promise house, inc. 401k plan financial … house, inc. 401k plan financial statements and...

TRANSCRIPT

PROMISE HOUSE, INC. 401K PLAN

FINANCIAL STATEMENTSAND

INDEPENDENT AUDITORS’ REPORT

DECEMBER 31, 2013

PROMISE HOUSE, INC. 401K PLANTABLE OF CONTENTS

DECEMBER 31, 2013

Independent Auditors’ Report .....................................................................................................1 -2

Statements of Net Assets Available for BenefitsDecember 31, 2013 and 2012 .......................................................................................................3

Statement of Changes in Net Assets Available for Benefits For the Year Ended December 31, 2013 ......................................................................................4

Notes to Financial Statements ..................................................................................................5 - 13

Supplemental Schedule..................................................................................................................14

Unaudited

2013 2012

ASSETS

Investments:

Common collective trust 125,714$ 119,048$

Mutual funds, at fair value 384,256 295,477

Total Investments 509,970 414,525

Receivables:

Participant loans 6,601 11,295

Net assets reflecting investments at fair value 516,571 425,820

Adjustment from fair value to contract value for fully benefit- responsive investment contract (834) -

NET ASSETS AVAILABLE FOR BENEFITS 515,737$ 425,820$

PROMISE HOUSE INC. 401k PLAN

STATEMENTS OF NET ASSETS AVAILABLE FOR BENEFITS

DECEMBER 31, 2013 and 2012

The accompanying notes are an integral part of these financial statements.

3

Additions:

Contributions:

Participants 57,587$

Earnings on Investments:

Interest - participant loans 548

Interest and dividends 14,373

Net appreciation in fair value of mutual funds 53,578

Net appreciation in common collective trust 11,301

Other income 184

Net Earnings on Investments 79,984

Total Additions 137,571

Deductions:

Benefits paid to participants and beneficiaries 46,879

Plan expenses 775

Total Deductions 47,654

Net Increase In Net Assets Available For Plan Benefits 89,917

Net Assets Available for Benefits:

Beginning of period 425,820

End of period 515,737$

PROMISE HOUSE INC. 401k PLAN

STATEMENT OF CHANGES IN NET ASSETS AVAILABLE FOR BENEFITS

FOR THE YEAR ENDED DECEMBER 31, 2013

The accompanying notes are an integral part of this financial statement.

4

PROMISE HOUSE, INC. 401K PLANNOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013_______________

5

Note 1. Plan DescriptionThe following description of the Promise House, Inc. (Organization) 401k Plan (Plan) provides only general information. The Organization is the Plan administrator and sponsor and State Street Bank and Trust Company is the Plan trustee. Participants should refer to the Plan agreement for a more complete description of the Plan’s provisions.

GeneralThe Plan was established as a defined contribution plan on January 1, 2007 and is subject to the provisions of the Employee Retirement Income Security Act of 1974 (ERISA) and Section 401(a) of the Internal Revenue Code of 1986 (IRC).

All employees of the Organization are eligible to participate upon completing the Plan’s eligibility requirements. Employees who have completed 6 months of service are eligible to participate. Employees receive credit for one month of service for each month in which they complete 1 hour of service.

FundingThe Plan is a defined contribution plan wherein participants elect to reduce their compensation and have such reductions contributed to the Plan on their behalf. Participants direct their investments in numerous investment options managed by ADP Retirement Services.

Participating employees may contribute 1% to 80% of eligible compensation through payroll deductions to the maximum amount permitted under applicable Internal Revenue Service provisions. Participants age 50 or over are allowed catch-up contributions. Rollover contributions to the Plan are also allowed.

The Organization may make a discretionary matching contribution. Participants must make elective deferrals into the Plan and be employed on December 31 to receive a matching contribution. The Organization may make nonelective contributions to the Plan based on eligible earnings. The Organization did not make a discretionary matching or nonelective contribution for the year ended December 31, 2013.

AllocationEach participant’s account is credited with the participant’s contribution and the Organization’s non-discretionary matching contribution. Investment income or loss is allocated daily based on the ratio of each participant’s account balance at the end of each day. Any discretionary or profit sharing contribution is made annually to participants employed on the last day of the Plan year.

ForfeituresThe Organization may reduce employer contributions by forfeitures occurring during the Plan year that are not used to pay Plan expenses. The Plan did not reduce employer contributions with forfeitures during the Plan year. The Plan maintained a balance of $0 in the forfeiture account at December 31, 2013 and 2012.

PROMISE HOUSE, INC. 401K PLANNOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013_______________

6

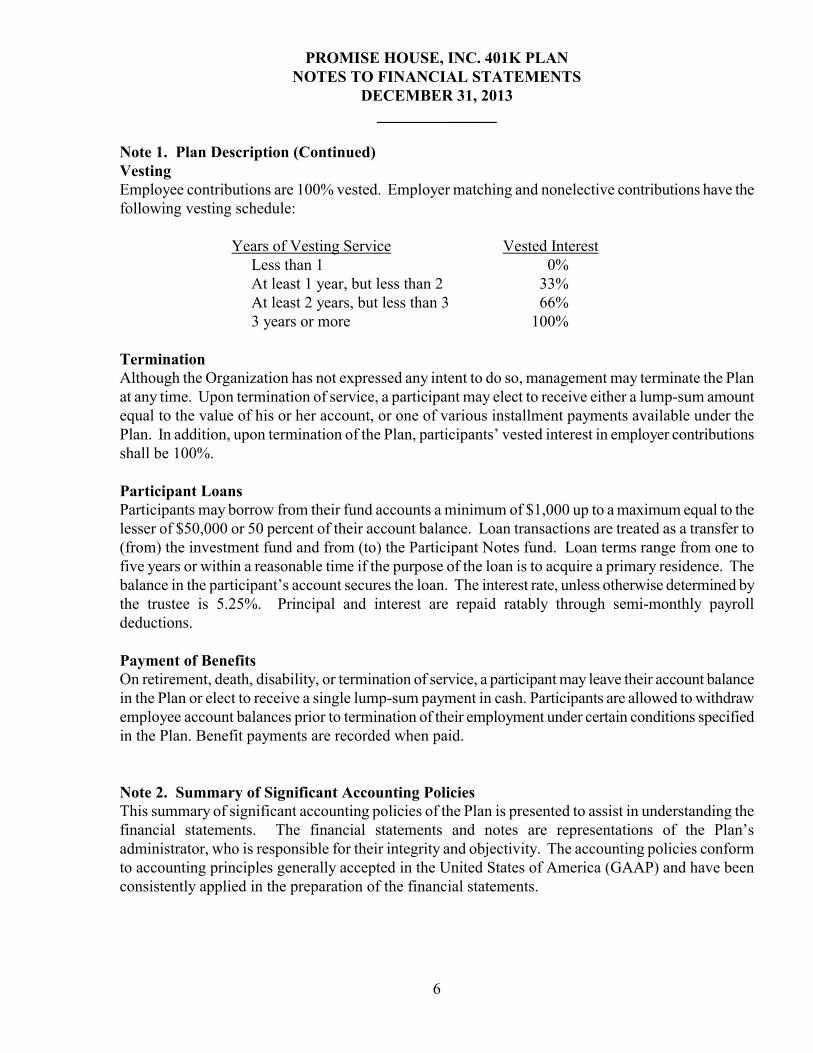

Note 1. Plan Description (Continued)VestingEmployee contributions are 100% vested. Employer matching and nonelective contributions have the following vesting schedule:

Years of Vesting Service Vested InterestLess than 1 0%At least 1 year, but less than 2 33%At least 2 years, but less than 3 66%3 years or more 100%

TerminationAlthough the Organization has not expressed any intent to do so, management may terminate the Plan at any time. Upon termination of service, a participant may elect to receive either a lump-sum amount equal to the value of his or her account, or one of various installment payments available under the Plan. In addition, upon termination of the Plan, participants’ vested interest in employer contributions shall be 100%.

Participant LoansParticipants may borrow from their fund accounts a minimum of $1,000 up to a maximum equal to the lesser of $50,000 or 50 percent of their account balance. Loan transactions are treated as a transfer to (from) the investment fund and from (to) the Participant Notes fund. Loan terms range from one to five years or within a reasonable time if the purpose of the loan is to acquire a primary residence. The balance in the participant’s account secures the loan. The interest rate, unless otherwise determined by the trustee is 5.25%. Principal and interest are repaid ratably through semi-monthly payroll deductions.

Payment of BenefitsOn retirement, death, disability, or termination of service, a participant may leave their account balance in the Plan or elect to receive a single lump-sum payment in cash. Participants are allowed to withdraw employee account balances prior to termination of their employment under certain conditions specified in the Plan. Benefit payments are recorded when paid.

Note 2. Summary of Significant Accounting PoliciesThis summary of significant accounting policies of the Plan is presented to assist in understanding the financial statements. The financial statements and notes are representations of the Plan’s administrator, who is responsible for their integrity and objectivity. The accounting policies conform to accounting principles generally accepted in the United States of America (GAAP) and have been consistently applied in the preparation of the financial statements.

PROMISE HOUSE, INC. 401K PLANNOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013_______________

7

Note 2. Summary of Significant Accounting Policies (Continued)EstimatesThe preparation of financial statements in conformity with GAAP requires the plan administrator to make estimates and assumptions that affect certain reported amounts and disclosures. Actual results could differ from those estimates.

Risks and UncertaintiesThe Plan invests in various investment securities. Investment securities are exposed to various risks, such as interest rate, market, and credit risks. Due to the level of risk associated with certain investment securities, it is at least reasonably possible that changes in the values of investment securities will occur in the near term and that such changes could materially affect participants’ account balances and the amounts reported in the statement of net assets available for benefits.

Investment Valuation and Income RecognitionInvestments are reported at fair value. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Purchases and sales of securities are recorded on a trade-date basis. Interest income is recorded on the accrual basis. Dividends are recorded on the ex-dividend date. Net appreciation includes the Plan’s gains and losses on investments bought and sold as well as held during the year.

Investment ContractsInvestment contracts held by a defined contribution plan are required to be reported at fair value. Contract value is the relevant measurement attributable to fully benefit-responsive investment contracts because contract value is the amount participants would receive if they were to initiate permitted transactions under the terms of the Plan.

The Plan invested in investment contracts through a collective trust in 2013 and 2012. Contract value for this collective trust was based on the net asset value of the fund as reported by the trustee, Invesco National Trust Company (Invesco). The statements of net assets available for benefits present the fair value of the investment contracts, as well as the adjustment of the fully benefit-responsive investment contracts from fair value to contract value for the year ended December 31, 2013.

Notes Receivable From ParticipantsNotes receivable from participants are measured at their unpaid principal balance plus any accrued but unpaid interest. Interest income is recorded on the accrual basis. Related fees are recorded as administrative expenses and are expensed as they are incurred. No allowance for credit losses had been recorded as of December 31, 2013 or 2012. If a participant ceases to make loan repayments and the plan administrator deems the participant loan to be in default, the participant loan balance is reduced and a benefit payment is recorded.

PROMISE HOUSE, INC. 401K PLANNOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013_______________

8

Note 2. Summary of Significant Accounting Policies (Continued)Administration of the PlanCertain administrative expenses of the Plan may be paid by the Organization. The Plan is not required to reimburse the Organization for any administrative expenses paid by the Organization. Expenses not paid by the Organization are paid by the Plan.

Date of Management’s ReviewSubsequent events have been evaluated for potential recognition or disclosure through October 10, 2014, which is the date the financial statements were available to be issued.

Note 3. Income Tax StatusThe Plan received a letter dated March 31, 2008 from the IRS identifying the Plan as acceptable under section 401 of the IRC. In the opinion of the plan administrator, the Plan is currently being operated in accordance with the Plan agreement and in conformity with the applicable provisions of the IRC and therefore exempt from federal income taxes. Therefore, no provision for income taxes has been included in the Plan’s financial statements.

GAAP require plan management to evaluate tax positions taken by the plan and recognize a tax liability or asset if the organization has taken an uncertain position that more likely than not would not be sustained upon examination by the IRS. The plan is subject to routine audits by taxing jurisdictions; however, there are currently no audits for any tax periods in progress. The plan administrator believes it is no longer subject to income tax examinations for years prior to 2010.

Note 4. Party-in-InterestCertain Plan investments are units of common/collective trust funds managed by State Street Bank &Trust Company through their ADP Retirement Services program. These transactions qualify as party-in-interest transactions; however, they are exempt from the ERISA prohibited transaction rules.

Note 5. InvestmentsInvestments representing 5% or more of the Plan’s net assets at December 31, 2013 are as follows:

T. Rowe Price Retirement 2040 - R $ 137,379

Invesco Stable Asset 85,082

T. Rowe Price Retirement 2010 - R 47,967

T. Rowe Price Retirement 2020 - R 31,691

PROMISE HOUSE, INC. 401K PLANNOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013_______________

9

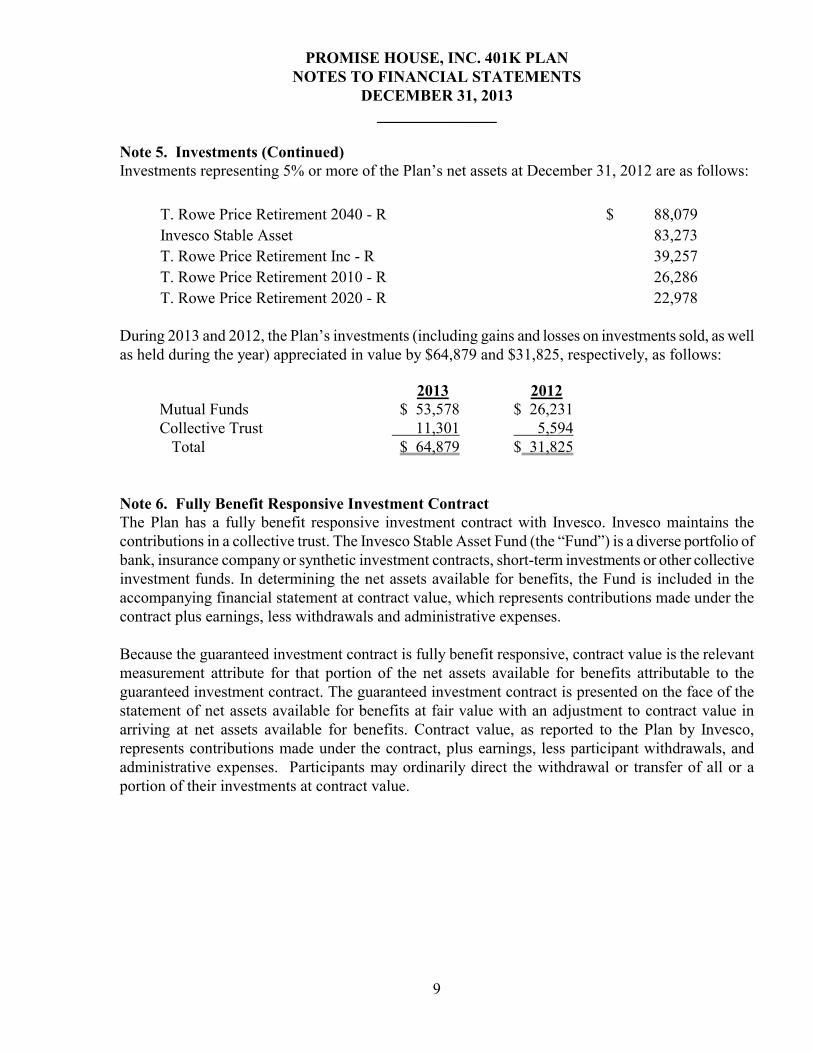

Note 5. Investments (Continued)Investments representing 5% or more of the Plan’s net assets at December 31, 2012 are as follows:

During 2013 and 2012, the Plan’s investments (including gains and losses on investments sold, as well as held during the year) appreciated in value by $64,879 and $31,825, respectively, as follows:

2013 2012 Mutual Funds $ 53,578 $ 26,231 Collective Trust 11,301 5,594 Total $ 64,879 $ 31,825

Note 6. Fully Benefit Responsive Investment ContractThe Plan has a fully benefit responsive investment contract with Invesco. Invesco maintains the contributions in a collective trust. The Invesco Stable Asset Fund (the “Fund”) is a diverse portfolio of bank, insurance company or synthetic investment contracts, short-term investments or other collective investment funds. In determining the net assets available for benefits, the Fund is included in the accompanying financial statement at contract value, which represents contributions made under the contract plus earnings, less withdrawals and administrative expenses.

Because the guaranteed investment contract is fully benefit responsive, contract value is the relevant measurement attribute for that portion of the net assets available for benefits attributable to the guaranteed investment contract. The guaranteed investment contract is presented on the face of the statement of net assets available for benefits at fair value with an adjustment to contract value in arriving at net assets available for benefits. Contract value, as reported to the Plan by Invesco, represents contributions made under the contract, plus earnings, less participant withdrawals, and administrative expenses. Participants may ordinarily direct the withdrawal or transfer of all or a portion of their investments at contract value.

T. Rowe Price Retirement 2040 - R $ 88,079

Invesco Stable Asset 83,273

T. Rowe Price Retirement Inc - R 39,257

T. Rowe Price Retirement 2010 - R 26,286

T. Rowe Price Retirement 2020 - R 22,978

PROMISE HOUSE, INC. 401K PLANNOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013_______________

10

Note 6. Fully Benefit Responsive Investment Contract (Continued)Certain events limit the ability of the Plan to transact at contract value with the issuer. Such events include the following: (1) amendments to the Plan documents (including complete or partial Plan termination or merger with another plan), (2) changes to the Plan’s prohibition on competing investment options or deletion of equity wash provisions, (3) bankruptcy of the Plan sponsor or other Plan sponsor events (for example, divestitures or spin-offs of a subsidiary) that cause a significant withdrawal from the Plan, or (4) the failure of the trust to qualify for exemption from federal income taxes or any required prohibited transaction exemption under ERISA. The Plan’s management believes that any events that would limit the Plan’s ability to transact at contract value with participants are probable of not occurring.

The average yields earned by the guaranteed investment contract are as follows:

Average Yields: 2013 2012

Based on actual earnings 1.15% 1.28%Based on interest credited to participants 1.31% 1.68%

Note 7. Information Certified By TrusteeUnder the Department of Labor’s regulations, certain assets and related information held by a bank, trust company or similar institution, or an insurance company, that is regulated and subject to periodic examination by a state or federal agency does not have to be audited, provided the plan administrator exercises this option and the institution holding the assets certifies the required information. State Street Bank & Trust Company has provided certification as to the completeness and accuracy of the investments presented in the accompanying statements of net assets available for plan benefits as of December 31, 2013 and 2012 and in the statement of changes in net assets available for benefits for the year ended December 31, 2013. The accompanying supplemental schedule also includes investment information certified by State Street Bank & Trust Company as being complete and accurate.

Note 8. Fair Value MeasurementsFinancial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) 820, Fair Value Measurements and Disclosures, provides the framework for measuring fair value. That framework provides a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (level 1 measurements) and the lowest priority to unobservableinputs (level 3 measurements).

PROMISE HOUSE, INC. 401K PLANNOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013_______________

11

Note 8. Fair Value Measurements (Continued)The three levels of the fair value hierarchy under FASB ASC 820 are described as follows:

Level 1 Inputs to the valuation methodology are unadjusted quoted prices for identical assets or liabilities in active markets that the plan has the ability to access.

Level 2 Inputs to the valuation methodology include Quoted prices for similar assets or liabilities in active markets; Quoted prices for identical assets or liabilities in inactive markets; Inputs other than quoted prices that are observable for the asset or liability; Inputs that are derived principally from or corroborated by observable market

data by correlation or other means. If the asset or liability has a specified (contractual) term, the level 2 input must be observable for substantially the full term of the asset or liability.

Level 3 Inputs to the valuation methodology are unobservable and significant to the fair value measurement.

The asset’s or liability’s fair value measurement level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. Valuation techniques used need to maximize the use of observable inputs and minimize the use of unobservable inputs.

Following is a description of the valuation methodologies used for assets measured at fair value. There have been no changes in the methodologies used at December 31, 2013 and 2012.

Registered investment companies – Valued at the daily closing price as reported by the fund. Mutual funds held by the Plan are open-end mutual funds that are registered with the SEC. These funds are required to publish their daily net asset value (NAV) and to transact at that price. The mutual funds held by the Plan are deemed to be actively traded.

Common collective trust – Valued at the NAV of units of a bank of collective trust. The NAV, as provided by the trustee, is used as a practical expedient to estimate fair value. The NAV is based on the fair value of the underlying investments held by the fund less its liabilities. This practical expedient is not used when it is determined to be probable that the fund will sell the investment for an amount different than the reported NAV. Participant transactions (purchased and sales) may occur daily.

The preceding method described may produce a fair value calculation that may not be indicative of net realizable value or reflective of future fair values. Furthermore, although the Plan believes its valuation methods are appropriate and consistent with other market participants, the use of different methodologies or assumptions to determine the fair value of certain financial instruments could result in a different fair value measurement at the reporting date.

PROMISE HOUSE, INC. 401K PLANNOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013_______________

12

Note 8. Fair Value Measurements (Continued)Fair values of assets measured on a recurring basis at December 31, 2013 are as follows:

Fair Value Measurements at Reporting Date Using:

Level 1 Level 2 Level 3 TotalCollective trust:- Growth funds $ - $ 22,647 $ - $ 22,647- Aggressive growth funds 17,985 - 17,985- Stable value fund 85,082 - 85,082Registered investmentcompanies:- Target date funds 239,014 - - 239,014- Growth funds 67,723 - - 67,723- Aggressive growth funds 64,936 - - 64,936- Income funds 12,583 - - 12,583Total Investments $ 384,256 $ 125,714 $ - $ 509,970

Fair values of assets measured on a recurring basis at December 31, 2012 are as follows:

Fair Value Measurements at Reporting Date Using: (Unaudited)

Level 1 Level 2 Level 3 TotalCollective trust:- Growth funds $ - $ 21,812 $ - $ 21,812- Aggressive growth funds 13,963 - 13,963- Stable value fund 83,273 - 83,273Registered investmentcompanies:- Target date funds 189,622 - - 189,622- Growth funds 45,482 - - 45,482- Aggressive growth funds 50,045 - - 50,045- Income funds 10,328 - - 10,328Total Investments $ 295,477 $ 119,048 $ - $ 414,525

PROMISE HOUSE, INC. 401K PLANNOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013_______________

13

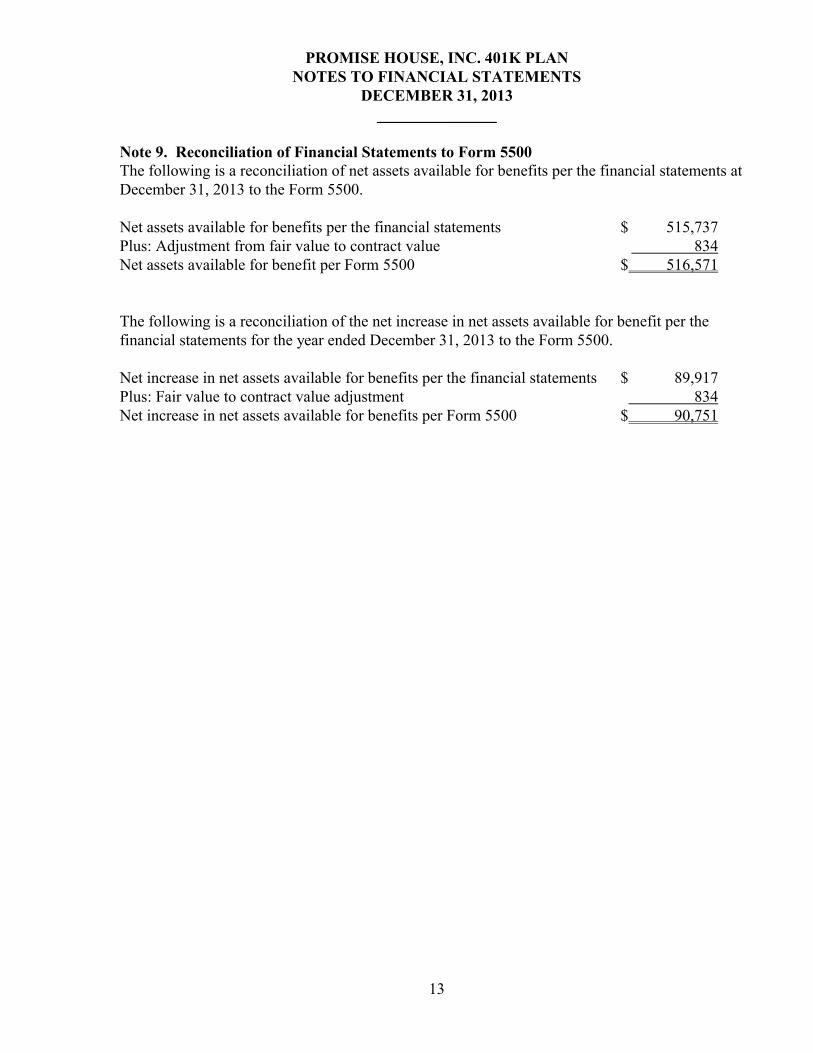

Note 9. Reconciliation of Financial Statements to Form 5500The following is a reconciliation of net assets available for benefits per the financial statements at December 31, 2013 to the Form 5500.

Net assets available for benefits per the financial statements $ 515,737Plus: Adjustment from fair value to contract value 834Net assets available for benefit per Form 5500 $ 516,571

The following is a reconciliation of the net increase in net assets available for benefit per the financial statements for the year ended December 31, 2013 to the Form 5500.

Net increase in net assets available for benefits per the financial statements $ 89,917Plus: Fair value to contract value adjustment 834Net increase in net assets available for benefits per Form 5500 $ 90,751

SUPPLEMENTAL SCHEDULE

(a)

(b) Identity of issue, borrower, lessor,

or similar party

(c) Description of investment, including

maturity date, rate of interest, collateral, par, or

maturity value (d) Cost

(e) Current

Value

Invesco National Trust Company Invesco Stable Asset ** 85,082$

* State Street Bank & Trust Co SSGA S&P 500 IDX IX ** 5,149

* State Street Bank & Trust Co SSGA S&P MD CP IDX NL J ** 17,498

* State Street Bank & Trust Co SSGA Russ SC IDX VIII ** 9,921

* State Street Bank & Trust Co SSGA Intl IDX Seclend Ser VIII ** 8,064

Deutsche Asset & Wealth Management DWS Large Cap Value Fund - A ** 11,550

Munder Capital Management Munder Mid-Cap Core Growth - A ** 14,928

MainStay Investments Mainstay Icap International R2 ** 14,423

Oppenheimer Funds Oppenheimer Core Bond Fund - A ** 12,583

Columbia Management Columbia Mid Cap Val Opp R4 ** 13,078

Allianz Global Investors Allianz NFJ Smallcap Value - A ** 20,662

Davis Funds Davis New Nork Venture Fund - A ** 14,005

Nuveen Investments Nuveen Small Cap Select A ** 13,122

T. Rowe Price T. Rowe Price Retirement 2010 - R ** 47,967

T. Rowe Price T. Rowe Price Retirement 2020 - R ** 31,691

T. Rowe Price T. Rowe Price Retirement 2030 - R ** 16,960

T. Rowe Price T. Rowe Price Retirement 2040 - R ** 137,379

T. Rowe Price T. Rowe Price Retirement Inc - R ** 5,017

T. Rowe Price T. Rowe Price Growth Stock Fund ** 14,162

Janus Capital Group Janus Overseas Fund - S ** 16,729

* Participants Participant Loans - Rates 5.25% 6,601516,571$

* denotes a party-in-interest

** cost omitted for participant directed

investments

PROMISE HOUSE INC. 401k PLAN

Schedule H, Line 4i-Schedule of Assets Held at December 31, 2013

EIN# 75-2180083

Plan Number: 002

See auditors' report.

14