ppaca impact on member institutions

DESCRIPTION

PPACA IMPACT ON MEMBER INSTITUTIONS. Why would you be Confused?. Health Care Reform Timeline. Insurance Market Post 2014. Most individuals in the U.S. are required to have health Insurance that qualifies as minimum essential coverage or be subject to a penalty. - PowerPoint PPT PresentationTRANSCRIPT

PPACA IMPACT ON MEMBER INSTITUTIONS

Why would you be Confused?

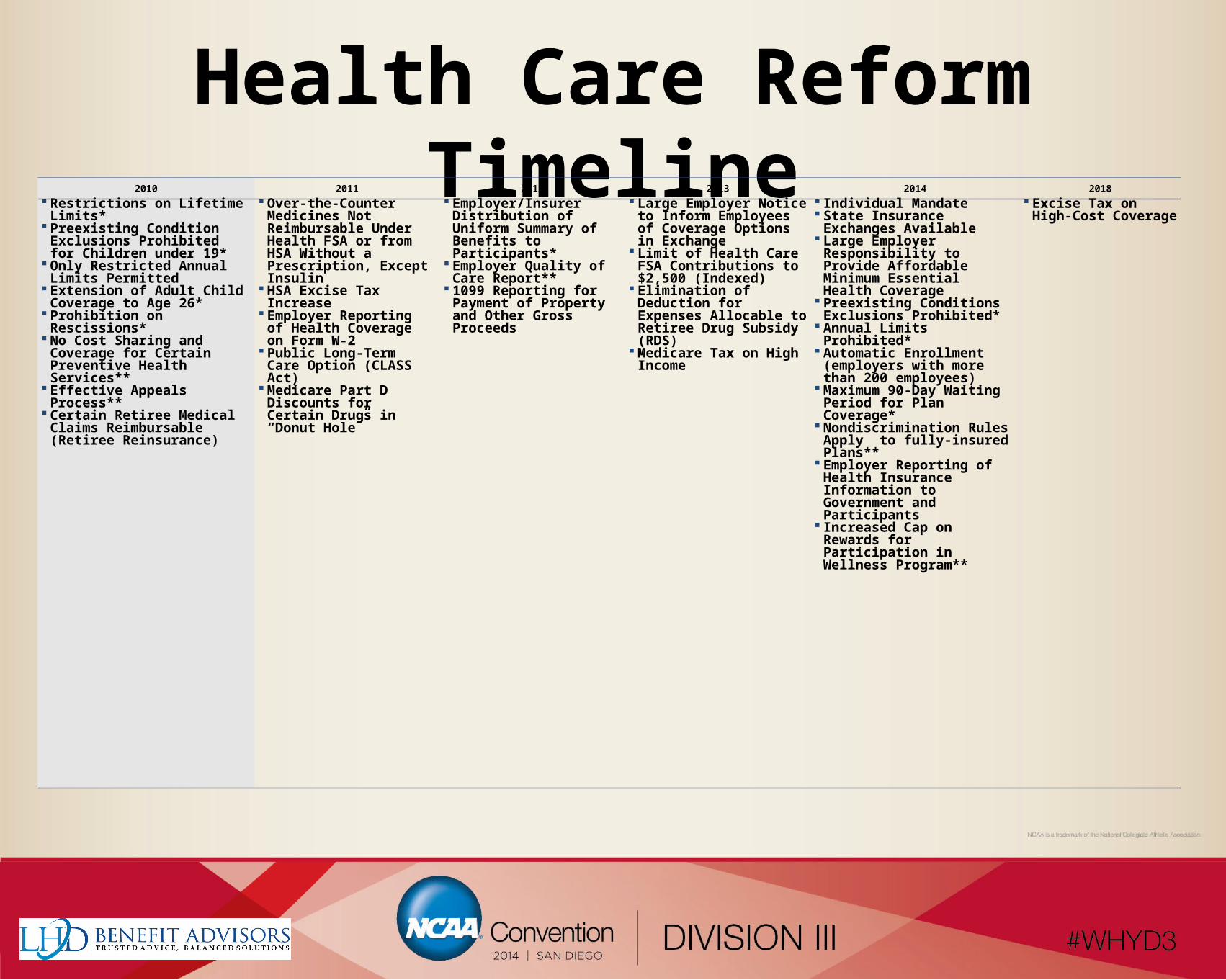

Health Care Reform Timeline2010 2011 2012 2013 2014 2018

Restrictions on Lifetime Limits*

Preexisting Condition Exclusions Prohibited for Children under 19*

Only Restricted Annual Limits Permitted

Extension of Adult Child Coverage to Age 26*

Prohibition on Rescissions* No Cost Sharing and Coverage

for Certain Preventive Health Services**

Effective Appeals Process** Certain Retiree Medical Claims

Reimbursable (Retiree Reinsurance)

Over-the-Counter Medicines Not Reimbursable Under Health FSA or from HSA Without a Prescription, Except Insulin

HSA Excise Tax Increase Employer Reporting of

Health Coverage on Form W-2

Public Long-Term Care Option (CLASS Act)

Medicare Part D Discounts for Certain Drugs in “Donut Hole”

Employer/Insurer Distribution of Uniform Summary of Benefits to Participants*

Employer Quality of Care Report**

1099 Reporting for Payment of Property and Other Gross Proceeds

Large Employer Notice to Inform Employees of Coverage Options in Exchange

Limit of Health Care FSA Contributions to $2,500 (Indexed)

Elimination of Deduction for Expenses Allocable to Retiree Drug Subsidy (RDS)

Medicare Tax on High Income

Individual Mandate State Insurance Exchanges

Available Large Employer

Responsibility to Provide Affordable Minimum Essential Health Coverage

Preexisting Conditions Exclusions Prohibited*

Annual Limits Prohibited* Automatic Enrollment

(employers with more than 200 employees)

Maximum 90-Day Waiting Period for Plan Coverage*

Nondiscrimination Rules Apply to fully-insured Plans**

Employer Reporting of Health Insurance Information to Government and Participants

Increased Cap on Rewards for Participation in Wellness Program**

Excise Tax on High-Cost Coverage

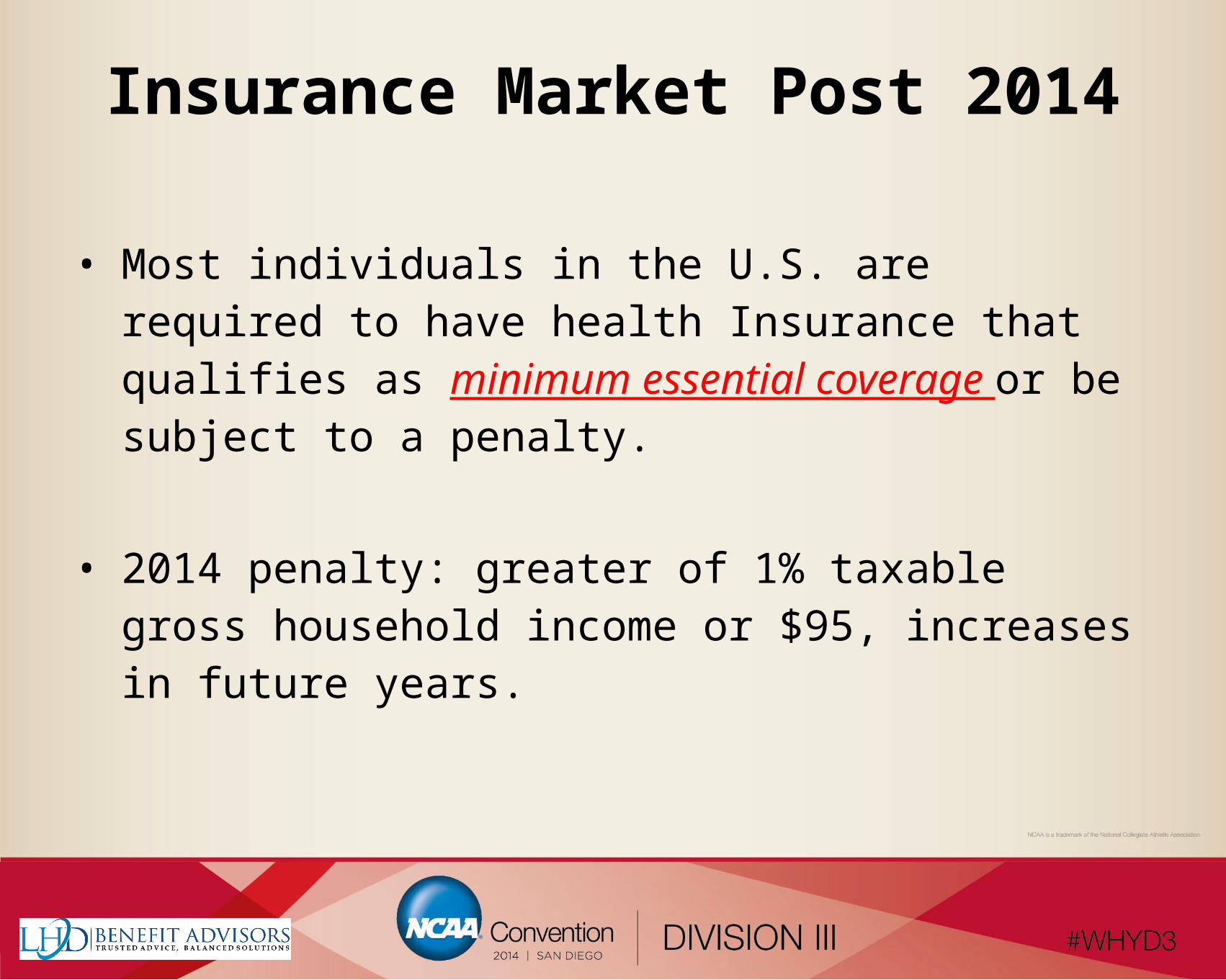

Insurance Market Post 2014

• Most individuals in the U.S. are required to have health Insurance that qualifies as minimum essential coverage or be subject to a penalty.

• 2014 penalty: greater of 1% taxable gross household income or $95, increases in future years.

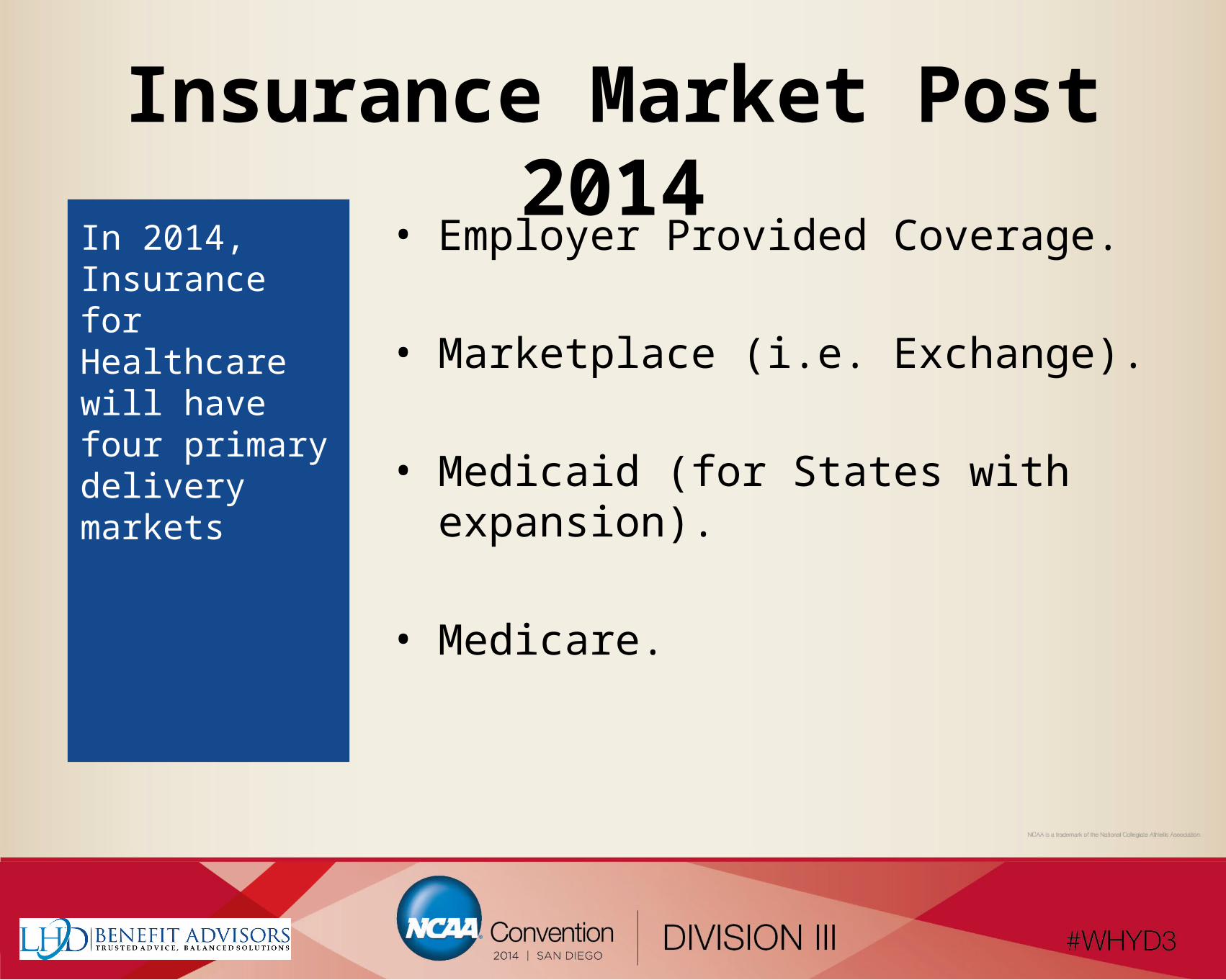

Insurance Market Post 2014

In 2014, Insurance for Healthcare will have four primary delivery markets

• Employer Provided Coverage.

• Marketplace (i.e. Exchange).

• Medicaid (for States with expansion).

• Medicare.

7

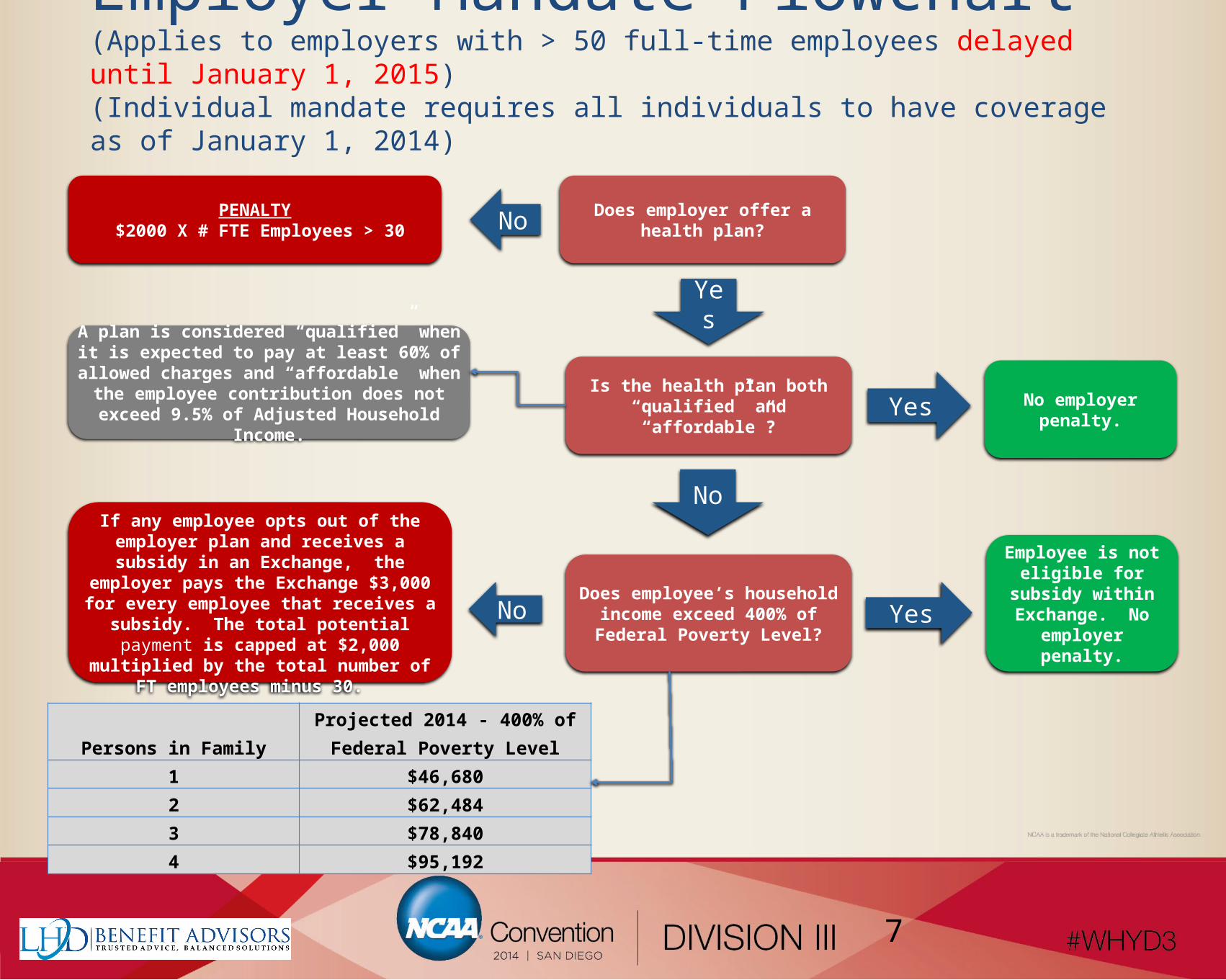

Employer Mandate Flowchart(Applies to employers with > 50 full-time employees delayed until January 1, 2015)(Individual mandate requires all individuals to have coverage as of January 1, 2014)

Persons in FamilyProjected 2014 - 400% of Federal

Poverty Level1 $46,6802 $62,4843 $78,8404 $95,192

Employee is not eligible for subsidy

within Exchange. No employer penalty.

No employer penalty.

Yes

Yes

Does employee’s household income exceed 400% of Federal Poverty

Level?

No

Is the health plan both “qualified” and “affordable”?

Yes

Does employer offer a health plan?PENALTY $2000 X # FTE Employees > 30 No

If any employee opts out of the employer plan and receives a subsidy in an Exchange, the employer

pays the Exchange $3,000 for every employee that receives a subsidy. The total potential payment is

capped at $2,000 multiplied by the total number of FT employees minus 30.

No

A plan is considered “qualified” when it is expected to pay at least 60% of allowed charges and “affordable”

when the employee contribution does not exceed 9.5% of Adjusted Household Income.

Insurance Market Post 2014:Employer Coverage

• Employers with over 50 employees are required to provide coverage or subject to penalties (delayed until 2015).

• Employer coverage must meet minimum standards and be affordable to avoid penalties (delayed until 2015).

The 30-Hour Dilemma

• defined under ACA as an average of 30 hours per week, or at least 130 hours in a month to be tracked and reported by employer.

• American Council on Education letter of March 18, 2013 to IRS requesting clarification on:– Student employees– Adjunct Faculty

• http://www.cupahr.org/advocacy/positions/ACE-Employer-Shared-Responsibility-Proposed-Regulations-03182013.pdf

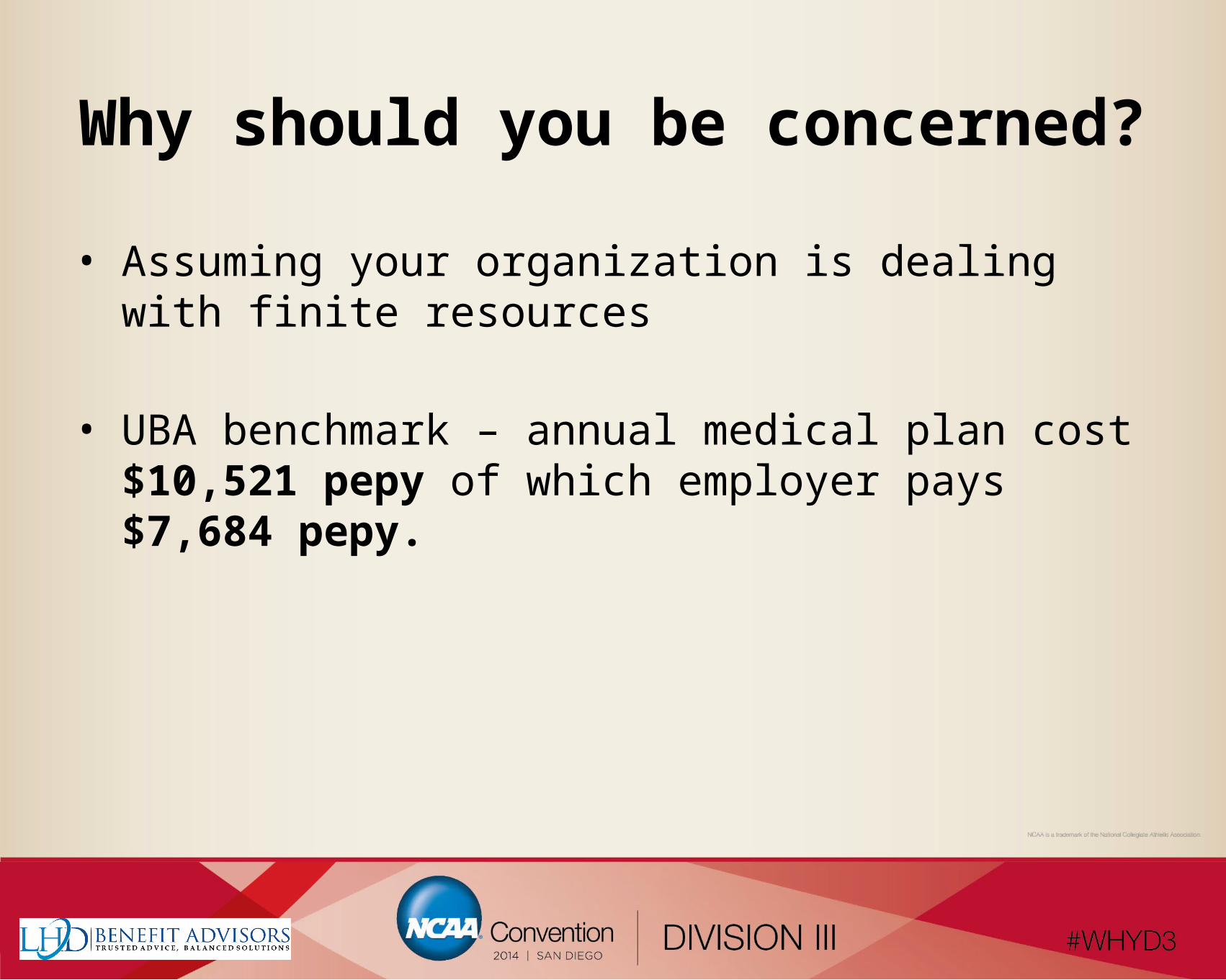

Why should you be concerned?

• Assuming your organization is dealing with finite resources

• UBA benchmark – annual medical plan cost $10,521 pepy of which employer pays $7,684 pepy.

Introduction to the Marketplace

• Marketplace, Exchange, “Obamacare”

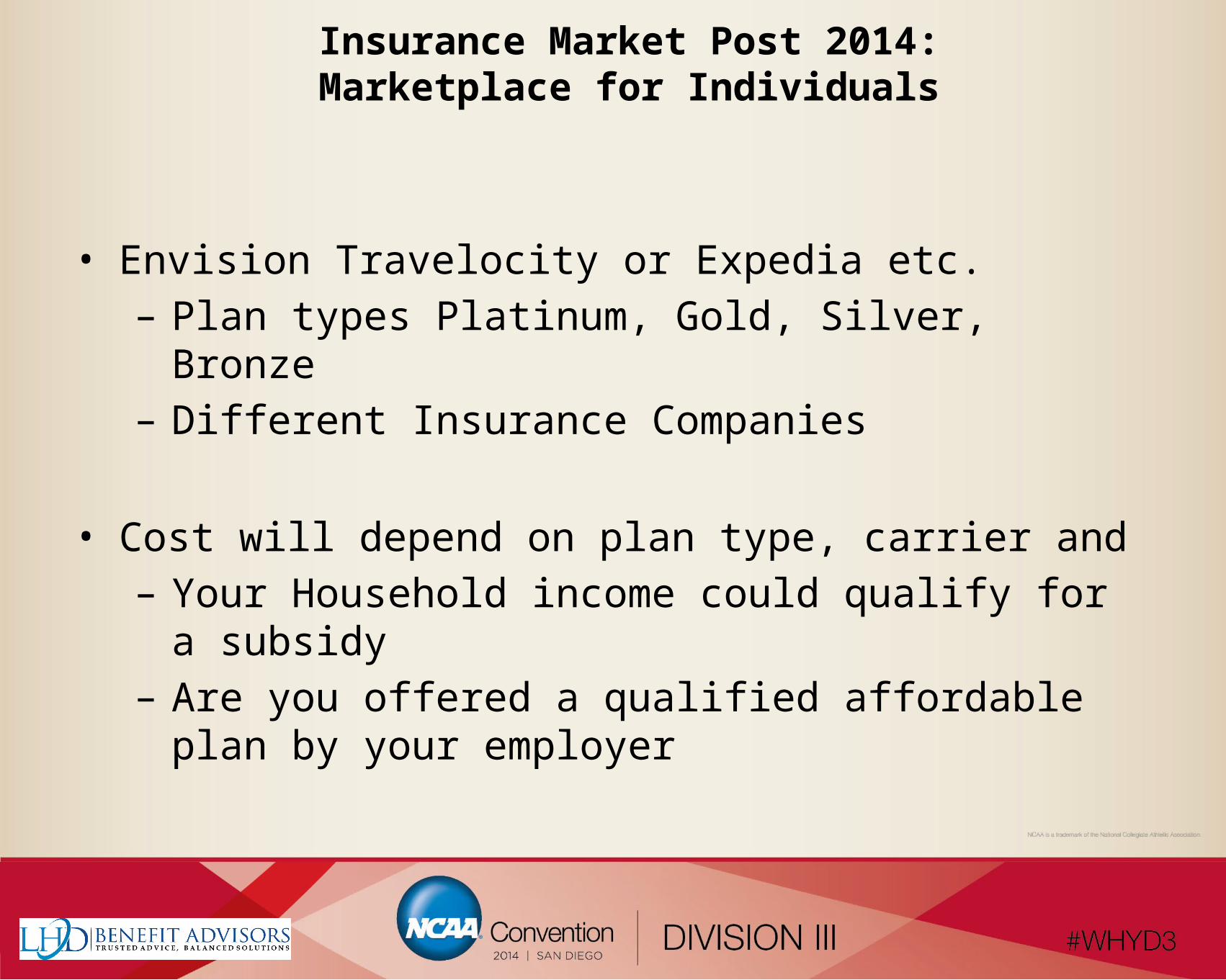

Insurance Market Post 2014:Marketplace for Individuals

• Envision Travelocity or Expedia etc.– Plan types Platinum, Gold, Silver, Bronze– Different Insurance Companies

• Cost will depend on plan type, carrier and– Your Household income could qualify for a subsidy – Are you offered a qualified affordable plan by your

employer

Insurance Market Post 2014:Marketplace for Individuals

• Eligible for subsidy if you are not offered a qualified affordable plan by your employer and your household income is below 400% of Federal Poverty Level.

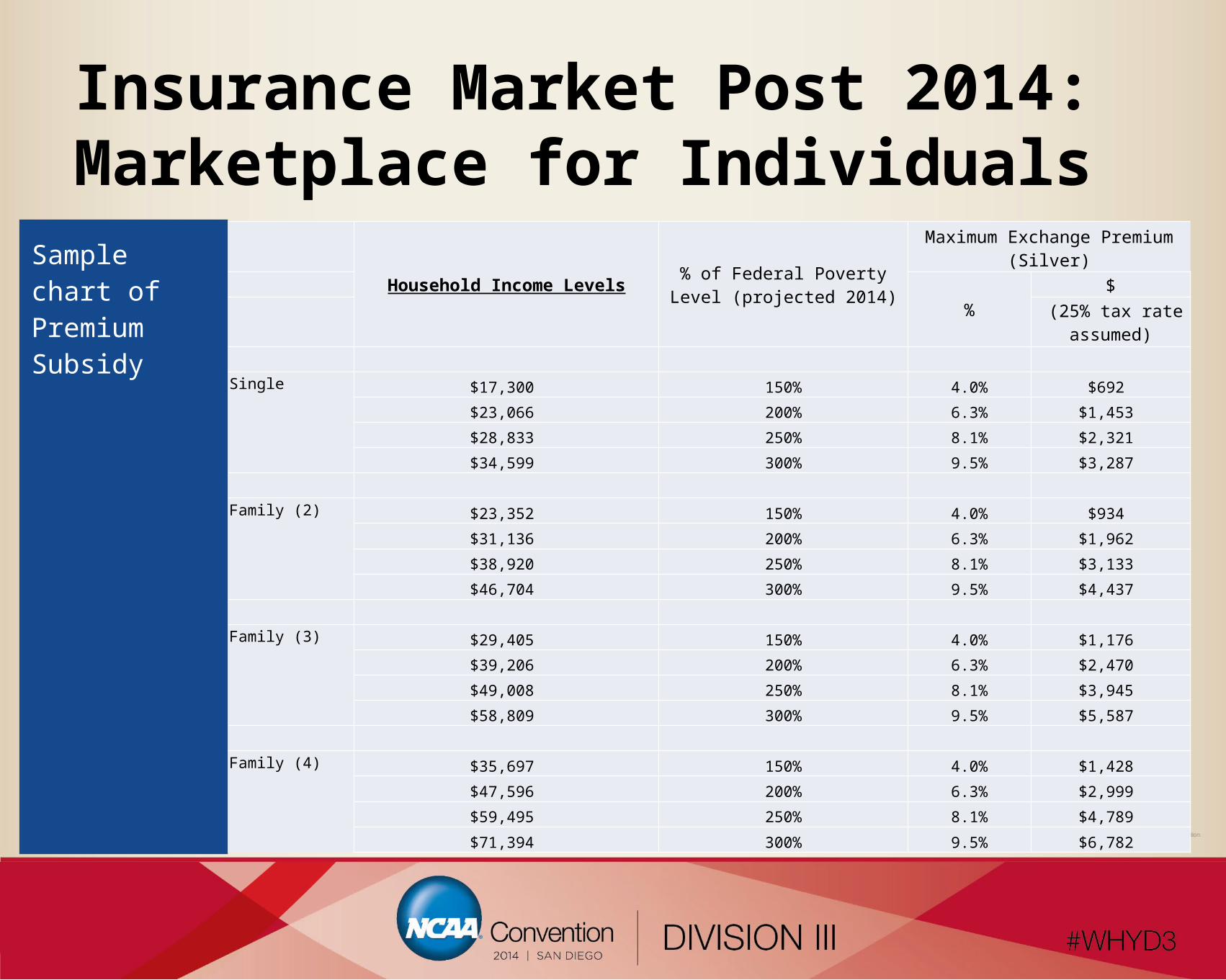

Insurance Market Post 2014:Marketplace for Individuals

Household Income Levels% of Federal Poverty Level

(projected 2014)

Maximum Exchange Premium (Silver)

%$

(25% tax rate assumed)

Single $17,300 150% 4.0% $692

$23,066 200% 6.3% $1,453

$28,833 250% 8.1% $2,321

$34,599 300% 9.5% $3,287

Family (2) $23,352 150% 4.0% $934

$31,136 200% 6.3% $1,962

$38,920 250% 8.1% $3,133

$46,704 300% 9.5% $4,437

Family (3) $29,405 150% 4.0% $1,176

$39,206 200% 6.3% $2,470

$49,008 250% 8.1% $3,945

$58,809 300% 9.5% $5,587

Family (4) $35,697 150% 4.0% $1,428

$47,596 200% 6.3% $2,999

$59,495 250% 8.1% $4,789

$71,394 300% 9.5% $6,782

Sample chart of Premium Subsidy

What next?

• May need to help your institutions “manage” eligibility for part time or adjunct staff (or understand the impact on institutional budgets).

• Define institutionally who owns this responsibility – limited H.R. staffs looking for help.

• Some institutions defining policies and procedures.