ready reckoner - post budget 2020revenue ready reckoner income earners by income tax and usc rates...

TRANSCRIPT

Ready Reckoner - Post Budget 2020

This Version: October 2019

Ready Reckoners are provided for the following taxes and duties:

Pages 2-11

Deposit Interest Retention Tax (DIRT) Page 12

Life Assurance Exit Tax (LAET) Page 13

Capital Gains Tax (CGT) Page 14

Capital Acquisition Tax (CAT) Pages 15-18

Stamp Duty Page 19

Excise Pages 20-25

Value Added Tax (VAT) Pages 26

Local Property Tax (LPT) Page 27

Please note that the costings provided in this Ready Reckoner are estimates and should be treated as such.

Unless otherwise indicated, costings assume no behavioural change.

In the case of large relative changes to tax rates or allowances, the cost or yield may not be directly in line with estimates shown.

Every reasonable effort has been made to ensure that the information provided is as accurate and clear as possible.

Revenue's Statistics webpage: http://www.revenue.ie/en/corporate/information-about-revenue/statistics/index.aspx

Email: [email protected]

Income Tax & Universal Social Charge

1

Revenue Ready Reckoner

Income Tax & Universal Social Charge

The Income Tax & Universal Social Charge (USC) Ready Reckoner covers the following:

Page 3

Page 4

Page 5

Cost of increasing Income Tax credits Page 6

Cost of widening of Income Tax standard rate bands Page 7

Cost of increasing USC rate bands Page 8

Cost of increasing Income Tax exemption limits Page 9

Cost of Indexation Page 10

Changes to Income Tax relief on pensions Page 11

These following costs / yields are based on 2020 estimates from the Revenue tax forecasting model using latest actual data for the year

2017, adjusted as necessary for income, self-employment and employment trends in the interim.

Increases and decreases to Income Tax and USC rates

Income earners by Income Tax and USC rates in 2020

Income earners by gross income range in 2020

2

Revenue Ready Reckoner

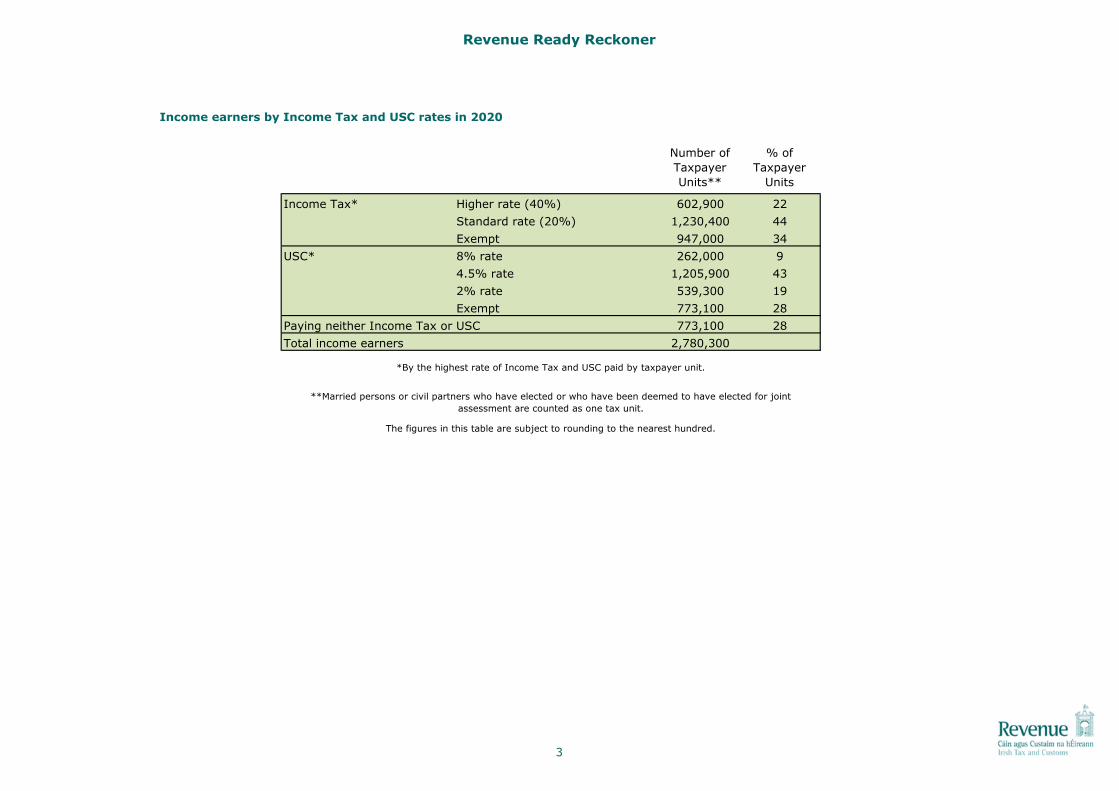

Income earners by Income Tax and USC rates in 2020

Income Tax* Higher rate (40%) 602,900 22

Standard rate (20%) 1,230,400 44

Exempt 947,000 34

USC* 8% rate 262,000 9

4.5% rate 1,205,900 43

2% rate 539,300 19

Exempt 773,100 28

Paying neither Income Tax or USC 773,100 28

Total income earners 2,780,300

*By the highest rate of Income Tax and USC paid by taxpayer unit.

The figures in this table are subject to rounding to the nearest hundred.

Number of

Taxpayer

Units**

**Married persons or civil partners who have elected or who have been deemed to have elected for joint

assessment are counted as one tax unit.

% of

Taxpayer

Units

3

Revenue Ready Reckoner

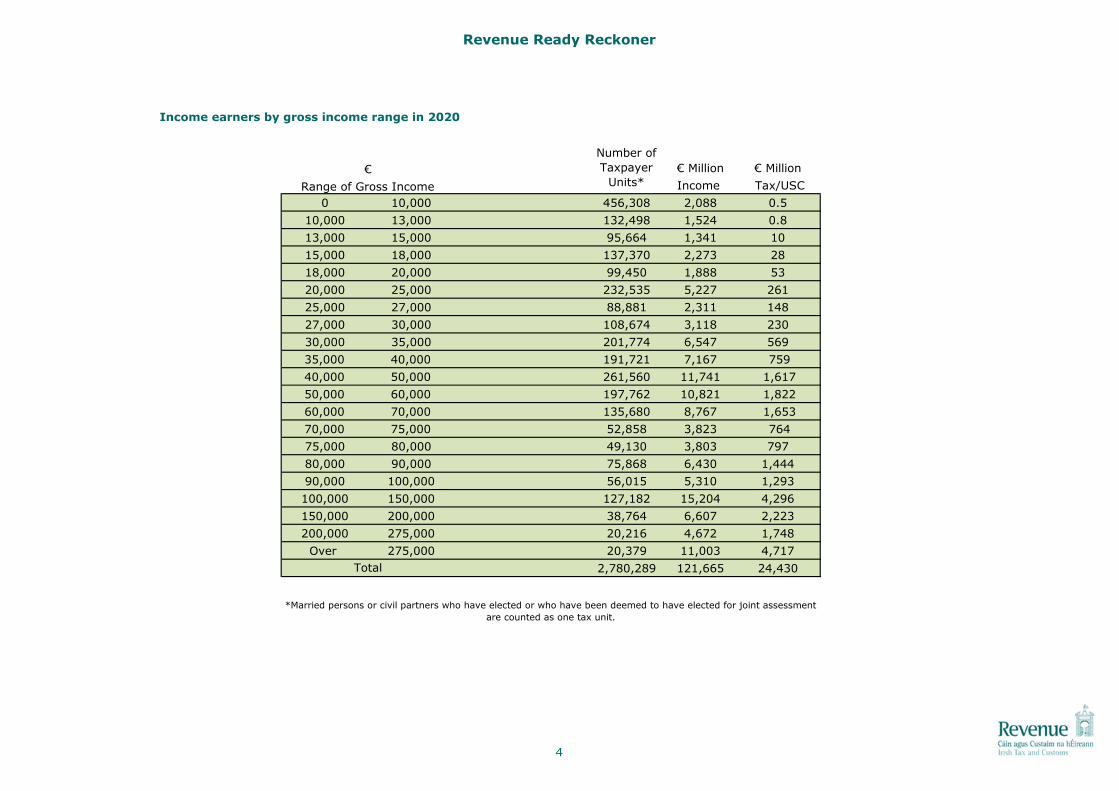

€ Million € Million

Income Tax/USC

0 10,000 456,308 2,088 0.5

10,000 13,000 132,498 1,524 0.8

13,000 15,000 95,664 1,341 10

15,000 18,000 137,370 2,273 28

18,000 20,000 99,450 1,888 53

20,000 25,000 232,535 5,227 261

25,000 27,000 88,881 2,311 148

27,000 30,000 108,674 3,118 230

30,000 35,000 201,774 6,547 569

35,000 40,000 191,721 7,167 759

40,000 50,000 261,560 11,741 1,617

50,000 60,000 197,762 10,821 1,822

60,000 70,000 135,680 8,767 1,653

70,000 75,000 52,858 3,823 764

75,000 80,000 49,130 3,803 797

80,000 90,000 75,868 6,430 1,444

90,000 100,000 56,015 5,310 1,293

100,000 150,000 127,182 15,204 4,296

150,000 200,000 38,764 6,607 2,223

200,000 275,000 20,216 4,672 1,748

Over 275,000 20,379 11,003 4,717

2,780,289 121,665 24,430

Number of

Taxpayer

Units*€

Total

Income earners by gross income range in 2020

*Married persons or civil partners who have elected or who have been deemed to have elected for joint assessment

are counted as one tax unit.

Range of Gross Income

4

Revenue Ready Reckoner

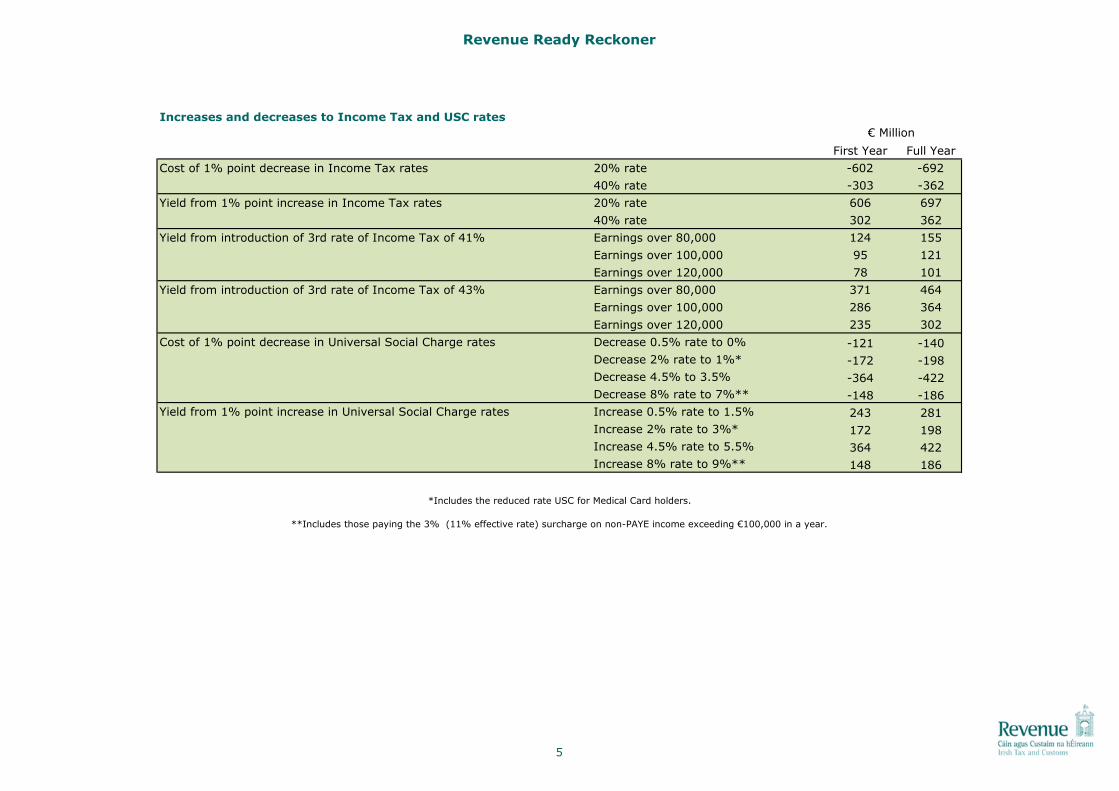

Increases and decreases to Income Tax and USC rates

First Year Full Year

Cost of 1% point decrease in Income Tax rates 20% rate -602 -692

40% rate -303 -362

Yield from 1% point increase in Income Tax rates 20% rate 606 697

40% rate 302 362

Yield from introduction of 3rd rate of Income Tax of 41% Earnings over 80,000 124 155

Earnings over 100,000 95 121

Earnings over 120,000 78 101

Yield from introduction of 3rd rate of Income Tax of 43% Earnings over 80,000 371 464

Earnings over 100,000 286 364

Earnings over 120,000 235 302

Cost of 1% point decrease in Universal Social Charge rates Decrease 0.5% rate to 0% -121 -140

Decrease 2% rate to 1%* -172 -198

Decrease 4.5% to 3.5% -364 -422

Decrease 8% rate to 7%** -148 -186

Yield from 1% point increase in Universal Social Charge rates Increase 0.5% rate to 1.5% 243 281

Increase 2% rate to 3%* 172 198

Increase 4.5% rate to 5.5% 364 422

Increase 8% rate to 9%** 148 186

*Includes the reduced rate USC for Medical Card holders.

**Includes those paying the 3% (11% effective rate) surcharge on non-PAYE income exceeding €100,000 in a year.

€ Million

5

Revenue Ready Reckoner

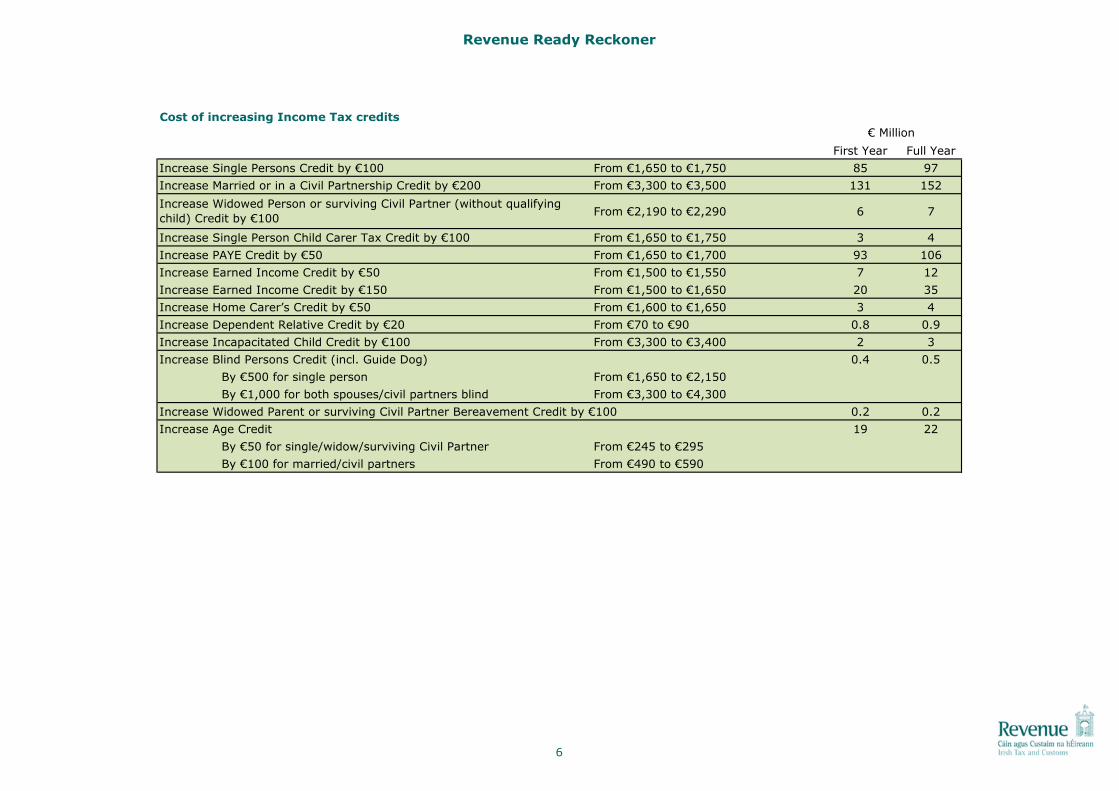

Cost of increasing Income Tax credits

First Year Full Year

Increase Single Persons Credit by €100 From €1,650 to €1,750 85 97

Increase Married or in a Civil Partnership Credit by €200 From €3,300 to €3,500 131 152

From €2,190 to €2,290 6 7

Increase Single Person Child Carer Tax Credit by €100 From €1,650 to €1,750 3 4

Increase PAYE Credit by €50 From €1,650 to €1,700 93 106

Increase Earned Income Credit by €50 From €1,500 to €1,550 7 12

Increase Earned Income Credit by €150 From €1,500 to €1,650 20 35

Increase Home Carer’s Credit by €50 From €1,600 to €1,650 3 4

Increase Dependent Relative Credit by €20 From €70 to €90 0.8 0.9

Increase Incapacitated Child Credit by €100 From €3,300 to €3,400 2 3

Increase Blind Persons Credit (incl. Guide Dog) 0.4 0.5

By €500 for single person From €1,650 to €2,150

By €1,000 for both spouses/civil partners blind From €3,300 to €4,300

Increase Widowed Parent or surviving Civil Partner Bereavement Credit by €100 0.2 0.2

Increase Age Credit 19 22

By €50 for single/widow/surviving Civil Partner From €245 to €295

By €100 for married/civil partners From €490 to €590

Increase Widowed Person or surviving Civil Partner (without qualifying

child) Credit by €100

€ Million

6

Revenue Ready Reckoner

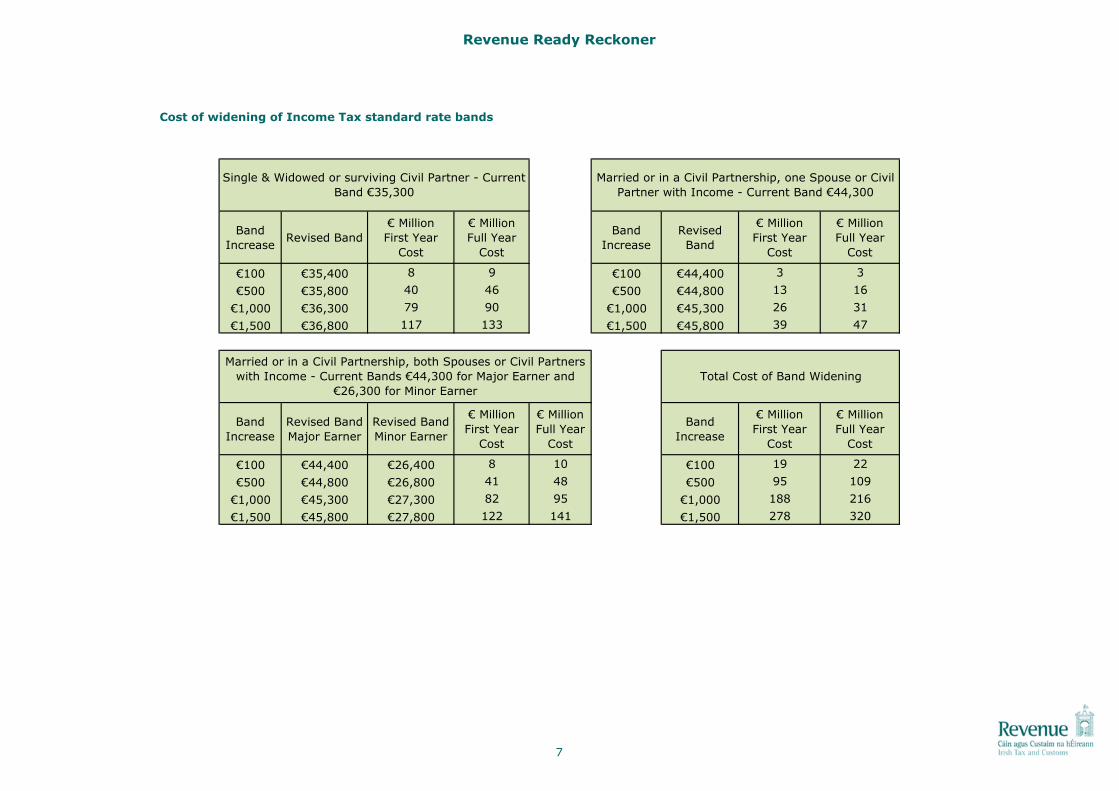

Cost of widening of Income Tax standard rate bands

Band

IncreaseRevised Band

€ Million

First Year

Cost

€ Million

Full Year

Cost

Band

Increase

Revised

Band

€ Million

First Year

Cost

€ Million

Full Year

Cost

€100 €35,400 8 9 €100 €44,400 3 3

€500 €35,800 40 46 €500 €44,800 13 16

€1,000 €36,300 79 90 €1,000 €45,300 26 31

€1,500 €36,800 117 133 €1,500 €45,800 39 47

Band

Increase

Revised Band

Major Earner

Revised Band

Minor Earner

€ Million

First Year

Cost

€ Million

Full Year

Cost

Band

Increase

€ Million

First Year

Cost

€ Million

Full Year

Cost

€100 €44,400 €26,400 8 10 €100 19 22

€500 €44,800 €26,800 41 48 €500 95 109

€1,000 €45,300 €27,300 82 95 €1,000 188 216

€1,500 €45,800 €27,800 122 141 €1,500 278 320

Single & Widowed or surviving Civil Partner - Current

Band €35,300

Total Cost of Band Widening

Married or in a Civil Partnership, both Spouses or Civil Partners

with Income - Current Bands €44,300 for Major Earner and

€26,300 for Minor Earner

Married or in a Civil Partnership, one Spouse or Civil

Partner with Income - Current Band €44,300

7

Revenue Ready Reckoner

Cost of increasing USC rate bands

First Year Full Year

Income under €13,000 is exempt Increase by €100 to €13,100 0.4 0.5

Increase by €500 to €13,500 2 3

Increase by €1,000 to €14,000 5 5

Increase by €1,500 to €14,500 7 8

First €12,012 is charged at 0.5% * Increase by €100 to €12,112 4 4

Increase by €500 to €12,512 16 18

Increase by €1,000 to €13,012 30 35

Increase by €1,500 to €13,512 46 53

From €12,013 to €19,874 is charged at 2% * Increase by €100 to €12,113 and €19,974 7 8

Increase by €500 to €12,513 and €20,374 34 39

Increase by €1,000 to €13,013 and €20,874 67 77

Increase by €1,500 to €13,513 and €21,374 100 116

From €19,874 to €70,044 is charged at 4.5% * Increase by €100 to €19,974 and €70,144 5 6

Increase by €500 to €20,374 and €70,544 23 27

Increase by €1,000 to €20,874 and €71,044 45 53

Increase by €1,500 to €21,374 and €71,544 68 79

Above €70,045 is charged at 8%* Increase by €500 to €70,544 5 5

Increase by €1,000 to €71,044 9 10

Increase by €2,000 to €72,044 17 20

Increase by €5,000 to €75,044 41 49

*The €13,000 exemption threshold remains unchanged for the USC rate band increases.

€ Million

8

Revenue Ready Reckoner

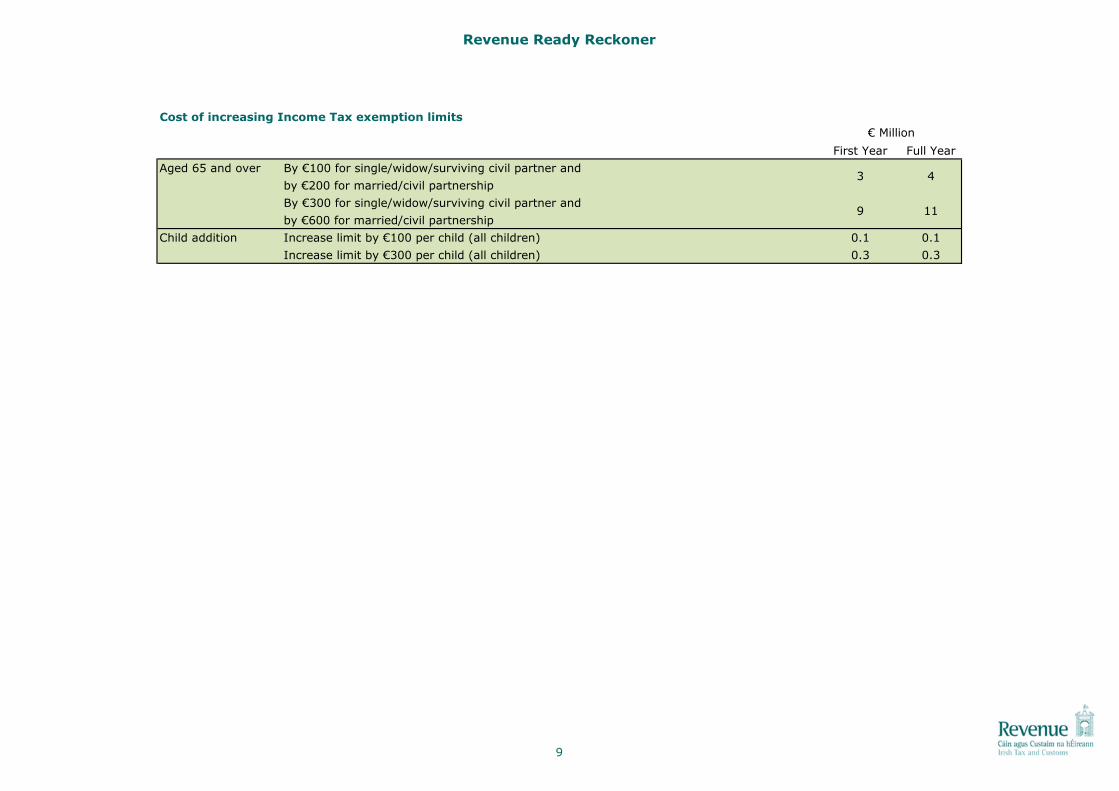

Cost of increasing Income Tax exemption limits

First Year Full Year

Aged 65 and over By €100 for single/widow/surviving civil partner and

by €200 for married/civil partnership

By €300 for single/widow/surviving civil partner and

by €600 for married/civil partnership

Child addition Increase limit by €100 per child (all children) 0.1 0.1

Increase limit by €300 per child (all children) 0.3 0.3

€ Million

4

9 11

3

9

Revenue Ready Reckoner

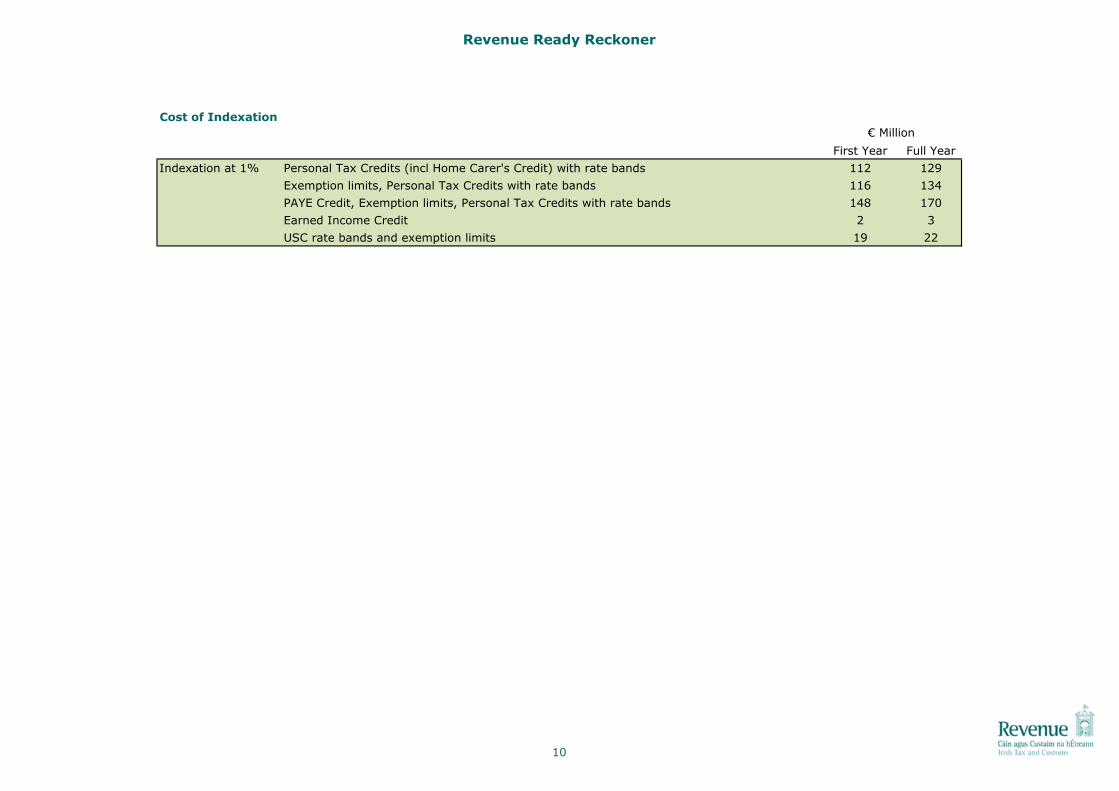

Cost of Indexation

First Year Full Year

Indexation at 1% Personal Tax Credits (incl Home Carer's Credit) with rate bands 112 129

Exemption limits, Personal Tax Credits with rate bands 116 134

PAYE Credit, Exemption limits, Personal Tax Credits with rate bands 148 170

Earned Income Credit 2 3

USC rate bands and exemption limits 19 22

€ Million

10

Revenue Ready Reckoner

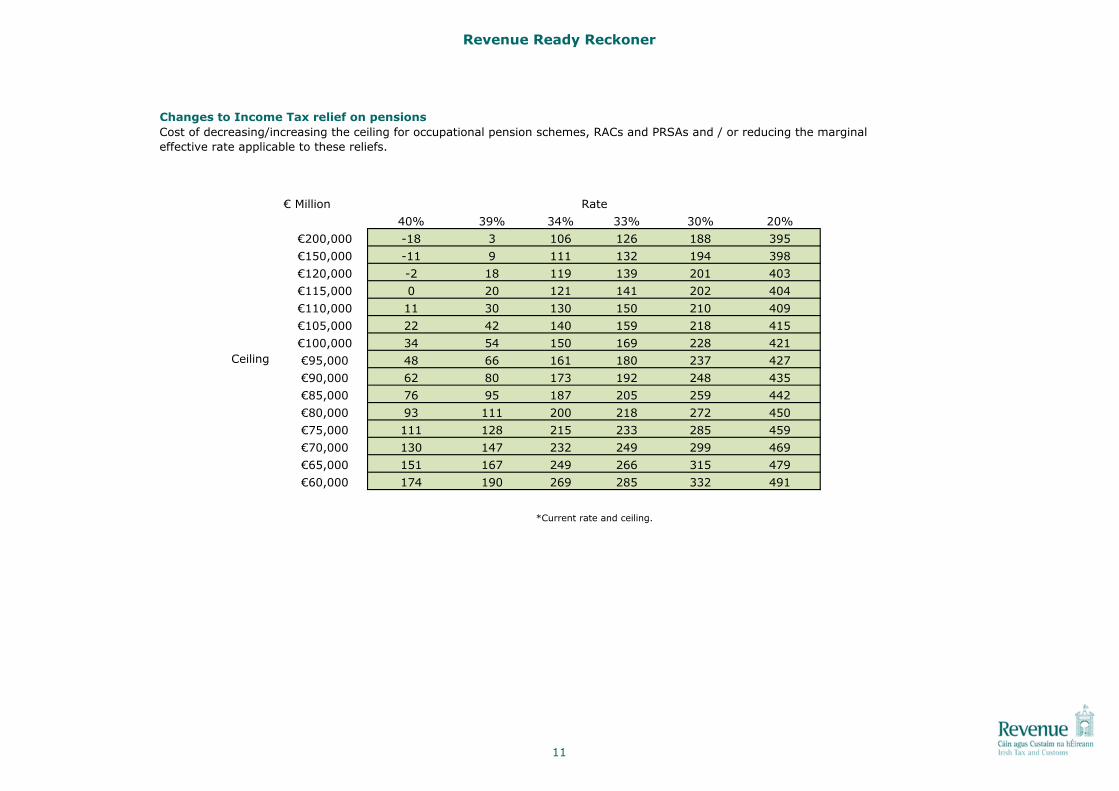

Changes to Income Tax relief on pensions

€ Million

40% 39% 34% 33% 30% 20%

€200,000 -18 3 106 126 188 395

€150,000 -11 9 111 132 194 398

€120,000 -2 18 119 139 201 403

€115,000 0 20 121 141 202 404

€110,000 11 30 130 150 210 409

€105,000 22 42 140 159 218 415

€100,000 34 54 150 169 228 421

€95,000 48 66 161 180 237 427

€90,000 62 80 173 192 248 435

€85,000 76 95 187 205 259 442

€80,000 93 111 200 218 272 450

€75,000 111 128 215 233 285 459

€70,000 130 147 232 249 299 469

€65,000 151 167 249 266 315 479

€60,000 174 190 269 285 332 491

*Current rate and ceiling.

Rate

Ceiling

Cost of decreasing/increasing the ceiling for occupational pension schemes, RACs and PRSAs and / or reducing the marginal

effective rate applicable to these reliefs.

11

Revenue Ready Reckoner

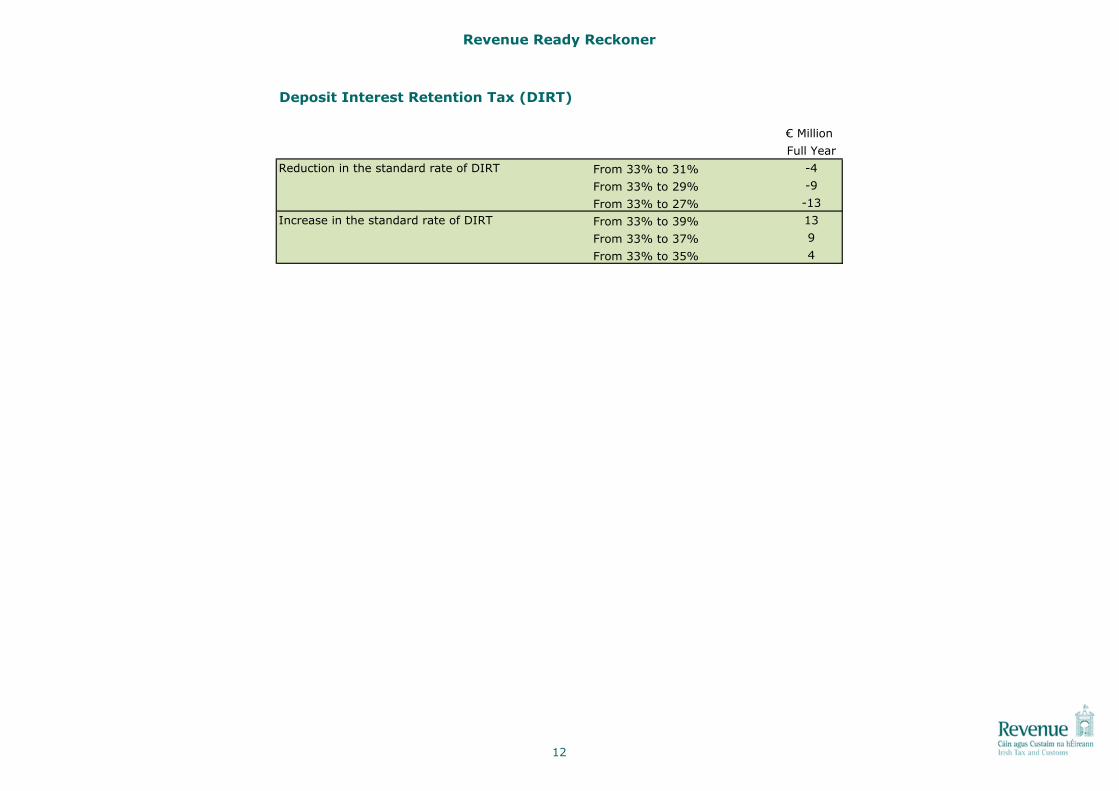

Deposit Interest Retention Tax (DIRT)

€ Million

Full Year

Reduction in the standard rate of DIRT From 33% to 31% -4

From 33% to 29% -9

From 33% to 27% -13

Increase in the standard rate of DIRT From 33% to 39% 13

From 33% to 37% 9

From 33% to 35% 4

12

Revenue Ready Reckoner

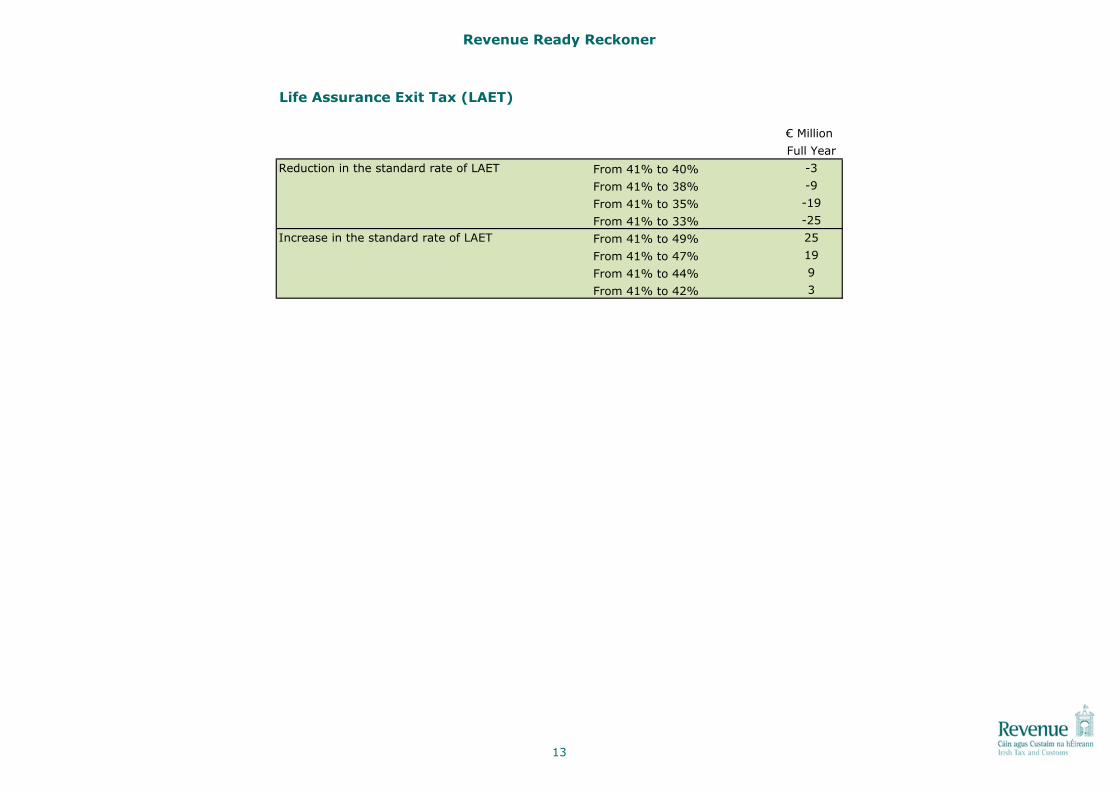

Life Assurance Exit Tax (LAET)

€ Million

Full Year

Reduction in the standard rate of LAET From 41% to 40% -3

From 41% to 38% -9

From 41% to 35% -19

From 41% to 33% -25

Increase in the standard rate of LAET From 41% to 49% 25

From 41% to 47% 19

From 41% to 44% 9

From 41% to 42% 3

13

Revenue Ready Reckoner

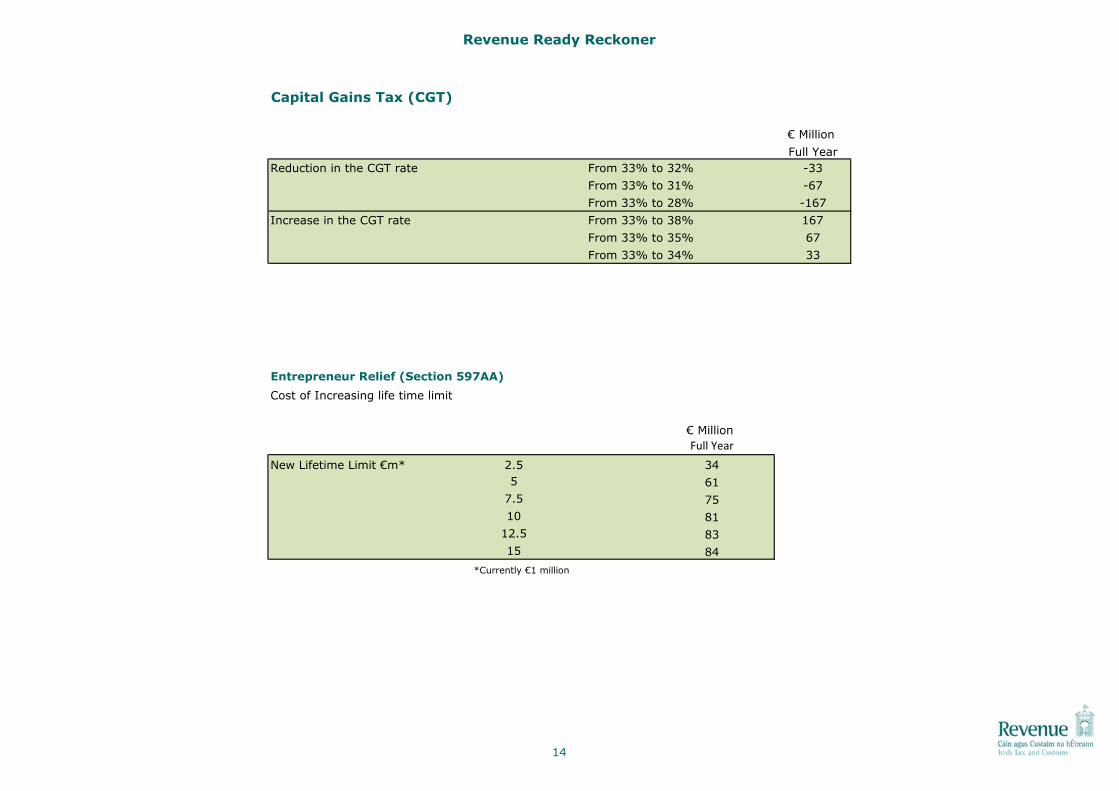

Capital Gains Tax (CGT)

€ Million

Full Year

Reduction in the CGT rate From 33% to 32% -33

From 33% to 31% -67

From 33% to 28% -167

Increase in the CGT rate From 33% to 38% 167

From 33% to 35% 67

From 33% to 34% 33

Entrepreneur Relief (Section 597AA)

Cost of Increasing life time limit

New Lifetime Limit €m* 2.5

5

7.5

10

12.5

15

*Currently €1 million

€ Million

84

75

81

83

Full Year

34

61

14

Revenue Ready Reckoner

Capital Acquisitions Tax (CAT)

The CAT Ready Reckoner covers the following:

Page 16

Page 17-18

Changes in CAT Rates, Thresholds or Reliefs

Simultaneous Change in CAT Rate and Thresholds

15

Revenue Ready Reckoner

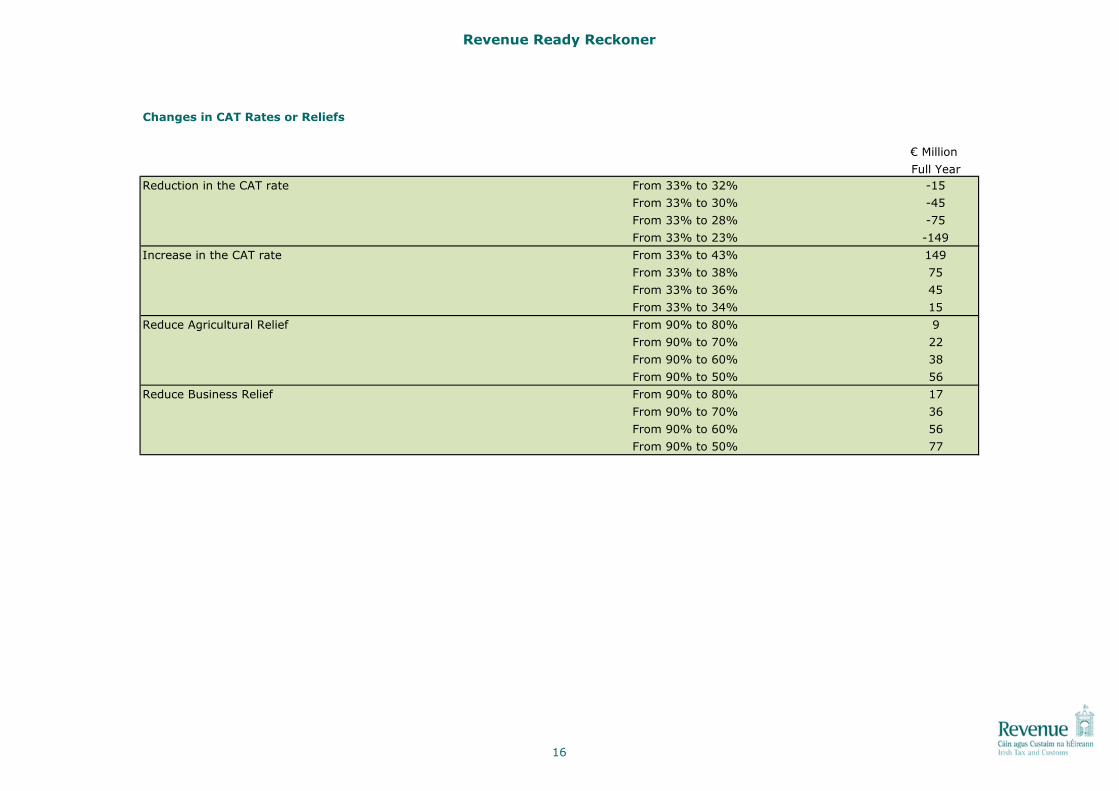

Changes in CAT Rates or Reliefs

€ Million

Full Year

Reduction in the CAT rate From 33% to 32% -15

From 33% to 30% -45

From 33% to 28% -75

From 33% to 23% -149

Increase in the CAT rate From 33% to 43% 149

From 33% to 38% 75

From 33% to 36% 45

From 33% to 34% 15

Reduce Agricultural Relief From 90% to 80% 9

From 90% to 70% 22

From 90% to 60% 38

From 90% to 50% 56

Reduce Business Relief From 90% to 80% 17

From 90% to 70% 36

From 90% to 60% 56

From 90% to 50% 77

16

Revenue Ready Reckoner

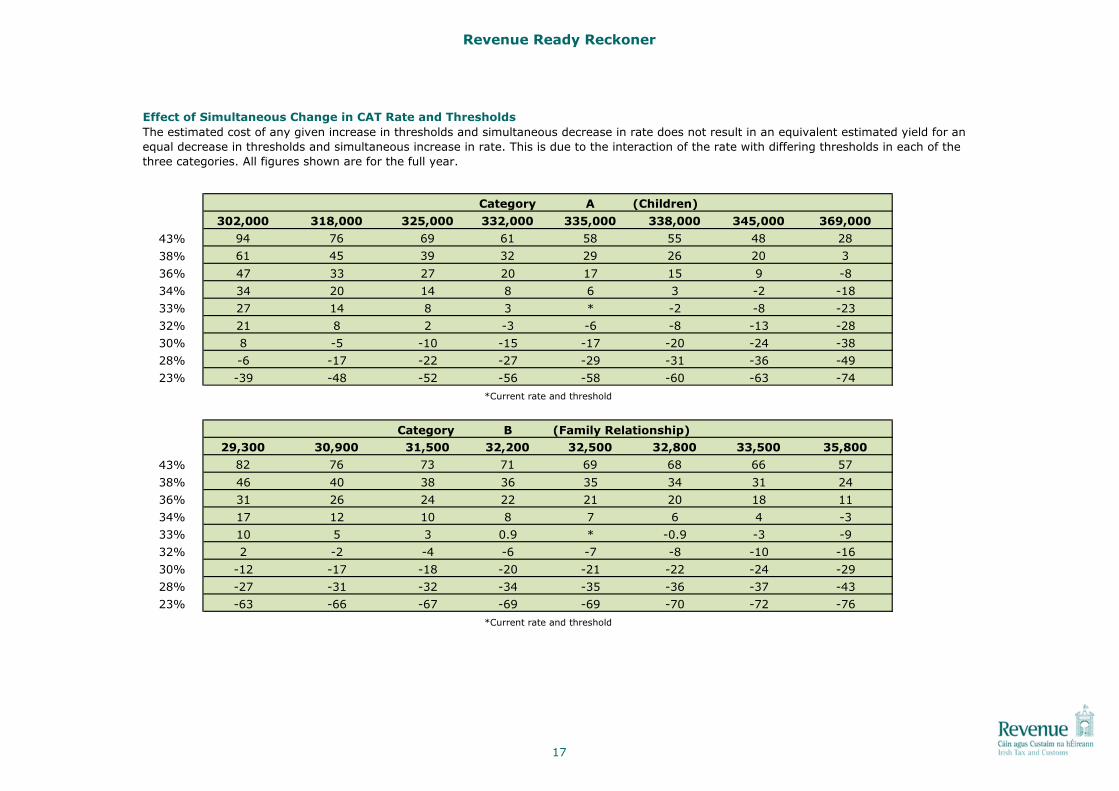

Effect of Simultaneous Change in CAT Rate and Thresholds

Category A (Children)

302,000 318,000 325,000 332,000 335,000 338,000 345,000 369,000

43% 94 76 69 61 58 55 48 28

38% 61 45 39 32 29 26 20 3

36% 47 33 27 20 17 15 9 -8

34% 34 20 14 8 6 3 -2 -18

33% 27 14 8 3 * -2 -8 -23

32% 21 8 2 -3 -6 -8 -13 -28

30% 8 -5 -10 -15 -17 -20 -24 -38

28% -6 -17 -22 -27 -29 -31 -36 -49

23% -39 -48 -52 -56 -58 -60 -63 -74

Category B (Family Relationship)

29,300 30,900 31,500 32,200 32,500 32,800 33,500 35,800

43% 82 76 73 71 69 68 66 57

38% 46 40 38 36 35 34 31 24

36% 31 26 24 22 21 20 18 11

34% 17 12 10 8 7 6 4 -3

33% 10 5 3 0.9 * -0.9 -3 -9

32% 2 -2 -4 -6 -7 -8 -10 -16

30% -12 -17 -18 -20 -21 -22 -24 -29

28% -27 -31 -32 -34 -35 -36 -37 -43

23% -63 -66 -67 -69 -69 -70 -72 -76

The estimated cost of any given increase in thresholds and simultaneous decrease in rate does not result in an equivalent estimated yield for an

equal decrease in thresholds and simultaneous increase in rate. This is due to the interaction of the rate with differing thresholds in each of the

three categories. All figures shown are for the full year.

*Current rate and threshold

*Current rate and threshold

17

Revenue Ready Reckoner

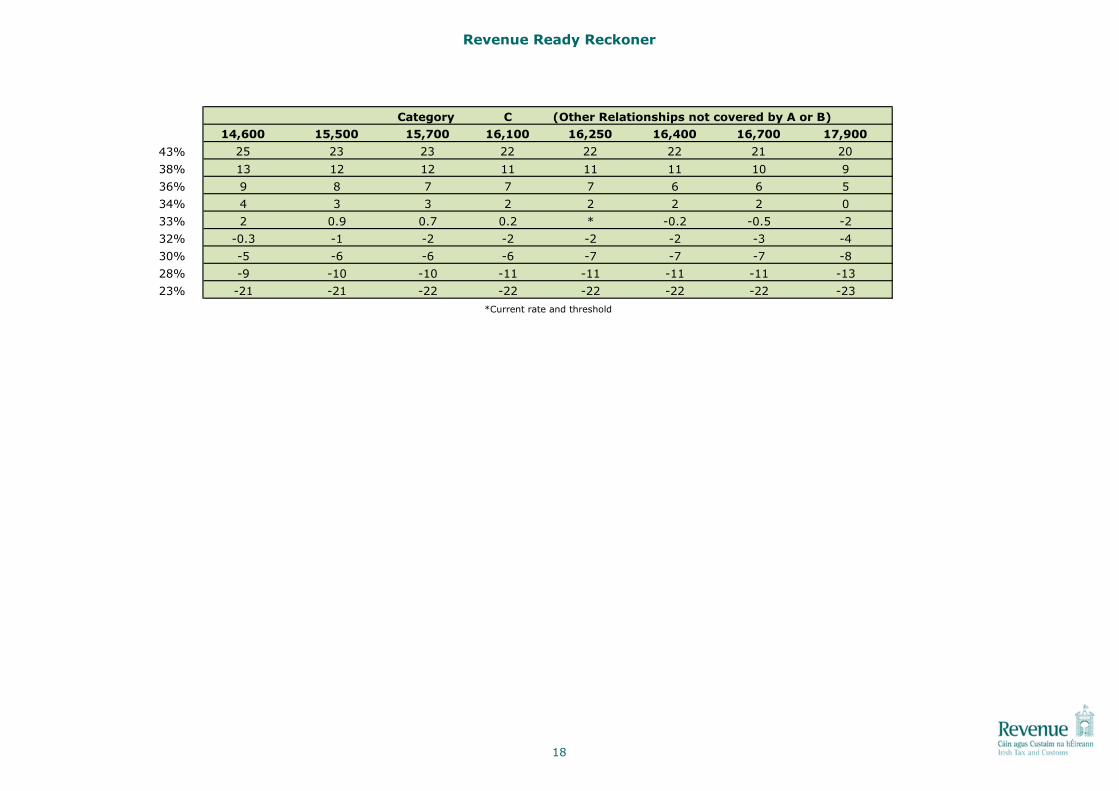

Category C (Other Relationships not covered by A or B)

14,600 15,500 15,700 16,100 16,250 16,400 16,700 17,900

43% 25 23 23 22 22 22 21 20

38% 13 12 12 11 11 11 10 9

36% 9 8 7 7 7 6 6 5

34% 4 3 3 2 2 2 2 0

33% 2 0.9 0.7 0.2 * -0.2 -0.5 -2

32% -0.3 -1 -2 -2 -2 -2 -3 -4

30% -5 -6 -6 -6 -7 -7 -7 -8

28% -9 -10 -10 -11 -11 -11 -11 -13

23% -21 -21 -22 -22 -22 -22 -22 -23

*Current rate and threshold

18

Revenue Ready Reckoner

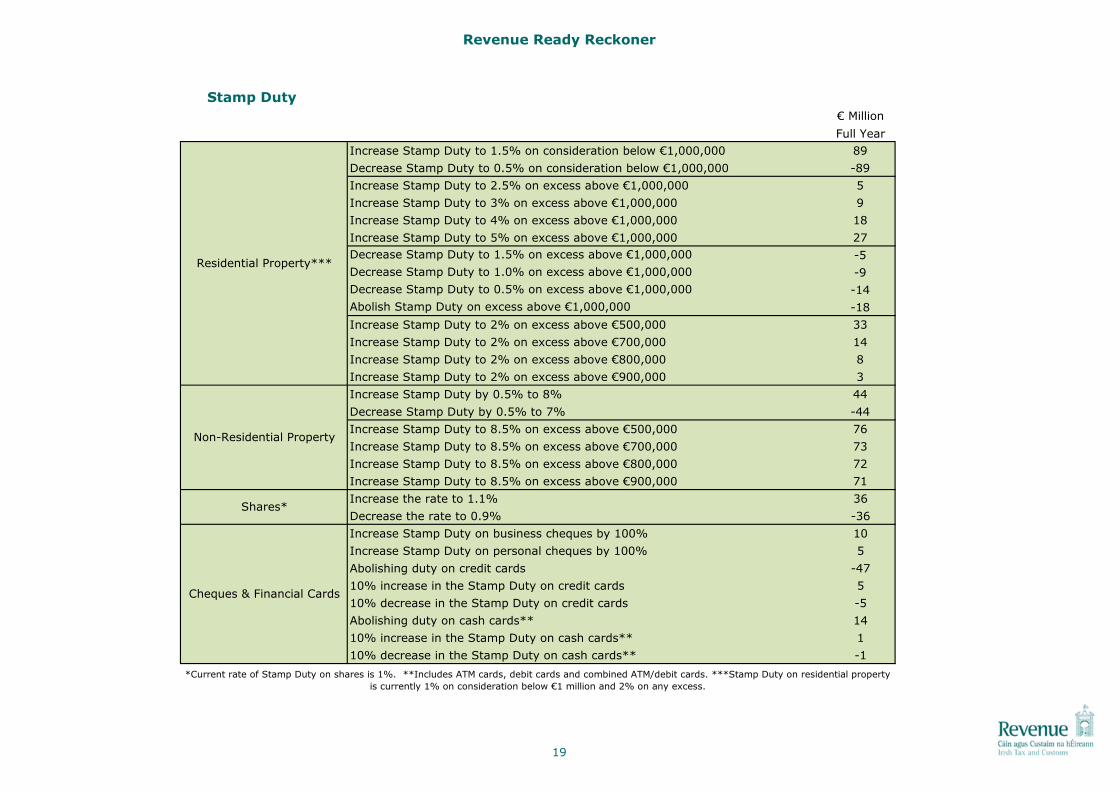

Stamp Duty

€ Million

Full Year

Increase Stamp Duty to 1.5% on consideration below €1,000,000 89

Decrease Stamp Duty to 0.5% on consideration below €1,000,000 -89

Increase Stamp Duty to 2.5% on excess above €1,000,000 5

Increase Stamp Duty to 3% on excess above €1,000,000 9

Increase Stamp Duty to 4% on excess above €1,000,000 18

Increase Stamp Duty to 5% on excess above €1,000,000 27

-5

-9

-14

-18

Increase Stamp Duty to 2% on excess above €500,000 33

Increase Stamp Duty to 2% on excess above €700,000 14

Increase Stamp Duty to 2% on excess above €800,000 8

Increase Stamp Duty to 2% on excess above €900,000 3

Increase Stamp Duty by 0.5% to 8% 44

Decrease Stamp Duty by 0.5% to 7% -44

Increase Stamp Duty to 8.5% on excess above €500,000 76

Increase Stamp Duty to 8.5% on excess above €700,000 73

Increase Stamp Duty to 8.5% on excess above €800,000 72

Increase Stamp Duty to 8.5% on excess above €900,000 71

Increase the rate to 1.1% 36

Decrease the rate to 0.9% -36

Increase Stamp Duty on business cheques by 100% 10

Increase Stamp Duty on personal cheques by 100% 5

Abolishing duty on credit cards -47

10% increase in the Stamp Duty on credit cards 5

10% decrease in the Stamp Duty on credit cards -5

Abolishing duty on cash cards** 14

10% increase in the Stamp Duty on cash cards** 1

10% decrease in the Stamp Duty on cash cards** -1

Cheques & Financial Cards

*Current rate of Stamp Duty on shares is 1%. **Includes ATM cards, debit cards and combined ATM/debit cards. ***Stamp Duty on residential property

is currently 1% on consideration below €1 million and 2% on any excess.

Non-Residential Property

Decrease Stamp Duty to 1.5% on excess above €1,000,000

Decrease Stamp Duty to 1.0% on excess above €1,000,000

Decrease Stamp Duty to 0.5% on excess above €1,000,000

Abolish Stamp Duty on excess above €1,000,000

Residential Property***

Shares*

19

Revenue Ready Reckoner

Excise

The Excise Ready Reckoner covers the following:

Mineral Oil Tax Page 21

Carbon Tax Page 22

Alcohol Products Tax Page 23

Tobacco Products Tax Page 24

Betting Duty Page 25

20

Revenue Ready Reckoner

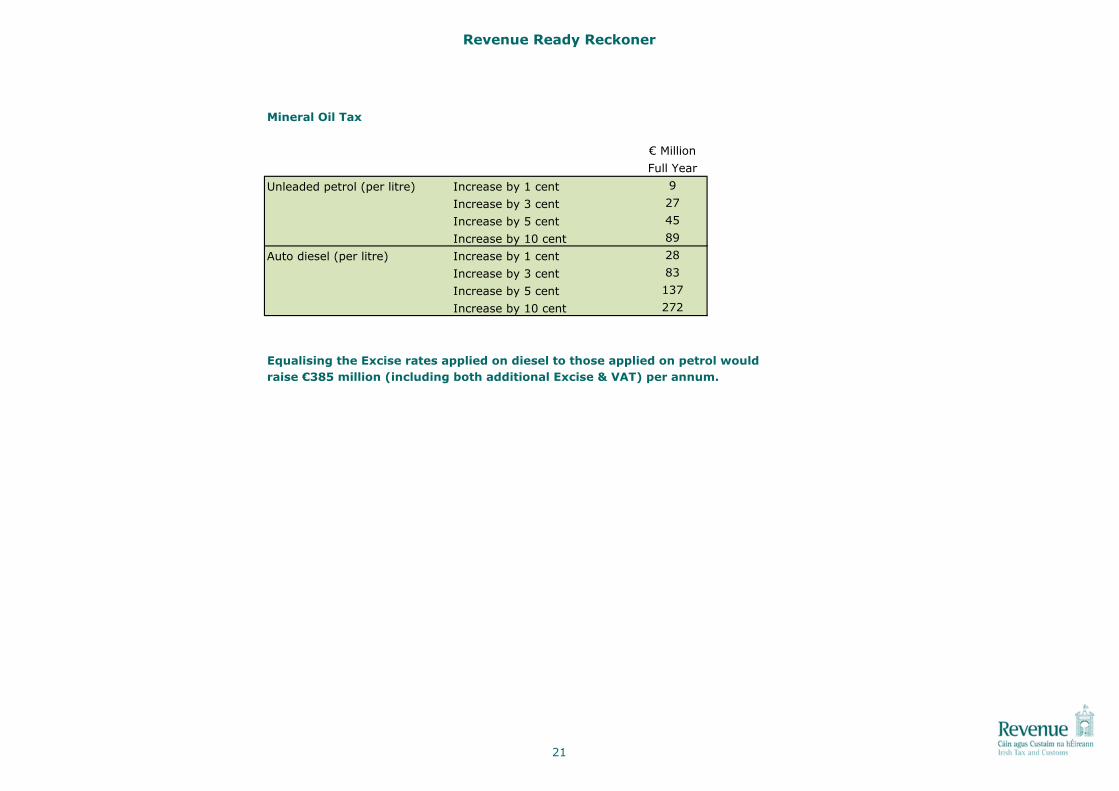

Mineral Oil Tax

€ Million

Full Year

Unleaded petrol (per litre) Increase by 1 cent 9

Increase by 3 cent 27

Increase by 5 cent 45

Increase by 10 cent 89

Auto diesel (per litre) Increase by 1 cent 28

Increase by 3 cent 83

Increase by 5 cent 137

Increase by 10 cent 272

Equalising the Excise rates applied on diesel to those applied on petrol would

raise €385 million (including both additional Excise & VAT) per annum.

21

Revenue Ready Reckoner

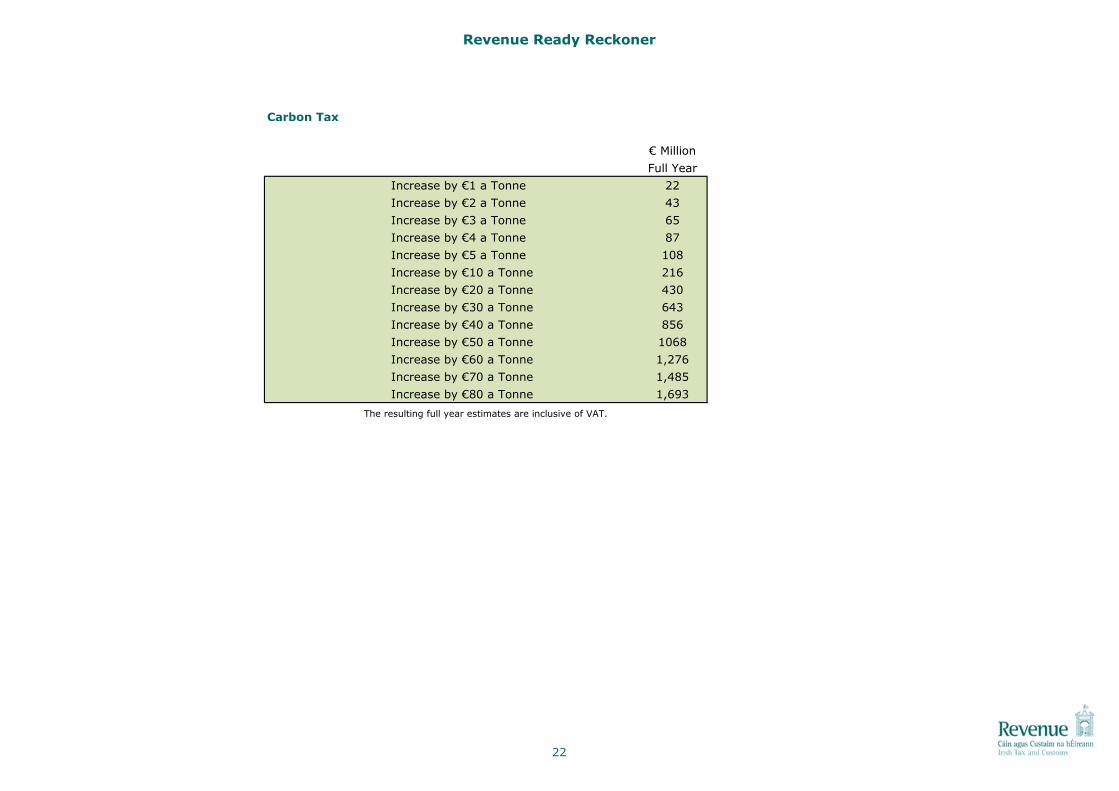

Carbon Tax

€ Million

Full Year

Increase by €1 a Tonne 22

Increase by €2 a Tonne 43

Increase by €3 a Tonne 65

Increase by €4 a Tonne 87

Increase by €5 a Tonne 108

Increase by €10 a Tonne 216

Increase by €20 a Tonne 430

Increase by €30 a Tonne 643

Increase by €40 a Tonne 856

Increase by €50 a Tonne 1068

Increase by €60 a Tonne 1,276

Increase by €70 a Tonne 1,485

Increase by €80 a Tonne 1,693

The resulting full year estimates are inclusive of VAT.

22

Revenue Ready Reckoner

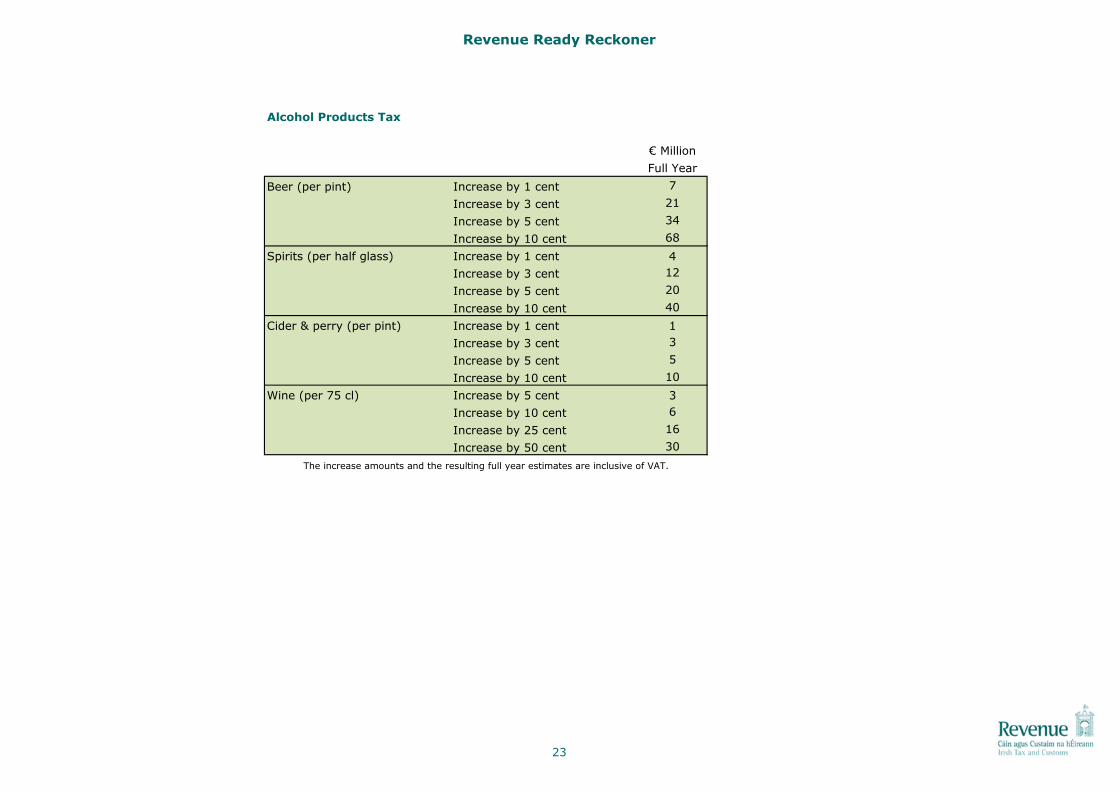

Alcohol Products Tax

€ Million

Full Year

Beer (per pint) Increase by 1 cent 7

Increase by 3 cent 21

Increase by 5 cent 34

Increase by 10 cent 68

Spirits (per half glass) Increase by 1 cent 4

Increase by 3 cent 12

Increase by 5 cent 20

Increase by 10 cent 40

Cider & perry (per pint) Increase by 1 cent 1

Increase by 3 cent 3

Increase by 5 cent 5

Increase by 10 cent 10

Wine (per 75 cl) Increase by 5 cent 3

Increase by 10 cent 6

Increase by 25 cent 16

Increase by 50 cent 30

The increase amounts and the resulting full year estimates are inclusive of VAT.

23

Revenue Ready Reckoner

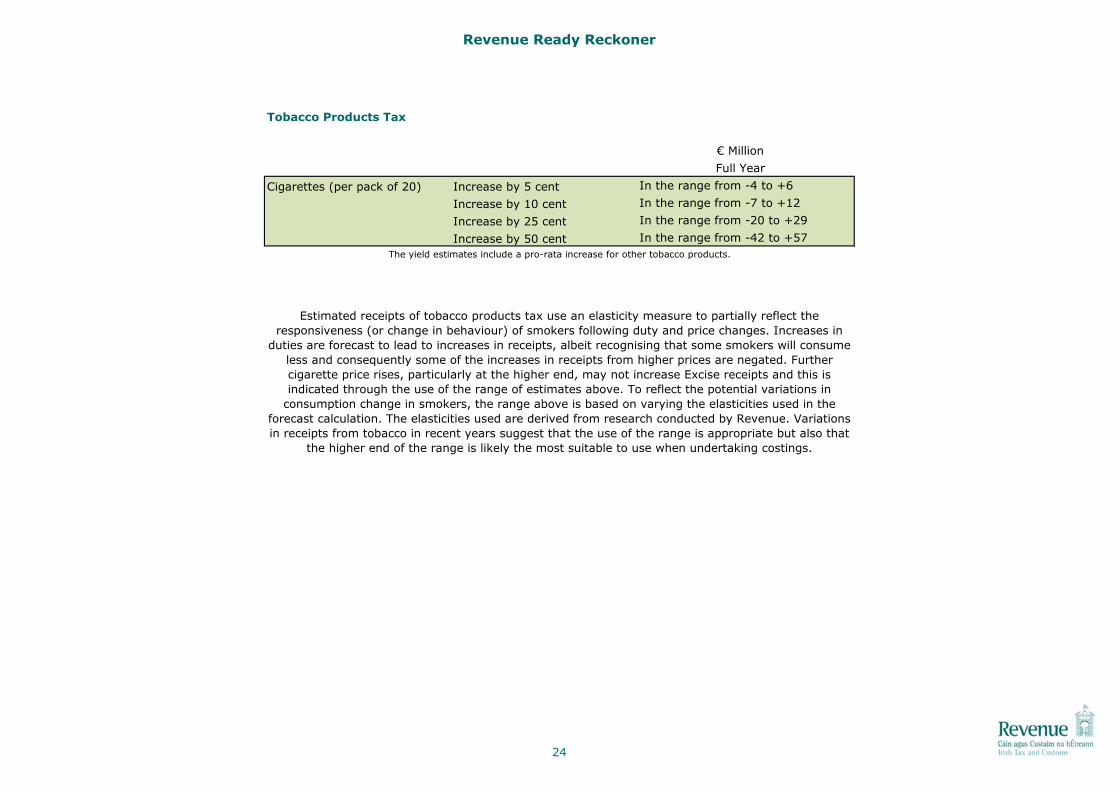

Tobacco Products Tax

€ Million

Full Year

Cigarettes (per pack of 20) Increase by 5 cent In the range from -4 to +6

Increase by 10 cent In the range from -7 to +12

Increase by 25 cent In the range from -20 to +29

Increase by 50 cent In the range from -42 to +57

Estimated receipts of tobacco products tax use an elasticity measure to partially reflect the

responsiveness (or change in behaviour) of smokers following duty and price changes. Increases in

duties are forecast to lead to increases in receipts, albeit recognising that some smokers will consume

less and consequently some of the increases in receipts from higher prices are negated. Further

cigarette price rises, particularly at the higher end, may not increase Excise receipts and this is

indicated through the use of the range of estimates above. To reflect the potential variations in

consumption change in smokers, the range above is based on varying the elasticities used in the

forecast calculation. The elasticities used are derived from research conducted by Revenue. Variations

in receipts from tobacco in recent years suggest that the use of the range is appropriate but also that

the higher end of the range is likely the most suitable to use when undertaking costings.

The yield estimates include a pro-rata increase for other tobacco products.

24

Revenue Ready Reckoner

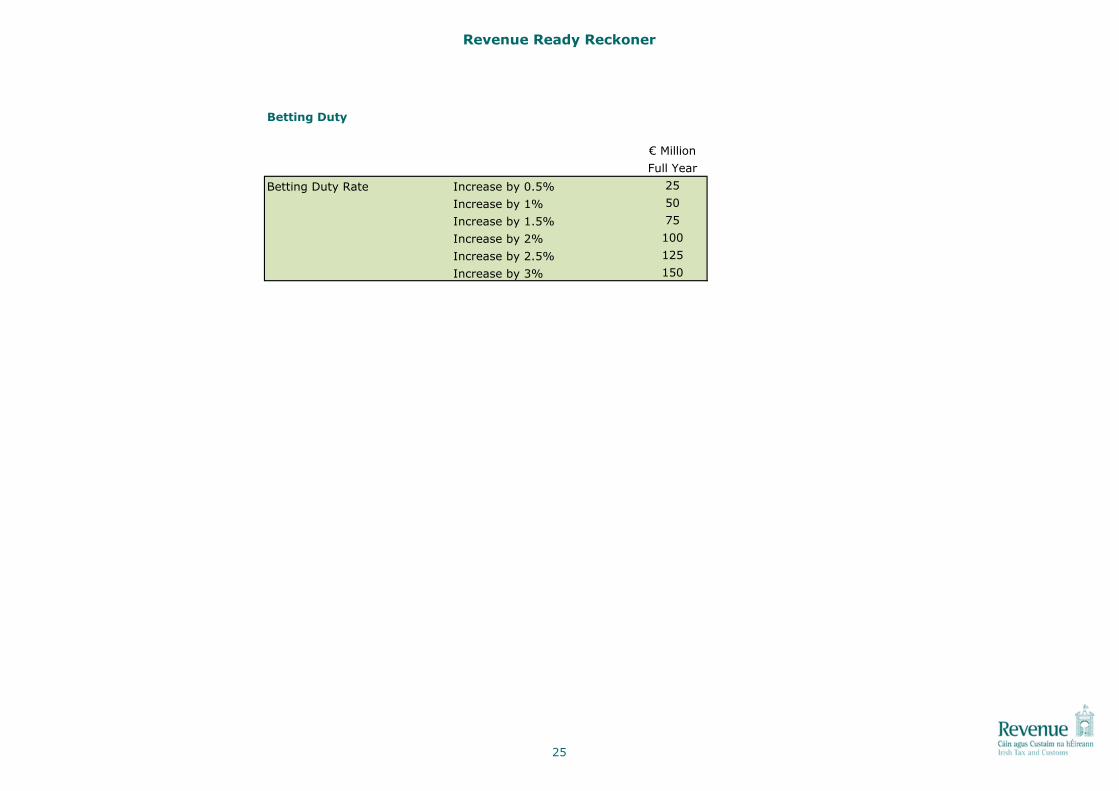

Betting Duty

€ Million

Full Year

Increase by 0.5% 25

Increase by 1% 50

Increase by 1.5% 75

Increase by 2% 100

Increase by 2.5% 125

Increase by 3% 150

Betting Duty Rate

25

Revenue Ready Reckoner

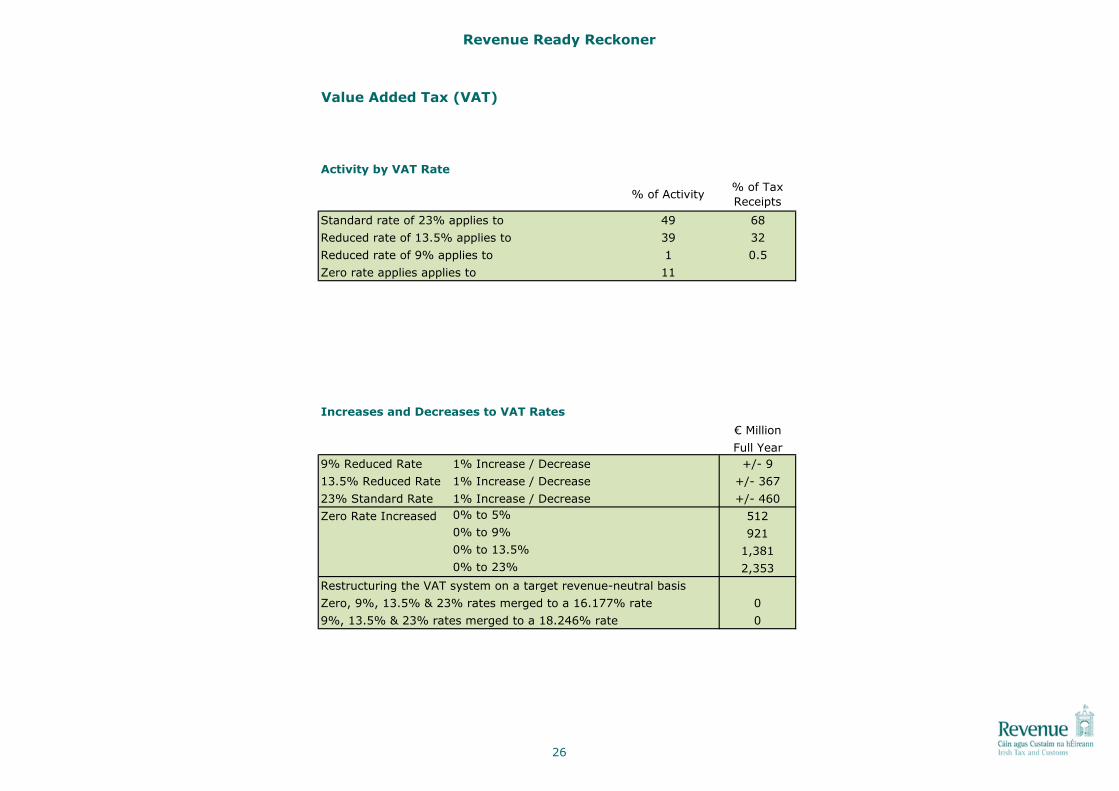

Value Added Tax (VAT)

Activity by VAT Rate

% of Activity% of Tax

Receipts

Standard rate of 23% applies to 49 68

Reduced rate of 13.5% applies to 39 32

Reduced rate of 9% applies to 1 0.5

Zero rate applies applies to 11

Increases and Decreases to VAT Rates

€ Million

Full Year

9% Reduced Rate 1% Increase / Decrease +/- 9

13.5% Reduced Rate 1% Increase / Decrease +/- 367

23% Standard Rate 1% Increase / Decrease +/- 460

Zero Rate Increased 0% to 5% 512

0% to 9% 921

0% to 13.5% 1,381

0% to 23% 2,353

Restructuring the VAT system on a target revenue-neutral basis

Zero, 9%, 13.5% & 23% rates merged to a 16.177% rate 0

9%, 13.5% & 23% rates merged to a 18.246% rate 0

26

Revenue Ready Reckoner

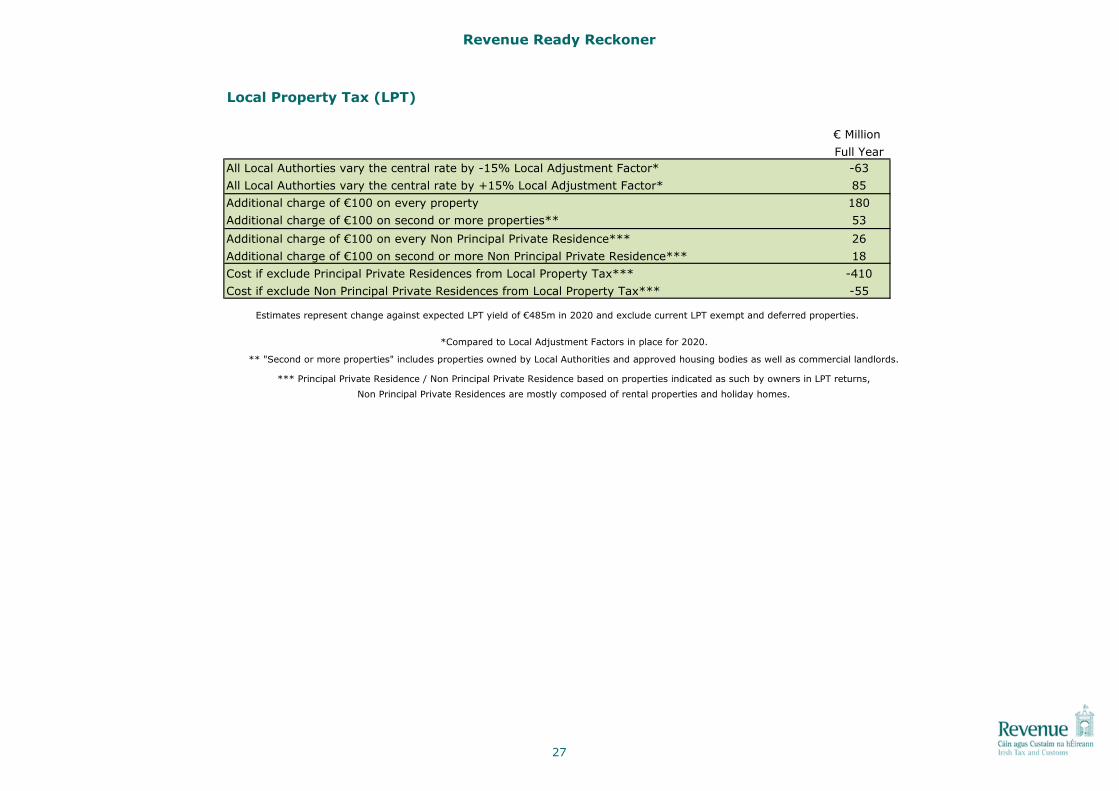

Local Property Tax (LPT)

€ Million

Full Year

All Local Authorties vary the central rate by -15% Local Adjustment Factor* -63All Local Authorties vary the central rate by +15% Local Adjustment Factor* 85Additional charge of €100 on every property 180

Additional charge of €100 on second or more properties** 53

Additional charge of €100 on every Non Principal Private Residence*** 26

Additional charge of €100 on second or more Non Principal Private Residence*** 18

Cost if exclude Principal Private Residences from Local Property Tax*** -410

Cost if exclude Non Principal Private Residences from Local Property Tax*** -55

*Compared to Local Adjustment Factors in place for 2020.

** "Second or more properties" includes properties owned by Local Authorities and approved housing bodies as well as commercial landlords.

*** Principal Private Residence / Non Principal Private Residence based on properties indicated as such by owners in LPT returns,

Non Principal Private Residences are mostly composed of rental properties and holiday homes.

Estimates represent change against expected LPT yield of €485m in 2020 and exclude current LPT exempt and deferred properties.

27