pricing interest rate derivatives in the multi-curve ... · pricing interest rate derivatives in...

TRANSCRIPT

1/34

Pricing Interest Rate Derivatives in the Multi-Curve Framework

Pricing Interest Rate Derivativesin the Multi-Curve Framework

Stochastic Basis Spread

Zakaria El Menouni910504-8772

KTH - Royal Institute of TechnologySF299X - Degree Project in Mathematical Statistics

March 30th, 2015

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

2/34

Pricing Interest Rate Derivatives in the Multi-Curve Framework

Summary

1 IntroductionThe Interest Rate Market TransformationConsequences

2 The Multi-Curve FrameworkPricing Interest Rate Derivatives: What has changed?Pricing Plain Vanilla Instruments: Deposits and Swaps

3 Case of a Stochastic SpreadModeling the Basis SpreadCaplet PricingIntroducing Shifted Log-Normal and SABR DynamicsModel Calibration

4 Results

5 Discussion & Improvement Suggestions

6 Conclusion

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

3/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkIntroduction

Summary

1 IntroductionThe Interest Rate Market TransformationConsequences

2 The Multi-Curve Framework

3 Case of a Stochastic Spread

4 Results

5 Discussion & Improvement Suggestions

6 Conclusion

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

4/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkIntroduction

The Interest Rate Market Transformation

Reference: Bloomberg.Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

5/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkIntroduction

The Interest Rate Market Transformation

• Divergence between interest rates ⇒ Appearance of a spread.

• Explosion of the spread in 2008 (august) and in 2011.

• Libor not considered risk-free anymore.

• Risky transactions.

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

6/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkIntroduction

Consequences

• Interest rate divergence ⇒ Market subdivision.

• Expansion of collateralized transactions (Over Night rate as therisk-free rate).

• Replacement of the now risky Libor by the approximately risk-freeOver night rate.

• Invalidity of the single-curve framework.

• Use of the Multi-curve framework: One discounting curve anddifferent forward curves.

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

7/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkThe Multi-Curve Framework

Summary

1 Introduction

2 The Multi-Curve FrameworkPricing Interest Rate Derivatives: What has changed?Pricing Plain Vanilla Instruments: Deposits and Swaps

3 Case of a Stochastic Spread

4 Results

5 Discussion & Improvement Suggestions

6 Conclusion

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

8/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkThe Multi-Curve Framework

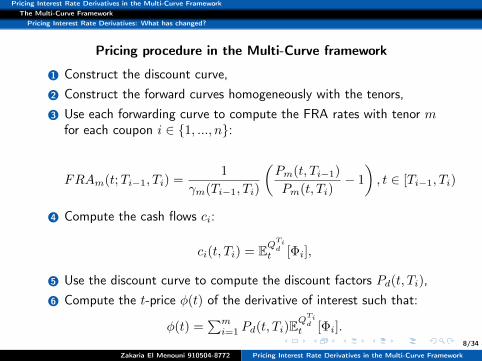

Pricing Interest Rate Derivatives: What has changed?

Pricing procedure in the Multi-Curve framework

1 Construct the discount curve,2 Construct the forward curves homogeneously with the tenors,3 Use each forwarding curve to compute the FRA rates with tenor m

for each coupon i ∈ 1, ..., n:

FRAm(t;Ti−1, Ti) =1

γm(Ti−1, Ti)

(Pm(t, Ti−1)

Pm(t, Ti)− 1

), t ∈ [Ti−1, Ti)

4 Compute the cash flows ci:

ci(t, Ti) = EQTid

t [Φi],

5 Use the discount curve to compute the discount factors Pd(t, Ti),6 Compute the t-price φ(t) of the derivative of interest such that:

φ(t) =∑mi=1 Pd(t, Ti)E

QTid

t [Φi].

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

9/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkThe Multi-Curve Framework

Pricing Plain Vanilla Instruments: Deposits and Swaps

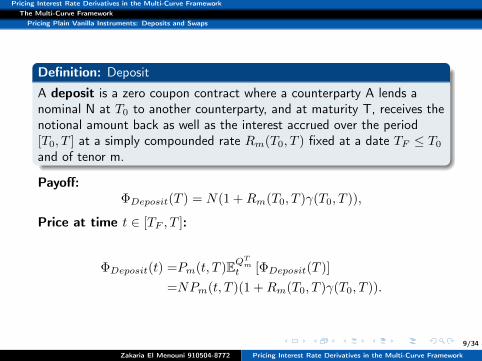

Definition: DepositA deposit is a zero coupon contract where a counterparty A lends anominal N at T0 to another counterparty, and at maturity T, receives thenotional amount back as well as the interest accrued over the period[T0, T ] at a simply compounded rate Rm(T0, T ) fixed at a date TF ≤ T0

and of tenor m.

Payoff:ΦDeposit(T ) = N(1 +Rm(T0, T )γ(T0, T )),

Price at time t ∈ [TF , T ]:

ΦDeposit(t) =Pm(t, T )EQTm

t [ΦDeposit(T )]

=NPm(t, T )(1 +Rm(T0, T )γ(T0, T )).

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

10/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkThe Multi-Curve Framework

Pricing Plain Vanilla Instruments: Deposits and Swaps

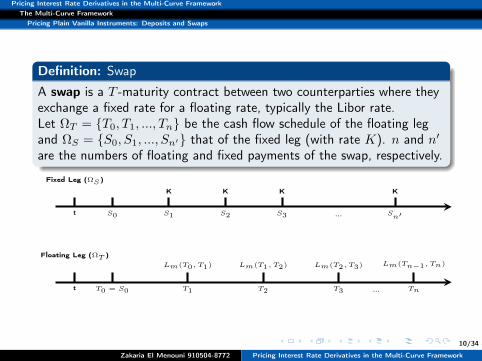

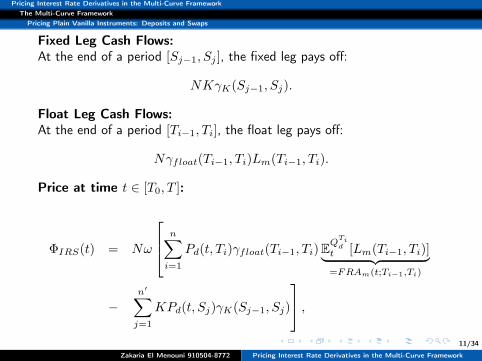

Definition: SwapA swap is a T -maturity contract between two counterparties where theyexchange a fixed rate for a floating rate, typically the Libor rate.Let ΩT = T0, T1, ..., Tn be the cash flow schedule of the floating legand ΩS = S0, S1, ..., Sn′ that of the fixed leg (with rate K). n and n′

are the numbers of floating and fixed payments of the swap, respectively.

Floating Leg (ΩT )

T0 = S0t T1 T2 T3 Tn...

Lm(T0, T1) Lm(T1, T2) Lm(T2, T3) Lm(Tn−1, Tn)

Fixed Leg (ΩS )

t S0 S1 S2 S3 Sn′...

K K K K

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

11/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkThe Multi-Curve Framework

Pricing Plain Vanilla Instruments: Deposits and Swaps

Fixed Leg Cash Flows:At the end of a period [Sj−1, Sj ], the fixed leg pays off:

NKγK(Sj−1, Sj).

Float Leg Cash Flows:At the end of a period [Ti−1, Ti], the float leg pays off:

Nγfloat(Ti−1, Ti)Lm(Ti−1, Ti).

Price at time t ∈ [T0, T ]:

ΦIRS(t) = Nω

n∑i=1

Pd(t, Ti)γfloat(Ti−1, Ti)EQTid

t [Lm(Ti−1, Ti)]︸ ︷︷ ︸=FRAm(t;Ti−1,Ti)

−n′∑j=1

KPd(t, Sj)γK(Sj−1, Sj)

,Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

12/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkThe Multi-Curve Framework

Pricing Plain Vanilla Instruments: Deposits and Swaps

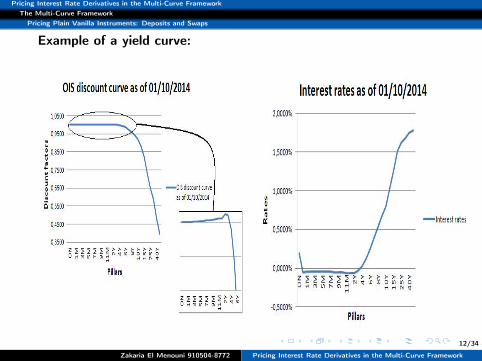

Example of a yield curve:

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

13/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkThe Multi-Curve Framework

Pricing Plain Vanilla Instruments: Deposits and Swaps

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

14/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkCase of a Stochastic Spread

Summary

1 Introduction

2 The Multi-Curve Framework

3 Case of a Stochastic SpreadModeling the Basis SpreadCaplet PricingIntroducing Shifted Log-Normal and SABR DynamicsModel Calibration

4 Results

5 Discussion & Improvement Suggestions

6 Conclusion

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

15/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkCase of a Stochastic Spread

Modeling the Basis Spread

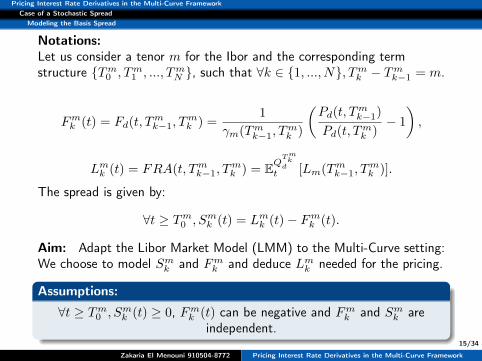

Notations:Let us consider a tenor m for the Ibor and the corresponding termstructure Tm0 , Tm1 , ..., TmN , such that ∀k ∈ 1, ..., N, Tmk − Tmk−1 = m.

Fmk (t) = Fd(t, Tmk−1, T

mk ) =

1

γm(Tmk−1, Tmk )

(Pd(t, T

mk−1)

Pd(t, Tmk )− 1

),

Lmk (t) = FRA(t, Tmk−1, Tmk ) = EQ

Tmkd

t [Lm(Tmk−1, Tmk )].

The spread is given by:

∀t ≥ Tm0 , Smk (t) = Lmk (t)− Fmk (t).

Aim: Adapt the Libor Market Model (LMM) to the Multi-Curve setting:We choose to model Smk and Fmk and deduce Lmk needed for the pricing.

Assumptions:

∀t ≥ Tm0 , Smk (t) ≥ 0, Fmk (t) can be negative and Fmk and Smk areindependent.

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

16/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkCase of a Stochastic Spread

Caplet Pricing

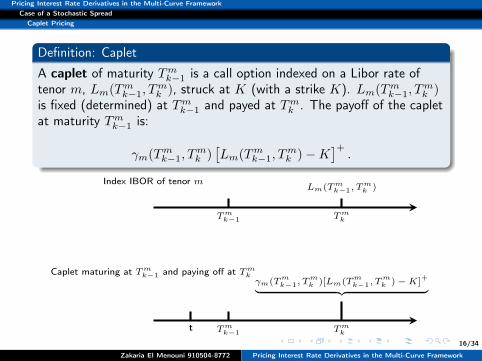

Definition: Caplet

A caplet of maturity Tmk−1 is a call option indexed on a Libor rate oftenor m, Lm(Tmk−1, T

mk ), struck at K (with a strike K). Lm(Tmk−1, T

mk )

is fixed (determined) at Tmk−1 and payed at Tmk . The payoff of the capletat maturity Tmk−1 is:

γm(Tmk−1, Tmk )[Lm(Tmk−1, T

mk )−K

]+.

Caplet maturing at Tmk−1 and paying off at Tmk

t Tmk−1 Tmk

γm(Tmk−1, T

mk )[Lm(T

mk−1, T

mk )−K]

+︸ ︷︷ ︸

Index IBOR of tenor m

Tmk−1 Tmk

Lm(Tmk−1, Tmk )

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

17/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkCase of a Stochastic Spread

Caplet Pricing

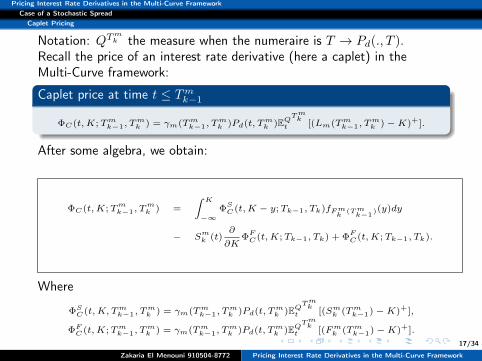

Notation: QTmk the measure when the numeraire is T → Pd(., T ).

Recall the price of an interest rate derivative (here a caplet) in theMulti-Curve framework:

Caplet price at time t ≤ Tmk−1

ΦC(t,K;Tmk−1, Tmk ) = γm(Tmk−1, T

mk )Pd(t, Tmk )EQ

Tmkt [(Lm(Tmk−1, T

mk )−K)+].

After some algebra, we obtain:

ΦC(t,K;Tmk−1, T

mk ) =

∫ K

−∞ΦSC(t,K − y;Tk−1, Tk)fFm

k(Tmk−1

)(y)dy

− Smk (t)

∂

∂KΦFC(t,K;Tk−1, Tk) + Φ

FC(t,K;Tk−1, Tk).

Where

ΦSC(t,K, Tmk−1, Tmk ) = γm(Tmk−1, T

mk )Pd(t, Tmk )EQ

Tmkt [(Smk (Tmk−1)−K)+],

ΦFC(t,K;Tmk−1, Tmk ) = γm(Tmk−1, T

mk )Pd(t, Tmk )EQ

Tmkt [(Fmk (Tmk−1)−K)+].

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

18/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkCase of a Stochastic Spread

Introducing Shifted Log-Normal and SABR Dynamics

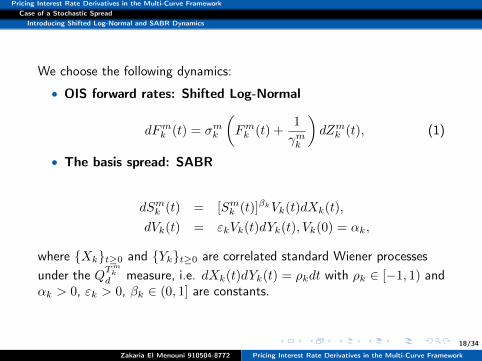

We choose the following dynamics:

• OIS forward rates: Shifted Log-Normal

dFmk (t) = σmk

(Fmk (t) +

1

γmk

)dZmk (t), (1)

• The basis spread: SABR

dSmk (t) = [Smk (t)]βkVk(t)dXk(t),

dVk(t) = εkVk(t)dYk(t), Vk(0) = αk,

where Xkt≥0 and Ykt≥0 are correlated standard Wiener processesunder the QT

mk

d measure, i.e. dXk(t)dYk(t) = ρkdt with ρk ∈ [−1, 1) andαk > 0, εk > 0, βk ∈ (0, 1] are constants.

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

19/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkCase of a Stochastic Spread

Introducing Shifted Log-Normal and SABR Dynamics

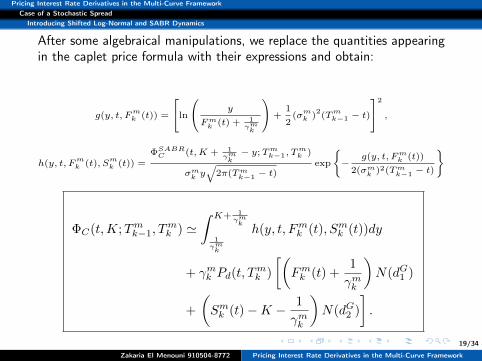

After some algebraical manipulations, we replace the quantities appearingin the caplet price formula with their expressions and obtain:

g(y, t, Fmk (t)) =

ln

y

Fmk (t) + 1γmk

+1

2(σmk )

2(Tmk−1 − t)

2

,

h(y, t, Fmk (t), S

mk (t)) =

ΦSABRC (t,K + 1γmk− y;Tmk−1, T

mk )

σmk y√

2π(Tmk−1 − t)exp

−

g(y, t, Fmk (t))

2(σmk )2(Tmk−1 − t)

ΦC(t,K;Tmk−1, Tmk ) '

∫ K+ 1γmk

1γmk

h(y, t, Fmk (t), Smk (t))dy

+ γmk Pd(t, Tmk )

[(Fmk (t) +

1

γmk

)N(dG1 )

+

(Smk (t)−K − 1

γmk

)N(dG2 )

].

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

20/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkCase of a Stochastic Spread

Introducing Shifted Log-Normal and SABR Dynamics

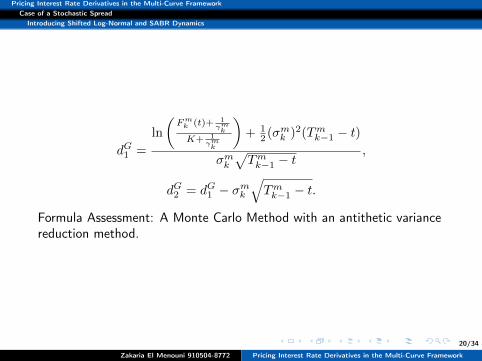

dG1 =

ln

(Fmk (t)+ 1

γmk

K+ 1γmk

)+ 1

2 (σmk )2(Tmk−1 − t)

σmk√Tmk−1 − t

,

dG2 = dG1 − σmk√Tmk−1 − t.

Formula Assessment: A Monte Carlo Method with an antithetic variancereduction method.

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

21/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkCase of a Stochastic Spread

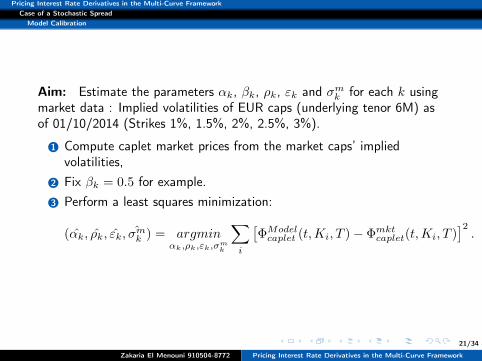

Model Calibration

Aim: Estimate the parameters αk, βk, ρk, εk and σmk for each k usingmarket data : Implied volatilities of EUR caps (underlying tenor 6M) asof 01/10/2014 (Strikes 1%, 1.5%, 2%, 2.5%, 3%).

1 Compute caplet market prices from the market caps’ impliedvolatilities,

2 Fix βk = 0.5 for example.3 Perform a least squares minimization:

(αk, ρk, εk, σmk ) = argminαk,ρk,εk,σmk

∑i

[ΦModelcaplet (t,Ki, T )− Φmktcaplet(t,Ki, T )

]2.

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

22/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkResults

Summary

1 Introduction

2 The Multi-Curve Framework

3 Case of a Stochastic Spread

4 Results

5 Discussion & Improvement Suggestions

6 Conclusion

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

23/34

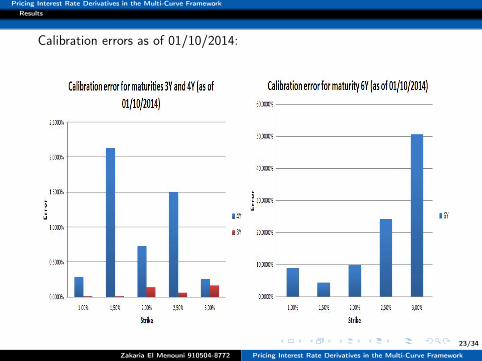

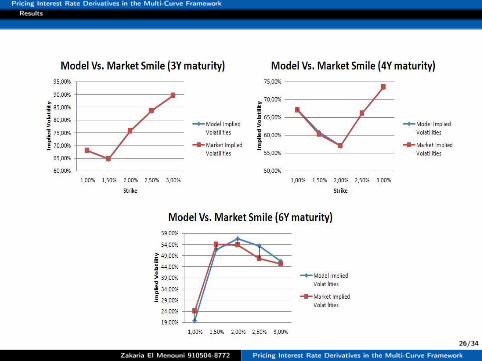

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkResults

Calibration errors as of 01/10/2014:

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

24/34

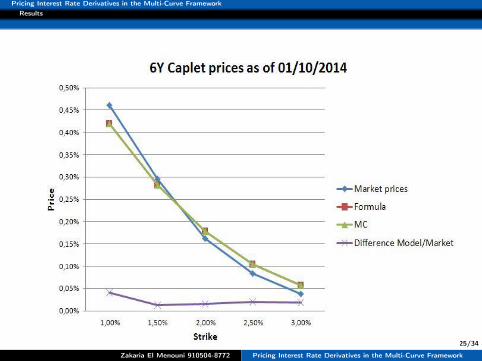

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkResults

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

25/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkResults

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

26/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkResults

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

27/34

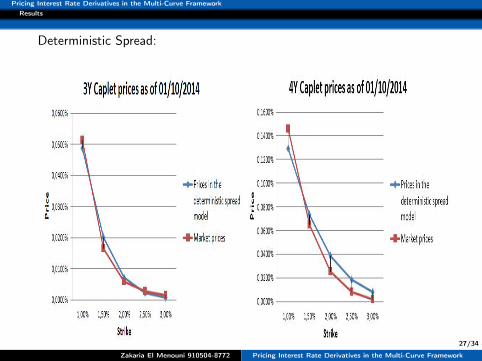

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkResults

Deterministic Spread:

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

28/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkResults

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

29/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkDiscussion & Improvement Suggestions

Summary

1 Introduction

2 The Multi-Curve Framework

3 Case of a Stochastic Spread

4 Results

5 Discussion & Improvement Suggestions

6 Conclusion

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

30/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkDiscussion & Improvement Suggestions

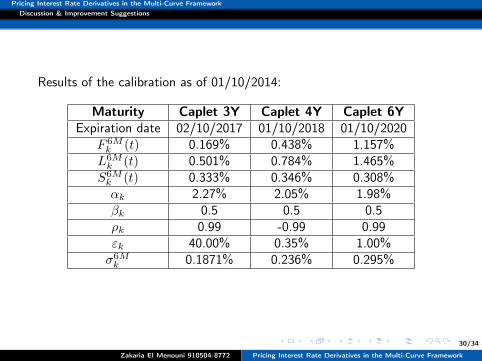

Results of the calibration as of 01/10/2014:

Maturity Caplet 3Y Caplet 4Y Caplet 6YExpiration date 02/10/2017 01/10/2018 01/10/2020

F 6Mk (t) 0.169% 0.438% 1.157%L6Mk (t) 0.501% 0.784% 1.465%

S6Mk (t) 0.333% 0.346% 0.308%αk 2.27% 2.05% 1.98%βk 0.5 0.5 0.5ρk 0.99 -0.99 0.99εk 40.00% 0.35% 1.00%σ6Mk 0.1871% 0.236% 0.295%

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

31/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkDiscussion & Improvement Suggestions

Remarks:

• Week sensitivity to the correlation ρk ⇒ Set ρk = 0,• The correlation between Forward OIS rates and the stochasticvolatility is set to zero ⇒ same volatility dynamics under differentmeasures,

• The rates are low so the calibration becomes hard because of datalacking for low strikes.

Improvement suggestions:

• Perform a weighted calibration (emphasis on the region where theFRA rate falls),

• Calibrate using other data sets (choose another reference date).

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

32/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkConclusion

Summary

1 Introduction

2 The Multi-Curve Framework

3 Case of a Stochastic Spread

4 Results

5 Discussion & Improvement Suggestions

6 Conclusion

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

33/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkConclusion

Advantages :• Tractability,• Possibility of closed formula derivation and thus easyimplementation and calibration,

• The model could be calibrated better in an unstressed market (nonnegative rates and/or higher rates) (F.Mercurio’s example).

Limitations:• In our example (i.e. low rates), the model only works for low andaverage maturitities,

• All market data (for all quoted strikes) cannot be fitted using thismodel because of the level of rates.

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework

34/34

Pricing Interest Rate Derivatives in the Multi-Curve FrameworkConclusion

Zakaria El Menouni 910504-8772 Pricing Interest Rate Derivatives in the Multi-Curve Framework