renault atlas 2013group.renault.com/.../atlas-renault-march-2014-en.pdf · renault atlas april 2014...

TRANSCRIPT

(www.renault.com)

(www.media.renault.com)

DRIVE THE CHANGE

RENAULT ATLAS 2013APRIL 2014 EDITION

Cove

r con

cept

: Eur

okap

i Gro

upe

- De

sign

/Pro

duct

ion:

Scr

ipto

ria -

Axi

om G

raph

ic P

rintin

g COUV-ATLAS-2014-ang 14/04/14 7:35 Page 1

RENAULT ATLAS APRIL 2014 01

CONTENTSRENAULT GROUP

04 Key figures05 One Group, 3 brands06 Group highlights08 Highlights for the Europe region09 Highlights for France10 Highlights for the Euromed-Africa region11 Highlights for the Eurasia region12 Highlights for the Asia-Pacific region13 Highlights for the Americas region14 Strategic plan15 Simplified structure / Equity ownership16 Organization chart18 Financial information19 Workforce20 Corporate social responsibility21 Points of reference, 115 years of history

MANUFACTURING AND SALES24 Industrial sites26 Global production32 Global sales35 Sales in the Europe region39 Sales in the Euromed-Africa region41 Sales in the Eurasia region42 Sales in the Asia-Pacific region44 Sales in the Americas region

PRODUCTS AND BUSINESS 48 Vehicle ranges54 Powertrains58 Motorsport62 Research and development65 Electric vehicles66 Purchasing67 Supply chain68 Sales network69 RCI Banque70 After-sales71 Renault Tech

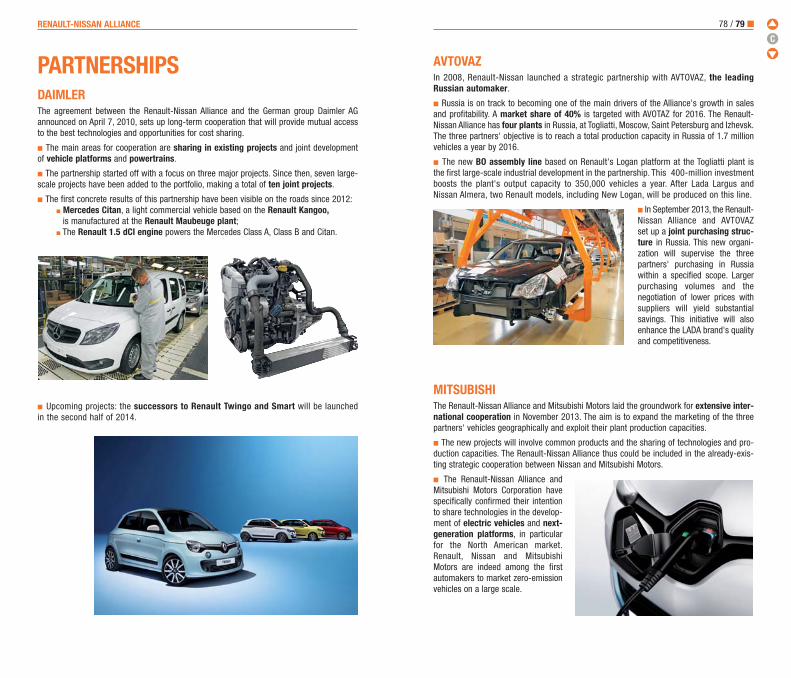

RENAULT-NISSAN ALLIANCE 74 Overview75 Highlights in 201376 Synergies78 Partnerships80 Sales

This document is also available on the websiteswww.renault.com and www.media.renault.com

RENAULTGROUPRenault has been making cars since 1898. Today, it is an international group with globalsales of over 2.6 million vehicles in 2013. The Group is developing three complementarybrands. Renault is a global brand, Dacia a regional brand, and Renault Samsung Motorsa local brand. The Renault-Nissan Alliance is the world's fourth biggest automotive group.

RENAULT ATLAS APRIL 2014 02 / 03 �

C

04 / 05 �

ONE GROUP,3 BRANDS

2,131,494 vehicles sold

429,540vehicles sold

67,174vehicles sold

Renault has been building automobiles since 1898. Today it is a multinational, multi-brand group that sold more than 2.6 million vehicles in 128 countries in 2013.

It has nearly 122,000 employees and 37 industrial sites, where it manufactures vehiclesand powertrain parts.

To meet the major technological challenges of the future while continuing to pursue its pro-fitable growth strategy, the Renault group is:� committed to sustainable mobility for all, with innovative solutions like electric

vehicles;� implementing an offensive strategy of international expansion;� developing its partnerships: alliance with Nissan, cooperation with AVTOVAZ in Russia,Daimler and Mitsubishi, agreement with Dongfeng in China;� benefiting from the complementary ranges of its three brands: Renault, Dacia, and

Renault Samsung Motors.

RENAULT

The Group's global brand,Renault is present in

128 countries, with over12,000 points of sale.

During its 115-year history,Renault has forged itsidentity as a companyserving people throughingenious innovation.

DACIA

Dacia is a regional brandof the Group, marketed in43 countries in Europe,North Africa and Turkey.

It has attracted 2.7 millioncustomers since 2004by offering a range of

robust vehicles ataffordable prices.

RSM*

RSM is a local brandof the Group that markets

mid-range and luxurycars as well as sportutility vehicles (SUVs)

in South Korea.

* Renault Samsung Motors

RENAULT GROUP

KEY FIGURES(1)

€ 40,932 million

2013 revenues

RENAULT GROUP

2012 20122013 restated published

Revenue 40,932 40,720 41,270€ million

Net incom 695 1,712 1,735€ million

2013 2012

Workforce 121,807 127,086

Number of vehicles sold(3) 2,628,208 2,548,622

(1) Published figures, except restated figures.(2) Restated to reflect the retroactive application of the IFRS 11 “Partnerships” and revised IAS 19“Employee benefits” standards.(3) All PC/LCV sales figures in the Atlas exclude Twizy.

(2)

C

06 / 07 �

HIGHLIGHTS OF2013

JANUARYDuster is voted Car of the Year in India.An enormous success, it has been theGroup's best-selling vehicle since itslaunch in 2010.

FEBRUARYClio R.S. 200 EDC and Clio Estate arelaunched.

Clio IV ranks third in Europe and first inFrance in full-year sales.

MARCHZOE, the first affordable all-electric car, islaunched. Renault is the leader in electricvehicle sales in Europe.

Competitiveness: the “Contract for a newdynamic of Renault growth and socialdevelopment in France” is signed.

Production capacity is increased at theCuritiba plant to support Renault's growthplan in Brazil.

APRILCaptur is launched. Renault's city-carcrossover is No. 1 in its category inFrance and Europe.

The Twin'Z concept car is unveiled.

MAYRenault vehicles shine in the ADAC 2013(German Automobile Club) reliabilitysurvey. The Group's models have beenconsistently judged “good” or “excellent”for six years running.

The Twin Run concept car is unveiled.

JUNERenault presents the results of itscollaboration with Nissan on commonarchitectures for future Alliance vehicles(Common Module Family). This approachwill reduce per-model engineering costsby an average of 30% to 40%.

Renault unveils the new Renault EnergyF1-2014 Power Unit with electrical energyrecovery. Renault capitalizes on know-how gained in F1 to continually improvethe efficiency of its series engines.

Alpine returns to the 24 Hours of LeMans.

Carlos Ghosn is appointed chairmanof the AVTOVAZ board of directors. Oneout of three cars sold in Russia comesfrom the Renault-Nissan Alliance and itspartner AVTOVAZ.

SEPTEMBERThe concept car that offers a glimpse ofEspace’s successor is presented at theFrankfurt Motor Show.

Renault signs a partnership deal withIndomobil aimed at developing businessin Indonesia.

Thierry Bolloré is appointed ChiefCompetitive Officer and Jérôme StollChief Performance Officer.

OCTOBERThe 2nd production line is inauguratedat the Tangiers plant in Morocco.

NOVEMBER

Victory in Formula One: Renault is theworld champion engine manufacturerfor the 12th time.

Captur is launched in South Korea.

The Renault-Nissan Alliance and MitsubishiMotors explore wide ranging globalproduct and technology cooperation.

DECEMBERRenault and Dongfeng sign an agreementenabling Renault to create an industrialfacility in China.

RENAULT GROUP

C

HIGHLIGHTS FOR REGIONS 08 / 09 �RENAULT GROUP

HIGHLIGHTS OF 2013EUROPE REGION

Captur, the first B segment SUV in EuropeThe crossover city car Captur stakes its claim as

the first B-segment SUV in Europe (and in France).

� With the launch of ZOE in Europe,Renault becomes the European leader inelectric vehicle sales, with a 37.1% mar-ket share.

� New Clio comes in third in Europe inits first full year on the market in numerousEuropean countries.

� Dacia records the fastest growth ratein Europe among all brands, with a 26%increase in volume. Driving the big gainwere Duster's popularity and the renewalof the Logan/Sandero range. Dacia alsoboasts the youngest vehicle range inEurope.

� Five models emit less than 100 gramsof CO2/km: Twingo, New Clio, Captur,Megane and Dacia Sandero. The Renaultgroup takes the lead in Europe in cuttingCO2 emissions, with an average of 115.9

grams of CO2/km per vehicle*. The key fac-tors are a younger vehicle range, the suc-cess of its Energy engines, and rising salesof its electric vehicles.

� The Renault brand ranks third in thePC + LCV market in Europe, with a 7.4%market share.

� In Spain, the Valladolid Motores plantsets an annual production record bymanufacturing 1.2 million engines andover 15 million machined parts.

* Average CO2 emissions of registered Renaultgroup PCs for the certification New EuropeanDriving Cycle (NEDC) in the first half of 2013 in 23EU countries (Source: AAA DATA).

� ZOE is the top-selling electric vehiclein France in the consumer market, with a62% market share.

� New Clio is the top-selling car in theFrench market, with 103,000 registrations.

� The Contract for a new dynamic ofRenault growth and social developmentin France is signed. Termed “historic” bythe media, this agreement guarantees thatFrench plants will be competitive.

� Dacia is the fifth-ranking brand in theFrench market. New Sandero becomes thethird-best-selling passenger car.

� The Renault brand takes first place inthe Passenger Car market and the LightCommercial Vehicle market. It remains thePC+LCV leader.

� The Renault network is voted No. 1 inafter-sales service by its customers.

FOCUS ON FRANCE

6 of the 10 best-selling vehiclesThe Renault group produces six of the ten

best-selling passenger cars: New Clio, Scenic,Megane, New Sandero, Captur and New Twingo.

C

� As part of Renault's development stra-tegy in Africa, new partnerships havebeen formed, including ones in Libya,Nigeria, Ghana, Mozambique and Kenya.

� At the Tangiers plant in Morocco, thesecond production line is inaugurated inOctober. It will increase production capaci-ty to 340,000 vehicles a year as of 2014,making this the largest car plant in Africa.The new line will be used to manufactureSandero and Sandero Stepway.

� In Algeria, construction of the Oranplant gets under way in September. Thefirst employees have been hired. The newplant, which will produce 25,000 NewSymbol a year, is to come on line inNovember 2014.

� For the eighth year in a row, theRenault group is the leader in Algeria,with sales of nearly 112,000 vehicles andmarket share of over 26%. The Daciabrand is on the podium for the first time.

� In Morocco, the Renault group winds up2013 with a 38.9% market share. TheDacia and Renault brands had six of theten best-selling models. They were, indescending order: Dacia Logan, Sandero,Dokker, Renault Kangoo, Dacia Duster andRenault Nouvelle Clio.

� Full-year sales of New Clio are strong. Itranks in the top 3 in its segment in themajor countries. In Turkey, New Clio is theB-segment leader, with a 16% segmentmarket share.

HIGHLIGHTS FOR REGIONS 10 / 11�RENAULT GROUP

EURASIA REGION

The N°1 foreignbrand in Russia

Renault, the leading foreign brand in Russia,ranks second in the Russian car market.

EUROMED-AFRICA REGION

Almost 13%market share in AfricaRenault has the third-largest market share

on the African continent.

� Renault Duster is the top SUV in theRussian market. Since its launch in March2012, over 100,000 Duster have beensold.

� The Moscow plant celebrated the pro-duction of its 500,000th Logan (since April2005), and its 100,000th Duster (sinceDecember 2011).

� New Fluence and Duster 4x4 BVA arri-ve at dealerships in the region.

� Dokker is launched in the Azerbaijan,Georgia, Belarus and Ukraine markets.

� More than 48,000 loans are granted inthe Renault CREDIT program. By creatingthe RN Bank, the Alliance has made finan-cial products and services even moreaffordable for the brand's customers.

� In Kazakhstan, sales quadruple, com-pared with 2012, rising to roughly 5,000cars, notably owing to Duster's popularity.

C

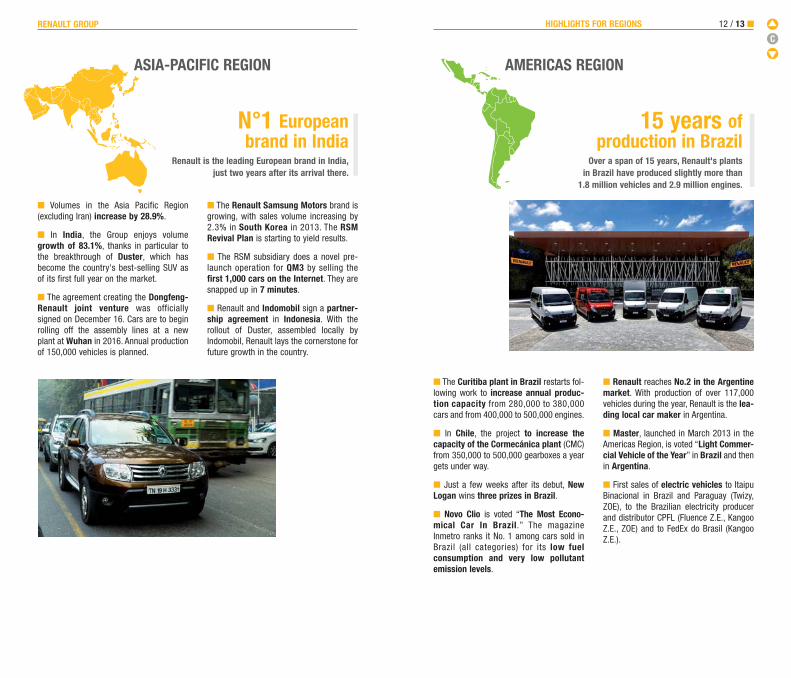

� Volumes in the Asia Pacific Region(excluding Iran) increase by 28.9%.

� In India, the Group enjoys volumegrowth of 83.1%, thanks in particular tothe breakthrough of Duster, which hasbecome the country's best-selling SUV asof its first full year on the market.

� The agreement creating the Dongfeng-Renault joint venture was officiallysigned on December 16. Cars are to beginrolling off the assembly lines at a newplant at Wuhan in 2016. Annual productionof 150,000 vehicles is planned.

� The Renault Samsung Motors brand isgrowing, with sales volume increasing by2.3% in South Korea in 2013. The RSMRevival Plan is starting to yield results.

� The RSM subsidiary does a novel pre-launch operation for QM3 by selling thefirst 1,000 cars on the Internet. They aresnapped up in 7 minutes.

� Renault and Indomobil sign a partner-ship agreement in Indonesia. With therollout of Duster, assembled locally byIndomobil, Renault lays the cornerstone forfuture growth in the country.

HIGHLIGHTS FOR REGIONS 12 / 13 �RENAULT GROUP

AMERICAS REGION

15 years ofproduction in Brazil

Over a span of 15 years, Renault's plantsin Brazil have produced slightly more than

1.8 million vehicles and 2.9 million engines.

ASIA-PACIFIC REGION

N°1 Europeanbrand in India

Renault is the leading European brand in India,just two years after its arrival there.

� The Curitiba plant in Brazil restarts fol-lowing work to increase annual produc-tion capacity from 280,000 to 380,000cars and from 400,000 to 500,000 engines.

� In Chile, the project to increase thecapacity of the Cormecánica plant (CMC)from 350,000 to 500,000 gearboxes a yeargets under way.

� Just a few weeks after its debut, NewLogan wins three prizes in Brazil.

� Novo Clio is voted “The Most Econo-mical Car In Brazil.” The magazineInmetro ranks it No. 1 among cars sold inBrazil (all categories) for its low fuelconsumption and very low pollutantemission levels.

� Renault reaches No.2 in the Argentinemarket. With production of over 117,000vehicles during the year, Renault is the lea-ding local car maker in Argentina.

� Master, launched in March 2013 in theAmericas Region, is voted “Light Commer-cial Vehicle of the Year” in Brazil and thenin Argentina.

� First sales of electric vehicles to ItaipuBinacional in Brazil and Paraguay (Twizy,ZOE), to the Brazilian electricity producerand distributor CPFL (Fluence Z.E., KangooZ.E., ZOE) and to FedEx do Brasil (KangooZ.E.).

C

RCI Banque

100%

RenaultSamsungMotors

80%*

Nissan Motor

Renault s.a.s.

43.4%

100% Dacia

99.4%

Daimler AG

1.55%

AVTOVAZ

35.91% Other industrialand commercial

companies

Renault SA

* Company indirectly owned by Renault S.A.S.

Associated companies

Sales financing

Not included in the scope of consolidation

Automotive division

STRUCTURE OF THE RENAULTGROUPSimplified organization chart at December 31, 2013(as a % of shares issued)

14 / 15 �

OWNERSHIP STRUCTUREAt December 31, 2013

(1) The employee-owned shares (present and former employees)counted in this category are those heldin company savings schemes.

SHARE CAPITAL€1,126,701,902.04

TOTAL NUMBER OF SHARES295,722,284

French state 15.01%

NissanFinance. Co, Ltd 15.00%

Daimler AG 3.10%Employees(1) 2.61%

Treasury stock 1.28%

Public 63%

RENAULT GROUP

STRATEGIC PLAN

� Renault exceeded its 2011-2013 objective and delivered €2.5 billion in cumulative freecash flow.

� The group has set new ambitious yet realistic targets to be reached by the end of theplan “Drive the Change” to be measured in 2017:

� To generate 50 billion(1) euros in consolidated turnover� To reach an operating margin greater than 5% of turnover with a positive free cash

flow each year

“Our strategy laid out in the first part of our plan Drive the Change has deliveredresults. Thanks to these achievements, the Renault group is well prepared to deploy asecond ambitious, yet realistic phase of the plan.”

Carlos Ghosn, Chairman and CEO of Renault.

2014 - 2016 action plans:

� Sustained renewal and expansion of the product line-up� International expansion and renewed growth in Europe� Improved competitiveness� Alliance synergies� Cost containment

(1) Based on bank consensus FX rates at the beginning of 2014.

Renault achieves its free cash flow objectiveand is ready to accelerate its growth plan.

C

16 / 17 �RENAULT GROUP

ORGANIZATION CHARTRenault Group top management organizationby the 1st of April 2014

PhilippeKLEIN

EVPProduct Planning

and Programs

ChristianMARDRUS

EVPAlliance CEO Office

& Renault-Nissan BV

LaurensVAN DEN ACKER

SVPIndustrial Design

ChristianVANDENHENDE

Alliance EVPPurchasing

Jean-MichelBILLIG

EVPEngineering,

Quality& IS/IT

ClotildeDELBOS

SVPPerformanceand Control

BrunoANCELIN

SVP Chairman ofEurasia Region

Managing Directorfor Russia

Jean-ChristopheKUGLER

SVP Chairman ofEuromed-Africa

Region

JacquesPROST

Managing Directorfor Morocco

JérômeSTOLL

Chief PerformanceOfficer

Sales & MarketingDirector

Marie-FrançoiseDAMESIN

Alliance EVPHuman Resources

Renault EVPHuman Resources

DominiqueTHORMANNChief Finance

OfficerChairman and CEO

of RCI Banque

MounaSEPEHRI

EVP Office

of the CEO

Members of GroupExecutive Committee

Members of RenaultManagement Committee

Carlos GHOSNChairmanand CEO

ThierryBOLLORÉ

ChiefCompetitive

Officer

José-VicenteDE LOS MOZOS

EVPManufacturing

& SupplyChain

GillesNORMAND

SVP Chairman ofAsia-Pacific Region

StefanMUELLER

EVP Chairman ofEurope Region

and RRG

BernardCAMBIER

SVPSales & Marketing

France

JérômeOLIVE

SVPManufacturing andLogistics Europe

MichaelVAN DER SANDE

SVPGlobal Marketing

NicolasWERTANS

SVPGlobal Sales

JacquesDANIEL

Chairman and CEOof Dongfeng RenaultAutomotive Company

(DRAC)

DenisBARBIER

SVP Chairman ofAmericas Region

NadineLECLAIR

SVPEngineering Project

Jean-PierreVALLAUDE

Deputy DirectorEngineering, Quality

& IS/IT incharge of operations

ChristianDELEPLACE

ExpertFellow

ThomasLANESVP

Product Planning

C

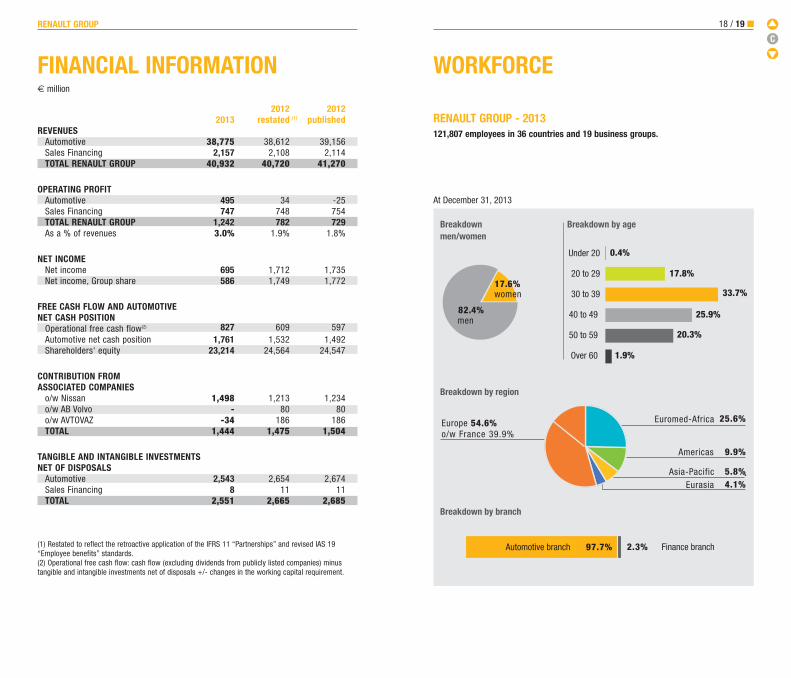

RENAULT GROUP - 2013121,807 employees in 36 countries and 19 business groups.

At December 31, 2013

18 / 19 �RENAULT GROUP

WORKFORCE

Under 20

20 to 29

30 to 39

40 to 49

50 to 59

Over 60

0.4%

17.8%

Automotive branch 97.7% 2.3% Finance branch

33.7%

25.9%

20.3%

1.9%

Breakdown Breakdown by agemen/women

Breakdown by region

Breakdown by branch

Europe

women

men

54.6%o/w France 39.9%

Eurasia 4.1%5.8%

9.9%

25.6%Euromed-Africa

Americas

Asia-Pacific

17.6%

82.4%

FINANCIAL INFORMATION€ million

2012 20122013 restated published

REVENUESAutomotive 38,775 38,612 39,156Sales Financing 2,157 2,108 2,114TOTAL RENAULT GROUP 40,932 40,720 41,270

OPERATING PROFITAutomotive 495 34 -25Sales Financing 747 748 754TOTAL RENAULT GROUP 1,242 782 729As a % of revenues 3.0% 1.9% 1.8%

NET INCOMENet income 695 1,712 1,735Net income, Group share 586 1,749 1,772

FREE CASH FLOW AND AUTOMOTIVE NET CASH POSITION

Operational free cash flow(2) 827 609 597Automotive net cash position 1,761 1,532 1,492Shareholders' equity 23,214 24,564 24,547

CONTRIBUTION FROMASSOCIATED COMPANIES

o/w Nissan 1,498 1,213 1,234o/w AB Volvo - 80 80o/w AVTOVAZ -34 186 186TOTAL 1,444 1,475 1,504

TANGIBLE AND INTANGIBLE INVESTMENTS NET OF DISPOSALS

Automotive 2,543 2,654 2,674Sales Financing 8 11 11TOTAL 2,551 2,665 2,685

(1) Restated to reflect the retroactive application of the IFRS 11 “Partnerships” and revised IAS 19“Employee benefits” standards.(2) Operational free cash flow: cash flow (excluding dividends from publicly listed companies) minustangible and intangible investments net of disposals +/- changes in the working capital requirement.

(1)

C

20 / 21 �RENAULT GROUP

CORPORATE SOCIALRESPONSIBILITY (CSR)As an economic player and a responsible vehicle manufacturer, Renault develops astrategy of social, society and environmental responsibility that reflects its coreactivities, its values, and the expectations of its stakeholders.

SUSTAINABLE MOBILITYCars must be part of a sustainable ecosystem that reflects the aspirations of custo-mers and citizens, ensures their safety, and respects the environment.

ENVIRONMENT - Examples:� Renault is a pioneer and European leader in the sale of all-

electric vehicles.� 10% reduction over three years in the Group's global car-

bon footprint per vehicle sold.

ROAD SAFETY - Examples:� 38 million people reached every year through the Global

Road Safety Partnership, primarily in emerging countries inSouth America, Asia and Africa, and in Central Europe.

� 15 vehicles in the Renault range with a five star score inEuroNCAP crash tests.

HUMAN CAPITAL Respecting and developing human capital - and its diversity - is an effective leverto boost collective performance and individual development, both inside the com-pany and across society as a whole.

DIVERSITY AND EQUAL OPPORTUNITIES - Examples:� Almost 4,000 members, men and women, belong to the social

network Women@Renault in twelve countries.� Renault España S.A. purchases more than 2 million worth of

goods and services from companies specializing in the employ-ment of the disabled.

EDUCATION AND TRAINING - Examples:� More than 3 million hours of training provided for employees

in the Group's ten main countries (automotive activities) in2013.

� 57 societal initiatives in the field of education were conduc-ted by the Group in 2013 (alone or with partner associations) in17 countries.

FUNDAMENTALSRenault has set seven goals, in line with the most demanding international CSRstandards, in the areas of governance, human rights, working relations and condi-tions, the environment, fair practices, consumer-related issues, communities andlocal development.

POINTS OF REFERENCE,115 YEARS OF HISTORY1898 � Louis Renault builds the Type Avoiturette.

1899 � Founding of the Renault Frèrespartnership (société en nom collectif).

1904 � Development of removable sparkplugs.

1912 � Invention of the removable wheel.

1914 � One thousand Renault taxis, the“Taxis de la Marne” are requisitioned totake men to the front.

1924 � Renault adopts a diamond-shapedlogo.

1929 � A new plant opens its doorson Ile Séguin, opposite the Billancourtworkshops.

1945 � S.A. des Usines Renault isnationalized to form the fully state-ownedRégie Nationale des Usines Renault(RNUR).

1946 � At the Paris Motor Show, Renaultpresents the new 4CV, the first productioncar to be build in more than one millionexamples.

1956 � Launch of the Dauphine, “asymbol of modern times”. More than 150patents are filed in this year alone.

1959 � Launch of the Estafette, a newlight commercial vehicle and Renault'sfirst front-wheel drive.

1961 � Launch of the Renault 4, aninnovative vehicle built in more than 8million examples.

1965 � Presentation of the Renault 16,the first executive hatchback, at theGeneva Motor Show.

1972 �Launch of the Renault 5,subsequently built in 5,325,000 examples.

1979 � The turbocharged engine,introduced in 1977, gains benchmarkstatus following Renault's first F1 win.

1980 � Launch of a new range of lightcommercial vehicles, with the first-generation Trafic and Master.

1984 � Launch of three models: RenaultSupercinq, Renault 25 and RenaultEspace, the first MPV in automotivehistory. Renault vehicles become “Lesvoitures à vivre” (cars for living).

1992 � Launch of Renault Safrane andpresentation of Renault Twingo.

1995 � Renault S.A is floated.Presentation of Renault Mégane. RenaultScénic is unveiled one year later.

1998 � Opening of the Curitiba plant inBrazil and the Renault Technocentre inGuyancourt.

1999 � The Renault-Nissan Alliance issigned. Renault acquires a majoritystakeholding in Dacia.

2000 � Renault acquires a 70.1% stake inSamsung Motors, leading to the foundingof Renault Samsung Motors.

2004 � Logan Reveal.

2007 � Renault eco2 signature created forthe most “eco-logical” and “eco-nomical”vehicles in the range.

2008 � Renault acquires a 25% stake inmanufacturer AVTOVAZ, No. 1 on theRussian market with the Lada brand.

2009 � New brand signature: Drive thechange.2010 � At the Paris Motor Show, Renaultpresents a full line-up of affordableelectric vehicles producing zero emissionsin use, alongside the Dezir concept car.Opening of the Chennai plant in India.

2012 � At the Paris Motor Show, Renaultpresents Clio IV, the first car to adopt thenew brand design. Opening of the Tangiersplant in Morocco. Founding of a joint-venture with AVTOVAZ to speed up Allianceexpansion in Russia.

2013 � Launch of Captur, the compacturban crossover. At the Frankfurt MotorShow, Renault presents the Initiale Parisconcept car, heralding the brand's returnto the premium segment. Renault gainsindustrial presence in China, through thefounding of a joint-venture with Dongfeng.

C

MANUFACTURINGAND SALESBuilding on its French roots, the Renault group is pursuing an offensive internationalstrategy. In 2013 it again made more than half of its sales outside the Europe region, settingnew records in sales and market share in the Americas and Eurasia. Brazil and Russiaremain the Group's second- and third-biggest markets, behind France.

RENAULT ATLAS APRIL 2014 22 / 23 �

C

Brazil

Argentina

Curitiba

Cordoba

Los Andes

Envigado

Chile

Colombia

236,360sales

141,217sales

TurkeyTurkeyTurkey

RomaniaRomaniaRomania

AlgeriaAlgeriaAlgeria

South Africa

Iran

Russia

India

Moscow Togliatti

Tehran

Pune

Chennaï

MoroccoMoroccoMorocco

Tangier

Pitesti

Bursa

Casablanca

Rosslyn

Busan

Vehicle plantsPassenger cars

Light commercial vehicles

Powertrain plantsChassis, engines,gearboxe

Chassis

Foundry

Partner plantsPassengers cars

Light commercial vehicles

Logistics sites

Alliance sites

Logistics platform

Renault-NissanAlliance plant

144,706sales

111,378sales

210,099sales

South Korea

Portugal

BarcelonaValladolid

Spain

Palencia

Seville

Cacia

98,024sales

CORDOBA

SITES IN THE AMERICAS

CURITIBA

ENVIGADO (Sofasa)

LOS ANDES (Cormecanica)

TANGIER (Renault-Nissan)

BURSA (Oyak-Renault)

PITESTI (Dacia)

EUROMED - AFRICA SITES

CASABLANCA (Somaca)

BUSAN (RSM)

ASIA - PACIFIC SITES

CHENNAI (Renault-Nissan)

PUNE

TEHRAN (Pars Khodro / Iran Khodro)*

ACI-PARS (Téhéran)*

MOSCOW (Avtoframos)

TOGLIATTI (AVTOVAZ)

EURASIA SITES

ROSSLYN (Nissan)

FLINS

CAUDAN (Fonderie de Bretagne)

GRAND-COURONNE

CLÉON

CHOISY-LE-ROI

LE MANS

MAUBEUGE (MCA)

DOUAI

DIEPPE (Renault Alpine)

BATILLY (SOVAB)

VILLEURBANNE

SANDOUVILLE

RUITZ (STA)

ST-ANDRÉ-DE-L’EURE (SFKI)

SITES IN FRANCE

BARCELONA (Nissan)

CACIA

SITES IN EUROPE

NOVO MESTO

PALENCIA

SEVILLE

VALLADOLID

EUROPE

EUROMED-AFRICA

EURASIA

ASIA-PACIFIC

AMERICAS

Sales atDecember 31, 2013

SloveniaNovo Mesto

Germany162,509

sales

Belgium-Luxembourg

77,353 sales

Italy101,387

sales

Caudan

DouaiDieppe MaubeugeRuitz

Sandouville Cléon

Le Mans

France547,693

sales

St-Andréde-l’Eure

FlinsChoisy-le-Roi

Grand-CouronneBatilly

Villeurbanne

INDUSTRIAL SITESAND SALES IN 2013Renault Group’s main ten markets (excl. AVTOVAZ)

24 / 25 �PRODUCTIONS AND SALES

*Plants on shutdown since end-June 2013.

C

GLOBAL PRODUCTION

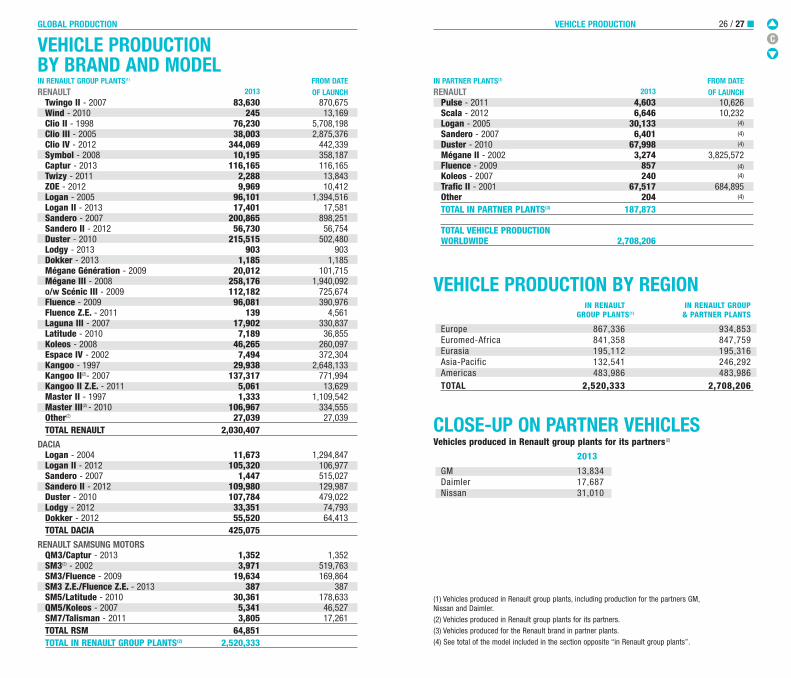

VEHICLE PRODUCTIONBY BRAND AND MODELIN RENAULT GROUP PLANTS(1) FROM DATERENAULT 2013 OF LAUNCH

Twingo II - 2007 83,630 870,675Wind - 2010 245 13,169Clio II - 1998 76,230 5,708,198Clio III - 2005 38,003 2,875,376Clio IV - 2012 344,069 442,339Symbol - 2008 10,195 358,187Captur - 2013 116,165 116,165Twizy - 2011 2,288 13,843ZOE - 2012 9,969 10,412Logan - 2005 96,101 1,394,516Logan II - 2013 17,401 17,581Sandero - 2007 200,865 898,251Sandero II - 2012 56,730 56,754Duster - 2010 215,515 502,480Lodgy - 2013 903 903Dokker - 2013 1,185 1,185Mégane Génération - 2009 20,012 101,715Mégane III - 2008 258,176 1,940,092o/w Scénic III - 2009 112,182 725,674Fluence - 2009 96,081 390,976Fluence Z.E. - 2011 139 4,561Laguna III - 2007 17,902 330,837Latitude - 2010 7,189 36,855Koleos - 2008 46,265 260,097Espace IV - 2002 7,494 372,304Kangoo - 1997 29,938 2,648,133Kangoo II(2)- 2007 137,317 771,994Kangoo II Z.E. - 2011 5,061 13,629Master II - 1997 1,333 1,109,542Master III(2) - 2010 106,967 334,555Other(2) 27,039 27,039TOTAL RENAULT 2,030,407

DACIALogan - 2004 11,673 1,294,847Logan II - 2012 105,320 106,977Sandero - 2007 1,447 515,027Sandero II - 2012 109,980 129,987Duster - 2010 107,784 479,022Lodgy - 2012 33,351 74,793Dokker - 2012 55,520 64,413TOTAL DACIA 425,075

RENAULT SAMSUNG MOTORSQM3/Captur - 2013 1,352 1,352SM3(2) - 2002 3,971 519,763SM3/Fluence - 2009 19,634 169,864SM3 Z.E./Fluence Z.E. - 2013 387 387SM5/Latitude - 2010 30,361 178,633QM5/Koleos - 2007 5,341 46,527SM7/Talisman - 2011 3,805 17,261TOTAL RSM 64,851TOTAL IN RENAULT GROUP PLANTS(2) 2,520,333

IN PARTNER PLANTS(3) FROM DATERENAULT 2013 OF LAUNCH

Pulse - 2011 4,603 10,626Scala - 2012 6,646 10,232Logan - 2005 30,133 (4)

Sandero - 2007 6,401 (4)

Duster - 2010 67,998 (4)

Mégane II - 2002 3,274 3,825,572Fluence - 2009 857 (4)

Koleos - 2007 240 (4)

Trafic II - 2001 67,517 684,895Other 204 (4)

TOTAL IN PARTNER PLANTS(3) 187,873

TOTAL VEHICLE PRODUCTION WORLDWIDE 2,708,206

VEHICLE PRODUCTION BY REGION IN RENAULT IN RENAULT GROUP

GROUP PLANTS(1) & PARTNER PLANTS

Europe 867,336 934,853Euromed-Africa 841,358 847,759Eurasia 195,112 195,316Asia-Pacific 132,541 246,292Americas 483,986 483,986TOTAL 2,520,333 2,708,206

CLOSE-UP ON PARTNER VEHICLESVehicles produced in Renault group plants for its partners (2)

2013

GM 13,834Daimler 17,687Nissan 31,010

(1) Vehicles produced in Renault group plants, including production for the partners GM,Nissan and Daimler.(2) Vehicles produced in Renault group plants for its partners.(3) Vehicles produced for the Renault brand in partner plants.(4) See total of the model included in the section opposite “in Renault group plants”.

VEHICLE PRODUCTION 26 / 27 �

C

GLOBAL PRODUCTION

(1) Employees (open-ended + fixed-term contract) published, including inactive (GPEC)(2) S.R.: standard replacement (a powertrain part rebuilt to the strict standards of the automaker).(3) Figure corresponding to 100% of the workforce (NB: 50% of the workforce at the Dieppe siteis consolidated in the Renault group registration document).

AUTOMOTIVE PLANTS IN EUROPE - 2013 - FRANCEActivities, production and workforce at December 31, 2013

Plants Activities Production Workforce(1)

Batilly (Sovab) Master III 92,811 2,377

CaudanFonderie de Bretagne Casting (in tonnes) 25,400 463

Choisy SR Gear boxes(2) 20,098 311European center SR kits 15,390,200for reconditioned SR cylinder heads(2) 3,718powertrain sub-systems SR engines(2) 28,262

Injectors 121,844SR injection pumps(2) 16,840

Cléon Gearboxes 581,528 3,366Engines 520,457Aluminium Casting (in tonnes) 11,900

Dieppe Clio IV Renault Sport 5,217 308(3) )

Douai Mégane III coupé-cabriolet 3,245 4,281Scénic III 112,182

Douvrin Engines 264,971 -(FM – Renault division)

Flins Clio III 21,886 2,505Clio III Van 10,978Clio IV 87,051ZOE 9,969

Le Mans (ACI) Subframes 705,000 1,818Bottom arms 2,561,000Rear axles 853,000Front axles 684,000Casting rotors 7,700,000

Maubeuge (MCA) Kangoo II 114,427 2,019Kangoo II Z.E. 5,061Citan 17,687

Ruitz (STA) Renault automatic gearboxes 83,066 577Automatic transmission 193,698part kits for PSATransmission parts for manual 6,186,665gearboxes

Plants Activities Production Workforce(1)

Sandouville Espace IV 7,492 2,198Laguna III Hatchback 8,464Laguna III Estate 7,522Laguna III Coupé 1,916

Villeurbanne (ACI) Bottom arms 619,746 285Front axles 247,130

AUTOMOTIVE PLANTS IN EUROPE - 2013 - OUTSIDE FRANCEActivities, production and workforce at December 31, 2013

Plants Activities Production Workforce

EspagneBarcelone (Nissan) Trafic II Renault 67,517 nc

Palencia Mégane III 65,886 1,739Mégane III Coupé 12,814Mégane III Estate 60,702Mégane III Van 3,347

Seville Gearboxes 789,298 1,006Valladolid Clio III 5,139 2,434

Twizy 2,288Captur 117,517

Valladolid Engines 1,247,579 1,799

PortugalCacia Gearboxes 649,169 955

Gearboxes components 2,245,589Engines components 3,070,759

SlovénieNovo mesto Clio II 9,858 2,026

Twingo II 83,630Wind 245

AUTOMOTIVE PLANTS IN EUROPE - 2013 - FRANCE (Cont’d)Activities, production and workforce at December 31, 2013

PRODUCTION BY PLANTAND BY REGION

Body assembly Powertrain Casting Partner Plants: Body assembly

Plant Plant

Plant

PRODUCTION BY PLANT AND BY REGION 28 / 29 �

C

GLOBAL PRODUCTION

AUTOMOTIVE PLANTS IN EUROMED-AFRICA - 2013Activities, production and workforce at December 31, 2013

AUTOMOTIVE PLANTS IN ASIA-PACIFIC - 2013Activities, production and workforce at December 31, 2013

Plants Activities Production Workforce

Marocco Casablanca (Somaca) Kangoo 5,145 1,442

Logan 8,426Logan II 5,845Sandero 4,371Sandero II 42,758

Tanger Lodgy 34,254 5,218Sandero II 10,095Dokker 36,548Dokker Van 20,157

Romania Pitesti (Dacia) Logan 6,966 10,955

Logan II 84,845Logan MCV 17,761Sandero II 113,827Duster 119,814Gearboxes 517,375Engines 308,077Return modules 123,079Subframes 665,036Front axles 388,815Axles 932,390Aluminium Casting (in tonnes) 16,701

Turquie Bursa (Oyak-Renault) Clio IV 181,434 5,145

Clio IV Estate 54,836Clio IV Van 15,531Symbol 7,093Fluence 52,092Fluence Z.E. 139Mégane Génération 19,421Gearboxes 276,656Engines 274,327Rear axles 363,556Front axles 339,546Subframes 357,674

Afrique du SudRosslyn (Nissan) Sandero 6,401 nc

AUTOMOTIVE PLANTS IN EURASIA - 2013Activities, production and workforce at December 31, 2013

Plants Activities Production Workforce

Russie Moscou (Avtoframos) Logan 51,901 4,126

Sandero 46,974Fluence 6,799Mégane Génération 591Duster 88,847

Togliatti (AVTOVAZ) Other 204 nc

Plants Activities Production WorkforceSouth KoreaBusan SM3 3,971 2,235(Renault Samsung Motors) SM3/Fluence 35,222

SM3/Fluence Z.E. 387SM5/Latitude 37,550QM5/Koleos 51,606SM7/Talisman 3,805Engines 115,542

IndiaChennai Pulse 4,603 nc

Scala 6,646Duster 67,998Fluence 857Koleos 240

IranIran Khodro Logan 10,521 nc

Logan pick-up 88 ncPars Khodro Logan 19,524 nc

Mégane II 3,274ACI Pars Subframes 26,272 nc

Bottom arms 31,047Rear axles 30,059Front axles 29,885

AUTOMOTIVE PLANTS IN AMERICAS - 2013Activities, production and workforce at December 31, 2013Plants Activities Production WorkforceArgentinaCordoba Clio II 62,381 1,905

Kangoo 5,203Kangoo Express 24,793Symbol 3,102Fluence 21,602

Planta Fundición Aluminio Aluminium casting (in tonnes) 4,476 178

BrazilCuritiba Master II 1,333 5,000

Master III 14,156VU Nissan 27,039Logan 27,006Logan II 14,270Sandero 131,313Sandero II 30Duster 77,094Engines 359,740 407

Chile Los Andes (Cormecanica) Boîtes de vitesses 352,079 531

ColombiaEnvigado (Sofasa) Clio II 3,991 1,554

Logan 13,475Sandero 19,654Duster 37,544

Body assembly Powertrain Casting Partner Plants: Body assembly Powertrain

PlantPlant

Plant

Plant

PRODUCTION BY PLANT AND BY REGION 30 / 31 �

C

GLOBAL SALESPRODUCTION AND SALES

GLOBAL SALESRENAULT GROUP’S MAIN FIFHTEEN MARKETS - 2013By volume and as a % of TIV, cars + LCVs, incl. Dacia and Renault Samsung Motors

Sales volume Market shareFrance 547,693 25.4%Brazil 236,360 6.6%Russia 210,099 7.6%Germany 162,509 5.1%Turkey 144,706 17.0%Argentina 141,217 15.4%Algeria 111,378 26.2%Italia 101,387 7.2%Spain 98,024 12.1%Belgium + Luxembourg 77,353 13.0%UK 77,163 3.0%India 64,368 2.1%South Korea 60,027 4.0%Marocco 47,030 38.9%Netherlands 46,040 9.8%

RENAULT GROUP WORLDWIDE SALES (1) BY BRAND AND MODELCARS 2012 2013RENAULT

Twingo 98,675 80,418Wind 1,663 394ZOE 68 8,803Modus 30,311 5,082Clio 338,103 434,094Captur - 93,634Thalia 61,749 16,238Pulse 6,217 4,791Dokker - 66Logan 219,859 187,481Sandero 205,678 204,289Kangoo 53,418 41,930Kangoo Z.E. 17 2Fluence 102,812 99,128Fluence Z.E. 2,154 917Mégane (incl. Scénic) 395,639 295,667Lodgy - 529Duster 158,035 250,273Scala 8,103 8,775Laguna 29,962 18,116Koleos 50,918 46,400Latitude 8,348 7,741Safrane II 832 206Espace 12 603 8,323Talisman 397 164Trafic 12,904 10,173Master 1,985 2,287Other 549 371TOTAL RENAULT 1,800,999 1,826,292

DACIALogan 89,999 68,725Sandero 94,063 150,567Lodgy 29,356 42,942Duster 129,129 113,565Dokker 2,369 23,722Other 188 62TOTAL DACIA 345,104 399,583

RENAULT SAMSUNG MOTORSSM3 22,793 25,990SM5 32,699 30,888SM7 5,263 3,680QM3 - 1,150QM5 4,936 5,466TOTAL RSM 65,691 67,174

TOTAL GROUP, CARS 2,211,794 2,293,049

LCVs 2012 2013RENAULT

Twingo 4,827 4,219ZOE - 54Modus 102 32Clio 28,261 27,953Captur - 230Mégane 8,206 6,849Duster 8,464 10,994Laguna 112 211Koleos 1,479 996Espace 92 46Dokker - 711Logan 1,692 704Kangoo 109,638 98,919Kangoo Z.E. 5,627 5,872Trafic 54,251 51,544Master 95,443 92,762Other 3,699 3,106TOTAL RENAULT 321,893 305,202

DACIASandero 177 105Lodgy 3 35Duster 1,988 1,840Logan 12,222 630Dokker 541 27,341Other 4 6TOTAL DACIA 14,935 29,957

TOTAL GROUP, LCVs 336,828 335,159

TOTAL GROUP, CARS + LCVs 2,548,622 2,628,208

RENAULT GROUP WORLDWIDE SALES BY BRANDBy volume, cars + LCVs

2012 2013RENAULT

Cars 1,800,999 1,826,292Light commercial vehicles 321,893 305,202TOTAL RENAULT 2,122,892 2,131,494

DACIACars 345,104 399,583Light commercial vehicles 14,935 29,957TOTAL DACIA 360,039 429,540

RENAULT SAMSUNG MOTORSCars 65,691 67,174

TOTAL GROUP 2,548,622 2,628,208

(1) Volume, cars + LCVs

32 / 33 �

C

34 / 35 �GLOBAL SALES

INTERNATIONALIZATION OF THE GROUP50.5% of sales outside the Europe region(1) in 2013 Group sales outside Europe (in %)

33.8%

30.4%26.9%

22.5%

34.6%36.7% 37.4%

20052004 2006 2007 2008 2009 20112010 2012 2013

43.1%

50.1% 50.5%

WORLDWIDE AUTOMOTIVE MARKET BY REGIONBy volume and as a % of TIV, cars + LCVs

Volume As a % of totalcar + LCV volume

TOTAL EUROPE (1) 13,750,151 16.7%France 2,157,787 2.6%G9 11,592,364 14.1%TOTAL INTERNATIONAL 68,640,223 83.3%Euromed-Africa 2,554,958 3.1%Eurasia 3,281,083 4.0%Asia-Pacific 38,476,550 46.7%Americas 6,993,036 8.5%North America 17,334,596 21.0%

TOTAL WORLD 82,390,374 100.0%

RENAULT GROUP WORLDWIDE SALES BY REGIONCars + LCVs, including Dacia and Renault Samsung Motors

2012 2013

TOTAL EUROPE (1) 1,271,393 1,301,864France 551,314 547,693G9 720,079 754,171TOTAL INTERNATIONAL 1,277,229 1,326,344Euromed-Africa 360,923 388,922Eurasia 207,808 232,001Asia-Pacific 257,564 238,445Americas 450,934 466,976TOTAL GROUP 2,548,622 2,628,208

(1) The EUROPE Region groups European Union countries, with the exception of Bulgaria and Romania,which are part of the EUROMED-AFRICA Region, along with Iceland, Norway and Switzerland.

TOTAL INDUSTRY VOLUMES, EUROPE REGIONBy volume (1) cars + LCVs

2012 2013

Germany 3,307,461 3,170,479Austria 367,653 349,928Other Balkans countries 42,602 36,200Belgium + Luxembourg 598,519 592,663Greek Cyprus 12,260 7,996Croatia 34,989 33,083Denmark 195,226 206,125Spain + Canaries 776,676 808,502Finland 123,445 114,412France 2,282,810 2,157,787Greece 62,259 62,230Hungary 64,117 67,701Ireland 90,387 85,381Iceland 8,393 7,897Italia 1,518,414 1,402,737Malta 6,450 6,307Norway 171,383 174,444Baltic countries 49,084 49,737Netherlands 559,191 467,803Poland 311,757 331,614Portugal 111,350 124,142Czech Republic 185,988 176,506UK 2,292,545 2,543,694Slovakia 74,403 69,953Slovenia 55,174 57,708Sweden 319,869 307,210Switzerland 359,485 337,912TIV EUROPE REGION 13,981,890 13,750,151

SHARE OF MAIN EUROPEAN COUNTRIESAs a % of TIV, cars + LCVs

SALES, EUROPE REGION

Other 19.0%

France 15.7%Spain+Canaries 5.9%Germany 23.1%

Italia 10.2%

UK 18.5%

Begium+Luxembourg 4.3%Netherlands 3.4%

(1) Excl. Sales to government departments.

C

36 / 37 �SALES IN THE EUROPE REGION

RENAULT REGISTRATIONS (1)

2012 2013France 466,792 453,890Germany 123,672 115,347Italia 69,375 73,289Spain + Canaries 65,522 65,736UK 56,204 60,017Belgium + Luxembourg 61,256 59,267Netherlands 51,068 42,546Poland 18,182 20,041Austria 20,324 19,627Switzerland 21,650 17,425Portugal 12,947 16,016Denmark 10,531 13,677Sweden 13,102 13,197Slovenia 8,916 9,555Czech Republic 11,748 7,206Ireland 6,536 4,491Hungary 4,334 3,625Baltics countries 2,824 3,220Slovakia 4,638 3,184Croatia 2 915 2,766Other Balkans countries 2,835 2,048Finland 1,834 1,496Norway 1,194 1,351Greece 1,101 1,248Greek Cyprus 352 369Iceland 247 324Malta 141 185TOTAL RENAULT 1,040,240 1,011,143

RENAULT MARKET SHARE AND RANKINGAs a % of TIV, cars + LCVs

Renault market share 2012 2013and ranking Market share Ranking Market share Ranking

France 20.4% 1 21.0% 1Germany 3.7% 8 3.6% 8Italia 4.6% 8 5.2% 5Spain + Canaries 8.4% 4 8.1% 3UK 2.5% 14 2.4% 16Belgium + Luxembourg 10.2% 2 10.0% 2Netherlands 9.1% 2 9.1% 2Poland 5.8% 7 6.0% 5Austria 5.5% 6 5.6% 6Switzerland 6.0% 3 5.2% 7Portugal 11.6% 1 12.9% 1Denmark 5.4% 7 6.6% 6Sweden 4.1% 10 4.3% 8Slovenia 16.2% 1 16.6% 1Czech Republic 6.3% 5 4.1% 6Ireland 7.2% 5 5.3% 8Hungria 6.8% 5 5.4% 7Baltic countries 5.8% 5 6.5% 4Slovakia 6.2% 6 4.6% 8Croatia 8.3% 5 8.4% 4Finland 1.5% 17 1.3% 19Noway 0.7% 22 0.8% 22Greece 1.8% 18 2.0% 17Iceland 2.9% 11 4.1% 11TOTAL RENAULT 7.4% 3 7.4% 3

DACIA REGISTRATIONS (1)

Main Dacia markets 2012 2013France 84,522 93,803Germany 46,617 47,162Spain + Canaries 17,847 32,288Italia 26,860 28,098Belgium + Luxembourg 13,536 17,982UK - 17,146Poland 10,274 12,208Austria 6,581 8,104Czech Republic 4,110 5,874Switzerland 5,608 5,371Netherlands 2,209 3,292Hungaria 2,259 3,256Sweden 1,071 2,498Slovakia 1,570 2,287Portugal 1,140 1,984Other Balkans countries 2,270 1,846Slovenia 1,014 1,372Baltics countries 1,061 1,340Ireland - 1,288Croatia 893 931Finland 734 859Denmark - 702Greece 390 272Norway 8 192TOTAL DACIA 230,592 290,415

DACIA MARKET SHAREAs a % of TIV, cars + LCVs

Main Dacia markets 2012 2013France 3.7 % 4.3 %Germany 1.4 % 1.5 %Spain + Canaries 2.3 % 4.0 %Italia 1.8 % 2.0 %Belgium + Luxembourg 2.3 % 3.0 %UK - 0.7 %Poland 3.3 % 3.7 %Austria 1.8 % 2.3 %Czech Republic 2.2 % 3,3 %Switzerland 1.6 % 1.6 %Netherlands 0.4 % 0.7 %Hungaria 3.5 % 4.8 %Sweden 0.3 % 0,8 %Slovakia 2.1 % 3.3 %Portugal 1.0 % 1.6 %Other Balkans countries 5.3 % 5.1 %Slovenia 1.8 % 2.4 %Baltics countries 2.2 % 2.7 %Ireland - 1.5 %Croatia 2.6 % 2.8 %Finland 0.6 % 0.8 %Denmark - 0.3 %Greece 0.6 % 0.4 %Norway - 0.1 %TOTAL DACIA 1.6 % 2.1 %

(1) Excl. sales to government departments.

By volume cars + LCVs

C

38 / 39 �SALES IN THE EUROPE REGION

RENAULT GROUP SALES BY BRAND AND MODELBy volume, cars + LCVsCARS 2012 2013RENAULT

Twingo 92,685 78,132Wind 1,557 360ZOE 68 8,792Modus 30,307 5,079Clio 243,492 286,214Captur - 86,575Thalia 4,557 824Kangoo 27,223 22,108Kangoo Z.E. 17 2Fluence 9,058 6,098Fluence Z.E. 1,400 350Mégane (incl. Scénic) 329,733 259,187Laguna 29,417 17,838Koleos 15,247 8,346Latitude 2,076 585Espace 12,594 8,322Trafic 12,122 9,595Master 1,490 1,561Other 311 196TOTAL RENAULT 813,354 800,164

DACIALogan 21,771 17,345Sandero 72,336 121,933Lodgy 27,610 34,446Duster 98,404 83,155Dokker 880 15,348Other 97 52TOTAL DACIA 221,098 272,279TOTAL GROUP, CARS 1,034,452 1,072,443

LCVs 2012 2013RENAULT

Twingo 4,577 3,986ZOE - 54Modus 102 32Clio 27,767 27,533Captur - 229Mégane 8,152 6,815Laguna 111 211Koleos 139 82Espace 92 46Kangoo 65,764 58,899Kangoo Z.E. 5,620 5,850Trafic 48,929 45,253Master 62,551 59,224Other 3,619 3,044TOTAL RENAULT 227,423 211,258

DACIASandero 174 103Lodgy 3 35Duster 1,871 1,538Logan 7,239 322Dokker 227 16,159Other 4 6TOTAL DACIA 9,518 18,163TOTAL GROUP, LCVs 236,941 229,421TOTAL GROUP, CARS + LCVs 1,271,393 1,301,864

SALES, EUROMED-AFRICA REGIONTOTAL INDUSTRY VOLUMES, EUROMED-AFRICA REGIONBy volume, cars + LCVs

Main markets 2012 2013Algeria 436,516 424,984Morocco 130,306 120,755Romania 84,412 78,614Tunisia 49,292 47,000Turkey 777,761 853,378TIV EUROMED 1 507,679 1,553,955South Africa & Namibia 515,958 538,934Egypt 189,275 177,052DOM 59,374 57,080TIV AFRICA + DOM 971,860 1,001,003TIV EUROMED-AFRICA REGION 2,479,539 2,554,958

RENAULT SALES AND MARKET SHAREBy volume and as a % of TIV, cars + LCVs

2012 2013Main Renault Market Marketmarkets Volume share Volume share

Algeria 71,947 16.5% 74.088 17.4%Marocco 20,612 15.8% 16.642 13.8%Romania 6,079 7.2% 5.096 6.5%Tunisia 6,158 12.5% 6.732 14.3%Turkey 89,205 11.5% 108.311 12.7%TOTAL RENAULT EUROMED 195,685 13.0% 212.794 13.7%South Africa & Namibia 10,555 2.0% 12.406 2.3%Egypt 11,344 6.0% 8.221 4.6%DOM 10,032 16.9% 9.968 17.5%TOTAL RENAULT AF. + DOM 37,590 3.9% 38.094 3.8%TOTAL RENAULT EUR. AF. 233,275 9.4% 250.888 9.8%

DACIA SALES AND MARKET SHAREBy volume and as a % of TIV, cars + LCVs

2012 2013Main Dacia Market Marketmarkets Volume share Volume shareAlgeria 41,710 9.6% 37,290 8.8%Morocco 27,097 20.8% 30,388 25.2%Romania 22,148 26.2% 24,890 31.7%Tunisia 1,588 3.2% 984 2.1%Turkey 28,964 3.7% 36,395 4.3%TOTAL DACIA EUROMED 124,155 8.2% 133,379 8.6%DOM 3,264 5.5% 3,673 6.4%TOTAL DACIA AF. + DOM 3,493 0.4% 3,868 0.4%TOTAL DACIA EUR. AF. 127,648 5.1% 137,247 5.4%

C

40 / 41 �SALES IN THE EUROMED-AFRICA REGION

RENAULT GROUP SALES BY BRAND AND MODELCARS 2012 2013RENAULT

Twingo 2,401 1,689ZOE - 9Clio 51,963 76,760Captur - 6,667Thalia 44,909 10,493Logan 7,863 47,357Sandero 10,083 9,094Kangoo 15,097 9,780Fluence 31,966 31,294Fluence Z.E. 184 31Mégane (incl. Scénic) 22,283 15,531Lodgy - 115Duster 3,055 3,991Scala - 1,700Laguna 266 132Koleos 820 566Latitude 2,603 1,901Safrane 3 -Espace 9 1Trafic 369 439Master 11 13Other 106 107TOTAL RENAULT 193,991 217,670

DACIALogan 67,697 50,946Sandero 21,573 28,438Lodgy 1,713 8,324Duster 29,981 29,686Dokker 1,489 8,311Other 91 10TOTAL DACIA 122,544 125,715

RENAULT SAMSUNG MOTORSSM3 - 587SM5 - 129SM7 - 10QM5 - 61TOTAL RSM - 787TOTAL GROUP, CARS 316,535 344,172

LCVs 2012 2013RENAULT

Twingo 245 227Clio 494 420Captur - 1Mégane 54 34Laguna 1 -Dokker - 10Logan 399 231Kangoo 17,329 13,032Kangoo Z.E. - 3Trafic 3,567 3,779Master 17,115 15,420Other 80 61TOTAL RENAULT 39,284 33,218

DACIASandero 3 2Duster 117 302Logan 4,670 143Dokker 314 11,085TOTAL DACIA 5,104 11,532TOTAL GROUP, LCVs 44,388 44,750TOTAL GROUP, CARS + LCVs 360,923 388,922

SALES, EURASIA REGIONTOTAL INDUSTRY VOLUMES, EURASIA REGIONBy volume, cars + LCVs

Main markets 2012 2013Russia 2,935,233 2,763,163Ukraine 232,184 216,170TIV EURASIA REGION 3,384,567 3,281,083

RENAULT SALES AND MARKET SHAREBy volume and as a % of TIV, cars + LCVs

2012 2013Main Renault Market Marketmarkets Volume share Volume shareRussia 189,852 6.5% 210,099 7.6%Ukraine 14,004 6.0% 12,417 5.7%TOTAL RENAULT 207,808 6.1% 232,001 7.1%

RENAULT GROUP SALES BY BRAND AND MODELBy volume, cars + LCVsCARS 2012 2013RENAULT

Clio 57 11Thalia 620 84Dokker - 66Logan 66,133 57,387Sandero 51,736 48,889Kangoo 2,310 2,253Fluence 18,784 16,435Mégane (incl. Scénic) 11,713 8,903Lodgy - 230Duster 50,604 90,126Laguna 33 16Koleos 1,818 3,160Latitude 612 526Trafic 343 47TOTAL RENAULT 204,763 228,133

RENAULT SAMSUNG MOTORSSM3 - 58SM5 - 33SM7 - 5QM5 - 26TOTAL RSM - 122TOTAL GROUP, CARS 204,763 228,255

LCVs 2012 2013RENAULT

Dokker - 684Logan 468 13Kangoo 1,426 868Trafic 138 175Master 1,013 2,006TOTAL RENAULT 3,045 3,746TOTAL GROUP, LCVs 3,045 3,746TOTAL GROUP, CARS + LCVs 207,808 232,001

C

SALES IN THE ASIA-PACIFIC REGION 42 / 43 �

SALES, ASIA-PACIFIC REGIONTOTAL INDUSTRY VOLUMES, ASIA-PACIFIC REGIONBy volume, cars + LCVs

Main markets 2012 2013Saudi Arabia 703,519 744,351Australia 1,087,671 1,112,706China 18,432,999 20,812,058South Korea 1,516,300 1,511,479India 3,206,794 2,994,810Iran 1,030,995 711,000Israel 204,891 212,581Japan 5,289,515 5,267,601TIV ASIA-PACIFIC REGION 36,444,350 38,476,550

RENAULT SALES AND MARKET SHAREBy volume and as a % of TIV, cars + LCVs

2012 2013Main Renault Market Marketmarkets Voume share Volume shareSaudi Arabia 7,005 1.0% 8,200 1.1%Australia 5,011 0.5% 7,016 0.6%China 27,857 0.2% 34,157 0.2%India 35,157 1.1% 64,368 2.1%Iran 100,783 9.8% 36,300 5.1%Israel 6,645 3.2% 10,264 4.8%Japan 3,108 0.1% 3,768 0.1%TOTAL RENAULT 195,863 0.5% 176,464 0.5%

DACIA SALES AND MARKET SHAREBy volume and as a % of TIV, cars + LCVs

2012 2013Main Dacia Market Marketmarkets Volume share Volume shareTOM 1,064 7.0% 1,015 7.7%Middle East 711 1.2% 836 1.4%TOTAL DACIA 1,775 0.00% 1,851 0.00%

RENAULT SAMSUNG MOTORS RENAULT SALES AND MARKET SHAREBy volume and as a % of TIV, cars + LCVsBy volume and as a % of TIV, cars

2012 2013Main RSM Market Marketmarkets Volume share Volume shareSouth Korea 59,926 4.6% 60,027 4.6%TOTAL RSM 59,926 0.2% 60,130 0.2%

RENAULT GROUP SALES BY BRAND AND MODELCARS 2012 2013RENAULT

Twingo 313 320Wind 106 34Modus - 1Clio 1,527 3,127Captur - 392Thalia 85 2Pulse 6,217 4,791Logan 89,522 35,486Sandero 390 244Kangoo 1,843 1,794Fluence 11,067 16,269Fluence Z.E. 570 536Mégane (incl. Scénic) 18,990 8,550Lodgy - 184Duster 26,136 58,210Scala 3,172 6,911Laguna 227 108Koleos 27,925 30,000Latitude 2,573 4,563Safrane II 572 0Talisman 397 163Trafic 70 92Master 2 5Other 121 46TOTAL RENAULT 191,825 171,828

DACIALogan 531 434Sandero 154 196Lodgy 33 172Duster 744 724Dokker - 63TOTAL DACIA 1,462 1,589

RENAULT SAMSUNG MOTORSSM3 17,331 19,287SM5 32,621 30,726SM7 5,038 3,588QM3 - 1,150QM5 4,936 5,379TOTAL RSM 59,926 60,130TOTAL GROUP, CARS 253,213 233,540

LCVs 2012 2013RENAULT

Twingo 5 6Koleos 6 8Dokker - 17Logan 825 460Kangoo 1,753 1,277Kangoo Z.E. 7 13Trafic 814 1,678Master 628 1,176Other - 1TOTAL RENAULT 4,038 4,636

DACIALogan 313 165Dokker - 97TOTAL DACIA 313 262TOTAL GROUP, LCVs 4,351 4,898TOTAL GROUP, CARS + LCVs 257,564 238,445

C

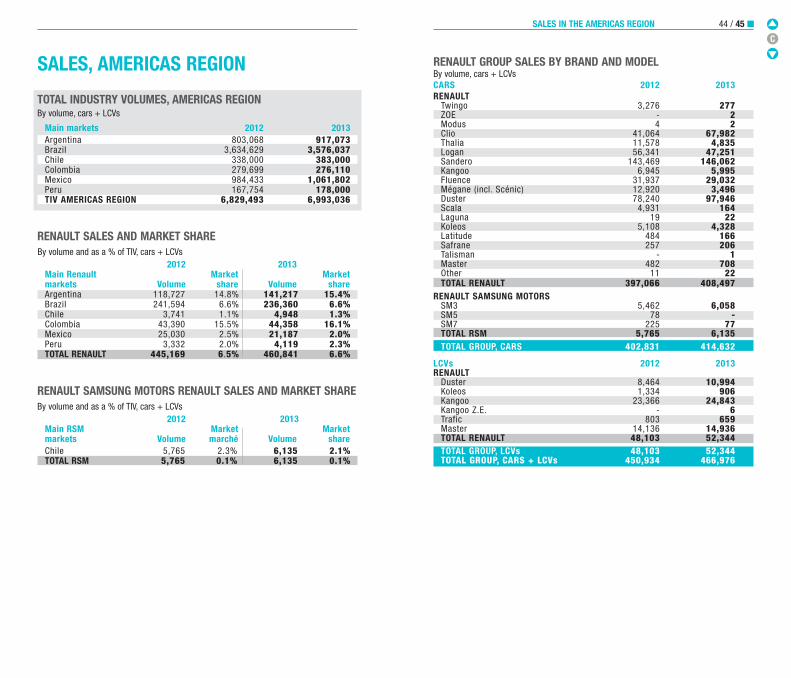

SALES IN THE AMERICAS REGION 44 / 45 �

RENAULT GROUP SALES BY BRAND AND MODELBy volume, cars + LCVsCARS 2012 2013RENAULT

Twingo 3,276 277ZOE - 2Modus 4 2Clio 41,064 67,982Thalia 11,578 4,835Logan 56,341 47,251Sandero 143,469 146,062Kangoo 6,945 5,995Fluence 31,937 29,032Mégane (incl. Scénic) 12,920 3,496Duster 78,240 97,946Scala 4,931 164Laguna 19 22Koleos 5,108 4,328Latitude 484 166Safrane 257 206Talisman - 1Master 482 708Other 11 22TOTAL RENAULT 397,066 408,497

RENAULT SAMSUNG MOTORSSM3 5,462 6,058SM5 78 -SM7 225 77TOTAL RSM 5,765 6,135TOTAL GROUP, CARS 402,831 414,632

LCVs 2012 2013RENAULT

Duster 8,464 10,994Koleos 1,334 906Kangoo 23,366 24,843Kangoo Z.E. - 6Trafic 803 659Master 14,136 14,936TOTAL RENAULT 48,103 52,344TOTAL GROUP, LCVs 48,103 52,344TOTAL GROUP, CARS + LCVs 450,934 466,976

SALES, AMERICAS REGION

TOTAL INDUSTRY VOLUMES, AMERICAS REGIONBy volume, cars + LCVs

Main markets 2012 2013Argentina 803,068 917,073Brazil 3,634,629 3,576,037Chile 338,000 383,000Colombia 279,699 276,110Mexico 984,433 1,061,802Peru 167,754 178,000TIV AMERICAS REGION 6,829,493 6,993,036

RENAULT SALES AND MARKET SHAREBy volume and as a % of TIV, cars + LCVs

2012 2013Main Renault Market Marketmarkets Volume share Volume shareArgentina 118,727 14.8% 141,217 15.4%Brazil 241,594 6.6% 236,360 6.6%Chile 3,741 1.1% 4,948 1.3%Colombia 43,390 15.5% 44,358 16.1%Mexico 25,030 2.5% 21,187 2.0%Peru 3,332 2.0% 4,119 2.3%TOTAL RENAULT 445,169 6.5% 460,841 6.6%

RENAULT SAMSUNG MOTORS RENAULT SALES AND MARKET SHAREBy volume and as a % of TIV, cars + LCVs

2012 2013Main RSM Market Marketmarkets Volume marché Volume shareChile 5,765 2.3% 6,135 2.1%TOTAL RSM 5,765 0.1% 6,135 0.1%

C

PRODUCTSAND BUSINESS The visionary strategy of the Renault group is based on bold choices that promotesustainable mobility for everybody. The ability to innovate off the beaten track is written intothe company's genes. The Group's men and women share the same passion: to drive carsforward.

RENAULT ATLAS APRIL 2014 46 / 47 �

C

RENAULTPASSENGER CARSEUROPE

PASSENGER CARSEUROPE

SPORT CARS

Kangoo

Trafic Passenger

Twingo

KoleosPresent in Europeand on international markets

Mégane Coupé Cabriolet

Laguna CoupéAlso exists in Hatchbackand Estate versions

Mégane BerlineAlso exists inCoupé and Estate versions

ClioAlso existsin an Estate version

ScénicAlso existsin Grand Scénic andX-mod versions

48 / 49 �VEHICLE RANGES

Latitude

Mégane R.S. 265

EspaceAlso exists in a Grand Espace version

Clio R.S. 200 EDC

Mégane Estate G.T. 220Also available: “GT-Line” sport pack forMégane Berline, Coupé and Estate

Captur

C

RENAULTPASSENGER CARSINTERNATIONAL - Main vehicles sold

LIGHT COMMERCIAL VEHICLES

Logan

TalismanVehicle intended solelyfor China

Trafic

Fluence Z.E.

ZOE

Kangoo ExpressAlso exists in Compactand Maxi versions

MasterAlso exists in a rearwheel-drive version

Twizy

Koleos

Sandero Stepway

ELECTRIC VEHICLES

Kangoo Z.E.

50 / 51 �VEHICLE RANGES

PulseVehicle intendedsolely for India

Latitude

Duster

Fluence

ScalaVehicle intended solelyfor India

C

Sandero Stepway

52 / 53 �VEHICLE RANGES

Logan MCV

Dokker

Dokker Van

Sandero

Logan

QM3

SM3 Z.E.

SM3

SM5

SM7

QM5

Lodgy

DACIA RSM

Duster

C

54 / 55 �PRODUCTS AND BUSINESS

MOTORS POWERTRAINS

ELECTRIC GASOLINE DIESEL

TWIZY 3CG (5hp) + BT33CG (17hp) + BT3 - -

TWINGO - D4F (75hp) + JB1/JH1D4Ft (100hp) + JHQ K9K (75hp) + JRQK4M RS (133hp) + JRQ K9K (90hp) + JRQ

WIND - D4Ft (100hp) + JHQ -

ZOE 5AGen2 (88hp) -+ BT4

CLIO II - D4D Flex (76hp) + JB1D4F (75hp) + JB1 -

CLIO III - D4F (75hp) + JHQ K9K (90hp) + JRQ

CLIO IV - D4F (75hp) + JHQ K9K (75hp) + JRQH4Bt (90hp) + JHQ K9K (90hp) + JRQ/DC4H5Ft (120hp) + DC4M5Mt RS (200hp) + DC4

PULSE - - K9K (65hp) + JHQ

SCALA - - K9K(86hp) + JRQ

SYMBOL - K4M Flex (110hp) + JB3 -

CAPTUR - H4Bt (90hp) + JHQ K9K (85hp) + JRQH5Ft (120hp) + DC4 K9K (90hp) + JRQ/DC4

KANGOO - K4M + JB3 K9K (60hp) + JB3K9K (70hp) + JH3

KANGOO II 5AGen1 (60hp) K7M (90hp) + JH3/JR5 K9K (70hp) + JH3/JR5+ BT1 K4M (105hp) + JR5/DP0/ K9K (75hp) + JR5

DP2 K9K (80hp) + JR5K4M E85 (105hp) + JR5 K9K (85hp) + JR5

K9K (90hp) + JR5K9K (105hp) + TL4K9K (110hp) + TL4

MÉGANE - K4M (105hp) + JHQ K9K (85hp) + JRQK4M (111hp) + JHQ/TL4 K9K (90hp) + JRQK4M Flex (110hp) + TL4 K9K (105hp) + TL4H5Ft (115hp) + TL4 K9K (110hp) + TL4/DC4H5Ft (130hp) + TL4 F9Q (130hp) + ND4M4R (140hp) + FK0 R9M (130hp) + ND4F4Rt (190hp) + PK4 M9R (165hp) + PK4F4Rt (220hp) + PK4F4Rt RS (250hp) + PK4F4Rt RS (265hp) + PK4(with or without HLSD)

RENAULTELECTRIC GASOLINE DIESEL

SCÉNIC - K4M (110hp) + TL4 K9K (95hp) + TL4K4M E85 (110hp) + TL4 K9K (105hp) + TL4K4M GPL (110hp) + TL4 K9K (110hp) + TL4/DC4M4R (140hp) + FK0 F9Q (130hp) + ND4H5Ft (115hp) + TL4 R9M (130hp) + ND4H5Ft (130hp) + TL4 M9R (150hp) + AJ0

M9R (160hp) + PK4

FLUENCE 5AGen1 K4M (110hp) + JRQ/DP2 K9K (85hp) + JR5(95hp) + BT2 K4M (105hp) + JRQ K9K (90hp) + JR5

H4M (110hp) + DK0 K9K (105hp) + TL4M4R (140hp) + TL4/FK0 K9K (110hp) + DC4M4R E100 (140hp) + TL4/FK0 R9M (130hp) + ND4

LAGUNA - M4R E85 (140hp) + TL4 K9K (110hp) + TL4/DC4F4Rt (170hp) + AJ0 M9R (130hp) + PK4V4Y (240hp) + AJ0 M9R (150hp) + PK4/AJ0

M9R (175hp) + AJ0M9R (180hp) + PK4V9X (240hp) + AJ0

LATITUDE / - M4R E85 (140hp) + TL4 K9K (110hp) + TL4SAFRANE M4R (140hp) + TL4/FK0 M9R (150hp) + PK4

V4U (178hp) + AJ0 M9R (175hp) + PK4/AJ0V4Y (240hp) + AJ0 V9X (240hp) + AJ0

TALISMAN - V4U (190hp) + AJ0 -V4Y (258hp) + AJ0

KOLEOS - M4R + FK0 M9R (150hp) TR25 (170hp) + AJ0/AJ8/ND5/ND8+ FK0/FK8/ND5/ND8 M9R (175hp)

+ AJ0/AJ8/ND8

ESPACE - F4Rt (170hp) + PK6 M9R (130hp) + PK4M9R (150hp) + PK4/AJ0M9R (175hp) + PK4/AJ0

TRAFIC - F4R (120hp) + PK6 F9Q (100hp) + PK5/PK6M9R (95hp) + PF6M9R (115hp) + PF6/PA0

MASTER - - M9T (100hp) + ZF4M9T (125hp)+ PF6/ZF4/PA0/ZA4M9T (150hp)+ PF6/ZF4/PA0/ZA4

RENAULT

C

56 / 57 �MOTORS POWERTRAINS

GASOLINE DIESEL

LOGAN II / SANDERO II / H4Bt (90hp) + JH3 K9K (75hp) + JHQSYMBOL II D4D (75hp) + JH3 K9K (85hp) + JHQ

D4F (75hp) + JH3 K9K (90hp) + JRQK7M (85hp) + JH3K7M Flex (90hp) + JH3K4M (105hp) + JH3K4M Flex (110hp) + JH3

LOGAN I / SANDERO I D4D (75hp) + JH3 K9K (65hp) + JH3D4F (75hp) + JH3 K9K (75hp) + JHQK7J (75hp) + JH3/JH1 K9K (90hp) + JRQK7M (85hp) + JH3/JRQK7M Flex (90hp) + JH3K4M (105hp) + JH3/DP0K4M GNV (85hp) + JH3K4M Flex (110hp) + JH3

LOGAN MCV K7J (75hp) + JH3/JRQ K9K (65hp) + JRQ5 et 7 places K7M (85hp) + JH3/JRQ K9K (70hp) + JRQ

K4M (105hp) + JRQ K9K (75hp) + JRQK9K (85hp) + JRQK9K (90hp) + JRQ

LODGY K7M (80hp) + JRQ K9K (85hp) + JRQK7M (85hp) + JH5 K9K (90hp) + JRQH5Ft (115hp) + JRQ K9K (110hp) + TL4

DOKKER K7M (85hp) + JRQ K9K (75hp) + JRQH5Ft (115hp) + JRQ K9K (85hp) + JRQ

K9K (90hp) + JRQ

LOGAN Van K7J (75hp) + JRQ K9K (65hp) + JRQK7M (85hp) + JRQ K9K (70hp) + JRQK4M (105hp) + JRQ/DPO K9K (75hp) + JRQ

K9K (85hp) + JRQK9K (90hp) + JRQ

LOGAN Pick Up K7M (85hp) + JRQ K9K (65hp) + JRQK4M (105hp) + JRQ/DP0 K9K (70hp) + JRQ

K9K (75hp) + JRQK9K (85hp) + JRQK9K (90hp) + JRQ

DUSTER K4M E85 (105hp) + JRQ/TL8 K9K (85hp) + JRQF4R (136hp) + TL4 / TL8/DP2 K9K (90hp) + JRQ/TL8

K9K (110hp) + TL4/TL8

GASOLINE DIESEL

SM3 H4M (115hp) + DK0 -

SM5 M4R (140hp) + FK0M4R GPL (140hp) + FK0M5Mt (190hp) + DC4

SM7 V4U (190hp) + AJ0 - V4Y (258hp) + AJ0

QM5 M9R (150hp) + AJ0/AJ8/ND5/ND8

DACIA RENAULT SAMSUNG MOTORS

GASOLINE DIESEL

LADA LARGUS K7M + JH3 / JRQ -LOGAN MCV K4M + JRQLOGAN Van

AVTOVAZ

C

F1 TECHNOLOGY FOR EVERYBODY

� Renault's string of victories on the track underline the performance, energy efficiency andconsistency of Renault engines.� The Renault Energy F1 2014 power-unit represents a high-tech breakthrough, deliveringa spectacular cut in fuel consumption, with its direct-injection turbocharged engine cou-pled to advanced energy recovery and electrification systems.� The power-unit shares its name and its DNA with the new-generation Energy engineslaunched in 2011 on production vehicles, symbolizing Renault's ambition to make F1technology available to all.

GLOBALLY RENOWNED TRACK EVENTS

� All over the world, drivers and teams are taking part in track events at the wheel ofRenault Sport vehicles.� Renault Sport Technologies designs, builds and markets track racing vehicles basedon production models (Clio Cup) as well as single-seater vehicles such as the FormulaRenault 3.5, Formula Renault 2.0 and Formula Renault 1.6.� Renault Sport Technologies is the leading organizer of motorsports events worldwide.It has an exceptional showcase with World Series by Renault. Held on tracks aroundEurope, this event provides free top-levelracing for motorsport enthusiasts as partof three international championships.Spectators are able to visit the paddockand take part in all sorts of activities for thepublic. With these popular, family events,visitors enjoy an unforgettable experiencein a setting that is 100% Renault.� Renault Sport Technologies is also pre-sent on the track through national cham-pionships, with the Clio Cup, FormulaRenault 2.0 and Formula Renault 1.6.

MOTORSPORTAn expert in motorsport since its founding, Renault shares its technology and itspassion with the public, its customers and its workforce.

� Motorsport is the ideal laboratory for developing new technical solutions and demonstra-ting their performance and reliability. Wherever possible, successful motorsport technolo-gies are carried over to production vehicles, bringing benefits for customers.� Through motorsport, Renault is able to establish or build its renown on all its markets.Motorsport is a showcase for Renault's high-tech know-how and the passion that drivesits staff.

FORMULA 1: 2013, A RECORD-BEATING YEAR

AN UNEQUALLED SPORTING RECORD

Over the past 36 years, Renault has taken on the best specialists in Formula 1:� with a sporting record unequalled for a full-line vehicle manufacturer: 12 Constructors'

titles, 11 Drivers' titles, i.e. one title every three years on average, under its own name in2005 and 2006, or as an engine manufacturer;

� 165 victories;� a new record in 2013 for the highest number of pole positions: 213.Renault is the most successful engine supplier of the V8 era, with 60 wins, 66 polepositions and 56 fastest laps, along with five Constructors' titles and five Drivers' titles.

AN EXPERT ENGINE MANUFACTURER

� This season, the emphasis is on downsizing and electric power. The Renault Energy F12014 power-unit complies with the new FIA rules, and brings F1 vehicles closer to theissues facing production vehicles: fuel consumption is reduced by 35% with no trade-off inperformance.� Renault Sport F1 powers one-third of the grid.� Partner teams for the 2014 season are: Infiniti Red Bull Racing, Scuderia Toro Rosso, LotusF1 Team and Caterham F1 Team.

58 / 59 �PRODUCTS AND BUSINESS

C

KEY FIGURES

� Founding of World Series by Renault in 2005 - tenth edition in 2014� 12 countries visited� More than five million spectators since its founding� 80 million TV viewers in 23 countries in 2013� In 2013, 60% of drivers in the F1 line-up started their careers in a Renault Formula

championship, including Sebastien Vettel, Kimi Raikkonen, Lewis Hamilton, RomainGrosjean, Daniel Ricciardo and Jean-Eric Vergne.

RALLY RACING: A COMMITMENT TO BRAND CUSTOMERS� Renault Sport Technologies designs, builds and markets rally cars based on theTwingo R.S., Clio R.S. and Mégane R.S. It provides customers with kits to build the cars,replacement parts to repair them and technical support to help them win.

� Renault Sport Technologies organizes Renault Sport Challenges and Trophies in manyEuropean countries. Enthusiasts can race their Twingo R.S. R1 and R2, Clio R.S. R3 orMéganeR.S. N4 against other vehicles in a friendly ambience that places all competitors on an equalfooting.

� The subsidiary is also supporting the 2013 French Junior Champion in 2014.

TECHNICAL EXPERT IN FORMULA E

� Renault is a technical partner in the development of the Spark Renault SRT_01E all-elec-tric single-seater that is set to take part in the FIA Formula E Championship, starting inChina in September 2014.

� Engineers and motorsports experts from Renault Sport Technologies worked with Spark- the designer of this all-electric single-seater - in developing the powertrain layout andspecifications and integrating the electric power systems.

� Working with Renault Sport F1, Renault Sport Technologies found original solutions to:� house the battery components in the chassis� provide the necessary range and performance� ensure safety (crash test + fire test).

AND ALSO…The Renault group is present - at corporate level through the efforts of its subsidiaries - inmany emblematic events including the: Rallye des Gazelles, Dakar, TC2000 and RallyMobil,to name just a few.

EUROPEAN ENDURANCE CHAMPIONSHIP WITH ALPINE

In 2013, Alpine made a victoriouscomeback to motorsport with theA450 and the Signatech team, win-ning the European EnduranceChampionship, LMP2 category.

Returning to the Le Mans 24-hourevent, 35 years to the day after itstriumph in 1978, Alpine thrilledenthusiasts once again, fighting itsway back to finish in 14th position.

60 / 61 �MOTORSPORT

C

62 / 63 �PRODUCTS AND BUSINESS

RESEARCH AND DEVELOPMENTInnovation is central to Renault's strategy and the primary dynamic force of theDrive the Change plan. In 2013, priorities were redefined and the engineering staffspurred on to boost performance and create more value. Thus, R&D is more than everthe cornerstone of the company's competitiveness.

� With more than €1.5 billion invested in 2013 and almost 16,500 employees, RenaultR&D is committed to addressing the challenges faced by the automotive industry and tosupporting key social trends.

2009 2010 2011 2012 2013Renault group patents 362 304 499 607 620

� In the field of engineering, Renault benefits from international expertise, thanks in par-ticular to its decentralized units.

� Units near the company's target markets: Renault Technology Romania, forRomania, Turkey, Russia, Slovenia, and Iran; Renault Technology Korea in SouthKorea; Renault Technology Spain, for Spain, Morocco, and Portugal; RenaultTechnology Americas, for Argentina, Brazil, Chile, Colombia, and Mexico.

� Their main role is to adapt products locally to new customers' needs and expec-tations, to regulatory requirements, and to economic conditions in each country.

THE SIX KEY PRIORITIES FOR RENAULT R&D:INNOVATIVE ARCHITECTURES This is one area where Renault has undoubtedly left its deepest mark on automotivehistory, in particular with the R16, Espace, Twingo, Scenic and Twizy. It is continuing to makehistory with new projects, too.

� In 2013 Renault unveiled the Twin Z concept car, prefiguring the styling for a small citycar. Looking back for inspiration to the Twingo and the R5, two groundbreaking city cars thateach set the trend for its times, this concept features a rear-engine architecture, allowingthe wheels to be pushed out to the four corners of the body. This provides not only excellentstability, but also a large floor area, thus offering an exceptional combination of comfort andcompactness.

ON-BOARD COMFORT AND PEACE OF MINDThese are key aspects of the brand identity. R&D seeks innovation in all areas that cancontribute to pleasurable and carefree motoring.

� With the NEXT TWO prototype, Renault has revealed its vision of the self-driving car thatwill be on the roads by 2020. Renault is aiming:

� to give motorists free time at the wheel by turning the driving over to the car at anaffordable cost, and

� enabling motorists to take advantage of this free time in fun and productive ways byproviding full on-board connectivity in complete safety.

ELECTRIC VEHICLES AND THE ECOSYSTEMRenault is a pioneer and leader in this burgeoning market, with a range of zero-emissionvehicles that achieve a genuine breakthrough in CO2 emissions.

� R&D efforts are focused mainly on increasing battery autonomy and controlling costs.This involves mastering battery chemistry, managing battery cooling, increasing capacityand endurance regardless of driving conditions, and shortening charging times.

C

64 / 65 �RESEARCH AND DEVELOPMENT

INTERNAL-COMBUSTION-ENGINE VEHICLESRenault has set an objective of significantlydecreasing CO2 emissions to address theenergy and environmental challengesfacing the planet..

� In the first half of 2013, the Renault groupwas the European leader in CO2 emissionsfor passenger cars sold, with an average of115.9 grams of CO2/km (Source: AAA DATA).More broadly, the average level of CO2 emis-sions/km for the Renault group's entire vehiclerange decreased by nearly 10 grams between2012 and the first half of 2013.

� Renault is getting ready to roll out a “2l/100 km - affordable by all” vehicle. The aim isto trim the vehicle's mass and aerodynamic drag by 30% without increasing its cost price.In 2014 a demonstrator will be unveiled that will feature numerous innovations.

NEW SERVICESSociety is evolving, with the new possibilities offered by technologies, new life styles andsocial relations, greater collaboration and interaction, networks and communities, the needfor continual connectivity and many other changes. Technology is also evolving, particular-ly when it comes to electronics and their many applications. At the convergence of thesetwo powerful trends, the automobile must evolve, too, particularly by providing not onlyinformation in real time, but also seamless utilization for drivers and passengers fromone situation to another.

� In its PAMU project (Advanced Platform for Urban Mobility), Renault is developing anautomated car valet service. The vehicle is designed to operate automatically, without adriver, in a controlled environment between a parking and charging area and a meetingpoint chosen by the driver.

AFFORDABILITY

To provide mobility for everyone, vehicles must be built with simplified and standardizedmodules, components and systems so they can be sold at affordable prices.

Vehicle supervision and control

� Autonomous operation of the vehicle� Perception� Localization� Navigation� Communication� User

ELECTRIC VEHICLESElectric vehicles are the solution that is most effective in cutting CO2 emissions inuse in vehicle transport.

� Reflecting this, and as part of the “Renault eco2” environmental policy deployed since2007, Renault is marketing a range of four electric vehicles, accessible to the greatestnumber.

� With market share of over 37%, Renault is No.1 for sales of electric vehicles in Europe.

� Alongside the environmental benefits, electric vehicles deliver radical improvements forusers, for a comfortable, silent, relaxed driving experience.

NEWS IN 2013� The Z.E. range now has a full line-up of four vehicles, now available across the network.

� Many competitors, particularly German makes, are developing electric models, so weexpect to see public charging stations being deployed at a faster pace.

� ZOE obtained the highest possible score of five stars in EuroNCAP tests in March. Theorganization also listed ZOE as the safest supermini in 2013, ahead of its ICE rivals.

� ZOE won the green car of the year prize at the Green Apple Awards in London and“Product design 2013” in the Red Dot Design award. This takes the number of awards wonby the Z.E. range to a total of eleven.

� A cable for charging ZOE from a conventional domestic socket was presented at theFrankfurt Motor Show.

KEY FIGURES� At the end of 2013, Renault

totalled 37,000 electricvehicle registrationsworldwide.

� 98% of ZOE drivers aresatisfied, and 95% forKangoo Z.E.

� Today, 23 countries marketthe Renault Z.E. range, in partor in full.

C

66 / 67 �PRODUCTS AND BUSINESS

PURCHASING SUPPLY CHAINThe Group's global Supply Chain function handles directly or coordinates all strate-gic and operational aspects of the supply chain, from the gates of the suppliers'plants to the vehicle's delivery to the customer.

AMOUNT OF RENAULT PURCHASESWorldwide - € billion

2012 2013

Composants automobiles 18.1 18.3Industrial goods and services, logistics 4.6 5.1After-sales 0.9 0.9

TOTAL 23.6 24.3

NUMBER OF RENAULT SUPPLIERSRenault s.a.s., including subsidiariesSuppliers paid at least 6,000 during the year.

2013

Automotive components 2,244Industrial goods and services,logistics 8,927 After-sales 393

RENAULT-NISSAN PURCHASING ORGANIZATIONThe Renault-Nissan Purchasing Organization (RNPO) has determined the purchasing strate-gy and selected the suppliers for all the Alliance's purchases since April 1, 2009. This repre-sents an estimated amount of more than 74 billion for 2013.

Also, 76% of suppliers are used by both Renault and Nissan(percentage calculated for the 100 largest suppliers of Renault and Nissan).

In September 2013, RNPO and AVTOVAZ set up a joint entity, the Common PurchasingOrganization LLC (CPO), to supervise purchasing by Renault, Nissan and AVTOVAZ inRussia. It will manage a defined scope of purchasing relating to industrial equipment,powertrains and vehicles based on shared platforms.

� 6,250 employees� 8 Operational Logistics Departments manage logistics in one or more countries.

In 2013, a new department was created in Morocco � 9 ILN logistics platforms (Bursa, Busan, Cordoba, Curitiba, Grand Couronne,

Pitesti, Pune, Tangiers, Valladolid): pick-up, consolidation and shipping of parts tomanufacturing sites

� 4 SFKI logistics platforms (SOFRASTOCK International - Saint-André-de-l'Eure,Valladolid, Cordoba, Curitiba): management and distribution of small automotiveparts and maintenance and tooling parts to manufacturing sites

ILN PLATFORM ACTIVITIESVolumes (m3) at December 31, 2013

ILN Platforms TOTAL Export Export localIPO KD distribution import

Bursa (Turkey) 536,514 327,422 25,398 134,783 48,911Busan (South Korea) 178,078 95,694 82,384Cordoba (Argentina) 74,702 74,702Curitiba (Brazil) 198,748 198,748Grand-Couronne (France) 568,096 537,238 1,350 29,998Pitesti (Romania) 1,925,387 1,837,485 87,902Pune (India) 53,859 53,859Tanger (Morocco) 2,200 2,200Valladolid (Spain) 332,650 299,652 32,998

TOTAL 3,870,234 3,427,000 109,132 134,783 199,319

C

68 / 69 �PRODUCTS AND BUSINESS

SALES NETWORKRenault sells its vehicles around the world through more than 12,000 points of sale.The Renault sales network is made up of:� a primary network of Renault Retail Group (RRG) outlets belonging to Renault and privatedealerships;� a secondary network of agencies, each under contract with an RRG outlet or privatedealership, which puts Renault in closer proximity to its customers.

STRUCTURENumber of Renault sites at end-June 2013

Region Primary Primary Totalnetwork network

France 707 3,650 4,357Europe (incl. France) 2,697 6,704 9,401Euromed-Africa 485 202 687Eurasia 223 15 238Asia-Pacific 813 50 863Americas 836 101 937

TOTAL 5,054 7,072 12,126

SATISFY CUSTOMERS� To meet the challenges of multichannel marketing, Renault is redefining the entirecustomer experience (for consumers and corporate customer, and for new and pre-ownedvehicles) in all channels (online, points of sale, and customer relations platforms).

� In line with the C@RE (Customer Approved Renault Experience) program begun inApril 2013, the Group is stepping up its transformation so as to provide customerswith better service by taking into account their new expectations.

� Renault is aiming for excellence in customer relations at every stage of the salesprocess - before, during and after the purchase.

� Each year Renault surveys more than one million customers in 31 countriesto assess its sales and after-sales network.

� In 2013, 8 out of 10 customers recommended either the Renault network, on thebasis of the service they received during the repair of their vehicle, or their dealer,following the purchase of a new vehicle, to people around them.

RENAULT RETAIL GROUP (RRG)� RRG, the No. 2 automobile distributor in Europe, is a wholly owned subsidiary of theRenault group that markets new vehicles under the Group's brands

� The RRG deals with all aspects of the marketing, from sales to after-sales service.� 3 brands: Renault, Nissan and Dacia� 209 sites� 10,416 employees� 13 countries: Austria, Belgium, Czech Republic, France, Germany, Ireland, Italy,

Luxembourg, Poland, Portugal, Spain, Switzerland and the United Kingdom

RCI BANQUERCI Banque SA is a 100% subsidiary of Renault S.A. RCI Banque provides financingproducts and services to support the sales of the Renault Group brands (Renault,Renault Samsung Motors, Dacia) throughout the world and for the Nissan Group(Nissan, Infiniti) primarily in Europe, Russia and South America. RCI Banque is presentin 36 countries.

� RCI Banque offers:� financing to consumers for the purchase, use or replacement of new or pre-

owned vehicles marketed under Renault-Nissan Alliance brands;� a full range of services to businesses, from long-term leasing with services to fleet

management without financing;� financing to the Alliance networks for their inventories of new and pre-owned

vehicles and replacement parts.

NEW FINANCING AND OUTSTANDING LOANSNew and pre-owned Renault, Dacia, Renault Samsung Motors, Nissan and Infiniti vehicles.€ million

2012 2013

Penetration rate (NV) 35.0% 34.6%New vehicle financing 10,800 11,400Number of vehicle contracts 976,000 1,161,000Average outstanding performing loans 24,185 24,219

PENETRATION RATE AND AVERAGE OUTSTANDINGPERFORMING LOANS BY REGIONRCI Banque penetration on the sales of new Renault, Dacia, Renault Samsung Motors,Nissan and Infiniti vehicles

% and € million

Penetration rate Average outstandingperforming loans

2012 2013 2012 2013

France 36.9% 36.9% 8,435 8,380Europe (incl. France) 33.9% 35.1% 20,036 19,933Euromed 26.3% 26.0% 278 339Americas 37.1% 42.7% 2,596 2,920Asia-Pacific 57.3% 47.4% 1,275 1,027

TOTAL RCI BANQUE 35.0% 34.6% 24,185 24,219

C

70 / 71 �PRODUCTS AND BUSINESS

AFTER-SALESRenault makes after-sales service a powerful loyalty builder by assisting customersthroughout the entire life of their vehicle.

SERVICES� Service contracts include insurance, maintenance, and warranty extensions.

� Almost 1 new vehicle out of 2 registered worldwide in 2013 was covered bya service contract.

� 1,300,000 service contracts were sold in 2013.� Fixed prices: Renault was one of the first automakers to offer a full range of fixedprices on many maintenance and repair services. Customers can thus manage theirbudgets without any unpleasant surprises.� An extended range of services: Renault Rent (vehicle rental), Renault Assistance(breakdown or accident assistance), Renault Minute (fast maintenance and repair), Pro+(maintenance and repair of company vehicles), etc.