ppaca overview

DESCRIPTION

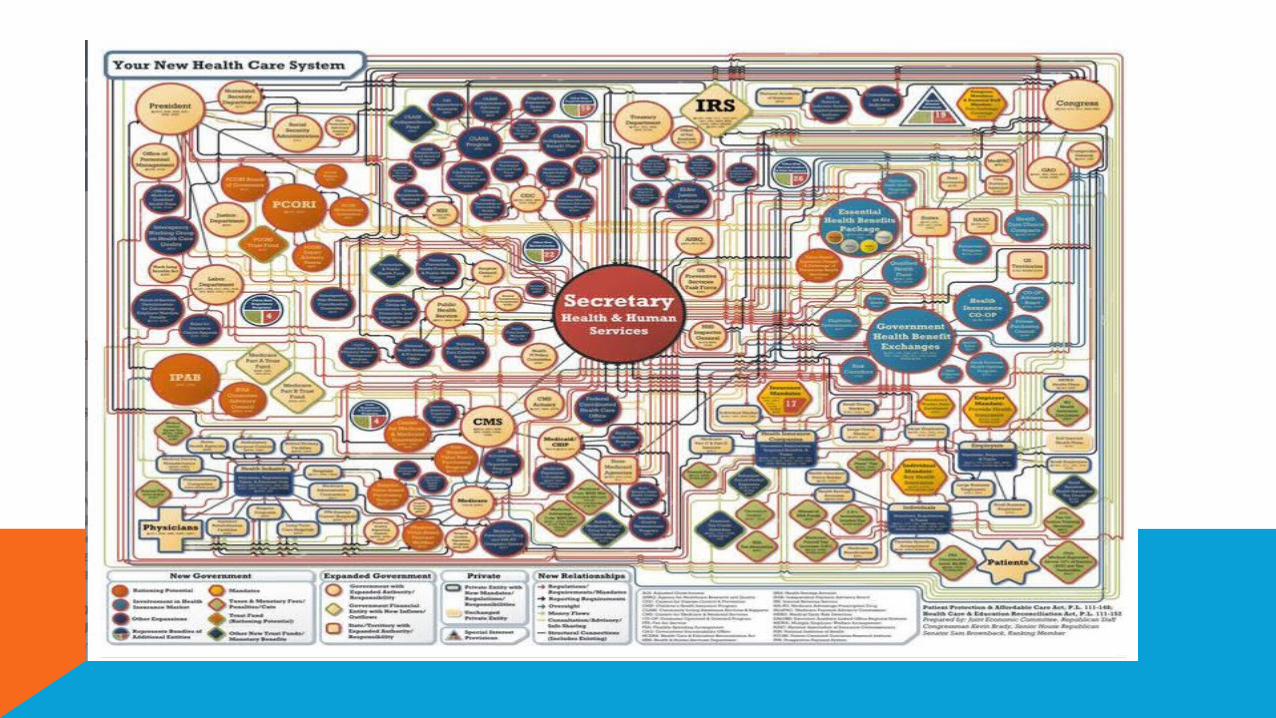

PPACA OVERVIEW. Leonard J. Nelson, III. Question One: What was the EFFECT of PPACA on the U.S. Health Care system?. It creates a new government health care plan to replace private insurance. - PowerPoint PPT PresentationTRANSCRIPT

PPACA O

VERVIEW

L E ON

AR

D J

. N

E L S ON

, I I

I

QUESTION ONE: WHAT WAS THE EFFECT OF PPACA ON THE U.S. HEALTH CARE SYSTEM?1. It creates a new government health care plan to replace private insurance.

2. It requires every working person to set up a Health Savings Account that is funded both by the employee and employer and coupled with a HDHP.

3. It provides incentives for the states to set up a comprehensive, universal health care system for their citizens.

4. It builds on the existing system by preserving Employer Sponsored Health Insurance (ESHI) and private individual health insurance but vastly increases federal regulatory authority over private insurance markets

PPACA

• Adopted March 2010 on a straight party line vote

• Based on Romneycare, a health care plan devised by the Heritage Foundation and adopted by the Commonwealth of Massachusetts when it had a Republican Governor and a legislature controlled by Democrats.

• Full implementation on January 1, 2014, but some features were implemented earlier and others have been delayed.

BASIC ELEMENTS

Insurance Exchanges

Qualified Health Plans

Three Legged Stool- Insurance Reforms; Individual Mandate; Premium and Cost-Sharing Subsidies

Large Employers-Pay or Play

Small Employers -Subsidies and SHOP Medicaid Expansion

INSURANCE EXCHANGES

• States were supposed to establish exchanges to facilitate purchase of “qualified health plans” by individuals and small businesses from private insurers

• But several state refused so Federal Government set up many of the exchanges

17 state-based, 7 partnerships, 27 federal

INSURANCE EXCHANGES

• Beginning fall 2013 with coverage effective January 1 2014, individuals may purchase qualified health plans (QHPs) on the exchanges during annual enrollment periods or after qualifying events

• Individuals may also purchase QHPs outside of exchanges but no subsidies are available

QUESTION TWO: WHAT IS A “QUALIFIED HEALTH PLAN” (QHP)?1. A plan that is approved by the Insurance Commissioner of

Insurance in the state where it is to be offered.

2. A health insurance policy that has a high deductible and can be coupled with a Health Savings Account.

3. A plan that is affordable.

4. A plan that is certified by the Health Insurance Marketplace as being in compliance with the requirements of PPACA.

“Under the Affordable Care Act, starting in 2014, an insurance plan that is certified by the Health Insurance Marketplace, provides essential health benefits, follows established limits on cost-sharing (like deductibles, copayments, and out-of-pocket maximum amounts), and meets other requirements. A qualified health plan will have a certification by each Marketplace in which it is sold.”

Qualified Health Plan, https://www.healthcare.gov/glossary/qualified-health-plan/

QUALIFIED HEALTH PLAN

QHPS: BENEFIT TIERSIn the Exchanges-Four Categories (all providing essential benefits package) plus separate

Catastrophic plan

Bronze: covers 60% of the standard benefits cost (actuarial value)

Silver: Covers 70% of the standard benefits cost

Gold: covers 80% of the standard benefits cost

Platinum: covers 90% of the standard benefits cost

Catastrophic:

Only available for those age <30 or with hardship exemptions

Only available in the individual market

• Small group and individual plans offered both within and outside exchanges must be QHPs offering at least EHBs

• EHBs are delineated in accordance with a benchmark plan offered by a private insurer in the State

• States required to choose benchmark plan by 12/26/2012 but if State failed to act default plan was largest small group plan in the state (e.g. BCBS of AL- 320 Plan, PPO)

• Must comply with statutory guidelines (10 essential benefits)

• Grandfathered small employer and individual plans, large employer group plans and Self Insured Plans not required to offer EHB or adhere to the actuarial value and metallic tier requirements

Essential Health Benefit (EHB) Benchmark Plans, as of January 3, 2013http://kff.org/health-reform/state-indicator/ehb-benchmark-plans/,

QHPS: ESSENTIAL HEALTH BENEFITS (EHBS)

EHBs include at least the following ten items and services :

Outpatient Care Trips to Emergency Room Treatment in the hospital for inpatient care Maternity and newborn care Mental health and substance use disorder services, including behavioral health treatment,

counseling and psychotherapy Prescription drugs Rehabilitative services and devices to including physical and occupational therapy, speech therapy,

etc. Laboratory services Preventive services including counseling, screenings, and vaccines and chronic disease

management Pediatric services, including dental and vision care

What’s Covered in the Marketplace, https://www.healthcare.gov/blog/10-health-care-benefits-covered-in-the-health-insurance-marketplace/

ESSENTIAL HEALTH BENEFITS

PREVENTIVE SERVICES

• All non-grandfathered private health plans including self-insured plans are required to provide coverage for preventive services including certain screenings and immunization without cost sharing

• For women preventive coverage includes Contraceptives, EC (including Ella) and sterilization

QUESTION THREE : WHAT DID SCOTUS HOLD IN THE HOBBY LOBBY CASE ?

1. Employers don’t have to provide contraceptives or Viagra to employees.

2. Employees of religious organizations can be fired for using birth control.

3. Requiring religious employers to provide contraceptives to employees violates the First Amendment.

4. Under the Religious Freedom Restoration Act, the owners of a closely held for profit corporation with a religious objection to certain contraceptives are entitled to the same accommodation given certain religious employers (i.e., their insurer will pay for the contraceptive if they fill out a form claiming an exemption)

Insurance Reforms

Individual Mandate

Premium and Cost Sharing Subsidies

http://theincidentaleconomist.com/wordpress/stools-need-more-than-two-legs/

“THE THREE LEGGED STOOL”

INSURANCE REFORMS

Prohibition on use of pre-existing condition limitations

Guaranteed Issuance and Renewal

Adjusted Community rating - age ratio limited to 3:1, geography, family size, and tobacco use (1.5:1 ratio)

No annual and lifetime caps

Individual Shared Responsibility Provision requires individual to maintain “minimum essential coverage” for themselves and their dependents

Insurers will be required to provide everyone that they cover each year with information that will help them demonstrate they had coverage beginning with the 2015 tax year.

Questions and Answers on the Individual Shared Responsibility Provision, http://www.irs.gov/uac/Questions-and-Answers-on-the-Individual-Shared-Responsibility-Provision

INDIVIDUAL MANDATE

QUESTION FOUR: WHAT DID THE SUPREME COURT HOLD IN NFIB V. SEBELIUS (DECIDED 6/28/2012)?

Congress had the power to enact the individual mandate under both its taxing power and its commerce clause power.

Congress had the power to impose individual mandate as a tax but not under ithe commerce clause.

Congress has plenary authority to enact all health care legislation including the individual mandate because there is a constitutional right to healthcare.

Only the States have the authority to require health insurance.

Individual mandate is an unconstitutional exercise of commerce clause power because it punishes inactivity rather than regulating activity

Individual mandate is constitutional as a tax

NFIB v. Sebelius, http://www2.bloomberglaw.com/public/desktop/document/Natl_Federation_of_Independent_Business_v_Sebelius_No_Nos_11393_1

NFIB V. SEBELIUS (DECIDED 6/28/2012)

• After NFIB v Sebelius held individual shared responsibility is a tax, PLF’s amended complaint alleged that the individual mandate tax is illegal because it was introduced in the Senate rather than the House, as required by the Constitution’s Origination Clause for new revenue-raising bills (Article I, Section 7).

• On June 28, 2013, U.S. District Court for DC dismissed the complaint holding that “the individual mandate was not a “Bill[] for raising Revenue,” and thus the plaintiff’s Origination Clause challenge likewise fails to state a claim upon which reliefmay be granted. In any event, even if the individual mandate were a “Bill[] for raising Revenue,” the Court holds that it was nevertheless an amendment to a bill that “originated in theHouse of Representatives” and thus was enacted in compliance with the Origination Clause.”

• Oral Argument before DC Circuit on May 8, 2014.

Sissell v HHS, http://www.pacificlegal.org/old-site/document.doc?id=917

SISSEL V. HHS- ORIGINATION CLAUSE CHALLENGE

1. The type of coverage an individual needs to have to meet the individual responsibility requirement under PPACA (includes individual exchange policies, employer-sponsored coverage, government-sponsored plans, and grandfathered plans )

2. Stand alone vision or dental coverage

3. Workers Compensation

4. Accident or Disability Policies

Questions and Answers on the Individual Shared Responsibility Provision, http://www.irs.gov/uac/Questions-and-Answers-on-the-Individual-Shared-Responsibility-Provision

QUESTION FIVE: WHAT IS “MINIMUM ESSENTIAL COVERAGE”?

QUESTION SIX: IS THE INDIVIDUAL MANDATE NECESSARY TO THE SUCCESS OF PPACA?

1. No, it is merely an attempt to raise taxes to redistribute wealth.

2. Yes, it is necessary to prevent adverse selection if you have insurance reforms and it may also reduce free riders and cost shifting.

3. No, it is merely a way to punish opponents of PPACA.

4. Yes, it provides essential funding.

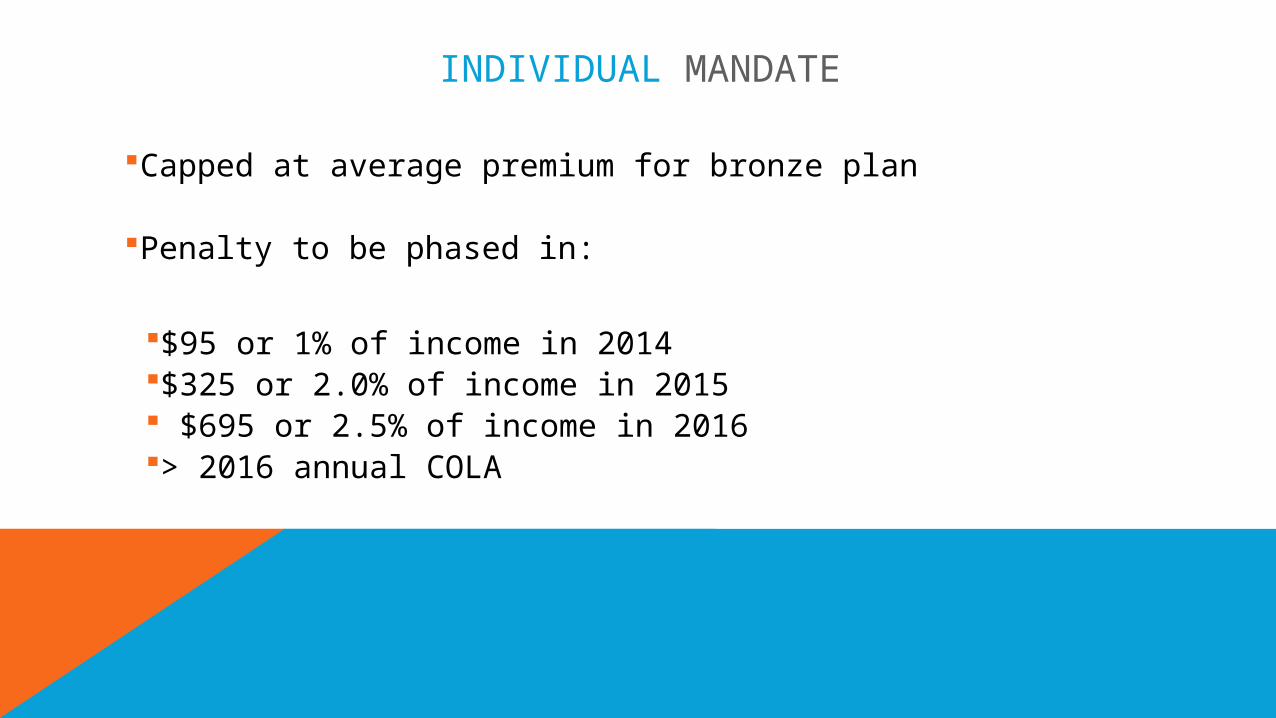

INDIVIDUAL MANDATE

Capped at average premium for bronze plan

Penalty to be phased in:

$95 or 1% of income in 2014 $325 or 2.0% of income in 2015 $695 or 2.5% of income in 2016> 2016 annual COLA

INDIVIDUAL MANDATE

Exemptions from fine:

Financial hardship religious objections Member of Health Care Sharing Ministry Indian Tribes Short coverage gap< 3 months Undocumented immigrants Incarceration Affordability: Those for whom the lowest cost plan option > 8% income Those with incomes <tax filing threshold Hardship

“If you have been notified that your health insurance policy will be cancelled, and you believe that the individual market health plan options available in your area are unaffordable, you will be eligible for a hardship exemption and will be able to enroll in catastrophic coverage available in your area.”Questions and Answers on Options Available for Consumers with Cancelled Policies, CMS Guidance, Jan. 3, 2014, http://www.cms.gov/CCIIO/Resources/Regulations-and-Guidance/Downloads/cancellation-consumer-options-faq-01-03-2014.pdf

HARDSHIP EXEMPTION

1.No, it is merely a mechanism to redistribute wealth.

2.Yes, it is necessary to garner votes to keep Democrats in power and prevent repeal.

3.No, it is merely vote buying.4.Yes, without these subsidies many low income

persons will be unable to gain coverage and access health care.

EXPLAINING HEALTH CARE REFORM: Questions About Health Insurance Subsidies, July 2012, http://kaiserfamilyfoundation.files.wordpress.com/2013/01/7962-02.pdf

QUESTION SEVEN: ARE PREMIUM AND COST-SHARING SUBSIDIES ESSENTIAL TO THE SUCCESS OF PPACA

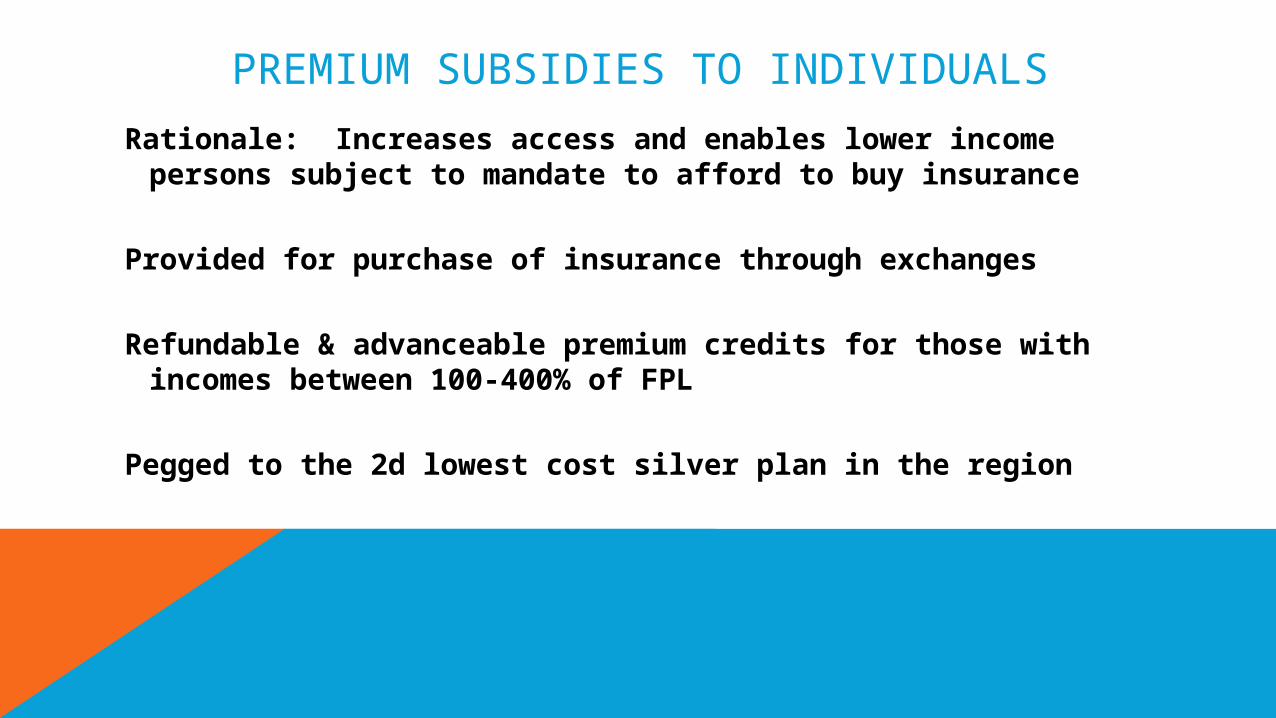

PREMIUM SUBSIDIES TO INDIVIDUALS

Rationale: Increases access and enables lower income persons subject to mandate to afford to buy insurance

Provided for purchase of insurance through exchanges

Refundable & advanceable premium credits for those with incomes between 100-400% of FPL

Pegged to the 2d lowest cost silver plan in the region

PREMIUM SUBSIDIES TO INDIVIDUALS

Sliding scale limiting premiums to % of income

Up to 133 %-2% 133-150% FPL: 3 – 4%150-200% FPL: 4 – 6.3%200-250% FPL: 6.3 – 8.05%250-300% FPL: 8.05 – 9.5%300-400% FPL: 9.5%

COST- SHARING SUBSIDIES• Reduces out of pocket maximum in silver plan

for households with incomes 100-250% FPL

• Increases actuarial value of silver plan for households with incomes of 100-250% FPL100-150% FPL: 94%150-200% FPL: 87%200-250% FPL: 73%

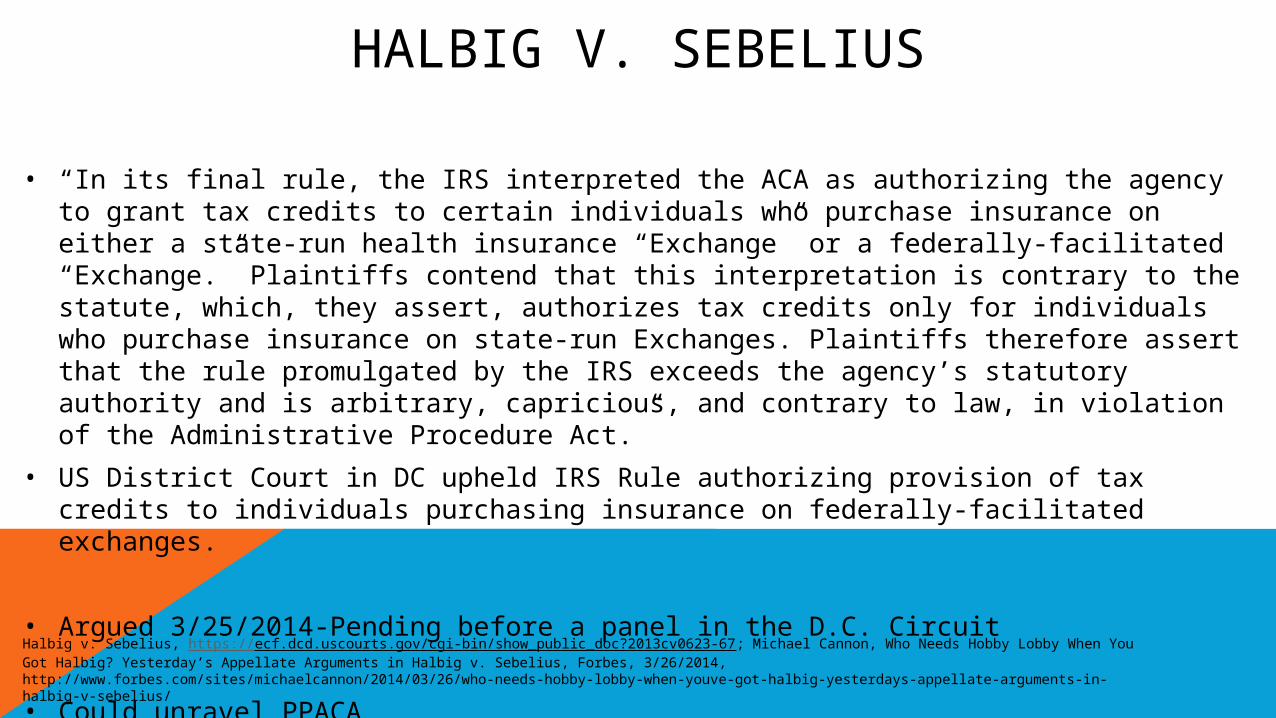

• “In its final rule, the IRS interpreted the ACA as authorizing the agency to grant tax credits to certain individuals who purchase insurance on either a state-run health insurance “Exchange” or a federally-facilitated “Exchange.” Plaintiffs contend that this interpretation is contrary to the statute, which, they assert, authorizes tax credits only for individuals who purchase insurance on state-run Exchanges. Plaintiffs therefore assert that the rule promulgated by the IRS exceeds the agency’s statutory authority and is arbitrary, capricious, and contrary to law, in violation of the Administrative Procedure Act.”

• US District Court in DC upheld IRS Rule authorizing provision of tax credits to individuals purchasing insurance on federally-facilitated exchanges.

• Argued 3/25/2014-Pending before a panel in the D.C. Circuit

• Could unravel PPACAHalbig v. Sebelius, https://ecf.dcd.uscourts.gov/cgi-bin/show_public_doc?2013cv0623-67; Michael Cannon, Who Needs Hobby Lobby When You Got Halbig? Yesterday’s Appellate Arguments in Halbig v. Sebelius, Forbes, 3/26/2014, http://www.forbes.com/sites/michaelcannon/2014/03/26/who-needs-hobby-lobby-when-youve-got-halbig-yesterdays-appellate-arguments-in-halbig-v-sebelius/

HALBIG V. SEBELIUS

SMALL EMPLOYERS

< 50 full-time employees

Not required to provide coverage or make contribution to coverage provided through exchanges

May purchase coverage outside or through exchange but subject to essential health benefits requirement unless “grandfathered”

Employers with no more than 25 employees and average annual wages of less than $50,000 that purchase health insurance for employees will be eligible for a tax credit to be phased in:

2010-2013-up to 35% if employer pays at least 50% of cost

2014 and later-two-year credit of up to 50% if employer pays 50% of the cost for insurance purchased through Exchange

Source: Side-by-Side Comparison, Kaiser Foundation, http://www.kff.org/healthreform/upload/housesenatebill_final.pdf

SMALL EMPLOYER SUBSIDIES

LARGE EMPLOYERS PAY OR PLAY

Larger Employers (50 or more full time employees)

Not required to offer coverage

Insured and self insured plans ) not subject to essential benefits requirement

If employer fails to offer “minimum essential coverage” and one fulltime employee receives a subsidy through the exchange, then employer will be assessed $2000 per full time employee (excluding first 30 employees)

If offers coverage, but one fulltime employee receives subsidy, employer will be assessed the lesser of $3000 for each employee receiving subsidy or $2000 per full time employee (excluding first 30 employees).

• Firms 100+ full time employees do not have to meet the employer mandate until 2015 Need only offer coverage to 70% of employees in 2015

95% required thereafter

• Firms with 50 to 99 full time employees do not have to meet the mandate until 2016 but they have to maintain current coverage

Questions and Answers on Employer Shared Responsibility Provisions Under the Affordable Care Act, http://www.irs.gov/uac/Newsroom/Questions-and-Answers-on-Employer-Shared-Responsibility-Provisions-Under-the-Affordable-Care-Act

EMPLOYER MANDATE DELAYED 34

• PPACA creates a new health insurance Exchange for small businesses called the SHOP (Small Business Health Options Program), to offer QHPs to small employers with 100 or fewer employees

• Uses Adjusted Community Rating rather than experience rating

• Delayed until 2015 for 32 states, until 2016 in 18 states

• Participation in the Exchanges limited to businesses with up to 50 employees until 2016.

• Employers with > 100 employees may be allowed in beginning in 2017

Patient Protection and Affordable Care Act; Establishment of Exchanges and Qualified Health Plan; Small Business Health Options Program, 78 Fed. Reg. 33233 Tuesday, June 4, 2013, http://www.gpo.gov/fdsys/pkg/FR-2013-06-04/pdf/2013-13149.pdf ; Small Business Health Options Program (SHOP), CMS, http://www.cms.gov/CCIIO/Programs-and-Initiatives/Health-Insurance-Marketplaces/2015-Transition-to-Employee-Choice-.html

PPACA-SHOP

• Under PPACA Insurers have Medical Loss Ratio Limits of 80% for individuals and small groups and 85% for large groups.

• Individual and small-group HDHP not likely to not spend 80 percent of premiums on medical claims because oftentimes members will never reach the deductible

• In testimony before Congress, HHS Director Gary Cohen stated that HSA contributions by employer will be considered first dollar coverage for MLR as long as it is spent.

Energy & Commerce Hearing: State of Uncertainty: Implementation of PPACA's Exchanges and Medicaid Expansion December 13, 2012, http://www.aba.com/Issues/HSA/Documents/EandC_hearing_12.13.12Cohen_Cassidy.pdf

IMPACT OF PPACA ON HSA/CDHP

CADILLAC TAX-PPACA

• Begins in 2018

• Imposes 40% tax on the value of ESHI plans that exceeds these thresholds >$10,200 single coverage and $27,500 for family coverage

• Threshold pegged to CPI but health insurance have historically increased at a rate > CPI

• Over time more plans will be subject to Cadillac tax

• Enrollment in ESHI has increased by 8.2 million people since September 2013

• Most of these people were previously uninsured

• May be due to individual mandate and lower unemployment rate

Rand Corporation, Change in Health Insurance Since 2013, file:///C:/Users/User/Documents/RAND_RR656.pdf

IMPACT OF PPACA ON ESHI

• 3/4 of employers will continue to provide coverage for full time employees in 2015

• 1/3 one-third of employers have increased out-of-pocket limits, increased participants' share of premium costs and/or increased in-network deductibles

• More than 1/5 have increased copayments or coinsurance for primary care and/or increased employee proportions of dependent coverage costs

• More than ¼ have increased emphasis on HDHP with HSAInternational Federation of Employee Benefit Plans, 2014 Employer-Sponsored Health Care: ACA's Impact, http://www.ifebp.org/pdf/research/ACASurvey_2014.PDF

IMPACT OF PPACA ON ESHI

MEDICAID EXPANSION

Expands Medicaid eligibility to all <age 65 w/ incomes below 133% FPL (actually 138% because of 5% income disregard)

All newly eligible adults to get at least essential benefits package

States have to expand eligibility if they participate in Medicaid (but see SCOTUS opinion holding this condition is unconstitutional)

Medicaid expansion violates Congressional spending power (and 10th amendment) by amounting to undue coercion

Remedy for unconstitutional Medicaid expansion is to limit penalty to loss of federal match for expansion

NFIB v. Sebelius, http://www2.bloomberglaw.com/public/desktop/document/Natl_Federation_of_Independent_Business_v_Sebelius_No_Nos_11393_1

NFIB V. SEBELIUS

MEDICAID EXPANSION

Increased Federal Funding for Medicaid Expansion2014 – 2016-100%2017 -95% 2018-94%2019-93%>2020-90%

Governors in several states including Alabama have rejected Medicaid expansion

Implementing Expansion in 2014 (26 States and DC)

Open Debate (3 States)

Not Moving Forward at this Time (21 States)

Status of State Action on the Medicaid Expansion Decision, June 2014, Kaiser Family Foundation, http://kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act/

MEDICAID EXPANSION