qatar‘s ict landscape 2014 - ningapi.ning.com/.../qatarsictlandscapereport2014househ… · ·...

TRANSCRIPT

QATAR‘SICTLANDSCAPE2014Households and Individuals

Qatar’s ICT Landscape 2014 Households and Individuals 1

FO R E WO R D 2

E x E c u t i v E S u m m a Ry 4

B ac kg R O u n D 7

Qata R S E g m E n tat i O n m O D E l 9

ICT IN QATAR 13

i c t D E v i c E P E n E t R at i O n 14

i n t E R n E t cO n n E c t i v i t y 17

i c t u Sag E a n D S P E n D i n g 19

Sat i S Fac t i O n W i t h m O B i l E a n D i n t E R n E t S E Rv i c E S 23

FoCus AReAs 27

S O c i a l n E t WO R k i n g a n D a R a B cO n t E n t O n l i n E 28

O n - l i n E B a n k i n g a n D E - cO m m E R c E 31

E - g Ov E R n m E n t 34

Q - P O St S E Rv i c E S 36

O n l i n E S E c u R i t y a n D P R i vac y 37

n E W S E Rv i c E S 40

cO n c lu S i O n 42

APPeNDIX 45

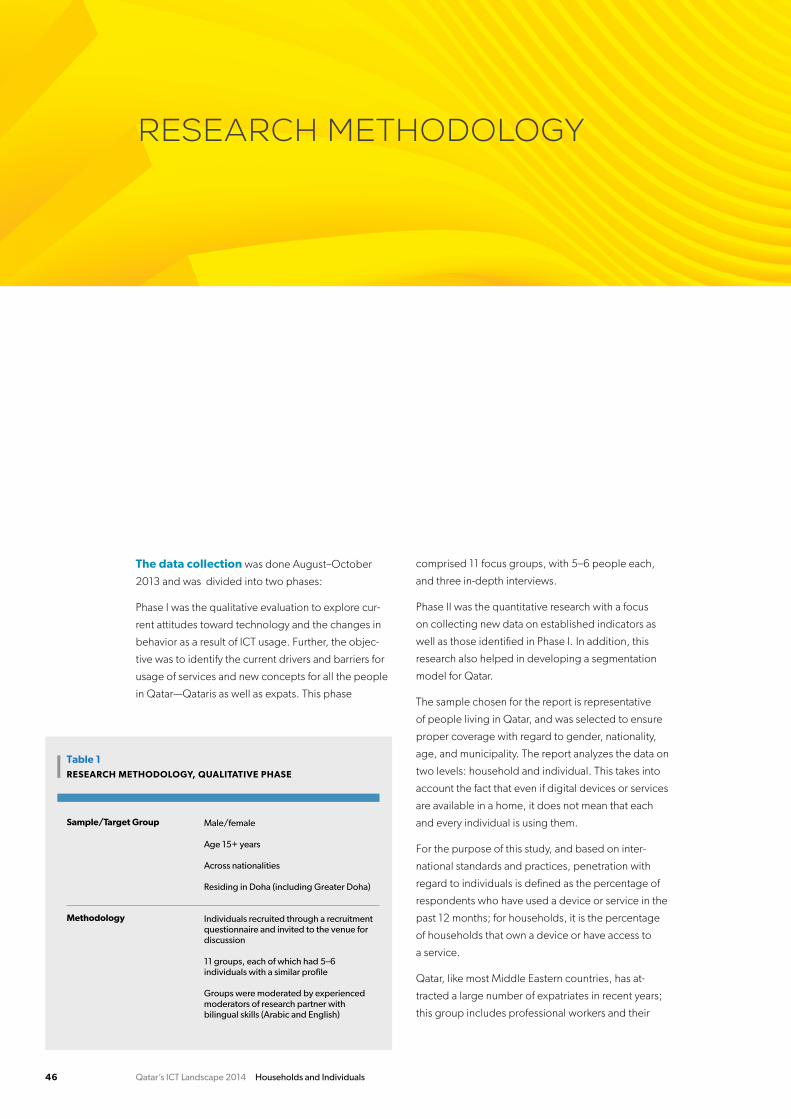

R E S E a R c h m E t h O D O lO gy 46

g lO SSa Ry 49

D E F i n i t i O n S 50

TABLE OF CONTENTS

Qatar’s ICT Landscape 2014 Households and Individuals2

over the past decade, Qatar has made great strides in building an advanced ict sector

that will benefit all sectors of society. the newly released World Economic Forum’s Global

Technology Report 2014 reaffirms the country’s place as one of the middle East’s—and the

world’s—most “networked ready” nations. the substantial investment in building a world-

class ict infrastructure with the capacity and speed to set the country apart in the region

and around the world is one of the main reasons for Qatar’s success.

as the pages of this report reveal, significant advances continue to be made by households

and individuals on most ict indicators since we started to survey Qatar’s ict landscape in

2008. Broad ict access has been achieved in Qatar, with all segments of the resident popu-

lation having access to internet-enabled ict devices. For the mainstream population, the

penetration of mobile phones and laptops has grown significantly, and ownership of mature

devices such as smartphones and tablets has also increased. the use of basic online services

such as email, internet browsing, and social networking is prevalent across all segments

of society, and people across the education spectrum access social networking, voiP, and

other basic internet services.

in spite of our achievements in such a short period of time, there are still areas where Qatar

can improve—in order to move to the next level of ict maturity. these improvements include

increasing the penetration of newer devices such as smartphones and tablets, particularly

in specific demographic segments like the transient labor population; expanding the use of

advanced online services such as e-commerce, e-banking, and e-government; and improv-

ing mobile broadband penetration to meet the rapidly growing need among consumers in

Qatar to be able to log on to the internet on-the-go “anytime, anywhere.” Qatar is in line

with the global trend of people demanding more mobility in their connectivity options.

FOREWORD

Qatar’s ICT Landscape 2014 Households and Individuals 3

to accomplish this, the ministry of information and communications technology will main-

tain its support of healthy telecom competition as it transitions to an independent telecom-

munications regulatory authority that will encourage and support an open and competitive

ict sector. We will continue to implement our national Broadband Plan to guarantee that

fixed and mobile infrastructures are deployed in the most effective and rapid manner. We

will expand the benefits of broadband not only by providing for and investing in extensive

and high-quality infrastructure but also by increasing the supply of broadband content and

services, which will, in turn, drive usage. We will bolster initiatives related to youth work-

force training and readiness. We will address digital literacy, affordability, quality of service,

awareness, and safety barriers, explicitly targeting 100 percent coverage with speeds of at

least 8 mbps in areas where transient workers live, reflecting Qatar’s ongoing commitment

to diversity and workers’ rights. We will build awareness of Qatar’s new telecommunications

consumer Protection Policy to ensure that consumers know their rights and responsibili-

ties in their dealings with service providers. and we are accelerating Qatar’s e-government

initiatives through a ministry-wide master plan designed to improve and add new e-govern-

ment services and make government more efficient and customer-centric.

this new research not only shows that our current programs and policies are working, it

also offers a blueprint for where we need to go—as well as insight into what we must do to

get there.

Dr. Hessa sultan Al-Jaber

Minister of Information and Communications Technology

Qatar’s ict landscape 2014 households and individuals4

atar’s ICT Landscape 2014: Households

and Individuals examines the ICT access and usage

behaviors and patterns of residents in Qatar. It is based

on an annual study that enables the Ministry of Infor-

mation and Communications Technology (ictQATAR)

to measure progress toward its overall ICT goals, as

well as to frame relevant new policies and programs

and report core ICT indicators to international organi-

zations.

Qatar has made significant advances in ICT develop-

ment over the past decade, and this report dem-

onstrates further progress. The levels of access and

usage of ICT in Qatar are high, with the country ranked

32nd and 26th (among 157 countries) in those cat-

egories, respectively, and an overall ranking of 31, on

the ICT Development Index in ITU’s 2013 Measuring

the Information Society report. Qatar has achieved

mobile subscription phone coverage above 100

percent, and Internet and broadband services are

growing as well. According to the 2013 households

and individuals survey results, 85 percent of the over-

all population in Qatar now has access to the Internet,

compared to 38 percent in 2008. The country is likely

to observe an additional uptick in broadband services

as aggressive plans to establish a robust infrastructure

and new initiatives continue to be implemented.

ExECuTivE SummARy

Specifically, the survey findings indicate that all

segments of Qatar’s resident population have ac-

cess to Internet-enabled ICT devices. While mature

devices including mobile phones are accessed by

nearly 100 percent of the population, newer devices

like smartphones and tablets have yet to penetrate

fully—particularly in segments such as the transient

labor population. In addition, the use of basic online

services such as email, Internet browsing, social

networking, and peer-to-peer file sharing is prevalent

across all segments of society; however, advanced

online services such as e-commerce, online bank-

ing, and transactional e-government services are

employed much more frequently among people with

higher levels of education, as well as among Qataris

and Westerners.

For the mainstream population, ownership of ICT

devices such as mobile phones and laptops has

grown significantly. In 2013, a household in Qatar had

approximately nine mobile phones, on average, com-

pared to nearly four in 2012. Laptop ownership also

increased from 2 to 3.2 laptops per household over

the same time period, while the growth in desktops

has been relatively flat due to the mounting demand

for mobility.

Qatar’s ict landscape 2014 households and individuals 5

Moving forward, the implementation of Qatar’s first

National Broadband Plan, released in 2013 with the

objective to promote broadband infrastructure de-

ployment and market development, should result in an

increase and improvement in broadband services. In

particular, the plan targets the speed and affordability

of both fixed and mobile broadband for consumers

and businesses as challenges to overcome.

In addition, to meet the increasing demand for

faster and more secure networks and with the aim of

boosting overall ICT access, ictQATAR continues to

work with telecommunication operators to build an

advanced FTTH (fiber-to-the-home) network that will

enable universal access to high-speed broadband.

In analyzing the ICT landscape survey results across

households and individuals in Qatar from current and

past years, three themes emerge, all cornerstones of

ICT development in the country.

mOving FROm accESS tO

aDvancED uSagE

The first is the ongoing transition from general ac-

cess to ICT devices and technologies to the use of

advanced online services. Usage of portable devices

such as laptops, tablet computers, and smartphones

among the overall population has increased. As men-

tioned above, mobile phones are now used by nearly

100 percent of the population, while smartphone

penetration stands at 65 percent; the penetration of

laptops also increased from 83 percent in 2012 to 93

percent in 2013. And the penetration of tablets tripled

over the same time period, from 10 percent in 2012 to

29 percent in 2013. Fifty-two percent of Qataris con-

nected to the Internet used a tablet computer in 2013,

compared to just 32 percent in 2012.

On the other hand, ICT usage is currently focused on

basic services, with nearly 100 percent of the overall

population using mobile phones for telephone calls

and SMS. Eighty-three percent of people use the

Internet for email services, and 93 percent of the

Internet users log on to various social networking plat-

forms. However, only 18 percent of the overall population

in Qatar uses Internet banking, with 15 percent

using the Internet for e-commerce. Thus, while the

households and individuals study shows that broad

ICT access has almost been achieved in Qatar, there is

still much room for improvement when it comes to the

sort of advanced usage that will drive future innova-

tion and economic success.

cOnnEctivity On-thE-gO,

anytimE, anyWhERE

The second persistent theme is connectivity on-the-

go. With the increased penetration of mobile phones

and laptops and greater acceptance of mobile

broadband as a medium to connect to the Internet,

the “need to be mobile” is on the rise in Qatar. Eighty-

five percent of the Internet users in Qatar use a laptop

and 71 percent a smartphone to get online. For laptop

use, the preferred mode of connection is wireless

LAN because of the convenience. With the increase

in smartphone penetration, the demand for mobile

broadband has also skyrocketed. According to the

survey, among households connected to the Internet

mobile broadband penetration now stands at 61

percent, compared with fixed broadband connectivity

at 94 percent. Qatar is in line with the global trend of

people demanding more mobility in their connectivity

options. The “on-the-go” usability of today’s devices

allows people to access online services anytime and

from any location, and consumers in Qatar increasing-

ly need and want the ability to log on to the Internet

“anytime, anywhere.”

intERnEt iS FOR EvERyOnE

A common perception is that the Internet is ac-

cessed solely by people with more education, with

less educated people forgoing the use of any online

services.1 However, the data from the households

and individuals survey negates this hypothesis, as the

results clearly show that people across the education

spectrum access social networking, VoIP, and other

basic Internet services. Social networking was, in fact,

used by almost 93 percent of respondents who are

active online.

[While] the households and individuals study shows that broad ICT access has almost been achieved in Qatar, there is still much room for improvement when it comes to the sort of advanced usage that will drive future innovation and economic success.

1 For this study’s analysis, people with secondary-level education or less are classified as “less educated,” while those with education beyond the second-ary level are classified as “more educated.”

Qatar’s ict landscape 2014 households and individuals6

Still, the data does show that as education levels

increase there is a shift toward using advanced online

services, with 22 percent of respondents whose edu-

cation is above the secondary level using e-commerce

in the past 12 months, compared with just 6.2 percent

of those with secondary education or less. In addition,

improvement in education level corresponds to a re-

duction in concerns about online security and threats.

Six aREaS OF in-DEPth StuDy

For the purposes of the households and individuals

survey, six areas of interest were identified for more

in-depth study: social networking, e-commerce, e-

government, online postal services offered by national

provider Q-Post, online privacy and security, and new

online services. The survey results captured the main

trends in each of these focus areas:

n 87% of Internet users access social networking at

least once a month in Qatar, an increase over prior

years.

n Penetration levels in advanced services such as

online banking and e-commerce are low, especially

among non-Westerners, with 44% of those who did

not use such services in the past year reporting that

they are concerned about the security of online por-

tals, 26% worried about having “no control,” and 31%

believing the process is too technical.

n In terms of e-government, the findings show that

55 percent of the overall population is aware of online

services, although only 16 percent used them in the

past year. Qualitative findings suggest that interaction

with the government could be handled more effective-

ly face-to-face rather than online.

n 88% of the population has not used Q-Post in the

past year, while nearly half of those who have not used

it were not aware and not interested in knowing about

Q-Post online services, as people are satisfied using

global private courier services such as DHL and Ara-

mex. Due to widespread negative perceptions about

Q-Post’s dependability, reliability, and convenience,

there is a general lack of awareness and willingness to

learn about Q-Post’s online services.

n 38% of Internet users are concerned about the lack

of privacy online, while 30% are concerned about

using services such as online banking.

n A growing interest in all mobile-based services

emerged from the survey. It’s clear that Qatari resi-

dents are willing to experiment with offerings such as

mobile wallet and mobile money transfer, providing

an opportunity for the development of additional

advanced online services.

challEngES

While it highlights many positive ICT-related devel-

opments, the households and individuals study also

identifies some key barriers to be addressed. For

instance, one of the major impediments to achieving a

true information-based society is the lack of advanced

ICT skills and knowledge among the population. The

digital literacy and IT skills programs that are currently

being implemented by the Ministry should go a long

way toward mitigating this problem.

Mirroring past studies, online security concerns

continue to be a major obstacle to widespread usage.

The continued education of consumers on the various

ways to safeguard themselves against cyber threats—

along with further institutional measures taken by

banks, corporations, the government, and others—

should over time ease such concerns.

Finally, most people in Qatar lack awareness about e-

government services. Better customer experience and

more value-added services, which are being planned

as part of the e-Government 2020 strategy, are likely

to help increase both awareness and usage.

Qatar’s ICT Landscape 2014 Households and Individuals 7

In the last decade, Qatar has been recognized as

a forerunner in ICT development in the region, and is

well on its way to becoming a global leader in this area

as well. Currently, the country leads the Arab world on

the World Economic Forum’s (WEF) 2014 Networked

Readiness Index, and ranks 31st overall out of the 157

countries on International Telecommunication Union’s

(ITU) 2013 ICT Development Index.

Qatar’s economic indicators reflect a strong founda-

tion for future economic growth. According to the

Qatar Statistics Authority (QSA), the real GDP of Qatar

has reached QAR 341 bn as of the end 2012. And the

WEF Global Competitiveness Report 2013 lists Qatar’s

GDP per capita at USD 99,731, one of the highest

in the world, and ranks the country 13th overall out

of 148 countries and first in the region on its Global

Competitiveness Index, reaffirming Qatar’s position as

the most competitive economy in the Middle East.

According to the ITU’s 2013 Measuring the Information

Society report, the country has the highest proportion

of households with a computer in the Middle East at

more than 90 percent, as well as the highest percent-

age of households with Internet access region-wide

at 88 per cent. Qatar’s best score is on the ICT use

sub-index (26th globally), putting it on par with world

ICT leaders.

In order to monitor Qatar’s continuing progress to-

ward becoming a vibrant knowledge-based economy,

in 2013 the Ministry of Information and Communica-

tions Technology (ictQATAR) commissioned Ericsson

ConsumerLab to conduct a large-scale study of ICT

penetration and usage among individuals and house-

holds in Qatar, following similar projects that have

taken place since 2008.

BACKGROuND

This resulting report, Qatar’s ICT Landscape Report

2014: Households and Individuals, focuses on the ICT

penetration, usage patterns, and behavior of residents

of Qatar. The research was divided into two phases:

Phase I was qualitative evaluation to explore current

attitudes toward technology and changes in behavior

as a result of ICT penetration and usage, with the goal

of identifying current drivers of and barriers to usage;

Phase II was quantitative research to augment the

findings of Phase I. A survey was conducted in this

phase, for which 2,207 people were interviewed. (For

further details on methodology, including definitions

of terms, see the Appendix [page 45]).

The population sample chosen for this report is rep-

resentative of the current population in Qatar (age 15

and older), including a mix of genders, nationalities,

ages, and geographic locations. Qatar, like most GCC

countries, has attracted a large number of expatriate

workers in recent years, including a large base of tran-

sient laborers. Further, for the purposes of this study,

the population of Qatar is divided into “mainstream”

and “overall”—with the mainstream population

excluding transient laborers.

In order to get as full a picture of technology usage

in Qatar as possible, the study results were analyzed

on both an individual and a household level, which

accounts for the fact that even if digital devices or

services are available in a home, it does not mean that

each and every individual is using them.

Due to the fact that Qatar’s population is cosmopoli-

tan, and includes people of different nationalities,

cultural beliefs, and attitudes, and varying economic

backgrounds, it is important to understand the needs

Qatar’s ICT Landscape 2014 Households and Individuals8

and expectations of each group individually. There-

fore, one of the main objectives of the households

and individuals study was to segment the population

by values and attitudes toward technology, as well as

current interaction with ICT. To that end, the resident

population of Qatar was divided into 10 segments:

1. young Qataris (15–34)

2. mid-Range adult/Older Qataris (35 and over)

3. Westerners

4. White-collar Expat arabs, technology

interested

5. White-collar Expat arabs, technology neutral

6. White-collar asians, technology interested

7. White-collar asians, technology neutral

8. non-Qataris, Blue collar (non-Shared

accommodation)

9. non-Qataris, Blue collar (Shared

accommodation)

10. transient laborers

The segmentation analysis is a critical tool that enables

ictQATAR to identify specific groups that continue to

lag behind when it comes to ICT access and usage.

It is also helpful when it comes to understanding the

needs of various segments with high exposure to ICT.

Qatar’s ICT Landscape 2014 Households and Individuals 9

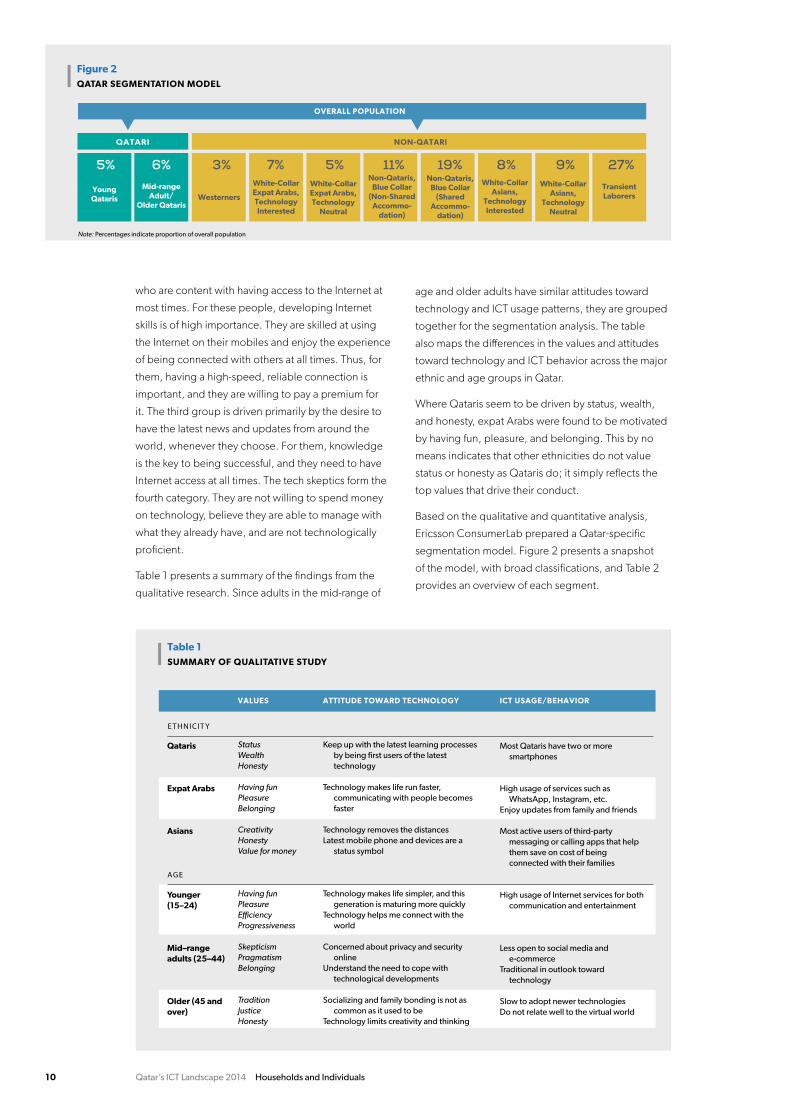

QATAR SEGmENTATiON mODEL

The population in Qatar, as of September 2013, is

estimated at approximately 2 million, of which close to

80 percent are men. This is due to the large migrating

workforce, which mainly comprises males. The popula-

tion in Qatar also includes a significant number of expa-

triates, both Arabs and non-Arabs. And the population

is young: 25- to 34-year-olds make up more than a

third of the population. See Figure 1 for a breakdown of

the population by age and gender.

Qatar today is modernizing and making its mark on the

global map while conserving its traditional values at

the same time. The findings of the qualitative research

show a split between the younger and older segments

of the country’s population—younger Qataris are more

accepting of the changes, whereas the older genera-

tion often maintains a more skeptical outlook about

the pace of change. Qataris look to the government to

maintain a balance between the modern and the tra-

ditional ways of life. The age divide is even more pro-

nounced when one looks at the various personal values

and attitudes captured by the qualitative research. The

analysis was done using basic moral parameters, and

included technology-specific aspects, to draw a profile

of the population’s attitudes toward technology.

The research shows that when it comes to values

pertaining to social responsibility, people in Qatar rate

honesty to be the most important. They also want a

society that is humane and conducive to creative ideas.

Interpersonal ties are still very strong, and although

there is an increase in the importance of women in the

society, people prefer the traditional gender roles.

Value systems are reflected in attitudes toward

technology, and Qatar’s residents can be grouped

into four categories. The first group includes people

who prefer having the latest technology at their

disposal as a way of life, boosting their confidence

and self-image. The second group consists of people

Figure 1QATAR’S POPULATION SPLIT, BY AGE AND GENDER

10.2%

4.2%

32.5%

7.3%

Source: Qatar Statistics Authority

20.2%

5.2%

11.7%

2.6%

4.3%

0.9%

0.7%0.2%

15–24 years

25–34 years

35–44 years

MALE

45–54 years

55–64 years

Over 65 years

FEMALE

Qatar’s ICT Landscape 2014 Households and Individuals10

who are content with having access to the Internet at

most times. For these people, developing Internet

skills is of high importance. They are skilled at using

the Internet on their mobiles and enjoy the experience

of being connected with others at all times. Thus, for

them, having a high-speed, reliable connection is

important, and they are willing to pay a premium for

it. The third group is driven primarily by the desire to

have the latest news and updates from around the

world, whenever they choose. For them, knowledge

is the key to being successful, and they need to have

Internet access at all times. The tech skeptics form the

fourth category. They are not willing to spend money

on technology, believe they are able to manage with

what they already have, and are not technologically

proficient.

Table 1 presents a summary of the findings from the

qualitative research. Since adults in the mid-range of

age and older adults have similar attitudes toward

technology and ICT usage patterns, they are grouped

together for the segmentation analysis. The table

also maps the differences in the values and attitudes

toward technology and ICT behavior across the major

ethnic and age groups in Qatar.

Where Qataris seem to be driven by status, wealth,

and honesty, expat Arabs were found to be motivated

by having fun, pleasure, and belonging. This by no

means indicates that other ethnicities do not value

status or honesty as Qataris do; it simply reflects the

top values that drive their conduct.

Based on the qualitative and quantitative analysis,

Ericsson ConsumerLab prepared a Qatar-specific

segmentation model. Figure 2 presents a snapshot

of the model, with broad classifications, and Table 2

provides an overview of each segment.

Figure 2QATAR SEGMENTATION MODEL

OVERALL POPULATION

QATARI NON-QATARI

Note: Percentages indicate proportion of overall population

Westerners

5% 6% 3% 7% 5% 11% 19% 8% 9% 27%Transient Laborers

Non-Qataris,Blue Collar

(Non-Shared Accommo-

dation)

White-Collar Asians,

Technology Neutral

White-Collar Asians,

Technology Interested

White-Collar Expat Arabs, Technology

Neutral

White-Collar Expat Arabs, Technology Interested

Mid-range Adult/

Older Qataris

Young Qataris

Non-Qataris, Blue Collar

(Shared Accommo-

dation)

Table 1SUMMARY OF QUALITATIVE STUDY

Most Qataris have two or more smartphones

High usage of services such as WhatsApp, Instagram, etc.

Enjoy updates from family and friends

Most active users of third-party messaging or calling apps that help them save on cost of being connected with their families

High usage of Internet services for both communication and entertainment

Less open to social media and e-commerce

Traditional in outlook toward technology

Slow to adopt newer technologiesDo not relate well to the virtual world

VALUES ATTITUDE TOWARD TECHNOLOGY ICT USAGE/BEHAVIOR

Qataris

Expat Arabs

Asians

Younger (15–24)

Mid–range adults (25–44)

Older (45 and over)

StatusWealth Honesty

Having funPleasureBelonging

Creativity HonestyValue for money

Having funPleasureEfficiency Progressiveness

SkepticismPragmatismBelonging

TraditionJusticeHonesty

Keep up with the latest learning processes by being first users of the latest technology

Technology makes life run faster, communicating with people becomes faster

Technology removes the distancesLatest mobile phone and devices are a

status symbol

Technology makes life simpler, and this generation is maturing more quickly

Technology helps me connect with the world

Concerned about privacy and security online

Understand the need to cope with technological developments

Socializing and family bonding is not as common as it used to be

Technology limits creativity and thinking

ETHNICITY

AGE

Qatar’s ICT Landscape 2014 Households and Individuals 11

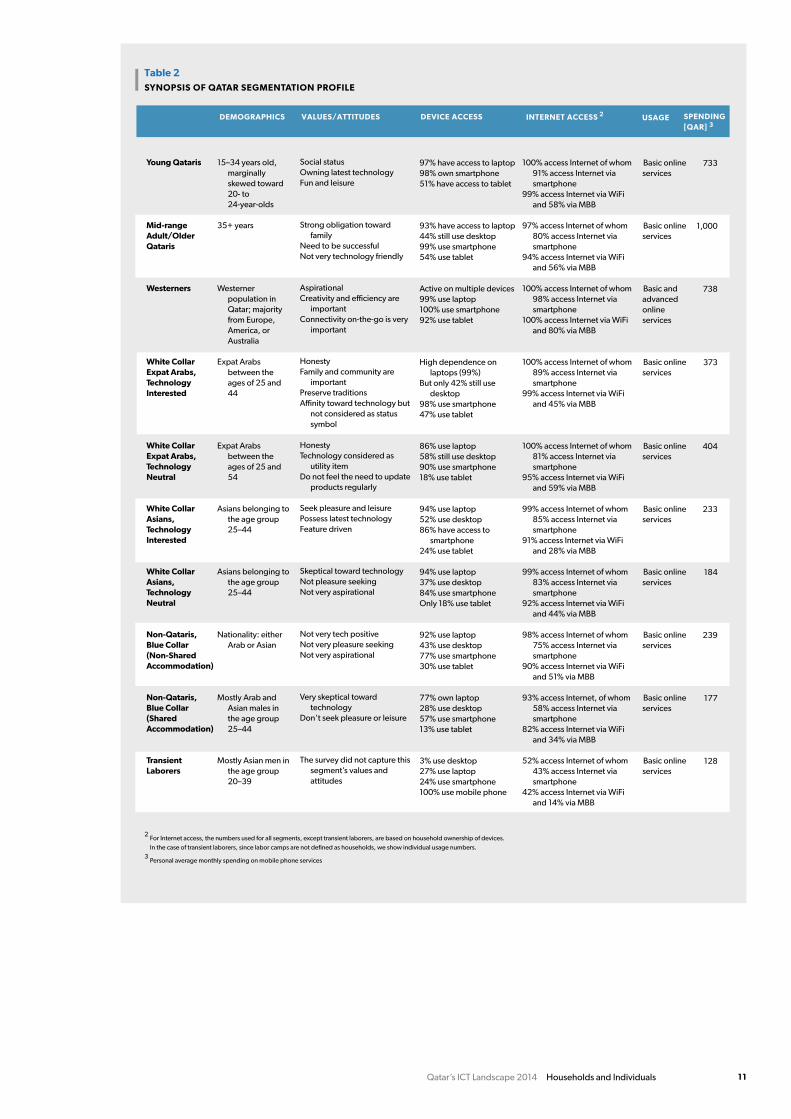

Table 2SYNOPSIS OF QATAR SEGMENTATION PROFILE

SPENDING[QAR]

USAGEINTERNET ACCESSDEVICE ACCESS 2

3VALUES/ATTITUDESDEMOGRAPHICS

Young Qataris

Mid-range Adult/Older Qataris

Westerners

White CollarExpat Arabs, Technology Interested

White CollarExpat Arabs, Technology Neutral

White Collar Asians, Technology Interested

White Collar Asians, Technology Neutral

Non-Qataris, Blue Collar (Non-Shared Accommodation)

Non-Qataris, Blue Collar (Shared Accommodation)

Transient Laborers

15–34 years old, marginally skewed toward 20- to 24-year-olds

35+ years

Westerner population in Qatar; majority from Europe, America, or Australia

Expat Arabs between the ages of 25 and 44

Expat Arabs between the ages of 25 and 54

Asians belonging to the age group 25–44

Asians belonging to the age group 25–44

Nationality: either Arab or Asian

Mostly Arab and Asian males in the age group 25–44

Mostly Asian men in the age group 20–39

Social statusOwning latest technologyFun and leisure

Strong obligation toward family

Need to be successfulNot very technology friendly

AspirationalCreativity and efficiency are

importantConnectivity on-the-go is very

important

HonestyFamily and community are

importantPreserve traditions Affinity toward technology but

not considered as status symbol

HonestyTechnology considered as

utility itemDo not feel the need to update

products regularly

Seek pleasure and leisurePossess latest technologyFeature driven

Skeptical toward technologyNot pleasure seekingNot very aspirational

Not very tech positiveNot very pleasure seekingNot very aspirational

Very skeptical toward technology

Don’t seek pleasure or leisure

The survey did not capture this segment’s values and attitudes

97% have access to laptop98% own smartphone51% have access to tablet

93% have access to laptop 44% still use desktop99% use smartphone54% use tablet

Active on multiple devices99% use laptop100% use smartphone92% use tablet

High dependence on laptops (99%)

But only 42% still use desktop

98% use smartphone47% use tablet

86% use laptop 58% still use desktop 90% use smartphone18% use tablet

94% use laptop52% use desktop86% have access to

smartphone24% use tablet

94% use laptop 37% use desktop 84% use smartphone Only 18% use tablet

92% use laptop 43% use desktop 77% use smartphone 30% use tablet

77% own laptop 28% use desktop 57% use smartphone 13% use tablet

3% use desktop27% use laptop 24% use smartphone 100% use mobile phone

100% access Internet of whom91% access Internet via smartphone

99% access Internet via WiFi and 58% via MBB

97% access Internet of whom80% access Internet via smartphone

94% access Internet via WiFi and 56% via MBB

100% access Internet of whom98% access Internet via smartphone

100% access Internet via WiFi and 80% via MBB

100% access Internet of whom 89% access Internet via smartphone

99% access Internet via WiFi and 45% via MBB

100% access Internet of whom81% access Internet via smartphone

95% access Internet via WiFi and 59% via MBB

99% access Internet of whom85% access Internet via smartphone

91% access Internet via WiFi and 28% via MBB

99% access Internet of whom83% access Internet via smartphone

92% access Internet via WiFi and 44% via MBB

98% access Internet of whom75% access Internet via smartphone

90% access Internet via WiFi and 51% via MBB

93% access Internet, of whom58% access Internet via smartphone

82% access Internet via WiFi and 34% via MBB

52% access Internet of whom43% access Internet via smartphone

42% access Internet via WiFi and 14% via MBB

Basic online services

Basic online services

Basic and advanced online services

Basic online services

Basic online services

Basic online services

Basic online services

Basic online services

Basic online services

Basic online services

733

1,000

738

373

404

233

184

239

177

128

For Internet access, the numbers used for all segments, except transient laborers, are based on household ownership of devices. In the case of transient laborers, since labor camps are not defined as households, we show individual usage numbers.

Personal average monthly spending on mobile phone services

2

3

Qatar’s ICT Landscape 2014 Households and Individuals 13

i c t D E v i c E P E n E t R at i O n

i n t E R n E t cO n n E c t i v i t y

i c t u Sag E a n D S P E n D i n g

Sat i S Fac t i O n W i t h m O B i l E a n D i n t E R n E t S E Rv i c E S

iCT iN QATAR

Qatar’s ICT Landscape 2014 Households and Individuals14

iCT DEviCE PENETRATiON

Key Findings

n almost 100% of the population, across a majority of the segments, has access to computers and mobile phones in Qatar, with high penetration of smart-phones across many segments

n 92% of households have a smartphone and 96% have a laptop

n Qatar enjoys higher penetration rates for laptops, smartphones, and tablets when compared with more ict mature economies such as Sweden, and Singapore; korea lags far behind in terms of laptops and tablets, and is equivalent to Qatar in terms of smartphone penetration

ICT access among the various segments

identified by Ericsson ConsumerLab is quite high.

Almost 100 percent of the population in the majority

of the segments has access to computers and mobile

phones, with the exception of blue-collar workers

living in shared accommodations and transient labor-

ers, who lag behind in computer and smartphone

penetration. Figure 3 also demonstrates a very high

penetration of smartphones across a majority of the

segments.

As seen in Figure 4, the survey mapped the pen-

etration of various ICT devices in a household. It is

interesting to note that penetration of smartphones

Figure 3INDIVIDUAL ICT PENETRATION, OVERALL AND BY SEGMENT

77.8

% 9

9.5

%

100

%

99

%

100

%

99

.1%

98

.1%

96

.8%

85

.9%

30

.4%

99

.9%

100

%

100

%

100

%

100

%

99

.3%

100

%

99

.7%

100

%

65

.1%

97.

5%

96

.1%

99

.7%

97.

7%

100

%

100

%

100

%

89

.8%

84

.9%

83

.1%

77%

56

.4%

23

.6%

MOBILE SMARTPHONECOMPUTER

1Overall 2 3 4 5 6 7 8 9 10

1. Young Qataris

2. Mid-range Adult/Older Qataris

3. Westerners

4. White-Collar Expat Arabs, Technology Interested

5. White-Collar Expat Arabs, Technology Neutral

6. White-Collar Asians, Technology Interested

7. White-Collar Asians, Technology Neutral

8. Non-Qataris, Blue Collar (Non-Shared Accommodation)

9. Non-Qataris, Blue Collar (Shared Accommodation)

10. Transient Laborers

Note: Mobile phone refers to any type of mobile device, including smartphoneSource: Households and Individuals Survey, 2013Overall population n=2,207

Qatar’s ICT Landscape 2014 Households and Individuals 15

“I would say that I have the world between my hands with my phone, because I am connected with my friends all the time. Without technology we all would be lost. ” —YOUNG QATARI, MALE

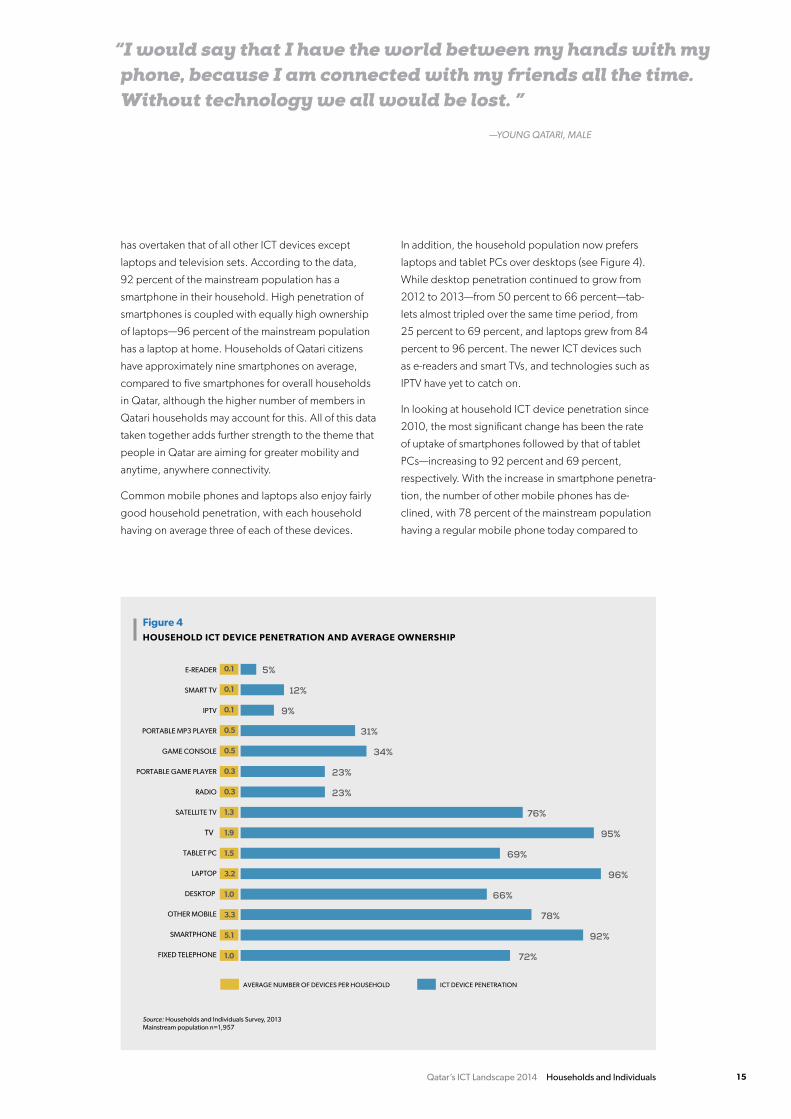

has overtaken that of all other ICT devices except

laptops and television sets. According to the data,

92 percent of the mainstream population has a

smartphone in their household. High penetration of

smartphones is coupled with equally high ownership

of laptops—96 percent of the mainstream population

has a laptop at home. Households of Qatari citizens

have approximately nine smartphones on average,

compared to five smartphones for overall households

in Qatar, although the higher number of members in

Qatari households may account for this. All of this data

taken together adds further strength to the theme that

people in Qatar are aiming for greater mobility and

anytime, anywhere connectivity.

Common mobile phones and laptops also enjoy fairly

good household penetration, with each household

having on average three of each of these devices.

In addition, the household population now prefers

laptops and tablet PCs over desktops (see Figure 4).

While desktop penetration continued to grow from

2012 to 2013—from 50 percent to 66 percent—tab-

lets almost tripled over the same time period, from

25 percent to 69 percent, and laptops grew from 84

percent to 96 percent. The newer ICT devices such

as e-readers and smart TVs, and technologies such as

IPTV have yet to catch on.

In looking at household ICT device penetration since

2010, the most significant change has been the rate

of uptake of smartphones followed by that of tablet

PCs—increasing to 92 percent and 69 percent,

respectively. With the increase in smartphone penetra-

tion, the number of other mobile phones has de-

clined, with 78 percent of the mainstream population

having a regular mobile phone today compared to

Figure 4HOUSEHOLD ICT DEVICE PENETRATION AND AVERAGE OWNERSHIP

E-READER

SMART TV

IPTV

PORTABLE MP3 PLAYER

GAME CONSOLE

PORTABLE GAME PLAYER

RADIO

SATELLITE TV

TV

TABLET PC

LAPTOP

DESKTOP

OTHER MOBILE

SMARTPHONE

FIXED TELEPHONE

0.1

0.1

0.1

0.5

0.5

0.3

0.3

1.3

1.9

1.5

3.2

1.0

3.3

5.1

1.0

AVERAGE NUMBER OF DEVICES PER HOUSEHOLD ICT DEVICE PENETRATION

72%

92%

78%

66%

96%

69%

95%

76%

23%

23%

34%

31%

9%

12%

5%

Source: Households and Individuals Survey, 2013 Mainstream population n=1,957

Qatar’s ICT Landscape 2014 Households and Individuals16

81 percent in 2012. The penetration of fixed tele-

phone lines has been relatively constant even with the

higher penetration of mobile phones.

In further analyzing device ownership, the study

compares household penetration levels of ICT devices

in various countries. Qatar enjoys higher penetration

rates for laptops, smartphones, and tablets compared

with more mature ICT economies such as Sweden

and Singapore, which trail Qatar significantly. Korea

lags far behind in terms of laptops and tablets, and is

equivalent to Qatar in terms of smartphone penetra-

tion. Given the high growth in the Qatar economy

and the speed of development of Qatar’s ICT sector,

higher adoption rates for technologies is not surpris-

ing (see Figure 5).

Figure 6 shows the improvement in the computer

penetration at the individual level in Qatar since

2010. Laptops and tablets have shown a great deal of

growth, while desktops registered a slight decrease.

Laptop penetration has increased to 93 percent and

94 percent in 2013 for the overall and mainstream

populations, respectively. Tablets jumped from ap-

proximately 10 percent to 29 percent from 2012 to

2013 for the overall population, and from 11 percent

to 32 percent for mainstream population during that

same period.

When comparing device ownership by gender in

the mainstream population, penetration levels for

desktops and laptops are almost the same for males

and females. In terms of tablets, penetration levels are

relatively higher for women (42 percent) than men (27

percent).

“I have my iPad, Galaxy, and laptop, which I cannot live without, and each is good for something. For example, I would rather watch a movie on my laptop because the screen is bigger, which makes it more enjoyable.

—YOUNG QATARI

”

FIGURE 6INDIVIDUAL ICT DEVICE PENETRATION, OVERALL VS MAINSTREAM, 2010–2013

35

%

35

%

19%

18

%

50

%

49

%

43

%

39

%

93

%

94

%

10%

11

%

29

%

32

%

87%

8

3%

Note: In 2010 data, tablets are included in the laptop number Source: Households and Individuals Survey, 2010, 2012, 2013Computer users in the overall population, 2010 n=1, 220, 2012 n=1,453, 2013 n=1,941Computer users in the mainstream population, 2010 n=1,184, 2012 n=1,391, 2013 n=1,865

2010 2012 2013

Desktop Laptop Tablet

2010 2012 2013 2010 2012

OVERALL

MAINSTREAM

2013

Figure 5HOUSEHOLD ICT PENETRATION, IN BENCHMARK COUNTRIES

2%

25%

44%

18%

74%

65%

27%

69%

58%

29%

66%

60%

42%

85%

60%

19%

74%

26%

16%

69%

42%

24%

62%

83%

69%

96%

66%

TABLET

LAPTOP COMPUTER

DESKTOP COMPUTER QATARKOREA

SAUDI ARABIAUAE

SINGAPORESWEDEN

UKGERMANY

INDIA

QATARKOREA

SAUDI ARABIAUAE

SINGAPORESWEDEN

UKGERMANY

INDIA

QATARKOREA

SAUDI ARABIAUAE

SINGAPORESWEDEN

UKGERMANY

INDIA

QATARKOREA

SAUDI ARABIAUAE

SINGAPORESWEDEN

UKGERMANY

INDIA

QATARKOREA

SAUDI ARABIAUAE

SINGAPORESWEDEN

UKGERMANY

INDIA

QATARKOREA

SAUDI ARABIAUAE

SINGAPORESWEDEN

UKGERMANY

INDIA

SMART TV

FIXED-LINE TELEPHONE

SMARTPHONE

61%

3%

12%

16% 15%

17% 18%

13% 19%

26% 12%

85% 77%

64% 73%

57% 59%

62% 72%

36%

67% 81%

83% 77%

74% 92% 92%

Sources: Ericsson ConsumerLab Analytical Platform, 2013Data for Qatar— Households and Individuals Survey, 2013Households n=1,957

Qatar’s ICT Landscape 2014 Households and Individuals 17

iNTERNET CONNECTiviTy

n internet penetration for both households and indi-viduals has increased since 2010 to near-universal levels—96% for households and 98% for the main-stream population—in 2013

n Overall, DSl is the most preferred type of internet ac-cess in households, followed by mobile broadband over the phone

n 85% of the overall population uses a laptop and 71% a smartphone to connect to the internet

n 52% of Qatari citizens connect to the internet using a tablet Pc in 2013 compared with 32% in 2012

n WiFi is the preferred mode of connecting to the in-ternet across the various internet-enabled devices used by the population in Qatar, except desktops

Key Findings

The growth in Internet penetration is seen at

both the household and individual levels. Internet

penetration is nearing 100 percent with 98 percent

of the mainstream population having an Internet con-

nection at home compared to 82 percent in 2010.

For individuals in the overall population, the Internet

penetration increased to 85 percent in 2013, up from

69 percent in 2010. This can be attributed to the

increase in the penetration of laptops, tablet PCs, and

smartphones (see Figure 7).

Nearly 100 percent of the Western and Qatari house-

holds have an Internet connection. The 2 percent of

the population that does not have Internet access at

home comprises expat Arabs and Asians, with high

cost cited as the main reason for lack of an Internet

connection. Fifty-five percent of Asian households

without Internet access think the cost of Internet is too

high and 32 percent of them cite lack of knowledge

or skills as a reason. Other main reasons cited by

respondents who did not have a household Internet

Figure 7HOUSEHOLD AND INDIVIDUAL INTERNET PENETRATION, 2010–2013

Source: Households and Individuals Survey, 2010, 2012, 2013Mainstream population, 2010 n=1,400, 2012 n = 1,566, 2013 n=1,957Overall population, 2010 n=1,700, 2012 n=1,880, 2013 n=2,207

84%

96%

69%

69%

85% 82%

88%

98%

2 0 1 0 2 0 1 2 2 0 1 3

HOUSEHOLDS

OVERALL POPULATION

MAINSTREAM POPULATION

Qatar’s ICT Landscape 2014 Households and Individuals18

connection were the lack of usefulness of the Internet

and lack of knowledge/skills to use the Internet.

As Figure 8 indicates, of the households that have

an Internet connection, the majority are connected

via fixed broadband—80 percent have other fixed

connections. As the fiber network is currently being

deployed and has not reached full coverage, the share

of FTTH, on a consolidated level, is still low, at around

24 percent. Across nationalities, Westerners, at 73

percent, are the biggest users of fiber-to-the-home.

Around 62 percent of mainstream Internet users also

use a mobile phone network—either via mobile phone

or USB dongle—to connect to the Internet. According

to the survey, over one-third of households use both

wired and WiFi connections at home, compared with

44 percent who use only wired connections and 21

percent of households who use only a WiFi connection.

With the increasing need to be connected to the Inter-

net at all times and with a faster connection, the people

of Qatar have migrated to higher Internet speeds. The

penetration of connections of less than 256 Kbps is

negligible now, with the 256 Kbps to 1 Mbps speed

connections also decreasing. On the other hand, high-

er speed connections are increasing—connections at 4

Mbps and above increased from 7 percent in 2010 to

14 percent in 2013 (see Figure 9). Speeds are expected

to further increase significantly with the deployment of

the nationwide fiber network.

In terms of devices that individuals prefer to use to con-

nect to the Internet, the tablet PC has shown substantial

growth. Fifty-two percent of Qataris connected using

a tablet PC in 2013 compared to just 32 percent in

2012. Overall, smartphones and laptops are preferred

by both Qatari and non-Qatari segments. At the overall

population level, 85 percent of Internet users use a

laptop and 71 percent a smartphone to connect to the

Internet.

Across all devices used to connect online, except desk-

tops, the preferred mode of connection is wireless LAN

because of the convenience it offers (see Figure 10).

The 2013 survey results compared to those from previ-

ous years show an increase in the use of smartphones,

tablets, and laptops as preferred devices to connect to

the Internet. Smartphones have witnessed the sharpest

increase, with 71 percent of Internet users in the overall

population using smartphones today compared to just

35 percent in 2010. Even tablets, from being nearly

nonexistent in 2010, are a device of choice to connect

to the Internet by 26 percent in 2013 (see Figure 11).

This bolsters the theme that Qatari residents increas-

ingly need and want “anywhere, anytime” connectivity.

Figure 8TYPES OF HOUSEHOLD INTERNET CONNECTIVITY, BY NATIONALITY

Note: Dial-up connections are maintained as an additional connection, along with other fixed or mobile broadband connections: of the 10% of households with dial-up connections, 94% have fixed broadband and 51% have mobile broadband connectivity

Source: Households and Individuals Survey, 2013Mainstream population Internet users n=1,877

DIAL-UP CONNECTION

FIBER-TO-THE-HOME

OTHER FIXED CONNECTIONS

MOBILE PHONE

MOBILE BROADBAND 10%

2

4%

8

0%

5

4%

12

%

Overall

2%

2

5%

76

%

66

%

21%

Qataris

3%

36

%

74%

5

9%

7%

Expat Arabs

18%

12

%

85

%

46

%

11%

Asians

2%

73

%

91%

8

5%

3

4%

Westerners

Figure 10MODES USED TO CONNECT TO INTERNET, INDIVIDUALS, BY DEVICE

MOBILE BROADBAND

WIFI OR WIRELESS LAN

FIXED CONNECTION 1%

4

6%

5

5%

Desktop

3%

8

6%

18

%

Laptop

9%

9

4%

Tablet PC

49

% 70

%

Smartphone

35

% 6

2%

Other mobile phone

Source: Households and Individuals Survey, 2013Devices used to access the Internet, desktop n=705, laptop n=1,830, tablet PC n=575, smartphone n=1,555, other mobile phone n=388

5% 3%

70%

86%

80%

85%

71%

33%

26% 22% 1% 0%

13%

35%

49%

19%

31%

Figure 11DEVICES USED BY INDIVIDUALS TO CONNECT TO INTERNET, SINCE 2010

2 0 1 0 2 0 1 3 2 0 1 2

Note: 2010 data for tablets not availableSource: Households and Individuals Survey, 2010, 2012, 2013Internet users in the overall population, 2010 n=1,171, 2012 n=1,485, 2013 n=2,045

DESKTOP

LAPTOP

TABLET

SMARTPHONE

OTHER MOBILEPHONE

OTHER FDEVICE

Figure 9HOUSEHOLD INTERNET CONNECTION SPEED, 2010–2013

2 0 1 0 2 0 1 3

5% 1%

37% 23%

39% 48%

7% 14%

Source: Households and Individuals Survey 2010, 2013Households with Internet access, 2010 n=1,176, 2013 n=1,877

4 MBPS AND ABOVE

LESS THAN 256 KBPS

>1 MBPS TO 4 MBPS

>256 KBPS TO 1 MBPS

Qatar’s ICT Landscape 2014 Households and Individuals 19

iCT uSAGE AND SPENDiNG

n People in Qatar have access to computers mostly from their homes, followed by their workplace and another person’s home; internet access preferences are similar, but people also want “on-the-go” con-nectivity via mobile phone or other mobile device

n 89% of the internet users in Qatar accesses the internet for downloading content (movies, images, music), watching tv or video, or listening to radio or music, and the survey results show a significant uptake of all online activities compared to 2012

n People use their mobile phones mostly for basic services such as phone calls and SmS, but also for browsing the internet, social networking, watching videos, and downloading apps

n Services such as e-commerce, online banking, and e-government are used by a small percentage of the overall population

n Qatari households spend almost three times as much on ict services per month as non-Qatari households

n at the individual level, Qataris spend almost three times as much as non-Qataris on mobile phone service

n average individual monthly spending on mobile phones decreased from QaR 417 in 2010 to QaR 292 in 2013

Key Findings

The overwhelming majority of people have ac-

cess to computers at home. Only 37 percent of 15- to

24-year-olds access computers at an educational insti-

tution. More than 60 percent of the working popula-

tion in Qatar access computers from their place of

work. As with computer access, home is the preferred

location for Internet users—this is valid across all seg-

ments (see Figure 12). The second-most preferred way

of accessing the Internet is through a mobile device.

Fifty-seven percent of the overall users access the

Internet from a place of work, but the trend varies for

individual segments. As with computer usage, Internet

usage at an educational institution is low, with only 37

percent of young Qataris accessing the Internet at an

educational institution (see Figure 13).

Downloading content (movies, images, music), watch-

ing TV or video, or listening to radio or music—

Figure 12LOCATION OF COMPUTER ACCESS, INDIVIDUALS, BY AGE GROUP

Source: Households and Individuals Survey, 2013Computer users in the overall population n=1,941

58

%

39

%

41%

6

2%

13

%

99

%

61%

4

3%

4

5%

4

6%

3

7%

99

%

59

%

38

%

41%

6

6%

6

%

99

%

49

%

33

%

38

%

63

%

11%

9

9%

EDUCATIONALINSTITUTION

WORKPLACE COMMUNITYINTERNET

COMMERCIAL INTERNET

ANOTHER PERSON’S HOME

HOME

Overall computer users 15–24 years 25–44 years Over 44 years

Figure 13LOCATION OF INTERNET ACCESS, INDIVIDUALS

97%

Any place via mobile

phone/mobile device

74%

Home

57%

Workplace

63%

Otherlocation

13%

Educationalinstitution

Overall Internet users

Note: Other location includes community Internet access facility, commercial Internet access facility, and another person’s homeSource: Households and Individuals Survey, 2013Internet users in the overall population n= 2,045

Qatar’s ICT Landscape 2014 Households and Individuals20

“Now, I can easily make contact with Skype, BBM, WhatsApp for minimal cost or free. Technology made our world a smaller place and connected our family and friends 24/7. Also, you know everything, every moment.” —MID-RANGE ADULT ASIAN, FEMALE

continue to be the most dominant activities undertak-

en online by people in Qatar. Tasks such as download-

ing software, reading and searching for information

online, file sharing, playing/downloading games, and

online learning have significantly increased since 2012

(see Figure 14). The decrease in the percentage of the

mainstream population conducting Internet banking

most likely reflects the concerns people have with

using these services on the Internet. This situation is

discussed in further detail later in the report.

Westerners are most active in using all services, while

sending/receiving e-mail and social networking are

the most common and used at least once per week

across all nationalities.

E-commerce, online banking, and e-government are

used by a small percentage of the overall population.

In an attempt to predict future Internet use, survey

respondents were asked to identify the device they

use the most for accessing a particular online service.

Given the high penetration of laptops, it is not surpris-

ing that a majority of the population preferred using a

laptop for accessing various Internet services. Mobile

phone is the second-most preferred device for access-

ing online services; however, people in general do not

seem to be very comfortable using their phones for

accessing services such as e-commerce, e-banking,

etc. Although further research on this topic is neces-

sary, concerns about the safety of mobile broadband,

lack of awareness of these services, and lack of skill in

using the services could explain such reluctance.

Figure 14TASKS PERFORMED ONLINE BY INDIVIDUALS, OVERALL AND

MAINSTREAM POPULATION, 2012 AND 2013

Source: Households and Individuals Survey, 2013, 2012Internet users in the overall population, 2013 n= 2,045Internet users in the mainstream population, 2013 n=1,916, 2012 n=1,405

69% 88% 89%

50% 86% 86%

59% 79%

74%

24% 77%

66%

55% 69%

59%

32% 69%

58%

35% 68%

65%

37% 64%

58%

45% 53%

46%

20% 31%

27%

24% 21%

18%

25% 18%

15% PURCHASING OR ORDERING GOODS OR SERVICES

INTERNET BANKING

INTERACTING WITH GOVERNMENT ORGANIZATIONS

GETTING INFORMATION FROM GOVERNMENT ORGANIZATIONS

EDUCATION OR LEARNING ACTIVITIES

PLAYING OR DOWNLOADING GAMES

USING PEER-TO-PEER FILE SHARING

GETTING INFORMATION ABOUT GOODS OR SERVICES

GETTING INFORMATION RELATED TO HEALTH OR HEALTH SERVICES

READING OR DOWNLOADING ONLINE NEWSPAPERS OR

MAGAZINES, OR ELECTRONIC BOOKS

DOWNLOADING SOFTWARE

DOWNLOADING/WATCHING MOVIES/MUSIC

2013—OVERALL

2013—MAINSTREAM

2012—MAINSTREAM

Table 3INDIVIDUAL USAGE OF SERVICES THROUGH MOBILE

PHONES, OVERALL, MAINSTREAM, MALE, FEMALE

OVERALLPOPULATION MAINSTREAM MALEFEMALE

Mobile banking

Social networking

Browse Internet

Make or receive calls

Send/receive text message (SMS)

Send/receive photo message (MMS)

15%

65%

76%

78%

100%

98%

73%

21%

80%

85%

89%

100%

98%

79%

14%

61%

74%

76%

100%

98%

72%

21%

83%

84%

88%

100%

99%

78%

Notes: Social networking includes posting and reading messages on online forums/websites and instant messaging100% figures shown above have been rounded to zero decimal placesSource: Households and Individuals Survey, 2013Mobile phone users in the overall population n=2,205

Qatar’s ICT Landscape 2014 Households and Individuals 21

“Before I used to call my family back in Tunisia every two weeks or a month because it is so expensive, now, with Skype I call my family and friends every day.

—MID-RANGE ADULT EXPAT ARAB

”

More women than men access various online activities

through mobile phones. This difference in usage pat-

terns is most obvious for accessing email on mobile

phones, mobile banking, and VoIP. This may be due to

the fact that women in Qatar show equal, if not higher,

penetration of ICT devices such as smartphones and

tablets (see Table 3).

Compared with those in various countries, people in

Qatar are actively using mobile phones for sending/

receiving SMS over the phone. However, coupled

with the lack of uptake of services such as mobile

banking and e-commerce, one can conclude that

people in Qatar have the technology but need more

education about the other services they could use

through mobile phones in order to move to the next

level of advanced usage (see Figure 15).

Figure 15ACTIVITIES ACCESSED THROUGH MOBILE PHONES,

INDIVIDUALS IN BENCHMARK COUNTRIES

BROWSING THE INTERNET

QATARUK

UAESWEDEN

SINGAPORESAUDI ARABIA

KOREAINDIA

GERMANY 56% 54%

92% 89%

88% 80%

78% 72%

78%

SENDING/RECEIVING MMS (VIDEOS OR PICTURES)

QATARUK

UAESWEDEN

SINGAPORESAUDI ARABIA

KOREAINDIA

GERMANY 45% 43%

87% 87%

73% 84%

71% 61%

73%

SENDING/RECEIVING TEXT MESSAGES

QATARUK

UAESWEDEN

SINGAPORESAUDI ARABIA

KOREAINDIA

GERMANY 93% 78%

97% 92%

98% 98%

94% 95%

98%

SENDING/RECEIVING EMAIL

QATARUK

UAESWEDEN

SINGAPORESAUDI ARABIA

KOREAINDIA

GERMANY 52% 40%

82% 87%

84% 69%

74% 64% 65%

Sources: Ericsson ConsumerLab Analytical Platform, 2013Data for Qatar—Households and Individuals Survey, 2013Mobile phone users in the overall population n=2,205

Qatar’s ICT Landscape 2014 Households and Individuals22

TRANSIENT LABORERS

128

MID-RANGE ADULT/OLDER QATARIS

1,000

YOUNG QATARIS

733NON-QATARIS, BLUE COLLAR (SHARED ACCOMMO-DATION)

177

WHITE-COLLAR ASIANS, TECHNOLOGYNEUTRAL

184WHITE-COLLAR ASIANS, TECHNOLOGY INTERESTED

233

NON-QATARIS, BLUE COLLAR (NON-SHARED ACCOMMO-DATION)

239WHITE-COLLAR EXPAT ARABS, TECHNOLOGY INTERESTED

373

WHITE-COLLAR EXPAT ARABS, TECHNOLOGY NEUTRAL

404WESTERNERS

738

Source: Households and Individuals Survey, 2013Mobile phone users in overall population n=2,205

Figure 17AVERAGE MONTHLY INDIVIDUAL SPENDING (QAR) ON MOBILE PHONE SERVICES, BY SEGMENT

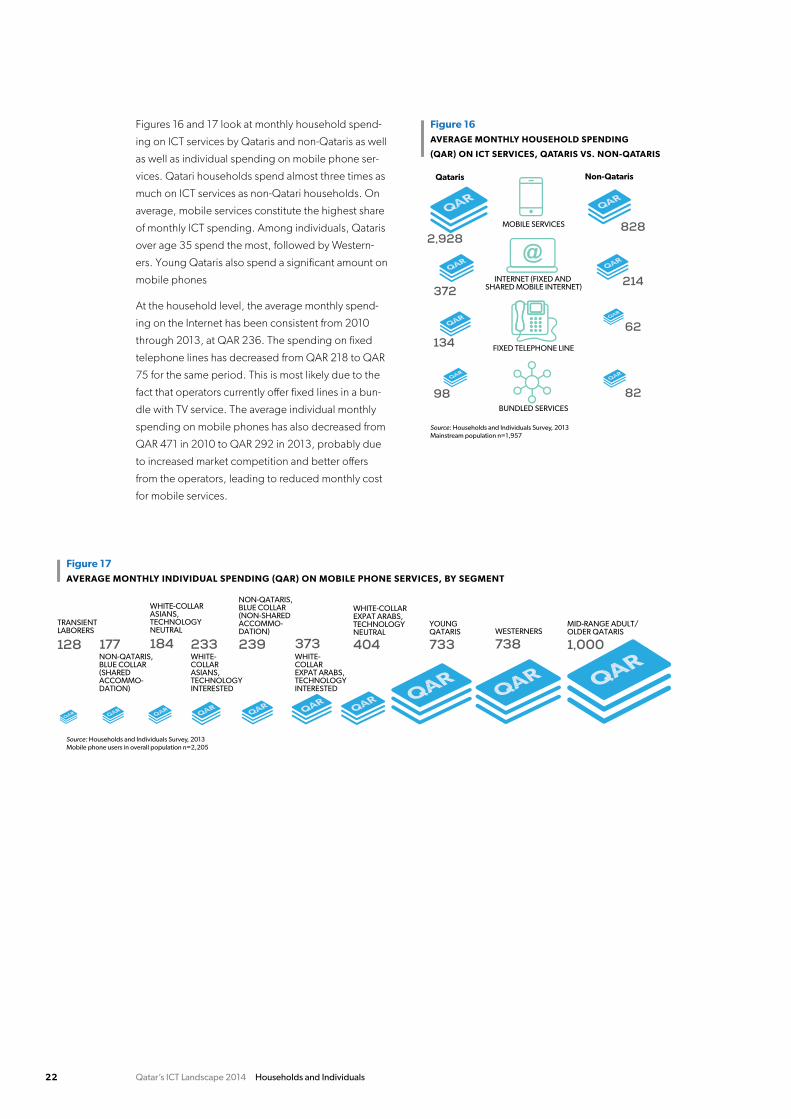

Figures 16 and 17 look at monthly household spend-

ing on ICT services by Qataris and non-Qataris as well

as well as individual spending on mobile phone ser-

vices. Qatari households spend almost three times as

much on ICT services as non-Qatari households. On

average, mobile services constitute the highest share

of monthly ICT spending. Among individuals, Qataris

over age 35 spend the most, followed by Western-

ers. Young Qataris also spend a significant amount on

mobile phones

At the household level, the average monthly spend-

ing on the Internet has been consistent from 2010

through 2013, at QAR 236. The spending on fixed

telephone lines has decreased from QAR 218 to QAR

75 for the same period. This is most likely due to the

fact that operators currently offer fixed lines in a bun-

dle with TV service. The average individual monthly

spending on mobile phones has also decreased from

QAR 471 in 2010 to QAR 292 in 2013, probably due

to increased market competition and better offers

from the operators, leading to reduced monthly cost

for mobile services.

Figure 16AVERAGE MONTHLY HOUSEHOLD SPENDING

(QAR) ON ICT SERVICES, QATARIS VS. NON-QATARIS

Source: Households and Individuals Survey, 2013Mainstream population n=1,957

Qataris Non-Qataris

MOBILE SERVICES

BUNDLED SERVICES

INTERNET (FIXED AND SHARED MOBILE INTERNET)

FIXED TELEPHONE LINE

828

214

62

82

2,928

372

134

98

Qatar’s ICT Landscape 2014 Households and Individuals 23

SATiSFACTiON WiTH mOBiLE AND iNTERNET SERviCES

Key Findings

n Overall, 60% of Qataris are satisfied with their mobile phone service

n Westerners are the least satisfied with Qatar’s cur-rent level of internet and mobile phone services

n across the overall population of Qatar, satisfaction rates for mobile broadband stands at 40%, while satisfaction for fixed broadband is 50%

n Overall satisfaction rates for both internet and mobile phone services have increased over time

n across all segments and nationalities, “customer support” and “ease of changes to account on your own” are the areas of least satisfaction among residents of Qatar, according to the survey

overall, individuals rate their satisfaction with

fixed broadband (50%) and mobile phone service

(50%) slightly higher than mobile broadband (40%).

While all Qataris and white-collar, technology-inter-

ested Arabs reported high overall satisfaction levels

for Internet and mobile phone services, Westerners

rated these services very low. The other segments

gave an average rating to the mobile phone and fixed

broadband services. The satisfaction levels for mobile

broadband across most of the segments was lower

than that of young Qataris, whose satisfaction rating

of mobile broadband services was 82 percent (see

Figure 18). The fact that Westerners rated fixed and

mobile broadband and mobile phone services very

Figure 18OVERALL SATISFACTION WITH INTERNET AND MOBILE PHONE SERVICES, INDIVIDUALS BY SEGMENT

50

%

78%

2%

60

%

11%

50

%

50

%

28

%

45

%

47%

40

%

82

%

70%

48

%

54

%

29

%

23

%

45

%

26

%

50

%

75%

21%

56

% 6

8%

74%

57%

54

%

51%

59

%

55

% MOBILE

BROADBAND

MOBILE PHONE SERVICE

FIXED BROADBAND

51%

2

6%

3

3%

1 2 3 4 5 6 7 8 9Overall users 10

Different modes used to connect to the Internet for devices, mobile broadband n=957, fixed broadband n=1,984 Mobile phone users in the overall population n=2,205

Note: Satisfaction refers to the top two boxes on a 7-point scaleSource: Households and Individuals Survey, 2013

1. Young Qataris 2. Mid-range Adult/Older

Qataris 3. Westerners

4. White-Collar Expat Arabs, Technology Interested

5. White-Collar Expat Arabs, Technology Neutral

6. White-Collar Asians, Technology Interested

7. White-Collar Asians, Technology Neutral

8. Non-Qataris, Blue Collar (Non-Shared Accommoda-tion)

9. Non-Qataris, Blue Collar (Shared Accommodation)

10. Transient Laborers

Qatar’s ICT Landscape 2014 Households and Individuals24

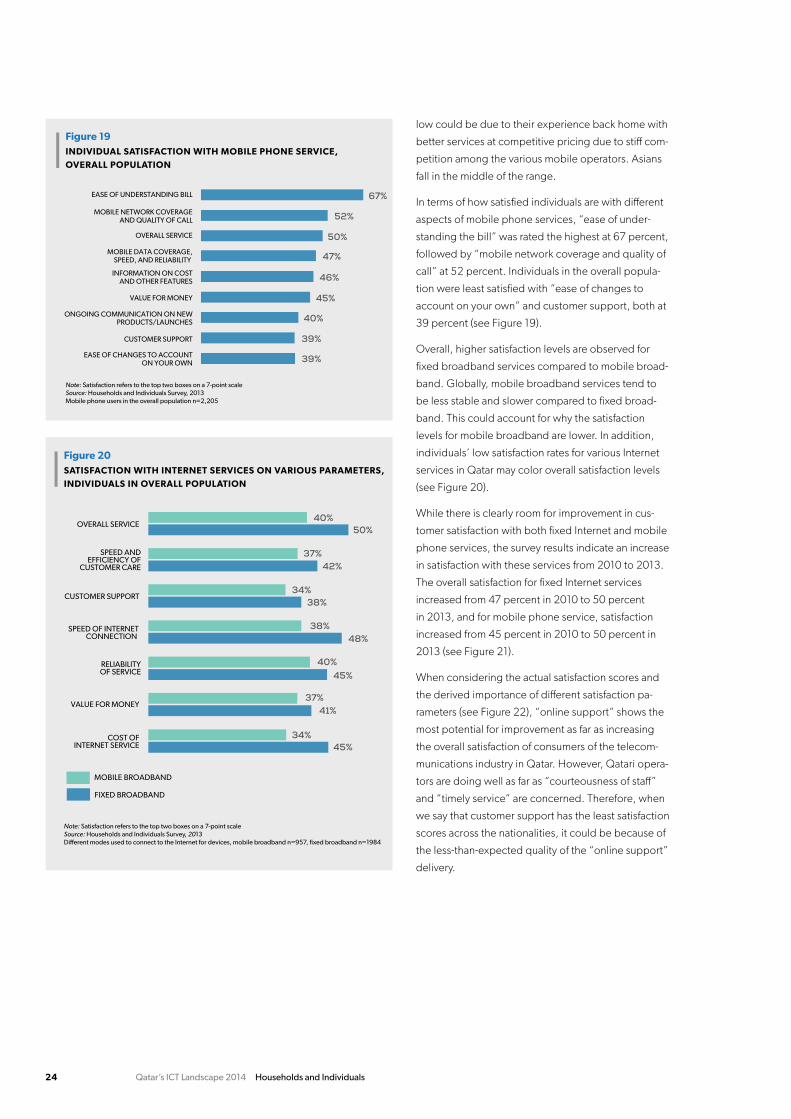

low could be due to their experience back home with

better services at competitive pricing due to stiff com-

petition among the various mobile operators. Asians

fall in the middle of the range.

In terms of how satisfied individuals are with different

aspects of mobile phone services, “ease of under-

standing the bill” was rated the highest at 67 percent,

followed by “mobile network coverage and quality of

call” at 52 percent. Individuals in the overall popula-

tion were least satisfied with “ease of changes to

account on your own” and customer support, both at

39 percent (see Figure 19).

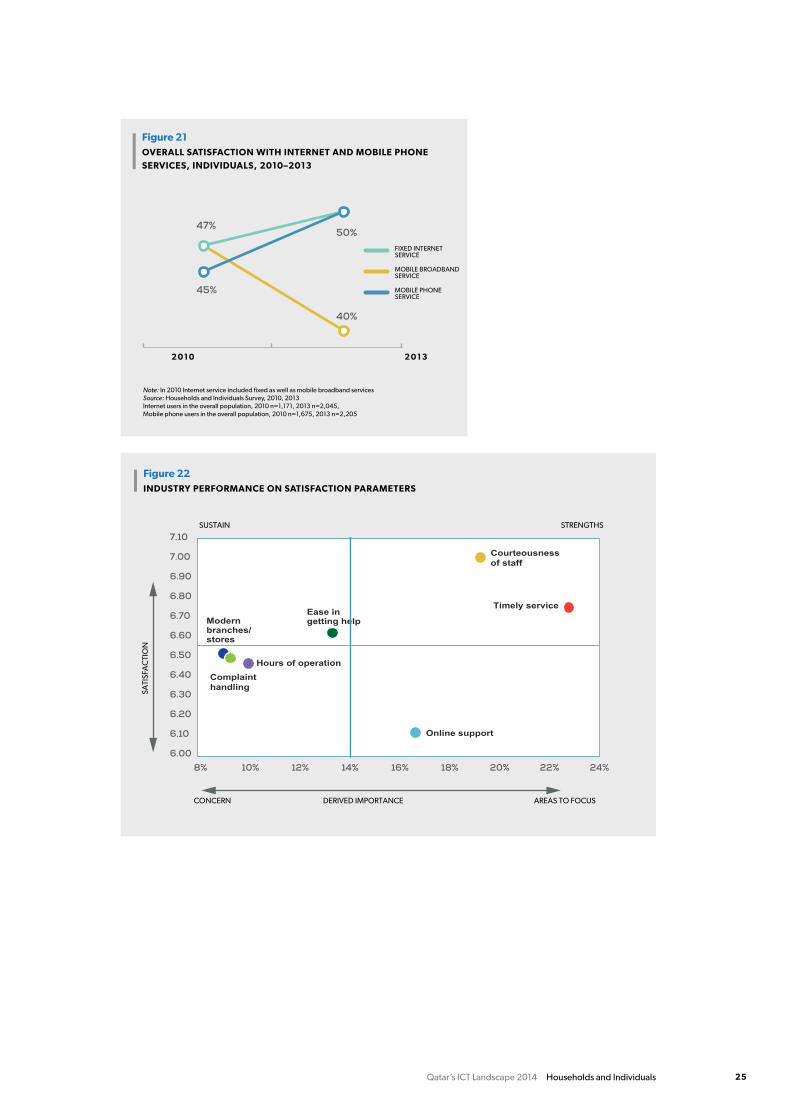

Overall, higher satisfaction levels are observed for

fixed broadband services compared to mobile broad-

band. Globally, mobile broadband services tend to

be less stable and slower compared to fixed broad-

band. This could account for why the satisfaction

levels for mobile broadband are lower. In addition,

individuals’ low satisfaction rates for various Internet

services in Qatar may color overall satisfaction levels

(see Figure 20).

While there is clearly room for improvement in cus-

tomer satisfaction with both fixed Internet and mobile

phone services, the survey results indicate an increase

in satisfaction with these services from 2010 to 2013.

The overall satisfaction for fixed Internet services

increased from 47 percent in 2010 to 50 percent

in 2013, and for mobile phone service, satisfaction

increased from 45 percent in 2010 to 50 percent in

2013 (see Figure 21).

When considering the actual satisfaction scores and

the derived importance of different satisfaction pa-

rameters (see Figure 22), “online support” shows the

most potential for improvement as far as increasing

the overall satisfaction of consumers of the telecom-

munications industry in Qatar. However, Qatari opera-

tors are doing well as far as “courteousness of staff”

and “timely service” are concerned. Therefore, when

we say that customer support has the least satisfaction

scores across the nationalities, it could be because of

the less-than-expected quality of the “online support”

delivery.

Figure 19INDIVIDUAL SATISFACTION WITH MOBILE PHONE SERVICE, OVERALL POPULATION

47%MOBILE DATA COVERAGE,SPEED, AND RELIABILITY

50%OVERALL SERVICE

67%EASE OF UNDERSTANDING BILL

46%INFORMATION ON COSTAND OTHER FEATURES

45%VALUE FOR MONEY

39%CUSTOMER SUPPORT

52%MOBILE NETWORK COVERAGEAND QUALITY OF CALL

40%ONGOING COMMUNICATION ON NEWPRODUCTS/LAUNCHES

39%EASE OF CHANGES TO ACCOUNTON YOUR OWN

Note: Satisfaction refers to the top two boxes on a 7-point scaleSource: Households and Individuals Survey, 2013Mobile phone users in the overall population n=2,205

Figure 20SATISFACTION WITH INTERNET SERVICES ON VARIOUS PARAMETERS, INDIVIDUALS IN OVERALL POPULATION

48% 38%

40% 50%

37% 42%

38% 34%

34% 45%

45% 40%

41% 37%

Note: Satisfaction refers to the top two boxes on a 7-point scaleSource: Households and Individuals Survey, 2013Different modes used to connect to the Internet for devices, mobile broadband n=957, fixed broadband n=1984

COST OF INTERNET SERVICE

VALUE FOR MONEY

RELIABILITYOF SERVICE

SPEED OF INTERNETCONNECTION

CUSTOMER SUPPORT

SPEED ANDEFFICIENCY OF

CUSTOMER CARE

OVERALL SERVICE

MOBILE BROADBAND

FIXED BROADBAND

Qatar’s ICT Landscape 2014 Households and Individuals 25

Modern branches/stores

Ease in getting help

Complaint

handling

Hours of operation

Online support

Courteousness

of staff

Timely service

Figure 22INDUSTRY PERFORMANCE ON SATISFACTION PARAMETERS

SATI

SFA

CTI

ON

DERIVED IMPORTANCE AREAS TO FOCUSCONCERN

6.00

6.10

6.20

6.30

6.40

6.50

6.60

6.70

6.80

6.90

7.00

7.10

8% 10% 12% 14% 16% 18% 20% 22% 24%

SUSTAIN STRENGTHS

Figure 21OVERALL SATISFACTION WITH INTERNET AND MOBILE PHONE SERVICES, INDIVIDUALS, 2010–2013

Note: In 2010 Internet service included fixed as well as mobile broadband servicesSource: Households and Individuals Survey, 2010, 2013Internet users in the overall population, 2010 n=1,171, 2013 n=2,045, Mobile phone users in the overall population, 2010 n=1,675, 2013 n=2,205

2 0 1 0 2 0 1 3

45%

47% 50%

40%

MOBILE BROADBAND SERVICE

MOBILE PHONE SERVICE

FIXED INTERNET SERVICE

Qatar’s ICT Landscape 2014 Households and Individuals26

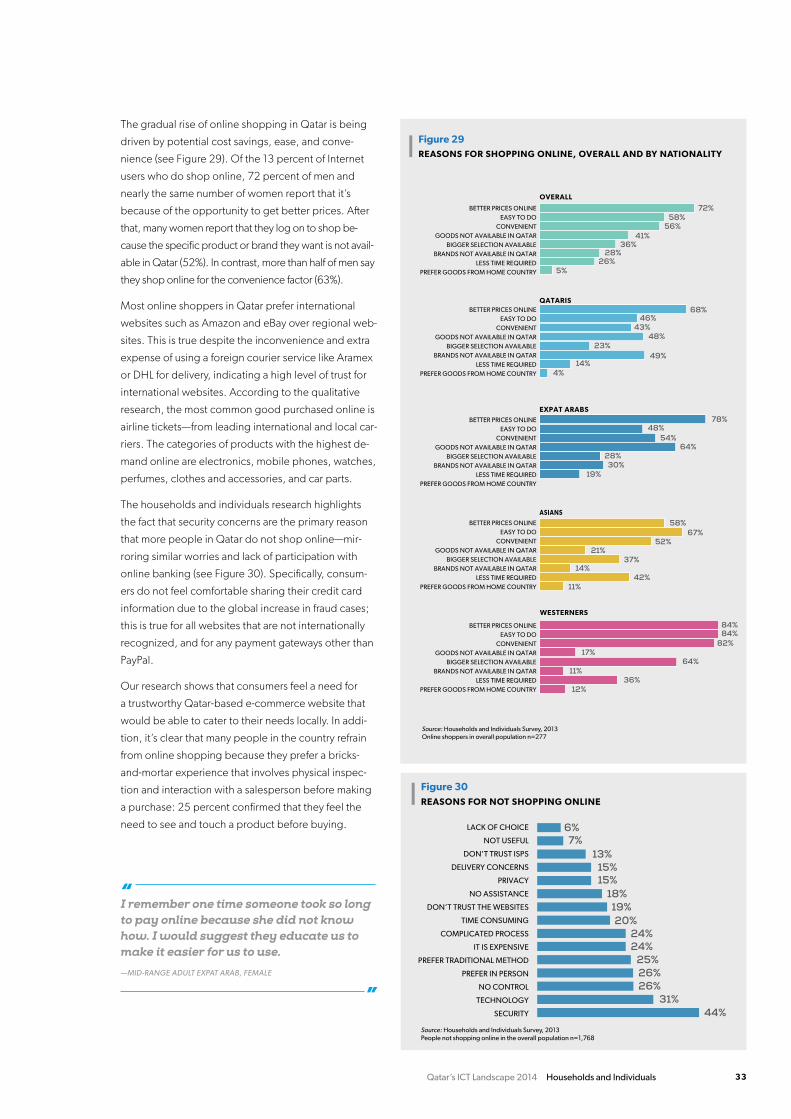

Qatar’s ICT Landscape 2014 Households and Individuals 27

S O c i a l n E t WO R k i n g a n D a R a B i c cO n t E n t O n l i n E

O n l i n E B a n k i n g a n D E - cO m m E R c E

E - g Ov E R n m E n t

Q - P O St S E Rv i c E S

O n l i n E S E c u R i t y a n D P R i vac y

n E W S E Rv i c E S

FOCuS AREAS

Qatar’s ICT Landscape 2014 Households and Individuals28

SOCiAL NETWORKiNG AND ARABiC CONTENT ONLiNE

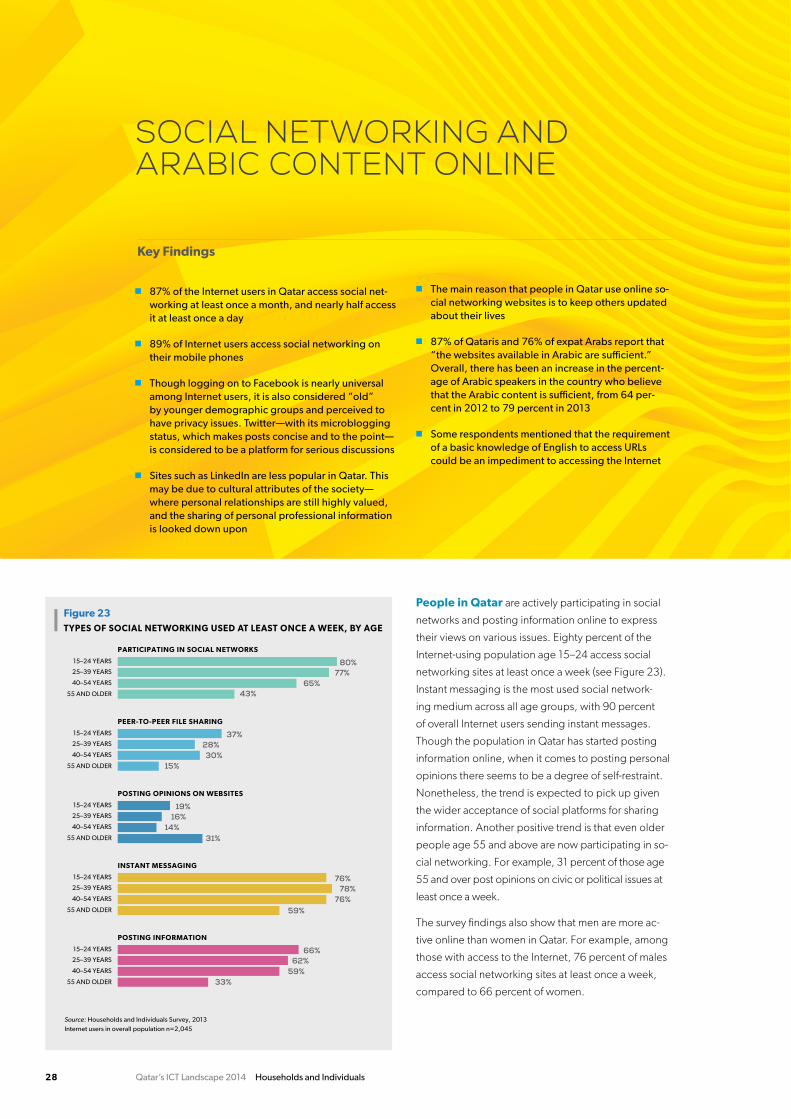

n 87% of the internet users in Qatar access social net-working at least once a month, and nearly half access it at least once a day

n 89% of internet users access social networking on their mobile phones

n though logging on to Facebook is nearly universal among internet users, it is also considered “old” by younger demographic groups and perceived to have privacy issues. twitter—with its microblogging status, which makes posts concise and to the point—is considered to be a platform for serious discussions

n Sites such as linkedin are less popular in Qatar. this may be due to cultural attributes of the society—where personal relationships are still highly valued, and the sharing of personal professional information is looked down upon

n the main reason that people in Qatar use online so-cial networking websites is to keep others updated about their lives

n 87% of Qataris and 76% of expat arabs report that “the websites available in arabic are sufficient.” Overall, there has been an increase in the percent-age of arabic speakers in the country who believe that the arabic content is sufficient, from 64 per-cent in 2012 to 79 percent in 2013

n Some respondents mentioned that the requirement of a basic knowledge of English to access uRls could be an impediment to accessing the internet

People in Qatar are actively participating in social

networks and posting information online to express

their views on various issues. Eighty percent of the

Internet-using population age 15–24 access social

networking sites at least once a week (see Figure 23).

Instant messaging is the most used social network-

ing medium across all age groups, with 90 percent

of overall Internet users sending instant messages.

Though the population in Qatar has started posting

information online, when it comes to posting personal

opinions there seems to be a degree of self-restraint.

Nonetheless, the trend is expected to pick up given

the wider acceptance of social platforms for sharing

information. Another positive trend is that even older

people age 55 and above are now participating in so-

cial networking. For example, 31 percent of those age

55 and over post opinions on civic or political issues at

least once a week.

The survey findings also show that men are more ac-

tive online than women in Qatar. For example, among

those with access to the Internet, 76 percent of males

access social networking sites at least once a week,

compared to 66 percent of women.

Key Findings

Figure 23TYPES OF SOCIAL NETWORKING USED AT LEAST ONCE A WEEK, BY AGE

15–24 YEARS

25–39 YEARS

40–54 YEARS

55 AND OLDER 43% 65%

77% 80%

PARTICIPATING IN SOCIAL NETWORKS

15–24 YEARS

25–39 YEARS

40–54 YEARS

55 AND OLDER 15% 30%

28% 37%

PEER-TO-PEER FILE SHARING

15–24 YEARS

25–39 YEARS

40–54 YEARS

55 AND OLDER 31% 14%

16% 19%

POSTING OPINIONS ON WEBSITES

15–24 YEARS

25–39 YEARS

40–54 YEARS

55 AND OLDER 59% 76%

78% 76%

INSTANT MESSAGING

15–24 YEARS

25–39 YEARS

40–54 YEARS

55 AND OLDER 33% 59%

62% 66%

POSTING INFORMATION

Source: Households and Individuals Survey, 2013Internet users in overall population n=2,045

Qatar’s ICT Landscape 2014 Households and Individuals 29

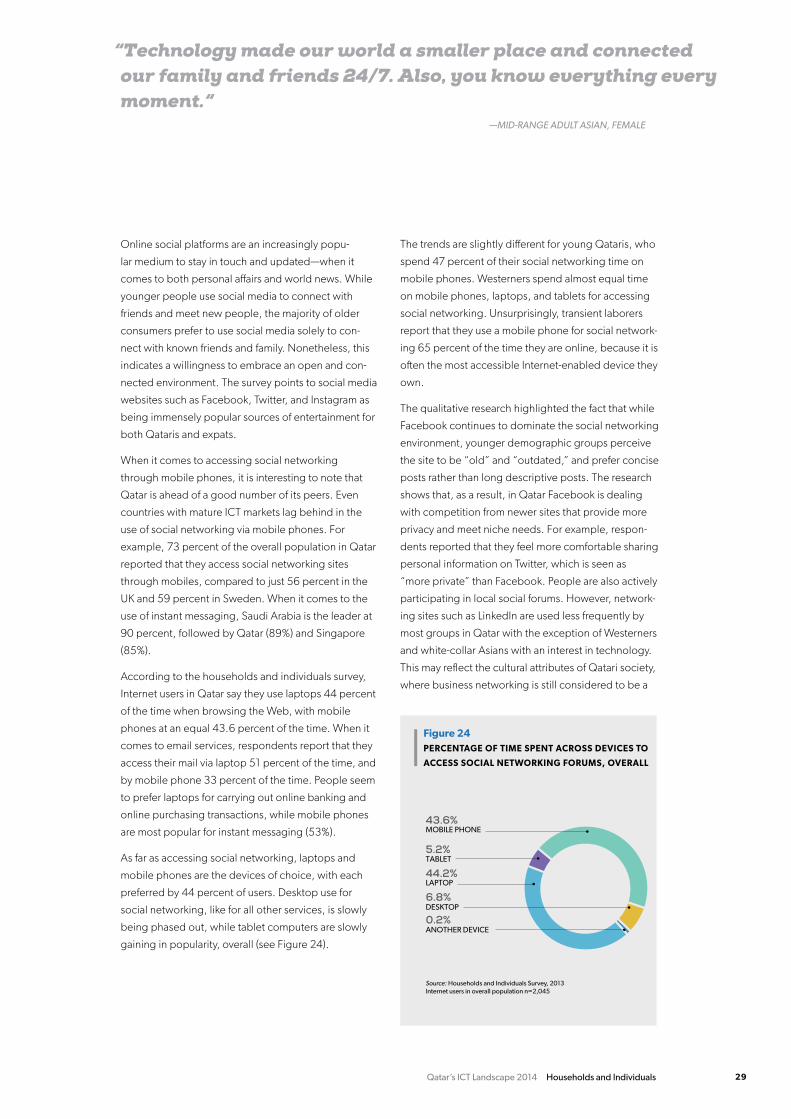

Online social platforms are an increasingly popu-

lar medium to stay in touch and updated—when it

comes to both personal affairs and world news. While

younger people use social media to connect with

friends and meet new people, the majority of older

consumers prefer to use social media solely to con-

nect with known friends and family. Nonetheless, this

indicates a willingness to embrace an open and con-

nected environment. The survey points to social media

websites such as Facebook, Twitter, and Instagram as

being immensely popular sources of entertainment for

both Qataris and expats.

When it comes to accessing social networking

through mobile phones, it is interesting to note that

Qatar is ahead of a good number of its peers. Even

countries with mature ICT markets lag behind in the

use of social networking via mobile phones. For

example, 73 percent of the overall population in Qatar

reported that they access social networking sites

through mobiles, compared to just 56 percent in the

UK and 59 percent in Sweden. When it comes to the

use of instant messaging, Saudi Arabia is the leader at

90 percent, followed by Qatar (89%) and Singapore

(85%).

According to the households and individuals survey,

Internet users in Qatar say they use laptops 44 percent

of the time when browsing the Web, with mobile

phones at an equal 43.6 percent of the time. When it

comes to email services, respondents report that they

access their mail via laptop 51 percent of the time, and

by mobile phone 33 percent of the time. People seem

to prefer laptops for carrying out online banking and

online purchasing transactions, while mobile phones

are most popular for instant messaging (53%).

As far as accessing social networking, laptops and

mobile phones are the devices of choice, with each

preferred by 44 percent of users. Desktop use for

social networking, like for all other services, is slowly

being phased out, while tablet computers are slowly

gaining in popularity, overall (see Figure 24).

The trends are slightly different for young Qataris, who

spend 47 percent of their social networking time on

mobile phones. Westerners spend almost equal time

on mobile phones, laptops, and tablets for accessing

social networking. Unsurprisingly, transient laborers

report that they use a mobile phone for social network-

ing 65 percent of the time they are online, because it is

often the most accessible Internet-enabled device they

own.

The qualitative research highlighted the fact that while

Facebook continues to dominate the social networking

environment, younger demographic groups perceive

the site to be “old” and “outdated,” and prefer concise

posts rather than long descriptive posts. The research

shows that, as a result, in Qatar Facebook is dealing

with competition from newer sites that provide more

privacy and meet niche needs. For example, respon-

dents reported that they feel more comfortable sharing

personal information on Twitter, which is seen as

“more private” than Facebook. People are also actively

participating in local social forums. However, network-

ing sites such as LinkedIn are used less frequently by

most groups in Qatar with the exception of Westerners