q1 us economic market overview for cre

TRANSCRIPT

© 2017 Ten-X, LLC. All Rights Reserved.

Outlook for the Economy, Capital Markets, and Real Estate

February 2017

Ten-X Client Webinar

Economic Overview

US Economic Expansion Continuing Despite Challenges Internationally and Domestically

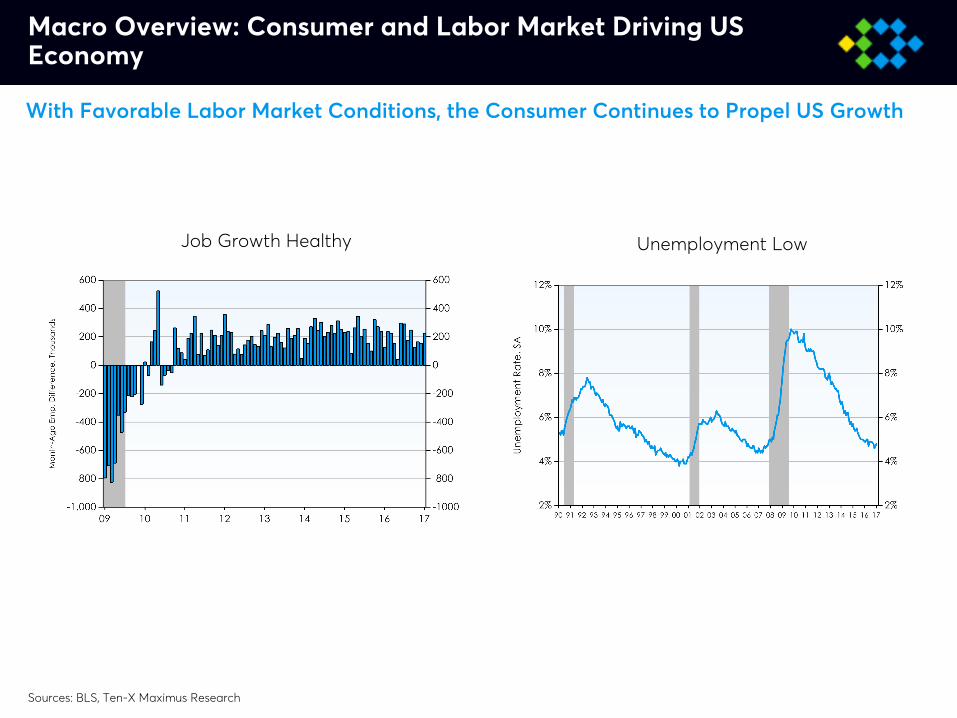

Macro Indicators Healthy and Weaving Through Volatility…Ø Headline payroll growth kicked off the year with a bang, resulting in average monthly

jobs gains of 188,000 over the last six months. Unemployment is low and under 5%, while the labor force participation rate seems to have found a bottom for the cycle. Average hourly earnings are climbing, up 2.5% year over year most recently, with other wage growth measures also on the rise.

Ø Household wealth is at an all-time peak, consumer confidence rising, households enjoying “energy dividend”, consumer spending at record high.

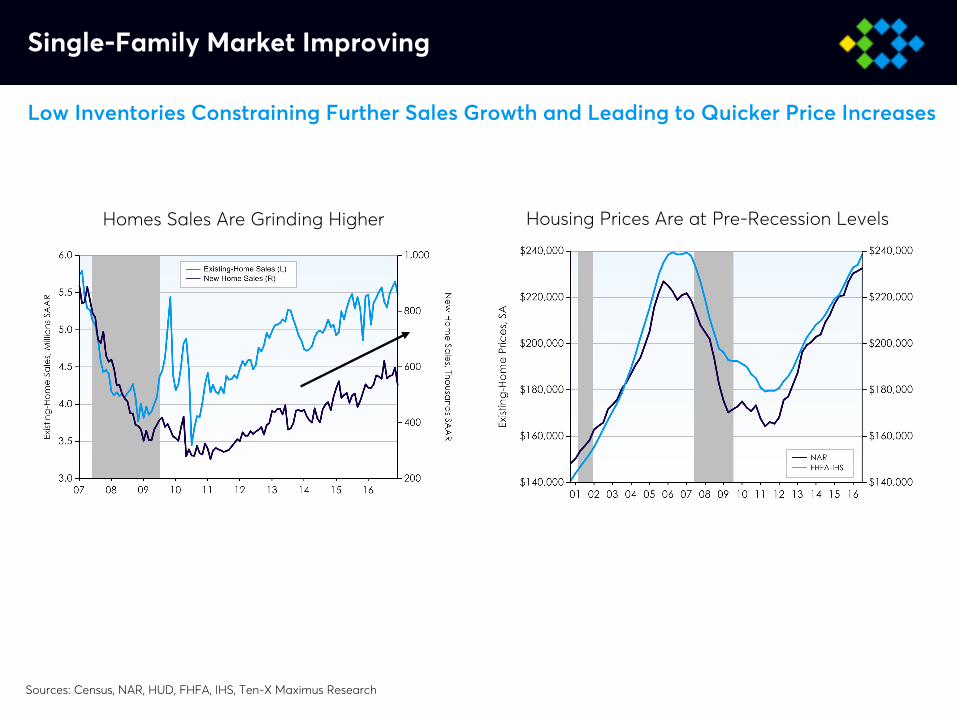

Ø Housing market recovering. Sales are at healthy pace and prices continue rising, though affordability is diminishing.

Ø The Federal Reserve raised rates 25 bps in December, a full year after the last hike.Some Weaker Spots…Ø The energy sector remains depressed, however prices have stabilized around $50/bbl

range and headwind to energy/industrial sectors diminishing.Ø Trade flows are stagnant amid a strong US dollar, subdued oil prices, and weak global

demand conditions. Ø Brexit rattling markets, while Europe, China and Japan’s economies continue to struggle.Ø Uncertainty regarding potential fiscal policies of the new US presidential administration

and their impact on CRE and capital flows.Looking Ahead…

Ø We expect the economy to continue growing despite the array of headwinds it faces, as the labor market remains healthy and continued wage growth serves to fuel the consumer and housing.

Macro Overview: Consumer and Labor Market Driving US Economy

With Favorable Labor Market Conditions, the Consumer Continues to Propel US Growth

Unemployment LowJob Growth Healthy

Sources: BLS, Ten-X Maximus Research

Various Wage Growth Measures Accelerating

Accelerating Wage Growth Lifting More Households, Supporting Spending

ECI Growth Stronger

Atlanta Fed’s Wage Growth Measure Is Climbing

Sources: BLS, BEA, Atlanta Fed, Current Population Survey, Ten-X Maximus Research

Average Hourly Earnings Picking Up

Single-Family Market Improving

Low Inventories Constraining Further Sales Growth and Leading to Quicker Price Increases

Homes Sales Are Grinding Higher Housing Prices Are at Pre-Recession Levels

Sources: Census, NAR, HUD, FHFA, IHS, Ten-X Maximus Research

Healthy Labor Market Translating into Higher Spending

Consumer Confidence Spiked to Close 2016 and Remains Elevated

Consumer Confidence Jumped to Highest Level Since 2001 Recently

Consumer Spending at All-Time High

Sources: BEA, Conference Board, Census, Ten-X Maximus Research

Uncertainty Calmed Briefly After US Presidential Election

However it Began Rising Again to Start 2017 as Uncertainty Swirls Around the New Presidential Administration

Sources: Steven Davis, Scott Baker and Nicholas Bloom, Ten-X Maximus Research

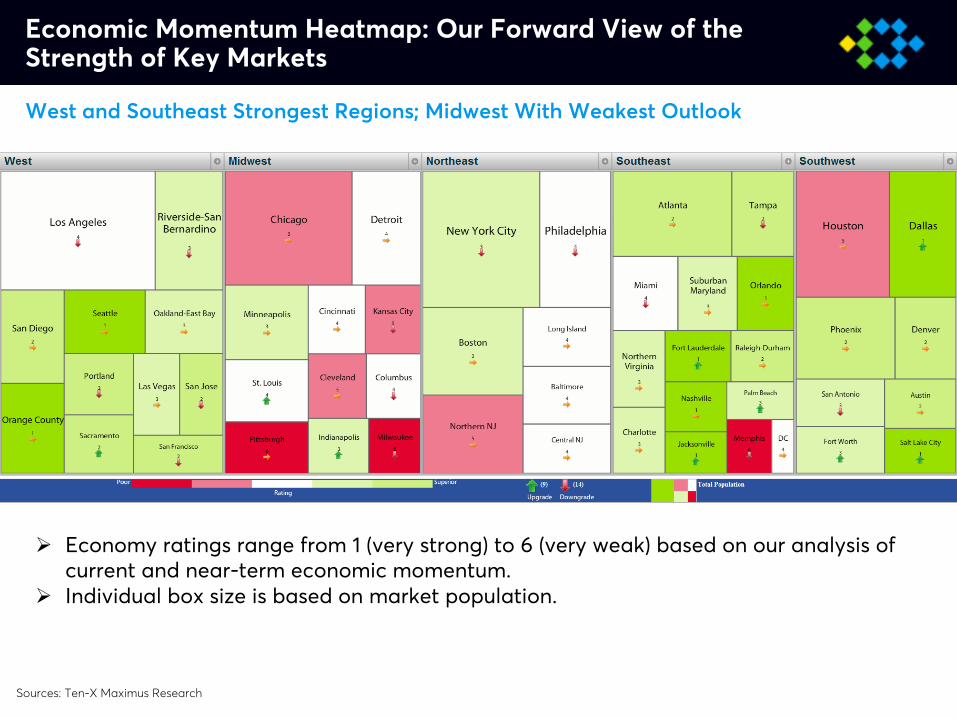

Economic Momentum Heatmap: Our Forward View of the Strength of Key Markets

West and Southeast Strongest Regions; Midwest With Weakest Outlook

Sources: Ten-X Maximus Research

Ø Economy ratings range from 1 (very strong) to 6 (very weak) based on our analysis of current and near-term economic momentum.

Ø Individual box size is based on market population.

Capital Markets Overview

US CRE Deal Volume Steadily Rising of Late

Nevertheless Fourth Quarter Volume Down a Substantial 20% from 2015’s Yearend Surge

Ø Deal volume across all asset classes measured around $134 billion in the fourth quarter.

Sources: RCA, Ten-X Maximus Research

Ten-X January CRE Nowcasts

All Property Nowcast Started Off 2017 With a Whimper

Sources: Situs/RERC, Google, Ten-X Maximus Research

Ø The All Property Nowcast failed to grow on a monthly basis in January for the first time since early 2016, though remains up 8.1% from a year ago.

CRE Segments

Apartment Segment

Supply risk in the immediate term in some markets with NOI growth being driven by rent gains. Great long-term prospects remain largely due to shifting

millennial lifestyles.

Homeownership Dropped to 51-Year Low Last Year

Sources: Census, Ten-X Maximus Research

Homeownership Ticking Up from 51-Year Trough, but Still Very Low

Strong Apartment Demand Dynamics Continue to Prevail

Household Formations Dropped Recently, but Remain Sound

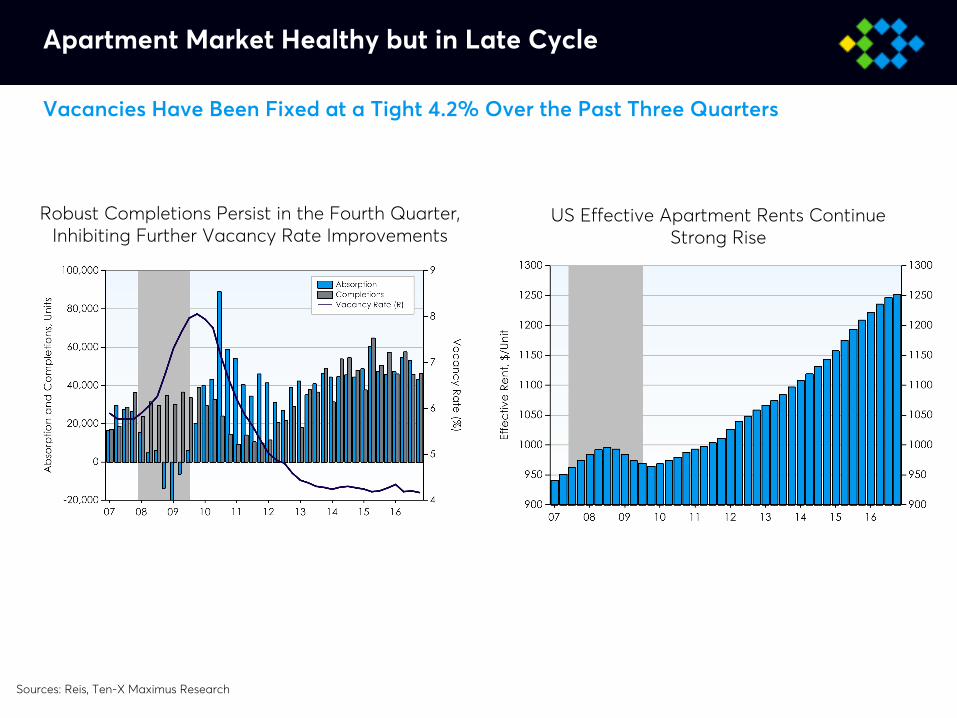

Apartment Market Healthy but in Late Cycle

Vacancies Have Been Fixed at a Tight 4.2% Over the Past Three Quarters

Robust Completions Persist in the Fourth Quarter, Inhibiting Further Vacancy Rate Improvements

US Effective Apartment Rents Continue Strong Rise

Sources: Reis, Ten-X Maximus Research

Millennials Slowly Beginning to Feed into Apartment Demand

Falling Youth Unemployment Helping to Generate Household Formations

Sources: Census, BLS, Ten-X Maximus Research

Young Adults’ Economic Standing Is Improving, Evidenced by Declining Unemployment RatesMillennials Are Now the Largest US Age Cohort

Other Factors:Ø High student debt loadØ Post housing bust fear of owningØ Later marriage ages

Ø More single-headed householdsØ Preference for urban living

Still, Many Millennials Living at Home Represent Pent-Up Demand

High Student Debt Has Lead to a New Generation of “Boomerangs” Moving Back Home

Sources: National Vital Statistics Report, BLS, Ten-X Research

…Leading to Nearly One-Third of 18-34 Year Olds Living With Their Parents

Student Loan Obligations Continue Rising, Up 6.5% from a Year Ago…

Deteriorating 1-Family Affordability Favors Renting

Rising Home Prices Could Favor Ongoing Healthy Apartment Demand

Sources: NAR, The Economist, OECD, Standard & Poor's, FHFA, Census, IHS, Reis, Ten-X Maximus Research

Higher Home Prices Have Tempered Affordability Despite Rising Home Prices, 1-Family Still Maintaining Affordability Relative to Apartment

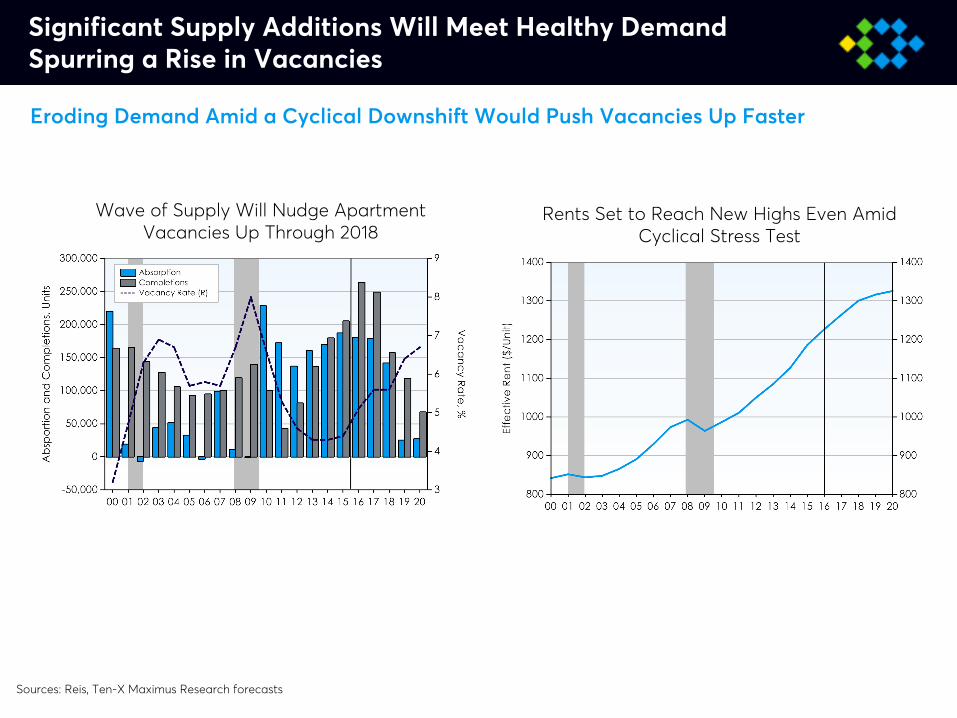

Significant Supply Additions Will Meet Healthy Demand Spurring a Rise in Vacancies

Eroding Demand Amid a Cyclical Downshift Would Push Vacancies Up Faster

Wave of Supply Will Nudge Apartment Vacancies Up Through 2018

Rents Set to Reach New Highs Even Amid Cyclical Stress Test

Sources: Reis, Ten-X Maximus Research forecasts

Overall Tint Continues to Fade as Apartment Sector Enters Later Cycle Phase

Ø Our forward view of segment fundamentals on scale of 1/dark green (very strong) to 6/dark red (very weak).

Ø Individual box size is based on market apartment inventory.

Sources: Ten-X Maximus Research

Some Key Markets Face Massive Influxes of New Supply

Office Segment

Tepid macro recovery masks subsurface market bifurcations. Hot (generally tech driven) markets outperforming markets barely out of downturn.

Headwinds from shrinking space per worker persist.

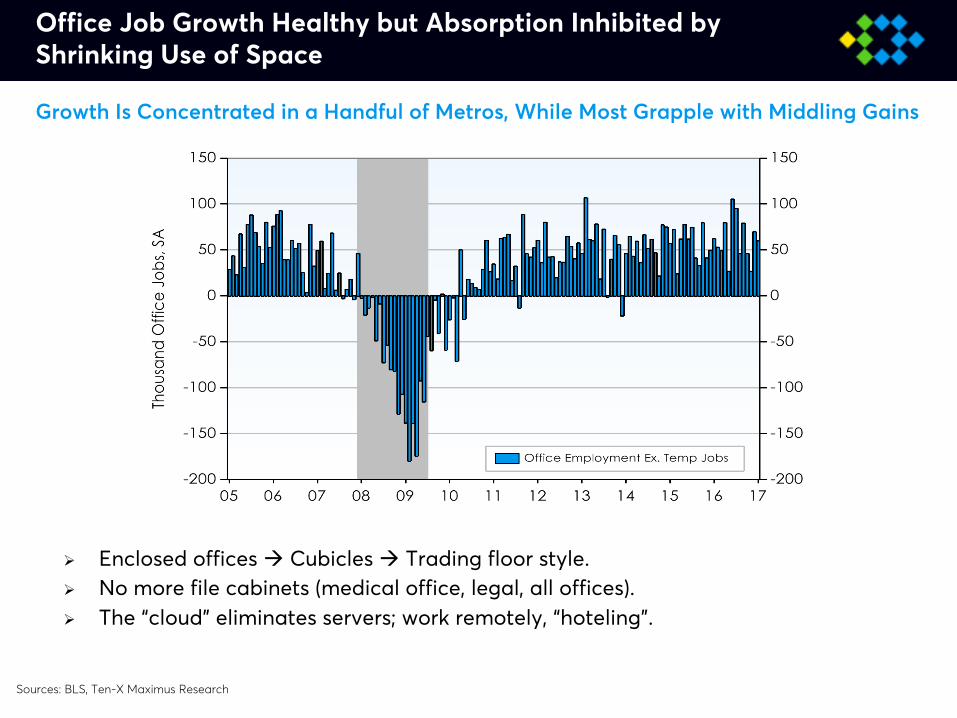

Office Job Growth Healthy but Absorption Inhibited by Shrinking Use of Space

Growth Is Concentrated in a Handful of Metros, While Most Grapple with Middling Gains

Sources: BLS, Ten-X Maximus Research

Ø Enclosed offices à Cubicles à Trading floor style.Ø No more file cabinets (medical office, legal, all offices).Ø The “cloud” eliminates servers; work remotely, “hoteling”.

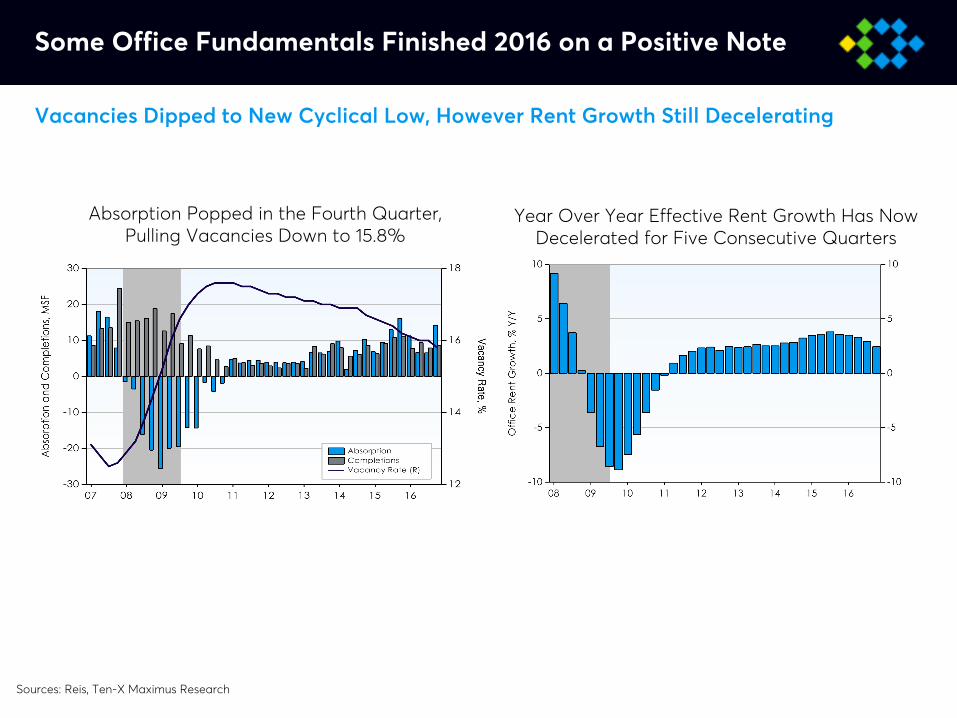

Some Office Fundamentals Finished 2016 on a Positive Note

Vacancies Dipped to New Cyclical Low, However Rent Growth Still Decelerating

Absorption Popped in the Fourth Quarter, Pulling Vacancies Down to 15.8%

Sources: Reis, Ten-X Maximus Research

Year Over Year Effective Rent Growth Has Now Decelerated for Five Consecutive Quarters

Office Fundamentals Will Continue Gradual Improvement

Risk of Economic Down Cycle Increases as the Business Cycle Ages

Vacancies Will Decline into the Low-15% Range Before Jumping Amid 2019/2020 Stress Test

Falling Availability Will Drive Effective Rents to Further Peaks Through 2018

Sources: Reis, Ten-X Maximus Research forecasts

Office Trending Toward CBD Assets and Urban Environments

The Preference Toward CBD Office Space Continues

Sources: RCA, Ten-X Maximus Research

Ø The “reverse donut” effect has been taking place across the country as an influx of college-educated millennials drive the revitalization of the urban core.

Regional Divergence in Office Market Outlooks

Sources: Ten-X Maximus Research

Ø Our forward view of segment fundamentals on scale of 1/dark green (very strong) to 6/dark red (very weak).

Ø Individual box size based on market office inventory.

West Coast Leads Pack; Midwest and Oil-Exposed Metros Look to Struggle Most

Retail Segment

Bricks & mortar getting eaten alive by e-retail as store footprints shrink or stores close. Problem markets reflect demand issues, not development pressures.

Urban/storefront the focus of investors.

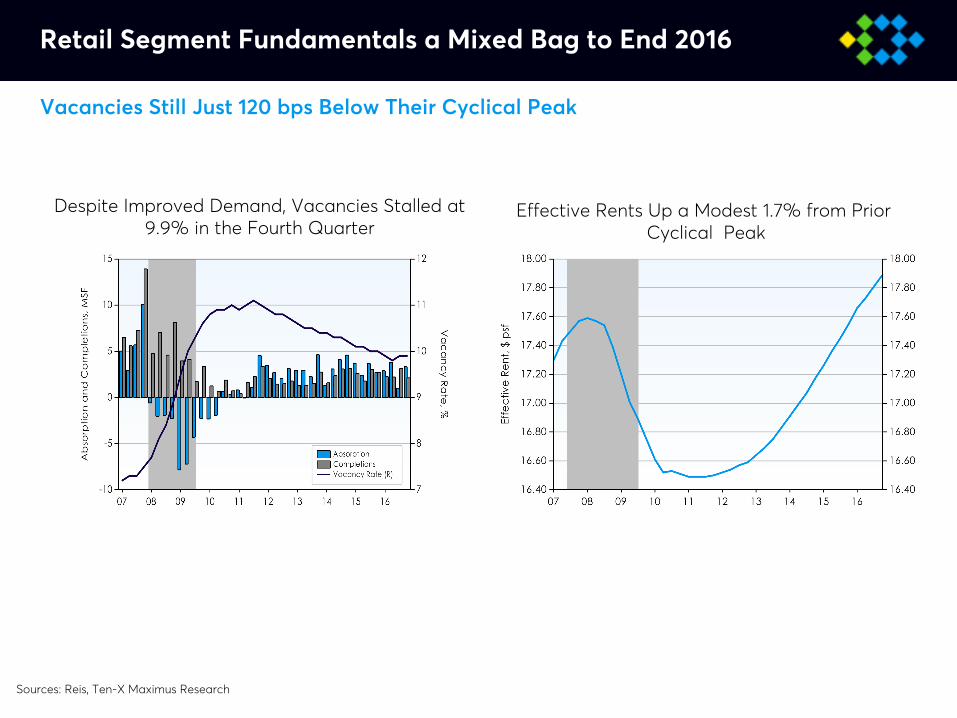

Retail Segment Fundamentals a Mixed Bag to End 2016

Effective Rents Up a Modest 1.7% from PriorCyclical Peak

Sources: Reis, Ten-X Maximus Research

Vacancies Still Just 120 bps Below Their Cyclical Peak

Despite Improved Demand, Vacancies Stalled at 9.9% in the Fourth Quarter

E-Retail Share of Total Retail Sales Continues Secular Rise

E-Retail Sales Growth Above an Impressive 13% Year Over Year

E-Retail Now Comprises 13.6% of Total Retail Sales

Bricks & Mortar Retail Sales Growing at a Substantially Slower Pace Than E-Retail

Retail Space Per Person Still Shrinking

Sources: Census, Reis, Ten-X Maximus Research

As Macroeconomy Improves the Retail Recovery Will Pick Up, However Battle With E-Retail Will Curb Gains

Stronger Demand Amid Subdued Completions Will Drive Recovery, but Any Cyclical Downshift Would Sap Demand

Sources: Reis, Ten-X Maximus Research forecasts

Retail Vacancies Will Decline Gradually to 9.3% by 2018, Before Snapping Upward Amid Stress Test Effective Rents Will Continue to Rise

Retail Investors Turning Toward Premium Assets and Urban Environments

Urbanization Is Leaving Lower-Quality Suburban Assets Behind

Sources: RCA, Ten-X Maximus Research

Urban/Storefront Cap Rates Compressing Notably More than Malls and Big Box

Urban/Storefront Retail Deal Volume Has Been Much Higher than Ever Before

Ø Retail is trending toward urbanization with demographics, especially younger consumers.

Ø Prospects for malls and strip centers has dampened, major anchor tenants facing severe trouble, with problems set to continue in 2017.

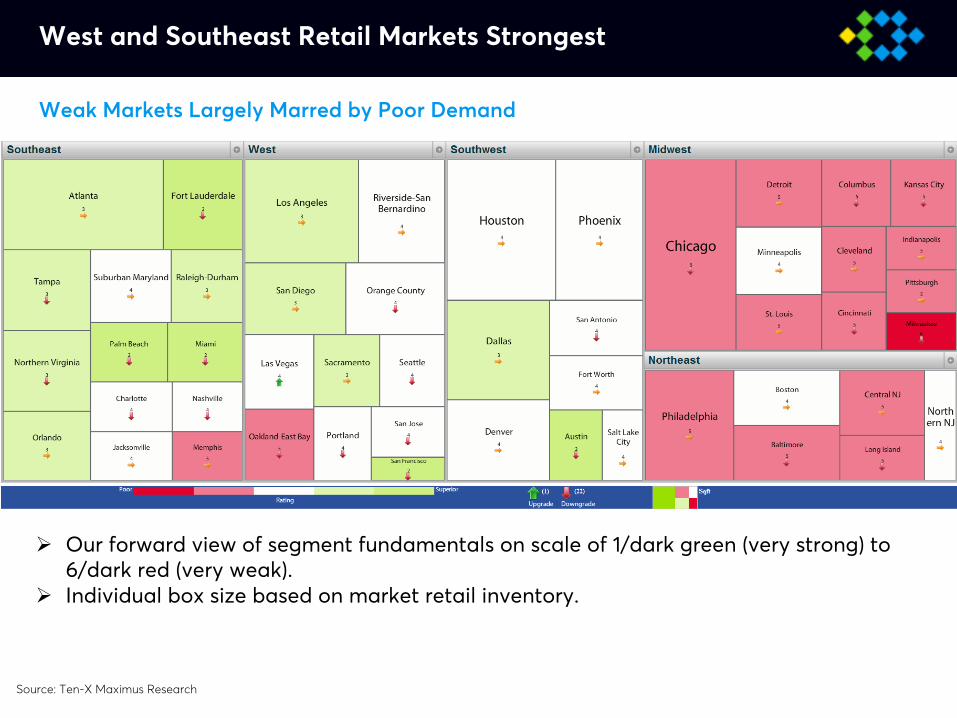

West and Southeast Retail Markets Strongest

Source: Ten-X Maximus Research

Ø Our forward view of segment fundamentals on scale of 1/dark green (very strong) to 6/dark red (very weak).

Ø Individual box size based on market retail inventory.

Weak Markets Largely Marred by Poor Demand

Industrial Segment

Withstanding onslaught from lower world trade and oil downturn with demand driven by the rise of e-commerce distribution centers and server farms

for cloud computing. Supply not a major threat yet.

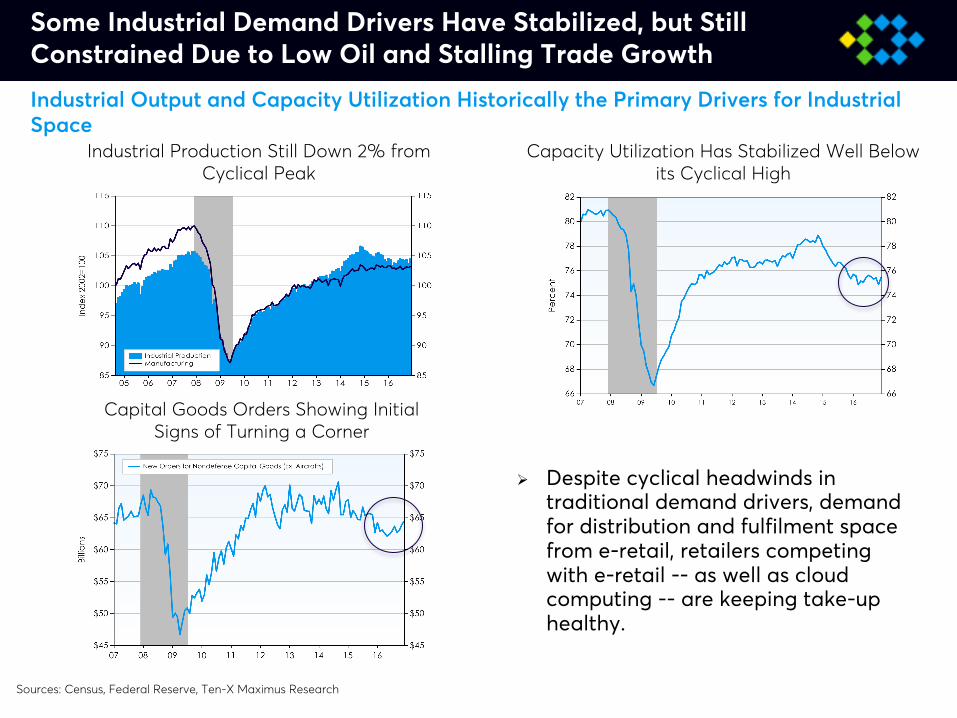

Some Industrial Demand Drivers Have Stabilized, but Still Constrained Due to Low Oil and Stalling Trade Growth

Capacity Utilization Has Stabilized Well Below its Cyclical High

Sources: Census, Federal Reserve, Ten-X Maximus Research

Industrial Output and Capacity Utilization Historically the Primary Drivers for Industrial Space

Industrial Production Still Down 2% from Cyclical Peak

Ø Despite cyclical headwinds in traditional demand drivers, demand for distribution and fulfilment space from e-retail, retailers competing with e-retail -- as well as cloud computing -- are keeping take-up healthy.

Capital Goods Orders Showing Initial Signs of Turning a Corner

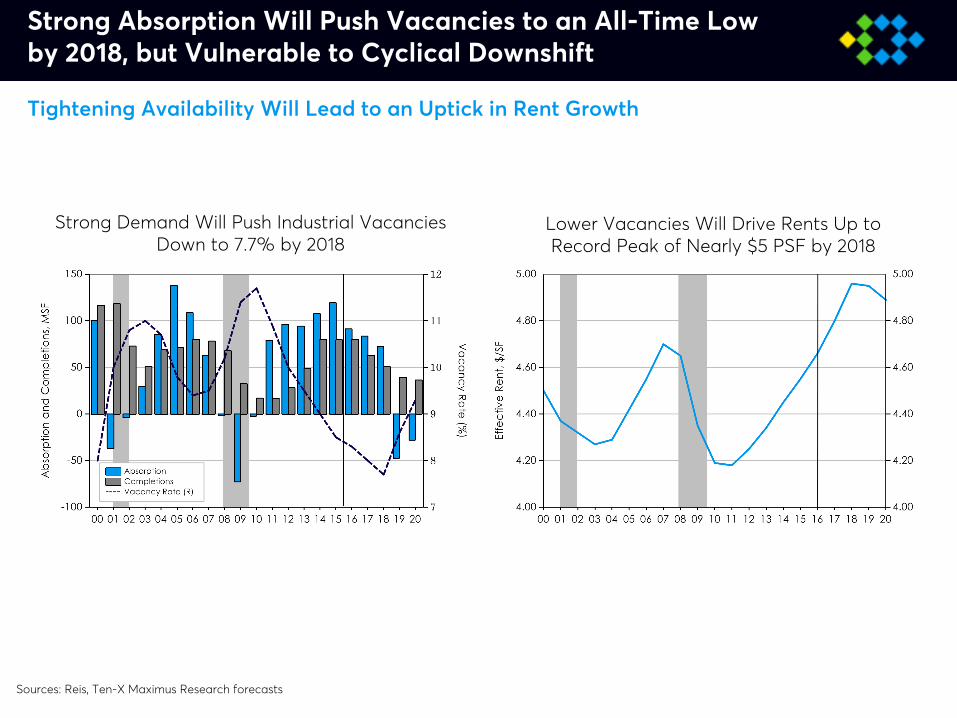

Strong Absorption Will Push Vacancies to an All-Time Low by 2018, but Vulnerable to Cyclical Downshift

Strong Demand Will Push Industrial Vacancies Down to 7.7% by 2018

Lower Vacancies Will Drive Rents Up to Record Peak of Nearly $5 PSF by 2018

Sources: Reis, Ten-X Maximus Research forecasts

Tightening Availability Will Lead to an Uptick in Rent Growth

Except for Few Outliers, Most Industrial Markets Maintain Solid Outlook

Largest Industrial Markets Still Healthy; Weakness Concentrated in the Southwest

Ø Our forward view of segment fundamentals on scale of 1/dark green (very strong) to 6/dark red (very weak).

Ø Individual box size based on market industrial inventory.

Source: Ten-X Maximus Research

Hospitality Segment

Supply and demand curves now tightly wound. Large markets most problematic ($, weak global economy,

supply). Airbnb is bigger threat than admitted (implicit supply, pricing power, business travel is next).

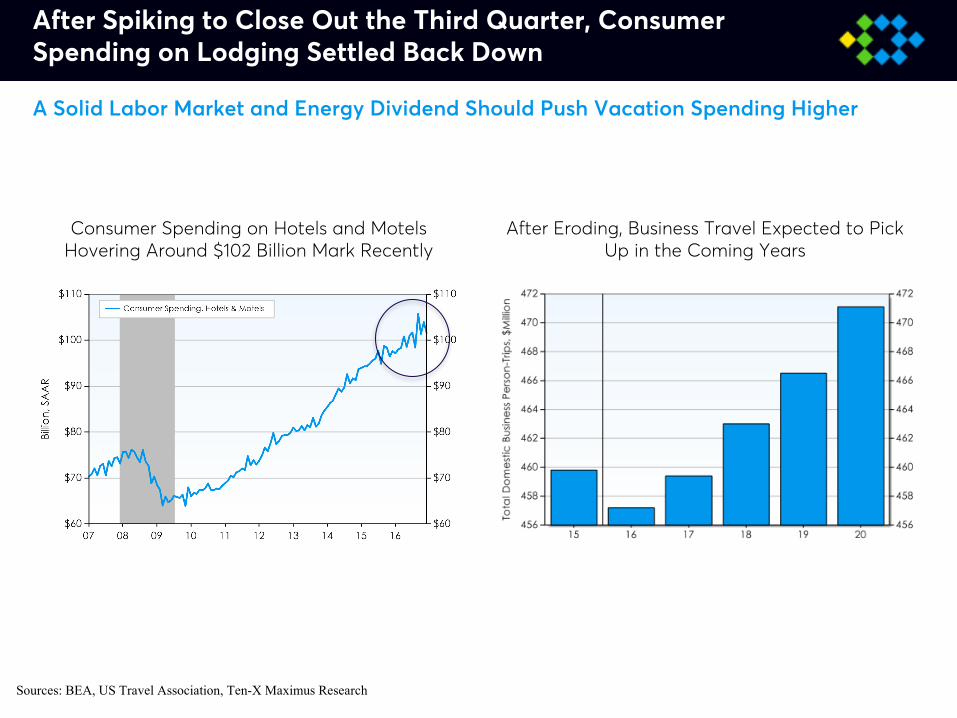

After Spiking to Close Out the Third Quarter, Consumer Spending on Lodging Settled Back Down

Consumer Spending on Hotels and Motels Hovering Around $102 Billion Mark Recently

After Eroding, Business Travel Expected to Pick Up in the Coming Years

Sources: BEA, US Travel Association, Ten-X Maximus Research

A Solid Labor Market and Energy Dividend Should Push Vacation Spending Higher

Despite the Latest Recovery, Foreign Travel in the US Will Face Headwinds Moving Forward Spurred by Brexit

Sources: ITA, Federal Reserve, Ten-X Maximus Research

Stronger Dollar Will Dovetail With Fragile Foreign Economies to Curb Growth

After Recent Rise, Foreign Travel Spending in the US Is Stabilizing

Dollar Strengthening Again Post Brexit

Supply Growth Picking Up Amid Slower Demand Gains

Sources: STR, Ten-X Maximus Research

Risks Continue to Mount for the Hotel Sector

Hotel Expansion Shifting into Slower Growth Phase

Occupancies Trended Upward Among All Class Cuts to Close Out 2016

RevPAR Growth Has Stabilized in the 3% Range from a Year Ago

Sources: STR, Ten-X Maximus Research

Both Room Rates and RevPAR Continue Seeing Slower Growth

Outlook for Operating Conditions

Occupancies Will Climb at a Slower Pace Through 2018, Then Fall Sharply Amid Stress Test

After Slowing Considerably in 2016, RevPAR Growth Looks to Accelerate Modestly Through 2018

Sources: STR, Ten-X Maximus Research forecasts

A Decelerating Market Will Remain Healthy, Before Potential Cyclicality Emerges

Waning Strength of Hotel Expansion Evident as Overall Tinge Decidedly Swings Toward Red

Sources Ten-X Maximus Research

Ø Our forward view of segment fundamentals on scale of 1/dark green (very strong) to 6/dark red (very weak).

Ø Individual box size based on market hotel inventory.

Largest High Profile Markets Face Combined Threat of Traditional and Non-Traditional Supply Additions

[email protected] (212) 871-2118 www.ten-x.com

Contact Us

555 Fifth Avenue, 4th Floor, New York, NY 10017

Peter Muoio, Ph.D.

For our latest insights follow us at:www.ten-x.com/company/blog

www.ten-x.com/company/commercial/researchTwitter: @TenXResearch

Linkedin: Auction.com Research