redefining value 1. complexpuzzle complicated world

TRANSCRIPT

Redefining Value

1

COMPLEX PUZZLE

Complicated World

Ecological Footprint = 1,5

Collaboration

Improve Business Case

Bu

sin

ess

So

lutio

ns

Today

Scaling up requires 3 key elements

PRIORITY AREAS

ACTION2020

TO REACH SOCIETAL MUST-HAVES

IMPROVE THE BUSINESS CASE

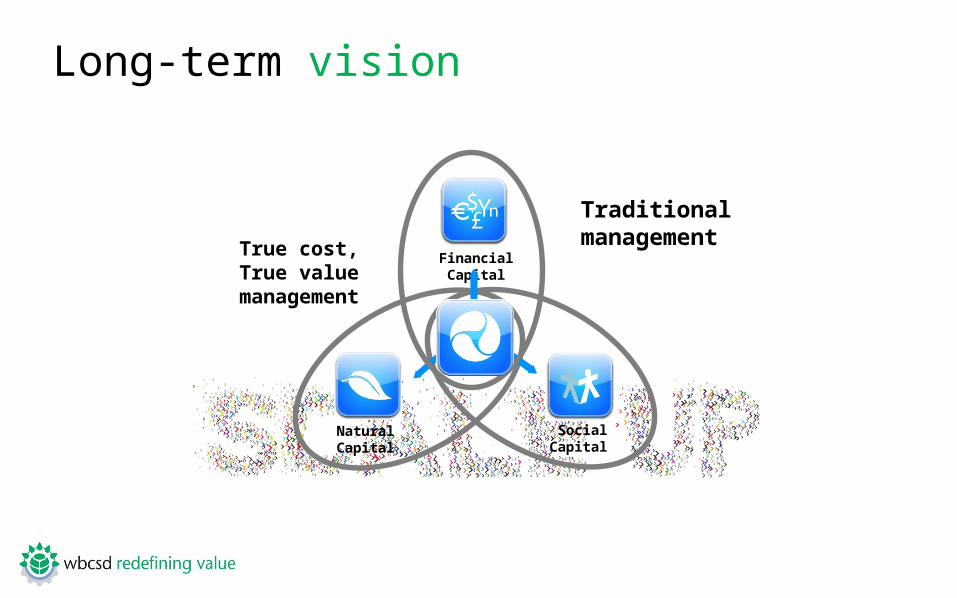

Long-term vision

True cost, True value management

Traditional managementFinancial

Capital

Natural Capital

Social Capital

Business Manageme

nt

Transformation Needed

Collaboration

Improve Business Case

Bu

sin

ess

Solu

tion

s

Today

PRIORITY AREAS

ACTION2020

TO REACH SOCIETAL MUST-HAVES

Cost of Risk

Radical Transparency

Changing the rulesof the game

Capital Market Valuations

WBCSD Redefining Value

14

Integrate natural and social capital measurement and valuation into corporate performance management.

Improve the effectiveness of non-financial internal and external reporting.

Measurement, valuation and reporting reflect the true value of a company and discloses true profit and true cost.

Accelerate progress to a world where more sustainable companies are recognized and rewarded, and therefore are more successful.

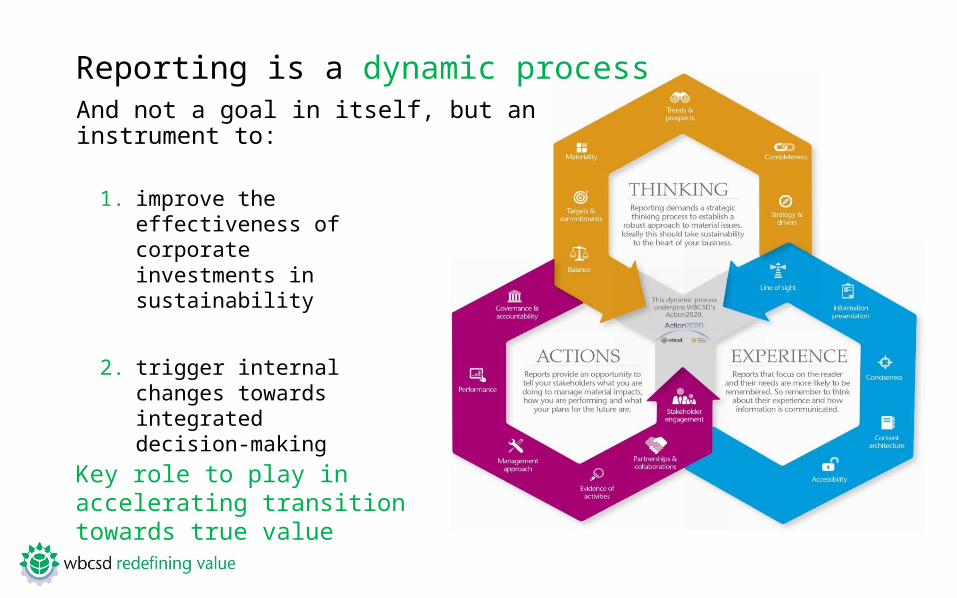

TRENDS in CORPORATE REPORTING

Reporting is a dynamic processAnd not a goal in itself, but an instrument to:

1. improve the effectiveness of corporate investments in sustainability

2. trigger internal changes towards integrated decision-making

Key role to play in accelerating transition towards true value

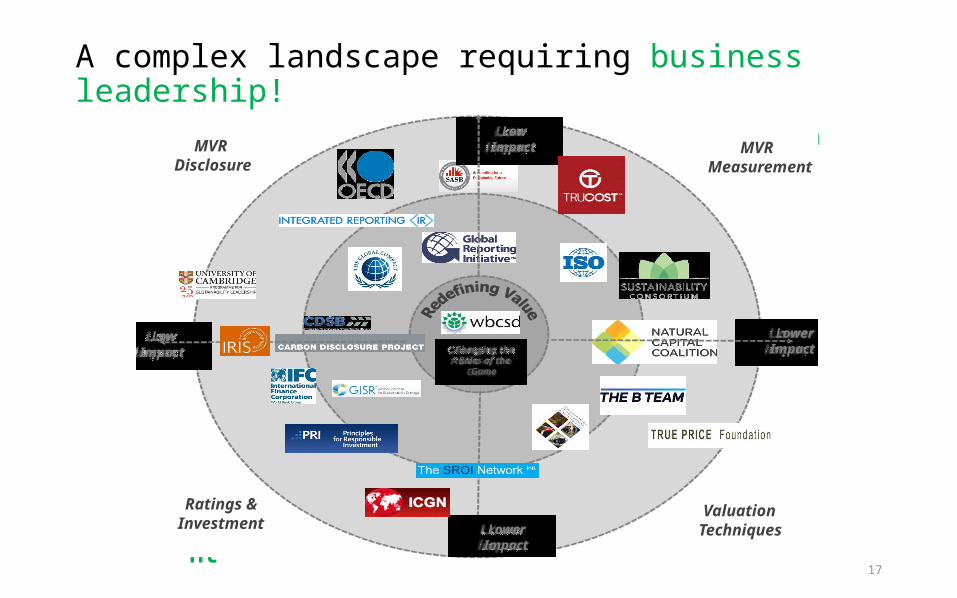

A complex landscape requiring business leadership!

17

Disclosure Measurement

ValuationRating & Investment

MVR Disclosure

MVRMeasurement

ValuationTechniques

Ratings & Investment

LowImpact

Lower Impact

Low Impact

Changing the Rules of the

Game

LowerImpact

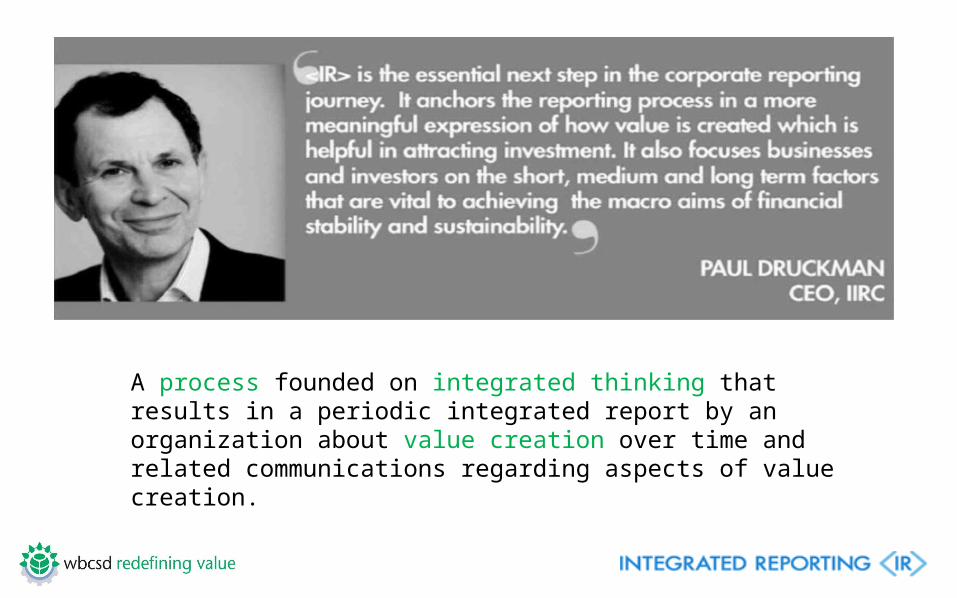

A process founded on integrated thinking that results in a periodic integrated report by an organization about value creation over time and related communications regarding aspects of value creation.

IIRC uptake: dependencies on capitals

Votorantim Group

And more …

• SASB established in the US in 2013 aims to develop sustainability accounting standards to support publicly-listed corporations disclose material factors in compliance with the US SEC requirements

• GRI G4 guidelines issued in 2013 with a strengthened focus on materiality (stakeholder approach)

• CDSB is expanding its Climate Change Reporting Framework to include information about environmental matters in mainstream corporate reports to be launched in 2015

• EU passed legislation to require member businesses (>500 employees and/or public interest) to disclose sustainability performance last April

20

INTEGRATED REPORTING

Financial Accounts

Accounting Principles- GAAP -

Management Accounts

FINANCIAL CAPITAL

Non-Financial Reporting

Non-Financial Principles- GASP -

NATURAL CAPITAL

SOCIAL CAPITAL

HOW-WHAT

Meaningful transparency

Comparability& Materiality

Better informed decisions

EP&L and other methodologies

SP&L and other methodologies

Natural Capital Protocol

Social Capital Protocol

TRUE VALUE

INTEGRATED VALUATION

What about corporate practice? Less than 12% of reports reviewed reflect those sustainability

issues considered to be material to the business.

80% of WBCSD members produce a stand-alone

sustainability report with the rest developing self-declared

integrated reports

75% use the GRI Guidelines with an upward trend to

combine the use of several frameworks

60% of total reports reviewed have some form of assurance

on their sustainability disclosures with limited level as the

dominant form

When known, the average time period between year-end and

the publication date is approximately six months reflecting a

disconnect between sustainability and financial reporting

cycles

22

23

Internal decision-making → External disclosureManagement tools →Reporting frameworks

WBCSD is not new to this space…

Social Profit & Loss AccountFeasibility Study

25

Natural and Social Capital Protocol Components

Protocol Frameworks

Sector Initiativesstandardized metrics / methodologies by

sector

Measurement & Valuation of Action 2020 Priority AreasMinimum standards > best practice > methodologies > KPIs

Practical Methodologies & Guidelines

Approaches to measurement & valuation, e.g. S P&L; E P&L; others

Metrics

Key Performance Indicators > Units of Measurement, incl. from SASB; GRI

Purpose > Principles > Scope & boundaries > Overview of Components

Human Rights

Skills & Employment

Inclusive Business

Rural Livelihoods

WaterClimate &

EnergyEcosystems &

Land Use

Sustain-able

Lifestyles

Chemicals

Forests Mobility Cement

Top-down Elements

Bottom-up Elements

26

• Generic Natural Capital Protocol

• Sector guides for Food & Beverage + Apparel

• Pilot testing

• Overall coordination• Multi-stakeholder

consultation process

27

28