third quarter economic report 2017 and updated economic ... · pdf file6 . continued expansion...

TRANSCRIPT

1

Third Quarter Economic Report 2017 &

Updated economic forecasts for 2017

10 November 2017

Hong Kong SAR Government

1

2

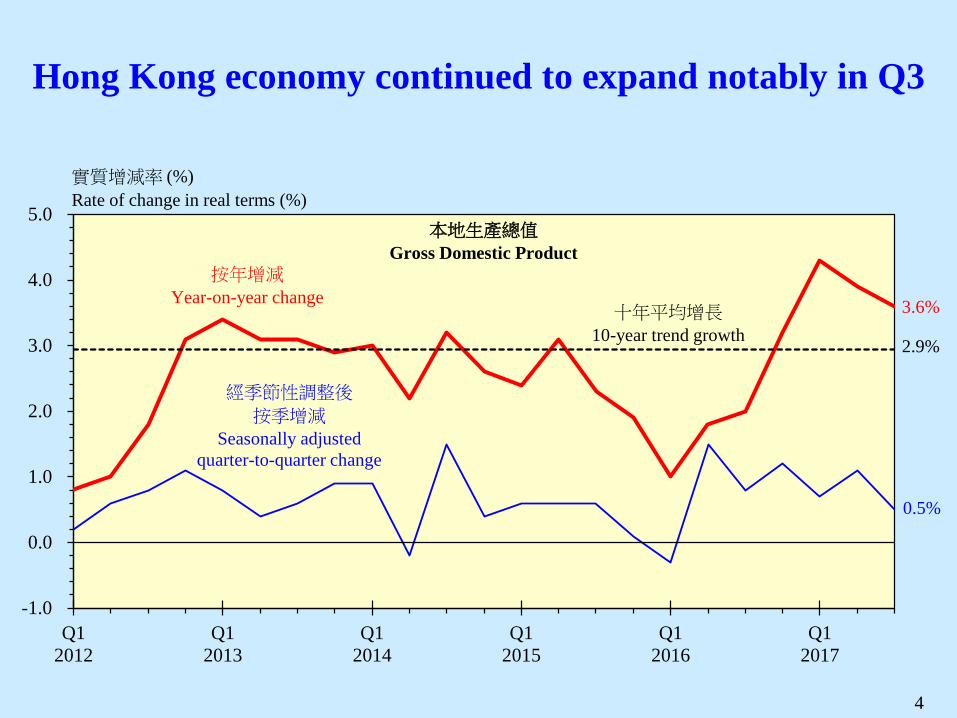

Highlights of the latest economic situation • Hong Kong’s economy continued to expand notably in Q3, by 3.6%

year-on-year

• External demand stayed vibrant, supported by the broadly benign global economic conditions

• Domestic demand stayed firm; labour market remained in a state of full employment

• Inflation pressure was largely contained

• Latest real GDP growth forecast for 2017 at 3.7%; underlying inflation rate forecast revised slightly down to 1.7%

3

Economic performance in Q3 2017

Hong Kong economy continued to expand notably in Q3

4

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

按年增減

Year-on-year change

經季節性調整後

按季增減

Seasonally adjusted quarter-to-quarter change

實質增減率 (%)Rate of change in real terms (%)

本地生產總值

Gross Domestic Product

3.6%

0.5%

十年平均增長

10-year trend growth 2.9%

5

External sector

5

6

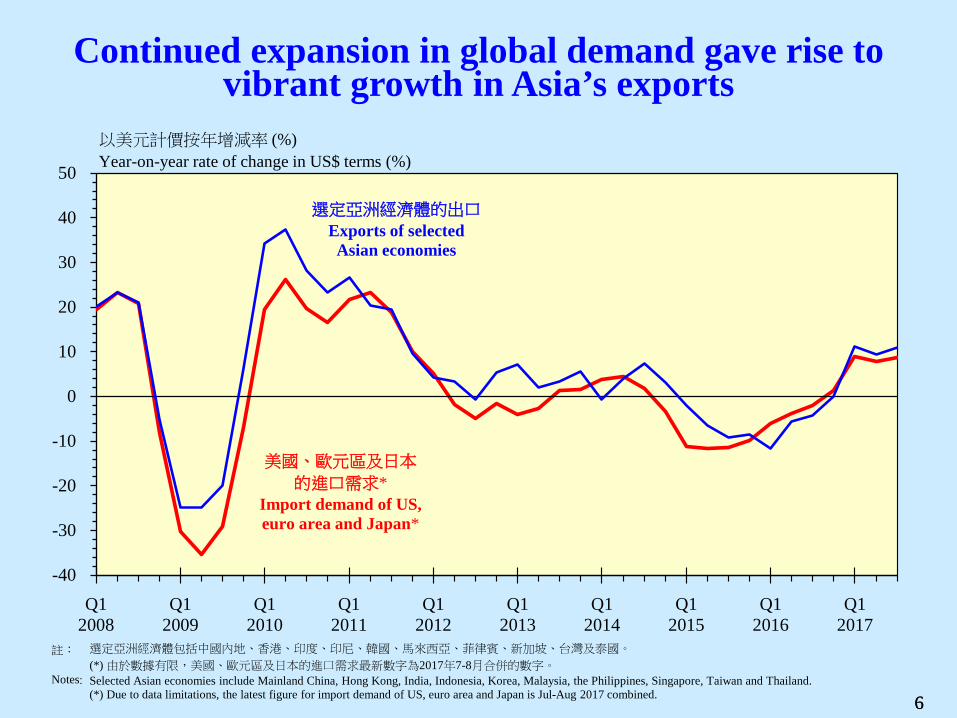

Continued expansion in global demand gave rise to vibrant growth in Asia’s exports

6

Q12008

Q12009

Q12010

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

-40

-30

-20

-10

0

10

20

30

40

50

以美元計價按年增減率 (%)Year-on-year rate of change in US$ terms (%)

美國、歐元區及日本

的進口需求*Import demand of US, euro area and Japan*

選定亞洲經濟體的出口

Exports of selected Asian economies

註:

Notes:

選定亞洲經濟體包括中國內地、香港、印度、印尼、韓國、馬來西亞、菲律賓、新加坡、台灣及泰國。

(*) 由於數據有限,美國、歐元區及日本的進口需求最新數字為2017年7-8月合併的數字。

Selected Asian economies include Mainland China, Hong Kong, India, Indonesia, Korea, Malaysia, the Philippines, Singapore, Taiwan and Thailand.(*) Due to data limitations, the latest figure for import demand of US, euro area and Japan is Jul-Aug 2017 combined.

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

-8

-6

-4

-2

0

2

4

6

8

10

12

實質增減率 (%)Rate of change in real terms (%)

貨物出口

Exports of goods

5.5%

0.7%

按年增減

Year-on-year change

經季節性調整後按季增減

Seasonally adjusted quarter-to-quarter change

7

Hong Kong’s exports of goods maintained visible growth

7

Total exports of goods by major market

Year-on-year rate of change in real terms (%)

2016 2017

Annual Q1 Q2 Q3

Mainland 2.2 9.3 3.9 6.0

U.S. -1.9 3.4 1.1 -0.5

E.U. -0.7 3.0 1.3 5.0

Japan -2.3 7.5 12.0 10.8

India 17.6 40.1 53.8 9.9

Taiwan 19.0 44.3 23.0 14.7

Korea 1.5 15.3 -2.8 -1.5

Singapore 5.9 -1.2 3.9 11.7

8

Exports of services picked up in growth

8

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

-8

-6

-4

-2

0

2

4

6

8

10服務輸出

Exports of services

實質增減率 (%)Rate of change in real terms (%)

3.7%

2.8%

按年增減

Year-on-year change

經季節性調整後按季增減

Seasonally adjusted quarter-to-quarter change

9 9

Exports of services

Year-on-year rate of change in real terms (%)

Travel

Transport

Financial services

Business and other services

2016 Annual -8.6 2.2 -3.7 -1.0

Q3 -8.1 2.5 -1.7 -1.1

Q4 -4.0 9.6 -0.2 0.2

2017 Q1 -1.1 9.2 2.4 0.9

Q2 -1.9 8.2 2.9 0.5

Q3 1.8 7.0 4.1 0.6

Exports of services saw growth in all segments; exports of travel services resumed growth

10

Domestic sector

10

11

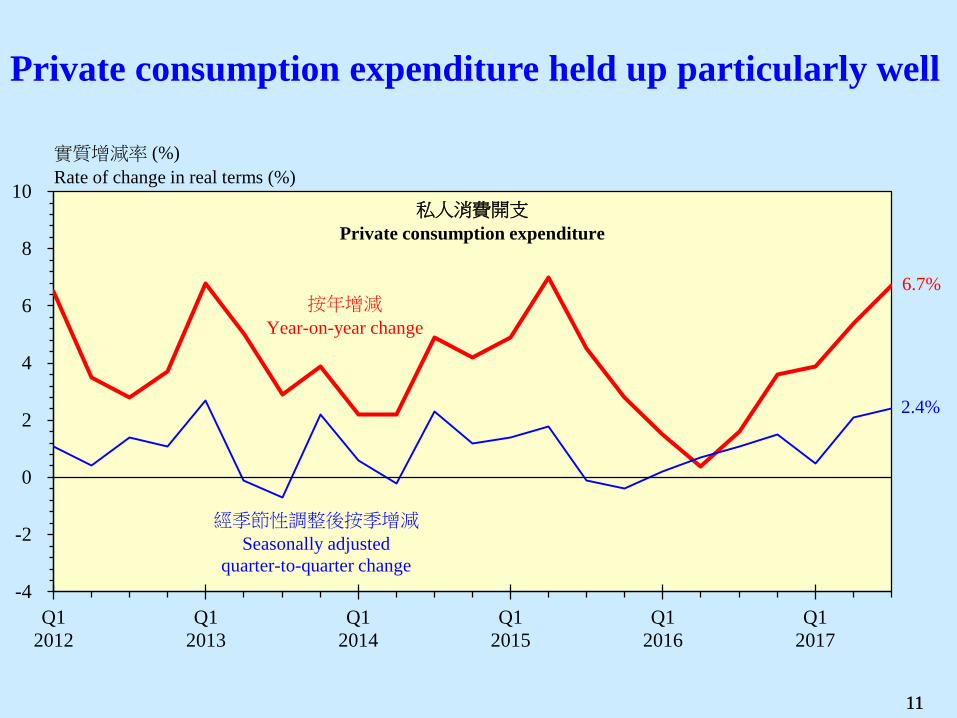

Private consumption expenditure held up particularly well

11

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

-4

-2

0

2

4

6

8

10

實質增減率 (%)Rate of change in real terms (%)

私人消費開支

Private consumption expenditure

6.7%

2.4%

按年增減

Year-on-year change

經季節性調整後按季增減

Seasonally adjusted quarter-to-quarter change

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

-15

-10

-5

0

5

10

15

本地固定資本形成總額

Gross domestic fixedcapital formation

按年實質增減率 (%)Year-on-year rate of change in real terms (%)

本地固定資本形成總額

Gross domestic fixedcapital formation

按年實質增減率 (%)Year-on-year rate of change in real terms (%)

-1.7%

12

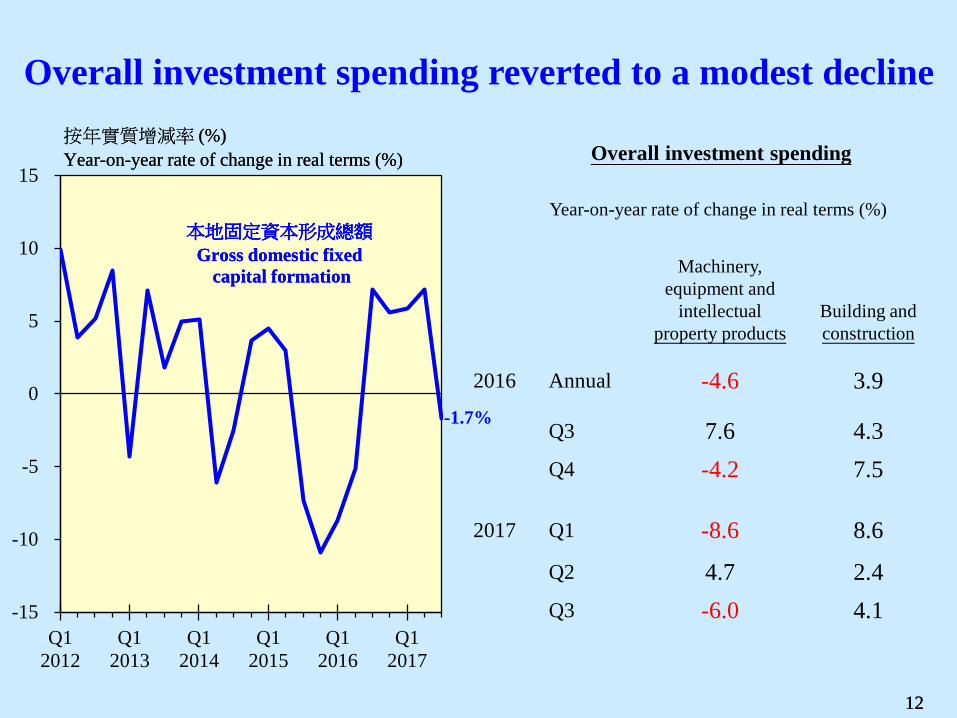

Overall investment spending reverted to a modest decline

12

Machinery,

equipment and intellectual

property products

Building and construction

2016 Annual -4.6 3.9

Q3 7.6 4.3 Q4 -4.2 7.5

2017 Q1 -8.6 8.6

Q2 4.7 2.4 Q3 -6.0 4.1

Year-on-year rate of change in real terms (%)

Overall investment spending

13

Labour market

13

14

Labour market remained in a state of full employment

註: 除整體失業率外,其他均為未經季節性調整數字。 Note: Not seasonally adjusted except the overall unemployment rate.

14

Q12000

Q12001

Q12002

Q12003

Q12004

Q12005

Q12006

Q12007

Q12008

Q12009

Q12010

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

0

2

4

6

8

10

12

較低技術勞工

Lower-skilled workers

整體

Overall

失業率 (%)Unemployment rate (%)

專業及管理員工

Professional andmanagerial staff

1.7%

3.1%3.3%

Year-on-year rate of change (%)

Nominal growth

Real growth

Index of payroll per person engaged (Q2 2017) 3.8 1.7

Wage index (June 2017) 3.8 1.5

Median monthly household income (Q3 2017) 4.9 3.1

Average monthly employment earnings of full-time employees of the lowest three decile groups (Q3 2017) 6.1 4.0

15 15

Note: (*) Excluding foreign domestic helpers.

Income*

Incomes generally sustained gains in real terms

16

Inflation

16

17

Inflation pressure was largely contained Contribution to the year-on-year rate of change in the underlying Composite Consumer Price Index (CCPI) by major component

17 註: (*) 根據以二零一四至一五年度為基期的消費物價指數新數列計算。 Note: (*) By reference to the new 2014/15-based CPI series.

1.2 1.2 1.3 1.2 1.2 1.1 1.1 1.1 1.1 1.0 1.2 1.1 1.2 0.9 0.8 0.8

0.4 0.6 0.7

1.5 1.6 1.8 1.9 1.7 1.6 1.4 1.3 1.3 1.2

1.3 1.3 1.3

1.1 0.9 0.7

0.6 0.7 0.6

3.8 3.9 4.3

4.0 3.8

3.5 3.3 3.3

2.7 2.5 2.4 2.2

2.8

2.3 2.1 2.1

1.4

2.0 1.7

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15* Q1 16* Q2 16* Q3 16* Q4 16* Q1 17* Q2 17* Q3 17*

其他

Others交通

Transport私人房屋租金

Private housing rentals食品

Food基本綜合消費物價指數

Underlying CCPI

(%)(%)

18

Property market

18

Note: Mass market flats refer to those with a saleable area of less than 70 m2, while large flats refer to those with a saleable area of at least 100 m2.

19

Residential property market transactions eased in Q3, flat prices recorded a decelerated increase

19

-4

-3

-2

-1

0

1

2

3

4

07/15 10/15 01/16 04/16 07/16 10/16 01/17 04/17 07/17

整體住宅價格

Overall flat prices

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

09/15 03/16 09/16 03/17 09/17

買賣合約數目

Agreements received

1997-2016年每月平均

1997-2016 monthly average

中小型單位價格

Mass market flat prices

大型單位價格

Large flat prices

按月升跌 (%)Monthly rate of change (%)

住宅售價

Flat prices住宅物業買賣合約數目

No. of S&P agreements for residential property

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 170

10

20

30

40

50

60

70

80

90

100

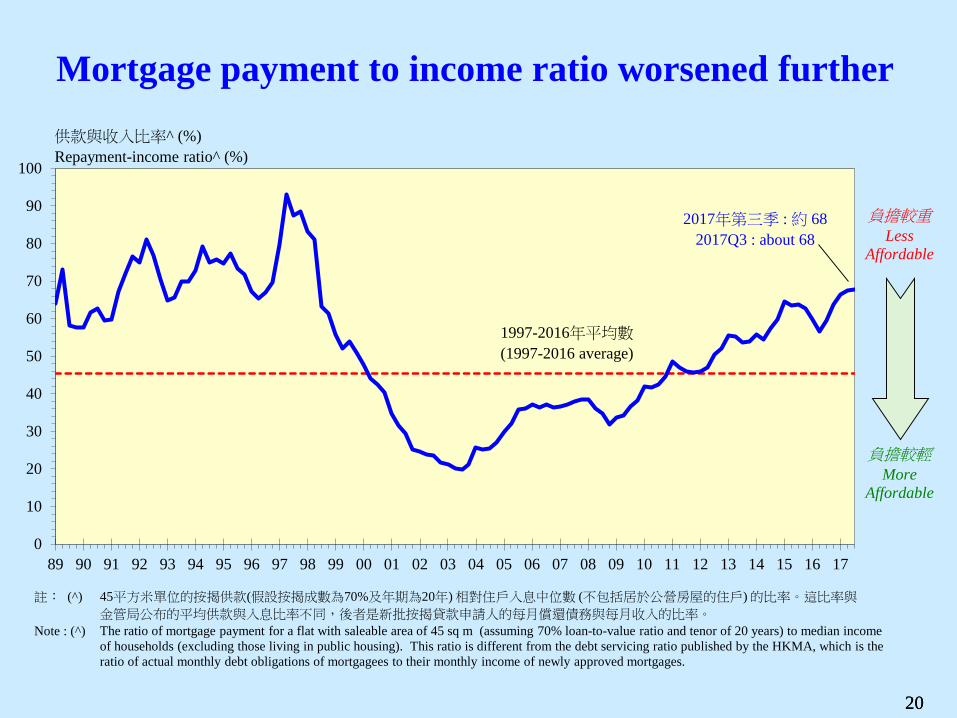

供款與收入比率^ (%)Repayment-income ratio^ (%)

1997-2016年平均數

(1997-2016 average)

45平方米單位的按揭供款(假設按揭成數為70%及年期為20年) 相對住戶入息中位數 (不包括居於公營房屋的住戶) 的比率。這比率與

金管局公布的平均供款與入息比率不同,後者是新批按揭貸款申請人的每月償還債務與每月收入的比率。

The ratio of mortgage payment for a flat with saleable area of 45 sq m (assuming 70% loan-to-value ratio and tenor of 20 years) to median incomeof households (excluding those living in public housing). This ratio is different from the debt servicing ratio published by the HKMA, which is theratio of actual monthly debt obligations of mortgagees to their monthly income of newly approved mortgages.

註︰ (^)

Note : (^)

負擔較輕More

Affordable

負擔較重Less

Affordable

2017年第三季 : 約 682017Q3 : about 68

20

Mortgage payment to income ratio worsened further

20

21

Total medium-term flat supply at a high level of 97 000

21

Q12006

Q12007

Q12008

Q12009

Q12010

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

50 000

60 000

70 000

80 000

90 000

100 000

住宅單位數目

Number of domestic units

未來三至四年可提供的私人住宅單位數目

Number of domestic units to be available in the coming three to four years

以上數字包括已落成樓宇但仍未售出的單位數目、建築中而且尚未預售的單位數目,及已批出土地並可隨時動工的項目。

運輸及房屋局。

The above figures included unsold units in completed projects, units under construction but not yet sold by presale, and units from disposed sites whereconstruction may start anytime.Transport and Housing Bureau.

註︰

資料來源:

Note :

Source :

22

Outlook for the remaining 2017

22

23

US: Solid economic growth has supported Fed to begin trimming its balance sheet

Euro area: More entrenched recovery

Japan: Recent economic data largely positive

Asia: Mainland’s economy poised to sustain medium-high speed growth; regional trading and manufacturing activities likely to remain vibrant

Global economy on track to expand further

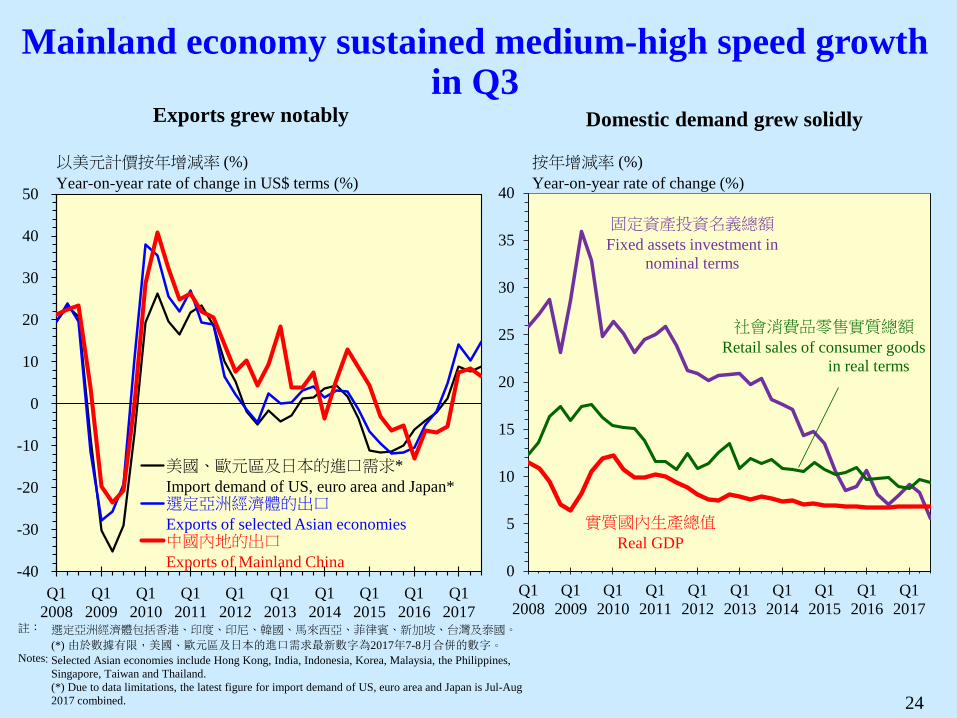

Mainland economy sustained medium-high speed growth in Q3

24

Exports grew notably Domestic demand grew solidly

Q12008

Q12009

Q12010

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

-40

-30

-20

-10

0

10

20

30

40

50

美國、歐元區及日本的進口需求* Import demand of US, euro area and Japan*選定亞洲經濟體的出口

Exports of selected Asian economies 中國內地的出口

Exports of Mainland China

以美元計價按年增減率 (%)Year-on-year rate of change in US$ terms (%)

0

5

10

15

20

25

30

35

40

Q12008

Q12009

Q12010

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

社會消費品零售實質總額

Retail sales of consumer goods in real terms

按年增減率 (%)Year-on-year rate of change (%)

固定資產投資名義總額

Fixed assets investment in nominal terms

實質國內生產總值

Real GDP

選定亞洲經濟體包括香港、印度、印尼、韓國、馬來西亞、菲律賓、新加坡、台灣及泰國。

(*) 由於數據有限,美國、歐元區及日本的進口需求最新數字為2017年7-8月合併的數字。

Selected Asian economies include Hong Kong, India, Indonesia, Korea, Malaysia, the Philippines, Singapore, Taiwan and Thailand.(*) Due to data limitations, the latest figure for import demand of US, euro area and Japan is Jul-Aug 2017 combined.

註:

Notes:

25

IMF revised up its global growth forecasts

GDP growth

in 2016

IMF forecasts for 2017 GDP growth

2017 Change between

Jul and Oct

Jul

Oct

World 3.2 3.5 3.6 0.1

U.S. 1.5 2.1 2.2 0.1

Euro area 1.8 1.9 2.1 0.2

Japan 1.0 1.3 1.5 0.2

Mainland China 6.7 6.7 6.8 0.1

Developing Asia 6.4 6.5 6.5 0.0

Emerging market and developing economies 4.3 4.6 4.6 0.0

26

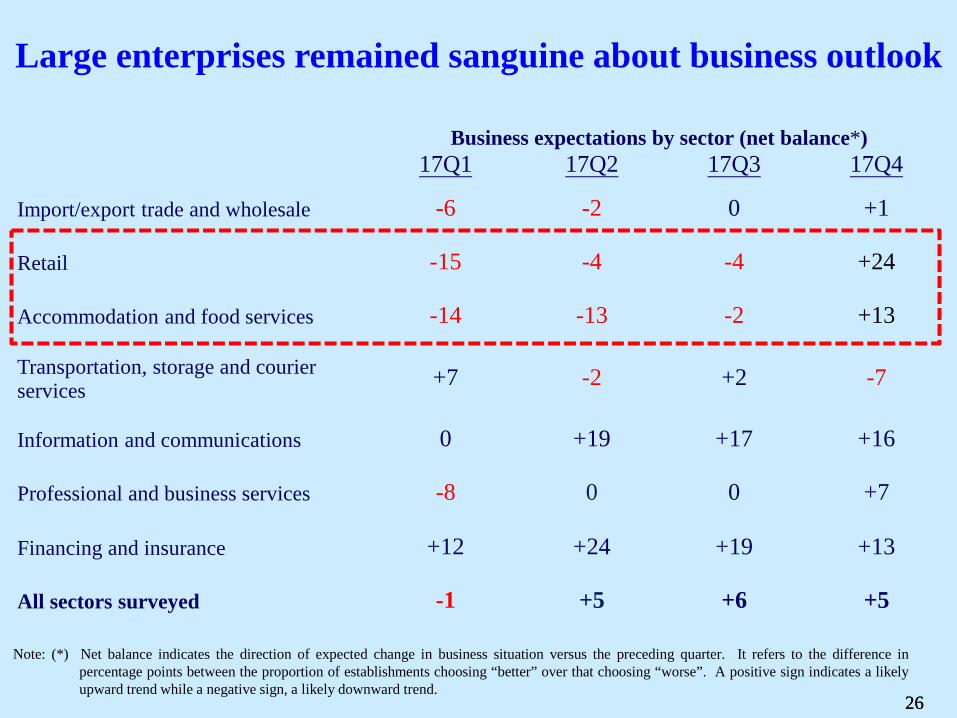

Business expectations by sector (net balance*) 17Q1 17Q2 17Q3 17Q4

Import/export trade and wholesale -6 -2 0 +1

Retail -15 -4 -4 +24

Accommodation and food services -14 -13 -2 +13

Transportation, storage and courier services +7 -2 +2 -7

Information and communications 0 +19 +17 +16

Professional and business services -8 0 0 +7

Financing and insurance +12 +24 +19 +13

All sectors surveyed -1 +5 +6 +5

Large enterprises remained sanguine about business outlook

26

Note: (*) Net balance indicates the direction of expected change in business situation versus the preceding quarter. It refers to the difference in percentage points between the proportion of establishments choosing “better” over that choosing “worse”. A positive sign indicates a likely upward trend while a negative sign, a likely downward trend.

27

Improving external environment should support our exports down the road

Domestic demand is likely to stay firm

While there remain various uncertainties in the external environment, Hong Kong economy is poised for further solid growth in the rest of this year

Upside risks to inflation remain limited

Near-term economic outlook

28

Latest economic forecasts for 2017 as a whole

Forecasts as released on 11 August

Latest

forecasts

Real GDP growth 3-4% 3.7%

Underlying inflation 1.8% 1.7%

Headline inflation 1.6% 1.5%

28

29

Third Quarter Economic Report 2017 &

Updated economic forecasts for 2017

10 November 2017

Hong Kong SAR Government

29