proposed basel changes: impacts for emerging market economies · proposed basel changes: impacts...

TRANSCRIPT

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

Proposed Basel Changes: Impacts for Emerging Market Economies

SEPTEMBER 2016

Brad Carr DEPUTY DIRECTOR 1-202-857-3648 [email protected]

Jaime Vazquez POLICY ADVISOR 1-202-857-3327 [email protected]

Richard Gray SENIOR POLICY ADVISOR 1-202-857-3307 [email protected]

Several of the current BCBS proposed amendments to the regulatory capital framework, if implemented as drafted, will have pronounced impacts on Emerging Market (EM) economies, directly and indirectly impacting the various avenues available for EM borrowers to obtain finance. Whilst it is understood that this is not the intent of the BCBS’s proposed changes, these concentrated impacts emerge as a factor of the prevailing market characteristics in EMs, where for instance there is often: Heavier reliance on bank intermediation; A more prevalent role for trade finance; A dearth of externally-rated entities; Greater need for new infrastructure investment. This paper summarizes some of the key impacts for borrowers and product-types that are central to EM economies, specifically where the proposals stand to impact the provision of finance to business, as well as other financial products that are essential for the ability of EMs to generate growth. The issues highlighted here are not exhaustive, and should be viewed alongside other EM-specific impacts amongst the BCBS proposals, including those affecting the provision of consumer finance, the efforts to reduce housing shortages in some countries, and local legal specificities that impact operational risk calculations. In particular, it is noted that the anticipated impacts in operational risk in some EMs are of a magnitude that could constrain balance sheet capacity. 1. Background: Basel proposals The suite of Basel proposals includes major changes to credit risk (both under the internal models and Standardized approaches), operational risk, the Fundamental Review of the Trading Book in market risk, and the Leverage Ratio. Focusing on credit risk, the most profound changes are: An increased reliance on the SA, including the introduction of a capital

floor; noting the SA’s dependency on external credit ratings, this has pronounced impacts for economies where corporates are less likely to be externally rated

Changes within the SA on Credit Conversion Factors (CCFs), with impacts for the provision of contingent credit

The move of all exposures to Banks and Financial Institutions from the Internal Ratings Based (IRB) approach to the Standardized Approach (SA)

The move of all Specialized Lending assets from IRB internal models to the Supervisory Slotting Criteria

The downstream impact of these changes is particularly important in Emerging Markets, where domestic capital markets tend to be less developed, resulting in a greater reliance on banks (both domestic and foreign/international) to finance the Corporate and SME sectors, as shown in Figure 1.

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 2 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

Figure 1: EM Non-Financial Corporate Indebtedness1 There remains a major funding gap in numerous EMs, where foreign direct investment is not sufficient, and commercial bank lending is needed – meaning that any change in the economics for the provision of bank finance will have an amplified impact compared to most developed economies. There are compounding impacts on derivatives, from the multiple perspectives of credit risk (the IRB consultative document’s proposals for Counterparty Credit Risk), Credit Valuation Adjustment (CVA), and market risk. These stand to impact the cost and availability of hedging products, which may in turn impact access to any alternate sources of funding. 2. Trade Finance Trade is a fundamental driver of economic development, and trade finance is an essential facilitating tool, especially in emerging markets. While estimating the global volume of trade finance transactions is difficult, most estimates place it in the region of US$8-10 trillion annually.2 Risk-based pricing is crucial to trade finance: it is through reflecting the underlying risk-profile that trade products can be provided as a low-cost enabler, whilst still satisfying banks’ ROE hurdles.

1 Source: IIF EM Debt Monitor; *domestic bank loans includes those provided via shadow banking. 2 The BIS’s Committee on the Global Financial System (CGFS) indicated in its January 2014 publication, ‘Trade Finance: developments and issues’ (http://www.bis.org/publ/cgfs50.pdf ) that bank-intermediated trade finance is at about 40% of total merchandise trade, which is in turn approximately US$20 trillion (ie. US$8 trillion); the African Development Bank (http://www.afdb.org/fileadmin/uploads/afdb/Documents/Publications/Fostering_Development_Through_Trade_Finance_Brochure_-_Full_Version.pdf) estimates that Africa has US $340b in bank-intermediated trade finance whilst ac-counting for 3.3% of global trade (by extrapolation, US$10.3 trillion).

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 3 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

The typically low-risk nature of trade finance transactions reflects attributes such as: Very short-dated tenors Often strongly-rated counterparties, including (depending on the product-type) regulated banks Tangible collateral Self-liquidating nature of some products, such as the Letters of Credit (LCs) that make up the bulk of

trade finance exposures in EMs Correctly reflecting the low risk of this asset class is not only desirable for the sake of accuracy, but it also helps to direct credit towards productive investments that are critical to growth in emerging markets, as well as recovery in developed economies. It should be noted that trade finance products tend to be low margin in nature, so any increase in capital requirement will result in a reduction in the credit and contingent finance provided. It is noted that the design of several other BCBS standards (including the leverage ratio, the liquidity coverage ratio and the supervisory framework for measuring and controlling large exposures) has often recognized trade finance as an important real-economy financing product, with commensurate treatment that reflects the underlying low-risk attributes.3 The current proposals, as drafted, would reverse much of this recognition and generate potential negative unintended consequences. The most significant impact to trade finance under the current BCBS proposals would be from the shift of Bank/Financials and Large Corporates from IRB to the SA.4 The bluntness of SA risk-weights is unduly punitive against strong counterparties, and even with a (similarly blunt) concession for shorter-dated transactions, it invariably over-states risk on higher quality transactions, particularly those that are collateralized. Similarly, proposed changes to Credit Conversion Factors (CCFs) stand to have a substantial impact on contingent products. Applying a “one-size-fits-all” 50% CCF floor across the spectrum of off-balance sheet exposures would significantly overstate the true risk on trade finance products. Whether the apparent assumption might hold that SMEs’ drawings peak before a default, this is less applicable for larger corporates, and does not apply to Trade, Export and Receivables Finance activity. Trade finance instruments are subject to globally-recognized International Chamber of Commerce (ICC) rules such as the Uniform Customs and Practice for Documentary Credits, but not to consumer protection laws or reputational risk considerations that might otherwise discourage banks from canceling such commitments. The potential negative impacts on trade finance from the BCBS proposals are substantial. The ICC has conducted a high level analysis on an average trade finance portfolio broken down into bank and corporate exposures and estimated the RWA and capital movement from the current approach under IRB to the new standards proposed by the Committee.5 Summary impacts from the ICC’s analysis are shown in Table 1.

3 It should be noted, however, that the Asset Value Correlations (AVC) multiplier for exposures to finan-cial institutions under Basel III did have an adverse impact on the cost of LCs. 4 Whilst the primary focus in this paper is on the IRB and SA changes for credit risk RWA, there are also impacts in proposed changes in the leverage ratio calculation for trade finance, with a 50% CCF to be applied to certain transaction-related contingent items (eg performance bonds, bid bonds, warranties and standby letters of credit related to particular transactions), and a 20% CCF applied to both the issu-ing and confirming banks of short-term self-liquidating trade letters of credit arising from the movement of goods (eg documentary credits collateralized by the underlying shipment). 5 ICC-BAFT response letter on BCBS consultative document Reducing variation in credit risk-weighted assets - constraints on the use of internal model approaches, June 2016. Please note that the ICC pro-jections are based on a stylized hypothetical portfolio and the actual impact will vary depending on jurisdiction and institution and the portfolio breakdown between classes of bank and corporate expo-sures.

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 4 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

Table 1: ICC Sample portfolio impacts (all numbers in US$ thousands)

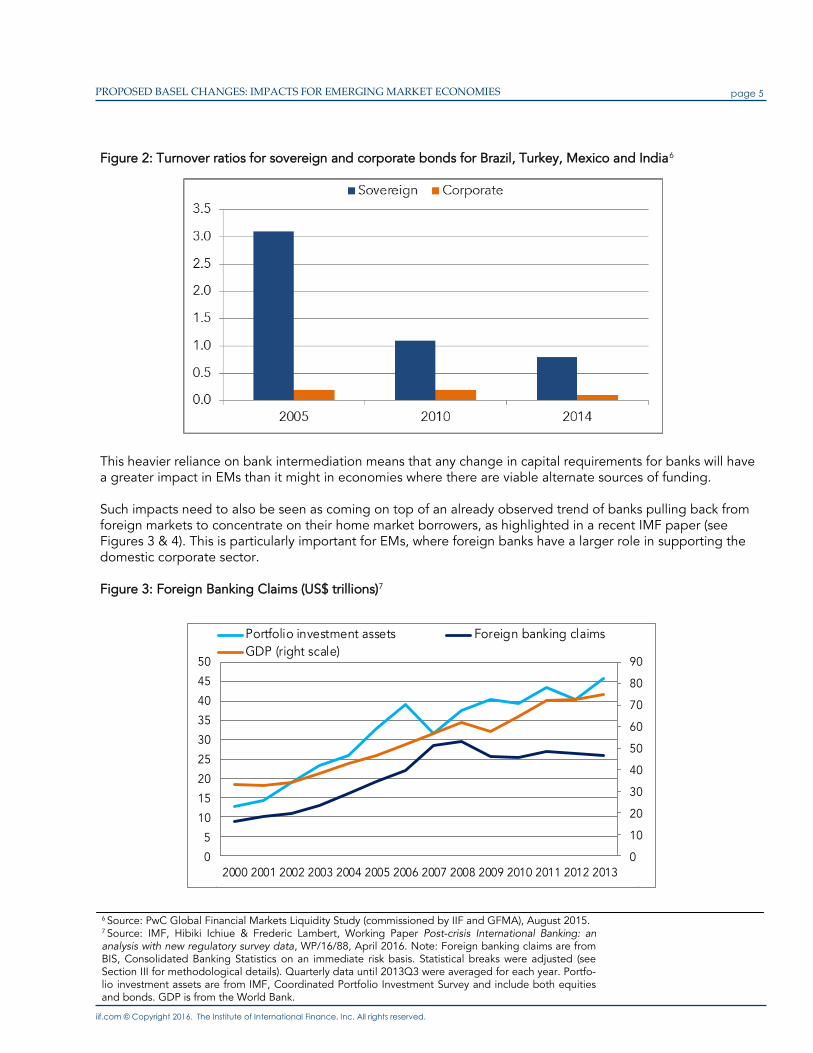

For bank exposures, the RWA expected for the highest rated exposures could feasibly triple or quadruple, whereas that impact is muted for entities rated B+ and below. A similar picture emerges for corporate exposures, with the BCBS proposals providing a range of scenarios depending on the corporate’s scale, each of which have distorted impacts across risk grades. 3. Corporate Borrowing The current BCBS proposals need to be considered in the particular market context of EM economies. Firstly, most EMs tend to not have active domestic corporate bond markets, with a consequential reliance on bank intermediation to finance the Corporate and SME sectors, whether with local or foreign/international banks, as was shown in Figure 1. To the extent that there are domestic markets for bonds, these tend to be illiquid, and likely to suffer from further reductions in their liquidity, with falling turnover ratios indicating a lack of market depth (see Figure 2).

Counterparty Type Rating scale

RWA based on current parameters

RWA based on proposed

changes

Expected RWA

movement (USD)

Expected RWA

movement (%)

Banks

AAA to AA- 55 181 +126 +230% A+ to A- 19,378 95,159 +75,781 +391% BBB+ to BB- 12,155 20,621 +8,466 +70% B+ and below 210 214 +4 +2%

Corporates: as-sets >€50b

AAA to AA- 447 2,957 +2,510 +562%

A+ to A- 14,856 74,104 +59,248 +399%

BBB+ to BB- 312,198 414,095 +101,897 +33%

B+ and below 54,203 46,157 +8,046 +15%

Corporates: as-sets≤€50b, turno-ver>€200m

AAA to AA- - -

A+ to A- 2,848 8,043 +5,194 +182%

BBB+ to BB- 259,179 320,672 +61,493 +24%

B+ and below 75,893 112,160 +36,267 +48%

Corporates: as-sets≤€50b, turno-ver<€200m

AAA to AA- - -

A+ to A- 1,431 2,440 +1,008 +70%

BBB+ to BB- 87,237 106,733 +19,496 +22%

B+ and below 25,424 45,964 +20,540 +81%

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 5 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

Figure 2: Turnover ratios for sovereign and corporate bonds for Brazil, Turkey, Mexico and India6

This heavier reliance on bank intermediation means that any change in capital requirements for banks will have a greater impact in EMs than it might in economies where there are viable alternate sources of funding. Such impacts need to also be seen as coming on top of an already observed trend of banks pulling back from foreign markets to concentrate on their home market borrowers, as highlighted in a recent IMF paper (see Figures 3 & 4). This is particularly important for EMs, where foreign banks have a larger role in supporting the domestic corporate sector. Figure 3: Foreign Banking Claims (US$ trillions)7

6 Source: PwC Global Financial Markets Liquidity Study (commissioned by IIF and GFMA), August 2015. 7 Source: IMF, Hibiki Ichiue & Frederic Lambert, Working Paper Post-crisis International Banking: an analysis with new regulatory survey data, WP/16/88, April 2016. Note: Foreign banking claims are from BIS, Consolidated Banking Statistics on an immediate risk basis. Statistical breaks were adjusted (see Section III for methodological details). Quarterly data until 2013Q3 were averaged for each year. Portfo-lio investment assets are from IMF, Coordinated Portfolio Investment Survey and include both equities and bonds. GDP is from the World Bank.

0

10

20

30

40

50

60

70

80

90

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Portfolio investment assets Foreign banking claims

GDP (right scale)

0

10

20

30

40

50

60

70

80

90

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Portfolio investment assets Foreign banking claims

GDP (right scale)

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 6 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

Figure 4: Foreign Banking Claims Relative to Total Banking Assets of Host Countries (percent)8

Secondly, the role of international banks in EM economies means that the potential impacts of the BCBS proposals extend well beyond the customers served in the home jurisdictions of IRB-accredited banks. As international banks look across their global portfolios in responding to proposed changes that place a greater reliance on the SA, the centrality of external ratings to the SA’s risk-weights means that EMs are more susceptible to adverse outcomes. As shown in Figure 5, corporates in many EMs typically do not have external credit ratings, in particular in Asia-Pacific, the Middle-East and Africa. Figure 5: Non-Financial Corporates with No External Credit Rating9

8 Source: IMF, Hibiki Ichiue & Frederic Lambert, Working Paper Post-crisis International Banking: an analysis with new regulatory survey data, WP/16/88, April 2016. Note: Foreign banking claims are from BIS, Consolidated Banking Statistics on an immediate risk basis. Statistical breaks were adjusted (see Section III for methodological details). Total banking assets are from IMF, International Financial Statis-tics. The data are used only when both foreign banking claims and total banking assets in a given coun-try are available for each quarter. Quarterly data until 2013Q3 were averaged for each year. The ratio is calculated by dividing total foreign banking claims by total bank assets for all host countries.

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 7 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

The BCBS proposals on IRB contain two items of particular relevance for Corporate borrowers in EMs: Large corporates and their subsidiaries move from IRB to the SA (ie. subject to the risk-weights as

prescribed under the SA) Other corporates and SMEs become subject to a capital floor based on the SA Whilst it is true that there are few corporates defined as “large” (consolidated groups with total assets greater than €50b) domiciled in EMs, the inclusion of subsidiaries is significant. The proposed treatment would require banks to apply the SA to each entity within the group, including what might be smaller subsidiaries based in EMs. While the scenario of a rated parent and unrated subsidiaries can occur in all economies, it is particularly common in EMs where ratings are less prevalent. Consequently, the EM subsidiary of a large corporate would be subject to the 100% risk-weight applicable for unrated corporates under the SA, irrespective of its own creditworthiness or the degree of parental support. But even for corporate borrowers that are independent and fall below that €50b total assets threshold, the capital floor means that the SA’s punitive treatment for unrated corporates still looms large. See Box 1 for an illustration of how the proposed framework can have a disproportionate impact on developing economies, disincentivizing global banks from banking the corporate sector in EMs, and putting EM companies at a potential disadvantage in the pricing of their financing.

The high risk-weights applicable under the SA also serve to deter banks from underwriting or making markets, further exacerbating EM corporates’ limited access to capital markets. Indeed, even where the proposed SA makes provision for banks in countries (such as the United States) that do not allow external ratings for the use of a slightly lower risk-weight for “investment grade” corporates, eligibility for this treatment requires that a corporate have securities traded in a recognized exchange. This again leaves out the majority of EM large corporates.

9 Non-financial corporates that do not have a rating with at least one of Moody’s, Fitch or S&P. Source: IIF, Bloomberg.

Box 1: Example Consider the scenario of an international bank that lends to two Corporates, A & B, as follows: Both Corporate A & Corporate B are of equal creditworthiness, each currently incurring

an IRB risk-weight of 30% Corporate A is domiciled in a developed economy and has an external credit rating,

whereas Corporate B is based in an EM and is not externally rated Under the SA, Corporate A would have a risk-weight of 50%, whereas Corporate B (being

unrated) would have a 100% risk-weight Applying a capital floor at a level of 60% (ie. the lower end of the 60-90% range stipulat-

ed in the BCBS consultation) would result in an effective risk-weight of 30% for Corporate A and 60% for Corporate B

In this example, an international bank can continue lending to Corporate A (perhaps domiciled in their own home market) as though nothing has really changed, but it will see a doubling in the capital requirement (and a halving in ROE) for loans to its EM client. The bank will need to either increase the margin it charges its EM client (to preserve ROE), or exit that business.

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 8 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

It is also noted that the BCBS’s proposed changes to the SA would require a further add-on of 50% (up to a maximum of a 150% risk-weight) for unhedged loans made in foreign currencies where it cannot be demonstrated that the borrower generates income in the loan currency. This proposal has a further disproportionate impact on EMs, with lending in USD (for instance) commonplace in some regions, and hedging costs set to increase as a result of other proposals (see Section 4). Whilst it is acknowledged that a currency mismatch is an additional source of risk that should be accounted for, this forms part of the rating and due diligence process, so an add-on could in fact be double-counting for this risk. Moreover, an add-on level of 50% appears excessive, particularly given the already high baseline set of SA risk-weights that would apply in EMs. 4. Corporate Hedging Noting the limited opportunities to borrow in domestic capital markets, and the potential headwinds for bank disintermediation from the BCBS proposals on banking book credit risk, some EM corporates may increasingly turn to capital markets in the US (eg. the 144A market), Europe or Japan for their funding. But these funding sources aren’t immune from the BCBS regulatory impacts either. Where an EM corporate raises funds in one of the world’s major capital markets, it typically does so denominated in USD, EUR, GBP or JPY. Depending on their industry and export profile, using that funding in support of domestic operations will then typically require that corporate to get a cross-currency swap, generally matched to the term of the bond issue. The measures adopted for derivatives since the crisis, including Basel 2.5 and Basel III, have had a profound impact in improving risk coverage and ensuring the safety and soundness of the system. They have also had their largest impacts on particular products, most notably those that are long-dated trades and that involve a principal exchange: ie. cross-currency swaps. The proposed changes in Credit Valuation Adjustment, Counterparty Credit Risk and the Fundamental Review of the Trading Book stand to compound these impacts, increasing capital requirements and encouraging banks to generate higher margins or fees attached to trades or to even reconsider continued participation in certain markets or products. With the removal of IMA-CVA, the current proposed framework leaves banks with two options, the Standardized Approach (SA-CVA) and the Basic Approach (BA-CVA). The SA-CVA approach is conceptually stronger than current approaches, but it would be problematic if this was calibrated without notable emerging market involvement. With the absence of liquid credit markets for EM counterparties, proxy hedges are often the only options for hedging the credit component of CVA. Furthermore, in order to be able to apply SA-CVA banks need to meet qualifying requirements, including a dedicated CVA desk and capacity to calculate CVA sensitivities. Consequently banks in EMs (including some foreign banks operating there) would likely have to apply BA-CVA which would result in a capital requirement which is several times the requirement under Basel III CVA. Consequently the cost of risk mitigation in such markets will be significantly increased, reducing the financing efficiency of local capital markets. The cost of derivative hedging can form a material portion of the total term financing costs, and a significant CVA charge for long dated derivatives, compounds the impacts of the proposals on reducing variation in credit RWA, in particular for the infrastructure projects on which emerging markets rely (refer Section 5).

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 9 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

The new SA-CCR regulations are more penal for uncollateralized trades, particularly long-dated transactions, and more beneficial for collateralized business. This has a pronounced impact in EMs where a larger portion of the market is likely to be uncollateralized (especially with the lower access to funding sources required for collateralization). Furthermore, banks operating in these markets are likely to have smaller less diversified portfolios, and the structure of SA-CCR is such that the capital treatment is likely to be more punitive for less diversified, more directional derivative portfolios. Compounding these CCR and CVA requirements, new FRTB standards for model approvals will become complex and costly, and requiring further investment in IT systems. In smaller countries or those with less developed capital markets, this may be uneconomical, even for large banking groups operating in those jurisdictions. The extent of uncertainty about meeting the P&L Attribution Tests and the consequent risk of cliff effects will give organizations cause to reconsider continued participation in non-core markets and products. Even considered in isolation, these reforms are likely to present significant challenges in EM economies, for both local banking organizations and international banks operating in these markets. However when considered in combination, these impacts are amplified, with many banks likely to withdraw from certain products or even entire markets, reducing the breadth and depth of these markets. 5. Infrastructure The adverse treatments proposed for the Specialized Lending asset classes will particularly impact on the ability of commercial banks to assist in the financing of key infrastructural developments. Infrastructural development remains critical to the growth of developing economies. With growing populations, urbanization and globalization, the demand for power, water, roads and railways and other key infrastructural developments is increasing rapidly in EMs. A recent World Bank Group study identified that the necessary investment in infrastructure in EMs over the next decade is around US$2 trillion annually, around double the current level.10

Each transaction presents a different risk profile and ought to be treated differently from other asset class exposures. The proposal to disallow the IRB approach for Specialized Lending has the potential to constrain capital from commercial banks, which will hinder growth in emerging markets. As outlined in the IIF submission on the BCBS IRB consultative document, it is acknowledged that infrastructure has a smaller volume of historical defaults (compared to the corporate, SME and retail sectors) available to form the basis of risk modeling, and that this is compounded by the very individualized deal structures that often apply.11 However, this same tendency towards very individualized deal structures also means that a simple, straitjacketed approach is grossly inappropriate for these types of assets, and does not give an accurate reflection of underlying risk levels. Indeed, structures are often put in place so that the lender not only controls the cash flows generated from the underlying asset but also benefits from the security of the asset itself, leading to lower loss rates. Banks can structure loans with conservative terms and Loan to Valuation (LTV) ratios, and tight collateral structures, or with higher LTVs and looser ones. Other variables include:

10 Inderst G. and Stewart, F. (2014). Institutional Investment in Infrastructure in Emerging Markets and Developing Economies, Public-Private Infrastructure Advisory Facility (PPIAF), World Bank Group; http://www.ppiaf.org/sites/ppiaf.org/files/publication/PPIAF-Institutional-Investors-final-web.pdf 11 IIF response letter, June 3, 2016, https://www.iif.com/publication/regulatory-comment-letter/iif-response-basel-committee-proposal-internal-modeling-credit

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 10 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

The level of equity or subordinated mezzanine debt that ranks below the bank debt facility; Whether there is a long-term off-take agreement in place with a high-grade offtaker; Essential infrastructure (eg. water, power) and social infrastructure (eg. schools, hospitals) projects for

which the cash flows are contracted to be paid by the government on an availability fee basis; Whether the project has commercial or patronage risk, or is a monopolist provider of essential services; The presence of other risk mitigation instruments, such as guarantees (eg. guarantees provided by

Export Credit Agencies are common in EMs). The capital framework should have the ability to reflect these dimensions, with sufficient granularity, and avoiding the over-statement of risk on the strongest assets, in particular those with valuable collateral. Slotting by definition is a less risk sensitive approach to determine the risk of an exposure. The current Supervisory Slotting approach is not capable of differentiating between the various individual deal structures, is overly conservative, and risks causing undesired cliff effects. With a minimum risk-weight of 70%, and all performing assets falling in the range of 70-115%, it really supports only a very narrow range of risks. Furthermore, observed default and recovery data collated by Global Credit Data supports the view that typical, comparable risk weights for Specialized Lending should be lower than those for unsecured corporate exposure (see Table 2). Table 2: Observed PD, LGD and implied risk-weight data (2003-2013)12

Whilst this paper focuses on the ‘infrastructure gap’ in EMs, it is noted that there is a similar ‘housing deficit’ in several EMs, and the similarly blunt treatment of Acquisition, Development and Construction (ADC) financing under the SA would impact the ability of banks to finance such developments. While the financing of speculative land development is indeed a higher-risk activity, it would appear inappropriate to extend a flat 150% risk-weight to products with a proven low-risk record, such as the Plano Empresario scheme in Brazil.13

6. Alternate Remedies The potential impact of the BCBS initiatives on the ability of EMs to generate growth warrants the examination of possible changes to those proposals. The IIF’s various submissions on the BCBS’s Consultative Documents this year have included a number of alternate proposals, supporting the BCBS’s objectives of reducing RWA variance and improving comparability, whilst seeking to avoid a loss in risk-sensitivity and a significant increase in capital requirements, as well as deleterious effects on EMs as outlined above. This follows the considerable investment and comprehensive analysis previously undertaken by the IIF RWA Task Force. Following the recent IIF-ISDA Cumulative Capital Impact study, the IIF provided an extensive set of alternate proposals and scenarios that warranted further examination. As a subset of such alternatives, some particular alternate proposals for credit risk that could help mitigate the envisaged impacts for EMs include the following:

12 Source: Global Credit Data. 13 Plano Empresario refers to a specific low-risk form of Land Acquisition, Development and Construction in Brazil, where the development project is embedded in a SPV structure, ring-fenced from instability or bankruptcy in the parent company. The SPV receives all cash flows from creditors and clients (sales), and throughout he construction phase, all resources are exclusively available to finish the project. In the event that the parent company faces financial problems, with potential impacts to the project, creditors have the right to substitute the sponsor to ensure its completion.

Borrower Grade (or equivalent)

Corporate Specialized Lending

PD LGD Maturity IRB RWA PD LGD Maturity IRB RWA

BB+ 0.75% 40% 3 years 83.8% 0.66% 25% 5 years 64.2%

BBB- 0.42% 40% 3 years 65.8% 0.42% 25% 5 years 54.3%

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 11 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

SA for Banks

Change the base risk weights between A and BBB rated banks. Currently the risk weights for both buckets are 50%, but the risk weight for banks rated A could be amended to 20% or 30%.

Extend the “short term” treatment to apply to all trade finance and money market trans-actions, including those that extend beyond a 3-month tenor.

SA for Cor-porates

Adjust the risk-weight of BBB exposures (BBB+ to BBB-) from 100% (which is the same as BB, ie. non-investment grade), to either (i) 50%, same as other investment-grade (A) ex-posures, or (ii) to a new additional bucket at 75%.

For unrated corporates, replace the flat 100% risk-weight for unrated exposures with the same 4-buckets approach that have been recommended for Bank exposures, with risk-weights of 20%, 50%, 100% and 150%.

Provide for adjustments to risk-weights based on maturity and seniority, recognizing that shorter-dated exposures and senior, secured exposures are relatively less risky. Please see Appendix A for more details.

IRB for Banks and Financial Institutions

Granular Bucketing/Slotting Approach: (i) create a series of 7-8 risk buckets, with suffi-cient width and granularity; (ii) banks continue using their internal models for the purpose of establishing which risk bucket each exposure will go in to.

Foundation IRB or similar, removing LGD modeling, and allowing firms the facility’s actu-al maturity to be applied, with the Maturity Floor Waiver (MFW) of 2011 for Trade Fi-nance to be preserved.

Constrained IRB Modelling: apply a set of (i) banks’ internal ratings mapped to regulator-defined PDs, (ii) granular, supervisor-defined LGDs which depend on seniority and securi-ty, and (iii) actual maturity values.

IRB for Large Cor-porates

Foundation IRB or similar, removing LGD modeling, and allowing firms the facility’s actu-al maturity to be applied, with the Maturity Floor Waiver (MFW) of 2011 for Trade Fi-nance to be preserved.

Where multiple approaches (eg. IRB, SA) are envisaged, apply differentiating thresholds according to the size of the counterparty rather than the group.

IRB for Spe-cialized Lending

Expanded Slotting Approach: expand the series of ‘slots’ to (for instance) 20%, 30%, 50%, 70%, 100%, 120%, 150% & 200%, with consideration of PD and LGD drivers and Maturity in the assignment of assets to those slots. This brings greater granularity and is consistent with other BCBS documents that have advocated having at least 7 risk grades. Please see Appendix B for more details.

CCFs

Not apply a 50% CCF floor to trade finance products.

Clarify that the CCF of 20% for Documentary Letters of Credit and 50% for transaction related contingent items applicable under the revised SA will also be available under Foundation IRB.

Capital Floor

Not apply an output floor.

Calibrate a floor at a lower level (eg. 50%).

Have the floor’s baseline (ie. the SA) materially adjusted to a lower level, and (ideally) a greater degree of risk-sensitivity.

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 12 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

Appendix A: Enhanced Standardized Approach proposal - illustrative multipliers and risk-weighs for corporate exposures

iif.com © Copyright 2016. The Institute of International Finance, Inc. All rights reserved.

page 13 PROPOSED BASEL CHANGES: IMPACTS FOR EMERGING MARKET ECONOMIES

Appendix B: Expanded Slotting Criteria for Specialized Lending In the IIF’s response letter on the BCBS internal models consultation document, the IIF proposed that an expanded, more granular slotting criteria be applied for Specialized Lending. In such a scenario, banks could use their IRB internal models to assign individual assets to their respective slots, as already happens in those jurisdictions that currently use the Slotting approach. The expanded slots could be 20%, 30%, 50%, 70%, 100%, 120% ,150% & 200% - a series that is supported by S&P and Moody’s data, as follows:

1. S&P Project Finance data consortium indicates an average default rate of 1.39% and an average recovery rate in the range of 74%-84%14

2. Moody’s Project Finance data consortium indicates an average default rate of 1.54% and an average recovery rate in the range of 76%-100%15

3. S&P’s default case study report indicates an average Probability of Default (PD) for A, BBB, BB, B, CCC or below rated project finance exposures of 0.13%, 0.30%, 0.90%, 3.60%, 17.6%,respectively16

From these default and recovery rates, indicative risk-weights can be calculated using the IRB formula. Matching the 5-year PDs aligns to our proposed series of expanded slots, as follows:

14 S&P Annual Global Project Finance Default & Recovery Study: see average default and recovery rates for Project Finance (1999-2014). 15 Moody’s, Default and Recovery Rates for Project Finance Bank Loans, 1983-2014; see Average default rate (1990-2014). 16 S&P, 2014 Annual Global Corporate Default Study And Rating Transitions; see average default rate for corporate exposures.