project blue india extract - pwc...inaugural address delivered by dr k. c. chakrabarty, deputy...

TRANSCRIPT

Reaping the rewards of the newglobal economy

www.pwc.com/projectblue

Project BlueCapitalising on thegrowth and globalinterconnectivity of theemerging markets:Financial services inIndia

2 PwC Project Blue

04 Foreword

05 Section one:Emerging superpower

10 Section two:Creating a platform for expansion

13 Opening up new frontiers

14 Making sense of an uncertain future

15 Project Blue framework

Contents

PwC Project Blue 3

Project Blue explores the major trends that are reshaping the competitive environmentfor financial services (FS) businesses worldwide. Our clients are using the frameworkto help them judge the implications of these developments for their particular business,and look at how to take advantage of the changes ahead.

The rise and interconnectivity of the emerging markets of South America, Asia, Africaand the Middle East (together these regions form what PwC terms ‘SAAAME’) is inmany ways the most far-reaching of the developments facing the FS sector. Tradewithin SAAAME is growing much faster than the flows between developed-to-developed and developed-to-emerging markets.

India’s businesses are well-placed to take advantage of this shift in the focus of globalgrowth and investment. Yet, they face strong competition from Chinese, Brazilianand other SAAAME multinationals, as well as businesses from the West. India’s FSbusinesses are set to play a key role in supporting their customers as they seek to makethe most of the acceleration in intra-SAAAME trade. As we examine in this paper, keyconsiderations include how to develop the presence on the ground needed to supportclients’ overseas expansion and how to manage risk and talent across more complexand diverse international operations. New approaches to growth and organisationaldesign may be needed as a result.

I hope you find this paper interesting and useful. If you would like to discuss any of theissues raised, please feel free to contact either me or my colleague, Robin Roy (contactdetails on page 14).

Manoj KashyapPwC (India)Financial Services Leader

Foreword

Welcome to ‘Capitalising on thegrowth and global interconnectivityof the emerging markets: Financialservices in India’. The paper isan India-focused companion toour global paper: ‘Capitalisingon the rise and interconnectivityof the emerging markets’,the latest viewpoint in ourProject Blue framework.

4 PwC Project Blue

What do we mean by SAAAME?

‘SAAAME’ refers to South America, Africa, Asia and the Middle East. SAAAMEdoesn’t include Japan as this is a developed G7 economy. Mexico is excluded as ittrades mainly within the North American Free Trade Agreement zone and lesswith SAAAME. For now, Russia and the Commonwealth of Independent States(CIS) are also excluded from SAAAME, as trade is largely internal or with Europe.

India’s emergence as an economic superpower over the past 20 years has beenmeteoric. While it may be difficult to sustain such a high rate of growth in the comingyears, the long-term potential remains strong.

India’s key strengths include the ‘demographic dividend’ of a young and expandingpopulation. Figure 1 compares India’s working age population to East Asia. If wecompare India to China, China’s working age population will begin to decline from2014, but India’s will continue to grow.1

Further potential comes from the increasing sophistication of India’s global deliverymodel, a key engine of growth, particularly in the services sector. Business servicecompanies are moving up the value chain to create centres of excellence in areas suchas software programming, financial reporting and legal support. Global FS businessesare following suit as their shared service centres here build up their deliverycapabilities in target areas such as trade finance, treasury settlements and transactionbanking. Many of these centres employ 10,000 people or more. They could provideincreasing competition for domestic FS businesses as international groups use them asa platform for expansion within India and Asia as a whole.

Section one:Emerging superpower

As India’s economy evolves andcustomer expectations increase, itsFS sector will need to keep pace. FSbusinesses will also need to findways to follow or help theircustomers into new markets andhelp them capitalise on the increasein intra-SAAAME commerce.

PwC Project Blue 5

1 Euromonitor International, 17.10.10

Figure 1: Growth of the working age to non-working age ratioin India

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.001950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

East Asia India low India med India high

Source: United Nations

Ratio of working age to non-working age population

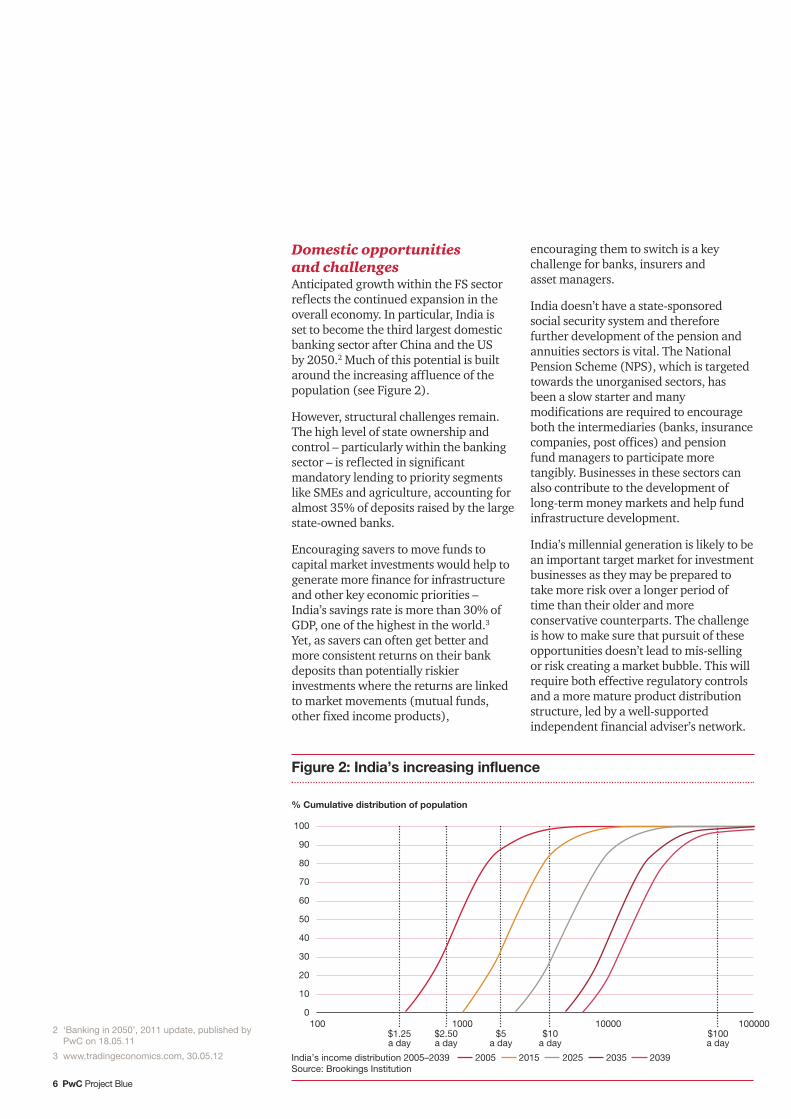

Domestic opportunitiesand challenges Anticipated growth within the FS sectorreflects the continued expansion in theoverall economy. In particular, India isset to become the third largest domesticbanking sector after China and the USby 2050.2 Much of this potential is builtaround the increasing affluence of thepopulation (see Figure 2).

However, structural challenges remain.The high level of state ownership andcontrol – particularly within the bankingsector – is reflected in significantmandatory lending to priority segmentslike SMEs and agriculture, accounting foralmost 35% of deposits raised by the largestate-owned banks.

Encouraging savers to move funds tocapital market investments would help togenerate more finance for infrastructureand other key economic priorities –India’s savings rate is more than 30% ofGDP, one of the highest in the world.3

Yet, as savers can often get better andmore consistent returns on their bankdeposits than potentially riskierinvestments where the returns are linkedto market movements (mutual funds,other fixed income products),

encouraging them to switch is a keychallenge for banks, insurers andasset managers.

India doesn’t have a state-sponsoredsocial security system and thereforefurther development of the pension andannuities sectors is vital. The NationalPension Scheme (NPS), which is targetedtowards the unorganised sectors, hasbeen a slow starter and manymodifications are required to encourageboth the intermediaries (banks, insurancecompanies, post offices) and pensionfund managers to participate moretangibly. Businesses in these sectors canalso contribute to the development oflong-term money markets and help fundinfrastructure development.

India’s millennial generation is likely to bean important target market for investmentbusinesses as they may be prepared totake more risk over a longer period oftime than their older and moreconservative counterparts. The challengeis how to make sure that pursuit of theseopportunities doesn’t lead to mis-sellingor risk creating a market bubble. This willrequire both effective regulatory controlsand a more mature product distributionstructure, led by a well-supportedindependent financial adviser’s network.

6 PwC Project Blue

2 ‘Banking in 2050’, 2011 update, published byPwC on 18.05.11

3 www.tradingeconomics.com, 30.05.12

Figure 2: India’s increasing influence

100

90

60

70

80

50

40

30

20

10

0100 1000 10000 100000

India’s income distribution 2005–2039 2005 2015 2025 2035 2039Source: Brookings Institution

% Cumulative distribution of population

$100a day

$10a day

$5a day

$2.50a day

$1.25a day

PwC Project Blue 7

More than 50% of the population doesnot have a bank account.4 Bringing thisunbanked population into formal FSservices is a key focus of the government’s‘inclusive growth agenda’, reflected in thefive-year plans and long-term growthplans of the economy.5 Reaching out intorural areas and bringing their financialsavings into the formal banking system isgoing to be critical, using a mix ofintermediaries and innovativepartnerships. Among these are plans tocapitalise on well-established distributionchains like the network of post offices,where the rural and semi-urbanpopulation deposit much of their cashsavings, indicating the strong element oftrust. At the same time, making use ofmobile phones for quicker and efficientpayments is also going to be importantas technology and regulations areconverging to make such peer-to-peertransactions easier.

At US$61, insurance premiums per capitaare some way behind China (US$158),Brazil (US$329) and South Africa(US$1,055),6 highlighting room forfurther growth. But while healthinsurance is growing strongly, life andnon-life businesses continue to facedifficult challenges on profitability andmaintaining increasing solvency ratios.

The life insurance sector is undergoinga significant overhaul, following theintroduction of caps on agentcommissions for unit-linked insurance

plans (ULIPs). ULIPs had been themainstay of the sector over the last fewyears, accounting for the bulk of newbusiness. The curbs on ULIP commissionsprecipitated a 9% fall in overall lifepremiums in 2011.7 The difficulties withinthe ULIP market are leading to a shifttowards more traditional products such aswhole life insurance. The pressure ontop-line growth should also provide theimpetus for better cost control andcustomer focus.

The mainstay of non-life insurancebusiness continues to be propertyand casualty, motor (includingmandatory third-party motor covers)and health. Some good traction has beenseen in travel-related products. Yet, thepremiums in the non-life sector are failingto cover the losses, particularly in motor,due to high claims’ ratios. The challengewill be how to develop the potential inother areas including comprehensivemotor, home cover, personal asset coverand health, while improving the quality ofunderwriting overall.

Looking ahead, insurers will need tocontend with a combination of tighterregulation and the difficult globaleconomic environment, calling forchanges in strategy, governance andrisk management, as well as opening theway for M&A and consolidation withinthe market.

4 New York Times reporting SBI, 29.09.11

5 Indian Banking Sector: Towards the Next Orbit,Inaugural address delivered by Dr K. C.Chakrabarty, Deputy Governor, Reserve Bank ofIndia at 9th Advanced Management Programme atIMI, Delhi, 13.02.12

6 Swiss Re Sigma, World Insurance in 2010

7 Financial Times, 27.05.12

FS follows intra-SAAAMEtrade flowsAlongside domestic growth, the rapid risein intra-SAAAME trade opens upsignificant opportunities for the FS sector.Emerging-to-emerging market commerceis now more valuable and growing muchmore quickly that emerging-to-developedand developed-to-developed trade (seeFigure 3). As Figure 4 highlights, amongthe fastest growing trade routes are thosebetween Asia and Africa and Asia andSouth America.

At present, SAAAME trade flows aredominated by commodities, but asconsumer markets continue to expandon the back of rising affluence(see Figure 5), the pattern of tradewill be increasingly focused onmanufactured goods.

India’s growing presence on the SAAAMEand wider global stage is exemplified bymultinational conglomerates such asTata. Tata employs more than 2,000people in China and generated sales ofmore than $3 billion in the country in2010.8 In South America, its companiesemploy more than 5,000 people.

8 PwC Project Blue

Figure 3: Transformation in global trade flows

Trade value: $6.92trCAGR 2002–10: 8.0%

Non-SAAAME

SAAAME

Trade value: $2.82trCAGR 2002–10: 19.4%

Trade value: $2.67trCAGR 2002–10: 13.6%

Trade value: $2.16trCAGR 2002–10: 12.9%

Sources: WTO and PwC analysisNote: Russia and the Commonwealth of Independent States (CIS) have not been included in SAAAME definition because trade is largely international and/or withEurope. Mexico is excluded as it trades mainly within the North American Free Trade Agreement zone and less with SAAAME. Both areas remain very important growthmarkets and should be considered in relation to the SAAAME region.

8 www.tata.com, 30.05.12

PwC Project Blue 9

The challenge for other businesses is howto follow the lead of groups like Tata bydeveloping and strengthening trade linksand operations within SAAAME. In doingso, they will face strong competition fromother countries, notably China and Brazil,which have been moving quickly to secureresources and tap into rising demand.India’s exports to China increased in2011, but the deficit was still $27 billionon overall trade of $74 billion and India’sbusinesses will be looking to close thegap. Notably, Brazil maintains a netsurplus on trade with China.9

Africa is emerging as a key competitivearena. India’s trade with Africa has grownfrom $620 million in 2001 to $62 billionin 2011. But China–Africa trade hasdeveloped quicker, rising from $10.6billion to more than $160 billion duringthis period.10

Clients are looking to FS institutions toprovide trade finance, insurance, mergerand acquisition services, and debt financein export markets. Serving Indiancommunities abroad has already givenIndian banks and insurers a presence onthe ground in many SAAAME countries.The challenge will be how to build on thisbridgehead and move into new markets.

Figure 4: Trading hot spots (growth in value of imports and exports)

N America

N America

5.4

4.5

17.7

8.8

19.2

8.7

10.0

8.0

8.6

18.8

13.6

12.6

14.7

12.8

13.4

17.5

17.2

16.0

21.2

29.9

24.1

13.7

11.3

5.4

16.8

21.6

24.1

15.1

13.5

12.6

16.4

17.9

19.0

22.5

15.7

9.1

12.0

19.3

25.6

24.5

15.2

18.9

12.9

11.7

16.4

18.0

27.8

18.7

20.2

Europe CIS South andCentral America

Africa Asia Middle East

Europe

CIS

South andCentral America

Africa

Asia

Middle East

ORIGIN

DESTINATION

SAAAMECAGR % 2002–2010: n <5 n 5–10 n 10–15 n 15–20 n 20–25 n >25

Sources: WTO and PwC analysisNotes: North America includes Mexico; Asia includes Japan, Australia and New Zealand

Figure 5: Increasing affluence in SAAAME markets

GDP per capita growth, CAGR %, 1980–2010

SAAAME Non-SAAAME

Sources: United Nations Population Division; World Bank World Development Indicators and PwC analysisNotes: GDP per capita is in constant 2005 US$

10

9

8

7

6

5

4

3

2

1

00 0.5 1 1.5 2

IndiaThailand

Indonesia

Turkey

FranceItaly

Germany

Chile

Philippines

United States

Brazil Nigeria

Japan

2.5 3

China

United Kingdom

Canada

Population growth, CAGR %, 1980–2010

09 Brazil-China Fact Sheet, www.brazil.gov, 30.05.12

10 Economic Times, 17.03.12

Using innovation to build market shareIndia was one of the countries analysed in a recent PwC study of digital banking.Demand and usage are exceptionally high in comparison to both developed andemerging markets (see Figure 6).

Digital FS can enhance customer insight and engagement and allow financialinstitutions to move into new markets without the need for branch or agency networkson the ground. It could be especially important in serving the highly connectedmillennial generation. It can also provide unbanked and remote customers with accessto payment and deposits via the mobile phone network – successful models includeKenya’s M-Pesa, which now has 15 million customers, more than all of the country’sbanks put together.11 Moreover, digital banking is going to be a key element of wealthmanagement, offering intuitive and interactive anytime and anywhere services.

Section two:Creating a platform for expansion

The ability to develop effectivedigital services, forge partnershipsin hard-to-access territories andmove ahead of competitors inseeking out untapped markets willbe crucial in helping FS institutionsto build a platform for sustainabledomestic and international growth.

10 PwC Project Blue

Figure 6: The global usage of internet and mobile usage in banking

100

90

80

70

60

50

40

30

20

10

0

Canada

China

France

Hong

Kong

India

Mexico

Poland

UAE

UK

Total

n% who currently use mobiles to purchase financial products

n% who currently use the internet to purchase financial products

Source: 3,800 consumers were polled for ‘The new digital tipping point’, a report published by PwC inJanuary 2012

11 www.thinkm-pesa.com, 16.04.12

PwC Project Blue 11

One way to augment technologicalcapabilities would be to buy a Westerninstitution. This could also provide accessto additional product expertise, orexperience of managing internationaloperations. Takeover prices in somedeveloped markets are generallyfavourable for now, especially within themid-market, but may not be so for long.

Reaching into new marketsPrior to the global financial crisis, anumber of leading international FSgroups were able to make multipleacquisitions to rapidly build up theirpresence in SAAAME. The problem is thatthis type of fast acquisitive growth is nowmuch more difficult, at least within themost attractive SAAAME markets.

Prospective entrants may face ceilings onforeign holdings, China and the MiddleEast being notable examples. Even inopen markets such as Brazil, there maybe little market share for sale and it may

be prohibitively expensive if it is.Entrants may also face entrenchedcompetition from dominant local rivals,especially within the core savings andcredit markets.

In many of the hard-to-access markets,the main route to customers is thereforegoing to be joint ventures. But with manyleading local firms having partnersalready, it will be important to thinkabout what to offer them that existingpartners and potential rivals cannot.This might be particular product orcredit risk expertise. It might also becomplementary international coverage,or access to customers and investmentopportunities within India. Very fewgroups are going to be able to cover all thekey markets. So collaboration betweencompetitors (co-opetition) is going tobecome evermore common in the future.

Moving into some of the frontier andstill largely unsaturated markets in Africaor South America could provide animportant foundation for future growth.The ability to support infrastructuredevelopment and facilitate two-way tradeis going to be important in winning overgovernments and customers.

Reinventing the organisationA new approach to organisationaldesign may be needed as India’s FSbusinesses seek to create more nimbleand adaptive operational capabilities andmake sure their talent, structure andgovernance reflect their increasinglyinternational horizons.

Businesses also need to contend with amore complex risk profile. SAAAMEcountries have varied legal and regulatoryframeworks, political systems, businessethics and cultures. It’s important forIndian groups to develop the timely andreliable management information andrisk management systems needed tooperate in new and unfamiliar markets.

Operating models will need to reflectthe changing geographical focus of thebusiness. They will also need to dealwith more extensive partnership andco-opetition arrangements and besufficiently agile to respond quickly tounfamiliar market conditions, distributionchannels and cultural preferences.

The underlying challenge is securingsufficient talent in markets where suitablyqualified and experienced people mayalready be in short supply. Short-term andreactive approaches, be this seeking tolure key people from competitors, orbringing in large numbers of expatriatepersonnel are likely to prove excessivelycostly and may still fail to provide thepeople needed to meet strategicobjectives. A more systematic andforward-looking workforce plan, capableof anticipating and meeting skills’ needscould reduce costs and allow FSorganisations to build a more sustainableplatform for business development.

Moving into IndiaInternational businesses looking to moveinto India face a number of challenges.Difficulties in securing licences, tightrestrictions on foreign ownership (5%limit for each firm and 74% overall) andrestricted voting rights have deterredinbound investment in the banking sector.Foreign stakes in Indian insurers arelimited to 26%, though M&A and IPOrules are under review. A morestraightforward route into India may beinvestment in non-bank financialinstitutions, which allow 100% foreignownership and offer access to fast-growing segments such as mortgages,vehicle finance, credit cards distributionand stockbroking.

12 PwC Project Blue

We believe that there are five key questions that FS businesses should consider as theylook at how to gear their strategy and operations to an increasingly competitive andglobalised sector:

• How is technology reshaping the expectations of your customers and how can youdevelop the intuitive and interactive services that would put you at the forefront ofthe market?

• How are your corporate clients responding to the shift in the focus of global growthand how can you develop your services and geographical reach to support themmore effectively?

• Are there opportunities to extend your regional and wider international footprintand what strengths would you be looking to leverage as part of such a strategy?

• Is your governance and risk management equipped to deal with a more complex andglobalised sector?

• Is the recruitment, retention and development of talent within your organisationequipped to meet long-term strategic objectives and how can you develop a moreproactive strategic plan?

Opening up new frontiers

India’s financial institutions havedeveloped rapidly in recent years.But they can no longer rely on thecountry’s GDP growth to deliverassured profitability andexpansion. They will need to meetrising customer expectations,increase financial inclusion andsupport corporate clients as theyreach into new markets. Failure tokeep pace could leave some playersat risk of losing business to fastermoving competitors, includingWestern or SAAAME groups.

PwC Project Blue 13

14 PwC Project Blue

Making sense of an uncertain future

We’re working with a range ofFS organisations to judge theimpact of the mega-trends shapingtheir industry, and where and howthey can compete most effectively.If you’d like to discuss any of theissues raised in this paper, or theimpact of other trends examined inProject Blue, please contact eitherof those who are listed here, or yourusual PwC contact.

Manoj K Kashyap Financial Services Leader PwC (India) Tel: +91 (22) 6669 1401 Email: [email protected]

Robin Roy Associate Director, Financial Services PwC (India) Tel:+ 91 (80) 4079 4009 Email: [email protected]

The Project Blue framework seen here begins with the considerations needed to adaptto the current instability. It then goes on to assess what FS businesses need to do to planfor, and ideally take advantage of, the changes ahead.

One of the main things we’ve been looking at is the extent to which these developmentscould disrupt existing business models. We’ve also been looking at how these trendsare feeding off each other. A clear case in point is the extent to which rapid growth inemerging markets is spurring a mass influx of people into the cities.

Our clients are using the framework to help them judge the implications of thesedevelopments for their particular business, and look at how to take advantage of thechanges ahead. Will business and operational models still be viable in this newlandscape? What strengths within the business would allow it to develop a leadingposition? What talent and investment will need to be put in place now, to prepare forthe changes ahead?

Project Blue framework

The Project Blue frameworkconsiders the major trendsthat are reshaping the globaleconomy and transforming thebehaviour of consumers, businessesand governments.

Figure 7: The Project Blue framework

Source: PwC Project Blue analysis

Project Blue Framework

Global instability

Regulatory environment Fiscal pressures Political and social unrestAdapt

Rise and interconnectivityof the emerging markets(SAAAME)

• Economic strength• Trade• Foreign direct investment

Demographic change • Population growthdiscrepancies

• Ageing populations

Social and behaviouralchange

• Urbanisation• Global affluence• Talent

• Capital balances• Resource allocation• Population

• Changing family structures• Belief structures

• Changing customerbehaviours – social media

• Attitudes to financialinstitutions

Technological change • Disruptive technologiesimpacting FS

• Digital and mobile

War for natural resources • Oil, gas and fossil fuels• Food and water• Key commodities

Rise of state-directedcapitalism

• State intervention• Country/city economicstrategies

• Technological and scientificresearch and developmentand innovation

• Ecosystems• Climate change andsustainability

• Investment strategies• Sovereign wealth funds/development banks

Plan

www.pwc.com/projectblue This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon theinformation contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers does not accept or assume any liability,responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

For more information on Project Blue, or other Financial Services programmes, please contact Áine Bryn, Global Financial Services Marketing Leader, PwC (UK)on +44 207 212 8839, or [email protected].

For additional copies, please contact Maya Bhatti, Global & UK Financial Services Marketing, PwC (UK) on +44 207 213 2302, or [email protected].

© 2012 PwC. All rights reserved. Not for further distribution without the permission of PwC. “PwC” refers to the network of member firms of PricewaterhouseCoopersInternational Limited (PwCIL), or, as the context requires, individual member firms of the PwC network. Each member firm is a separate legal entity and does not act asagent of PwCIL or any other member firm. PwCIL does not provide any services to clients. PwCIL is not responsible or liable for the acts or omissions of any of itsmember firms nor can it control the exercise of their professional judgment or bind them in any way. No member firm is responsible or liable for the acts or omissions ofany other member firm nor can it control the exercise of another member firm’s professional judgment or bind another member firm or PwCIL in any way.