401k update

TRANSCRIPT

AN UPDATE

ON:

401k A

udits

1

JOSEPH VENTURA, CPAAUDIT AND ACCOUNTING MANAGER, GUMBINER SAVETT

• Audit and accounting specialist who works with clients of various sizes such as venture- backed start-ups through established corporations with multiple entities and also specializes on the audits of employee benefit plans

• Graduate of the University of California, Santa Cruz

• Member of the American Institute of Certified Public Accountants and the California Society of Certified Public Accountants

2

3

LEARNING OBJECTIVES• Identify new accounting standards affecting defined contribution

retirement plans• Identify common fraud risks that defined contribution plans are

susceptible to• Identify common issues found during audits of defined contribution

retirement plans• Summarize the entire process of auditing a defined contribution

plan

4

ECONOMIC AND INDUSTRY DEVELOPMENTS• Economic Updates• U.S. economy grew at a slow to moderate pace in 2015• S&P 500 and the Dow Jones Industrial Average closed with their

worst year since 2008• Chicago Board Options Exchange Volatility Index (VIX) showed

extreme ups and downs during 2015, ending on an upward trend• VIX is a key measure of market expectations of near-term

volatility• Considered by many to indicate investor sentiment, market

volatility, and best gauge of fear in the market• Volatility during 2015 shows continued uncertainty that the

economy is recovering

5

ECONOMIC AND INDUSTRY DEVELOPMENTS, CONTINUED• Employee Benefit Plan Considerations – challenges and

trends to be aware of Increase in mergers and terminations of plans, particularly as

companies increase merger and acquisition activity Continued termination of defined benefit pension plans (DB plans)

in favor of a defined contribution approach to retirement provisions for employees

Increase in the number of participating employers withdrawing from multiemployer plans, resulting in underfunded obligations and possible legal action related to withdrawal liabilities

Increase in investments not properly recorded at fair value as of the reporting date Due to the use of inappropriate valuation methodologies,

mathematical errors in the application of the methodologies, or inaccurate inputs

Continued emphasis on investment portfolio diversification and investor sophistication Had led to a more complex composition of retirement assets that

include more international influence than in the past

6

ECONOMIC AND INDUSTRY DEVELOPMENTS, CONTINUED

Addition of auto escalation feature to a plan’s existing auto enrollment feature

Increase in the number of outstanding loans to participants and in the number of delinquent or defaulted loans

Increases in distributions resulting in a decrease in asset levels due to baby boomers retiring at record rates According to the U.S. Census Bureau, the number of Americans

reaching age 65 is expected to increase at a rate of 10,000 per day through 2029

Significant cutbacks to the determination letter program for individually designed plans by the IRS After 2017, the determination letters for individually designed

plans will be limited to initial plan qualification and qualification upon termination

Previous policy was on a 5-year cycle based on last digit of the plan sponsor’s EIN

ACCOUNTING UPD

ATES

8

FASB ASC 250ACCOUNTING CHANGES AND ERROR CORRECTIONS

• Requires a reporting entity to change an accounting principle if the change is required by a newly issued codification update

• Describes the information an entity is required to disclose about the change

• Disclosures are required in the fiscal year the change is made

9

FASB ASU NO. 2015-17DISCLOSURE FOR INVESTMENTS IN CERTAIN ENTITIES THAT CALCULATE NET ASSET VALUE PER SHARE• Under FASB ASC 820

• A reporting entity was permitted to measure the fair value of certain investments using the net asset value (NAV) per share (or its equivalent) of the investment

• Investments were then categorized within the fair value hierarchy

• In order to be valued using NAV, investment must:• Not have a readily determinable fair value• Investment is in an entity that has all of the attributes of the

investment company

10

FASB ASU NO. 2015-17DISCLOSURE FOR INVESTMENTS IN CERTAIN ENTITIES THAT CALCULATE NET ASSET VALUE PER SHARE• Main Provisions of FASB ASU No. 2015-17• Investments measured at fair value using the NAV practical expedient no

longer included in the fair value hierarchy• Fair value hierarchy should include a reconciling item between the

investments included in the hierarchy and total investments on the statement of net assets available for benefits.

• NAV disclosures required for investments actually measured using the NAV practical expedient as opposed to eligible for the NAV practical expedient

• Effective Dates• Public Business entities – fiscal years beginning after December 15, 2015• All others (including employee benefit plans) – fiscal years beginning after

December 15, 2016• Early application permitted• Apply retrospectively

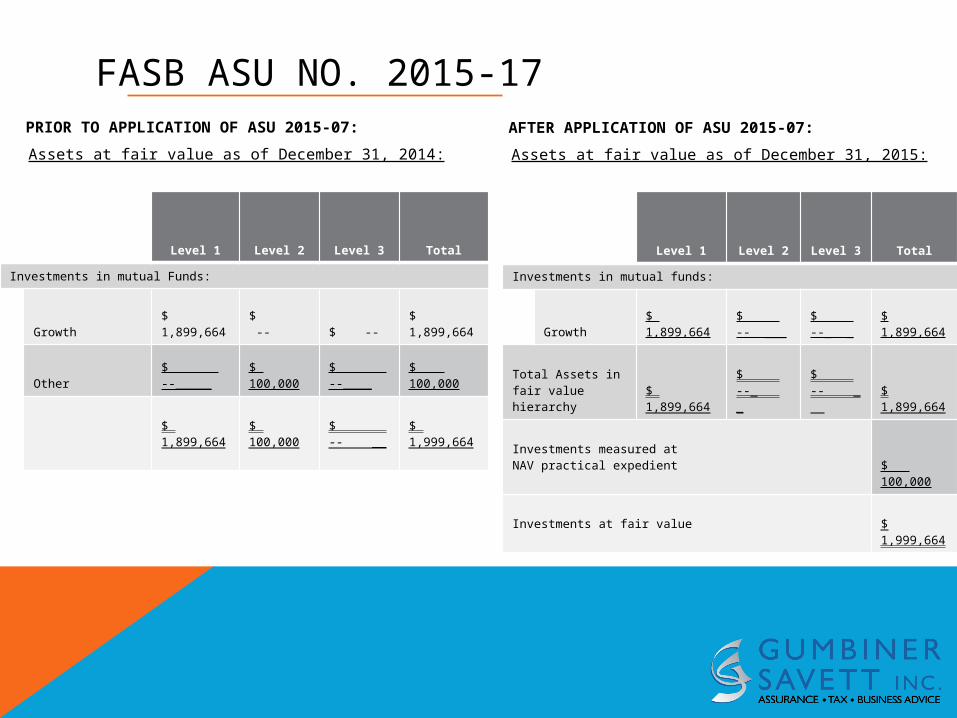

FASB ASU NO. 2015-17AFTER APPLICATION OF ASU 2015-07:

Assets at fair value as of December 31, 2015:PRIOR TO APPLICATION OF ASU 2015-07:

Assets at fair value as of December 31, 2014:

Level 1 Level 2 Level 3 Total

Investments in mutual Funds:

Growth$ 1,899,664 $ -- $ --

$ 1,899,664

Other$ --_____

$ 100,000

$ --____

$ 100,000

$ 1,899,664

$ 100,000

$ -- __

$ 1,999,664

Level 1 Level 2 Level 3 TotalInvestments in mutual funds:

Growth$ 1,899,664

$ -- ___

$ --_ _

$ 1,899,664

Total Assets in fair value hierarchy

$ 1,899,664

$ --_ _

$ -- _

$ 1,899,664

Investments measured at NAV practical expedient $

100,000

Investments at fair value $ 1,999,664

12

ASU NO. 2015-10READILY DETERMINABLE FAIR VALUE• An equity security has a “readily determinable fair value” if it meets

any of the following conditions: Sales price or bid-and-asked quotations are currently available on a

securities exchange registered with the SEC or in the over the counter market.

The fair value of an equity security traded only in a foreign market is readily determinable if that foreign market is of a breadth and scope comparable to one of the U.S. markets referred to above.

The fair value of an equity security that is an investment in a mutual fund or in a structure similar to a mutual fund (that is, a limited partnership or a venture capital entity) is readily determinable if the fair value per share (unit) is determined and published and is the basis for current transactions.

• Effective Dates• All entities – fiscal years beginning after December 15, 2015 • Early adoption is permitted

13

ASU NO. 2015-12SIMPLIFICATION OF EMPLOYEE BENEFIT PLAN REPORTING —PART I• Designates contract value as the only required measure for

fully benefit-responsive investment contracts (FBRICs)• Maintains relevant information while reducing cost and

complexity of reporting for FBRICs• Current guidance requires plans to measure FBRICs at both fair

value and contract value, and to present an adjustment on the face of the financial statements to reconcile the two amounts

14

ASU NO. 2015-12SIMPLIFICATION OF EMPLOYEE BENEFIT PLAN REPORTING —PART I• What effect does this have?

• Presentation of the contract value of these investments on a new line on the statement of net assets.

• Removal of these investments from fair value disclosure requirements.

• Removal of the requirement to disclose average yield for fully benefit-responsive contracts.

• What doesn’t change?• The other disclosure requirements for FBRICs• Description of the contract and how it operates• Method of determining crediting rates• Description of events that would limit the plan from transacting

or settling at contract value and if these events are probable.

ASU NO. 2015-12PRIOR TO APPLICATION OF ASU 2015-12:ASSETS 2014 2013

Investments, at fair value:Mutual funds $ 9,192,853 $ 8,144,907 Guaranteed investment contract 613,937 659,807 Cash - 11,597 Money market fund - -

Total investments 9,806,790 8,816,311 Receivables:

Notes receivable from participants 147,221 113,240 Employer contributions 34,113 40,611

Total receivables 181,334 153,851

TOTAL ASSETS 9,988,124 8,970,162 LIABILITES - -

Adjustment from fair value to contract value forfully benefit-responsive investment contract (38,966) (48,648)

NET ASSETS AVAILABLE FOR BENEFITS $ 9,949,158 $ 8,921,514

ASU NO. 2015-12AFTER APPLICATION OF ASU 2015-12: ASSETS 2014 2013

Investments, at fair value: Mutual funds $ 9,192,853 $ 8,144,907

Cash - 11,597 9,192,853 8,156,504Guaranteed investment contract 574,971 611,159

Total investments 9,767,824 8,767,663 Receivables:

Notes receivable from participants 147,221 113,240

Employer contributions 34,113 40,611

Total receivables 181,334 153,851

NET ASSETS AVAILABLE FOR BENEFITS $ 9,949,158 $ 8,921,514

17

ASU NO. 2015-12SIMPLIFICATION OF EMPLOYEE BENEFIT PLAN REPORTING —PART II• Simplifies and makes more effective the investment

disclosure requirements under Topic 820 and under Topics 960, 962, and 965 through the following:• Removes disclosure of individual investments comprising more

than 5% of total net assets available for benefits• Removes gain/loss by investment type disclosure• ASC 820 table to be presented only by investment type (i.e.

mutual funds, collective trusts, etc.), no disaggregation required• Investments valued using the NAV no longer need to disclose

investment strategies, if that investment files as a Direct Filing Entity (“DFE”)

18

ASU NO. 2015-12SIMPLIFICATION OF EMPLOYEE BENEFIT PLAN REPORTING —PART III• Allows a plan with a fiscal year end of other than a calendar

month-end to measure its investments and investment-related accounts using the month-end date that is nearest to its fiscal year-end. • FASB recognized that the use of a month end date to measure

investments and investment related accounts is consistent with how trustees or custodians provide information used to prepare the financial statements.

• Effective dates• All entities– fiscal years beginning after December 15, 2015• Early adoption is permitted

19

EXAMPLE ACCOUNTING POLICY FOOTNOTE

Changes in accounting principles: In May 2015, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”)

2015-07 Fair Value Measurement (Topic 820), Disclosures for Investments in Certain Entities that Calculate Net Asset Value per Share (or Its Equivalent), which eliminates the requirement to categorize investments in the fair value hierarchy if their fair value is measured using net asset value per share as a practical expedient. The amendments in ASU 2015-07 are effective for fiscal years beginning after December 15, 2016, with early adoption permitted.

In July 2015, the FASB issued ASU 2015-12, Plan Accounting: Defined Benefit Pension Plans, Defined Contribution Pension Plans, Health and Welfare Benefit Plans: (Part I) Fully Benefit-Responsive Investment Contracts, (Part II) Plan Investment Disclosures, (Part III) Measurement Date Practical Expedient. This amendment removes the requirement to report fully benefit-responsive investment contracts at fair value with an adjustment to contract value. Under the amendment, fully benefit-responsive investment contracts are measured, presented, and disclosed only at contract value. In addition, this amendment simplifies the investment disclosures required for employee benefit plans, including eliminating the requirements to disclose: (a) individual investments that represent 5% or more of net assets available for benefits, (b) net appreciation (depreciation) by individual investment type, and (c) investment information disaggregated based on the nature, characteristics and risks. The requirement to disaggregate participant-directed investments within a self-directed brokerage account has also been eliminated. Self-directed brokerage accounts should be reported as a single type of investment. The amendment also allows plans to measure investments and investment-related accounts as of a month-end date that is closest to the plan’s fiscal year-end, when the fiscal period does not coincide with a month-end. ASU 2015-12 is effective for fiscal years beginning after December 15, 2015, with early adoption permitted. Parts I and II should be applied retrospectively, while Part III should be applied prospectively.

The Plan elected to early adopt ASU 2015-07 and the applicable parts of ASU 2015-12.

20

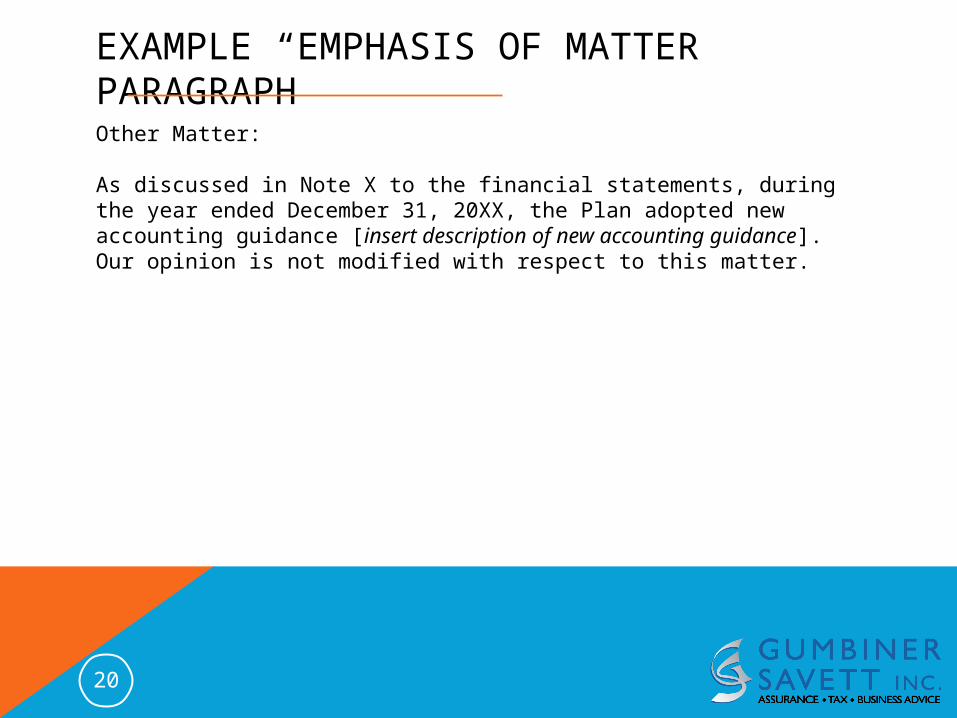

EXAMPLE “EMPHASIS OF MATTER” PARAGRAPHOther Matter:

As discussed in Note X to the financial statements, during the year ended December 31, 20XX, the Plan adopted new accounting guidance [insert description of new accounting guidance]. Our opinion is not modified with respect to this matter.

21

EXAMPLE MANAGEMENT REPRESENTATION LETTER

The Plan adopted the provisions of Accounting Standards Update (ASU) 2015-07 Fair Value Measurement (Topic 820); Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or its Equivalent) for the year ended December 31, 20XX. ASU 2015-07 is effective for fiscal years beginning after December 15, 2016, with early adoption permitted. The Plan’s management has elected to adopt ASU 2015-07 early. The Plan adopted the provisions of ASU 2015-12, Plan Accounting: Defined Benefit Pension Plans, Defined Contribution Pension Plans, Health and Welfare Benefit Plans: (Part I) Fully Benefit-Responsive Investment Contracts, (Part II) Plan Investment Disclosures, (Part III) Measurement Date Practical Expedient for the year ended December 31, 20XX. ASU 2015-12 is effective for fiscal years beginning after December 15, 2015, with early adoption permitted. The Plan’s management has elected to adopt the applicable parts of ASU 2015-07 early.

AUDITING UPD

ATES

23

DOL AUDIT QUALITY STUDY• DOL Employee Benefits Security Administration (EBSA)

published its study on the quality of benefit plan audits performed by CPAs on May 28, 2015• Included a statistical review of 400 plan audits performed by 232

CPA firms for the 2011 plan year and revealed deficiencies in the quality of audit work performed by independent CPAs:• 61% of the audits fully complied with professional auditing

standards or had minor deficiencies• 39% of the audits had one or more major deficiencies with

respect to one or more relevant GAAS requirements that would lead to a rejection of the Form 5500 filing

• 17% of the audit reports failed to comply with one or more of ERISA’s reporting and disclosure requirements

24

DOL AUDIT QUALITY STUDY, CONTINUED• Audit areas with more frequent deficiencies were in areas

specific to employee benefit plan auditing: • Contributions• Participant data• Party-in-interest and prohibited transactions

25

DOL AUDIT QUALITY STUDY, CONTINUED• Recurring deficiencies included the following:• Failure to sufficiently perform participant testing related to

demographic data & payroll• Failure to sufficiently perform and document reliance on SOC

1 Reports.• Failure to sufficiently perform procedures related to benefit

and claims payment testing, including evaluating participant’s eligibility, examining approvals, and recalculation of benefit or claim amounts

• Failure to report significant plan information, such as related party and party in interest transactions, and prohibited transactions between a plan and a party in interest

• Failure to present a Schedule of Assets (held at year end)

26

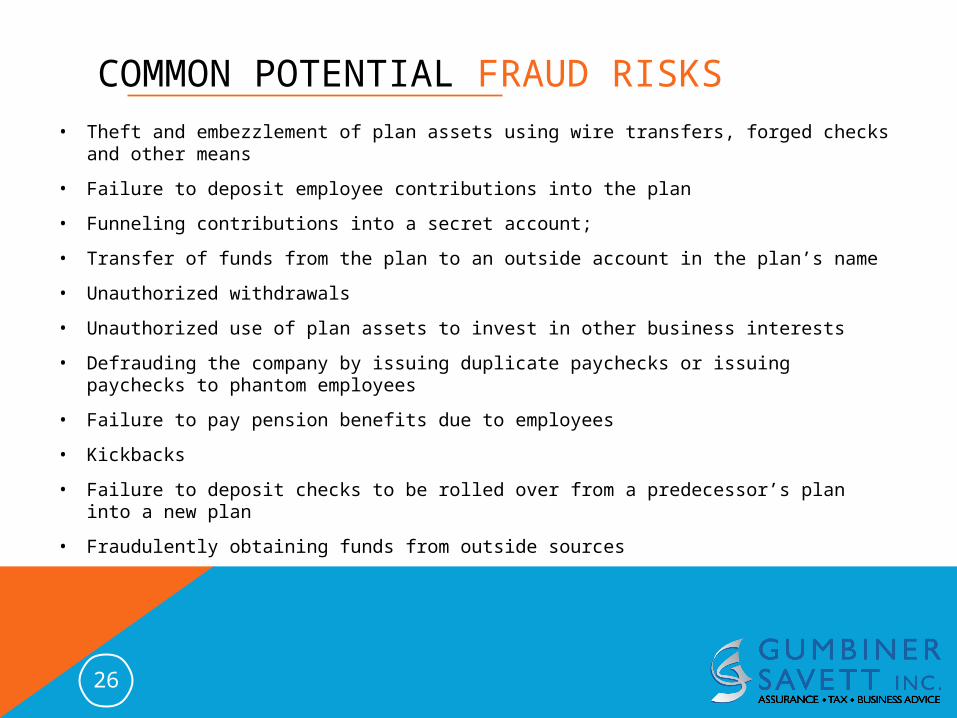

COMMON POTENTIAL FRAUD RISKS• Theft and embezzlement of plan assets using wire transfers, forged checks and

other means• Failure to deposit employee contributions into the plan• Funneling contributions into a secret account; • Transfer of funds from the plan to an outside account in the plan’s name• Unauthorized withdrawals• Unauthorized use of plan assets to invest in other business interests• Defrauding the company by issuing duplicate paychecks or issuing paychecks to

phantom employees• Failure to pay pension benefits due to employees• Kickbacks• Failure to deposit checks to be rolled over from a predecessor’s plan into a new plan• Fraudulently obtaining funds from outside sources

27

WHAT COULD GO WRONG?• Timeliness of contribution remittances to trustee/custodian and their

possible identification as prohibited transactions• Incorrect reporting of census information by the plan sponsor to the

trustee• Withholding of incorrect amounts from participants• Compensation used by the plan sponsor in the payroll system to

calculate participant deferrals is not consistent with compensation as defined in the Plan provisions

• Improper disclosures of investments• Improper exclusion of component of a control from compliance testing• Need to determine what the investment is in order to determine the

appropriate disclosures made

FOLLO

W GS

29

http://g

scpa.c

om

www.linkedin.com/company/[email protected]/GumbinerSavettInc google.com/+Gscpa_gumbiner search “gumbiner savett inc”