venture capital report - dow jones & company · 2019-07-11 · venture capital report venture...

TRANSCRIPT

V E N T U R E C A P I T A L R E P O R T

Venture Capital Report Europe | 2Q | 2019

V E N T U R E C A P I T A L R E P O R T

VENTURE CAPITAL REPORT

The following report presents Dow Jones VentureSource’s quarterly findings for European venture capital fundraising, investment, valuation,

and liquidity. The included charts and graphs offer a comprehensive view of the trends currently affecting the venture capital market.

Highlights for 2Q 2019 include:

• European companies set a new record for equity investment, with €9.29 billion raised in 802 rounds of financing.

• Despite the issues surrounding Brexit, the UK continued to take the lion’s share of startup investment, VC fundraising, and liquidity events.

• VC fundraising enjoyed the best quarter in three years, more than doubling from 1Q.

• While the M&A market appeared relatively stable, IPOs had another anemic quarter.

2

V E N T U R E C A P I T A L R E P O R T

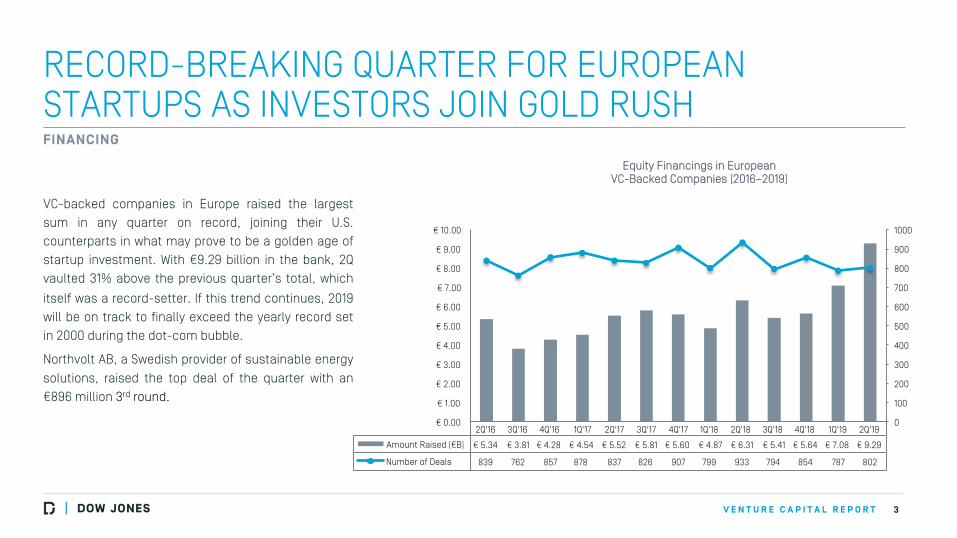

RECORD-BREAKING QUARTER FOR EUROPEAN STARTUPS AS INVESTORS JOIN GOLD RUSH

VC-backed companies in Europe raised the largest

sum in any quarter on record, joining their U.S.

counterparts in what may prove to be a golden age of

startup investment. With €9.29 billion in the bank, 2Q

vaulted 31% above the previous quarter’s total, which

itself was a record-setter. If this trend continues, 2019

will be on track to finally exceed the yearly record set

in 2000 during the dot-com bubble.

Northvolt AB, a Swedish provider of sustainable energy

solutions, raised the top deal of the quarter with an

€896 million 3rd round.

3

FINANCING Equity Financings in European

VC-Backed Companies (2016–2019)

2Q'16 3Q'16 4Q'16 1Q'17 2Q'17 3Q'17 4Q'17 1Q'18 2Q'18 3Q'18 4Q'18 1Q'19 2Q'19

Amount Raised (€B) € 5.34 € 3.81 € 4.28 € 4.54 € 5.52 € 5.81 € 5.60 € 4.87 € 6.31 € 5.41 € 5.64 € 7.08 € 9.29

Number of Deals 839 762 857 878 837 826 907 799 933 794 854 787 802

0

100

200

300

400

500

600

700

800

900

1000

€ 0.00

€ 1.00

€ 2.00

€ 3.00

€ 4.00

€ 5.00

€ 6.00

€ 7.00

€ 8.00

€ 9.00

€ 10.00

V E N T U R E C A P I T A L R E P O R T

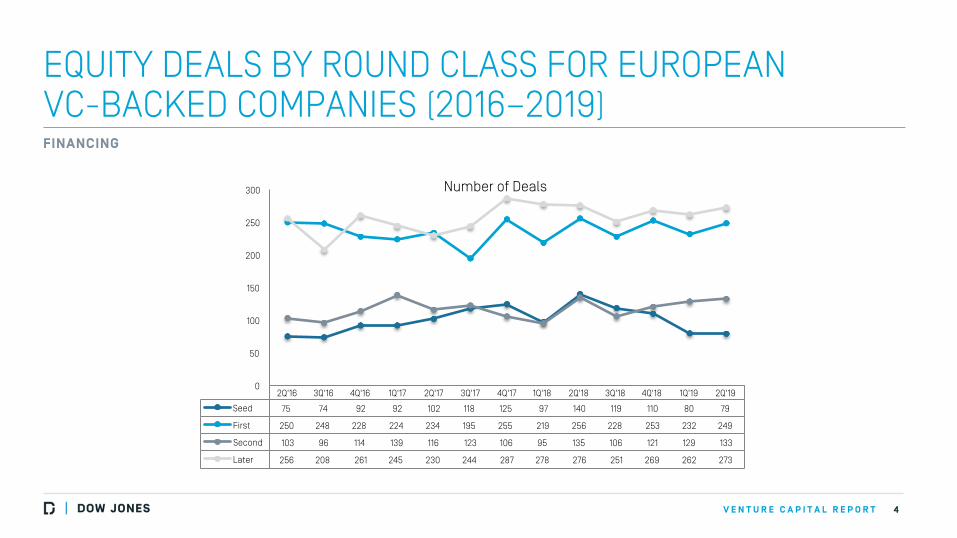

EQUITY DEALS BY ROUND CLASS FOR EUROPEAN VC-BACKED COMPANIES (2016–2019)

4

FINANCING

2Q'16 3Q'16 4Q'16 1Q'17 2Q'17 3Q'17 4Q'17 1Q'18 2Q'18 3Q'18 4Q'18 1Q'19 2Q'19

Seed 75 74 92 92 102 118 125 97 140 119 110 80 79

First 250 248 228 224 234 195 255 219 256 228 253 232 249

Second 103 96 114 139 116 123 106 95 135 106 121 129 133

Later 256 208 261 245 230 244 287 278 276 251 269 262 273

0

50

100

150

200

250

300 Number of Deals

V E N T U R E C A P I T A L R E P O R T

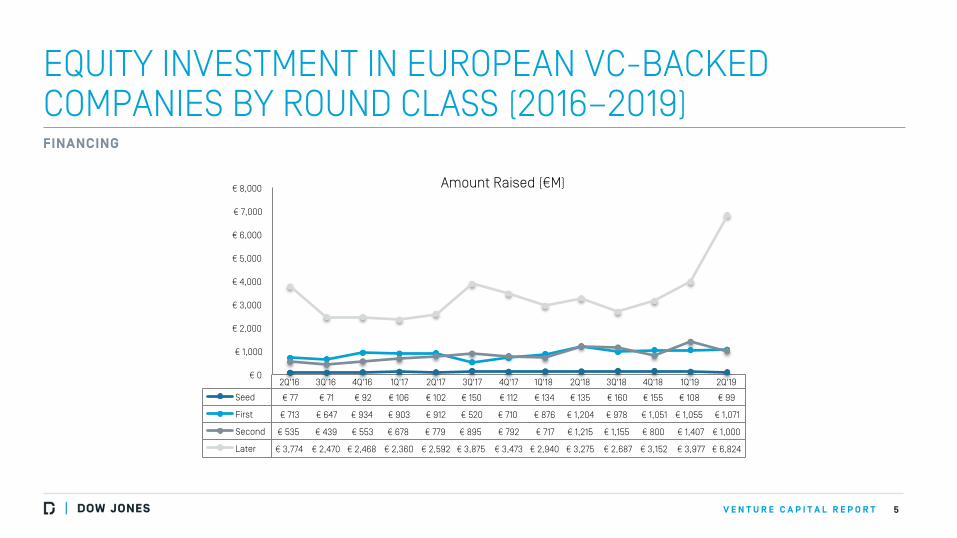

EQUITY INVESTMENT IN EUROPEAN VC-BACKED COMPANIES BY ROUND CLASS (2016–2019)

5

FINANCING

2Q'16 3Q'16 4Q'16 1Q'17 2Q'17 3Q'17 4Q'17 1Q'18 2Q'18 3Q'18 4Q'18 1Q'19 2Q'19

Seed € 77 € 71 € 92 € 106 € 102 € 150 € 112 € 134 € 135 € 160 € 155 € 108 € 99

First € 713 € 647 € 934 € 903 € 912 € 520 € 710 € 876 € 1,204 € 978 € 1,051 € 1,055 € 1,071

Second € 535 € 439 € 553 € 678 € 779 € 895 € 792 € 717 € 1,215 € 1,155 € 800 € 1,407 € 1,000

Later € 3,774 € 2,470 € 2,468 € 2,360 € 2,592 € 3,875 € 3,473 € 2,940 € 3,275 € 2,687 € 3,152 € 3,977 € 6,824

€ 0

€ 1,000

€ 2,000

€ 3,000

€ 4,000

€ 5,000

€ 6,000

€ 7,000

€ 8,000 Amount Raised (€M)

V E N T U R E C A P I T A L R E P O R T

EQUITY FINANCINGS IN EUROPEAN VC-BACKED COMPANIES, MEDIAN DEAL SIZE (2016–2019)

6

FINANCING

2Q'16 3Q'16 4Q'16 1Q'17 2Q'17 3Q'17 4Q'17 1Q'18 2Q'18 3Q'18 4Q'18 1Q'19 2Q'19

Median Equity Deal Size (€M) € 1.41 € 1.57 € 1.73 € 2.00 € 1.65 € 2.00 € 1.58 € 1.80 € 2.50 € 2.50 € 2.00 € 2.67 € 2.60

€ 0.00

€ 0.50

€ 1.00

€ 1.50

€ 2.00

€ 2.50

€ 3.00 Median Equity Deal Size [€M]

V E N T U R E C A P I T A L R E P O R T

EQUITY INVESTMENT IN EUROPEAN VC-BACKED COMPANIES BY INDUSTRY GROUP (2Q 2019)

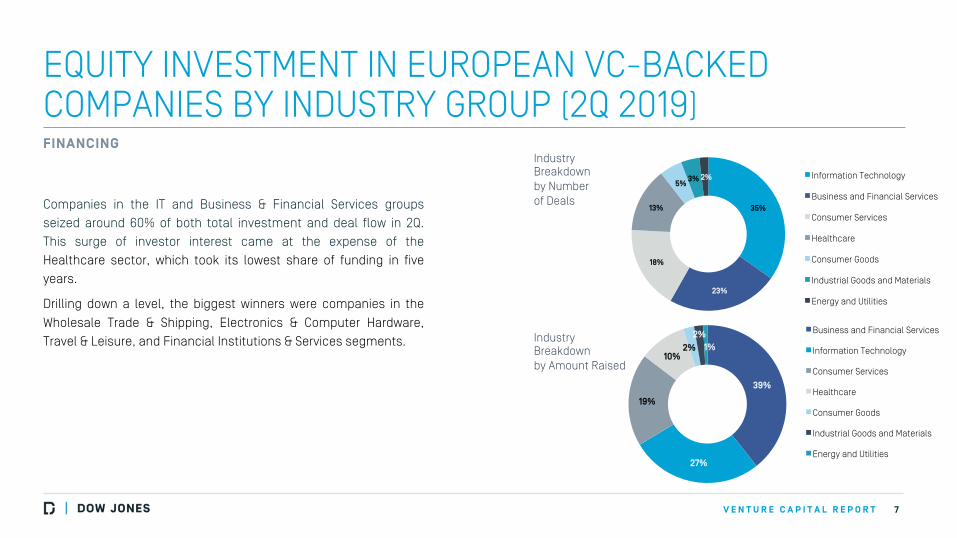

Companies in the IT and Business & Financial Services groups

seized around 60% of both total investment and deal flow in 2Q.

This surge of investor interest came at the expense of the

Healthcare sector, which took its lowest share of funding in five

years.

Drilling down a level, the biggest winners were companies in the

Wholesale Trade & Shipping, Electronics & Computer Hardware,

Travel & Leisure, and Financial Institutions & Services segments.

7

FINANCING Industry Breakdown by Number of Deals

Industry Breakdown by Amount Raised

35%

23%

18%

13%

5% 3% 2% Information Technology

Business and Financial Services

Consumer Services

Healthcare

Consumer Goods

Industrial Goods and Materials

Energy and Utilities

39%

27%

19%

10% 2%

2% 1%

Business and Financial Services

Information Technology

Consumer Services

Healthcare

Consumer Goods

Industrial Goods and Materials

Energy and Utilities

V E N T U R E C A P I T A L R E P O R T

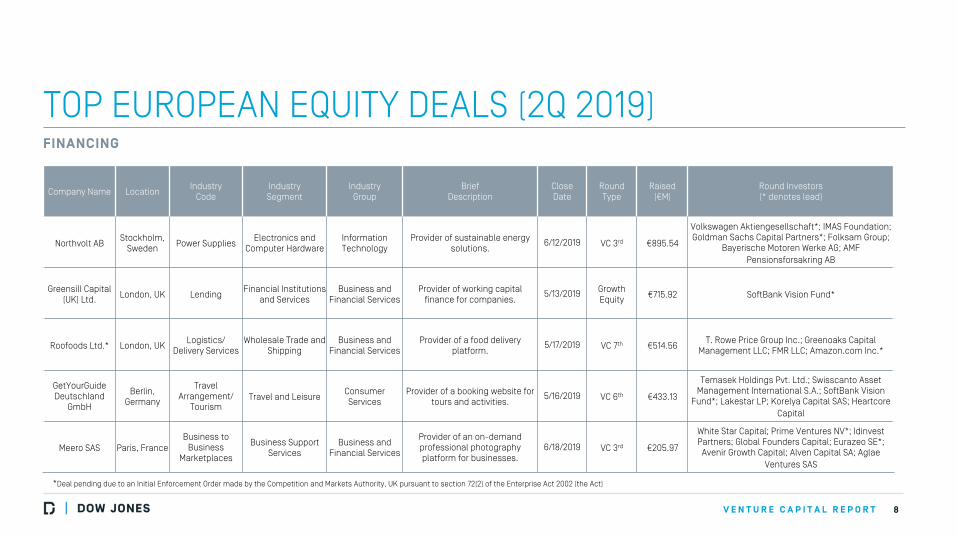

TOP EUROPEAN EQUITY DEALS (2Q 2019)

8

Company Name Location Industry

Code Industry Segment

Industry Group

Brief Description

Close Date

Round Type

Raised (€M)

Round Investors (* denotes lead)

Northvolt AB Stockholm,

Sweden Power Supplies

Electronics and Computer Hardware

Information Technology

Provider of sustainable energy solutions.

6/12/2019 VC 3rd €895.54

Volkswagen Aktiengesellschaft*; IMAS Foundation; Goldman Sachs Capital Partners*; Folksam Group;

Bayerische Motoren Werke AG; AMF Pensionsforsakring AB

Greensill Capital (UK) Ltd.

London, UK Lending Financial Institutions

and Services Business and

Financial Services Provider of working capital

finance for companies. 5/13/2019 Growth

Equity €715.92 SoftBank Vision Fund*

Roofoods Ltd.* London, UK Logistics/

Delivery Services Wholesale Trade and

Shipping Business and

Financial Services Provider of a food delivery

platform. 5/17/2019 VC 7th €514.56

T. Rowe Price Group Inc.; Greenoaks Capital Management LLC; FMR LLC; Amazon.com Inc.*

GetYourGuide Deutschland

GmbH

Berlin, Germany

Travel Arrangement/

Tourism Travel and Leisure

Consumer Services

Provider of a booking website for tours and activities.

5/16/2019 VC 6th €433.13

Temasek Holdings Pvt. Ltd.; Swisscanto Asset Management International S.A.; SoftBank Vision

Fund*; Lakestar LP; Korelya Capital SAS; Heartcore Capital

Meero SAS Paris, France Business to

Business Marketplaces

Business Support Services

Business and Financial Services

Provider of an on-demand professional photography platform for businesses.

6/18/2019 VC 3rd €205.97

White Star Capital; Prime Ventures NV*; Idinvest Partners; Global Founders Capital; Eurazeo SE*;

Avenir Growth Capital; Alven Capital SA; Aglae Ventures SAS

FINANCING

*Deal pending due to an Initial Enforcement Order made by the Competition and Markets Authority, UK pursuant to section 72(2) of the Enterprise Act 2002 (the Act)

V E N T U R E C A P I T A L R E P O R T

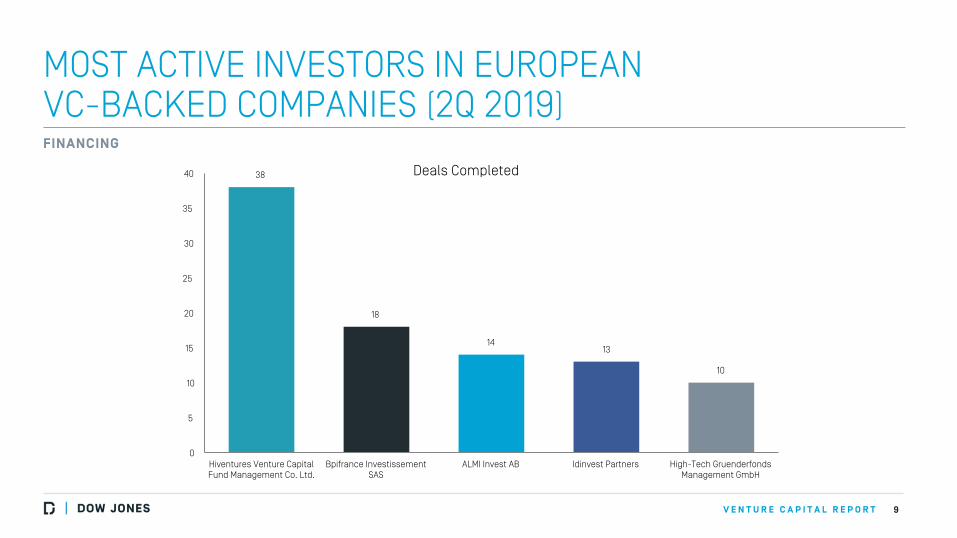

MOST ACTIVE INVESTORS IN EUROPEAN VC-BACKED COMPANIES (2Q 2019)

9

FINANCING

38

18

14 13

10

0

5

10

15

20

25

30

35

40

Hiventures Venture Capital Fund Management Co. Ltd.

Bpifrance Investissement SAS

ALMI Invest AB Idinvest Partners High-Tech Gruenderfonds Management GmbH

Deals Completed

V E N T U R E C A P I T A L R E P O R T

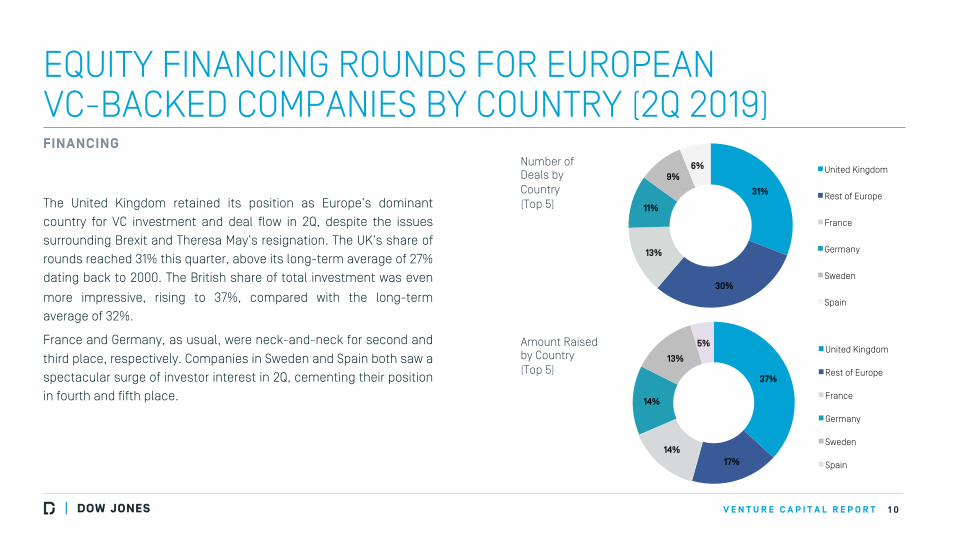

EQUITY FINANCING ROUNDS FOR EUROPEAN VC-BACKED COMPANIES BY COUNTRY (2Q 2019)

The United Kingdom retained its position as Europe’s dominant

country for VC investment and deal flow in 2Q, despite the issues

surrounding Brexit and Theresa May’s resignation. The UK’s share of

rounds reached 31% this quarter, above its long-term average of 27%

dating back to 2000. The British share of total investment was even

more impressive, rising to 37%, compared with the long-term

average of 32%.

France and Germany, as usual, were neck-and-neck for second and

third place, respectively. Companies in Sweden and Spain both saw a

spectacular surge of investor interest in 2Q, cementing their position

in fourth and fifth place.

1 0

FINANCING Number of Deals by Country (Top 5)

Amount Raised by Country (Top 5)

23%

19%

31%

30%

13%

11%

9% 6% United Kingdom

Rest of Europe

France

Germany

Sweden

Spain

37%

17% 14%

14%

13%

5% United Kingdom

Rest of Europe

France

Germany

Sweden

Spain

V E N T U R E C A P I T A L R E P O R T

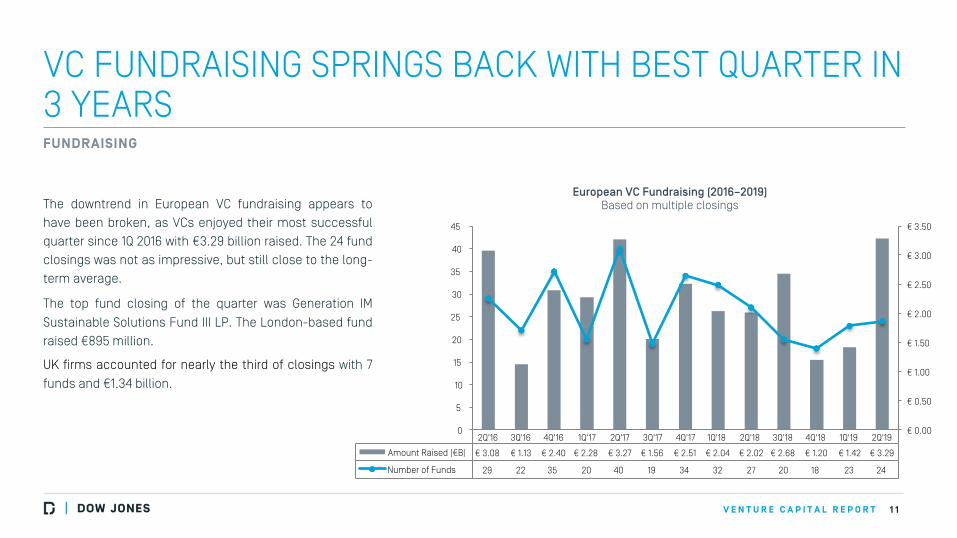

VC FUNDRAISING SPRINGS BACK WITH BEST QUARTER IN 3 YEARS

1 1

FUNDRAISING

European VC Fundraising (2016–2019) Based on multiple closings The downtrend in European VC fundraising appears to

have been broken, as VCs enjoyed their most successful

quarter since 1Q 2016 with €3.29 billion raised. The 24 fund

closings was not as impressive, but still close to the long-

term average.

The top fund closing of the quarter was Generation IM

Sustainable Solutions Fund III LP. The London-based fund

raised €895 million.

UK firms accounted for nearly the third of closings with 7

funds and €1.34 billion.

2Q'16 3Q'16 4Q'16 1Q'17 2Q'17 3Q'17 4Q'17 1Q'18 2Q'18 3Q'18 4Q'18 1Q'19 2Q'19

Amount Raised (€B) € 3.08 € 1.13 € 2.40 € 2.28 € 3.27 € 1.56 € 2.51 € 2.04 € 2.02 € 2.68 € 1.20 € 1.42 € 3.29

Number of Funds 29 22 35 20 40 19 34 32 27 20 18 23 24

0

5

10

15

20

25

30

35

40

45

€ 0.00

€ 0.50

€ 1.00

€ 1.50

€ 2.00

€ 2.50

€ 3.00

€ 3.50

V E N T U R E C A P I T A L R E P O R T

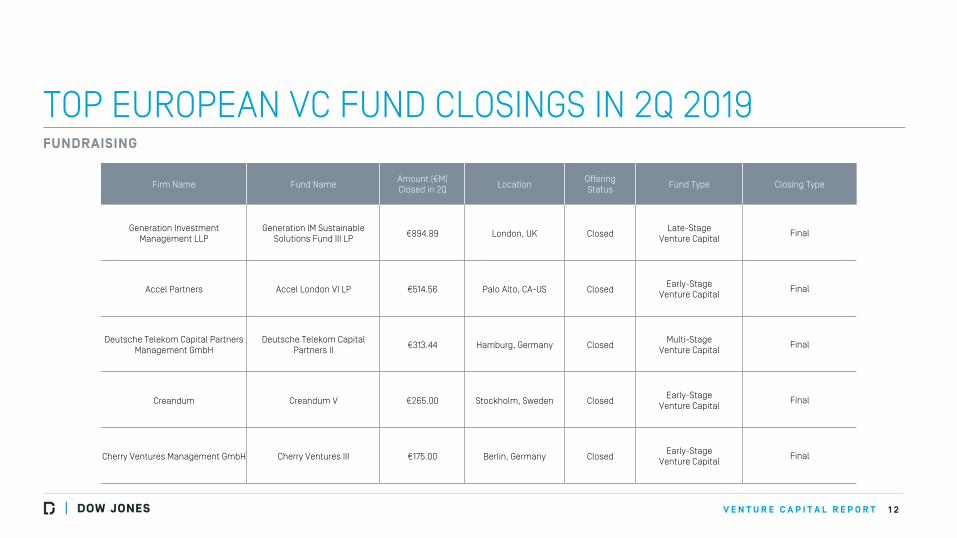

TOP EUROPEAN VC FUND CLOSINGS IN 2Q 2019

1 2

FUNDRAISING

Firm Name Fund Name Amount (€M) Closed in 2Q

Location Offering Status

Fund Type Closing Type

Generation Investment Management LLP

Generation IM Sustainable Solutions Fund III LP

€894.89 London, UK Closed Late-Stage

Venture Capital Final

Accel Partners Accel London VI LP €514.56 Palo Alto, CA-US Closed Early-Stage

Venture Capital Final

Deutsche Telekom Capital Partners Management GmbH

Deutsche Telekom Capital Partners II

€313.44 Hamburg, Germany Closed Multi-Stage

Venture Capital Final

Creandum Creandum V €265.00 Stockholm, Sweden Closed Early-Stage

Venture Capital Final

Cherry Ventures Management GmbH Cherry Ventures III €175.00 Berlin, Germany Closed Early-Stage

Venture Capital Final

V E N T U R E C A P I T A L R E P O R T

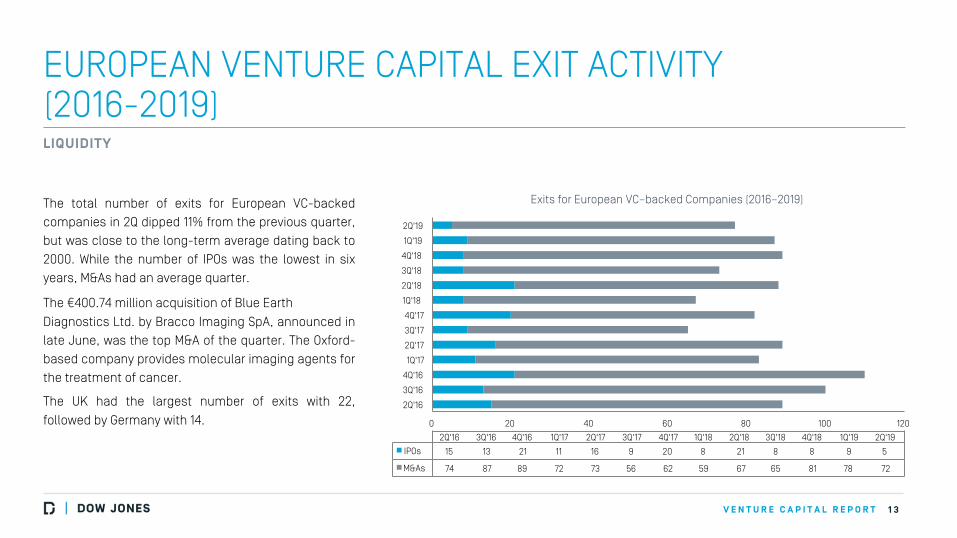

EUROPEAN VENTURE CAPITAL EXIT ACTIVITY (2016-2019)

The total number of exits for European VC-backed

companies in 2Q dipped 11% from the previous quarter,

but was close to the long-term average dating back to

2000. While the number of IPOs was the lowest in six

years, M&As had an average quarter.

The €400.74 million acquisition of Blue Earth

Diagnostics Ltd. by Bracco Imaging SpA, announced in

late June, was the top M&A of the quarter. The Oxford-

based company provides molecular imaging agents for

the treatment of cancer.

The UK had the largest number of exits with 22,

followed by Germany with 14.

1 3

LIQUIDITY

Exits for European VC–backed Companies (2016–2019)

0 20 40 60 80 100 120

2Q'16

3Q'16

4Q'16

1Q'17

2Q'17

3Q'17

4Q'17

1Q'18

2Q'18

3Q'18

4Q'18

1Q'19

2Q'19

2Q'16 3Q'16 4Q'16 1Q'17 2Q'17 3Q'17 4Q'17 1Q'18 2Q'18 3Q'18 4Q'18 1Q'19 2Q'19

IPOs 15 13 21 11 16 9 20 8 21 8 8 9 5

M&As 74 87 89 72 73 56 62 59 67 65 81 78 72

V E N T U R E C A P I T A L R E P O R T

TOP M&As IN EUROPE (2Q 2019)

1 4

Company Name Location Brief

Description Industry

Code Industry Segment Industry Group

Close Date

Round Type

Amount Paid (€M)

Acquirer

Blue Earth Diagnostics Ltd.* Oxford, UK

Provider of molecular imaging agents for the treatment of

cancer.

Diagnostic Imaging Equipment

Medical Devices and Equipment

Healthcare 6/27/2019 Acquisition €400.74 Bracco Imaging SpA

Therachon Holding AG

Basel, Switzerland

Developer of therapeutics for serious, rare conditions.

Biotechnology Therapeutics

Biopharmaceuticals Healthcare 5/8/2019 Acquisition €304.26 Pfizer Inc.

Drivy SAS Paris, France Provider of a peer-to-peer car

rental online platform. Shopping

Facilitators Consumer

Information Services Consumer Services 4/24/2019 Acquisition €267.75 Getaround Inc.

LIQUIDITY

*Deal pending regulatory approval

V E N T U R E C A P I T A L R E P O R T

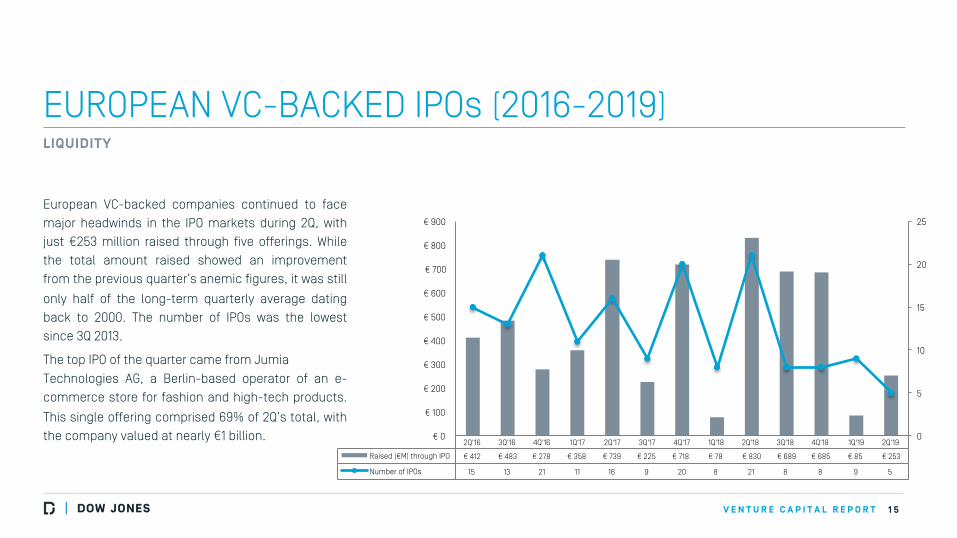

EUROPEAN VC-BACKED IPOs (2016-2019)

1 5

LIQUIDITY

European VC-backed companies continued to face

major headwinds in the IPO markets during 2Q, with

just €253 million raised through five offerings. While

the total amount raised showed an improvement

from the previous quarter’s anemic figures, it was still

only half of the long-term quarterly average dating

back to 2000. The number of IPOs was the lowest

since 3Q 2013.

The top IPO of the quarter came from Jumia

Technologies AG, a Berlin-based operator of an e-

commerce store for fashion and high-tech products.

This single offering comprised 69% of 2Q’s total, with

the company valued at nearly €1 billion.

2Q'16 3Q'16 4Q'16 1Q'17 2Q'17 3Q'17 4Q'17 1Q'18 2Q'18 3Q'18 4Q'18 1Q'19 2Q'19

Raised (€M) through IPO € 412 € 483 € 278 € 358 € 739 € 225 € 718 € 78 € 830 € 689 € 685 € 85 € 253

Number of IPOs 15 13 21 11 16 9 20 8 21 8 8 9 5

0

5

10

15

20

25

€ 0

€ 100

€ 200

€ 300

€ 400

€ 500

€ 600

€ 700

€ 800

€ 900

V E N T U R E C A P I T A L R E P O R T

TOP IPOs IN EUROPE (2Q 2019)

1 6

LIQUIDITY

Company Name Location Brief

Description Industry

Code Industry Segment Industry Group

Close Date

Raised through IPO (€M)

Exchange: Ticker

Jumia Technologies AG

Berlin, Germany Operator of an e-commerce store

for fashion and high-tech products.

Shopping Facilitators Consumer

Information Services Consumer Services 4/12/2019 €174.71

NYSE: JMIA

Bicycle Therapeutics Ltd.

Cambridge, UK Developer of a biotherapeutics platform using bicyclic peptide

technology.

Biotechnology Therapeutics

Biopharmaceuticals Healthcare 5/23/2019 €54.29 Nasdaq:

BCYC

OssDsign AB Uppsala, Sweden Developer of implantable

materials for bone healing. Therapeutic Devices

(Invasive) Medical Devices and

Equipment Healthcare 5/24/2019 €14.14

Nasdaq: OSSD

V E N T U R E C A P I T A L R E P O R T

ABOUT US & METHODOLOGY

Dow Jones VentureSource helps venture capitalists, corporate development executives, investment bankers and service providers find deal and

partnership opportunities, perform comprehensive due diligence and examine trends in venture capital investment, fund-raising and liquidity. It provides

accurate, comprehensive data on venture-backed companies – including their investors and executives – in every region, industry and stage of

development throughout the world.

The investment figures included in this report cover venture backed companies headquartered in Europe, and are based on aggregate findings of Dow

Jones’ proprietary research for VentureSource.

This data was collected through surveys of professional firms, interviews with company executives, and from secondary sources. To be included,

companies have to receive financing from a venture capital or private equity firm. Our figures do not include companies that have received funding solely

from individual, corporate and/or government investors. The data in this report only accounts for equity funding, not convertible debt deals.

Figures contained throughout the report are current at time of editorial but subject to change without notice. No statement herein is to be construed as a

recommendation to buy or sell securities, or to provide investment advice.

1 7

V E N T U R E C A P I T A L R E P O R T

ABOUT DOW JONES

Dow Jones is a global provider of news and business information, delivering content to consumers and organizations around the world across multiple

formats, including print, digital, mobile and live events. Dow Jones has produced unrivaled quality content for more than 125 years and today has one of

the world’s largest newsgathering operations globally. It produces leading publications and products including the flagship Wall Street Journal,

America’s largest newspaper by paid circulation; Factiva, Barron’s, MarketWatch, Financial News, DJX, Dow Jones Risk & Compliance, Dow Jones

Newswires, and Dow Jones VentureSource.

MEDIA CONTACT:

Sophie Bent

+44 (0) 203 426 1381

1 8