quarterly economic review of the food and beverages

TRANSCRIPT

Quarterly Economic Review of the Food

and Beverages Industry in South Africa

April to June 2018

Volume 5, number 1

DIRECTORATE: AGRO-PROCESSING SUPPORT

agriculture,forestry & fisheries

i

PREFACE

The agro-processing industry is among the sectors identified by the Industrial Policy Action Plan

(IPAP) and the National Development Plan for its potential to spur growth, development and

job creation via its strong backward and forward linkages with the other sectors of the

economy. DAFF established the Directorate: Agro-processing Support in 2011 to facilitate the

processing of raw primary agriculture, forestry and fisheries commodities into value added

products.

One of the functions of the directorate is to provide timely and updated economic information

regarding the agro-processing industry as part of monitoring and evaluating the performance

of the industry. Additionally, economic indicators provide an insight into the effects of

economic policies and other exogenous factors. To achieve this purpose, the directorate

publishes regular quarterly economic reviews of the agro-processing industry.

The main economic indicators reviewed are the changes in prices, production, capacity

utilisation, value of sales, formal employment and trade. An outlook of the industry for the next

quarter is also presented. In addition, some indicators of the food and beverages service

industry, wholesale and retail sectors are reviewed to evaluate the forward linkages of the

food and beverages industry.

Any comments and suggestions on the content of the publication are most welcome.

Mahlogedi Victor Thindisa

Director: Agro-processing Support

Pretoria

Disclaimer: The Department of Agriculture, Forestry and Fisheries did everything to ensure the

accuracy of the information reported in this publication. The department will, however, not be

liable for the results of action based on this publication.

ii

CONTENTS

PREFACE ................................................................................................................................................ i

1. INTRODUCTION ........................................................................................................................... 1

2. FOOD PRODUCTS ....................................................................................................................... 1

2.1 PRICE ..................................................................................................................................... 1

2.2 PRODUCTION ...................................................................................................................... 4

2.3 VALUE OF SALES .................................................................................................................. 5

2.4 INCOME FROM FOOD SALES IN THE SERVICE INDUSTRY .......................................... 7

2.5 TRADE .................................................................................................................................... 8

2.6 EMPLOYMENT .................................................................................................................... 17

2.7 OUTLOOK ............................................................................................................................ 18

3. BEVERAGES ................................................................................................................................ 19

3.1 PRICE ................................................................................................................................... 19

3.2 PRODUCTION .................................................................................................................... 20

3.3 VALUE OF SALES ................................................................................................................ 21

3.4 INCOME FROM BAR SALES IN THE SERVICE INDUSTRY ............................................ 22

3.5 TRADE .................................................................................................................................. 23

3.6 EMPLOYMENT .................................................................................................................... 32

3.7 OUTLOOK ............................................................................................................................ 32

4. CONCLUSION ............................................................................................................................ 33

5. REFERENCES ............................................................................................................................... 34

NOTES: ................................................................................................................................................. 35

Compiled by Directorate: Agro-processing Support

Department of Agriculture, Forestry and Fisheries

Sefala Building

503 Belvedere Street, Arcadia, South Africa

All correspondence can be addressed to:

Director: Agro-processing Support

Private Bag X416, Pretoria 0001, South Africa

Tel.: +27 (12) 319 8457

Fax: +27 (12) 319 8093

E-mail: [email protected]

This publication is also available on the internet at: http://www.daff.gov.za

1

1. INTRODUCTION

The South African real gross domestic product (GDP) continued to contract at an annualized

rate of 0,7% in the second quarter of 2018. This followed a revised decline of 2,6% in the first

quarter of 2018, which consequently led the economy entering into a technical recession. The

real output of the primary sector contracted further in the second quarter of 2018 as

agricultural output again decreased sharply, owing to the lower production of horticultural

products and in particular field crops, in part due to a delay in the harvesting of maize. Similarly,

the manufacturing sector contracted marginally in the second quarter of 2018, mainly

impacted by higher input costs and weak domestic demand (SA Reserve Bank 2018).

This quarterly review provides an analysis of the economic performance of the food and

beverages industry. The variables that are analysed are exports and imports of food and

beverages, employment, net balance survey, price index, volume of production, sales,

utilisation capacity, and wholesale and retail performances.

2. FOOD PRODUCTS

According to the Standard Industrial Classification, the food industry incorporates groups of

products that are categorised into the following four codes:

Code 301: refers to manufacturing, processing and preservation of meat, fish,

vegetables, fruits, oils and fats

Code 302: refers to manufacturing, processing and preservation of dairy products

Code 303: refers to manufacture of grain mill products, starch products and prepared

animal feeds

Code 304: refers to manufacture of other food products like bread, sugar, chocolate,

pasta, coffee, nuts and spices.

Hereafter, food products refer to those primary agricultural and fisheries products that have

undergone some form of change through manufacturing and processing or performed some

value addition activities such as preservation.

2.1 PRICE

Consumer Price Index (CPI)1

The quarter-to-quarter consumer price index of all items grew by 1,4% in 2018: Q2. Some of the

items that grew in the period under review were: fish (2,4%), vegetables (2,3%), other foods

(1,2%), milk, eggs and cheese (0,3%). However, fruit (4,2%), sugar, sweets and deserts (2,8%),

oils and fats (1,7%), and bread and cereals (0,6%) declined during the period under review.

Similarly, the year-on-year consumer price index increased for meat (7,8%), fish (7,5%), milk,

eggs and cheese(4,5%), vegetables (3,7%). However, fruit (6,3%), bread and cereals (5,3%) ,

sugar, sweets and deserts (3,9%) and oils and fats (2,5%) declined, year-on-year during the

period under review.

1 Stats SA defines CPI as a current social and economic indicator that is constructed to measure changes over time in

the general level of prices of consumer goods and services that households acquire, use, or pay for.

2

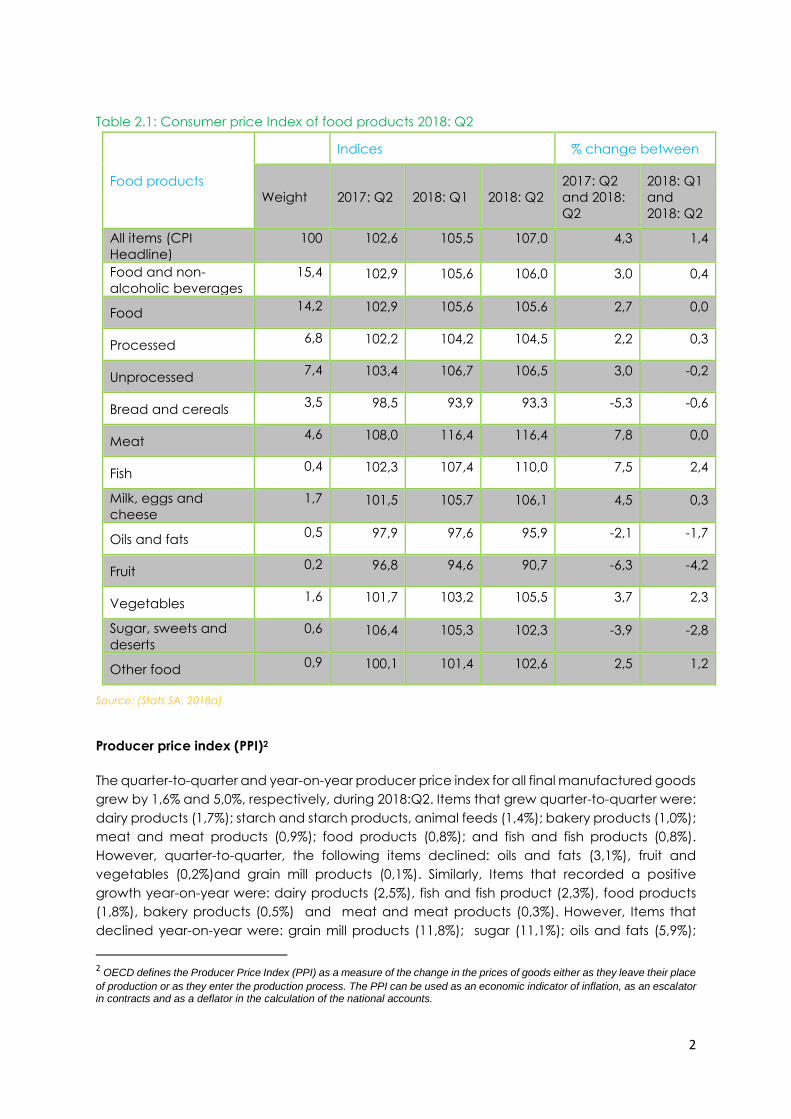

Table 2.1: Consumer price Index of food products 2018: Q2

Indices % change between

Food products

Weight 2017: Q2 2018: Q1 2018: Q2

2017: Q2

and 2018:

Q2

2018: Q1

and

2018: Q2

All items (CPI

Headline)

100 102,6 105,5 107,0 4,3 1,4

Food and non-

alcoholic beverages

15,4 102,9 105,6 106,0 3,0 0,4

Food 14,2 102,9 105,6 105.6 2,7 0,0

Processed 6,8 102,2 104,2 104,5 2,2 0,3

Unprocessed 7,4 103,4 106,7 106,5 3,0 -0,2

Bread and cereals 3,5 98,5 93,9 93,3 -5,3 -0,6

Meat 4,6 108,0 116,4 116,4 7,8 0,0

Fish 0,4 102,3 107,4 110,0 7,5 2,4

Milk, eggs and

cheese

1,7 101,5 105,7 106,1 4,5 0,3

Oils and fats 0,5 97,9 97,6 95,9 -2,1 -1,7

Fruit 0,2 96,8 94,6 90,7 -6,3 -4,2

Vegetables 1,6 101,7 103,2 105,5 3,7 2,3

Sugar, sweets and

deserts

0,6 106,4 105,3 102,3 -3,9 -2,8

Other food 0,9 100,1 101,4 102,6 2,5 1,2

Source: (Stats SA, 2018a)

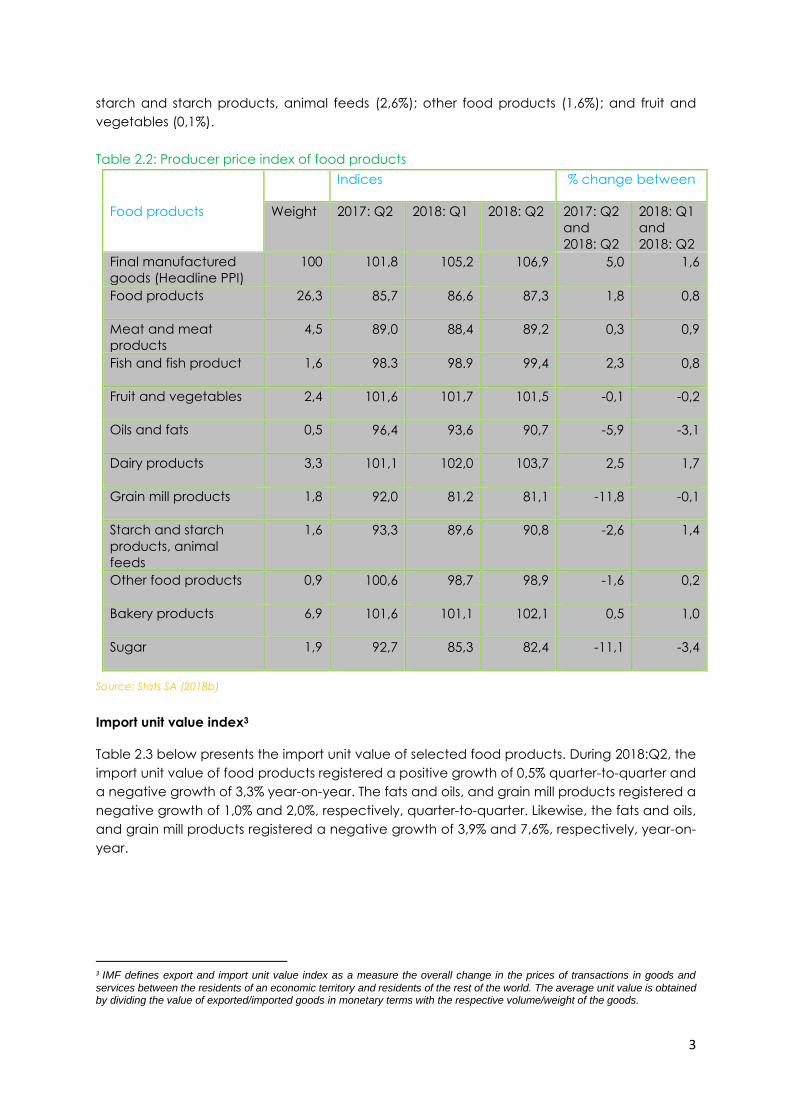

Producer price index (PPI)2

The quarter-to-quarter and year-on-year producer price index for all final manufactured goods

grew by 1,6% and 5,0%, respectively, during 2018:Q2. Items that grew quarter-to-quarter were:

dairy products (1,7%); starch and starch products, animal feeds (1,4%); bakery products (1,0%);

meat and meat products (0,9%); food products (0,8%); and fish and fish products (0,8%).

However, quarter-to-quarter, the following items declined: oils and fats (3,1%), fruit and

vegetables (0,2%)and grain mill products (0,1%). Similarly, Items that recorded a positive

growth year-on-year were: dairy products (2,5%), fish and fish product (2,3%), food products

(1,8%), bakery products (0,5%) and meat and meat products (0,3%). However, Items that

declined year-on-year were: grain mill products (11,8%); sugar (11,1%); oils and fats (5,9%);

2 OECD defines the Producer Price Index (PPI) as a measure of the change in the prices of goods either as they leave their place

of production or as they enter the production process. The PPI can be used as an economic indicator of inflation, as an escalator in contracts and as a deflator in the calculation of the national accounts.

3

starch and starch products, animal feeds (2,6%); other food products (1,6%); and fruit and

vegetables (0,1%).

Table 2.2: Producer price index of food products

Indices % change between

Food products Weight 2017: Q2 2018: Q1 2018: Q2 2017: Q2

and

2018: Q2

2018: Q1

and

2018: Q2

Final manufactured

goods (Headline PPI)

100 101,8 105,2 106,9 5,0 1,6

Food products 26,3 85,7 86,6 87,3 1,8 0,8

Meat and meat

products

4,5 89,0 88,4 89,2 0,3 0,9

Fish and fish product 1,6 98.3 98.9 99,4 2,3 0,8

Fruit and vegetables 2,4 101,6 101,7 101,5 -0,1 -0,2

Oils and fats 0,5 96,4 93,6 90,7 -5,9 -3,1

Dairy products 3,3 101,1 102,0 103,7 2,5 1,7

Grain mill products 1,8 92,0 81,2 81,1 -11,8 -0,1

Starch and starch

products, animal

feeds

1,6 93,3 89,6 90,8 -2,6 1,4

Other food products 0,9 100,6 98,7 98,9 -1,6 0,2

Bakery products 6,9 101,6 101,1 102,1 0,5 1,0

Sugar 1,9 92,7 85,3 82,4 -11,1 -3,4

Source: Stats SA (2018b)

Import unit value index3

Table 2.3 below presents the import unit value of selected food products. During 2018:Q2, the

import unit value of food products registered a positive growth of 0,5% quarter-to-quarter and

a negative growth of 3,3% year-on-year. The fats and oils, and grain mill products registered a

negative growth of 1,0% and 2,0%, respectively, quarter-to-quarter. Likewise, the fats and oils,

and grain mill products registered a negative growth of 3,9% and 7,6%, respectively, year-on-

year.

3 IMF defines export and import unit value index as a measure the overall change in the prices of transactions in goods and

services between the residents of an economic territory and residents of the rest of the world. The average unit value is obtained by dividing the value of exported/imported goods in monetary terms with the respective volume/weight of the goods.

4

Table 2.3: import unit value index of food products

Source: Stats SA (2018c)

2.2 PRODUCTION

Source: Statistics SA (2018d)

Figure 2.1: presents a physical volume of production for the food products division. The quarter-

to-quarter physical volume of production for meat, fish, fruit; dairy products; and grain mill

products contracted by 1,5, 0,9%, and 2,1% in 2018: Q2 as compared to a growth of 2,5%,

3,2% and 2,9%, respectively, in the preceding quarter. However, other food products grew

marginally by 2,6% from a 1,8 growth in the last quarter. The year-on-year physical volume of

production for meat, fish, fruit; dairy; grain mill products; and other food products moderated

by 2,6%, 2,8%, 2,9% and 9,1% from a growth of 3,4%, 7,3%, 6,1% and 11,0% respectively, in the

preceding quarter.

50

60

70

80

90

100

110

120

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

20

14

: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

20

17

: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

(R m

illio

n)

Figure 2.1: Seasonally adjusted physical volume of production: food

products

Meat, fish, fruit etc Dairy products Grain mill products Other food products

Food products

Indices % change between

2017: Q2 2018: Q1 2018: Q2

2017: Q2

and 2018:

Q2

2018: Q1

and 2017:

Q2

Food (total) 91,9 88,5 88,9 -3,3 0,5

Fats and oils 99,6 96,7 95,7 -3,9 -1,0

Grain mill products 100,0 94,2 92,4 -7,6 -2,0

5

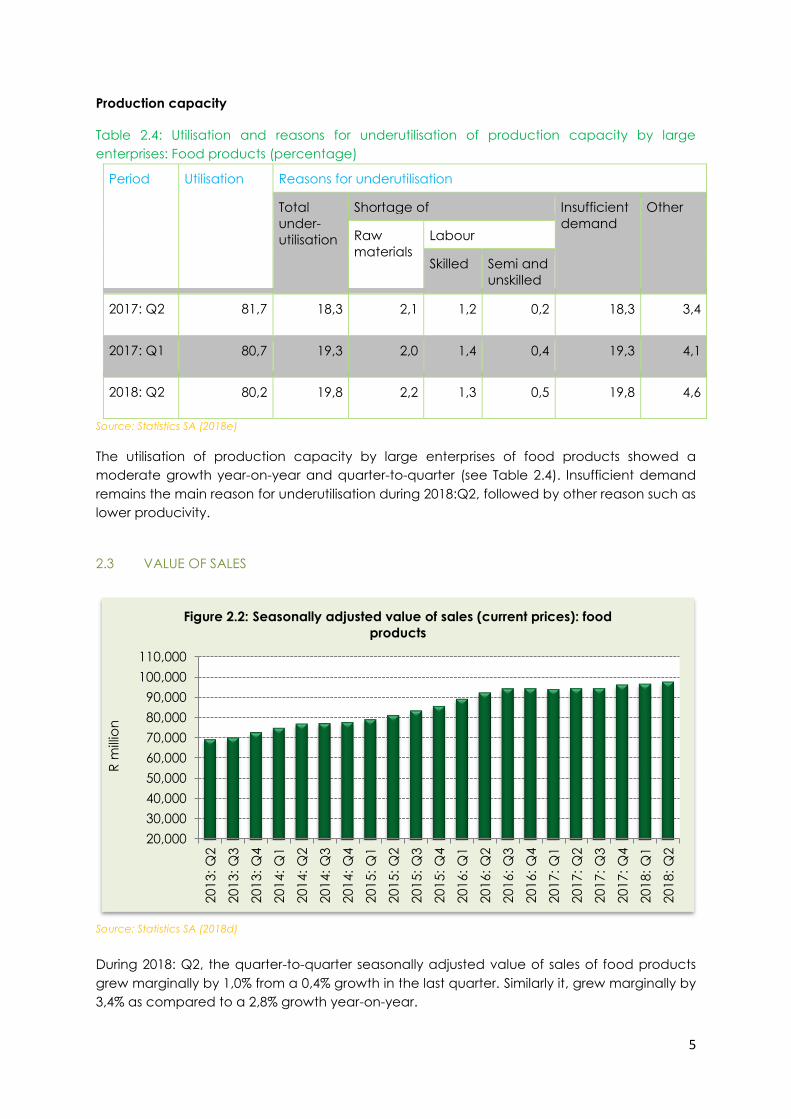

Production capacity

Table 2.4: Utilisation and reasons for underutilisation of production capacity by large

enterprises: Food products (percentage)

Period Utilisation Reasons for underutilisation

Total

under-

utilisation

Shortage of Insufficient

demand

Other

Raw

materials

Labour

Skilled Semi and

unskilled

2017: Q2 81,7 18,3 2,1 1,2 0,2 18,3 3,4

2017: Q1 80,7 19,3 2,0 1,4 0,4 19,3 4,1

2018: Q2 80,2 19,8 2,2 1,3 0,5 19,8 4,6

Source: Statistics SA (2018e)

The utilisation of production capacity by large enterprises of food products showed a

moderate growth year-on-year and quarter-to-quarter (see Table 2.4). Insufficient demand

remains the main reason for underutilisation during 2018:Q2, followed by other reason such as

lower producivity.

2.3 VALUE OF SALES

Source: Statistics SA (2018d)

During 2018: Q2, the quarter-to-quarter seasonally adjusted value of sales of food products

grew marginally by 1,0% from a 0,4% growth in the last quarter. Similarly it, grew marginally by

3,4% as compared to a 2,8% growth year-on-year.

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

110,000

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

20

16

: Q

1

201

6: Q

2

20

16

: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

R m

illio

n

Figure 2.2: Seasonally adjusted value of sales (current prices): food

products

6

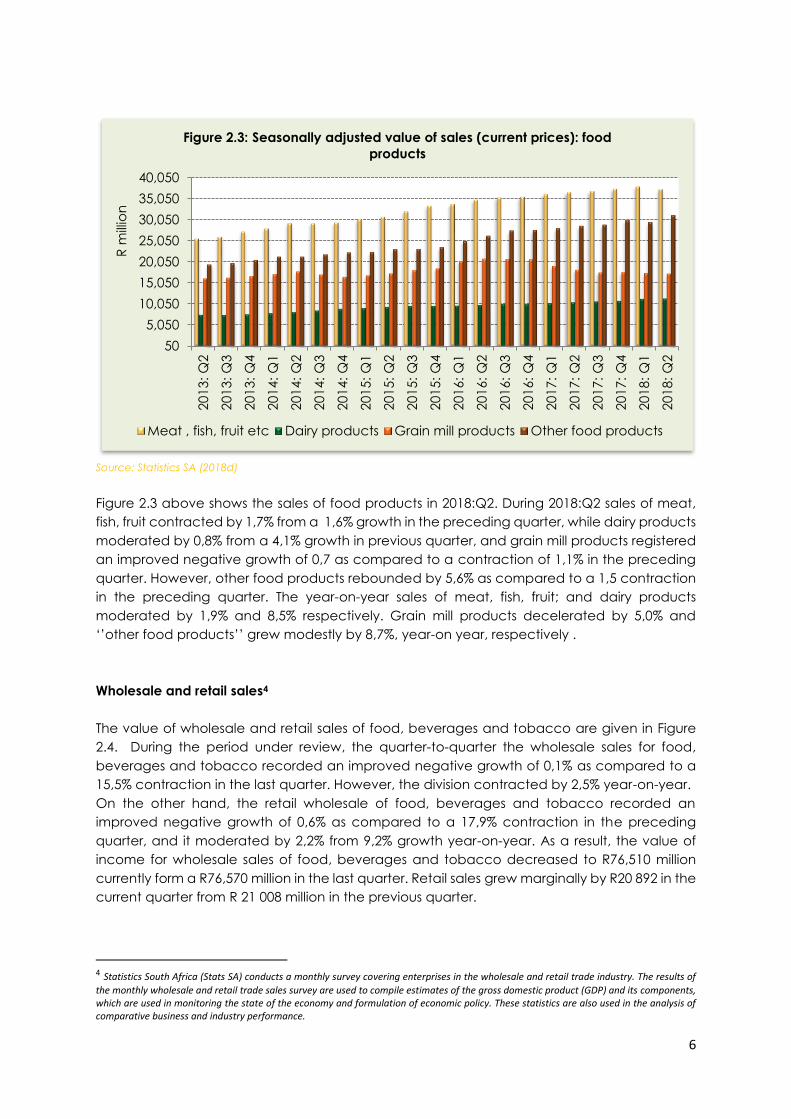

Source: Statistics SA (2018d)

Figure 2.3 above shows the sales of food products in 2018:Q2. During 2018:Q2 sales of meat,

fish, fruit contracted by 1,7% from a 1,6% growth in the preceding quarter, while dairy products

moderated by 0,8% from a 4,1% growth in previous quarter, and grain mill products registered

an improved negative growth of 0,7 as compared to a contraction of 1,1% in the preceding

quarter. However, other food products rebounded by 5,6% as compared to a 1,5 contraction

in the preceding quarter. The year-on-year sales of meat, fish, fruit; and dairy products

moderated by 1,9% and 8,5% respectively. Grain mill products decelerated by 5,0% and

‘’other food products’’ grew modestly by 8,7%, year-on year, respectively .

Wholesale and retail sales4

The value of wholesale and retail sales of food, beverages and tobacco are given in Figure

2.4. During the period under review, the quarter-to-quarter the wholesale sales for food,

beverages and tobacco recorded an improved negative growth of 0,1% as compared to a

15,5% contraction in the last quarter. However, the division contracted by 2,5% year-on-year.

On the other hand, the retail wholesale of food, beverages and tobacco recorded an

improved negative growth of 0,6% as compared to a 17,9% contraction in the preceding

quarter, and it moderated by 2,2% from 9,2% growth year-on-year. As a result, the value of

income for wholesale sales of food, beverages and tobacco decreased to R76,510 million

currently form a R76,570 million in the last quarter. Retail sales grew marginally by R20 892 in the

current quarter from R 21 008 million in the previous quarter.

4 Statistics South Africa (Stats SA) conducts a monthly survey covering enterprises in the wholesale and retail trade industry. The results of

the monthly wholesale and retail trade sales survey are used to compile estimates of the gross domestic product (GDP) and its components, which are used in monitoring the state of the economy and formulation of economic policy. These statistics are also used in the analysis of comparative business and industry performance.

50

5,050

10,050

15,050

20,050

25,050

30,050

35,050

40,050

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

R m

illio

n

Figure 2.3: Seasonally adjusted value of sales (current prices): food

products

Meat , fish, fruit etc Dairy products Grain mill products Other food products

7

Source: Statistics SA (2018f, 2018g)

2.4 INCOME FROM FOOD SALES IN THE SERVICE INDUSTRY5

Table 2,5 below, shows, the income from food sales5 in the service industry includes food sales

in restaurants and coffee shops6, take-away and fast food outlet7 and catering services8.

5 Income from food sales in the service industry refers to income from the sale of meals and non-alcoholic drinks.

6 Restaurants and coffee shops refers to enterprises involved in the sale and provision of meals and drinks, ordered from a menu, prepared on the premises for immediate consumption and with provided seating. 7 Take-away and fast food outlet refers to eenterprises involved in the sale and provision of meals and drinks, ordered from a menu, prepared on the premises for takeaway purposes in a packaged format, at a stand or in a location, with or without provided seating. 8 Catering services refers to eenterprises involved in the sale and supply of meals and drinks prepared on the premises on a contract basis and brought to other premises chosen by the person ordering them, to be served for immediate consumption to guests or customers. Catering services also include bars, taverns, other drinking places, ice-cream parlours, etc.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

20

14

: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

R m

illio

nFigure 2.4: Wholesale and retail trade sales of food, beverages and

tobacco (current prices)

Wholesale Retail Trade Sales

5001,0001,5002,0002,5003,0003,5004,0004,5005,0005,5006,0006,5007,0007,5008,0008,5009,0009,500

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

20

15

: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

R m

illio

n

Figure 2.5: Income from food sales in the service industry

8

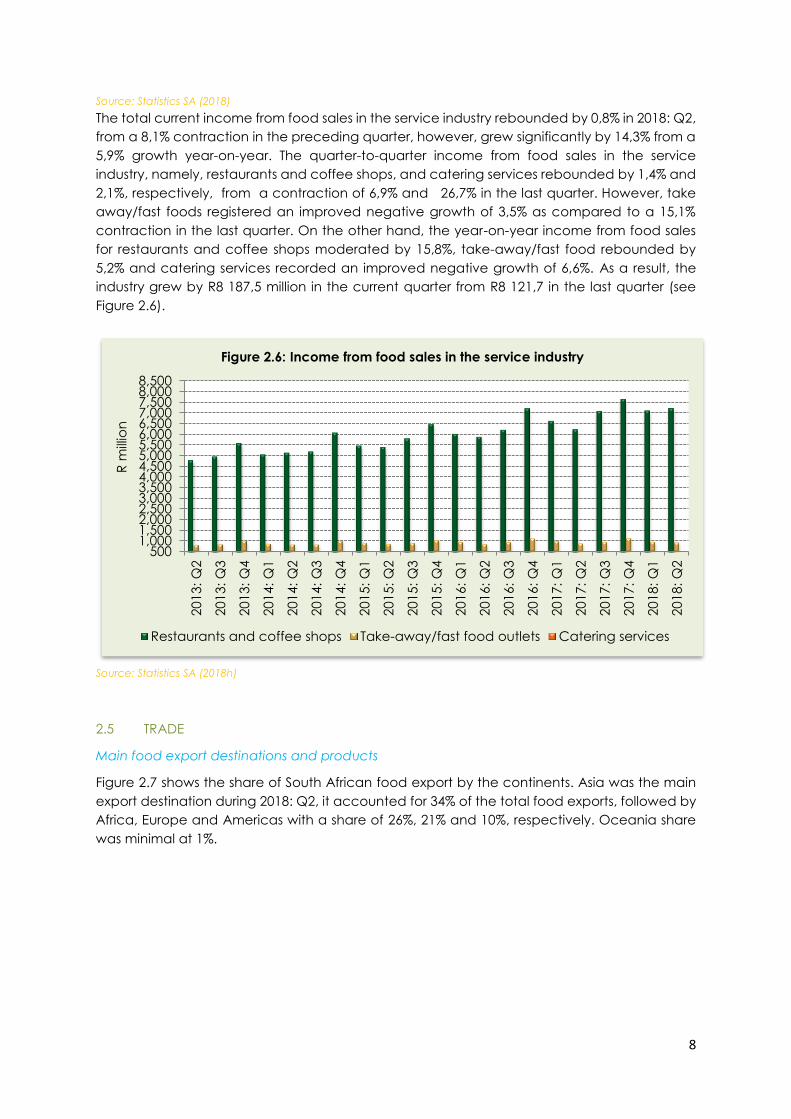

Source: Statistics SA (2018)

The total current income from food sales in the service industry rebounded by 0,8% in 2018: Q2,

from a 8,1% contraction in the preceding quarter, however, grew significantly by 14,3% from a

5,9% growth year-on-year. The quarter-to-quarter income from food sales in the service

industry, namely, restaurants and coffee shops, and catering services rebounded by 1,4% and

2,1%, respectively, from a contraction of 6,9% and 26,7% in the last quarter. However, take

away/fast foods registered an improved negative growth of 3,5% as compared to a 15,1%

contraction in the last quarter. On the other hand, the year-on-year income from food sales

for restaurants and coffee shops moderated by 15,8%, take-away/fast food rebounded by

5,2% and catering services recorded an improved negative growth of 6,6%. As a result, the

industry grew by R8 187,5 million in the current quarter from R8 121,7 in the last quarter (see

Figure 2.6).

Source: Statistics SA (2018h)

2.5 TRADE

Main food export destinations and products

Figure 2.7 shows the share of South African food export by the continents. Asia was the main

export destination during 2018: Q2, it accounted for 34% of the total food exports, followed by

Africa, Europe and Americas with a share of 26%, 21% and 10%, respectively. Oceania share

was minimal at 1%.

5001,0001,5002,0002,5003,0003,5004,0004,5005,0005,5006,0006,5007,0007,5008,0008,500

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

20

14

: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

R m

illio

n

Figure 2.6: Income from food sales in the service industry

Restaurants and coffee shops Take-away/fast food outlets Catering services

9

Source: Quantec EasyData (2018)

Source: Quantec EasyData (2018)

Figure 2.9 shows the South African food export destinations’ share of the main regions9 in 2018:

Q2. Among the main regions, Eastern Asia accounted for a largest share of around 21%,

9 The main regions which are included in the analysis are the top eight regions: SADC, Western Africa, EU; NAFTA (North Atlantic

Free Trade Area consists of USA, Canada and Mexico); Eastern Asia (includes China, Japan, North Korea, South Korea); Western Asia (mostly middle east countries); South Central Asia (include India, Pakistan and Bangladesh) and Australia and New Zealand.

Africa

26%

Americas

10%

Asia

34%

Europe

21%

Oceania

1%

Others

8%

Figure 2.7: The Food export destinations'share of continents in 2018: Q2

0

5

10

15

20

25

30

35

40

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

20

16

: Q

4

201

7: Q

1

20

17

: Q

2

201

7: Q

3

20

17

: Q

4

201

8: Q

1

201

8: Q

2

% s

ha

re

Figure 2.8: The food export destination's share of the continents

(2013:Q2-2018:Q2)

Africa Americas Asia Europe

10

followed by the European Union (20%), then SADC (excluding SACU) and SACU (Excluding

RSA) with 11% share each. NAFTA, South central Asia, Western Asia and Southern Eastern Asia

accounted for a share of 8%, 7%, 4% and 3%, respectively, in 2018:Q2.

Source: Quantec EasyData (2018)

Source: Quantec EasyData (2018)

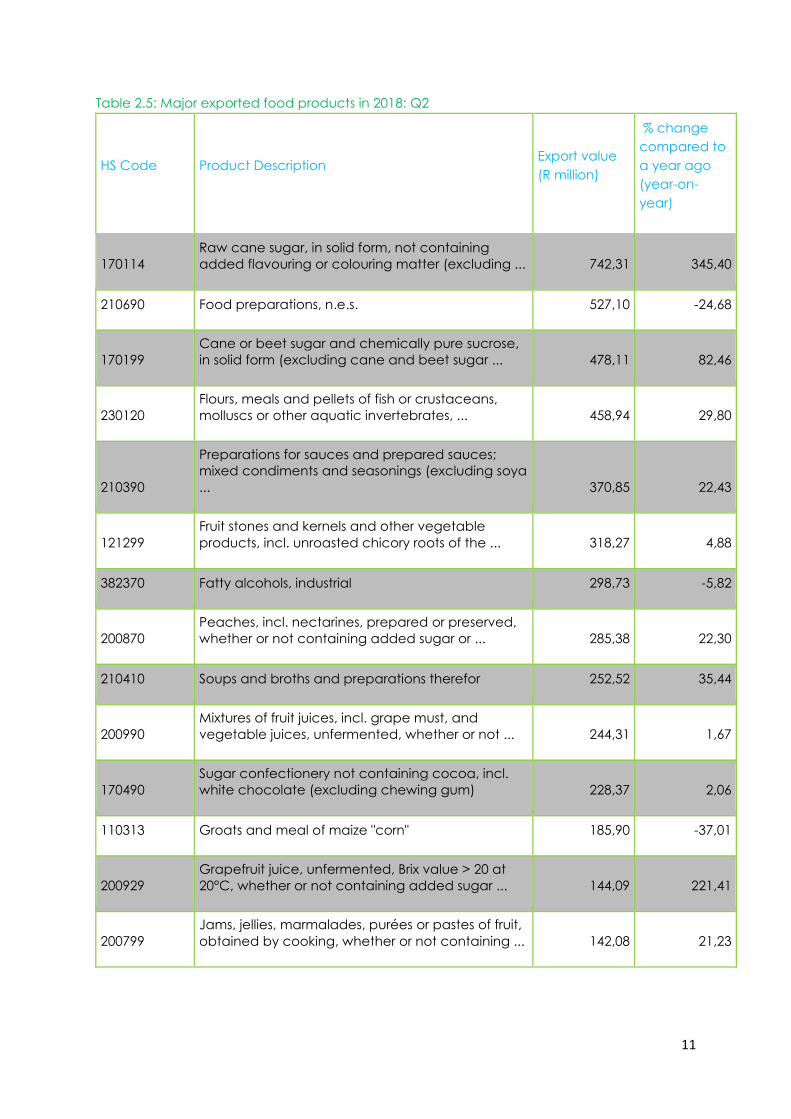

Figure 2.10 shows the share of top the food export destination by countries in 2018: Q2. The

leading countries as South African food export destinations in 2018: Q2 were: China (8,9%), The

United States (6,7%), India (5,0%), Japan (4,5%), Uganda (3,6%), Mozambique (3,5%), the

Netherlands (3,2%), Belgium (2,9%), Zambia (2,6%) and Zimbabwe (2,6%). Table 2.5 presents

the major exported food products during 2018: Q2. It shows the current quarter performance

values and their percentage change as compared to a year ago (year-on-year).

SADC (excluding

SACU)

11%

SACU (Excluding

RSA)

11%

NAFTA

8%

South-central

Asia

7%South-eastern

Asia

3%European Union

20%

Eastern Asia

21%

Western Asia

4%

Others

15%

Figure 2.9: The Food export destinations'share of main regions in 2018:

Q2

0

1

2

3

4

5

6

7

8

9

10

Ch

ina

Un

ite

d S

tate

s

Ind

ia

Ja

pa

n

Ug

an

da

Mo

zam

biq

ue

Ne

the

rla

nd

s

Be

lgiu

m

Za

mb

ia

Zim

ba

bw

e

% s

ha

re

Figure 2.10: The share of top ten food export destination countries in

2018: Q2

11

Table 2.5: Major exported food products in 2018: Q2

HS Code Product Description Export value

(R million)

% change

compared to

a year ago

(year-on-

year)

170114

Raw cane sugar, in solid form, not containing

added flavouring or colouring matter (excluding ... 742,31 345,40

210690 Food preparations, n.e.s. 527,10 -24,68

170199

Cane or beet sugar and chemically pure sucrose,

in solid form (excluding cane and beet sugar ... 478,11 82,46

230120

Flours, meals and pellets of fish or crustaceans,

molluscs or other aquatic invertebrates, ... 458,94 29,80

210390

Preparations for sauces and prepared sauces;

mixed condiments and seasonings (excluding soya

... 370,85 22,43

121299

Fruit stones and kernels and other vegetable

products, incl. unroasted chicory roots of the ... 318,27 4,88

382370 Fatty alcohols, industrial 298,73 -5,82

200870

Peaches, incl. nectarines, prepared or preserved,

whether or not containing added sugar or ... 285,38 22,30

210410 Soups and broths and preparations therefor 252,52 35,44

200990

Mixtures of fruit juices, incl. grape must, and

vegetable juices, unfermented, whether or not ... 244,31 1,67

170490

Sugar confectionery not containing cocoa, incl.

white chocolate (excluding chewing gum) 228,37 2,06

110313 Groats and meal of maize "corn" 185,90 -37,01

200929

Grapefruit juice, unfermented, Brix value > 20 at

20°C, whether or not containing added sugar ... 144,09 221,41

200799

Jams, jellies, marmalades, purées or pastes of fruit,

obtained by cooking, whether or not containing ... 142,08 21,23

12

040210

Milk and cream in solid forms, of a fat content by

weight of <= 1,5% 138,41 30,02

190531 Sweet biscuits 138,01 1,79

200989

Juice of fruit or vegetables, unfermented, whether

or not containing added sugar or other

sweetening ... 137,14 21,69

190190

Malt extract; food preparations of flour, groats,

meal, starch or malt extract, not containing ... 127,94 35,66

020130 Fresh or chilled bovine meat, boneless 127,35 -21,74

190590

Bread, pastry, cakes, biscuits and other bakers'

wares, whether or not containing cocoa;

communion ... 124,17 26,86

020120 Fresh or chilled bovine cuts, with bone in

(excluding carcasses and 1/2 carcasses) 121,13 29,10

Source: Trade map (2018)

Main source of food imports and imported food products

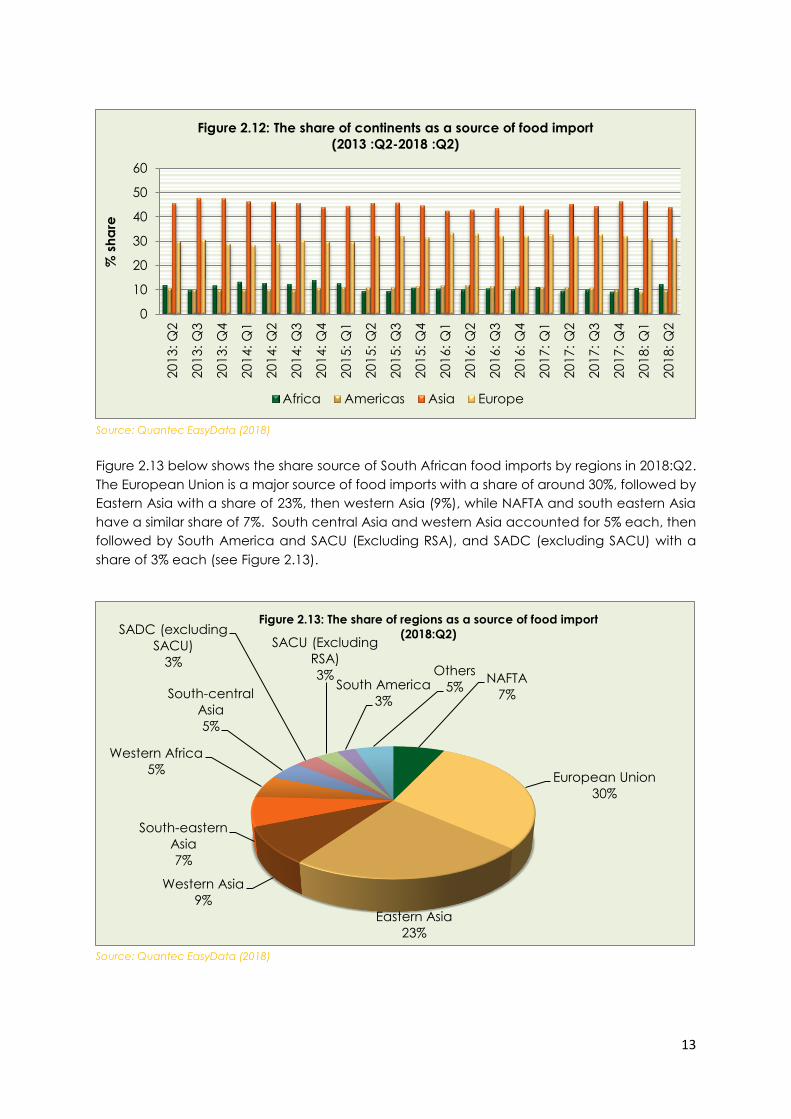

South Africa’s main source of food imports during 2018: Q2 is presented in Figure 2.11. Asia

accounted for a large share of food imports of approximately 44%, followed by Europe with

31%, then Africa and Americas with 12% and 10%, respectively. Oceania accounted for a

share of around 1%.

Source: Quantec EasyData (2018)

Africa

12%

Americas

10%

Asia

44%

Europe

31%

Oceania

2%Others

1%

Figure 2.11: The share of continents as a source of food import

(2018:Q2)

13

Source: Quantec EasyData (2018)

Figure 2.13 below shows the share source of South African food imports by regions in 2018:Q2.

The European Union is a major source of food imports with a share of around 30%, followed by

Eastern Asia with a share of 23%, then western Asia (9%), while NAFTA and south eastern Asia

have a similar share of 7%. South central Asia and western Asia accounted for 5% each, then

followed by South America and SACU (Excluding RSA), and SADC (excluding SACU) with a

share of 3% each (see Figure 2.13).

Source: Quantec EasyData (2018)

0

10

20

30

40

50

60201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

% s

ha

re

Figure 2.12: The share of continents as a source of food import

(2013 :Q2-2018 :Q2)

Africa Americas Asia Europe

NAFTA

7%

European Union

30%

Eastern Asia

23%

Western Asia

9%

South-eastern

Asia

7%

Western Africa

5%

South-central

Asia

5%

SADC (excluding

SACU)

3%

SACU (Excluding

RSA)

3%South America

3%

Others

5%

Figure 2.13: The share of regions as a source of food import

(2018:Q2)

14

Source: Quantec EasyData (2018)

Among the top ten countries that accounted for a large share of food imports in the 2018:Q2

were: China (17,7%), Germany (10,1%), the United States (6,0%), Saudi Arabia (5,2%), Nigeria

(4,4%), India (4,3%), United Kingdom (3,7%), Thailand (3,2%), Japan(3,2%) and Italy (2,8%).

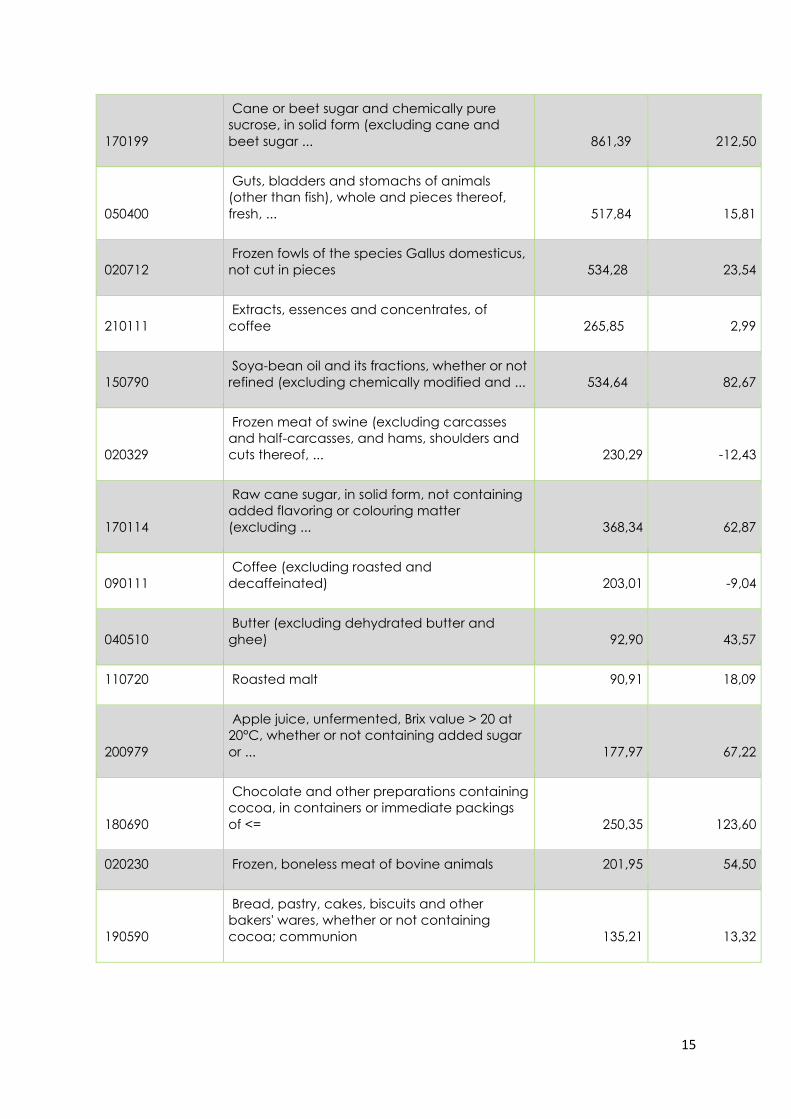

Table 2.6: Major imported food products in 2018: Q2

Table 2.6 presents the major imported food products during 2018: Q2, their current quarter

performance values and the year-on-year percentage changes.

HS Code Product description Import value

(R million)

% change

compared to a

year ago (year-

on-year)

020714

Frozen cuts and edible offal of fowls of the

species Gallus domesticus 961,80 -11,69

230400

Oilcake and other solid residues, whether or

not ground or in the form of pellets, resulting ... 543,01 -7,62

210690 Food preparations, n.e.s. 573,66 11,71

170113

Raw cane sugar, in solid form, not containing

added flavouring or colouring matter,

obtained ... 450,53 -46,77

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Ch

ina

Ge

rma

ny

Un

ite

d S

tate

s

Sa

ud

i A

rab

ia

Nig

eria

Ind

ia

Un

ite

d K

ing

do

m

Tha

ilan

d

Ja

pa

n

Ita

ly

% s

ha

re

Figure 2.14: The share of top ten countries as a source of food import in

2018: Q2

15

170199

Cane or beet sugar and chemically pure

sucrose, in solid form (excluding cane and

beet sugar ... 861,39 212,50

050400

Guts, bladders and stomachs of animals

(other than fish), whole and pieces thereof,

fresh, ... 517,84 15,81

020712

Frozen fowls of the species Gallus domesticus,

not cut in pieces 534,28 23,54

210111

Extracts, essences and concentrates, of

coffee 265,85 2,99

150790

Soya-bean oil and its fractions, whether or not

refined (excluding chemically modified and ... 534,64 82,67

020329

Frozen meat of swine (excluding carcasses

and half-carcasses, and hams, shoulders and

cuts thereof, ... 230,29 -12,43

170114

Raw cane sugar, in solid form, not containing

added flavoring or colouring matter

(excluding ... 368,34 62,87

090111

Coffee (excluding roasted and

decaffeinated) 203,01 -9,04

040510

Butter (excluding dehydrated butter and

ghee) 92,90 43,57

110720 Roasted malt 90,91 18,09

200979

Apple juice, unfermented, Brix value > 20 at

20°C, whether or not containing added sugar

or ... 177,97 67,22

180690

Chocolate and other preparations containing

cocoa, in containers or immediate packings

of <= 250,35 123,60

020230 Frozen, boneless meat of bovine animals 201,95 54,50

190590

Bread, pastry, cakes, biscuits and other

bakers' wares, whether or not containing

cocoa; communion 135,21 13,32

16

170490

Sugar confectionery not containing cocoa,

incl. white chocolate (excluding chewing

gum) 132,93 18,64

020629

Frozen edible bovine offal (excluding tongues

and livers) 77,34 -0,87

350510

Dextrins and other modified starches, e.g.

pregelatinised or esterified starches 122,15 13,56

Source: Trade map (2018)

Source: Quantec EasyData (2018)

Figure 2.15 shows the quarterly trade balance of food products. The quarter-to-quarter exports

of food rebounded by 10,1% from a 17,0% contraction in the last quarter, however, registered

an improved negative growth of 1,1% year-on-year. Imports on the other hand, stagnated at

5,9% quarter-to-quarter, while they contracted by 1,0% year-on-year from a 11,0% growth in

the last quarter. As a result, the trade balance rebounded from R435,5 million deficit in the last

quarter to a R729,6 million surplus in the current quarter.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

20

16

: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

20

17

: Q

4

201

8: Q

1

201

8: Q

2

R m

illio

n

Figure 2.15: Quarterly trade balance of food products

Export Import

17

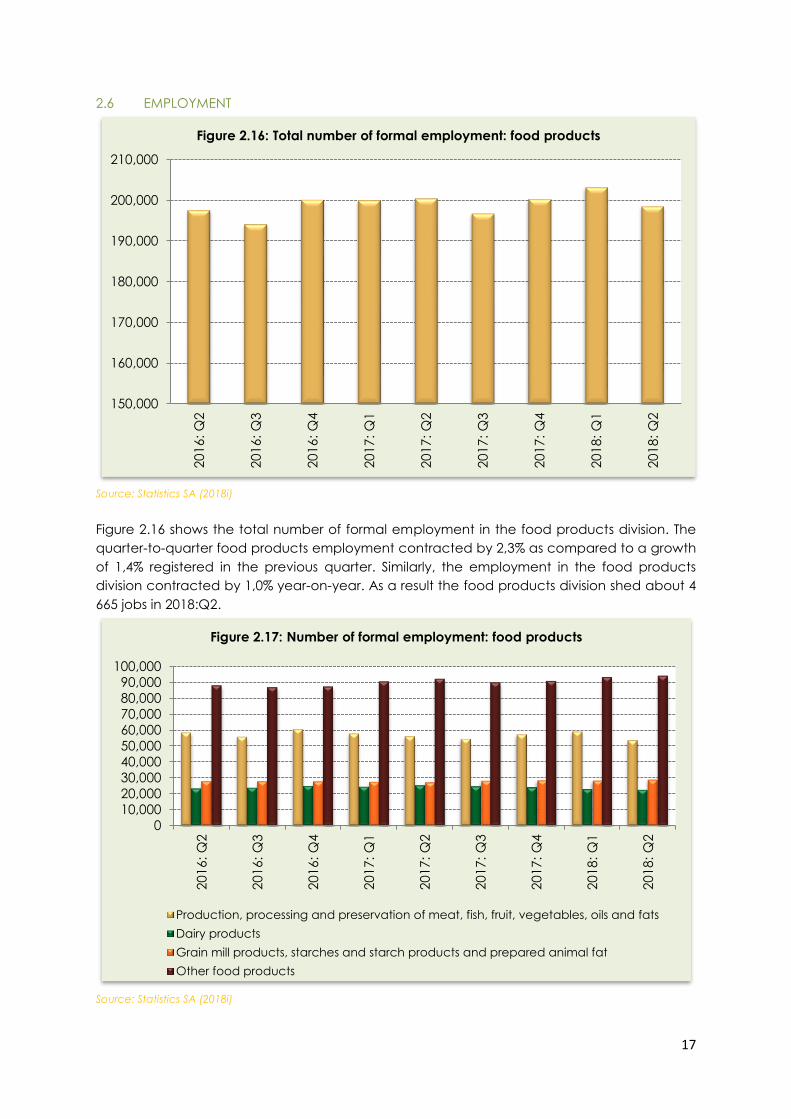

2.6 EMPLOYMENT

Source: Statistics SA (2018i)

Figure 2.16 shows the total number of formal employment in the food products division. The

quarter-to-quarter food products employment contracted by 2,3% as compared to a growth

of 1,4% registered in the previous quarter. Similarly, the employment in the food products

division contracted by 1,0% year-on-year. As a result the food products division shed about 4

665 jobs in 2018:Q2.

Source: Statistics SA (2018i)

150,000

160,000

170,000

180,000

190,000

200,000

210,000

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

Figure 2.16: Total number of formal employment: food products

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

201

6: Q

2

20

16

: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2Figure 2.17: Number of formal employment: food products

Production, processing and preservation of meat, fish, fruit, vegetables, oils and fats

Dairy products

Grain mill products, starches and starch products and prepared animal fat

Other food products

18

Figure 2.17 shows the number of formal employment in the food products division items. The

quarter-to-quarter formal employment of meat, fish, fruit contracted by 9,4%, dairy products

registered an improved negative growth of 1,7%, grain mill products rebounded by 1,8%,

‘’other food’’ products moderated by 0,8%. In terms of the year-on-year employment

performance, meat fish fruit contracted by 4,5%, dairy decelerated by 11,2%, grain mill

products grew modestly by 6,1% and ‘’other food products’’ moderated by 2,0%.

2.7 OUTLOOK

Table 2.7: Net balance10 of BER manufacturing survey: food products

2017: Q4 2017: Q1 2018: Q2 2018: Q3*

Domestic sales volumes 9 9 -14 32

Export sales volumes 20 12 -30 15

Production volumes 30 19 -15 32

Domestic order volumes received 42 16 -17 32

Export order volumes received 37 12 -33 12

General business conditions 0 3 -36 23

Number of factory workers -24 -29 0 3

Fixed investment 43 -24 70 67

Business confidence11 53 49 33

Expected volume of goods imported in

12 months’ time -6 19 -35

Expected volume of goods exported in

12 months’ time 29 54 18

10 BER calculates the net balance statistics by subtracting the percentage of the respondents replying “down” from

the percentage replying “up” to a particular question. Respondents are asked to compare the current quarter’s

experience to that of a year ago. A positive net balance implies an improvement (i.e. positive year-on-year growth)

and vice versa. Therefore, the net balance varies from -100 to 100 where -100 is the most negative response; zero is a

situation of no change and 100 is the most positive response.

11 BER calculates the business confidence index by asking respondents to rate current business conditions as “satisfactory” or

“unsatisfactory”. Then the index is derived as a gross percentage of the respondents replying “satisfactory.” A value of 50 is

indicative of neutrality, 100 indicative of extreme confidence and 0 of extreme lack of confidence. An index greater than 50 shows

the majority of respondents are satisfied with the prevailing economic conditions.

19

2017: Q4 2017: Q1 2018: Q2 2018: Q3*

Expected real investment in machinery

and equipment in 12 months’ time -37 40 -17

Expected business conditions in 12

months’ time -14 54 18

*Expected Source: BER (2018)

A survey of food manufacturing by the Bureau for Economic Research (BER) is presented in

Table 2.7. The survey shows that the year-on-year outlook for 2018: Q3 is positive for all the

variables.

3. BEVERAGES

Beverages according to SIC classification is code 305 and comprises of the following beverage

products:

Distilling, rectifying and blending of spirits; ethyl alcohol production from fermented

materials;

Manufacture of wine

Manufacture of beer and other malt liquors and malt

Breweries, except sorghum beer breweries

Sorghum beer breweries

Manufacture of malt

Manufacture of soft drinks; production of mineral waters.

3.1 PRICE

Table 3.1 below shows the consumer price indices, producer price indices and export unit

value of beverages. The year-on-year and quarter-to-quarter consumer price inflation for

alcoholic beverages grew by 4,3% and 1,4% respectively. The beverages products that grew

during the period under review were: beer, spirits, wine, cold beverages and hot beverages

by 8,7%, 7,6%, 7,5%, 6,5% and 4,9%, respectively.

Table 3.1: Price indices of beverages

Indices % change between

Beverages products

Weight 2017:

Q2

2018:

Q1 2018: Q2

2017: Q2

and 2018:

Q2

2018: Q1

and 2017:

Q2

Consumer price indices

All items (CPI

Headline)

100 102,6 105,5 107,0 4,3 1,4

Alcoholic beverages 3,9 101,4 106,4 109,7 8,2 3,0

Spirits 0,8 101,5 105,1 109,1 7,6 3,8

20

Wine 0,7 104,4 108,5 112,3 7,5 3,5

Beer 2,5 100,0 106,0 108,7 8,7 2,5

Non-alcoholic

beverages

1,2 103,1 105,4 109,2 5,9 3,5

Hot beverages 0,3 104,9 107,7 110,1 4,9 2,2

Cold beverages 0,9 102,1 104,2 108,7 6,5 4,3

Source: Stats SA (2018a, 2018b, 2018

Producer price index and export unit value

Producer price index

Weight 2017:

Q2

2018:

Q1 2018: Q2

2017: Q2

and 2018:

Q2

2018: Q1

and 2017:

Q2

Beverages 8,5 100,6 105,6 108,2 7,6 2,5

Export Unit value

Beverages 135,2 91,9 88,5 88,9 -3,3 0,5

Source: Quantec, 2018

The producer price index for beverages was 7,6% year-on-year and 2,5% quarter-to-quarter.

The exports unit value for beverages was negative at 3,3% year-on-year, however, grew by

0,5% quarter-to-quarter

3.2 PRODUCTION

Source: Statistics SA (2018d)

50

60

70

80

90

100

110

201

2: Q

4

201

3: Q

1

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

20

15

: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

Ind

ex (

2015=

100)

Figure 3.1: Seasonally adjusted physical volume of production:

beverages

21

Figure 3.1 presents the seasonally adjusted physical volume of production for beverages.

During 2018: Q2, the quarter-to-quarter seasonally adjusted physical volume of production for

beverages moderated by 0,8% from a 1,2% growth recorded in the last quarter, however

contracted by 1,4% year-on-year.

Production capacity

Table 3.2: Utilisation and reasons for underutilisation of production capacity by large

enterprises: Beverages division (percentage)

Period Utilisation Reasons for underutilisation

Total

under-

utilisation

Shortage of Insufficient

demand

Other

Raw

materials

Labour

Skilled Semi and

unskilled

2017: Q2 84,5 15,5 3,6 0,9 0,3 8,2 2,6

2017: Q1 83,4 16,6 4,4 0,9 0,3 8,5 2,5

2018: Q2 83,8 16,2 3,7 0,9 0,3 8,3 3,0

Source: Statistics SA (2018e)

Table 3.2 shows that the year-on-year utilisation capacity by large enterprises for beverages

division moderated year-on-year, however, grew marginally quarter-to-quarter. Insufficient

demand, remains the main reason for underutilisation, followed by shortage of raw materials.

3.3 VALUE OF SALES

Source: Statistics SA (2018d)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

201

3: Q

2

201

3: Q

3

201

3: Q

4

20

14

: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

R m

illio

n

Figure 3.2: Seasonally adjusted value of sales (current prices): beverages

22

During 2018: Q2. The quarter-to-quarter seasonally adjusted value of sales for beverages grew

marginally by 2,0% in 2018: Q2, from 0,7% growth in the last quarter. However, the year-on-year

seasonally adjusted value of sales for beverages moderated by 4,5% from 4,6% growth in the

preceding quarter (see Figure 3.2).

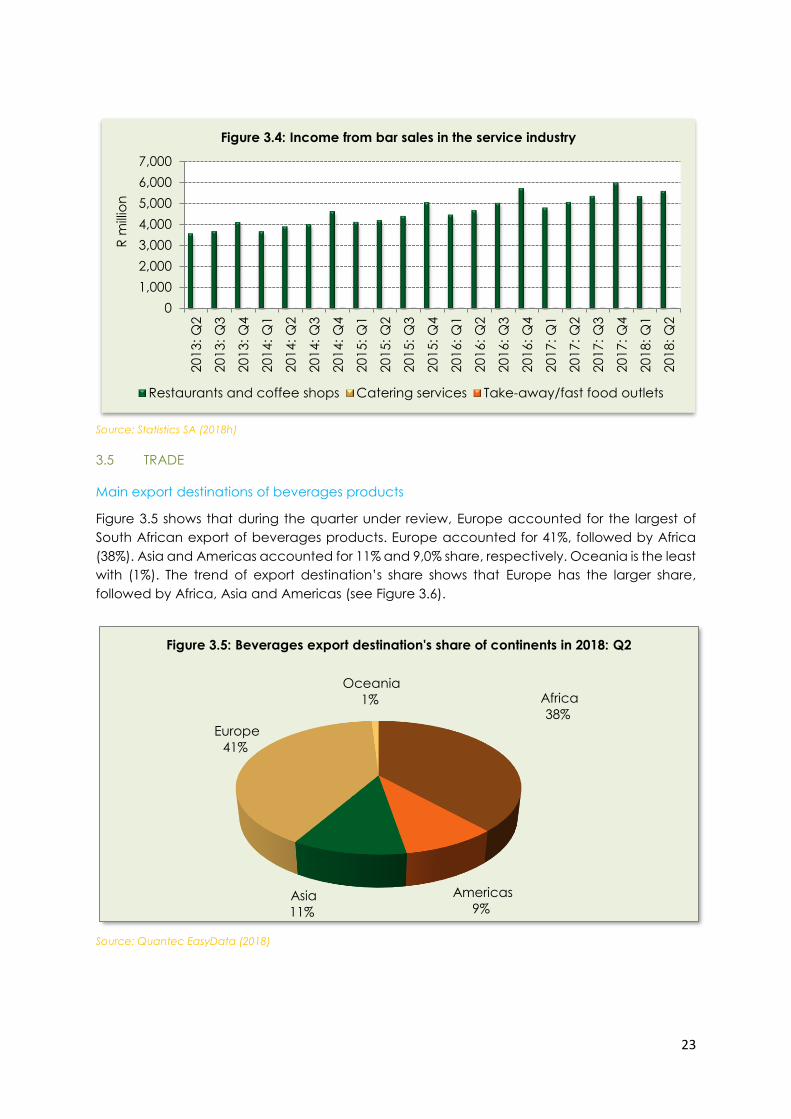

3.4 INCOME FROM BAR SALES IN THE SERVICE INDUSTRY12

Figure 3.3 below shows the total income for bar sales in the food and beverages service

industry in 2018: Q2. The income from bar sales in the food and beverages service industry

rebounded by 4,7% as compared to a 10,8% contraction in the previous quarter. However, it

moderated by 10,4% year-on-year. The total income stood at R1,8 billion under the period from

R1,7 billion in the previous quarter.

Source: Statistics SA (2018h)

Figure 3.4 below shows the performance of the bar sales in the service industry, which include

restaurant and coffee shops, take-away/fast food outlets and catering services. During 2018:

Q2, restaurant and coffee shops moderated by 4,7% from 10,8% growth in the last quarter,

However, take-away/fast food remained unchanged as compared to last quarter

performance of a negative 7,9% growth. Catering services remained unchanged also for two

last consecutive quarters. On the other hand, the year-on-year income for restaurants and

coffee shops and Take away/fast food outlets moderated by 10,4% and 14,7% from a 11,5%

and 27,9% growth respectively in the last quarter. However catering services stagnated at

3,8%.

12 Income from bar sales refers to income from liquor sales.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

20

16

: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

R m

illio

n

Figure 3.3: Total income from bar sales in the service industry

23

Source: Statistics SA (2018h)

3.5 TRADE

Main export destinations of beverages products

Figure 3.5 shows that during the quarter under review, Europe accounted for the largest of

South African export of beverages products. Europe accounted for 41%, followed by Africa

(38%). Asia and Americas accounted for 11% and 9,0% share, respectively. Oceania is the least

with (1%). The trend of export destination’s share shows that Europe has the larger share,

followed by Africa, Asia and Americas (see Figure 3.6).

Source: Quantec EasyData (2018)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

20

17

: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

R m

illio

n

Figure 3.4: Income from bar sales in the service industry

Restaurants and coffee shops Catering services Take-away/fast food outlets

Africa

38%

Americas

9%Asia

11%

Europe

41%

Oceania

1%

Figure 3.5: Beverages export destination's share of continents in 2018: Q2

24

Source: Quantec EasyData (2018)

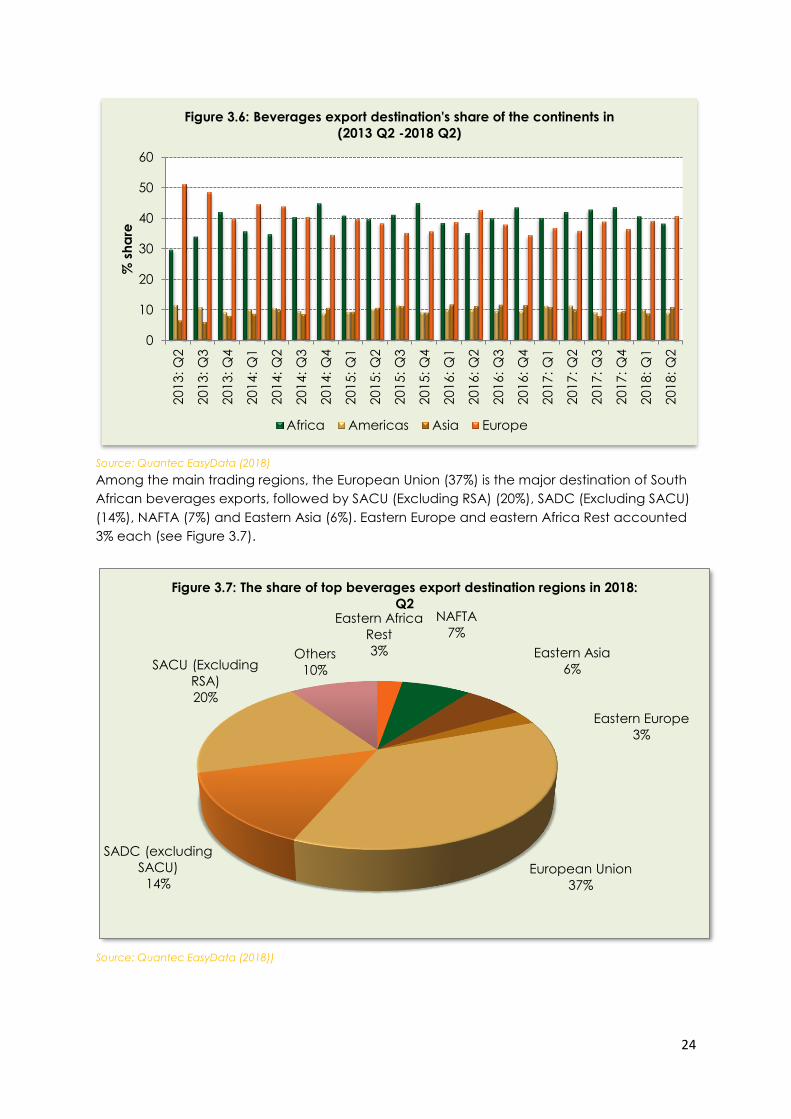

Among the main trading regions, the European Union (37%) is the major destination of South

African beverages exports, followed by SACU (Excluding RSA) (20%), SADC (Excluding SACU)

(14%), NAFTA (7%) and Eastern Asia (6%). Eastern Europe and eastern Africa Rest accounted

3% each (see Figure 3.7).

Source: Quantec EasyData (2018))

0

10

20

30

40

50

60

201

3: Q

2

201

3: Q

3

201

3: Q

4

20

14

: Q

1

201

4: Q

2

201

4: Q

3

201

4: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

% s

ha

reFigure 3.6: Beverages export destination's share of the continents in

(2013 Q2 -2018 Q2)

Africa Americas Asia Europe

Eastern Africa

Rest

3%

NAFTA

7%

Eastern Asia

6%

Eastern Europe

3%

European Union

37%

SADC (excluding

SACU)

14%

SACU (Excluding

RSA)

20%

Others

10%

Figure 3.7: The share of top beverages export destination regions in 2018:

Q2

25

Source: Quantec EasyData (2018)

Figure 3.8 above shows the share of top ten beverages export destinations during 2018: Q2.

The following are the main countries that accounted for a significant share of beverages

exported by South Africa during the quarter under review: Namibia (8,8%), Germany (7,9%),

the United States of America (4,5%), the Netherlands (4,5%), Zambia (4,1%), France (3,8%),

Mozambique (3,6%), China (3,1%), Denmark (2,9%) and Canada (2,8%). Table 3.3 below

presents the major exported beverages during the current quarter of review and the year-on-

year performance.

Table 3.3: Major exported beverages products in 2018: Q2 and year-on-year percentage

change

0

1

2

3

4

5

6

7

8

9

10

Na

mib

ia

Ge

rma

ny

Un

ite

d S

tate

s

Ne

the

rla

nd

s

Za

mb

ia

Fra

nc

e

Mo

zam

biq

ue

Ch

ina

De

nm

ark

Ca

na

da

% s

ha

re

Figure 3.8: The share of top ten beverages export destination countries in

2018: Q2

Hs code Product description Export

value

(R million)

% change

compared to

a year ago

(year-on-year)

220421

Wine of fresh grapes, incl. fortified wines,

and grape must whose fermentation has

been arrested 1678,1 6,2

220429

Wine of fresh grapes, incl. fortified wines,

and grape must whose fermentation has

been arrested 587,2 21,8

220710

Undenatured ethyl alcohol, of actual

alcoholic strength of >= 80% 340,9 -64,1

26

220210

Waters, incl. mineral and aerated, with

added sugar, sweetener or flavour, for

direct consumption 320,8 22,7

220422

Wine of fresh grapes, incl. fortified wines,

and grape must whose fermentation has

been arrested 226,4 13,1

220300 Beer made from malt 219,9 5,1

220600

Cider, perry, mead and other fermented

beverages and mixtures of fermented

beverages and non-alcoholic 213,4 2,4

220870 Liqueurs and cordials 184,0 -18,6

220299

Non-alcoholic beverages (excl. water, fruit

or vegetable juices, milk and beer) 126,3 -13,6

220820

Spirits obtained by distilling grape wine or

grape marc 121,6 -3,6

220410 Sparkling wine of fresh grapes 103,3 43,1

220830 Whiskies 76,3 -26,2

220720

Denatured ethyl alcohol and other spirits of

any strength 69,6 -34,5

220860 Vodka 64,5 -34,7

220850 Gin and Geneva 43,3 19,6

220890

Ethyl alcohol of an alcoholic strength of <

80% vol, not denatured; spirits and other

spirituous 36,3 -7,5

220110

Mineral waters and aerated waters, not

containing added sugar, other sweetening

matter or flavoured 15,4 6,6

220840

Rum and other spirits obtained by distilling

fermented sugar-cane products 15,3 -21,2

220900

Vinegar, fermented vinegar and substitutes

for vinegar obtained from acetic acid 12,9 20,9

27

Source: trade map 2018

Main imported beverage products and the source

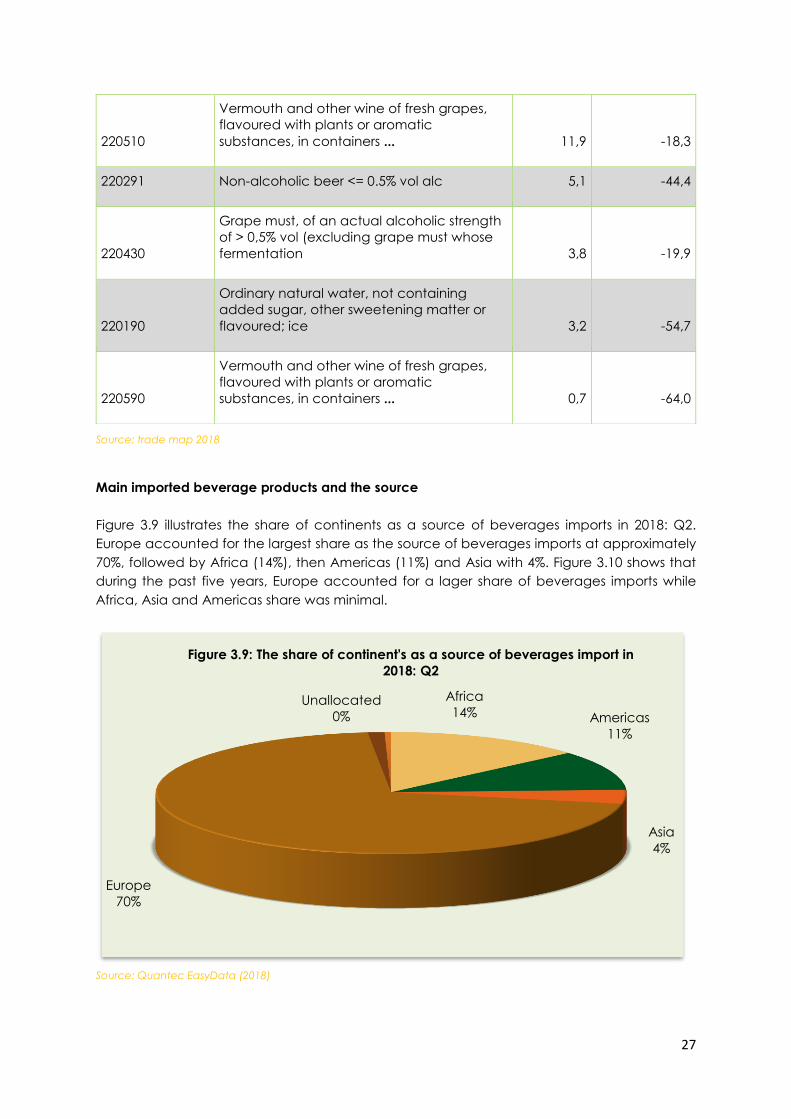

Figure 3.9 illustrates the share of continents as a source of beverages imports in 2018: Q2.

Europe accounted for the largest share as the source of beverages imports at approximately

70%, followed by Africa (14%), then Americas (11%) and Asia with 4%. Figure 3.10 shows that

during the past five years, Europe accounted for a lager share of beverages imports while

Africa, Asia and Americas share was minimal.

Source: Quantec EasyData (2018)

Africa

14% Americas

11%

Asia

4%

Europe

70%

Unallocated

0%

Figure 3.9: The share of continent's as a source of beverages import in

2018: Q2

220510

Vermouth and other wine of fresh grapes,

flavoured with plants or aromatic

substances, in containers ... 11,9 -18,3

220291 Non-alcoholic beer <= 0.5% vol alc 5,1 -44,4

220430

Grape must, of an actual alcoholic strength

of > 0,5% vol (excluding grape must whose

fermentation 3,8 -19,9

220190

Ordinary natural water, not containing

added sugar, other sweetening matter or

flavoured; ice 3,2 -54,7

220590

Vermouth and other wine of fresh grapes,

flavoured with plants or aromatic

substances, in containers ... 0,7 -64,0

28

Source: Quantec EasyData (2018)

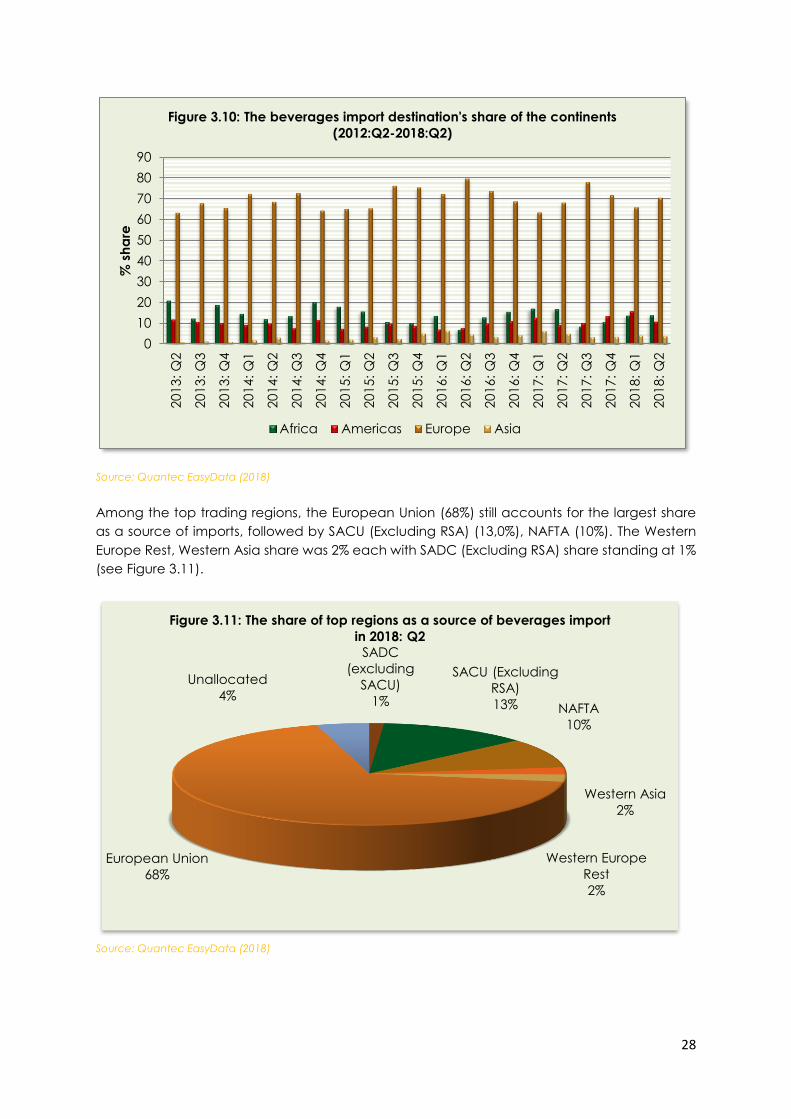

Among the top trading regions, the European Union (68%) still accounts for the largest share

as a source of imports, followed by SACU (Excluding RSA) (13,0%), NAFTA (10%). The Western

Europe Rest, Western Asia share was 2% each with SADC (Excluding RSA) share standing at 1%

(see Figure 3.11).

Source: Quantec EasyData (2018)

0

10

20

30

40

50

60

70

80

90

201

3: Q

2

201

3: Q

3

201

3: Q

4

201

4: Q

1

201

4: Q

2

201

4: Q

3

20

14

: Q

4

201

5: Q

1

201

5: Q

2

201

5: Q

3

201

5: Q

4

201

6: Q

1

201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

20

18

: Q

1

201

8: Q

2

% s

ha

re

Figure 3.10: The beverages import destination's share of the continents

(2012:Q2-2018:Q2)

Africa Americas Europe Asia

SADC

(excluding

SACU)

1%

SACU (Excluding

RSA)

13% NAFTA

10%

Western Asia

2%

Western Europe

Rest

2%

European Union

68%

Unallocated

4%

Figure 3.11: The share of top regions as a source of beverages import

in 2018: Q2

29

Source: Quantec EasyData (2018)

Figure 3.12 above shows the share of the top ten countries as a source of beverages imports.

During 2018: Q2, the United Kingdom accounted for 23,1% share of beverages imports,

followed by France (17,6%), Namibia (12,1%), Netherlands (7,2%), Belgium (5,5%), the United

States (4,6%), Mexico (4,4%), Spain (3,6%), Germany (3,3%) and Austria (3,2%). Table 3.5

presents major imported beverages products during the current quarter of review, and the

year-on-year performance.

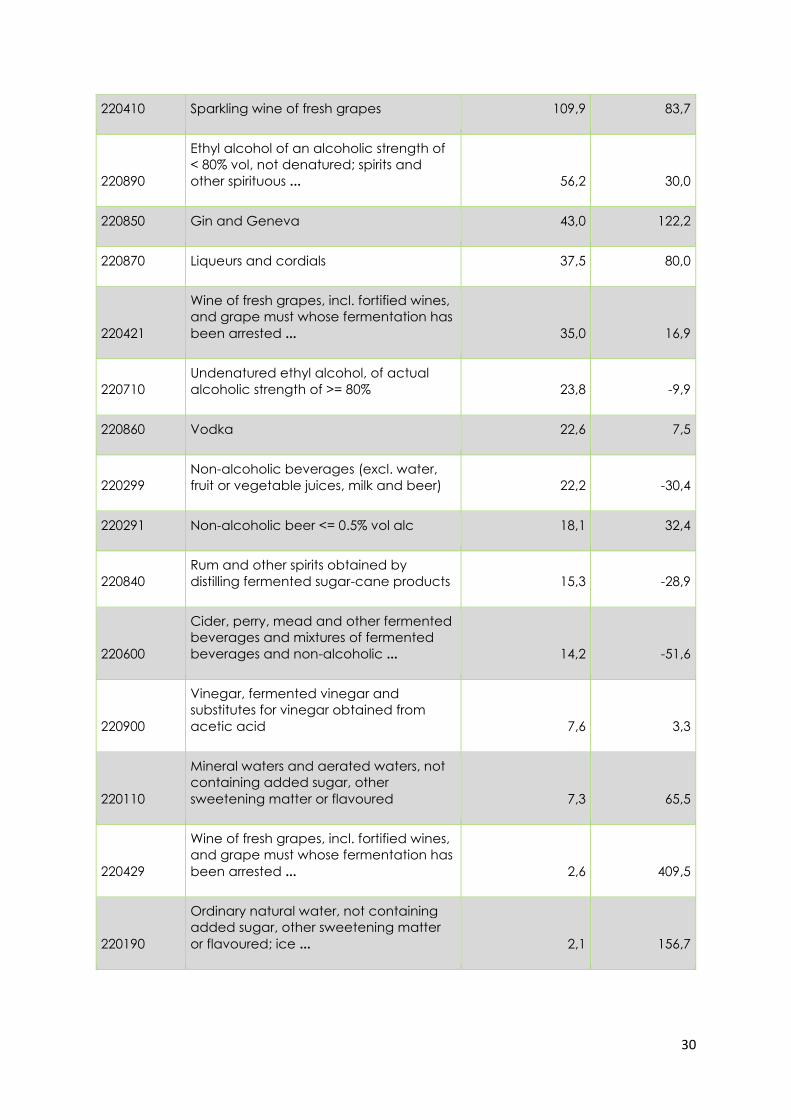

Table 3.5: Imported beverages in 2018: Q2 and year-on-year percentage change

HS CODE Product description Import value

(R million)

% change

compared to

a year ago

(year-on-year)

220300 Beer made from malt 512,5 112,0

220830 Whiskies 479,7 2,2

220820

Spirits obtained by distilling grape wine or

grape marc 219,2 183,0

220210

Waters, incl. mineral and aerated, with

added sugar, sweetener or flavour, for

direct consumption ... 198,4 13,3

0

5

10

15

20

25

30

35

40

Un

ite

d K

ing

do

m

Fra

nc

e

Na

mib

ia

Ne

the

rla

nd

s

Be

lgiu

m

Un

ite

d S

tate

s

Me

xic

o

Sp

ain

Ge

rma

ny

Au

stria

% s

ah

re

Figure 3.12: The share of top ten countries as a source of beverages

import in 2018: Q2

30

220410 Sparkling wine of fresh grapes 109,9 83,7

220890

Ethyl alcohol of an alcoholic strength of

< 80% vol, not denatured; spirits and

other spirituous ... 56,2 30,0

220850 Gin and Geneva 43,0 122,2

220870 Liqueurs and cordials 37,5 80,0

220421

Wine of fresh grapes, incl. fortified wines,

and grape must whose fermentation has

been arrested ... 35,0 16,9

220710

Undenatured ethyl alcohol, of actual

alcoholic strength of >= 80% 23,8 -9,9

220860 Vodka 22,6 7,5

220299

Non-alcoholic beverages (excl. water,

fruit or vegetable juices, milk and beer) 22,2 -30,4

220291 Non-alcoholic beer <= 0.5% vol alc 18,1 32,4

220840

Rum and other spirits obtained by

distilling fermented sugar-cane products 15,3 -28,9

220600

Cider, perry, mead and other fermented

beverages and mixtures of fermented

beverages and non-alcoholic ... 14,2 -51,6

220900

Vinegar, fermented vinegar and

substitutes for vinegar obtained from

acetic acid 7,6 3,3

220110

Mineral waters and aerated waters, not

containing added sugar, other

sweetening matter or flavoured 7,3 65,5

220429

Wine of fresh grapes, incl. fortified wines,

and grape must whose fermentation has

been arrested ... 2,6 409,5

220190

Ordinary natural water, not containing

added sugar, other sweetening matter

or flavoured; ice ... 2,1 156,7

31

220422

Wine of fresh grapes, incl. fortified wines,

and grape must whose fermentation has

been arrested ... 0,7 989,4

220510

Vermouth and other wine of fresh

grapes, flavoured with plants or aromatic

substances, in containers ... 0,3 -74,2

220720

Denatured ethyl alcohol and other spirits

of any strength 0,1 120,0

Source: Source: trade map 2018

Source: Quantec EasyData (2018)

During 2018: Q2: the quarter-to-quarter exports of beverages rebounded by 15,9%, following

a 24,5% contraction recorded in the last quarter. However, the year-on-year exports

moderated by 4,5% from a 7,2% growth in the preceding quarter. Imports on the other hand,

rebounded by 17,4% from 0,6% contraction quarter-to-quarter, but grew by 46,8% year-on-

year. As a result, the trade surplus widened from R2 032.4 million in the previous quarter to R2

327.8 million in the current quarter.

0

1,000

2,000

3,000

4,000

5,000

6,000

20

13

: Q

2

20

13:

Q3

20

13

: Q

4

20

14:

Q1

20

14:

Q2

20

14:

Q3

20

14:

Q4

20

15:

Q1

20

15:

Q2

20

15:

Q3

20

15:

Q4

20

16:

Q1

20

16:

Q2

20

16:

Q3

20

16:

Q4

20

17:

Q1

20

17:

Q2

20

17:

Q3

20

17:

Q4

20

18:

Q1

20

18:

Q2

R m

illio

n

Figure 3.13: Quarterly trade balance of beverages

Export Import

32

3.6 EMPLOYMENT

Source: Quantec EasyData (2018i)

Figure 3.14 shows the number of formal employment in the beverages and tobacco products

industry. The quarter-to-quarter formal employment in the beverages and tobacco division

contracted by 8,1% from a 6,1% growth in the last quarter. However, it decelerated by 6,7%

year-on-year from 6,0% contraction in the preceding quarter. As a result, 3 362 jobs were shed.

3.7 OUTLOOK

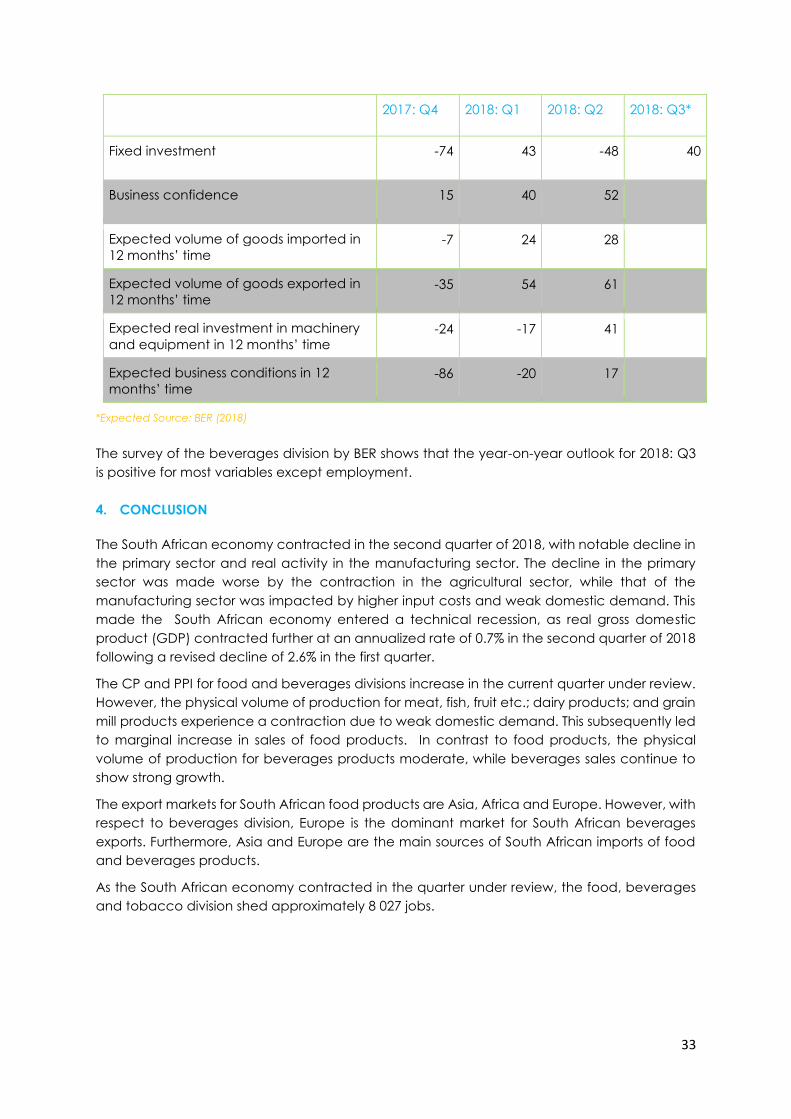

Table 3.6: Net balance of BER manufacturing survey: Beverages

2017: Q4 2018: Q1 2018: Q2 2018: Q3*

Domestic sales volumes -44 30 76 96

Export sales volumes -67 9 54 61

Production volumes 2 30 71 81

Domestic order volumes received 7 43 88 87

Export order volumes received -67 16 52 61

General business conditions -75 6 65 56

Number of factory workers -27 14 -37 -37

34,000

35,000

36,000

37,000

38,000

39,000

40,000

41,000

42,000

43,000

44,000

45,000201

6: Q

2

201

6: Q

3

201

6: Q

4

201

7: Q

1

201

7: Q

2

201

7: Q

3

201

7: Q

4

201

8: Q

1

201

8: Q

2

Figure 3.14: Number of formal employment: beverage and tobacco

products

33

2017: Q4 2018: Q1 2018: Q2 2018: Q3*

Fixed investment -74 43 -48 40

Business confidence 15 40 52

Expected volume of goods imported in

12 months’ time -7 24 28

Expected volume of goods exported in

12 months’ time -35 54 61

Expected real investment in machinery

and equipment in 12 months’ time -24 -17 41

Expected business conditions in 12

months’ time -86 -20 17

*Expected Source: BER (2018)

The survey of the beverages division by BER shows that the year-on-year outlook for 2018: Q3

is positive for most variables except employment.

4. CONCLUSION

The South African economy contracted in the second quarter of 2018, with notable decline in

the primary sector and real activity in the manufacturing sector. The decline in the primary

sector was made worse by the contraction in the agricultural sector, while that of the

manufacturing sector was impacted by higher input costs and weak domestic demand. This

made the South African economy entered a technical recession, as real gross domestic

product (GDP) contracted further at an annualized rate of 0.7% in the second quarter of 2018

following a revised decline of 2.6% in the first quarter.

The CP and PPI for food and beverages divisions increase in the current quarter under review.

However, the physical volume of production for meat, fish, fruit etc.; dairy products; and grain

mill products experience a contraction due to weak domestic demand. This subsequently led

to marginal increase in sales of food products. In contrast to food products, the physical

volume of production for beverages products moderate, while beverages sales continue to

show strong growth.

The export markets for South African food products are Asia, Africa and Europe. However, with

respect to beverages division, Europe is the dominant market for South African beverages

exports. Furthermore, Asia and Europe are the main sources of South African imports of food

and beverages products.

As the South African economy contracted in the quarter under review, the food, beverages

and tobacco division shed approximately 8 027 jobs.

34

5. REFERENCES

BER (2018), Manufacturing Survey. Bureau for Economic Research, University of Stellenbosch.

Quantec EasyData (2018), RSA International Trade. Accessed in December 2018.

SA Reserve Bank (2018), Quarterly Bulletin, September 2018, South African Reserve Bank.

Statistics SA (2018a), Consumer Price Index, various issues. Statistics South Africa.

Statistics SA (2018b), Producer Price Index, various issues. Statistics South Africa.

Statistics SA (2018c), Export and Import Unit Value Indices, various issues. Statistics South Africa.

Statistics SA (2018d), Manufacturing: Production and Sales, various issues. Statistics South

Africa.

Statistics SA (2018e), Manufacturing: Utilisation of Production Capacity by Large Enterprises.

Statistics South Africa.

Statistics SA (2018f), Wholesale Trade Sales, various issues, Statistics South Africa.

Statistics SA (2018g), Retail Trade Sales, various issues, Statistics South Africa.

Statistics SA (2018h), Food and Beverages, various issues, Statistics South Africa.

Statistics SA (2018i), Quarterly Employment Statistics, various issues. Statistics South Africa.

35

NOTES:

----------------------------------------------------------------------------------------------------------------------------- ----------

------------------------------------------------------------------------------------------------------------------- --------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

----------------------------------------------------------------------------------------------------- ----------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

-------------------------------------------------------------------------------------------------------------------------------- -------

---------------------------------------------------------------------------------------------------------------------------- -----------

----------------------------------------------------------------------------------------------------------------------------- ----------

-------------------------------------------------------------------------------------------------------------- -------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

------------------------------------------------------------------------------------------------ ---------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

----------------------------------------------------------------------------------------------------------------------------- ----------

----------------------------------------------------------------------------------------------------------------------- ----------------

----------------------------------------------------------------------------------------------------------------------------- ----------

--------------------------------------------------------------------------------------------------------- ------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

36

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------

---------------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------- ----------