rcm 401

DESCRIPTION

Responsibility Center Management. RCM 401. David Proulx, Assistant Vice President for Financial Planning and Budgeting EMail: [email protected] Budget Office Website: http://www.unh.edu/budget RCM Website: http://www.unh.edu/rcm. RCM 401. Presentation Outline. 1. UNH Overview - PowerPoint PPT PresentationTRANSCRIPT

David Proulx, Assistant Vice President for Financial Planning and BudgetingDavid Proulx, Assistant Vice President for Financial Planning and BudgetingEMail: [email protected]: [email protected]

Budget Office Website: http://www.unh.edu/budgetBudget Office Website: http://www.unh.edu/budgetRCM Website: http://www.unh.edu/rcmRCM Website: http://www.unh.edu/rcm

Responsibility Center ManagementResponsibility Center Management

Presentation OutlinePresentation Outline

1. UNH Overview1. UNH Overview2. What is RCM?2. What is RCM?

3. 5 year review3. 5 year review

Current Fund Revenue FY06*$435.1 Million**

28.5%

Tuition and Fees, net of Financial

Aid$123.9M

25.3%

Other Sources, Primarily

Auxiliaries$110.1M

5.0%

Gifts & Endowment

Income$21.6M

27.0%

Sponsored Programs & Federal Aid$117.8M

14.2%

State of NH General

Appropriations$61.7M

*Includes Durham, Manchester, NHPTV and UNH-Foundation **Excludes Loan, Plant, and Endowment & Similar Funds

State Appropriations for Higher Education Operations Per Capita

FY 2006

Vermont #48

Colorado #49

New Hampshire #50

$50 $65 $80 $95 $110 $125 $140

Per Capita Appropriation Dollars

New Hampshire would have to increase it's funding by: 44% to reach #49 (Colorado) and

48% to reach #48 (Vermont)

Source: National Center for Public Policy and Higher Educationhttp://measuringup.highereducation.org/

UNH Resident Cost of AttendanceTuition/Room/Board/Fees

vs. New England Land Grant Institutions

$10,000

$11,000

$12,000

$13,000

$14,000

$15,000

$16,000

$17,000

$18,000

$19,000

FY 02 FY 03 FY 04 FY 05 FY 06

UVM

UNH

UMASS/AMHERST

AVERAGE

UCONN

URI

UMAINE

UNH Non-Resident Cost of AttendanceTuition/Room/Board/Fees

vs. New England Land Grant Institutions

$18,000

$20,000

$22,000

$24,000

$26,000

$28,000

$30,000

$32,000

$34,000

FY 02 FY 03 FY 04 FY 05 FY 06

UVM

UNH

UCONN

URI

AVERAGE

UMASS/AMHERST

UMAINE

UNH Durham General Fund Undergraduate Aid

$-

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

$18,000,000

FY1998 FY1999 FY2000 FY2001 FY2002 FY2003 FY2004 FY2005 FY2006

Fiscal Year

Fin

an

cia

l A

id $

Need Based Financial Aid

Merit Based Financial Aid

Athletic Scholarships

Cooperative Agreements

Entitlements

Revenue SummaryRevenue Summary

$435 million current fund revenues$435 million current fund revenues

Research, net tuition and auxiliary revenue Research, net tuition and auxiliary revenue greatest sourcesgreatest sources

Major challenges in state appropriation Major challenges in state appropriation revenues, financial aid and grant fundingrevenues, financial aid and grant funding

Great dependence on out of state studentsGreat dependence on out of state students

Current Fund Expenditures FY06*$427.6 Million**

24.4%Supplies & Services$104.5M

47.3%Salaries & Wages

$202.1M

15.7%Fringe Benefits

$67.3M

9.1%Transfers$38.8M

3.5%Utilities$14.9M

**Excludes Unfunded Benefits, Loan, Plant and Endowment & Similar Funds*Durham, Manchester, NHPTV, UNH-Foundation

UNH Durham Energy Costs

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,000

$8,000,000

FY02 FY03 FY04 FY05 FY06

Electricity (14,8% Growth)

Heating Oil #6 (18% Growth)

Natural Gas (38.3% Growth)Heating Oil #2 (38.9% Growth)

Propane (22.9% Growth)

Expense SummaryExpense Summary

Personnel – largest component of expensePersonnel – largest component of expenseMedical benefit cost growing significantlyMedical benefit cost growing significantlyEnergy costs growing significantlyEnergy costs growing significantlyBehind on renewal and replacement of Behind on renewal and replacement of physical plantphysical plantGrowth rate on general fund revenue – 4% Growth rate on general fund revenue – 4% and expense – 4.5%. Need to address and expense – 4.5%. Need to address structural issuestructural issue

Presentation OutlinePresentation Outline

1. UNH Overview1. UNH Overview

2. What is RCM?2. What is RCM?3. 5 year review3. 5 year review

What is RCM?Responsibility Center Management

A tool to help UNH manage its resources in a manner to meet the goals outlined in the University’s Academic Plan Informs management of financial impact of

decisions Makes explicit where revenues go and how

they are spent Promotes accountability at all levels of

management

Old Old

BudgetBudget

SystemSystem

Old Old

BudgetBudget

SystemSystem

Institutional Revenue- Tuition- Indirect Cost Recovery- State AppropriationRevenue

UNH Divisions- Colleges/Library- Research and PublicService Units- Auxiliary Operations

Direct Expense- Payroll- Support- Debt service

University Budget Panelallocates revenue to

departments in form of $142million E&G Budget

Department (Direct) Revenue- Grant/Contracts- RestrictedGifts/Endowment- Sales of goods/services- Fees

Institutional Overhead (Service Units)- Facilities- CIS- Student Affairs- VP Research- General Admin- Academic Affairs

RCM RCM

BudgetBudget

SystemSystem

RCM RCM

BudgetBudget

SystemSystem

Revenue- Tuition- Indirect Cost Recovery- State AppropriationRevenue- Direct Revenue (Grant,Gift, Sales, Fees, etc.)

RC Units- Academic- Research- Auxiliary

Direct Expense- Salaries, Wages & Benefits- Support- Debt service

Central Budget Committee

- Incremental fundingdecisions- $700k University Fundallocation- Service Unit Advisory Boardsubcommittee to reviewService Units if necessary

Institutional Overhead- Facilities- CIS- Student Affairs- VP Research- General Admin- Academic Affairs

RC Units

Colleges and Related Service Units Research and Public Service Units College of Life Sciences and

Agriculture College of Liberal Arts College of Engineering and Physical

Sciences Whittemore School of Business and

Economics School of Health and Human Services UNH – Manchester Library

Cooperative Extension Research and Public Service New Hampshire Public Television Institute for Earth, Oceans and Space

Student and Community Life Units Governance, Advancement andInfrastructure Units

Student Affairs Housing Hospitality Services Intercollegiate Athletics Whittemore Center Arena

Facilities Services Computing and Information Services General Administration Academic Affairs

RCM Principles

1. It should be simple to provide easy comprehension and efficient administration

2. It should produce results that are widely perceived as fair

3. It should encourage behaviors that support the institution’s mission and academic plan

4. It should have strong governance and planning mechanisms

Shared GovernanceCentral Budget Committee

The governing group on budget policy and financial planning for the campus community.

Responsibilities include oversight of RCM, review of internal fees, oversight of assessment rates and central service budgets, oversight of facilities chargeout rates, and advising President on significant budgetary/financial issues.

Comprised of President (Chair), Vice Presidents, 2 Deans, 4 Faculty, 2 RC Unit Directors, Staff rep, Student Treasurer, Graduate Student Organization rep

Unit Financial Unit Financial StructureStructure

Units receive direct revenues (fees, grants, gifts, Units receive direct revenues (fees, grants, gifts, etc) as well as applicable allocated revenues etc) as well as applicable allocated revenues (net tuition, state appropriations, indirect cost (net tuition, state appropriations, indirect cost recovery, CBC allocations and hold harmless)recovery, CBC allocations and hold harmless)Units are responsible for direct expenses Units are responsible for direct expenses (salaries, wages, fringe benefits, support) as (salaries, wages, fringe benefits, support) as well as indirect expenses (facilities, general and well as indirect expenses (facilities, general and academic overhead)academic overhead)Unspent funds at end of year are allowed to Unspent funds at end of year are allowed to drop to a unit “reserve”drop to a unit “reserve”Most auxiliary operations (MUB, Campus Rec, Most auxiliary operations (MUB, Campus Rec, Health Services, Counseling Center, Housing Health Services, Counseling Center, Housing and Dining) have operated in a RCM type and Dining) have operated in a RCM type system prior to campus wide implementation of system prior to campus wide implementation of RCMRCM

Before and AfterBefore and AfterRCM implemented on July 1, 2001.RCM implemented on July 1, 2001.

Item Before After Overhead for Auxiliaries Admin Service charge, safety and

security allocation, facilities charge General assessment and facilities allocation

Academic incentives No incentives for schools and colleges to pay attention to enrollments, curriculum and retention of students

Direct financial incentives for enrollments, curriculum and retention

Governance No participation in central financial governance by students, faculty or staff

Central Budget Committee – seats for faculty, students and staff

Incentives for good financial management

Few incentives in non auxiliary units to be efficient or generate new revenues

Incentives for all units to be efficient and generate new revenues

Presentation OutlinePresentation Outline

1. Overview1. Overview

2.2. What is RCM?What is RCM?

3. 5 year review3. 5 year review

PurposePurpose

Understand impact of RCM over the past 5 Understand impact of RCM over the past 5 yearsyears

Align RCM allocation methodologies to Align RCM allocation methodologies to goals outlined in Academic Plangoals outlined in Academic Plan

Provide opportunity for community to be Provide opportunity for community to be informed and participate in discussionsinformed and participate in discussions

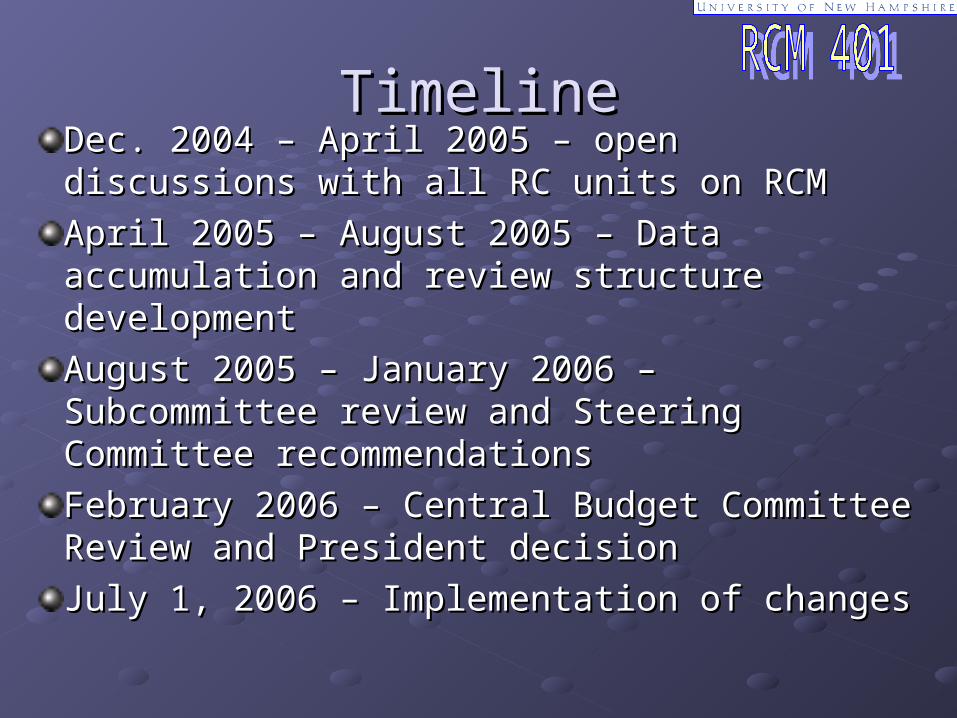

TimelineTimelineDec. 2004 – April 2005 – open discussions Dec. 2004 – April 2005 – open discussions with all RC units on RCM with all RC units on RCM

April 2005 – August 2005 – Data accumulation April 2005 – August 2005 – Data accumulation and review structure developmentand review structure development

August 2005 – January 2006 – Subcommittee August 2005 – January 2006 – Subcommittee review and Steering Committee review and Steering Committee recommendationsrecommendations

February 2006 – Central Budget Committee February 2006 – Central Budget Committee Review and President decisionReview and President decision

July 1, 2006 – Implementation of changesJuly 1, 2006 – Implementation of changes

ParticipationParticipation

Steering Committee and 7 subcommittees Steering Committee and 7 subcommittees – 58 total members including 2 students – 58 total members including 2 students on Steering Committeeon Steering Committee

17 meetings and 2 open forums for 17 meetings and 2 open forums for information gathering/feedback. 2 open information gathering/feedback. 2 open forums for initial recommendations. forums for initial recommendations.

Review ResultsReview Results

RCM works well for UNH and should remain as RCM works well for UNH and should remain as budgeting toolbudgeting tool

Enhance communications in some areasEnhance communications in some areas

Allocation formulas changed to create better Allocation formulas changed to create better incentives/more alignment with Academic Plan incentives/more alignment with Academic Plan (impact in FY07 of changes was zero – offset by (impact in FY07 of changes was zero – offset by hold harmless allocation)hold harmless allocation)

Elimination of hold harmless allocation and review Elimination of hold harmless allocation and review of assessment funded unitsof assessment funded units

RCM should be reviewed again in FY11RCM should be reviewed again in FY11

Where to get help?Where to get help?

UNH RCM Website – information on 5 year UNH RCM Website – information on 5 year review, RCM principles, RCM manual, etc – review, RCM principles, RCM manual, etc – www.unh.edu/rcm

Call David Proulx at 2-2421 or send me email at Call David Proulx at 2-2421 or send me email at [email protected]