presentation to standard & poors - guam power...

TRANSCRIPT

1

Presentation to Standard & Poors

Guam Power AuthorityJune 6, 2007

2

AgendaBoard GovernanceManagement UpdateFinancial ConditionOperations UpdateCapital Improvement ProjectsOutlookConclusion

3

Board Governance

4

Consolidated Commission on Utilities

From Left to Right:

Eloy P. Hara, Treasurer and CCU Chairman for the Committee on Customer Relations

Tom C. Ada, Resigned

Gloria B. Nelson, Secretary and Chairwoman for the CCU Committee for Employee Development and Relations

Simon A. Sanchez, II, Chairman

Benigno M. Palomo, Vice Chairman – Guam Power Authority and CCU Chairman for the Committee on Social Welfare

5

Governance Goals

Prudent Fuel Use Reduction of Unaccounted for EnergyCompensation StudyRight-SourcingRight-SizingRight-HiringQuality Processes

6

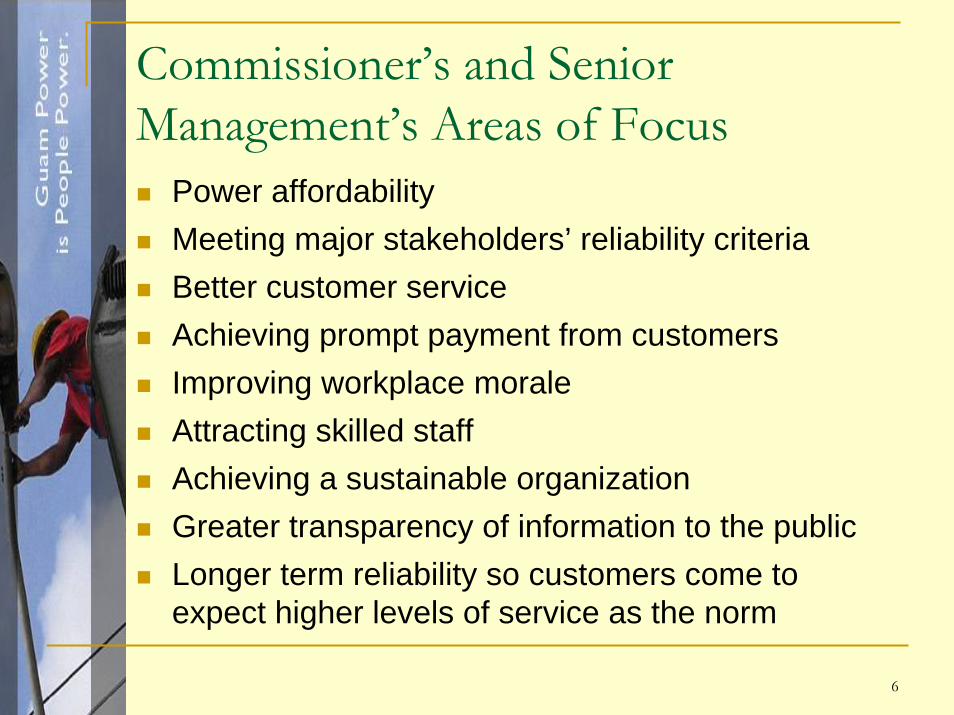

Commissioner’s and Senior Management’s Areas of Focus

Power affordabilityMeeting major stakeholders’ reliability criteriaBetter customer serviceAchieving prompt payment from customersImproving workplace moraleAttracting skilled staffAchieving a sustainable organizationGreater transparency of information to the publicLonger term reliability so customers come to expect higher levels of service as the norm

7

Management

8

Professional Executive Management

9

Management Priorities

Institutionalized planning processes;Sound financial and operating policies;A deep and experienced executive team;A solid grasp of industry issues that extends beyond the local utility;Extensive knowledge of customers and their needs;A proactive and farsighted management approach that has the support of an informed board.

10

Financial Condition

11

GPA Revenue BaseGPA Customer Accounts Number by Class

As of Fiscal Year 2006

Residential, 37,709

Department of Defense, 1

Others, 1,087

Large Commercial ,

223

Small Commercial ,

5,709

12

GPA Revenue BaseGPA Revenues ($000) by Customer Class

As of Fiscal Year 2006

Large Commercial, 79,365 , 27%

Small Commercial, 74,489 , 26%

Residential, 79,563 , 28%

Department of Defense, 50,422 , 17%

Others, 4,986 , 2%

13

Flat Base Rate Revenues

26,061 21,040 21,820 23,782 24,548 24,669

18,08816,454 17,942 16,840 17,172 18,197

33,09731,508

34,302 35,063 33,235 35,096

54,077

49,473

55,979 56,965 56,44857,435

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

2002 2003 2004 2005 2006 2007Fiscal Year

Base

Rat

e R

even

ues

($00

0)

Govt Navy Res CommAM

OU

NT $

14

O&M Expenses

$ (000)

24,599 24,906 26,690 28,427 28,198 31,926

26,752 23,934 28,775 27,098 27,918 26,900

74,820 79,14088,045

111,178

162,721175,752

$0

$50,000

$100,000

$150,000

$200,000

$250,000

2002 2003 2004 2005 2006 2007Fiscal Year

Ope

ratio

ns &

Mai

nten

ance

Spe

ndin

g ($

000) LABOR NON-LABOR FUEL

Revised Budget

15

Debt Service Coverage FY07 FY08

Debt Service Coverage CalculationEarnings From Operations 37,544,539 25,956,601 Add: Depreciation 26,036,273 26,463,307 Balance Available for Debt Service 63,580,812 52,419,908 Debt ServiceBond Interest Expense 20,711,453 20,400,763 Bond Principal 6,770,000 7,080,000 Total Debt Service 27,481,453 27,480,763

Debt Service Coverage (According to Bond Covenant) 2.31 1.91 Debt Service Coverage w/o IPP Acctg change 1.82 1.07

16

Debt service coverage ratio(S&P and Bond Covenant Methods)

1.271.42

1.08

1.431.27

2.27

2.11

2.26

2.11

1.92

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

FY2002 FY2003 FY2004 FY2005 FY2006

Fiscal Year

Deb

t-Ser

vice

Rat

io

S&P Method Bond Covenant Method

Bond Target - 1.3

PUC Target - 1.75

17

Accounts Payable Aging

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

FY 2002 FY 2003 FY 2004 FY 2005 FY 2006

0-30 Days 31-60 Days 61-90 Days 91-120 Days Over 120 Days

$11.2m

$17.3m

$14.7m

$10.8m

$27.0m

18

Accounts Receivable Aging

-2,000,0004,000,0006,000,0008,000,000

10,000,00012,000,00014,000,00016,000,000

FY 2001 FY 2002 FY 2003 FY 2004 FY 2005 FY 2006

0-30 Days 31-60 Days 61-90 Days 91-120 Days Over 120 Days

$8.0m$9.0m $10.2m

$10.7m$13.9m $14.0m

19

Government ReceivablesGovGuam Receivable Buildup

$-

$10,000,000

$20,000,000

$30,000,000

$40,000,000

$50,000,000

$60,000,000

Sep-96

Sep-97

Sep-98

Sep-99

Sep-00

Sep-01

Sep-02

Jan-03

20

Government ReceivablesGov't Rec'bles Trending Downward

-5,000,000

10,000,00015,000,00020,000,00025,000,00030,000,00035,000,00040,000,00045,000,00050,000,000

2003 2004 2005 2006 2007

GWAGPSSGMHDPW

21

Other Financial RatiosFINANCIAL RATIOS Targets 2002 2003 2004 2005 2006

Current Ratios > 2.6 2.9 2.37 2.55 2.61 2.1

Internal Funds to Debt Service > 2.25 1.24 0.82 1.11 1.27 1.18

Debt to Equity < 1.6 2.3 2.46 2.58 2.54 2.53

Gross Margin > 18.00% 19.69% 15.65% 15.46% 15.99% 12.91%

Operating Margin > 10.00% -1.74% -12.41% -4.20% -0.32% -1.30%

Return on Assets > 4.3% / 2.5% 0.44% -2.99% -1.18% -0.10% -0.49%

Operating Return on Net Fixed Assets > 8.00% 11.19% 9.63% 10.78% 11.79% 11.30%

Return on Net Fixed Assets > 6.50% 0.63% -4.26% -1.66% -0.15% -0.69%

Internal Funds to Capital Expenditure > 1.7 3.1 -0.01 2.72 1.21 0.99

Depreciation Expense to Gross Fixed Assets > 2.90% 3.24% 3.14% 3.16% 3.15% 3.00%

Percent Depreciated Plants < 32.50% 25.64% 28.11% 30.68% 32.53% 34.00%

Inventory Turnover > 10 4.21 3.61 4.72 4.5 4.99

Tier > 2.2 0.83 0.43 0.78 0.98 0.91

22

FINANCIAL RATIOS Targets 2002 2003 2004 2005 2006

Equity Capitalization > 50.00% 30.31% 28.86% 0.28% 28.25% 28.29%

Debt to Net Fixed Assets < 60.00% 68.33% 69.61% 70.12% 69.73% 68.96%

Internal Funds to Interest > 3.00% 1.92% 1.00% 1.37% 1.60% 1.51%

LTD Capitalization < 50.00% 69.69% 71.14% 72.09% 71.75% 71.71%

Fixed Asset Turnover > 55.00% 36.00% 34.00% 41.00% 45.00% 53.00%

Gross Margin Excluding Depreciation > 27.50% 31.14% 28.02% 26.18% 26.02% 21.15%

Operating Margin Excluding Interest & Depreciation > 30.00% 29.71% 21.18% 24.47% 25.71% 20.22%

Return on Equity > 8.00% -2.11% -15.10% -6.10% -0.53% -2.55%

Depreciation Expense to Total Assets > 3.00% 2.91% 2.98% 3.15% 3.27% 3.11%

Depreciation Expense to Capital Expenditures > 0.85 3.66 4.08 4.36 1.25 1.18

Internal Funds to Debt Service (With Interest Income) > 1.3 2.38 1.99 2.18 2.36 2.27

Debt Service Ratio (Excluding Interest Income) > 1.3 2.19 1.89 2.08 2.23 2.11

Other Financial Ratios (continued)

23

Working Capital Fund ($000)$17,984

$11,669

$2,291

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

Oct-05

Nov-05

Dec-05

Jan-06

Feb-06

Mar-06

Apr-06

May-06

Jun-06

Jul-06

Aug-06

Sep-06

Oct-06

Nov-06

Dec-06

Jan-07

Feb-07

Mar-07

Apr-07

Month-Year

Wor

king

Cap

ital F

und

Bal

ance

($00

0)

24

GPA’s Proposed Petition

19.72% base rate revenue increase (average impact of 6.22% for residential power bill based on 1000 kwh consumption)Base rate increase of $26.9 millionDouble the insurance surcharge and increase the cap to $25 millionImplement a $5 per transaction credit card surcharge for residential customers

25

Operations

26

Energy Production from Baseloads

27

SafetyAPPA / NSC

Incident Rates

4.42

3.41

1.5

2.19

3.173.733.67

00.5

11.5

22.5

3

3.54

4.55

2000 2001 2002 2003 2004 2005 2006

APPA Incident Rates

28

Demand Forecast

250

275

300

325

350

375

400

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Fiscal Year

MW

2007 - 275 MW

2016 - 348 MW

2011 - 331 MW

2008 - 298 MW

29

Demand Forecast (continued)

250

300

350

400

450

500

550

600

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

MW

Actual High Tourism/High InfrastructureHigh Tourism /Low Infrastructure Low Tourism/High InfrastructureBaseline

Installed Capacity by

1 Day in 4.5 Year Reserve

H/H Grow th Rate: 2.28% (2006-2016)3.13% (2006-2012)5.65% (2010-2011)

Tw o Largest Units Capacity Resrve Curve

30

Capital Improvement Projects

31

Northern Underground Projects Linking The Macheche CT And Tanguisson Power Plants

32

Capital Improvement Projects5-Year Plan

SUMMARY BY PROJECT TYPE

Generation Projects $13 million

FEMA UG Projects $27 million

Studies/Other Improvements $403 million

Grand Total $477 million

Substation Projects $11 million

Transmission & Distribution Projects $23 million

• Projects will straddle multiple fiscal years • Projects will commence within the next 5 years but may extend beyond

this time frame• Projects are reviewed each fiscal year and priorities are adjusted as

necessary

33

GENERATIONCapital Improvement Projects

FY ’08 – FY ’12 (x $1,000)Fire Protection - Insurance Mitigation 4,198Cabras 1 & 2 Projects 3,875Cabras 3 & 4 Projects 2,550

Agana Power Plant Asbestos Removal/New WSD Facility 200TOTAL ESTIMATE 12,823

USN 8" Above Ground Pipeline Upgrade 600Underground Fuel Pipeline 1,400

34

FEMACapital Improvement Projects

FEMA Funding: $17,000,000

GPA Cost: $ 10,000,000

FEMA PROJECTSHarmon to Tumon 34. 5 kV Underground Conversion

Tamuning Tumon 34.5 Underground Conversion

San Vitores to Macheche 34.5 kV Underground Conversion

Harmon to Tanguisson 34.5 kV Underground Conversion

Macheche to GAA 34.5 kV Underground Conversion

Agana to Tamuning and P202 Underground Conversion

P401 Underground Conversion to Memorial Hospital - Completed

P003 Underground Conversion to Cabras-Completed

Umatac Substation Drainage Modification -Completed

35

SUBSTATIONSCapital Improvement Projects

FY ’08 – FY ’12 (x $1,000)System Stability/Relay Coordination 1,190

Pulantat Substation Grounding Transformer 200

Hagatna 34.5 kV Protection Refurbishment and Upgrade 1,124

Hagatna 115 kV Protection Refurbishment and Upgrade 710Hagatna 115 kV and 34.5 kV Breaker Replacement 872

Andersen Substation Control System Reconstruction 1,340

Hagatna-Tamuning Protection System Upgrade 629

Orote Substation Control System Reconstruction 1,410

Piti-Anigua-Hagatna Protection System Upgrade 750

Tumon Substation Fence 280

Harmon Substation Switchyard Reconstruction 1,000Talofofo Substation 30 MVA Upgrade 933Tamuning-Tumon Protection System Upgrade 359

TOTAL ESTIMATE 10,797

36

TRANSMISSION & DISTRIBUTIONCapital Improvement Projects

FY ’08 – FY ’12 (x $1,000)

34.5 kV Transmission Line Along Rt. 2A 860

Marbo to Pagat 34.5 KV Line 3,534

Harmon to GIAT 34.5 kV Line Reconductoring 403

Harmon to Yigo 34.5 KV Line Reconductoring 1,840Agana to Radio Barrigada Reconductoring 700

San Vitores to Agana 34.5 KV Line 841Substation and Distribution Capacitor Program 450

Village Distribution Upgrades 6,125

Distribution System Improvements 300P-27 U/G Reconstruction 540P-330 Hardening and Reconductoring 160

Tumon Bay Lateral Conversion 925P003 Underground Extension to Port Authority 2,894U/G Reconstruction - Sinajana, Latte Heights, Yona 3,775

TOTAL ESTIMATE 23,347

37

STUDIES/OTHER IMPROVEMENTSSTUDIES/OTHER IMPROVEMENTS

FY ’08 – FY ’12 (x $1,000)Long Range Transmission Planning (Study) 135Integrated Resource Plan (Study) 450Guam Sea Water Air Conditioning (GSWAC) –

(Design & Construction) 100,000T&D Asset Assessment & Mapping 100System Stability/Relay Coordination 1200Distribution System Medium Range Planning &

Performance Analysis 600Load Research and Cost of Service Studies 55060MW Baseload Design & Construction (Pending

Completion of IRP and Military Buildup Input) 300,000TOTAL ESTIMATE 403,035

38

Outlook

39

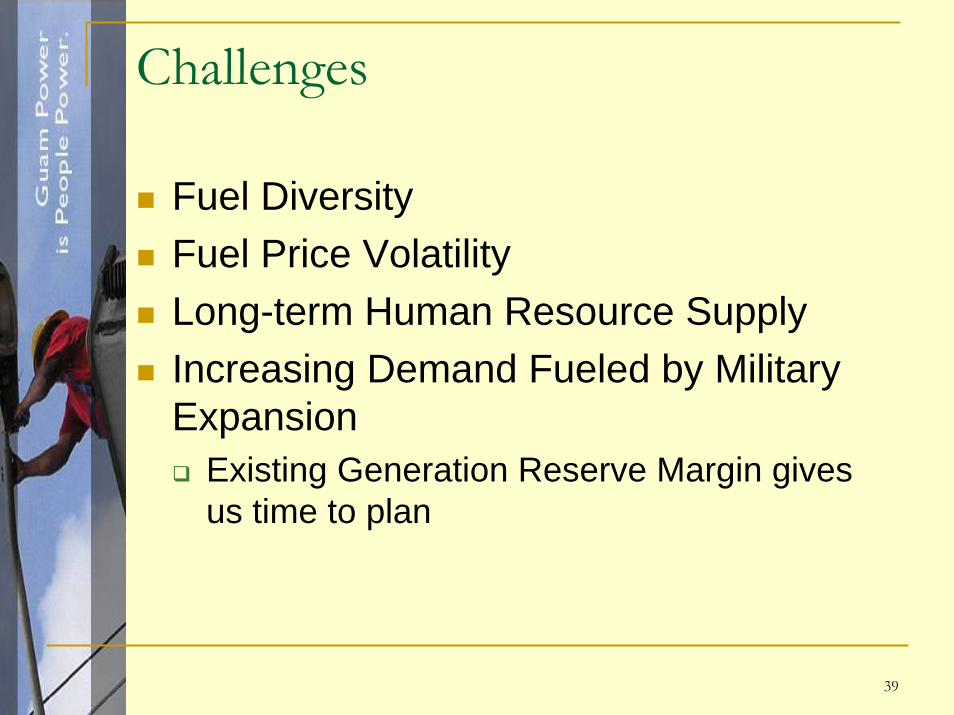

Challenges

Fuel DiversityFuel Price VolatilityLong-term Human Resource SupplyIncreasing Demand Fueled by Military Expansion

Existing Generation Reserve Margin gives us time to plan

40

Opportunities

GPA anticipates increased revenues with the Military buildupGrowth in Japan and Korea tourism markets will improve Guam economy and increase or maintain demand for electricityIncreased revenues will allow GPA to focus on system reliability, power quality, fuel diversity, new generation, and possible rate reduction

41

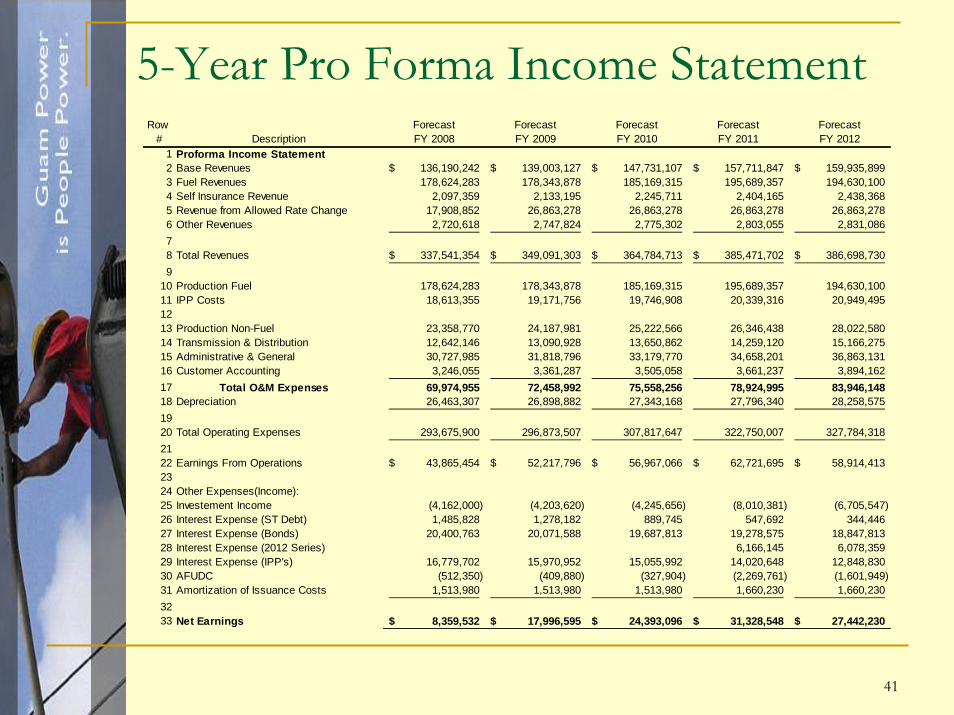

5-Year Pro Forma Income StatementRow Forecast Forecast Forecast Forecast Forecast

# Description FY 2008 FY 2009 FY 2010 FY 2011 FY 20121 Proforma Income Statement 2 Base Revenues 136,190,242$ 139,003,127$ 147,731,107$ 157,711,847$ 159,935,899$ 3 Fuel Revenues 178,624,283 178,343,878 185,169,315 195,689,357 194,630,100 4 Self Insurance Revenue 2,097,359 2,133,195 2,245,711 2,404,165 2,438,368 5 Revenue from Allowed Rate Change 17,908,852 26,863,278 26,863,278 26,863,278 26,863,278 6 Other Revenues 2,720,618 2,747,824 2,775,302 2,803,055 2,831,086 78 Total Revenues 337,541,354$ 349,091,303$ 364,784,713$ 385,471,702$ 386,698,730$ 9

10 Production Fuel 178,624,283 178,343,878 185,169,315 195,689,357 194,630,100 11 IPP Costs 18,613,355 19,171,756 19,746,908 20,339,316 20,949,495 1213 Production Non-Fuel 23,358,770 24,187,981 25,222,566 26,346,438 28,022,580 14 Transmission & Distribution 12,642,146 13,090,928 13,650,862 14,259,120 15,166,275 15 Administrative & General 30,727,985 31,818,796 33,179,770 34,658,201 36,863,131 16 Customer Accounting 3,246,055 3,361,287 3,505,058 3,661,237 3,894,162 17 Total O&M Expenses 69,974,955 72,458,992 75,558,256 78,924,995 83,946,148 18 Depreciation 26,463,307 26,898,882 27,343,168 27,796,340 28,258,575 1920 Total Operating Expenses 293,675,900 296,873,507 307,817,647 322,750,007 327,784,318 2122 Earnings From Operations 43,865,454$ 52,217,796$ 56,967,066$ 62,721,695$ 58,914,413$ 2324 Other Expenses(Income):25 Investement Income (4,162,000) (4,203,620) (4,245,656) (8,010,381) (6,705,547) 26 Interest Expense (ST Debt) 1,485,828 1,278,182 889,745 547,692 344,446 27 Interest Expense (Bonds) 20,400,763 20,071,588 19,687,813 19,278,575 18,847,813 28 Interest Expense (2012 Series) 6,166,145 6,078,359 29 Interest Expense (IPP's) 16,779,702 15,970,952 15,055,992 14,020,648 12,848,830 30 AFUDC (512,350) (409,880) (327,904) (2,269,761) (1,601,949) 31 Amortization of Issuance Costs 1,513,980 1,513,980 1,513,980 1,660,230 1,660,230 3233 Net Earnings 8,359,532$ 17,996,595$ 24,393,096$ 31,328,548$ 27,442,230$

42

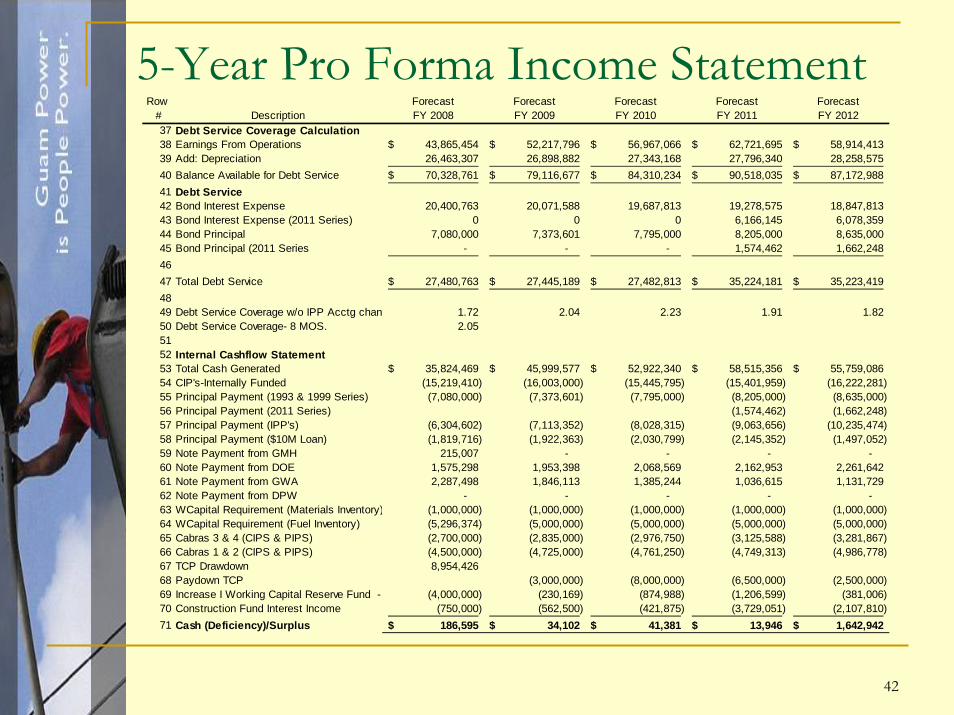

5-Year Pro Forma Income StatementRow Forecast Forecast Forecast Forecast Forecast

# Description FY 2008 FY 2009 FY 2010 FY 2011 FY 201237 Debt Service Coverage Calculation38 Earnings From Operations 43,865,454$ 52,217,796$ 56,967,066$ 62,721,695$ 58,914,413$ 39 Add: Depreciation 26,463,307 26,898,882 27,343,168 27,796,340 28,258,575 40 Balance Available for Debt Service 70,328,761$ 79,116,677$ 84,310,234$ 90,518,035$ 87,172,988$ 41 Debt Service42 Bond Interest Expense 20,400,763 20,071,588 19,687,813 19,278,575 18,847,81343 Bond Interest Expense (2011 Series) 0 0 0 6,166,145 6,078,35944 Bond Principal 7,080,000 7,373,601 7,795,000 8,205,000 8,635,000 45 Bond Principal (2011 Series - - - 1,574,462 1,662,248 4647 Total Debt Service 27,480,763$ 27,445,189$ 27,482,813$ 35,224,181$ 35,223,419$ 4849 Debt Service Coverage w/o IPP Acctg chan 1.72 2.04 2.23 1.91 1.82 50 Debt Service Coverage- 8 MOS. 2.05 5152 Internal Cashflow Statement53 Total Cash Generated 35,824,469$ 45,999,577$ 52,922,340$ 58,515,356$ 55,759,086$ 54 CIP's-Internally Funded (15,219,410) (16,003,000) (15,445,795) (15,401,959) (16,222,281) 55 Principal Payment (1993 & 1999 Series) (7,080,000) (7,373,601) (7,795,000) (8,205,000) (8,635,000) 56 Principal Payment (2011 Series) (1,574,462) (1,662,248) 57 Principal Payment (IPP's) (6,304,602) (7,113,352) (8,028,315) (9,063,656) (10,235,474) 58 Principal Payment ($10M Loan) (1,819,716) (1,922,363) (2,030,799) (2,145,352) (1,497,052) 59 Note Payment from GMH 215,007 - - - - 60 Note Payment from DOE 1,575,298 1,953,398 2,068,569 2,162,953 2,261,642 61 Note Payment from GWA 2,287,498 1,846,113 1,385,244 1,036,615 1,131,729 62 Note Payment from DPW - - - - - 63 WCapital Requirement (Materials Inventory) (1,000,000) (1,000,000) (1,000,000) (1,000,000) (1,000,000) 64 WCapital Requirement (Fuel Inventory) (5,296,374) (5,000,000) (5,000,000) (5,000,000) (5,000,000) 65 Cabras 3 & 4 (CIPS & PIPS) (2,700,000) (2,835,000) (2,976,750) (3,125,588) (3,281,867) 66 Cabras 1 & 2 (CIPS & PIPS) (4,500,000) (4,725,000) (4,761,250) (4,749,313) (4,986,778) 67 TCP Drawdown 8,954,426 68 Paydown TCP (3,000,000) (8,000,000) (6,500,000) (2,500,000) 69 Increase I Working Capital Reserve Fund - (4,000,000) (230,169) (874,988) (1,206,599) (381,006) 70 Construction Fund Interest Income (750,000) (562,500) (421,875) (3,729,051) (2,107,810) 71 Cash (Deficiency)/Surplus 186,595$ 34,102$ 41,381$ 13,946$ 1,642,942$

43

Conclusion

GPA believes that there will be accelerated economic and business growth in the near term by 2014 resulting in a significant potential increase in revenues.