public disclosure authorized taxation in decentralizing ...€¦ · taxation in decentralizing...

TRANSCRIPT

Wpof ZoPolicy Research

WORKING PAPERS

Country Operations

Country DCpartinent IAsia Regional OfHice

The World BankJanuary 1992

WPS 820

Taxation in DecentralizingSocialist Economies

The Case of China

Christopher J. Headyand

Pradeep K. Mitra

The nature and pace of tax reform in China depends on progressin price and enterprise reform, highlightinfg the need to view theproblem in a systemwide perspective.

Po!lc% Rcsearth Worrkmg I'dpcm d :sscrninate Lhc !ind;ngs .' Wrx u,; pn,grcs and wz'czragc thc c-.nange ,! dcas flnElg 13Hank iaff a:rJab] oLhers %nwc%sacd m dcshcoim]d *s.cs i hesedp apcrs d 5 h 4g c t±.h ReIca r. e\s sor S:,' carr Lhcndnc.rn! Le - .aho r rflc TIond Uher s es s.and sho.Md herased and crcd acordsaiozg. I hcf !zd.^gs., *:cercprc;.rrr,sanz . :oanH .0. r hC O -hor's rssr [he I x 2dn.g be aitobut,:e totheWotid Hank. Qs Hadrd ci )trsel.~.; maaKrcrn'.u c,! s.1tmc:tre!.cru.ntc.s

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Policy Research

Country Operations

WPS 820

This paper- a product of the Country Operations Division, Country Department ' Asia Regional Office-- is part of a larger Asia Region/PRE study on revenuc mobilization in China. Copies are available freefrom the World Bank, 181 8 H Street NW, Washington DC 20433. Please contact Dakshi Sebastian, roomD9-1 1, extension 8(A23 (33 pages). Januarl 1992.

Heady and Mitra analyze the tax system in * The state's role as owner of enterprises mustChina, where reforrns designed to move the be treatcd separatcly from its role as tax collec-economic svstem toward a market econom) have tor. All enterprises should pa) statutory profitsbeen occurring for more than a decade. taxes. Negotiation (of the kind that characterizes

the contract responsibility system) should beHeady and Mitra characterize the compre- confined to the payments to govemment from

hensive changes in the tax system that could be after-tax profits. Those payments could be set toundertaken in the presence of systcmwide balance incentives to enterprises with the needreform, especially of prices and entcrprises, as for the state to earm a return on assaes historicallyw,ell as of more moderate relforms that must provided free to those enterpnisec.suffice in the absence of reforms elsevwhere inthe economic system. In connection with tax 'Tle modie of analysis that Heady and Mitrareform per se, they emphasize two important develop in this paper can be applied to a widerconclusions: range of economies --- whether emerging from a

socialist past or not - that are progressing at- It is possible to simplify signiiificantly the varying speeds in ithe interlinked areas of tax

rate structure for indirect taxes in the presence of' reform, price relor-ni, antd enterprise reform.price controls, but a unitied rate for value-addedtax is undesirable without full decontrol ofprices.

The lPohic Research Working Plqer Series ii di,enntn.te the I intdi,g'\ ol ss,rk under A \ irIn the Bank An ohbecti% e of thc seriesi to gel these findings iut qui .Ki_ . even if presentations are less th.n [(Li posk hd The findinFs., iterpretations, andLonclusioris in these papers do noi neiessr,srik epre.ent ofilnii Hank pollk

Pr0dLJe(d h! die IC 011 Re wsar hi Disse iknina.t ion (enltvr

Taxation in Decentralizing Socialist Economies:The Case of China

byChristopher J. Heady

University of Bath

and

Pradeep K MitraWorld Bank

Table of Contents

1. Introduetion 1

2. Indirect Taxes 2

2.1 The Current Tax Structure 22.2 Taxes and Enterprise Profitability 82.3 Simplification of the Rate Structure 92.4 Tax Simplification 112.5 Cascading 122.6 Equity 142.7 Price Controls as Implicit Taxes 16

3. Direct Taxes 19

3.1 The System of Enterprise Income Tax 193.2 Contract Responsibility System 213.3 Problems with the Current System 233.4 Statutory and Effective Rates of Tax 243.5 Resource Tax 29

4. Conclusions 30

References 33

* The analysis of this paper was undertaken as part of a World Bank study on revenuemobilization in China. We thank Patrick Honohan and Christine Wallich for theirhelpful comments on an earlier draft.

1

i. INTRODUCTION

Scope

China has been gradually reforming its economic system towards that of amarket economy over the last ten years. That process has, inter alia,necessitated a restructuring of the system of taxation. It is the principaltask of this paper to describe the tax system, to analyze its economicconsequences and to highlight the close relationship between further taxreform and other reforms, most notably those in the price system and themanagement of State enterprises. A secondary task is to study the Chineseexperience with a view to eliciting lessons for other countries that arecurrently moving towards a free market system.

China's tax system has several features in common with those of theemerging market economies of Central and Eastern Europe. As far as indirecttaxes are concerned, the nominal burden falls on enterprises rather thanconsumers, and there are large numbers of different rates. Direct taxes arealso complex in part because they are mainly levied on e.aterprises whose closerelationship with the State makes the application of uniform tax rulesdifficult to operate but also because numerous anomalies in the tax systemintroduce significant and unfcrseen distortions in the incentives forinvestments. These characteristics of the tax system have led to difficultiesas the free market has expanded in China. The lessons from these difficultiesshould help other countries in reforming their tax systems to meet therequirements of a market economy.

Notwithstanding these similarities, the gradual nature of reform inChina means that its experience must be regarded as somewhat special whencompared to the emerging market economies of Central and Eastern Europe. Noneof the latter is characterized, for example, by the coexistence of free marketprices and controlled prices for the same goods (the "dual pricing system").For this reason a number of important policy issues raised by the dual pricingsystem and discussed in this paper are not applicable to those economies.They may however find application in a range of developing countries, whetheror not emerging from a socialist past, that are attempting to reforminterlinked systems of administered prices and taxes.

Reforms

Prior to 1978 state enterprises remitted all profits to the state.Fiscal reforms were initially aimed at improving efficiency of stateenterprises and involved the substitution of taxation for full profitremittance. A trial system of profit retention-cum-taxation was introduced forselected enterprises in Sichuan province in 1978. The experiment wassuccessful and by the end of 1980, 6,600 state-owned industrial enterprises,accounting for 16 percent of the total number of such firms but 60 percent oftheir output value and 70 percent of their profits, i.e., most large- andmedium-sized firms, were on the system. This first phase of enterprise reformculminated towards the end of 1983 with over 90 percent of profitable stateenterprises adopting profit retention.

2

The second stage of enterprise reform involved the restructuring ofindirect taxation and the creation of a dual pricing system. Up to 1983 theindirect taxation of enterprises was carried out through the ConsolidatedIndustrial and Commercial Tax (CICT) that had been introduced in 1958, andsimplified in 1972. This was a turnover tax that was applied to industrialproduction, agricultural sales, imports, retailing, transport andcommunications and services. It was replaced in 1984 by the Product Tax, VATand Business Tax. The CICT however continues to apply to foreign enterprisesand joint ventures.

Plan of the paper

Section 2, following this introduction, provides a detailed analysis ofthe structure and reform of indirect taxes in China. Section 3 of the paperis concerned with direct taxes. Section 4 concludes by drawing together themain issues and considering their implications for other de_entralizingsocialist economies in transition.

2. INDIRECT TAXES

2.1 The Current Tax Structure

As is the case with most countries, China has a very large number oftaxes but only a small number of them raise substantial revenues. Theprincipal revenue-raising instruments are indirect taxes on goods and services(Product Tax, Value Added Tax and Business Tax) and the Enterprise Income Tax,and it is on those taxes that this paper concentrates.-" The system of pricecontrols is an implicit subsidy to users, financed by an implicit tax onproducers. Hence price controls on final goods subsidize final consumers atthe expense of consumer goods-producing enterprises, while price controls onintermediate goods boost profitability in consumer goods producing enterprisesat the expense of those producing intermediate goods. Since indirect taxesmust operate within the overall framew,rk of price controls, it is desirableto view taxes and price controls as cone W-uting an integrated system. Thisperspective is more fully developed in ! tion 2.7.

Product Tax

Product tax is levied on the manufacture and import of certain goods.Goods are valued (for tax purposes) at the price paid by purchasers. Thisdiffers from normal international practice, where tax rates are expressed as apercentage of the producer price. It means that, with controlled prices, taxesreduce the revenue received by the enterprise and do not increase the pricespaid by the consumer.

V The tax system, and its evolution, are described in more detail in Eassonand Li (1987). A general analysis of its strengths and weaknesses, includingrecommendations for reform, are given in World Bank (1990).

3

This distinction is also important in interpreting the tax rates onmajor categories of goods, presented in Table 2.1. To take an example, one oftne tobacco products is grade A cigarettes, with a product tax rate of 60percent. This means that ror every 100 Yuan spent by consumers on thisproduct, 60 Yuan is paid in tax and 40 Yuan is received by producers. Thus,the tax paid is 150 percent of the producer price. In other words, the 60percent product tax is equivalent to a sales tax (defined by normal practice)of 150 percent.

Table 2.1 shows that there is substantial variation in tax rates. Thisis a common feature of tax systems in socialist economies, such asCzechoslovakia and the Soviet Union, but it constitutes a major diff,trencebetween the Chinese tax system of indirect taxes and the systems in use inmarket economies. Nonetheless, the structure of rates shows certainsimilarities with the structure of indirect taxes in other countries. Forexample, the application of especially high rates of tax to tobacco products,alcoholic beverages and gasoline is virtually universal practice. Taxes onthese three groups raised approximately 27 percent of total Product Taxrevenue in 1986.

Value Added TaxV

Value Added Tax (VAT) is gradually replacing Product Tax as the majorindirect tax on manufacturing and imports. The replacement is carried out insuch a way that while both .axes cover all manufactured goods, no product issimultaneously liable to both. VAT rates have also been decided on aproduct-by-product basis with rates set to yield the same revenue as theformer Product Tax (although there are some goods, such as textiles, that haveseen a reduction in their tax burden). This means that there is also a largenumber of VAT rates. The current range of goods subject to VAT is indicated byTable 2.2, which also shows the rates. VAT is not applied to agriculture,services, construction, transport and communications or wholesale and retaildistribution. In keeping with general international practice, exports arezero-rated.

As with Product TPx, VAT is applied to the purchase price of a good, notits producer price. The difference from Product Tax is that taxes paid onintermediate inputs into production are credited and so reduce the taxliability. The nominal rates of tax are therefore increased when goods areswitched from Product Tax to VAT, in order to maintain revenue and preventexcess profits.

The coexistence of Product Tax and Value Added Tax is unusual, as is thelarge number of different rates. Both features are administratively costly.First, it is difficult to calculate the tax that should be credited forintermediate inputs, some of which have paid Product Tax and others VAT attypically different rates. Second, the above difficulty is compounded by thefact that invoices do not show the amount of tax paid.

For a discussion of different variants of the value added tax, see Shoup(1990).

4

TABLE 2.1

Froduct Tax Rates on Major Product Groups

May 1988

Product Group Rates

Tobacco Products 35Z 60ZBeers, Wines and Spirits 10% - 50ZRubber Products 10% - 202Building Materials 3% - 1zZMinerals 32 - 12%Electric Power 5Z - 252Gas 3% - 15%Gasoline 4Diesel 10oKerosene 25%Other Petroleum Products 3% - 35ZChemicals 3Z - 25zMetals 3% - 15XTea 102 - 25XLuxury Foods 5% - 357Timber, Bamboo and Lacquer 5b - 15ZMeat 3Z

Source: General Taxation Bureau

In principle, the VAT should credit enterprises for both the product taxand the VAT that has been paid on purchased intermediate inputs. However, inpractice, the credit for inputs that have Daid Product Tax is made at acomposite rate of 14 percent. For some enterprises this composite rate isextended to include all intermediate inputs, including those that have paidVAT. This practice is administratively attractive when firms purchase a rangeof inputs that have paid VAT at different rates. The operation of the ChineseVAT is therefore one of "presumptive" crediting and thus differs from thestandard invoice method.

VAT in China does not allow credit for tax paid on purchases of fixedassets. Such discrimination against investment goods makes the taxincome-based in contrast to the consumption-type VAT that appears on thestatute books of many countries.

5

TABLE 2.2

Value Added Tix Rates on Major Product Groups

May 1988

Product Group Rates

Textiles 14Z - 232Clothing and Footwear 14Z - 202Enamel Products 202Glass and Glass Products 142 - 26ZMedicines 14ZHousehold Machinery 14% - 43ZElectrical Appliances 14% - 20XElectronic Appliances 142 - 16ZMachinery 12% - 14ZSteel 8ZSteel Products 14XPaper 142 - 302Stationery 122 - 302Household Chemicals 142 - 452Ceramics 122 - 202Processed Food and Beverages 14X - 302Leather 142 - 202Furniture 142

Source: General Taxation Bureau

Business Tax

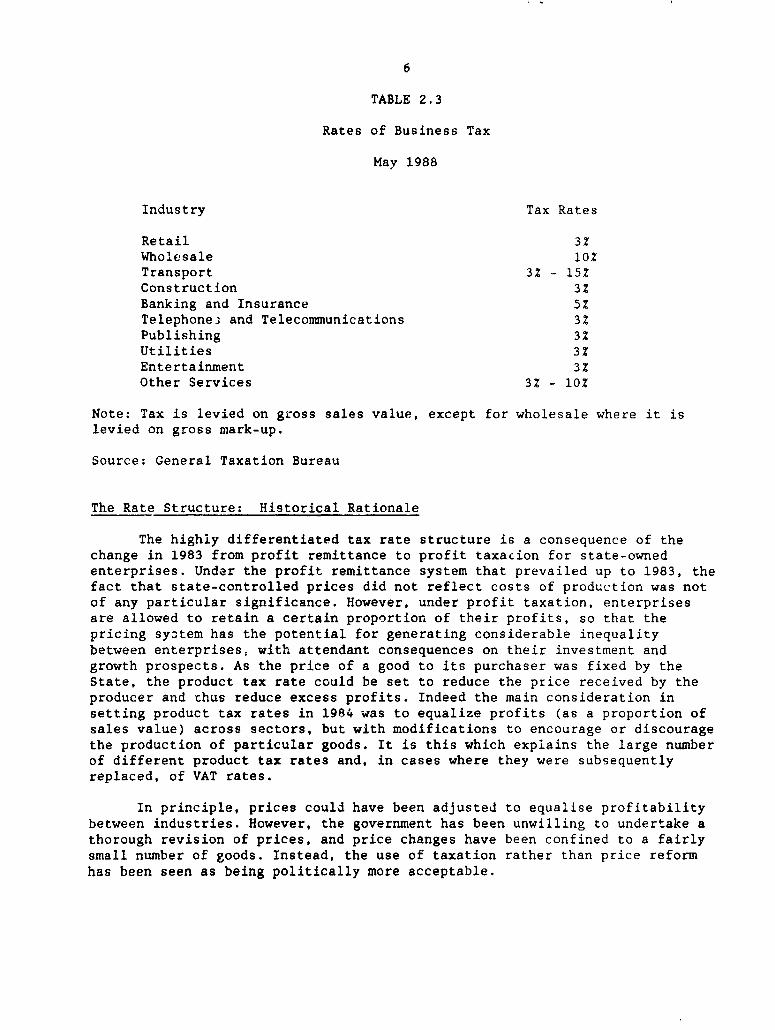

The Business Tax replaced that part of the Consolidated Industrial andCommercial Tax that applied to wholesale and retail distribution,construction, transport and communications and services. It is applied tonon-agricultural activities outside manufacturing: retail, wholesale,transport, construction, banking and insurance, telephones andtelecommunications, publishing, utilities, entertainment and other services.It is a turnover tax on gross sales value in all sectors except wholesalewhere it is levied on the gross value of the mark-up. The rate structure isshown in Table 2.3.

6

TABLE 2.3

Rates of Business Tax

May 1988

Industry Tax Rates

Retail 3ZWho'lesale lOZTransport 3Z - 15XConstruction 3ZBanking and Insurance 5%Telephone; and Telecommunications 3ZPublishing 3ZUtilities 3ZEntertainment 3ZOther Services 3X - 10%

Note: Tax is levied on gross sales value, except for wholesale where it islevied on gross mark-up.

Source: General Taxation Bureau

The Rate Structure: Historical Rationale

The highly differentiated tax rate structure is a consequence of thechange in 1983 from profit remittance to profit taxacion for state-ownedenterprises. Under the profit remittance system that prevailed up to 1983, thefact that state-controlled prices did not reflect costs of production was notof any particular significance. However, under profit taxation, enterprisesare allowed to retain a certain proportiorn of their profits, so that thepricing system has the potential for generating considerable inequalitybetween enterprises, with attendant consequences on their investment andgrowth prospects. As the price of a good to its purchaser was fixed by theState, the product tax rate could be set to reduce the price received by theproducer and thus reduce excess profits. Indeed the main consideration insetting product tax rates in 1984 was to equalize profits (as a proportion ofsales value) across sectors, but with modifications to encourage or discouragethe production of particular goods. It is this which explains the large numberof different product tax rates and, in cases where they were subsequentlyreplaced, of VAT rates.

In principle, prices could have been adjusted to equalise profitabilitybetween industries. However, the government has been unwilling to undertake athorough revision of prices, and price changes have been confined to a fairlysmall number of goods. Instead, the use of taxation rather than price reformhas been seen as being politically more acceptable.

7

The fact that differential indirect taxes are used to equalize profitsis further illustrated by the fact that the product tax rates on cement, crudeo.l and electricity also depend on the size of the producing cnterprises. Thuslarger enterprises in the cement industry pay 10 percent Product Tax whilesmaller enterprises pay 5 percent.

As well as equalising profitability, some dom-stic indirect taxes arepartly set with reference to considerations of industrial policy. For example,the recent switch of the textile industry from Product Tax co VAT wasaccompanied by a reduction in the industry's overall tax burden, apparentlvwith the aim of promoting the industry.

The use of taxes to encourage or discou:..age particular industries can bequite effective in an economy with limited foreign trade, althougn directsubsidies would be an economically more cost-effective policy. However, asChina's foreign trade expands, the effects of taxes will change. First, thepossibility of foreign trade means that domestic production and consumption ofparticular goods need not be equal and so a distinction can be drawn betweenthe aim of discouraging consumption and that of discouraging production. Inthe case of cigarettes, it is probable that the authorities' aim would be todiscourage consumption (there is no obvious need to reduce production so longas increased production reduces imports or increases exports) and increasedtaxes with fixed consumer prices will not reduce consumption. Second, changesin taxes will no longer have such a large effect on domestic productionbecause a tax change that alters incentives for domestic producers will alsoalter incentives for importers. Thus, a tax reduction will stimulate importsas well as domestic production. In these circumstances, direct subsidiesbecome a more effective method of promoting particular industries.

The reform of indirect taxation was accompanied by the introduction ofthe dual pricing system in 1985/86. This allowed enterprises to purchase partof their inputs and sell part of their output at market prices. However, Stateenterprises must first deliver their plan quota at State list prices beforeselling output on the free market. At the same time enterprises may buy acertain quota of inputs at list prices. The proportion of consumer goodstransacted at list prices had fallen from 97 percent in 1978 to 47 percent in1986. By 1986, the proportion of intermediate goods sold at list prices hadfallen to 60Z.

Indirect tax rates in China were therefore designed for a fixed priceeconomy, but row operate in an economy with both fixed and flexible prices.The effects of tax changes are however very different on plan transactions andfree market sales. A tax increase will reduce enterprise profitability onsales at fixed prices but will not distort consumer choice. However, a taxincrease on free market sales will mainly be passed on to final consumers,unless the supply of the good is unresponsive to price changes, and thedifferentiated tax structure will have adverse incentivt effects.

Of course, some differentiation of the tax structure is desirable ever.in a market economy for several reasons: (i) to discourage the consumption ofsocially harmful goods, (ii) to tax luxury goods that are consumed veryheavily by the rich, (iii) to tax goods with price-inelastic demands so as to

8

allow revenue to be raised in an efficient way. However, the differentiationrequired on the above grounds bears little relationship with that stt by thetax authorities to equalize sectoral profitability. In any event, theefficiency objective of distortionary taxation can usually be achieved inpractice by setting particularly high tax rates on a small number ofparticular goods, rather than by highly differentiated taxes across the wholerange of industrib± products. Excessive sectoral differentiation in China hasnegative incentive effects that depend, inter alia, on the proportion of salestransacted at market prices.

2.2 Taxes and Enterprise Profitability

As stated above, the General Taxation Bureau sets VAT and Product TaxRates in order to generate producer prices (i.e., plan prices less taxes) thatallow enterprises to earn "reasonable" profits, subject to additionalconsiderations of industrial policy.

The 1984 tax reforms set indirect cax rates to equalize profitability onsales across sectors to the profit margins prevailing in 1983. This may beseen as a substitute for the tendency towards equalization of returns onequity that characterizes market economies. However, profitability on salesthat forms the basis for tax policy bears little relationship withprofitability on assets, which one expects to be equalised in a competitivemarket economy. And the two notions are noticeably different in r,ianyindustries. Thus, in ferrous metals, mining and preparation, profits and taxesin relation to Rmib 100 of sales revenue are, at 20.27, well above the nationalaverage of 9.79, making that industry a candidate for heavy indirect taxation.In contrast, profits and taxes in relation to Rmb 100 of the original value offixed assets, at 12.65, are below the national average of 109.00 so thattaxes, if set with reference to the latter measure of profitability, would berelative low in that industry.

The measure of profitability that currently guides the setting ofindirect tax rates is particularly problematic when consideration is given tothe principal uses to which after-tax profits in State-owned enterprises areput. "nese are broadly speaking, of two kinds: (1) investment in expansion ofthe enterprise, and (2) provision of bonuses and other 'anefits to workers.

While an enterprise's need for funds under (1) depends on its capital-intensity and rate of growth, its needs under (2) depend on the number ofworkers. Given that retained earnings accounted for 38 percent of investmentin fixec. dssets in 1986, this has meant that equalizing sales profitabilitycould starve capital-intensive industries of funds for expansion. This wasparticularly marked in railways and electricity. Hence the Business Tax onrailways was reduced in 1986 and th- ax rules for electricity altered toallow a e costs to be deducted for tax purposes. By the same token,l1'-our-ilitensive industries have found it more difficult to afford bonusesthai. less labour-intensive industries.

The issue of enterprise profitability is important in any decision tosimplify the tax rate structure, as discussed in :he next section.

9

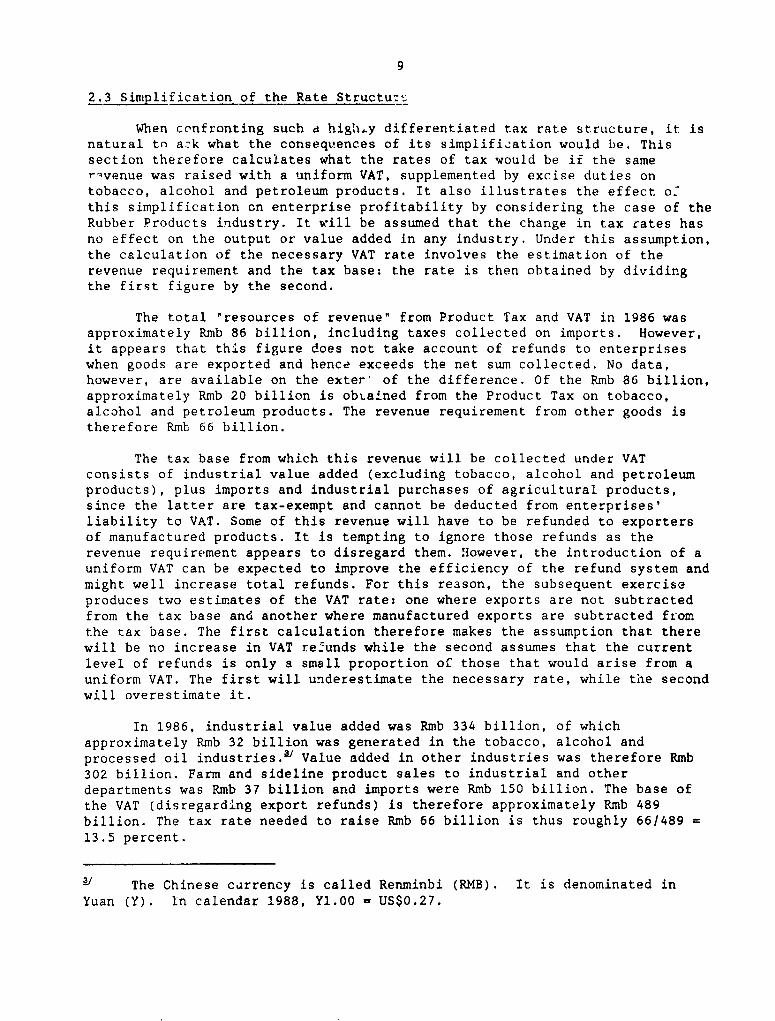

2.3 Simplification of the Rate Structu-.

When confronting such d high.y differentiated tax rate structure, it isnatural tn azk what the consequences of its simplifi_ation would be. Thissection therefore calculates what the rates of tax would be if the samer-venue was raised with a uniform VAT, supplemented by excise duties ontobacco, alcohol and petroleum products. It also illustrates the effect o.this simplification on enterprise profitability by considering the case of theRubber Products industry. It will be assumed that the change in tax rates hasno effect on the output or value added in any industry. Under this assumption,the calculation of the necessary VAT rate involves the estimation of therevenue requirement and the tax base: the rate is then obtained by dividingthe first figure by the second.

The total "resources of revenue" from Product Tax and VAT in 1986 wasapproximately Rmb 86 billion, including taxes collected on imports. However,it appears that this figure does not take account of refunds to enterpriseswhen goods are exported and hence exceeds the net sum collected. No data,however, are available on the exter of the difference. Of the Rmb 86 billion,approximately Rmb 20 billion is obLained from the Product Tax on tobacco,alcohol and petroleum products. The revenue requirement from other goods istherefore Rmb 66 billion.

The tax base from which this revenue will be collected under VATconsists of industrial value added (excluding tobacco, alcohol and petroleumproducts), plus imports and industrial purchases of agricultural products,since the latter are tax-exempt and cannot be deducted from enterprises'liability to VAT. Some of this revenue will have to be refunded to exportersof manufactured products. It is tempting to ignore those refunds as therevenue requirement appears to disregard them. However, the introduction of auniform VAT can be expected to improve the efficiency of the refund system andmight well increase total refunds. For this reason, the subsequent exerciseproduces two estimates of the VAT rate: one where exports are not subtractedfrom the tax base and another where manufactured exports are subtracted fromthe tax base. The first calculation therefore makes the assumption that therewill be no increase in VAT refunds while the second assumes that the currentlevel of refunds is only a small proportion of those that would arise from auniform VAT. The first will underestimate the necessary rate, while the secondwill overestimate it.

In 1986, industrial value added was Rmb 334 billion, of whichapproximately Rmb 32 billion was generated in the tobacco, alcohol andprocessed oil industries.Y Value added in other industries was therefore Rmb302 billion. Farm and sideline product sales to industrial and otherdepartments was Rmb 37 billion and imports were Rmb 150 billion. The base ofthe VAT (disregarding export refunds) is therefore approximately Rmb 489billion. The tax rate needed to raise Rmb 66 billion is thus roughly 66/489 =13.5 percent.

3/ The Chinese carrency is called Renminbi (RMB). It is denominated inYuan (Y). In calendar 1988, Y1.00 = US$0.27.

10

Turning to the second calculation, it is necessary to subtract

approximately 85 percent4' of export value, which equals Rmb 92 billion. Thetax base then becomes Rmb 397 billion and the necessary tax rate is 66/397 =

16.6 percent approximately.

These two estimates represent the upper and lower bounds on plausibleVAT rates and it is not unreasonable to take an intermediate figure of 15

percent as representing the "best guess". This is broadly consistent with the

current approach used by the General Taxation Bureau in setting VAT rate' 14percent is taken as a standard rate that is used most often, although

substantial deviations from this figure are used in particular circumstances.Upward deviations from this figure are the most frequent, and this isconsistent with the fact that 14 percent is very near the lower end of therange calculated above.

To see how a uniform rate of VAT at 15 percent can be supplemented byexcise taxes, consider the case of the tobacco industry. This example is only

an illustration of the principles involved as it neglects untaxed inputs intotobacco manufacturing and assumes that all tobacco products are taxed at the

same rate. fhe value added in this industry is approximately Rmb 14 billion,so that a 15 percent VAT would raise Rmb 2.1 billirn. This contrasts with the

Rmb 11.3 billion currently collected from the proauct tax. Maintenan,ce of thecurrent total tax receipts from the tobacco industry would therefore require asupplementary excise tax that would raise Rmb 9.2 billion. Such a tax would

be based on the total output of the industry, Rmb 17.2 billion. The excise taxrate would therefore be 92/172 = 53 percent. Similarly, turning to petroleumproducts, value added equals Rmb 12.83 bi.llion, so that a 15 percent VAT would

raise Rmb 1.93 billion. Since total output is Rmb 23.37, maintenance of theexisting tax receipts of Rmb 5.67 billion would require an excise tax rate of

16 percent.

The effect of unifying the VAT rate on enterprise profitability may be

illustrated using the following example based on the rubber products industry.In 1986, the tax revenue from rubber products was approximately Rmb 1.634billion. The unification of VAT discussed above would lead to a rate of 15

percent, which would have yielded Rmb 0.758 billion (on a 1986 value added ofRmb 5.05 billion).

The effect of this tax reduction on profitability in the rubber products

industry will depend on the degree of price control to which the industry is

subject. Assume first that all output is subject to price control. In that

case, enterprises in the industry increase their income by Rmb 0.876 billion.

Taking the current rate of enterprise income tax, 55 percent, after-taxprofits will rise by Rmb 0.394 billion. A perspective on this figure is

provided by comparing it with the industry wage bill of approximately Rmb

1.857 billion (value added minus Rmb 3.293 billion of profits and taxes).Thus, for example, if all extra profits were paid as bonuses, they wouldamount to 21 percent of the wage bill.

9 As the average rate of VAT is approximately 152, the 85 percent of export

value represents the factor cost of the exports.

11

This result under price control may be compared with what would happenwith no price controls. In this case, the increase in profitability willencourage enterprises to lower prices in order to capture a larger share ofthe market. If the industry is competitive and there is no shortage of supply,prices will fall until the level of profitability is the same as before. Totalprofits will rise if output increases in response to the increased demandgenerated by lower prices, but profits per unit of sales would continue to bethe same.

It is not known what proportion of rubber products are sold on the freemarket. Suppose, in line with the average situation for intermediate goods,that the figure is 60 percent for plan sales and 40 percent for sales atmarket prices. In this case, the reduction in taxes will, as before, increasethe profitability of production. Since enterprises can sell additional outputat free market prices, they will cut those prices as in the case of no pricecontrols. Thus the free market price will fall by as much as before, so longas there is sufficient competition and there will be no increase in profitsper unit of sale on goods sold on the free market. The effect on profitabilityis then confined to the output that is sold at fixed prices. As this is 60percent of sales revenue, the profit increase is 60 percent of that availablewhen all the product was sold at fixed prices.

This analysis could equally well be applied to an industry that wouldsuffer an increase in taxation following attempts to unify the VAT. In such acase, the reduction in profitability will depend on the proportion of outputthat is sold at fixed prices. In general, the effects of tax changes onprofitability will be smaller for industries that sell high proportions ofoutput at free market prices.

2.4 Tax simplification

The discussion in section 2.3 suggests that there would be considerablegains and losses for enterprises in different industries as a result ofcomplete simplification of indirect taxes. These gains and losses would createinequality in wage bonuses and in access to investment funds (which would, inturn, increase future inequality in wage bonuses). This is an example of atrade-off between equity and efficiency: uniform taxes promote efficiency but,in these institutional circumstances, create inequality. Such a trade-off canbe analyzed using optimal tax theory and this is presented in Heady and Mitra(1991), where an analytical framework is developed and illustrative optimaltaxes are calculated.

Such optimal taxes are highly differentiated if the administrative costsof taxation are ignored. However, in view of the considerable difficulties ofadministering a highly differentiated tax structure it is worth asking whetherlimited tax simplification might allow most of the advantages ofdifferentiated taxation without excessive administrative cost. To this end,tables 2.4 and 2.5 present the results of allocating goods into threetax groups and calculating the optimal tax rate for each group. The groupswere chosen by calculating optimal taxes for each of the 24 goods, andgrouping together goods with similar tax rates. In addition to

12

presenting the optimal tax rates, tables 2.4 and 2.5 present the welfareloss from imposing completely uniform taxation and the welfare gain fromsetting each good's tax rate separately (unrestricted taxes). The welfaregains and losses are measured in GDP equivalents.

Table 2.4 reports the optimal taxes and welfare losses for varyingproportions of the output of each industry being sold at plan prices, holdingthe degree of inequality aversion, e, equal to zero (implying that twice as

much weight is put on income gains to individuals with half the income). Table2.5 holds the proportion subject to plan prices constant, and illustrates theeffects of changing e from unity (no inequality aversion) to minus ten (very

high inequality aversion).

The results show an increased spread of tax rates as either theextent of planning or the degree of inequality aversion increases. The role of

the extent of planning follows from the fact, illustrated in section 2.3, thatthe effect of tax changes on profitability depends on the extent of pricecontrol. The role of inequality aversion reflects the fact that moreefficiency will be sacrificed if the removal of inequality is given higherpriority. The losses from uniform taxation and the gains fromunrestricted taxation increase similarly. However, in all but one case, theloss from imposing uniformity is more than twice the gain from allowingunrestricted taxation.

Thus, the introduction of three separate tax rates captures at

least two-thirds of the gains that would be made in moving from uniformtaxation to unrestricted taxation. The analysis makes clear that reducingthe number of VAT rates without, however, moving to unification, would lead tosignificant welfare gains while permitting greater efficiency in taxadministration.

2.5 Cascading

As in many developing countries, the indirect tax system derives a

significant amount of revenue from the taxation of raw materials and capitalgoods entering the production process. To the extent that enterprisesincreasingly choose techniques of production, the taxation of such goods is

distortionary and detracts from efficiency in production. By adding to the

costs of production, it also increases the cost of exports, adverselyaffecting China's competitive position. The gradual replacement of Product Tax

by VAT is designed to address these problems. However, inasmuch as the VAT,though growing in coverage, is still partial, allowance is not made for taxespaid on all inputs. For these reasons, the full tax burden borne by acommodity does not consist simply of the tax applied to final output. It also

includes the taxes paid on inputs, and on the inputs used in producing the

inputs all the way back through the process of production.

13

TABLE 2.4

The Effect of Planning n Tax Rates

Degree of inequality aversion, e = 0

Tax Group 1/4 Plan 1/2 Plan 3/4 Plan

Low 41? 28Z 21ZMedium 46Z 45Z 42ZHigh 75Z 76Z 67Z

Welfare loss ofuniform taxes 1.OZ 3.7Z 7.2Z

Welfare gain ofunrestricted taxes 0.4Z 1.OZ 2.3Z

TABLE 2.5

The Effect of Aversion to Inequality with half plan

Tax Group e=1 e=0.5 e=O e=-l e=-2 e=-10

Low 41Z 322 28Z 24Z 23Z 23ZMedium '1Z 43Z 45Z 47? 47Z 47ZHigh 41Z 72Z 76Z 79Z 81Z 84Z

Welfare loss ofuniform taxes 1.7Z 3.7Z 7.0? 9.5Z 12.2ZWelfare gain ofunrestricted taxes 0.5Z 1.O 1.8? 2.9Z 9.9Z

Note: The low tax group contains goods 1, 2 and 3 (Agriculture, Forestry

and Animals). The high tax group contains goods 6, 7, 9, 10 and 12(Metallurgy, Electricity, Petroleum, Heavy Chemicals and Heavy Machinery).All other goods are in the medium tax group.

The analysis of the effects of cascading is made more complex in Chinabecause of the coexistence of VAT and Product Tax. Since an industry subjectto VAT can reclaim taxes paid on inputs a distinction must be drawn betweenindustries subject to VAT and those subject to Product Tax. Also, the amountof taxation that has been borne by inputs into an industry subject to ProductTax will depend on whether those inputs were produced in an industry subjectto VAT or in an industry subject to Product Tax. Cascading is also present inindustries subject to VAT: while the tax paid on immediate inputs is refunded,this is not the case for taxes paid on inputs into the supplying industry(unless that industry is also subject to VAT). This point is of importance in

14

the design of export rebates that typically refund taxes paid only on firstround inputs, thereby depriving exporters of the full competitive edge whichwould otherwise prevail. Nonetheless, it must be expected that the effect ofcascading is less for goods produced in industries subject to VAT; this isborne out by the calculations reported below.

Column (4) of Table 2.6 shows the cascading effect0l, i.e., the wedgebetween producer prices under the existing system of taxation and thatprevailing under a VAT covering all sectors at the same statutory rates as atpresent. To this column (5) adds the present wedge between consumer andproducer prices [column (3)] to arrive at the full tax burden. The table showsthat there are considerable differences between the statutory tax rate and thefull tax burden. Thus, some basic intermediates such as electricity, coal andcoke and heavy chemicals suffer taxation that is well in excess of theirstatutory rates; this is also true of the sectors statutorily subject toBusiness Tax. It also illustrates the point that sectors subject to VAT sufferless from cascading, although they are affected to some extent.

The extent of cascading is, however, understated by Table 2.6. This isbecause unavailability of data precluded incorporating the effect of taxespaid on capital goods. In contrast to other intermediate inputs, the effect ofcascading is not ameliorated in this case even in sectors under the existingVAT, because the VAT does not allow credit for taxes paid on purchases offixed assets.

The calculations confirm that the existing system of indirect taxationis less efficient than a single stage sales tax or a value added tax. Theyalso lend support to the notion that a VAT covering all sectors would, byeliminating the cascading effect of indirect taxes, make the incidence oftaxation more closely approach that desired by policymakers in formulating thestatutory rates of taxation. It would also provide a framework that ensuresduty free access to all inputs, direct and indirect, going into exportproduction.

2.6 Equity

Indirect taxes are not seen as an equity-enhancing instrument in China,except in the sense of equalizing profitability across enterprises. However,the equity impact of existing taxes is complicated by the fact that taxes setwith reference to enterprise profitability, when shifted on to prices of freemarket sales, have different effects on households at different income levels.

W The way in which this is calculated is explained in World Bank (1990, p.221).

15

Table 2.6. The Effects of Tax Cascading

4) (2) (3) (4) (5)Type Statutory Cascading Full

Sector of Tax Tax Effect Tax

Agriculture Exempt 0 4Z 4ZForestry Exempt 0 1% 1%Animal husbandry Exempt 0 2Z 2%Sideline Exempt 0 7% 7ZFishery Exempt 0 5Z 5%Metallurgy VAT 142 3Z 17ZElectricity Product 5Z 5% lOZCoal and coke Product 32 6% 9%Petroleum Product 30Z 11% 41ZHeavy chemicals Product 15Z 112 26ZLight chemicals VAT 20X 4% 24%Heavy machinery VAT 14% 2% 16%Light machinery VAT 16Z 3% 19%Constructionmaterials Product 5% 8% 13%Heavy forestry Product 1OZ 8% 18%Light forestry VAT 14Z 3% 17%Food VAT 16Z 2% 18ZTextiles VAT 18% 2Z 20%Clothing VAT 14% 2Z 16ZPaper VAT 14% 2% 16%Othermanufacturing VAT 14% 3% 17%Construction Business 3% 10% 13ZTransport Business 5% 7% 12%Commerce Business 3X 6% 9%

Data that would permit an analysis of the effects of taxes on marketprices and thus on the distribution of real income among households are notavailable. However, two observations may be made. First, given the highproportion of food in the expenditures of almost all Chinese households, it isthe exemption of most foods from Product Tax/VAT that has the greatest effecton distribution among consumers. Changes in taxes on other goods, that form asmall proportion of household budgets, will have little effect. Second, luxurygoods have high consumer prices, presumably partly for distributional reasons.This could not have been sustained after the replacement of profit remittancewith taxes unless high product tax rates had been used to reduce theprofitability of their production. Thus luxury goods are subject to high taxrates in China, as elsewhere. But with given consumer prices, their impactappears to fall on producers.

16

2.7 Price controls as implicit taxes

In view of the fact that the system of price controls is an implicitsubsidy to users financed by an implicit tax on producers, reference was made

above to the need to view taxes and price controls an integrated system. This

has already been illustrated in terms of the constraining role of the dualpricing system in tax reform. This subsection looks at price reform more

closely. Since indirect taxes are levied principally on non-agriculturalgoods, the discussion on price controls is confined to non-agricultural goods

as well.

The subsidy to consumers implicit in price controls on final goods maybe tentatively calculated as follows. These are based on data published in the

Statistical Yearbook of China 1987 (SYC) and relate to the year 1986. The SYC

presents data on the ratios of market prices to state list prices for

'Miscellaneous goods for daily use' and 'Other'. The former category is taken

to mean the same as 'Daily articles' in the table on retail sales while the

latter is taken to include all other categories of consumer goods apart from

food. The ratio of rural market price to state list price is less than one for

"Miscellaneous goods for daily use' and this suggests that the rural goods may

be of inferior quality. For this reason, the urban market price (for both

categories of goods) is used as the best measure of the market price. This may

lead to an overestimate of the subsidy implicit in price controls.

The ratio of urban market price to state list price was 1.08 for

'Miscellaneous goods for daily use' and 1.30 for 'Other".6' The magnitude of

the subsidy also depends on the proportion of sales that take place at

controlled prices. It is difficult to obtain detailed information on this, but

the State Price Bureauz/ says that in 1986, 47 percent of consumer goods

were sold at state list prices, 19 percent at guidance prices§' and 34

percent at market prices. No figures are available on the relationship between

guidance prices and state list prices. The present calculations assume that

they are equal, and this provides another element of overestimation of subsidy

implicit in controls on non-agricultural final goods.

The above implies that about 70 percent of 'daily use goods" are sold at

state-list prices. The prices of these goods are 8 percent below market price.

The average price of daily use goods is therefore reduced by 70 percent of 8

percent = 5.6 percent. For other goods, 60 percent of the sales are at a pricethat is 30 percent lower so that average prices are lower by 18 percent. The

table of retail sales indicates that daily use goods account for approximately10 percent of retail sales, while other non-agricultural goods account for

§/ These ratios have varied considerably over the last few years, increasing

during the inflationary period of 1988/9 and decreasing more recently.

7/ Quoted in World Bank (1990).

8/ Guidance prices are applied to some consumer prices instead of State listprices. They are maximum prices, rather than fixed prices, and are easier to

change than list prices.

17

approximately 36.5 percent of retail sales. The effect of controlling pricesof non-agricultural goods on an index of retail prices is thereforeapproximately 7 percent (0.1 times 5.6 percent plus 0.365 tines 18 percent).This is something of an overestimate of the subsidy implicit in price controlson non-agricultural goods, first, because of the assumptions stated above, andsecond, because households spend some of their income on items that are notincluded in retail sales.

This subsidy to consumers is financed by the producing enterprises. Itis therefore interesting to consider the effect of removing these controls onrevenue and industry profitability. The simplest assumption on the effects ofeliminating price controls on non-agricultural final goods is that theseprices will rise to the current level of free market prices. It could beargued that free market prices might be reduced somewhat by the generalreduction in households' real incomes, following withdrawal of the subsidyimplicit in controlled prices, although this in turn could be offset byexplicit subsidies to households. The simple assumption is adopted here.

Revenue effect

With the above assumption, the argument used before may be adapted toshow that the average price increase for articles of daily use would be 5.6percent. Total retail sales for these goods in 1936 was Rmb 43.5 billion. Theprice increase would therefore yield a potential transfer to enterprises of0.056 times this figure = Rmb 2.436 billion. The average price increase forother non-agricultural goods would be 18 percent on retail sales of Rmb 154.2billion and yield a potential transfer to enterprises of Rmb 27.756 billion.The total potential gain in profits from the price increases would thereforebe Rmb 30.192 billion. However, with an average VAT rate of 15 percent, anamount equalling Rmb 4.53 billion would accrue as extra VAT revenue, leavingRmb 25.66 billion or a little under 8 percent of total industrial value added.With an enterprise income tax of 49 percent, the revenue gain from this sourcewould equal Rmb 12.57 billion. The total revenue gain would thus be Rmb 17.1billion or close to 20 percent of total Product Tax and VAT revenue.Additional after-tax profits would, according to existing guidelines, bedistributed among investment and workers' remuneration.

Profitability effect

In order to look at the sectoral distribution of increased profits, itis necessary to make assumptions about which industries produce each categoryof goods. The tentative allocation of industries, together with their 1986value added figures are listed here:

18

Articles for Daily Use

Chemicals for Daily Use Rmb 2.689 billionMetal Products for Daily Use Rmb 2.788 billionMachinery for Daily Use Kmb 5.291 billionElectric Equipment for Daily Use Rmb 2.830 billionFurniture Rmb 1.727 billion

Total Value Added Rmb 15.325 billion

Note: Value added for the first four industries was not directly availableand had to be estimated by calculating the ratio of value added to net outputfor a broader industry definition (for example, chemicals), and using thisratio to convert from net output to value added.

Other Goods

Coal Rmb 12.898 billionTextiles Rmb 30.875 billionClothing Rmb 5.642 billionLeather and Fur Rmb 2.817 billionPaper Rmb 5.669 billionCultural Goods Rmb 1.647 billionArts and Craft Rmb 2.950 billionRubber Rmb 5.050 billionPlastics Rmb 4.652 billion

Total Value Added Rmb 72.200 billion

Looking at the industries producing Articles for Daily Use, the increase inpotential profit is Rmb 2.436 billion against a 1986 value added of Rmb 15.325billion. Therefore the potential gain to those industries from relaxing pricecontrols would be approximately 16 percent of value added. For the industriesproducing other goods, the potential gain of Rmb 27.756 billion may becompared with a value added of Rmb 72.200 billion to give a ratio of 38percent. While both sets of numbers would have to be revised downwards by theVAT rate applicable to those industries, as in the aggregative calculationsabove, were the corresponding classification of rates available, the exerciseindicates that the profitability effects of price decontrol will vary greatlyacross sectors of the economy.

Consider finally the effects of decontrolling intermediate goods priceson industrial profitability. It is assumed (i) that enterprises maximizeprofits9 and (ii) that the dual pricing system has encouraged marginalenterprise decisions to be made on the basis of uncontrolled market prices.This implies that the increase in intermediate goods prices to free marketlevels, being analogous to the removal of a lump sum subsidy,will have no

2/Perkins (1988) suggests that enterprise managers pursue increased profits inorder to benefit their employees, through the profit retention system

19

effect on prices faced by consumers. The extent of sales between agricultureand non-agriculture suggests that it makes sense to examine the effects ofdecontrolling all intermediate prices (not just of non-agricultural goods).

The effect of decontrolling intermediate goods prices is thereallocation of profits between supplier enterprises and purchasingenterprises. Unfortunately, hardly any information is available on the extentof the differences between free market prices and state list prices forintermediate goods. Also, up to date information on inter-industrytransactions was not available. However, table 2.7 presents illustrativecalculations of the effects on industrial profitability (measured as apercentage of gross value added) of raising intermediate good prices, usingthe 1981 input-output table for China. The precise effects of priceincreases would depend on the proportions in which each industry bought eachof its inputs at State list prices and free market prices. As we have noinformation on this, it is assumed that, for any one input, each industry hasthe same ratio of list price to market price purchases.

The first column reports the calculated effects of a 20 percent increasein the average price of all intermediate goods. However, not allintermediate goods are underpriced to the same extent: Dai (1989) regards theunderpricing of "higher" level intermediates such as elect.icity andcommunications as more serious than the underpricing of "middle' levelintermediates such as ferrous and non-ferrous metals. It is thereforenecessary to look at examples of increasing individual intermediategood prices. The second column reports the calculated effects of a 20percent increase in the price of electricity. The third column reports theeffect of a 16 percent increase in the average price for metallurgy. Thefourth column reports the same figures for a 16 percent rise in average coalprices. The fifth column reports the effects of a 10 percent rise in theaverage price of construction materials.

These changes in sectoral profitability in relation to value addedfollowing price reform could in principle be offset by suitable changes in therates of VAT. However, this will not necessarily lead to a more uniform set oftax rates because price controls are not the only cause of differences inprofitability; another major cause is the unequal distribution acrossenterprises of capital goods historically provided without charge by theState. Free markets with uniform taxes will only equalize profitability ifall sources of inequality are removed.

3. DIRECT TAXES

3.1 The system of enterprise income tax

From the point of view of revenue, the income tax from enterprises issecond to the Product Tax, VAT and Business Tax. Direct taxation of businessincome varies according to the type of enterprise. These include (i) stateenterprises, (ii) collective enterprises, (iii) individual householdenterprises, (iv) joint ventures, and (v) foreign enterprises.

20

TABLE 2.7Effects of Intermediate Goods Price Changes on Sectoral

Profitability

Sector (1) (2) (3) (4) (5)

Metallurgy +20% - 4.1% +30.6Z - 2.2Z -0.4ZElectricity +17% +25.3% - 0.1Z - 2.82 0

Coal and Coke +13% - 1.52 - 1.0Z +20.1Z -0.3%

Petroleum +12% - 0.8Z - 0.7Z 0 -0.2Z

Heavy Chemicals +21Z - 4.9Z - 0.4Z - 2.2Z -0.1Z

Light Chemicals - 52 - 0.5% - 0.42 - 0.2Z -0.1%

Heavy Machinery - 9% - 1.1% - 6.8Z - 0.3Z -0.2%

Light Machinery -18% - 0.9% -10.0% - 0.3Z -0.2%

Construction Mats +15Z - 3.4% - 1.1% - 2.8Z +17.2Z

Heavy Forestry +13% - 0.7Z - 0.32 - 0.42 -0.12

Light Forestry -11% - 0.8% - 2.1% - 0.2Z -0.2Z

Food -37Z - 0.2X 0 - 0.1Z 0

Textiles - 3% - 0.7% - 0.2% - 0.2Z 0

Clothing -40% - 0.1X - 0.1% 0 0

Paper - 3Z - 1.3Z - 0.2% - 0.5Z -0.1Z

Other Manufactures + 1Z - 3.9X - 0.3Z - 0.5% -0.3%

Construction -53% - 0.7Z - 5.2Z - 0.2Z -7.0O

Transport +10% - 0.2% - 0.2Z - 0.4% 0

Commerce, etc. - 2X - 0.3% 0 - 0.1% -0.lZ

Notes:

Column (1): 20% increase in the average price of all intermediate goods

Column (2): 20Z increase in the price of electricity.

Column (3): 16% increase in the average price for metallurgy.

Column (4): 16% increase in average coal prices.

Column (5): 10% increase in the average price of construction materials.

State Enterprises

State enterprises are divided into three categories for tax purposes.

Large- and medium-sized enterprises pay a flat tax rate of 55 percent on their

taxable profits. Small enterprises use an eight bracket progressive structure

with rates ranging from 7 to 55 percent. Taxable income equals enterprise

income minus business costs. Depreciation of fixed assets is an important

deductible cost and is accumulated in a depreciation fund. The enterprise

income tax further allows deductibility of principal as well as interest

repa-ments on bank loans, a point that is taken up in more detail below.

In addition to income taxes, large- and medium-sized state enterprises

face an income adjustment tax on profits net of income tax, that varies from

entetprise to enterprise. This tax addresses the wide variation in enterprise

profits reflecting circumstances other than enterprise efficiency. It is used

21

to equalize profitability within a sector, given that the differentialstructure of product tax-cum-VAT rates can only achieve such equalization on across-sectoral basis. Part of its rationale derives from the need to chargeenterprises for variations in profit arising from historically given andunequal endowments of free fixed assets. However, it is difficult todistinguish between differences in profitability arising for this reason asopposed Lo variations in quality of management. The income adjustment tax isbased on 1983 profit margins and is seen as temporary.

Collective Enterprises

An income tax on collective enterprises was introduced in 1985.Collective enterprises are collectively owned rather than state owned andrange from large businesses to small partnerships. Taxable income equalscollective enterprise income minus business costs and indirect taxes.Depreciation, which must be accumulated in a fund, is broadly similar to thatallowed for State enterprise. While interest payments on bank loans are fullydeductible, only 60 percent of principal payments enjoy tax-deductibility.Income tax is computed accordingly to an eight bracket progressive schedulethat is different from that used for small State enterprise. The income taxburden on collectives is generally lower than that on a State enterpriseearning the same profits.

Individual Household Enterprises

An individual household enterprise income tax was introduced in 1986. Aswith state and collective enterprises, taxable income equals business incomeminus costs and indirect taxes. Individual household enterprises face a tenbracket progressive schedule with rates rising from 7 to 60 percent. A surtaxof 10 to 40 percent is imposed on taxable income above 50,000 yuan per year.

Other Enterprises

The taxation of joint ventures and foreign enterprises is complex andlies outside the scope of this paper.' Taxes on state enterprises raise thebulk of the revenue from enterprise income tax, the remainder of this sectionconcentrates on them.

3.2 Contract Responsibility System

Income taxation of state enterprises can be substantially altered by thecontract responsibility system. This appears to be modelled on the"responsibility system" for agriculture, which set quota outputs that had tobe sold to the state at fixed prices, leaving farms free to sell any outputover the quota on the free market. It is also based on the old quotaresponsibility system, otherwise known as the "economic responsibilitysystem", that was tried in some enterprises in 1981/82 as part of the

12See World Bank (1990, pp. 172-174) for a description of the main features ofthe tax treatment of joint ventures and foreign enterprises.

22

evolution of enterprise reform. That system required the enterprise to delivera "profit quota" to the government and allowed it to retain a very highproportion of above-quota profits.

It was thought that the low marginal tax rate on above-quota profitwould infuse a measure of dynamism and risk-taking into State enterprises.However, since quotas under the "economic responsibility system" were setevery year, enterprises in practice made little effort to produce above theirdesignated quota, fearing that superior performance would send the authoritiesa signal about the true potential of the enterprise and elicit a higher quotain subsequent years (the "ratchet effect"1"/). The quota responsibilitysystem led, furthermore, to extensive bargaining both before and after thecontract, thereby running counter to the spirit of substituting rules fordiscretion in relations between the State and State-owned enterprises.

The contract responsibility systems that are currently in use arenegotiated between the enterprise director and the supervisory agencies andcover items such as profit delivery, investment, technical innovations and thetying of wages to economic efficiency. They usually cover a period rangingfrom two to five vears, a feature that is intended to alleviate theconsequences of the short-term ratchet effec-. Of the large number of systemsin operation, the most common is the Contract Management ResponsibilitySystem, (CMRS), which is believed to cover between 60-70 percent ofenterprises. This typically selects the existing enterprise director as thecontractor and ties employee rewards directly to enterprise performance. Inone form of the CMRS (double contracting and single linkage), enterprises mustturn over a certain amount of direct plus indirect taxes every year, withshortfalls if any being made up from its own funds. The growth in reinvestmentand the wage bill is tied to the growth of profits and taxes Another variant(responsibility for annual increase in profit remittance) grants exemptionfrom indirect taxes but requires that profits equalling a fixed base amountplus an annual percentage increase (usually 7 percent) be handed over to thegovernment. A third variant fixes a constant annual profit delivery for theduration of the contract, with a specified sharing ratio for above-quotaprofit, whereas a fourth variant differs from the third in allowing theenterprise 100 percent of above-quota profits or lower-than-targeted losses.Finally, the sectoral input-output responsibility systems of the CMRS apply topetroleum, coal, chemicals, iron and steel, nonferrous metals, railways, postsand telecommunications, and civil aviation. Contracts range from 3 to 4 years.

Approximately 9 percent of enterprises fail to meet profit targets undercontract. In such cases, the shortfall is supposed to be made up from retainedearnings and depreciation funds of enterprises. In practice, enterpri.ses donot take the entire shortfall 'rom these sources. There are two solutions: (1)banks forgive loans to enterprises; and (2) the Finance Department compensatesfor the loss from its budget. Furthermore, where the enterprise fails to meetits contract because of unfavorable price changes, it can appeal to theFinance Department of its relevant industry ministry on "objective" grounds.

11The ratchet effect has been extensively discussed in the literature onSoviet planning, for example Weitzman (1976).

23

3.3 Problems with the current system

Although revenue from the enterprise income tax is second only toindirect taxes, its recent growth appears not to have kept pace with profits.The profit tax and adjustment tax together raised Rmb 81.9 billion in 1986 andRmb 81.5 billion in 1987. This appears, in part, to be a consequence of thecontract responsibility system which uses profit quotas that are eitherconstant or gr3w at a rate less than that of the industrial sector, togetherwith a marginal rate of tax that is significantly below the basic rate.

The substitution of profit remittances by profit taxation at a uniformrate and the resulting link between profits and remuneration of staff inenterprises can be seen as an attempt to increase enterprises' responsibilityfor their own profits and to reduce the role of discretion in dealings betweenenterprises and their supervising bureaus in favour of rules. Although itc%used a decline in budgetary receipts vis-a-vis 100 percent taxation, therapid growth of enterprises in Sichuan province where it was experimentallyintroduced (three to four times that of the average State enterprise)indicated that it had very positive incentive effects.

Although this development served to harden the budget constraint inState enterprises, it is nevertheless true that considerable disc.:etioncharacterizes the interpretation of tax rules. This manifests itself indeviations in practice from the 55 percent income tax rate, in the applicationof various extrabudgetary 'clawback" measures to profitable enterprises and,correspondingly, in the extension of subsidies and other preferences tofinance wage increases and bonus payments in loss-making units.

The role of discretion has been further heightened with the introductionof the contract responsibility system, which appears to provide a vehicle forextending significant tax preferences to enterprises that are able to bargainsuccessfully with the authorities. The CMRS allows tax liabilities to becontracted virtually on an enterprise-by-enterprise basis and this strengthensrather than weakens the symbiotic relationship between supervisory agenciesand State enterprises. Consider three examples: one enterprise suffered an 85percent marginal tax rate on above quota profits, another was characterized bya profit quota and a zero marginal tax rate on above quota profits, and athird had enjoyed exemption fromr both income and indirect taxes.

The tendency to so tailor tax liabilities is sometimes defended on thegrounds that variations in contract terms simply reflects variations inenterprise circumstances. Endowments of freely provided fixed assets varyacross enterprises for historical reasons, as does the mix between such assetsand more recent acquisitions which are no longer free to State enterprises.Since contracts attempt, inter alia, to encourage efficient use of fixedassets and elicit some payment to their owner, i.e., the State, it is arguedthat they must be tailor made to individual enterprise circumstances.

The introduction of a degree of discretion as high as that called for bythe above argument, however, has a number of serious disadvantages. First,enterprise-specific variations in tax payments inhibit competition and limit

24

incentives to restructure inefficient enterprises. Second, inter-provincialrivalries reflecting lack of coordination among the industrial policies of theprovinces add pressures for tax preferences via the contract responsibilitysystem, leading to erosion of tax revenue.

Finally, the inclusion of tax payments in contracts removes an importantinstrument of macroeconomic management from central government conitrol. Theproblem is exacerbated by the fact that the alleviation of ratchet effectsrequires such contracts typically to run for 3 to 4 years, thus lengtheningthe period over which direct tax instruments becomes unavailable. The existingcontracting system, while credible as an attempt to separate ownership andmicroeconomic management does not distinguish clearly between the role of thegovernment as owner of assets in State enterprises and the role of thegovernment as macroeconomic manager for the economy as a whole.

Some of these difficulties could be avoided if state enterprises paidboth direct and indirect taxes on the same basis as other categories ofenterprise, thus fulfilling their obligations to the State as a collector ofrevenue. The State as owner of the enterprises could then take some share ofthe after tax profits, and it is here that contracting can have a role inproviding incentives and allowing enterprises with different quantities offreely provided assets to make different payments to their provider.

3.4 Statutory and Effective Rates ot Tax

The statutory rate of tax may be combined with depreciation allowances,interest and principal deductibility and other provisions to calculate how thecash flow from an investment project is affected by applying the rules of theenterprise income tax. This effect is summarized in the 'marginal effectivetax rate" (METR), estimates of which are presented in Table 3.1.12, Thesefigures are best treated as illustrative. But they serve to indicate thedivergences between statutory and effective rates arising from interactionsbetween taxation, inflation and the mode of financing of investment projects.The complexities of the institutional setup governing investment ir. China,together with the pressure from enterprises to invest imply that the METR isbut one determinant of incentives to invest, particularly in Stateenterprises. With a progressive hardening of the budget constraint, however,it can be expected to assume greater importance.

Column (2) shows the METR on a project financed entirely by retainedearnings with an inflation rate of 20 percent. Large State enterprises facethe highest METRs because of their high statutory rate and an additionaltransportation and energy fee. The advantages of debt financing are shown incolumn (3) for a project financed 50 percent by debt and 50 percent byretained earnings. The sharp decline in METR for all three types ofenterprises is due to two reasons. First, the deductibility of

I1We are indebted to Tony Pellechio for performing these calculations. Themethodology is described in Pellechio (1987).

25

Table 3.1 China: Marginal Effective Tax Rates for Investment inFixed Assets by Type of Enterprise

(In percent)

10OZ financingthrough retained 50 Z debt financing;

Statutory earnings 50Z retained earningstax rate 20Z inflation 20Z inflation

Large stateenterprises 55 87.3 48.4

Small stateand collectiveenterprises 35 50.3 30.1

Individualhouseholdenterprises 40 57.5 34.6

nominal interest payments overstates true interest payments in the presence ofinflation; the decline in the real debt balance implies that a portion ofinterest payments is actually implicit repayment of principal. Second, thefact that principal repayments are also deductible confers a significant taxadvantage, and represents a major difference between enterprise income tax inChina and international practice.

Two alternative kinds of corporate taxation are considered efficient oneconomic grounds. The first, or income tax approach, tries to make taxableincome approach economic income as closely as possible. A second approachattempts to tax the enterprise on a so-called "cash flow" basis, either byusing real cash flow (r base), the difference between sales and purchases ofgoods and services, or by using real plus financial cash flow (r + f base),the difference between cash receipts (including loan proceeds) and cashexpenditures (including principal and interest payments).

Both the comprehensive income tax and the cash flow tax can be shown topreserve efficiency by neither taxing nor subsidizing debt-financed investmentat the margin. The income tax reduces both the cost of capital, comprisingdepreciation and financial costs, and profits by the rate of tax. Under thecash flow tax, the complete writeoff of investment expenditures againstenterprise taxation at the time of the investment also reduces the cost of aproject to the investor by the rate of tax, while profits from the investment

26

are taxed at the same rate. This symmetric treatment of costs and benefitsmakes the tax on marginal investments zero.>/

It is therefore seen that the tax-deductibility of principal andinterest in China embodies part of the provisiors of the real plus financialcash flow tax ("r + f base") but without including loan proceeds as part ofthe tax base. While the replacement of budgetary grants with bank loans hasbeen a step consistent with enterprise reform, this generous treatment ofamortization and interest on the latter provides very substantial incentivesto investment. This is anomalous in general but particularly so at times whenozer-investment by enterprises is considered to be a serious problem.

Most loans in China are amortized over five years. Table 3.2 providesinformation on gross fixed investment by State-owned units for the years 1982to 1986, together with the amount of domestic bank loans involved in suchinvestment. It is also known that interest rates on fixed investment lendingwere increased in 1985 by about 3 percent to somewhat over 10 percent for fiveyear funds. The left-hand side of the last column in the table presentsfigures on amortization of those loans by State enterprises in 1986, on theassumption that interest rates were 7 percent for loans extended from 1981through 1984 and 10 percent thereafter. It calculates amortization in 1986 tobe Rmb 23.92 billion.

There are instances of enterprises being allowed to repay loans overperiods longer than five years. To assess the importance of such a provision,the calculations above were reworked with a loan term of eight years. Theamortization figures for this case appear on the right-hand side of the lastcolumn in Table 3.2.

The Statistical Yearbook of China, 1987 reports that profits and taxesfrom State enterprises equalled Rmb 134.14 billion in that year, of which Rmb65.15 was taxes, leaving Rmb 68.99 billion as after- tax profits.This yieldsan effective tax rate of 49 percent = (65.15/134.14). Inclusion ofamortization on existing loans in the tax base would lead to the situationdescribed in Table 3.3.

W1 These arguments are spelt out in Atkinson and Stiglitz (1980) and King(1986).

27

Table 3.2 Amortization of Bank Loans by State-OwnedEnterprises, 1986

(Rmb billion)

1981 1982 1983 1984 1985 1986 -

Gross FixedInvestment byState-OwnedUnits a/ 101.1 120.0 136.9 183.3 254.3 302.0

of whichFinancing throughDomestic Banks 9.1 13.7 13.6 18.3 38.7 45.0

5 year 8 Year c/Term Term

Amortization of Loansextended in 1981 b/ - 1.25

1982 3.14 1.751983 2.90 1.621984 3.64 2.031985 6.94 3.681986 7.30 3.87

Total Amortization 23.92 14.20

a/ Gross fixed investment equals "investment for capital construction' and"investment for equipment renewal and technical transformation".

b/ It is assumed that the interest rate was 7 percent on loansextended in the first four years and 10 percent for those in the lasttwo years.

c/ Bank loans are taken to be zero before 1981.

28

Table 3.3 Enterprise Profitability with and withoutPrincipal Deductibility

BEFORE CHANGE IN AFTER CHANGE IN

TAX TREATMENT TAX TREATMENT

(Rmb billion)

5 Year Term b/ 8 Year Term c/

Taxable profit 134.14 134.14+23.92=158.06 134.14+14.20=148.34Taxes - 65.16 Taxes a/ = -76.77 Taxes a/ = -72.08

After taxprofit = 68.99 = 81.29 = 76.26

LESSAmortization -23.92 -14.20

Retentions = 68.99 = 57.37 = 62.06

Revenue increase 18Z 11zPercentage decline 17Z 10oin retentions

a/ Using a rate of 49 percent.b/ Calculated amortization in 1986 with 5 year term = Rmb 23.92billionc/ Calculated amortization in 1986 with 8 year term = Rmb 14.20billion

Thus a change in tax treatment of existing loans would have led for 5

and 8 year term loans respectively to increases of 18 percent and 11 percentin income tax revenue from State enterprises. There would have been

respectively a 17 percent and 10 percent decline in retentions of State

enterprises and, hence, a corresponding decline in any measure of their

profitability, whether defined vis-a-vis the value of fixed assets or relative

to sales.

This calculation embodies a number of biases. First, the cost of credit

is effective in controlling investment only if disallowance of amortization

leads to a reduction in borrowing, so that the fixed base assumption used here

in the absence of other information overestimates both the revenue gain and

the resulting decline in enterprise profitability. This is partially offset by

the fact that the figures do not take into account the situation in

collectives, where the share of bank loans is significantly higher than that

for State enterprises. Second, inasmuch as the figures for tax collections

include the adjustment tax, the average rate of income tax would have been

29

somewhat lower than 49 percent. This leads to an upward bias in the estimatesfor revenue gains but also overstates the decline in retentions.

There is, however, an important offsetting influence. The calculationsrefer to 1986, the latest year for which data were available. Inasmuch asborrowing from the banking system has been higher in 1987 and 1988 compared toprevious years, the calculations probably underestimate the proportionate gainin revenue and decline in retentiun-z by State enterprises that would occur

were the calculations to be done fo, those later years.

In summary, these calculations show that the disallowance ofamortization payments as an expense against the enterprise income tax is

likely to result in significant change in income tax revenue and enterpriseprofitability. Also, the removal of tax-deductibility of amortization wouldmake it easier to introduce a VAT of the consumption type without stimulatingexcessive investment in enterprises.

3.5 Resource Tax

The controlled price system and state provision of assets are not theonly factors that could potentially give rise to inter-enterprise inequality.Some inequality is caused by unequal access to natural resources, particularlyin the production of coal, oil, gas and minerals. This was partly alleviatedby introducing the Resource Tax in 1984 which, while it can in principle be

applied to all of these products, applies in practice only to the first three.The tax rules require the Resource Tax to be levied on profit (relative toenterprise sales) as follows. Enterprise with profit rates up to 12 percent

are exempt; those earnings between 12 to 20 percent of sales are taxed at 50percent; those between 20 to 25 percent at 60 percent; while profits in excess

of 25 percent of gross sales are taxed at 70 percent. However, frequentchanges in profitability cause the tax to be levied in practice atenterprise-specific rates related to the amount of extraction of the resourceand its quality.

The fact that it is levied on profit relativ( to sales means that the

use of some exhaustible resources (e.g., coal, oil and gas) are indeeddiscouraged by it. However, the rates of taxation are not calculated to

reflect such exhaustibility. Also, it is levied in a way that reduces theefficiency with which those resources are extracted. Efficiency in nationwide

resource extraction requires that, for each resource, the marginal cost ofextraction (including transport costs) be equal for all enterprises engaged in

extraction. This condition would be satisfied if producers wereprofit-maximizing and faced the same producer price for output. However,

since, the Resource Tax is enterprise-specific, being levied at a higher rateon more profitable enterprises, it can offer more efficient producers a lowerproducer price. The tax system can, therefore perversely encourage lessprofitable producers to expand activity even if their marginal cost is higherthan that of more profitable enterprises.

Finally, the effectiveness of taxes/charges on resource use is reducedin the presence of price controls. In a market economy, a tax on resource usewill discourage production, raise the market price and therefore discourage

30