preparing the sbc for open enrollment

TRANSCRIPT

©2012 Warner Norcross & Judd LLP. All rights reserved.

Preparing the SBC for Open Enrollment

2

©2012 Warner Norcross & Judd LLP. All rights reserved.

Overview

� Why is the SBC Required

� What’s Required to be on the SBC

� How Many SBCs do you have to Distribute

� Who has to Receive an SBC

� Who is Responsible for Compliance

� What Happens if You Don’t Comply

3

©2012 Warner Norcross & Judd LLP. All rights reserved.

Why Have an SBC?

� Rationale:� Goal of Health Care Reform Give individuals more choice

regarding health coverage

� Uniform, Basic Information about plan coverage

� Comparison Make it easier for individuals to compare coverage options

4

©2012 Warner Norcross & Judd LLP. All rights reserved.

When Must Group Health Plans Start Distributing the SBC?

� For existing employees:� Open enrollment periods

� starting on or after September 23, 2012

� For newly eligible employees:� First day of plan year

� that begins on or after September 23, 2012

5

©2012 Warner Norcross & Judd LLP. All rights reserved.

Benefits Subject to SBC Requirement

� Applies to health plan coverage� Medical� Prescription drug� Integrated dental/vision benefits

� Health Reimbursement Arrangements:� Stand-alone HRA must have its own SBC� Integrated HRA can be reported as part of health plan’s SBC

� Health Savings Accounts:� No duty to have an SBC for HSAs� Can choose to report employer contributions to HSA on the

SBC

6

©2012 Warner Norcross & Judd LLP. All rights reserved.

Benefits Subject to SBC Requirement

� Exceptions:� Stand-alone dental and

vision plans� Stand-alone long-term

care benefits� Non-coordinated benefits:

� Specified disease or illness (e.g. cancer-only coverage)

� Hospital indemnity or other fixed indemnity coverage

� Accident coverage� Disability coverage � Liability/auto insurance

(including auto medical coverage)

� Workers compensation� Credit-only insurance� Coverage for on-site

medical clinics

7

©2012 Warner Norcross & Judd LLP. All rights reserved.

Benefits Subject to SBC Requirement

� Health FSAs that are excepted benefits are exempt.

� When is a health FSA not an excepted benefit?� Offered to class of employees who do not qualify for other health

coverage

� Employer contributes too much money to the health FSA

� How much is too much?

� If Health FSA is not exempt, then must have SBC.� If integrated with medical plan option, can be described in medical

plan SBC

� If stand-alone FSA, then must have its own SBC

8

©2012 Warner Norcross & Judd LLP. All rights reserved.

Form of the SBC

� Appearance must be in a uniform format:� Not more than 4 double-sided pages� At least 12 point font size� Understandable terminology� “Culturally and linguistically appropriate”

� Support and Translation services if at least 10% or more of population in the county is literate only in Chinese, Spanish, Tagalog or Navajo

� Can be at the front of the SPD� SBC Samples:

� http://www.dol.gov/ebsa/SBCtemplate.doc� http://www.dol.gov/ebsa/SBCSampleCompleted.doc

9

©2012 Warner Norcross & Judd LLP. All rights reserved.

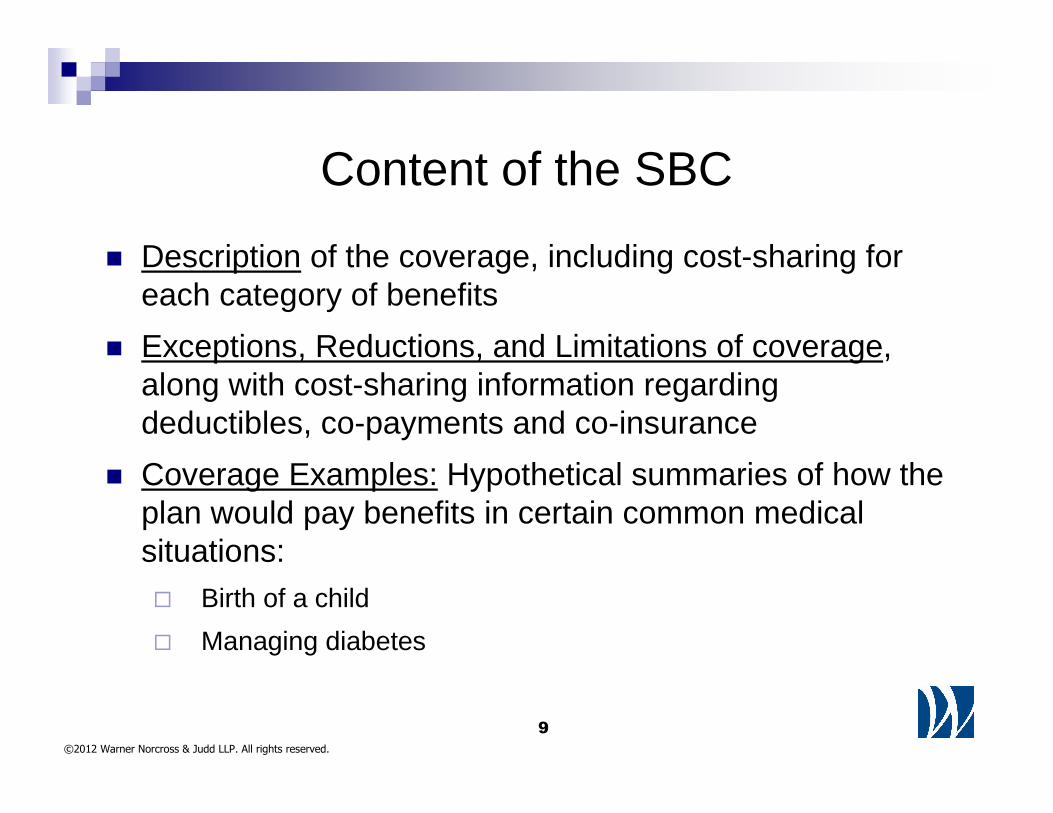

Content of the SBC

� Description of the coverage, including cost-sharing for each category of benefits

� Exceptions, Reductions, and Limitations of coverage, along with cost-sharing information regarding deductibles, co-payments and co-insurance

� Coverage Examples: Hypothetical summaries of how the plan would pay benefits in certain common medical situations: � Birth of a child

� Managing diabetes

10

©2012 Warner Norcross & Judd LLP. All rights reserved.

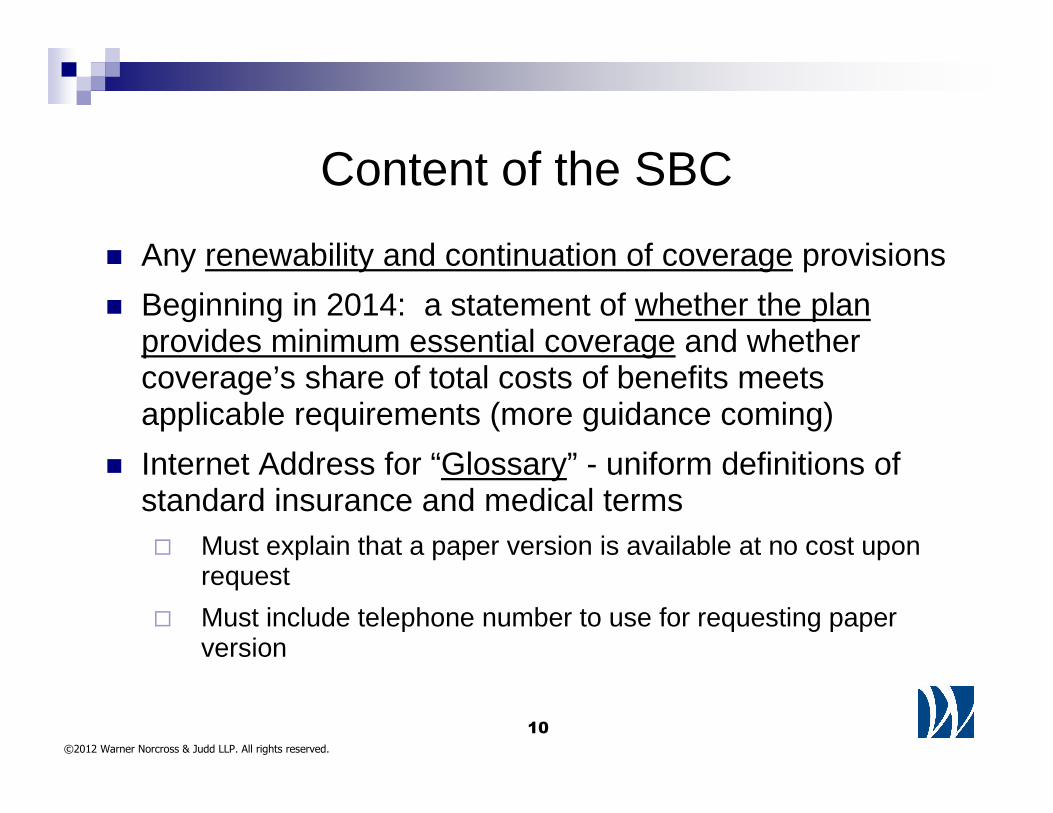

Content of the SBC

� Any renewability and continuation of coverage provisions

� Beginning in 2014: a statement of whether the plan provides minimum essential coverage and whether coverage’s share of total costs of benefits meets applicable requirements (more guidance coming)

� Internet Address for “Glossary” - uniform definitions of standard insurance and medical terms� Must explain that a paper version is available at no cost upon

request

� Must include telephone number to use for requesting paper version

11

©2012 Warner Norcross & Judd LLP. All rights reserved.

Content of the SBC

� Internet Address for formulary

� Internet Address for any provider network

� Disclaimer Statement: SBC is only a summary and the plan document, policy or certificate of insurance should be consulted to determine governing provisions

� Contact number to call with questions

� Internet address where copy of group certificate of coverage can be viewed and obtained

� For coverage provided to expatriates outside U.S., internet address for coverage details

12

©2012 Warner Norcross & Judd LLP. All rights reserved.

Who Must Receive the SBC?

� Participants and beneficiaries� One SBC per address� Separate SBC for each available plan option

� Two HMOs, Two PPOs? Four SBCs!� Differences between different tiers of coverage (e.g.,

single and family coverage) can be explained in one SBC

13

©2012 Warner Norcross & Judd LLP. All rights reserved.

Distributing the SBC

� Open Enrollment: open enrollment periods beginning on or after September 23, 2012.� Unenrolled employees: SBC for each available coverage option

� Current enrollees: SBC for their current coverage

� Deadlines:� With paper enrollment/application materials� If no paper materials distributed, then by the first day may enroll

� If have automatic renewal of coverage, then at least 30 days prior to start of new plan year (but if insurance contract still under negotiation, within 7 business days that new coverage issues)

� Upon request, as soon as practicable—no more than 7 business days

� If information changes before start of plan year—must distribute updated SBC by first day of plan year

14

©2012 Warner Norcross & Judd LLP. All rights reserved.

Distributing the SBC

� Newly eligible employees and special enrollees: starting on the first day of the new plan year beginning on or after September 23, 2012.

� Deadlines:� For newly eligible: with written enrollment materials/first date

may enroll� For special enrollees: within same time frame as SPD (within

90 days of enrollment)� Upon request: as soon as practicable, but no later than 7

business days following receipt of request

15

©2012 Warner Norcross & Judd LLP. All rights reserved.

Distributing the SBC� General Rule: method reasonably calculated to ensure receipt� Electronic Distribution Rules

� Those already participating:

� Same DOL rules as apply to an SPD

� Can use ERISA electronic distribution safe harbor rules described on next slide for � Workforce members with ready access to computers� Others who consent

� Those not yet covered under the plan:

� Format must be readily accessible� Paper copy provided free of charge

� If distribution is by Internet (or Intranet) posting, must advise individuals:� Document is available� Internet address where it can be accessed� That paper copy is available upon request free of charge

16

©2012 Warner Norcross & Judd LLP. All rights reserved.

DOL Electronic Safe Harbor Distribution

� Participants With Electronic Media Access at Work: The employer must take the following steps: � Notify each individual at the time a document is disclosed electronically in a way

that communicates the significance of the document� Furnish a paper version of the document upon request � Take steps to ensure actual receipt of the documents� Protect the confidentiality of any personal information that may be communicated

in the document being disclosed � Additional steps necessary if Participants do not have electronic media access at

work: � Notify Participant of ability to withhold or revoke consent � Obtain consent� Have Participant consent in a manner that demonstrates ability to utilize

technology � Communicate changes in hardware or software

17

©2012 Warner Norcross & Judd LLP. All rights reserved.

Who Must Prepare the SBC?

� Insurers must provide SBC to health plans� Within 7 business days of health plan’s application for

coverage� If information changes before 1st day of coverage, then must

provide updated SBC by the 1st day of coverage

� Upon health plans application to renew coverage� With application materials

� If automatic renewal, at least 30 days before start of new plan/policy year (but if contract still being negotiated, within 7 business days that new coverage issues)

� Within 7 business days of receiving request from group health plan

18

©2012 Warner Norcross & Judd LLP. All rights reserved.

Who Must Prepare the SBC?

� Self-insured health plans

� Plan sponsor is primarily responsible, but

� Can delegate out responsibility by contract

� Address contractually

� Drafting responsibility

� Distribution responsibility

19

©2012 Warner Norcross & Judd LLP. All rights reserved.

Who Must Prepare the SBC?

� Coordination issues: benefits under same coverage option administered by different insurers/TPAs� Example: insured medical, self-insured pharmacy benefits,

and self-insured HRA

� Plan sponsor may have to consolidate information into one SBC

20

©2012 Warner Norcross & Judd LLP. All rights reserved.

Modifications to the SBC

� Must provide a Notice of Modifications whenever:� Material modification to information reported on the SBC� Not already reflected on the most recent SBC� Occurs other than in connection with renewal or

reissuance of coverage

� Timing: no later than 60 days PRIOR to date on which change becomes effective

� Note: change in regulatory requirements as to content of SBC does not trigger duty to notify (unless otherwise specified)

21

©2012 Warner Norcross & Judd LLP. All rights reserved.

State Law Preemption

� State laws that require an SBC with less information are preempted

� State laws that require a more detailed SBC are not preempted—but must require additional information be provided in a separate document

22

©2012 Warner Norcross & Judd LLP. All rights reserved.

Penalties

� Willful failure to provide SBC: statutory penalty of $1,000 for each violation

� Each individual who fails to receive an SBC is a separate violation

� Potentially larger penalty: Tax code excise tax also applies to non-governmental plans

� $100 per individual for each day the plan fails to comply (with self-reporting obligation)

23

©2012 Warner Norcross & Judd LLP. All rights reserved.

Questions?Norbert Kugele(616) [email protected]

April Goff(616) [email protected]