q. 1. define accounting explain. the accounting concepts ... · pdf filelet us discuss some...

TRANSCRIPT

1

N

2

N

3

NAttempt all the questions.Q. 1. Define Accounting Explain. the accounting concepts which guide the accountant at the recording

stage.Ans. Accounting: An Overview: Book-keeping is the recording of all financial transactions undertaken by an

individual or organisation (including a corporation or legal person). Book-keeping is “keeping records of what isbought, sold, owed, and owned; what money comes in, what goes out, and what is left.” Book-keeping is a part of theaccounting cycle, and book-keepers’ work is closely related to that of accountants.

The American Institute of Certified Public Accountants defines accounting as “the art of recording, classifyingand summarising in a significant manner and in terms of money transactions and events, which are, in part at least,of a financial character, and interpreting the results thereof.” A business house must necessarily keep a systematicrecord of its day-to-day transactions to enable stakeholders to get a complete financial picture of the company and totake stock of its financial position on a periodic basis. Stakeholders include the company’s promoters, shareholders,creditors, employees, government and the public.

Accounting is the system a company uses to measure its financial performance by noting and classifying all thetransactions like sales, purchases, assets, and liabilities in a manner that adheares to certain accepted standardformats. It helps to evaluate a company’s past performance, present condition, and future prospects.

Accountancy or Accounting is the measurement, statement, or provision of assurance about financial informationprimarily used by lenders, managers, investors, tax authorities and other decision makers to make resource allocationdecisions between and within companies, organisations, and public agencies.

Basic Accounting Concepts: The two fundamental accounting concepts which were developed centuries ago,but remain central to the accounting process are:

1 The Accounting Equation2 Double-entry Book-keepingNow let us discuss the accounting equation, which keeps all the business accounts in balance. We will create this

equation in steps to clarify your understanding of this concept. In order to start a business, the owner usually has toput some money down to finance the business operations. Since the owner provides this money, it is called Owner’sequity. In addition, this money is an Asset for the company. This can be represented by the equation:

Assets= Owner’s EquityIf the owner of the business were to close down this business, he would receive all its assets. Let’s say that owner

decides to accept a loan from the bank. When the business decides to accept the loan, their assets would increase bythe amount of the loan. In addition, this loan is also a Liability for the company. This can be represented by the

ASSIGNMENT SOLUTIONS GUIDE (2015-2016)

E.C.O.-2Accountancy-I

Disclaimer/Special Note: These are just the sample of the Answers/Solutions to some of the Questions given in theAssignments. These Sample Answers/Solutions are prepared by Private Teacher/Tutors/Authors for the help and guidanceof the student to get an idea of how he/she can answer the Questions given the Assignments. We do not claim 100%accuracy of these sample answers as these are based on the knowledge and capability of Private Teacher/Tutor. Sampleanswers may be seen as the Guide/Help for the reference to prepare the answers of the Questions given in the assignment.As these solutions and answers are prepared by the private teacher/tutor so the chances of error or mistake cannot bedenied. Any Omission or Error is highly regretted though every care has been taken while preparing these Sample Answers/Solutions. Please consult your own Teacher/Tutor before you prepare a Particular Answer and for up-to-date and exactinformation, data and solution. Student should must read and refer the official study material provided by the university.

4

N

equation: Assets = Liabilities + Owner’s Equity. Now the Assets of the company consist of the money invested bythe owner, (i.e. Owner’s Equity), and the loan taken from the bank, (i.e. a Liability) . The company’s liabilities areplaced before the owners’ equity because creditors have first claim on assets. If the business were to close down,after the liabilities are paid off, anything left over (assets) would belong to the owner.

The Double Entry System: As we had mentioned earlier that today’s accounting principles are based on thesystem created by an Italian Monk Luca Pacioli. He developed this system over 500 years ago. Pacioli had devisedthis method of keeping books, which is today known as the Double Entry system of accounting. He explained thatevery time a transaction took place whether it was a sale or a collection – there were two offsetting sides. The entryrequired a two-part “Give-and-take’ entry for each transaction. Here is a simple explanation of the double entrysystem. Say you took a loan from the bank for Rs. 5,000. Now if you can recall in an earlier discussion we hadmentioned that: Assets = Liabilities + Owner’s Equity.

Since the company borrowed money from the bank, the Rs. 5,000 is a liability for the company. In addition, nowthat the company has the extra Rs. 5,000, this money is an asset for the company. If we were to record this informa-tion in our accounts, we would put Rs. 5,000 in an account called Loan taken from the Bank, and Rs. 5,000 in anaccount called Cash saved in the Bank. The former account will be a Liability and the second account would be anAsset. As you can see, we created two entries. The first one is to show from where the money was received (i.e. thesource of the money). The second entry is to show where the money was sent (i.e. the destination of the moneyreceived). In a double entry accounting system, every transaction is recorded in the form of debits and credits. Evenfor the simplest double entry, transaction there will be a debit and a credit. In simpler terms, a debit is the applicationof money, and credit is the source of money. Let us discuss some examples to help you understand the concept ofdebits and credits:

Example 1: Let’s say you wrote a cheque for Rs.100 to purchase some stationery. This transaction would berecorded as a Credit of Rs.100 to the Cash in Bank Account, and a Debit of Rs.100 to the Stationary Account. In thiscase, we made a credit to the Cash in Bank, as it was the source of the money. The Stationery Account was debited,as it was the application of the money.

Example 2: Let’s say you received Rs. 200 cash for services rendered to a client. This transaction would berecorded as a Credit of Rs. 200 to the Income from Services account, and a Debit of Rs. 200 to the Cash in Bankaccount. In this case, we made a credit to the Income from Services, as it was the source of the money. The Cash in Bankaccount was debited, as it was the application of the money.

Systems of Book-Keeping: The systems of book-keeping are divided in to two namely double entry system andsingle entry system.

Double Entry System: In the 15th century an Italian Monk, Luca Pacioli, described a method of arrangingaccounts in such a way that the dual aspect (present in every account transaction) would be expressed by a debitamount and an equal and offsetting credit amount. Double Entry system is the system under which each transactionis regarded to have two fold aspects and both the aspects are recorded to obtain complete record of dealings. DoubleEntry system of book-keeping adhares to the rule that for each transaction the debit amount(s) must equal the creditamount(s). That is why this system is called Double Entry.

Advantages of Double Entry System(i) It enables to keep a complete record of business transactions.

(ii) It provides a check on the arithmetical accuracy of books of accounts based on equality of debit and credit.(iii) It gives the results of business activities either profit or loss during the accounting period.(iv) It tells the financial position of the business at a point of time. Total resources of the business, claims of

the outsiders, amount due by outsiders etc. are revealed by a statement known as Balance Sheet.(v) It makes possible comparison of the current year with those of previous years helping the owner to man-

age his business on better lines.(vi) It reduces the chances of errors creeping in the accounting records because of its equality principle.(vii) It helps to ascertain the details regarding any account easily and accurately.The process of accounting that we deal with is called the “Double Entry System of Accounting”. This is called so,

based on the dual entity concept–“Every transaction has its effect on two accounts/elements.” One another interpreta-

5

N

tion being every transaction has its effect on two Ledger Accounts i.e. it has got two entries in the ledger. This is theaccounting system that is predominantly in use in most parts of the world.

Single Entry System: Single-entry book-keeping uses only income and expense accounts, recorded primarily ina Revenue and Expense Journal. Single-entry book-keeping is adequate for many small businesses. The single-entrysystem is “a system of book-keeping in which as a rule only records of cash and of personal account are maintained”;it is always incomplete double entry varying with circumstances. Such system may be economical but it is incom-plete, unscientific and full of defects.

Q. 2. (a) Name items which are recorded at the invoice price in the Consignment Account. Give reasonsfor consigning the goods at the invoice price.

Ans. Concepts of Invoice Price: Invoice price is the amount in excess of the cost price of the goods consigned.Thus, it is the amount of profit margin above the cost price.

The consignor can transfer goods to the consignee at an inflated price instead of cost of these goods. Thereasons behind such practice could be manifold:

● The consignor does not want the consignee to know his exact cost and consequently his exact profitability;● The consignor wants to put pressure on the consignee by specifying higher cost so that he tries to extract the

maximum price for the goods consigned;● The consignor by showing increased cost and lower profitability tries to reduce the bargaining capacity of the

consignee to ask for increased commission from him etc.● Gives an idea to the consignee of the minimum price at which he can sell the goods.

Calculation of Cost Price and Invoice PriceCost price is the amount of expenses incurred in really producing the goods or making it marketable. When

certain amount of profit is charged to such cost price it is called invoice price. This can be expressed in the form ofan equation:

Invoice price = Cost Price + ProfitThus, this equation helps to find out any missing element in it.For example, when cost price of goods Rs. 100 is given and the profit Rs. 25 is also given then to calculate the

invoice price we use the above equation i.e.Invoice price= Cost Price + Profit or simply + CP + Profit

= 100 + 25= Rs. 125

In the same way when invoice price is given as Rs.250 and profit is given as Rs. 75 cost price can be calculatedas follows:

Invoice price= Cost Price + Profit250 = CP + 75CP = 250 – 75

= Rs. 175.Thus, the calculation of missing figures can be calculated even when the data is given in the form of percentage

with the help of the above said equation.Accounting for Goods Sent at Invoice Price

When goods are consigned to consignee at loaded price an adjustment needs to be made in their value so thatcorrect profit/loss on consignment can be calculated. The adjustment is needed for three aspects as they happen tobe recorded at invoice price namely:

● Goods sent on consignment,● Goods returned by the consignee to the consignor;● Stocks on consignment.The entries for rest of the aspect continue to be recorded in the same manner. Adjustments are needed in the

books of the consignor only and accounts in the books of the consignee continue to be maintained in the samemanner as before.

6

N

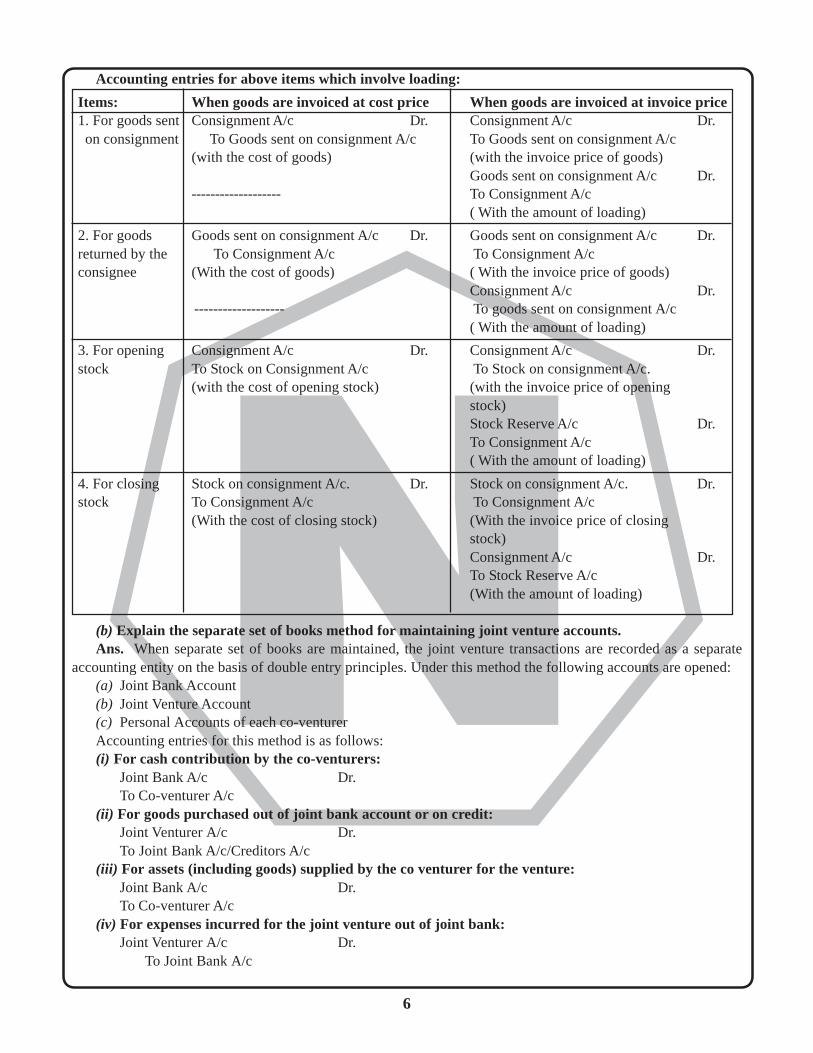

Accounting entries for above items which involve loading:

Items: When goods are invoiced at cost price When goods are invoiced at invoice price1. For goods sentConsignment A/c Dr. Consignment A/c Dr. on consignment To Goods sent on consignment A/c To Goods sent on consignment A/c

(with the cost of goods) (with the invoice price of goods)Goods sent on consignment A/c Dr.

------------------- To Consignment A/c( With the amount of loading)

2. For goods Goods sent on consignment A/c Dr. Goods sent on consignment A/c Dr.returned by the To Consignment A/c To Consignment A/cconsignee (With the cost of goods) ( With the invoice price of goods)

Consignment A/c Dr. ------------------- To goods sent on consignment A/c

( With the amount of loading)

3. For opening Consignment A/c Dr. Consignment A/c Dr.stock To Stock on Consignment A/c To Stock on consignment A/c.

(with the cost of opening stock) (with the invoice price of openingstock)Stock Reserve A/c Dr.To Consignment A/c( With the amount of loading)

4. For closing Stock on consignment A/c. Dr. Stock on consignment A/c. Dr.stock To Consignment A/c To Consignment A/c

(With the cost of closing stock) (With the invoice price of closingstock)Consignment A/c Dr.To Stock Reserve A/c(With the amount of loading)

(b) Explain the separate set of books method for maintaining joint ventur e accounts.Ans. When separate set of books are maintained, the joint venture transactions are recorded as a separate

accounting entity on the basis of double entry principles. Under this method the following accounts are opened:(a) Joint Bank Account(b) Joint Venture Account(c) Personal Accounts of each co-venturerAccounting entries for this method is as follows:(i) For cash contribution by the co-venturers:

Joint Bank A/c Dr.To Co-venturer A/c

(ii) For goods purchased out of joint bank account or on credit:Joint Venturer A/c Dr.To Joint Bank A/c/Creditors A/c

(iii) For assets (including goods) supplied by the co venturer for the venture:Joint Bank A/c Dr.To Co-venturer A/c

(iv) For expenses incurred for the joint venture out of joint bank:Joint Venturer A/c Dr. To Joint Bank A/c

7

N

(v) For expenses incurred by the co venturer:Joint Venturer A/c Dr. To Co-venturer A/c

(vi) For payment made by one co-venturer to another co-venturer:Co-Venturer A/c Dr. (Receiver) To Co-Venturer A/c (Giver)

(vii) For goods sold by joint venturer on cash or credit:Joint Bank A/c/Debtors A/c Dr.. To Joint Venturer A/c(viii) For goods sold by the co venturer and proceeds kept with him:

Co-venturer A/c Dr. To Joint Venturer A/c

(ix) For payments made to the creditors:Creditors A/c Dr. (with the amount due) To Joint Bank A/c (with payment s made) To Joint Venturer A/c (with discount received)

(x) For payment received from debtors:Joint Bank A/c Dr. (with amount received)Joint Venture A/c Dr. (with discount allowed) To Debtors A/c

(xi) For bill accepted by a co-venturer for the mutual accommodation:Bill Receivable A/c Dr. To Co-venturer a/c

(xii) For discounting of the bill:Joint bank A/c Dr. (with the amount received)Joint Venture A/c Dr. (with discounting charges) To Bills Receivable Account (with the amount of the bill)

(xiii) For assets (including goods) taken over by the co-venturer:Co-venturer A/c Dr To Joint Venturer A/c

Q. 3. What is meant by single entry system? Distinguish it from Double Entry System. Explain the twomethods of ascertaining profile when accounting records are incomplete.

Ans. What is Single Entry System: Two common book-keeping methods used by businesses and other organi-zations are the single-entry book-keeping system and the double-entry book-keeping system. Single-entry book-keeping uses only income and expense accounts, recorded primarily in a Revenue and Expense Journal. Single-entrybook-keeping is adequate for many small businesses. Double-entry book-keeping requires posting (recording) eachtransaction twice, using debits and credits.

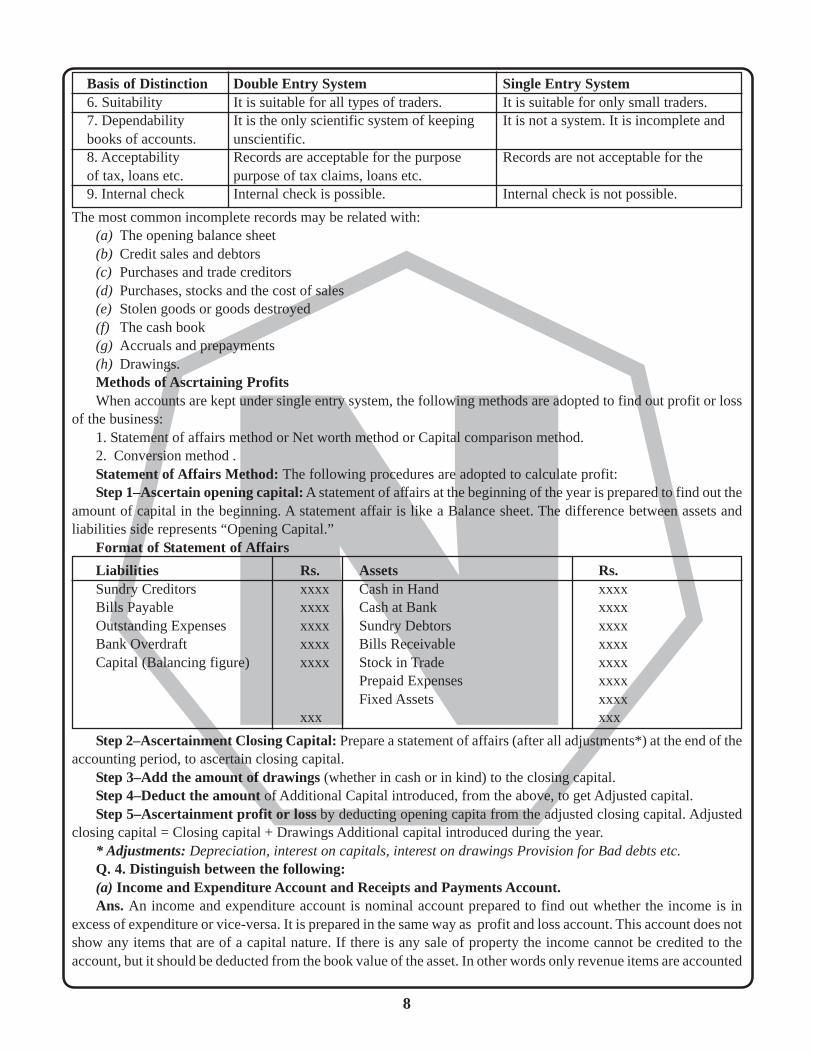

Dif ference between Double Entry System and Single Entry System:Basis of Distinction Double Entry System Single Entry System1. Principle For every debit there is a corresponding Debit and credits do not agree.credit and vice versa.2. Recording of Debit and credit aspects of all transactionsDebit and credit aspects of all transactionstransaction are recorded. are not recorded.3. Nature of accounts Maintains complete record of personal, An incomplete record. Only personalmaintained real and nominal accounts. and cash accounts are maintained.4. Trial Balance Arithmetical accuracy of the records can beTrial Balance cannot be prepared.checked by preparing a Trial Balance.5. Determination of A Profit and Loss Account and Balance A Profit & Loss Account and Balanceprofit or loss and Sheet can be conveniently prepared since Sheet cannot be conveniently preparedfinancial position the book of accounts present a complete since the accounting records arepicture. incomplete.

8

N

Basis of Distinction Double Entry System Single Entry System6. Suitability It is suitable for all types of traders. It is suitable for only small traders.7. Dependability It is the only scientific system of keeping It is not a system. It is incomplete andbooks of accounts. unscientific.8. Acceptability Records are acceptable for the purpose Records are not acceptable for theof tax, loans etc. purpose of tax claims, loans etc.9. Internal check Internal check is possible. Internal check is not possible.

The most common incomplete records may be related with:(a) The opening balance sheet(b) Credit sales and debtors(c) Purchases and trade creditors(d) Purchases, stocks and the cost of sales(e) Stolen goods or goods destroyed(f) The cash book(g) Accruals and prepayments(h) Drawings.Methods of Ascrtaining ProfitsWhen accounts are kept under single entry system, the following methods are adopted to find out profit or loss

of the business:1. Statement of affairs method or Net worth method or Capital comparison method.2. Conversion method .Statement of Af fairs Method: The following procedures are adopted to calculate profit:Step 1–Ascertain opening capital: A statement of affairs at the beginning of the year is prepared to find out the

amount of capital in the beginning. A statement affair is like a Balance sheet. The difference between assets andliabilities side represents “Opening Capital.”

Format of Statement of Af fairs

Liabilities Rs. Assets Rs.Sundry Creditors xxxx Cash in Hand xxxxBills Payable xxxx Cash at Bank xxxxOutstanding Expenses xxxx Sundry Debtors xxxxBank Overdraft xxxx Bills Receivable xxxxCapital (Balancing figure) xxxx Stock in Trade xxxx

Prepaid Expenses xxxxFixed Assets xxxx

xxx xxx

Step 2–Ascertainment Closing Capital: Prepare a statement of affairs (after all adjustments*) at the end of theaccounting period, to ascertain closing capital.

Step 3–Add the amount of drawings (whether in cash or in kind) to the closing capital.Step 4–Deduct the amount of Additional Capital introduced, from the above, to get Adjusted capital.Step 5–Ascertainment profit or loss by deducting opening capita from the adjusted closing capital. Adjusted

closing capital = Closing capital + Drawings Additional capital introduced during the year.* Adjustments: Depreciation, interest on capitals, interest on drawings Provision for Bad debts etc.Q. 4. Distinguish between the following:(a) Income and Expenditure Account and Receipts and Payments Account.Ans. An income and expenditure account is nominal account prepared to find out whether the income is in

excess of expenditure or vice-versa. It is prepared in the same way as profit and loss account. This account does notshow any items that are of a capital nature. If there is any sale of property the income cannot be credited to theaccount, but it should be deducted from the book value of the asset. In other words only revenue items are accounted

9

N

for here. It shows details only for the relevant period. No transactions relating to the previous period or the nextperiod can be shown. This applies to both revenue and expenditure items.

Receipts and Income & ExpenditurePayments Account Account

Receipts are shown on Expenses are shown ondebit side and payment debit side and Incomesshown on credit side. are shown on credit side.Starts with the opening It has no opening balance.balance of cash in handand at bank.

Only cash transactions Other transactions alsotakes place. takes place.

Capital as well as Only revenue itemsrevenue items appear. appear.

The difference of two The difference betweensides is the cash in hand the two is either surplus orand at bank at the end deficit for the period.of the periods.

All receipts and payments Only those expensesare shown irrespective and incomes are shownof the year to which they which related to therelate. period for which the

account is prepared.

(b) Straight line method and diminishing balance method of depreciation.Ans. Straight-Line: This method is the simplest of the three. It takes the original cost of the asset less its

expected salvage value (see above for the definition) and divides it by the number of years in its expected usefullife. In the above example of the truck, if you purchased it for Rs. 27,000, the depreciable value would beRs. 27,000 – Rs.7,500, or $19,500. This amount would be divided by the useful life of five years to come to anannual depreciation amount of Rs. 3,900. Every year, you would take a Rs.3,900 expense on your income statementto reflect the depreciation on the truck.

Declining Balance: This method, as well as the sum-of-the-years-digits, is called an accelerated depreciationmethod because, by nature of its calculation, it allows more depreciation in earlier years and less in later years.

The declining balance method (sometimes called the double declining balance method, but meaning the samething) applies a constant percentage to the declining book value of the asset.

Let’s go back to the truck example above. If your depreciation rate is 20 percent, the depreciation over the fiveyears that you own the truck would look like this:

Year Percentage Book value Depreciation

1 20% 27,000 5,400

2 20% 21,600 4,320

3 20% 17,280 3,456

4 20% 13,824 2,765

5 20% 11,059 2,212The book value at the end of the five years is Rs.8,847. If you sell the vehicle for Rs 7,500 at the end of the five

years, you have a loss on sale because the book value is higher than the sale price. Remember that book value has norelationship to market value. If you sold the vehicle for Rs.9,500 you would have taken too much depreciation overthe years and would have a gain on sale.

10

N

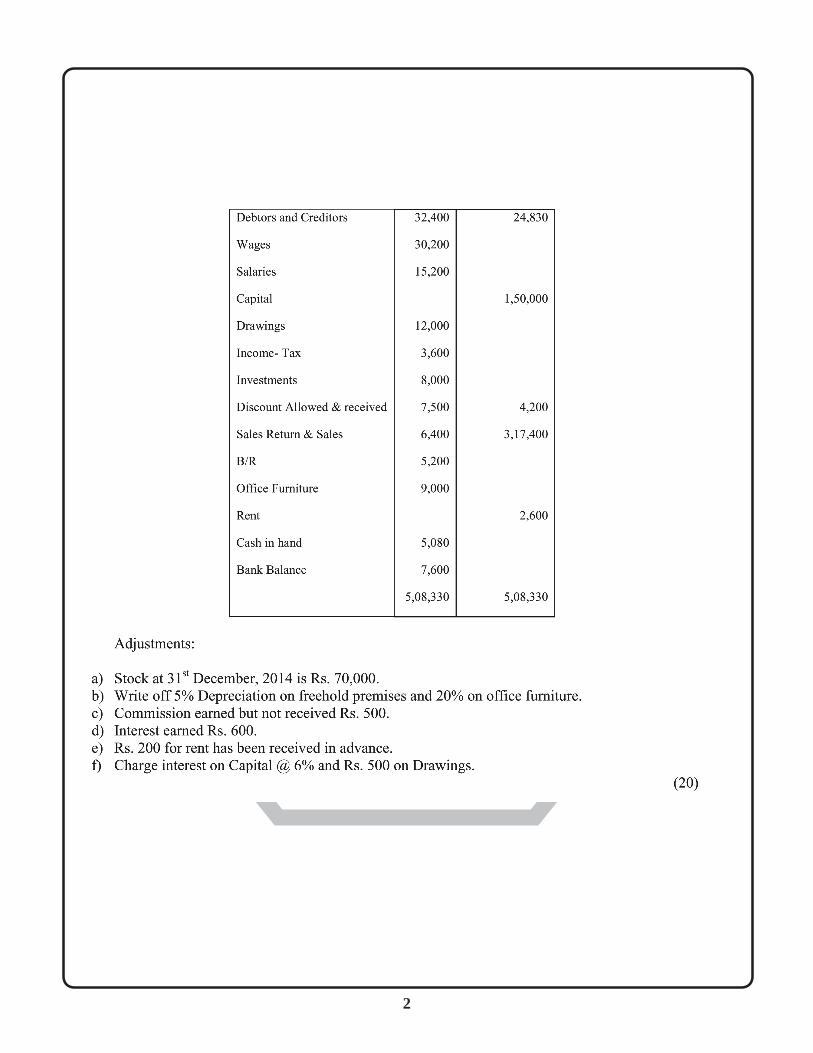

Q. 5. From the following Trial Balance prepare Trading and Profit and Loss Account for the year ended31st Dec., 2014 and Balance Sheet as on that date:

Dr. (Rs.) Cr. (Rs.)

Stock 1st Jan, 2014 22,300Purchases and Purchases 2,30,00 5,200ReturnFreehold Premises 1,00,000Incidental Trade Exp. 11,200Insurance 1,850

` Audit Fees 800Commission Received 2,700Interest 1,400Debtors and Creditors 32,400 24,830Wages 30,200Salaries 15,200Capital 1,50,000Drawings 12,000Income-Tax 3,600Investments 8,000Discount Allowed & Sales 7,500 4,200Sales Return & Sales 6,400 3,17,400B/R 5,200Office Furniture 9,000Rent 2,600Cash in hand 5,080Bank Balance 7,600

5,08,330 5,08,330

Adjustments:(a) Stock at 31st December, 2014 is Rs. 70,00.(b) Write off 5% Depreciation on freehold premises and 20% on office furnitur e.(c) Commission earned but not received Rs. 500.(d) Interest earned Rs. 600.(e) Rs. 200 for rent has been received in advance.(f) Charge interest on Capital @60% and Rs. 500 on Drawings.Ans. Trading and Profit & Loss account for the year ended 31st Dec, 2014

Particulars Amount Particulars AmountTo Opening stock 22300 By Sales 317400To Purchases 230000 Less: Sales Returns –6400 311000Less: Purchase Returns –5200 224800 By Closing Stock 70000To Wages 30200To Gross Profit C/d 103700Total 381000 Total 381000To salary 15200 By Gross Profit B/d 103700To incidental expenses 11200 By Discount Given 4200To Insurance 1850 By Rent received 2600To Audit Fees 800 Less: Received in advance –200 2400

To discount 7500 By Intrest Received 1400

11

N

Particulars Amount Particulars AmountAdd: interest earned 600 2000By Commission received 2700

To Depreciation: Add: Commission earned 500 3200

Free Hold Premises 5% 5000Furniture 20% 1800 6800To Interest of Capital 9000Less: Interest on drawings –500 8500To Income Tax 3600To Net Profit Transferred toCapital Account 60050Total 115500 Total 115500

Balance sheet as at 31st Dec,2014Liabilities Assets

Capital Account 150000Add: Net Profit 60050 Furniture 9000

Add: Interest on Capital (Net) 8500 Less: deperecation –1800 7200

Less: Drawings –12000 206550 Free Hold Premises 100000

Rent received in advance 200 Less: deperecation –5000 95000

Creditors 24830 Closing Stock 70000

Cash in hand 5080

Cash at Bank 7600

Investment 8000

Commission Receivable 500

Bills Receivable 5200

Debtors 32400

Interest Receivable 600

Total 231580 Total 231580

■ ■