regional economic scorecard - wilmington...

TRANSCRIPT

Produced for the community by:

Cape Fear FutureAn initiative of the Wilmington Chamber of Commerce

WILMINGTONREGIONAL ECONOMIC

SCORECARD|

||

||

||

||

||

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | ||

||

||

||

|| |2015

Building Regional ProsperityDuring the severe recession that began in 2008, our Region suffered major

job losses. The recovery which began mid-year 2009 differed from previous

recoveries, with job creation being especially weak. As we monitored those losses

and the anemic recovery, we looked to other regions to learn how they measured

their economic growth and development. Many produce regional scorecards

in order to assess themselves without bias, and our Cape Fear Future board

determined that it was time for our Region to evaluate itself in the same fashion.

This 2015 Regional Economic Scorecard is intended to provide our Region’s

business, governmental, community and academic leaders with objective data for

use in addressing our top development opportunities and challenges.

Our Scorecard will be published annually, so that we may measure our

progress in the key areas of economic development outcomes, human

capital, innovation and entrepreneurship and quality of place. The research,

conducted by Dr. Adam Jones and UNCW’s Swain Center, reflects data

collected from New Hanover, Pender and Brunswick counties.

Our task team selected our “comparative” cities based on population size

as well as a diverse mix of economic assets comparable to our Region.

Charleston and Raleigh were selected as “aspirational” cities – that is, cities

which are not strictly comparable but are well known to people in our Region

and have had recent success in economic development.

How Do We Define the “Wilmington Region?”Historically, the Wilmington MSA has been comprised of New Hanover,

Pender, and Brunswick Counties. In 2012, the federal Office of Management &

Budget removed Brunswick County from the Wilmington MSA and realigned

it as part of the Myrtle Beach MSA. Nonetheless, for purposes of this

Scorecard, it was determined that, where feasible, Brunswick County should

be included in the Wilmington Region’s data. Much of the data reported in

this Scorecard is available on a county level and aggregated to the three-

county “Wilmington Region.” However, Gross Regional Product, a major

economic indicator, is only available at an MSA level. Brunswick County’s

contribution to the Wilmington Region’s GRP was determined through

estimation. In instances where data is reported only on an MSA level and

no estimation has been made for Brunswick County, the two-county (New

Hanover and Pender) data is indicated by the notation “Wilmington MSA.”

Key TakeawaysThe Wilmington Region is exhibiting relatively moderate economic growth, but

has transformational opportunities in entrepreneurship and innovation. Our

quality of place has attracted a talented workforce, despite relatively low annual

pay and slow per capita income growth. Wilmington has enjoyed a reasonably

diverse economy with strong sectors in pharmaceuticals/CROs, healthcare, retail,

and film, although generally our traded sector lags that of our comparative peers.

1. Employment: Our economy is growing in absolute terms, but adjusted for

population growth, the level of economic activity is relatively steady.

2. Large Business v. Small Business: The data show that the Wilmington

Region’s small business sector is very strong. While this indicates a

positive entrepreneurial environment, it also reflects a relative lack of

traded-sector businesses which tend to pay higher wages and grow

regional wealth.

3. Entrepreneurship: The Region has good entrepreneurial growth,

supported organically by the community and by UNCW’s CIE, tech

transfer at UNCW, and privately-owned incubators. However, the data

suggests a lack of growth in small business and an emphasis on the

service and non-traded sectors.

4. Film Industry: This desirable, traded-sector industry is at risk to be lost to

other states which use enhanced tools to attract productions.

2 | Wilmington Regional Economic Scorecard

Introduction

“Developing goals that will enable economic progress can’t be

accomplished without having a baseline of where our Region

stands, especially against peer cities that compete with us

for skilled workers, new business, and the entrepreneurs and

mobile workforce that are driving the new world economy.

This economic scorecard will be a valuable tool in establishing

a clear focus on our Region’s challenges and opportunities,

and, more importantly, can help develop a concerted effort

between our economic development organizations and

leaders to address our needs. Tracking progress on an annual

basis will keep us centered and focused on improving the key

areas that will lead to long-term economic prosperity.”

Michele HolbrookPlant Manager, Corning Incorporated

How to Read the DataThe report examines many indicators of regional economic competitiveness.

Each indicator is compared to the national average. For example, an index of

110 for our Region means that our Region is performing 10% above the U.S.

average. Likewise, an index of 90 means our Region is performing 10% below

the U.S. average.

The report follows the Model for Economic Prosperity Pyramid developed

by Clemson University professors David Barkley and Mark Henry, which

illustrates the building blocks of economic success. The 2015 Regional

Economic Scorecard assesses the economic development outcomes and

competitiveness inputs from the top and bottom of the pyramid model.

Because of the time lag in data availability, this 2015 report highlights data

captured from 2010-2014.

Wilmington Regional Economic Scorecard | 3

Our Comparative Locations

Model for Economic ProsperityEconomic Development Outcome• Economic Output

• Employment

• Earnings & Income

Environment for Development• Industrial Composition

• Physical Infrastructure

• Social, Cultural &

Institutional Environment

Competitiveness Inputs• Human Capital

• Innovative Activity

• Entrepreneurial Environment

• Quality of Place

A task force of business and community leaders selected seven metropolitan areas based on population and

a mix of economic assets comparable to the Wilmington Region. Charleston and Raleigh were selected as

aspirational cities due to their exceptional growth and ability to maintain quality of place.

AspirationalComparative

Asheville, NChigher education, healthcare, arts and culture, tourism, and entrepreneurial environment

Chattanooga, TNhigher education, tourism,

historic, redeveloped riverfront, and arts and culture

Myrtle Beach, SCtourism and entertainment

Roanoke, VAhealthcare, tech research and

higher education

Savannah, GAseaport, working river, military,

creative economy, tourism industry, and coastal location

Pensacola, FLtourism, arts and culture,

business growth, seaport, and coastal location

Mobile, ALseaport, transportation, coastal

location, manufacturing, and foreign investment presence

Charleston, SCtourism, strong manufacturing

base, seaport, higher education, coastal, and working river

Raleigh, NChigher education, technology,

pharmaceutical, and telecommunications

4 | Wilmington Regional Economic Scorecard

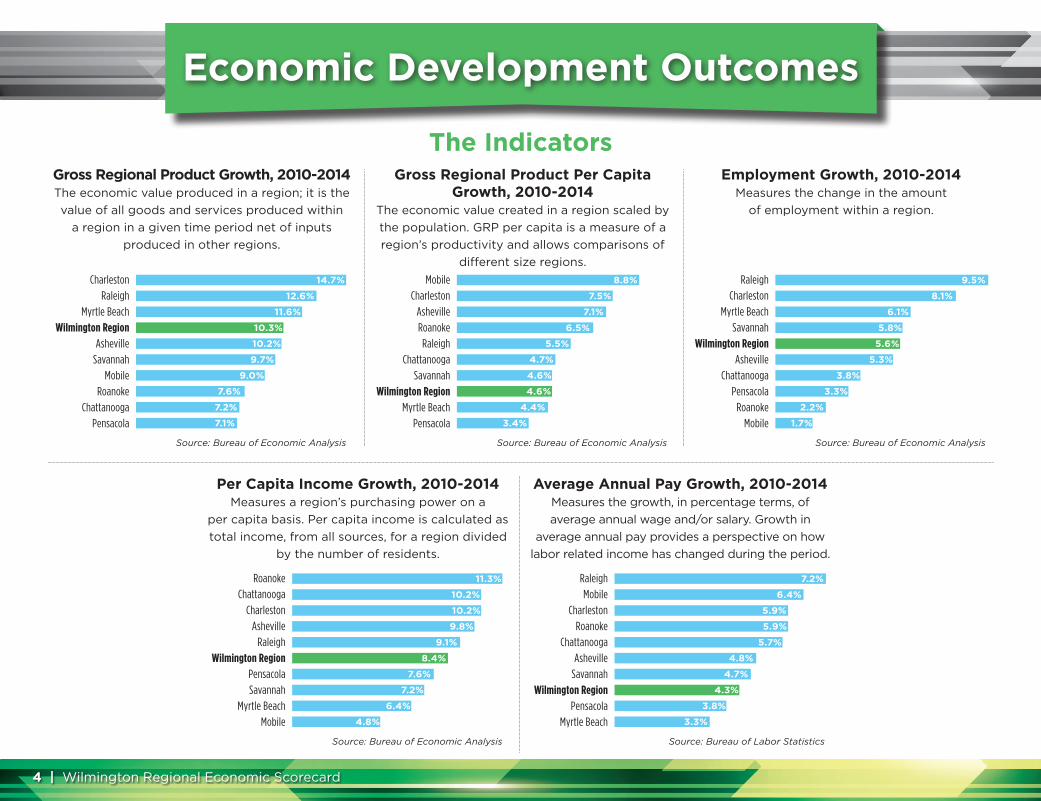

Economic Development Outcomes

The IndicatorsGross Regional Product Growth, 2010-2014The economic value produced in a region; it is the

value of all goods and services produced within

a region in a given time period net of inputs

produced in other regions.

Gross Regional Product Per Capita Growth, 2010-2014

The economic value created in a region scaled by

the population. GRP per capita is a measure of a

region’s productivity and allows comparisons of

different size regions.

Employment Growth, 2010-2014Measures the change in the amount

of employment within a region.

Average Annual Pay Growth, 2010-2014Measures the growth, in percentage terms, of

average annual wage and/or salary. Growth in

average annual pay provides a perspective on how

labor related income has changed during the period.

Per Capita Income Growth, 2010-2014Measures a region’s purchasing power on a

per capita basis. Per capita income is calculated as

total income, from all sources, for a region divided

by the number of residents.

Charleston

Raleigh

Myrtle Beach

Wilmington RegionAsheville

Savannah

Mobile

Roanoke

Chattanooga

Pensacola

Raleigh

Charleston

Myrtle Beach

Savannah

Wilmington RegionAsheville

Chattanooga

Pensacola

Roanoke

Mobile

Raleigh

Mobile

Charleston

Roanoke

Chattanooga

Asheville

Savannah

Wilmington RegionPensacola

Myrtle Beach

Roanoke

Chattanooga

Charleston

Asheville

Raleigh

Wilmington RegionPensacola

Savannah

Myrtle Beach

Mobile

14.7%

12.6%

11.6%

10.3%

10.2%

9.7%

9.0%

7.6%

7.2%

7.1%

8.8%

7.5%

7.1%

6.5%

5.5%

4.7%

4.6%

4.6%

4.4%

3.4%

Source: Bureau of Economic Analysis Source: Bureau of Economic Analysis Source: Bureau of Economic Analysis

Source: Bureau of Economic Analysis

Mobile

Charleston

Asheville

Roanoke

Raleigh

Chattanooga

Savannah

Wilmington RegionMyrtle Beach

Pensacola

9.5%

8.1%

6.1%

5.8%

5.6%

5.3%

3.8%

3.3%

2.2%

1.7%

11.3%

10.2%

10.2%

9.8%

9.1%

8.4%

7.6%

7.2%

6.4%

4.8%

7.2%

6.4%

5.9%

5.9%

5.7%

4.8%

4.7%

4.3%

3.8%

3.3%

Source: Bureau of Labor Statistics

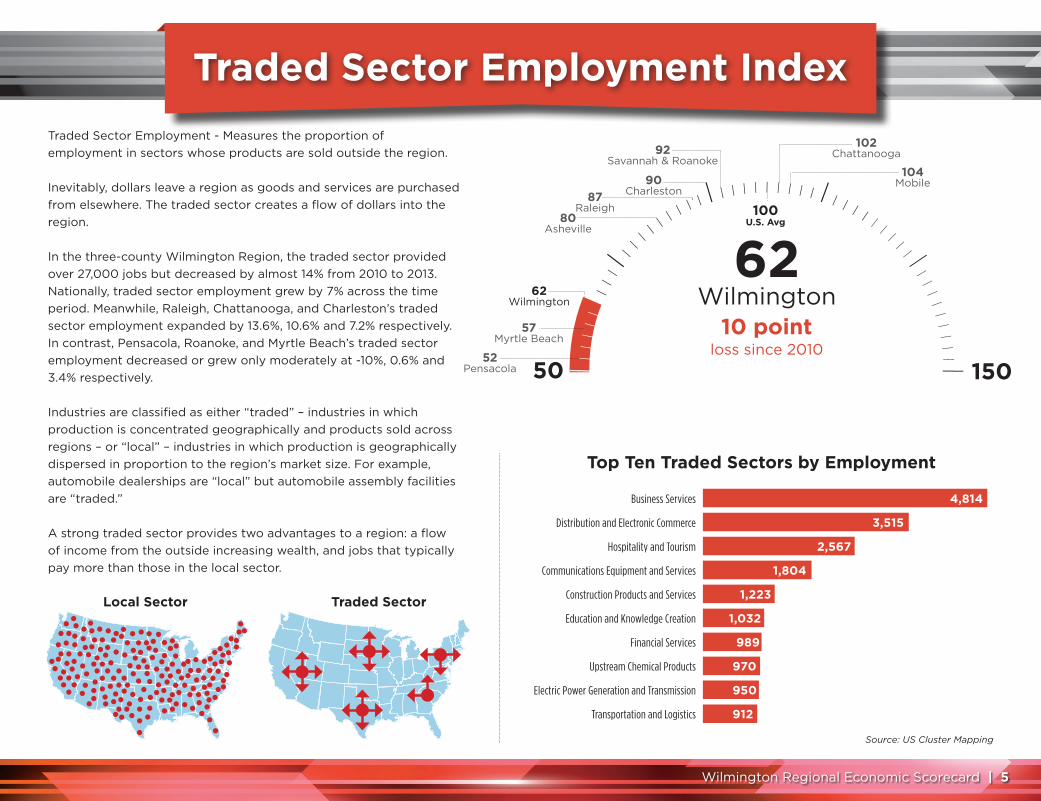

Traded Sector Employment - Measures the proportion of

employment in sectors whose products are sold outside the region.

Inevitably, dollars leave a region as goods and services are purchased

from elsewhere. The traded sector creates a flow of dollars into the

region.

In the three-county Wilmington Region, the traded sector provided

over 27,000 jobs but decreased by almost 14% from 2010 to 2013.

Nationally, traded sector employment grew by 7% across the time

period. Meanwhile, Raleigh, Chattanooga, and Charleston’s traded

sector employment expanded by 13.6%, 10.6% and 7.2% respectively.

In contrast, Pensacola, Roanoke, and Myrtle Beach’s traded sector

employment decreased or grew only moderately at -10%, 0.6% and

3.4% respectively.

Industries are classified as either “traded” – industries in which

production is concentrated geographically and products sold across

regions – or “local” – industries in which production is geographically

dispersed in proportion to the region’s market size. For example,

automobile dealerships are “local” but automobile assembly facilities

are “traded.”

A strong traded sector provides two advantages to a region: a flow

of income from the outside increasing wealth, and jobs that typically

pay more than those in the local sector.

Traded Sector Employment Index

Wilmington Regional Economic Scorecard | 5

| |||||

|||| |

|

||| |

| || | | | | | | | | | | | | | | | | |

|

|| |

||||||||| |

57Myrtle Beach

52Pensacola

92Savannah & Roanoke

80Asheville

50 150

90Charleston87

Raleigh 100U.S. Avg

62Wilmington

10 pointloss since 2010

104Mobile

102Chattanooga

Top Ten Traded Sectors by Employment

Business Services

Distribution and Electronic Commerce

Hospitality and Tourism

Communications Equipment and Services

Construction Products and Services

Education and Knowledge Creation

Financial Services

Upstream Chemical Products

Electric Power Generation and Transmission

Transportation and Logistics

Source: US Cluster Mapping

Local Sector Traded Sector

4,814

3,515

2,567

1,804

1,223

1,032

989

970

950

912

62 Wilmington

| |||||||||| |

|

||| |

| || | | | | | | | | | | | | | |

| ||

|| |

||||||||| |

81Myrtle Beach

109Wilmington

1 pointgain since 201075 125

89Mobile

92Pensacola

94Chattanooga

98Savannah

118Raleigh

109Wilmington

100Asheville

100U.S. Avg

104Charleston & Roanoke

6 | Wilmington Regional Economic Scorecard

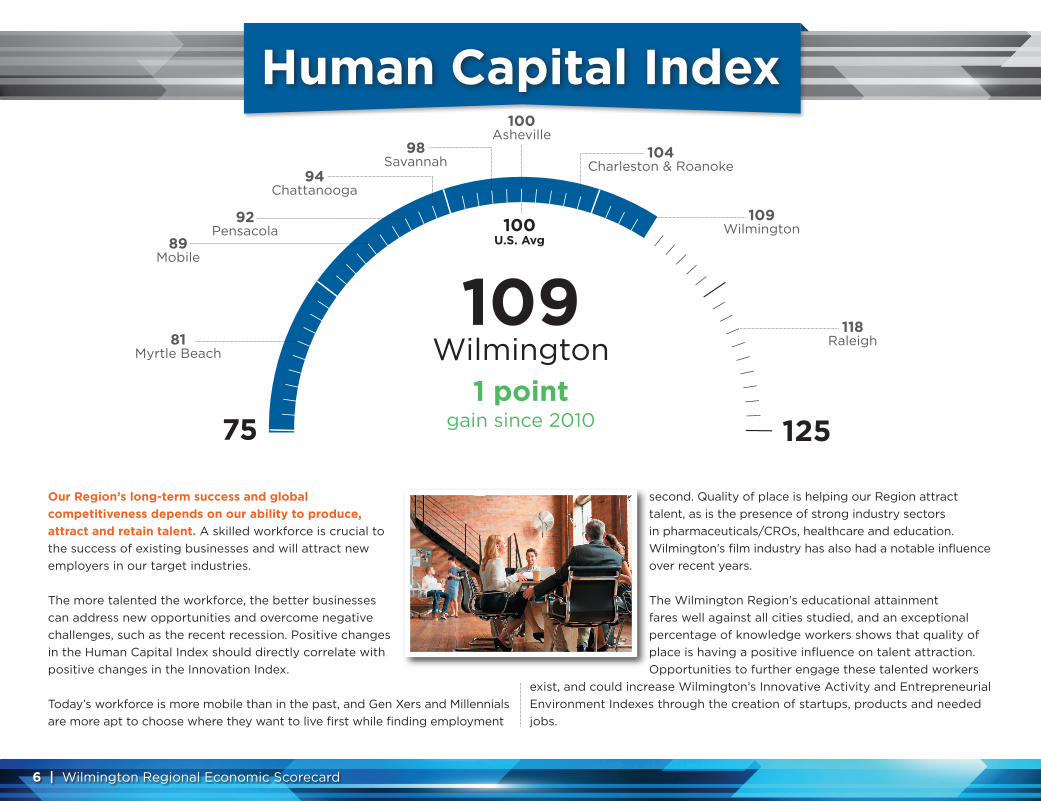

Our Region’s long-term success and global

competitiveness depends on our ability to produce,

attract and retain talent. A skilled workforce is crucial to

the success of existing businesses and will attract new

employers in our target industries.

The more talented the workforce, the better businesses

can address new opportunities and overcome negative

challenges, such as the recent recession. Positive changes

in the Human Capital Index should directly correlate with

positive changes in the Innovation Index.

Today’s workforce is more mobile than in the past, and Gen Xers and Millennials

are more apt to choose where they want to live first while finding employment

second. Quality of place is helping our Region attract

talent, as is the presence of strong industry sectors

in pharmaceuticals/CROs, healthcare and education.

Wilmington’s film industry has also had a notable influence

over recent years.

The Wilmington Region’s educational attainment

fares well against all cities studied, and an exceptional

percentage of knowledge workers shows that quality of

place is having a positive influence on talent attraction.

Opportunities to further engage these talented workers

exist, and could increase Wilmington’s Innovative Activity and Entrepreneurial

Environment Indexes through the creation of startups, products and needed

jobs.

Human Capital Index

125

Wilmington Regional Economic Scorecard | 7

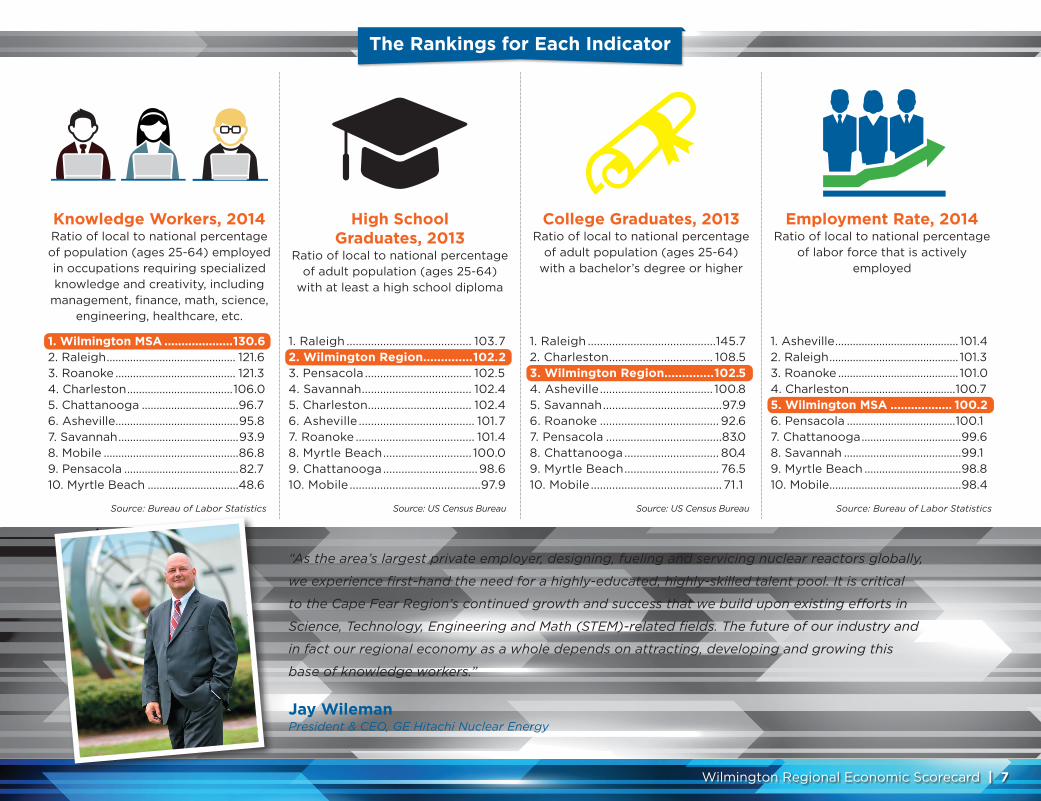

Knowledge Workers, 2014Ratio of local to national percentage of population (ages 25-64) employed in occupations requiring specialized knowledge and creativity, including

management, finance, math, science, engineering, healthcare, etc.

High School Graduates, 2013

Ratio of local to national percentage of adult population (ages 25-64)

with at least a high school diploma

“As the area’s largest private employer, designing, fueling and servicing nuclear reactors globally,

we experience first-hand the need for a highly-educated, highly-skilled talent pool. It is critical

to the Cape Fear Region’s continued growth and success that we build upon existing efforts in

Science, Technology, Engineering and Math (STEM)-related fields. The future of our industry and

in fact our regional economy as a whole depends on attracting, developing and growing this

base of knowledge workers.”

Jay WilemanPresident & CEO, GE Hitachi Nuclear Energy

College Graduates, 2013Ratio of local to national percentage

of adult population (ages 25-64) with a bachelor’s degree or higher

Employment Rate, 2014Ratio of local to national percentage

of labor force that is actively employed

1. Wilmington MSA ....................130.62. Raleigh ............................................ 121.63. Roanoke ......................................... 121.34. Charleston ....................................106.05. Chattanooga .................................96.76. Asheville ..........................................95.87. Savannah .........................................93.98. Mobile ..............................................86.89. Pensacola .......................................82.710. Myrtle Beach ...............................48.6

1. Raleigh ......................................... 103.72. Wilmington Region ..............102.23. Pensacola ................................... 102.54. Savannah .................................... 102.45. Charleston .................................. 102.46. Asheville ...................................... 101.77. Roanoke ....................................... 101.48. Myrtle Beach ............................. 100.09. Chattanooga ...............................98.610. Mobile ...........................................97.9

1. Raleigh ..........................................145.72. Charleston .................................. 108.53. Wilmington Region ..............102.54. Asheville ..................................... 100.85. Savannah .......................................97.96. Roanoke ....................................... 92.67. Pensacola ......................................83.08. Chattanooga ............................... 80.49. Myrtle Beach ............................... 76.510. Mobile ........................................... 71.1

1. Asheville .......................................... 101.42. Raleigh ............................................ 101.33. Roanoke ......................................... 101.04. Charleston ....................................100.75. Wilmington MSA .................. 100.26. Pensacola .....................................100.17. Chattanooga ..................................99.68. Savannah ........................................99.19. Myrtle Beach .................................98.810. Mobile .............................................98.4

The Rankings for Each Indicator

Source: Bureau of Labor Statistics Source: US Census Bureau Source: US Census Bureau Source: Bureau of Labor Statistics

| |||||||||| |

|

||| |

| || | | | | | | | | | | | | | | | | |

|

|| |

||||||||| |

10Myrtle Beach

19Savannah

22Asheville

0 200

84Charleston

30Mobile

41Pensacola

53Wilmington

189Raleigh

100U.S. Avg

28Chattanooga & Roanoke

8 | Wilmington Regional Economic Scorecard

Innovation is critical to developing a region’s

competitive advantage. An environment that generates

new ideas, products and processes encourages

the creation of new businesses, provides growth

opportunities for existing businesses, and encourages

relocation of cutting-edge businesses. The result is often

new, higher-wage jobs for area residents.

Positive changes in our Innovative Activity Index will be

fueled by graduating, retaining and attracting talent with

needed workforce skills, particularly knowledge and STEM workers.

There is a staggering disparity within the peer and aspirational cities in the

Innovative Activity data sets, with ranges as broad as 0 to 233. Overall the

Wilmington Region does well against its peer cities, leading in nearly every

area. Despite losing ground against the national average

since 2010, Wilmington still shows good employment

levels in technical positions, moderate activity in issuance

of patents, and reasonably strong performance in

the ratio of local to national science-related graduate

students.

In Raleigh’s rankings, influence of North Carolina

State University and some from the Research Triangle Park

(RTP)* is present in the contrast in both patents issued

and NIH/NSF/NEA funding. It should be noted that the NIH/NSF/NEA funding

figures are based on only one year of data, thereby creating the potential that

one large grant could skew the outcomes and create large fluctuations on

an annual basis. NC State University factors prominently in Raleigh’s ratio of

science-related graduate students.

* RTP is divided between Wake and Durham MSAs.

Innovative Activity Index

53Wilmington

18 pointloss since 2010

Wilmington Regional Economic Scorecard | 9

Employment in Technical Positions, 2014

Ratio of local to national percentage of employment in computer, science,

and engineering occupations

NIH/NSF/NEA Funding, 2014

Ratio of local to national funding from NIH, NSF, and NEA per local job

“The Innovative Activity Index represents a critical component in regional economic analysis.

The report provides entrepreneurs and investors with much-needed information about the area’s

capacity to support innovation. Empowered by the report’s results, regional leaders are better

positioned to make data-driven decisions about our vision and goals for increasing economic

growth across Southeastern North Carolina.”

Jose V. “Zito” SartarelliChancellor, University of North Carolina Wilmington

Patents Issued, 2013Ratio of local to national, number of patents issued in an area, per 10,000

workers

Science Related Graduate Students, 2013

Ratio of local to national graduate students in health science, science,

and engineering per 10,000 residents

1. Raleigh ............................................ 152.32. Charleston ...................................... 97.83. Wilmington Region ................ 73.44. Roanoke ..........................................66.65. Chattanooga .................................63.26. Pensacola ...................................... 60.57. Mobile ...............................................59.88. Savannah ........................................59.09. Asheville ..........................................45.410. Myrtle Beach ...............................22.4

1. Charleston ..................................... 186.22. Raleigh .............................................83.23. Mobile ..............................................43.14. Wilmington Region .................. 6.15. Roanoke ............................................4.96. Chattanooga ................................... 2.37. Asheville ............................................ 2.18. Savannah ........................................... 1.89. Pensacola .........................................0.510. Myrtle Beach .................................0.0

1. Raleigh ........................................... 263.62. Wilmington Region ................ 43.23. Roanoke ..........................................38.54. Asheville ......................................... 37.0 5. Charleston .......................................31.36. Pensacola .......................................22.37. Chattanooga ...................................21.08. Mobile ...............................................19.59. Myrtle Beach .................................. 17.610. Savannah ........................................ 12.3

1. Raleigh .........................................234.02. Wilmington Region ............... 85.93. Pensacola ..................................... 79.24. Charleston ................................... 35.65. Chattanooga ................................ 21.86. Asheville ......................................... 0.07. Roanoke .......................................... 0.08. Savannah ........................................ 0.09. Myrtle Beach ................................. 0.010. Mobile ............................................ 0.0

The Rankings for Each Indicator

Source: Bureau of Labor Statistics Source: NIH, NSF, NEA, Bureau of Economic Analysis Source: U.S. Patent & Trademark Office, Bureau of Economic Analysis

Source: NSF Survey of Graduate Students and Postdocs in Science and Engineering

$

| |||||||||| |

|

||| |

| || | | | | | | | | | | | | | |

| ||

|| |

||||||||| |75 125

87Mobile

92Asheville

84Pensacola

94Myrtle Beach

78Savannah

82Chattanooga & Roanoke

105Charleston

108Wilmington100

U.S. Avg

104Raleigh

10 | Wilmington Regional Economic Scorecard

Entrepreneurs flourish in a supportive environment,

adding to a region’s new business creation and growth.

An unfavorable climate may drive away startups, leading

them to seek more hospitable communities.

Growth of small businesses – in particular the Business

Services Sector – is dependent on the continued

growth of the Region’s GRP and economic engines

of growth, including (but not limited to) the industry

clusters identified in the Garner Report: life/marine

sciences research and development, high-value office operations, precision

manufacturing, and aircraft assembly, modification and maintenance.

The Wilmington Region’s first-place ranking in Entrepreneurial Environment,

slightly above even the aspirational cities of Charleston and Raleigh, is likely

cause for both celebration and concern. While there is clearly a growing and

desirable base of entrepreneurial activity with the ability to grow into larger

businesses providing well-paying jobs, too many of our area’s entrepreneurial

ventures are service-based, will never grow beyond a

handful of employees, and don’t add significantly to the

tax base. The data suggests what many have seen as a

core problem for some time - people wishing to stay in

the area are often unable to find suitable employment, so

they are forced to create their own jobs.

Nonetheless, entrepreneurial spirit is a positive asset for

our Region, and organizations like the UNCW Center

for Innovation & Entrepreneurship, the Small Business

Technology Development Center, UNCW’s CREST Research Park, and

privately owned entities like Castle Branch’s tekMountain incubator and

Elite Innovations’ Makerspace are providing valuable support for start-ups,

with the goal of helping them grow into larger ventures. Supporting and

expanding our Region’s innovation assets should yield positive results. A

notable example is the community’s support for Cucalorus Connect, a 3-day

conference on capital, entrepreneurship, innovation and entertainment with a

focus on the intersection between business and creativity.

Entrepreneurial Environment Index

108Wilmington

3 pointloss since 2010

Wilmington Regional Economic Scorecard | 11

Concentration of Small to Mid-size Businesses, 2013Small to mid-size firms per 1,000

employees relative to national ratio

Total Establishments, 2013Total establishments per 1,000

employees relative to national ratio

“Entrepreneurism lives in the heart of all good communities across America and while it

may seem like a trend in some communities, it has been commonplace for Wilmington.

Our community, for the last few years, has redefined itself and turned our sign around to

OPEN for Businesses. Funds are available, talent is building, tech is alive and the pockets

of entrepreneurs are spreading from river to ocean. It’s exciting to watch and even more

exciting to be a part of the build.”

Shaun OlsenPresident, CLOUDWYZE, INC

Proprietor’s Income Share, 2013

Business owner’s income as a percentage of total income for the area relative to national percentage

Business Services, 2013Percentage of business services

employment to total employment relative to national percentage

1. Wilmington Region .............. 137.52. Myrtle Beach ..............................136.73. Asheville ......................................123.84. Pensacola .....................................118.95. Charleston .................................. 108.66. Raleigh ........................................ 103.77. Savannah .................................... 100.68. Roanoke........................................94.19. Mobile ............................................. 91.610. Chattanooga ............................. 83.7

1. Wilmington Region .............. 137.32. Myrtle Beach ..............................136.53. Asheville ......................................123.74. Pensacola .....................................118.75. Charleston .................................. 108.56. Raleigh ........................................ 103.77. Savannah .................................... 100.58. Roanoke........................................94.19. Mobile ............................................. 91.710. Chattanooga ............................. 83.8

1.Charleston ....................................... 121.12. Wilmington Region ................112.73. Chattanooga ...............................109.64. Raleigh .......................................... 103.85. Mobile ..............................................93.16. Asheville ..........................................83.27. Myrtle Beach ..................................76.98. Roanoke ...........................................61.49. Savannah ....................................... 60.010. Pensacola ......................................35.5

1. Raleigh ......................................... 106.42. Charleston ....................................80.43. Roanoke ........................................ 76.74. Mobile ........................................... 72.75. Pensacola ..................................... 63.56. Chattanooga ................................ 51.97. Savannah ......................................50.38. Wilmington Region............... 43.09. Asheville ....................................... 36.310. Myrtle Beach ............................. 24.5

The Rankings for Each Indicator

Source: US Census Bureau Source: US Census Bureau Source: Bureau of Economic Analysis Source: US Cluster Mapping

| |||||||||| |

|

||| |

| || | | | | | | | | | | | | | | | | |

|| |

||||||||| |50 150

91Pensacola

134Asheville

120Roanoake124

Wilmington

104Charleston

107Raleigh & Myrtle Beach

92Mobile

93Chattanooga

100Savannah

100U.S. Avg

124WilmingtonNo change

since 2010

12 | Wilmington Regional Economic Scorecard

Global competition has made attracting and retaining

a talented workforce one of the most critical issues in

economic development. Highly educated workers aren’t

bound by location. Strong demand for their skills allows

flexibility in where they choose to live and work to a

greater extent than any other time in history.

One of the Wilmington Region’s biggest assets is quality

of place, including its beaches, riverfront, the largest

historic district in the state, and an enviable climate. Wilmington also

scores very well on less subjective factors such as culture and recreation,

healthcare access, and air quality. The relatively high percentage of healthcare

practitioners per capita is likely influenced by the attraction of quality of place

in luring medical professionals to the area, although our Region’s growing

retiree demographic is also likely a driver of the healthcare sector.

Measuring a community’s arts and entertainment assets using NAICS Code

71 captures not only traditional urban arts and entertainment activity,

but other elements as well, such as tourist-oriented

entertainment and the movie, television and film

industry. Myrtle Beach’s focus on creating a vacation

destination accounts for its high ranking in arts and

entertainment employment. The Wilmington Region’s

strength in this category is likely due to the influence

of our tourism industry as well as our historically robust

film industry. The extent to which the recent changes

to our state’s film incentives program and increased

competition from other states negatively affect the Wilmington Region’s

arts and entertainment employment remains to be seen.

Although an informal poll of Wilmington drivers might not support this

conclusion, the data shows that our Region’s rush-hour travel time ranks

in the middle of the pack relative to our comparative cities. However,

foreseeable growth in the Region, especially in Brunswick County, remains a

concern, and rush-hour travel times will likely suffer in the mid- to long-term

without additional investments in our regional transportation infrastructure.

Quality of Place Index

Wilmington Regional Economic Scorecard | 13

Culture and Recreation, 2013

Percent of employment in the arts, entertainment, and recreation

(NAICS 71) relative to national percentage

Healthcare Access, 2013Number of healthcare practitioner and technical positions per capita

relative to national average

“Our quality of place is crucial as we compete with other regions for the same

skilled workforce. Wilmington continues to be an attractive option for retirees.

Over 50% of the residents in our senior living communities in-migrated from

outside this area. Attracting and retaining a talented workforce is more

difficult. Highly-educated workers and retirees come here for the same

reasons, not just our mild climate and beaches, but also the artistic, cultural,

and historical offerings. These assets, along with high quality hospitals and

overall healthcare services, also drive more medical professionals to the area.

Maintaining our transportation infrastructure is an obstacle we face as our

Region grows. Short commutes between moderately priced housing and

employment centers are crucial for young professionals and the long-term

growth of the entire workforce.”

Will PurvisChief Development Officer, Liberty Healthcare Management, Inc.

Crime Rate, 2012Violent crimes per capita relative to

national crime rate (higher number means less crime)

Rush Hour Travel Times, 2013

Average commute time of workers leaving home between 6:00-8:30 AM

relative to national average (higher number means less travel time)

Air Quality, 2013Percentage of days with air quality

measured as “good” relative to national average.

1. Myrtle Beach ...............................193.22. Asheville ......................................142.23. Wilmington Region ..............130.74. Raleigh ......................................... 110.45. Charleston ....................................98.66. Pensacola ..................................... 92.67. Savannah .......................................87.48. Chattanooga ............................... 72.49. Roanoke........................................69.010. Mobile .......................................... 58.0

1. Roanoke .........................................160.02. Wilmington MSA ....................143.13. Asheville ....................................... 137.44. Charleston ................................... 125.95. Chattanooga ................................123.16. Mobile .............................................110.87. Savannah ...................................... 102.28. Pensacola ......................................96.79. Raleigh ...........................................88.910. Myrtle Beach ..............................52.4

1. Asheville, NC ............................... 173.72. Raleigh, NC .................................158.03. Roanoke, VA ...............................153.04. Wilmington Region ............. 127.35. Savannah, GA .............................118.96. Charleston, SC ............................ 93.77. Myrtle Beach, SC .........................77.28. Chattanooga, TN ....................... 76.09. Mobile, AL .................................... 70.610. Pensacola, FL ............................66.6

1. Wilmington Region ............. 104.92. Mobile .......................................... 104.93. Roanoke ........................................99.94. Myrtle Beach ...............................99.05. Charleston ....................................98.06. Asheville .......................................96.67. Pensacola ..................................... 89.38. Savannah ......................................84.69. Chattanooga ............................... 79.710. Raleigh .........................................77.0

1. Asheville ........................................119.12. Roanoke ........................................118.03. Myrtle Beach ...............................115.44. Mobile ...........................................113.35. Wilmington Region...............113.06. Chattanooga ...............................112.17. Pensacola .................................... 110.48. Savannah .................................... 109.29. Charleston ................................. 102.910. Raleigh ...................................... 100.9

The Rankings for Each Indicator

Source: Bureau of Economic Analysis Source: Bureau of Labor Statistics Source: Federal Bureau of Investigation/ICPSR Source: US Census Bureau

Source: US Environmental Protection Agency

TICKET

14 | Wilmington Regional Economic Scorecard

About the Wilmington Chamber of CommerceThe Wilmington Chamber of Commerce is the

largest membership-based business association

in Southeastern North Carolina. Our mission

is to ensure economic prosperity throughout

the Region. This is accomplished by creating a

diverse organization that serves as a strong voice

for businesses in the Greater Wilmington area;

offering unique membership benefits, services

and education; and challenging government

officials to address long-term community and

business interests. Our mission is enhanced through proactive leadership and

partnerships throughout our Region.

Despite governmental chartering, the Wilmington Chamber is not a

governmental entity. Instead, the Chamber has a long tradition of activity

in North Carolina as a membership-based, nonprofit organization of diverse

membership. Members and volunteers share the goals of improving the

economy and enhancing the overall quality of life in our community by

harnessing the collective vision and power of local business.

About Cape Fear Future The Chamber’s flagship initiative, Cape Fear

Future (CFF), began as an idea developed at

the Wilmington Chamber of Commerce Board

of Directors 2006 Retreat to further develop

the Cape Fear region’s knowledge sector economy to promote economic

development and ensure the future prosperity of the Region. The effort is

helping the Region keep stride with globalization and remain competitive with

other cities vying for skilled workers. The world has witnessed the impact that

the knowledge sector has had on economic growth through the development

of new businesses, business models, and technological innovation.

Priority areas for CFF include:

• Quality of Life: improve area amenities to attract and retain knowledge

sector workers, and design and develop strategies and plans aimed at

improving the special characteristics of Wilmington’s quality of place;

• Entrepreneurship: help foster job creation through support of UNCW’s

Center for Innovation and Entrepreneurship; and

• Education & Workforce Development: improve K-12 education with STEM

(science, technology, engineering, mathematics) integration to better

prepare and equip our future workforce.

Recent CFF initiatives have included:

• Starting the STEM program Project Lead The Way at Trask Middle School

and funding the program for 6th, 7th and 8th grade classes;

• Providing substantial funding for UNCW’s Center for Innovation and

Entrepreneurship;

• Advocating for additional open space and a signature park in downtown

that helped lead to the expansion and revitalization of Riverfront Park and

the purchase of new park space adjacent to the Wilmington Convention

Center;

• Hosting the Crime Hurts Kids…and Business event to fund the Youth

Enrichment Zone Summer Initiative aimed at reducing summer learning

loss in at-risk youth;

• Partnering with UNCW on creation of a new website that lists area STEM

resources; and

• Creation of this Economic Scorecard to provide our Region’s business,

governmental, community and academic leaders with unbiased data to

help focus a collective effort to address our challenges and highlight

strengths.

“The importance of attracting and

keeping talented folks in Wilmington

cannot be understated. We need the

next generation of workers prepared

for a high-tech work environment, and

investments to that end will reap huge

rewards for the businesses in our area.

It is investments like these that have

benefitted Live Oak, and supported

our rapid growth, as they say ‘a rising

tide floats all boats.’ From the UNCW

Cameron School of Business, to many

other professional development

programs, our community is up for the

challenge of meeting these demands.”

Chip MahanChairman & CEO, Live Oak Bank

Wilmington Regional Economic Scorecard | 15

Cape Fear Future Board of DirectorsHal Kitchin, McGuireWoods LLP, Chairman

Charlie Mattox, BB&T

Chris Boney, LS3P Associates LTD

Connie Majure-Rhett, Wilmington Chamber of Commerce

John Gizdic, New Hanover Regional Medical Center

Mitch Lamm, First Citizens Bank & Trust

Rickey Godwin, McGladrey LLP

Rob Kaiser, Greater Wilmington Business Journal

Regional Economic Scorecard Task TeamHal Kitchin, McGuireWoods LLP

John Nelms, Duke Energy

Glenn Harbeck, City of Wilmington

Beth Schrader, New Hanover County

Robin Spinks, Greenfield Development

Dean Robert Burrus, UNCW Cameron School of Business

Dr. Thomas Porter, UNCW Cameron School of Business

Dr. Adam Jones, UNCW Cameron School of Business

Ryan C. Beckner, UNCW Intern

Designed and published by SC Biz News

www.scbiznews.com | 843.849.3143

Produced for the community by:

Cape Fear FutureAn initiative of the Wilmington Chamber of Commerce

One Estell Lee Place | Wilmington, NC 28401

910.762.2611 | www.wilmingtonchamber.org

View the Economic Scorecard online at www.wilmingtonchamber.org