pro-competitive regulation of the markets for electronic ... · for electronic communications and...

TRANSCRIPT

Pro-competitive regulation of the markets

for electronic communications and

relationship with competition law and the

competition authority in Europe

Regulatel – V Reunión de Grupos de Trabajo

Dr. Annegret Groebel, BNetzA (Germany)

Head of Department International Relations / Postal Regulation

Cartagena – 13 April 2015

Regulatory governance: ensuring effective regulation (1)

Effective regulation is based on professional expertise (analysis) and delivers on

the objectives set out in the law following the overall agenda of the government,

i.e. the regulatory body must have a clear mandate and ex-ante powers (incl.

enforcement/sanctioning powers to enforce compliance)

This requires a strong legal basis and an independent regulator (otherwise

regulation will not be effective)

Institutional design: independence and accountability

Organisational design: sector-specific regulator; multi-sector regulator

Procedural principles: sound administrative procedures in place to perform

effectively (good governance)

Fundamental principles: predictability, forward looking and long term commitment

(credibility) and a principle based approach

Judicial review: on the merits of the decision

For effective regulation the NRA needs to be independent and has regulatory

discretion to impose ex-ante sector-specific obligations

Multi-sector regulator in Germany was built up gradually by adding further

responsibilities to RegTP, change of names in 2005: Bundesnetzagentur (BNetzA)

Independent higher federal authority in the scope of business of the Federal Ministry of Economics and Energy

Sector-specific authority tasked with promoting

effective competition in 5 network industries by

means of ex-ante regulation

Telecoms (incl. spectrum) and Post (since 1998),

Electricity and Gas (since 2005), and

Railways (since 2006)

Electricity + gas grid development plan (since 2011)

BNetzA employs ar. 200 staff in energy regulation,

up to 240 staff are being recruited for electricity grid expansion

planning and (nationwide) permitting (2013)

Overall headcount for all sectors: ar. 2900 staff, 196.3 mio € tax-funded

budget (2014), besides sector-specific legislation, there is one act

containing all BNetzA governance rules

– BNetzA is member of CEER/ACER, IRG/BEREC, ERG-P and IRG Rail

Bundesnetzagentur: National German regulator

HQ in Bonn

4 © Bundesnetzagentur 4

Overall Mission of Bundesnetzagentur…

… to promote sustainable competition in the markets for electricity, gas,

telecommunications, postal services and railways...

… to promote effective competition and efficient infrastructures in telecommunications

and to guarantee appropriate and adequate services throughout Germany (Art. 1 Tel. Act)

…via regulating these markets, i.e. market regulation by a regulatory body with ex-ante

powers (to impose sector specific obligations)

administrative body whose decisions are administrative acts

(subject to juridical control)

no micromanagement of markets, but pro-competitive regulation: setting conditions by

implementing the rules and giving price signals in order to steer market forces towards a

competitive market development as competition is the best driver for efficient investment

and delivering benefits to consumers (more choice and more value for money)

Overall approach: pro-competitive regulation as competition delivers

benefits for consumers and results in competitiveness as well as driving

efficient investment in infrastructure

No micromanagement, but setting conditions prevailing in a competitive

market in order to drive rational (undistorted) economic decisions of market

players, i.e. simulate competition to stimulate competition, it is up to the

operators to decide on investments acc. to their business models

This includes accepting market outcomes, i.e. no corrections, no interference

Process of liberalisation was initiated by the European directives in order to

open up markets for competition while the state influence was restricted to

regulation in order to promote and safeguard competition.

Process of legal market opening (liberalisation) will not work without

economic regulation to ensure new entrants (competitors) can make use of

new possibilities and compete effectively: regulation guarantees a level

playing field!

Competition is the best driver for efficient investment and consumer

benefits, but in network industries it can only be achieved with strict access

and price control regulation applied ex-ante, thus competition and regulation

are not opposed to each other, but reinforcing each other

Regulatory governance: ensuring effective regulation (2)

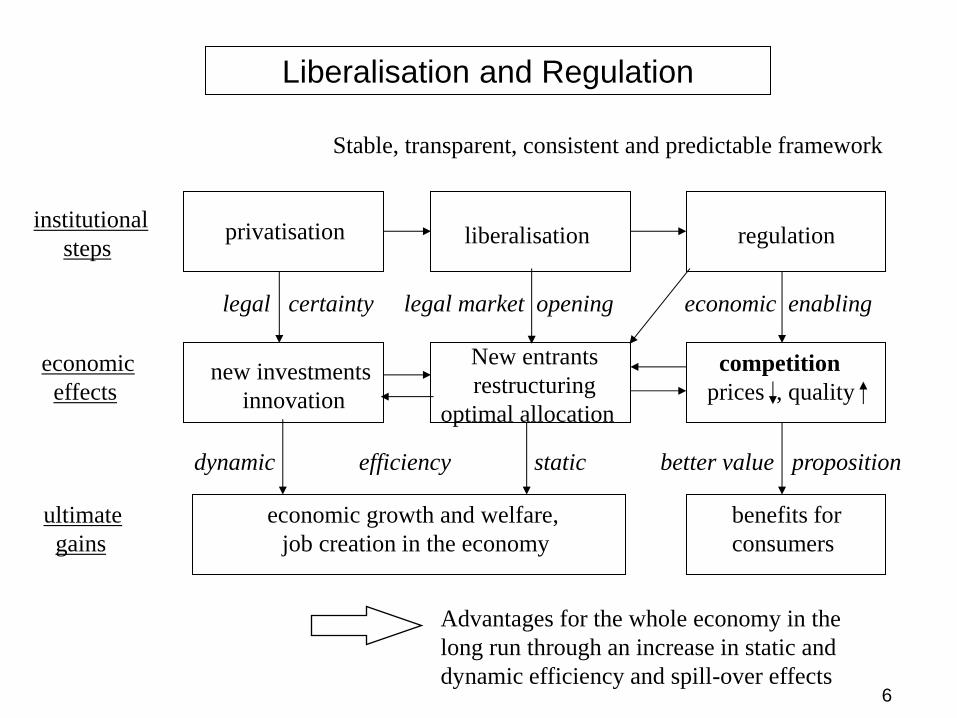

6

privatisation liberalisation regulation

competition

prices , quality

New entrants

restructuring

optimal allocation

new investments

innovation

economic growth and welfare,

job creation in the economy

benefits for

consumers

institutional

steps

economic

effects

Stable, transparent, consistent and predictable framework

legal certainty

Advantages for the whole economy in the

long run through an increase in static and

dynamic efficiency and spill-over effects

ultimate

gains

legal market opening economic enabling

dynamic efficiency static better value proposition

Liberalisation and Regulation

7

Regulation Competition

Consumer

benefits

Efficient

investment

MARKET

LEGAL FRAMEWORK

Administrative acts

Liability, contractual and company law etc.

Property rights framework

Contractual relations

Pro-competitive regulation setting incentives to behave acc.

to econ. rationality is in conformity with market mechanisms

Competitiveness

Regulatory approach and mechanism

Regulatory principles • Competition as a means to create economic welfare and in

particular consumer benefit (lower prices, better quality and more

choice, i.e. a better value proposition for the user)

• Regulation as a means to promote sustainable competition via

opening markets in network industries a. creating a level playing field

• Network industries are characterised by market entry barriers

resulting from substantial economies of scale + scope as well as

network effects requiring sector specific regulation to overcome

market entry barriers

• 2002 ECNS Framework based on competition law principles, i.e.

regulation of the relevant market susceptible to ex-ante regulation,

requiring a market analysis and imposition of sector specific

obligations (remedies) on an SMP operator (asymmetric regulation)

• Review of the Framework: proposals of publ. 13/11/07

• 2009 Revised Framework: basic principles still apply, but adjusted

to objectives of ensuring investment in next generation networks

(NGN/NGA) + level of competition reached with the 2002 framework

Regulatory objectives and priorities (1) • Regulatory objectives:

– Promote effective competition for the benefit of the

European citizen

– Promote efficient investment through predictability

– Promote the internal market through a consistent

application of the regulatory framework

• Regulatory priorities:

- maintain level of competition (avoid re-monopolization) and

incentivise efficient investment in NGA and NGN core (IP)

- maintain balance of service and infrastructure competition

- maintain the institutional balance in Europe

• Investing in new technologies: beginning of the investment

cycle, and overcoming at the same time the effects of the

financial crisis for financing new investments in NGA / NGN

as well as ensuring a competitive roll-out is a challenge

• Providing a stable, transparent and predictable framework for

the market players to take economically rational decisions

• Promote competition and enable new services, market entry

and investment in network industries

generating efficient investment is of key importance, more

emphasis is put on investment incentives: dynamic approach

this can best be achieved with pro-competitive regulation

as competition is the best driver of investment

• Balanced incentives to invest in NGN/NGA and not to hamper

the level of infrastructure competition reached with (LLU)

regulation so far

Regulatory objectives and priorities (2)

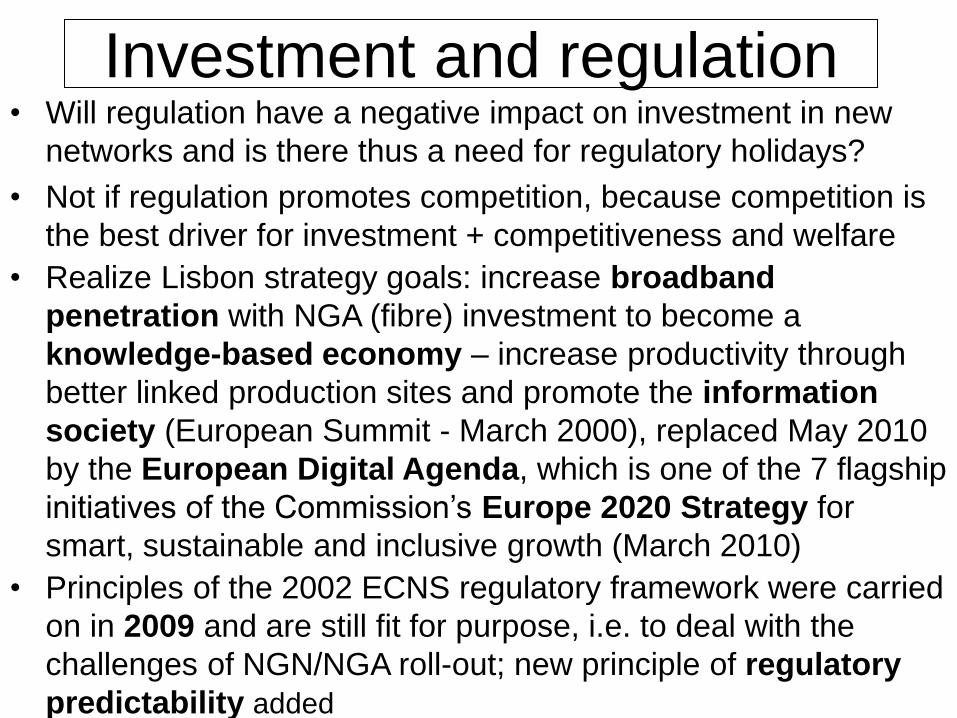

• Will regulation have a negative impact on investment in new

networks and is there thus a need for regulatory holidays?

• Not if regulation promotes competition, because competition is

the best driver for investment + competitiveness and welfare

• Realize Lisbon strategy goals: increase broadband

penetration with NGA (fibre) investment to become a

knowledge-based economy – increase productivity through

better linked production sites and promote the information

society (European Summit - March 2000), replaced May 2010

by the European Digital Agenda, which is one of the 7 flagship

initiatives of the Commission’s Europe 2020 Strategy for

smart, sustainable and inclusive growth (March 2010)

• Principles of the 2002 ECNS regulatory framework were carried

on in 2009 and are still fit for purpose, i.e. to deal with the

challenges of NGN/NGA roll-out; new principle of regulatory

predictability added

Investment and regulation

Service

Network

Terminal

Voice

telephony

Fixed

Mobile

Telephone/

Handset

Data

Fixed

PC

Broadcasting

Cable

Satellite

Terrestrial

Television

Until 2002: separate networks and separate regulatory rules

Convergence is a reality !

TV & Games

WLAN/WiMAX UMTS

VoIP

Videotele-

phony

PSTN

Content Triple Play

• Convergence of voice, data, internet, TV and other media services is no longer a vision but already reality, but require investment in powerful network infrastructure providing a higher capacity (to cope with the traffic)

• Consumers have more choice and can use their devices to receive different

types of services, e.g. watch TV on their PCs, mobile Internet, mobile TV

and be interactive

• Triple play bundles are a chance for telcos to compensate for revenue loss

in voice services, but new tariff structures are offered as well: flat rates

• Convergence of communications and broadcasting services as well as

• Convergence of fixed and mobile services with potentially changing market boundaries; furthermore the increased usage of so-called OTT services

• This will impact on the market definition as well as on the market structure

• Convergence is a key driver for market dynamics and an enabler of growth

• New services, new players, new business models are likely to lead to a higher market dynamic, supply side and demand side changes indicate

• Chances and risks (leverage of market power) for competition

Convergence of services and markets (1)

• The degree of convergence is very different from nation to nation and between different consumer groups

• The pace of adaptation will vary, and for some time markets will be split in many segments: early adopters, technology freaks and frontrunners, smart followers and people who are unwilling to change and are only looking for cheap voice calls will coexist

• With services converging, markets will slowly be converging as well, e.g. a separate fixed services and mobile services market will in the long run become a single market for communications services, consumer considering fixed and mobile calls substitutable, more and more they will replace traditional voice services with VoIP services

• Regulation has to guarantee open markets for innovation and

cooperation as well as a level playing field by applying the

principle of technological neutrality and ensuring transparency

for consumers to choose according to their preferences

Convergence of services and markets (2)

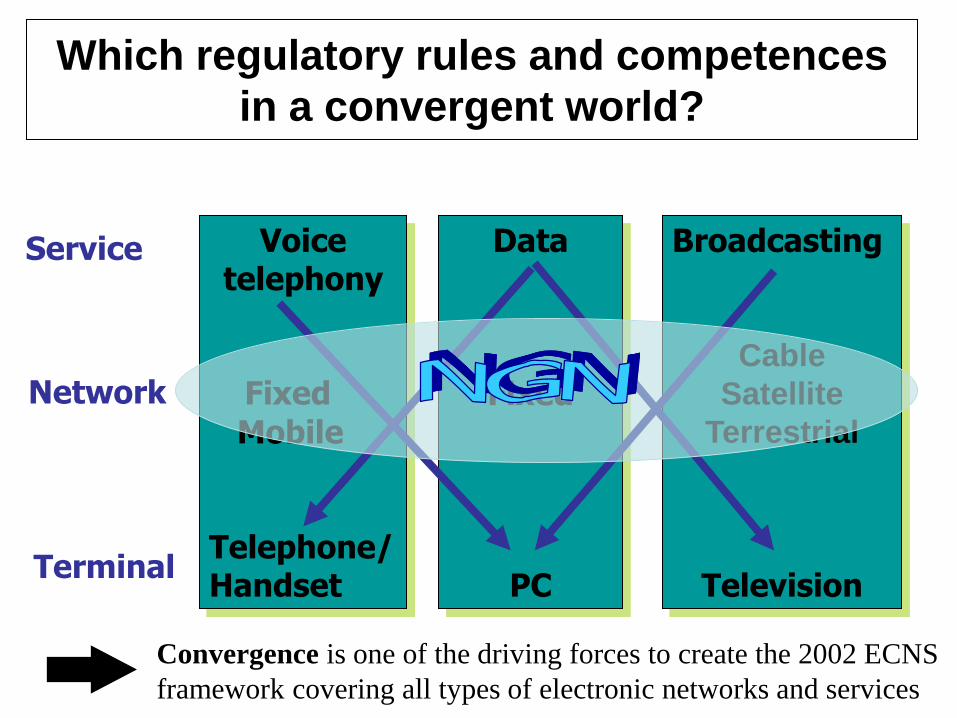

Which regulatory rules and competences

in a convergent world?

Data

Fixed

PC

Broadcasting

Cable

Satellite

Terrestrial

Television

Voice telephony

Fixed

Mobile

Telephone/Handset

Service

Network

Terminal

Convergence is one of the driving forces to create the 2002 ECNS

framework covering all types of electronic networks and services

Data Protection Directive

Spectrum

Decision

(Art. 95)

Framework

Directive

(Art. 95)

Authorisation Directive

Access & Interconnection Directive

Users’ Rights Directive

Guidelines on SMP

Recommendation on relevant markets

Liberalisation

Directive

(Art. 86)

Recommendation on Article 7

2002 ECNS Regulatory Package

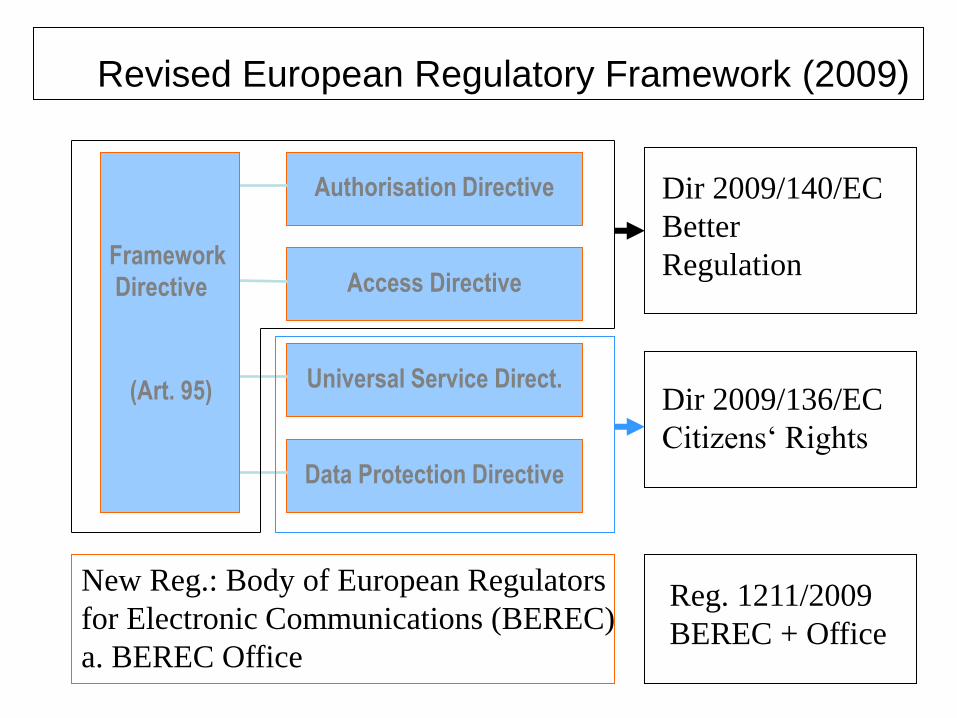

Revised European Regulatory Framework (2009)

Authorisation Directive

Access Directive

Universal Service Direct.

Data Protection Directive

Framework

Directive

(Art. 95)

Dir 2009/140/EC

Better

Regulation

Dir 2009/136/EC

Citizens‘ Rights

Reg. 1211/2009

BEREC + Office

New Reg.: Body of European Regulators

for Electronic Communications (BEREC)

a. BEREC Office

• The 2002 ECNS regulatory framework gives NRAs the powers to:

• to intervene in a timely manner

• to react flexible

• to make a more differentiated use of the remedies by choosing the

appropriate remedy from the toolbox

• to focus regulatory intervention to a minimum and to those cases

where it is inevitable for the time being

• to give adaquate answers according to the state of competition

and stage of the national market:

- with less intrusive interventions in more advanced markets

and

- continued strict regulation where needed to prevent

leveraging of market power

(as in bottleneck type markets such as the local loop)

Principles of the ECNS Regulatory Framework (1)

Changing market structures,

convergence of markets, high market dynamics

Technological neutrality

Harmonisation

Competition law principles

Flexibility for NRAs

Principles of the ECNS Regulatory Framework (2)

Objectives

competition +

internal market

(Art. 8 FD)

Flexibility =

discretion to choose

among remedies

(Art. 8 AD)

Consistent Applic.

BEREC + NRA

co-regulation proc.

(Reg., Art.7/a FD)

Regulatory Balance (1)

Control = Veto

power of the Cion:

Consolidation proc.

(Art. 7 FD)

Role of the NRA

(Art. 3/a FD)

Reliance on

competition law

Development of

internal market

Technological

neutrality

Effectively

competitive

markets

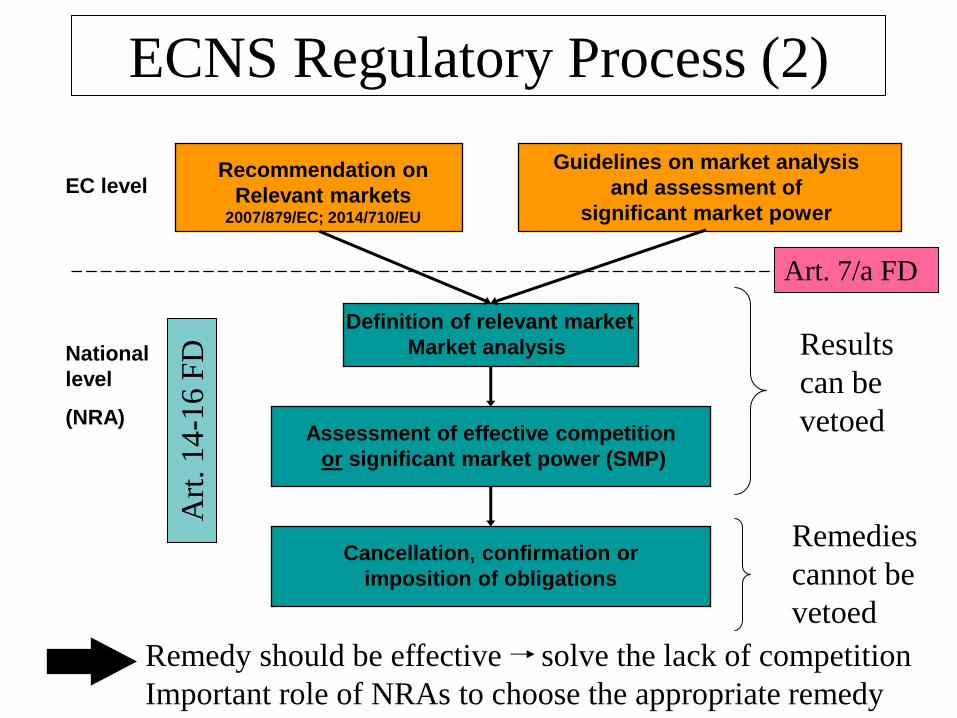

ECNS Regulatory Process (1) • 3 Stages:

- market definition: relevant market (list of 7 markets; 2014: 5 markets) - market analysis: designation of SMP operator(s) - choice of remedy: imposition of regulatory obligation(s)

• If an operator is found to be dominant (either individually or jointly), at least one specific regulatory obligation must be imposed, which must be proportionate to remedy the problem, justified in the light of the Art. 8 FD objectives and based on the nature of the problem

• Instead of the former automatism, NRAs are now given the flexibility (discretion) to choose the appropriate remedy: increased role for NRAs

• Remedies must be effective: solve the lack of competition

• Remedies are to be chosen from the list in the AD/UD (“toolbox”)

• Remedies on the retail level to be applied only in case wholesale obligations do not work (concept of the priority of strict wholesale reg.)

• Notification (consolidation/co-regulation) procedure acc. to Art. 7/a FD: Veto power on stages 1 + 2 (market definition + SMP), but no veto power on the application of remedies (stage 3), only comments and the recommendation addressed to the NRA which have to be taken into utmost account by the NRAs when adopting the final measures

Recommendation on

Relevant markets 2007/879/EC; 2014/710/EU

Guidelines on market analysis

and assessment of

significant market power

Assessment of effective competition

or significant market power (SMP)

Cancellation, confirmation or

imposition of obligations

National

level

(NRA)

EC level

ECNS Regulatory Process (2)

Results

can be

vetoed

Remedies

cannot be

vetoed

Remedy should be effective solve the lack of competition

Important role of NRAs to choose the appropriate remedy

Definition of relevant market

Market analysis

Art. 7/a FD

Art

. 14

-16 F

D

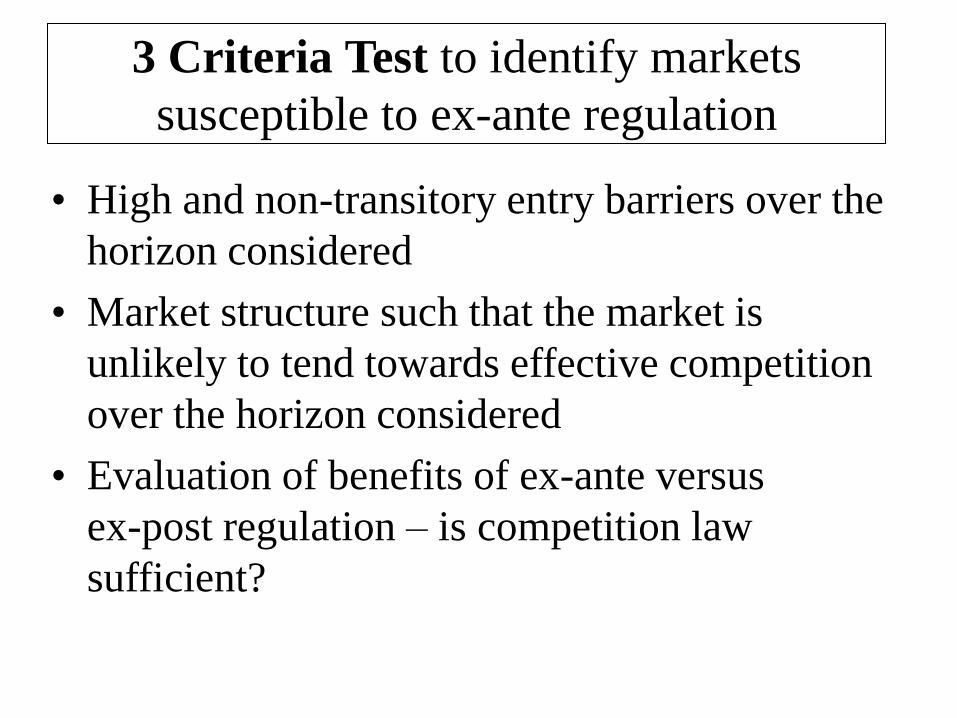

3 Criteria Test to identify markets

susceptible to ex-ante regulation

• High and non-transitory entry barriers over the

horizon considered

• Market structure such that the market is

unlikely to tend towards effective competition

over the horizon considered

• Evaluation of benefits of ex-ante versus

ex-post regulation – is competition law

sufficient?

List of markets acc. to the Recommendation 2007/879/EC

Changes of the List of markets in the new Recommendation 2014/710/EU

• Market 1: Wholesale call termination on individual

public telephone networks provided at a fixed

location

• Market 2: Wholesale voice call termination on

individual mobile networks

• Market 3:

(a) Wholesale local access provided at a fixed

location

(b) Wholesale central access provided at a fixed

location for mass-market products

• Market 4: Wholesale high-quality access provided

at a fixed location

List of relevant markets acc. to the Rec. 2014/710/EU

28

Sector specific regulation: general competition law is not sufficient, regulatory instruments must go beyond competition law interventions

• Natural monopolies (energy/railway networks) and dominance (telecoms/postal markets) are the trigger for regulation

• Incumbents = vertically integrated companies

own essential facilities (or enduring bottlenecks)

incumbent = competitor to entrants on the retail level

• Incumbent would be able to maintain its dominant position after market opening (liberalisation) unless ex-ante regulation acts as a counterpart and ensures a level playing field through non-discrimination, access and cost-oriented price regulation where the price is set at the level of the efficient costs as this is the price prevailing in a competitive market (as well as different forms of separation/unbundling)

Regulation vs. Application of competition law (1)

Regulation vs. Application of competition law (2)

Competition law intervention:

abuse of dominance (i.e. anti competitive behaviour) by dominant firms

(ex- post intervention)

ban on cartels (incl. some exceptions) (ex-post)

merger control (ex ante/ ex post)

No ex-ante price approval, but ex-post price examination by BKartA (NCA):

usually prices of comparable competitive markets (benchmarking) as market is

functioning,i.e. returning to the equilibrium after abuse of market power whereas in

a liberalised market with structural barriers it is assumed that there is a structural

imbalance and the market would not tend towards competition after an abuse of

market power which must therefore prevented before it can happen: ex-ante

regulation required

checking for margin squeeze

Ex-ante powers of the national regulator BNetzA when applying regulatory law: ex-ante

price control: prices based on costs of efficient service provision (stricter standard) and

ex-ante margin squeeze test, but: competition law applies as a safety net!

• BNetzA: Regulatory body for sector regulation: • economic (and technical) regulation

• economic regulation: ex-ante regulation: access and price control obligations, ex-post control of abusive practices

• technical regulation: frequency allocation, technical standards, radio monitoring etc.

• Cartel office (BKartA) for competition law intervention

• Clear line between regulator and cartel office: • definition of regulated services laid down in:

• separate laws (e.g. Telecommunications Act, Energy Industry Act, Postal Act)

• legal provision for information exchange to ensure legal certainty and avoid misunderstanding and double work

• no concurrent powers (i.e. no application of general competition law by BNetzA, but elements of the general competition law are directly incorporated provisions in the Telecommunications Act and the Energy Industry Act)

• But: Acc. to the ECJ ruling (case C-280/08) in 2010, competition law always applies, also in regulated sectors!

BNetzA & BKartA (1) BNetzA & BKartA (1)

© Bundesnetzagentur 31

BNetzA & BKartA (2)

• Umbrella approach:

BKartA alone handles merger control, but coordinating

function regarding definition of relevant markets by NRA

(telecoms, post)

BNetzA obliged to seek agreement on definition of relevant

market as well as determination of an operator with significant

market power. BKartA has the right to give its opinion on

planned remedies. (telecoms, post)

Same threshold & criteria for dominance applied to all sectors

to guarantee a close link between general competition law

and sector-specific regulation

© Bundesnetzagentur 32

• Cooperation between regulator and cartel office:

• comments by cartel office prior to publishing decisions

• agreements on defining relevant markets & determining SMP

• facilitates investigating for both authorities

• Applying same standards:

• same threshold for dominance applied to all sectors to ensure close link between

general competition law intervention and sector regulation

BNetzA & BKartA (3) BNetzA & BKartA (3)

© Bundesnetzagentur 33

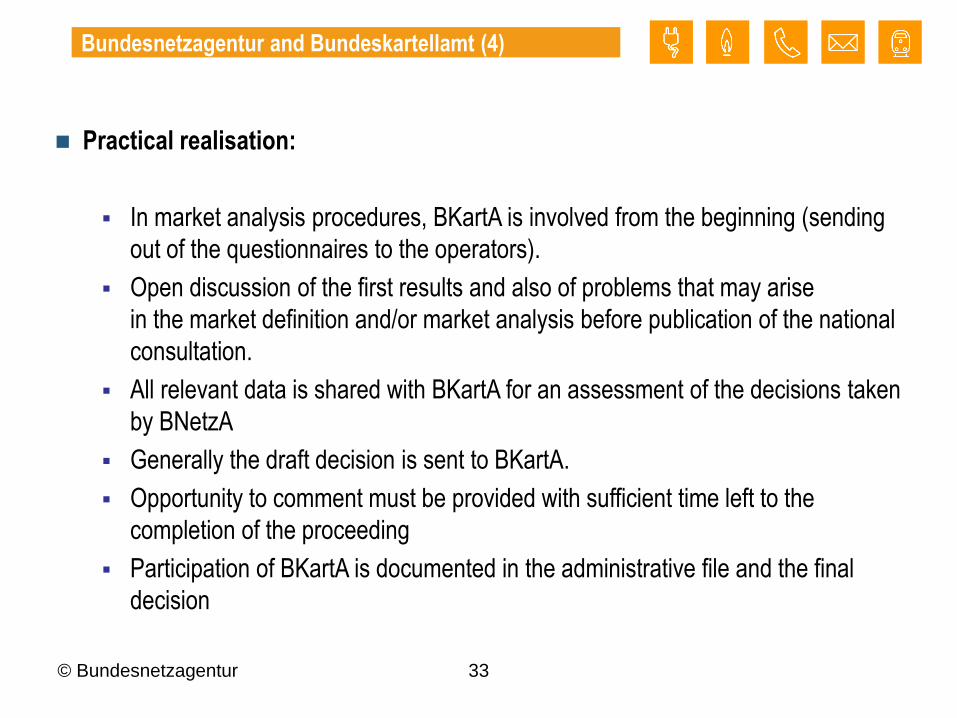

Bundesnetzagentur and Bundeskartellamt (4)

Practical realisation:

In market analysis procedures, BKartA is involved from the beginning (sending

out of the questionnaires to the operators).

Open discussion of the first results and also of problems that may arise

in the market definition and/or market analysis before publication of the national

consultation.

All relevant data is shared with BKartA for an assessment of the decisions taken

by BNetzA

Generally the draft decision is sent to BKartA.

Opportunity to comment must be provided with sufficient time left to the

completion of the proceeding

Participation of BKartA is documented in the administrative file and the final

decision

© Bundesnetzagentur 34

Bundesnetzagentur and Bundeskartellamt (5)

Co-operation with the Federal Cartel Office in the Telecommunications sector

Market Definition

and Analysis (Decision taken by the

President‘s chamber)

Imposition of

regulatory

obligations

Regulatory

decisions (such as price approval,

order to grant access)

Decision must be

taken in agreement Cartel Office has

right to comment Cartel Office has

right to comment

Opportunity to comment must be provided with sufficient time left to the completion of the proceedings.

© Bundesnetzagentur 35

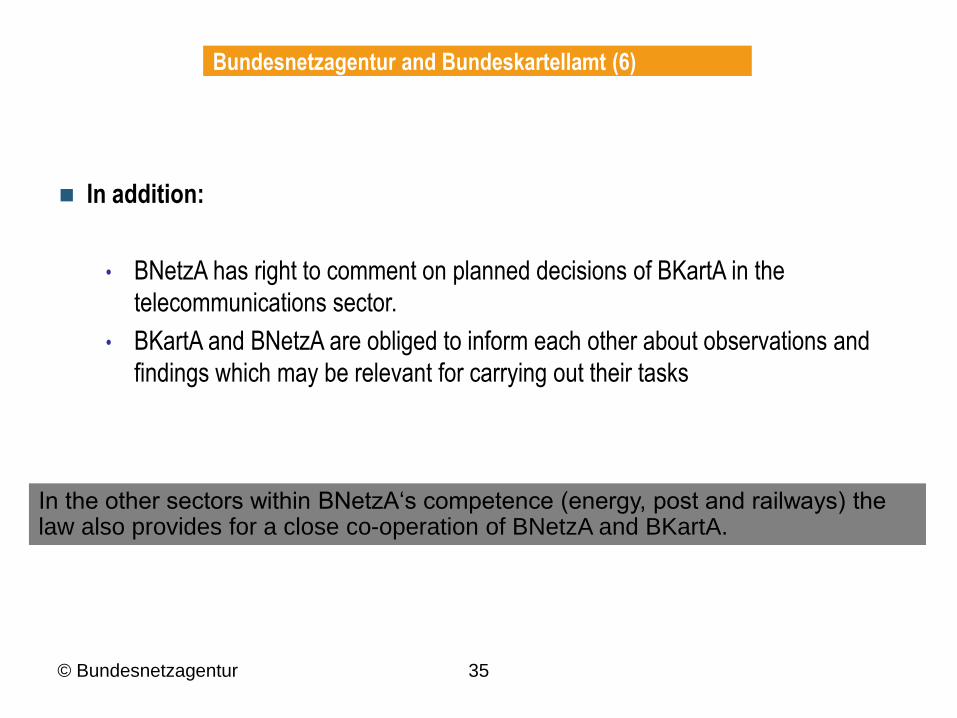

Bundesnetzagentur and Bundeskartellamt (6)

In addition:

• BNetzA has right to comment on planned decisions of BKartA in the

telecommunications sector.

• BKartA and BNetzA are obliged to inform each other about observations and

findings which may be relevant for carrying out their tasks

In the other sectors within BNetzA‘s competence (energy, post and railways) the law also provides for a close co-operation of BNetzA and BKartA.

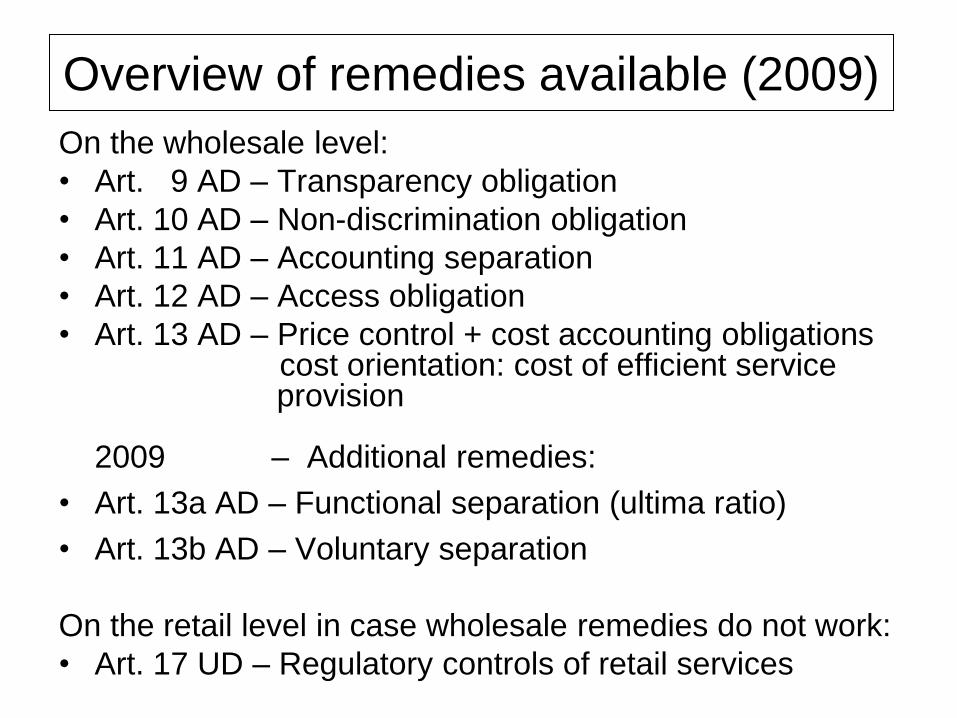

Overview of remedies available (2009)

On the wholesale level:

• Art. 9 AD – Transparency obligation

• Art. 10 AD – Non-discrimination obligation

• Art. 11 AD – Accounting separation

• Art. 12 AD – Access obligation

• Art. 13 AD – Price control + cost accounting obligations cost orientation: cost of efficient service provision 2009 – Additional remedies:

• Art. 13a AD – Functional separation (ultima ratio)

• Art. 13b AD – Voluntary separation

On the retail level in case wholesale remedies do not work:

• Art. 17 UD – Regulatory controls of retail services

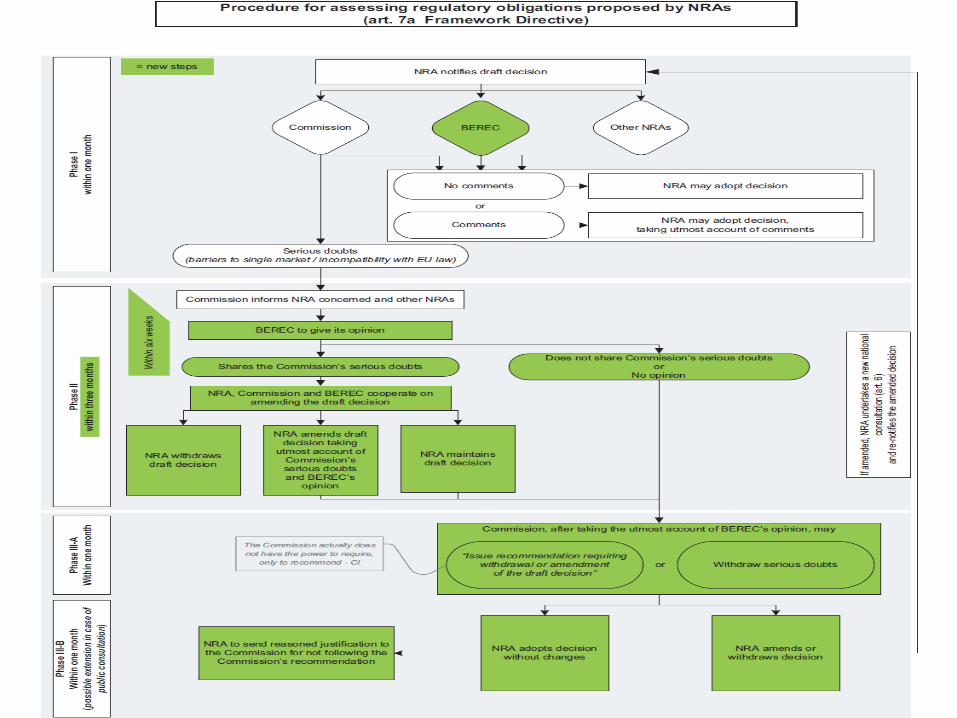

Article 7/7a

Art 3.1.a Opinions on draft measures of NRAs concerning market definition,

designation of undertakings with significant market power and

imposition of remedies, and to cooperate and work together with the

NRAs

This task did not become operative until the date for transposition of the Directives –

May 2011

The modified Article 7 and the new Article 7a impose new obligations on the NRAs and

therefore required transposition into national law.

During the 18 month transposition period, the existing practice of IRG expert teams

considering the Commission’s serious doubts letter continued.

After the 2009 regime started, BEREC took up its statutory role of providing an Opinion

by setting up teams of experts from NRAs when a Phase-II was opened

37

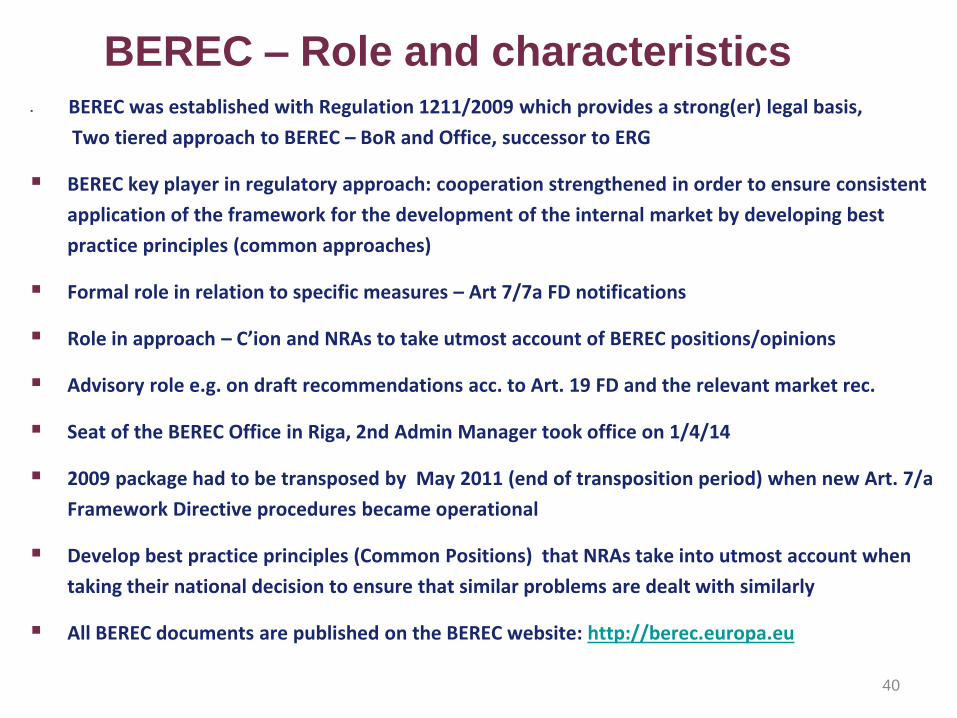

BEREC – Role and characteristics BEREC was established with Regulation 1211/2009 which provides a strong(er) legal basis,

Two tiered approach to BEREC – BoR and Office, successor to ERG

BEREC key player in regulatory approach: cooperation strengthened in order to ensure consistent

application of the framework for the development of the internal market by developing best

practice principles (common approaches)

Formal role in relation to specific measures – Art 7/7a FD notifications

Role in approach – C’ion and NRAs to take utmost account of BEREC positions/opinions

Advisory role e.g. on draft recommendations acc. to Art. 19 FD and the relevant market rec.

Seat of the BEREC Office in Riga, 2nd Admin Manager took office on 1/4/14

2009 package had to be transposed by May 2011 (end of transposition period) when new Art. 7/a

Framework Directive procedures became operational

Develop best practice principles (Common Positions) that NRAs take into utmost account when

taking their national decision to ensure that similar problems are dealt with similarly

All BEREC documents are published on the BEREC website: http://berec.europa.eu

40

BEREC

European Parliament Council of Ministers European Commission

Issue reports, provide advice and

deliver opinions on any matter

regarding electronic

communications within its

competence, Art. 2 (d)

same as

Parliament

Opinions on draft decisions,

recommendations and guidelines

Commission shall take utmost

account of BEREC opinions, Art. 3

(3) BEREC Reg., Art. 7/a, Art. 19 FD

National Regulatory Authorities (NRAs)

Develop and disseminate among NRAs regulatory

best practice, Art. 2 (a)

Provide assistance to NRAs on regulatory issues,

Art. 2 (b)

NRA shall take utmost account of any opinion,

recommendation, guideline, advice or regulatory best

practice adopted by BEREC, Art. 3 (3) and Art. 3 (3c) FD

BEREC’s role in interacting with the institutions

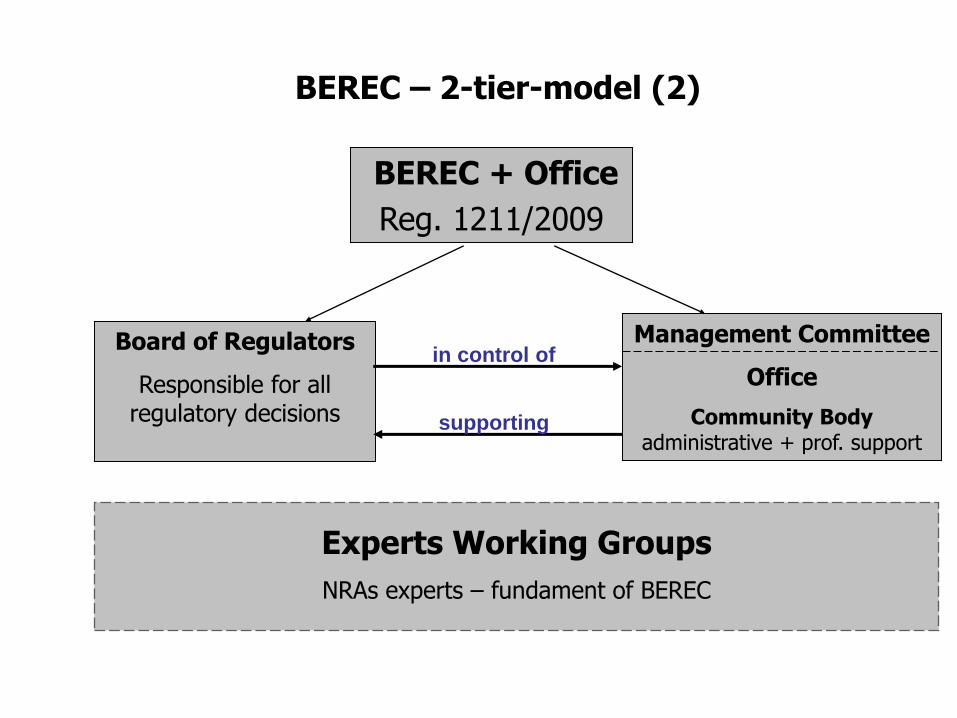

BEREC – 2-tier model (1)

Board of Regulators

Regulatory decision making group

BEREC

Not an agency

The Office

Community Body, funded from the

Community budget

in control of

supporting

• Office is controlled by the Management Committee

• Office is accountable to Management Committee

• Management Committee replaces Administrative Board in regular

European agencies, identical with BoR (+1 Cion), thus NRAs are

in full control of the supporting Office

Board of Regulators

Responsible for all regulatory decisions

BEREC + Office

Reg. 1211/2009

Management Committee

Office

Community Body administrative + prof. support

in control of

supporting

BEREC – 2-tier-model (2)

Experts Working Groups

NRAs experts – fundament of BEREC

BEREC – BoR (28 NRA heads + observers)

Contact Network

Preparation of Plenary meetings, senior representatives of 28 NRAs with a mandate to speak for their NRA

Expert Working Groups – EWG 2014

Roaming (ES, AT)

Radio Spectrum (ITA, Swe)

Next Generation Networks (DE)

Termination Rates (FR, IT)

Benchmarking (ES) End-User (RO, PT)

Net Neutrality (NO, FR) Regulatory Accounting (IT, DE)

BEREC Evaluation (NL)

Remedies (UK)

Framework Implementation (IT)

Market Econ Analysis (ES, FR)

A – Boosting NGN B – Consumer empowerm. D – Horizontal/Quality aspe.

C – Boost. internal mark./DSM

BEREC EWG Structure 2015

Promoting Competition and

Investments

Next Generation Networks

EWG

Market and Economic analysis

EWG

Empowering and Protecting End-

users

Net Neutrality EWG

End-user EWG

Promoting the Internal market

Regulatory Framework EWG (FR

IMP / Spectrum)

Remedies TR EWG

Roaming EWG

Benchmarking and Cooperation

Benchmarking EWG

Regulatory Accounting

EWG

Pro-competitive regulation

effectively implemented, relying

on competition law principles

Effective

Competition

Efficient

investment and

consumer benefits

Consistency and

developing the

internal market

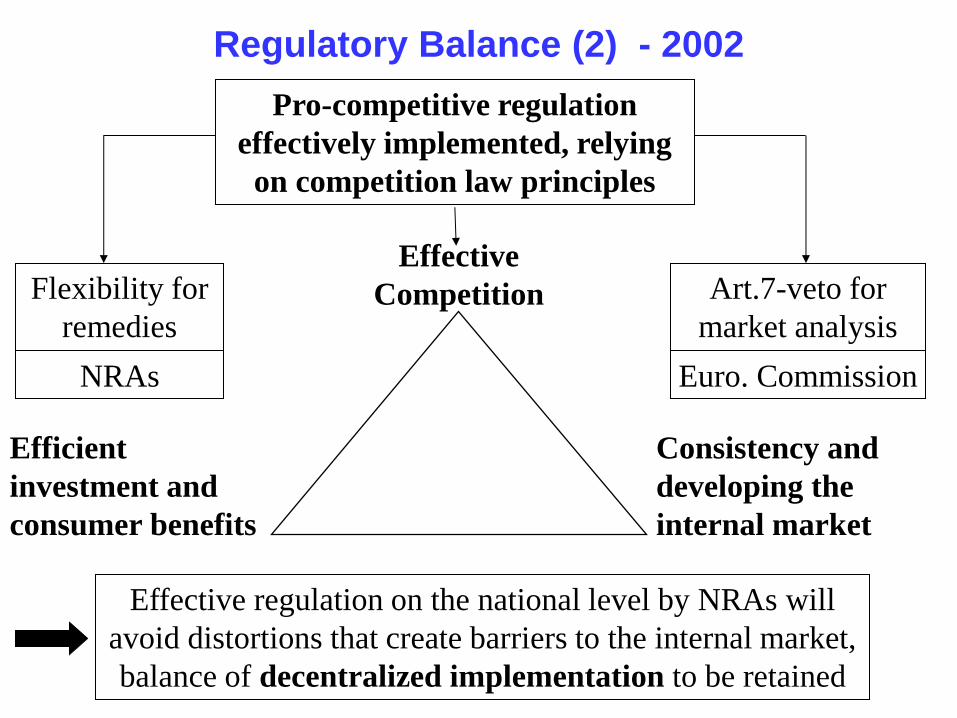

Effective regulation on the national level by NRAs will

avoid distortions that create barriers to the internal market,

balance of decentralized implementation to be retained

Flexibility for

remedies

Art.7-veto for

market analysis

NRAs Euro. Commission

Regulatory Balance (2) - 2002

Pro-competitive regulation

effectively implemented, relying

on competition law principles

Effective

Competition

Efficient

investment and

consumer benefits

Consistency and

developing the

internal market

No veto on remedies,

but a complex Art. 7a – co-regulation procedure

shifting the balance towards the European level

Flexibility for

remedies

Art.7-veto for

market analysis

NRAs Euro. Commission

Regulatory Balance (3) - 2009

BEREC /Art.7a

Political pressure

government

Regulatory capture

market players

Commission

NRA

independence

Effective regulation

right level of intervention

no over-/underregulation, no distortion

Multi-level model of regulation in Europe (1)

Political pressure

government

Regulatory capture

market players

Commission

NRA

Cooperation bodies

BEREC / ACER

Effective regulation

right level of intervention

risk of centralisation

NRA

independence

Multi-level model of regulation in Europe (2)

Comparative Overview Telecoms Energy

Informal NRA-platform /

formal non-profit

association (ASBL)

IRG

1997 / May-2008

CEER

2000 / June-2003

Official Commission

advisory group

(decisions)

ERG

2002

ERGEG

November 2003

Commision‘s proposals

European Agency:

top-down approach

EECMA (13-11-07)

European Electronic

Comm. Market Authority

ACER (19-09-07)

Agency for t.

Cooperat. of Energy

Regulators

2009 EU framework

EC Regulations

adopted by Council and

EP

BEREC (26-10-09)

2-tier model consisting of

Board of Regulators /

BEREC Office

ACER (25-06-09)

Agency solution

Reg. EC-713/2009

NRA platforms under

private Belgian law

2010 IRG decided to

continue IRG in parallel

CEER continues as

well, no formal deci.

Overview of remedies available (2009)

On the wholesale level:

• Art. 9 AD – Transparency obligation

• Art. 10 AD – Non-discrimination obligation

• Art. 11 AD – Accounting separation

• Art. 12 AD – Access obligation

• Art. 13 AD – Price control + cost accounting obligations cost orientation: cost of efficient service provision 2009 – Additional remedies:

• Art. 13a AD – Functional separation (ultima ratio)

• Art. 13b AD – Voluntary separation

On the retail level in case wholesale remedies do not work:

• Art. 17 UD – Regulatory controls of retail services

Art. 10 Non-discrimination obligation

• 1. A national regulatory authority may, in accordance with the provisions of Article 8, impose obligations of non-discrimination, in relation to interconnection and/or access.

• 2. Obligations of non-discrimination shall ensure, in particular, that the operator applies equivalent conditions in equivalent circumstances to other undertakings providing equivalent services, and provides services and information to others under the same conditions and of the same quality as it provides for its own services, or those of it subsidiaries or partners.

Article 11 Access Directive

Obligation of accounting separation 1. A national regulatory authority may, in accordance with the

provisions of Article 8, impose obligations for accounting separation

in relation to specified activities related to interconnection and/or access.

In particular, a national regulatory authority may require a vertically

integrated company to make transparent its wholesale prices and its

internal transfer prices inter alia to ensure compliance where there is a

requirement for non-discrimination under Article 10 or, where

necessary, to prevent unfair cross-subsidy. National regulatory authorities

may specify the format and accounting methodology to be used.

2. Without prejudice to Article 5 of Directive 2002/21/EC

(Framework Directive), to facilitate the verification of compliance

with obligations of transparency and non-discrimination, national regulatory

authorities shall have the power to require that accounting

records, including data on revenues received from third parties, are

provided on request. National regulatory authorities may publish such

information as would contribute to an open and competitive market,

while respecting national and Community rules on commercial confidentiality.

Art. 11 - Accounting Separation (2)

• Article 11 (1) refers (in particular) to the need for the vertically integrated company to make transparent their wholesale prices and their internal transfer prices

– No mention of costs

– Cross-market obligation

• But accounting separation implies need for cost information: Art. 11.2

– Art. 11.2 provides for the power to request cost accounting information

– Accounting separation needed to demonstrate cost orientation of services through disclosure of the costs of key components of the service

– Paragraph 18 of preamble to Access Directive also relates to Part 2 Recommendations which do go further with reference to cost data

Relevance of margin squeeze

tests • The application of margin squeeze tests has received considerable attention in electronic communication markets

• This sector usually is characterized by the presence of a vertically integrated network operator providing access to its competitors

• NRAs so far have mainly been involved in assessing whether margin squeeze occurred at the individual service level

• However, in a convergent world competition among operators will increasingly occur on multi-play offers, where various services (e.g. voice, data and video) will be provided in a bundle.

• In this scenario one of the new challenges NRAs will have to face is how to carry out a proper MS assessment.

• The challenge is even stronger in cases where bundled offers include both regulated and unregulated services.

Relevance of margin squeeze tests

Perspective to be used for a

MS test (I) Two tests to be distinguished: EEO vs. REO

• The first test (Equally Efficient Operator test, EEO) involves assessing whether the SMP firm’s downstream operations could trade profitably if it had to pay an upstream price that was equivalent to that charged to rival competitors.

• The second test (Reasonably Efficient Operator test, REO) involves examining whether the difference between the vertically integrated firm’s retail and input prices is sufficient for a “reasonably efficient” downstream competitor to make a “normal” profit.

In competition law the EEO approach is therefore applicable because the SMP company must be able to conclusively assess the abusiveness of its behaviour.

In ex-ante regulation, however, the MS test is intended to take effect before any distortion of competition can occur.

Types of margin squeeze tests

• The BEREC Guidance document is analysing the economic

replicability test (ERT) included as an ex-ante (sector specific)

margin squeeze test to safeguard competition in the

“Recommendation on consistent non-discrimination obligations

and costing methodologies to promote competition and

enhance the broadband investment environment

2013/466/EU“ from a regulatory accounting perspective.

• It looks in particular at Recommend 56 + Annex II of the Rec.

• As the Recommendation it focuses on ex-ante margin squeeze

tests conducted in Market 4 and Market 5 of the

Recommendation on relevant markets susceptible to ex-ante

regulation 2007/879/EC (Market 3a and 3b of 2014/710/EU).

• ERT is a lighter test than the ex-ante MS tests used by NRAs,

it is without prejudice of an ex-post competition law MS test

Recommendation on non-discrimination

obligations and Costing methodologies

58

ECJ Rulings on Margin Squeeze

• ECJ ruling C-280/08 of 14 October 2010 confirmed the Commission‘s MS decision against DTAG applying a margin squeeze in fixed telephony markets, the ECJ confirmed the EEO test used by the Cion in its 2003 decision, the ECJ also confirmed that Art. 102 (ex Art. 82) is applicable in regulated sectors if the operator is dominant and has a room for action

• Along the same line the ECJ ruling C-52/09 of 17 February 2011 (TeliaSonera)

• Court of 1st Instance confirmed fine of Telefónica for the application of a MS in the Spanish broadband market in its rulings T-336/07 and T-398/07 (March 2012); confirmed finally by ECJ ruling C-295/12 P of 10 July 2014

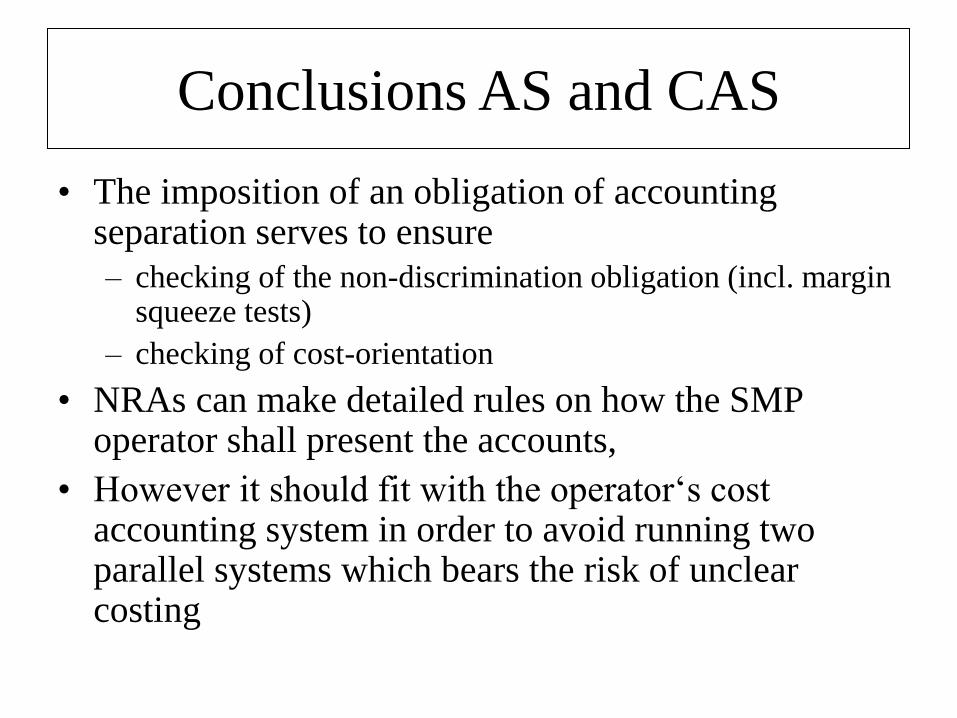

Conclusions AS and CAS

• The imposition of an obligation of accounting separation serves to ensure

– checking of the non-discrimination obligation (incl. margin squeeze tests)

– checking of cost-orientation

• NRAs can make detailed rules on how the SMP operator shall present the accounts,

• However it should fit with the operator‘s cost accounting system in order to avoid running two parallel systems which bears the risk of unclear costing

• 1. A national regulatory authority may, in accordance with

• the provisions of Article 8, impose obligations on operators to

• meet reasonable requests for access to, and use of, specific network elements and associated facilities, inter alia in

• situations where the national regulatory authority considers

• that denial of access or unreasonable terms and conditions having a similar effect would hinder the emergence of a sustainable competitive market at the retail level, or would not be in the end-user's interest.

• NRAs can impose an obligation to interconnect networks

• National regulatory authorities may attach to those obligations

• conditions covering fairness, reasonableness and timeliness.

Art. 12 Access obligation

The Regulatory Model • The ladder of investment or infrastructure construction is

a concept formulated among others by Martin Cave. It explains how infrastructure competition can develop on the basis of mandated access allowing new entrants to invest in a step by step manner in parallel to reaching a sufficiently big customer base to fill the newly built capacity and make a business case earning the financial means for investment

• Thus it functions as a bridge from (short term) service towards (long term) infrastructure competition

• The ladder concept is a useful model for regulators to achieve a consistent regulatory approach across a chain of access markets, often applied to e.g. broadband markets

• The concept of the ladder of investment provides – at least ex post – a good explanation for recent developments in European BB market competition

Ladder of investment in a traditional environment

Resale

Bitstream

Shared /

full

unbundling

Own

infrastructure

Subloop unbundling Market 4 –

physical access

(passive, ULL)

Market 5 –

broadband access

(active, bitstream)

Resale market

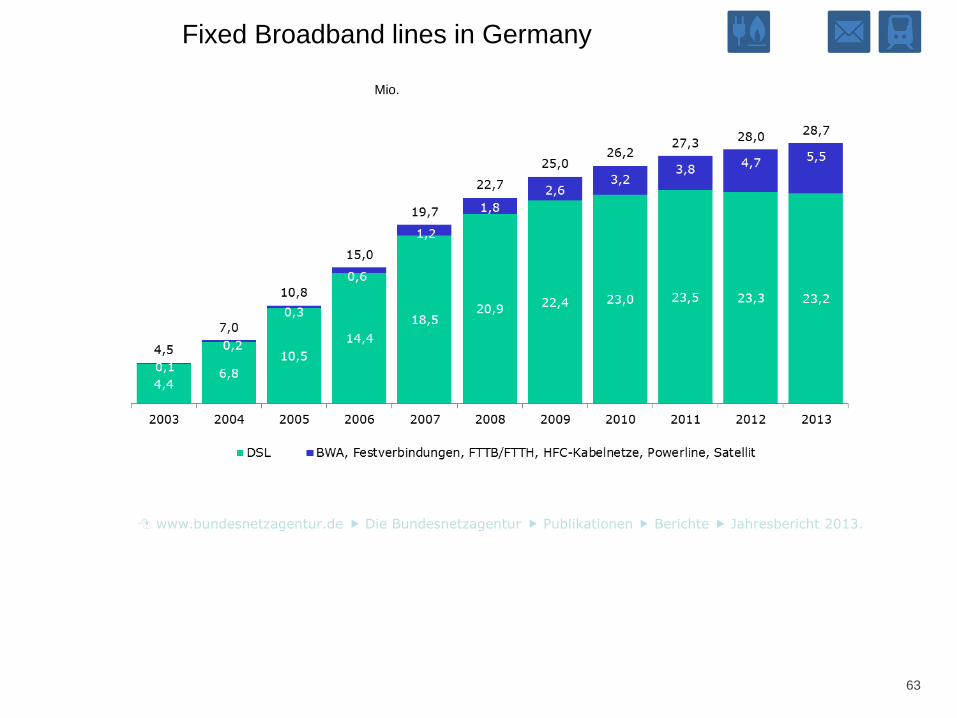

Fixed Broadband lines in Germany

Mio.

63

www.bundesnetzagentur.de Die Bundesnetzagentur Publikationen Berichte Jahresbericht 2013.

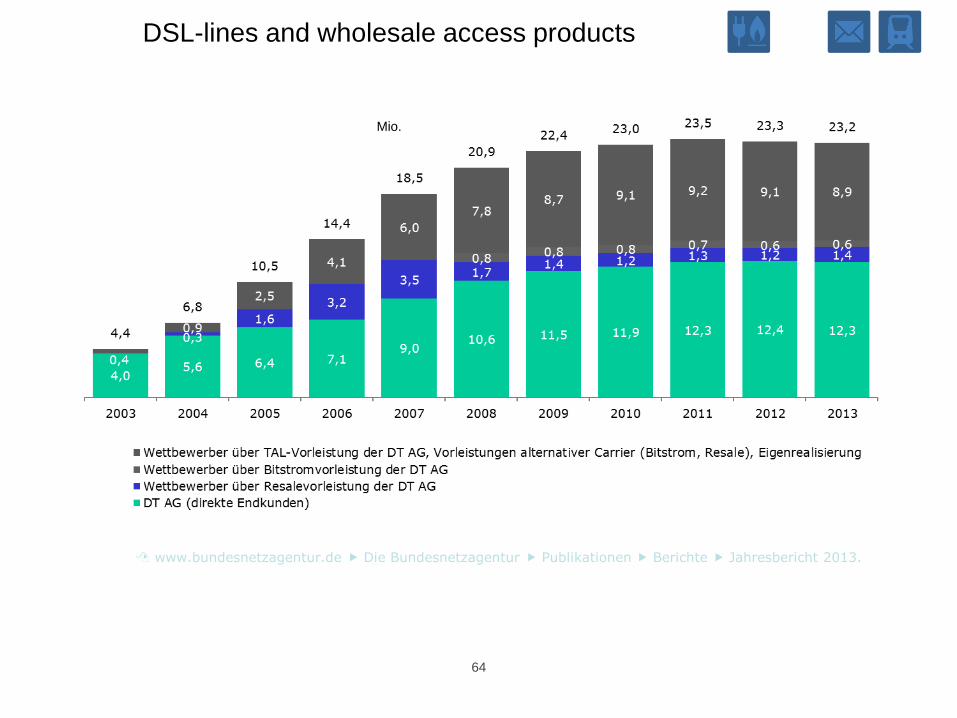

DSL-lines and wholesale access products

Mio.

64

www.bundesnetzagentur.de Die Bundesnetzagentur Publikationen Berichte Jahresbericht 2013.

Fixed broadband lines – market shares in per centage

65

www.bundesnetzagentur.de Die Bundesnetzagentur Publikationen Berichte Jahresbericht 2013.

66

Economics of NGA • Next generation access (NGA) networks are generally understood to be fibre

networks allowing higher bandwidth (i.e. more speed) and NGA economics describe the economic factors influencing the migration from copper to fibre access networks

• A mixture of technologies will be used for NGA deployment depending on a number of parameters and specific local characteristics, including – copper local loop and sub-loop lengths, quality of lines

– customer density and dispersion, presence of multi-dwelling units

– topology of the network, in particular the number of street cabinets per MDF, availability of ducts.

• Economics of NGA networks are likely to vary across different technologies and different geographies, i.e. between MS + within MS

• Increase in costs per line/user due to a lower number of end users per node.

• Civil engineering costs are the most significant cost factor (up to 80%), 2014 Directive on broadband cost reduction foresees measures to facilitate infrastructure sharing also with passive infrastructure of other sectors such as energy

• Viability of the business case also depends on the demand side and additional ARPU that can be attained by offering customers innovative services, but “willingness to pay” a premium price still lacking (overall the actual take-up rate is rather low).

• NGA investments are likely to reinforce the importance of scale and scope economies, thereby reducing the degree of replicability, potentially leading to an enduring economic bottleneck.

67

NGA Recommendation

• Commission‘s Digital Agenda for Europe (DAE) in 05/2010 • By the end of 2020 - nationwide broadband coverage of 30 Mbit/s

• Commission issued on 20 Sept. 2010 the Recommendation on regulated access to NGA (2010/572/EU)

• Confirming that unbundling obligation should apply to fibre loops as well in order to ensure competition

• That prices of unbundled fibre loops should also be regulated acc. to cost-orientation

• Margin squeeze to be avoided

• Risk premium to be taken into account to ensure a risk adequate rate of return in order to provide incentives to invest in NGA infrastructure and roll-out fibre networks so that the objectives of the European Digital Agenda to provide broadband access to all European citizens is realized

Ladder of Investment in a NGA environment In

cre

asin

gpro

port

ion

of

ow

nin

frastr

uctu

re

Incre

asin

gpro

port

ion

of

ow

nin

frastr

uctu

re

MDF/ODF

unbundling

Resale

Bitstream(Ethernet incl. ALA, IP, ATM)

- DSLAM- parent node- distant node

Cabinet

unbundling

ConcentrationPoint/Manhole

unbundling

Access to in-house wiringor equivalent

Access to the end user using own

infrastructure only

Access products

Leased Lines(incl. Ethernet)

Dark fibre

Duct access

Only owninfrastructure

+

Wholesale products to reachaccess point

MDF/ODF

unbundling

Resale

Bitstream(Ethernet incl. ALA, IP, ATM)

- DSLAM- parent node- distant node

Cabinet

unbundling

ConcentrationPoint/Manhole

unbundling

Access to in-house wiringor equivalent

Access to the end user using own

infrastructure only

Access products

Leased Lines(incl. Ethernet)

Dark fibre

Duct access

Only owninfrastructure

+

Wholesale products to reachaccess point

Art. 13 Price control obligation • To make the access obligation effective, generally a price-

control obligation is needed: cost-orientation + cost-accounting

obligations acc. to Art. 13 (sect. 30, 31 Tel. Act)

• The regulator is placing himself in the same situation as a new

operator having to make the investment decisions related to

market entry now:

• By setting prices equivalent to the costs of efficient service

provision the regulator anticipates future prices prevailing on a

fully competitive market reflecting the costs of efficient service

provision (defined as CCA/LRIC) thus simulating competition

and thereby stimulating the process

• Cost-orientation is especially important as it allows to steer the market forces in the right direction by ensuring the optimal allocation of resources at the same time (creating competitive pressure for econ. rational behaviour, no market distortion)

Why cost-orientation?

• The regulator is placing himself in the same situation as a

new operator having to make the investment decisions

related to market entry now:

• By setting prices equivalent to the costs of efficient service

provision the regulator anticipates future prices prevailing on

a fully competitive market reflecting the forward looking

investment costs which are the costs of efficient service

provision (defined as LRICs)

• LRIC = Long Run Incremental Costs including an appropriate

rate of return on capital employed plus an appropriate mark-

up for common costs (cost allocation method)

• CCA = Current Cost Accounting as the relevant cost of a

network operator rolling out an efficient network today (cost

base)

Regulatory Rationale (1) • Decision to enter the market depends on the forward looking

investment costs, which will be reflected in the price prevailing on a

fully competitive market

• The price prevailing on a fully competitive market reflects the costs

of efficient service provision as in the long run only efficient

operators will survive, competitive pressure will push others to exit

the market; in a competitive market only the costs efficiently

incurred can be recovered (principle of cost recovery), not the

actually incurred costs (may include inefficencies or wrongly

allocated common costs)

• Level + structure of access (incl. IC) charges must be in line with the

costs of efficient service provision, because a charging according to

the cost causation principle stimulates competition best and

simultanously minimises distortionary effects

Regulatory Rationale (2) • If prices are set on an economically sound basis

(i.e. cost-oriented) competition is stimulated while

resources are put to best use at the same time, i.e. used

efficiently

• Efficiency is the best possible relation between input and

output for a given technology (optimization under

constraints)

• The regulator simulates the market process and acts as a

temporary substitute till market forces take over

• The regulator is placing himself in the same situation as a

new operator having to make the investment decisions

related to market entry now: current costs (CCA) are to

be used (today‘s prices) as otherwise the make-or-buy

decision would be distorted

Regulatory Aim • Competition in the national fixed (core + access) network as

well as for mobile networks, which means evaluating the efficiency of the existing network by calculating the investment of an efficient network roll-out (opportunity costs): by anticipating the future price of a competitive market with the regulated price there is

no distortion of the make-or-buy- decision by wrong economic signals, which means:

• a clear signal to invest if the entrant is more efficient

• an incentive to produce efficiently to the incumbent, i.e. to use the existing capacity efficiently and to improve performance

• With a price based on LRIC, no under- or over-investment will be induced, but the right amount of investment as operators can decide on investments according to economic rationality

• Concept of LRIC and CCA ensures a balanced approach to promote infrastructure as well as service competition

Regulatory Aim and LRIC/CCA as Cost Concept

ne

w in

fra

str

uctu

re r

oll-

ou

t

utilisation of existing network

price line = efficient capacity use

• Cost-orientation applied to NGA/N: is it different?

• No, same logic applies as with legacy networks:

• To make the access obligation effective, generally a price-control

obligation is needed: cost-orientation + cost-accounting obligations acc. to

Art. 13 AD

• The regulator is placing himself in the same situation as a new operator having to make the investment decisions related to market entry now:

• By setting prices equivalent to the costs of efficient service provision the regulator anticipates future prices prevailing on a fully competitive market reflecting the costs of efficient service provision (defined as LRIC/CCA/MEA) thus simulating competition and thereby stimulating the process as well as promoting efficient investment in network infrastructure by providing the right (undistorted) make-or-buy-signal

• Cost-orientation is especially important as it allows to steer the market forces in the right direction by ensuring the optimal allocation of resources (including dynamic efficiency) at the same time

• WACC must be set to reflect the risk of the investment, however this does not automatically include an “extra” risk premium (only if the risk is higher)

• Principles of cost recovery and cost causality

Cost-orientation and incentives to invest in

NGA/N infrastructure

Why LRIC?

Long Run Incremental Costs • LRIC = Long Run Incremental Costs including an

appropriate rate of return on capital employed plus an

appropriate mark-up for common costs

• Decision to enter the market depends on the long run costs,

because an investment decision cannot be reversed in the

short term

• Incremental costs: to catch the characteristics of telecoms

production determining the cost structure, i.e. economies of

scale + scope, which is reflected by using the whole service to

be priced as an increment added to other services offered

• Forward looking, because the investment decision would have

to be made now, considering the prospects for future returns

(forecasting traffic volumes, market dynamics, planni. efficient

capacity to serve the forecasted traffic volumes/demand)

77

Cost-oriented rates regulation FL-LR(A)IC cost standard

• Forward looking long run average incremental cost (FL-LRAIC) – Forward looking requirement:

no consideration of historic costs, application of best technology

– Long run: all investments are variable (disposable), all services are ranked in equal order

– Average: costs are averaged over all services using a particular element, no discrimination of a particular service using the element

– Incremental: a whole service is the increment, i.e. not a unit (as is the case for marginal costs), but a new (additional) service, provided in addition to a portfolio of other services, here: the whole access-network can be considered the increment for the provision of the access-service. Whereas the total amount of access units can be derived from the number of subscribers.

– Interpretation of FL-LRAIC: FL-LRAIC are costs incurred by a hypothetical efficient competitor (new entrant) who offers the same service to the same extent as the SMP operator.

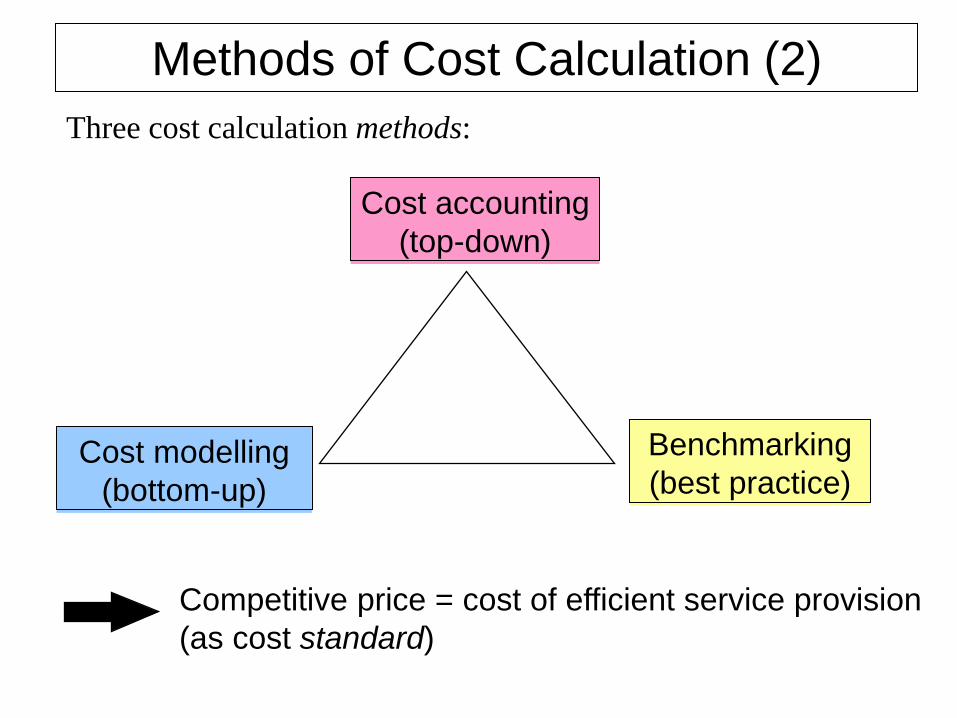

Methods of Cost Calculation (1)

• 3 methods of cost calculation:

• Cost accounting (checking of the submitted cost documentation, top-down approach), reducing costs to the efficient level by deducting inefficient costs + correcting wrongly allocated costs

• International benchmarking: prices of markets open to competition, using the best practice approach

• Analytical cost models constructing an efficient network with technology available today (bottom-up approach)

• Correctly applied all 3 methods should give the same result: a price that is equivalent to the cost of efficient service provision

• Prices prevailing in a competitive market are equal to the cost of efficient service provision (cost standard) as only efficient operators will stay in the market („survival of the fittest“)

Cost accounting

(top-down)

Cost modelling

(bottom-up)

Three cost calculation methods:

Benchmarking

(best practice)

Competitive price = cost of efficient service provision

(as cost standard)

Methods of Cost Calculation (2)

18 April 2013 80

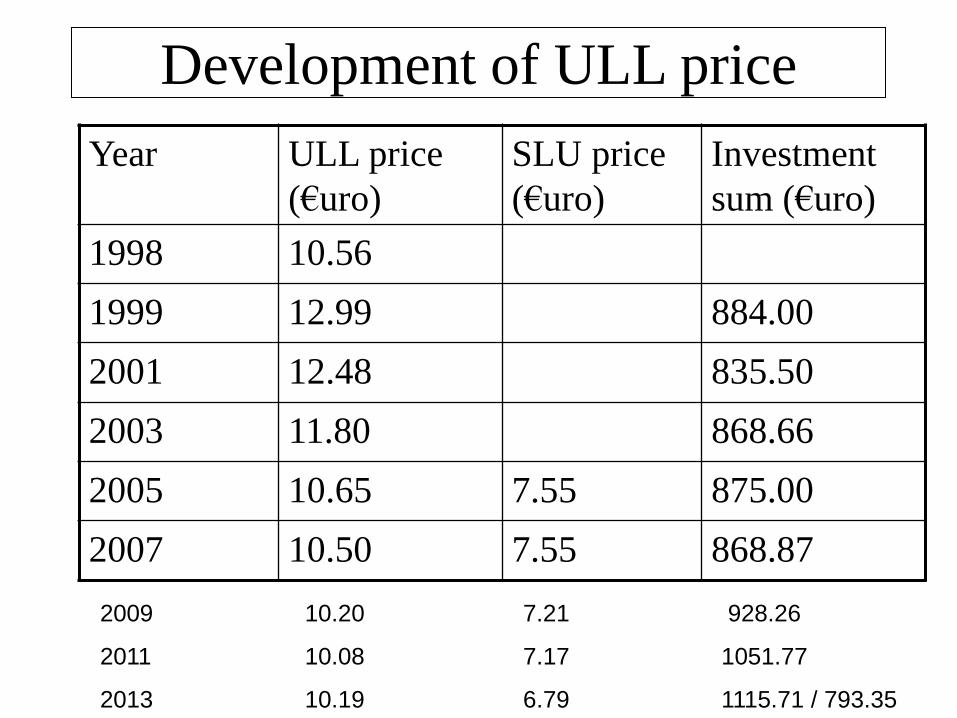

ULL Decision 2013 • 21 March 2011

– last Regulatory Order covering Market 4, inter alia mandating access to the ULL and SLU

– Copper lines regulated ex-ante

– Fibre lines are regulated ex post

– ULL decision in 2011 fixed the price at 10.08 €

– Draft ULL decision published for consultation on 10 April 2013

– ULL monthly rate slightly increased for copper access to 10.19 € and slightly decreased for SLU to 6.79 € (from 7.17 €)

– Prices entered into force on 1 July 2013 and be valid for 3 years

– Consultation period ended on 24 April 2013

– Art. 7a Notification to the Commission on 22 May 2013

– Comments received on 24 June 2013

– Final decision published on 26 June 2013 confirming the preliminary rates

ULL Decision of 2013 cont. – All assets valued at current replacement costs as the best make-or-buy-

signal for investment as in all previous decisions

– BU-LRIC+ analytical cost model of WIK used to calculate the efficient

costs of rebuilding a modern access network

– Depriciation period for the feeder cable (and buried cable) shortened

from 20 to 15 years and prolonged for the distribution cable incl. buried

cables from 20 to 25 years as technology is being moved down to the

street cabinet

– Civil engineering: 40 years (before 35 years)

– Rate of return: 6.77% (lower than in 2011: 7.11%)

– Investment per local loop: 1,115.71 € (2011: 1051.77)

– Investment per subloop: 793.35 €

– Further prices fixed for e.g. multifunctional cabinet and duct access

(0.09 € per meter per month)

– Investment signals encouraging competition at the street cabinet level

Year ULL price

(€uro)

SLU price

(€uro)

Investment

sum (€uro)

1998 10.56

1999 12.99 884.00

2001 12.48 835.50

2003 11.80 868.66

2005 10.65 7.55 875.00

2007 10.50 7.55 868.87

2009 10.20 7.21 928.26

2011 10.08 7.17 1051.77

2013 10.19 6.79 1115.71 / 793.35

Development of ULL price

Unbundled local loops (ULL)

83

EC / BEREC docs on RA The EC continuously adjusts the Directives and Recommendations to provide harmonised accounting systems and methodologies throughout the EU.

• EC Directive 2002/19/EC on access to, and interconnection of, electronic communications networks and associated facilities (in par. Art. 11 and Art. 13 Access Directive, AD)

• EC Directive 2002/22/EC on universal service and users' rights relating to electronic communications networks and services (in part. Art. 17 Universal Service Directive, USD)

• EC Rec. 2005/698/EC on Accounting separation and cost accounting systems (updates EC Rec. 98/322/EC following the application of the regulatory framework for electronic communications (25 July 2003);

• ERG (now BEREC) Common Position (CP) on EC Rec. on AS and CA;

• BEREC Reports “Regulatory Accounting in Practice 2010, 2011, 2012, 2013, 2014”

• EC Rec. 2009/396/EC on the Regulatory Treatment of Fixed and Mobile Termination Rates in the EU

• EC Rec. 2013/466/EU on consistent non-discrimination obligations and costing methodologies to promote competition and enhance the broadband investment environm.

• BEREC Guidance document on the regulatory accounting approach to the economic replicability test (i.e. ex-ante/sector specific margin squeeze tests), BoR(14)190

Conclusions (1) • The 2002 European Regulatory Framework on Electronic

Communications Networks and Services (ECNS) provides a stable and

predictable framework for the challenges of a converging and highly

dynamic environment

• Emerging competitive market structures require that sector specific

regulation is aligned with general competition law

• However, regulation is still needed, but needs to be justified in greater detail

and must be applied in a technological neutral way, which becomes more

important in a convergent environment

• While the initial phase of liberalization required strict automatic reactions, the

second phase of market development requires a more tailored approach

• Regulatory measures depend on the outcome of the market reviews and

must be proportionale and appropriate to remedy the competition problem

identified in national markets

• The 2009 framework builds on the 2002 using the same principles. It allows

a differentiated approach to address different market stages adaquately,

less intrusive intervention in more advanced markets

• ECNS framework is suitable/capable to deal also with NGN/NGA

• Promoting competition, because competition is the best driver for

investment, competitiveness and users‘ welfare

• Best incentive to invest is confidence of investors in a sound and predictable regulatory environment

• Announcing the regulatory strategy in advance to ensure stability and predictability of the regulatory environment

• Answer could be: WACC that properly reflects the riskyness of investing in new technologies and upgrading networks

• Both ways – providing a clear vision of the regulatory strategy as well

as a signal that risks will be rewarded appropriately – can incentivise

investments as it helps building the necessary confidence of

investors reducing the risk by providing planning certainty

• BEREC believes that the challenges from increasingly dynamic markets can be dealt adequately by continuing a pro-competitive regulation implemented by independent NRAs exercising their discretion in line with common best practice principles of BEREC

Conclusions (2)

• The discussion about the upcoming Review of the European Regulatory Framework should be structured as a rational dialogue about lessons learned, any proposed changes must be reasoned and evidence-based as well as based on a sound impact assessment

• It‘s too easy to expect ideal solutions just by switching more decision making power to Brussels, the benefits of the current institutional design with BEREC + the Art. 7/7a process have proven to work well

• Tendency towards convergent markets requires maintaining the principle of technological neutrality

• Overall, ECNS RF fundamentally sound and fit for purpose! The current approach of decentralized implementation combined with the Art. 7/a FD procedure and the role of BEREC to achieve a consistent application of the regulatory framework via common positions and best practice principles provide for the development of the internal market bottom up have proven to keep the balance between national flexibility and the European level

Conclusions (3)

• Regulatory coordination (including also an appropriate degree of harmonisation) is an invaluable asset for promoting the competitiveness of Europe in the global market

• Cooperation amongst independent NRAs is the best way to promote a consistent application of the framework to develop the internal market

• BEREC believes that the challenges from the need to invest in NGN/NGA infrastructure can be dealt with adequately with a pro-competitive regulation using the instruments of the framework thus ensuring a competitive NGN/NGA roll-out for the achievement of the European Digital Agenda targets

• Sector specific regulation remains necessary for network industries, but relationship with competition law is changing as sectors are changing and convergence is changing market boundaries

Conclusions (4)

• As in a market economy regulation always requires justification, the analysis of its impact gets more and more important to evaluate the effectiveness of regulatory interventions

• The more effective regulation is, the less is the regulatory burden for market players as well as possible adjustment costs as economic decisions of market players are less distorted

• Effective regulation requires a clear mandate (powers), independence and accountability, governance rules, transparency and credibility (commitment) as well as juridical control (on the merits of the case)

• We have seen that pro-competitive regulation is based on the same principles + requires an independent well-resourced professional regulator

• Ensure consistency of regulatory measures in a very dynamic environment of the telecoms sector with more differentiated and more competitive (retail) markets, also convergence between telecoms and media sector (e.g. net neutrality, offers of so-called Over-the-top players)

• Cross-sectoral as well as cross-border aspects gain increasingly importance requiring closer cooperation among sector-specific national regulators within a country and among NRAs across countries, i.e. within the EU as well as internationally

Conclusions (5)

• New regulatory bodies on the European level for the cooperation of

NRAs such as BEREC and ACER increased influence and standing of

NRAs both on the European as well as on the national level.

• Furthermore as all national regulation is embedded in the European

regulatory frameworks, it is important to also ensure consistent

application of the European regulatory framework on the national level;

this can be achieved via networks of regulators and/or regulatory bodies

where independent NRAs are members

• It is important to allow NRAs flexibility to take into account national

circumstances such as different roll-out strategies and national plans

regarding infrastructure modernization, but also different administrative

structures in Member States

• A common challenge in all network industries is the modernization of the

infrastructure, this is particularly important in telecoms (highspeed

broadband networks) and energy (to integrate renewables)

• Competitive markets and modernized networks increase the overall

competitiveness of Europe

Conclusions (6)

© Bundesnetzagentur 91

Thank you for your attention

© Bundesnetzagentur 92

A N N E X

Delegation of power to a

professional independent body

Control that powers are

not overstretched

Accountability

Judicial review Governance rules

Ensure that powers are used in line with the

law and regulation is implemented effectively

© Bundesnetzagentur 94

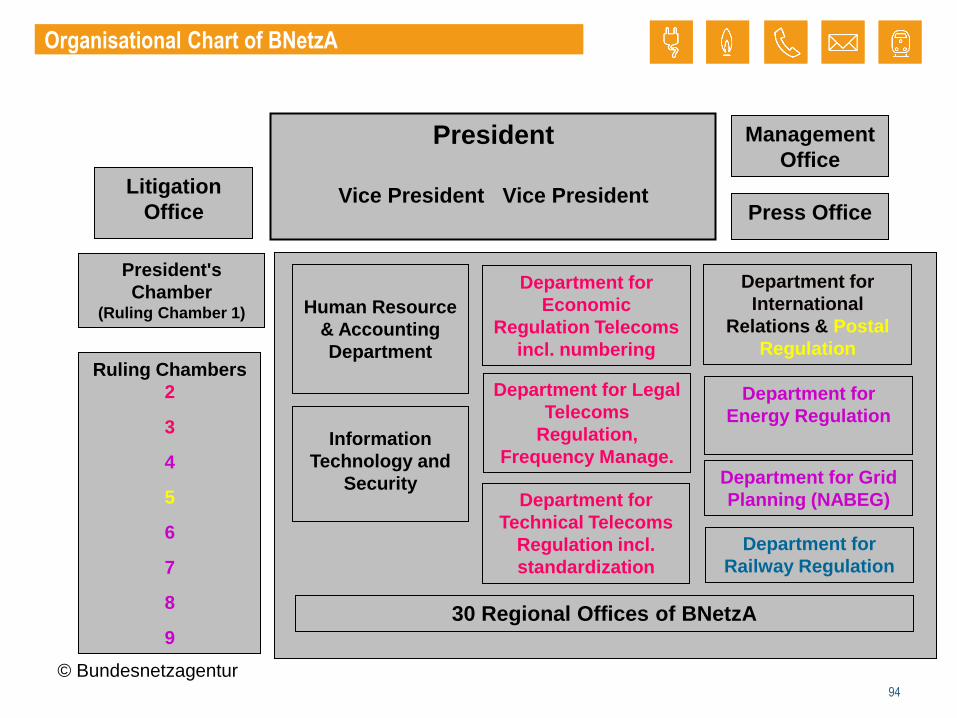

Organisational Chart of BNetzA

President

Vice President Vice President

Management

Office

President's

Chamber (Ruling Chamber 1)

Ruling Chambers

2

3

4

5

6

7

8

9

Information

Technology and

Security

Human Resource

& Accounting

Department

30 Regional Offices of BNetzA

Department for

International

Relations & Postal

Regulation

Department for

Energy Regulation

Department for

Railway Regulation

Department for

Economic

Regulation Telecoms

incl. numbering

Department for Legal

Telecoms

Regulation,

Frequency Manage.

Department for

Technical Telecoms

Regulation incl.

standardization

Department for Grid

Planning (NABEG)

Press Office

Litigation

Office

BEREC – BoR (28 NRA heads + observers)

Contact Network

Preparation of Plenary meetings, senior representatives of 28 NRAs with a mandate to speak for their NRA

Expert Working Groups – EWG 2013

NRA experts

Benchmarking (ES) BEREC-RSPG Cooperation (IT)

Next Generation Networks (DE)

Termination Rates (FR, IT)

Roaming (ES, DE) End-User (RO, PT)

Net Neutrality (NO, FR)

Regulatory Accounting (IT, DE)

BEREC Evaluation (NL)

Remedies (UK)

Framework Implementation (IT)

Convergence (ES, FR)

A – Boosting NGN B – Consumer empowerm. C – Boosti. t. internal market

D – Other activities

Market definition and SMP-finding – Art. 7 RRL

Remedies imposition

– Art. 7a RRL

Quelle: EU-KOM

Art. 7/7a Procedure

Cost structure and

potential to abuse market power

• Economies of scale & density

decreasing long run average costs

• Economies of scope

stand alone costs are higher than incremental costs

the cost structure gives an advantage to the incumbent and

offers him possibilities of strategic pricing, because his

relevant costs are lower than those of potential competitors:

– endogenous barrier to market entry

– unbundled access to the local loop is key to break up the

barrier to entry of the access level and to open the access

and broadband market

Consultation on costing methodologies

• On October 3rd 2011 the Commission launched a consultation on costing methodologies for key wholesale access prices in electronic communications

• The consultation looks at the best way to calculate the costs of access networks in

the light of the EDA targets and the roll-out of NGA (fibre) infrastructure

• 32 questions related to costing methodologies for ULL (M4), BSA (M5) and terminating segments of leased lines (M6)

• Focus on dealing with the migration from a copper access network to a fibre network, raises the question of whether a return to HCA rather than CCA could be an option to speed up roll-out of fibre

• Consultation deadline 28 November 2011

• BEREC had been granted an extension and submitted the final BEREC response after discussion at the Plenary in Bucharest on 8/9 December (published on the BEREC website on 12 Dec. 2011, BoR (11) 65)

• Commission assessed the comments received and published on 7 Dec. 2012 a draft

recommendation on non-discrimination and NGA costing methodologies

• BB policy statement of Com. Kroes on 12 July 2012: U-turn with regard to ULL

prices: replacement costs accepted as appropriate, no decrease planned anymore

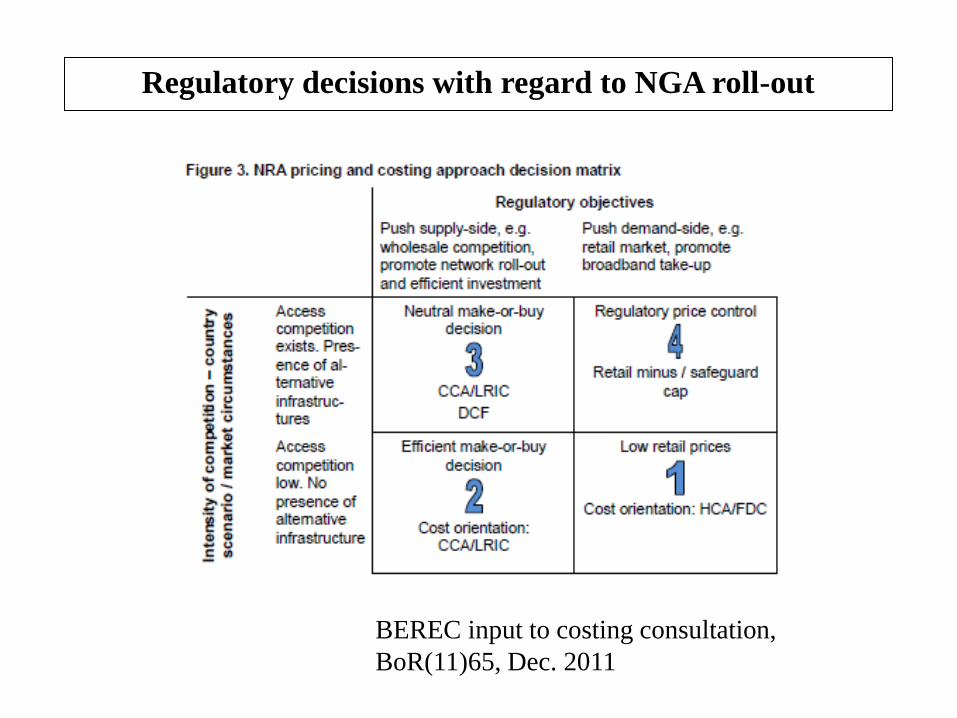

BEREC input to costing consultation,

BoR(11)65, Dec. 2011

Regulatory decisions with regard to NGA roll-out

Dynamic regulatory path

3 4

2 1

Regulatory objectives

Inte

nsi

ty o

f co

mp

etit

ion

mark

et c

ircu

mst

an

ces

Presence of access competition/ alternative infrastructure

Push demand-side, e.g. retail market, promote broadband take-up

Low access competition/ no alternative infrastructure

Push supply-side, i.e. wholesale market, promote network roll-out and eff. investment

Investments in Germany

Mrd. Euro

Nationale Daten | Gesamtmarkt

101

www.bundesnetzagentur.de Die Bundesnetzagentur Publikationen Berichte Jahresbericht 2013.

Investments in Germany 1998 - 2013

Nationale Daten | Gesamtmarkt 102

Since market opening in 1998 112.4 bn. Euro were invested; of which more than half (52 %) by competitors of Deutsche Telekom . www.bundesnetzagentur.de Die Bundesnetzagentur Publikationen Berichte Jahresbericht 2013.