practical issues in australia a credit union perspective

DESCRIPTION

TRANSCRIPT

Practical Issues in AustraliaPractical Issues in Australia

A Credit Union PerspectiveA Credit Union Perspective

Australian-Italian Co-operative Symposium15-17 February 2010 - Sydney University Village

The Co-operative Finance Sector

Presentation OverviewPresentation Overview

An Australian Perspective:

• History of credit unions

• Legislative structure prior to July 1992

• The Financial Institutions Scheme

• The Wallis Report

• Regulators - APRA & ASIC

• The experience

Credit Unions Meet a NeedCredit Unions Meet a NeedAt first, the philosophy of equality, equity & self-help was confined mainly to the area of retail trade. In the late 1840s it broke new ground in Germany, where Frederick Whilhelm Raiffeissen, the mayor of a small village, embraced the democratic principles of cooperation to form a mutual cooperative through which local farmers could pool their savings & lend to one another at reasonable rates of interest.

Under the guidance of mayor Raiffeissen and judge Schulze-Delitzsch, "credit unions" gained popularity and by the turn of the century had been adopted by urban & rural communities across Europe

Credit Union OriginsCredit Union Origins

The cooperative principles at the core of credit union operation can be traced to the 1800s, to the early stages of Europe’s Industrial revolution.

For many people of this era, cooperation represented an opportunity to escape exploitation and to regain dignity and self-respect through collective action and mutual self-help.

History of Credit UnionsHistory of Credit Unions• Franz Hermann Schulze-Delitzsch established

the first credit unions in the 1850s in Germany to give those lacking access to financial services the opportunity to borrow from the savings pooled by themselves and their fellow members

• Friedrich Wilhelm Raiffeissen transported the financial cooperative concept to rural Germany a decade later

• Experience in Munich & Bavaria in 1994 & ‘98

History of Credit UnionsHistory of Credit Unions

• Early in the 20th century, credit union idea expanded to North America

• 1947 Universal Credit Union founded by Kevin Yates in Sydney (Post exposure to credit unions in North America while training as a pilot during 2nd World War)

• Industrial & Parish credit unions developed & supported by Credit Union Leagues in 1960s

• Birth of Hastings Rural Credit Union in 1967

Credit UnionsCredit UnionsCredit unions worldwide offer members much more than financial services.

They provide members the opportunity to own their own financial institution, help them create opportunities such as starting small businesses, building family homes & educating their children.

In some countries, members encounter their first taste of democratic decision making through their credit unions eg Poland

Legislative Structure Pre 1992Legislative Structure Pre 1992• Disparate Laws of the States & Territories

regulated credit unions – the encouragement of thrift & the wise use of credit

• Interstate Trading inhibited - State borders with differing legislation

• Differences in standards of operation & supervision between States

• A lack of uniformity in structure & performance, between States impact on brand

The Birth of the Financial The Birth of the Financial Institutions SchemeInstitutions Scheme

• Crisis of Confidence - Collapse Pyramid Building Society in Victoria 1990

• Commonwealth Government unwilling to take responsibility for non-banks

• States agreed to Uniform State based legislation in Canberra 31 May 1991

• Uniformity & Stability through cooperation between the States & Territories

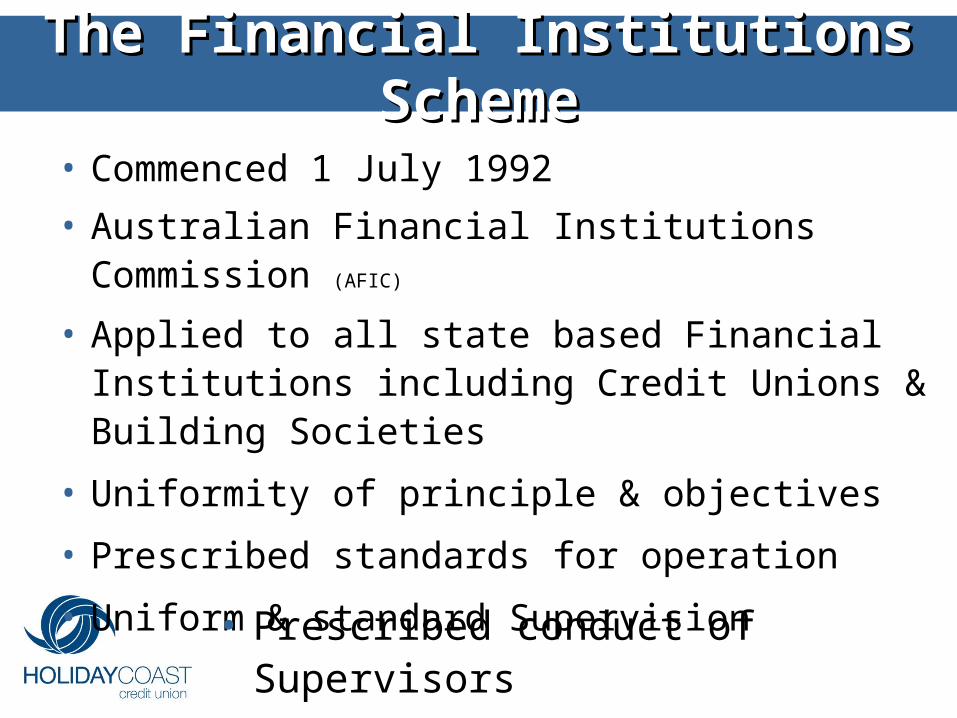

The Financial Institutions SchemeThe Financial Institutions Scheme

• Commenced 1 July 1992

• Australian Financial Institutions Commission (AFIC)

• Applied to all state based Financial Institutions including Credit Unions & Building Societies

• Uniformity of principle & objectives

• Prescribed standards for operation

• Uniform & standard Supervision

• Prescribed conduct of Supervisors

Objects of FI SchemeObjects of FI Scheme

• The principal objects of the financial institutions scheme were —

• (a) to protect and promote the financial integrity and the efficiency of the State-based financial institutions system; and

• (b) to protect the interests of depositors

The Financial Institutions SchemeThe Financial Institutions Scheme

• Australian Financial Institutions Commission - Peak Regulator

• State Supervisory Authorities - implement supervision at State level

• Special Services Providers eg Credit Union Services

• Standards for Credit Unions & Building Societies prescribed

Financial Institutions Scheme Financial Institutions Scheme ObjectivesObjectives

• National Coordination of high uniform standards and practices

• Uniform Prudential Supervision of NBFI based on Prudential Standards, Reporting & Disclosure requirements

• Maintain stability & efficiency of the NBFI System in Australia

Financial Institutions Scheme Financial Institutions Scheme PhilosophyPhilosophy

• The responsibility for the financial success and viability of financial institutions rests with their boards and management not with governments or supervisors

The Need for ReviewThe Need for Review• Inconsistencies in application of supervision

on a State to State basis

• The Changing Financial Marketplace – products & services aligned with banks

• The need for efficiencies in the Supervisory arena

• Technological developments - a global market

• New FI’s not within the regulatory net

Reasons for ReviewReasons for Review

• Era of accelerated change in the financial system

• Regulation must adapt both to facilitate greater competition and efficiency in the financial marketplace and to secure the integrity and stability of its operations

• Wallis Inquiry established by Federal Government May 1996

Taxation of Mutual FI’sTaxation of Mutual FI’s

Before 1995, credit unions in Australia were exempt from payment of company tax on profits (surplus) arising from business transacted with members.

Since business with non-members comprised primarily the investment of liquid asset reserves in deposits & marketable securities, credit unions in effect paid no company tax.

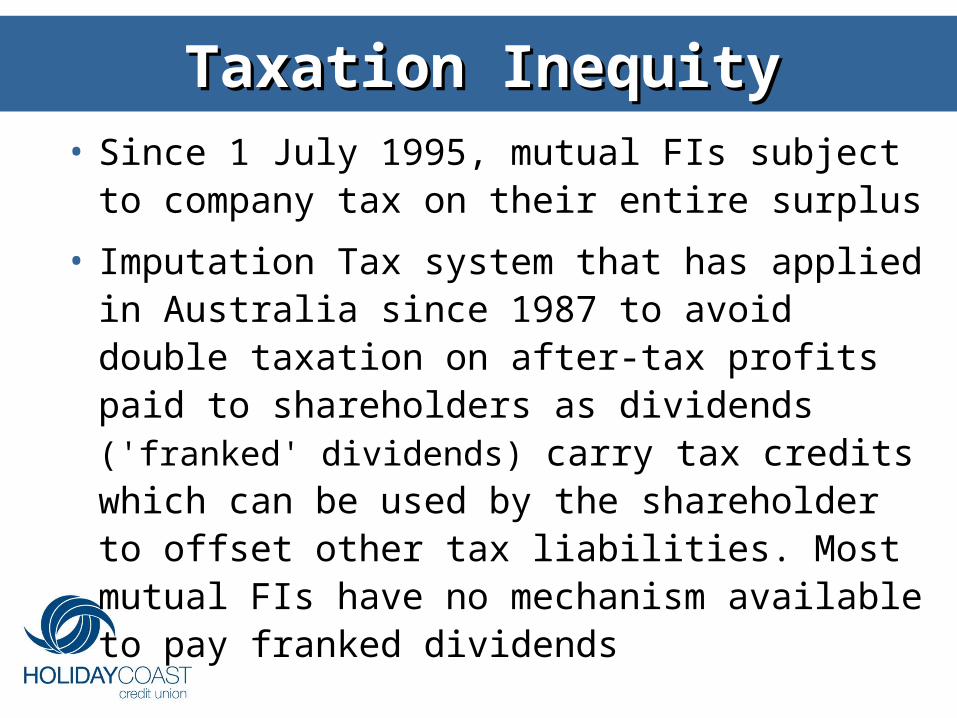

Taxation InequityTaxation Inequity• Since 1 July 1995, mutual FIs subject to

company tax on their entire surplus

• Imputation Tax system that has applied in Australia since 1987 to avoid double taxation on after-tax profits paid to shareholders as dividends ('franked' dividends) carry tax credits which can be used by the shareholder to offset other tax liabilities. Most mutual FIs have no mechanism available to pay franked dividends

The Wallis ReportThe Wallis Report

• Report delivered March 1997

• Clarified regulatory roles

• Consistent regulation of similar financial products

• Competitive neutrality across the financial system

• Foundation for FI’s to adapt to change

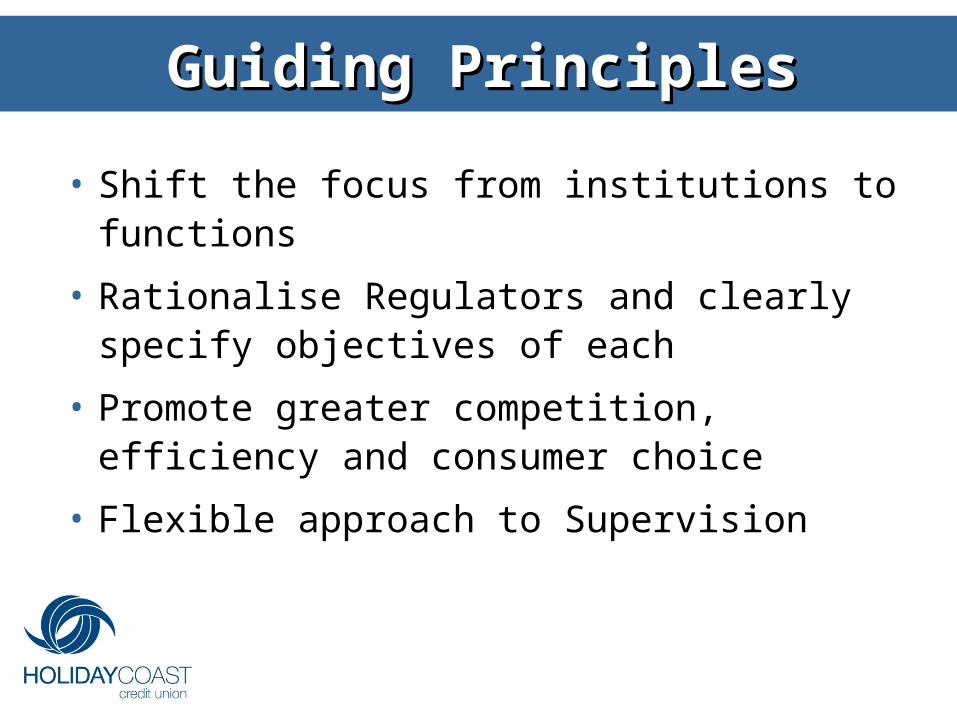

Guiding PrinciplesGuiding Principles

• Shift the focus from institutions to functions

• Rationalise Regulators and clearly specify objectives of each

• Promote greater competition, efficiency and consumer choice

• Flexible approach to Supervision

Wallis Regulatory StructureWallis Regulatory Structure

• Australian Prudential Regulation Commission (APRC) to supervise all institutions engaged in deposit taking, insurance and superannuation – Created as APRA

• Reserve Bank of Australia separate from APRC & will maintain overall responsibility for financial system stability

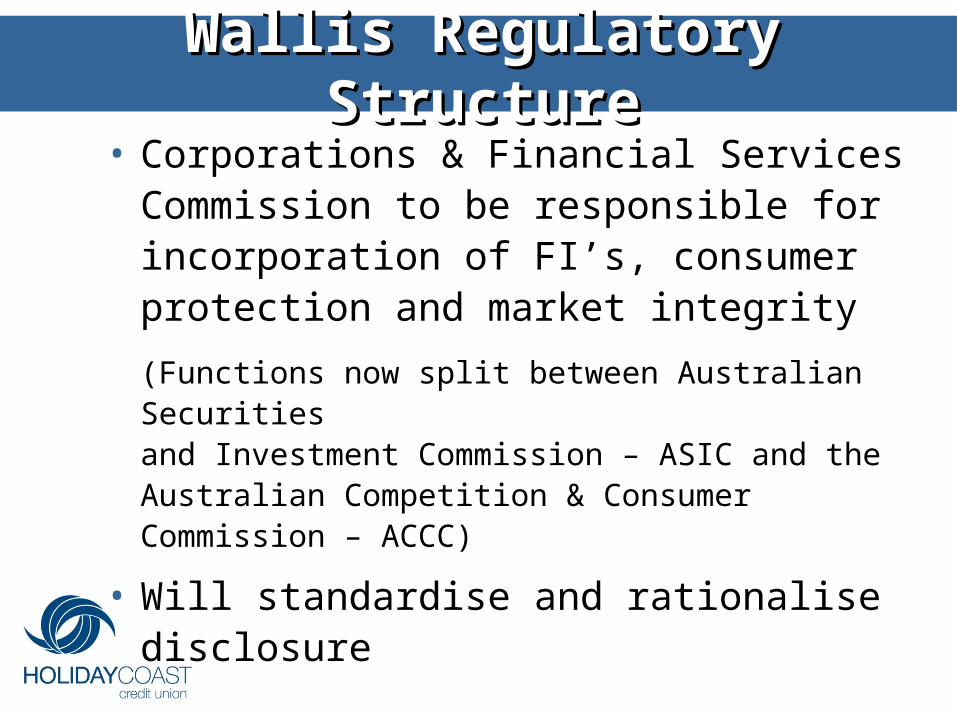

Wallis Regulatory StructureWallis Regulatory Structure• Corporations & Financial Services

Commission to be responsible for incorporation of FI’s, consumer protection and market integrity

(Functions now split between Australian Securities and Investment Commission – ASIC and the Australian Competition & Consumer Commission – ACCC)

• Will standardise and rationalise disclosure

RegulationRegulation• An ADI, subject to APRA regulation (Jul 1999) &

supervision as well as ASIC regulation under the Financial Services Reform (FSR) legislation & the Corporations Act as well as Austrac - AML

• Must adhere to APRA prudential standards & practices to ensure that financial promises made by ADI’s are met within a stable, efficient & competitive financial system

• Licenced under the Banking Act & hold an ADI Licence & an Australian Financial Services (AFS) Licence under FSR supervised by ASIC

APRA RoleAPRA Role

• APRA is the prudential regulator of the Australian financial services industry overseeing banks, credit unions, building societies, general insurance & reinsurance companies, life insurance, friendly societies, & most members of the superannuation industry

• APRA is funded largely by the industries that it supervises

• It was established on 1 July 1998

ASIC RoleASIC Role

• ASIC is Australia’s corporate, markets and financial services regulator

• Ensures Australia’s financial markets are fair and transparent, supported by confident and informed investors and consumers

• Maintain, facilitate and improve the performance of the financial system and entities in it

ACCC RoleACCC Role

ACCC - The ACCC promotes competition and fair trade in the market place to benefit consumers, businesses and the community.

It also regulates national infrastructure services. Its primary responsibility is to ensure that individuals and businesses comply with the Commonwealth competition, fair trading and consumer protection laws.

Mutuality in FIMutuality in FI• Holiday Coast Credit Union is a public

company limited by shares, organised on the basis of the principles of mutuality

• Holiday Coast Credit Union has set out in the preamble to its constitution that these principles of mutuality, although not binding, will provide a keystone for the basis of decision-making

• Board of Directors elected by members

WOCCU Operating PrinciplesWOCCU Operating Principles

Democratic Structure

Open and Voluntary Membership within “Bond” & member responsibilities

Democratic Controla cooperative enterprise serving and controlled by its members

Non-Discriminationnon-discriminatory in relation to race, nationality, sex, religion, and politics

WOCCU Operating PrinciplesWOCCU Operating PrinciplesService to Members• Service to Members

Credit unions services are directed to improve the economic and social well-being of all members

• Distribution to MembersTo encourage thrift through savings and thus to provide loans and other services

• Building Financial StabilityBuild the financial strength to ensure continued service to membership

WOCCU Operating PrinciplesWOCCU Operating PrinciplesSocial Goals• On-Going Education

The promotion of thrift and the wise use of credit, and the rights and responsibilities of members

• Cooperation Among Cooperativesto best serve the interests of their members and their communities

• Social Responsibilityto the individual members & to the larger community in which they work and reside

Other LegislationOther Legislation• Subject to regulation in accordance with

numerous other pieces of legislation, including: Trade Practices, Taxation, OH & S, Industrial Relations / Workplace laws, Environmental legislations and other legislation pertaining to corporations

• Holiday Coast Credit Union considers the compliance with legislation as a key operational risk and has various systems and processes to monitor ongoing compliance with these requirements

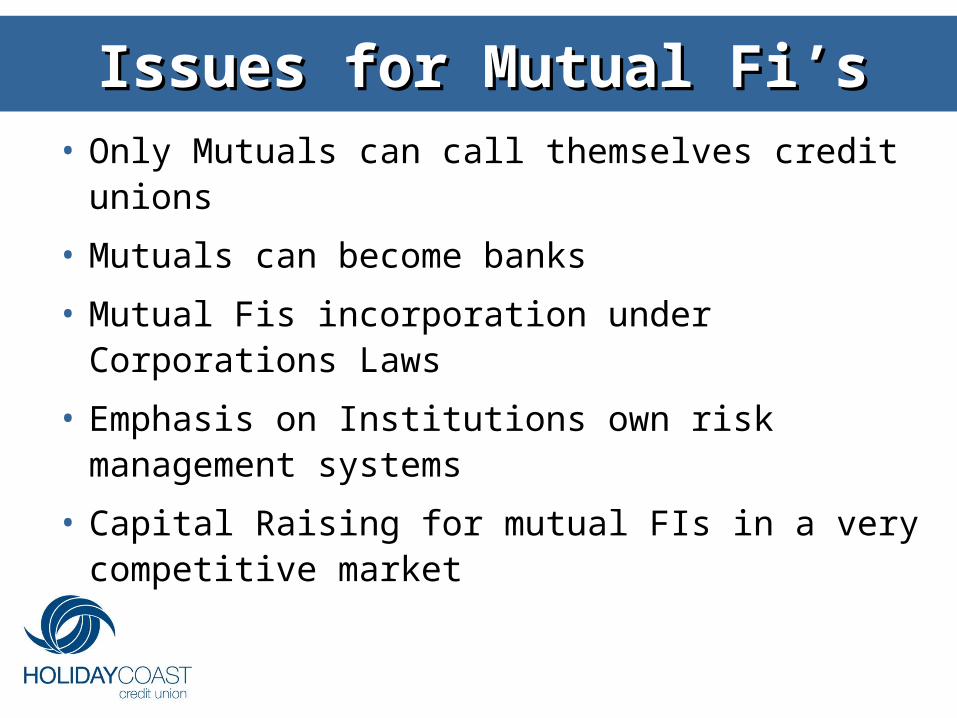

Issues for Mutual Fi’sIssues for Mutual Fi’s• Only Mutuals can call themselves credit unions

• Mutuals can become banks

• Mutual Fis incorporation under Corporations Laws

• Emphasis on Institutions own risk management systems

• Capital Raising for mutual FIs in a very competitive market

• Determine definition of “Mutual”

• Determine impact of mutuality on Capital, Liquidity, Depositor Protection & Supervision

• Decide how to fit into new national system and retain credit union identity and collective endeavour

• Managing the loss of taxation concessions

Post Wallis Challenges Post Wallis Challenges for Movementfor Movement

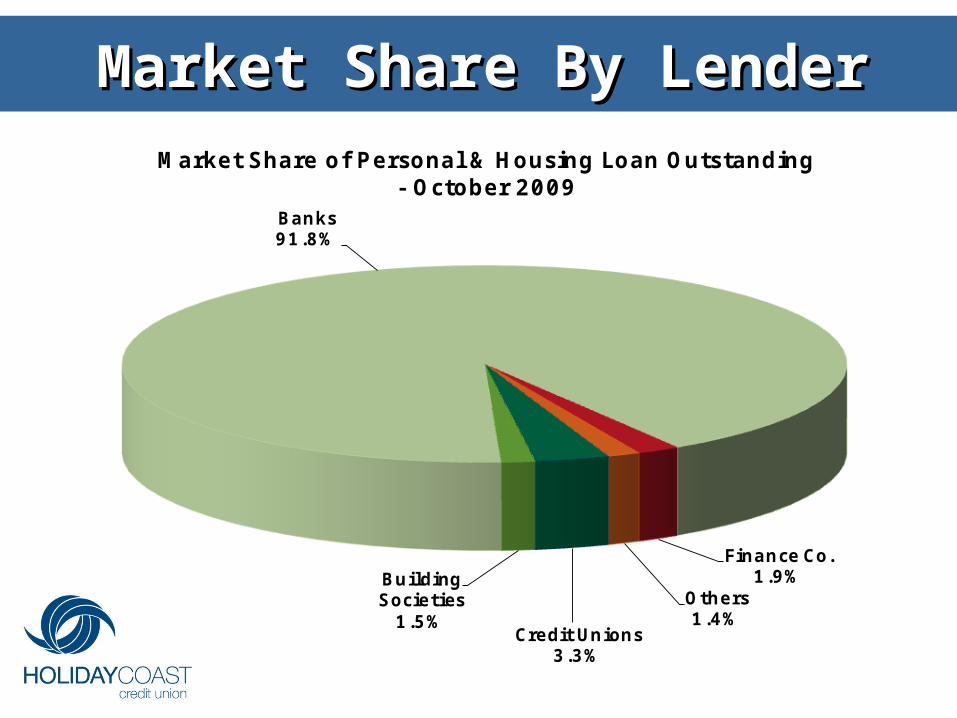

Market Share By LenderMarket Share By Lender

Credit Unions3.3%

Building Societies

1.5%

Banks91.8%

Finance Co.1.9%

Others1.4%

Market Share of Personal & Housing Loan Outstanding- October 2009

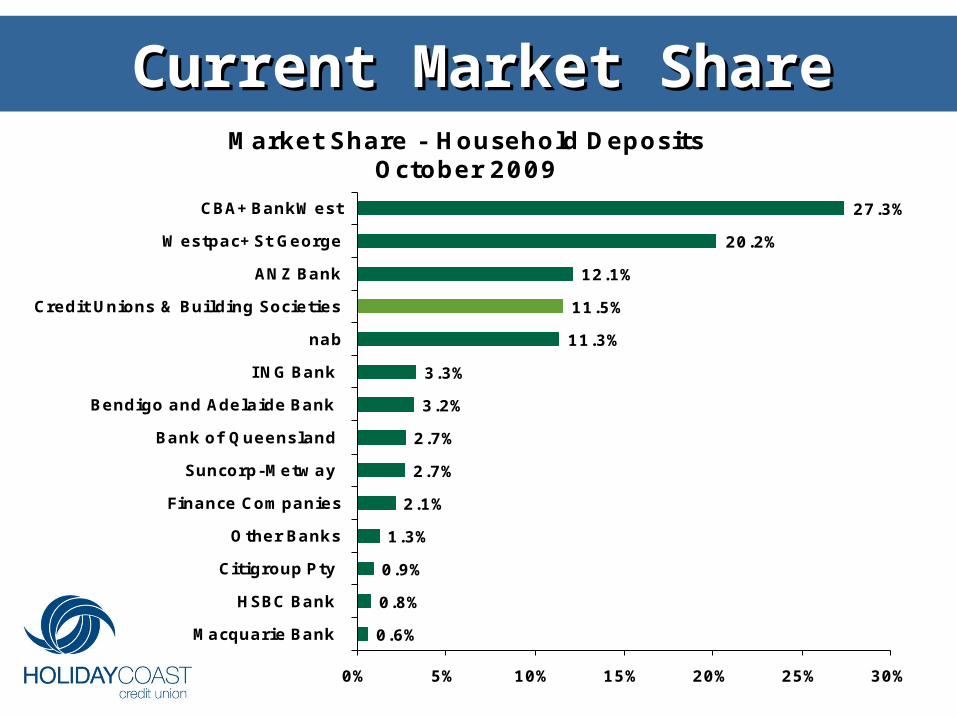

Current Market ShareCurrent Market Share

27.3%

20.2%

12.1%

11.5%

11.3%

3.3%

3.2%

2.7%

2.7%

2.1%

1.3%

0.9%

0.8%

0.6%

0% 5% 10% 15% 20% 25% 30%

CBA+BankWest

Westpac+St George

ANZ Bank

Credit Unions & Building Societies

nab

I NG Bank

Bendigo and Adelaide Bank

Bank of Queensland

Suncorp-Metway

Finance Companies

Other Banks

Citigroup Pty

HSBC Bank

Macquarie Bank

Market Share - Household DepositsOctober 2009

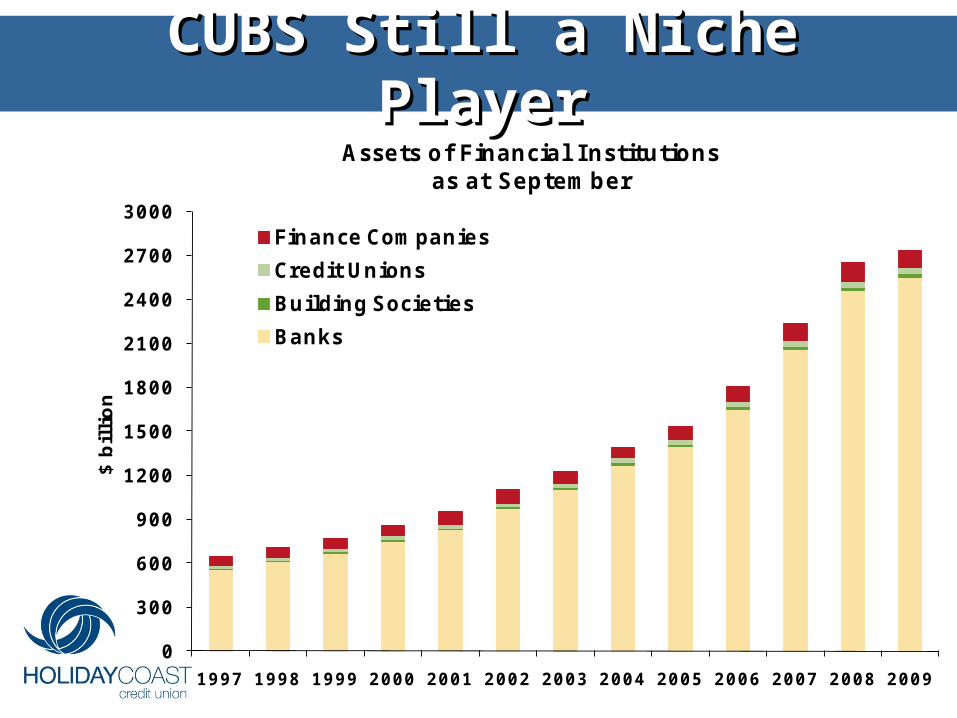

CUBS Still a Niche PlayerCUBS Still a Niche Player

0

300

600

900

1200

1500

1800

2100

2400

2700

3000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

$ b

illi

on

Assets of Financial I nstitutionsas at September

Finance Companies

Credit Unions

Building Societies

Banks

But Assets Growing SteadilyBut Assets Growing Steadily

46,016

46,847

21,504

22,656

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

J un-94 J un-98 J un-02 J un-06 Sep-09

On-Balance Sheet Total AssetsAs at June

Credit Unions

Building Societies

million

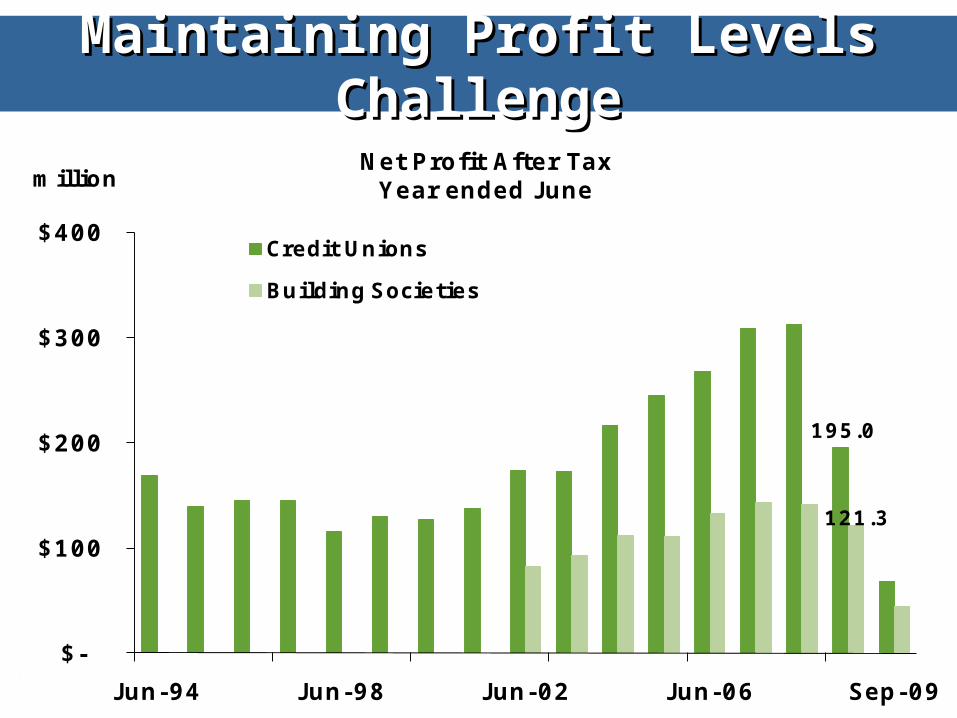

Maintaining Profit Levels ChallengeMaintaining Profit Levels Challenge

195.0

121.3

$-

$100

$200

$300

$400

Jun-94 Jun-98 Jun-02 Jun-06 Sep-09

Net Profit After Tax Year ended June

Credit Unions

Building Societies

million

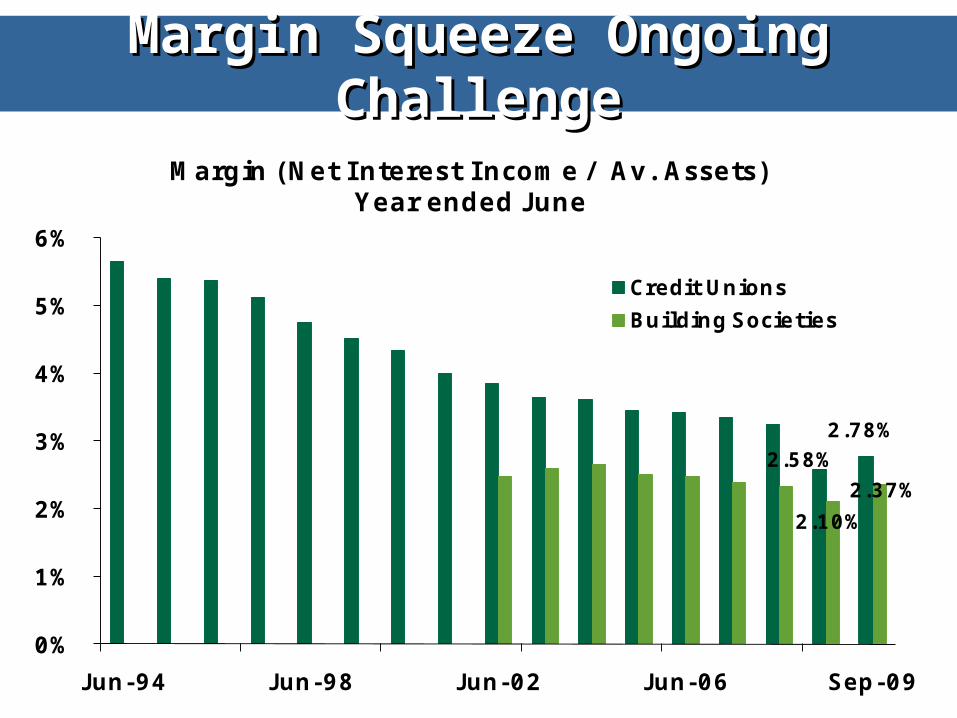

Margin Squeeze Ongoing ChallengeMargin Squeeze Ongoing Challenge

2.58%2.78%

2.10%

2.37%

0%

1%

2%

3%

4%

5%

6%

Jun-94 Jun-98 Jun-02 Jun-06 Sep-09

Margin (Net I nterest I ncome / Av. Assets)Year ended J une

Credit Unions

Building Societies

Market Share Slipped Over The YearsMarket Share Slipped Over The Years

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

Oct-04 Oct-05 Oct-06 Oct-07 Oct-08 Oct-09

Market Share - Housing and Personal Loan Outstanding

Credit Unions Building Societies

41

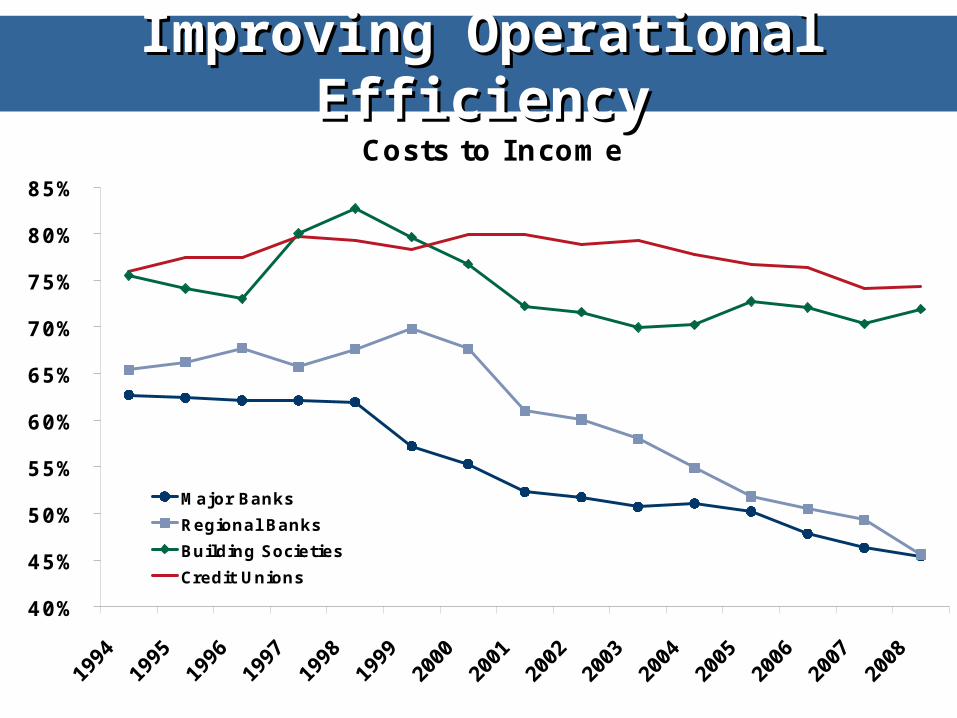

Improving Operational Improving Operational EfficiencyEfficiencyCosts to I ncome

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

Major Banks

Regional Banks

Building Societies

Credit Unions

42

0

170

340

510

680

850

0

10

20

30

40

50

1972 1982 1992 2002

No

. o

f C

red

it U

nio

ns

To

tal A

ssets

($

bn

)

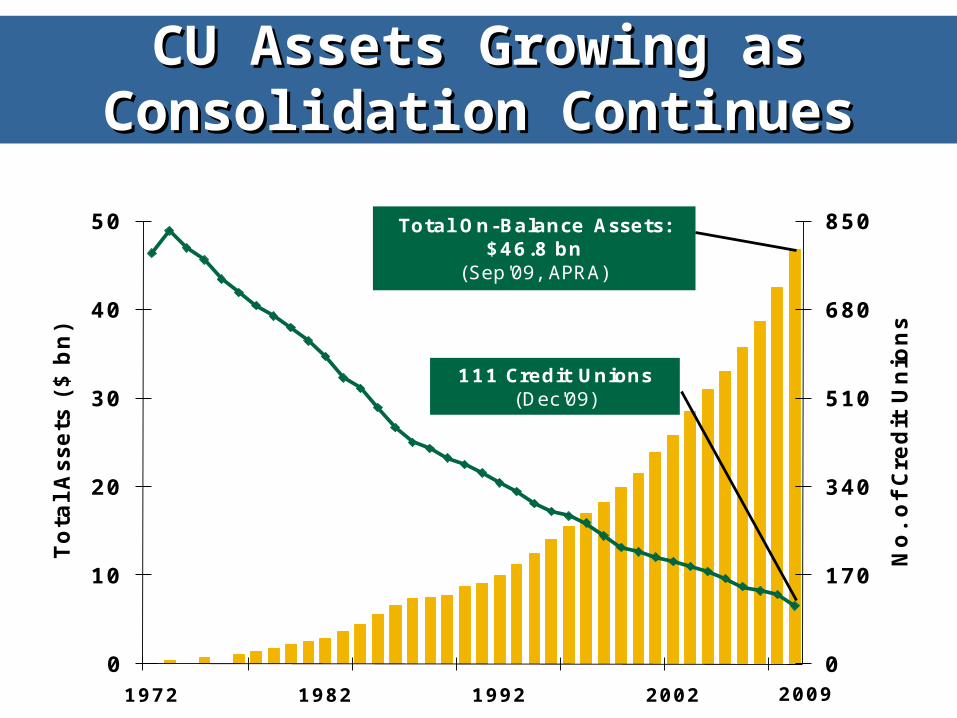

Total On-Balance Assets: $46.8 bn

(Sep'09, APRA)

111 Credit Unions(Dec'09)

2009

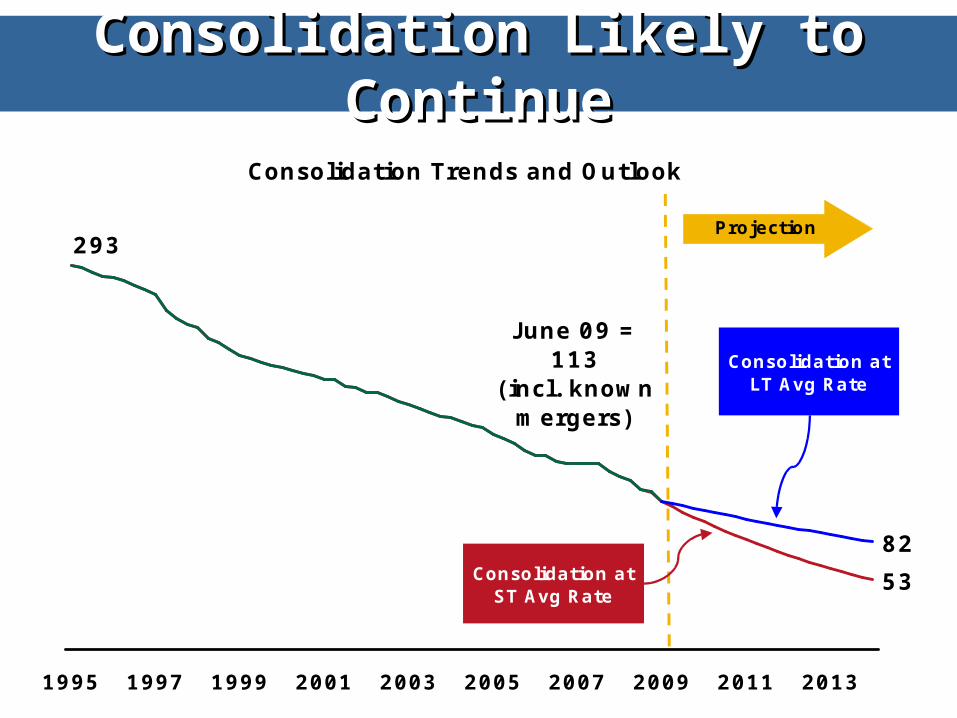

CU Assets Growing as CU Assets Growing as Consolidation ContinuesConsolidation Continues

Consolidation Likely to ContinueConsolidation Likely to Continue

Consolidation Trends and Outlook

53

J une 09 = 113

(incl. known mergers)

293

82

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Consolidation at LT Avg Rate

Consolidation at ST Avg Rate

Projection

Lessons LearntLessons Learnt

• Mutual FIs must maintain close liaison with Governments to ensure that the legislative framework desired is achieved

• Protect the fundamentals of credit unions at all costs - the International Credit Union Operating Principles should be non negotiable

Lessons LearntLessons Learnt

• Competitors will seek to also enforce a level playing field eg Taxation treatment

• Commit to a unified voice and utilise all avenues of carrying the unified position

• Be prepared to source competitors with the same end goal for structure and lobby with them

Lessons LearntLessons Learnt• Do not succumb to short term solutions for

issues that are the cornerstone of the credit union movement eg capital raising and its alignment with Mutuality

• Commit to a regime of Self Regulation to underpin sound prudential practices and procedures

• The importance of lobbying with a single voice – Cuscal, Creditlink & NCUA, Assoc Building Societies now ABACUS

Global Financial CrisisGlobal Financial Crisis• The role of APRA

• The importance of the APRA Prudential Standards and a strong FI sector & regulator

• The Federal Government Deposit Guarantee introduced 12 October 2008 for minimum 3 year period – automatic cover for deposits of up to $1m

• A solid performance by APRA regulated FIs

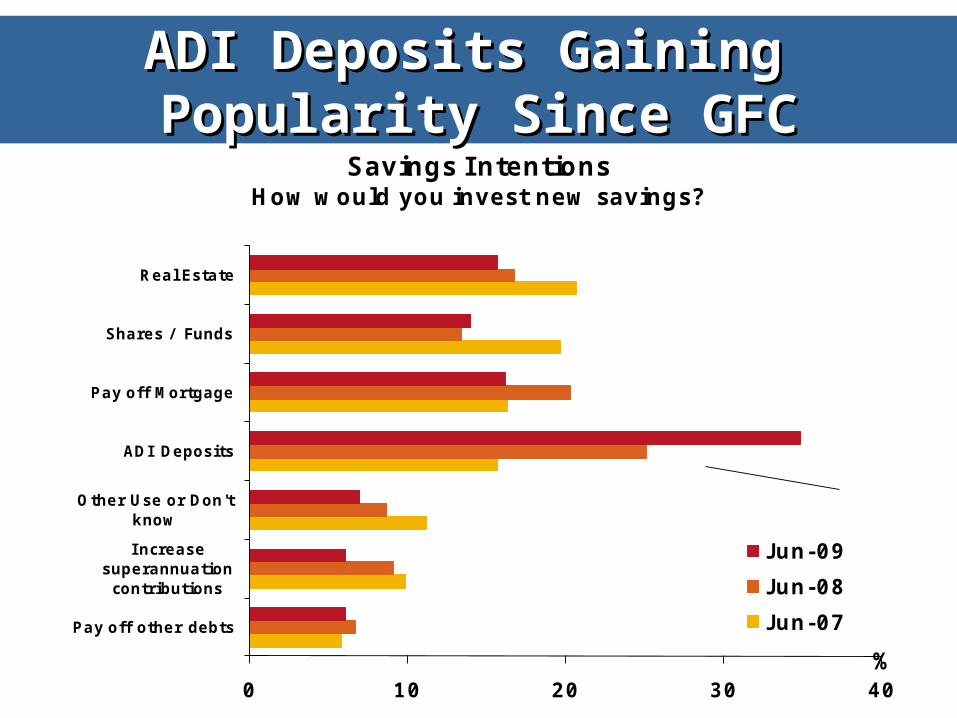

0 10 20 30 40

Pay off other debts

I ncrease superannuation contributions

Other Use or Don't know

ADI Deposits

Pay off Mortgage

Shares / Funds

Real Estate

Savings I ntentionsHow would you invest new savings?

J un-09

Jun-08

Jun-07

%

ADI Deposits Gaining ADI Deposits Gaining Popularity Since GFCPopularity Since GFC

SummarySummary• Mutual FIs must play an active & influential

role in ensuring that the legislative framework enshrines the fundamental philosophies and values of mutual FIs and at the same time delivers a “level playing field” for competing in the financial marketplace.

• Lobbying and speaking with one voice is key

• Corporations Regulator to be educated in the principles of mutuals

Philosophies & ValuesPhilosophies & Values

“If an organisation is to meet the challenges of a changing world, it must be prepared to change everything about itself except its basic beliefs as it moves through corporate life…The only sacred cow in an organisation should be its basic philosophy of doing business.”

Tom Watson Jr - IBM

QuestionsQuestions???