report no. 20283-et ethiopia public expenditure...

TRANSCRIPT

Report No. 20283-ET

EthiopiaPublic Expenditure Review(In Two Volumes) Volume 1: Main Report

November 30, 1999

World Bank Country Office in EthiopiaCountry Department 6Africa Region

Document of the World Bank

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

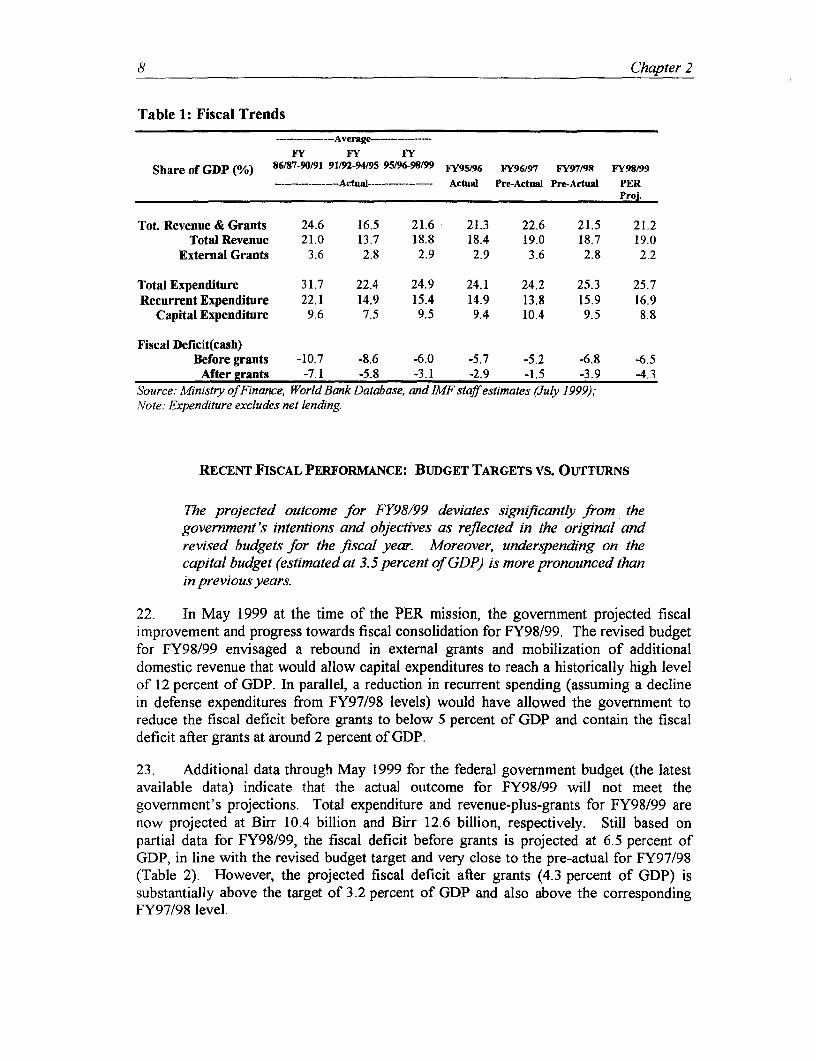

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

GOVERNMENT FISCAL YEARJuly 8 - July 7

CURRENCY EQUIVALENTSCurrency Unit: Ethiopian Birr (Br)

Official Rate: US$ 1.00-Br 8.00 (September 7, 1999)

ACRONYMS AND ABBREVIATIONS

AfDB African Development BankARM Annual Review MeetingCAD Central Accounts DepartmentCSC Civil Service CollegeCSR Civil Service ReformDIFD Department for Intemational DevelopmentDSA Decentralization Support ActivityEC European CommissionEFY Ethiopian Fiscal YearEMC Expenditure Management and ControlERA Ethiopian Road AuthorityESDP Education Sector Development ProgramFAGO Federal Auditor General's OfficeFDRE Federal Democratic Republic of EthiopiaFIS Financial Information SystemGDP Gross Domestic ProductGoE Govemment of EthiopiaHIID Harvard Institute for Intemational DevelopmentHIPC Healthy Indebted Poor CountriesHSDP Health Sector Development ProgramIMF Intemational Monetary FundIPF Indicative Planning FiguresMEDaC Ministry of Economic Development and CooperationMEFF Macroeconomic and Fiscal FrameworkMoE Ministry of EducationMoF Ministry of FinanceMoH Ministry of HealthMTEF Medium-Term Expenditure FrameworkPAP Program Action PlanPEP Public Expenditure ProgramPER Public Expenditure ReviewPIM Program Implementation ManualPIP Public Investment ProgramPMO Prime Minister's OfficeRMI Regional Management InstitutesSDP Sector Development ProgramSIDA Swedish Intemational Development AssociationSNNPS Southem Nations, Nationalities and People's StateTA Technical AssistanceUNDP United Nations Development ProgramUSAID United States Agency for Intemational Development

Vice President Callisto E. MadavoCountry Director Oey Astra MeesookSector Manager Peter MiovicTask Team Leader Hart Schafer

PREFACE

The 1999 Public Expenditure Review (PER) for Ethiopia was prepared by a teamfrom the government and a donor team.

The government team was led by H.E. Ato Hailemelekot T/Giorgis, Vice Ministerof Finance, and included Ato Asrat K/Work, Ato Amare Gebrewold, Ato Tesfaye Kassa,Ato Mesfin Asrat, Ato Anemwa Ebay, Ato Fantahun Belew (MoF), Ato Melaku Kifle,Dr. Meshesha Getahun (MEDaC), Ato Tesfamichael Nahusenay (ERA), Dr. DemekeYigletu, Ato Kassahun Habte-Mariam (MoT), Ato Gebre-Medhin Belay (MoA), AtoGirma Asfaw, Ato Teferi Hagos (MoE), Ato Ketemaw Yimam (MoTC), Dr.Gebremaskal Habte-Mariam, and Ato Abebe Gesit (MoH).

The donor team was led by Hart Schafer (World Bank) and included DavidCowen (EMF), Kurt Cornelis (EC), Roland Martin (Netherlands), Stephen Lister (DFIDConsultant), Stephen Olanrewaju (AfDB), Filiberto Sebregondi (EC), and Doug Addison,Nicholas Bennett, Eyerusalem Fasika, and Fred Kilby (World Bank). During the fieldwork, the team liaised closely with Nigel Roberts (World Bank Country OfficeManagers/Ethiopia).

The main field work for the 1999 Ethiopia PER was carried out jointly fromMay 3 through May 18, 1999. The PER teams visited regional authorities in AddisAbaba, Amhara, Oromiya, Harari, and Dire Dawa. This report was prepared under thegeneral guidance of Oey Astra Meesook (Country Director) and Nigel Roberts (WorldBank Resident Representative in Ethiopia). Peter Miovic was the Sector Manager(AFTM2), Vinaya Swaroop (DECRG) the Lead Advisor, and Gene Tidrick (AFTMI) thePeer Reviewer. Special thanks goes to Tanisha McGill for editing and desk-toppublishing support of the final report.

The draft 1999 Ethiopia PER was discussed with the government in workshopsheld in Debre Zeit, Ethiopia (September 13-15, 1999) and Brussels, Belgium (October27-28, 1999).

Contents

PREFACE ...... .............................................................. I

EXECUTIVE SUMMARY .................................................................... I

CHAPTER 1: INTRODUCTION .................................................................... 1

SETTING ..................................................................... 1FOCUS OF THE 1999 PER .................................................................... 1STATUS OF PREVIOUS PER RECOMMENDATIONS .............................. ...................................... 3DATA ISSUES-AN IMPORTANT CAVEAT .................................................................... 5

CHAPTER 2: DEVELOPMENTS IN BUDGETARY AGGREGATES ............................................... 7

FISCAL TRENDS .................................................................... 7RECENT FISCAL PERFORMANCE: BUDGET TARGETS VS. OUTTTURNS ....................................................... 8ECONOMIC AND FUNCTIONAL EXPENDITURE CLASSIFICATION ............................................................. 13REAL AND PER CAPITA EXPENDITURE .................................................................... 16CONSTRAINTS To MOBILIZING EXTERNAL RESOURCES FOR SPS ........................................................... 20IMPACT ON SOCIAL SECTOR EXPENDITURE ..................... ............................................... 20

CHAPTER 3: FISCAL IMPLICATIONS OF THE WAR .................................................................. 25

FUNDING OF INCREASES IN DEFENSE BUDGET .......................... .......................................... 25SECOND ROUND EFFECTS OF THE WAR .................................................................... 26

CHAPTER 4: FISCAL SUSTAINABILITY OF SECTOR PROGRAMS ......................................... 29

BROAD MACROECONOMIC OBJECTIVES .................................................................... 3 1MACROECONOMIC SCENARIOS .................................................................... 31IMPLICATIONS FOR IMPLEMENTATION OF SECTOR PROGRAMS .............................................................. 35CONCLUSIONS .................................................................... 37

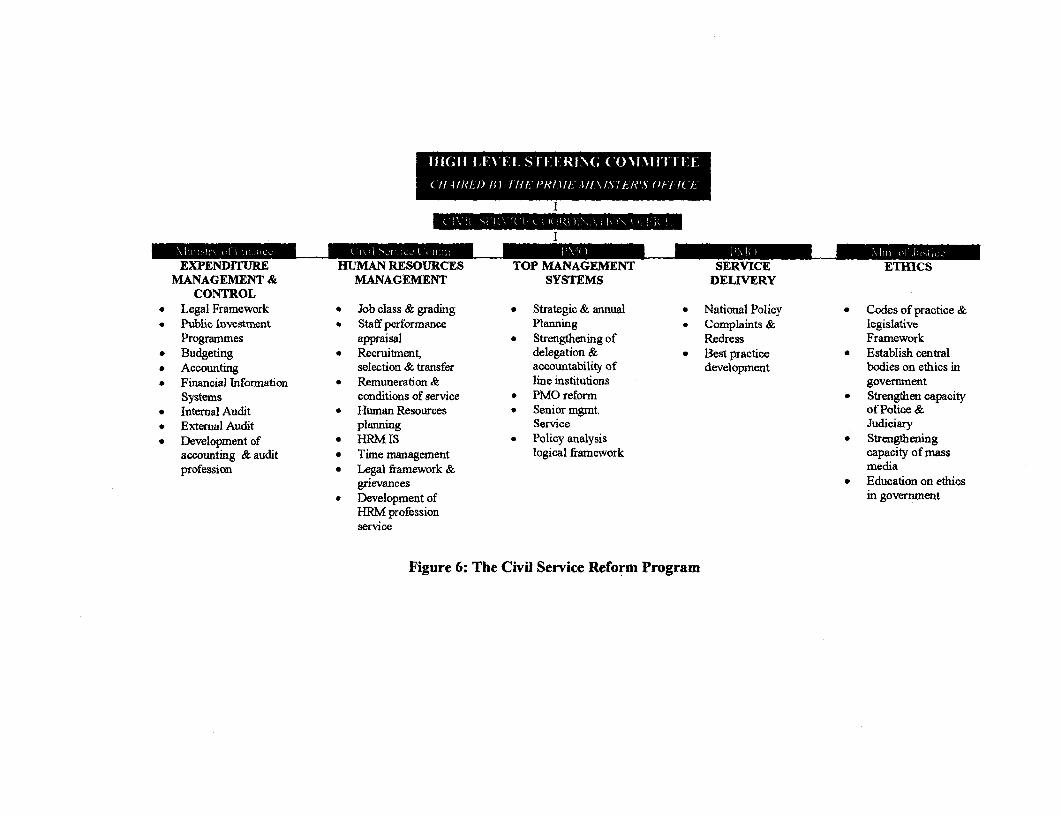

CHAPTER 5: CAPACITY BUILDING IN PUBLIC FINANCE MANAGEMENT .......... ............... 39

INTRODUCTION .................................................................... 39ONGOING REFORMS IN PUBLIC FINANCE MANAGEMENT .................................................................... 39FISCAL DECENTRALIZATION .................................................................... 40REFORM OF EXPENDITURE MANAGEMENT .................................................................... 44SECTOR DEVELOPMENT PROGRAMS .................................................................... 50RECOMMENDATIONS ON CROSS-CUTTING ISSUES ...................................... .............................. 56

CHAPTER 6: PER PROCESS .................................................................... 61

ANNEXES AND ANNEX TABLES .................................................................... 65

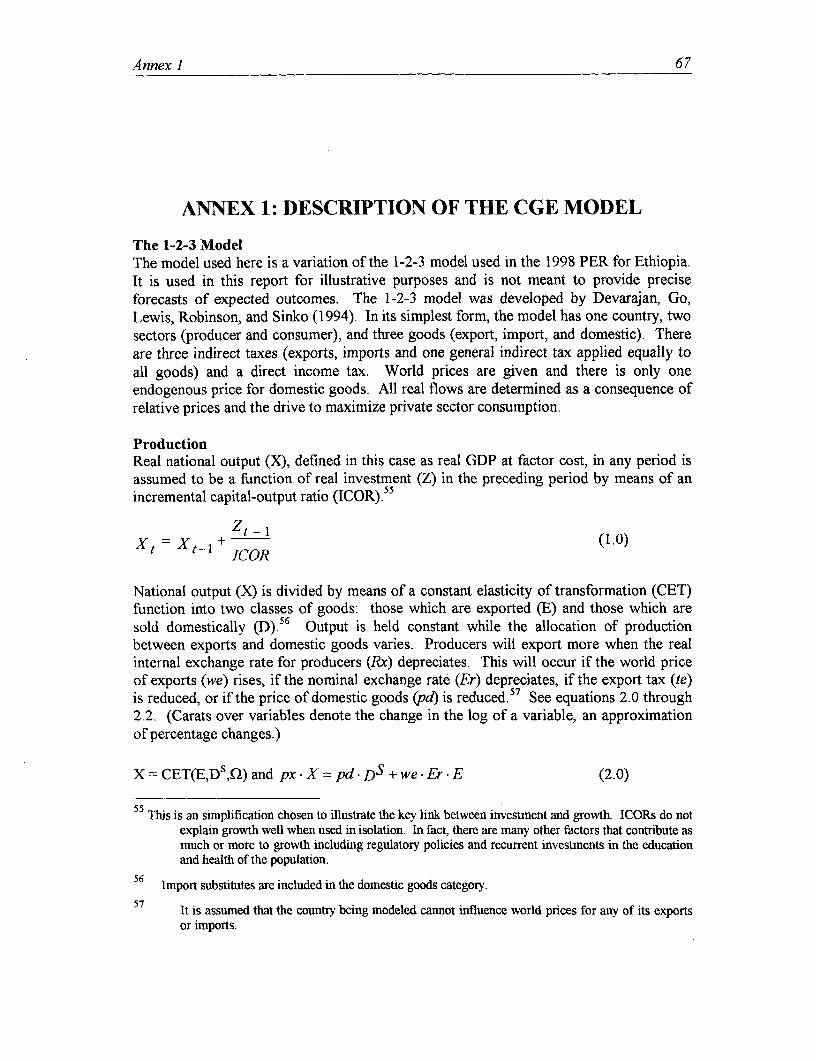

ANNEX 1: DESCRIPTION OF THE CGE MODEL .................................................................... 67

ANNEX 2: OUTCOME AND RECOMMENDATIONS OF DEBREZEIT WORKSHOP ............... 73

ANNEX 3: GOVERNMENT OF ETHIOPIA COMMENTS ON PER 1999 .............. ....................... 79

ANNEX 4: OUTCOME AND RECOMMENDATIONS OF BRUSSELS WORKSHOP .................. 81

Tables, Figures, and Boxes

Table 1: Fiscal Trends .......................................................... 8Table 2: Budget Execution .......................................................... 9Table 3: Economic Classification of Public Expenditures .............................................. 13Table 4: Functional Classification of General Government Expenditure ........................ 14Table 5: Real Expenditure .......................................................... 17Table 6: Real Per Capita Expenditure ........................................................... 18Table 7: Sectoral Expenditure-Actuals/Projections vs. Targets .................................... 21Table 8: Road Transportation Cost Addis Ababa to Assab and Djibouti ........................ 28Table 9: Macroeconomic Scenarios-Outcomes .......................................................... 33Table 10: SP Expenditures as Share in Total Spending .................................................. 36Table 11: Base Case Scenario - Per Capita Spending in Education, Health, Roads ......... 36

Figure 1: Capital Budget Implementation Rate in Priority Sectors ................................. 10Figure 2: Trends in Defense Expenditure .......................................................... 15Figure 3: Per Capita Spending in Social Sectors for Selected SSA Countries ................. 19Figure 4: Disbursement of Capital Expenditures by Source ........................................... 21Figure 5: Modified Implementation Path for Sector Programs ....................................... 38Figure 6: The Civil Service Reform Program .......................................................... 45Figure 7: Alternative Disbursement Channels for SPs ................................................... 52

Box 1: Economic Cost of Chronic Underspending on the Capital Budget ...................... 11Box 2: The Limited Effectiveness of Supplementary Budgets on Spending Levels ....... 11Box 3: EC Structural Adjustment Support and Stabex ................................................... 23Box 4: Important Deviations in FY99/00 Budget from Base Case ................................. 34Box 5: Budget Management Issues in Previous Studies ................................................. 39Box 6: Fiscal Devolution Below the Regional Level ...................................................... 41

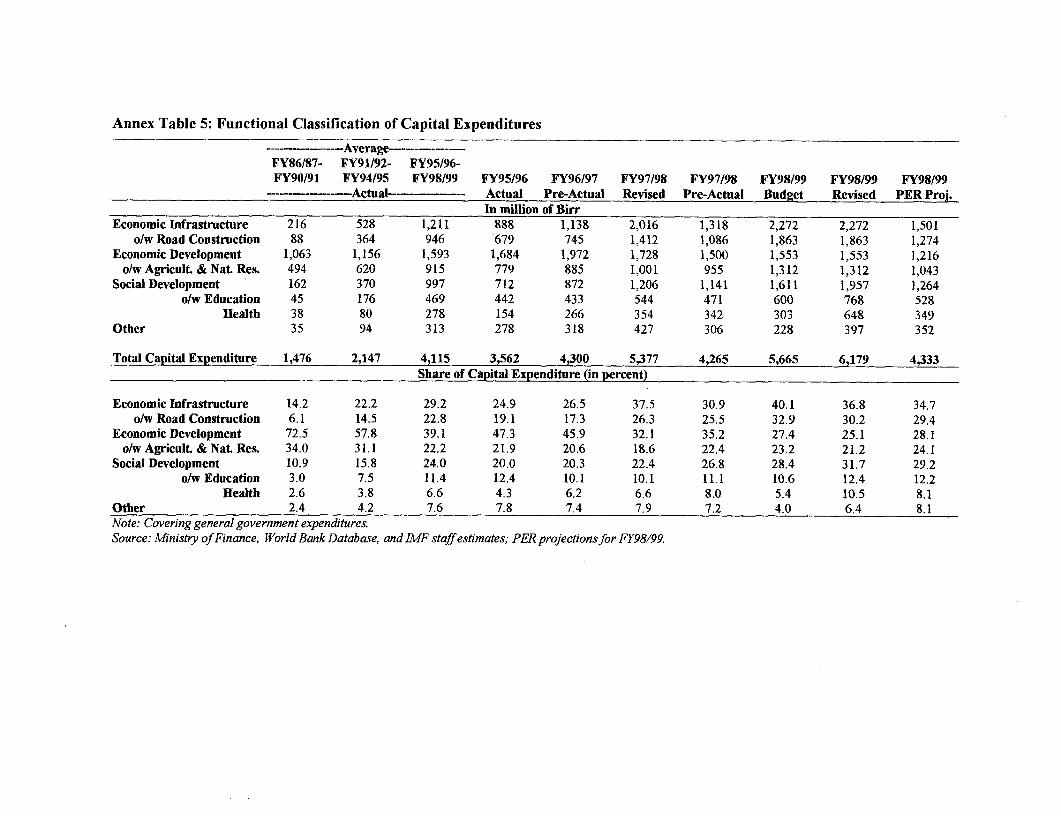

Annex Tables

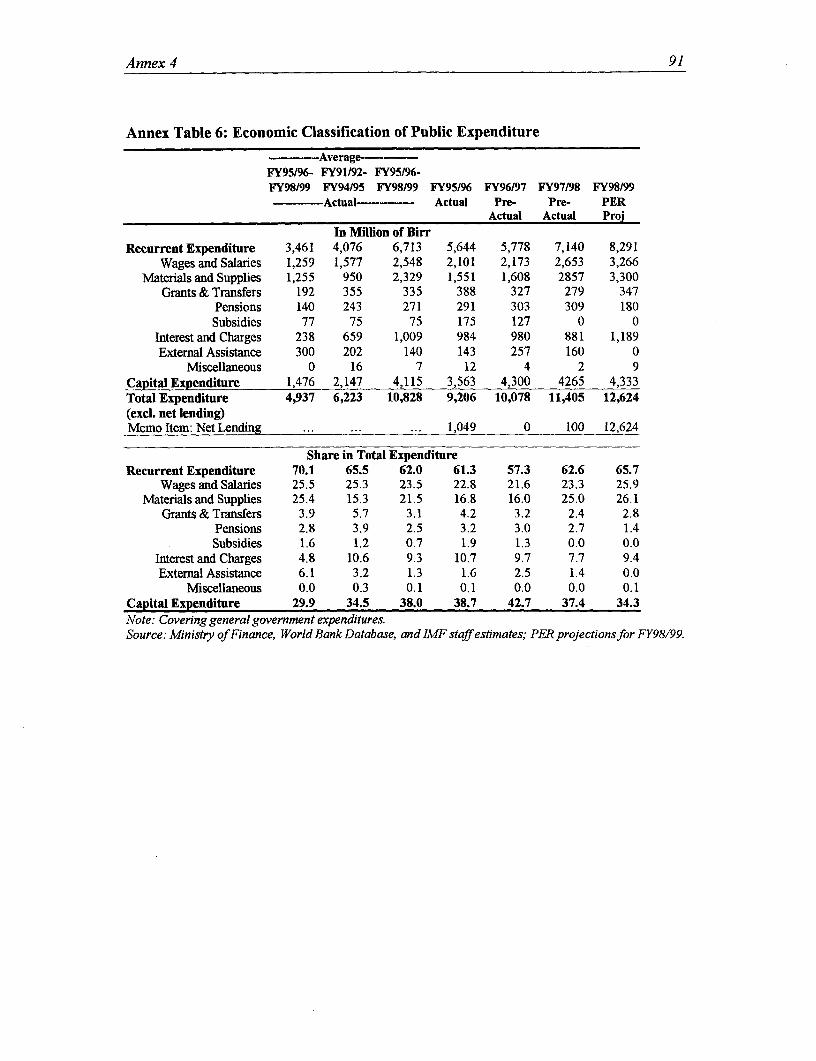

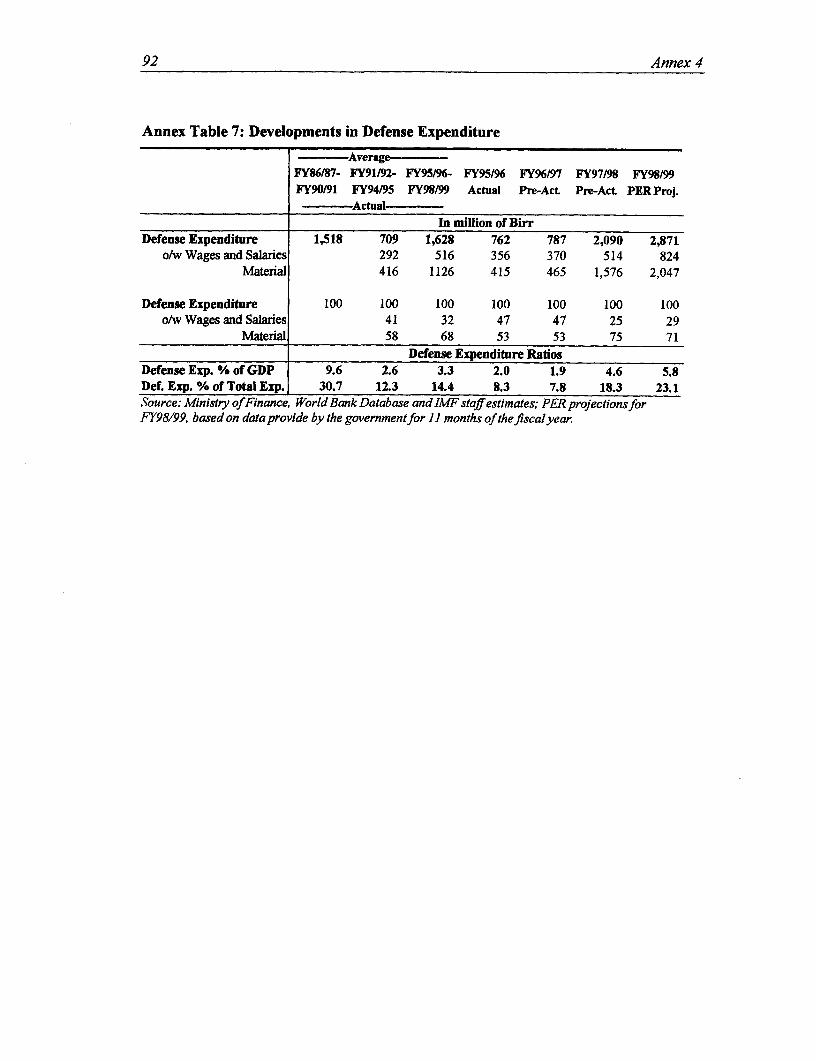

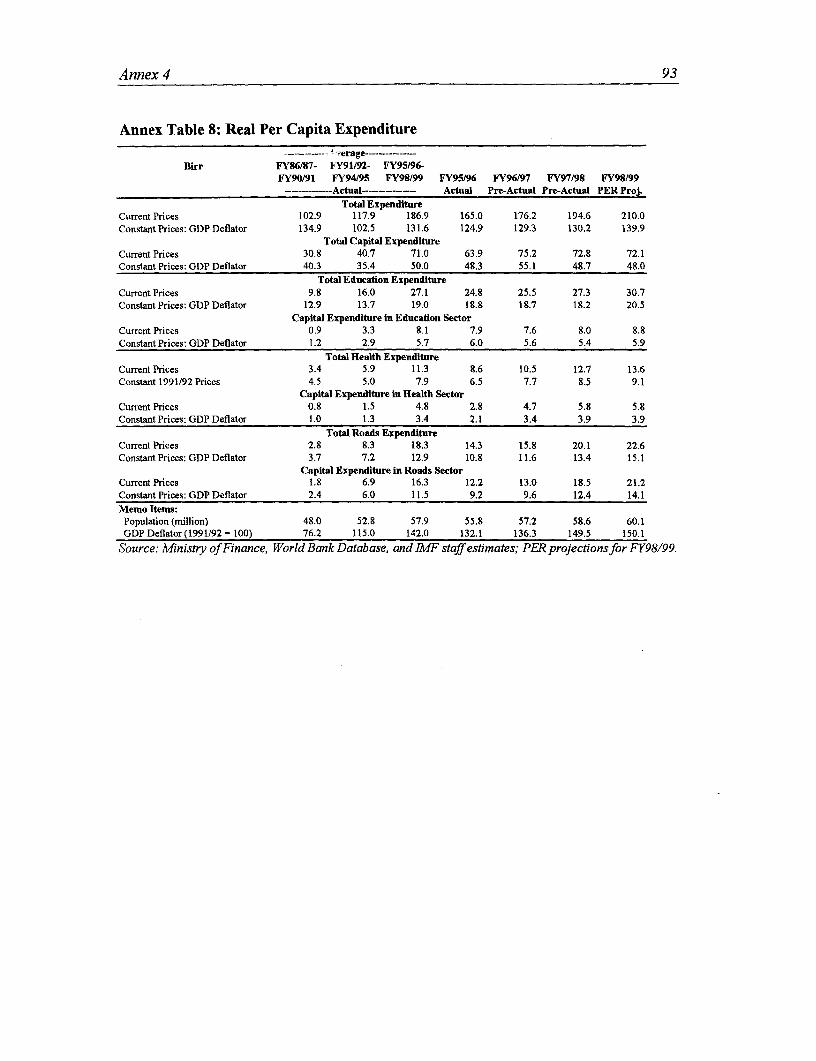

Annex Table 1: Progress on Previous PER Recommendations ....................................... 84Annex Table 2: Fiscal Trends FY98/87-FY98/99 .......................................................... 87Annex Table 3: Functional Classification of General Government Expenditures ........... 88Annex Table 4: Functional Classification of Recurrent Expenditures ............................. 89Annex Table 5: Functional Classification of Capital Expenditures ................................. 90Annex Table 6: Economic Classification of Public Expenditure .................................... 91Annex Table 7: Developments in Defense Expenditure ................................................. 92Annex Table 8: Real Per Capita Expenditure .......................................................... 93Annex Table 9: Financial Calendar .......................................................... 94

You cannot build a housefor lastyear's summer

(Ethiopian Proverb)

Ethiopia1999 Public Expenditure Review

An Exerciseby the Government ofEthiopia andDonors

EXECUTIVE SUMMARY

Focus of the 1999 PER1. Since May 1998, the war between Ethiopia and Eritrea has been the center ofattention of the Ethiopian government and its donors. In addition to the human toll of thewar, there have been concerns that the sharp rise in defense expenditure could jeopardizethe substantive macroeconomic and structural progress made in recent years.Consequently, one major area of attention of the present report is to review themacroeconomic impact of the war and the financing of the associated defenseexpenditures, and to determine whether defense spending pressures have divertedresources from priority development programs. At the time of writing this report, effortsto reach a peaceful resolution of the war are ongoing. Although the available fiscal datafor the past two years are still incomplete or preliminary, enough is available to allowsome important conclusions to be drawn'. The 1999 Public Expenditure Review (PER)

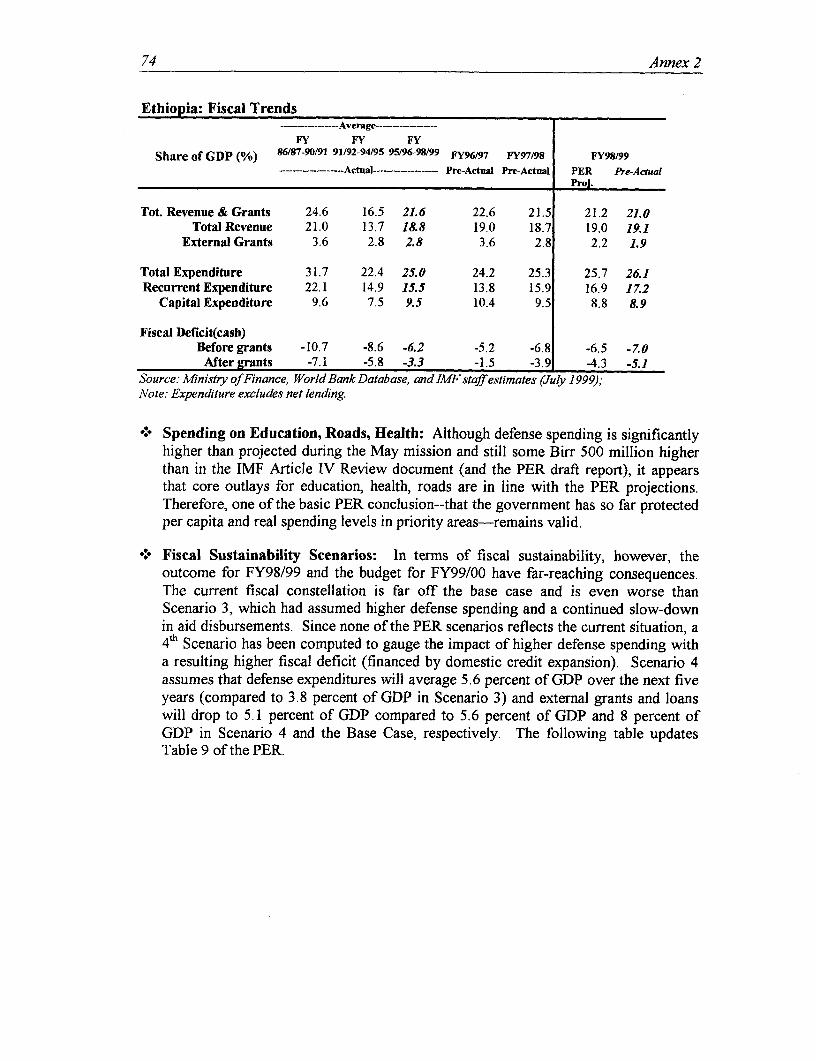

In the PER discussion workshops in Debre Zeit and Brussels, the Government made available revisedprojections for FY98/99. In comparison to the PER data base, the latest fiscal estimates indicate thatdefense expenditures may reach a share in GDP close to 7%, and 1.2 percentage points higher than the

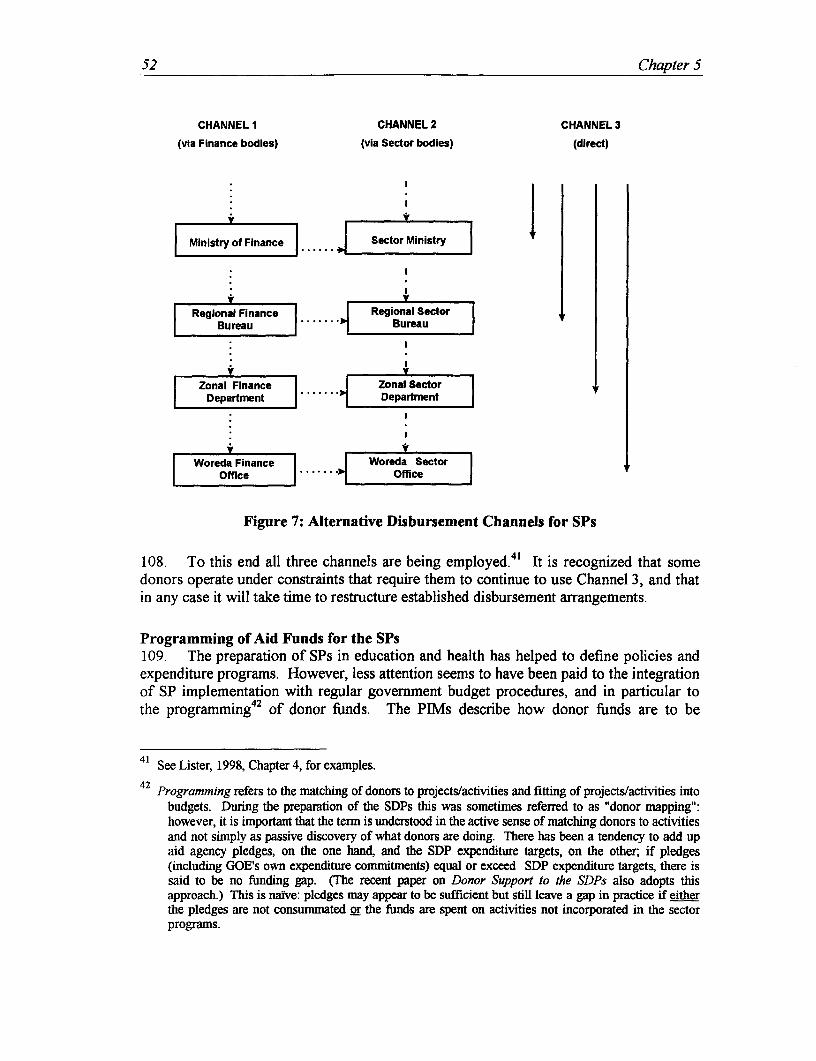

ii Executive Summary

concentrates on: (a) recent fiscal developments with a specific focus on the fiscal impactof the war; (b) fiscal sustainability of the expenditure program in general and the sectorprograms in education, health, and roads in particular; (c) public finance management;and (d) the PER process itself

Recent Fiscal Developments2. Ethiopia has followed a policy of not permitting the war to interfere with theconsolidation of macroeconomic stability and continuation of structural reforms. Indeed,except for the floor on net foreign assets of the banking system, all quantitative targetsunder the 1998/99 program with the IMF were met. Despite the shortfalls in officialloans and grants official reserves at the end of FY98/99 were slightly higher than oneyear ago (in terms of months of import coverage). The government has appropriatelyprotected core spending in priority sectors, while financing the increased defense budgetthrough extraordinary revenue efforts, including one-time financing measures such asutilization of privatization receipts.

3. But, the fiscal stress posed by the war is reflected in the projected fiscal outcomefor FY98/99, which is a clear outlier to the trend and deviates substantially from thegovernment's intentions and objectives as reflected in the original and revised budgets forthe fiscal year. Unless timely corrective actions are taken, performance over the past twoyears could put the long-term positive trend in jeopardy. While capital spending willremain below budgeted figures, total recurrent expenditure is likely to exceed budgettargets because of the excess in defense outlays. Although real per capita spendingincreases are still projected for education, health, and roads, the chronic underspending inthese sectors (compared to budget targets) appears to be more pronounced in FY98/99than in previous years. This reflects capacity constraints and teething problems with thesector programs in education, health, and roads, as well as lower-than-expected aiddisbursements (overestimation of the availability of funds), rather than deliberate budgetcuts. So, while pre-war gains have been preserved, the past two years expose missedopportunities to accelerate progress toward a more poverty-sensitive expenditurecomposition.

Reasons for Underspending on the Capital Budget4. The puzzling chronic under-execution on the capital budget is a recurring themeof this PER because of concerns with regard to the ambitious sector programs (SPs) ineducation, health, and roads. The issue is reviewed from various angles, includingwhether the binding constraints to disbursement are external resource availability,administrative bottlenecks, limited implementation capacity, or fiscal constraints.

5. Observed delays in the disbursement of external resources for SPs point to start-up problems during FY97/98 and FY98/99 in concluding external assistance agreements.There were also significant delays in achieving effectiveness of aid agreements because

PER estimate. Despite the increase in defense spending (compared to earlier projections) it appearsthat core outlays for education, health, and roads are in line with the PER projections. Therefore, oneof the basic PER conclusions--that the government has so far protected per capita and real spendinglevels in priority areas-remains valid.

Executive Summary iii

the specific financial reporting system-which is required by donors and has been agreedto by the government-was not operational (such as, IDA support to the education andhealth sectors). In addition, there are technical bottlenecks within the government tomove funds to the beneficiary level, for example, the insufficient capacity to handle asubstantive increase in civil works contracts and tenders for procurement of goods.

6. Delays in the release of external resources due to political considerations arecertainly another reason for the slowdown in disbursement of external financing inFY98/99. In a number of cases, donors have adopted a wait-and-see approach infinalizing their support to sector programs because of concerns about the fungibility ofresources and the possibility to indirectly fund the defense budget, combined withhesitation in donor capitals to support countries in conflict. A quick survey of donorsshowed that the most serious impact has been on counterpart funds from balance ofpayment support and on new aid commitments, while disbursements under existingcommitments have only been affected marginally. However, future commitments couldbe seriously affected if peace remains elusive in FY99/00.

Expenditures Related to the War7. The long-term decline in Ethiopia's defense expenditure was reversed in FY97/98with the outbreak of the war with Eritrea. Defense expenditure as a share of GDP is nowapproximately triple its historically low level of the mid-1990s, but still significantlybelow the war-time levels in the 1980s. The PER mission estimated the costs of second-round effects of the war between Birr 1,100 million and Birr 1,600 million annually,comprising immediate assistance to the displaced, replacement of assets, and highertransport costs due to the rerouting of freight from Eritrean ports through Djibouti. Thisis equivalent to 2.5 percent and 3.3 percent of GDP per annum in FY97/98 and FY98/99,respectively. Together with the additional defense spending over and above levels of themid-1990s (about 3.8 percent of GDP in FY98/99), the fiscal burden of the war would beequivalent to between 6 percent and 7 percent of GDP per annum in the two yearsconsidered. In addition, because of donors' concerns about the war, external loans andgrants of some Birr 1,500 million have been delayed in FY98/99.2

Fiscal Sustainability of Sector Programs8. Ethiopia faces the challenge of having to balance the need for tremendousincreases in per capita spending in poverty-sensitive areas with the need to maintainfiscal stability. In the past, fiscal constraints have not been binding, becauseimplementation capacity and external resource flows were the primary factors thatdetermined expenditure levels in priority areas. If a peace agreement is reached, thebinding constraints are likely to change. External resource flows will probably notremain a binding constraint if all aid pledges are turned into formal agreements. Withtime, implementation capacity should also improve and help overcome the teethingproblems of the first few years of SP implementation. If so, the overall fiscalsustainability will become the major determinant for the balance between recurrent andcapital expenditure and between spending on SPs and in non-SP areas.

2 After the completion of the PER draft, the Govemnment shared revised projections for FY98/99 with thePER team. The revised data are reflected in Annex 2.

iv Executive Summary

9. A base case scenario-premised on Ethiopia's ability to reach lasting peace,rebuild investor confidence, and reduce the vulnerability to external shocks-assumessubstantial GDP growth of between 5 percent and 6 percent per annum over the next fiveyears. This outcome will require a gradual reduction in defense expenditures and atimely and realistic acceleration of development expenditures in infrastructure, education,health, and social services. Macroeconomic stability will also be underpinned byachieving overall fiscal objectives, including single digit budget deficits (includinggrants) supported by increased foreign exchange inflows and balance of payment support.Conversely, if the war continues, the government's long-term economic growthobjectives and poverty reduction strategy will be jeopardized. The main risks result fromthe cumulative negative impact that the war would continue to have on governmentfinances, public and private investment, and the external current account. These risks addto the challenges that Ethiopia already faces, including weakening of the terms-of-tradeand recurrence of drought in 1999.

10. The base case provides a fiscal envelope that has to accommodate fundingrequirements for SPs and non-SP activities. The appraisal documents for the three SPslay out ambitious annual expenditure targets, which may be feasible individually, but arenot consistent with a sustainable macroeconomic framework if taken together. Even withsufficient external funding, the government's entire resources would not be sufficient tomeet the domestic financing share under the SPs. By FY01/02, the SPs wouldcompletely exhaust the notional capital expenditure envelope and there would be no roomleft for capital expenditure outside the three SPs. This is clearly not a feasible option.

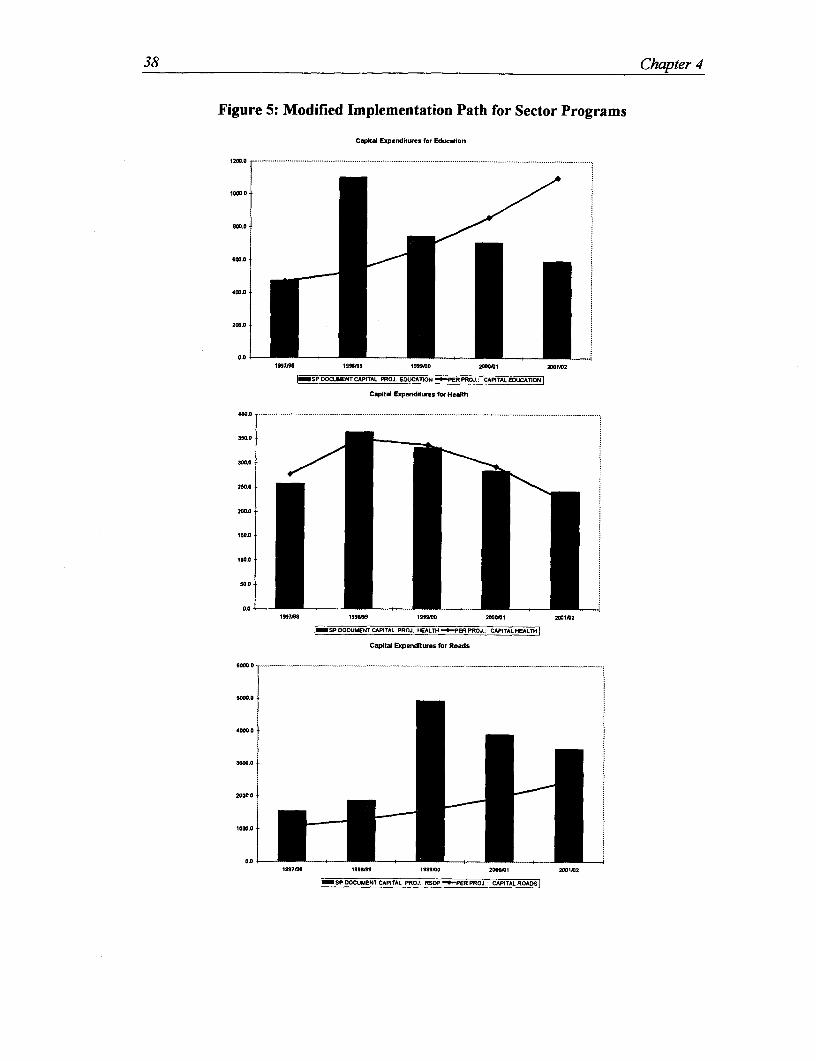

11. Alternatively, the base case could provide room for healthy growth in non-SPspending and still allow for substantial increases in real per capita spending in education,health, and roads, if the implementation timeframes for the three SPs were modified.Originally, all three SPs were heavily front-loaded with the lion's share of disbursementsexpected in the second and third year of a five-year implementation period. These targetsseem no longer attainable in view of the encountered obstacles to a timely mobilization ofexternal resources. In addition, these assumptions are not consistent with overall fiscalconstraints. It is therefore appropriate to envisage a more pronounced back-loading ofcapital expenditures, with gradually increasing disbursements for the education andhealth SPs-thereby maintaining the five-year implementation period-and the extensionof the implementation period for the roads SP from five to seven years'.

Capacity Building in Public Finance Management12. To some degree, the underspending on the capital budget reflects limitedimplementation capacity which is closely linked to the quality of budget planning and thefinancial relationship between the center and the regions. Public finance management inEthiopia is complex because three important reform exercises are proceeding

3Since the fiscal constellation in September 1999 was off the base case and worse than Scenario 3, whichhad assumed higher defense spending and a continued slow-down in aid disbursements, a 4h Scenariowas computed to gauge the impact of higher defense spending with a resulting higher fiscal deficit(financed by domestic credit expansion). The results for that scenario are presented in the Annex 2, aspart of the outcome of the Debre Zeit PER workshop.

Executive Summary v

simultaneously: fiscal decentralization, civil service reform, and comprehensive sectoralbudgeting and sector development programs. The PER reviews each area of reform withregard to its implications for effective expenditure execution.

Decentralized Budgeting13. In general, budgeting procedures in the regions broadly mirror the federal systemand echo federal financial regulations. Besides exhibiting the considerable strength of adisciplined, well-documented, systematic process, there are also inherent weaknesses inregional budgeting. These weaknesses are reflected by the pervasive separation betweenrecurrent and capital budgets. Budget preparation is often done without the knowledge ofceilings (so-called "blue-sky budgeting"). The one-year budgeting horizon createsinflexibility. There are capacity limits at zonal and especially woreda levels, and timelyreporting on budget implementation is weak. There are also problems with incorporatingaid into the regional planning and budget system. To incorporate donor funds into theirbudgets, regions and zones need to know the amount, the source, and any specialconditions attached to such funds. This information needs to be available well before thefiscal year begins to include it in the budget and allow the timely implementation ofdonor-funded activities. This PER develops the observation that the "offset" system, as itis currently operated, leads local governments to prefer central government fundingrelative to aid-financed projects, because of simpler procedures associated with theutilization of resources.

Reform of Expenditure Management14. In parallel with the decentralization, Ethiopia embarked on a comprehensive CivilService Reform (CSR). The PER focuses in particular on the Expenditure Managementand Control component (EMC) which aims at strengthening financial managementsystems.

* In 1996, the Financial Legal Framework was promulgated. Atpresent, the legislative drafting and approval process for numerousrequired regulations, directives and guidelines is underway. Priorityshould be given to issue the remaining financial directives, inparticular those on budget management, including the budget calendar,procedures of budget control, and procedures for submission ofsupplementary appropriation.

* The 1997 and 1998 PERs recommended the preparation of a three-yearMedium-Term Expenditure Framework (MTEF) to strengthen theweak link between policy formulation, planning, and budgeting. Thegovernment has accepted this recommendation and has launched aprocess that will eventually culminate in an MTEF by expanding thePublic Investment Program (PIP) into a Public Expenditure Program(PEP), which would cover both capital and recurrent expenditures andwould be based on a Macroeconomic and Fiscal Framework (MEFF)that accounts for total revenue and expenditure commitments. Thegovernment also plans to roll out the federal PIP to the regions. The

vi Executive Summary

first round of the PIP (FY98/99-00/01; EFYs 1991-1993) wasconsidered a dry run. The preparation of the second round PIP hasbeen obstructed by uncertainties about the war. Operationalization ofthe PIP/MEFF exercise is extremely important and should be the toppriority for the FY0O/Ol budget exercise. The Ministry of EconomicDevelopment and Cooperation (MEDaC), in conjunction with theMinistry of Finance (MoF), should take the lead: intensivecoordination with the donors will be indispensable.

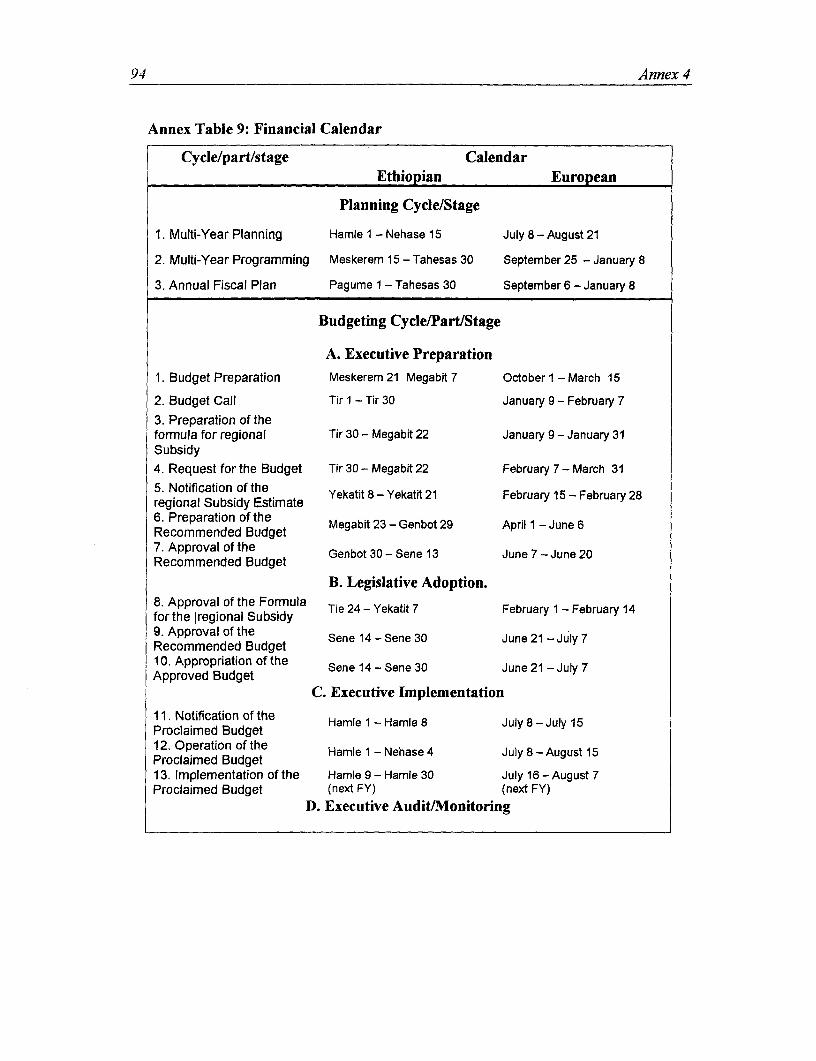

+ The aim of the budget reform component is to produce annualbudgets of a higher quality on a federal and regional level in a moretimely manner by moving towards activity-center (also called cost-center) budgeting. The two Budget Reform Design Manuals that havealready been completed lay out the revised procedures for capital andrecurrent budgeting at federal and regional levels, and introducechanges in the structure of the budget with regard to classification,expenditure codes, revenue codes, financial calendar, and budgetformats. It is critical that the new principles and guidelines forbudgeting permeate through all government institutions, at a centraland regional level. Specific follow-up is required on theimplementation of the financial calendar, which covers both planningand budgeting cycles, and aims at the adequacy and the timeliness ofthe budgeting exercise. Some difficulties encountered during thepreparation of the budget for FY99/00 were to a large extent due to theabsence of such an authoritative calendar.

+ The components on accounting and audit are the least advancedwithin the EMC program because of a shortage of donor funding anddelays in contracting consultants. It is important that EMC-management accelerates the implementation of these components. Inparticular, the government needs to operationalize the financialreporting system on the use of donor funds under the SPs foreducation and health.

Sector Development Programs15. The preparation of SPs in education and health has materially assisted thedefinition of policies and expenditure programs. However, less attention seems to havebeen paid to the integration of SP implementation with regular government budgetprocedures, and in particular to the programming of donor funds. The PER missionfound large discrepancies between the government's estimates/projections of externalresource flows and donors' planned aid disbursements. This raises a number of issues.Inconsistency between donor and government records is clearly a problem (reflecting theextent to which disbursement is still taking place outside the government budget) becauseincomplete recording of aid flows make budget planning and the calculation of regionaloffsets a matter of chance.

Executive Summary vii

Cross-Cutting Issues16. The three areas of reform-decentralization, strengthening of expendituremanagement and control, and sector development programs-are all making goodprogress. All, however, involve major institutional change which naturally takes years toconsolidate. Moreover, donors have an important role to play in supporting the reformsthat the government is undertaking and in helping to ensure a coordinated approach. ThePER identifies steps to strengthen the government's strategic planning of publicexpenditure and makes recommendations for better management of aid within thegovernment's strategic planning framework.

* Important steps to improve the strategic planning of publicexpenditure have already been taken through the preparation of theSPs and the launching of the MEFF/PIP exercise. It is now importantto move swiftly to a full MTEF/PEP to ensure that medium-termexpenditure plans are consistent with resource availability, and thatbudget holders are able to plan and implement expenditures effectivelyand efficiently. To operationalize the medium-term planning of publicexpenditure, the government now needs to adopt and adhere to theproposed financial calendar. There needs to be broad acceptance of anMTEF or PEP as a new way of budget planning. The MoF andMEDaC need to collaborate systematically in preparing the MEFF andin proposing indicative planning figures. When the PIP is extended tothe regions, sector planners should be required from the outset toprepare consistent medium-term plans for both recurrent and capitalexpenditure, and regional and zonal councils should be required toundertake joint reviews of recurrent and capital budgets for eachsector.

+ The collaboration of aid agencies is essential to achieve more rationalplanning and utilization of public expenditure. Credible projections ofaid flows are an essential input into the MEFF and are needed for threeor four years ahead, not just for the imminent budget year. Anessential foundation for MEDaC is to maintain, with donor assistance,a reliable and comprehensive database of ongoing and expected aidprojects and programs, which can be clearly mapped into the SPs thathave been agreed, as well as into the PIP and successive annualbudgets. In addition, the government and donors need to collaboratein making projections of aid flows available to the regions withsufficient advance notice to take them into account for budgetpreparation (by end-December if the proposed financial calendar is tobe observed). The government should continue to encourage aidagencies to move towards unearmarked Channel 1 support.

* The budget "offset" system continues to be an obstacle to the rationalutilization of aid. The Government has taken steps to address this

viii Executive Summary

issue and has carried out an analysis with the aim to improve thesystem. Without departing from the principle of regional equity, thefollowing improvements could be adopted. The planning bodies'projections of aid flows should be published when ceilings areannounced, so that the offset is transparent. In subsequent years, theseprojections should be compared with actual aid flows, and, if there aresignificant divergences, adjustments should be made. The aim shouldbe to achieve equity in the actual flow of resources to regions (andwithin regions to zones) not just in the expected resource flows.Ceilings for Treasury funds and for aid should be clearly separated,and it should be made clear that if regions are unable to utilizeavailable aid in a given budget year, it will normally remain availablein subsequent years. If implementing agencies can clearly see that aidis additional, and can be drawn down over a practical time frame, theyshould be more ready to invest the additional effort needed to utilizeaid funds.

PER Process and Focus17. The Ethiopia PER is an annual exercise carried out by the government anddonors. The 1999 PER expands on previous PERs by focusing more on a continuousprocess and dialogue on public expenditures than on the production of a final report.With this objective in mind, two follow-up workshops are planned with the governmentand with the donors to explore the implementation of the PER recommendations and tolink the PER process closer with the budget planning cycle. The partnership aspect of thePER process is reflected by the close collaboration on analytical issues and the

4commitment to a more systematic follow-up process.

18. There are implications both for the scope and for the timing of future PERs. Asregards timing, it is proposed to undertake future PERs much earlier in the fiscal year inorder to support the planning phase, rather than the budgeting phase, of the financialcalendar. As regards their scope, future PERs can be important in reconcilinggovernment and donor estimates of aid flows, and could help extend the sector dialogueassociated with the SPs into a broader dialogue on overall public expenditures andenhancing the poverty impact of government and donor assistance. This could supportfurther progress towards provision of aid in the form of unearmarked budget support.While recent PERs have focused mainly on budget inputs, it will be necessary to shift thefocus of the next PER to the effectiveness and efficiency of public spending. This aspectwill become particularly relevant in the context of Ethiopia's envisaged participationunder the HIPC debt initiative.

4Summaries of the main findings and agreements of those two workshops are attached in the Annexes.

CHAPTER 1: INTRODUCTION

SETrING

1. Since May 1998, the war between Ethiopia and Eritrea has been the center ofattention of the Ethiopian government and its donors. In addition to the human toll of thewar, there have been concerns that the sharp rise in defense expenditure could jeopardizethe substantive macroeconomic and structural progress made in recent years. At the timeof writing this report, efforts to reach a peaceful resolution of the war are continuing.Although the fiscal data for the past two years is still incomplete or preliminary, it allowssome important conclusions.

2. Ethiopia has followed a policy of not permitting the war to interfere with theconsolidation of macroeconomic stability and continuation of structural reforms. Indeed,with the exception of the floor on net foreign assets of the banking system, all thequantitative targets under the 1998/99 program with the IMF were met. Despite theshortfalls in official loans and grants official reserves at the end of FY98/99 are expectedto be slightly higher than one year ago (in months of import coverage). The governmenthas appropriately protected core spending in priority sectors, while financing theincreased defense budget through extraordinary revenue efforts, including one-timefinancing measures such as utilization of privatization receipts.

3. Yet the fiscal stress posed by the war is reflected in the projected fiscal outcomefor FY98/99, which is a clear outlier to the trend and deviates substantially from thegovernment's intentions and objectives as reflected in the original and revised budgets forthe fiscal year. Prudent fiscal policies and the timely resolution of the conflict are twocritical elements that will help Ethiopia limit the short and medium-term economicimpact of the war. Conversely, if the war continues, the govemment's long-termeconomic growth objectives and poverty reduction strategy will be placed in jeopardy.The main risks result from the cumulative negative impact that the war would continue tohave on government finances, public and private investment, and the external currentaccount. These risks add to the challenges that Ethiopia faces including weakening of theterms-of-trade and recurrence of drought in 1999.

Focus OF THE 1999 PER

4. The Ethiopia PER is an annual exercise of the government and donors. The jointeffort is reflected by the strong collaboration during the field mission, sharing ofinformation, a common approach to the analyses, and a strong buy-in to the follow-upprocess and sharing of recommendations of the report. For the next PER, it is envisaged

2 Chapter ]

that the government will also share in the drafting of background notes for the PERmission.

5. The PER has become a key analytical tool for allocation of public expenditure inline with the overall resource envelope and the broad range of development priorities. Inline with Ethiopia's partnership approach to external assistance, PERs have becomeincreasingly important in the dialogue between the government and the donorcommunity. Typically Ethiopia's PERs center on the resource framework, budgetsystems, and expenditure patterns. In addition, each PER includes a specific analyticalfocus on key issues or recent developments with a view to developing specificrecommendations for improving the design and implementation of priority sectorexpenditure programs.

6. The 1999 PER-the sixth PER since 19945 -builds upon and expands thepartnership approach started in 1997. The 1999 PER expands on previous PERs in that itis no longer focused so much on the production of a final report, but aims at a morecontinuous process and dialogue on public spending. With this objective in mind, thegovernment shared the Aide Memoire of the main PER mission with the donorcommunity at large in May 1999. The donor community responded well to the AideMemoire and followed up on a number of findings individually, as well as in the contextof the Annual Review Meeting (ARM) of the Sector Programs6 (SP) for education andhealth. Two follow-up workshops are planned with the government and with the donorsto pursue the PER recommendations and to link the PER process closer with the budgetplanning cycle7.

7. The 1999 PER has a more limited scope than originally envisaged. The mainfield work for the PER was originally scheduled for mid-February 1999, with theintention to build upon the outcome of the IMF mission that, among other things, was toassess the government's current macroeconomic stance. As the IMF mission left AddisAbaba early because of security concerns, the PER mission was postponed. During thecontinuation of policy discussions between the IMF and the Ethiopian authorities in April1999, the government presented a revised set of fiscal projections for FY98/99, whichprovided the basis for the analyses during the May 1999 PER mission.

8. The main PER mission focused on the original issues presented in the ConceptPaper (January 15, 1999), except for the fiscal assessment of debt relief under the HiPC

5The previous reviews of Ethiopia's public finances were: Ethiopia: Public Expenditure Policy inTransition, Report No. 12992-ET, October 1994 (1994 PER); Ethiopia: Public Expenditure Review,World Bank "White Cover" Report, May 1995 (1995 PER); Paul Collier (ed.), Ethiopia: Social SectorReview, Center for the Study of African Economies, Oxford University, July 1996 (1996 PER);Ethiopia: Public Expenditure Review, Report No. 16593-ET, November, 1997 (1997 PER); andEthiopia: Public Finances, Report No. 18369-ET, December, 1998 (1998 PER).

6 The term Sector Programs is used to refer to Sector Investment Programs (SIP) as well as SectorDevelopment Programs (SDP).

Outcome and main findings of these two workshops are attached in the Annex.

Introduction 3

Debt Initiative8. The 1999 PER also deviates from the general trend of the "newgeneration" PERs, which focus more on effectiveness and efficiency of public spendingrather than on budget composition and inputs. In view of the war, there is an overridinginterest in the impact of the war on public spending. Consequently, one major area ofattention of the present report is to review the macroeconomic impact of the war and thefinancing of the associated defense expenditures, and to determine whether defensespending pressures have diverted resources from priority development programs. Themajor areas of focus of this report follow:

* Recent Fiscal Developments: Has the trend toward fiscalstabilization continued? How has the war with Eritrea affected fiscalaggregates?

* Fiscal Sustainability: In light of lessons learned from the first twoyears of implementation of SPs in education, health, and roads, whatare the implications for their fiscal sustainability? What are theoptions for modifications in the financing and timing framework of theSPs?

+ Public Finance Management: The PER reviews the progress inimplementing measures to improve budget formulation and execution,and identifies areas for additional measures to enhance theeffectiveness and efficiency of public spending by focusing on therelationship between the center and the regions.

* PER Process: The follow-up process to the PER and a morecontinuous dialogue on public expenditures between the governmentand the donors are central components of the. 1999 PER. The reporthighlights the implications for future PERs.

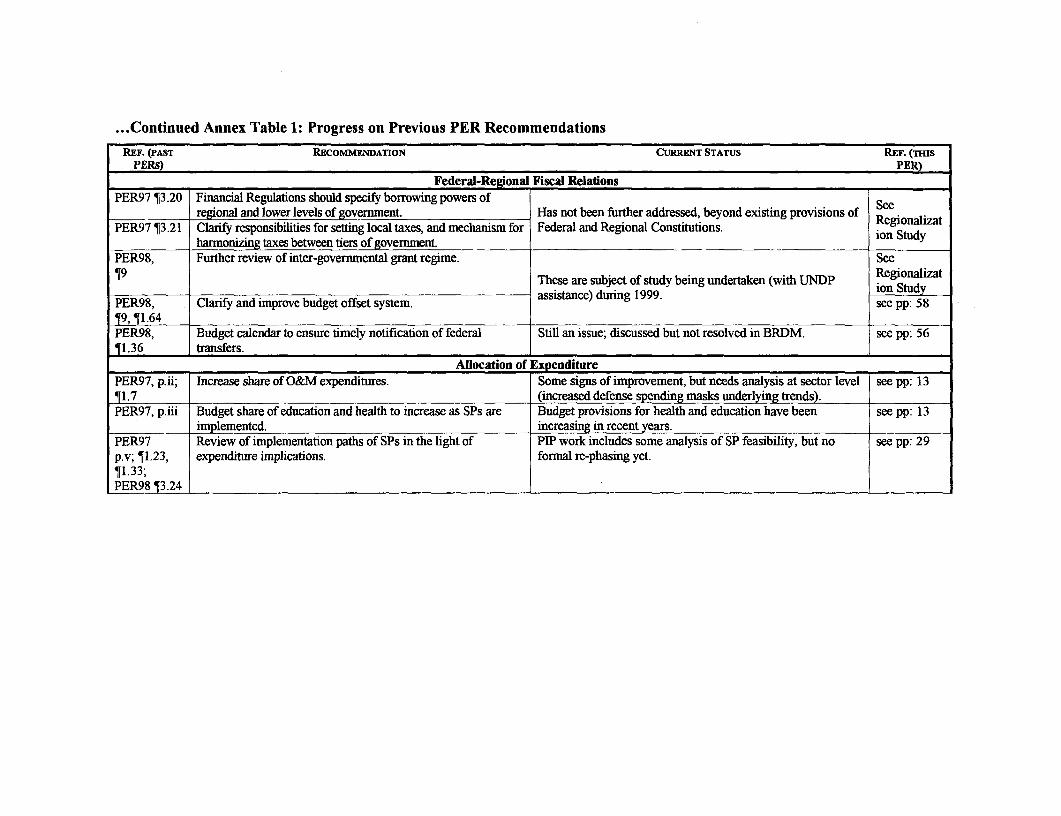

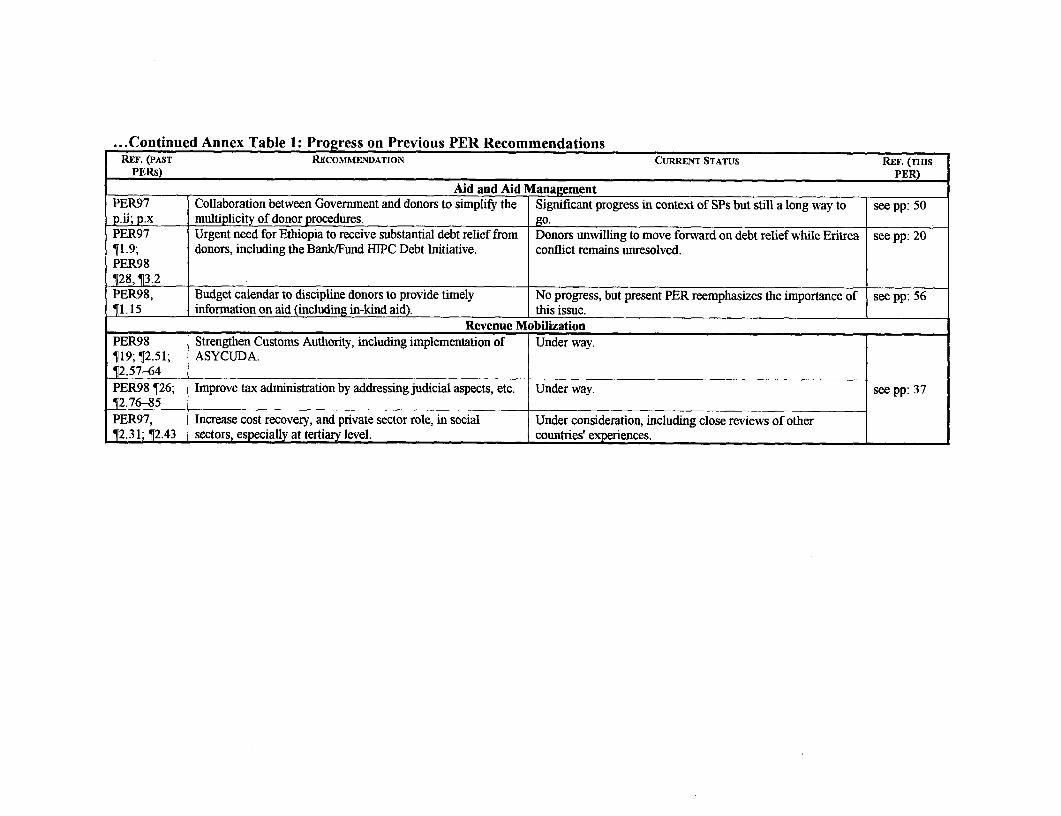

STATUS OF PREVIOUS PER RECOMMENDATIONS

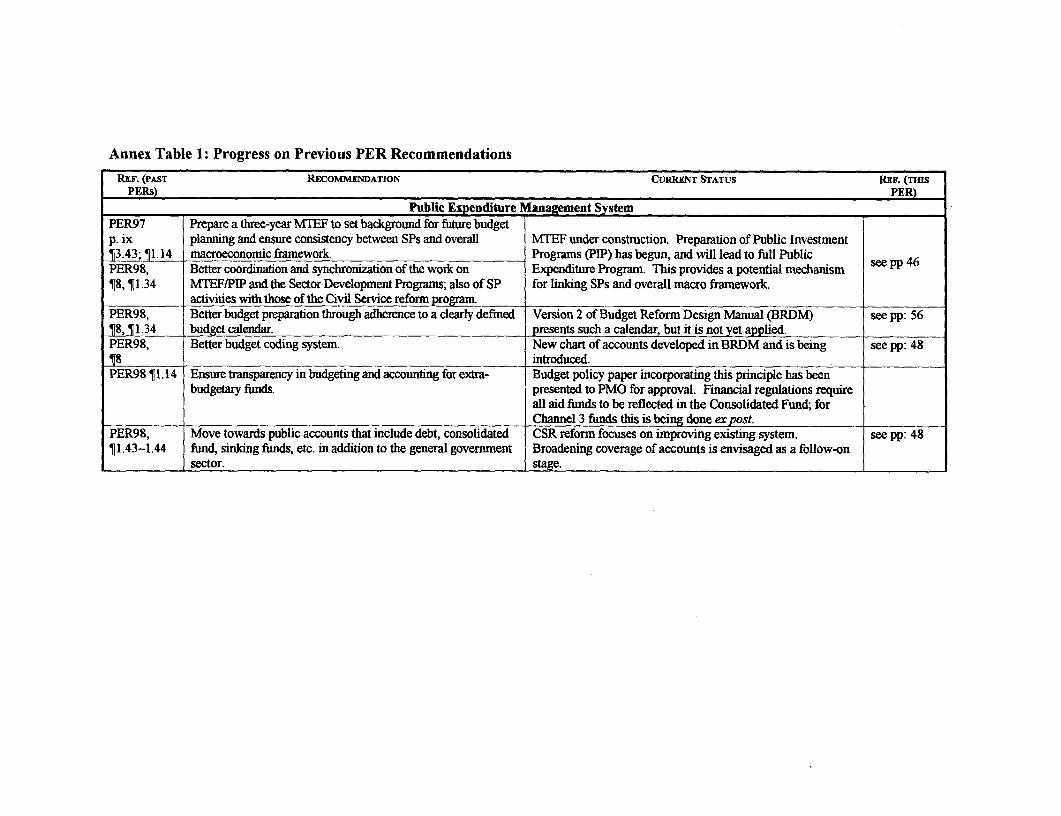

9. Considerable progress has been made with regard to recommendations made inprevious PERs. A summary of previous PER recommendations and their status ofimplementation is presented in Annex Table 1. The main focus of the 1997 and 1998PERs was-in addition to the review of fiscal trends-on Ethiopia's expendituremanagement system, tax and expenditure assignments in the context of fiscaldecentralization, the sustainability of public expenditure, and revenue mobilization andaid management.

10. With a view to improve public expenditure management within a Medium-Term Expenditure Framework (MTEF)-a core recommendation of the 1997 PER- the

8The compilation of debt data for the HIPC Debt Initiative has been delayed with the IMF ESAF Mid-Term Review.

4 Chapter I

government has embarked on a complex process that will expand the Public InvestmentProgram (PIP) into a Public Expenditure Program (PEP). This will provide a mechanismfor linking the sector programs with the overall macroeconomic framework and capitalwith recurrent expenditures. Several PER recommendations are being implemented inthe context of the Civil Service Reform (CSR) program launched in 1996. Under theExpenditure Management and Control (EMC) component, good progress has been madewith regard to enhancing transparency of the budget process. For instance, two BudgetDesign Manuals have been prepared, the chart of accounts has been updated, and abudget calendar has been designed. In the next phase, these new procedures will need tobe implemented on the ground.

11. The fiscal relations between the center and the regions were addressed in both,the Regionalization Study and previous PERs. Only limited progress has been made oncore recommendations, such as the need to clarify the borrowing powers of regionalinstitutions, illuminate the responsibilities for setting local taxes, and improve the budgetoffset system. A study supported by UNDP focuses on the inter-governmental grantregime, and budget offset is ongoing. The other issues have not been resolved andprobably will need to be addressed in the context of a center-region dialogue.

12. Good progress has been made with regard to the implementation of a number ofrevenue mobilization measures. The Federal Inland Revenue Authority and CustomsOffice were initiated and the computerized customs reporting and recording system(ASYCUDA) was introduced at the main customs station. It is now being madeoperational along with the introduction of taxpayer identification numbers. Penalties andinterest charges are levied on late tax payments, and the tax fraud unit is being expanded.The expansion of cost recovery measures, user charges, and a greater role of the privatesector are under consideration, however, without visible progress to date.

13. The improvement of aid management has taken a major step forward with threeSPs in education, health, and roads. Policy discussions and aid flows are bettercoordinated and options for harmonization of implementation arrangements are beingexplored. However, there is still a long way to go toward providing budget support andadopting one set (preferably the government's) of implementation procedures. Theagreed financial reporting system for the SPs is not yet operational.

14. The fiscal sustainability of the three SPs and the required inter-sectoralexpenditure allocations have been investigated in the two previous PERs. Budgetprovisions for the three SPs have been increasing in recent years; yet these lag behind theambitious targets set out in the appraisal documents. Actual spending has not reachedbudgeted levels. There are clearly costs plus lost credibility-associated with over-optimistic implementation projections. In addition, it is necessary to identify the bindingconstraints to implementation. It has not become clear whether these are deficientimplementation capacity, insufficient external resources, or overall fiscal constraintswithin a sound macroeconomic framework. This aspect will be explored in the currentPER.

Introduction 5

DATA ISSUEs-AN IMORTANT CAVEAT

15. The main mission for the 1999 PER took place in May 1999. At that time,detailed fiscal accounts for FY98/99 were available for seven months of the fiscal year.For the mission's Aide Memoire, the PER teams decided to use the government'sprojections for the fiscal year. In May 1999, the government had projected a fiscal deficit(on a cash basis and including grants) of 2.1 percent of GDP and defense expenditure of4.6 percent of GDP.

16. As the fiscal year progressed and additional fiscal data were made available, itbecame clear that actual performance would probably not meet the government'sprojections. As a result, the IMF's 1999 Article IV consultation staff report (issued inmid-July 1999) projected a fiscal deficit of 4.3 percent of GDP and defense expendituresof 5.8 percent of GDP. From the most recent federal government data for 11 months ofthe fiscal year, it appears that defense expenditures might even reach a level of more than6 percent of GDP. Consequently, the fiscal deficit might be slightly higher than projectedby the LvIF.

17. The quantitative analyses of this report are based on federal budget data for thefirst 11 months of the fiscal year, and projections made by the PER teams. Theprojections for fiscal aggregates are broadly consistent with the data in the IMF's ArticleIV consultation staff report and will be revised in light of the planned discussions withthe government in September.

18. In the PER discussion workshops in Debre Zeit and Brussels, the Governmentmade available revised projections for FY98/99. In comparison to the PER data base, thelatest fiscal estimates indicate that defense expenditures may reach a share in GDP closeto 7 percent, and 1.2 percentage points higher than the PER estimate. Despite theincrease in defense spending (compared to earlier projections) it appears that core outlaysfor education, health, and roads are in line with the PER projections. Therefore, one ofthe basic PER conclusions--that the government has so far protected per capita and realspending levels in priority areas--remains valid.

CHAPTER 2: DEVELOPMENTS IN BUDGETARYAGGREGATES

FISCAL TRENDS

Despite the war, Ethiopia has managed to avoid a significant reversal inoverall fiscal trends. Nevertheless, fiscal performance over the past twoyears could put the long-term positive trend in jeopardy.

19. Public expenditure trends underscore Ethiopia's improved fiscal performance andprogress towards fiscal stabilization over the past 12 years, although FY98/99 is a clearoutlier compared to the trend. Therefore, a timely correction in expenditure levels andcomposition is necessary-preferably in FY99/00-to help preserve Ethiopia's mediumto long-term progress towards fiscal sustainability. Details on fiscal aggregates arepresented in Table 1.

20. The period FY86/87-98/99 can be divided into three distinct sub-periods: the latecivil war period (FY86/87-90/91), the reconstruction period (FY91/92-94/95); and thestabilization period (FY95/96-98/99). A comparison of fiscal performance over the threesub-periods reveals a steady decline in the fiscal deficit on cash basis (before and aftergrants), thus underscoring Ethiopia's strong commitment to fiscal discipline. Theaverage general government fiscal deficit before grants declined from 10.7 percent ofGDP to 8.6 percent and 6.0 percent over the three sub-periods. Similarly, thecorresponding fiscal deficit after grants also declined from 7.1 percent of GDP to5.8 percent and 3.1 percent.

21. On the revenue side, the performance has been uneven over the three sub-periods.The total ratio of revenue and grants to GDP decreased from 24.6 percent duringFY86/87-90/91 to 16.5 percent during FY91/92-94/95, but increased to 21.6 percentduring FY95/96-98/99. Total expenditure, on average, declined from 31.7 percent ofGDP during FY86/87-90/91 to 22.4 percent during FY91/92-94/95, but increased to24.9 percent of GDP during FY95/96-98/99 due to a commendable rise in the share ofcapital expenditure from 7.5 percent of GDP to 9.5 percent, but more recently mainly onaccount of increased defense spending. Over the period FY86/87-98/99, the capitalexpenditure to GDP ratio rebounded to levels equivalent to those in the late 1980s.Recurrent expenditure however, has been reduced from 22.1 percent of GDP in the late1980s to between 14.9 percent and 15.4 percent over the past two sub-periods.

8 Chapter 2

Table 1: Fiscal Trends

------------ Average-FY FY FY

Share of GDP (%) 86/87-90/91 91/92-94/95 95/6-98/99 FY9S/96 FV96/97 FY97/98 Ff98/99-------------- Actual--------------- Actual Pre-Actual Pre-Actual PER

Proj.

Tot. Revenue & Grants 24.6 16.5 21.6 21.3 22.6 21.5 21.2Total Revenue 21.0 13.7 18.8 18.4 19.0 18.7 19.0

External Grants 3.6 2.8 2.9 2.9 3.6 2.8 2.2

Total Expenditure 31.7 22.4 24.9 24.1 24.2 25.3 25.7Recurrent Expenditure 22.1 14.9 15.4 14.9 13.8 15.9 16.9

Capital Expenditure 9.6 7.5 9.5 9.4 10.4 9.5 8.8

Fiscal Deficit(cash)Before grants -10.7 -8.6 -6.0 -5.7 -5.2 -6.8 -6.5

After grants -7.1 -5.8 -3.1 -2.9 -1.5 -3.9 -4.3Source: Ministry of Finance, World Bank Database, and IMF staff estimates (July 1999);Note: Expenditure excludes net lending.

RECENT FISCAL PERFORMANCE: BUDGET TARGETS VS. OUTTURNS

The projected outcome for FY98/99 deviates significantly from thegovernment's intentions and objectives as reflected in the original andrevised budgets for the fiscal year. Moreover, underspending on thecapital budget (estimated at 3.5 percent of GDP) is more pronounced thanin previous years.

22. In May 1999 at the time of the PER mission, the government projected fiscalimprovement and progress towards fiscal consolidation for FY98/99. The revised budgetfor FY98/99 envisaged a rebound in external grants and mobilization of additionaldomestic revenue that would allow capital expenditures to reach a historically high levelof 12 percent of GDP. In parallel, a reduction in recurrent spending (assuming a declinein defense expenditures from FY97/98 levels) would have allowed the government toreduce the fiscal deficit before grants to below 5 percent of GDP and contain the fiscaldeficit after grants at around 2 percent of GDP.

23. Additional data through May 1999 for the federal government budget (the latestavailable data) indicate that the actual outcome for FY98/99 will not meet thegovernment's projections. Total expenditure and revenue-plus-grants for FY98/99 arenow projected at Birr 10.4 billion and Birr 12.6 billion, respectively. Still based onpartial data for FY98/99, the fiscal deficit before grants is projected at 6.5 percent ofGDP, in line with the revised budget target and very close to the pre-actual for FY97/98(Table 2). However, the projected fiscal deficit after grants (4.3 percent of GDP) issubstantially above the target of 3.2 percent of GDP and also above the correspondingFY97/98 level.

Developments In Budgetary Aggregates 9

Table 2: Budget Execution

Fiscal DeficitFY97/98 FY98199

Revised Pre-Actual Revised Pre-ActualBudget Budget

Fiscal Deficit (cash basis)Excluding Grants .- 7.4 -6.8 -6.7 -6.5Including Grants -2.8 -3.9 -3.2 -4.3

Total Revenue and Grants 24.5 21.5 24.0 21.2Total Revenue 19.9 18.7 20.5 19.0

External Grants 4.6 2.8 3.5 2.2

Total Expenditure 27.3 25.3 27.2 25.7Recurrent Expenditure 15.4 15.9 14.9 16.9

Capital Expenditure 11.9 9.5 12.3 8.3Source: Ministry of Finance, World Bank Database, and PER estimates (July 1999).Note: Expenditure excludes net lending.

24. Total revenue and grants are projected at 21.2 percent of GDP (similar inmagnitude to the 21.5 percent in FY97/98) and clearly below the FY96/97 pre-actual.The discrepancies between targets and projected outturns on the revenue side arecomparable to FY97/98, with external grants projected to reach only two-thirds of thebudget target and domestic revenues reaching 93 percent of the budget target. Theshortfall on domestic revenues is mainly attributable to the lower-than-budgeted taxreceipts. A closer examination of the past four fiscal years reveals the offsetting effectsof a continuous and substantive decline in the ratio of external grants to GDP and anincrease in the ratio of domestic revenue (tax revenue plus non-tax revenue) to GDP. Thedecline in external grants has been in the order of between 1 - 1.5 percent of GDPbetween FY96/97 and FY98/99.

25. Total expenditure is projected at 25.7 percent of GDP, thus remaining around thesame level as in FY97/98. Recurrent expenditure is projected to continue to increasefrom 15.9 percent of GDP in FY97/98 to 16.9 percent in FY98/99 while the share ofcapital expenditure is projected to further decline from 9.5 percent of GDP in FY97/98 to8.8 percent of GDP in FY97/98. It is striking, however, that the offsetting effects ofunderspending on the capital budget (equivalent to 3.5 percent of GDP) and overspendingon the recurrent budget (equivalent to 2 percent of GDP) are more pronounced inFY98/99 than in previous years.

26. The large discrepancy between capital expenditure budget targets and outcomes isof particular concern with regard to the ambitious sector programs in education, health,and roads. Disbursement of capital expenditures in the three priority sectors is expectedto reach only two-thirds of the revised target in FY98/99, and will remain even behind theprevious year's performance, thus exacerbating implementation delays (Figure 1).

10 Chapter 2

100

90-/_

80-/:0

Helt Education Reads

60 /0-: -0:;j4-

Percent 50 o_- 0 _I1FY79

Z'- 0 0 000i0i i0 FY98199|30- //j 02 0020- 000

20- /Z_ 0

Health Education Reads

Sectors

Figure 1: Capital Budget Implementation Rate in Priority Sectors

27. In theory, the chronic underspending on the capital budget could be (a) thereflection of chronic over-optimism when setting budget targets and/or (b) the effectof deliberate budget cuts (during the fiscal year) to increase funding for other budgetitems9. The former effect could be the result of either continuous overestimation ofimplementation capacity or recurrent overestimation of available resources. The lattereffect (deliberate budget cuts), because of the war, is a particular concern to donors, whowere alarmed by the rising financing needs for defense during the fiscal year. In anycase, chronic overestimation of budget allocations carries significant economic costswhich are summarized in Box 1.

9It should be noted that 100% implementation of capital budgets is unlikely to ever be achieved.Expenditure discipline means that all projects are prevented from spending more than the budgetedamounts. Inevitably some projects will experience delays. The overall implementation rate willtherefore never reach 100%.

Developments In Budgetary Aggregates 11

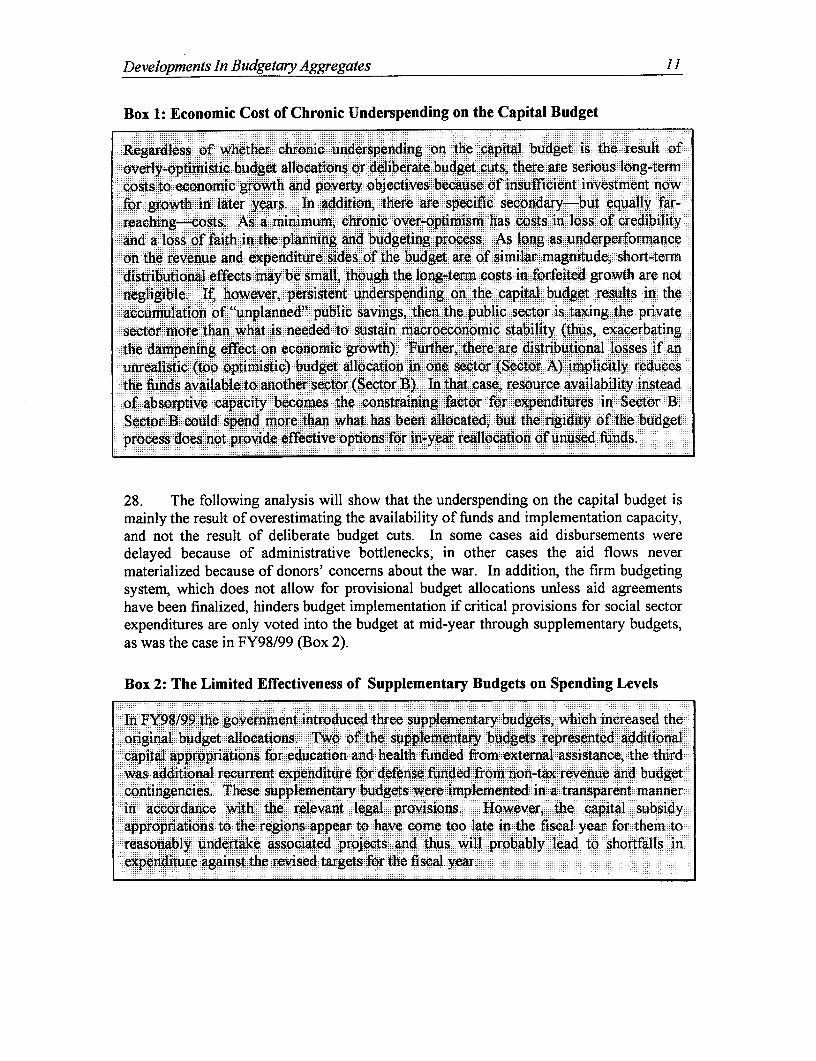

Box 1: Economic Cost of Chronic Underspending on the Capital Budget

Regardless of whethert.chronic.'undrspending' onthe capDil budget is the result ofoverly-optimistic' budget allocations:or deliberate budgetc..uts, there are serious long-termcosts to economic growth and poverty objectives,.because of insufficient investment nowfbr growth: in later years. In addition,. there are specific isecondary-but equally far-reaching-costs. As -a minimum, chronic over-optim,ism has costs in: loss of credibilityand a loss of faith in the planni.ng and budgeting proess, As long as underperformanceon the revenue and expenditure sides. of the.budget are of similar magnitude, short-termdistributional effects m,.ay be small, thou h the lon-term costs in frfeited growth are notnegligible. ' If, however, persistent u Ierspending on :the. cpital budget results in theaccumulation of "unplanned"' public savings, thenAthe public sector is taxing the privatesector more than::what.is. needed to sustain matcroeconomic stability (thus, exacerbatingthe dampening effect:on economic growth). Further, there.are distributional losses if anunrealisic(too optimisc) budg't iallcation in one sector (Sector A) implicitly reducesthe funds available to another sector (Sectr B). In.thatfcase, resource availability insteadof::abs,optiv,e capacity becomes the constraining factor fo:r expenditures in :Sector B.Sector B .culd spend .more than w'hat.h has been. allocated, but the 'rigidity of the budgetprocess does.not provide effective.options fobr in-year reallocation of unused funds.

28. The following analysis will show that the underspending on the capital budget ismainly the result of overestimating the availability of funds and implementation capacity,and not the result of deliberate budget cuts. In some cases aid disbursements weredelayed because of administrative bottlenecks; in other cases the aid flows nevermaterialized because of donors' concerns about the war. In addition, the firm budgetingsystem, which does not allow for provisional budget allocations unless aid agreementshave been finalized, hinders budget implementation if critical provisions for social sectorexpenditures are only voted into the budget at mid-year through supplementary budgets,as was the case in FY98/99 (Box 2).

Box 2: The Limited Effectiveness of Supplementary Budgets on Spending Levels

In FY98/99:the government-introduced three :supplementary.budgets, which increased theoriginal budget-allocations.'. Two of ithe sup lementary budgets represented additionalcapital appropriations. for education and health funded from.external. assistance,. the thirdwas additional recurrent expeindit.re fr dedense funde from n on-tax revenue and budgetcontingencies. These supplementary budgets were implemented in:a transparent mannerin accordance with the relevant legal provisions. 1lHowever, :the capital subsidyappropriations to, the regions appear to have come too late in. the fiscal year for them toreasotnably undertake associated -projects and: thus .will probably lead to shortfalls inexpenditure agains,t the revised targets fbr the fiscal year.

12 Chapter 2

29. The analysis on whether under-execution on the capital budget is the result ofchronic over-optimism or deliberate budget cuts, however, is only indicative because ofthe dearth of data on the availability of aid and the lack of quantitative data onimplementation capacity. Nevertheless, the following steps should help shed more lighton the issue:

+ As a first step, the development of expenditure shares and real percapita spending could indicate if there has been a deliberate andmajor reversal in the expenditure composition compared to previousyears. The analysis of year-to-year changes in the shares and in realper capita spending is presented in the following section.

+ Second, a review of external aid flows could provide information onwhether external resource availability was overestimated. This part ofthe analysis will be presented at the end of this chapter.

+ Finally, only qualitative information is available with regard toimplementation capacity constraints or over-rigid procedureswhich unduly delay implementation of development projects; thisanalysis is presented in the chapter on budget management.

Developments In Budgetary Aggregates 13

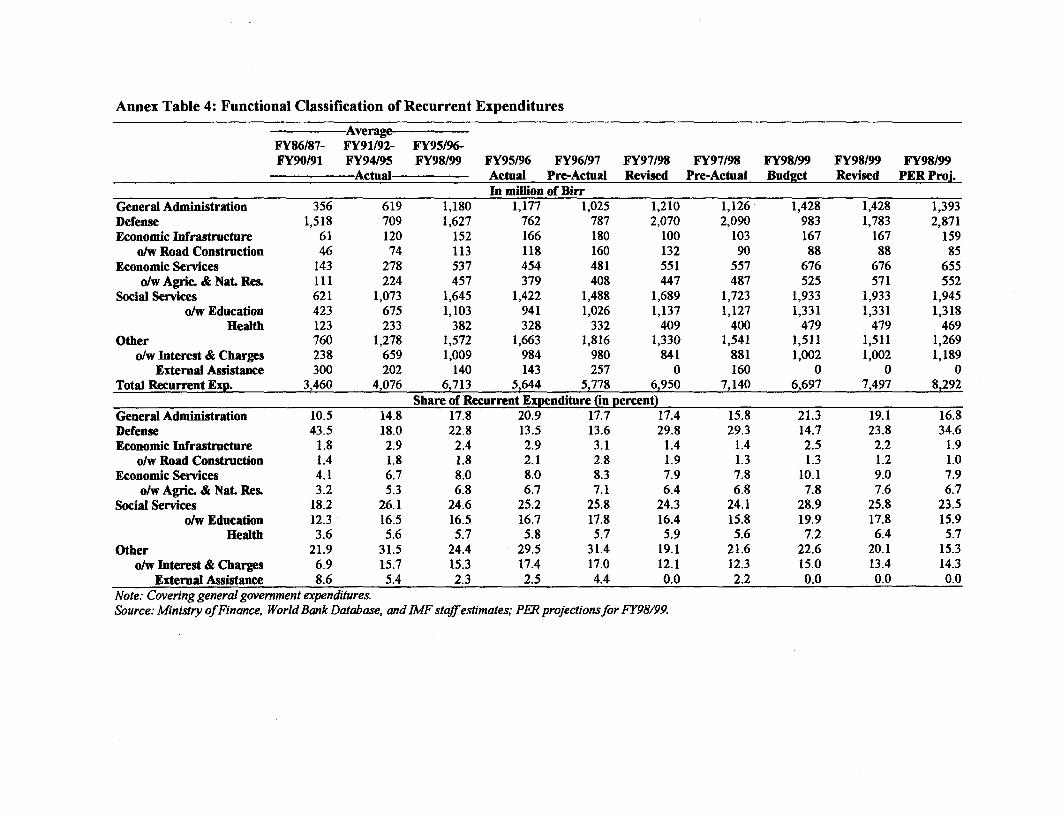

ECONoMIC AND FUNCTIONAL EXPENDITURE CLASSIFICATION

Notwithstanding an overall shift toward recurrent expenditures, especiallydefense, over the past two fiscal years, the functional expenditureclassification reveals that the spending shares for priority areas have beenby-and-large protected. Over the past three years, the expenditure sharesfor education, health, and roads-for total as well as capital spending-have continued to increase.

30. The sharp rise in defense expenditure has resulted in a substantial shift in theexpenditure composition. The year-to-year changes in expenditure shares are much moreremarkable than the development of nominal and real expenditure aggregates net ofdefense. Because of the defense-related increase in recurrent spending, the share ofcapital expenditures in total spending has dropped significantly. Higher defenseexpenditure is also reflected by the striking increase in the share of wages and salariesand of materials and supplies from a combined 38 percent of total expenditure in the pre-war years to over 50 percent in the past two fiscal years (Table 3).

Table 3: Economic Classification of Public Expenditures

FY FY FYIn Million of Birr 86/87- 91/92- 95/96- FY95/96 FY96/97 FY97/98 FY98/99

90/91 94195 98199----------- Actual------------ Actual Pre-Actual Pre-Actual PER

Proj.

Nominal ExpenditureTotal Expenditure 4,937 6,223 10,828 9,206 10,078 11,405 12,624Recurrent Expenditure 3,461 4,076 6,713 5,644 5,778 7,140 8,291

o/w Wages & Salaries 1,259 1,577 2,548 2,101 2,173 2,653 3,266Materials & Supplies 1,255 950 2,329 1,551 1,608 2857 3,300

Capital Expenditure 1,476 2,147 4,115 3,563 4,300 4265 4,333Share in Total Expenditure

Recurrent Expenditure 70.1 65.5 62.0 61.3 57.3 62.6 65.7o/w Wages & Salaries 25.5 25.3 23.5 22.8 21.6 23.3 25.9Materials & Suppies 25.4 15.3 21.5 16.8 16.0 25.0 26.1

Capital Expenditure 29.9 34.5 38.0 38.7 42.7 37.4 34.3Source: Ministry ofFinance, World Bank Database, and PER projections for FY98/99.Note: Covering general government expenditure and excluding net lending.

31. Nevertheless sectoral expenditure reflects the government's commitment toincrease expenditure shares for social services and economic infrastructure. At present,the three priority areas (education, health, and roads) account for almost one-third of totalspending and half of capital expenditures. The dramatic increase in spending shares forthese three sectors was accompanied by the long-term decline in the expenditure sharesfor economic services (excluding agriculture) and-until recently-defense. Theanalysis of sectoral expenditure shares, covering both federal and regional governmentexpenditures, is summarized in Table 4.

14 Chapter 2

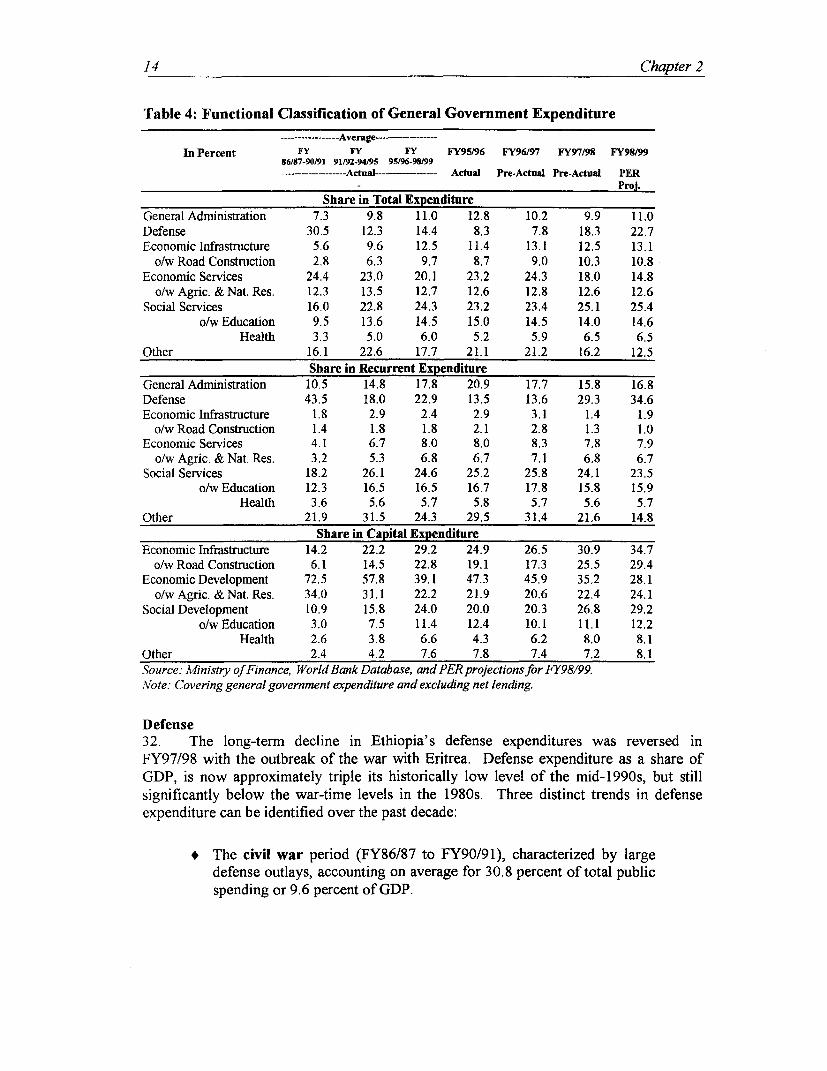

Table 4: Functional Classification of General Government Expenditure

------ Average---------

In Percent FY FY FY FY95/96 FY96197 FY97198 FY98/9986/87-90/91 91s92-94n95 95196-9S199----------------- Actual---------- Actual Pre-Actual Pre-Actual PER

Proj.

Share in Total ExpenditureGeneral Administration 7.3 9.8 11.0 12.8 10.2 9.9 11.0Defense 30.5 12.3 14.4 8.3 7.8 18.3 22.7Economic Infrastructure 5.6 9.6 12.5 11.4 13.1 12.5 13.1

o/w Road Construction 2.8 6.3 9.7 8.7 9.0 10.3 10.8Economic Services 24.4 23.0 20.1 23.2 24.3 18.0 14.8

o/w Agric. & Nat. Res. 12.3 13.5 12.7 12.6 12.8 12.6 12.6Social Services 16.0 22.8 24.3 23.2 23.4 25.1 25.4

o/w Education 9.5 13.6 14.5 15.0 14.5 14.0 14.6Health 3.3 5.0 6.0 5.2 5.9 6.5 6.5

Other 16.1 22.6 17.7 21.1 21.2 16.2 12.5Share in Recurrent Expenditure

General Administration 10.5 14.8 17.8 20.9 17.7 15.8 16.8Defense 43.5 18.0 22.9 13.5 13.6 29.3 34.6Economic Infrastructure 1.8 2.9 2.4 2.9 3.1 1.4 1.9

o/w Road Construction 1.4 1.8 1.8 2.1 2.8 1.3 1.0Economic Services 4.1 6.7 8.0 8.0 8.3 7.8 7.9

o/w Agric. & Nat. Res. 3.2 5.3 6.8 6.7 7.1 6.8 6.7Social Services 18.2 26.1 24.6 25.2 25.8 24.1 23.5

o/w Education 12.3 16.5 16.5 16.7 17.8 15.8 15.9Health 3.6 5.6 5.7 5.8 5.7 5.6 5.7

Other 21.9 31.5 24.3 29.5 31.4 21.6 14.8Share in Capital Expenditure

Economic Infrastructure 14.2 22.2 29.2 24.9 26.5 30.9 34.7o/w Road Construction 6.1 14.5 22.8 19.1 17.3 25.5 29.4

Economic Development 72.5 57.8 39.1 47.3 45.9 35.2 28.1o/wAgric. &Nat.Res. 34.0 31.1 22.2 21.9 20.6 22.4 24.1

Social Development 10.9 15.8 24.0 20.0 20.3 26.8 29.2o/w Education 3.0 7.5 11.4 12.4 10.1 11.1 12.2

Health 2.6 3.8 6.6 4.3 6.2 8.0 8.1Other 2.4 4.2 7.6 7.8 7.4 7.2 8.1Source: Ministry of Finance, World Bank Database, and PER projectionsfor FY98/99.Note: Covering general government expenditure and excluding net lending.

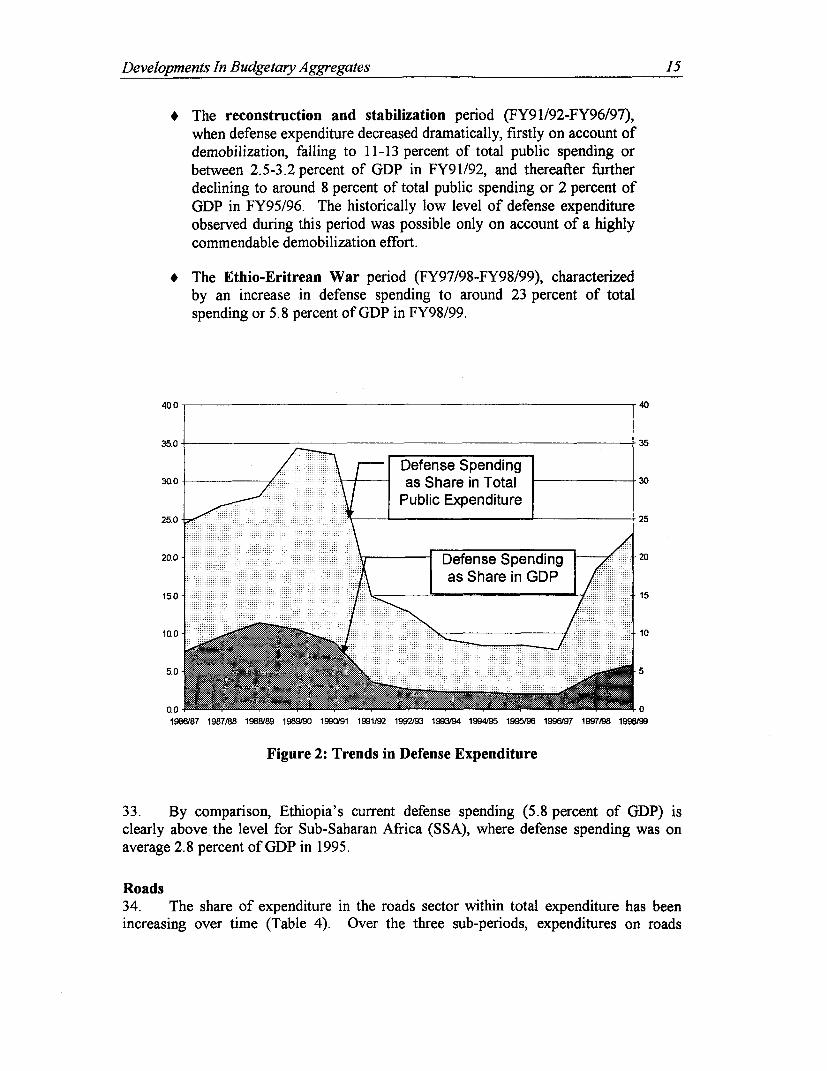

Defense32. The long-term decline in Ethiopia's defense expenditures was reversed inFY97/98 with the outbreak of the war with Eritrea. Defense expenditure as a share ofGDP, is now approximately triple its historically low level of the mid-1990s, but stillsignificantly below the war-time levels in the 1980s. Three distinct trends in defenseexpenditure can be identified over the past decade:

* The civil war period (FY86/87 to FY90/91), characterized by largedefense outlays, accounting on average for 30.8 percent of total publicspending or 9.6 percent of GDP.

Developments In Budgetary Aggregates 15

+ The reconstruction and stabilization period (FY91/92-FY96/97),when defense expenditure decreased dramatically, firstly on account ofdemobilization, falling to 11-13 percent of total public spending orbetween 2.5-3.2 percent of GDP in FY91/92, and thereafter furtherdeclining to around 8 percent of total public spending or 2 percent ofGDP in FY95/96. The historically low level of defense expenditureobserved during this period was possible only on account of a highlycommendable demobilization effort.

* The Ethio-Eritrean War period (FY97/98-FY98/99), characterizedby an increase in defense spending to around 23 percent of totalspending or 5.8 percent of GDP in FY98/99.

40.0 40

35.0 35

~~~~Defense Spending30,0 as Share in Total 30

250- S sL ~~~~Public Expenditure 225.0 25

200 Defense Spending 20

as Share in GDP15.0 15

5 .,' ' 5

0.0 ~~~~~~~~~~~~~~~~~~~~~~~~~~01986187 1987/88 1988/89 1989/90 1990/91 1991/92 1992/93 1993/94 1994195 1995/96 1998/97 1997/98 1998t99

Figure 2: Trends in Defense Expenditure

33. By comparison, Ethiopia's current defense spending (5.8 percent of GDP) isclearly above the level for Sub-Saharan Africa (SSA), where defense spending was onaverage 2.8 percent of GDP in 1995.

Roads34. The share of expenditure in the roads sector within total expenditure has beenincreasing over time (Table 4). Over the three sub-periods, expenditures on roads

16 Chapter 2

increased from 2.8 percent of total expenditure during FY86/87-90/91 to 6.3 percentduring FY91/92-94/95 and 9.7 percent during FY95/96-98199. In recent years, this trendhas continued with the share of roads expenditures rising from 8.7 percent in FY95/96(actual) to 10.4 percent in FY97/98 (pre-actual), and is projected to further increase to10.8 percent in FY98/99. Despite the increasing trend, actual spending continues to fallshort of budget targets, and future budget allocations may need to become more realisticwith regard to implementation capacity.

Education35. Total expenditure on education has followed an upward trend over the pastdecade. On average, sectoral expenditure shares increased from 9.5 percent of totalexpenditure during the civil war period to 13.6 percent during the reconstruction periodand 14.5 percent during the stabilization period. Despite the increasing trend fromFY86/87 to FY98/99, concerns were expressed in the 1998 PER report over the decline inthe share of education expenditure in recent years. Table 4 shows that expenditure oneducation declined from 15.0 percent of total expenditure in FY95/96 to 14.0 percent inFY97/98. The government is addressing this concern and the share of expenditure oneducation is projected to rise to 14.6 percent of total expenditure in FY98/99, with mostof the increase resulting from capital expenditures under the education SP.

Health36. The share of expenditure on health in total expenditure increased, on average,from 3.3 percent of total expenditure during the civil war period to 5.0 percent during thereconstruction period and 6.0 percent during the most recent five-year period. The trendhas also continued in recent years-from 5.3 percent in FY95/96 (actual) to 6.0 percent inboth FY97/98 (pre-actual) and FY98/99 (projection). Again, most of the increase isattributable to the capital budget where expenditures under the health SP are recorded.

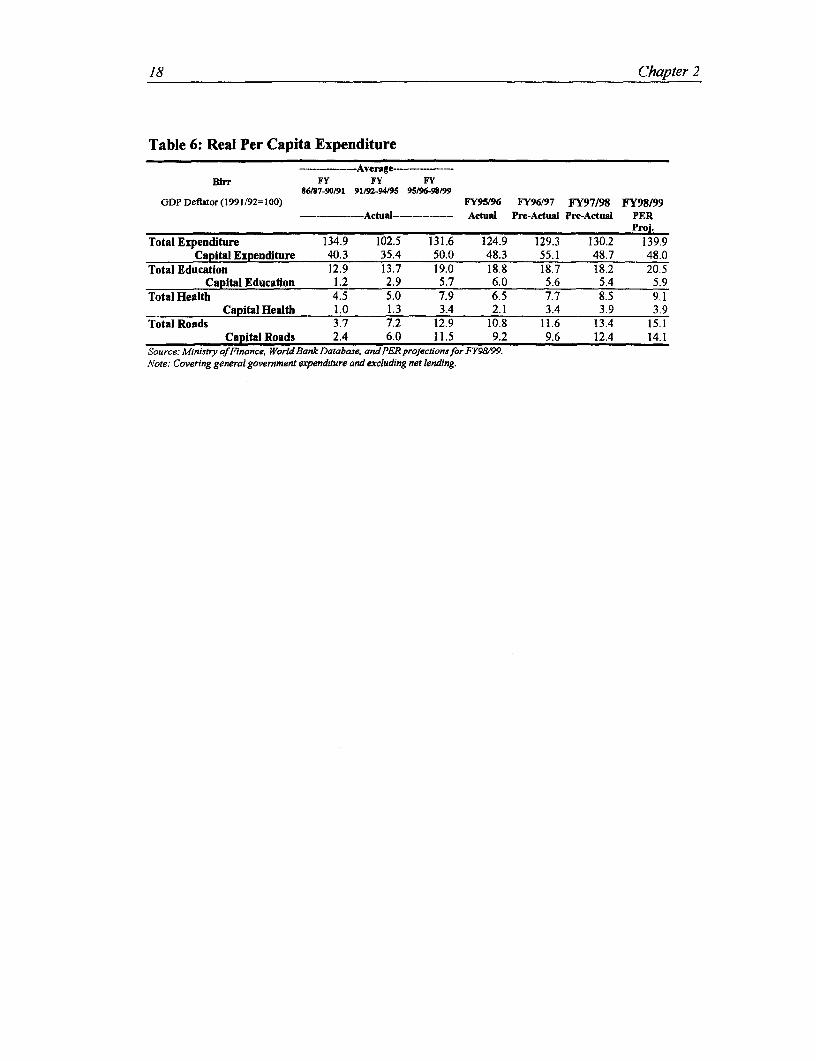

REAL AND PER CAP1TA EXPEND1TURE

Real expenditure levels for capital expenditures and for non-defensespending are comparable with pre-war levels. The good news is that pre-war gains have been preserved However the past two years exposemissed opportunities to accelerate progress toward a more poverty-sensitive expenditure composition.

37. As indicated earlier, the recent nominal increases in total expenditures are mainlythe result of the increases in defense spending. Between FY96/97 and FY97/98, overallpublic expenditure increased in nominal terms by about Birr 1.3 billion, which wasbroadly equivalent to the increase in defense spending. In FY98/99, an increase of totalexpenditure by about Birr 1.2 billion is projected, of which the lion's share is again onaccount of the increase in defense expenditure in the fiscal year. Therefore, it is moreappropriate to look at real expenditure levels. Table 5 reveals that real non-defenseexpenditure has remained broadly constant at levels equivalent to pre-war years.

Developments In Budgetary Aggregates 17

FY98/99 real capital expenditure is comparable to FY97/98, yet about 10 percent lowerthan the historically high levels in FY96/97.

Table 5: Real Expenditure

------ Average ----- - -------

I million of Birr FY FY FY FY95/96 FY96197 FY97/98 FY98/9986/87-90191 91192-94/95 95196-98/99--- ----------- Actual------- Actual Pre-Actual Pre-Actual PER

Proj.

NominalTotal Expenditure 4937 6223 10828 9206 10078 11405 12624

o/w Non-Defense 3418 5514 9190 8444 9291 9315 9708Recurrent Expenditure 3461 4076 6713 5643 5778 7140 8291

Capital Expenditure 1476 2147 4115 3563 4300 4265 4333Real (GDP Deflator 1991/92 = 100)

Total Expenditure 6479 5411 7626 6969 7394 7629 8410o/w Non-Defense 4486 4795 6477 6392 6817 6231 6468

Recurrent Expenditure 4539 3543 4727 4272 4239 4776 5524Capital Expenditure 1936 1866 2898 2698 3155 2853 2887

Source: Ministry of Finance, World Bank Database, and PER projections for FY98/99.Nlote: Cavering general government expenditure and excluding net lending.

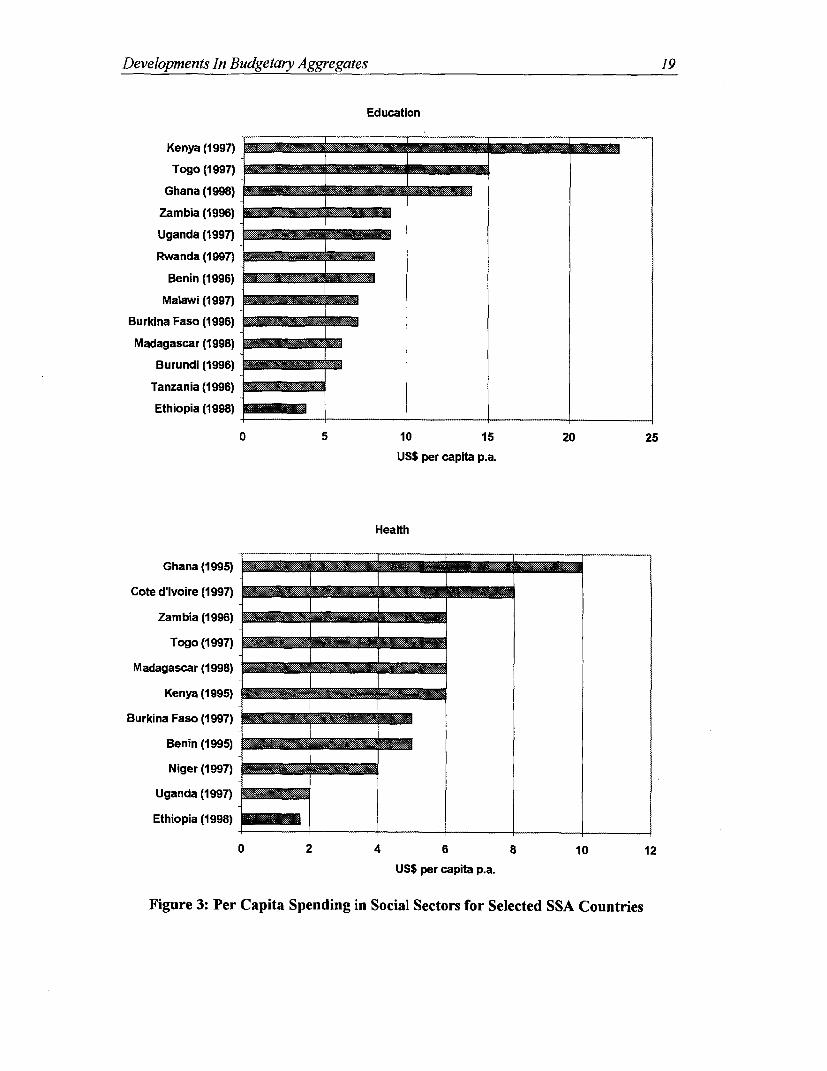

38. Despite the low budget execution rate (63 percent of the capital budget) and theoverall stagnation of real expenditure levels, FY98/99 projections indicate that real percapita spending in education, health, and roads has continued to improve over previousyears. While real per capita capital expenditures have declined from Birr 55 (in 1991/92Birr) to Birr 48 in FY98/99 (Table 6), the sectoral equivalent for the three priority sectorshave more than doubled since the early 1990s and have continued to rise in recentyears-reflecting the government's commitment to safeguard the three sectors from theimpact of war-related expenditure shifts. Nevertheless, there is no reason forcomplacency since Ethiopia's levels of per capita spending are lagging significantlybehind SSA averages (Figure 3). Per capita education and health expenditures in themajority of low-income Sub-Saharan African countries (for instance Kenya, Ghana, orMalawi) are two to three times higher than Ethiopia's current per capita spending onhealth and education of about $1.7 and $3.8, respectively.

18 Chapter 2

Table 6: Real Per Capita ExpenditureAver*ge--- -

Blrr FY FY FY861/7-90/91 91/92-94/95 95/96-98/99

GDP Deflator (1991/92= 100) FY95/96 FY96t97 FY97/98 FY98/99-------- Actual------- Actual Pre-Actual Pre-Actual PER

Proj.

Total Expenditure 134.9 102.5 131.6 124.9 129.3 130.2 139.9Capital Expenditure 40.3 35.4 50.0 48.3 55.1 48.7 48.0

Total Education 12.9 13.7 19.0 18.8 18.7 18.2 20.5Capital Education 1.2 2.9 5.7 6.0 5.6 5.4 5.9

Total Health 4.5 5.0 7.9 6.5 7.7 8.5 9.1Capital Health 1.0 1.3 3.4 2.1 3.4 3.9 3.9

Total Roads 3.7 7.2 12.9 10.8 11.6 13.4 15.1Capital Roads 2.4 6.0 11.5 9.2 9.6 12.4 14.1

Source: Ministry ofTFInance, World Bank Database, and PER projectionsjfor FY9/&99.Note: Covering general government expenditure and excluding net lending.

Developments In Budgetary Aggregates 19

Education

Kenya (1997)

Togo (1997)

Ghana (1998)

Zambia (1996)

Uganda (1997)

Rwanda (1 997)Benin (1996)

Malawi (1997)

Burkina Faso (1996)

Madagascar (1998)

Burundi (1996)

Tanzania (1996)

Ethiopia (1998)

0 5 10 15 20 25

USS per capita p.a.

Health

Ghana (1995)

Cote d'lvoire (1997)

Zambia (1996)

Togo (1997)

Madagascar (1998)

Kenya (1995)

Burkina Faso (1997)

Benin (1995) _ _ _

Niger (1997)

Uganda (1997)

Ethiopia (1998)

0 2 4 6 8 10 12

US$ per capita p.a.

Figure 3: Per Capita Spending in Social Sectors for Selected SSA Countries

20 Chapter 2

CONSTRAINTS To MOBILIZING EXTERNAL RESOURCES FOR SPS

The analysis of available-but still partial-fiscal data for FY98/99 doesnot support concerns that the government initiated deliberate budget cutsto fund the increased resource requirements for the defense budget. Asubstantial shorlfall is projected for external resources. Estimates ofactual disbursement of external resources are expected to fall short byapproximately Birr 1,300 million, which would account for almost threequarters of the underspending on the capital budget. The reasons for thisshortfall are a combination of (1) the delays in turning aid pledges intoformal agreements due to donor 's concerns about the war; (2) proceduraldelays in taking formal aid agreements to effectiveness; (3) complexfinancial and reporting requirements on donors' side, particularly in thecase of SPs; and (4) technical capacity constraints within the governmentparticularly related to an increased amount of civil works. Theseproblems will need to be resolved within the government/donorpartnership.

IPACT ON SOCIAL SECrOR EXPENDITURE

39. A comparison of disbursement rates between external funds and the government'sown funds-cumulative for the third quarter of the fiscal year-confirms that lowdisbursement of external resources is a major factor for underspending on the capitalbudget. At the time of the May 1999 PER mission, expenditure data for three quarters ofthe fiscal year indicated that the disbursement rate for external resources on the FY98/99capital budget expenditures was significantly lower than the comparable figure forprevious years. Conversely, the disbursement rate for the government's own funds wasabove that for external resources and higher than in FY97/98 (Figure 4). Estimates ofactual disbursement of external resources are expected to fall short by approximately Birr1,300 million, which would account for almost three quarters of the underspending on thecapital budget.

40. The comparison of the planned average funding shares for the three SPs (asagreed between donors and the government during the program appraisal) withactual/projected funding shares is presented in Table 7. In the case of education, it wasplanned that the government would provide on average 73 percent of sectoralexpenditures and external resources would cover 27 percent. The government's share ofthe financing burden is 55 percent for health and between 40 percent and 50 percent forroads. In the past two years, the government's actual/projected financing shares haveexceeded targets across all sectors and external resources have lagged behind. Forexample, in education where external resources were expected to provide some27 percent of funding, only 6 percent and 8 percent of external funding was achieved inFY97/98 and FY98/99, respectively.

Developments In Budgetary Aggregates 21

50

45

,40 *|l

13535

la.

25

FY94/95 FY95/96 FY96197 FY97/98 FY9BW9

Fiscal Year

INDomeic Resoure lExtemal Resource.

Figure 4: Disbursement of Capital Expenditures by Source

Table 7: Sectoral Expenditure-Actuals/Projections vs. Targets

Education Health RoadsFY97F98 FY98/99 FY97/98 FY98/99 FY97/98 FY98/99Pre-Act. PER Proj. Pre-Act. PER Proj. Pre-Act. PER!Proj

Planned Average Funding SharesGoE Resources 73% 73% 55% 55% 50% 40%External Resources 27% 27% 45% 45% 50% 60%

Pre-ActuallProjected Average Funding SharesGoE Resources 94% 88% 82% 68% 670% 58%Extem|al Resources 6% 12% 18% 32% 33% 42%

41. The delays in mobilizing extenal resources for the SPs could be the result ofcapacity bottlenecks, extensive donor procedures, or political considerations associatedwith the war. The PER mission collected information from donors on expected andactual disbursement flows and on the reason for the slowdown in aid disbursements.There is quantitative and qualitative evidence to conclude that delays in closing exteealassistance agreements (converting donor pledges into formal agreements) and taking

22 Chapter 2

those agreements to effectiveness were the most important factors behind underspendingon the capital budget in the past two years. 10