact of findings on ASIC’s approach to IPOs

18 ASIC’s main focus with regulating IPOs is to ensure that investors have sufficient information to make informed decisions. The legislation regulating IPO disclosure is predicated on retail investor participation. We also seek to ensure that the sector meets the needs of institutional investors because of the important role they play in IPOs.

19 Our perception of how institutional investors and retail investors assess an IPO is summarised in Table 1.

Table 1: Comparison of institutional and retail investors’ approach to investing in IPOs

Institutional investors Retail investors

Institutional investors rely on the pathfinder prospectus and the lodged prospectus because: these are the main sources of information on an

IPO offer; directors and others have potential liability for the

prospectus disclosure; and there is regulatory oversight of the prospectus lodged

with ASIC.

However, institutional investors also seek out other sources of information about the IPO.

Retail investors read the prospectus but find it challenging.

There is a perception that the prospectus, at least in part, is a marketing document and therefore does not provide the whole picture.

Institutional investors said that questioning the issuer’s management was an essential part of their investment process.

Management is considered important, and retail investors want more information about the issuing company’s management.

The institution’s own technical analysis is important to assess the value of the offer.

Retail investors value ‘independent’ analysis, but their access may be limited to informal sources such as the media or online investor forums.

Institutional investors are sceptical of information if there is a conflict of interest.

Some retail investors do not trust brokers because of perceived conflicts of interest.

Note: The institutional investor findings are based on ASIC’s informal meetings with institutional investors, while the retail investor findings are based on the third-party market research conducted by Whereto Research.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 7

20 The findings from our discussions with institutional investors, and the market research, have improved our understanding of how investors participate in IPOs. Based on these findings, we believe that ASIC’s regulation of IPOs is largely sound. We propose to enhance our approach only in relatively minor ways, as explained below and in Section E.

Prospectus

21 We consider that high-quality prospectuses are important for investors’ decision making about IPOs. They also form the basis for a listed company’s future continuous disclosure obligations.

22 Further, the Corporations Act contains a number of disclosure exemptions for post-IPO fundraising by listed companies. These exemptions operate on the premise that the company’s initial disclosure in the prospectus, combined with continuous and periodic disclosure, provide sufficient information for investors. In this way, prospectuses have a central role in ensuring Australia’s capital markets are fair and efficient.

23 This project confirmed that the prospectus is a key document for institutional investors, partly because of the role that ASIC plays in IPOs. We will continue to review a significant proportion of prospectuses to help ensure they are reliable documents. We will focus on the sections that are of most importance to institutional investors, such as the risk section and the financial information section.

24 It is likely that prospectuses will always be challenging documents for less experienced retail investors to read and understand. There are constraints on making prospectuses shorter documents because they need to cater to institutional investors. The issuer, its directors and any underwriter also have potential liability for the disclosure, including material omissions.

25 However, within these constraints, we consider that the market research shows that there is significant scope for improving the effectiveness of prospectuses for retail investors. In fact, the Corporations Act requires the prospectus to be ‘clear, concise and effective’ for retail investors: s715A.

Other sources of information

26 The market research found that retail investors use a variety of information to assess an IPO, and there are a number of factors other than the prospectus that influence their investment decision. We will therefore increase our monitoring of the wide variety of sources of information available to retail investors about IPOs. These include investment newsletters, magazines and subscription services dedicated to investing.

27 Table 2 provides a summary of our key messages for companies based on our interpretation of the market research findings. The market research

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 8

findings, and our inquiries with institutional investors, reinforced the relevance of our guidance in Regulatory Guide 228 Prospectuses: Effective disclosure for retail investors (RG 228).

Table 2: Summary of ASIC’s key messages for companies

Communication style The market research showed that retail investors were likely to dismiss the prospectus if it was too hard to read, and rely on other sources of information. A good investment overview is essential for helping retail investors.

Sections B and C of RG 228 contain extensive guidance on how to make prospectuses more effective disclosure documents.

Management A number of retail investors said they wanted more information on the issuing company’s management—its track record and what skills executives had to contribute (which may need to be explained).

Retail investors said that, if they found out from other sources that an executive had been involved with a failed business, and this was not explained in the prospectus, this could be a powerful disincentive to invest.

Section G of RG 228 contains guidance on disclosure about management.

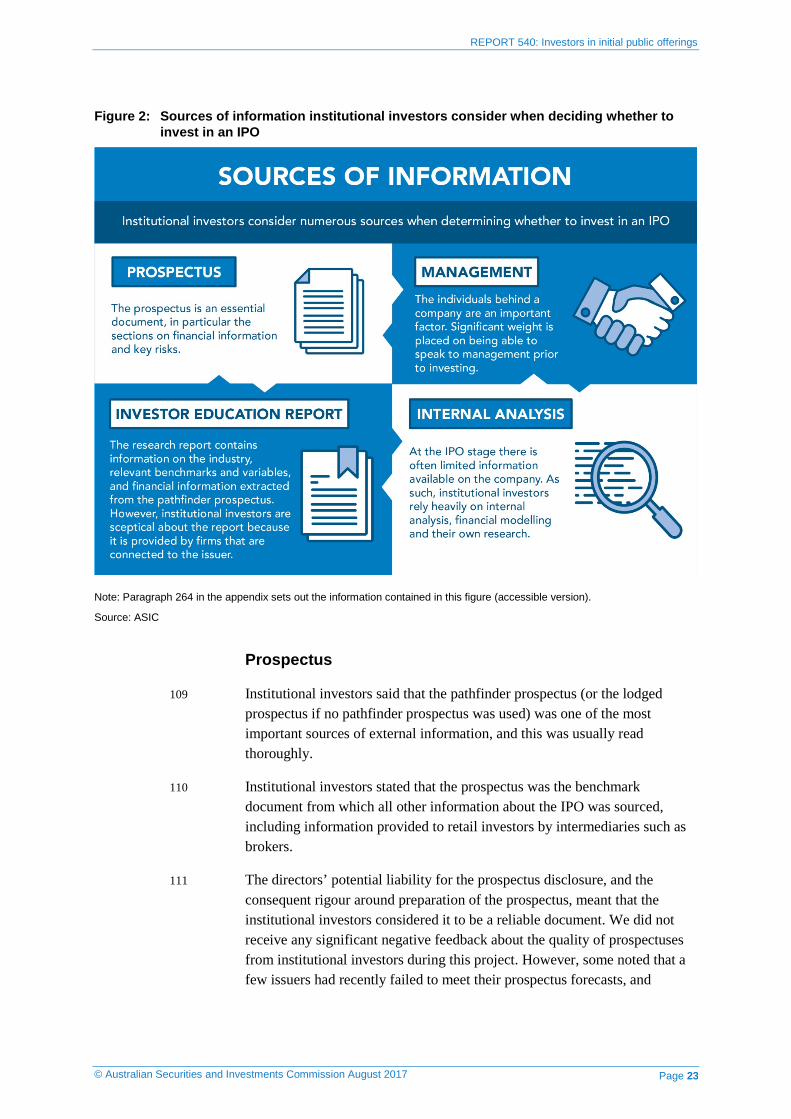

Issuers and their advisers should consider ways to improve retail investors’ access to information on the issuer’s management—for example, by making IPO roadshow sessions available online for retail investors after the prospectus is lodged.

Risk disclosure Disclosure about risks must be specific to the issuing company. Retail investors are frustrated with risk disclosure that looks like it has been copied directly from another prospectus.

Section E of RG 228—in particular, paragraphs 78–82—contains guidance on disclosing specific risks.

Financial information The investment overview should include a plain English explanation of the key relevant financial data for less financially capable investors.

Issuers should ensure the financial note disclosure in the financial information section contains sufficient information for more financially capable investors.

Disclosure of assumptions underlying any forecasts is also important: Regulatory Guide 170 Prospective financial information (RG 170).

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 9

A Commercial and legal context of IPOs

Key points

The Australian disclosure-based regime assists investors to assess the risks associated with IPOs and to make informed investment decisions.

The Corporations Act imposes strict limits on the advertising and publicity that can take place before and during an IPO, with the aim that investors make decisions based on disclosure in the prospectus.

ASIC has a broad role in the regulation and oversight of IPOs. We may:

• review prospectuses that are lodged with ASIC;

• monitor advertising and publicity about an IPO;

• conduct surveillances;

• request changes to prospectuses and advertising;

• impose a stop order if a prospectus or advertising contains misleadingor deceptive information; and

• take enforcement action.

We have published extensive guidance to help companies conducting IPOs.

Australia’s IPO market

28 Australia has an active IPO market. In 2016 (12 months), 571 disclosure documents were lodged with ASIC—112 of which were IPO prospectuses. Consistent with 2016, 210 disclosure documents have been lodged with ASIC in the first half of 2017 (six months)—60 of which were IPO prospectuses.

Note: We regularly publish corporate finance reports, which outline the level of activity in the public fundraising market: see Report 539 ASIC regulation of corporate finance: January to June 2017 (REP 539).

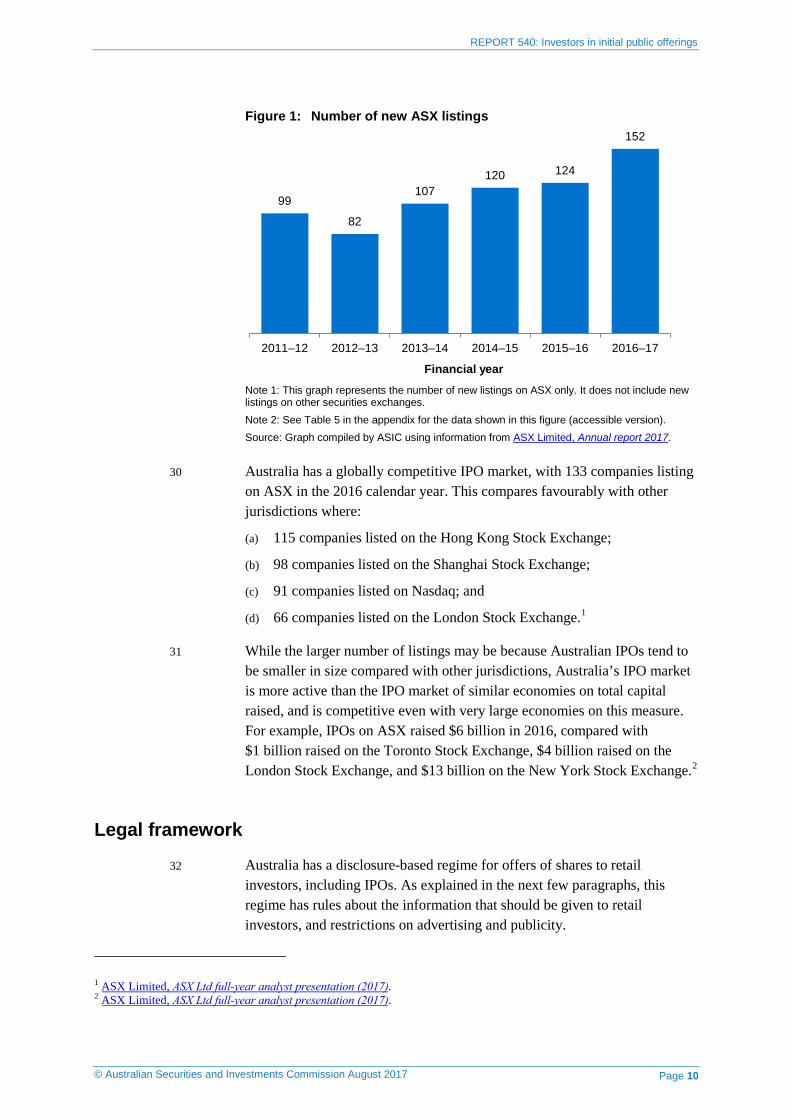

29 The number of new listings on ASX has also increased since the 2012–13 financial year: see Figure 1.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 10

Figure 1: Number of new ASX listings

99

82

107120 124

152

2011–12 2012–13 2013–14 2014–15 2015–16 2016–17

Financial yearNote 1: This graph represents the number of new listings on ASX only. It does not include new listings on other securities exchanges. Note 2: See Table 5 in the appendix for the data shown in this figure (accessible version). Source: Graph compiled by ASIC using information from ASX Limited, Annual report 2017.

30 Australia has a globally competitive IPO market, with 133 companies listing on ASX in the 2016 calendar year. This compares favourably with other jurisdictions where:

(a) 115 companies listed on the Hong Kong Stock Exchange;

(b) 98 companies listed on the Shanghai Stock Exchange;

(c) 91 companies listed on Nasdaq; and

(d) 66 companies listed on the London Stock Exchange.1

31 While the larger number of listings may be because Australian IPOs tend to be smaller in size compared with other jurisdictions, Australia’s IPO market is more active than the IPO market of similar economies on total capital raised, and is competitive even with very large economies on this measure. For example, IPOs on ASX raised $6 billion in 2016, compared with $1 billion raised on the Toronto Stock Exchange, $4 billion raised on the London Stock Exchange, and $13 billion on the New York Stock Exchange.2

Legal framework

32 Australia has a disclosure-based regime for offers of shares to retail investors, including IPOs. As explained in the next few paragraphs, this regime has rules about the information that should be given to retail investors, and restrictions on advertising and publicity.

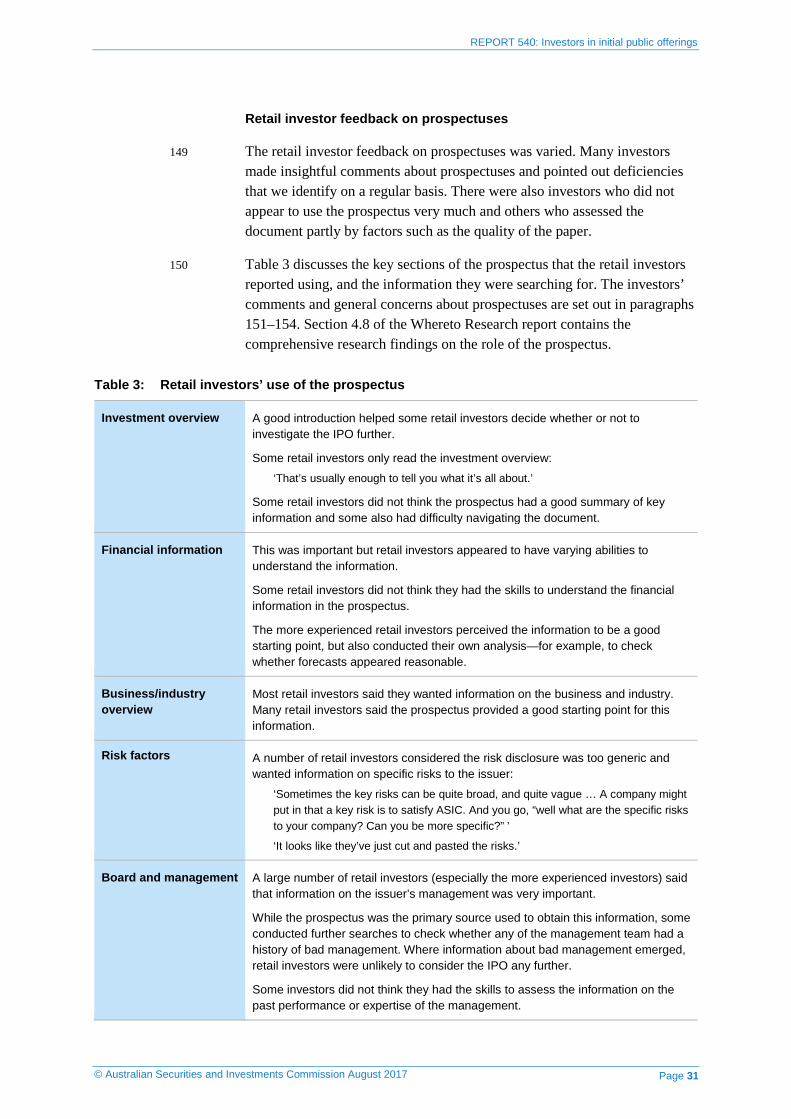

1 ASX Limited, ASX Ltd full-year analyst presentation (2017).2 ASX Limited, ASX Ltd full-year analyst presentation (2017).

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 11

33 A disclosure-based regime does not pre-judge the merits of an offer. It aims to give retail investors and their advisers sufficient information to make their own investment decisions: see RG 228.

34 Australia is not alone in adopting a disclosure-based regime. A similar approach is used in many jurisdictions. The US Securities and Exchange Commission (SEC) recently confirmed its commitment to disclosure:

By arming investors with information, they can evaluate and make investment decisions that support more accurate valuations of securities and more efficient allocation of capital.3

Advertising and publicity restrictions

35 The Corporations Act imposes strict limits on the advertising that can take place before a prospectus is lodged with ASIC: see s734(2). Only ‘tombstone’ advertising, which contains very basic information about an upcoming IPO, is permitted before lodgement: s734(5). These provisions aim to ensure that retail investors are not significantly influenced by marketing before they have a chance to review the prospectus.

Note: Broader exceptions are available for pre-prospectus material provided to sophisticated and professional investors: see s734(9) and ASIC Corporations (Market Research and Roadshows) Instrument 2016/79.

36 After the prospectus is lodged, any advertising or promotion of an IPO must still:

(a) refer to the prospectus;

(b) explain how the prospectus can be obtained;

(c) recommend that investors consider the prospectus when deciding whether to acquire the securities; and

(d) state that anyone who wants to acquire the securities will need to complete the application form (in or accompanying the prospectus): s734(6).

37 The advertising prohibition in s734(2) does not restrict independent reports on IPOs, as long as they are not published at the instigation of the issuer or someone connected with the offer, and no payment is given for their publication: s734(7).

38 Therefore, in the lead-up to an IPO and during the offer period, retail investors may receive information about an IPO from various sources. This includes information from brokers, financial media, and research analyst reports.

3 SEC, Remarks at the ‘SEC Speaks’ conference 2017: Remembering the forgotten investor, speech, 24 February 2017.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 12

39 If the information comes from the issuer or someone connected with the offer, s734 should ensure that investors are alerted to the importance of the prospectus, and also the need to complete the application form attached to the prospectus.

40 For an explanation of how participants in the market research accessed information on IPOs, see Section C—in particular, paragraphs 137–139.

41 For detailed information about the IPO investment process from the perspective of institutional investors, see Section B.

Disclosure requirements

42 An IPO that involves an offer of securities to retail investors in Australia requires a prospectus to be prepared and lodged with ASIC.

43 The prospectus must contain all the information that investors and their professional advisers would reasonably require to make an informed decision about the IPO. This includes an assessment of:

(a) the rights and liabilities attaching to the securities offered; and

(b) the assets and liabilities, financial position and performance, profits and losses, and prospects of the body that is to issue the securities: s710.

Note: The prospectus must contain this information only to the extent to which it is reasonable for investors and their professional advisers to expect to find that information in the prospectus: s710(1)(a). The Corporations Act also requires other specific information to be included in the prospectus: s711 and 716.

44 Offers to institutional investors do not require a prospectus on the basis that they do not require the same level of regulatory protection as retail investors. However, IPOs of securities that will be quoted on ASX are made under a prospectus as a result of ASX listing requirements, and the fact that the Corporations Act would otherwise restrict public trading of the securities: see s707. Disclosure in the IPO prospectus is important for informed secondary trading, and forms the basis for a listed company’s future continuous disclosure obligations.

ASIC’s role in IPOs

Our guidance on IPOs

45 We have published extensive guidance to help companies and their advisers conducting IPOs. Regulatory Guide 254 Offering securities under a disclosure document (RG 254) explains the procedural requirements for an IPO and how ASIC will exercise our specific powers under the Corporations Act. RG 228 explains how to prepare a prospectus that contains information

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 13

required by s710 of the Corporations Act and comply with the ‘clear, concise and effective’ requirement in s715A. Recently, we updated RG 228 to clarify the disclosure requirements for historical financial information.

46 We also communicate regularly with advisers on current fundraising issues at our Corporate Finance Liaison meetings and through publications such as our corporate finance reports.

Review of prospectuses after lodgement

47 In some overseas jurisdictions, regulators review all prospectuses, and often require that changes are made before the document can be registered. This can be a very lengthy process. This is not the case in Australia, where the requirement for ASIC to review and then register all prospectuses was removed many years ago, making the fundraising process more efficient for issuers.

48 While ASIC does not review prospectuses before they are available to retail investors, we do scrutinise a significant proportion of them after lodgement. In some instances, we conduct surveillances—including surveillances on whether proper procedures have been followed in preparing the prospectus (due diligence surveillance): see Report 484 Due diligence practices in initial public offerings (REP 484).

49 Section L of Regulatory Guide 254 contains information on the approach we take to reviewing prospectuses, and the powers we have under the Corporations Act to extend the exposure period, obtain corrective disclosure in the form of a replacement or supplementary prospectus, and impose stop orders.

50 We use these powers regularly. For example, in relation to prospectuses lodged with ASIC:

(a) in 2016 (12 months), we:

(i) extended the exposure period 78 times;

(ii) obtained corrective disclosure (other than under a stop order) 134 times;

(iii) issued 56 interim stop orders; and

(iv) issued five final stop orders; and

(b) in the first half of 2017 (six months), we:

(i) extended the exposure period 34 times;

(ii) obtained corrective disclosure (other than under a stop order) 63 times;

(iii) issued 14 interim stop orders; and

(iv) issued one final stop order.

Note: These figures include prospectuses that were lodged in relation to non-IPO offers.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 14

51 We also recently took action against Sino Australia Oil and Gas Ltd (Sino Australia), including in relation to the IPO prospectus containing misleading and deceptive statements. On 8 December 2016, the Federal Court of Australia ordered that:

(a) Sino Australia pay a penalty of $800,000;

(b) former chairman Tianpeng Shao be disqualified from managing corporations for 20 years; and

(c) Mr Shao pay compensation to Sino Australia of $5,539,758 (being the company’s estimated liability to shareholders).

Note: For further details, see Media Release (16-431MR) Court fines Sino Australia Oil and Gas Limited and disqualifies former chairman, Tianpeng Shao (9 December 2016).

Marketing practices in IPOs

52 If we decide to review a prospectus, we also monitor advertising of the offer. Section J of RG 254 sets out the factors that we take into account when determining whether to take action in relation to advertising.

53 We have noticed a trend where issuers or their advisers fail to correct advertising to make it consistent with changes we have required to be made to their prospectus. For example, we may require an issuing company to remove a misleading forecast from the prospectus but references to the forecast remain in various forms of marketing.

54 In the first half of 2016, we monitored a small sample of IPO prospectuses, and requested advertising to be removed or corrected in over 20% of the offers. We also have a stop order power over advertising if necessary.

Study on marketing practices

55 In 2016, we conducted a study on the way that IPOs were marketed to investors over a six-week period, and published a report of our findings: see REP 494.

56 We found that brokers primarily used traditional marketing methods, such as telephone calls, emails and professional investor roadshows. ‘Investor education’ reports were also distributed within an issuer’s adviser networks, and to sophisticated or professional investors. Only small-to-medium brokers tended to use more innovative methods, such as social media and online investor forums.

57 REP 494 concluded that most firms were using acceptable marketing practices. Our main recommendation for traditional marketing focused on better compliance oversight of telephone calls, such as the use of standardised telephone scripts. We also recommended that firms take more

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 15

measures to ensure that institutional roadshows were restricted to Australian financial services (AFS) licensees.

58 We had more concerns relating to innovative marketing methods. In particular, our review of media coverage indicated that some issuers and their advisers may be providing information to the media before the prospectus was lodged with ASIC.

59 We also noticed that some posts on investor forums appeared to have originated from someone involved in the IPO, and that the messages were not balanced. There were also failures to ensure that videos and other multimedia were accurate and consistent with the disclosure in the prospectus.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 16

B Our inquiries—How institutional investors make decisions about IPOs

Key points

We conducted interviews with institutional investors to explore what influences them when they are deciding whether to invest in an IPO.

We found that, when assessing an IPO, institutional investors:

• considered the prospectus (or pathfinder prospectus), meetings with management, and internal analysis to be the most important sources of information; and

• placed less weight on investor education reports provided by research analysts.

Background to our interviews

60 Institutional investors are integral to the functioning of Australia’s IPO market. They comprise the bulk of IPO investment and often their views help determine the price of the offer—either through a formal bookbuild process or by more informally indicating whether they are prepared to invest at the suggested price during the roadshow.

Note: See the ‘Key terms’ for the meaning of ‘bookbuild’ and ‘roadshow’.

61 Many larger IPOs do not have a retail public offer and it is likely that many retail investors’ main exposure to IPOs is indirectly through their investments managed by financial institutions.

62 Given their involvement in the IPO investment process, we sought input from a range of institutional investors. In late 2016, we conducted interviews with a selection of institutional investors about how they assess IPOs. The interviews were conducted on a voluntary basis.

63 We sought to understand the institutions’ decision-making process, and gain insight into the relative importance of different information sources. We were also interested to understand the different approach taken to the decision-making process by institutional investors in comparison with retail investors: see Table 1.

Note: Our interviews with institutional investors were conducted by ASIC officers experienced in regulating IPOs. This differed from the market research that we commissioned on retail investors, which was conducted by a professional market researcher.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 17

64 While we conducted a behavioural analysis of the market research findings (see Section D), we did not conduct a behavioural analysis of the feedback we received from institutional investors because this was acquired through informal interviews. This lack of formal analysis does not suggest that institutional investors’ decisions were not affected by behavioural biases.

65 The institutional investors we selected were managers of retail and wholesale investment funds and listed investment companies. They included both large and smaller institutions, and each had one or more actively managed investment offerings focusing on Australian equities (as opposed to passive, index-tracking funds or mixed asset class funds). Some focused on a particular subset of Australian equities, such as issuers with smaller capitalisations, while others offered a range of Australian equities funds with different kinds of mandates.

66 We also spoke to a selection of financial intermediaries who act as lead managers on both large and small IPOs. Lead managers play an important role in IPOs because they usually have the primary responsibility for coordinating the IPO process on behalf of the issuer.

67 The lead manager’s role normally includes advising on the structuring of the offer, including timing, price and size. They also advise on and conduct marketing of the offer, including the coordination of investor roadshows. Lead managers can, but do not always, act as the underwriter to the offer.

68 Our conversations with these institutional investors and lead managers confirmed our understanding of the IPO process from the perspective of an institutional investor, and allowed us to understand the various sources of information used by institutional investors when making their investment decision.

69 This section outlines the investment process for institutional investors, and the information they said they considered when deciding whether to invest in an IPO.

Assessment of IPO investment opportunities

70 The institutional investors we spoke to said they generally considered all IPO opportunities within their mandate even if they did not ultimately invest.

71 They told us that they generally avoided speculative IPOs, including mining exploration companies and technology start-up companies. They were also cautious about investing in emerging market issuers (where the reason for listing in Australia was unclear, or they operated in a risky jurisdiction) and private equity sell-downs (where the timing or rationale was unclear).

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 18

Sources of information

72 The institutional investors reported that they used a range of information sources when determining whether to invest in an IPO. The relative importance of these sources is discussed in paragraphs 106–122.

Non-deal roadshow

73 The first time an institutional investor meets with a company that is considering an IPO may be through a ‘non-deal’ roadshow. We received feedback that non-deal roadshows were more common for larger IPOs because institutional investor support was critical for the success of the offer.

74 Sometimes, when a company is considering whether to proceed to an IPO, a non-deal roadshow will be used to:

(a) introduce the company’s management to potential institutional investors, and give those investors an understanding of the business and industry; and

(b) give the company and its advisers an indication of the level of investor interest in the company, and help determine whether it is the right time to conduct an IPO.

75 No securities are offered for sale at this time. The non-deal roadshow is normally organised by the adviser firm who will often go on to play a role in managing the IPO if the company decides to proceed.

76 Documents provided to institutional investors at a non-deal roadshow usually contain only a high-level overview of the issuer’s business and the industry it operates in. Historical benchmarks and industry comparables may be provided. The issuer’s full historical financial statements and forecast financial information are not provided at this time.

77 We were told that sometimes a research analyst connected with the issuer’s adviser would be involved in a non-deal roadshow, but this involvement was limited to giving information about the industry and relevant benchmarks.

78 Sometimes institutional investors are not allowed to keep any materials handed out during a non-deal roadshow. We were told that this practice was designed to reduce investor reliance on roadshow materials, and instead focus attention on the prospectus when it was later released.

Initial analyst meetings—‘Investor education’

79 After it is decided that an IPO will proceed, and the lead manager’s firm has a research analyst who is covering the issuer’s shares, the firm managing the issue will invite some of its institutional clients to participate in ‘investor education’.

REPORT 540: Investors in initial public offerings

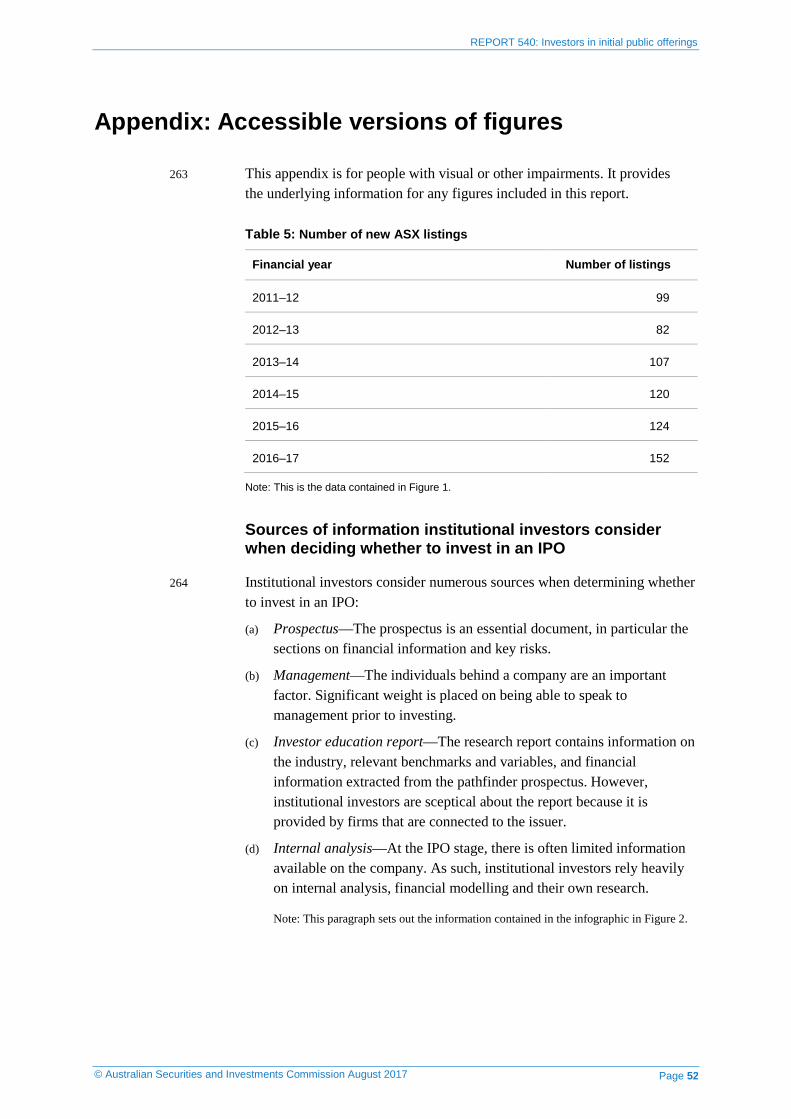

© Australian Securities and Investments Commission August 2017 Page 19

80 Investor education generally involves institutional investors meeting with the lead manager’s research analyst and being provided with a copy of the research analyst’s investor education report. This report generally contains information about the issuer’s business, industry, and relevant benchmarks and comparables.

81 At these meetings, which are held separately from the management roadshow, the research analyst will provide institutional investors with their views on the issuer’s business, risks and prospects.

82 We understand that investor education reports may include an overall company value or value range, but do not usually contain price targets or recommendations. This may be attributed to concerns that, if the research is released too soon after listing, it may attract prospectus liability.

83 As a result, a number of AFS licensees impose a blackout period after the prospectus is lodged before a research analyst connected to the issuer’s adviser can cover the stock. Following this period, the analyst will release their ‘initiation report’, which contains price targets and recommendations.

Note 1: International firms may adopt blackout periods for research analysts in the immediate period following lodgement of the prospectus in order to comply with requirements in other jurisdictions, such as the United States, rather than in compliance with a requirement under Australian law.

Note 2: Report 486 Sell-side research and corporate advisory: Confidential information and conflicts (REP 486) contains further information about the potential conflicts of interest associated with investor education. See also our proposed guidance in Consultation Paper 290 Sell-side research (CP 290).

84 In REP 486, we looked at investor education and found that this may provide potential institutional investors with an indication of a research analyst’s approach to valuation: see paragraphs 72–78 of REP 486. We also found, however, that there was some cynicism towards this information: see paragraphs 121–122 below.

85 CP 290 includes our proposed additional guidance on the investor education process. This is intended to supplement the guidance in Regulatory Guide 79 Research report providers: Improving the quality of investment research (RG 79).

Pathfinder prospectus

86 A pathfinder prospectus is a draft, but near final, version of the prospectus which excludes the offer price. It is primarily used where the institutional bookbuild for the IPO is conducted at the front end of the offer—which is when most bookbuilds happen in Australia, apart from offers at the larger end of the market: see paragraphs 90–93.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 20

87 The pathfinder prospectus is usually given to institutional investors at the start of the IPO roadshow period: see paragraph 88. Some institutional investors observed that sometimes the pathfinder prospectus is only given to them just before the IPO roadshow, which does not provide them with sufficient time to review the information.

IPO roadshow

88 The next step in the process is a roadshow where the issuing company’s management gives a presentation to institutional investors about the issuer and the offer.

89 Roadshows are a key opportunity for the issuer to tell its story in person and can provide useful pricing feedback for lead managers and underwriters. For institutional investors, the roadshow presents an opportunity to evaluate the issuer’s management—in particular, the executives’ ability to respond to questions about their business.

Timing of IPO roadshows—Institutional bookbuild

90 The timing of the IPO roadshow can depend on the point at which the institutional bookbuild for the IPO takes place (if there is one). Many offers in Australia use a front-end bookbuild, which means that the price of the offer is set through the institutional bookbuild a short time (usually two to three days) before the prospectus is lodged with ASIC and the retail offer opens.

91 When a front-end bookbuild is used, the IPO roadshow will usually start two to four weeks before the prospectus is lodged with ASIC. Front-end bookbuilds are more common for offers that are smaller in size (under $500 million market capitalisation) and are primarily aimed at domestic institutional investors.

92 In larger IPOs, the bookbuild sometimes takes place after the prospectus is formally lodged with ASIC (a ‘back-end bookbuild’). In these cases, the price of the offer is not set at the time the prospectus is lodged with ASIC but an indicative price range will be identified.

93 In these types of IPOs, the roadshow may take place after the prospectus is lodged with ASIC. Once the price has been determined under the back-end bookbuild, a replacement prospectus will be lodged with ASIC.

Information provided at IPO roadshows

94 There are usually two types of information provided to institutional investors as part of an IPO roadshow:

(a) management information—this is provided at group presentations and one-on-one meetings with institutional investors; and

(b) investor education reports—these typically include financial information from the prospectus, including forecasts.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 21

Management information

95 As part of the roadshow process, the senior management of the issuer will present to institutional investors. Slides of the presentation are usually distributed to these investors.

96 We were told that that the content of the presentation and associated slides provided a summary of key information from the pathfinder prospectus.

97 We were also told that issuers and their advisers were aware of the need to ensure that institutional investors were not provided with any material information about the offer that was not contained in the prospectus. We have previously commented on this risk in REP 486.

98 Sometimes a site visit to the issuer’s business operations may be organised for institutional investors as part of the roadshow.

99 In certain circumstances, meetings between senior management and select individual investors will also occur. The lead manager usually advises the issuer about which investors should have access to these meetings. Often only the larger investors are granted this kind of access.

100 Feedback from institutional investors was that an important part of the roadshow is the ability for them to ask the issuer’s management questions about the issuer and its prospects. An institutional investor will clearly have a greater opportunity and willingness to question management at one-on-one meetings than at larger group presentations. However, there is still some opportunity to ask questions at group presentations.

Internal analysis

101 All the institutional investors we spoke to conducted their own internal analysis. This can include:

(a) industry research—this includes consideration of the issuer’s position in that industry. The sources of information for industry analysis can vary depending, for example, on how familiar the research analyst is with the industry and how much information is publicly available. In some instances, the analyst will speak with competitors, suppliers and customers to help them form a view about the issuer;

(b) financial analysis—this includes scrutiny of historical financial information, as well as forecast financial information and the assumptions underlying that forecast; and

(c) rationale for the IPO—the institutional investors stated that it was important to understand why the issuer was pursuing an IPO at this time—for example, whether this was to access funding for the business, or was intended primarily as a liquidity event for existing shareholders.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 22

Prospectus and supplementary disclosure

102 In IPOs that have a front-end bookbuild, institutional investors are required to make their investment decision before the final prospectus is lodged with ASIC. Instead, they rely on the draft (pathfinder) prospectus.

103 In other types of IPOs, such as those using a back-end bookbuild, institutional investors may not receive a pathfinder prospectus and will instead rely on the lodged prospectus to make their investment decision.

104 The institutional investors told us they believed it was rare for material changes to be made from the pathfinder version of the prospectus to the lodged version. However, they did rely on the lead manager to inform them of any changes. The institutional investors were aware that these changes were often, but not always, prompted by ASIC’s review of the original prospectus.

105 Many of these institutional investors said they paid particular attention to supplementary or replacement disclosure that related to changes to the financial information. In contrast, less attention was paid to supplementary or replacement disclosure that merely clarified information or made changes to the presentation—for example, the more prominent disclosure of key information. Institutional investors who read the prospectus in full considered these kinds of changes were more important for retail investors.

Information that is important to institutional investors

106 Institutional investors said that the prospectus and access to management were particularly important to their assessment of an IPO.

107 The Financial Conduct Authority (FCA) in the United Kingdom also found that the prospectus and access to management were central to institutional investors’ assessment of an IPO. The FCA is exploring a range of proposals to enable investors to access the prospectus sufficiently early in the IPO process for the document to play its proper role in informing their investment decisions: see FCA Consultation Paper 17/5 Reforming the availability of information in the UK equity IPO process (March 2017).

108 The key sources of information that institutional investors consider when deciding whether to invest in an IPO are set out in Figure 2.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 23

Figure 2: Sources of information institutional investors consider when deciding whether to invest in an IPO

Note: Paragraph 264 in the appendix sets out the information contained in this figure (accessible version).

Source: ASIC

Prospectus

109 Institutional investors said that the pathfinder prospectus (or the lodged prospectus if no pathfinder prospectus was used) was one of the most important sources of external information, and this was usually read thoroughly.

110 Institutional investors stated that the prospectus was the benchmark document from which all other information about the IPO was sourced, including information provided to retail investors by intermediaries such as brokers.

111 The directors’ potential liability for the prospectus disclosure, and the consequent rigour around preparation of the prospectus, meant that the institutional investors considered it to be a reliable document. We did not receive any significant negative feedback about the quality of prospectuses from institutional investors during this project. However, some noted that a few issuers had recently failed to meet their prospectus forecasts, and

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 24

investors had therefore questioned the rigour of how these forecasts had been compiled.

Note: See paragraphs 149–154 for the feedback that retail investors gave on prospectuses during the market research. We comment in Section E on a few possible reasons why retail investors were more critical of prospectuses than institutional investors: see paragraphs 237–238.

Key sections of the prospectus for institutional investors

112 All of the institutional investors we spoke to identified the following sections of the prospectus as being very important:

(a) the financial information, including management’s explanation of historical financial performance; and

(b) the key risks.

113 Other sections that were also identified as being important, but were not nominated by all of the institutional investors, included:

(a) board and management;

(b) material contracts;

(c) related party transactions; and

(d) additional information.

ASIC’s review of prospectuses

114 Institutional investors involved with IPO offers told us that ASIC’s scrutiny of prospectuses had a positive influence on the preparation of the document. They considered that they could place more weight on the pathfinder prospectus, which includes similar information to the lodged prospectus, because the lodged prospectus may be subject to our review and possible regulatory action.

115 One of the implications of front-end bookbuilds is that institutional investors are required to make their investment decision, and participate in the offer, on the basis of a pathfinder prospectus which has not yet been subject to any regulatory oversight.

116 The institutional investors told us that this issue did not affect their reliance on the pathfinder prospectus. The fact that the lodged version of the prospectus may subsequently be reviewed by ASIC brings a rigour to the preparation of the document, which extends both to the pathfinder and final versions of the prospectus. Regulatory action by ASIC relating to the lodged prospectus can have significant consequences for the offer, even if it is largely pre-sold to institutional investors before the prospectus is lodged.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 25

Access to management

117 Institutional investors place significant weight on meeting the issuer’s management when assessing an offer, and meetings with the management were usually integral to institutions’ assessment of an offer. All of the institutional investors we spoke with said they would not invest unless they had access to the management.

118 We were told that the roadshow gave institutional investors a valuable opportunity to get an impression about the issuer’s management and its competence, which could sometimes be difficult to do through the prospectus alone.

119 During roadshows, the institutional investors can ask the issuer questions about their forecasts and the underlying assumptions. They can assess how readily the issuer’s management is able to respond to questions, how well they know the business and industry, and how prepared they are for the future.

‘Until we can meet with management, we’re not willing to invest. We need evidence they know what they are doing and have a solid plan for the future.’

Internal analysis

120 All of the institutional investors we spoke to emphasised the importance of their in-house analysis of the offer. At the IPO stage, there is often limited information available on the issuer. Institutional investors therefore place heavy emphasis on their own internal analysis, financial modelling and research.

‘We can’t just rely on what the issuer says it’s worth. Or what the lead manager says the issuer is worth. We need our own analysts to run the numbers and look at the sector more broadly.’

Investor education report

121 There was varied feedback from the institutional investors that we spoke to about the importance of investor education. Some institutional investors treated this information with scepticism because it was provided by the sell-side firm—however, others noted that background information on the industry could be useful.

122 CP 290 contains a number of proposed recommendations on how potential conflicts of interest that compromise investor education can be addressed: see Sections C and D of CP 290. The feedback provided by institutional investors on their concerns about the reliability of investor education may be an added incentive to improve practices in this area.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 26

C Market research—How retail investors make decisions about IPOs

Key points

We commissioned third-party qualitative market research to explore the factors that influence retail investors in deciding whether to invest in IPOs.

The market research found that:

• most retail investors said they used the prospectus—however, the extent of that use varied considerably;

• most retail investors reported looking for information outside the prospectus for a number of reasons; and

• only a small number of retail investors said they used online investor forums or social media to help them assess IPO offers.

Background to the market research

Objective of the market research

123 As stated above, prospectuses are required by the Corporations Act for IPOs that involve an offer of securities to retail investors in Australia. A prospectus is intended to be the most important source of information on an IPO for retail investors and their advisers. However, retail investors are increasingly receiving information and advice about IPOs from a number of different sources.

124 To complement our work discussed in REP 494, we decided that our regulation of IPOs would benefit from a better understanding of how different types of information and other factors influence retail investors.

Scope of the market research

125 The market research involved retail investors who invest for their own personal account rather than on behalf of other investors or entities. There were 11 high net worth investors and 41 retail investors. Eight retail investors used a self-managed superannuation fund (SMSF).

126 We included a proportion of SMSF investors and high net worth investors (who would qualify as sophisticated investors) in the sample because:

(a) we anticipated that SMSF investors or high net worth investors may make up a significant proportion of non-institutional IPO investors; and

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 27

(b) we also thought that high net worth investors may have a similar approach to assessing IPOs as retail investors, given the relatively low financial tests for sophisticated investors under the Corporations Act.

Note: Professional and institutional investors were excluded from the market research. We separately examined the factors and information that influence institutional investors in IPOs in Section B.

Methodology of the market research

Qualitative research

127 We considered that qualitative research comprising in-depth interviews with retail investors was the most appropriate method for exploring their process of investing in IPOs.

Structure of the research

128 A third-party research firm, Whereto Research, conducted interviews and group discussions with a total of 52 participants located in Sydney, Melbourne, Brisbane and Perth.

Note: We have included as an attachment to this document the report Factors that influence retail investors in IPOs, issued in August 2017, based on the qualitative market research conducted by Whereto Research and commissioned by ASIC (Whereto Research report).

129 The participants had a broad range of investment experience but there were more experienced retail investors than inexperienced retail investors. This may be due to the perception that IPOs are difficult and relatively high-risk investments.

130 The market research was conducted in two stages in late 2016 and early 2017:

(a) Stage 1 of the market research involved 17 interviews that were participant-led discussions focusing on the retail investors’ recent IPO investments. Stage 1 also included two group discussions involving participants with similar investment profiles.

(b) The information obtained in Stage 1 allowed Stage 2 of the market research to focus on particular issues, which were explored in 24 semi-structured interviews. These interviews were conducted over the telephone to increase geographic representation of the research.

Note: Further details of the market research methodology are contained in Section 3 of the Whereto Research report and the appendix to the report.

Features of the market research

131 The participants in the market research reflected a range of ages, gender and ethnicity—however, the limited sample size means that these retail investors,

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 28

and the findings, might not be representative of the total IPO investor population. In particular, only a small number of participants in the sample used a full-service broker, whereas full-service brokers tend to dominate retail access to larger IPOs: see paragraphs 155–156.

132 To maximise what investors would remember about their investment decision, we asked Whereto Research to select participants who had all either invested, or seriously considered investing, in an IPO in the previous 12 months. However, the findings still reflect retail investors’ own recollection of their investments, with no verification of what they actually did at the time.

133 The findings from the market research could therefore be influenced by participants’ memory of events, as well as factors such as:

(a) hindsight bias—which can change how an event is remembered or affect the recall of different memories over time; and

(b) social biases—which can affect how events are reported in a social context, such as in interviews and focus groups.

Note: In this report, for ease of reference, we generally discuss the market research findings as if they reflect what retail investors actually did. However, it should be noted that the findings are based only on what retail investors said they did.

134 The IPOs that participants had considered over the previous 12 months did not necessarily reflect the full spectrum of companies, which would tend to float over a longer period of time. However, the recent IPOs were from a diverse range of companies—from established ‘blue chip’ companies through to small start-up companies, and operating in a variety of industries. In addition, the majority of participants had invested in many IPOs over a long period of time, and this would tend to increase the type of IPOs they gave feedback about.

Note: For further details on the range of investors who participated in the market research, including a breakdown of their ages, ethnicity, gender and investment experience, see the appendix to the Whereto Research report.

Summary of the market research findings

Retail investors perceive IPOs to be complex

135 Retail investors who participated in the market research unanimously acknowledged that IPOs were complex investment decisions. They all wanted to make money on their IPO investment but recognised that IPOs were inherently risky.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 29

136 Aside from just making money, some of the retail investors also derived intellectual satisfaction from the challenge of investing in IPOs, or said they were excited about being part of something new.

Diverse investment processes

137 Retail investors in the market research said that each IPO was different. They did not have set sources of information that they consulted in a linear fashion, and there was no single pathway to making their investment decision.

138 The retail investors’ recall of formal advertising about IPOs was extremely low. However, Whereto Research noted that this could have been because promotional content in investment newsletters or online broker platforms was perceived to be information rather than advertising.

139 The process for deciding whether to invest in an IPO appeared to differ between individual investors based on a number of factors such as the individual’s level of self-reported confidence, their experience and their appetite for risk. The process could also differ depending on the IPO.

140 Most of the retail investors said that they completed considerable research and considered the offer in detail before making their investment decision. The Whereto Research report noted that:

Most investors did not seriously consider IPOs that operated in industries they did not believe they understood. Where a participant was interested in an IPO of a company that operated in an industry they felt they did not understand well, they conducted quite considerable research to help them better understand the market. In the majority of cases, investors eventually decided against an IPO they had been considering if they felt after some research that they didn’t have a reasonable level of understanding about the company, its market and its business.

141 In our view, many of the participants were able to articulate sound factors that they took into account before investing—including, for example:

(a) how the issuer planned to make money;

(b) the expertise of the issuer’s management;

(c) the competitors operating in the same market;

(d) the issuer’s financial position; and

(e) the specific risks the issuer might encounter: see pages 59–64 of the Whereto Research report.

142 However, the market research also identified potential behavioural factors that may have affected investors’ decision making. These are explained in Section D.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 30

Awareness of ASIC’s role

143 Nearly all of the retail investors were aware of ASIC as a regulator, but very few were aware of our role specifically in relation to IPOs.

144 In some cases, retail investors appeared to think that ASIC assessed whether companies met certain merit-based criteria before listing. In fact, we do not have the power to prevent an IPO merely because it appears to have little merit. Although Australian exchange markets require companies to meet certain listing criteria, these criteria are not based on the merits of the investment, apart from certain basic requirements such as size and spread.

145 There also appeared to be a perception among some retail investors that ASIC reviewed all prospectuses and checked the integrity of the information. A number of retail investors said they wanted to better understand ASIC’s role in relation to IPOs.

Types and sources of information

Prospectus

146 Most retail investors who participated in the market research said the prospectus was a key source of information, mainly because it was a document required by law and was regulated by ASIC. However, as discussed in paragraphs 147–154, the use of the prospectus varied considerably.

147 Most retail investors felt comfortable ignoring large sections of the document and only focused on the parts they considered to be the most important or which they said they could understand. Some retail investors only mentioned the prospectus when prompted by the researcher, suggesting it may not have had a significant influence on their investment decision.

148 These findings are consistent with some of the results of the quantitative research by the New Zealand Stock Exchange and the New Zealand Financial Markets Authority in 2014. This research found that, of those investors who reviewed the offer document, 15% said they read all of it, 52% said they read most of it, and 33% said they read some of it. The report concluded:

Most investors/potential investors surveyed say they at least looked at the documents before making their investment decision. However, few read the documents thoroughly—most dipped into them rather than read them cover to cover and it’s probable that some merely opened them to satisfy registration process requirements.4

4 New Zealand Stock Exchange (NZX) and Financial Markets Authority (FMA) New Zealand, NZX–FMA, Investor experience of IPOs, February 2014, p. 8.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 31

Retail investor feedback on prospectuses

149 The retail investor feedback on prospectuses was varied. Many investors made insightful comments about prospectuses and pointed out deficiencies that we identify on a regular basis. There were also investors who did not appear to use the prospectus very much and others who assessed the document partly by factors such as the quality of the paper.

150 Table 3 discusses the key sections of the prospectus that the retail investors reported using, and the information they were searching for. The investors’ comments and general concerns about prospectuses are set out in paragraphs 151–154. Section 4.8 of the Whereto Research report contains the comprehensive research findings on the role of the prospectus.

Table 3: Retail investors’ use of the prospectus

Investment overview A good introduction helped some retail investors decide whether or not to investigate the IPO further.

Some retail investors only read the investment overview:

‘That’s usually enough to tell you what it’s all about.’

Some retail investors did not think the prospectus had a good summary of key information and some also had difficulty navigating the document.

Financial information This was important but retail investors appeared to have varying abilities to understand the information.

Some retail investors did not think they had the skills to understand the financial information in the prospectus.

The more experienced retail investors perceived the information to be a good starting point, but also conducted their own analysis—for example, to check whether forecasts appeared reasonable.

Business/industry overview

Most retail investors said they wanted information on the business and industry. Many retail investors said the prospectus provided a good starting point for this information.

Risk factors A number of retail investors considered the risk disclosure was too generic and wanted information on specific risks to the issuer:

‘Sometimes the key risks can be quite broad, and quite vague … A company might put in that a key risk is to satisfy ASIC. And you go, “well what are the specific risks to your company? Can you be more specific?” ’

‘It looks like they’ve just cut and pasted the risks.’

Board and management A large number of retail investors (especially the more experienced investors) said that information on the issuer’s management was very important.

While the prospectus was the primary source used to obtain this information, some conducted further searches to check whether any of the management team had a history of bad management. Where information about bad management emerged, retail investors were unlikely to consider the IPO any further.

Some investors did not think they had the skills to assess the information on the past performance or expertise of the management.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 32

Length and complexity

151 A significant proportion of retail investors, particularly those who were less experienced, said that prospectuses were too long and that this contributed to difficulties in understanding the document or even attempting to read large parts of it. The behavioural biases associated with lengthy disclosure documents are discussed further in Section D at paragraphs 209–213.

152 Prospectuses are not only challenging because they are long. They are also difficult because they are repetitive and the language used is often archaic, technical or legalistic. The market research findings indicated that retail investors would be likely to find prospectuses more useful if the key information was explained in clear language. For example, one retail investor said:

‘[P]rospectuses are too hard to understand. They’re written by lawyers and people with vested interests. [They should] … provide information that the average investor who doesn’t have the knowledge can understand … I honestly believe it has to be spelt out clearly and align with the modern practices of explaining things that are critical in a simple way.’

153 Some retail investors gave feedback during the market research that they wanted a good investment overview to help them understand the key issues and navigate the document. One investor, referring to a third-party report on an IPO, said they appreciated:

‘… a really good summary, how the company runs, its regulatory requirements, the sort of headwinds it might encounter, all in plain language. But you don’t get that in a prospectus.’

Lack of candid information

154 Some retail investors also said that some prospectuses failed to contain important relevant information—such as the assumptions underlying the forecasts, disclosure on specific risks facing the issuer, and detailed information on management. There was also a perception that the prospectus was an unbalanced marketing document that did not tell the whole story.

‘The prospectus is useful but there is no way I’d make a decision based just on that. I know it has a positive slant, so I read it, and then I look for other information.’ ‘There are some prospectuses that are very glossy, they have information about their projections, but they don’t explain their underlying assumptions. And if you don’t understand that, how can you understand if it’s a risk worth taking?’

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 33

Full-service brokers

155 Most of the retail investors who took part in the market research were ‘self-directed’ and did not use a full-service broker or other paid investment advice. This is in contrast with quantitative research on IPOs conducted in 2003, which found that 60% of respondents used a full-service broker.5

156 It is not always easy for ‘self-directed’ retail investors to obtain allocations in capital raisings (particularly for IPOs that are keenly sought after). Most large IPOs have a limited, if any, public offer component. For example, allocations of shares for 13 of the 15 largest IPOs during 2016 were limited to clients of the broker who was managing the offer (with only two of these also having a general public offer).

157 Even where a general public offer is included, and a broker is appointed by the issuing company to manage the offer, the broker still largely manages the allocation of shares in a capital raising, and these are generally allocated to clients of the broker.

158 However, the findings from the market research were consistent with other research that shows increasing numbers of retail investors are self-directed.6 As noted in the ASX Australian investor study 2017, this may have implications for the financial advice sector and how financial advisers engage with retail investors.

159 Although most of the participants in the market research said they preferred a ‘do-it-yourself’ approach to investing, the research findings showed that many of them were seeking some kind of informal assistance. This suggests that there is still a need or desire for investment advice in some form.

Why retail investors did not use a full-service broker for IPOs

160 The retail investors who participated in the market research gave a number of reasons for not using a full-service broker. Some of the more experienced retail investors said they used a full-service broker when they first started investing because there had been no other option, but they now used online brokerage services.

161 A few retail investors said they did not trust brokers to provide unbiased information. For example, one retail investor said:

‘If the broker is going to buy into the IPO, they are going to want to create some movement, to push up the price. So they need to create a demand, and they are obviously receiving a very large fee for managing the IPO.’

5 Ian Ramsay, Use of prospectuses by investors and professional advisers (PDF 481 KB), Centre for Corporate Law and Securities Regulation, The University of Melbourne, 2003, p. 14. 6 ASX Limited, ASX Australian investor study 2017, May 2017, p. 26.

REPORT 540: Investors in initial public offerings

© Australian Securities and Investments Commission August 2017 Page 34

162 Other reasons for not using a full-service broker included the perceived cost of using a broker, doubt that brokers added sufficient value, and the belief that brokers were only for high net worth investors.

Note: Some of the participants had never used a broker, so the perceptions about brokers may not have come from personal experience.

163 The ASX Australian investor study 2017 commented that, currently, most retail investors in Australia are ‘self-directed’. Investors’ main reasons for not using advice were that they preferred to be in control and they were not convinced that advice added value.

Note: The ASX study noted that, although around 61% of investors used some form of financial advice when investing (i.e. a financial planner or full-service broker), only 45% of investors were estimated to use financial advice in general. Quite a large proportion of investors using advice did so for assistance with administrative and taxation requirements.7

How retail investors used full-service brokers for IPOs