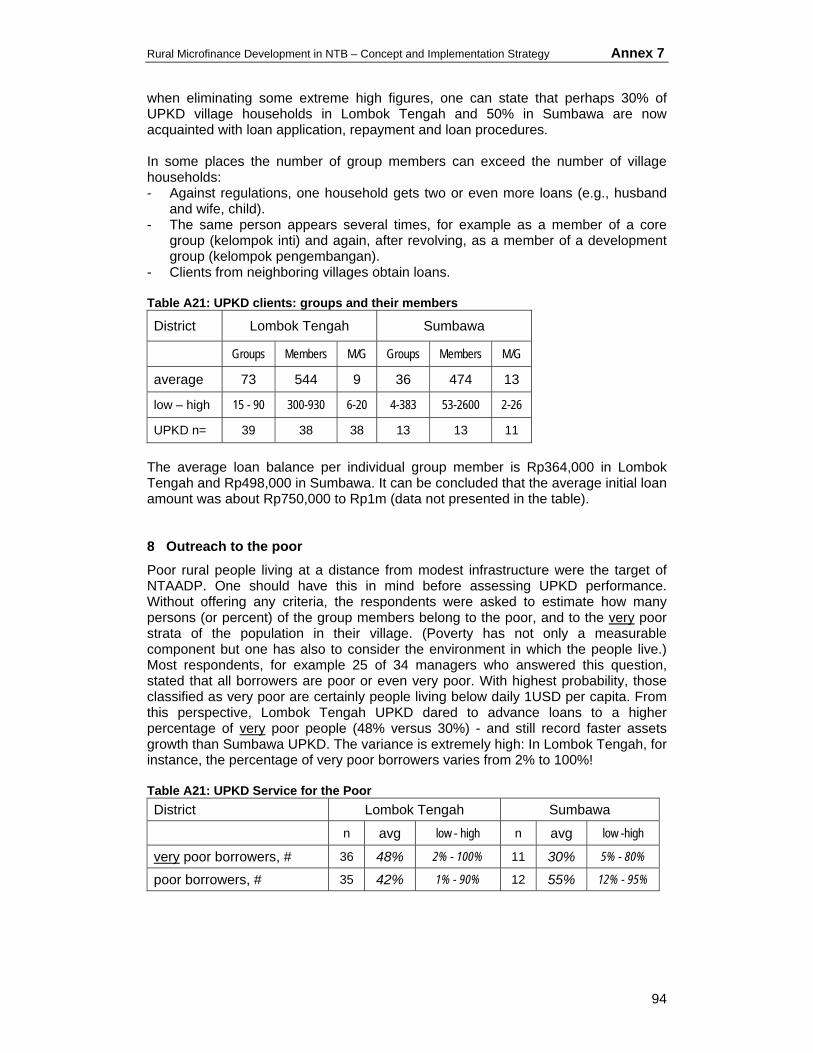

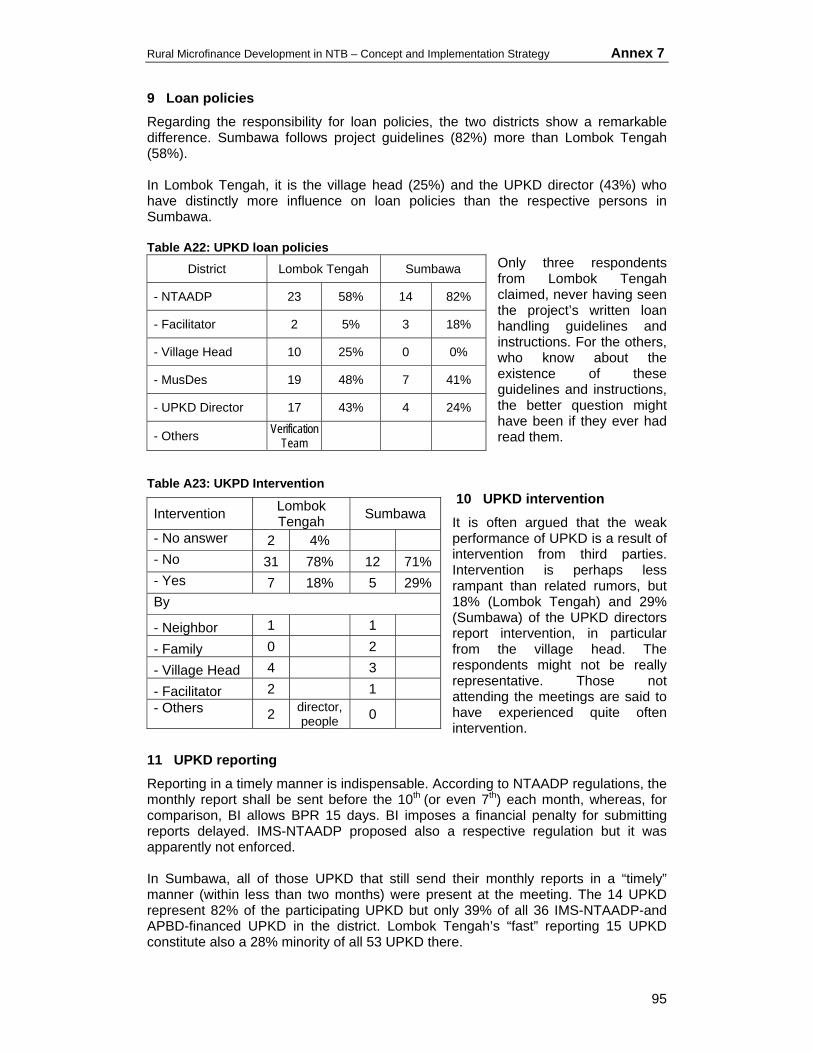

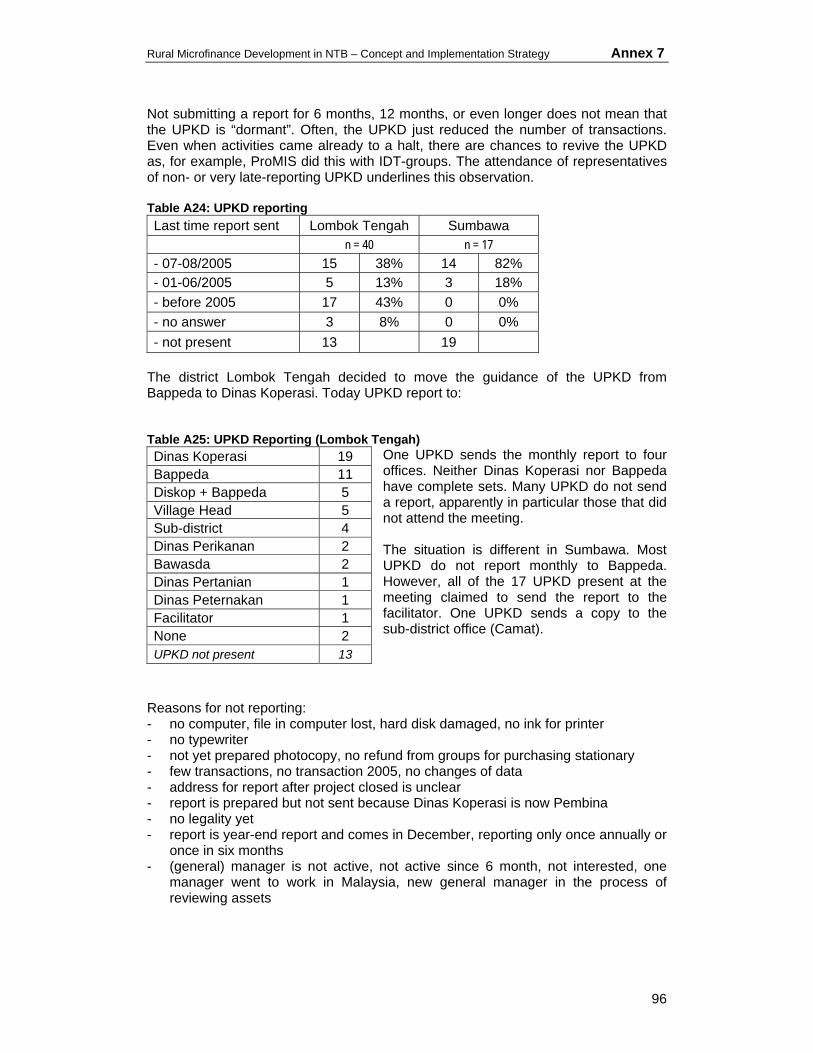

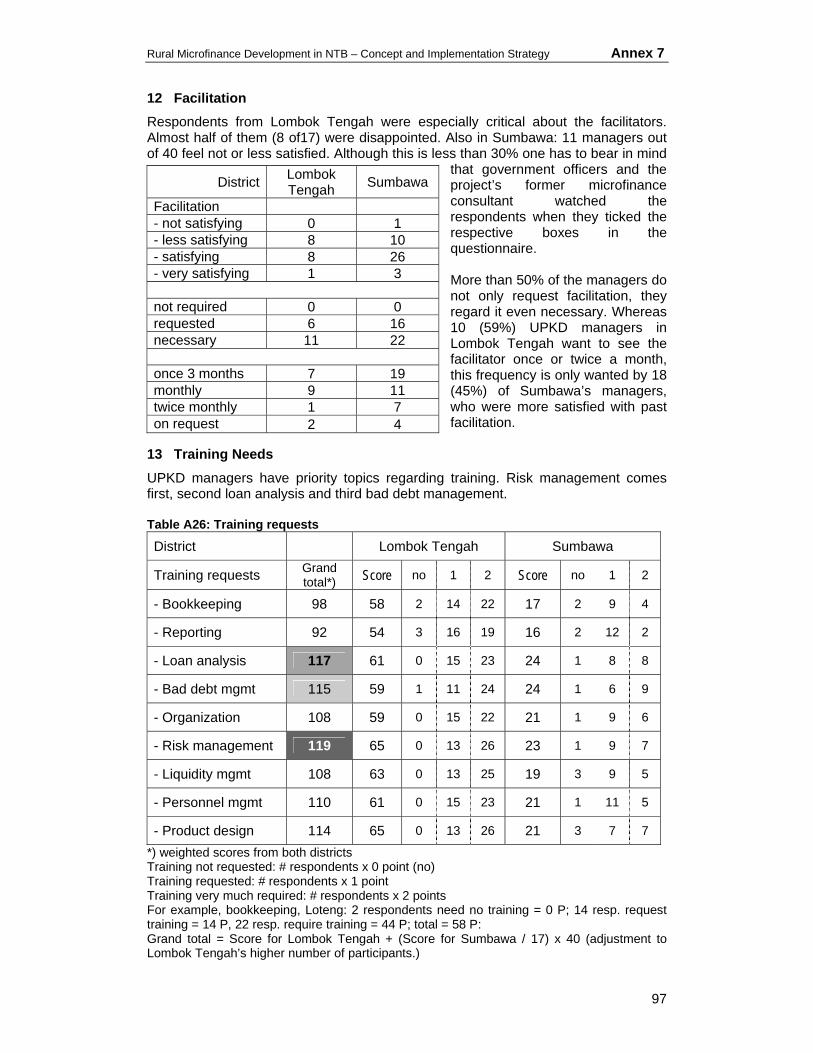

regional microfinance development - cgap · regional microfinance development nusa tenggara barat...

TRANSCRIPT

Regional Microfinance Development

Nusa Tenggara Barat (NTB)

Concept and Implementation Strategy

Dr. Wolfram Hiemann, Berlin Stefan Jansen, Denpasar I Ketut Budastra, Ph.D., Mataram November 2005

EXECUTIVE SUMMARY I

RINGKASAN EKSEKUTIF IX

1 INTRODUCTION 1

2 THE PROVINCE OF NUSA TENGGARA BARAT (NTB) 2

3 THE RURAL MICROFINANCE MARKET IN NTB 4

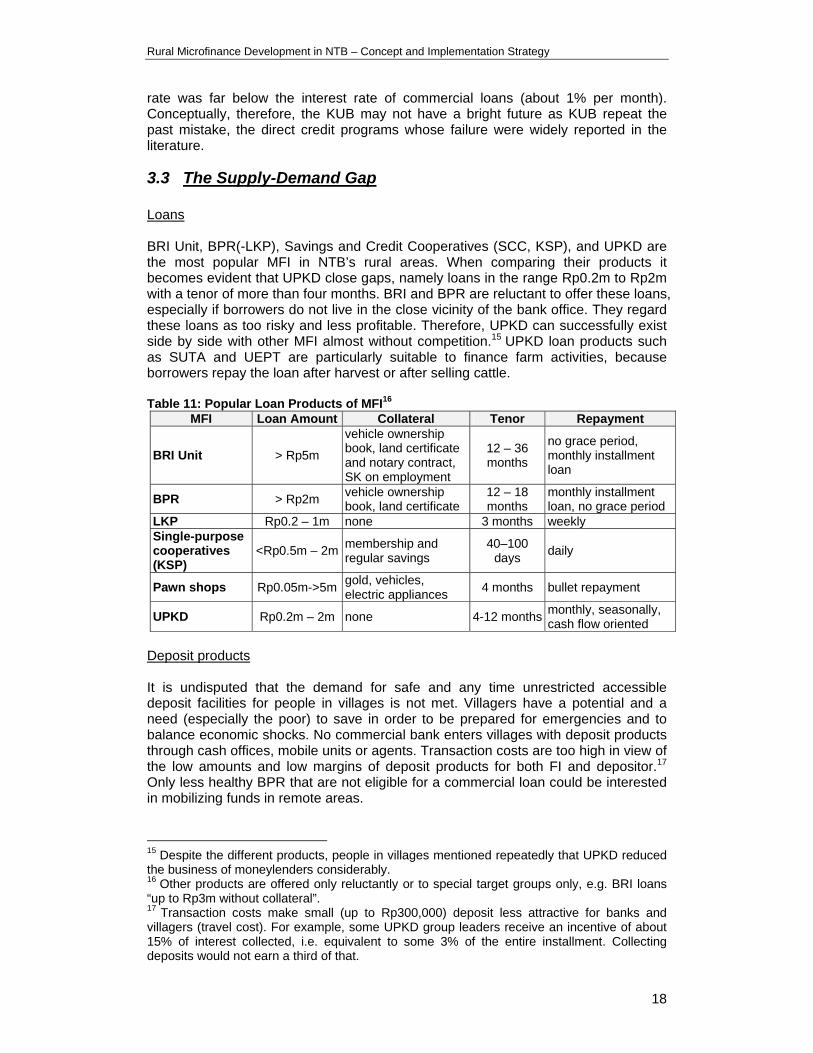

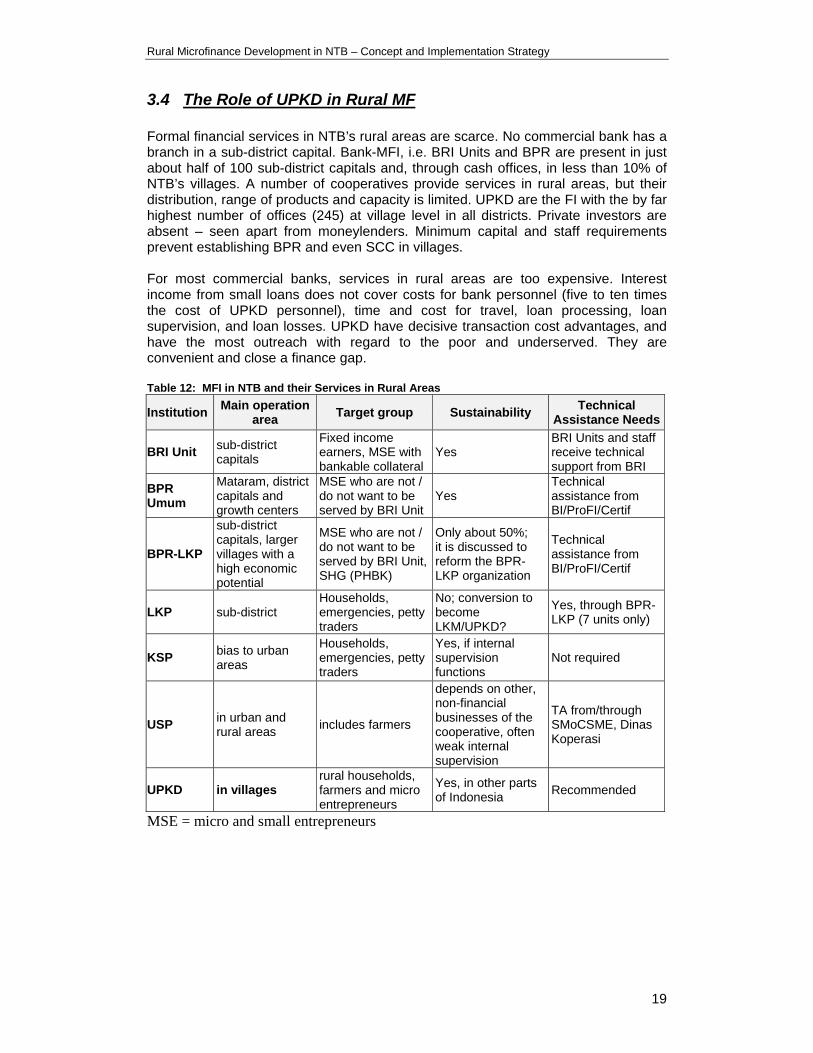

3.1 DEMAND FOR MICROFINANCE 4 3.2 SUPPLY OF MICROFINANCE 5 3.3 THE SUPPLY-DEMAND GAP 18 3.4 THE ROLE OF UPKD IN RURAL MF 19

4 UPKD: OUTREACH AND SUSTAINABILITY AT THE VILLAGE LEVEL 20

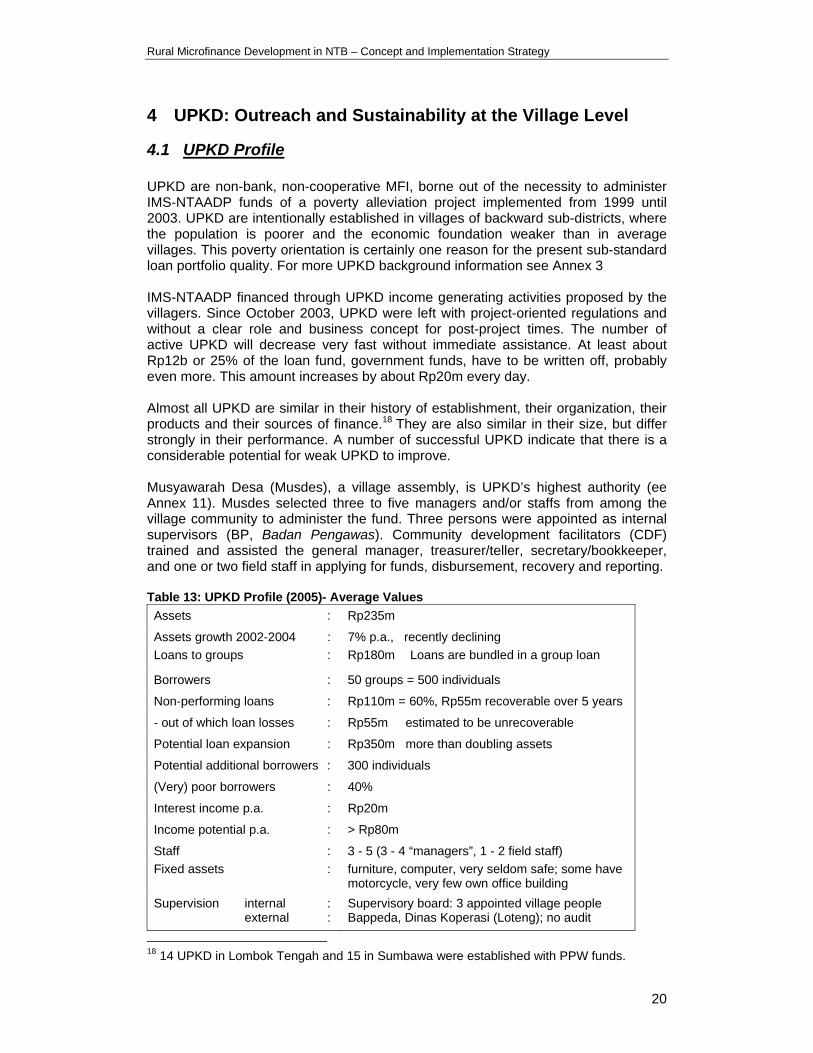

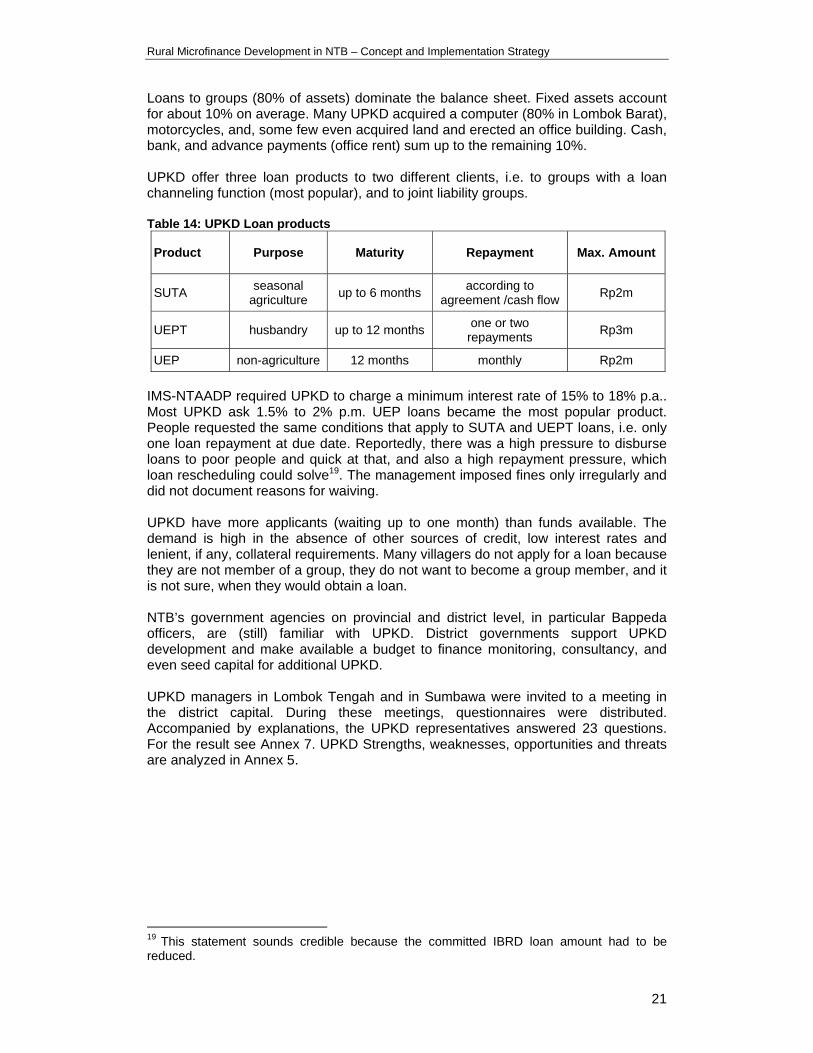

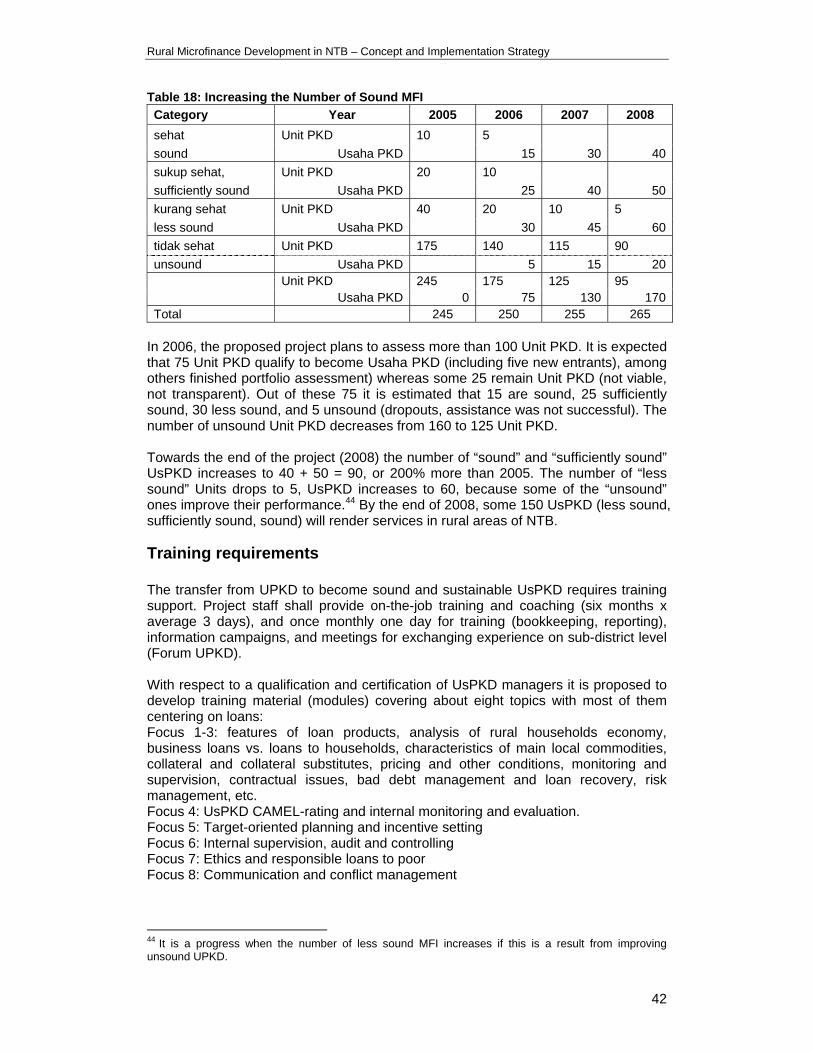

4.1 UPKD PROFILE 20 4.2 UPKD PERFORMANCE 22 4.3 CONCLUSION 28

5 THE PROJECT CONCEPT: STRENGTHENING UPKD 29

5.1 RATIONALE 30 5.2 ELEMENTS OF A FINANCIAL SYSTEMS APPROACH FOR NTB 31

6 IMPLEMENTATION STRATEGY: ACHIEVING RESULTS 36

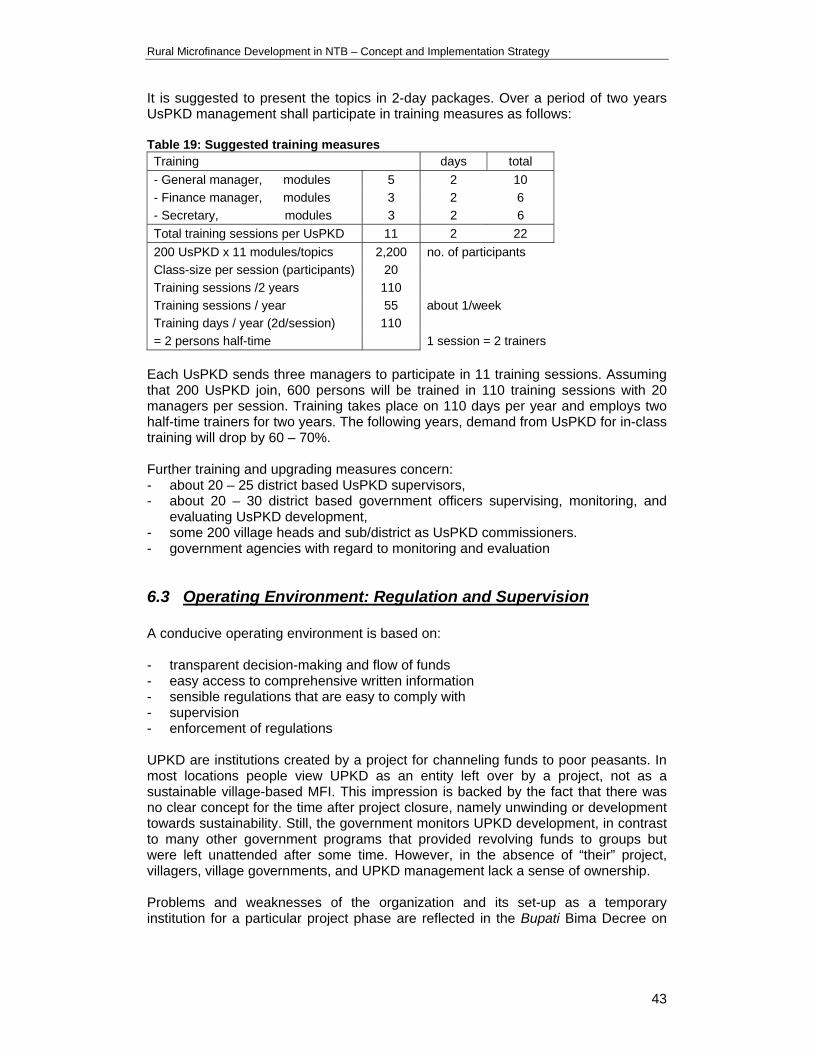

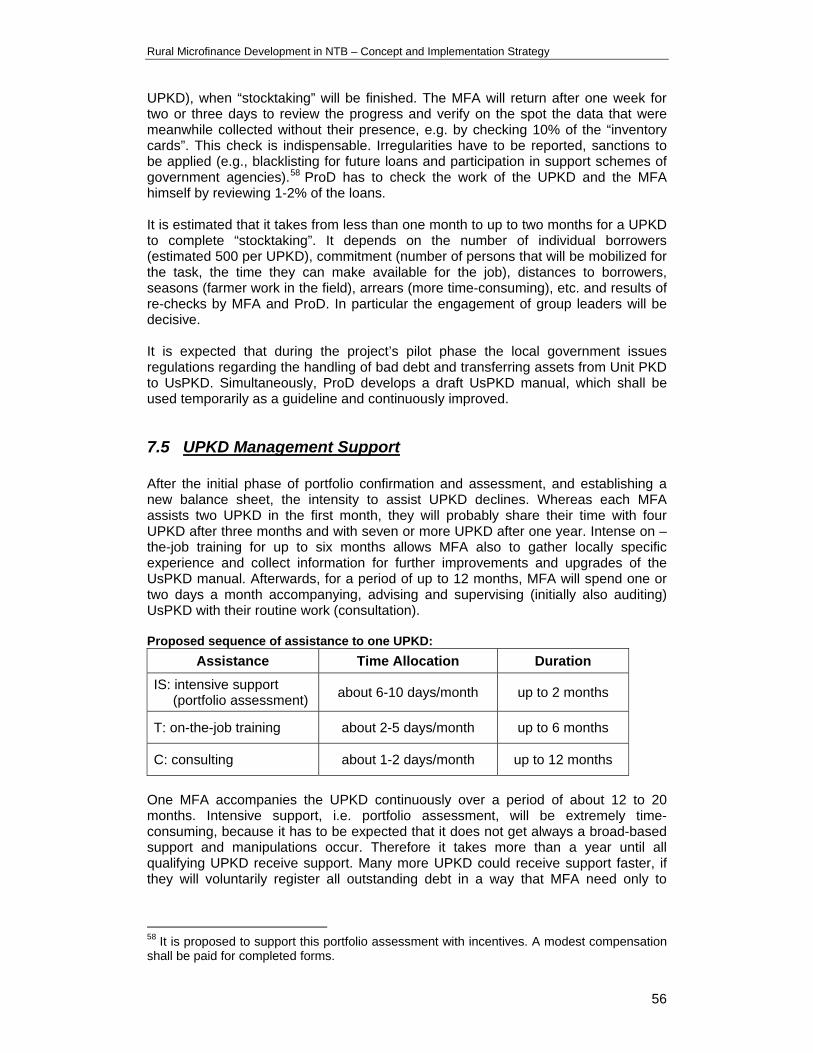

6.1 IMPROVING SERVICE QUALITY 36 6.2 INCREASING THE NUMBER OF SOUND MFI 38 6.3 OPERATING ENVIRONMENT: REGULATION AND SUPERVISION 43 6.4 UPKD IN THE REGIONAL FINANCIAL SYSTEM 49 6.5 UPKD ACCESS TO FINANCE 50

7 IMPLEMENTATION 2006-2008 52

7.1 UPKD DEVELOPMENT AND ENABLING ENVIRONMENT 52 7.2 SEQUENCE OF ACTIVITIES 53 7.3 DRAFT CONCEPT: IMPLEMENTATION PHASE 53 7.4 UPKD PORTFOLIO VERIFICATION AND ASSESSMENT 55 7.5 UPKD MANAGEMENT SUPPORT 56 7.6 SUGGESTIONS FOR MID-TERM PLANNING 63

ANNEX 1: HOUSEHOLD SURVEY RESULTS 64

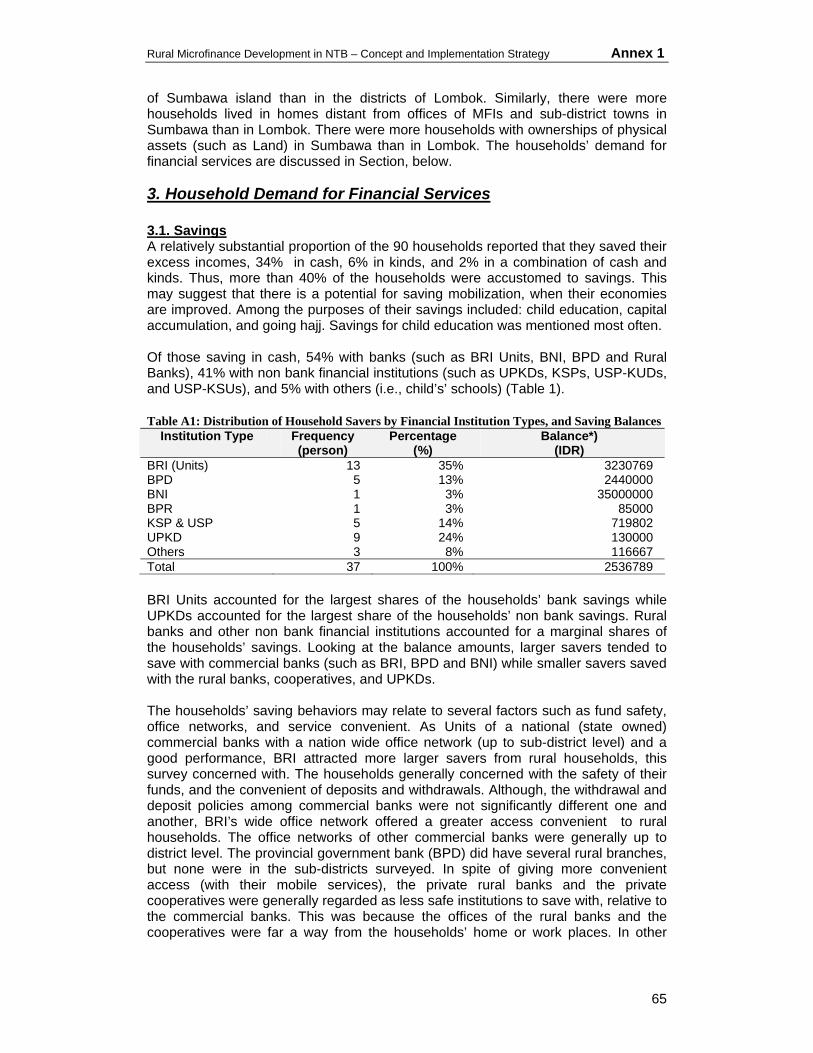

1. INTRODUCTION 64 2. THE SAMPLE HOUSEHOLDS 64 3. HOUSEHOLD DEMAND FOR FINANCIAL SERVICES 65

4. HOUSEHOLD PERCEPTIONS OF MICROFINANCE SUPPLY 68 5. SUMMARY AND CONCLUSIONS 69

ANNEX 2: MFI SURVEY RESULTS 70

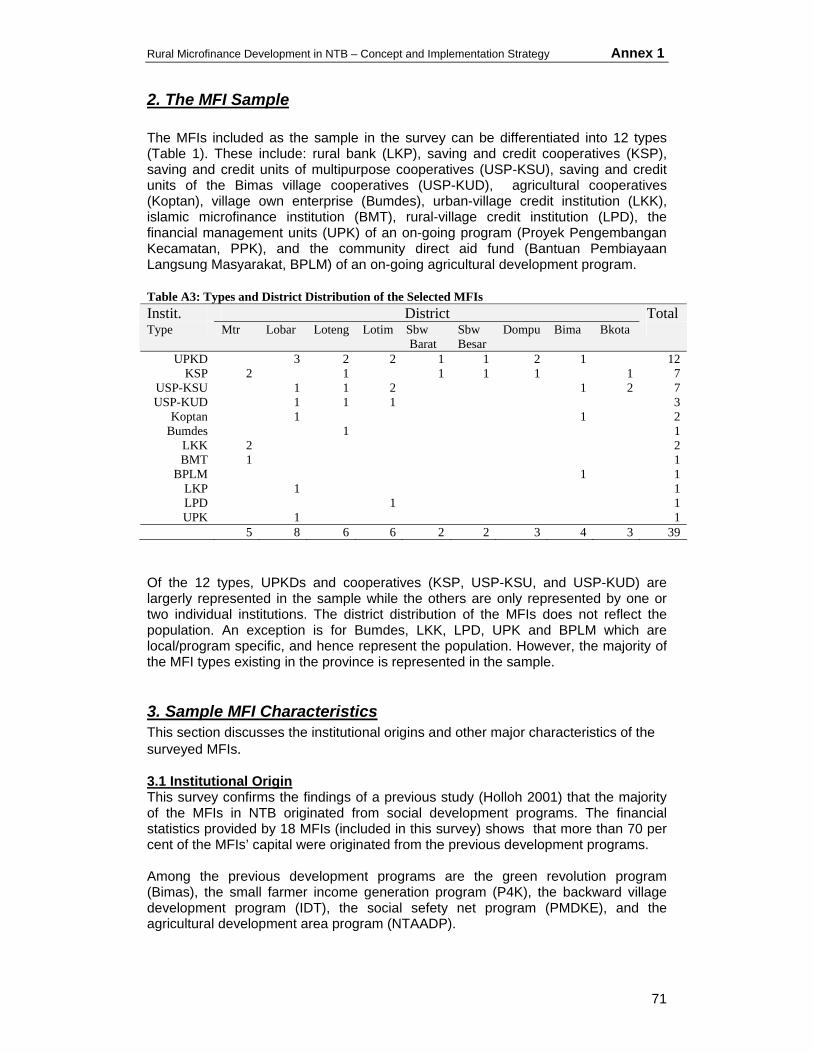

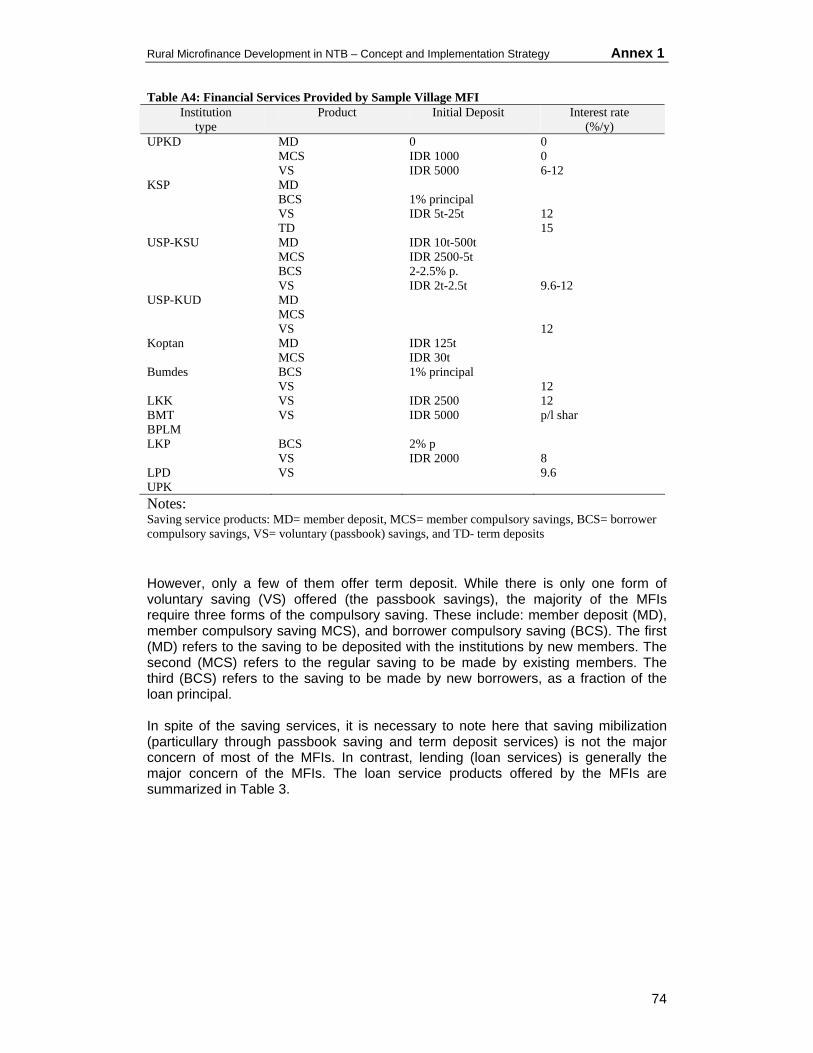

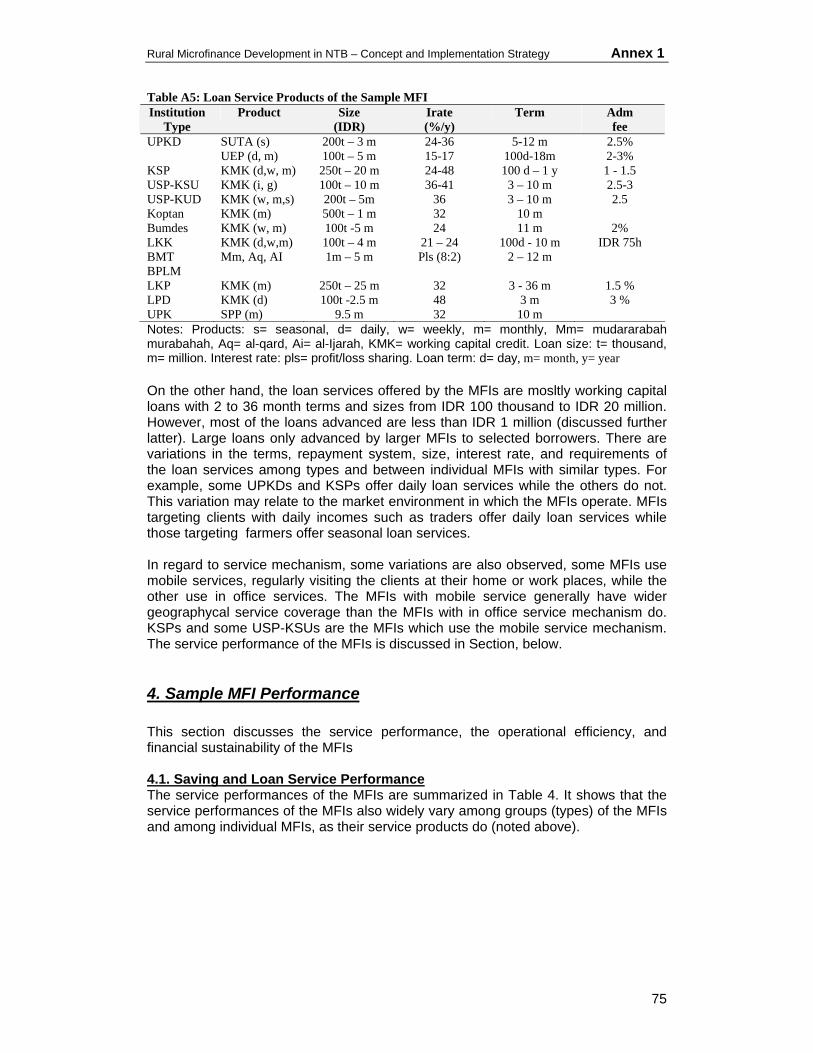

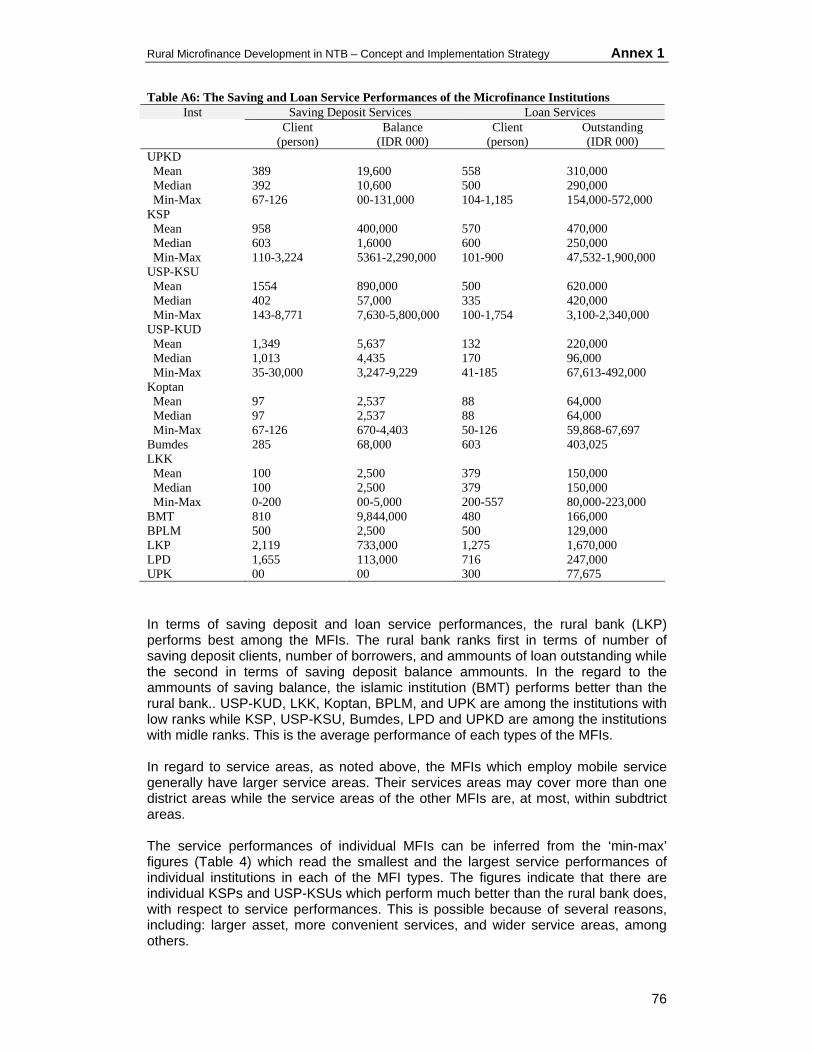

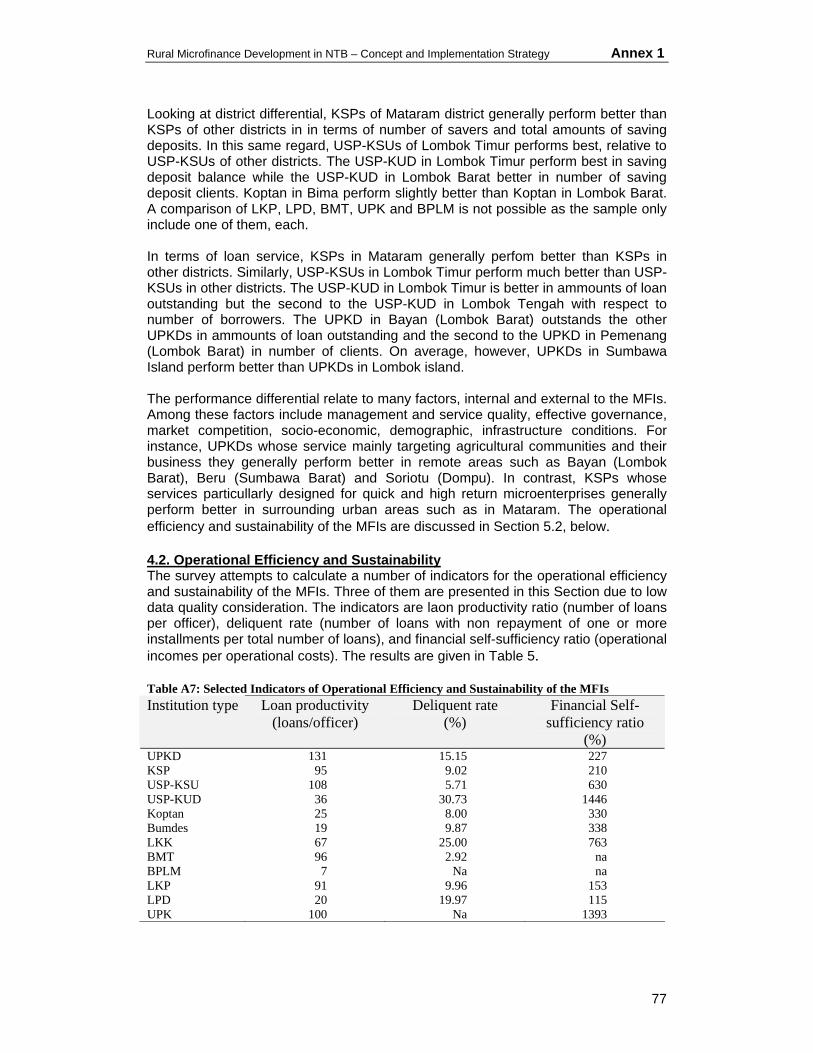

1. THE MICROFINANCE SYSTEM IN NTB PROVINCE 70 2. THE MFI SAMPLE 71 3. SAMPLE MFI CHARACTERISTICS 71 4. SAMPLE MFI PERFORMANCE 75 5. SUMMARY & CONCLUDING REMARKS 79

ANNEX 3: UPKD – ORIGINS 81

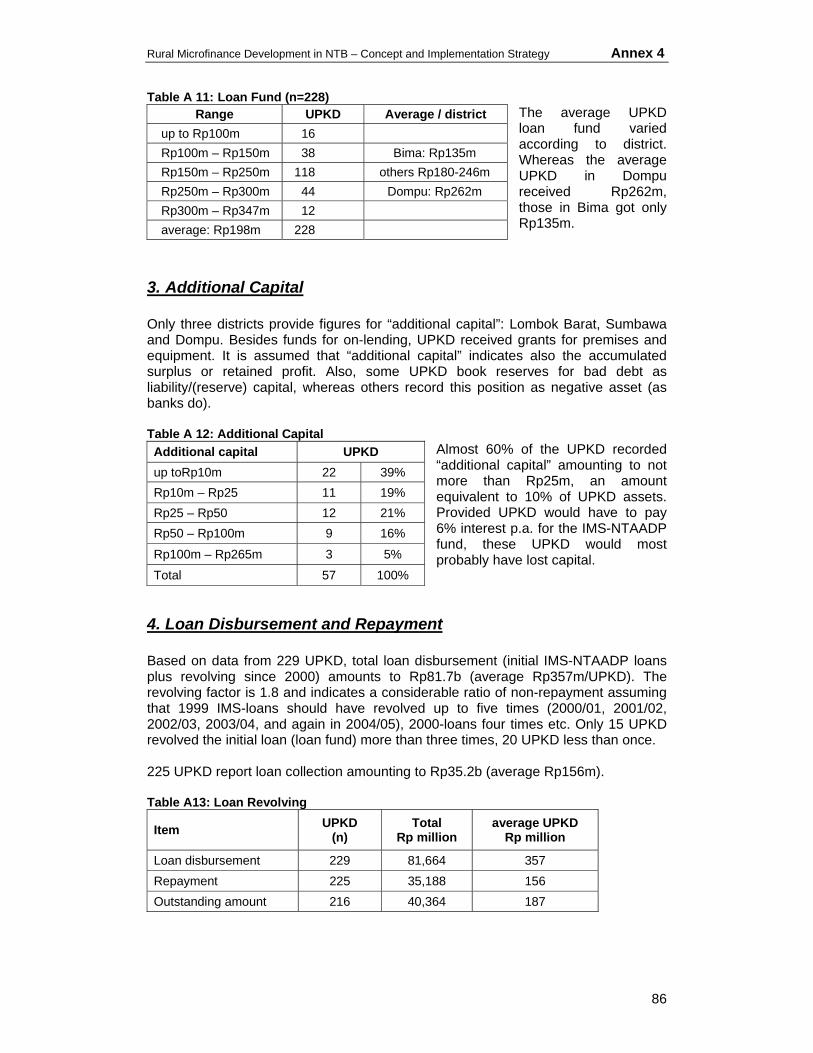

ANNEX 4: UPKD – FINANCIAL PERFORMANCE 84

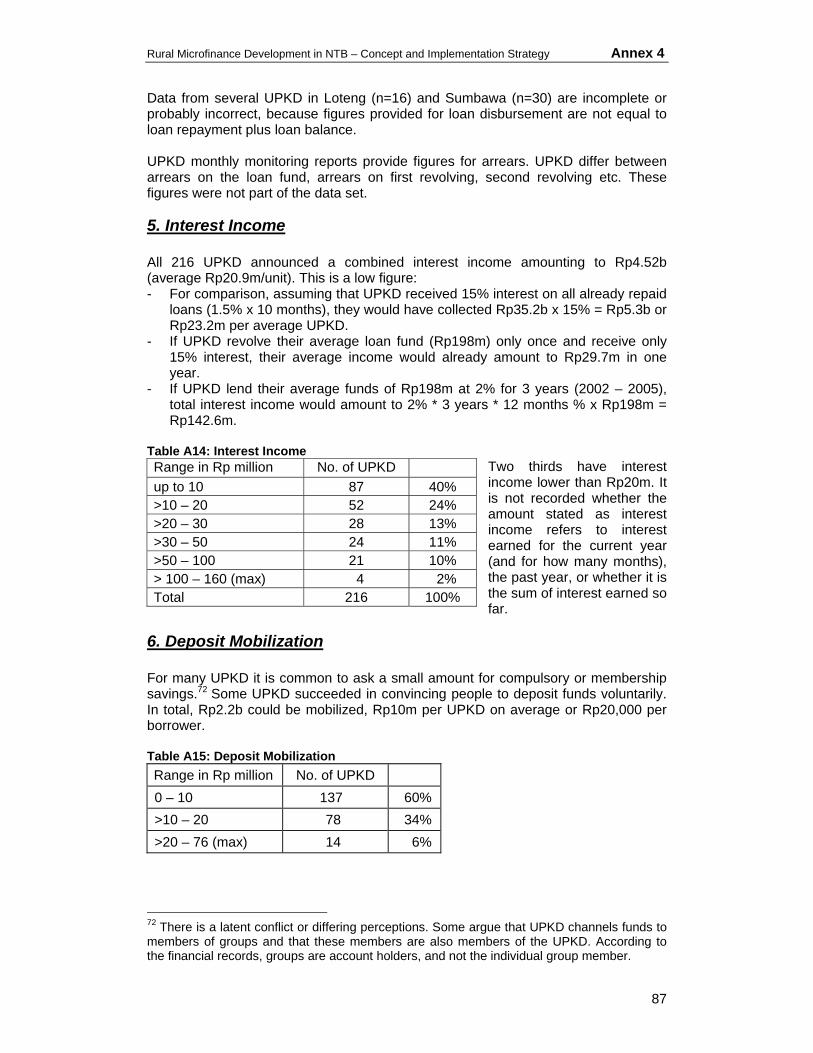

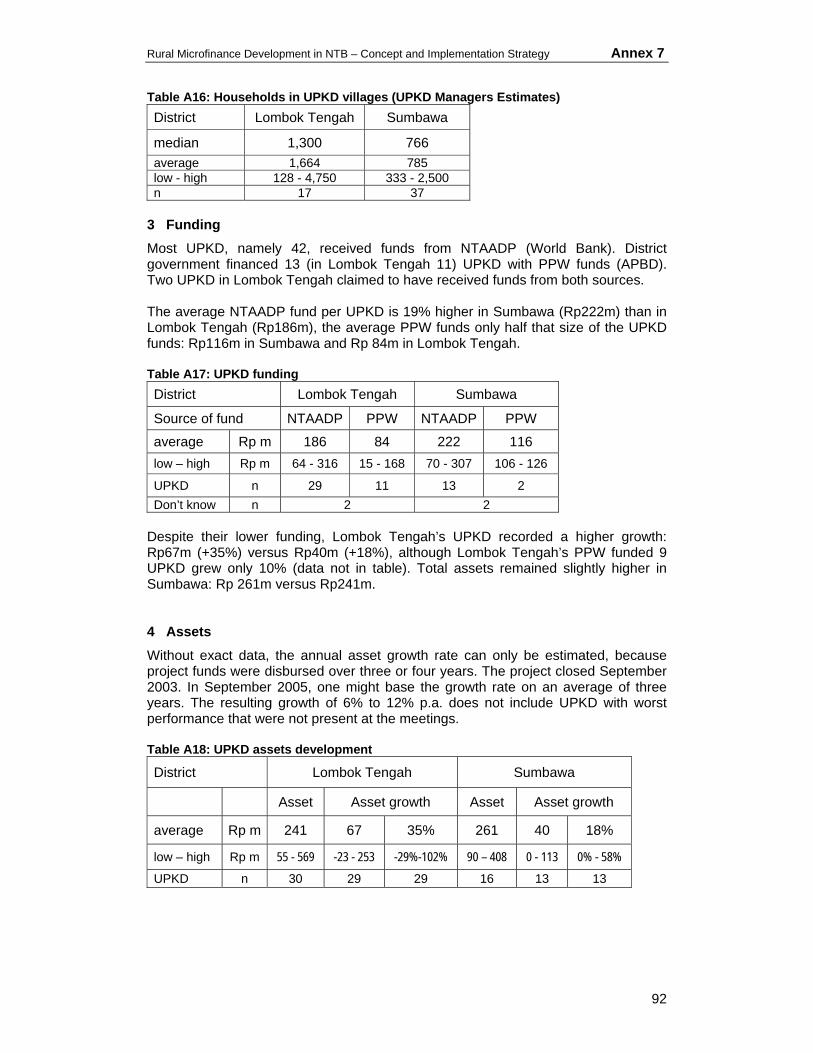

1. ASSETS 84 2. LOAN FUND OR INITIAL FUND 85 3. ADDITIONAL CAPITAL 86 4. LOAN DISBURSEMENT AND REPAYMENT 86 5. INTEREST INCOME 87 6. DEPOSIT MOBILIZATION 87

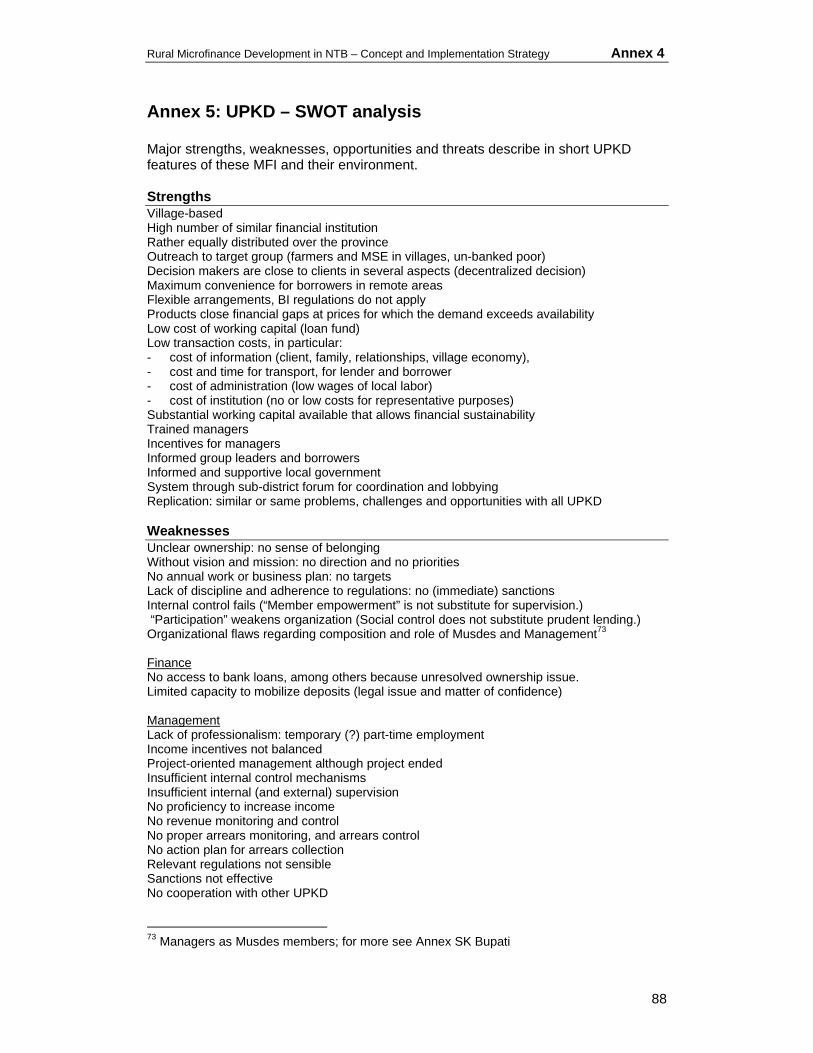

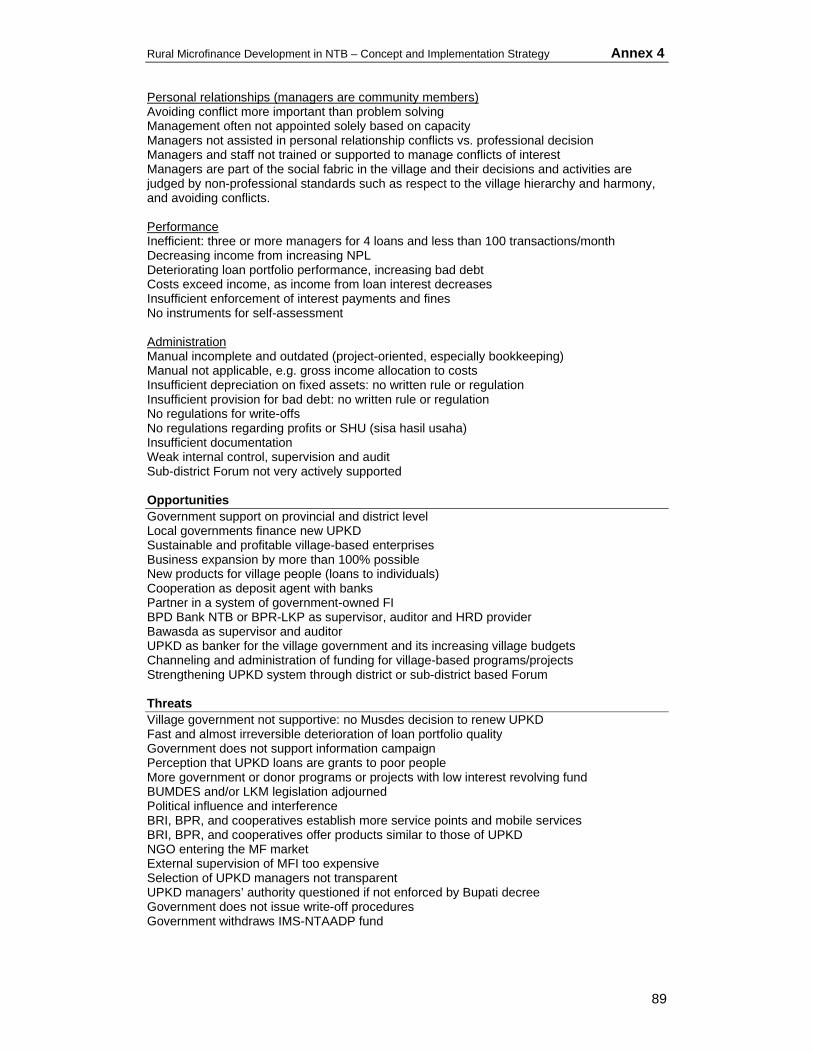

ANNEX 5: UPKD – SWOT ANALYSIS 88

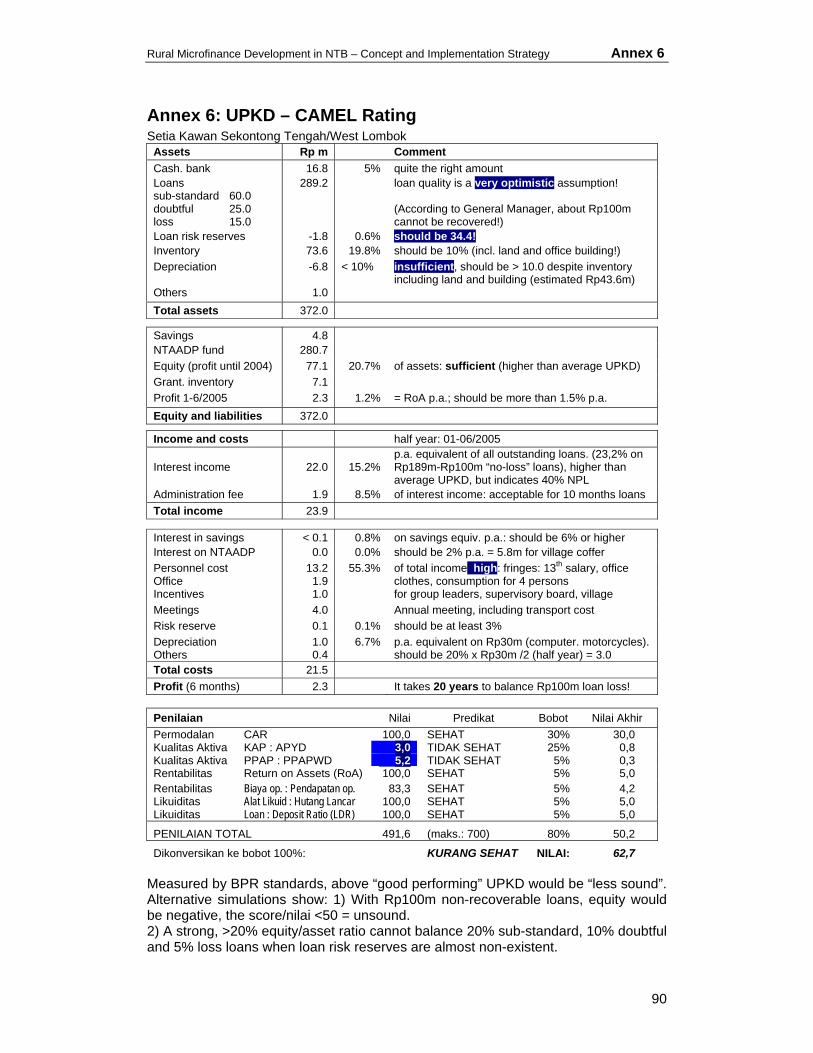

ANNEX 6: UPKD – CAMEL RATING 90

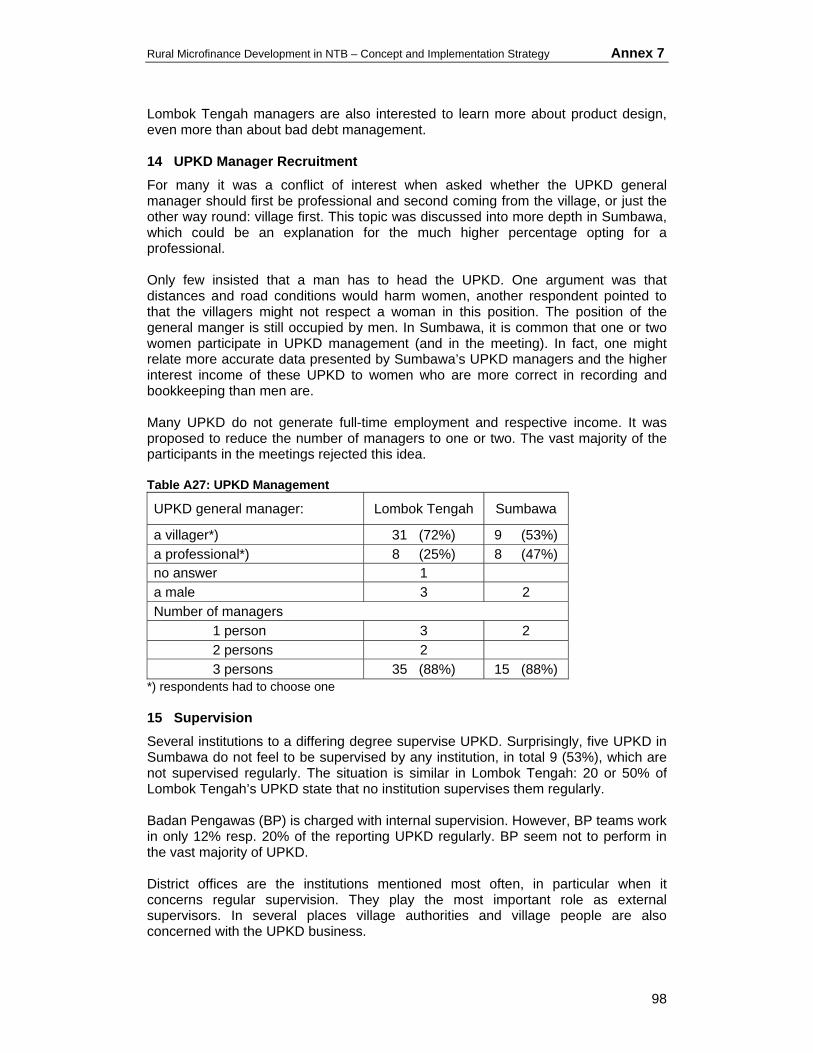

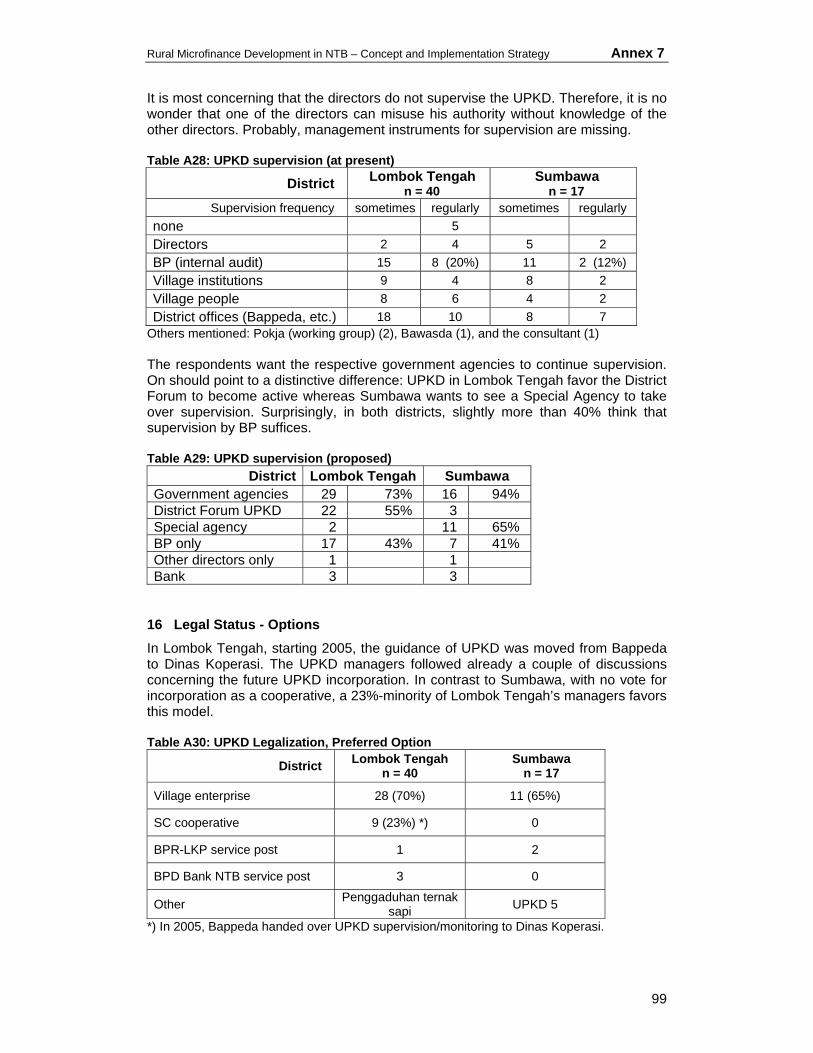

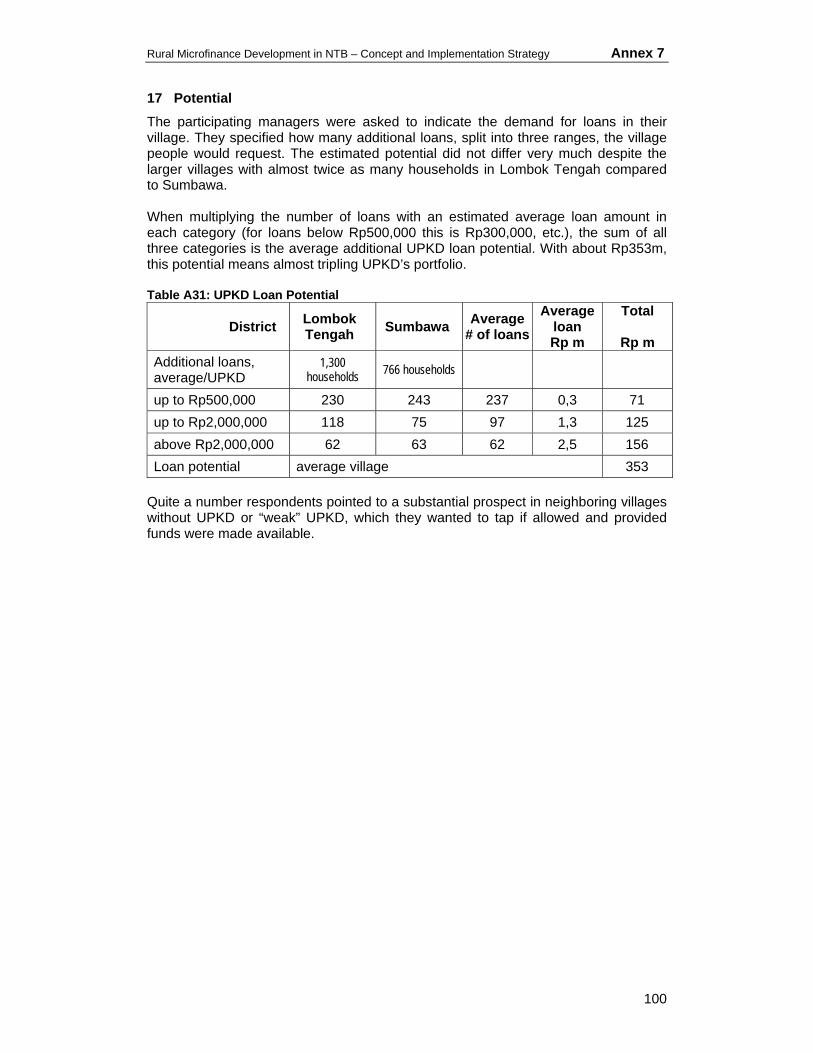

ANNEX 7: UPKD – MANAGEMENT SURVEY 91

ANNEX 8: UPKD – COMMENTS ON REGULATIONS 101

1. SK BUPATI BIMA ON UPKD 102 2. STATUTES (ANGGARAN DASAR, AD) 104 3. BYLAWS (ANGGARAN RUMAH TANGGA, ART) 105 4. MANUAL AND GUIDELINES FOR UPKD OPERATION 108

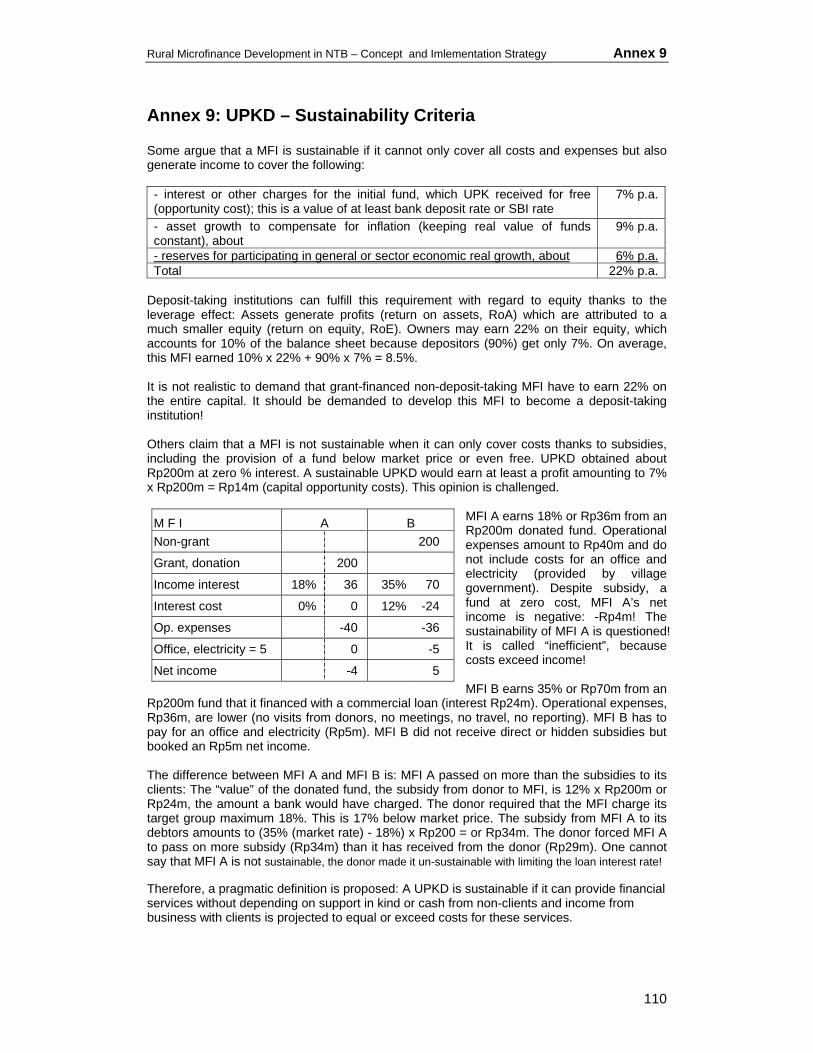

ANNEX 9: UPKD – SUSTAINABILITY CRITERIA 110

ANNEX 10: TRANSFER OF ASSETS TO USPKD 111

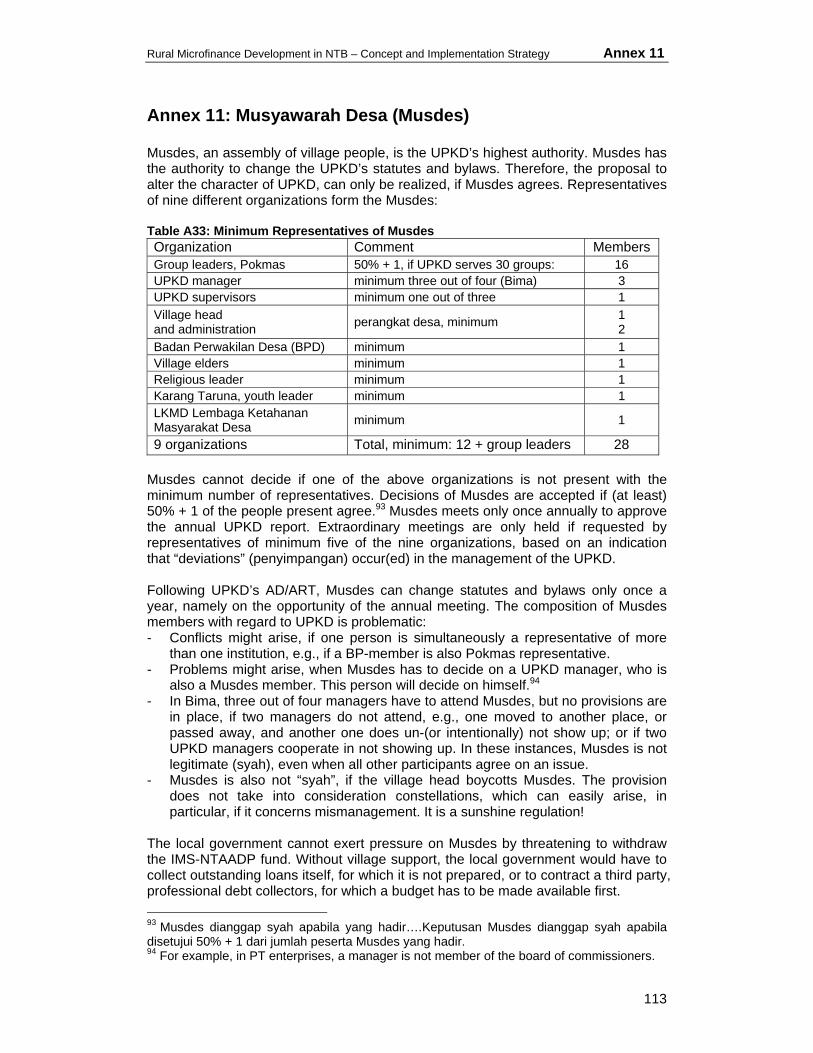

ANNEX 11: MUSYAWARAH DESA (MUSDES) 113

ANNEX 12: BADAN KREDIT DESA (BKD) 114

ANNEX 13: “THE YOGYAKARTA COMMUNIQUÉ 2004” 115

REFERENCES 117

Currency Equivalents (as of September 2005) Rp Rupiah Rp m Rupiah million Rp b Rupiah billion USD1 = Rp10,300

Disclaimer

The authors attempted to provide useful and accurate information wherever possible. The authors had to rely on statistics, information gathered and processed by other institutions, and on the statements of respondents, most of which were not further verified. Some information was fragile and required skilled interpretation.

The authors judged the information based on their professional experience very carefully. They believe that the findings presented in this report reflect sufficiently accurate the conditions in the institutions and the environment in which they operate.

This report also contains personal opinion, both of the authors and opinions of various contributors, which are offered in good faith. They are not necessarily the opinions of Bank Indonesia, GTZ or the Government of Nusa Tenggara Barat.

Abbreviations 5C Character, capital, conditions, collateral, capacity (Loan assessment criteria) AD Anggaran Dasar (Statutes) ART Anggaran Rumah Tanggah (Bylaws) BI Bank Indonesia BKD Badan Kredit Desa BMT Baitul Mal Ta’mil (Non-bank financial institution based on syariah/Islamic principle) BP Badan Pengawas (Supervisory board of UPKD) BPD Bank Pembangunan Daerah (Regional Development Bank) BPR Bank Perkreditan Rakyat (People's Credit Bank or Rural Bank) BRI Bank Rakyat Indonesia (Commercial bank, 51% state-owned) BUMD Badan Usaha Milik Daerah (Province/district-owned enterprise) BUMN Badan Usaha Milik Negara (state-owned enterprise) CAMEL (bank rating or assessment by:) capital, assets, management, earnings, liquidity CDF Community development facilitator CGAP Consultative Group to Assist the Poorest FI Financial institution GDP Gross Domestic Product GoI Government of Indonesia GoNTB I / II Provincial / District Government(s) of Nusa Tenggara Barat (PemDa I / II) GTZ Gesellschaft für Technische Zusammenarbeit IMS-NTAADP Inisiatif masyarakat setempat (local people’s initiative) of NTAADP KSP Koperasi Simpan Pinjam (Savings and credit cooperative) KUD Koperasi Unit Desa (Village cooperative) KUT Kredit usaha tani (Farm enterprise loan) LKP Lembaga Kredit Pedesaan (Rural credit institution) MF Microfinance MFA Microfinance advisor, field worker, facilitator MFI Microfinance institution MoA Ministry of Agriculture MoF Ministry of Finance MoHA Ministry of Home Affairs MSE Micro small enterprise MSME Micro small medium enterprise Musdes Musyawarah desa (Village consultation) NPL Non-performing loan NTAADP Nusa Tenggara Agriculture Development Project NTB Nusa Tenggara Barat

PDM-DKE Pemberdayaan Daerah dalam Mengatasi Dampak Krisis Ekonomi (Local empowerment by overcoming the impact of the economic crises)

PHBK Proyek Hubungan Bank dengan Kelompok Swadaya Masyarakat (Project linking banks and SHG)

PKS-BBM Pengganti Kompensasi Subsidi Bahan Bakar Minyak (Compensation for fuel subsidy)

PNM PT Permodalan Nasional Madani (PNM) (State-owned financing agency in charge for BI liquidity financed program loans)

PPK Program Pengembangan Kecamatan (Sub-district development fund) ProFI Promotion of Small Financial Institutions SCC Savings and credit cooperative SCG Savings and credit group SHG Self-help group, savings and credit group SME Small medium enterprises SMoCSME State Ministry of Cooperatives and small medium enterprises SUTA Sistem Usaha Tani, Agriculture loan scheme of UPKD

UEP Usaha Ekonomi Produktif Ternak (Productive husbandry business, UPKD Loan scheme)

UEPT Usaha Ekonomi Produktif (Productive business, a UPKD Loan scheme) UPK Unit Pengelola Keuangan (Financial management Unit of PPK project) USP Usaha Simpan Pinjam (Savings and credit business of multi-purpose cooperatives

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

i

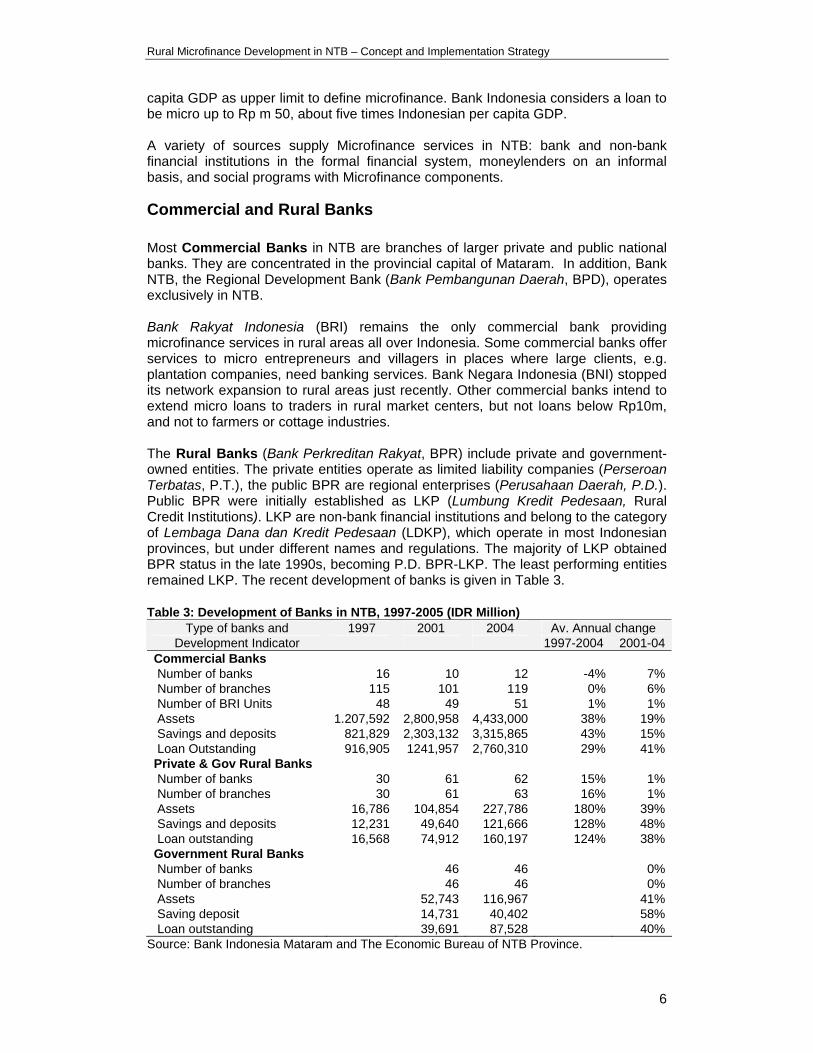

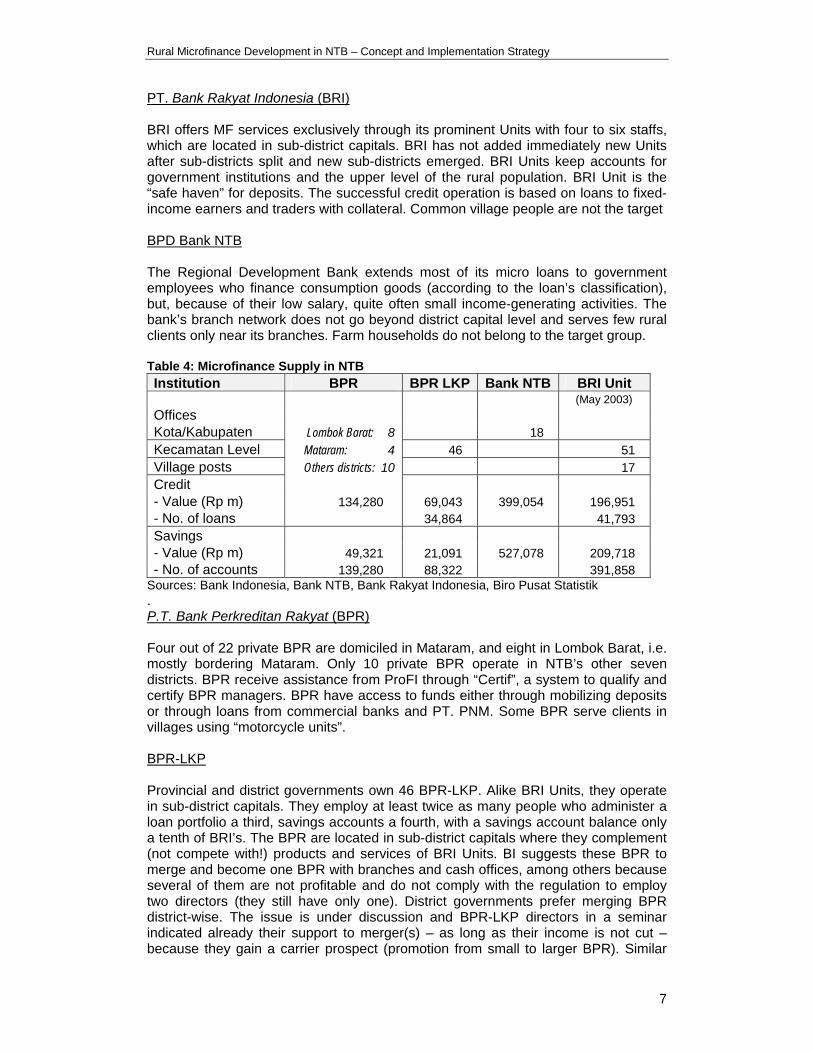

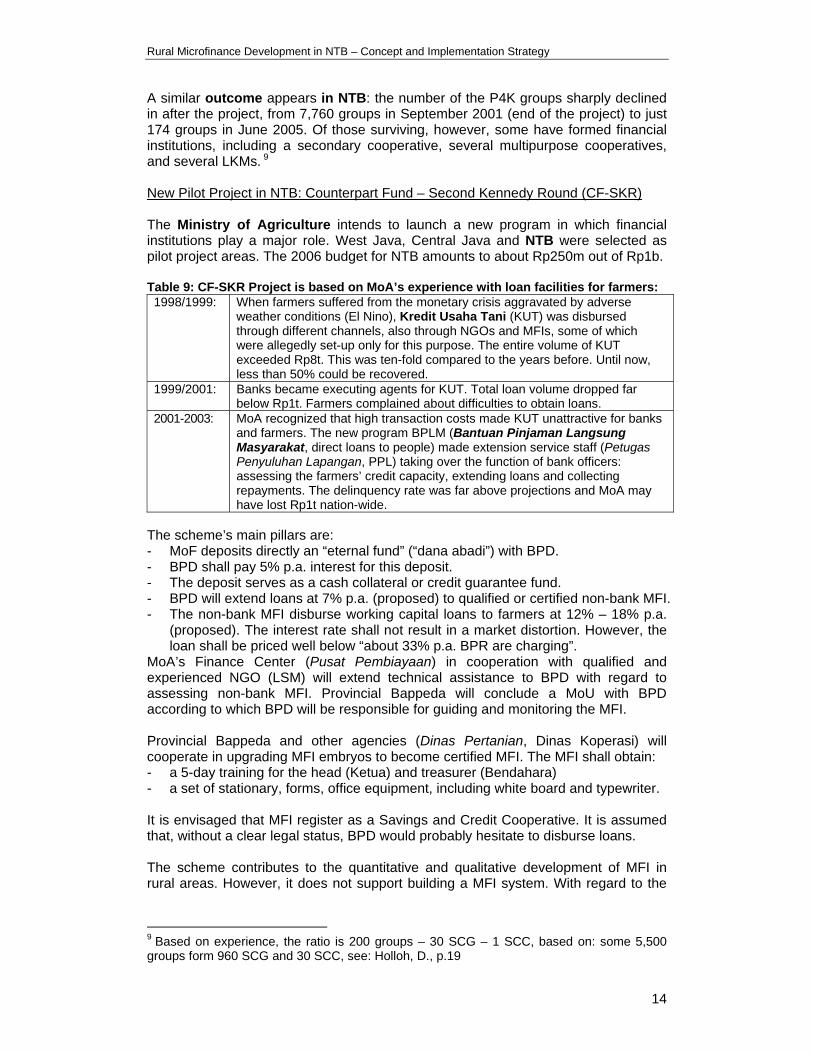

Executive Summary In May 2005, the Government of the Province of Nusa Tenggara Barat (NTB) and ProFI – Promotion of Small Financial Institutions (a joint project of Bank Indonesia, Ministry of Finance, and GTZ) signed Agreed Minutes concerning the Microfinance Development Project in NTB. NTB belongs to the provinces with below average GDP, and has the second-lowest Human Development Index in Indonesia. Its 4.2 million inhabitants live on the islands Lombok (almost 3m) and on Sumbawa (about 1m). They earn income mainly from agriculture, fishery, and from working abroad. The rural microfinance market analysis compares current demand and supply to identify gaps. The demand side analysis draws on a survey of 90 households in all administrative units of NTB. The survey found that a substantial proportion of the households save their excess incomes. Large savings are generally placed with commercial banks, while small savings are generally placed with nearby non-bank financial institutions (particularly UPKDs). More than half of the households regularly borrow from financial institutions, particularly from UPKD and credit cooperatives. Most loans from these MFI are small, with sizes less than IDR 2 million. A few of the households also borrow from informal sources, in particular friends and family. Child education is the main purpose of saving, whereas the main purpose of borrowing is working capital. The households generally accept that financial services apply interest, and that borrowers should repay their loans. The households suggested that microfinance could be improved through demand-driven and convenient services, and better marketing of available services. The survey concludes that household demand for financial services indicates a large potential for savings mobilization and effective financial intermediation. The households are generally accustomed to saving and the application of interest rates on financial services. These provide the basis for the use of the financial system approach for further development of the rural-microfinance sector in the province. Based on the sample, the potential demand of rural households in NTB for institutional saving and loan services has been estimated very roughly. It amounts to between 275,000-288,000 saving deposit clients, and between 372,000-390,000 loan clients, including almost 40% of the households. Microfinance supply comes from a broad range of sources. Commercial Banks are centered in Mataram, the capital with about 700,000 inhabitants. Two banks are leading with regard to their presence in district capitals, i.e. Bank Rakyat Indonesia (BRI) and Bank NTB, the regional development bank owned jointly by the province and district governments. BRI’s branches do not offer micro loans and Bank NTB only to fixed income earners (government employees) and selected urban clients. BRI’s microfinance outlets are 51 BRI Units in about every second of the 100 urban and rural sub-district capitals. BRI Unit clientele are fixed-income earners and in particular traders with bankable collateral. Also on sub-district level, NTB’s government operates 46 Rural Banks, BPR-LKP. BPR-LKP provide complementary financial services by extending smaller loans with more lenient collateral requirements. These institutions reach village people through PHBK (loans to groups), but these loans contribute to only about 3% of the loan portfolio.

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

ii

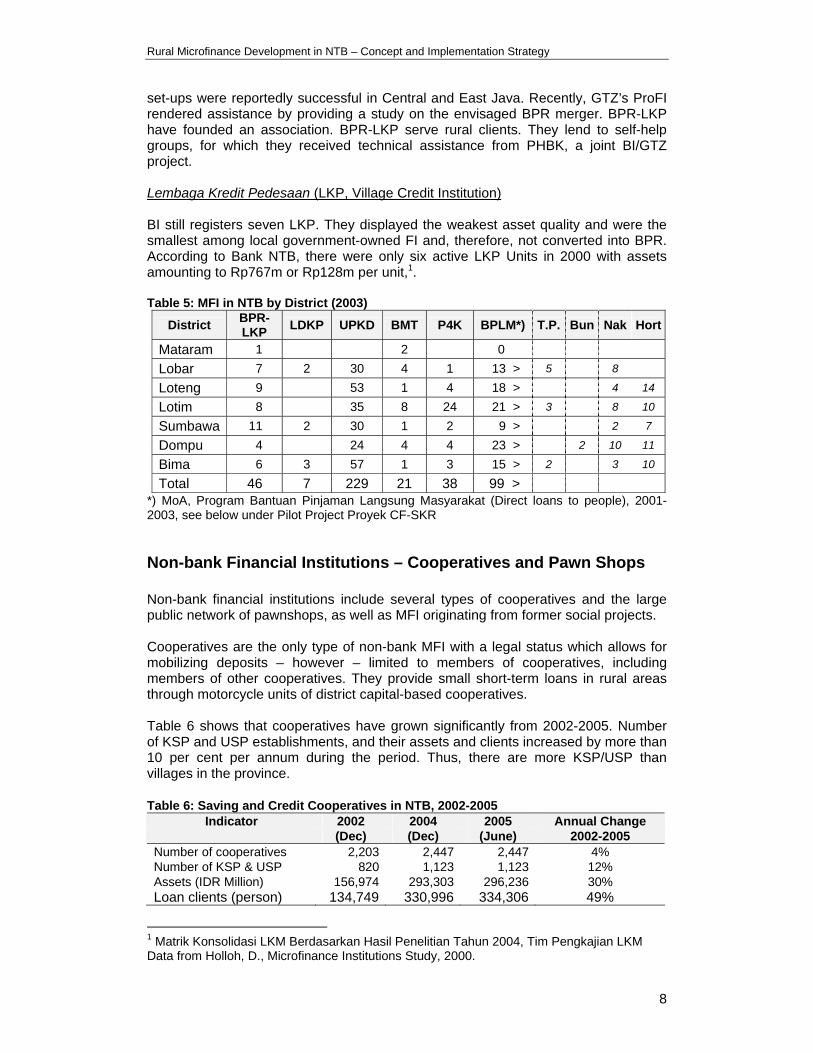

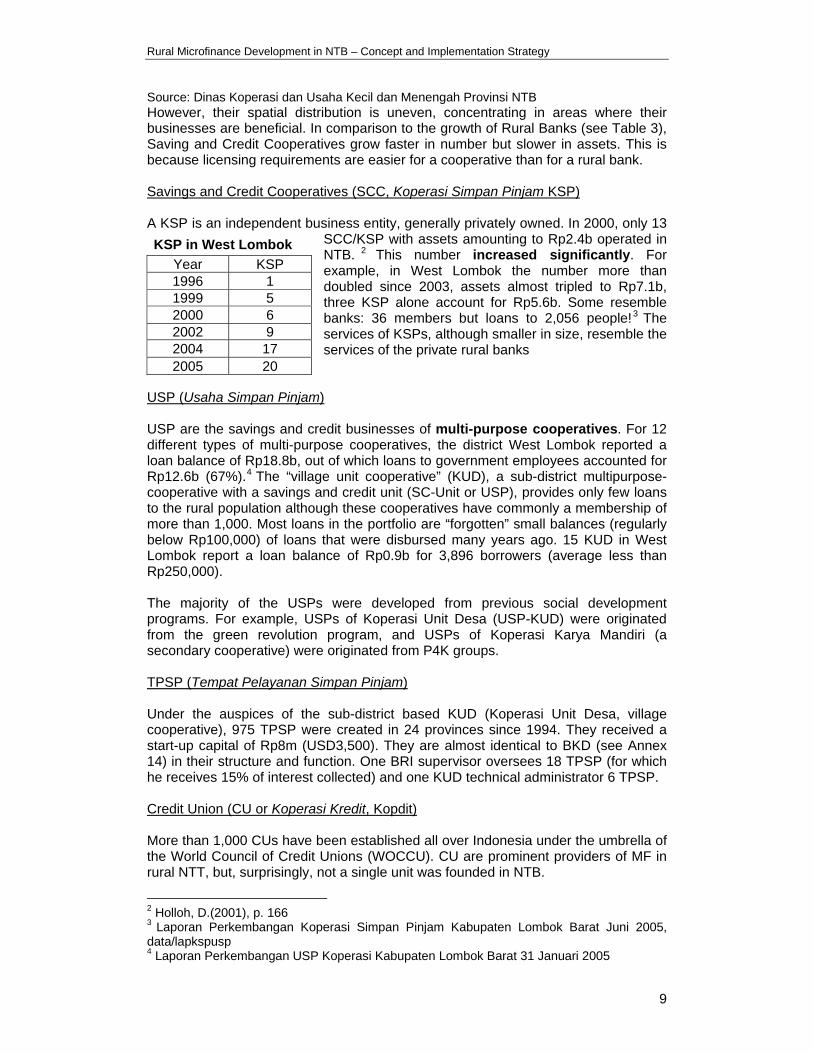

The cooperative sector recorded substantial growth if measured by the number of institutions and their balance sheets. In particular savings and credit cooperatives (SCC) have an urban bias. Many government and private enterprise employees are members of a cooperative just for the purpose to obtain a loan. In rural areas, SCC are known as moneylenders for short-term loan with daily repayment. The multi-purpose village cooperatives (KUD), also in sub-district capitals, do not have sufficient funds just when farmers would need them most. Recently, “members” founded a number of SCC with a prohibitive high membership fee (and effective interest rates twice those BRI Units charge), so that these cooperatives appeared like a privately-owned BPR. They reported a demand, also from farmers, in excess of their capacity. In contrast to NTT, credit unions are not established in NTB. Also in contrast to NTT, only very few NGO support villagers with microfinance for self-help groups (SHG). SHG are popular in NTB though: the Kecamatan (Sub-district) Development Program (PPK) supports more than 500 SHG in 23 sub-districts. Many people enjoy the quick and uncomplicated services of moneylenders, who help with their loans settling installments with banks and MFI. All major national social programs with microfinance components were implemented in NTB: MoA experienced low repayment rates for its KUT and BPLM programs. The P4K facility was more successful until recently, but it is not anymore prolonged. Revolving funds (IDT, Inpres Desa Tertinggal; PDM-DKE, an economic crisis assistance program) turned out to be problematic as many groups were just arranged only to receive “capital assistance”. They easily dissolved. PKS-BBM, a working capital support project for cooperatives and Microfinance Institutions (MFI), implemented by the State Ministry for Cooperatives and SME (SMoCSME) between 2000 and 2003, incorporated training, monitoring and supervision by commercial banks for fund recipients. The banks, notably BRI and BPD, did not fulfill their contractual obligations, although MFI even paid a fair amount. The project was seemingly less successful and the funds, which were planned to remain with the MFI, have to be repaid in ten annual installments. The Kecamatan development project presents a unique feature, namely UPK (Unit Pengelola Keuangan, finance management unit) as a second-tier or apex organization providing loans to SHG and MFI. Preliminary figures indicate a high loan quality but also very high administrative cost. Projects and programs assist only temporarily and often only locally. Most MFI do not provide loans to villagers, because of the distance, or they provide a facility that villagers cannot use for their businesses. UPKD close both gaps, the distance gap and the financial gap: they are village institutions and they offer three loan products that are in demand: loans from Rp0.2m to Rp2m, no monthly installment, maturities of 4 to 12 months, and lenient collateral requirements. UPKD have a profound transaction cost advantage for both the lender and the borrower. However, UPKD do not close the gap for deposit services. The 245 UPKD in NTB are unrivalled in NTB in their number as a group of similar MFI. 214 UPKD were founded 1999 as non-bank, non-cooperative MFI to administer some Rp45b funds from IMS-NTAADP, the World Bank financed Nusa Tenggara Agriculture Area Development Project that started 1996. This poverty-oriented project assisted villages in backward districts. IMS stands for “inisiatif masyarakat setempat”, local people’s initiative. People empowerment, decision and implementation of investments, and control by villagers through joint liability groups and Musdes, a village forum, became prominent project features. District

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

iii

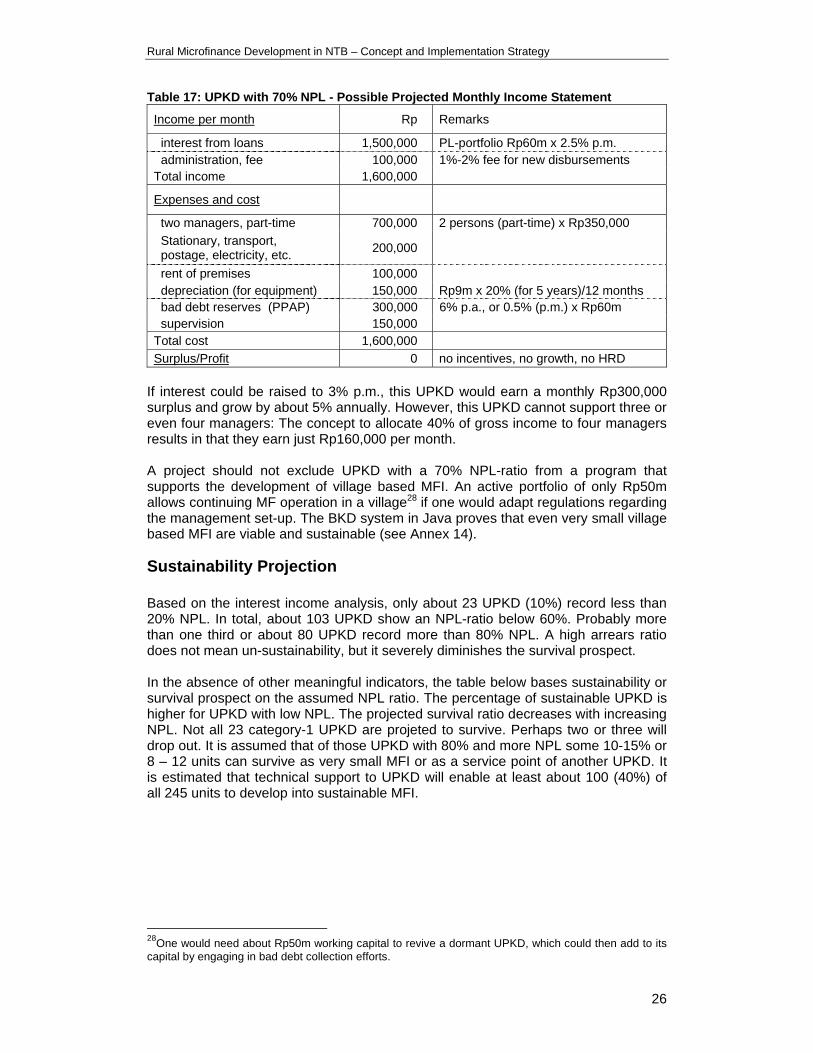

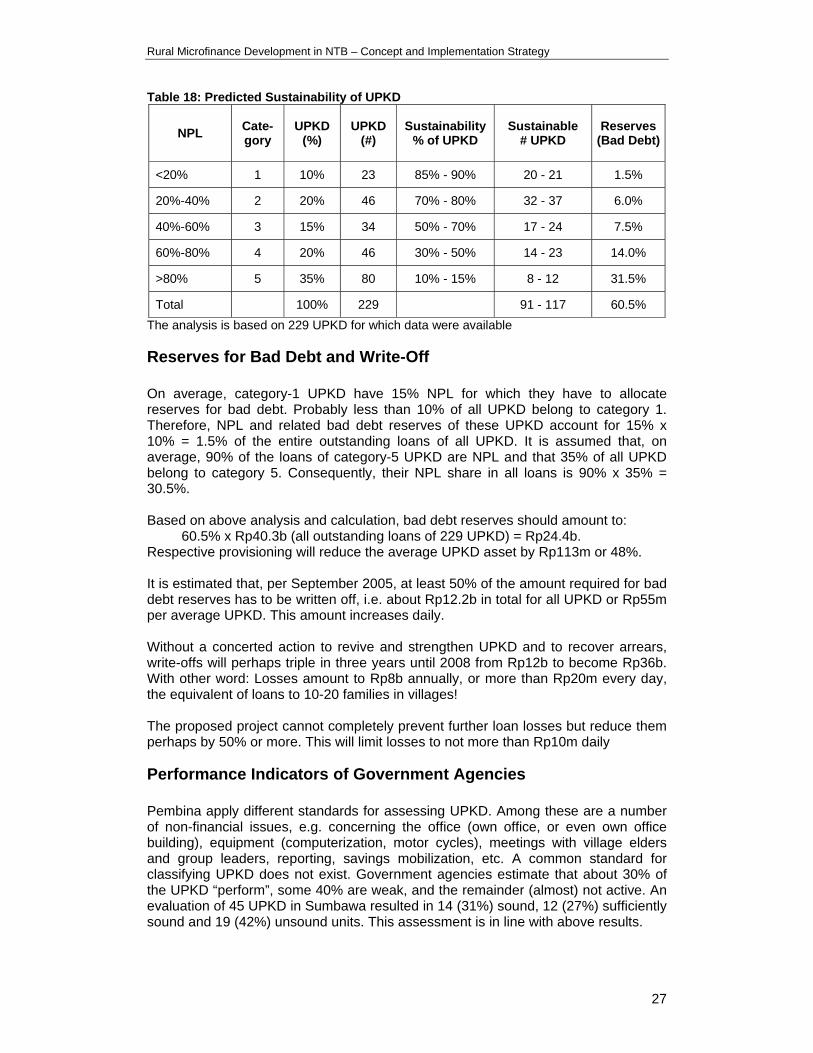

governments financed the establishment of at least 30 additional UPKD village financial institutes. Until its closure in September 2003, IMS-NTAADP trained UPKD management (three or four managers, and a supervisory team (Badan Pengawas, BP), in administration, bookkeeping and loan appraisal. Monthly reports were submitted to district Bappeda, the implementing agency. Already at that time, quite a number of UPKD reported increasing arrears, averaging at 17%. In 2005, all respondents reported further deteriorating conditions of most UPKD. It is difficult to describe this development with figures, as an increasing number of UPKD, in Sumbawa more than 50%, stops reporting. However, this does not always mean discontinuation of activities. There are significant differences among UPKD even in close vicinity, concerning performance, assets, and income, although they were guided by the same institutions and facilitators. Flourishing UPKD can be found even in dry areas, which are commonly considered very poor. In 2005, the average UPKD reports assets of Rp235m, almost the same as in 2003. The average loan portfolio of Rp180m is shared among about 50 groups with 500 members. Analyzing (fragile) interest income data yields an average of Rp110m non-performing loans, a 60% NPL-ratio. In the absence of reliable figures, it is assumed that at least Rp55m (>25% of all loans) are not at all recoverable. In total, some Rp12b of the original Rp40b loan fund have certainly to be written off. About 40% of all loans went repeatedly to (very) poor people. Many simply do have not the means to repay. These loans need to be finally written off. The remainder, Rp55m, can presumably be recovered through various measures, including loan reconditioning or seizing assets, political will and support provided. Only few UPKD practice appropriate bad-debt provisioning. The managers contribute decreasing loan income to seasonal influence, deferred payments which ”will be paid soon”, and to the social orientation, i.e. prolongation of loans without interest payment. UPKD contribution to the village coffers amounts to perhaps 1% of the loan fund, often it is a donation to the village head. A high NPL-ratio does not immediately endanger the viability and sustainability of a UPKD – although, of course – a lower NPL-ratio increases sustainability prospects. If stripped of its bad debt, UPKD are still about twice the size of Java’s quite sustainable BKD (Badan Kredit Desa, village credit board). The remaining performing portfolio of between some Rp60m to Rp100m generates sufficient income to cover expenses (not costs!), which are flexible to a very high degree. As long as they operate, UPKD have much better chance to recover bad debt and increase the performing loan portfolio. Calculations, based on NPL-assumptions and different sustainability ratios, predict that 91 to 117 UPKD have a realistic survival prospect, if political will and assistance are provided. Most reasons for increasing NPL and decreasing income are related to the nature of UPKD as a former project institution. When the project closed, UPKD management lost (also moral) support from facilitators, and debtors start questioning the origin and nature of the fund and the legality of the institution from which they received a loan. UPKD managers were burdened with too many and too conflicting aspirations and they were neither sufficiently prepared for this, nor had many actively applied for a management position in the UPKD.

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

iv

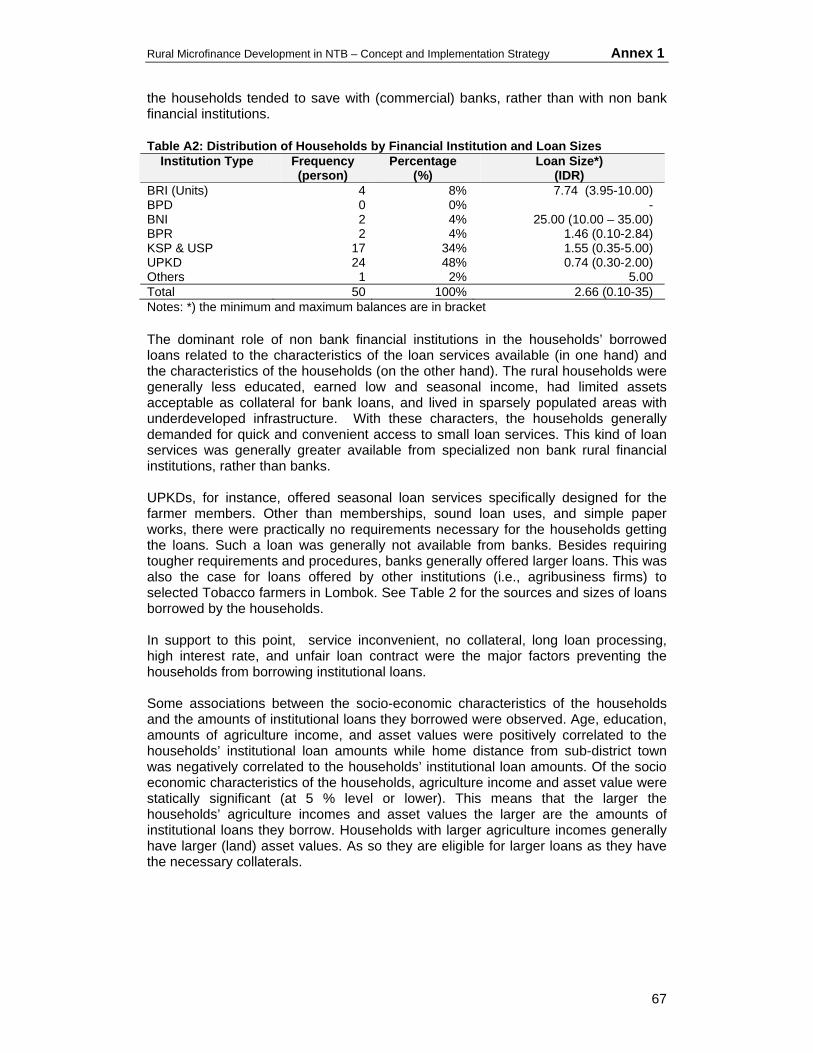

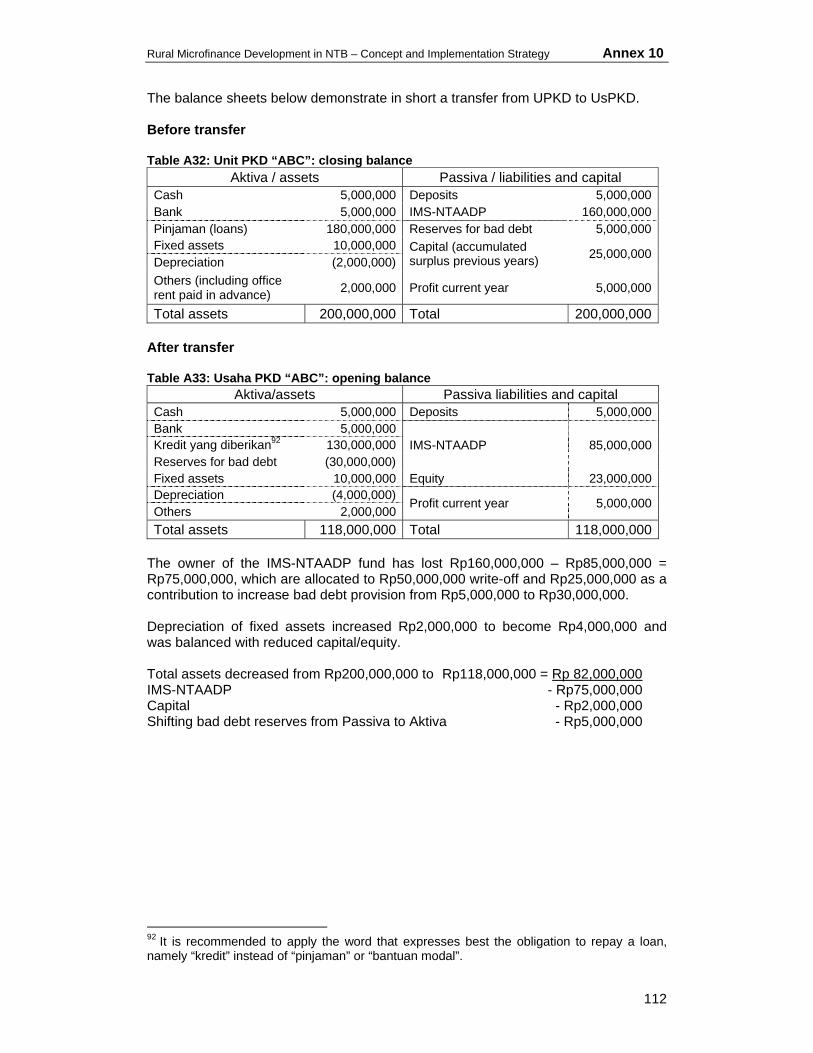

Another important reason for increasing NPL is weak credit risk management: non-prudential loans to people without diversified sources of income, who cannot offer “the second way out”, and to people who, as fixed income earners, are anyway indebted. The managers could not prevent this: they complied with the request of the project and with the request of their fellow villagers. Largely, supervision “by the people” failed. The conflict is perhaps best described by BP members who received loans and defaulted. UPKD managers and BP members cannot be dismissed because auf missing regulations. IMS-NTAADP financed and developed a microfinance infrastructure in rural areas of NTB: working capital, fixed assets, rented offices, human resources development, products and marketing channels. Without further attention, the number of NTB’s active UPKD-MFI will decrease by about 3 or 4 per month. Financial losses due to worsening loan portfolio quality alone are estimated to amount to Rp20m every day. The question is, whether and how these losses can be prevented or at least substantially reduced. Fortunately, most of the infrastructure is still in place: people in government agencies monitoring UPKD development, statutes and bylaws, UPKD offices, records, working capital and fixed assets, and the managers. The proposed new approach to UPKD development departs from the identified weaknesses, resulting from the UPKD nature as a project institution with exclusively social orientation. Its statutes and bylaws, the legal foundation, are entirely unsuitable for post-project times. Consequently, a follow-up project has to focus the attention to one single objective, the sustainability of UPKD. The vision for UPKD is proposed as: “increasing the welfare of village households through offering its services and products, and contributing to the community through its profits”. The corresponding UPKD mission shall be: “the sustainable provision of financial services and products, which are adapted to the demand of village-community members and based on prudent procedures”. It is suggested to change the name of the institution: “Unit” should be substituted by “Usaha” (Company, Business) to express the new orientation: generating profits for the village community. Simultaneously, social tasks should be transferred to the village government. This allows UsPKD (Usaha Pelayanan Keuangan Desa, Village Financial Services Company) to act market-oriented and increase interest rates to get closer to market rates. The village government decides, who will be eligible for interest subsidy and use UsPKD profits, i.e. only the surplus and not the substance, to finance (transfer to UsPKD) this subsidy. People, who can afford higher interest payments, contribute to more profits for more village development and assistance to the needy. Financial transparency and village solidarity can become reality. It is essential that UsPKD become profitable entities because only strong and profitable financial institutions can gain the community’s confidence and grow. People repay loans when the prospect of a larger follow-up loan looms. In particular it is proposed that: - The transfer of assets from Unit PKD to Usaha PKD includes verification and re-

assessment of all loans. They amount to about 80% of UPKD assets. The real value of many loans has to be established, which is often much lower than the nominal value or the book value. One cannot create sound financial institutions without transparent accounting. UPKD cannot carry past project burden. It is expected that loan verification will meet reluctance or even resistance from various persons. Government assistance on all levels is required for this task.

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

v

- The village shall 100%-own the new UsPKD. The ownership of IMS-NTAADP funds needs to be clarified before deciding on a legal status of UsPKD. The role of district governments in a board of commissioners will also depend on IMS-NTAADP fund ownership. A law on MFI or implementing regulations on BUMDES (Badan Usaha Milik Desa, village-owned enterprise) could provide options for UsPKD legality. Cooperatives are less suitable: they member-oriented companies from which their members benefit, but not the community.

- The IMS-NTAADP loan fund shall become a long-term sub-ordinate loan to UsPKD, which strengthens equity, a key feature when UsPKD look for finance to expand their business.

The objectives of the “Regional MF Development in NTB” project, as laid out in the Agreed Minutes, are:

a) improve the quality of MFI services; b) increase the number of sound MFI; c) create a conducive environment by means of regulation and supervision; d) increase the cooperation between MFI and other financial institutions; e) increase the capacity of MFI to access capital from various sources.

Strengthening UPKD will contribute to achieving these objectives. a) Service quality: On average, UPKD mobilize Rp10m deposits, most of all

compulsory fees from borrowers. UPKD have not been active or inventive in attracting deposits, among others due to a Bank Indonesia regulation that restricts mobilizing deposits to banks. On the other hand, people are reluctant to deposit funds when they question the sustainability of the MFI. UsPKD might cooperate with a bank. Regarding lending, most people want access to individual loans with individual repayment schedules instead of the current group loans.

b) Increasing the number of sound MFI has two components: the number of

institutions and the quality, or soundness of MFI. Uplifting less sound MFI to become sound MFI counts also. Unfortunately, improvement from unsound to less sound does not. District governments intend financing the formation of new UPKD. It is believed that some 20 of these MFI will be added in three years. Whether the project will succeed increasing the number of sound MFI can only be answered once the initial number of sound MFI, here: UPKD, is known, which is certainly below 10 if measured by BPR standards. The standard for a “sound” non-bank non-cooperative MFI needs to be developed. However, an assessment based on the five CAMEL rating criteria appears to be suitable for UPKD, too. “C”apital rating, derived from the capital adequacy ratio (CAR), increases when

bad loans are removed from the balance sheet, when IMS-NTAADP funds becomes a sub-ordinate loan, and if part of this loan is converted to equity.

“A”ssets consist mainly of the loan portfolio. Renewal and rescheduling of overdue loans are methods to improve portfolio quality. A “sound” portfolio is also a result of suitable loan products and conditions, i.e., when loan contracts or products are adjusted to the borrower’s cash flow and risk structure, such as loans that allow flexible repayment.

“M”anagement rating improves through introduction of manuals and other written procedures, implementation of internal supervision and control mechanisms. Managers need training to comprehend and apply these tools.

“E”earnings can be doubled by enforcing interest payments for the time an installment or loan is overdue and by introducing penalties for late payments.

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

vi

The income will again double when UPKD management applies interest conditions similar to those of savings and credit cooperatives in rural areas. Earnings increase when costs decrease but only few high income UPKD can think about decreasing expenses. Costs for bad debt provisioning decrease because of prudent lending.

“L”iquidity is, in general, not a particular UPKD concern. Deposit withdrawals are predictable or negligible. Other expenses can be deferred and negotiated.

Summarized, there is an extensive field of activities to improve UPKD “soundness”. As a best guess, if one would qualify the ten best performing UPKD as “sound” today, some 20 would be sufficiently sound, 40 less sound and 160 unsound. It is expected that an intervention would see after 2 to 3 years about 40 (+30) sound UsPKD, 50 (+30) sufficiently sound, 65 (+25) less sound and 95 (-65) unsound. These 95 MFI are estimated to drop out or remain “dormant”, among others because already the portfolio verification fails.

c) Regarding regulations, three issues need attention: (i) for UsPKD incorporation

still missing procedures for BUMDES, and the Law on MFI, which will impact the formulation of new statutes and bylaws; (ii) regulations allowing village MFI to accept deposits (probably a chapter in a Law on MFI); and (iii) regulations and clarifications regarding ownership of the IMS-NTAADP fund, including write-off procedures. The project left UPKD with a set of “sunshine” rules and regulations, which might have been applicable for the project implementation, but become an obstacle for UsPKD development. It is proposed to prepare decrees for portfolio verification, and for temporary UsPKD statutes and bylaws. The case should be re-opened after a Law on MFI and regulations concerning BUMDES were issued. Without a regulation on write-offs it seems not possible to increase the number of sound MFI, unless only the sound loans are transferred to UsPKD and the unrecoverables remain “UPKD assets”. This report discusses supervision extensively because the success of UsPKD hinges on people having access to means that they do not own in a society that values family and neighbor bonds, and respect and obedience to superiors much higher than temporary (project!) employment regarding administrating anonymous funds. The presence of supervision, i.e. internal audit, strengthens the morale of managers. UPKD performance would be worse without supervision by BP-teams. However, their strength, i.e. being embedded in and knowing the village people, is also a major weakness. Supervisors are fellow villagers, therefore often not neutral, and shy conflicts. For many the task is too demanding, for others too irregular (once in three months). No one guides, supervises, controls, or monitors supervisors. Consequently, the formation of full-time semi-professional supervisor teams on district level, an externalization of internal audit, is recommended. About 15 to 25 specialized and – over time - experienced and full-time employed persons can perform this task better than the 735 persons can now. On provincial level, a professional coordinator shall guide, train, and supervise the performance of these teams. The expenses for financing supervision will increase substantially to about Rp500m annually. UsPKD can carry these expenses and they are very low compared with costs for proper bad debt provisioning amounting to probably more than Rp5b at present.

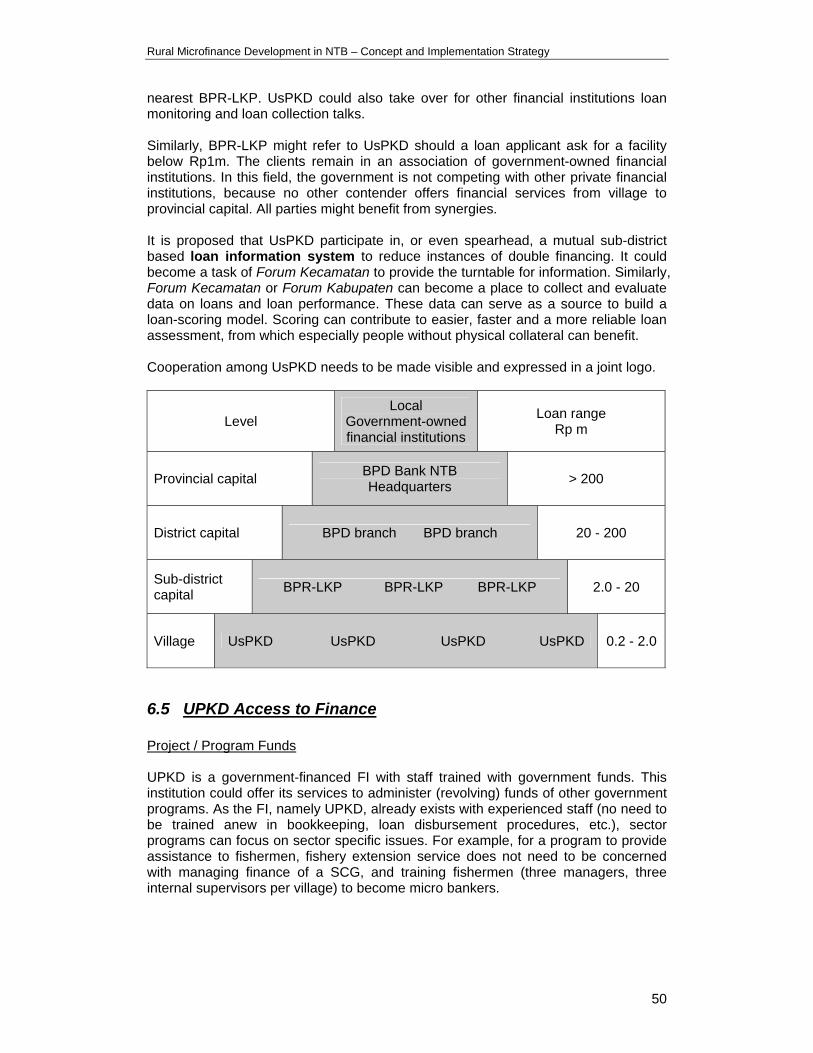

d) BPD Bank NTB, BPR-LKP and UPKD have a common bond in that they are

owned by the Government of NTB. Their products and the area they are covering complement each other. UsPKD could serve as a prolonged arm, e.g. as a

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

vii

savings collector for the banks. For UsPKD clients it would be attractive to know that their FI is not entirely standing alone but part of a province-wide financial system. In addition, cooperation among UsPKD (Forum) should be enforced, not only regarding supervision, but also in fields such as developing simple information and scoring systems.

e) UsPKD can provide services as cashier of the village government and its

deposits. They could offer their services to administer financial components of government programs. With an immediate unmet loan demand of about Rp350m per village UsPKD may attract the attention of lenders for whom it is impossible to tap this market segment directly. UsPKD cannot offer physical collateral. They have to offer a performance record and this is a main reason why UsPKD managers have to learn to monitor the CAMEL rating of their UsPKD.

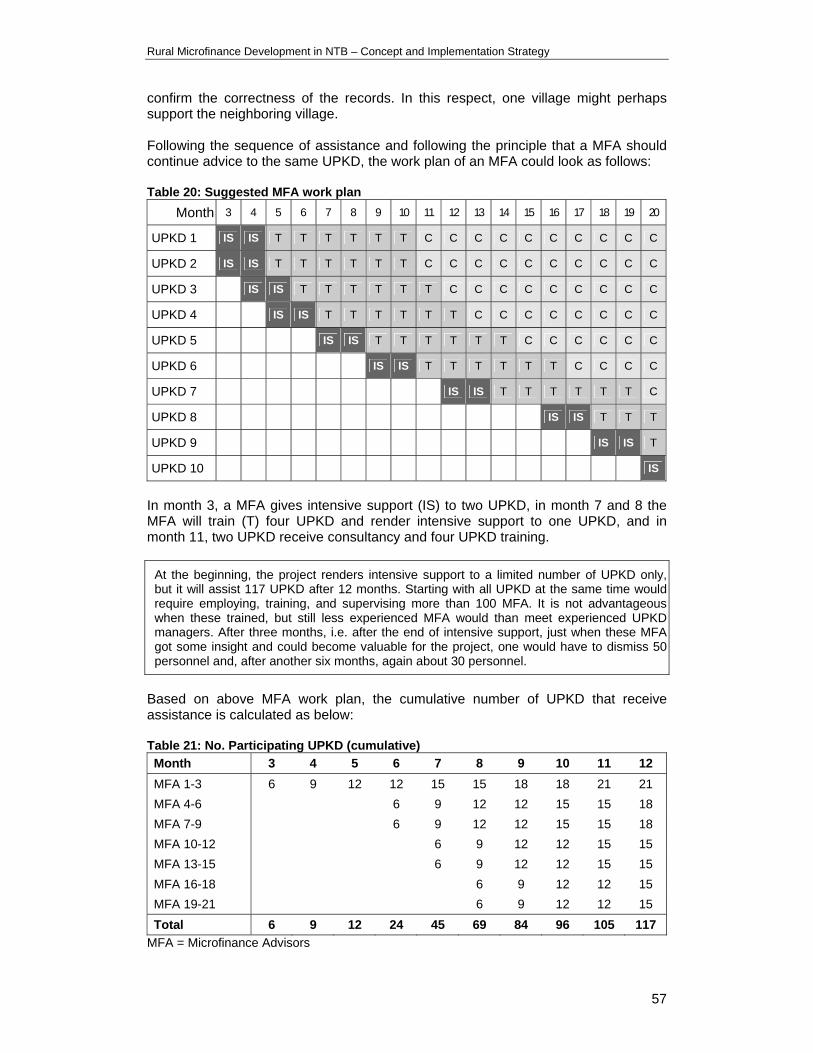

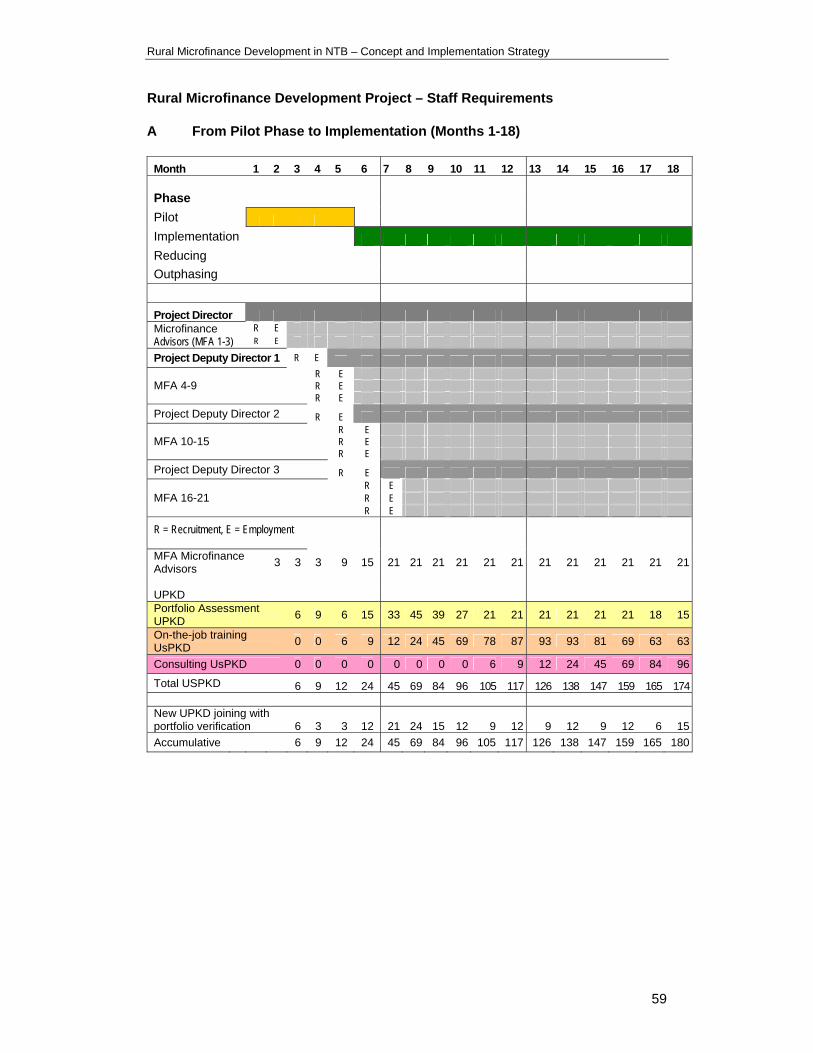

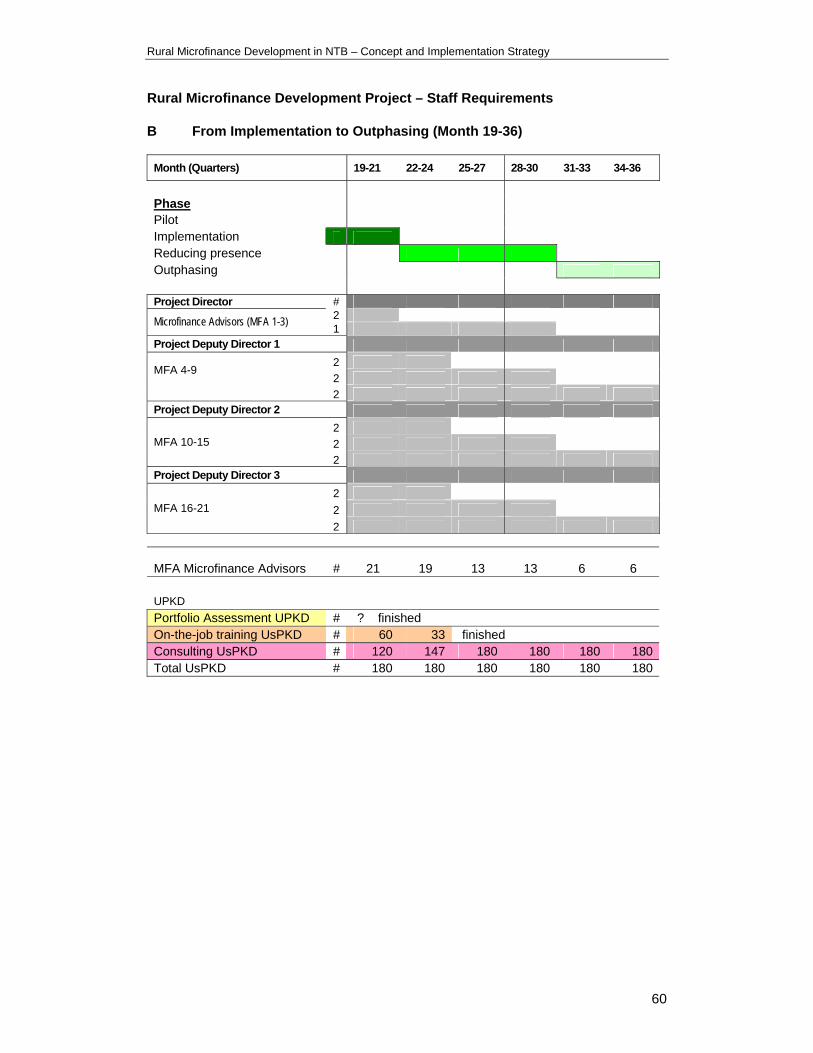

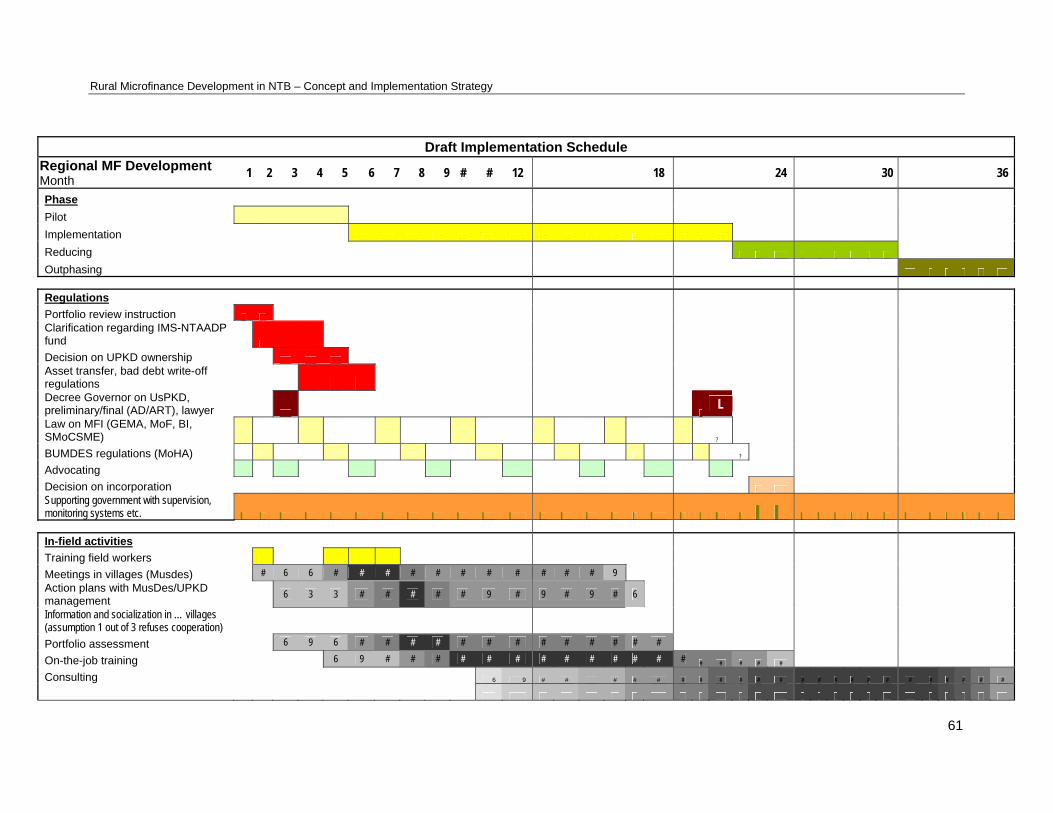

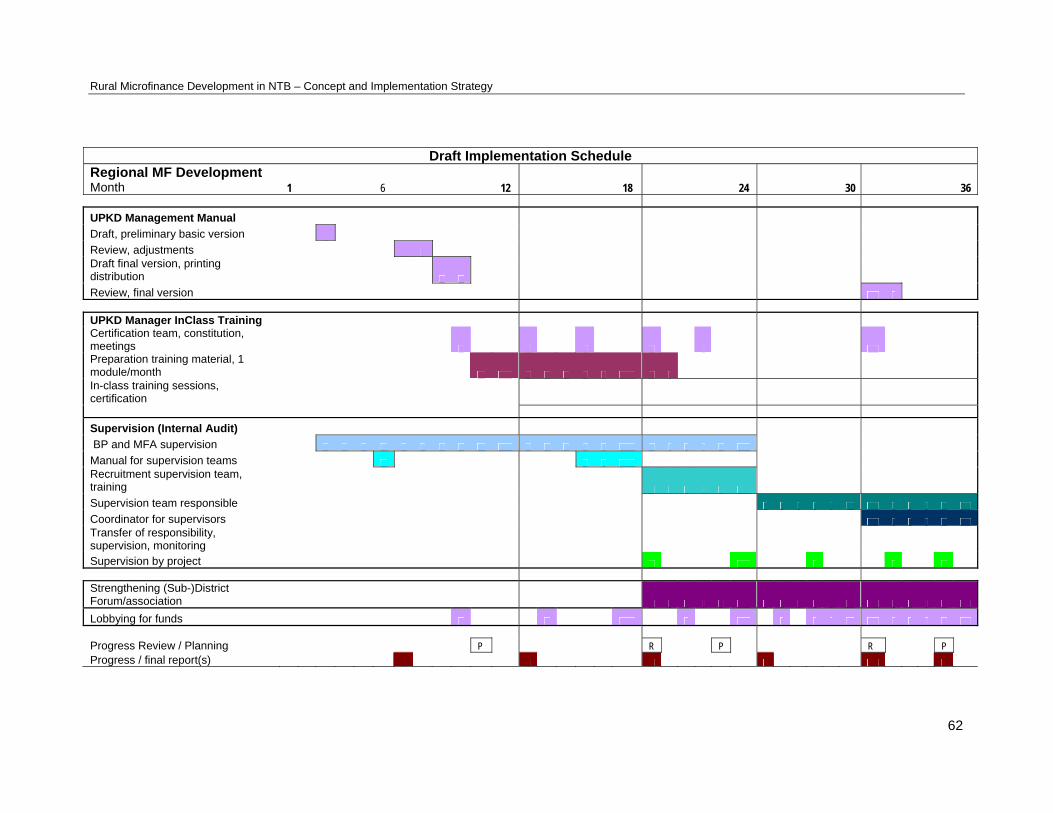

Project implementation includes several UPKD support measures. The sustainability of UsPKD shall be achieved through a sequence of following measures: (i) asset verification to increase transparency (2 months), (ii) on-the-job training (business-orientation, 4-6 months), (iii) consultation (problem solving, 6-12 months), (iv) co-operation among MFI, especially regarding supervision, and with other FI. The sequence of institution building will be accompanied by provision of manuals, in-class training, and certification. The project will have a pilot phase, including preparation, pilot-testing of asset verification in selected villages and clarification of IMS-NTAADP fund ownership. The project will be continued if these activities have been implemented successfully. At the beginning of the pilot phase, consultations with GoNTB in the Forum of Regional Microfinance Policy (FoMFIDa) aim at an agreement about common objectives and the basic project design. A Project Director will use a preparation phase of two months to conclude cooperation agreements with selected village governments. This is one of the project’s most crucial points: An environment that does not support asset confirmation, i.e. transparency, is not conducive. Time should be allowed between announcing asset verification and the actual start to give some people the opportunity to settle their overdues. Latest in the third month, three Microfinance Advisors (MFA) shall begin portfolio verification in two villages each. Successful portfolio verification is one of the preconditions for asset transfer from UPKD to UsPKD and further assistance. Simultaneously, GoNTB will clarify the ownership of IMS-NTAADP funds and develop guidelines on handling bad debt and write-off procedures, which constitutes the other precondition for granting further assistance after the test phase. MFA will add a third and fourth support village the following months. The project should have gained sufficient experience after three months of pilot-testing asset verification and cooperation with 12 villages to decide on and design the multiplication in other districts. Provided the pilot phase was successful, i.e. asset verification has been conducted in at least 12 villages, and ownership of IMS-NTAADP funds has been clarified and allows for village-owned MFI development, the project will begin scaling-up. Based on the pilot experience, it will be decided how many new MFA and Deputy Project Directors would be recruited to continue the UsPKD institution building sequence of asset verification, followed by on-the-job training, consulting and parallel training. Up to 3 Deputy Directors and 21 MFA may be needed in total if UsPKD development realizes its full potential. Before new MFA would be hired, co-financing during project time and cost coverage after out-phasing need to be clarified to ensure sustainability.

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

viii

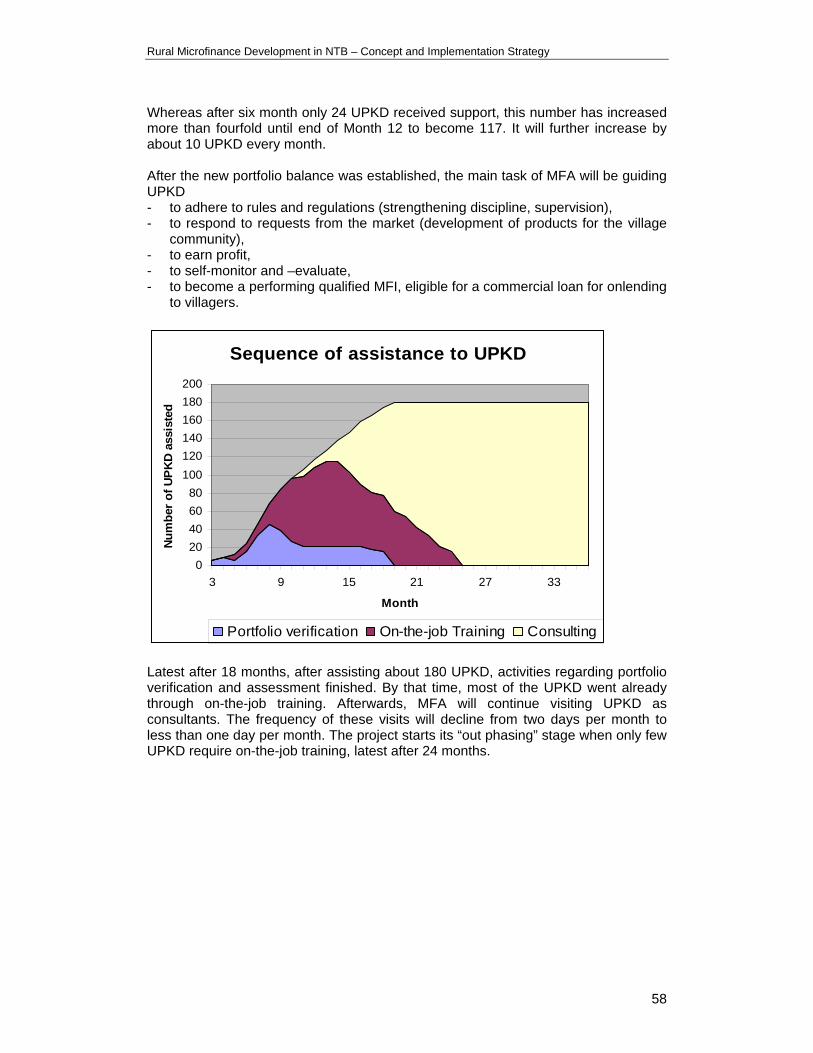

The proposed project implementation will see an overlapping of these sequences because it starts in a pilot area and will be multiplied in stages only after having gained experience and made necessary adjustments. It is estimated that asset verification of one UPKD employs a MFA for about 7-10 days per month, whereas on-the-job training requires only 2 to 5 days presence and consulting just 1 to 2 days a month. Therefore, one MFA will assist simultaneously, for example, one UPKD with asset confirmation, three UsPKD with on-the-job training, and another three with consulting. The project directors themselves have to visit UsPKD in order to confirm and learn first hand about the UsPKD performance and their problems, and in order to assure that the MFA fulfill their duties, among others regular internal audits until the supervision teams take over this task in the project’s second year. It is envisaged that during the second year scheduled in-class training takes place and scheduled visits by supervision teams start. The number of MFA can be reduced latest starting at the beginning of the third year. The project will concentrate on developing and strengthening the Forum or association towards supporting a certification system for managers as well as for institutions. It will also be concerned with attracting funds to performing UsPKD. Many of the proposed measures, such as manuals and training materials, shall be made available to all interested other MFI. The training capacity will allow inviting also non-UsPKD participants. Although the proposed project concentrates on UsPKD, it is beneficial for the rural people and for the financial system development when they operate in an environment with healthy, i.e. self-sustaining, competition.

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

ix

Ringkasan Eksekutif Pada bulan Mei tahun 2005, Pemerintah Propinsi Nusa Tenggara Barat (NTB) dan ProFi – Promotion of Small Financial Institutions (proyek bersama Bank Indonesia, Departemen Keuangan, dan GTZ) telah menandatangani sebuah Nota Kesepakatan tentang Pengembangan Keuangan Mikro di NTB. NTB termasuk golongan propinsi dengan GDP dibawah rata-rata, dengan Indeks Pengembangan Manusia terendah kedua di Indonesia. Jumlah penduduknya sebesar 4,1 juta orang tinggal di pulau Lombok (hampir 3 juta orang) dan di pulau Sumbawa (sekitar 1 juta orang). Mereka memperoleh penghasilan terutama dari pertanian, perikanan, dan dari bekerja di luar negeri. Analisis pasar keuangan mikro pedesaan membandingkan permintaan dengan penawaran pada saat ini untuk mengetahui berbagai kesenjangan yang ada. Analisis dari segi permintaan termasuk survai terhadap 90 rumah tangga di NTB. Survai tersebut menemukan bahwa sebagian besar rumah tangga menabung kelebihan penghasilan mereka. Tabungan besar pada umumnya ditempatkan pada bank umum, sedangkan tabungan kecil pada umumnya ditempatkan pada lembaga keuangan mikro bukan bank yang letaknya berdekatan (termasuk UPKD). Lebih setengah dari jumlah rumah tangga meminjam dari lembaga keuangan secara teratur, terutama dari UPKD dan koperasi kredit. Sebagian besar pinjaman dari berbagai LKM ini jumlahnya kecil, dengan ukuran kurang dari IDR 2 juta. Sebagian rumah tangga juga meminjam uang dari sumber tidak resmi, khususnya dari teman dan keluarga. Pendidikan anak adalah tujuan utama dari menabung, sedangkan tujuan utama meminjam adalah untuk mendapatkan modal kerja. Rumahtangga umumnya sadar bahwa jasa keuangan memperhitungkan pembayaran bunga, dan bahwa peminjam wajib membayar kembali pinjaman mereka. Berbagai rumahtangga menyarankan bahwa keuangan mikro ditingkatkan melalui pelayanan yang digerakkan oleh permintaan dan rasa nyaman, serta pemasaran yang lebih baik dari jasa pelayanan yang ada sekarang. Survai menyimpulkan bahwa permintaan jasa keuangan oleh rumahtangga menunjukkan adanya potensi besar bagi penggalangan tabungan serta intermediasi keuangan secara efektif. Berbagai rumahtangga pada umumnya sudah biasa menabung dan membayar bunga atas jasa keuangan. Hal ini menyediakan landasan bagi pendekatan sistem keuangan untuk pengembangan lebih lanjut dari sektor keuangan mikro didalam propinsi. Berdasarkan contoh tersebut diatas, maka potensi permintaan rumahtangga pedesaan di NTB bagi jasa tabungan dan pinjaman secara kasar dapat diperkirakan. Jumlahnya berkisar antara 275,000-288,000 pelanggan tabungan, dan antara 372,000-390,000 pelanggan pinjaman, termasuk hampir 40% dari jumlah rumahtangga. Penawaran keuangan mikro datang dari beraneka ragam sumber. Pemusatan Bank Umum terjadi di Mataram, ibukota NTB yang memiliki sekitar 700.000 orang penduduk. Dua bank mengemuka sehubungan dengan kehadiran mereka di ibukota kabupaten, yaitu Bank Rakyat Indonesia (BRI) dan Bank NTB, sebuah bank pembangunan daerah yang dimiliki bersama oleh pemerintah propinsi dan kabupaten. Kantor-kantor cabang BRI tidak menyediakan pinjaman mikro sedangkan Bank NTB hanya menyediakan pinjaman bagi peminjam yang berpenghasilan tetap

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

x

(pegawai negeri sipil) dan pelanggan pilihan di pedesaan. BRI menyalurkan jasa keuangan mikro melalui 51 kantornya di setiap dua dari 100 ibukota kecamatan yang ada. Pelanggan BRI Unit umumnya berpenghasilan tetap dan khususnya terdiri dari pedagang dengan agunan yang memenuhi persyaratan bank. Ditingkat kecamatan, pemerintah NTB juga mengoperasikan 46 Bank Pedesaan, yaitu BPR-LKP. BPR-LKP menyediakan jasa keuangan pelengkap melalui pemberian pinjaman yang lebih kecil dengan persyaratan agunan yang lebih lunak. Lembaga-lembaga ini menjangkau penduduk desa melalui PHBK (pinjaman kepada kelompok), tetapi pinjaman jenis ini hanya sekitar 3% dari seluruh portofolio pinjaman. Sektor koperasi berhasil mencatat pertumbuhan yang pesat bila diukur dari jumlah lembaga dan laporan keuangan mereka. Khususnya pertumbuhan koperasi simpan pinjam (KSP) di perkotaan. Banyak pegawai negeri sipil dan karyawan perusahaan swasta menjadi anggota koperasi hanya untuk memperoleh pinjaman. Didaerah pedesaan, KSP dikenal sebagai pemberi pinjaman jangka pendek dengan angsuran harian. Koperasi usaha desa (KUD), juga di ibukota kecamatan, tidak mempunyai cukup dana bahkan di saat para petani paling membutuhkan bantuan mereka. Belum lama ini, sejumlah KSP didirikan oleh “para anggota” mereka dengan iuran keanggotaan yang sangat tinggi (dan suku bunga efektif dua kali dari BRI Unit), sehingga berbagai koperasi ini ibarat BPR yang dimiliki oleh pihak swasta. Mereka menunjukkan adanya permintaan, juga dari para petani, yang melebihi kemampuan mereka. Berlainan dengan NTT, koperasi kredit tidak terdapat di NTB. Juga berlainan dengan NTT, hanya sedikit sekali NGO yang membantu penduduk desa melalui kelompok arisan. Namun demikian arisan sangat populer di NTB: Program pengembangan kecamatan (PKK) memberikan bantuan kepada lebih dari 500 kelompok arisan di 23 kecamatan. Banyak orang menikmati pelayanan yang cepat dan tidak rumit dari para pelepas uang (moneylenders), yang dengan pinjaman mereka, membayar angsuran kepada bank dan LKM. Berbagai program pembangunan nasional yang berkomponen keuangan mikro dilaksanakan di NTB: Departemen Pertanian mencatat adanya tingkat pembayaran kembali yang rendah dari program-program KUT dan BPLM-nya. Fasilitas P4K lebih berhasil baik, namun demikian tidak lagi diperpanjang. Dana bergulir (IDT, Inpres Desa Tertinggal, PDM-DKE, sebuah program bantuan krisis ekonomi) ternyata bermasalah karena banyak kelompok hanya diatur untuk menerima “bantuan modal”. Mereka mudah bubar. PKS-BBM, sebuah proyek modal kerja pendukung bagi koperasi dan Lembaga Keuangan Mikro (LKM), dikelola oleh Departemen Koperasi dan UKM sejak tahun 2000 hingga 2003, mengikut sertakan pelatihan, pemantauan dan pengawasan dari bank umum bagi para penerima dana. Bank-bank bersangkutan, yaitu BRI dan BPD, masih kurang optimal dalam memenuhi kewajiban sebagaimana diperjanjikan, meskipun LKM sudah membayar secukupnya. Proyek tersebut nampaknya kurang berhasil dan dananya, yang menurut rencana tetap tinggal di LKM, wajib dibayar kembali dalam sepuluh kali angsuran tahunan. Proyek pengembangan kecamatan tersebut menghadirkan ciri-ciri yang khas, yakni UPK (Unit Pengelola Keuangan atau satuan pengelola keuangan) sebagai second-tier atau organisasi apex yang menyediakan pinjaman kepada kelompok arisan dan LKM. Angka-angka secara kasar menunjukkan mutu pinjaman yang tinggi tetapi juga biaya administrasi yang sangat tinggi. Proyek dan program hanya membantu untuk sementara waktu dan seringkali hanya bagi masyarakat setempat. Sebagian besar LKM sperti BRI Unit dan BPR-LKP tidak menyediakan pinjaman untuk penduduk desa, karena jarak yang jauh, atau mereka menyediakan fasilitas yang tidak bisa dimanfaatkan oleh para penduduk desa bagi usaha mereka. UPKD bisa menutup kedua kesenjangan tersebut, yaitu

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

xi

kesenjangan jarak dan kesenjangan keuangan: mereka merupakan lembaga pedesaan dan menyediakan tiga produk pinjaman yang dibutuhkan: pinjaman dari Rp0,2 juta sampai dengan Rp2juta, tanpa angsuran bulanan, jangka waktu dari 4 hingga 12 bulan, dan persyaratan agunan yang lunak. UPKD memiliki keunggulan tinggi dalam biaya transaksi bagi pemberi pinjaman dan peminjam dua-duanya. Namun demikian, UPKD tidak dapat menutup kesenjangan jasa pelayanan simpanan. Sebagai kelompok LKM serupa jika dilihat dari segi jumlah, maka seluruh 245 UPKD yang ada di NTB tidak punya bandingan. Pada tahun 1999 terdapat 214 UPKD yang didirikan sebagai LKM bukan bank bukan koperasi untuk mengelola sekitar Rp45 milyar dana yang dikucurkan oleh IMS-NTAADP, sebuah Proyek Pengembangan Daerah Pertanian Di Nusa Tenggara yang dibiayai oleh Bank Dunia sejak tahun 1996. Proyek yang berorientasi pada pengentasan kemiskinan ini menyediakan bantuan kepada desa tertinggal di berbagai kabupaten. IMS adalah singkatan dari Inisiatif Masyarakat Setempat. Pemberdayaan masyarakat, putusan dan pelaksanaan investasi, serta kendali oleh penduduk desa melalui kelompok kewajiban bersama dan Musdes, sebuah forum desa, adalah ciri-ciri terkemuka dari proyek. Pemerintah kabupaten membiayai pembentukan sekurang-kurangnya 30 UPKD tambahan. Hingga proyek ditutup pada bulan September tahun 2003, IMS-NTAADP telah menyelenggarakan pelatihan bagi para pengelola UPKD (tiga dari antara empat manajer, dan satu tim pengawasan (Badan Pengawas, BP), di bidang administrasi, pembukuan dan penilaian pinjaman. Laporan bulanan dikirimkan ke Bappeda tingkat kabupaten, selaku badan pelaksana. Banyak juga UPKD yang melaporkan tunggakan, yang rata-rata adalah 17%. Dalam tahun 2005, sebagaimana dilaporkan oleh semua responden, sebagian besar UPKD makin memburuk kondisinya. Sulit untuk memaparkan perkembangan ini dalam angka, karena makin banyak UPKD di Sumbawa, lebih dari 50%, yang berhenti mengirimkan laporan. Namun demikian, ini tidak selalu berarti berhentinya kegiatan. Ada perbedaan yang signifikan diantara UPKD bahkan yang saling berdekatan, perihal kinerja, aktiva, dan pendapatan, meskipun mereka menerima pembinaan dari lembaga dan fasilitator yang sama. UPKD yang tumbuh bagus dapat dijumpai bahkan di daerah yang tandus, yang lazimnya dianggap sangat miskin. Dalam tahun 2005, UPKD rata-rata melaporkan jumlah aktiva sebesar Rp235 juta, yang hampir sama dengan tahun 2003. Portofolio rata-rata sebesar Rp180 juta dimiliki oleh sekitar 50 kelompok dengan 500 orang anggota. Analisis (cermat) dari data pendapatan bunga menghasilkan adanya kredit bermasalah rata-rata sebesar Rp110 juta, dan rasio NPL sebesar 60%. Dengan tidak adanya angka-angka yang dapat dipercaya, menurut taksiran sekurang-kurangnya Rp55 juta (>25% dari seluruh pinjaman) macet. Secara keseluruhan, sekitar Rp12 milyar dari pinjaman awal sebesar Rp40 milyar secara pasti harus dihapuskan. Sekitar 40% dari seluruh pinjaman bergulir ditujukan kepada masyarakat (sangat) miskin. Banyak yang tidak sanggup membayar kembali. Berbagai pinjaman ini akhirnya harus dihapuskan. Sisanya, yang Rp55 juta, agaknya dapat ditagih kembali melalui berbagai cara, termasuk reconditioning pinjaman atau penyitaan harta, kemauan politis dan pemberian bantuan. Hanya sebagian kecil UPKD yang membentuk penyisihan penghapusan kredit macet secara benar. Para manajer menyalahkan berkurangnya pendapatan pinjaman pada pengaruh musim, tunggakan pembayaran yang “akan diselesaikan segera”, serta orientasi sosial, seperti perpanjangan jangka waktu pinjaman tanpa pembayaran bunga. Jumlah kontribusi UPKD untuk kas desa

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

xii

mungkin sebesar 1% dari jumlah dana pinjaman, yang seringkali adalah sumbangan bagi kepala desa. Rasio NPL yang tinggi tidak serta merta membahayakan kelangsungan hidup dan berkelanjutannya sebuah UPKD – walaupun, tentu saja – rasio NPL yang lebih rendah meningkatkan prospek berkelanjutannya. JIka kredit macet dihilangkan, maka ukuran UPKD masih sekitar dua kali BKD (Badan Kredit Desa). Sisa portofolio sehat sekitar Rp60 juta hingga Rp100 juta menghasilkan pendapatan yang cukup untuk menutup pengeluaran (bukan biaya!), yang lentur (flexible) hingga ambang batas sangat tinggi. Sepanjang mereka beroperasi, UPKD punya peluang yang jauh lebih baik untuk memperoleh pembayaran kembali kredit macet dan meningkatkan portofolio pinjaman. Berbagai perhitungan, yang berlandaskan perkiraan NPL dan berbagai rasio berkelanjutan yang beragam, meramalkan bahwa 91 dari 117 UPKD punya prospek kelangsungan hidup yang realistis, jika saja ada kemauan politis dan bantuan tersedia. Alasan paling sering bagi meningkatnya NPL dan berkurangnya pendapatan terkait erat dengan sifat UPKD sebagai bekas lembaga proyek. Ketika proyek bersangkutan ditutup, pengelola UPKD kehilangan (juga dukungan moral) dukungan dari para fasilitatornya, dan para debitur mulai mempertanyakan asal dan sifat dari dana bersangkutan serta keabsahan lembaga dari mana mereka menerima pinjaman. Para manajer UPKD merasa terbebani oleh aspirasi yang terlampau banyak dan yang saling bertentangan, serta mereka tidak memiliki cukup persiapan untuk menghadapi hal ini, atau banyak dari mereka kurang mendambakan kedudukan sebagai manajer UPKD. Alasan penting lain bagi peningkatan NPL adalah lemahnya manajemen risiko kredit: pemberian pinjaman dilakukan tanpa mengacu pada prinsip kehati-hatian, tanpa adanya diversifikasi sumber pendapatan, yang tidak dapat menyediakan “cara pemecahan kedua”, dan kepada mereka yang, yang berpenghasilan tetap tetapi sudah memeroleh pinjaman dari pihak lain. Para manajer tidak bisa mencegah terjadinya hal demikian: mereka memenuhi permintaan dari proyek dan permintaan dari sesama penduduk desa. Sebagian besar pengawasan “oleh masyarakat umum” mengalami kegagalan. Konflik tersebut mungkin paling tepat digambarkan seperti para anggota BP yang menerima pinjaman dan lalu macet. Para manajer UPKD dan para anggota BP bersangkutan tidak mungkin dipecat karena telah mengabaikan peraturan yang berlaku. IMS-NTAADP membiayai dan mengembangkan infrastruktur keuangan mikro di daerah pedesaan NTB: modal kerja, aktiva/harta tetap, sewa ruangan, pengembangan sumber daya manusia, produk dan saluran pemasaran. Namun tanpa adanya perhatian lebih lanjut setelah proyek NTAADP berakhir, jumlah UPKD-LKM yang aktif di NTB akan berkurang dengan sekitar 3 atau 4 lembaga tiap bulannya. Kerugian uang karena memburuknya mutu portofolio pinjaman diperkirakan sebesar Rp20 juta tiap hari. Pertanyaannya adalah, apakah dan bagaimana kerugian ini dapat dicegah atau sekurang-kurangnya dikurangi secara signifikan. Untunglah, sebagian besar infrastruktur masih berjalan baik: para pejabat di lembaga-lembaga pemerintah yang memantau perkembangan UPKD, anggaran dasar dan anggaran rumahtangga mereka, kantor-kantor UPKD, catatan pembukuan, modal kerja dan harta/aktiva tetap, serta para manajer mereka. Pendekatan baru bagi pengembangan UPKD diusulkan untuk dilaksanakan setelah berbagai kelemahan mereka diketahui, sebagai akibat dari sifat UPKD selaku lembaga proyek yang semata-mata berorientasi sosial. Anggaran dasar dan anggaran rumahtangga, serta dasar hukum mereka sama sekali tidak sesuai

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

xiii

manakala proyek tersebut sudah selesai. Maka dari itu, proyek susulan perlu memusatkan perhatian pada satu tujuan tunggal, yaitu berkelanjutannya UPKD. Visi UPKD yang diusulkan adalah: “meningkatkan kesejahteraan anggota masyarakat desa melalui penyediaan produk dan jasa keuangan, serta menyumbangkan labanya untuk pembangunan desa”. Bersamaan dengan itu maka misi UPKD yang diusulkan adalah: “menyediakan produk dan jasa keuangan secara berkelanjutan, yang sesuai dengan permintaan masyarakat setempat dan menerapkan prinsip kehati-hatian”. Disarankan untuk merubah nama dari lembaga: “Unit” diganti menjadi “Usaha” (Perusahaan, Bisnis) untuk menyatakan orientasi yang baru: menghasilkan laba bagi masyarakat desa. Bersamaan dengan itu, berbagai tugas sosial perlu dialihkan kepada pemerintah desa. Ini memperkenankan UsPKD (Usaha Pelayanan Keuangan Desa) untuk bertindak sesuai dengan orientasi pasar dan meningkatkan suku bunga mendekati suku bunga yang berlaku di pasar. Pemerintah desa akan memutuskan, siapa saja yang memenuhi syarat untuk menerima subsidi bunga dan menggunakan laba UsPKD, yaitu hanya kelebihannya (surplus) dan bukan isi pokoknya (substance), untuk membiayai (transfer ke UsPKD) subsidi ini. Mereka, yang sanggup membayar bunga lebih tinggi, menyumbang lebih banyak laba bagi pengembangan lebih besar dari desa dan memberikan bantuan kepada yang membutuhkan. Keterbukaan dibidang keuangan dan kesetiakawanan/solidaritas desa bisa diwujudkan. Adalah penting bahwa UsPKD menjadi badan usaha yang menguntungkan karena hanya lembaga keuangan yang tangguh dan menguntungkan yang dapat menarik kepercayaan masyarakat serta tumbuh. Orang membayar kembali pinjamannya dengan prospek untuk memperoleh pinjaman susulan yang lebih besar. Khususnya diusulkan: - Pengalihan harta/aktiva dari Unit PKD ke Usaha PKD termasuk verifikasi dan

penilaian kembali seluruh portofolio pinjaman. Jumlah mereka sekitar 80% dari jumlah harta/aktiva UPKD. Nilai sesungguhnya dari seluruh pinjaman harus ditentukan, yang mungkin sekali jauh lebih rendah dari nilai nominal atau nilai buku. Orang tidak bisa menciptakan lembaga keuangan yang sehat tanpa adanya akuntansi yang terbuka (transparent). UPKD tidak bisa menanggung beban dari proyek lama. Mungkin verifikasi pinjaman akan dihadapkan pada keengganan atau bahkan perlawanan dari banyak orang. Bantuan pemerintah di semua tingkatan dibutuhkan untuk pelaksanaan tugas ini.

- Desa akan menjadi pemilik 100% dari UsPKD yang baru. Kepemilikan dana IMS-NTAADP perlu di klarifikasi sebelum menetapkan status hukum UsPKD. Peran pemerintah kabupaten dalam dewan komisaris juga akan bergantung pada kepemilikan dana IMS-NTAADP. Undang-undang tentang LKM atau peraturan pelaksanaan BUMDES (Badan Usaha Milik Desa) dapat menyediakan pilihan bagi keabsahan UsPKD. Koperasi kurang cocok: mereka merupakan perusahaan yang berorientasi pada keanggotaan dari mana para anggota mereka menarik manfaat, jadi bukan masyarakat.

- Dana pinjaman dari IMS-NTAADP akan menjadi pinjaman subordinasi jangka panjang untuk UsPKD, yang memperkuat permodalan mereka, sebuah fitur kunci ketika UsPKD mencari pembiayaan untuk memperluas bisnis mereka.

Tujuan proyek “Pengembangan Keuangan Mikro Wilayah di NTB”, sebagaimana dipaparkan dalam Risalah Perjanjian, adalah:

a) meningkatkan mutu pelayanan LKM; b) meningkatkan jumlah LKM yang sehat;

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

xiv

c) menciptakan lingkungan yang kondusif melalui peraturan/pengaturan dan pengawasan;

d) meningkatkan kerjasama diantara LKM dengan lembaga-lembaga keuangan lainnya;

e) meningkatkan kemampuan LKM dalam menjangkau modal dari berbagai sumber.

Memperkuat UPKD menyumbang pencapaian berbagai tujuan ini. a) Mutu pelayanan: Secara rata-rata, UPKD menghimpun Rp10jt simpanan, yang

sebagian besar merupakan pembayaran wajib (compulsory fee) dari para peminjam. UPKD kurang aktif atau kurang berdaya cipta dalam menarik simpanan, antara lain disebabkan oleh peraturan Bank Indonesia yang membatasi penggalangan simpanan oleh bank saja. Sebaliknya, orang segan menyimpan dana kalau mereka meragukan berkelanjutannya LKM. Dalam hal ini UsPKD bisa mengikat kerjasama dengan bank. Berkenaan dengan pemberian pinjaman, kebanyakan orang menginginkan akses atas pinjaman pribadi dengan jadwal pembayaran angsuran pribadi daripada pinjaman kepada kelompok yang ada sekarang.

b) Meningkatkan jumlah LKM sehat mengandung dua komponen: jumlah lembaga

dan mutu, atau kesehatan dari LKM. Memperbaiki tingkat kesehatan LKM dari kurang sehat menjadi sehat juga masuk dalam perhitungan. Sayang bahwa perbaikan dari tidak sehat menjadi kurang sehat tidak masuk dalam perhitungan. Pemerintah-pemerintah kabupaten telah menyatakan minat mereka untuk turut membiayai pembentukan UPKD baru. Diharapkan bahwa dalam jangka waktu tiga tahun ada sekitar 20 LKM tambahan seperti ini. Apakah proyek berhasil meningkatkan jumlah LKM sehat hanya dapat dijawab segera sesudah jumlah LKM yang sehat, disini: UPKD, diketahui, yang nampaknya dibawah 10 jika diukur dengan standar BPR. Sebuah standar bagi LKM “sehat” bukan bank bukan koperasi perlu dikembangkan. Namun demikian, penilaian yang berlandaskan kelima kriteria penilaian CAMEL kelihatannya sesuai juga bagi UPKD. “C”apital rating atau peringkat modal, yang berasal dari rasio kecukupan modal

atau capital adequacy ratio (CAR), meningkat kalau kredit macet dihilangkan dari neraca, ketika dana IMS-NTAADP menjadi pinjaman subordinasi, dan jika sebagian dari pinjaman ini diubah bentuknya menjadi modal.

“A”ssets atau harta/aktiva sebagian besar terdiri dari portofolio pinjaman. Perpanjangan dan penjadwalan kembali (rescheduling) pinjaman tertunggak dapat meningkatkan mutu portofolio, yaitu, ketika perjanjian pinjaman atau produk disesuaikan dengan arus kas peminjam beserta struktur risikonya, seperti pinjaman yang membolehkan pembayaran kembali secara lentur (flexible).

“M”anagement rating atau peringkat pengelolaan meningkat melalui pemberlakuan berbagai pedoman dan prosedur tertulis lainnya, pelaksanaan pengawasan intern dan mekanisme pengendalian. Para manajer membutuhkan pelatihan supaya dapat mengerti dan mengaplikasikan peralatan ini.

“E”earnings atau penghasilan dapat mencapai duakali melalui penagihan pembayaran secara intensif pada saat jatuh temponya angsuran pinjaman dan pembebanan denda bagi keterlambatan bayar. Pendapatan akan mencapai duakali lagi kalau pengelola UPKD menerapkan kondisi bunga yang serupa dengan yang diterapkan oleh koperasi simpan pinjam di

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

xv

pedesaan. Penghasilan meningkat kalau biaya berkurang namun hanya sedikit UPKD yang tinggi pendapatannya yang mampu memikirkan bagaimana mengurangi pengeluaran. Biaya penyisihan penghapusan kredit macet akan berkurang karena pinjaman diberikan berdasarkan prinsip kehati-hatian.

“L”iquidity atau likuiditas, pada umumnya, bukan merupakan keperihatinan khusus dari UPKD. Penarikan kembali simpanan bisa diramalkan atau bisa diabaikan. Pengeluaran lainnya dapat ditangguhkan dan dirundingkan.

Jika diringkas, ada banyak kegiatan untuk meningkatkan “kesehatan” UPKD. Sebagai terkaan yang paling tepat, jika hari ini ada sepuluh UPKD yang kinerjanya paling bagus, maka sekitar 20 cukup sehat, 40 kurang sehat dan 160 tidak sehat. Dengan adanya campur tangan diharapkan bahwa setelah 2 hingga 3 tahun ada 40 (+30) UsPKD sehat, 50 (+30) cukup sehat, 65 (+25) kurang sehat dan 95 (-65) tidak sehat. Menurut perkiraan 95 LKM ini tetap “dormant” atau tidur/tidak aktif, antara lain karena dari hasil verifikasi, portofolio mereka sudah terlanjur rusak.

c) Berkenaan dengan peraturan, ada tiga persoalan yang perlu disikapi: (i) untuk

menjadikan UsPKD sebagai badan hukum maka prosedur bagi BUMDES belum ada, dan juga belum ada Undang-undang tentang LKM, yang akan berdampak pada perumusan anggaran dasar dan anggaran rumahtangga yang baru; (ii) peraturan yang membolehkan LKM di pedesaan untuk menghimpun simpanan (mungkin bisa ditambahkan satu bab dalam Undang-undang tentang LKM); dan (iii) peraturan dan klarifikasi berkenaan dengan kepemilikan dana IMS-NTAADP, termasuk prosedur penghapusannya. Proyek meninggalkan sekumpulan ketentuan dan peraturan “sunshine” bagi UPKD, yang berguna bagi pelaksanaan proyek lama, namun menjadi hambatan bagi pengembangan UsPKD. Diusulkan untuk menyiapkan surat ketetapan (decree) bagi verifikasi portofolio, serta bagi anggaran dasar dan rumahtangga sementara UsPKD. Kasus tersebut perlu dibuka kembali sesudah Undang-undang tentang LKM terbentuk dan keluarnya peraturan tentang BUMDES. Tanpa adanya peraturan tentang penghapusan rasanya tidak mungkin meningkatkan jumlah LKM yang sehat, kecuali kalau hanya pinjaman sehat yang dipindahkan (transfer) ke UsPKD dan pinjaman yang tidak tertagih ditinggalkan sebagai “harta/aktiva UPKD”. Laporan ini membahas pengawasan secara luas karena keberhasilan UsPKD berpusat pada orang yang menangani uang yang bukan miliknya didalam sebuah masyarakat yang menghargai ikatan keluarga dan tetangga, serta rasa hormat dan kepatuhan kepada atasan yang jauh lebih tinggi daripada pekerjaan (proyek!) sementara berkenaan dengan pengaturan dana tanpa nama (anonymous funds). Kehadiran dari pengawasan, yaitu pemeriksaan intern (internal audit), memperkuat moral dari para manajer. Kinerja UPKD akan semakin memburuk tanpa adanya pengawasan dari tim-tim BP. Namun demikian, kekuatan mereka, yang terlekat dalam dan mengenal penduduk desa, juga merupakan kelemahan utama mereka. Para pengawas adalah sesama penduduk desa, dan oleh karena itu seringkali tidak netral, dan cenderung menghindari perselisihan. Bagi banyak orang tugas tersebut terlampau besar tuntutannya, sedangkan bagi orang lain terlalu tidak menentu (satu kali dalam tiga bulan). Tidak ada pihak yang membina, mengawasi, mengendalikan, atau memantau para pengawas. Maka dari itu, direkomendasikan pembentukan tim-tim pengawas yang bekerja penuh waktu dan semi-profesional di tingkat kabupaten, sebagai perwujudan dari pemeriksaan intern. Sekitar 15 hingga 25 orang spesialis yang dipekerjakan – dengan

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

xvi

lewatnya waktu – akan sudah berpengalaman dan mampu melaksanakan tugas ini dengan lebih baik dibandingkan 735 orang yang ada sekarang. Di tingkat propinsi, seorang koordinator profesional akan membina, melatih, dan mengawasi kinerja tim-tim ini. Pengeluaran untuk membiayai pengawasan akan meningkat tinggi dan mencapai sekitar Rp500jt per tahun. UsPKD mampu menanggung pengeluaran ini yang relatif sangat kecil jika dibandingkan dengan besarnya biaya untuk membentuk penyisihan penghapusan kredit macet yang sekarang sudah mencapai lebih dari Rp5 milyar.

d) BPD Bank NTB, BPR-LKP dan UPKD mempunyai ikatan bersama dalam hal

kepemilikan oleh Pemerintah NTB. Berbagai produk serta cakupan daerah bersifat saling melengkapi. UsPKD dapat bertindak sebagai kepanjangan tangan, misalnya sebagai penghimpun tabungan bagi bank. Bagi para pelanggan UsPKD menarik untuk mengetahui bahwa lembaga keuangan tersebut tidak sepenuhnya berdiri sendiri tetapi merupakan bagian dari sebuah sistem keuangan propinsi yang menyeluruh. Tambahan pula, kerjasama diantara UsPKD perlu diterapkan, bukan saja berkenaan dengan pengawasan, melainkan juga di berbagai bidang seperti pengembangan sistem informasi dan pemberian nilai yang sederhana.

e) UsPKD dapat menyediakan pelayanan sebagai kasir dari pemerintah desa serta

simpanannya. Mereka dapat menawarkan pelayanan untuk mengurus komponen keuangan dari berbagai program pemerintah. Dengan adanya permintaan yang belum dapat dipenuhi yang jumlahnya sekitar Rp350jt per desa, maka UsPKD bisa menarik perhatian para pemberi pinjaman yang tidak mampu melayani segmen pasar ini secara langsung/sendiri. UsPKD tidak dapat menyerahkan agunan fisik. Mereka harus membuktikan prestasi kinerja dan ini adalah alasan utama mengapa para manajer UsPKD perlu mempelajari bagaimana memantau pemeringkatan CAMEL dari UsPKD mereka.

Pelaksanaan proyek mengikut sertakan beberapa langkah pendukung UPKD. Berkelanjutannya UsPKD bisa dicapai melalui urutan langkah sebagai berikut: (i) verifikasi harta/aktiva untuk meningkatkan keterbukaan (2 bulan), (ii) pelatihan on-the-job (orientasi bisnis, 4-6 bulan), (iii) konsultasi (pemecahan masalah, 6-12 bulan), (iv) kerjasama diantara LKM, terutama berkenaan dengan pengawasan, dan dengan lembaga keuangan lain. Urutan pengembangan kelembagaan akan dilengkapi dengan penyediaan berbagai pedoman, pelatihan kelas (in-class training), dan sertifikasi. Proyek melalui tahap percobaan (pilot phase), termasuk persiapan, uji coba verifikasi harta/aktiva di berbagai desa pilihan dan klarifikasi kepemilikan dana IMS-NTAADP. Proyek dapat dilanjutkan jika seluruh kegiatan ini telah berhasil dilaksanakan dengan baik. Pada awal tahap percobaan, dilakukan konsultasi dengan Pemerintah NTB dalam Forum Kebijakan Keuangan Mikro Wilayah (FoMFIDa) yang bertujuan memperoleh persetujuan atas berbagai tujuan bersama serta rancangan dasar dari proyek. Seorang Direktur Proyek membutuhkan waktu dua bulan untuk tahap persiapan menyelesaikan berbagai perjanjian kerjasama dengan pemerintah dari desa-desa yang terpilih. Ini merupakan salah satu bagian paling gawat (crucial) dari proyek: Lingkungan yang tidak mendukung konfirmasi harta/aktiva (asset confirmation), yakni keterbukaan, akan tidak kondusif. Waktu yang cukup perlu disediakan sebelum pengumuman verifikasi harta/aktiva untuk memberikan kesempatan kepada sementara orang untuk menyelesaikan tunggakan pinjaman (overdues) mereka. Paling lambat dalam bulan ketiga, tiga orang Penasehat Keuangan Mikro (Microfinance Advisors) atau MFA dapat masing-masing mulai

Executive Summary - Rural Microfinance Development in NTB – Concept and Implementation Strategy

xvii

melaksanakan verifikasi portofolio di dua desa. Verifikasi portofolio secara sukses adalah salah satu pra-kondisi bagi transfer harta/aktiva dari UPKD ke UsPKD serta pemberian bantuan selanjutnya. Bersamaan dengan itu, Pemerintah NTB akan mengklarifikasi kepemilikan dari dana IMS-NTAADP dan mengembangkan garis pedoman tentang penanganan pinjaman macet beserta prosedur penghapusannya, yang membentuk pra-kondisi lain bagi pemberian bantuan selanjutnya setelah tahap uji coba. MFA menambah dengan desa ketiga dan keempat dalam bulan-bulan berikutnya. Proyek seharusnya sudah menimba cukup pengalaman sesudah tiga bulan uji coba verifikasi harta/aktiva dan kerjasama dengan 12 desa untuk memutuskan dan merancang duplikasi (multiplication) di berbagai kabupaten lainnya. Sekiranya tahap percobaan (pilot phase) sukses, yakni verifikasi harta/aktiva telah selesai diselenggarakan di sekurang-kurangnya 12 desa, dan kepemilikan dana IMS-NTAADP sudah diklarifikasi dan memperkenankan pengembangan LKM yang dimiliki desa, maka proyek akan mulai beranjak ketingkatan yang lebih tinggi (scaling-up). Berdasarkan pengalaman uji coba, akan diputuskan berapa banyak MFA baru dan Deputi Direktur Proyek akan diterima bekerja untuk melanjutkan urutan pengembangan kelembagaan UPKD dari verifikasi harta/aktiva, yang diikuti dengan pelatihan on-the-job, konsultasi dan pelatihan yang sejajar (parallel). Maksimal 3 orang Deputi Direktur dan 21 orang MFA mungkin akan dibutuhkan jika pengembangan UsPKD mewujudkan potensi sepenuhnya. Sebelum MFA baru dipekerjakan, maka pembiayaan bersama selama jangka waktu proyek dan cakupan biaya setelah out-phasing perlu diklarifikasi untuk memastikan berkelanjutannya. Pelaksanaan proyek yang diusulkan akan menjumpai tumpang tindihnya barbagai urutan ini karena proyek tersebut akan dimulai di daerah percobaan (pilot area) dan akan digandakan secara bertahap hanya setelah berhasil memperoleh pengalaman dan membuat berbagai penyesuaian yang perlu. Diperkirakan bahwa verifikasi harta/aktiva dari satu UPKD akan mempekerjakan seorang MFA untuk 7-10 hari per bulan, sedangkan pelatihan on-the-job hanya membutuhkan kehadiran selama 2 hingga 5 hari dan konsultasi hanya 1 hingga 2 hari per bulan. Oleh karena itu, MFA akan membantu secara bersamaan, misalnya, satu UPKD dengan konfirmasi harta/aktiva, tiga UPKD dengan pelatihan on-the-job, dan tiga lain dengan konsultasi. Para direktur proyek sendiri perlu mengunjungi UsPKD untuk mengkonfirmasikan dan mempelajari dari tangan pertama perihal kinerja UsPKD dan permasalahan mereka, dan untuk memastikan bahwa MFA memenuhi tugas mereka, antara lain melalui pemeriksaan intern yang teratur hingga saatnya tim-tim pengawas mengambil alih tugas ini pada tahun kedua dari proyek. Diperkirakan bahwa selama tahun kedua dijadwalkan pelatihan kelas (in-class training) dan kunjungan dimulai oleh tim-tim pengawas. Jumlah MFA dapat dikurangi paling lambat diawal tahun ketiga. Proyek akan memusatkan pikiran pada pengembangan dan penguatan Forum atau asosiasi yang menuju pada pemberlakuan sistem sertifikasi bagi manajer dan lembaga. Proyek juga akan terlibat dalam penggalangan dana bagi UsPKD yang bagus kinerjanya. Banyak dari langkah-langkah yang diusulkan, seperti pedoman dan materi pelatihan, juga tersedia bagi semua LKM lain yang berminat. Pelatihan dapat mengundang partisipasi dari peserta yang bukan berasal dari UsPKD. Meskipun proyek yang diusulkan memusatkan pikiran pada UsPKD, proyek tersebut juga bermanfaat bagi masyarakat pedesaan dan bagi pengembangan sistem keuangan pada saat mereka beroperasi dalam sebuah lingkungan yang sehat, yakni persaingan tanpa memerlukan bantuan dari pihak lain.

Rural Microfinance Development in NTB – Concept and Implementation Strategy

1

1 Introduction Sustainable access to financial services has a powerful impact on economic growth and poverty reduction. Indonesia has a substantial and very diverse landscape of Microfinance Institutions (MFI), but access to finance is still very limited in rural areas, and most difficult at the village level. The Government of Indonesia (GoI) has made reducing poverty and achieving the Millenium Development Goals a top policy priority. To assist these efforts, German Technical Cooperation (GTZ) supports Bank Indonesia and Ministry of Finance in implementing the “Promotion of Small Financial Institutions” Program (ProFI). ProFI aims at increasing outreach and sustainability of MFI in Indonesia. Developing sustainable MFI with outreach to the poor has been most successful when following the “Financial Systems Development” paradigm. This implies that the Government provides an enabling environment to facilitate MFI growth, and assumes a promotional role in MFI capacity building. ProFI advocates these principles, including a commercial approach to microfnance, because it is most likely to reach more clients on a sustained basis. ProFI works with a diverse range of institutions, from Rural Banks and Cooperatives to village-based MFI, and supports MFI development through four components:

(1) National Microfinance Policy (2) Development Strategy and Enabling Environment for BPR and LPD (3) Capacity Building and Professional Certification (4) Regional Financial Systems Development

Decentralization opens new opportunities to improve access at the village level, because it enables locally adapted conditions for successful MFI development. ProFI is pilot-testing decentralized approaches under Component 4: “Regional Financial Systems Development” aims at creating an enabling environment and improving institutional capacities of MFI in Nusa Tenggara Barat (NTB) and Nusa Tenggara Timur (NTT). Agreed Minutes between the Provincial Government of NTB and GTZ, signed on May 17, 2005, create the framework for the “Regional Microfinance Development in NTB” project. The project objectives aim at adapting a financial systems development approach to the market for rural microfinance in NTB. This study has the purpose to develop a feasible concept and an implementation strategy from 2006-2008. To this end, demand and supply of financial services to village households have been investigated to identfy potential gaps. The MFI landscape in NTB has been screened for institutions which could contribute to narrowing these gaps. 245 Unit Pengelola Keuangan Desa (Village Financial Management Units, UPKD) are the most promising development option to increase sustainable outreach to the village level. They have been set-up as village-owned MFI by a World Bank poverty alleviation project from 1999-2003. UPKD are analyzed in detail, and the study proposes both a concept and an implementation strategy for achieving the project objectives. The concept builds on transforming UPKD into profitable business units. Implementation focuses on UPKD portfolio review and intensive capacity buidling through on-the-job training, feeding lessons learnt back into improved UPKD regulations.

Rural Microfinance Development in NTB – Concept and Implementation Strategy

2

2 The Province of Nusa Tenggara Barat (NTB) NTB covers some 20,000 km2 and is composed of Lombok and Sumbawa, and more than a hundred minor islands. The distance from Western Lombok to Eastern Sumbawa is about 350km. NTB is inhabited by slightly more than 4 million people, living in about 1 million households. The population is unevenly distributed: Lombok covers slightly more than 20% of the area, but accounts for more than 70% of the population (population density 600/km2). In contrast, Sumbawa occupies 76% of the province, but accounts for less than 30% (population density 80/km2). Government Administration The province is divided into nine administrative units: seven districts and two municipalities, which are divided into 100 sub-districts / municipalities, and 792 villages. Four of them are in Lombok (Mataram, West, Central, and East Lombok) and five in Sumbawa (West Sumbawa, Sumbawa, Dompu, Bima, and Bima City). Mataram, Bima City and West Sumbawa came into existence after decentralization, separating from the districts West Lombok, Bima, and Sumbawa. Hence, official data are often not yet available for these new districts. Demography and employment The majority of the population lives in rural areas (65% according to the 2000 Population Census) and more than 50% of the labor force works in the agricultural sector. Other important employment sectors include industry (manufacturing), trade, and service, which account for 10% or more of the labor force. The majority of the industrial entities are labor intensive and family owned small and micro enterprises processing foods, wood (furniture), and tobacco. Socio-economic conditions The province is one of the least developed economies in Indonesia. It has the second-lowest Human Development Index. 20 per cent of the population were very poor (earning less the dollar value of 240 kg rice p.a.), and more than half of the villages were ‘backward’ villages in 1993. The poverty level should have even more risen following the 1997 economic crisis and several recent vast increases in fuel prices. After the 1998 financial crisis with a shrinking GDP, the economy began to grow around 3 per cent in 1999. The inflation rate was down from 90% in 1998 to 6% in 2004. The growth of the economy, however, is about half of the growth level prior to the crisis (1993-1997). In 2003, the Regional Gross Domestic Product (RGDP) was estimated about IDR 17 trillion or IDR 4 million per capita. After the Mining and quarrying sector which contributed 28 % to the RGDP (foreign investment), the agriculture sector contributed most (24% of RGDP) to the economy. Two other sectors with a relatively substantial contribution to the economy were trade, and hotel and restaurant (13% of RGDP) and the service sector (12% of RGDP). The manufacturing sector consists of micro- and small enterprises. Although it played a relatively important role in number of business entities and employment, it contributes little value to RGDP.

Rural Microfinance Development in NTB – Concept and Implementation Strategy

3

The provincial RGDP is not evenly distributed. For instance, the mining activities are concentrated in Sumbawa and West Sumbawa districts. In 2003, both districts accounted for the largest share of the sector’s provincial RGDP (40%) while the other districts accounted for 14% or less. On the other hand, the Trade, Hotel and Restaurant activities are concentrated in West Lombok and Mataram City districts. The agriculture sector is equally important across the districts, except for the city districts where the service sector is dominant. Paddy, soybeans, peanuts, maize, shallots, garlic, chili and cassava are the major agricultural food products of the province. The major cash crops are coconut, coffee, cashew, and tobacco. The livestock sector is dominated by the production of cows and buffalos. The major manufacturing sectors include food, tobacco, wood and non-metal processing. The main export products are copper concentrate, pearls, cashew nuts, and various fishery products. In 2004, however, the copper concentrate made up almost 100% of the total export value (USD 975 million). Japan, The Philippines, India, Korea, and Germany were the major recipients of the exports.

Rural Microfinance Development in NTB – Concept and Implementation Strategy

4

3 The Rural Microfinance Market in NTB The analysis of the market for rural microfinance investigates demand and supply to identify gaps. Potential demand has been estimated through surveys of 90 households and the management of 60 UPKD. Both surveys indicate substantial scope for more savings and loan services in rural areas of NTB. Analysis of rural microfinance supply aims at identifying MFI which could be developed further to narrow the identified gaps.

3.1 Demand for Microfinance To identify demand-supply gaps, 90 households from villages in the 9 districts / municipalities were surveyed during June/July 2005. The first objective was a better understanding of household demand for financial services. The second objective was to investigate household perceptions of microfinance supply. The survey is attached in Annex 1, the following summarizes the main results. The households in the sample have an average annual income of around to Rp15m, the estimated value of their physical assets is Rp18m. The household heads, mostly farmers and traders, have on average eight years formal education. They live at a six km distance from the nearest MFI offices. The households’ demand for institutional savings and loans are summarized in the table below: Table 1: Household Demand for Institutional Savings and Loans

Institution Saving: Share of

HH

Avg. Savings balance (Rp’000)

Borrowing: Share of

HH

Avg. Loan amount

(Rp million) BRI (Units) 14% 324 4% 7.7 BPD 6% 2,440 0% - BNI 1% 35,000 2% 25.0 BPR 1% 85 2% 1.5 KSP & USP 6% 720 19% 1.5 UPKD 10% 130 27% 0.7 Others 3% 117 1% 5.0 Total 41% 2,537 56% 2.7

Source: The Household Survey, 2005, see Annex 1 The survey found that a substantial proportion of the households normally save their excess incomes: 34% in cash (mostly with financial institutions), 6% in kind, and 2% in a combination of cash and kinds. Large savings are generally placed with commercial banks (particularly BRI Units) while small savings are generally placed with nearby non-bank financial institutions (particularly UPKD). More than half of the households regularly borrow from financial institutions, particularly from UPKD and credit cooperatives. Most loans from these MFI are small, with sizes less than IDR 2 million. Larger loans were borrowed from the commercial banks, mainly BRI Units. A few of the households also borrow from informal sources, in particular friends and family. Child education is the main purpose of saving, whereas the main purpose of borrowing is working capital. Based on the household sample, a very rough estimate of the potential demand of rural households in NTB for institutional saving and loan services can be made. The results are arrived at by simple projection of the samples behavior on the entire population or rural households in NTB, and are given in the table below. The

Rural Microfinance Development in NTB – Concept and Implementation Strategy

5

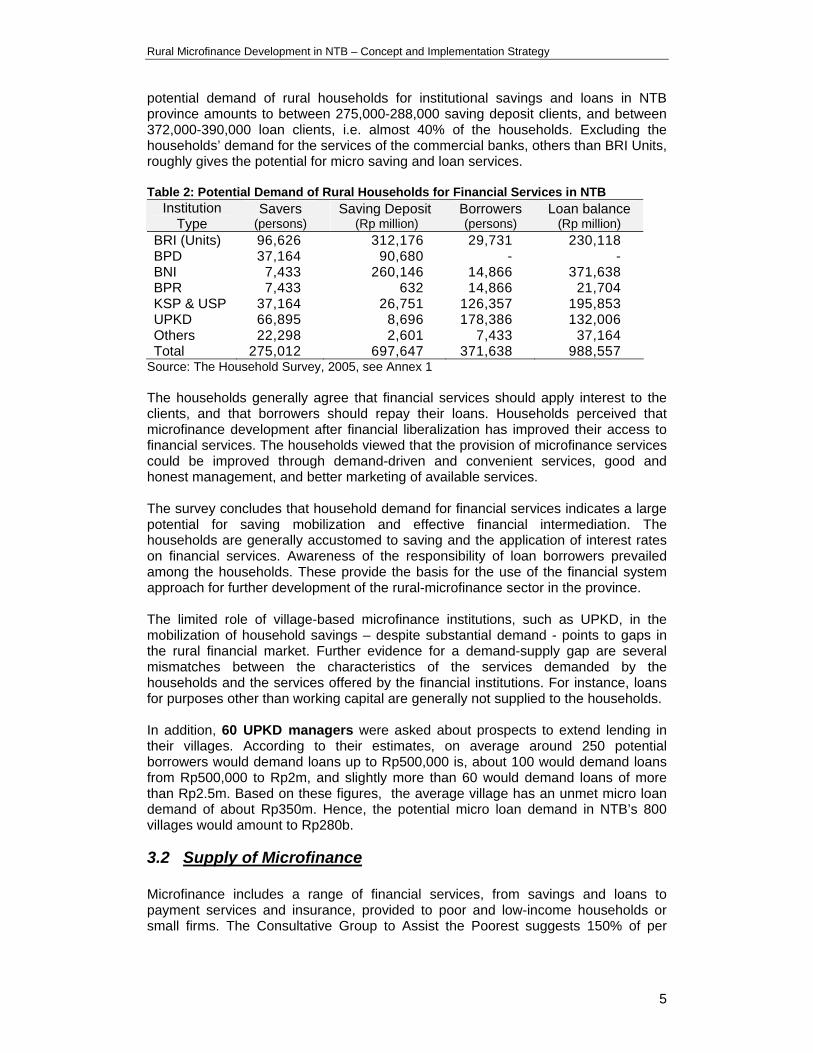

potential demand of rural households for institutional savings and loans in NTB province amounts to between 275,000-288,000 saving deposit clients, and between 372,000-390,000 loan clients, i.e. almost 40% of the households. Excluding the households’ demand for the services of the commercial banks, others than BRI Units, roughly gives the potential for micro saving and loan services. Table 2: Potential Demand of Rural Households for Financial Services in NTB

Institution Type

Savers

(persons) Saving Deposit

(Rp million) Borrowers

(persons) Loan balance

(Rp million) BRI (Units) 96,626 312,176 29,731 230,118 BPD 37,164 90,680 - - BNI 7,433 260,146 14,866 371,638 BPR 7,433 632 14,866 21,704 KSP & USP 37,164 26,751 126,357 195,853 UPKD 66,895 8,696 178,386 132,006 Others 22,298 2,601 7,433 37,164 Total 275,012 697,647 371,638 988,557