renewable fuel — biofuels · sustainable development business case report renewable fuel —...

TRANSCRIPT

Power Generation

Energy Utilization

Transportation

Agriculture

Forestry

Waste Management

Biocombustibles

Biofuels

Bio-oil

RenewableFuel

Energy Exploration and Production

Biodiesel

Bioethanol

Biogas

Biosyngas

Sustainable Development Business Case Report

Renewable Fuel — BiofuelsSD Business Case™ Version 2 • December 2006

BC_RFB_V8.5.5_EG_061207

Biocombustibles

Biofuels

Bio-oil

RenewableFuel

Energy Exploration and Production

Biodiesel

Bioethanol

Biogas

Biosyngas

Sustainable Development Business Case Report*

Renewable Fuel — BiofuelsSD Business Case™ Version 2 • December 2006

* Copyright © 2006 by Canada Foundation for Sustainable Development Technology (“SDTC™”). All Copyright Reserved. Published in Canada by SDTC™. No part of the SD Business CaseTM may be produced, reproduced, modified, distributed, sold, published, broadcast, retransmitted, communicated to the public by telecommunication or circulated in any form without the prior written consent of SDTC, except to the extent that such use is fair dealing for the purpose of research or private study (unpublished, or an insubstantial copy). To request consent please contact SDTC. All insubstantial copies for research or private study must include this copyright notice.

The SD Business Case™ is provided “as is” without warranty or representation of any kind. Use of the information provided in the SD Business Case is at your own risk. SDTC does not make any representation or warranty as to the quality, accuracy, reliability, completeness, or timeliness of the information provided in the SD Business Case.

Sustainable Development Technology Canada™, SDTC™, SD Business Case™ and SDTC STAR™ are trade marks of Canada Foundation for Sustainable Development Technology.

Table of Contents1 Overview : SD Business Case™ Plan and the SDTC STAR™ Process ......................... 1

1.1 The SD Business Case™ Plan ............................................................................................................................................................ 1

1.1.1 Primary Audience ........................................................................................................................................................................ 1

1.1.2 The SDTC STAR™ Tool ................................................................................................................................................................. 2

1.1.3 Sectors to be assessed by the SD Business Case™ ...................................................................................................... 2

Figure 1 : SD Business Case Investment Roadmap ............................................................................................................................................ 3

1.1.4 Investment Categories to be Analysed ............................................................................................................................ 4

1.1.5 Conclusions Framework ........................................................................................................................................................... 4

1.2 The SDTC STAR™ Process : Data Collection And Analysis ...................................................................................... 5

Figure 2 : The SDTC STAR Process ........................................................................................................................................................................... 5

1.2.1 Assessment Descriptions ......................................................................................................................................................... 6

Figure 3 : SDTC Funding Support ............................................................................................................................................................................ 7

1.2.2 Output Structure .......................................................................................................................................................................... 8

Figure 4 : Sample Technology Plot ........................................................................................................................................................................ 10

1.3 Conclusions And Investment Priorities ............................................................................................................................... 12

2 Executive Summary : Biofuels ................................................................................................................................ 13

2.1 Biofuels ........................................................................................................................................................................................................... 13

2.2 Biofuel Resources ................................................................................................................................................................................... 13

2.3 A Vision for the Future ....................................................................................................................................................................... 13

2.4 The Biofuels Market ............................................................................................................................................................................. 13

2.5 Biofuel Technologies ........................................................................................................................................................................... 14

2.6 Achieving the Vision ............................................................................................................................................................................ 15

2.6.1 Technical Needs ........................................................................................................................................................................... 15

2.6.2 Non-Technical Needs ................................................................................................................................................................ 15

2.7 Statements Of Interest Review .................................................................................................................................................. 16

2.8 Investment Priorities .......................................................................................................................................................................... 16

2.8.1 Near Term ....................................................................................................................................................................................... 16

2.8.2 Longer Term .................................................................................................................................................................................. 17

2.8.3 National Strategy Impacts .................................................................................................................................................... 17

3 Industry Vision/Background ....................................................................................................................................... 18

Figure 5 : Biofuels SD Business Case Investment Report Study Scope ............................................................................................................ 18

3.1 General Description ............................................................................................................................................................................. 18

3.2 Types of Biofuels ..................................................................................................................................................................................... 18

3.2.1 Solid Biofuels ................................................................................................................................................................................ 18

3.2.2 Liquid Biofuels ............................................................................................................................................................................. 18

3.2.3 Gaseous Biofuels ........................................................................................................................................................................ 19

3.3 Biofuel Resources ................................................................................................................................................................................... 19

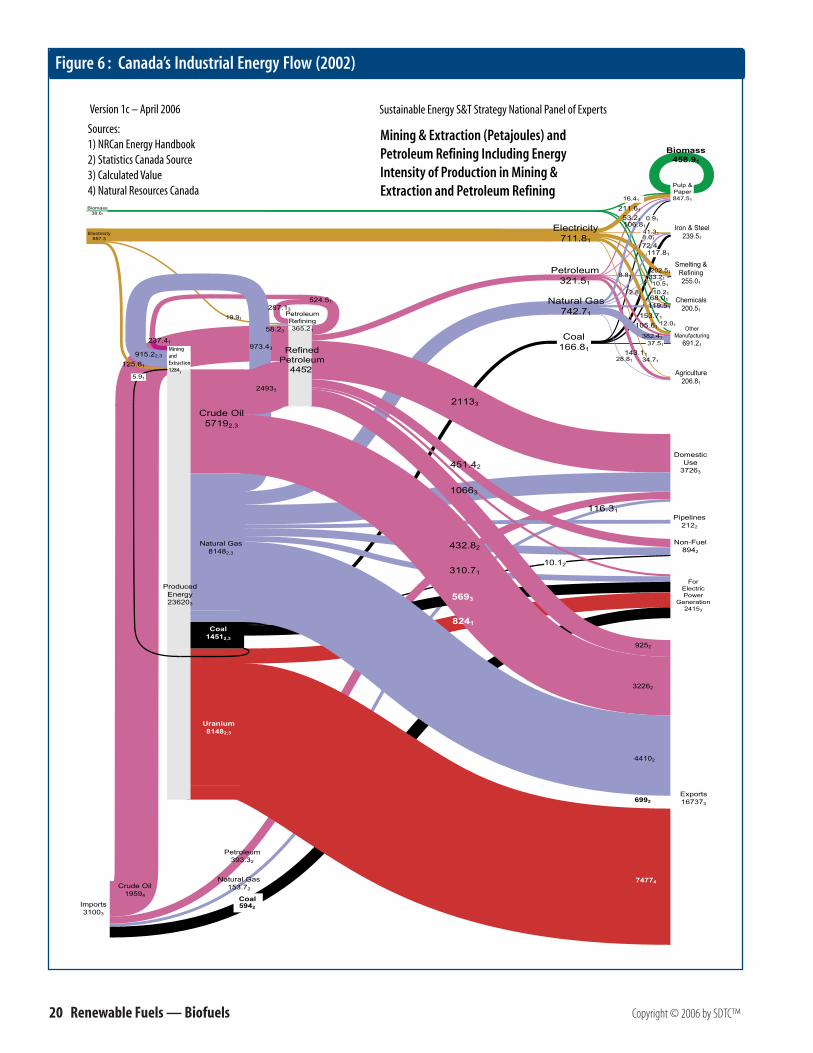

3.3.1 Canada’s Energy Mix ................................................................................................................................................................. 19

Figure 6 : Canada’s Industrial Energy Flow (2002) ............................................................................................................................................... 20

3.3.2 Canada’s Biomass Resources................................................................................................................................................ 21

Table 1 : Canada’s Biomass Feedstock Supply ...................................................................................................................................................... 22

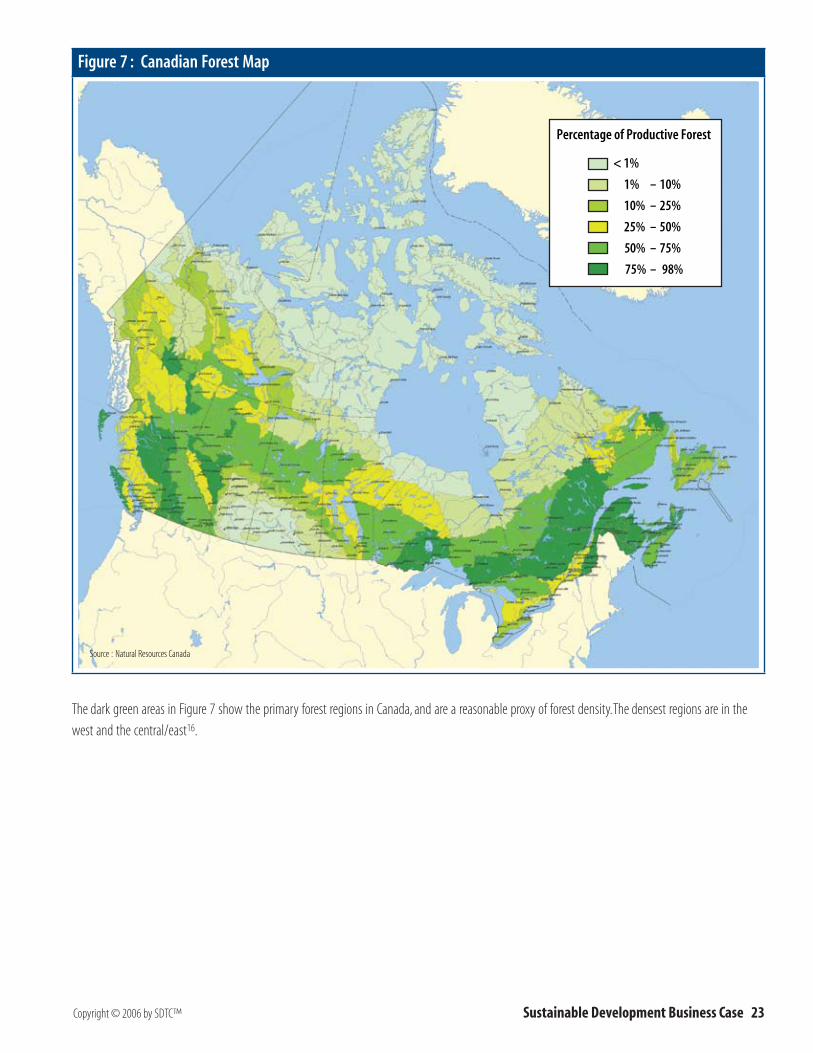

3.3.3 Feedstock Availability and Regional Distribution ................................................................................................... 22

Figure 7 : Canadian Forest Map ............................................................................................................................................................................ 23

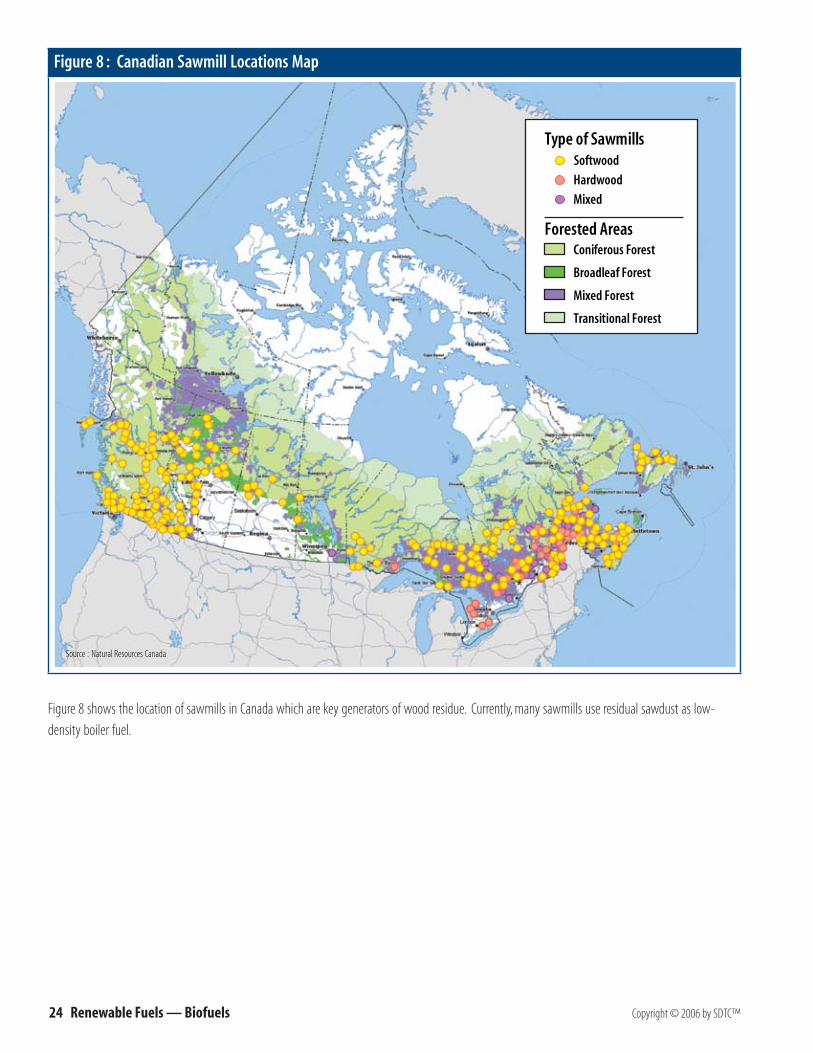

Figure 8 : Canadian Sawmill Locations Map ........................................................................................................................................................ 24

Figure 9 : Canadian Farming Map ......................................................................................................................................................................... 25

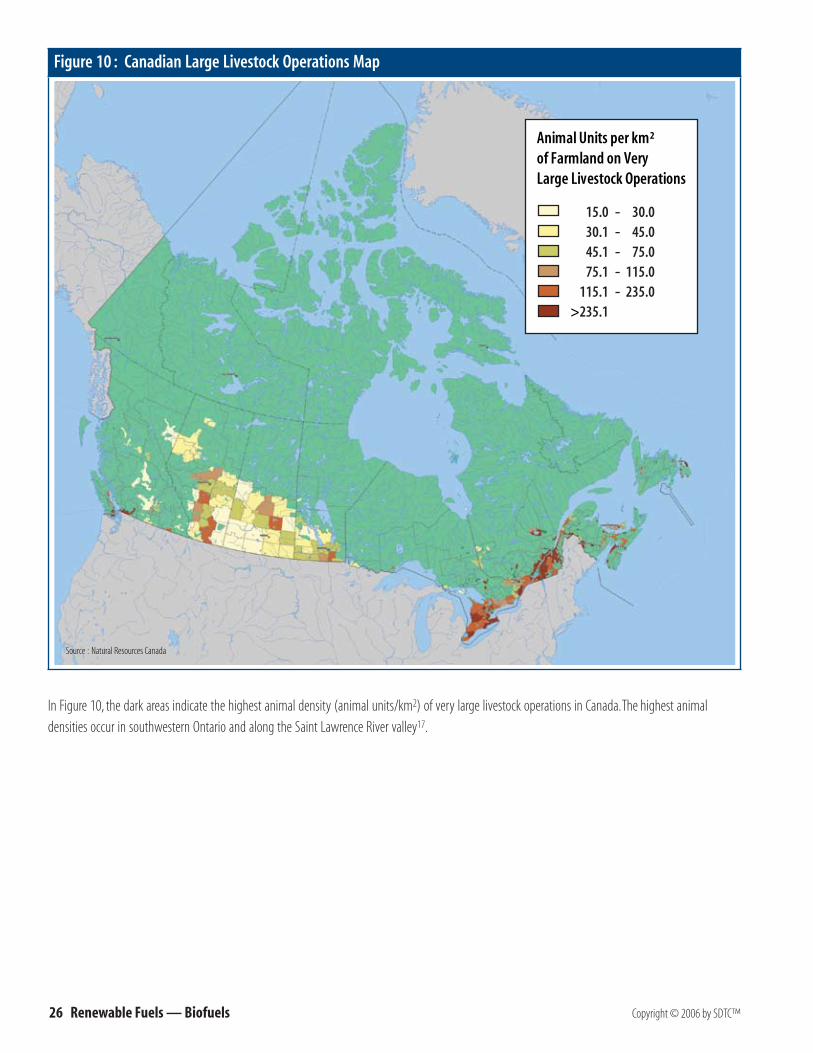

Figure 10 : Canadian Large Livestock Operations Map ........................................................................................................................................ 26

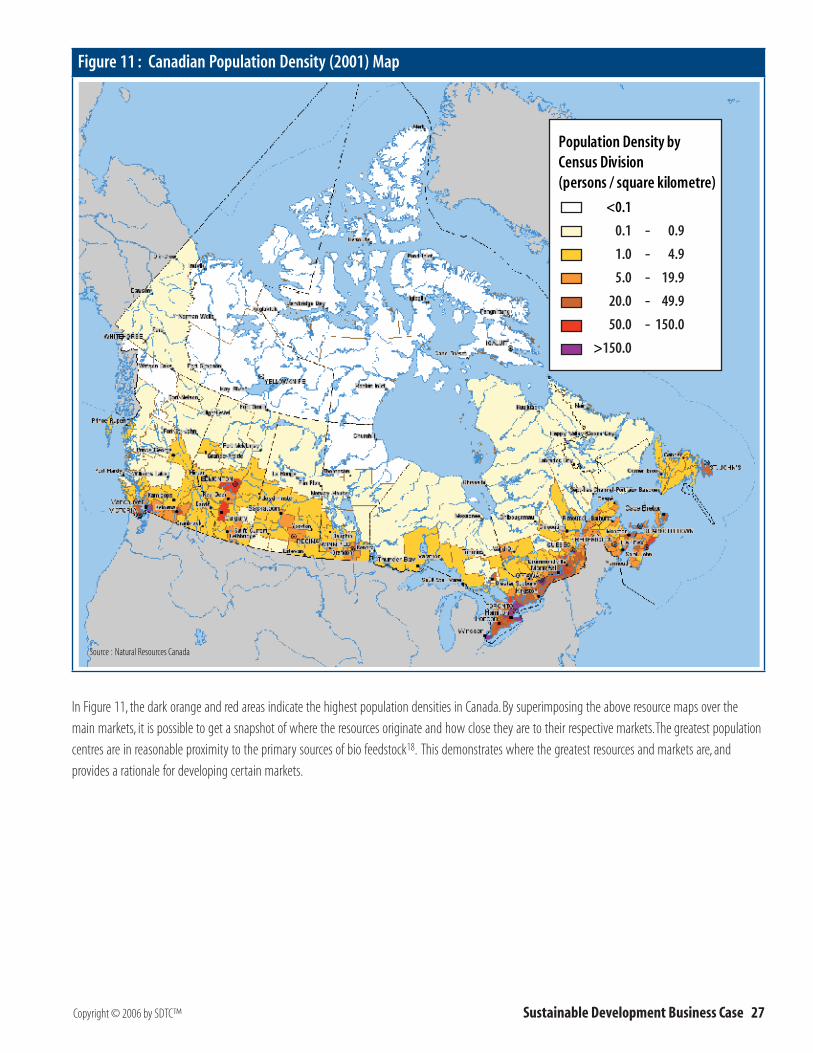

Figure 11 : Canadian Population Density (2001) Map ........................................................................................................................................ 27

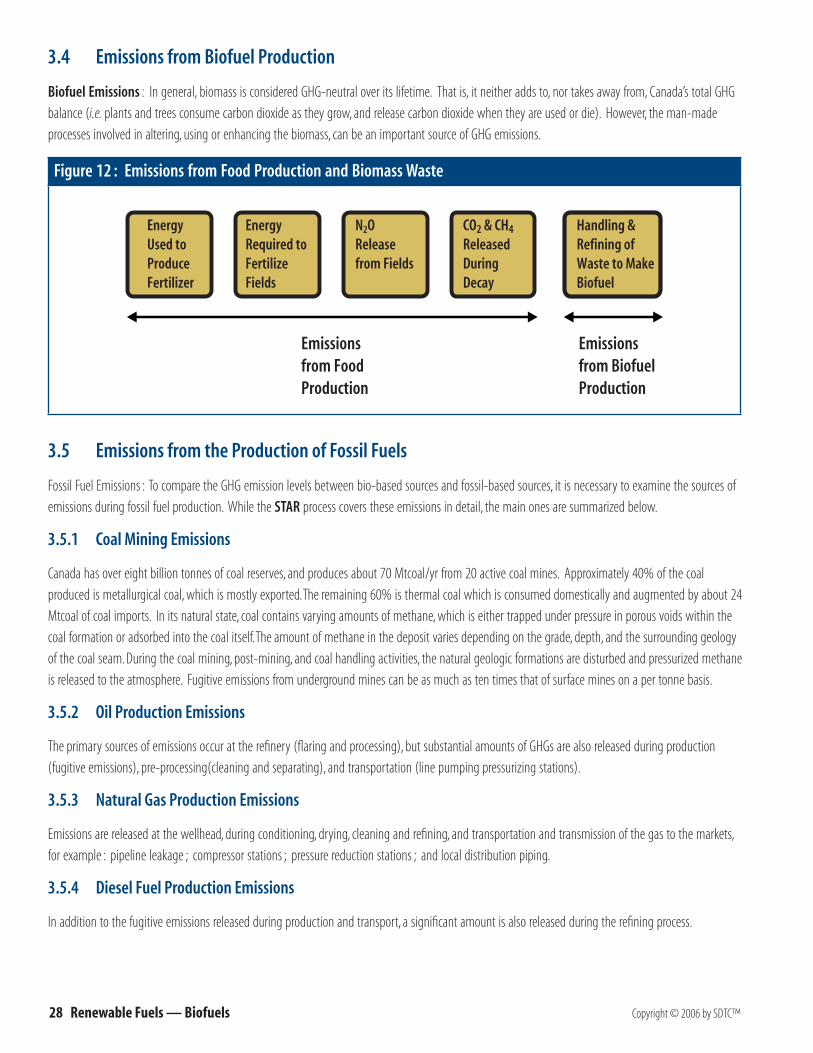

3.4 Emissions from Biofuel Production ........................................................................................................................................ 28

Figure 12 : Emissions from Food Production and Biomass Waste ..................................................................................................................... 28

3.5 Emissions from the Production of Fossil Fuels ............................................................................................................. 28

3.5.1 Coal Mining Emissions ............................................................................................................................................................. 28

3.5.2 Oil Production Emissions ....................................................................................................................................................... 28

3.5.3 Natural Gas Production Emissions ................................................................................................................................... 28

3.5.4 Diesel Fuel Production Emissions ..................................................................................................................................... 28

3.6 Key Drivers and Influencers .......................................................................................................................................................... 29

3.6.1 Political & Regulatory Drivers ............................................................................................................................................. 29

3.6.2 Political Attention ..................................................................................................................................................................... 29

3.6.3 Regulation ..................................................................................................................................................................................... 29

3.6.4 Tax Treatment .............................................................................................................................................................................. 30

3.7 Technical Drivers ..................................................................................................................................................................................... 30

3.7.1 Energy Content ............................................................................................................................................................................ 30

3.7.2 Moisture Content ....................................................................................................................................................................... 30

3.7.3 Infrastructure Requirements .............................................................................................................................................. 30

3.7.4 Airborne Emissions.................................................................................................................................................................... 30

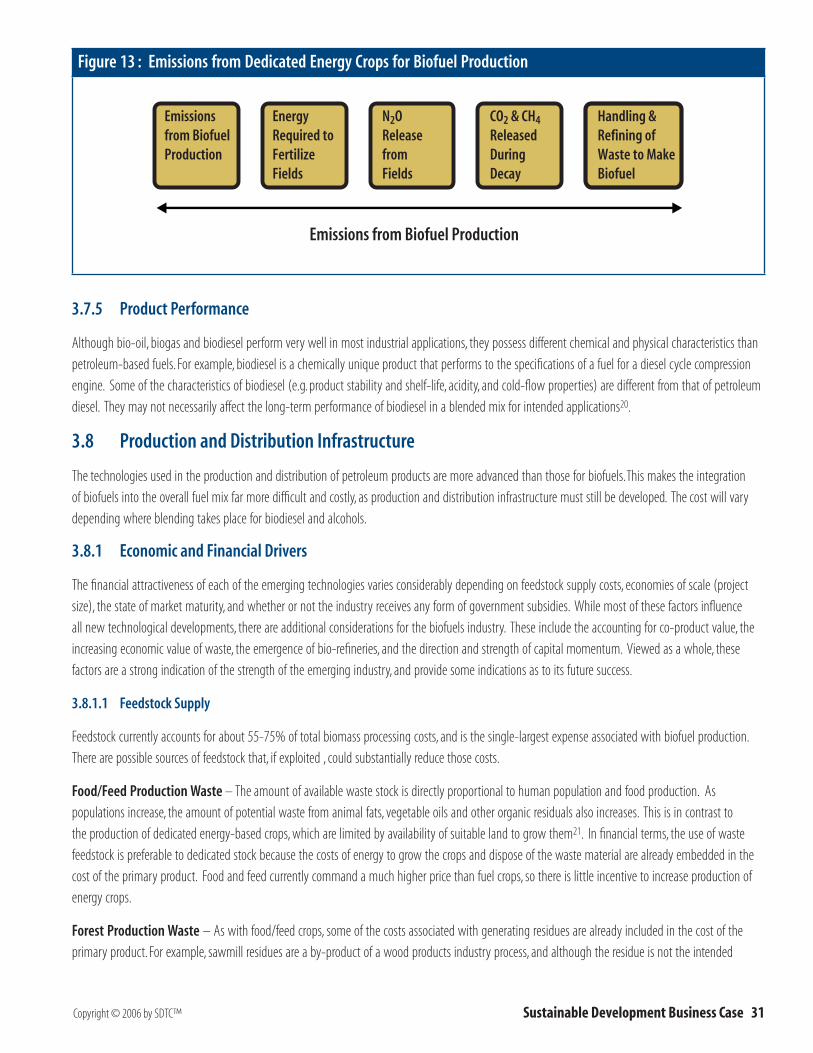

Figure 13 : Emissions from Dedicated Energy Crops for Biofuel Production ....................................................................................................... 31

3.7.5 Product Performance............................................................................................................................................................... 31

3.8 Production and Distribution Infrastructure ................................................................................................................... 31

3.8.1 Economic and Financial Drivers ......................................................................................................................................... 31

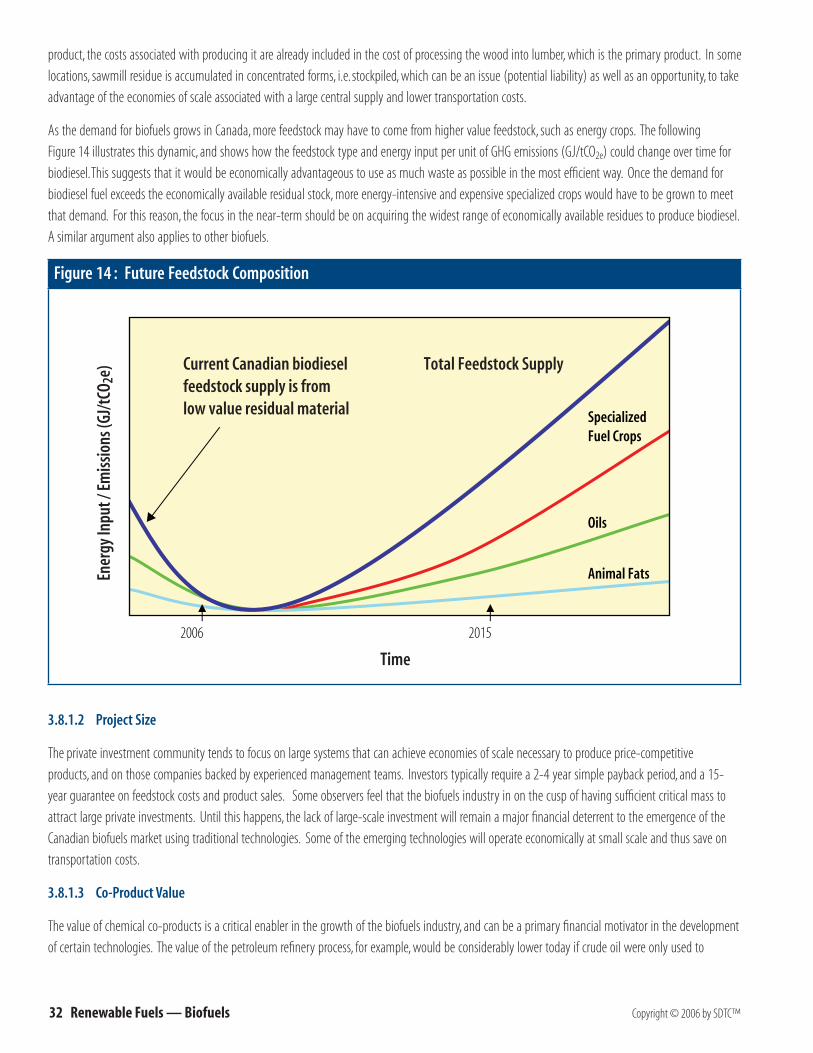

Figure 14 : Future Feedstock Composition ............................................................................................................................................................ 32

3.9 Market Infrastructure & Market Demand Drivers ..................................................................................................... 34

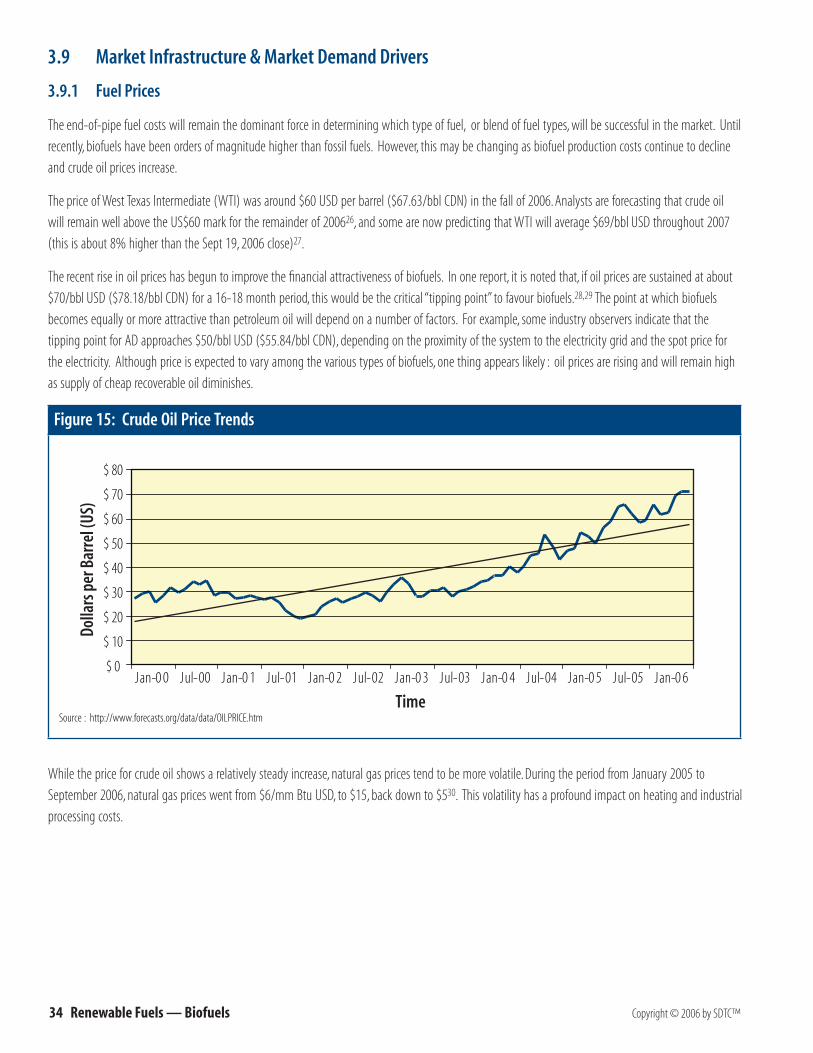

3.9.1 Fuel Prices....................................................................................................................................................................................... 34

Figure 15: Crude Oil Price Trends .......................................................................................................................................................................... 34

3.9.2 Market Proximity ....................................................................................................................................................................... 35

3.9.3 Replicability and Portability ............................................................................................................................................... 35

3.9.4 Sources of Risk ............................................................................................................................................................................. 35

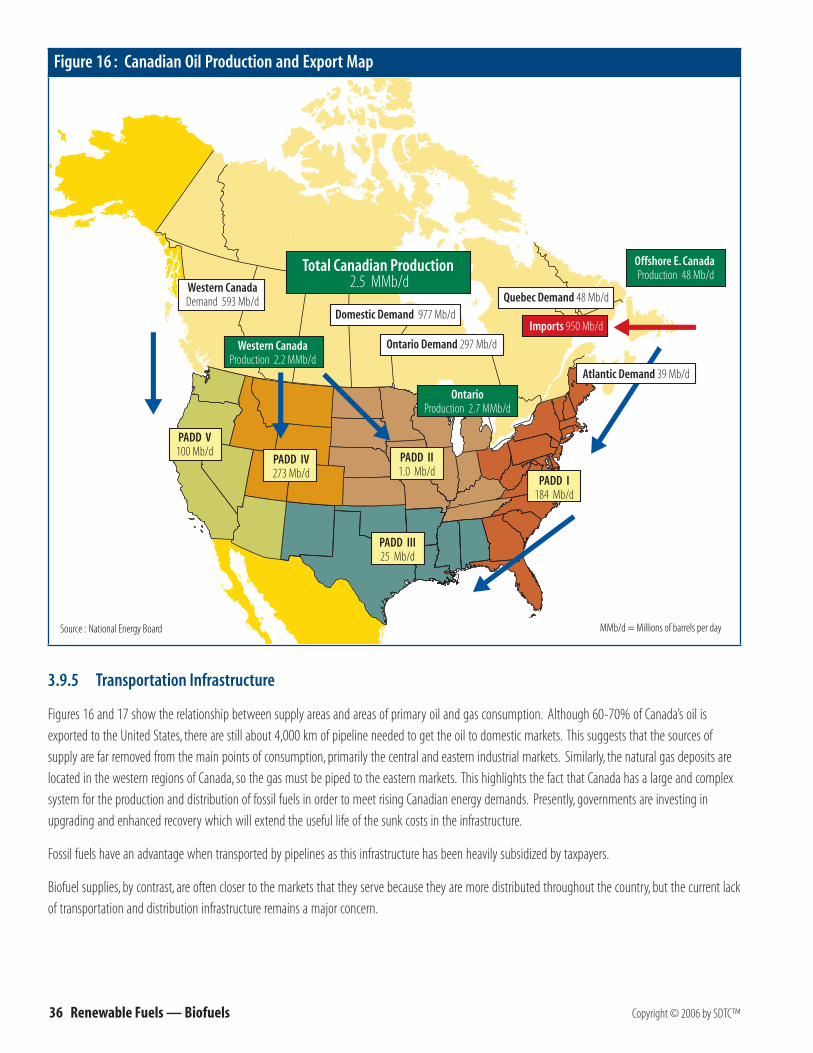

Figure 16 : Canadian Oil Production and Export Map.......................................................................................................................................... 36

3.9.5 Transportation Infrastructure ............................................................................................................................................ 36

Figure 17 : Canadian Natural Gas Supply and Distribution ................................................................................................................................ 37

3.9.6 Market Development Trends ............................................................................................................................................... 38

3.10 Societal Issues & Trends .................................................................................................................................................................... 38

3.10.1 Acceptance of Sustainability ............................................................................................................................................... 38

3.10.2 Local Economic Impacts ......................................................................................................................................................... 38

3.10.3 Public Concerns ........................................................................................................................................................................... 38

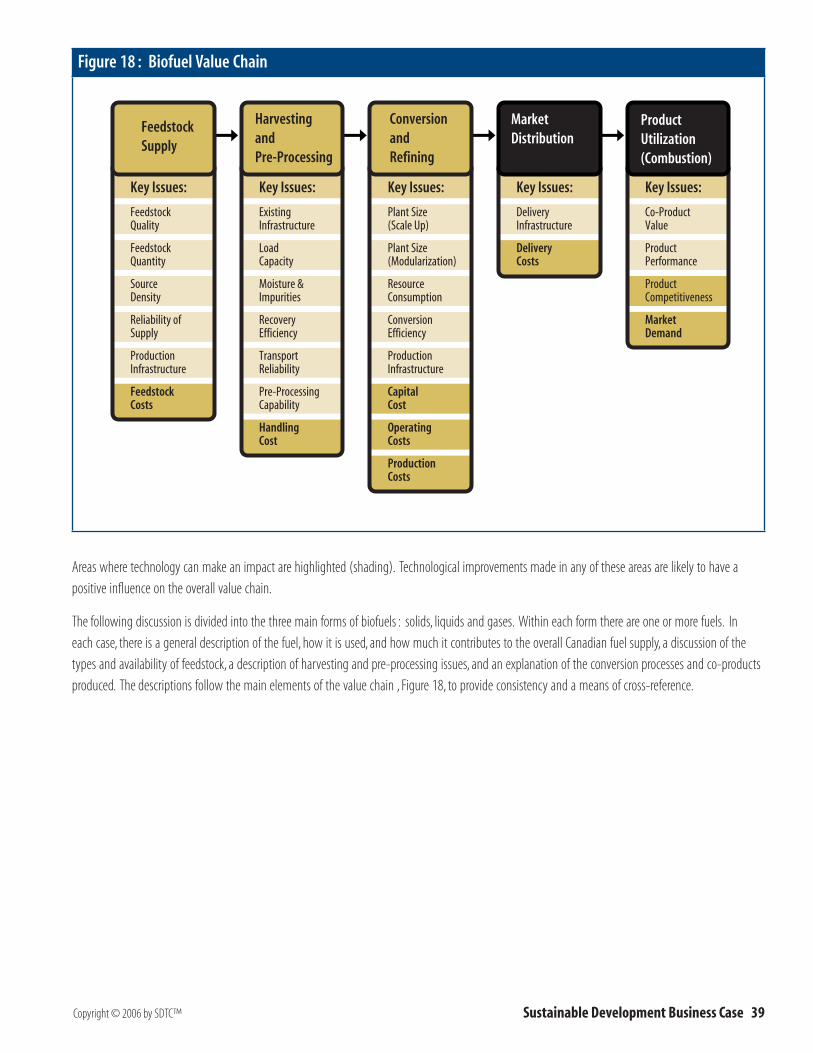

Figure 18 : Biofuel Value Chain ............................................................................................................................................................................. 39

3.11 Solid Biofuels ............................................................................................................................................................................................. 40

3.11.1 Biocombustibles ......................................................................................................................................................................... 40

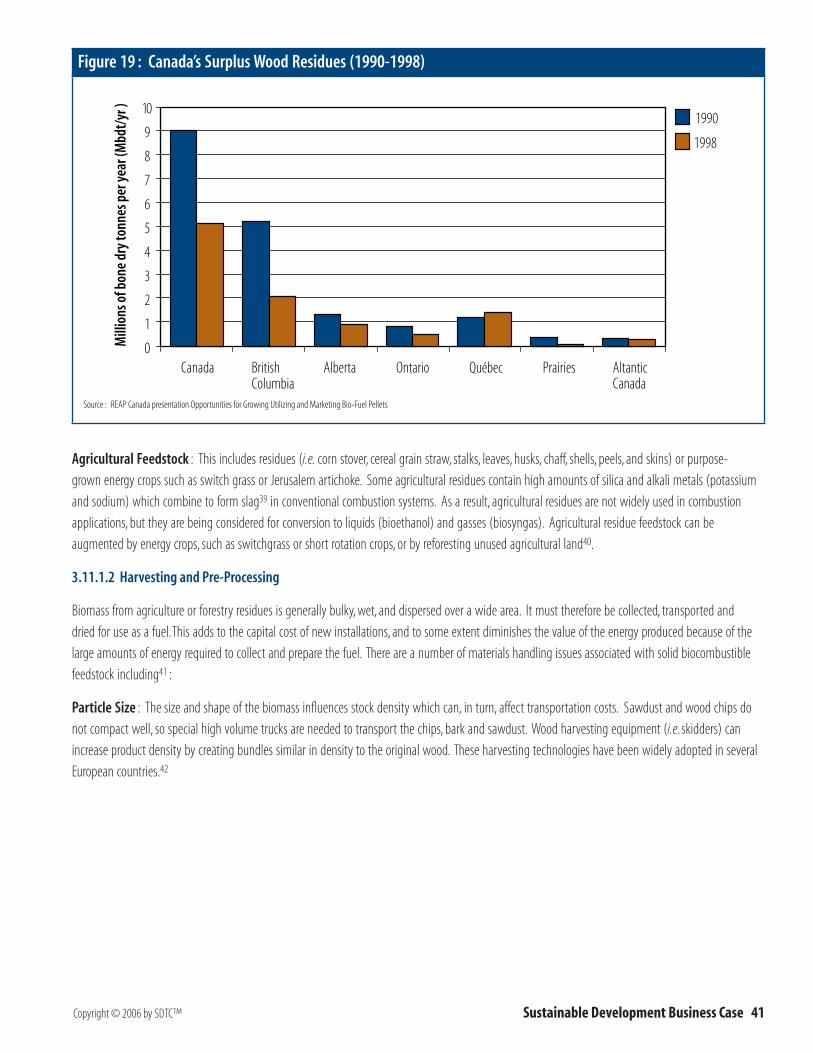

Figure 19 : Canada’s Surplus Wood Residues (1990-1998) ................................................................................................................................. 41

Figure 20 : Harvesting Skidder .............................................................................................................................................................................. 42

3.12 Liquid Biofuels .......................................................................................................................................................................................... 43

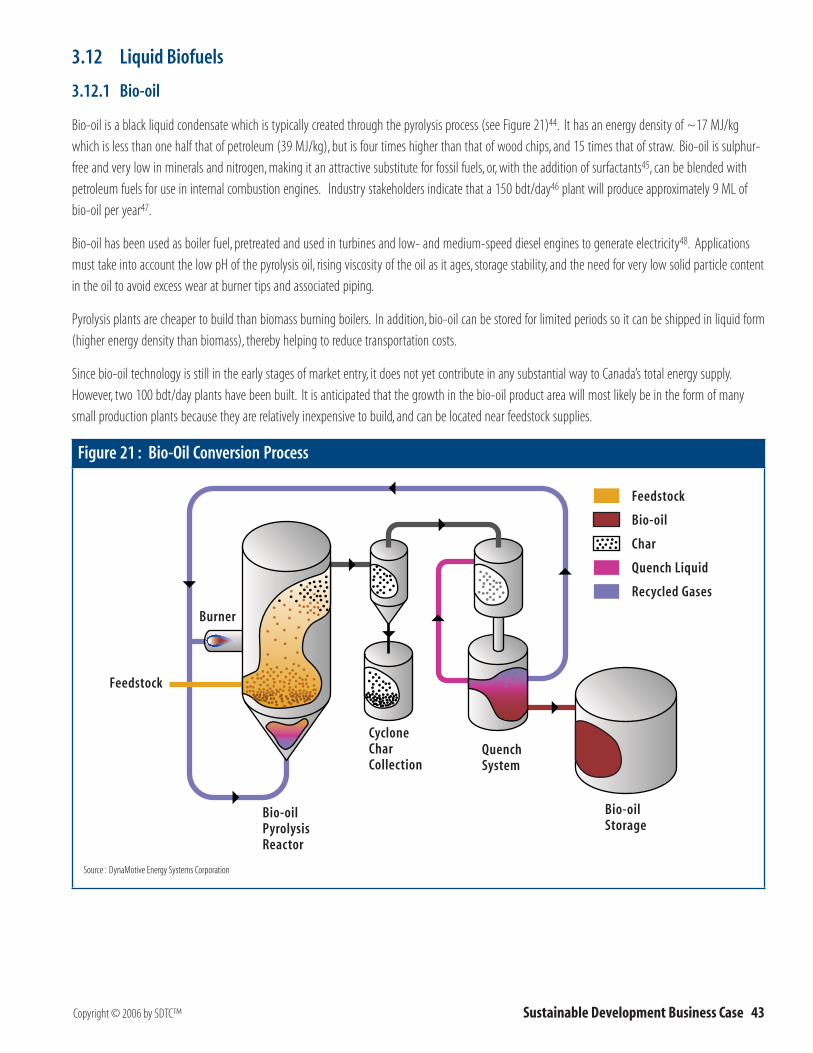

3.12.1 Bio-oil ............................................................................................................................................................................................... 43

Figure 21 : Bio-Oil Conversion Process.................................................................................................................................................................. 43

3.12.2 Biodiesel .......................................................................................................................................................................................... 44

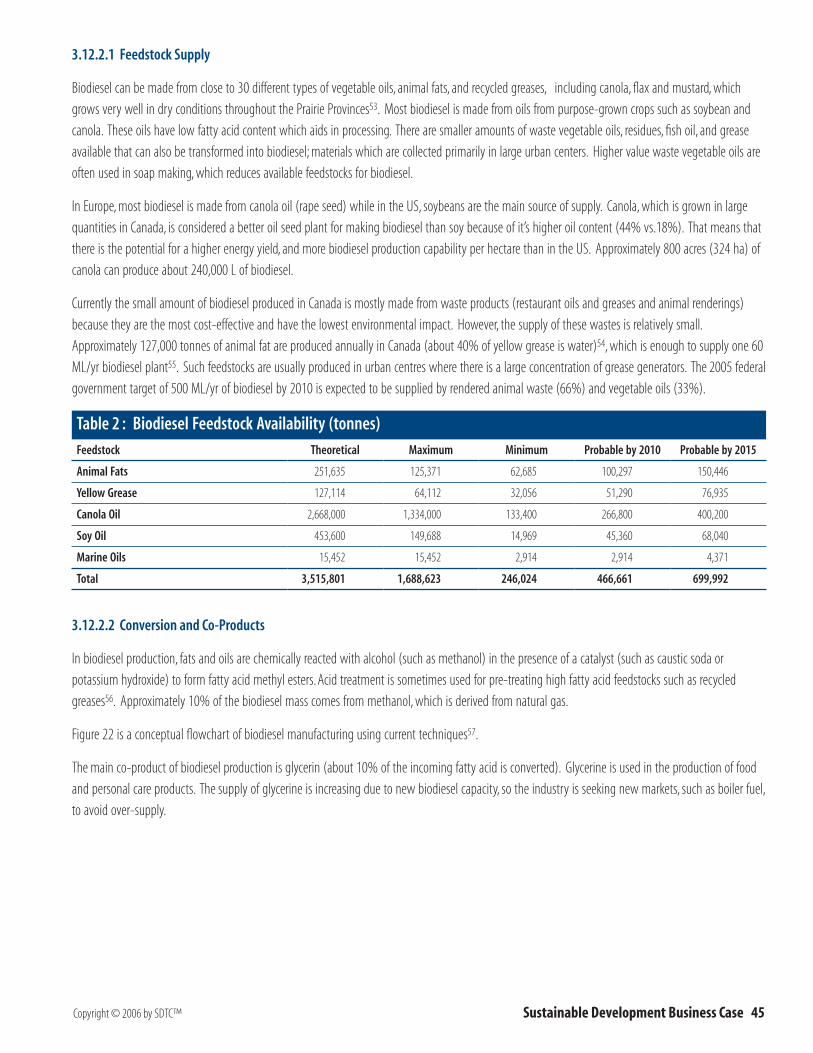

Table 2 : Biodiesel Feedstock Availability (tonnes) ............................................................................................................................................... 45

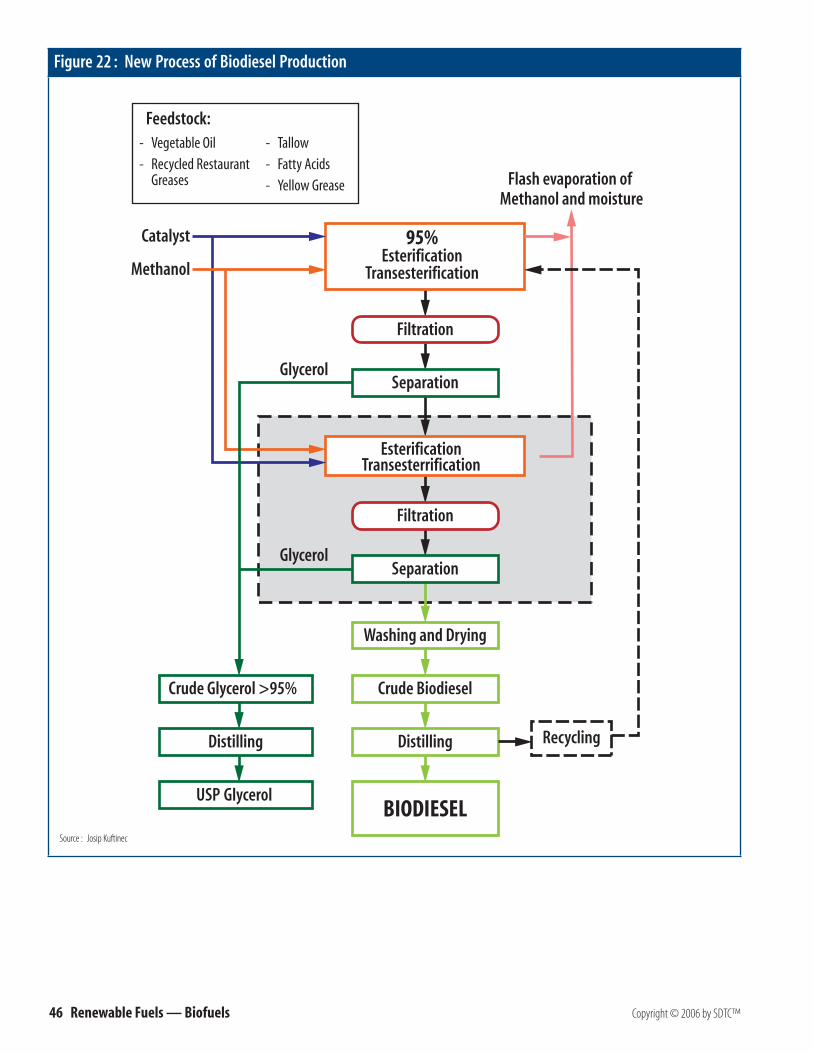

Figure 22 : New Process of Biodiesel Production ................................................................................................................................................. 46

3.12.3 Bioethanol ..................................................................................................................................................................................... 47

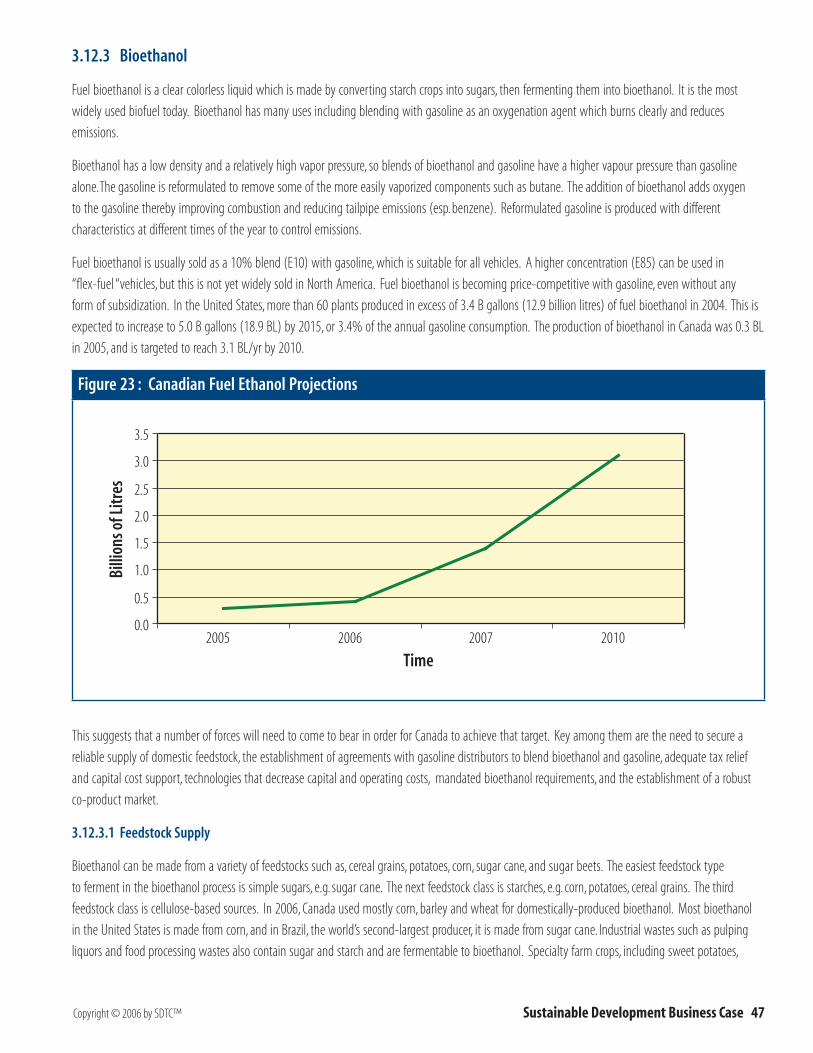

Figure 23 : Canadian Fuel Ethanol Projections ..................................................................................................................................................... 47

Figure 24 : Corn Ethanol Net Energy Balance ....................................................................................................................................................... 48

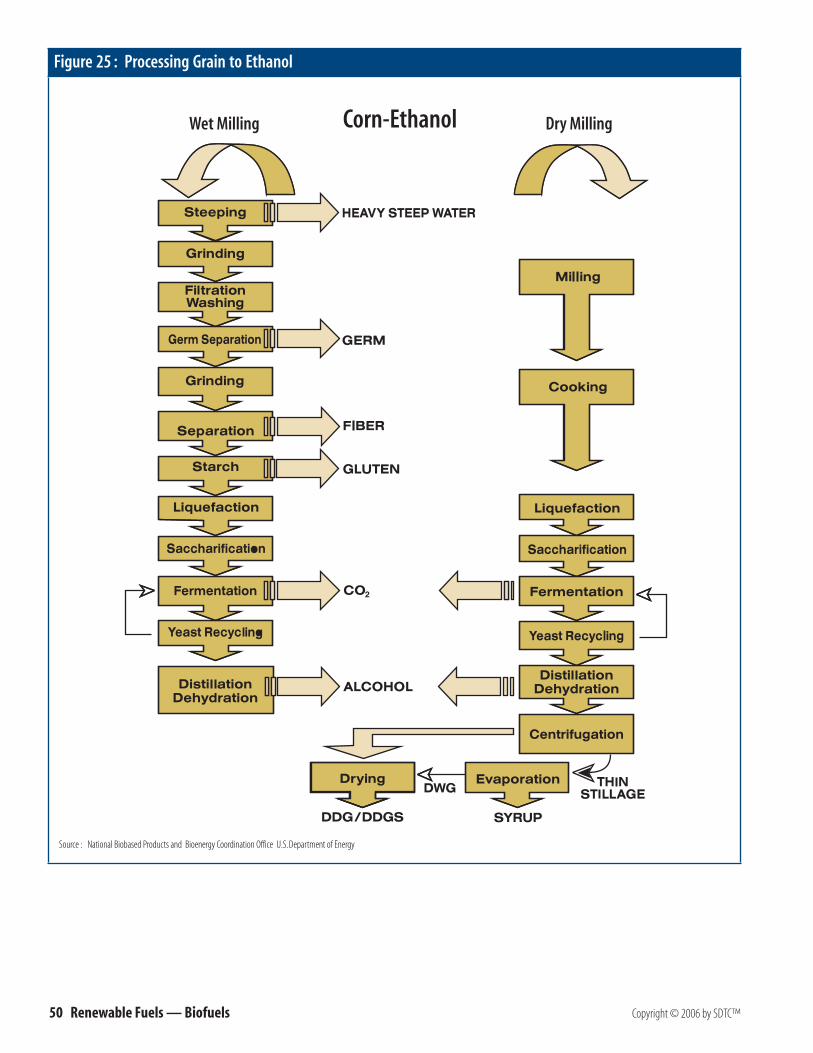

Figure 25 : Processing Grain to Ethanol ................................................................................................................................................................ 50

3.12.4 Mixed Alcohols from Gasification ..................................................................................................................................... 51

3.13 Gaseous Biofuels..................................................................................................................................................................................... 52

3.13.1 Biogas – Anaerobic Digestion ............................................................................................................................................ 52

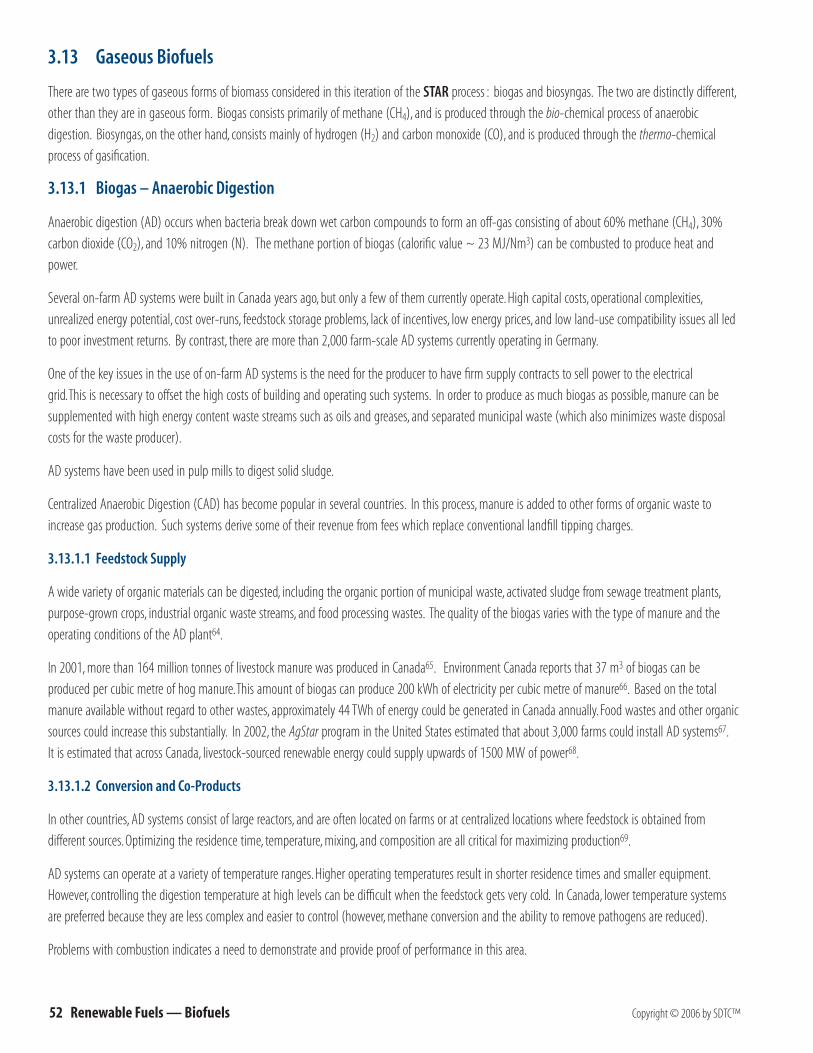

Figure 26 : Anaerobic Digestion of Hog Manure .................................................................................................................................................. 53

3.13.2 Biogas – Landfill Gas ............................................................................................................................................................... 53

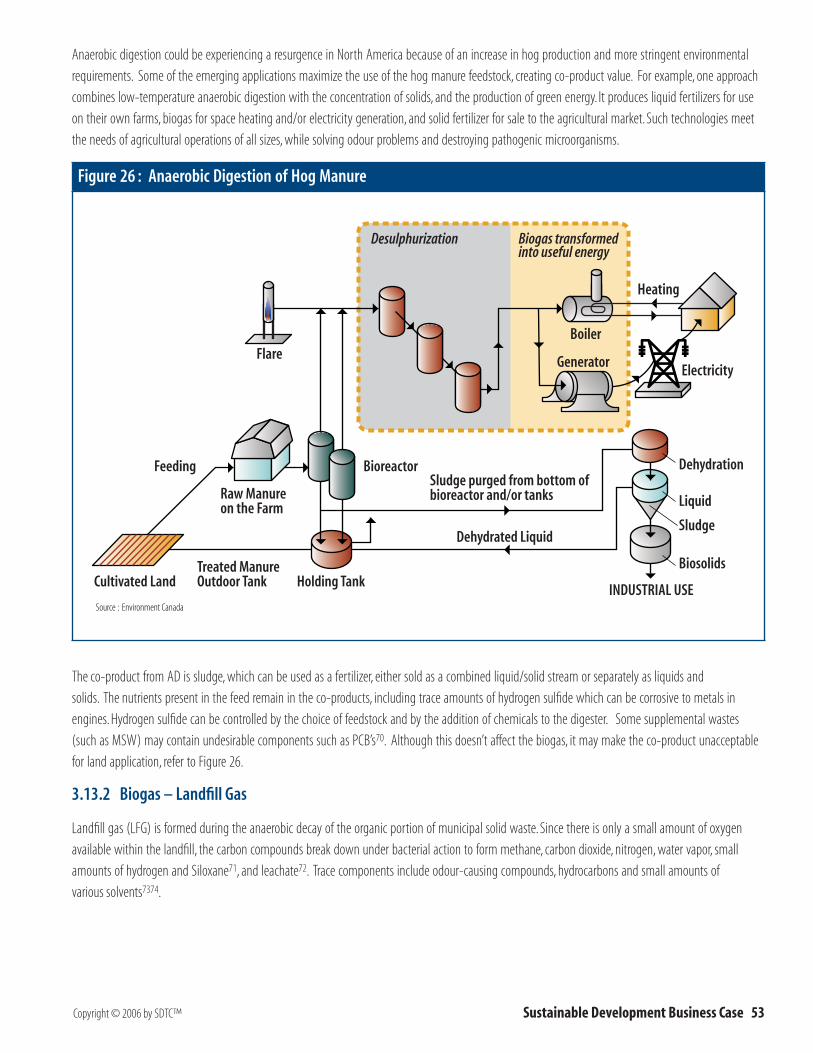

Table 3 : Landfill Gas in Canada ............................................................................................................................................................................ 54

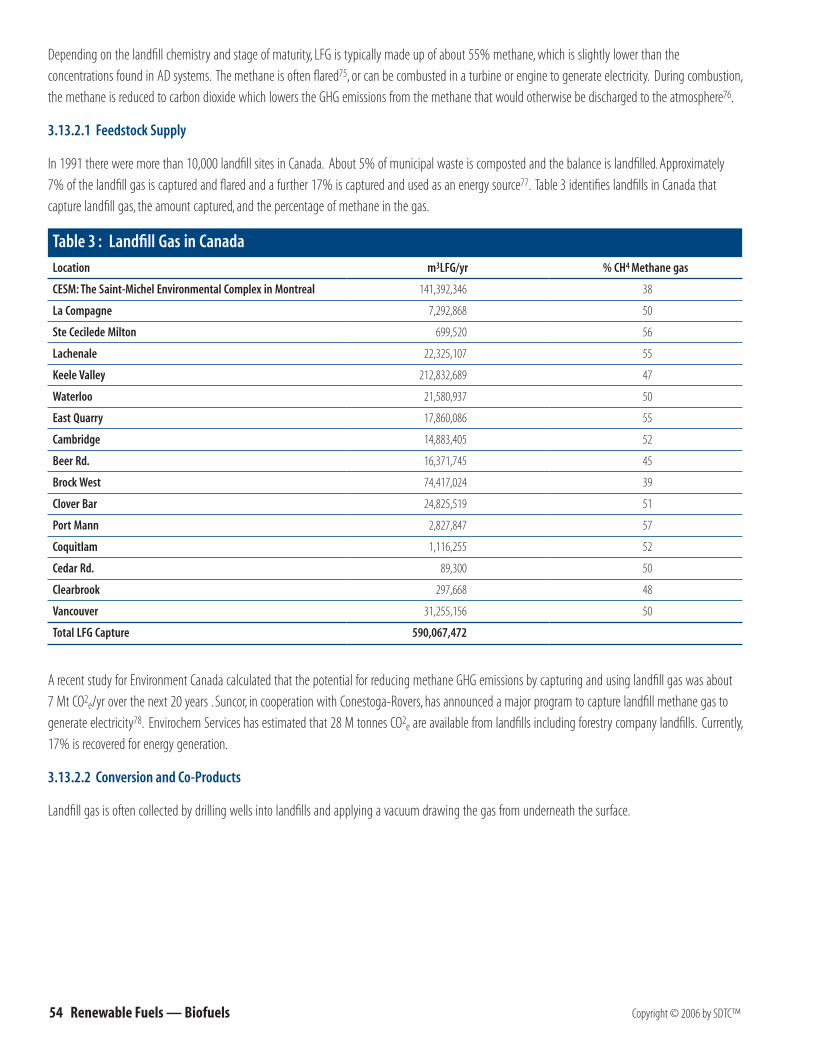

Figure 27 : Landfill Gas Collection and Beneficial Use ......................................................................................................................................... 55

3.13.3 Biosyngas........................................................................................................................................................................................ 55

Figure 28 : Syngas and Methanol Feedstock to Product Threads ........................................................................................................................ 56

Table 4 : Types of Biomass and the Sources ......................................................................................................................................................... 57

Figure 29 : Simplified Gasification Process ........................................................................................................................................................... 58

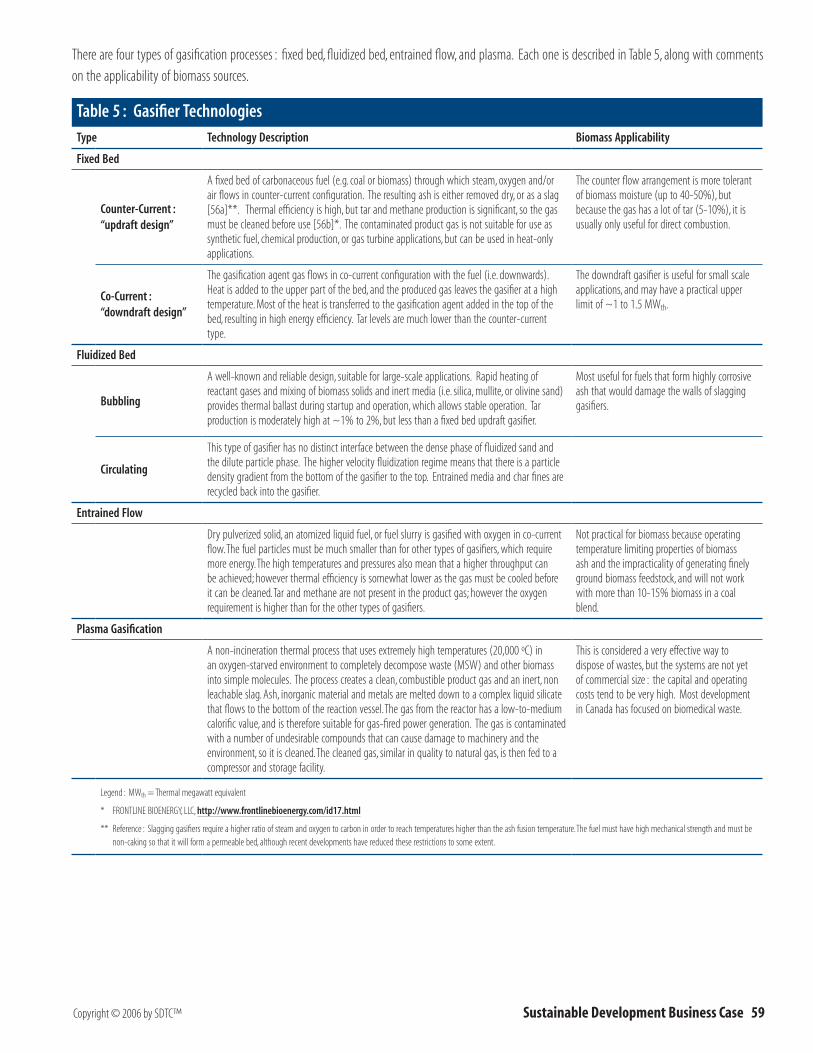

Table 5 : Gasifier Technologies............................................................................................................................................................................... 59

3.14 Vision Statement .................................................................................................................................................................................... 60

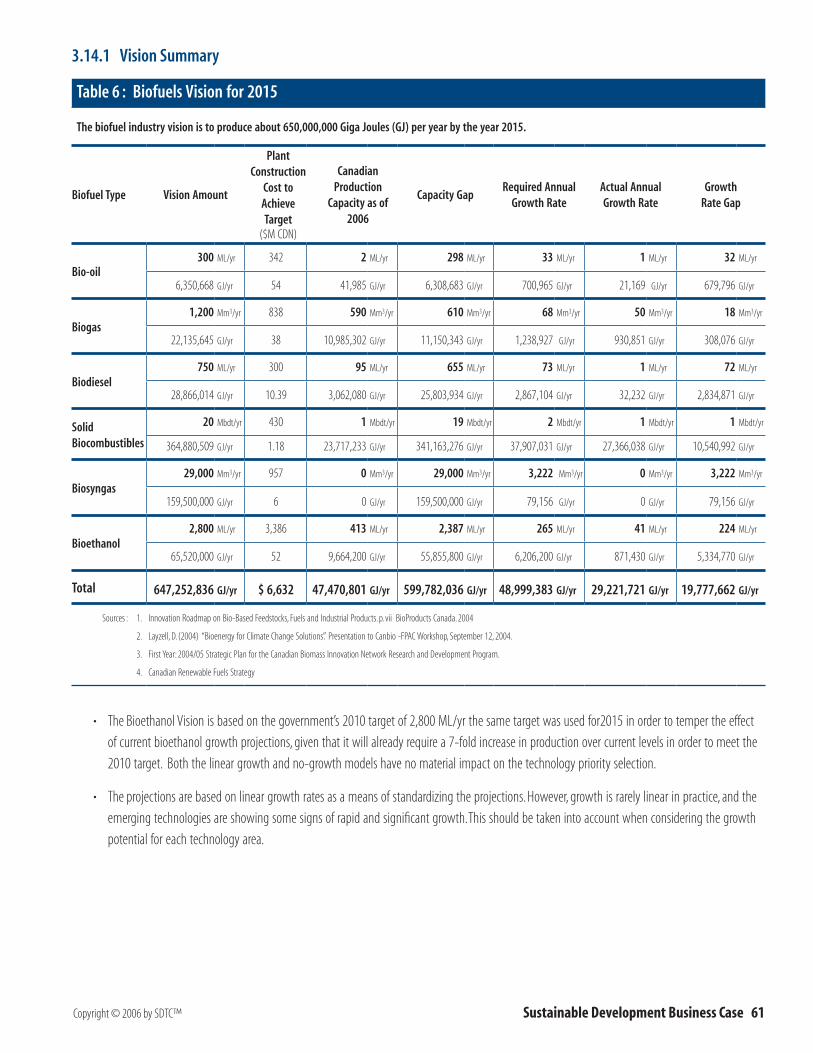

3.14.1 Vision Summary .......................................................................................................................................................................... 61

Table 6 : Biofuels Vision for 2015 .......................................................................................................................................................................... 61

3.14.2 Vision Assessment ..................................................................................................................................................................... 62

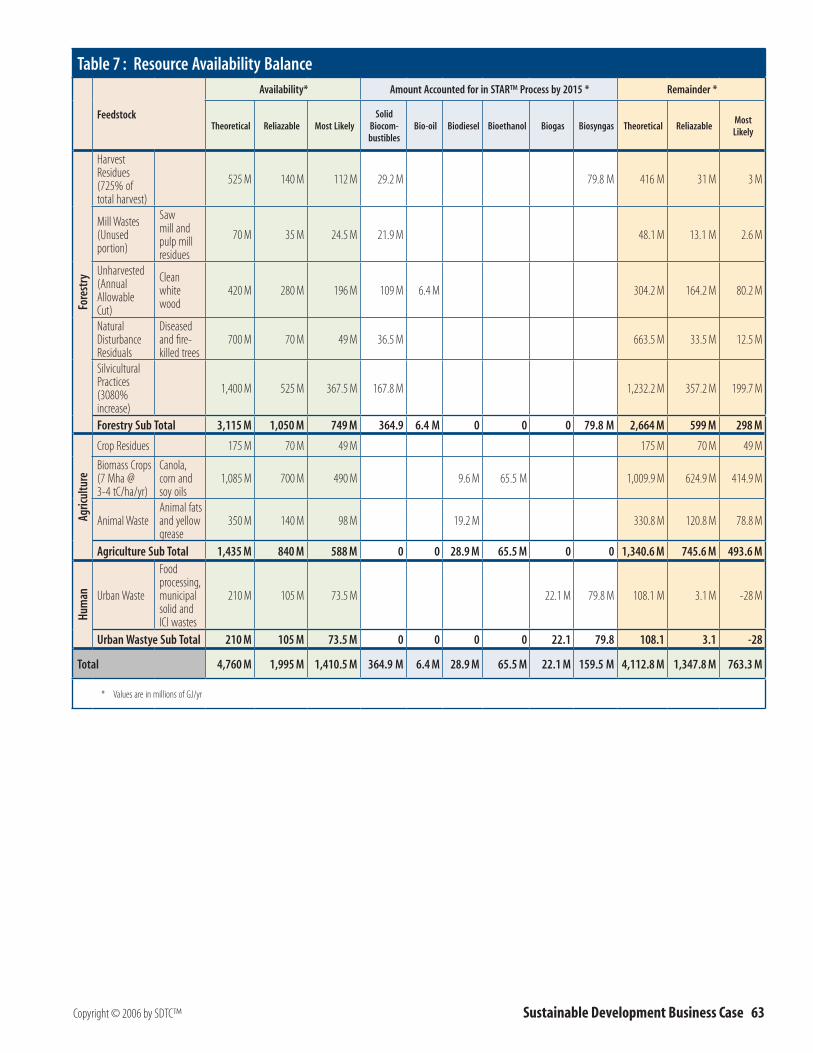

Table 7 : Resource Availability Balance ................................................................................................................................................................. 63

4 Risk and Needs Assessment and Analysis ............................................................................................... 64

4.1 Needs Summary ...................................................................................................................................................................................... 64

4.1.1 Technical Needs ........................................................................................................................................................................... 64

Table 8 : Common Biofuel Technology Needs ....................................................................................................................................................... 64

4.1.2 Non-Technical Needs ................................................................................................................................................................ 64

4.1.3 Solutions to Non-Technical Needs .................................................................................................................................... 65

Table 9 : Non-Technology Needs and Solutions ................................................................................................................................................... 66

4.2 Market Assessment .............................................................................................................................................................................. 66

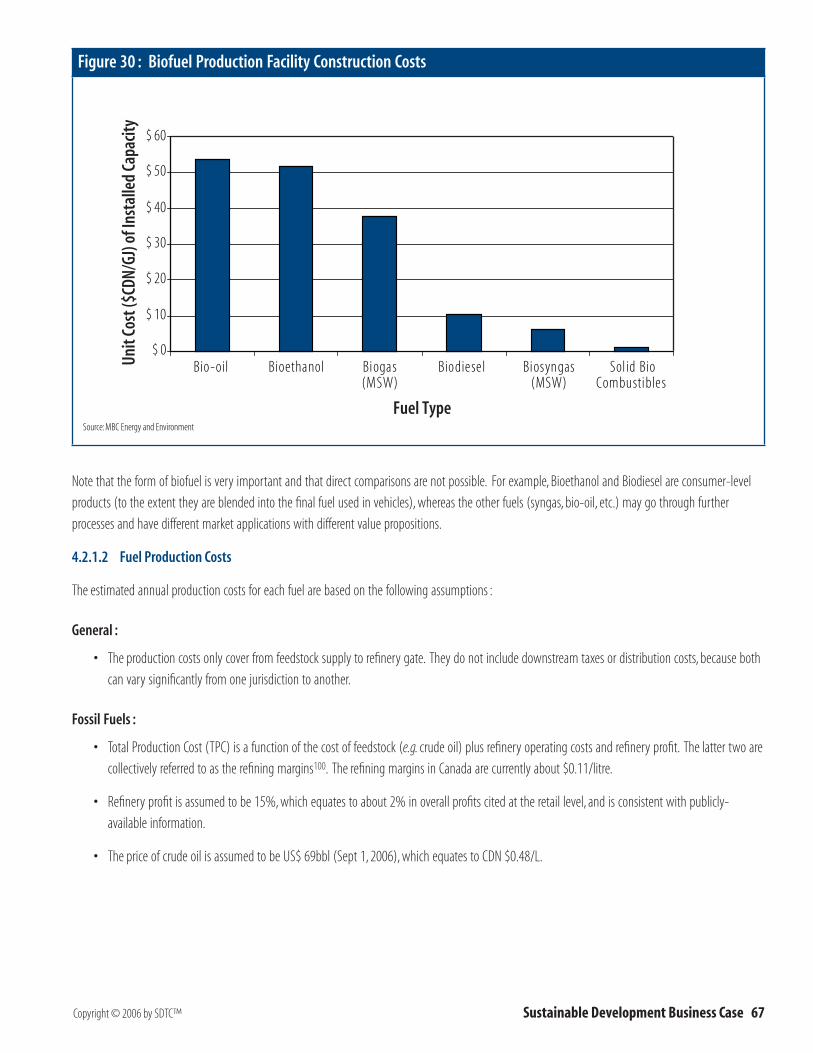

4.2.1 Biofuel Economics ...................................................................................................................................................................... 66

Figure 30 : Biofuel Production Facility Construction Costs ................................................................................................................................... 67

Figure 31 : Canadian Average Refinery Margin (1994 to 2005) ......................................................................................................................... 68

Figure 32 : Crude Oil Price Trends .......................................................................................................................................................................... 68

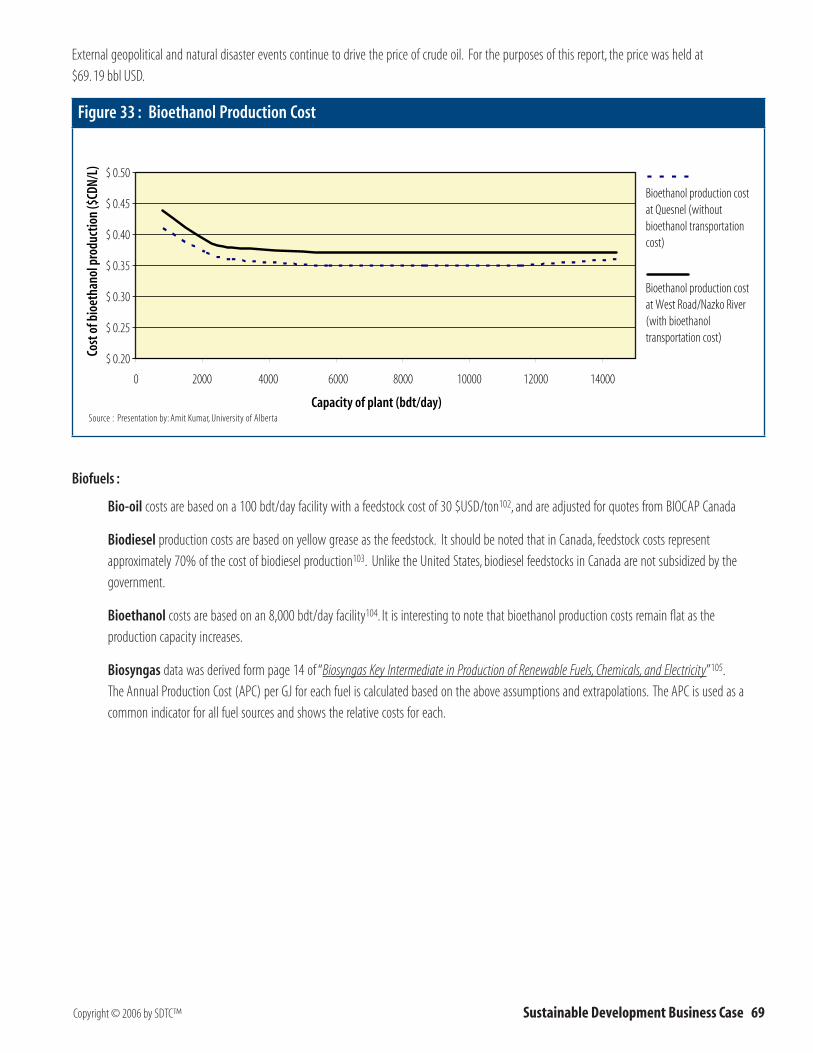

Figure 33 : Bioethanol Production Cost ................................................................................................................................................................ 69

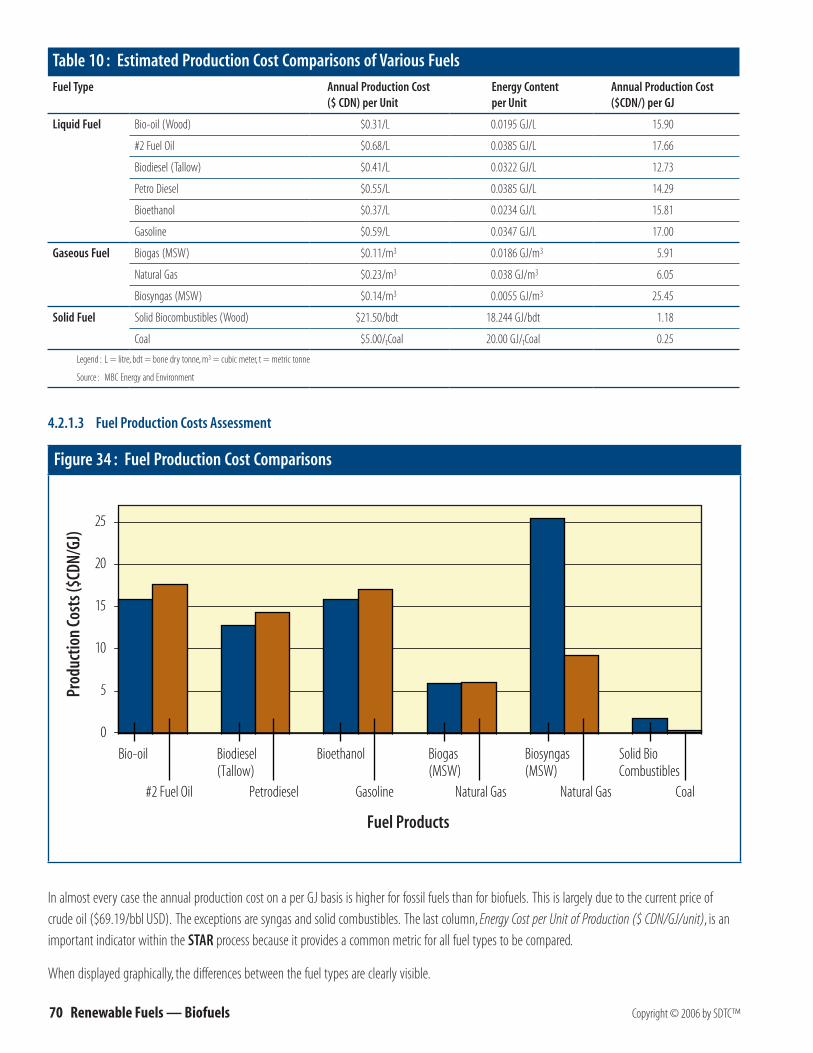

Table 10 : Estimated Production Cost Comparisons of Various Fuels .................................................................................................................. 70

Figure 34 : Fuel Production Cost Comparisons ..................................................................................................................................................... 70

4.2.2 Biofuel Market Potential ....................................................................................................................................................... 71

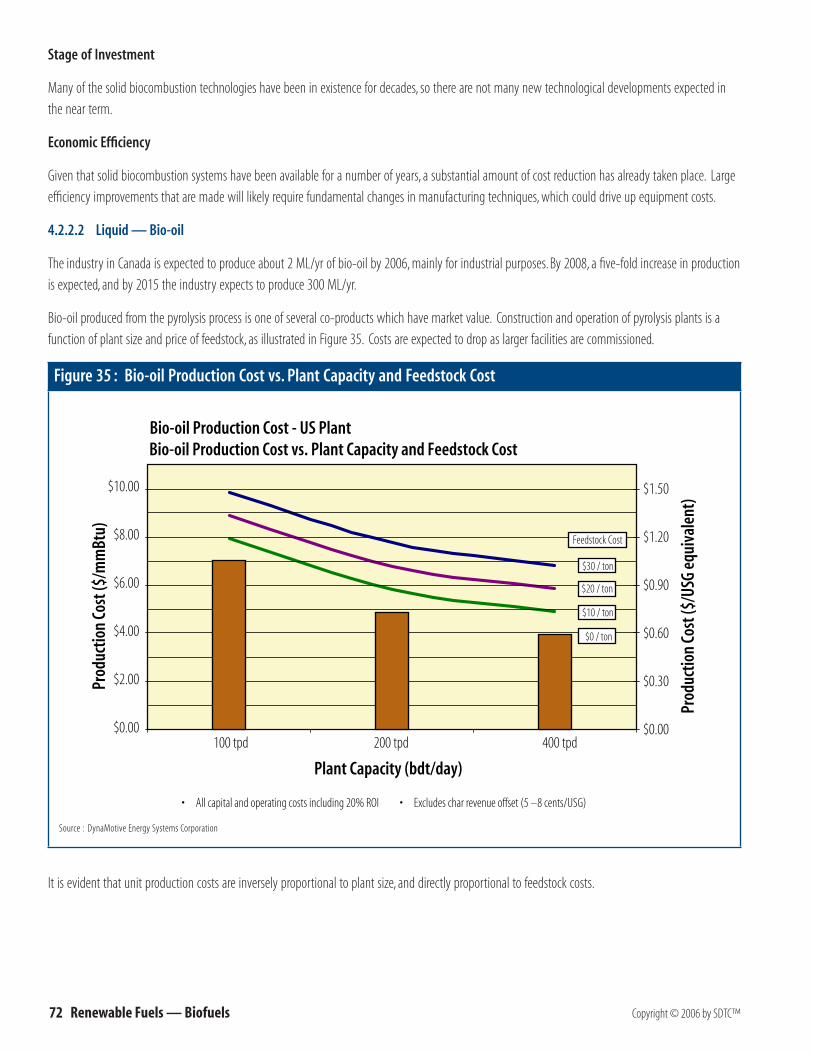

Figure 35 : Bio-oil Production Cost vs. Plant Capacity and Feedstock Cost ......................................................................................................... 72

Table 11 : Biodiesel Capital Costs .......................................................................................................................................................................... 74

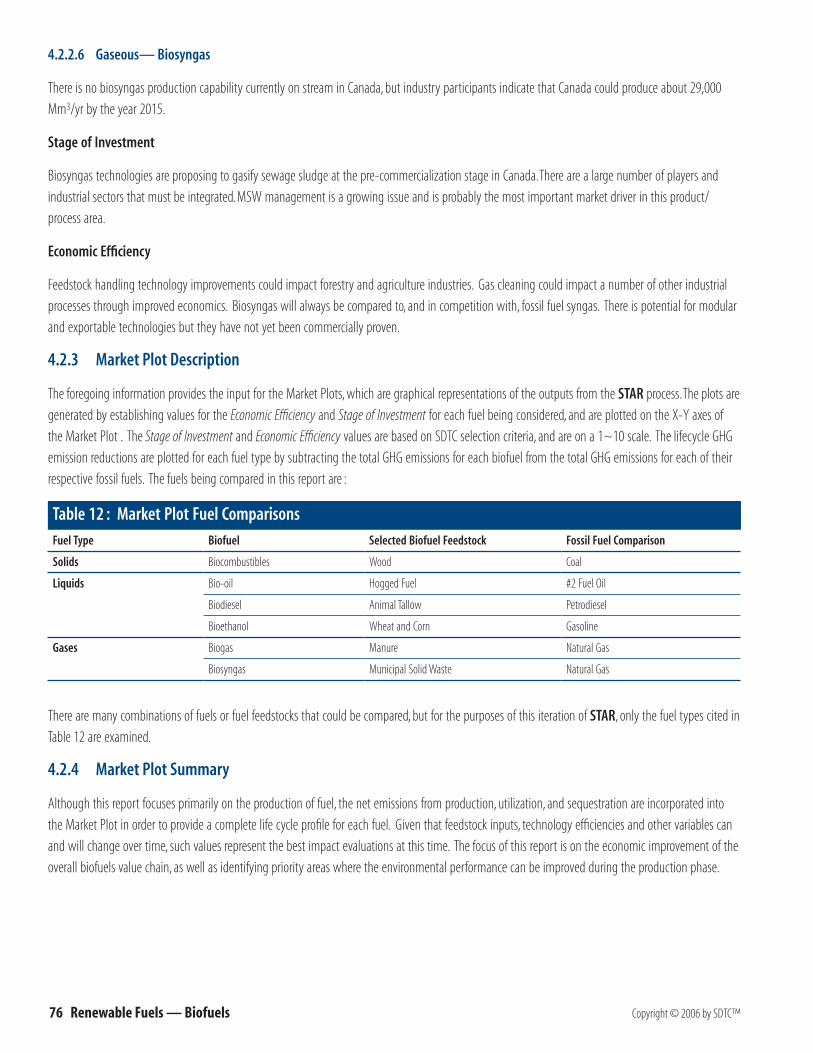

4.2.3 Market Plot Description ......................................................................................................................................................... 76

Table 12 : Market Plot Fuel Comparisons.............................................................................................................................................................. 76

4.2.4 Market Plot Summary ............................................................................................................................................................. 76

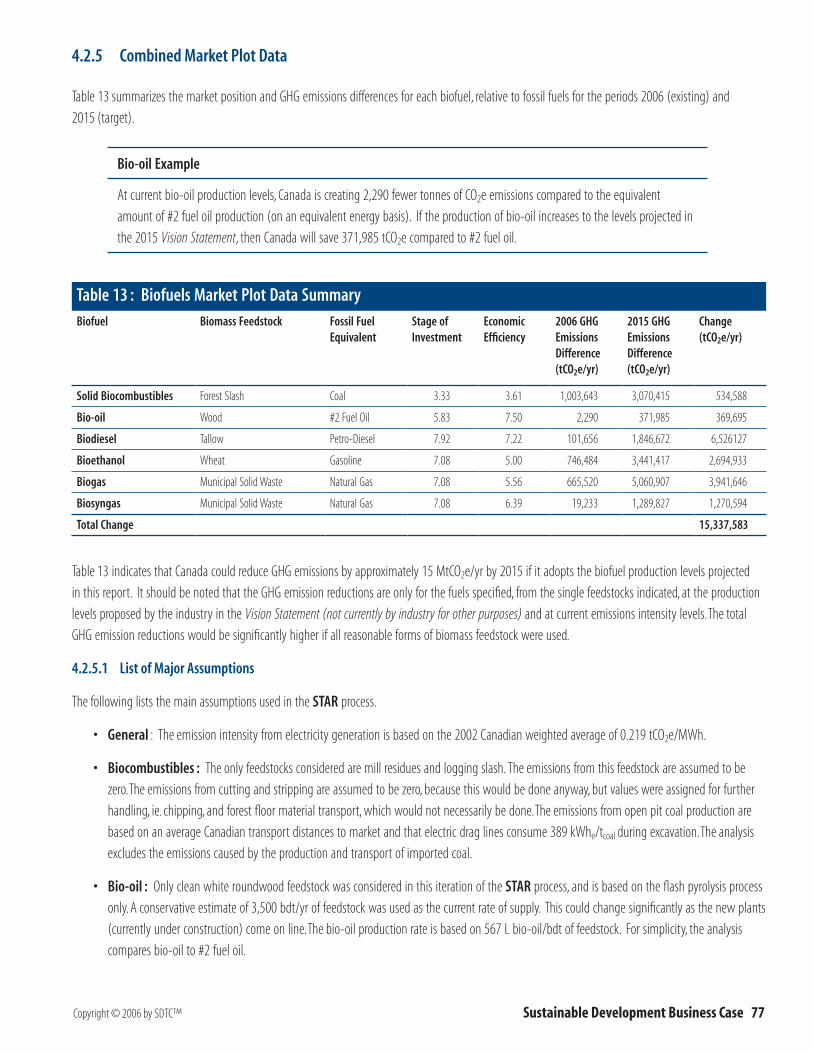

4.2.5 Combined Market Plot Data ................................................................................................................................................ 77

Table 13 : Biofuels Market Plot Data Summary .................................................................................................................................................... 77

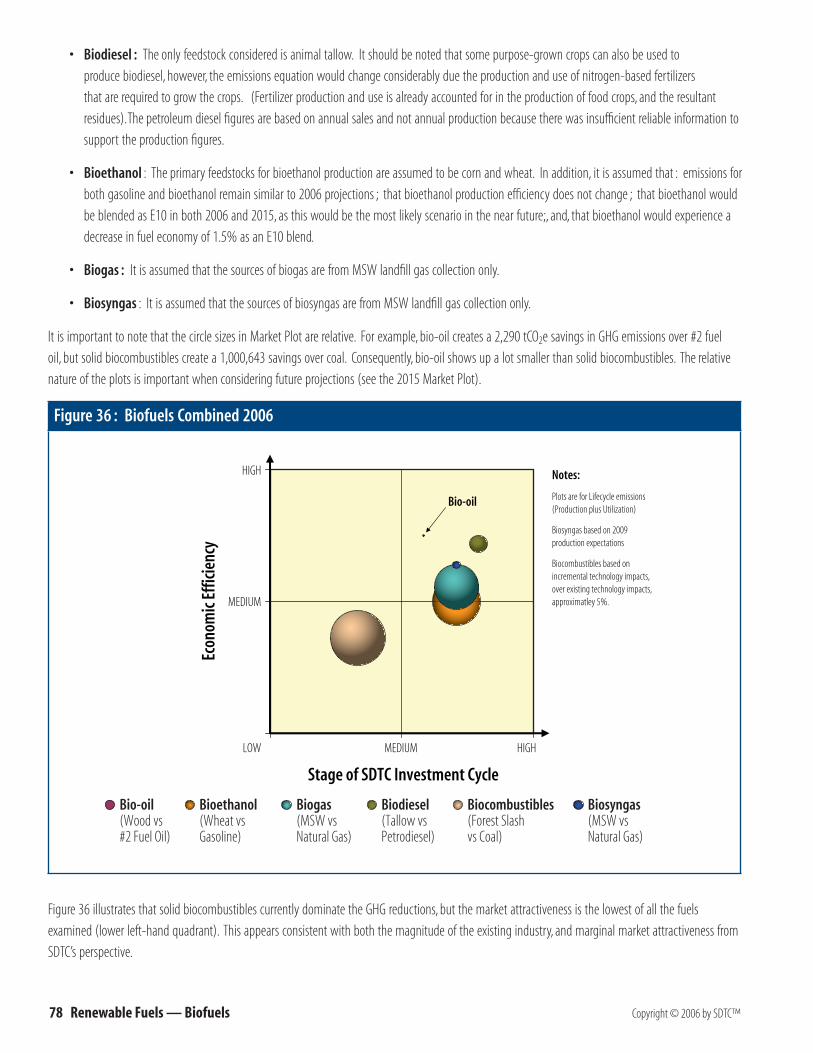

Figure 36 : Biofuels Combined 2006 ..................................................................................................................................................................... 78

Figure 37 : Biofuels Combined 2015 ..................................................................................................................................................................... 80

4.3 Technology Assessment ................................................................................................................................................................... 81

4.3.1 Solid – Biocombustibles ........................................................................................................................................................ 81

Table 14 : Solid Biocombustibles Technology Summary ...................................................................................................................................... 81

Figure 38 : Solid Biocombustibles Technology Plot .............................................................................................................................................. 82

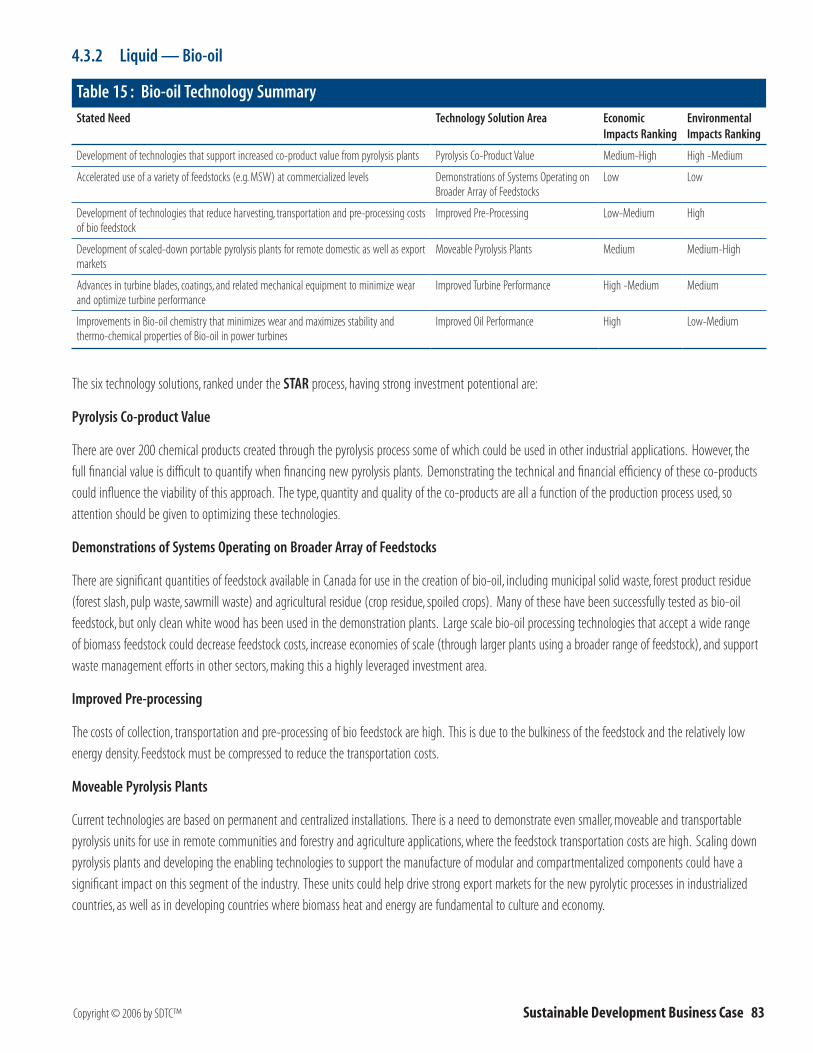

4.3.2 Liquid — Bio-oil ........................................................................................................................................................................ 83

Table 15 : Bio-oil Technology Summary ............................................................................................................................................................... 83

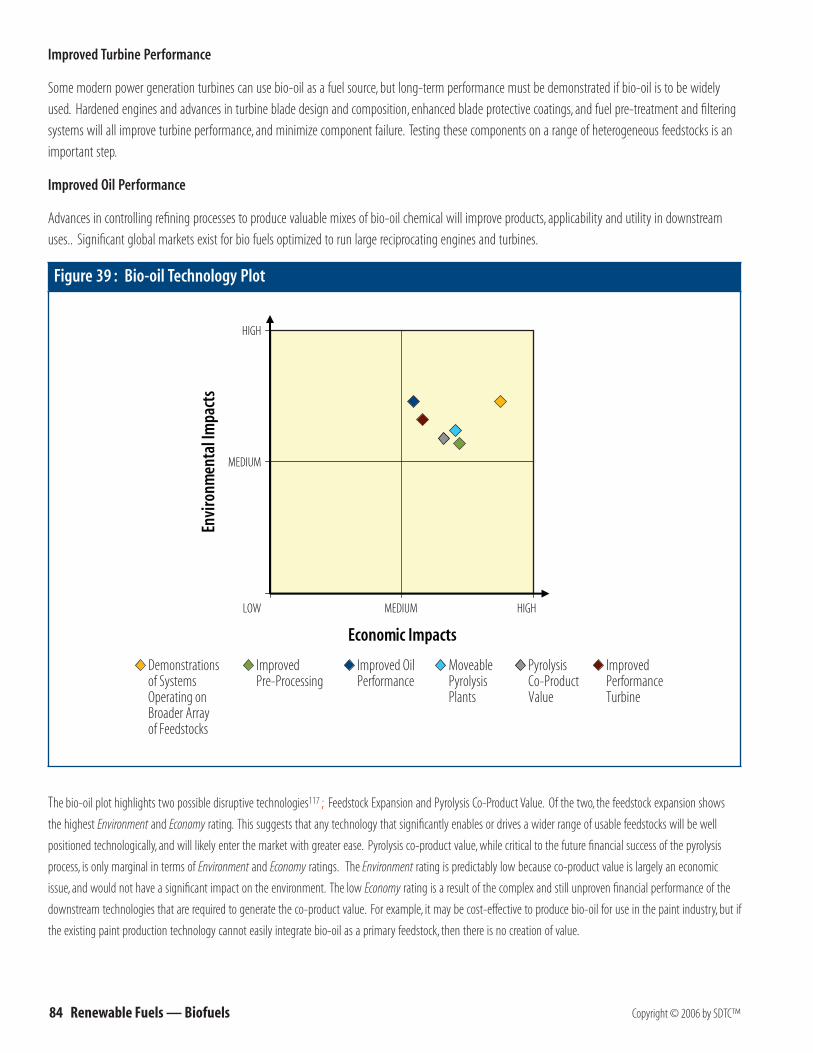

Figure 39 : Bio-oil Technology Plot ....................................................................................................................................................................... 84

4.3.3 Liquid — Biodiesel ................................................................................................................................................................. 85

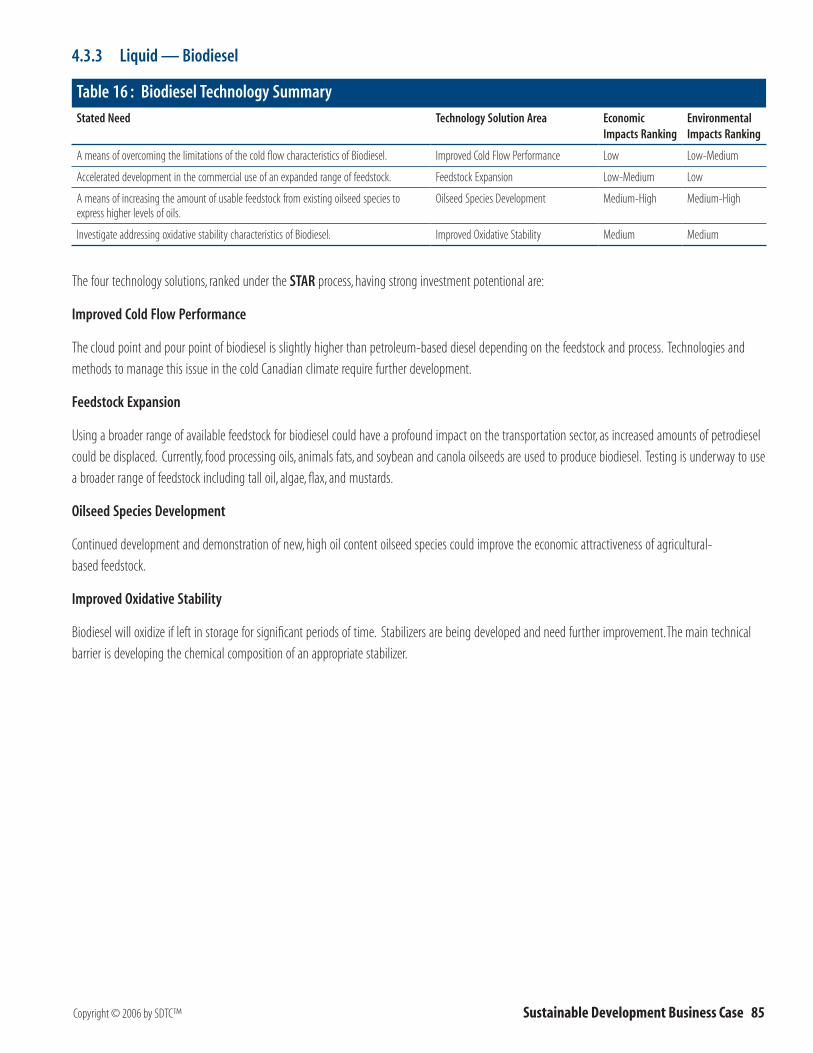

Table 16 : Biodiesel Technology Summary ........................................................................................................................................................... 85

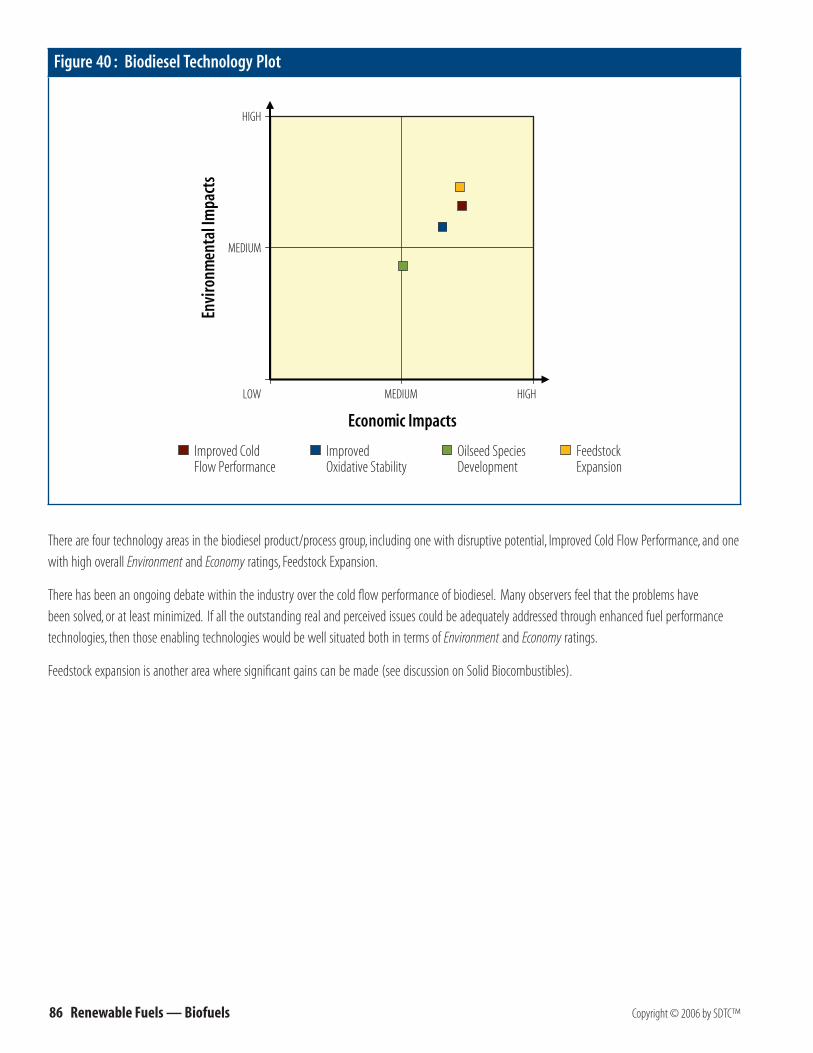

Figure 40 : Biodiesel Technology Plot ................................................................................................................................................................... 86

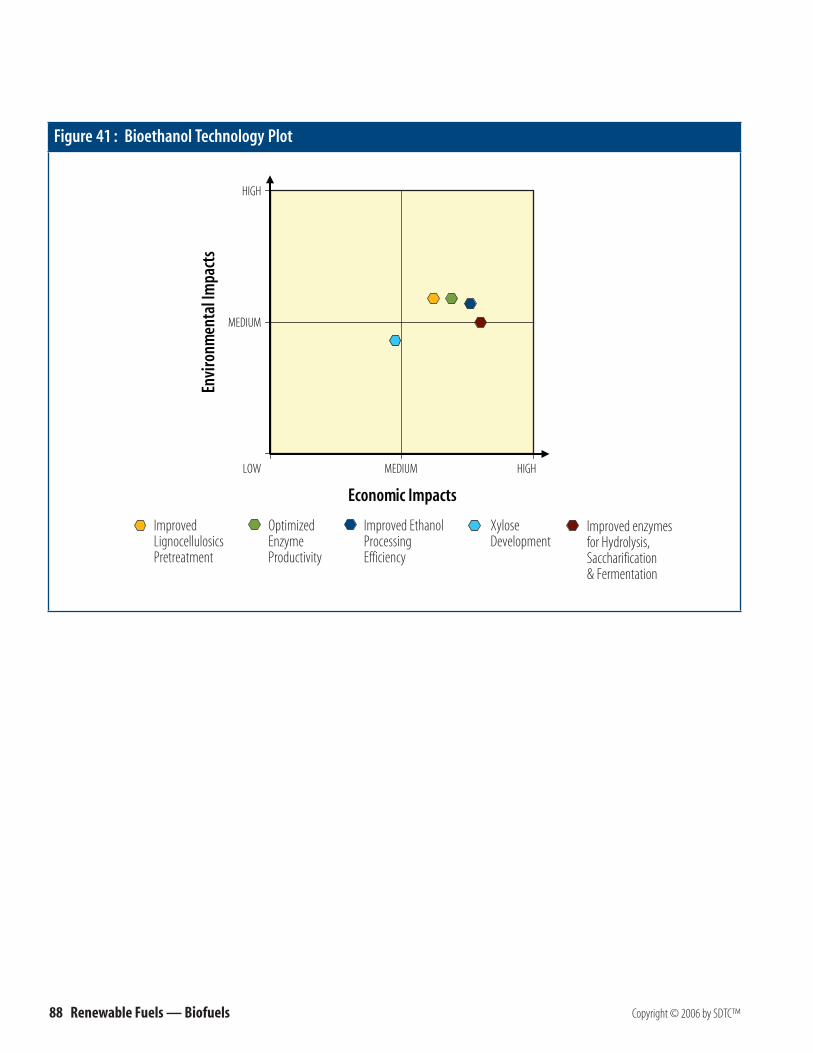

4.3.4 Liquid — Bioethanol .............................................................................................................................................................. 87

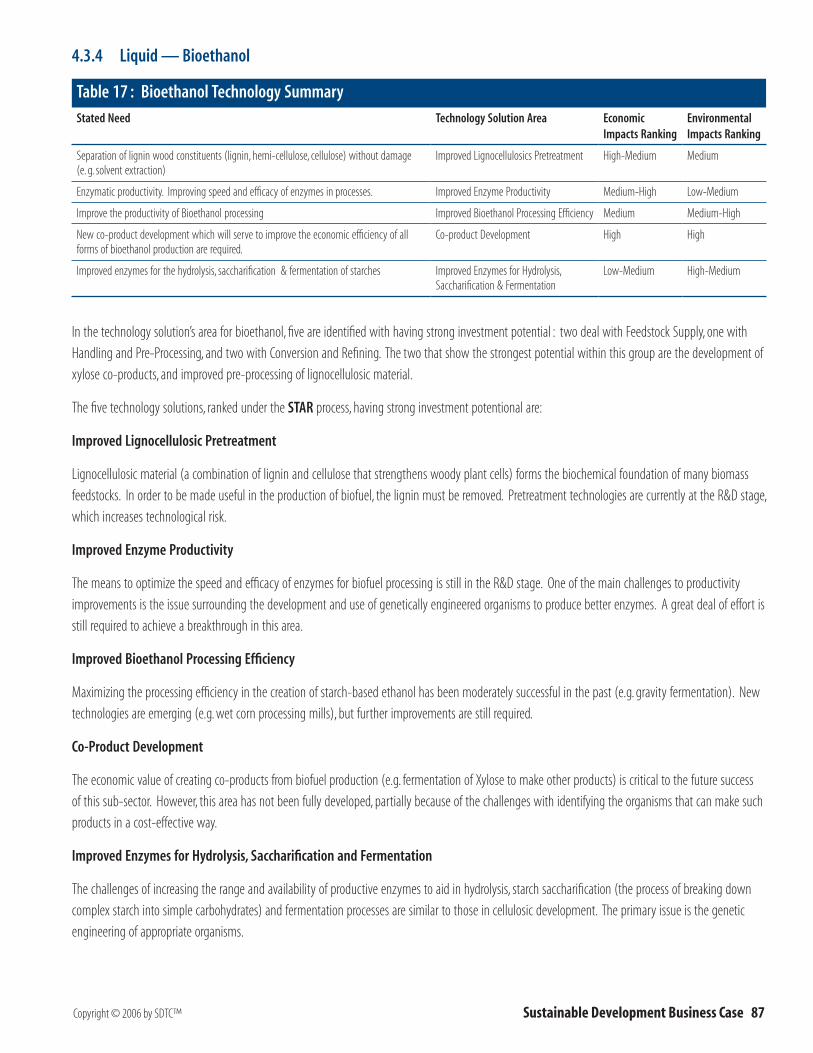

Table 17 : Bioethanol Technology Summary ........................................................................................................................................................ 87

Figure 41 : Bioethanol Technology Plot ................................................................................................................................................................ 88

4.3.5 Gaseous — Biogas .................................................................................................................................................................... 89

Table 18 : Biogas Technology Summary ............................................................................................................................................................... 89

Figure 42 : Biogas Technology Plot ....................................................................................................................................................................... 90

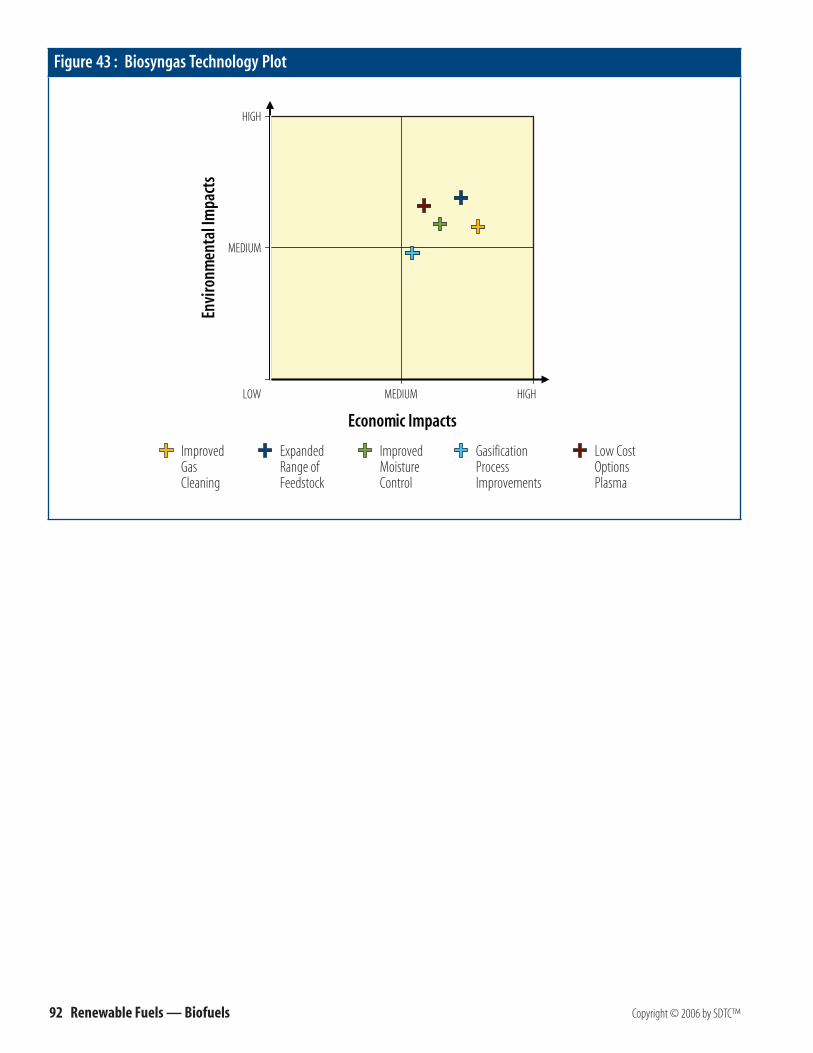

4.3.6 Gaseous — Biosyngas ............................................................................................................................................................ 91

Table 19 : Biosyngas Technology Summary ......................................................................................................................................................... 91

Figure 43 : Biosyngas Technology Plot.................................................................................................................................................................. 92

4.4 Combined Technology Summary ............................................................................................................................................. 93

Table 20 : Combined Biofuel Technology Summary ............................................................................................................................................. 93

4.5 Statements Of Interest Responses.......................................................................................................................................... 94

Table 21 : Biofuel SOI Summary ........................................................................................................................................................................... 94

5 Investment Priorities ............................................................................................................................................................ 95

5.1 Solid Biofuels ............................................................................................................................................................................................. 95

5.1.1 Biocombustibles ........................................................................................................................................................................ 95

5.2 Liquid Biofuels .......................................................................................................................................................................................... 95

5.2.1 Bio-oil .............................................................................................................................................................................................. 95

5.2.2 Biodiesel ......................................................................................................................................................................................... 95

5.2.3 Bioethanol .................................................................................................................................................................................... 95

5.3 Gaseous Biofuels..................................................................................................................................................................................... 96

5.3.1 Biogas .............................................................................................................................................................................................. 96

5.3.2 Biosyngas ...................................................................................................................................................................................... 96

5.4 Sustainability Assessment ............................................................................................................................................................ 96

5.4.1 Common Environmental Issues ......................................................................................................................................... 96

5.4.2 Specific Environmental Sustainability .......................................................................................................................... 98

Table 22 : Biofuel Environmental Sustainability Impacts ..................................................................................................................................... 98

5.4.3 Common Economic Issues ..................................................................................................................................................... 98

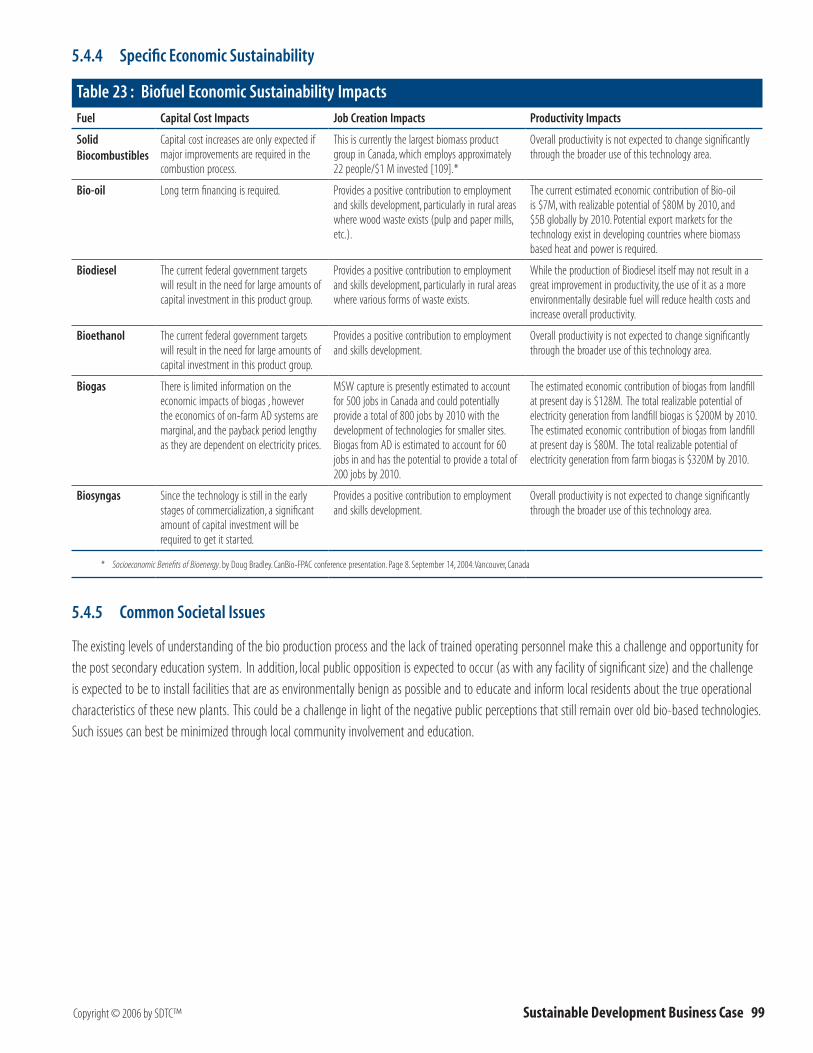

5.4.4 Specific Economic Sustainability....................................................................................................................................... 99

Table 23 : Biofuel Economic Sustainability Impacts ............................................................................................................................................. 99

5.4.5 Common Societal Issues ......................................................................................................................................................... 99

5.4.6 Specific Societal Sustainability ........................................................................................................................................ 100

Table 24 : Biofuel Societal Sustainability Impacts .............................................................................................................................................. 100

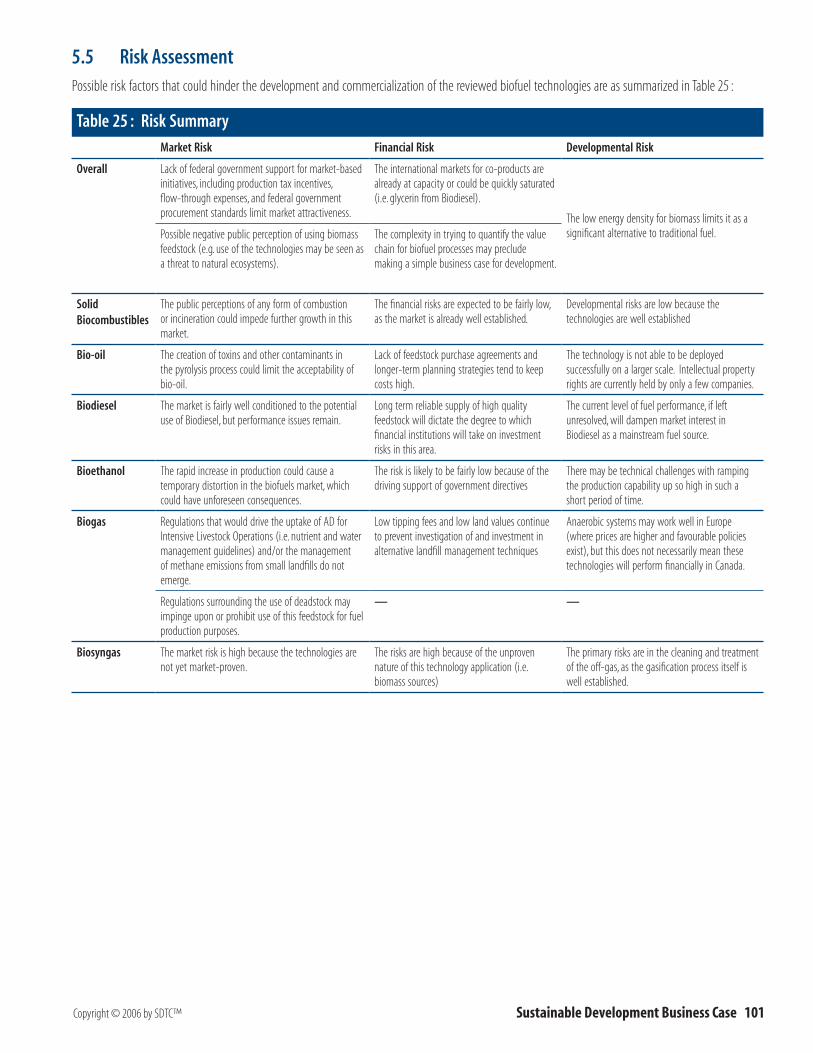

5.5 Risk Assessment .................................................................................................................................................................................... 101

Table 25 : Risk Summary ..................................................................................................................................................................................... 101

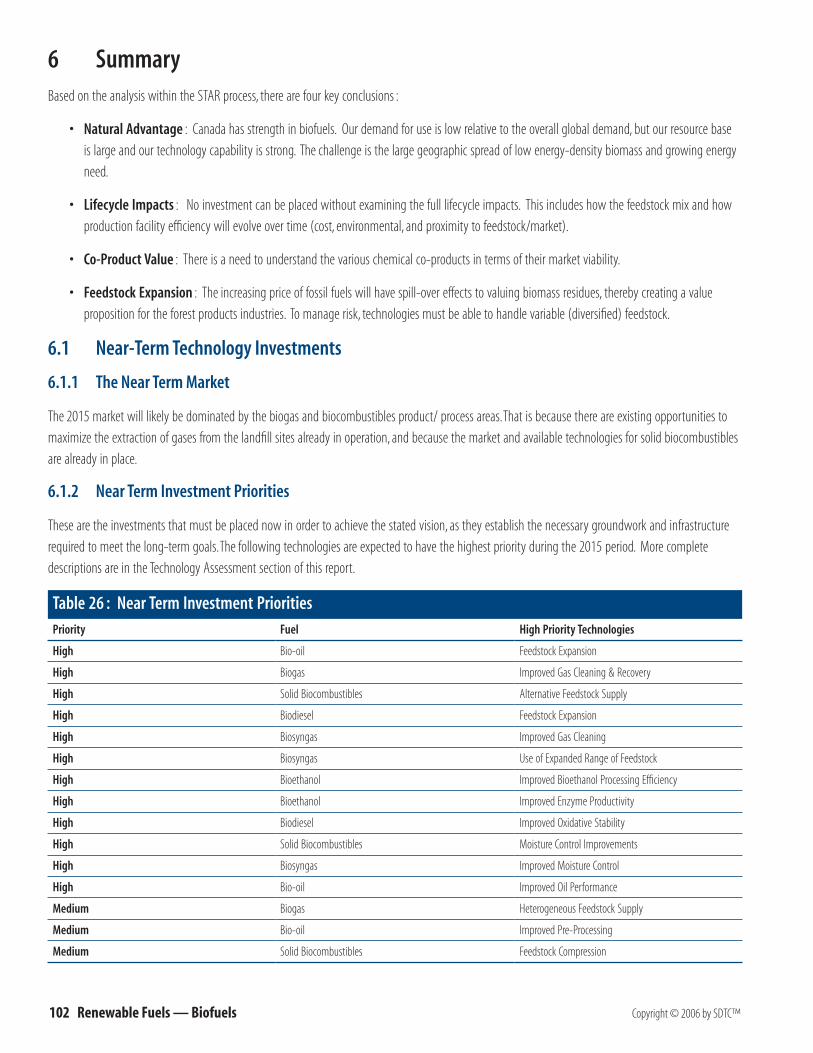

6 Summary ............................................................................................................................................................................................... 102

6.1 Near-Term Technology Investments ................................................................................................................................... 102

6.1.1 The Near Term Market ........................................................................................................................................................... 102

6.1.2 Near Term Investment Priorities ..................................................................................................................................... 102

Table 26 : Near Term Investment Priorities ......................................................................................................................................................... 102

6.1.3 Near Term Sustainability Impacts .................................................................................................................................. 103

6.1.4 Near Term Risks ......................................................................................................................................................................... 103

6.2 Long Term Technology Investments .................................................................................................................................... 103

6.2.1 The Long Term Market .......................................................................................................................................................... 103

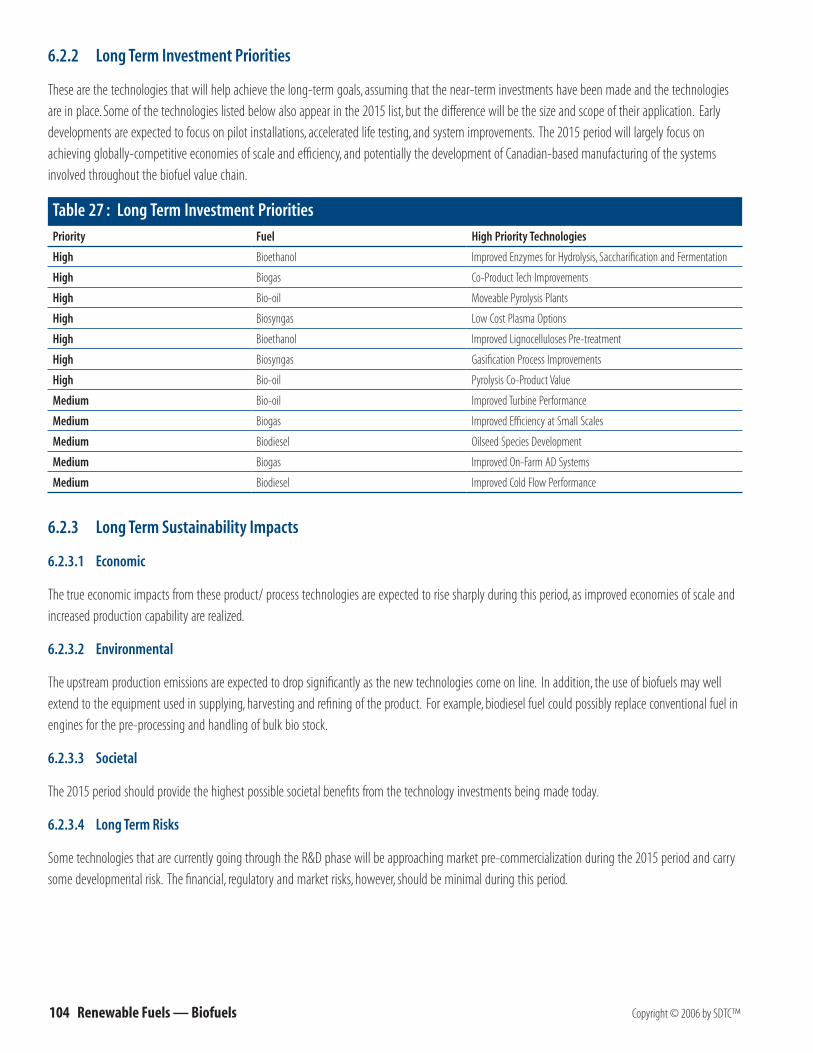

6.2.2 Long Term Investment Priorities .................................................................................................................................... 104

Table 27 : Long Term Investment Priorities......................................................................................................................................................... 104

6.2.3 Long Term Sustainability Impacts.................................................................................................................................. 104

6.3 National Strategy Impacts ........................................................................................................................................................... 105

6.3.1 Strategic Advancement ........................................................................................................................................................ 105

6.3.2 Intellectual Property ............................................................................................................................................................. 105

7 Acknowledgements .............................................................................................................................................................. 106

7.1 SDTC Thanks the Following Contributors ........................................................................................................................ 106

8 Endnotes ................................................................................................................................................................................................ 107

Copyright © 2006 by SDTC™ Sustainable Development Business Case �

1 Overview : SD Business Case™ Plan and the SDTC STAR™ Process Sustainable Development Technology Canada is a foundation created by the Government of Canada that operates a $550 million fund to support the development and demonstration of clean technologies — solutions that address issues of climate change, clean air, clean water, and clean soil to deliver environmental, economic and health benefits to Canadians.

SDTC is pleased to present this Biofuels Investment Report, which is one in a series on the current state of sustainable development and future investment priorities in Canada. This report is the result of collaboration from a wide range of stakeholders. It is based on reports, studies, and research findings by various industry associations and government initiatives. We hope you find the information useful, and look forward to working with you as we further sustainability in Canada.

1.1 The SD Business Case™ Plan

SDTC invests in areas where Canada has a strong capability, and where SDTC can provide the most value. To that end, SDTC has developed a comprehensive evaluation and decision-support process that investigates various technologies, their markets, the needs they address, and the barriers they must overcome to achieve market success.

The SD Business Case is founded on the concept of creating a common vision of market potential, as described by those in the industry. It incorporates their ideas, expectations and knowledge into a single statement of purpose, so that the outcomes are relevant, pragmatic, and realizable. There are many different approaches that could be used to analyze individual technologies or economic sub-sectors. Each stakeholder group has unique challenges and expectations, which are expressed and analyzed to suit their own needs. With this in mind, the SD Business Case has been developed to provide a common benchmark for all participants, as well as a consistent and reliable means of comparing technologies in a number of diverse and expanding areas. The SD Business Case serves as a guide to SDTC for future investment priorities as well as a means of collecting non-technology input that may be useful in policy development.

Work on the SD Business Case could not have been done without the participation and guidance of opinion leaders and experts throughout the country. Our philosophy at SDTC is to work with and through others, and we thank all these individuals for their assistance to SDTC and contributions to the success of the SD Business Case.

1.1.1 Primary Audience

The primary audiences for the SD Business Case include :

Industry Stakeholders – to help them identify key sectoral challenges and priority areas for potential future investment, and to assist in partnering with SDTC.

Canadian Researchers – to assist in providing direction and focus for successful future endeavours including indicators of the key challenges to be addressed in priority technology areas as they enter or exit the development and demonstration stages of the commercialization process.

Relevant Government Departments – to provide a comprehensive decision making framework to assist with technology investment priorities to its key stakeholders and funders. The SD Business Case may also be used to help identify and manage technological issues that are beyond SDTC’s immediate mandate, as well as non-technical market barriers that can be addressed by other players, policies, funding sources, and financial instruments.

Other Stakeholders – to provide a clear and consistent information base on relevant technology sectors, and an open dialogue on non-technology issues facing companies in a number of Canadian economic sectors.

SDTC – to highlight areas of priority attention for future investment focus and investigation.

� Renewable Fuels — Biofuels Copyright © 2006 by SDTC™

1.1.2 The SDTC STAR™ Tool

The Sustainable Technology Assessment Roadmap (STAR) tool is an iterative analytical process that combines data, reports, stakeholder input, and industry intelligence in a common information platform. It uses a series of criteria selection screens to assess and sort relevant information from a variety of sources. The output is a series of Investment Reports that highlight key technology investment opportunities for each sector under study.

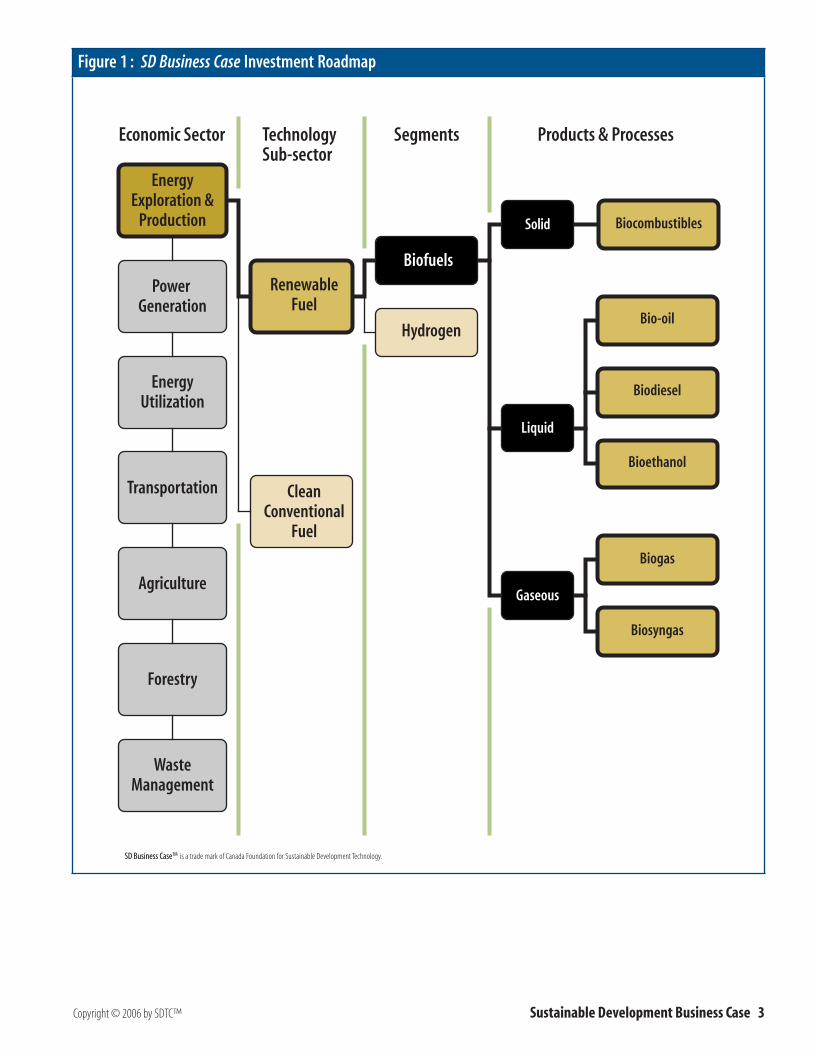

1.1.3 Sectors to be assessed by the SD Business Case™

The overall SD Business Case project focuses on seven of Canada’s primary economic sectors.1 An illustrated version of the full project and master roadmap, Figure 1, is provided on p.3 to highlight the selected areas of study.

Energy Exploration & Production – including Clean Conventional (oil and gas) and Renewable Fuels (bio-fuels, hydrogen production and purification). Note that Renewable Electricity and Renewable Fuels are linked as they share a number of technological platforms.

Power Generation – including Clean Conventional and Renewable Electricity Generation (wind, solar PV, bioelectricity and stationary fuel cells).

Energy Utilization – improving the effectiveness of the application of current end-use technologies in industrial, commercial and residential sectors (i.e. improving energy efficiency).

Transportation – including Systems Efficiency and Fuel Switching. Also note that Fuel Switching and Renewable Fuels are linked as they share a number of technological platforms.

Agriculture – addressing solid waste or Biomass conversion to Fuels and eliminating air and water contaminants produced by manure.

Forestry and Wood Products – addressing development of wood waste recycling technologies to harness energy resource potential, reduce emissions and improve productivity and profits.

Waste Management – addressing the various forms of waste management from municipal (residential and commercial) and primary and secondary industrial sources.

Note : Some of these sectors may be covered through work in other sectors. For example, many Agriculture and Forestry technologies are common to Renewable Fuels in the Energy Exploration and Production Sector.

Copyright © 2006 by SDTC™ Sustainable Development Business Case �

Figure 1 : SD Business Case Investment Roadmap

Economic Sector Technology Sub-sector

Segments Products & Processes

EnergyExploration &

Production

Power Generation

EnergyUtilization

CleanConventional

Fuel

RenewableFuel

Biofuels

Solid

Liquid

Biodiesel

Bioethanol

Biogas

Biosyngas

Gaseous

Biocombustibles

Bio-oil

Transportation

Agriculture

Forestry

WasteManagement

Hydrogen

SD Business CaseTM is a trade mark of Canada Foundation for Sustainable Development Technology.

� Renewable Fuels — Biofuels Copyright © 2006 by SDTC™

1.1.4 Investment Categories to be Analysed

The SD Business Case provides conclusions in three primary categories of investment opportunities :

• Short Term Investment Priorities – These are investments that could be made within the next 3-5 years that could have a direct and positive impact in the next 6-8 years.

• Long-Term Investment Priorities – These are early stage investments that could be made within the next 3-5 years but where the environmental impacts are realized over the longer term (greater than 8 years).

• National Strategy Impacts – Although it is not in SDTC’s mandate to advance policy initiatives, over the course of developing the SD Business Case™ a number of policy-related enablers and barriers to the development and implementation of sustainable technologies have been identified. A summary of these issues and their potential impact on Canada’s ability to meet its environmental goals is included in the analysis.

1.1.5 Conclusions Framework

The SD Business Case provides a consistent and fully referenced set of recommendations and investment indicators that can be used by stakeholders to support possible investment opportunities and priorities. It does not produce a single number, answer or result as the range of technologies and the interpretation of their future potential is too large and complex to simplify to a single solution. The output should only be viewed, and can only be understood, within the context of the information collected during the business case development process. Contributors to the business case have made every effort to be as objective, comprehensive and analytical as possible. Although based on rigorous analysis of the best available information, the SD Business Case serves only as a guide to future investment priorities ; it is not to be used as a definitive tool to accept or reject individual projects or technologies. Final decisions on whether SDTC will invest will be made by taking into account all relevant conditions and requirements.

Copyright © 2006 by SDTC™ Sustainable Development Business Case �

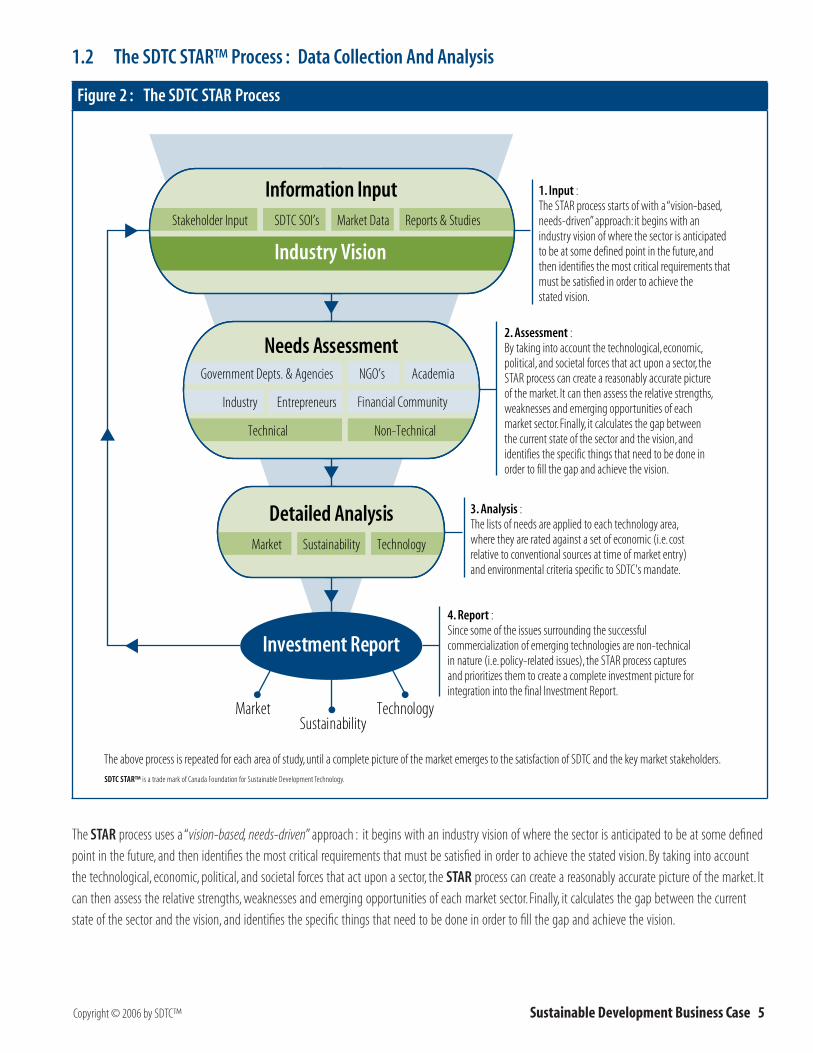

1.2 The SDTC STAR™ Process : Data Collection And Analysis

Figure 2 : The SDTC STAR Process

Industry Vision

SDTC SOI’sStakeholder Input Market Data Reports & Studies

Industry Entrepreneurs

Government Depts. & Agencies

Financial Community

NGO’s

Needs Assessment

Non-TechnicalTechnical

Information Input

Market Sustainability Technology

Detailed Analysis

MarketSustainability

Technology

Investment Report

Academia

1. Input : The STAR process starts of with a “vision-based, needs-driven” approach: it begins with an industry vision of where the sector is anticipated to be at some defined point in the future, and then identifies the most critical requirements that must be satisfied in order to achieve the stated vision.

2. Assessment : By taking into account the technological, economic, political, and societal forces that act upon a sector, the STAR process can create a reasonably accurate picture of the market. It can then assess the relative strengths, weaknesses and emerging opportunities of each market sector. Finally, it calculates the gap between the current state of the sector and the vision, and identifies the specific things that need to be done in order to fill the gap and achieve the vision.

3. Analysis : The lists of needs are applied to each technology area, where they are rated against a set of economic (i.e. cost relative to conventional sources at time of market entry) and environmental criteria specific to SDTC's mandate.

4. Report : Since some of the issues surrounding the successful commercialization of emerging technologies are non-technical in nature (i.e. policy-related issues), the STAR process captures and prioritizes them to create a complete investment picture for integration into the final Investment Report.

The above process is repeated for each area of study, until a complete picture of the market emerges to the satisfaction of SDTC and the key market stakeholders.

SDTC STAR™ is a trade mark of Canada Foundation for Sustainable Development Technology.

The STAR process uses a “vision-based, needs-driven” approach : it begins with an industry vision of where the sector is anticipated to be at some defined point in the future, and then identifies the most critical requirements that must be satisfied in order to achieve the stated vision. By taking into account the technological, economic, political, and societal forces that act upon a sector, the STAR process can create a reasonably accurate picture of the market. It can then assess the relative strengths, weaknesses and emerging opportunities of each market sector. Finally, it calculates the gap between the current state of the sector and the vision, and identifies the specific things that need to be done in order to fill the gap and achieve the vision.

� Renewable Fuels — Biofuels Copyright © 2006 by SDTC™

The lists of needs are applied to each technology area, where they are rated against a set of economic (i.e. cost relative to conventional sources at time of market entry) and environmental criteria specific to SDTC’s mandate. Since some of the issues surrounding the successful commercialization of emerging technologies are non-technical in nature (i.e. policy-related issues), the STAR process captures and prioritizes them to create a complete investment picture for integration into the final Investment Report.

The above process is repeated for each area of study, until a complete picture of the market emerges to the satisfaction of SDTC and the key market stakeholders.

1.2.1 Assessment Descriptions

Once the market vision has been accepted, the economic sectors and their associated technologies are assessed through the following four screens :

1.2.1.1 Market

This focuses on the ability of the market to carry the emerging technologies that are currently at the development and demonstration stages. It identifies what needs to be done in order to maximize the application and acceptance of the technology, with a focus on financial and economic performance.

The main components of the assessment are ;

General Market Description – an overview of the sector under consideration, with a comparison to conventional or competing sectors.

Market Potential – an indication of the immediate growth potential for the sector under consideration. The data is drawn from industry literature and stakeholder feedback, and shows the theoretical and realizable potential as well as equipment installed costs (where available). Using linear extrapolation, it then estimates the anticipated potential over the next three to five years. Due to the rapidly evolving nature of emerging markets, it is necessary to conduct this assessment a number of times as conditions change. The primary purpose is to understand the gap between today’s situation and the vision for each sub-sector. This helps to determine the required rate of innovative developments and the amount and timing of capital placements.

There are three Market Assessment criteria used in the STAR process ;

• Stage of Investment – An assigned value (on a scale of 1~10) that takes into account market barriers, the amount of time expected for the technology to achieve full commercialization, market infrastructure issues and impediments, and current state of codes, standards and regulations.

• Economic Efficiency – An assigned value (on a scale of 1~10) that takes into account technology spin-off potential, product replicability and scale-up potential, market size and dynamics, competitiveness, pricing and financing, and export potential.

• Emissions Reduction Potential – A calculated value of the difference in GHG emissions between conventional technologies and the alternative technologies within the sub-sectors under consideration. It is shown in megatonnes of carbon dioxide equivalent (MtCO2e) and is the amount of CO2e expected to be reduced or displaced within the next three to five years as a consequence of commercializing the subject technologies. Note that GHG is a proxy used as a general indicator of emissions reductions as, for most technologies, there is a positive correlation between GHG and other air emissions. Exceptions (such as the inverse relationship with NOx associated with combustion-based technologies) are noted where applicable.

The Market Assessment is conducted from the perspective of SDTC’s mandate, which is to support the development and demonstration of emerging sustainable technologies in Canada at critical stages in the development cycle. Specifically, SDTC is focused on those technologies that are between prototype development and market-ready product stages. The size and span of the blocks in Figure 3 are indicative of the relative timing and amount of funding from various sources.

Copyright © 2006 by SDTC™ Sustainable Development Business Case �

Figure 3 : SDTC Funding Support

R & D

FundementalResearch

ProductPrototype

Development

SDTC

SDTC BRIDGES THE FUNDING GAP

Demonstration Market-readyProducts

MarketEntry

COMMERCIALIZATION

Angel Investors

Venture Capital

Governments

Industry

Banks

SDTC’s Mandate :The Market Assessment is conducted from the perspective of SDTC’s mandate, which is to support the development and demonstration of emerging sustainable technologies in Canada at critical stages in the development cycle. Specifically, SDTC is focused on those technologies that are between prototype development and market-ready product stages. The size and span of the above blocks are indicative of the relative timing and amount of funding from various sources.

1.2.1.2 Technology

This concentrates on the technologies that need to be brought to market in order to achieve the stated vision. There are 15 fundamental ranking criteria, which are weighted and rolled up into two principal impact criteria :

a. Economic Impact : The developmental and financial issues related to a specific technology that can/will influence sector growth, technological inter-dependencies, infrastructure improvement, and the cost of environmental improvement ; and,

b. Environmental Impact : The magnitude of the emissions reduction potential, reductions of regional environmental pollutants, the life cycle emission returns, and the time at which these emissions reductions are most likely to occur.

1.2.1.3 Sustainability

This section describes the impact that these technologies are likely to have on individuals, communities and regions. Each technology group is evaluated in terms of its potential impact in three key areas :

a. Economic – current investment capital, company and job creation, productivity impacts ; b. Environmental – impacts on wildlife, air (GHG and regional pollution emissions), water and land and ; and,

c. Societal – health and safety, training and education, and aesthetics and property value impacts.

� Renewable Fuels — Biofuels Copyright © 2006 by SDTC™

1.2.1.4 Risk

This outlines the potential risks associated with the development and implementation of the technology, and are divided into three criteria :

• Development Risk – will the technology work as intended?• Financial Risk – is there enough private capital to fully commercialize the technology and will it be financially viable once commercialized? • Market Risk – is there sufficient market demand and infrastructure to support the technology?

1.2.2 Output Structure

There are five categories in the output : Vision and Needs, Market Assessment, Technology Assessment, Sustainability Assessment, and Risk Assessment. The STAR process combines the results from these Assessments to develop the investment report conclusions.

1.2.2.1 Vision and Needs

Vision Statements are derived from the industry, typically through industry association-published statements. The statement is reviewed by key industry stakeholders, who check for accuracy and realistic potential. The purpose is to provide focus for further discussions and analysis within the STAR process. In the case of the upstream oil and gas industry, vision is production or output driven and measured in barrels/day or Nm3/day or MCF/day. In turn, this production driven vision translates into environmental impacts such as GHG emissions, water and land usage under a “business as usual scenario”.

Typically, there are gaps between the actual current production capability and the envisioned target. The magnitude of any such gaps is the primary driver behind the analysis that follows. For example, if the gap is very small, and the target easily achievable within the near term, then proportionally fewer resources are applied to examine ways to bridge that gap. If, however, the gap is very large (as is often the case), then a considerable amount of time and resources are applied to help determine the best course of action to minimize the gap. In these cases, therefore, the industry must consider and apply more aggressive and/or effective means of achieving that target. Emerging sustainable technologies are a part of the solution, and could assist in achieving the targets set by the vision. It is also notable from this example that, without efficiency or technology improvements, significant capital investment would be required to achieve the target.

1.2.2.2 Market Assessment

The Market Assessment output data is presented in a “Circle Chart,” with Stage of Investment on the X-axis, Economic Efficiency on the Y-axis, and Emissions Reduction Potential on the Z-axis.

Circle Location – In general, plots that show in the upper right-hand corner are considered attractive because they have high Economic Efficiency and are at the optimum Stage of Investment from SDTC’s perspective. Conversely, anything in the lower left-hand corner is considered less attractive from an investment perspective.

Circle Size – The size of each circle represents the magnitude of the emissions difference between the base case and the alternative case. Note that Greenhouse Gases (expressed in CO2e) have been used as a proxy for all air-related emissions. In instances where there is a negative correlation amongst CO2e and other forms of emissions (for example NOx acts inversely to CO2e in many combustion processes), these will be noted in the model or in the actual technology as it is evaluated. The next point to note is the base case used for comparison. The alternative can produce more – or less – emissions than the conventional technology, depending on where in the value chain that the analysis is conducted. For example, the production of a new fuel can create more emissions than the production of the conventional fuel it is to replace, but the utilization of that new fuel may create fewer emissions than the utilization of the conventional fuel. As such, lifecycle analyses are conducted to help draw appropriate investment conclusions. When examining a new technology or process, the lifecycle analysis helps determine whether or not it is a beneficial area of investment. The individual process steps help determine where further improvements can best be made.

Circle Colour – In general, each circle represents a different sub-sector and is identified by a unique colour in order to distinguish them on the plot. The colour red is used exclusively to indicate negative reductions (i.e. anything in red represents a net increase in emissions relative to

Copyright © 2006 by SDTC™ Sustainable Development Business Case �

the baseline that it is being compared to). This can occur when the emissions created by the production using the new technology, process, or feedstock exceed the emissions created from the production using the baseline process or feedstock, resulting in a negative emission reduction. However, this condition may be reversed during the utilization phase—resulting in overall beneficial lifecycle emissions reductions.

Production vs. Utilization – In some cases, the STAR process includes two circle graphs or bar charts for each type of technology being examined. The inner circle (or first bar chart) represents production or upstream emissions, and is determined by calculating the difference between the GHG emissions created through the production using the baseline technology or process and the production using the new technology. The outer circle (or right-hand bar chart) represents utilization or downstream emissions, and is determined by calculating the difference between the GHG emissions caused by the utilization of the baseline technology and the utilization of the new technology. Although utilization is not the focus of this report, it is included here in order to place the entire fuel life cycle into proper context.

Because of the variation in emission creation from one stage of the value chain to another, it is important to understand the exact location of the topic under consideration in the value chain.

It is important to note that no investment can be placed without examining the full lifecycle cost and environmental impact, including how the inputs may change over time, and how the production efficiency and technologies will change over time.

By plotting the outcomes in this way it is possible to get an overall snapshot of the position and potential of each sub-sector relative to one another.

It should be noted that many of the emerging technologies have the capacity to also reduce regional pollutants (Clean Air) and other environmental impacts (Clean Water and Land) : this information is captured within the tool, but is not illustrated separately on the market plot. Separate plots can be generated for these environmental aspects.

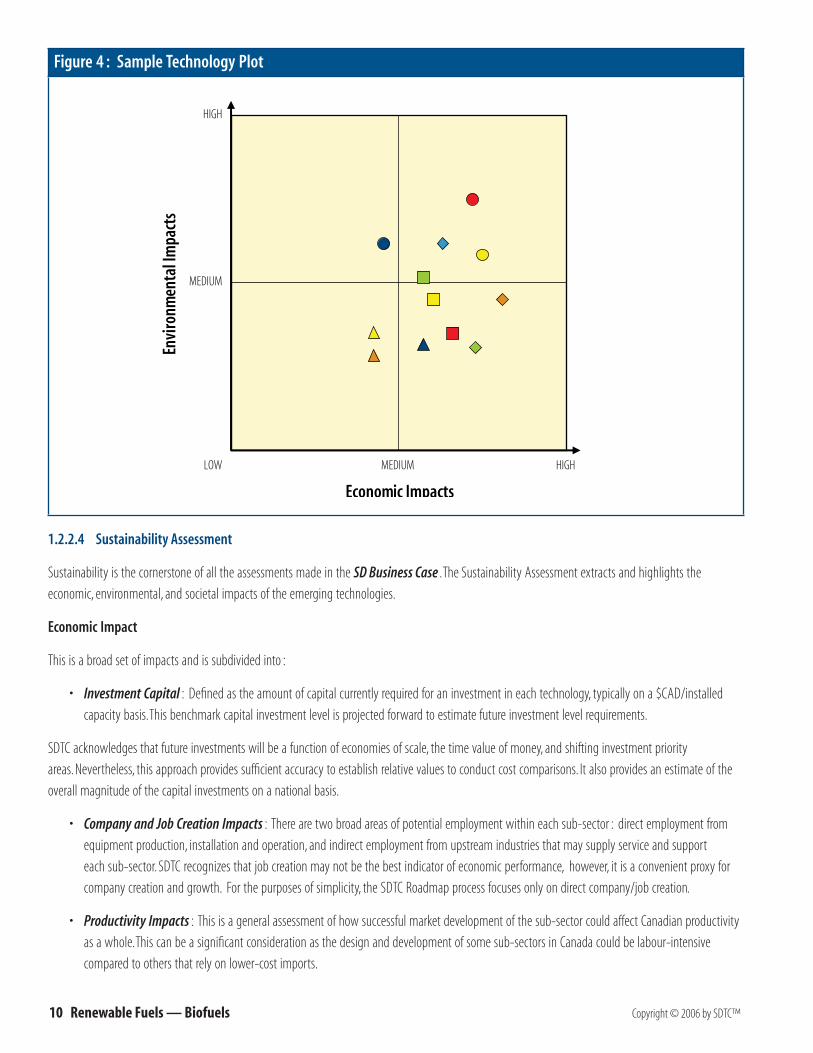

1.2.2.3 Technology Assessment

This assessment focuses on the technology plot position of each technology area. The position of each plot is the result of the numerical ranking of the individual technological assessments. Each technology is mapped on a scatter graph, with Economic Impact on the X-axis and Environmental Impact on the Y-axis.

The closer a technology plots to the upper right hand corner, the greater it’s potential, relative to the other plotted technologies. When the available processed data supports, technologies that are considered breakthrough or have a potentially disruptive impact1 are shown, in red, on the supporting scatter graph table. Since this is an iterative process, the plot values change over time as new information becomes available, new technologies are developed, and renewable energy markets continue to develop.

�0 Renewable Fuels — Biofuels Copyright © 2006 by SDTC™

Figure 4 : Sample Technology Plot

Economic Impacts

LOW

HIGH

HIGH

MEDIUM

MEDIUM

Envi

ronm

enta

l Im

pact

s

1.2.2.4 Sustainability Assessment

Sustainability is the cornerstone of all the assessments made in the SD Business Case . The Sustainability Assessment extracts and highlights the economic, environmental, and societal impacts of the emerging technologies.

Economic Impact

This is a broad set of impacts and is subdivided into :

• Investment Capital : Defined as the amount of capital currently required for an investment in each technology, typically on a $CAD/installed capacity basis. This benchmark capital investment level is projected forward to estimate future investment level requirements.

SDTC acknowledges that future investments will be a function of economies of scale, the time value of money, and shifting investment priority areas. Nevertheless, this approach provides sufficient accuracy to establish relative values to conduct cost comparisons. It also provides an estimate of the overall magnitude of the capital investments on a national basis.

• Company and Job Creation Impacts : There are two broad areas of potential employment within each sub-sector : direct employment from equipment production, installation and operation, and indirect employment from upstream industries that may supply service and support each sub-sector. SDTC recognizes that job creation may not be the best indicator of economic performance, however, it is a convenient proxy for company creation and growth. For the purposes of simplicity, the SDTC Roadmap process focuses only on direct company/job creation.

• Productivity Impacts : This is a general assessment of how successful market development of the sub-sector could affect Canadian productivity as a whole. This can be a significant consideration as the design and development of some sub-sectors in Canada could be labour-intensive compared to others that rely on lower-cost imports.

Copyright © 2006 by SDTC™ Sustainable Development Business Case ��

Environmental Impact

There are a number of additional environmental considerations that must be taken into account beyond the immediate and visible climate change and clean air impacts of the technologies employed. Although some quantitative data is available, there are instances, e.g. notably Bioelectricity, where SDTC has been unable to locate or establish a definitive position on environmental footprint. In the Bioelectricity example, there is ongoing debate on the most appropriate use of biomass waste, such as, forest floor impacts, energy versus food crops, etc. This will continue to be a challenge for the Roadmap process moving forward, but new information is constantly emerging from both internal and external sources. The future iterations of the process will continue to track new findings surrounding the following areas :

Air Impacts : The potential beneficial air impacts are evaluated under GHG Emissions Reduction Potential and Clean Air Emissions Reduction Potential.

• GHG Emissions Reduction Potential : The amount of greenhouse gases (measured as CO2e) that the technologies are expected to displace or reduce.

- Clean Air Emissions Reduction Potential : The amount of air pollutants that the technologies are expected to displace or reduce.

Water Impacts : Requirements for base material provisioning, component fabrication, and production processes often mean that a significant amount of water is stored, consumed or degraded (thermal and chemical contamination). This section examines the technology impacts on water quality and quantity.

Land Impacts : Some technologies occupy significant amounts of land while others could use sizeable land resources. This section examines land use issues, and provides a brief comparison of each.

Wildlife Impacts : Sustainable technologies, while for the most part benign, could have some negative impacts on local wildlife. Such impacts are noted and compared where applicable.

Societal Impact

From a sustainability perspective, technologies must not only be environmentally benign but must also address the educational, job growth, and property value needs that can arise as a result of their use. Impact on individuals and communities are also assessed in the following areas :

Health & Safety Impacts : The health and safety of local residences could possibly be affected by emerging technologies. While these impacts are not expected to be large, they are nonetheless identified where applicable.

Training & Education Impacts : While there may be common training and education requirements across the sub-sectors analyzed, the design, installation and operational complexity of each specific system would be assessed individually.

Aesthetics & Property Value Impacts : There are concerns (both perceived and real) that accompany the potential installation of some technologies. Where applicable, these issues are identified.

1.2.2.5 Risk Assessment

Each of the selected product or process technology area must manage various associated levels and types of risks throughout the course of becoming fully commercialized. There are two main types of risk considered : the non-technology related risks which are dependent upon political, financial and regulatory issues that may directly or indirectly influence the technology, and the technology-related risks that include developmental, financial, and market risks, as described below :

Developmental Risks : The probability that the technology will work as designed and as intended. Developmental risk is highest in the earliest stages of technology development.

�� Renewable Fuels — Biofuels Copyright © 2006 by SDTC™

b. Financial Risks : The probability that the technology will perform to the point where it is financially viable, and that there will be sufficient private funding available to see it through to commercialization.

c. Market Risks : The probability that there is sufficient demand for the technology and that market infrastructure can support the introduction and ongoing use of the technology.

1.3 Conclusions And Investment Priorities

The STAR process concludes by combining the results from the Vision and Needs, Market, Technology and Sustainability Assessments, and divides them into short and long term priorities and strategic impacts.

Short-Term Investment Priorities

These are investments that could be made within the next three to five years that could have a direct and positive impact on the environment.

Long-Term Investment Priorities

These are early stage investments that could be made within the next three to five years but that would aid Canada in meeting its longer-term, emissions-reductions objectives. SDTC recognizes that the investments must be made now in order to produce results in the future.

National Strategy Impacts

A summary is created outlining the potential impact that the investments may have on Canada’s national strategy to meet its climate change and sustainable development commitments.

The successful emergence of sustainable technologies in Canada will be largely dependant upon the resolution of a range of non-technical issues. These issues, when combined with the technology issues and opportunities, could have a profound impact on the direction of Canada’s national strategy.

Important Notes to the Reader :

While these conclusions indicate areas to place emphasis, SDTC recognizes that it is not possible to anticipate all new technologies and their impacts, and new technologies in areas or sectors not on the list are not excluded from consideration.

The output of the Roadmap process is not a single digit, answer or result. It is a series of indicators that support a set of possible investment opportunities, which can only be viewed within the context of the information provided. The final investment decision must still be made by accounting for all possible and relevant conditions and requirements, as viewed by the final decision-maker. The contributors to the Roadmap process have made every effort to be as objective, comprehensive and analytical as possible.

The numeric ratings used in the assessment process are relative ; they are not absolute. For example, the Time to Market rating is based on a scale of one to ten ; it does not indicate the actual number of years to get to market. This approach is necessary to overcome the wide range of qualifiers associated with each projection made by industry and government. The one to ten scale provides a common benchmark approach.

Unless otherwise stated, the term “market” refers to the set of technology areas under examination as a direct result of a scoping exercise to determine an appropriate breadth of coverage. It does not refer to an entire market.

Emerging Technologies that have not been included within any current sector assessment may be considered in future upgrades and published releases. SDTC will receive and evaluate opportunities in all areas falling within the SDTC mandate. However, where there is insufficient material or interest identified, no assessment priority will be assigned to the STAR tool.

Copyright © 2006 by SDTC™ Sustainable Development Business Case ��

2 Executive Summary : BiofuelsThere is enough biomass feedstock currently available in Canada to realistically satisfy about 6% of the country’s total energy needs, (not counting current forest product industry uses as stated by BIOCAP 2006). The challenge is to optimize the processing and conversion of this renewable resource into a usable and reliable source of fuel. Because of Canada’s increasing need for energy, and a desire to reduce emissions, the Canadian biofuels industry could go through a radical transformation in the next few years.

2.1 Biofuels

Biofuels are any renewable fuel that can be derived from living and recently living, biological material (biomass). They can be in the form of a solid, liquid or gas and can either be used directly as a primary fuel for electricity and heat generation, or as a feedstock to produce intermediate refined secondary fuels and chemicals. Biomass can be converted into biofuels by thermal, chemical, biological and/or physical processes.

Primary feedstocks include a variety of non-homogeneous materials such as agricultural crops and crop residues, manures, animal deadstock, forestry residues, forestry products industry residues, food processing industry residues, energy crops, and the organic portion of waste. This distinguishes biofuels from other fossil fuel industries that typically use homogeneous of raw materials. The dominant feedstocks today are residues and wastes from processing industries, especially forest and farming residues. In the future, it is expected that a greater range of biomass (such as purpose-grown crops) could be

used.