emerging economies and the impacts of globalized trade and investment on forests and...

TRANSCRIPT

Emerging economies and the impacts of globalized

trade and investment on forests and forest-

dependent communitiesD. Andrew Wardell, CIFOR

CIFOR Side Event, UNIKIS, Kisangani – 7 June 2014

Emerging economies and the impacts of globalized

trade and investment - Overview

History matters

34

12 China in Africa – dispelling some myths

Case studies - Gabon and Ghana

Opportunities through Aid-for-Trade

Global context - WTO International Trade Statistics 2011

F1

F2

F3

F1 = Forest products, world, 245 US$ bn

F2 = Roundwood & sawnwood, world, 50 US$ bn

F3 = Roundwood & sawnwood, Africa, 2 US$ bnSource: FAO Forest products yearbook 2011

Global developments 1960-2010B

illio

n p

eo

ple

Source: Holmgren, 2013

What to expect

9.6 billion people in 2050

Changing consumption patterns

Continued economic growth

Growing expectations of justice and equity

Migrations to seek new opportunities

Increased climate variability

Growing demand for food, fibre, fodder and fuel

(notably BRICS)

Continued deforestation but at a lower rate

EU impact on deforestation

Only 2% of global deforestation

attributed to logging

0.7 Mha/year of deforestation

caused by EU27 imports

cf. Tropical Forest Alliance

aiming for “Zero deforestation”

through commodity chains

History matters1

Major shifts in dominant producing

regions, 1900-2000

CocoaBananas

Rubber

Oil palm

Source: Byerlee and Rueda, 2013

Map indicates colonial boundaries in 1900

Rubber

1900Wild harvest—Congo,

Amazon

Major human rights issues!

1900-1914Plantation rubber Malaysia

> 1920Southeast Asia

Smallholders share 85%0

10

20

30

40

50

60

70

80

1900 1910 1930 1950 1970 1990 2010

% share of production

Americas

Africa

Malaysia

Indonesia

Other SE Asia

Source: Byerlee and Rueda, 2013

Oil palm

1900 Wild palm West Africa by

smallholders

> 1911Unilever rejected Nigeria

Congo--First large plantations

> 1920 Sumatra plantations

> 1965Malaysia plantations

> 1990 Indonesia (40% smallholders)

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

1910 1930 1950 1970 1990 2010

Percent export shares of the world palm oil market

Congo

Indonesia

MalaysiaNigeria

Source: Byerlee and Rueda, 2013

Agricultural certification – slow progress

Status

Bananas Chiquita 100% RFA certified

Oil palm 14% RSPO certified in 2012

Rubber < 5% certifiedOpportunity for premium eco-certification in agroforestry systems

Cocoa < 5% certified (Sub-Saharan Africa)Opportunity for premium eco-certification in agroforestry systems

Lessons learned

• Perceived low value of forests, and hence dominant ethos:

deforestation = development

• Long history of concerns about land use for tropical exports

Land and forest rights

- Slow and lacked international agreements and institutions

- Championed by civil society + sometimes colonial governments and private

companies

Ecosystem services of forests

- Late comer (at global level) but rapid progress in agreements

- Initially championed by science

• Progressive shift to smallholder production systems

• Prevailing ‘standards’ have often had major impact on how and

where produced

Need for international minimum standards to avoid a ‘race to the bottom’

• Weak institutions, lack of resources, and vested interests are

recurring themes in implementation

China in Africa – dispelling some myths 2

Global

Source: Adapted from Lua Xinjian, 2010

• 1,950 million ha of forest

area

• Total stock of forest is

13.7 billion cubic meter

Key challenges for China

Forest Area 3-4% of the world

Land Area 7% of the world

Population 22% of the world

Production and living demand

Ecological conservation

Source: Lua Xinjian, 2010

Poverty reduction and economic development

Chinese forest products – imports and exports

Source: Lua Xinjian, 2010

Evolution of China’s OFDI Policy

• Phase 1: 1979-1990: Tentative development

• China formally recognized the legal status of overseas

investments and several tentative but favourable

policies were developed to facilitate OFDI activities

• Phase 2: 1991-2001: Sporadic development

• Restrictive policies were developed to control

predominantly large-scale investments

• Phase 3: 2002 to 2011: Fast and stable development

• “Going out” strategy was implemented and the whole

policy system was reformed to promote ODFI.

Regulatory activities were also strengthened

• Phase 4: April 2011-present: First White Paper on Foreign

Aid (State Council)

Source: Adapted from CIFOR, 2011

Preliminary findings

• China’s imports from Africa in 2008 (petroleum - ca.

US$40b; mining - ca. US$7b; and forestry - ca. US$1b)

• Almost half of all African timber exports from Gabon

• China’s OFDI in Africa grew from ca. US$1b in 2000 to

over US$56b in 2009

• 30% of investments in the mining sector (2009)

• 16% of investments in agriculture, forestry, fisheries

and animal husbandry (2009)

• Chinese firms (and SMEs) also investing in banks,

manufacturing, telecommunications and retailing

• “Chinese infrastructure projects are knitting the

African continent together from wireless networks to

roads and bridges” (Brautigam, 9/2/2012)

Dispelling some myths

• The West is worried (again) about Chinese investment

in Africa (cf. veiled references to the danger of

Africa’s “new colonialists”)

• But little evidence to support alleged large-scale

Chinese land grabbing,

• to suggest that Chinese firms (or companies from

other BRICS countries) operate with any different

standards than their European or North American

counterparts,

• to indicate that Chinese companies are investing

more or less than Western firms in countries ruled by

unsavoury regimes and

• to affirm that Chinese companies bring in all their own

workers (but depends on type of investment)

Understanding Chinese investments

• Chinese investments are not simply motivated by short-

term commercial and strategic interests but by broader

and longer-term interests

• But methodological challenges remain in terms of being

able to identify and distinguish between different types

of Chinese investment and investors in e.g. Ethiopia

which include Huajian (shoe factory), Sino-Ethiopian

Associates (pharmaceutical joint venture) and David

Huang’s (7 ha farm producing vegetables for the

growing Chinese population) and the extent to which

each has benefited (or not) from state-financing

• Need for greater recognition of China’s own efforts to

comply with international standards cf. the new

Forest Certification Scheme

China’s Forest Certification Scheme

Source: Lua Xinjian, 2010

Case study – Gabon

3

Gabon – supplying logs to China

• Investment Charter, 1998 and Private Investment

Promotion Agency (APIP), 2000

• New Forest Law, 016, 2001

• Gabon – largest African supplier of logs to China until

logging ban introduced in 2010

• Chinese companies currently own 121 concession

permits (out of total of 500 active permits) to manage

and log 2.67 million ha of forestland esp. in the Province

of Ogooue Ivindo (half of which belong to 5 companies)

• Annual timber exports ca. 1 million m3 (70% of total)

• Timber investments by private companies and

individuals (not known if backed by Chinese

development banks or not)

Timber Exports to China - Gabon, Cameroon and DRC,

1998-2009 (million US$)

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

450.00

199819992000200120022003200420052006200720082009

YEAR

USD

(m

illi

on

s)

0.10

1.00

10.00

100.00

1000.00

199819992000200120022003200420052006200720082009

YEAR

USD

(m

illi

on

s)

Gabon

Cameroon

DRC

Gabon

Cameroon

DRC

Normal scale Log scale

Source: CIFOR WP #

Chinese OFDI - Gabon

Gabon – shifting investments in forestry

• Investors must enter into a ‘provisional convention of

management, exploitation and transformation’ (CPAET -

Forest Law, Art. 23)

• 3 types of logging permit viz., CFAD (SFM concession);

PFA (Gabonese forestry associates permit), and PGG

(over-the-counter permit)

• By 2010 Gabon had 7m ha (CPAETs), 3.4m (CFADs with

approved management plans) and 5 concessions owned

by 2 companies under FSC certification (1.3m ha)

• Special Economic Zone jointly managed by Gabonese

government and Olam

• Olam owns 400,000 ha of timber concessions in Gabon

• Now targeting companies for investments in processing

in wake of 2010 logging ban

Special Economic Zone - Gabon

Gabon SEZ strategically located at Nkok offers optimum logistic advantage by way multiple

connectivity port Owendo 30 Km from the site, nearest rail connectivity from Ntoum and Owendo,

nearest national highway RN 1 connecting just 500m away from northern boundary of the site.

Fiscal incentives

Income Tax holiday for 10 yrs & then concessional tax of 10% for next 5 yrs

Complete waiver on import of material & export of manufactured product

Duty exemptions on import of Plant &Machinery and spares

Exemption of VAT (Value Added Tax)

Relaxations & waivers

50% concession on power tariff

100% repatriation of funds

Relaxed labour laws

Up to 5% DTA sales permitted without any tax implication

Common infrastructure

Water treatment plant

Sewage & effluent treatment plant

Common Log Park

Common Dry kiln facility

A 15 MW capacity Eco-friendly Co-gen power plant to generate power from the wood waste

generated in the zone.

Forest Concessions offered to the units

The forest concession under sustainable management which can cover a surface area between

50,000 ha and 200,000 ha.

A single logging company can be granted many CFADs, however the cumulative area granted to one

company cannot exceed 600,000 ha.

Regulatory and statutory clearances

Gabon SEZ would facilitate to obtain all such necessary regulatory and statutory clearances

required for setting up an industry in Gabon SEZ from various government departments of Gabon

by way of single window clearance approach, simplifying the process in granting speedy approvals

to the units.

Forest concessions - Gabon

Source: Projet d’accompagnement des petits permis forestier gabonais (PAPPFG, 2010)

Gabon – acquiring logging rights

• Chinese companies use diverse ways to obtain logging

rights sometimes in the ‘margins of the law’ including:

• Acquisition of multiple PFAs

• Purchase of larger established companies e.g. Leroy

Gabon – Plyrosol (by Honest Timber) and Gabon Export

Bois (by Shengyang group: Euro 68m for a 1.47m ha

concession)

• Renting rights from French companies in anticipation of

a planned acquisition

• Other alleged violations include i.a. failure to pay area

taxes, illegal logging of national parks bordering

concessions, logging of trees below the legal minimum

diameter, improper documentation of timber and incorrect

listing of volumes on waybills

New opportunities through Aid-for-Trade?

4

What is Aid-for-Trade?

Aid-for-Trade (AfT) launched in 2005

5 AfT categories:

• Trade-related infrastructure

• Support to trade policy and regulations

• Addressing trade-related adjustment costs

• Building productive capacity

• Trade development

Increased from US$20.6b in 2006 to US$32.1b in 2010

OECD and emerging companies contribute to AfT

Sub-Saharan Africa largest regional recipient

AfT help LICs and LDCs to reduce reliance on aid and...

...ensure trade delivers growth, jobs and structural

economic reformsSource: Basnett and Engel, 2013

Aid for trade – lessons learned

3rd review (2011) based on 270 cases identified need to

target:

• reducing costs of trading

• improving administrative procedures (such as border

clearing times, and times to register a new business or

obtain certificates of origin)

• binding constraints to growth (inc. infrastructure, skills,

transport and energy costs)

• blending financial instruments to address trade-related

constraints at transnational and regional levels

• More effective coordination between (and within) donors

and recipient country institutions at design,

implementation and monitoring of AfT initiatives Source: Basnett et al, 2012

Conclusions

• China successfully promoted domestic growth by combining state

intervention and private investment

• China has, more recently, successfully applied a similar model

during the evolution of the country’s OFDI in Africa

• History does matter particularly in terms of securing access to land

and resource extraction rights

• China’s trade in tropical timber is relatively small in the bigger

picture

• Much of what “everyone knows” about Chinese investment in Africa

is simply wrong (Brautigam, 2012)

• But need for caution given some evidence of continued illegality in

the forest sector

• Aid for Trade can help ensure trade delivers growth, jobs and

structural economic change, and more effectively leverage private

investments

Focus remains on wood supplies.....

...although significant trade in NTFPs (e.g. Cameroon)

613,600,000

378,641,309

12,197,503

8,089,580

4,040,000

2,874,928

2,799,330

1,574,661

989,504

847,182

730,325

585,586

430,639

284,013

269,083

249,938

244,420

171,175

124,489

94,803

61,105

31,500

18,000

11,868

5,911

78.9

1 10 100 1,000 10,000 100,000 1,000,000 10,000,000 100,000,000 1,000,000,000

Fish (catfish and other species)

Fuelwood (wood, charcoal and chips)

Gnetum africanum, Gnetum buchholzianum

Irvingia gabonensis, Irvingia wombulu

Acacia senegal, Acacia polyacantha

Prunus africana

Bushmeat

Raphia spp.

Dacryodes edulis

Pausinystalia johimbe

Ricinodendron heudelotii

Voacanga africana

Cola nitida

Ratan

Cola acuminata

Garcinia kola

Beekeeping: bee wax

Garcinia lucida

Tetrapleura tetraptera

Rauvolfia vomitoria

Beekeeping: honey

Cinchona spp.

Kigelia africana

Baillonella toxisperma

Carpolobia lutea, Carpolobia albea

Piper guineensis

$

New research initiatives

Emerging countries (Brazil, China, Malaysia and

Indonesia) in transition to a green economy: Will it make a

difference for forests and people in the Mekong, Sub-

Saharan Africa and Western Amazon regions?

Building enabling legal frameworks for low carbon

investment in sustainable land-use (IDLO-CIFOR, initially

focusing on Tanzania, Mozambique and Zambia)

Corporate governance in the oil palm and domestic timber

sectors

Evidence-based forestry

Initiated by CIFOR, CATIE, ICRAF, CIRAD, IUFRO

and University of Oxford

Broad collaboration anticipated

1. Determining priority policy-relevant questions

2. Systematic reviews to analyse evidence

Evidence-based forestry initiative

Initial tranche of systematic reviews as of 14 June 2013

1. Does production of oil palm, soybean and jatropha lead to the loss of biodiversity and ecosystem functions in tropics due to deforestation and fragmentation?

2. Environmental impacts of different property regimes.

3. Forests sustaining agriculture: the contribution of forest-based ecosystem services to agricultural production

4. Gender, Forests and Food security

5. Alternative livelihoods and biodiversity conservation for evidence-based policy

6. What are appropriate criteria and indicators for defining and measuring research quality in the realm of applied natural resources management?

7. What is the potential role of land use change dynamics in miombo woodlands in relation to REDD+?

Linking forestry and bigger-picture policies

Political

relevance

Positive

contributions

Not only

problems

Sustainable Development

“Big 5”

THANK YOU

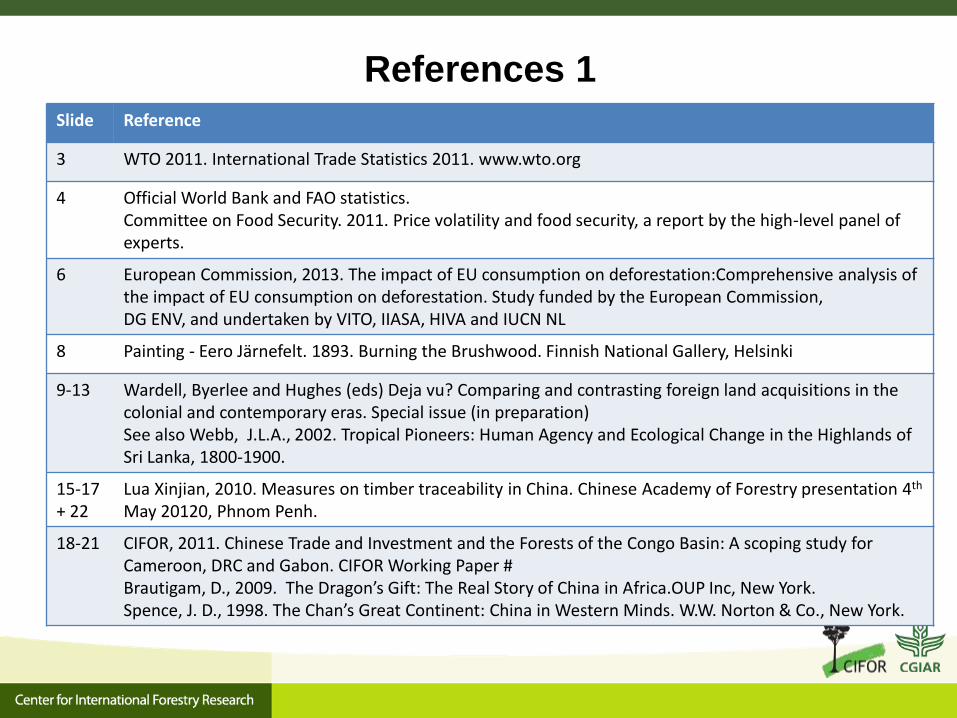

References 1

Slide Reference

3 WTO 2011. International Trade Statistics 2011. www.wto.org

4 Official World Bank and FAO statistics.Committee on Food Security. 2011. Price volatility and food security, a report by the high-level panel of experts.

6 European Commission, 2013. The impact of EU consumption on deforestation:Comprehensive analysis ofthe impact of EU consumption on deforestation. Study funded by the European Commission,DG ENV, and undertaken by VITO, IIASA, HIVA and IUCN NL

8 Painting - Eero Järnefelt. 1893. Burning the Brushwood. Finnish National Gallery, Helsinki

9-13 Wardell, Byerlee and Hughes (eds) Deja vu? Comparing and contrasting foreign land acquisitions in the colonial and contemporary eras. Special issue (in preparation)See also Webb, J.L.A., 2002. Tropical Pioneers: Human Agency and Ecological Change in the Highlands of Sri Lanka, 1800-1900.

15-17 + 22

Lua Xinjian, 2010. Measures on timber traceability in China. Chinese Academy of Forestry presentation 4th

May 20120, Phnom Penh.

18-21 CIFOR, 2011. Chinese Trade and Investment and the Forests of the Congo Basin: A scoping study for Cameroon, DRC and Gabon. CIFOR Working Paper # Brautigam, D., 2009. The Dragon’s Gift: The Real Story of China in Africa.OUP Inc, New York. Spence, J. D., 1998. The Chan’s Great Continent: China in Western Minds. W.W. Norton & Co., New York.

References 2

Slide Reference

23-30 CIFOR Working Papers (2011)• Analysis of approvals for Chinese companies to invest in Africa’s mining, agricultural and forestry sectors• Analysis of China’s overseas investment policies• Chinese trade and investment and the forests of the Congo Basin• Chinese trade and investment and its impacts A scoping study in the miombo woodlands• Wenbin Huang, Andreas Wilkes, Ziafang Sen and Ann Terheggen, 2012 Who is importing forest products from Africa? Environment, Development and Sustainability DOI 10.1007/s10668-012-9413

31-35 Wardell, D.A. and Schoneveld, G., 2013. “Still trying to kill two birds with one stone?” 250 years of land acquisitions in Ghana. Paper presented at the 14th IASC, 4th June 2013, Fujiyoshida, Japan. Schoneveld, G., L. German and E. Nukator. 2011. Land-based investments for rural development? A grounded analysis of the local impacts of biofuel feedstock plantations in Ghana. Ecology and Society

36-37 Cali, M. and te Velde, D.W., 2011. Does Aid-for-Trade really improve trade performance? World Development 39 (5): 725-740Basnett, Y. and Engel, J., 2013. Focusing on what matters in Aid-for-Trade: Increasing effectiveness and delivering results. ODI Briefing Paper # 79; and Basnett, Y. et al, 2012. Increasing the effectiveness of Aid for Trade: the circumstances under which it works best. ODI Working Paper # 353.

38 Patey, L.A. and Large, D., 2012. Cooperating with China in Africa. DIS Policy Brief, Copenhagen.

39 Cerruti, P., 2013 (unpublished)

40 OFAC, State of the Forests 2010

42 CIFOR, 2013. Evidence-based forestry. www.cifro.org/ebf