power division, mpemr - home page - gsep generation company of bangladesh (egcb) ashugonj power...

TRANSCRIPT

8-10 September 2009

Power Division, MPEMRPower Division, MPEMR

Present Structure of Power Sector

Generation Bangladesh Power Development Board (BPDB) Electricity generation Company of Bangladesh

(EGCB) Ashugonj Power Station Company Limited

(APSCL) North West Power Generation Company

Limited (NWPGC) IPPs

Present Structure of Power Sector

Transmission Power Grid Company of Bangladesh (PGCB)

Distribution Bangladesh Power Development Board (BPDB) Rural Electrification Board (REB) Dhaka Power Distribution Company (DPDC) Dhaka Electric Supply Company Ltd. (DESCO) West Zone Power Distribution Company (WZPDC) North West Power Distribution Company (NWPDC)

Installed capacity by owner basis and fuel basis for FY 2009

GAS83.4%

HYDRO4.0%

FO4.9%

DIESEL3.3%

COAL4.4%

GAS HYDRO FO DIESEL COAL

TOTAL INSTALLED CAPACITY 5719 MW

INSTALLED CAPACITY

PUBLIC 66.66%

PRIVATE33.34%

PUBLIC PRIVATE

TOTAL INSTALLED CAPACITY -5719 MW

INSTALLED CAPACITY

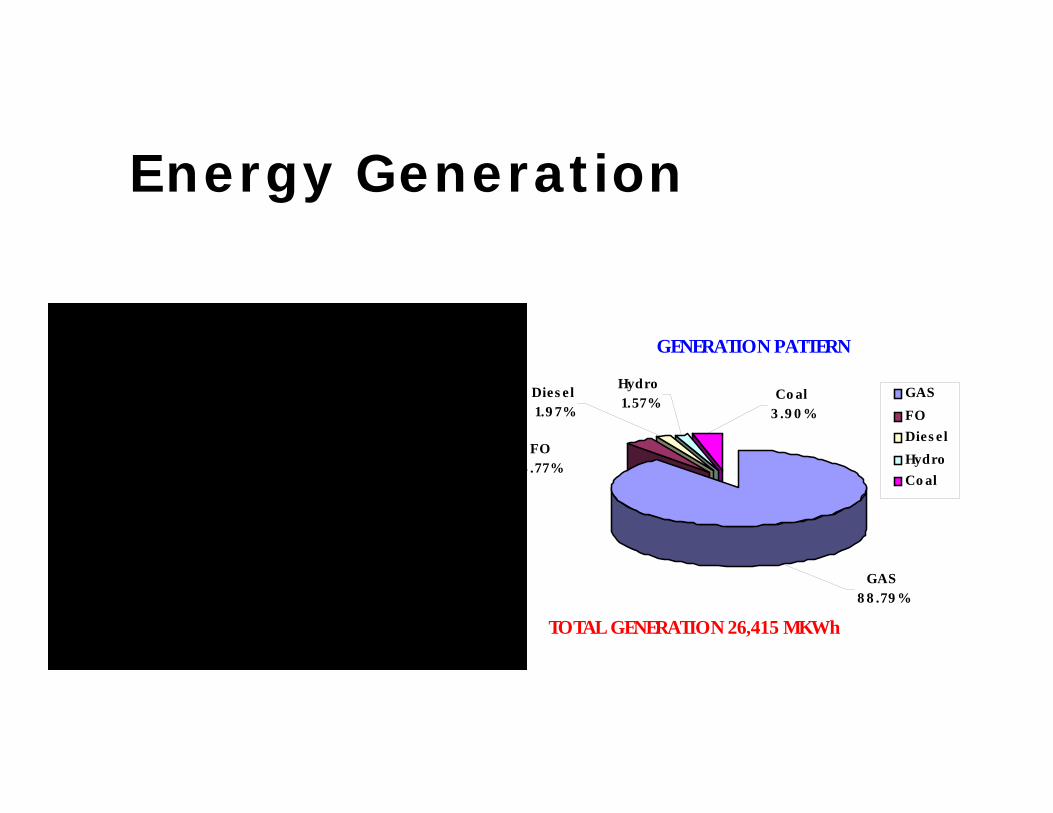

Energy Generation

GAS8 8 .79 %

Co al3 .9 0 %

Hydro1.57%

Dies el1.9 7%

FO3 .77%

GASFODies elHydroCo al

TOTAL GENERATION 26,415 MKWh

GENERATION PATTERN

PUBLIC58.49%

PRIVATE41.51%

PUBLIC

PRIVATE

TOTAL GENERATION 26415 MKWh

GENERATION PATTERN

Vision

- To make electricity available for all. - To ensure reliable and quality supply of electricity. - To provide electricity at a reasonable price.

Policy Objectives-Bringing entire country under electricity service by 2021. -Power sector financially viable able to facilitate economic growth. -Increasing the sectors efficiency.-Making the sector commercial. -Improving the reliability and quality of electricity supply. -Using coal, liquid fuel etc. as the primary fuel. -Increasing private sector participation to mobilize finance. -Increasing renewable energy such as solar, wind, micro-hydro, bio-mass etc.-Ensuring reasonable and affordable price for electricity by pursuing least cost options. -Promoting competition among various entities.

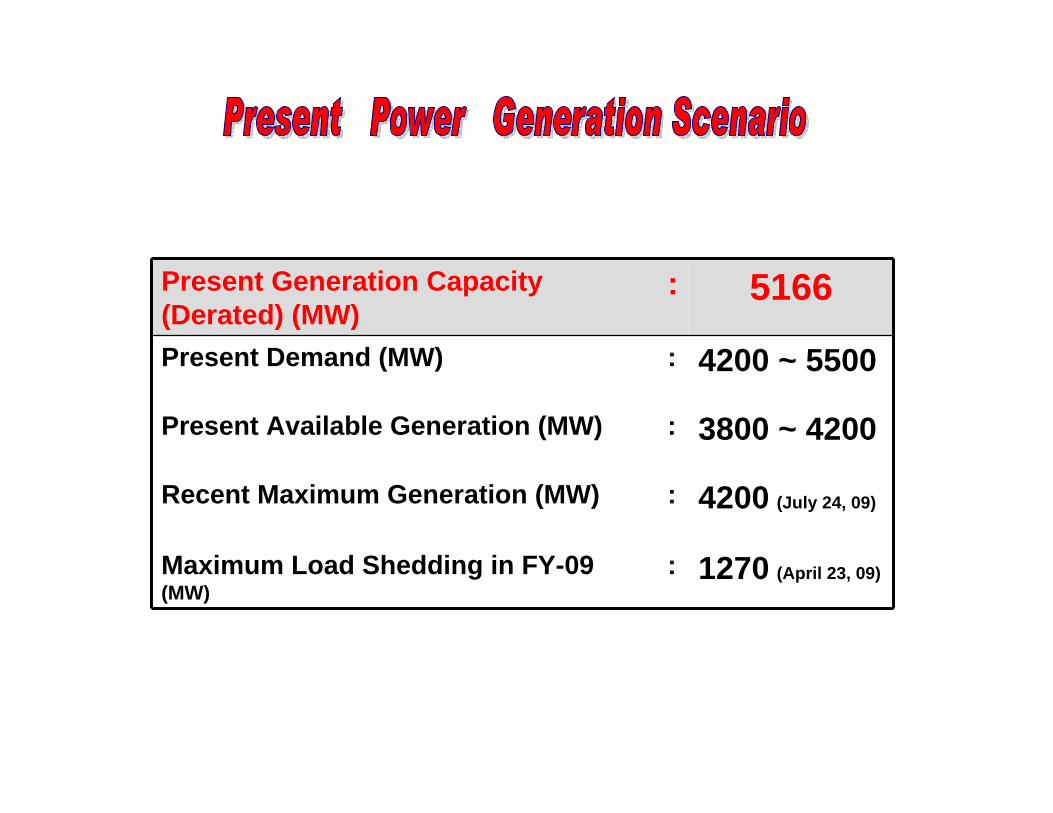

Present Generation Capacity (Derated) (MW)

: 5166

Present Demand (MW) : 4200 ~ 5500

Present Available Generation (MW) : 3800 ~ 4200

Recent Maximum Generation (MW) : 4200 (July 24, 09)

Maximum Load Shedding in FY-09 (MW)

: 1270 (April 23, 09)

Electricity Growth : 7.2 % in 2008 7.5 % Av. since 1990

Total Consumer : 11 Million (FY 2008)

Transmission Line : 8000 km Distribution Line : 2,56,000 km Distribution Loss : 14.7 % (FY 2008)

Per Capita Generation : 175 kWh / annum (FY 2008)

Access to Electricity : 45 % (FY 2008)

Key StatisticsKey Statistics

AshuganjAshuganj -- 724 MW724 MW

GhorasalGhorasal -- 950 MW950 MW

RaujanRaujan & & SikolbahaSikolbaha -- 508 MW508 MW

KaptaiKaptai -- 230 MW230 MW

BheramaraBheramara -- 60 MW60 MW

BaghabariBaghabari -- 261 MW261 MW

HaripurHaripur -- 569 MW569 MW

ShahjibazarShahjibazar & & FenchuganjFenchuganj-- 217 MW217 MW

Khulna Khulna -- 270 MW270 MW

SiddhirganjSiddhirganj -- 210MW210MW

MymensinghMymensingh -- 210 MW210 MW

BarapukuriaBarapukuria -- 250 MW250 MW

Barisal Barisal -- 440 MW0 MW

TongiTongi -- 105 MW105 MW

Public Sector : 480 MW Private Sector : 272 MW

Subtotal : 752 MW (Commissioning expected by Dec 2009)

UNDER CONSTRUCTION

Public Sector : 900 MW Private Sector : 450 MW

Subtotal : 1350 MW (Commissioning expected by FY11-FY13)

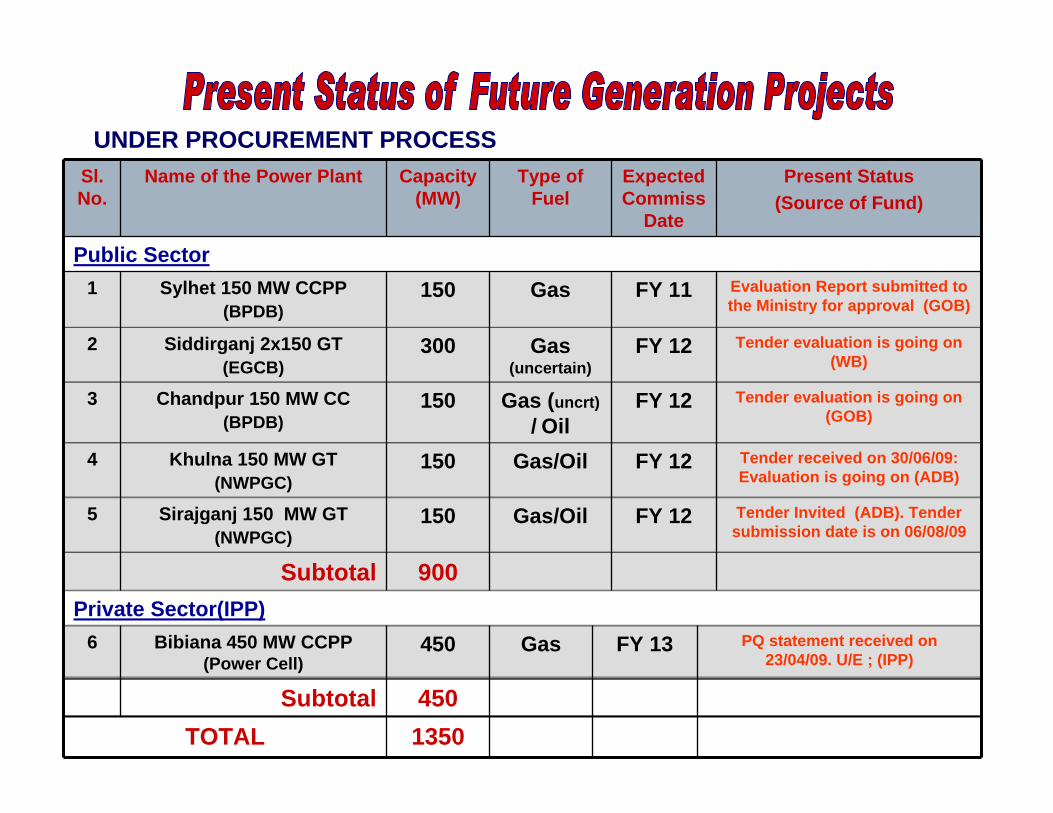

UNDER PROCUREMENT PROCESS

COMMITTED

Public Sector : 995 MW Private Sector : 450 MW

Subtotal : 1445 MW (Commissioning expected by FY13-FY14)

Total : 3547 MW

Sl. No.

Name of the Power Plant Capacity (MW)

Type of Fuel

Expected Commiss

Date

Present Status(Source of Fund)

Public Sector1 Sylhet 150 MW CCPP

(BPDB)150 Gas FY 11 Evaluation Report submitted to

the Ministry for approval (GOB)

2 Siddirganj 2x150 GT(EGCB)

300 Gas (uncertain)

FY 12 Tender evaluation is going on (WB)

3 Chandpur 150 MW CC(BPDB)

150 Gas (uncrt) / Oil

FY 12 Tender evaluation is going on (GOB)

4 Khulna 150 MW GT(NWPGC)

150 Gas/Oil FY 12 Tender received on 30/06/09: Evaluation is going on (ADB)

5 Sirajganj 150 MW GT(NWPGC)

150 Gas/Oil FY 12 Tender Invited (ADB). Tender submission date is on 06/08/09

Subtotal 900Private Sector(IPP)

6 Bibiana 450 MW CCPP(Power Cell)

450 Gas FY 13 PQ statement received on 23/04/09. U/E ; (IPP)

Subtotal 450TOTAL 1350

UNDER PROCUREMENT PROCESS

Sl. No.

Name of the Power Plant Capacity (MW)

Type of Fuel

Expected Commis. Date

Present Status(Source of Fund)

Public Sector1 Bhola 150 MW CCPP

(BPDB)150 Gas FY 13 Feasibility Study will

start soon; (IDB)

2 Barapukuria 125 MW Coal (3rd Unit) (BPDB)

125 Coal FY 13 Under Process; (GOB)PDPP in Planning Comm.

3 Haripur 360 MW CCPP(EGCB)

360 Gas (uncertain)

FY 14 Loan Agreement signed. Doc Under Preparation;

(JICA)

4 Bheramara 360 MW CCPP(NWPGC)

360 Gas (uncertain)

FY 14 Feasibility Completed. LA yet to be signed; (JICA)

Subtotal 995Private Sector (IPP)

5 Serajganj 450 MW CCPP/ 500 MW Coal (Power Cell)

450 Gas (uncrt) / Coal

FY 13 PQ Invitation soon ;(IPP)

Subtotal 450TOTAL 1445

COMMITTED

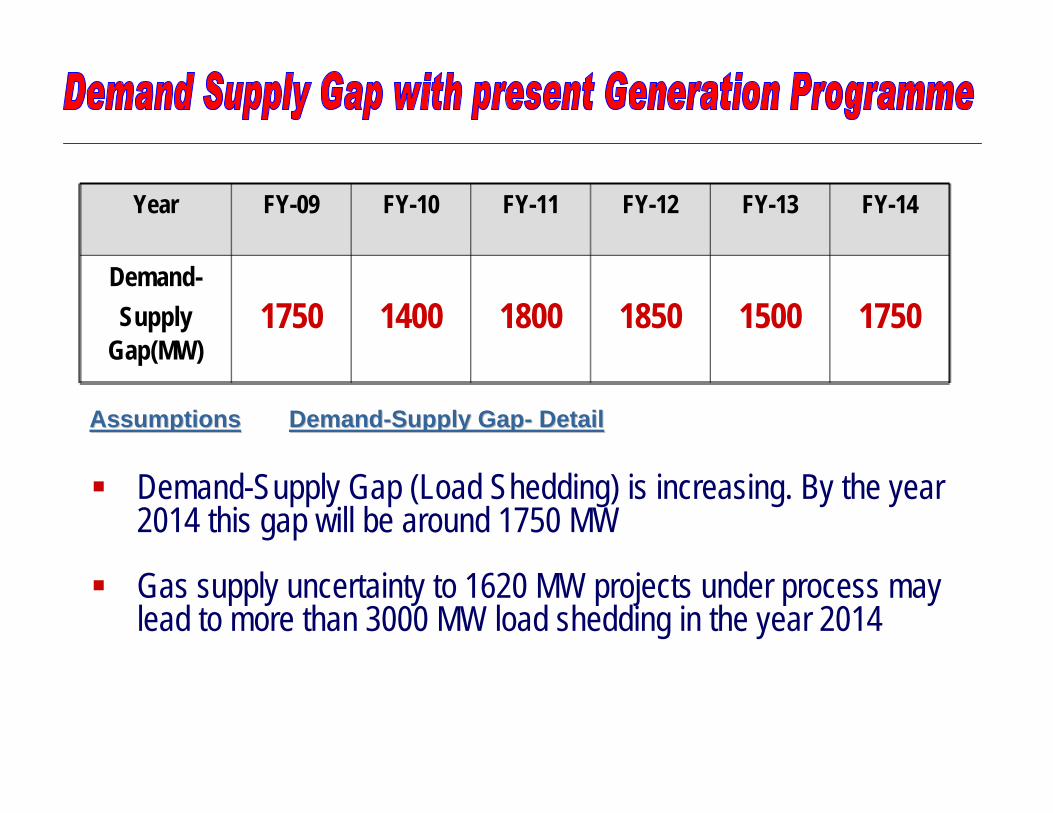

Year FY-09 FY-10 FY-11 FY-12 FY-13 FY-14

Demand-Supply

Gap(MW)1750 1400 1800 1850 1500 1750

Demand-Supply Gap (Load Shedding) is increasing. By the year 2014 this gap will be around 1750 MW

Gas supply uncertainty to 1620 MW projects under process may lead to more than 3000 MW load shedding in the year 2014

AssumptionsAssumptions DemandDemand--Supply GapSupply Gap-- DetailDetail

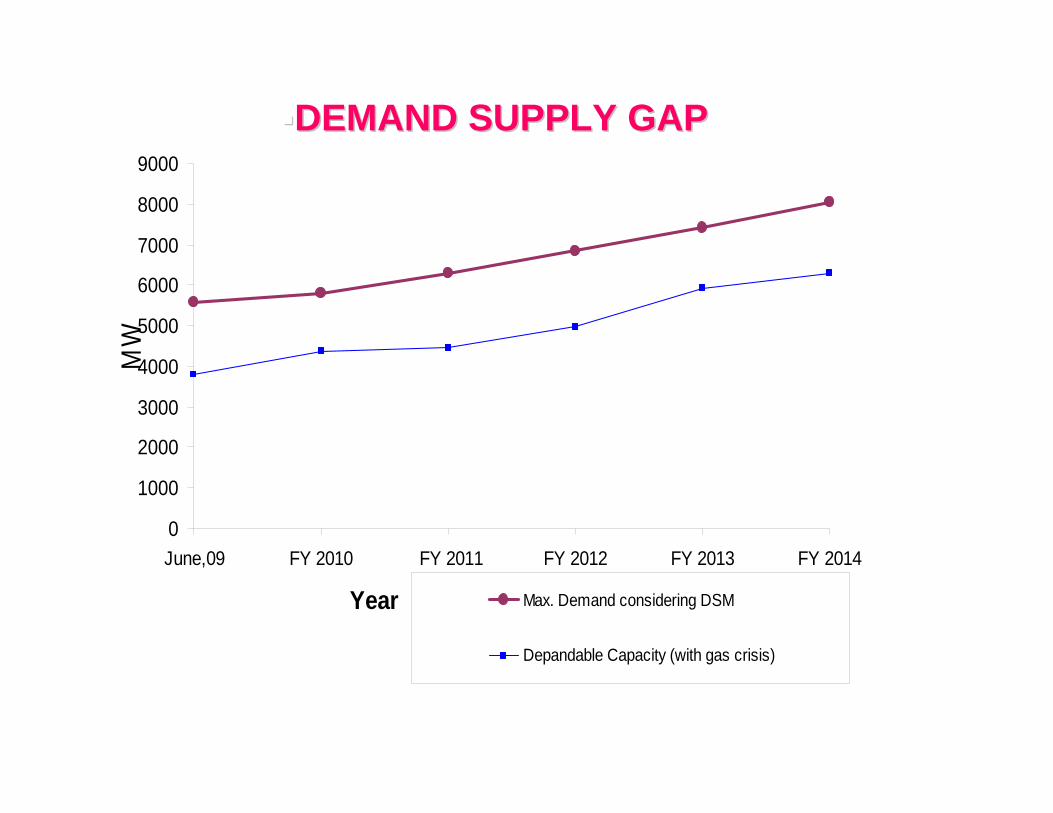

DEMAND SUPPLY GAPDEMAND SUPPLY GAP

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

June,09 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014

Year

MW

Max. Demand considering DSM

Depandable Capacity (with gas crisis)

GAS

COAL

PRIVATE GEN.

HydroOIL

SHORTAGE

0

500

1000

1500

2000

2500

3000

3500

4000

4500

0:00

1:00

2:00

3:00

4:00

5:00

6:00

7:00

8:00

9:00

10:00

11:00

12:00

13:00

14:00

15:00

16:00

17:00

18:00

19:00

20:00

21:00

22:00

23:00

24:00

Hour

MW

GAS COAL PRIVATE GEN. Hydro OIL SHORTAGE

4162 MW4162 MW

Peak LoadPeak Load

Base LoadBase Load

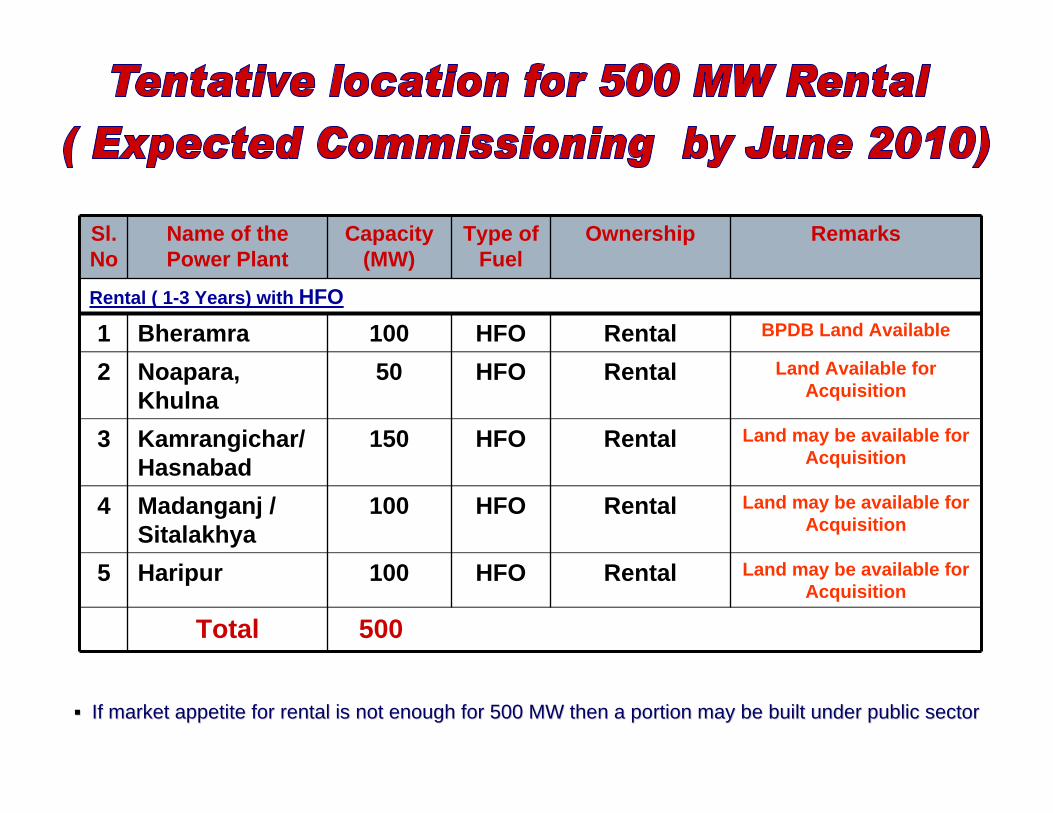

Immediate: 6-12 Months- Rental Plants: 500-1500 MW- Per unit cost: Tk 10 (FO) / Tk 16 (Diesel)

Short term: 18-24 Months- Peaking Plants: 800 MW - Per unit cost: Tk 8

Medium term: 4-5 years- Base plants: 4X500 MW Coal- Per unit cost: Tk 3.5

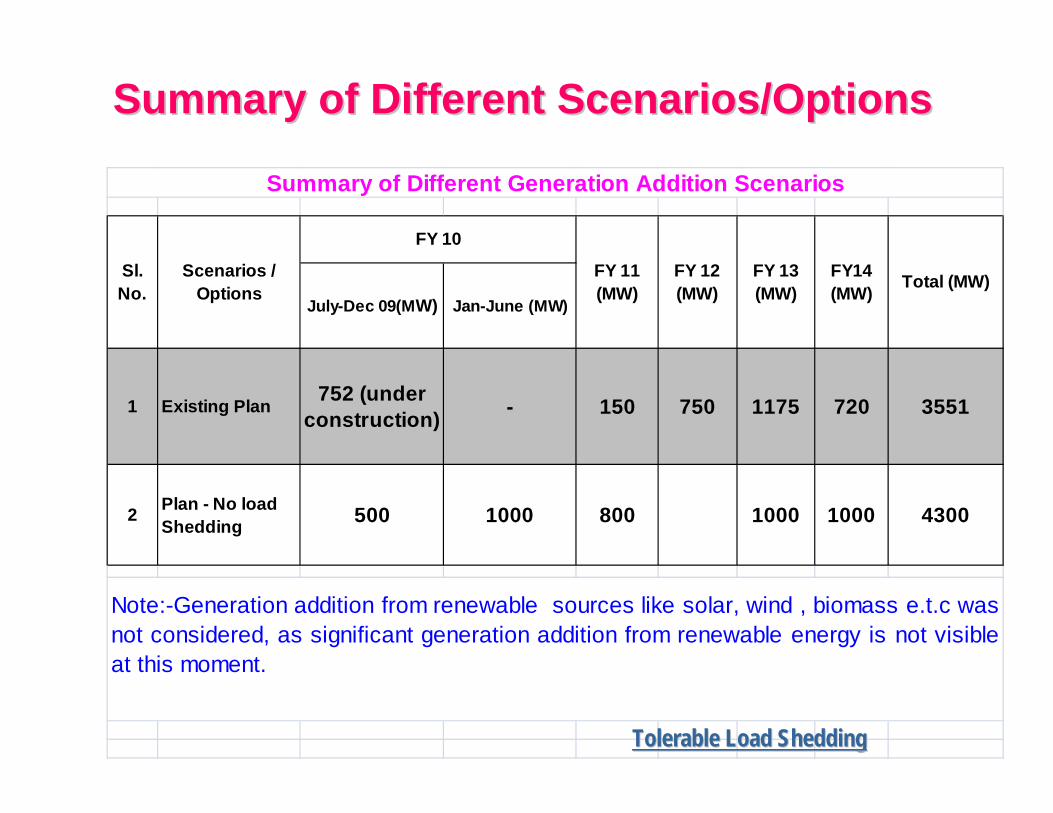

Summary of Different Scenarios/OptionsSummary of Different Scenarios/Options

July-Dec 09(MW) Jan-June (MW)

1 Existing Plan 752 (under construction) - 150 750 1175 720 3551

2 Plan - No load Shedding 500 1000 800 1000 1000 4300

Note:-Generation addition from renewable sources like solar, wind , biomass e.t.c wasnot considered, as significant generation addition from renewable energy is not visibleat this moment.

FY 13 (MW)

FY14 (MW) Total (MW)

Summary of Different Generation Addition Scenarios

Scenarios / Options

FY 10

Sl. No.

FY 11 (MW)

FY 12 (MW)

Tolerable Load SheddingTolerable Load Shedding

Renewable Energy Policy (2008)- 5 % of total generation by 2015 : 450 MW- 10 % of total generation by 2020 : 1600 MW

Hydro: small hydro potential exists; limited scope

Wind: At least 200 MW wind by 2013

Solar: Existing Capacity: 15 MW – 20 MW- Need at least 80 – 100 MW by 2013- Still high cost ; off grid solution; may compete with oil

Renewable will help in mitigating balance deficit

Fuel cost of HFO ‘Rental’ : 50 % cheaper than HSD

Per unit cost of HFO ‘Rental’: 35 % cheaper than HSD

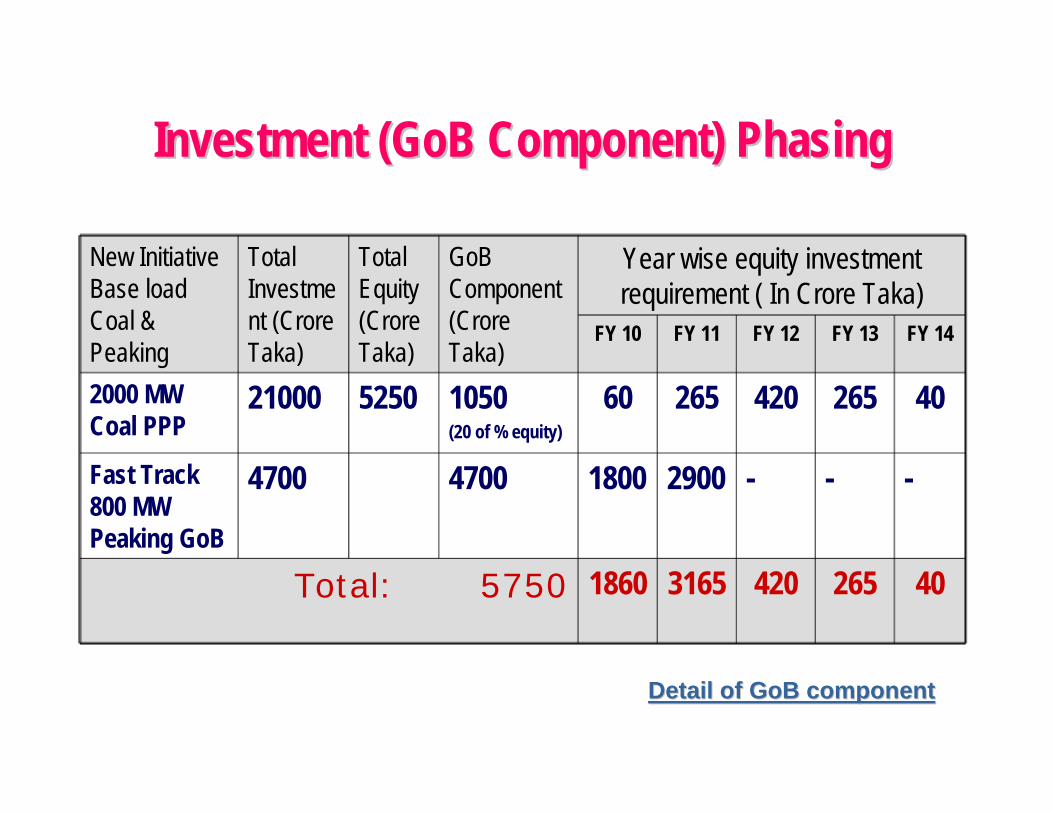

New Initiative Base load Coal & Peaking

Total Investment (CroreTaka)

Total Equity (CroreTaka)

GoBComponent (CroreTaka)

Year wise equity investment requirement ( In Crore Taka)

FY 10 FY 11 FY 12 FY 13 FY 14

2000 MW Coal PPP

21000 5250 1050 (20 of % equity)

60 265 420 265 40

Fast Track 800 MW Peaking GoB

4700 4700 1800 2900 - - -

Total: 5750 1860 3165 420 265 40

Investment (Investment (GoBGoB Component) PhasingComponent) Phasing

Detail of Detail of GoBGoB componentcomponent

Sl. No

Name of the Power Plant

Capacity (MW)

Type of Fuel

Ownership Remarks

Rental ( 1-3 Years) with HFO

1 Bheramra 100 HFO Rental BPDB Land Available

2 Noapara, Khulna

50 HFO Rental Land Available for Acquisition

3 Kamrangichar/ Hasnabad

150 HFO Rental Land may be available for Acquisition

4 Madanganj / Sitalakhya

100 HFO Rental Land may be available for Acquisition

5 Haripur 100 HFO Rental Land may be available for Acquisition

Total 500

If market appetite for rental is not enough for 500 MW then a poIf market appetite for rental is not enough for 500 MW then a portion may be built under public sectorrtion may be built under public sector

Sl. No.

Name of the Power Plant Capacity (MW)

Type of Fuel

Ownership Remarks

Peaking 800 MW (Public Sector)

1 Katakhali, Rajshahi 100 HFO BPDB BPDB Land Available

2 Dohazari, Chittgong 100 HFO BPDB BPDB Land Available

3 Thakurgaon 50 HFO BPDB BPDB Land Available

4 Cox’s Bazar 50 HFO BPDB BPDB Land Available

5 Gopalganj 50 HFO BPDB Land Available for Acquisition

6 Faridpur 50 HFO BPDB Land Available for Acquisition

7 Nawgaon 50 HFO BPDB Land Available for Acquisition

8 Bera/Baghabari 50 HFO Rental Land Available for Acquisition

9 Khulna South 100 HFO BPDB Land Available for Acquisition

10 Ashuganj / Ghorasal 200 Gas/Oil BPDB BPDB Land Available

Total 800 MW

Considering gas supply situation, 200 MW gas based Peaking PlaConsidering gas supply situation, 200 MW gas based Peaking Plant be considered in nt be considered in SylhetSylhet Mixed fuel (Gas/FO) based 400 Combined Cycle be considered at Mixed fuel (Gas/FO) based 400 Combined Cycle be considered at SirajganjSirajganj/ / MeghnaghatMeghnaghat

Sl. No.

Name of the Power Plant

Capacity (MW)

Type of Fuel

Ownership Remarks

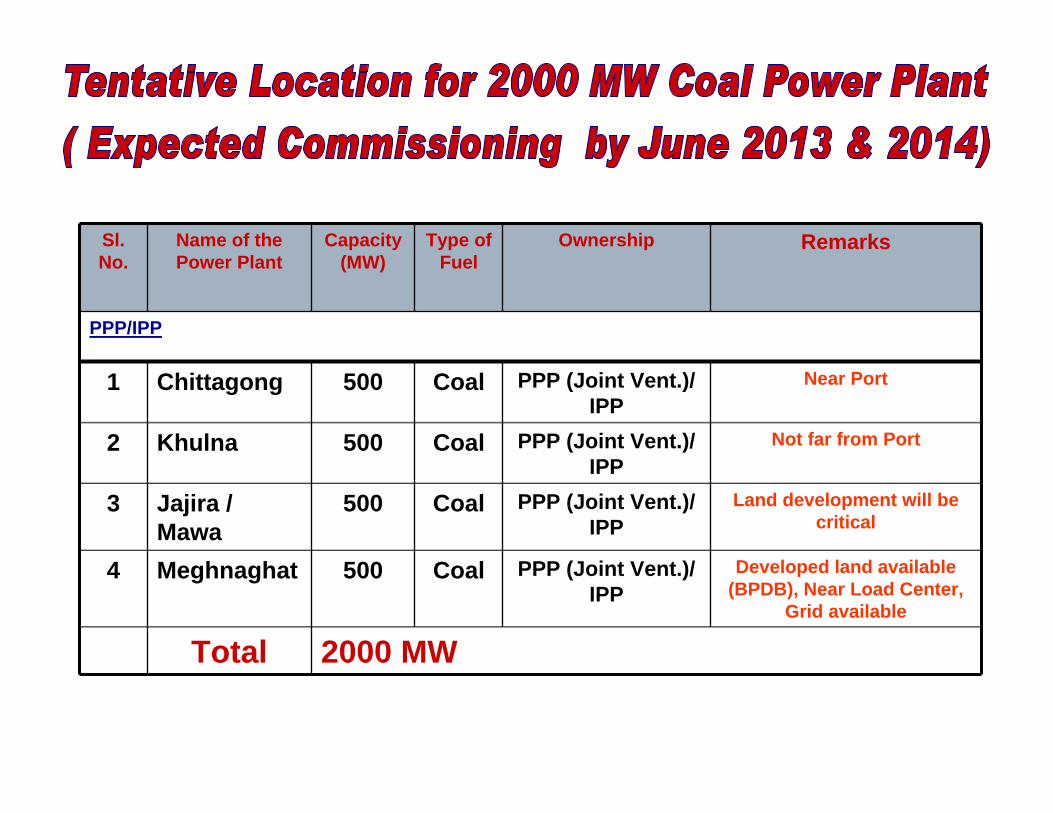

PPP/IPP

1 Chittagong 500 Coal PPP (Joint Vent.)/ IPP

Near Port

2 Khulna 500 Coal PPP (Joint Vent.)/ IPP

Not far from Port

3 Jajira / Mawa

500 Coal PPP (Joint Vent.)/ IPP

Land development will be critical

4 Meghnaghat 500 Coal PPP (Joint Vent.)/ IPP

Developed land available (BPDB), Near Load Center,

Grid available

Total 2000 MW

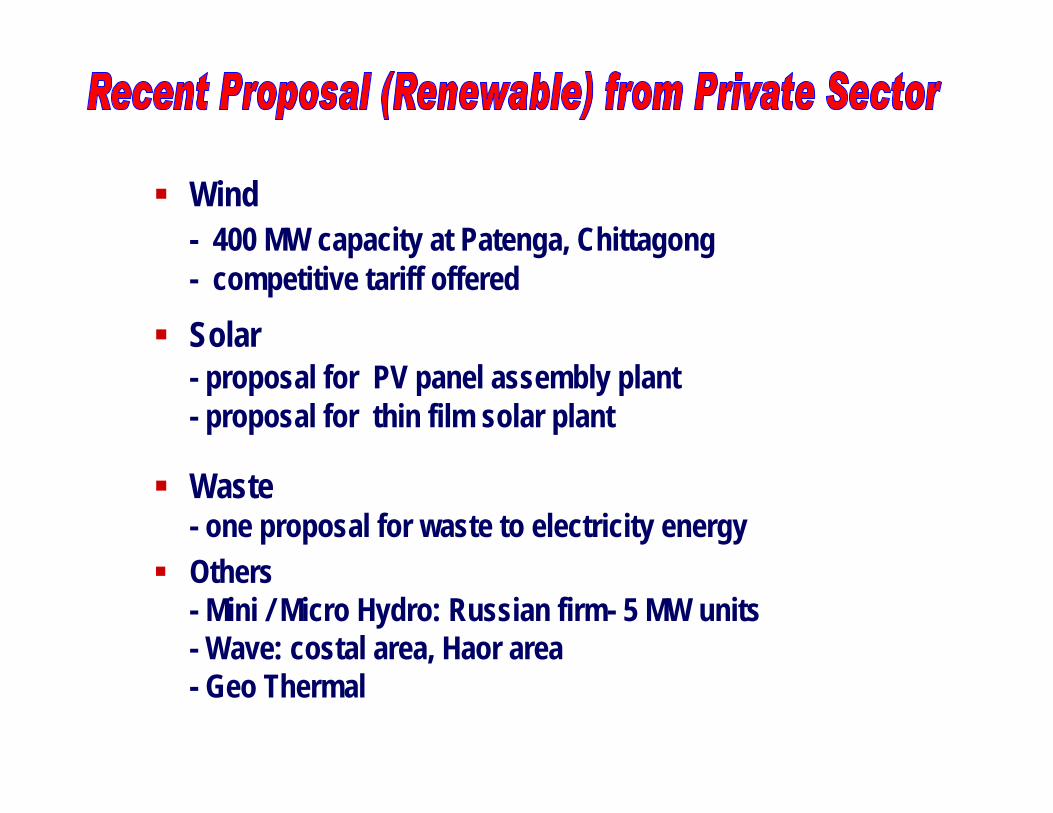

Wind- 400 MW capacity at Patenga, Chittagong - competitive tariff offered

Solar- proposal for PV panel assembly plant- proposal for thin film solar plant

Waste- one proposal for waste to electricity energy

Others- Mini / Micro Hydro: Russian firm- 5 MW units- Wave: costal area, Haor area- Geo Thermal

Tripura, India- Import offer from Tripura 740 MW Gas Power Plant

West Bengal, India- 250 / 500 MW from Bahrampur, West Bengal

Assam, India- Hydro Power from North East India

Bhutan- Hydro Power though SAARC Grid

Estimated Total Investment Cost ( During 5 Year)Estimated Total Investment Cost ( During 5 Year)

Generation : 30,000 Crore Taka (US$ 428 M)

Transmission : 4,000 Crore Taka (US$ 57M)

Distribution : 7,000 Crore Taka (US$ 100M)

Total : 41,000 Crore Taka (US$ 585M)

Balanced expansion and up gradation of Transmission and Distribution with Generation Expansion Plan will improve overall power supply situation and thereby help economic and social development of the country

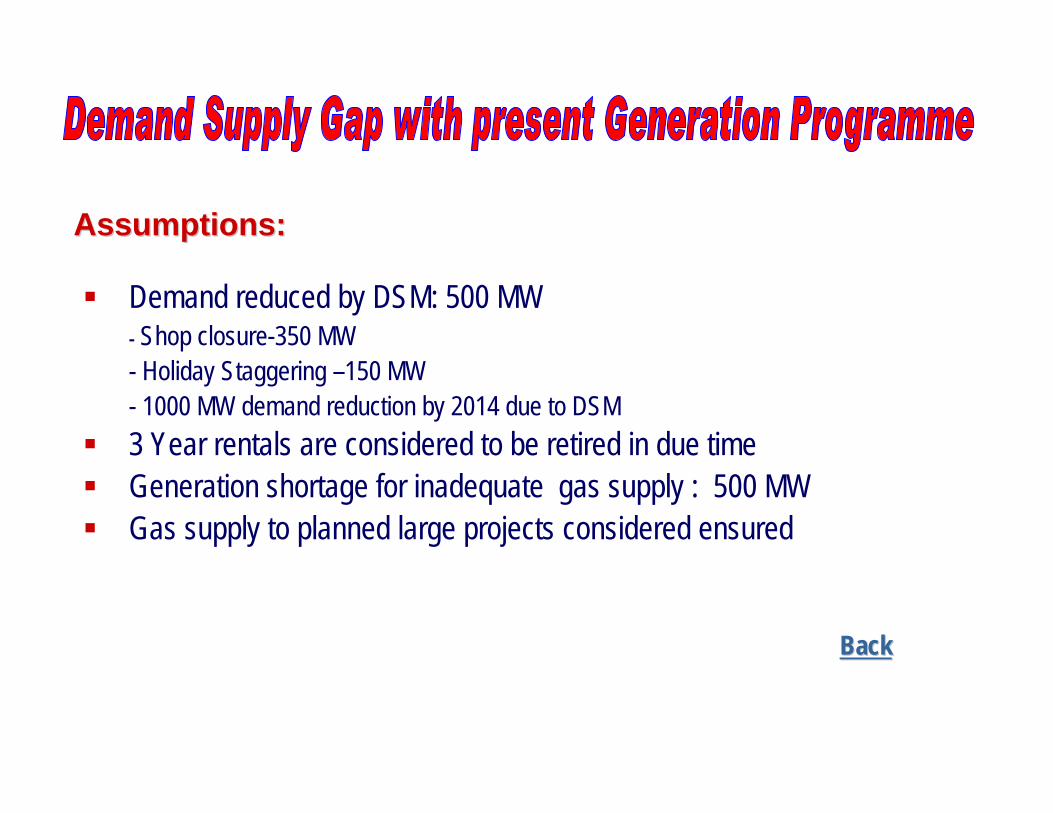

Assumptions:Assumptions:

Demand reduced by DSM: 500 MW- Shop closure-350 MW- Holiday Staggering –150 MW- 1000 MW demand reduction by 2014 due to DSM

3 Year rentals are considered to be retired in due time Generation shortage for inadequate gas supply : 500 MW Gas supply to planned large projects considered ensured

BackBack

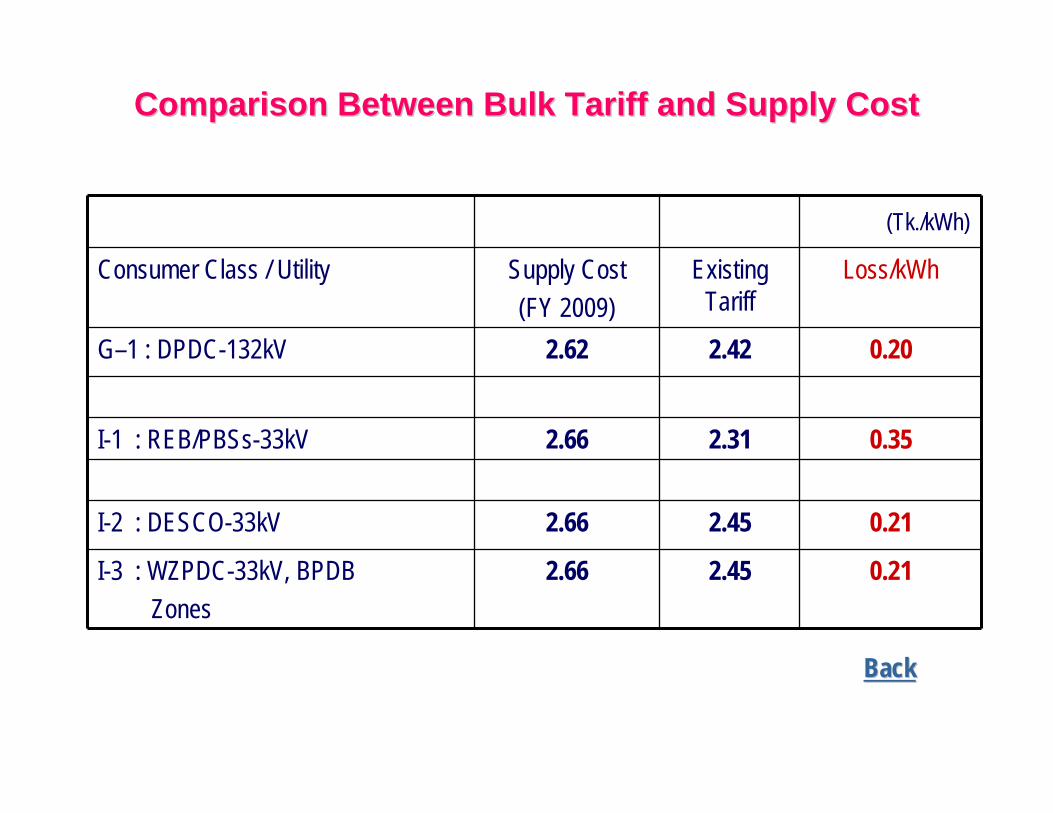

Comparison Between Bulk Tariff and Supply CostComparison Between Bulk Tariff and Supply Cost

Consumer Class / Utility Supply Cost (FY 2009)

Existing Tariff

Loss/kWh

G–1 : DPDC-132kV 2.62 2.42 0.20

I-1 : REB/PBSs-33kV 2.66 2.31 0.35

I-2 : DESCO-33kV 2.66 2.45 0.21

I-3 : WZPDC-33kV, BPDB Zones

2.66 2.45 0.21

(Tk./kWh)

BackBack

Strategies & Constraints and Possibilities of the Power Sector Strategy

-To diversify the use of primary fuel such as gas, coal, liquid fuel etc. will be used for power generation. -To have provision for dual fuel in power plants whereas possible. -To increase power generation through renewable sources e.g solar, wind, Micro hydro etc.-To implement nuclear fuel based power plant.-To finance power generation projects through Public –-Private Partnership (PPP), GOB funding, IPP etc. To increase the sector efficiency, the reform measures will be implemented.

Challenges:

-To install adequate generation, transmission and distribution facilities to meet the demand reliably-To augment and diversify of fuel supply- Reduce dependancy on fast deplting gas-To secure adequate financing for power system expansion-To improve efficiency in the performance of the utilities and set adequate tariff to recover costs -To make the utilities financially viable

OPPORTUNITIES

Fast growing economy(6% GDP in 2008)

Lucrative incentive package: 100% investment and income repatriation

Huge potential for Solar Upcoming 2000 MW coal fired power

plant in the process..

Key actions required

Promote investment friendly environment

Create transparent bidding process Gas excavation initiative National energy policy Enhance renewable policy

Key actors involved

Ministry of Power Parliament Sub-Committee Domestic Private Banks Foreign financiers

Timeline:

Enact Energy Policy by Dec 2009 Arrange meeting with stakeholders by Dec 2009

Areas where assistance needed

Expert power project evaluation High level Government engagement Creation of a ministry of Renewable

Resources

Key contact

M.Mosharraf Hossain Bhuyian ndcAddl. Secretary: Economic Relations

Division..MoF Bangladesh

Thanks again!!

Bhutan Presentation

Background

Development Philosophy of ‘Gross National Happiness’ Bhutan has a population of approx 6,30,000 people with an

area of 38394 sq. km and follows Gross National Happiness (GNH) as its Development Policy

One of the four pillars of GNH is ‘Sustainable and Equitable Economic Development’.

Energy Sector plays a major role in Economic Development of Bhutan.

Hydropower/Green Energy is the main source of energy, with an installed capacity of 1500 MW and a target to install 10, 000 MWby 2020.

Another pillar of GNH is ‘Conservation of the Environment’ and Bhutan is focusing mainly on Green Energy

Endorsement of the Minutes of the 1st Board Audit Committee Meeting of BPC held on 7th August, 2008.

Rural Electrification Highlights1. CDM Project at Chendebji The e7 funded the 70 kW Chendebji Clean Development

Mechanism (CDM) Micro Hydropower Project in Bhutan in 2005 in order to contribute to the sustainable development of the un-electrified village and lighting up around 50 Households, a Health Unit and a school in Chendebji village. E7 facilitated the purchase of rice cookers and water boilers for each household in the village.

2. The project is handed over to the Local Community 3. Distribution of CFL light bulbs in Bumthang and Trongsa towns

by the power utility corporation.

Current Obstacles and Challenges

1. Financial Capacity No financial and execution capacity to carry out the major

projects (to achieve the target of 10, 000 MW by 2020). Require approx. 12 billion dollars but adequate fund not

available locally Projects are mainly executed bilaterally with India.

2. Sustainable Rural Electrification RE goal of providing electricity to all by 2013 Due to geographical conditions, it is too expensive and cost of

electrification per Household is approx. USD 5000.

Current Obstacles and Challenges

Transportation of heavy equipment (transformers) to remote sites

Tariff not sustainable for Rural Electrification- no affordability Rural Electrification in Bhutan not attractive to private

investors but could be attractive to e8, ADB since it would givea high ERR.

No Policies or laws for RE. Huge investment into the RE by the Power Utility (BPC) which

would be difficult gain back due to subsidized domestic tariffs. Therefore, not sustainable to BPC.

Subsidy element not very clear Huge costs involved in maintaining the large transmission

structure

Current Obstacles and Challenges

The national policy of preserving the environment also acts a constraint while carrying out RE.

Off-Grid energy (Solar) not preferred by consumers.3. Revenue from hydro export to India is nullified by the

expenditure in fossil fuel import. Huge dependence on fossil fuel import.

4. Deforestation due to RE works5. Threat of Glacial Lake Outburst Flood (GLOF) due to global

warming

Opportunities

Rural Electrification1. Positive Socio-economic Impact after completion of RE works2. Off-grid opportunities by Mini, Micro hydro and Solar energy3. CDM and Environment conservation4. Poverty alleviation in terms of improved health , education,

flourishing cottage industries. Remote villages will open up to tourism.

5. Encourage and promote Clean Industries (Tourism, ICT, Data Centers)

Hydro Sector1. Balance of Payment

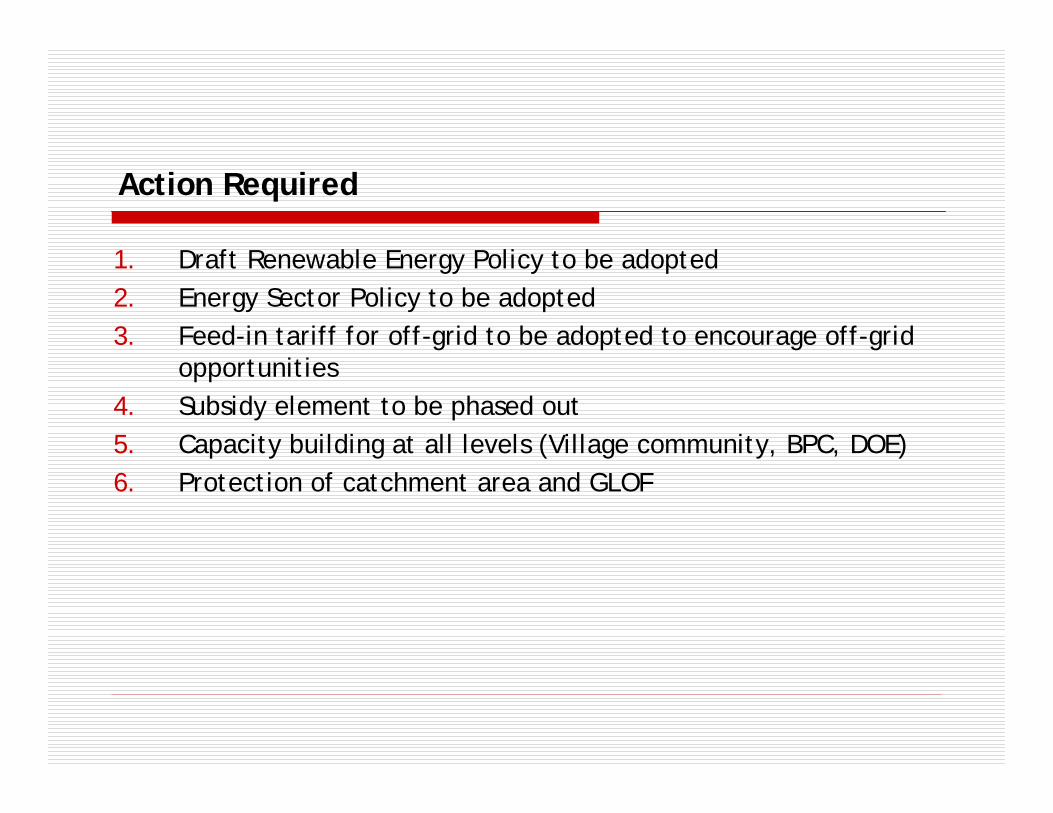

Action Required

1. Draft Renewable Energy Policy to be adopted2. Energy Sector Policy to be adopted3. Feed-in tariff for off-grid to be adopted to encourage off-grid

opportunities4. Subsidy element to be phased out5. Capacity building at all levels (Village community, BPC, DOE)6. Protection of catchment area and GLOF

Timeline1. 40, 000 HHs to be electrified by 20132. Additional 10, 000 MW by 20203. Energy Policy by December 20094. Economic Development Policy by December 20095. Revised FDI policy for Indirect Investment by June 20106. Renewable Energy Policy - ?7. Subsidy phase out by 20138. Provide employment for 10, 000 Bhutanese over the next 12

years9. Maintain GDP rate at 8%-9%.10. Poverty alleviation- reduce to 27% by 201311. Diversification to Wind and Solar Energy – Plan to be put up by

2013

Timeline12. Completion of the East-West National Grid by 2012

Areas where Assistance is needed:1. Financing for RE2. Capacity Building-HR and technical, at different levels3. Setting up micro and mini hydro and off-grid projects4. Diversification into Renewable Energy such as Solar and

Wind

THANK YOU

Development of Geothermal Power Plan in Indonesia

Bangkok, 10 September2009

1

ELECTRICITY PROVISION STATUSELECTRICITY PROVISION STATUSELECTRICITY PROVISION STATUS

Electrification ratio: 65.1% and rural electrified ratio 92.2% Composition of primary energy for power generation

utilization:Geothermal

3%

Coal39%

Oil30%

Hydro8%

Gas20%

Electricity System: Interconnected system: Java-Madura-Bali and

Sumatera Island The rest is still isolated system

Growth rate of demand for electricity: 6.9% p.aand 9.2% p.a (projection for up to 2027)

Total installed capacity 30. 504 MW :PLN25.315 83%

IPP4.269 14%

PPU920 3%

MW MW

MW

2

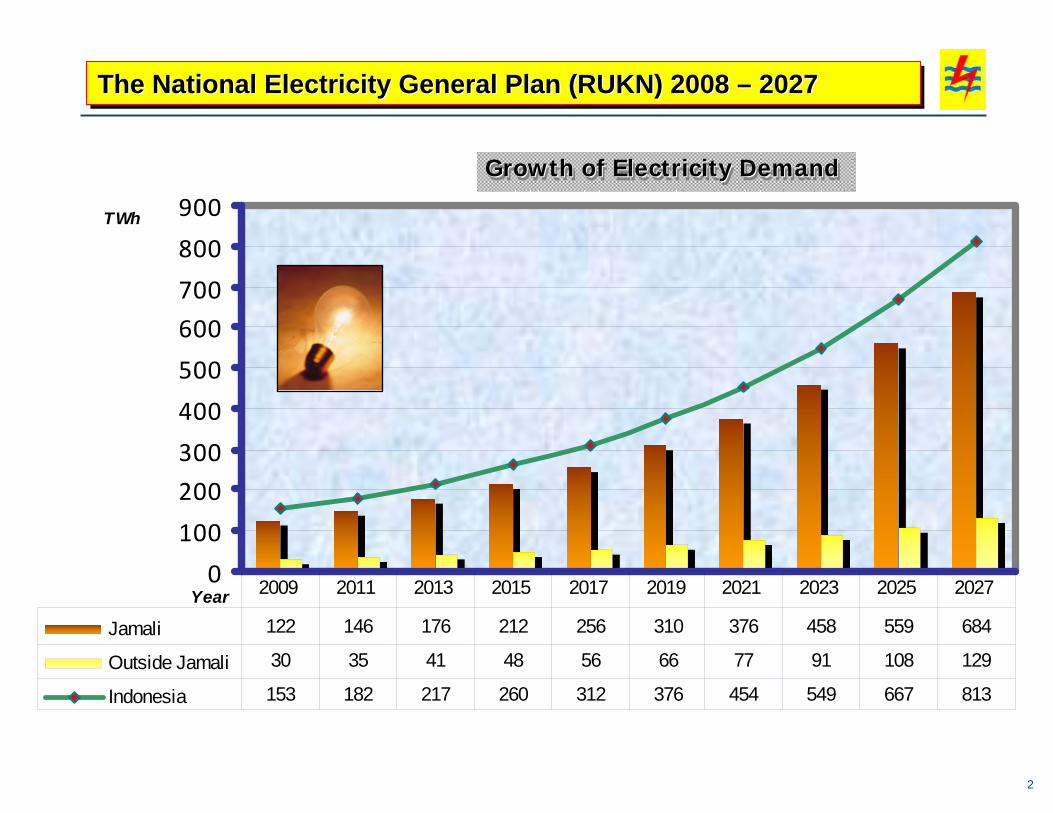

0

100

200

300

400

500

600

700

800

900

Year

TWh

Jamali 122 146 176 212 256 310 376 458 559 684

Outside Jamali 30 35 41 48 56 66 77 91 108 129

Indonesia 153 182 217 260 312 376 454 549 667 813

2009 2011 2013 2015 2017 2019 2021 2023 2025 2027

Growth of Electricity DemandGrowth of Electricity DemandGrowth of Electricity Demand

The National Electricity General Plan (RUKN) 2008 – 2027The National Electricity General Plan (RUKN) 2008 The National Electricity General Plan (RUKN) 2008 –– 20272027

3

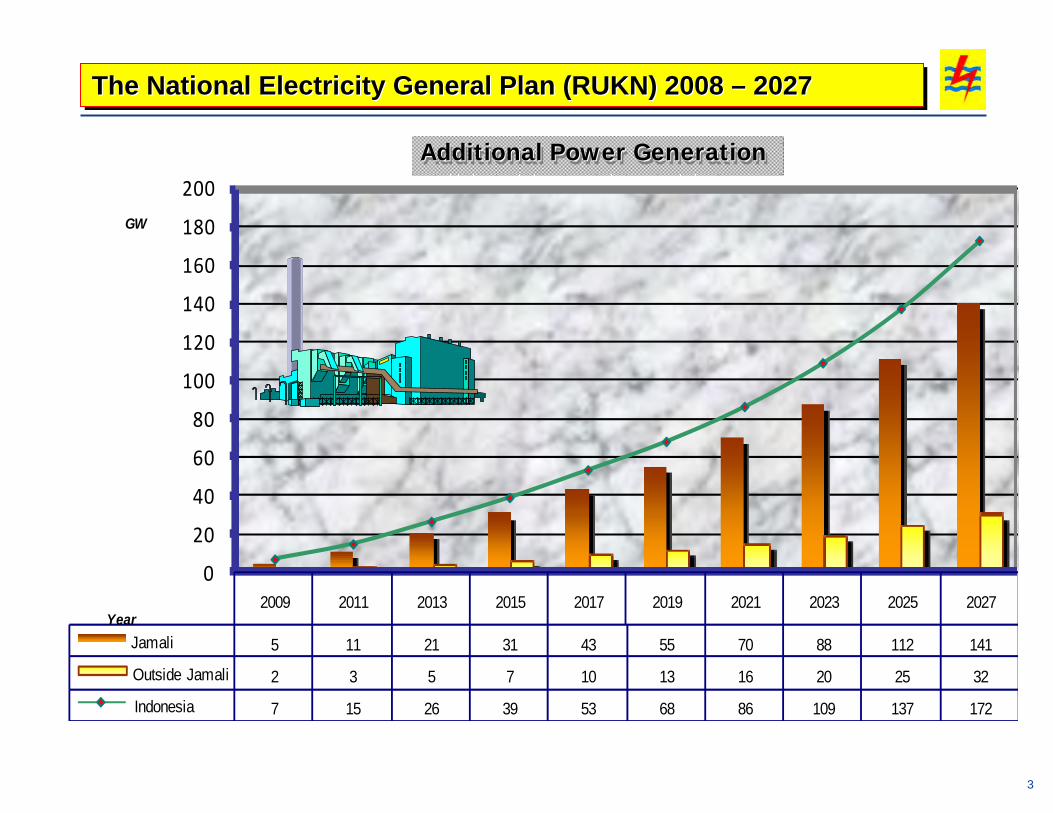

2009 2011 2013 2015 2017 2019 2021 2023 2025 2027

Jamali 5 11 21 31 43 55 70 88 112 141

Outside Jamali 2 3 5 7 10 13 16 20 25 32

Indonesia 7 15 26 39 53 68 86 109 137 172

0

20

40

60

80

100

120

140

160

180

200GW

Year

Additional Power GenerationAdditional Power GenerationAdditional Power Generation

The National Electricity General Plan (RUKN) 2008 – 2027The National Electricity General Plan (RUKN) 2008 The National Electricity General Plan (RUKN) 2008 –– 20272027

4

Fuel mix composition:

Action Plan Outline

Our target is to achieve 100% electrification ratio in 2020 and decrease cost of production

4

Increase of renewable power plant

Increase of coal-steam power plant

Reduce oil power plant

2007 2018

12% 18%

40 % 63 %

34 % 2 %

Change the fuel mix composition

Why Renewable is important ?1.Clean – green energy2.Resistance to the volatility of other global fuel price such as oil, natural gas and coal.3.Long term contract fuel supply.4.Indonesia has abundant resource of geothermal, which has not been exploited. The exploited Geothermal is 3% of total potencial geothermal energy. (27.140 MW)

5

We need of 7% to 9% electricity growth to boost the economic growth of 6% to 7%

Current Obstacles and challenges

It needs financial investment of about US$ 10 billions yearly.

Current Conditions in 2008, 40% of Company’s revenue was from Government Subsidies, meanwhile

Average of Retail Tariff is US$ 6.60 cent per kWh and the production cost is US$ 12 cents per kWh

due to huge CAPEX requirement, government is to invite the private sector to participate in electricity development.

Strong support and commitment from stake holder to boost the Renewable power project, especially Geothermal Power plant.

6

Central and Local GovernmentGovernment actives to promote the utilization of Geothermal Project, that can not be

exported.

Key Actors to be involved in Geothermal Power

Creditor and investor,There are many available fund for green power such as multilateral or bilateral fund.

PLNTo maximize the cheap and stable of energy price.

Private Many flexibilities and incentives are given from government such as Taxes

reduction (VAT) during constriction and government guarantee.

7

The development program of geothermal projects have been planned by Government with 4733 MW. The capacity of 4078 MW is allocated for IPP project until 2014 in the 2nd Phase of Fast Tract Program.

Timeline of Geothermal Development

The investment is estimated around USD 10 Billion or USD 2 Billion per annum.

8

Technical assistance on :

- Pricing Geothermal

- Risk assessments of geothermal project

- Financial Scheme which can attractive for IPP

Area where assistance is needed

Capacity building on Regulatory body:

- Central Government

- Regional Government

All the Technical assistance and capacity building is needed in year 2010

9

Thank you

1

Action Plan Outline for

Pakistan

E8E8--GEFGEF--UNDESAUNDESA--UNESCAPUNESCAPFinancing Sustainable ElectrificationFinancing Sustainable Electrification

South and SouthSouth and South--East Asia DialoguesEast Asia DialoguesBangkok, Thailand, September 8Bangkok, Thailand, September 8--10 200910 2009

September 10, 2009

2

Pakistan Power SectorPakistan Power Sector

MINISTRY OF WATER & POWER

WAPDA PEPCO PPIB

GOVERNMENT OF PAKISTAN

MegaDams

Water Projects

GENCOsGeneration Companies

DISCOsDistributionCompanies

NTDCNational Transmission & Dispatch Company

CHASHNUPP KANUPP

NEPRAPakistan AtomicEnergy

Commission

AEDB IPPsSPPsCPPs

PRIVATE SECTOR

KESC2

3

1. Private Power & Infrastructure Board2. Small Power Producer3. Captive Power Producer

1

3

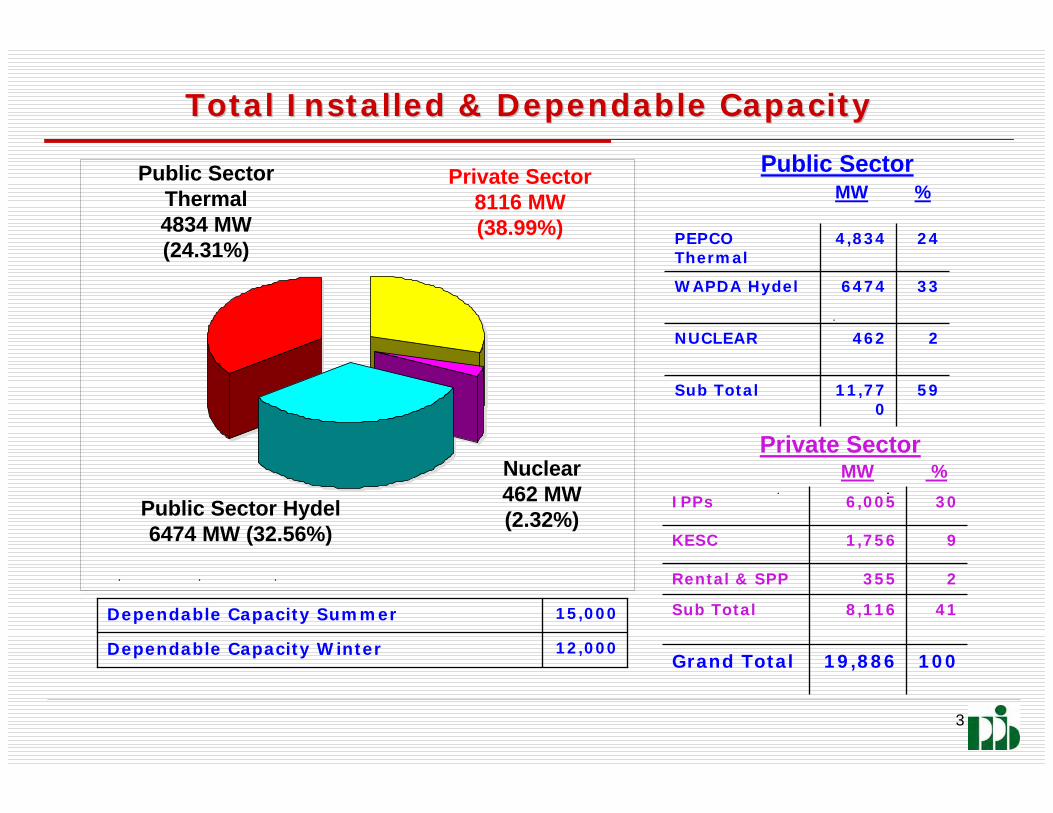

Private Sector8116 MW(38.99%)

Public SectorThermal4834 MW(24.31%)

Public Sector Hydel6474 MW (32.56%)

Nuclear462 MW(2.32%)

Total Installed & Dependable CapacityTotal Installed & Dependable Capacity

10019,886Grand Total

418,116Sub Total

2355Rental & SPP

91,756KESC

306,005IPPs

5911,770

Sub Total

2462NUCLEAR

336474WAPDA Hydel

244,834PEPCO Thermal

Public Sector

Private Sector

MW %

MW %

12,000Dependable Capacity Winter

15,000Dependable Capacity Summer

4

Peak Demand vs. Installed Capacity (2010 Peak Demand vs. Installed Capacity (2010 -- 2015)2015)

20000

30000

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Years

MW

Peak DemandInstalled Capacity

21,840 M W

24,793 M W

27,002 M W

30,309 M W30,836 M W

32,636M W

24,474 M W

26,520 M W

28,683 M W

30,944 M W

33,394 M W

36,217 M W

5

Power Sector OverviewPower Sector Overview

Historically, Water & Power Development Authority (WAPDA), and Karachi Electric Supply Company (KESC), were fully-owned by GOP and served the entire country

KESC was privatised in 2005 by selling 74% interest of the Government to a consortium of private investors

WAPDA and KESC systems are interconnected through 500 KV and 220KV transmission lines for power interchange

National Electric Power Regulatory Authority (NEPRA) was established in 1997 as a statutory, independent regulatory body with power and functions to grant licenses, determine tariffs, prescribe rules, procedures, standards etc.

Pakistan Electric Power Company (PEPC0) was established in 1992 to carry forward reforms in the power sector

As a result, 4 Generation Companies (GENCOs), 1 National Transmission & Dispatch Company (NTDC) and 9 Distribution Companies (DISCOs) were formed

6

Power Sector Overview Power Sector Overview (contd..)(contd..)

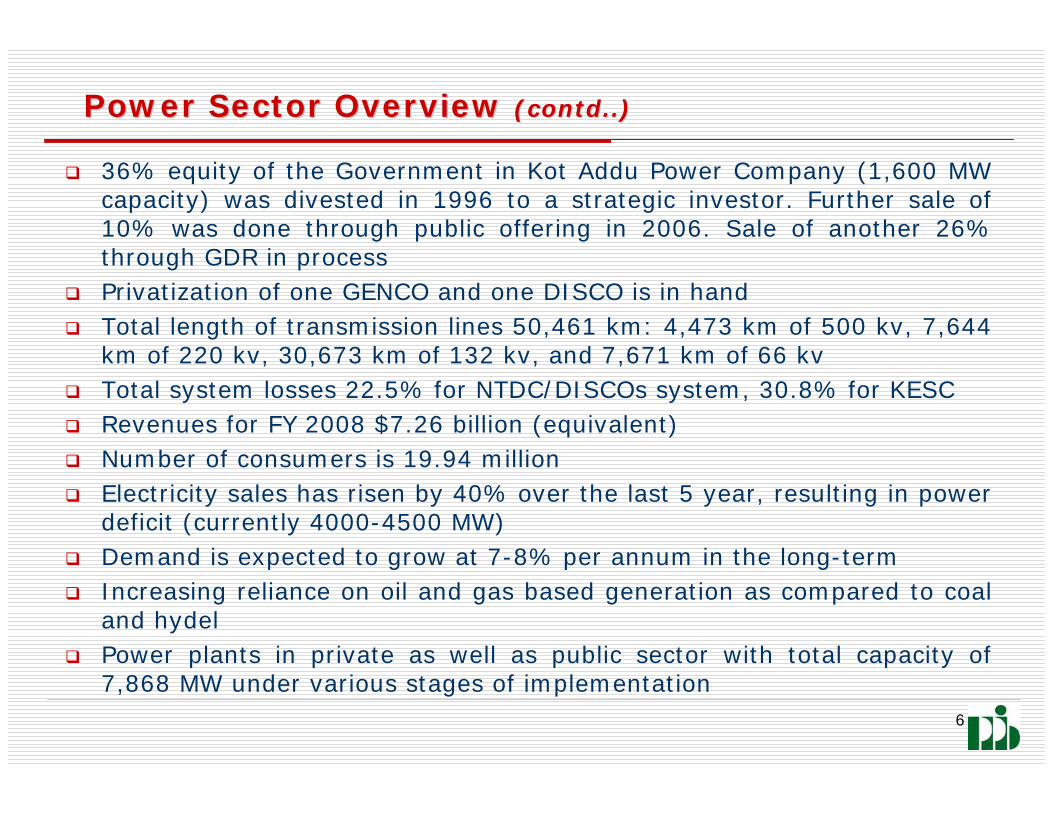

36% equity of the Government in Kot Addu Power Company (1,600 MW capacity) was divested in 1996 to a strategic investor. Further sale of 10% was done through public offering in 2006. Sale of another 26% through GDR in process

Privatization of one GENCO and one DISCO is in hand Total length of transmission lines 50,461 km: 4,473 km of 500 kv, 7,644

km of 220 kv, 30,673 km of 132 kv, and 7,671 km of 66 kv Total system losses 22.5% for NTDC/DISCOs system, 30.8% for KESC Revenues for FY 2008 $7.26 billion (equivalent) Number of consumers is 19.94 million Electricity sales has risen by 40% over the last 5 year, resulting in power

deficit (currently 4000-4500 MW) Demand is expected to grow at 7-8% per annum in the long-term Increasing reliance on oil and gas based generation as compared to coal

and hydel Power plants in private as well as public sector with total capacity of

7,868 MW under various stages of implementation

7

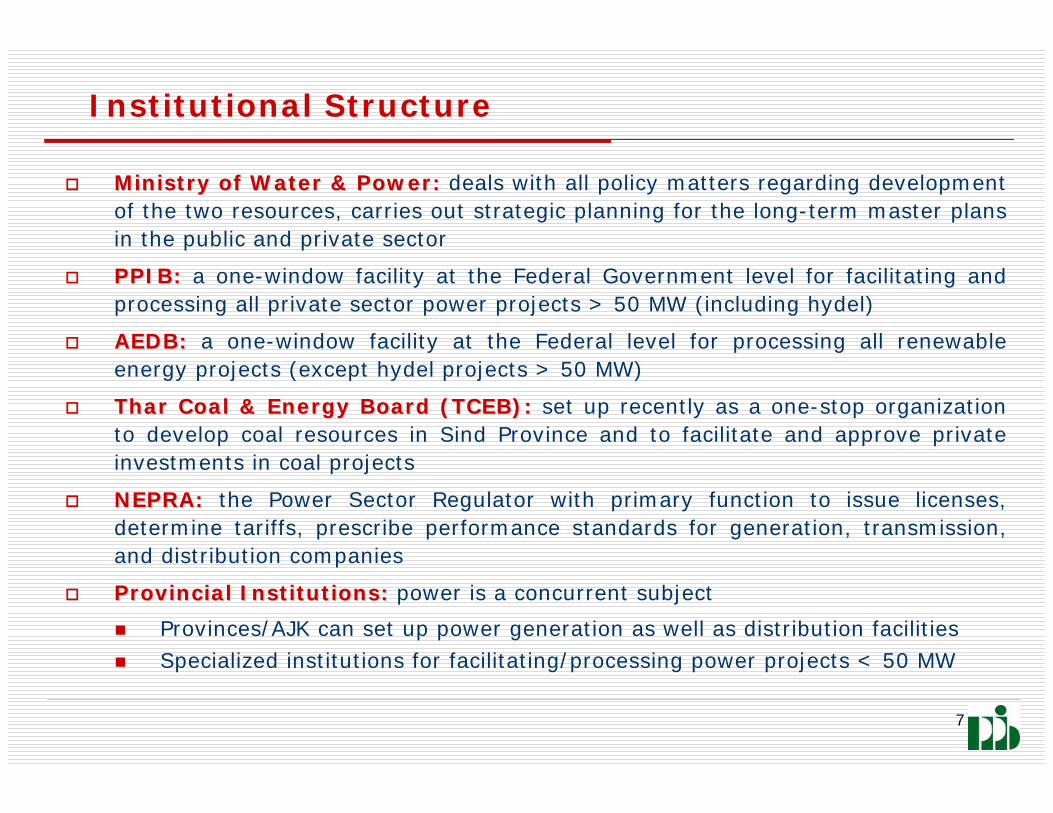

Ministry of Water & Power: Ministry of Water & Power: deals with all policy matters regarding development of the two resources, carries out strategic planning for the long-term master plans in the public and private sector

PPIB:PPIB: a one-window facility at the Federal Government level for facilitating and processing all private sector power projects > 50 MW (including hydel)

AEDB:AEDB: a one-window facility at the Federal level for processing all renewable energy projects (except hydel projects > 50 MW)

TharThar Coal & Energy Board (TCEB):Coal & Energy Board (TCEB): set up recently as a one-stop organization to develop coal resources in Sind Province and to facilitate and approve private investments in coal projects

NEPRA:NEPRA: the Power Sector Regulator with primary function to issue licenses, determine tariffs, prescribe performance standards for generation, transmission, and distribution companies

Provincial Institutions:Provincial Institutions: power is a concurrent subject

Provinces/AJK can set up power generation as well as distribution facilities Specialized institutions for facilitating/processing power projects < 50 MW

Institutional Structure

8

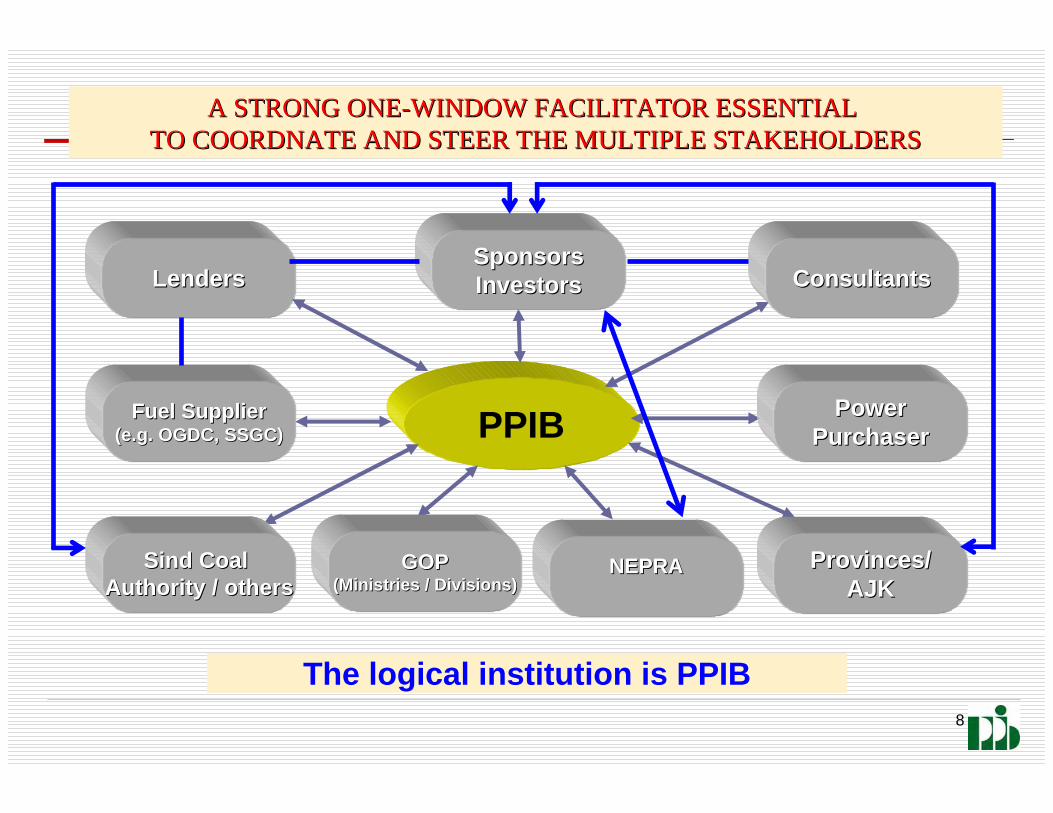

LendersLenders

PPIB PowerPowerPurchaserPurchaser

SponsorsSponsorsInvestorsInvestors ConsultantsConsultants

SindSind Coal Coal Authority / othersAuthority / others

GOPGOP(Ministries / Divisions)(Ministries / Divisions)

Fuel SupplierFuel Supplier(e.g. OGDC, SSGC)(e.g. OGDC, SSGC)

Provinces/Provinces/AJKAJK

A STRONG ONEA STRONG ONE--WINDOW FACILITATOR ESSENTIAL WINDOW FACILITATOR ESSENTIAL TO COORDNATE AND STEER THE MULTIPLE STAKEHOLDERSTO COORDNATE AND STEER THE MULTIPLE STAKEHOLDERS

The logical institution is PPIB

NEPRANEPRA

9

Established in 1994 as a oneEstablished in 1994 as a one--window facilitator to promote private window facilitator to promote private investment in power sectorinvestment in power sector

15 new projects commissioned with total capacity of 4300 MW duri15 new projects commissioned with total capacity of 4300 MW during 90sng 90s

Succeeded in attracting US$ 4.5 Billion of FDI & elimination of Succeeded in attracting US$ 4.5 Billion of FDI & elimination of load sheddingload shedding

Attracted worldAttracted world--leading energy players to Pakistanleading energy players to Pakistan’’s Private Power Sectors Private Power Sector

Successfully negotiated, executed and administered longSuccessfully negotiated, executed and administered long--term concession term concession agreements such as IA, PPA and agreements such as IA, PPA and FSAsFSAs with with IPPsIPPs

Bulk of financing was foreign through multiBulk of financing was foreign through multi--lateral lending agencieslateral lending agencies

2002 Power Policy for Power Generation Projects:2002 Power Policy for Power Generation Projects:

Contracts signed for 2500 MW with Commissioning Dates till 2010 Contracts signed for 2500 MW with Commissioning Dates till 2010

Financial Close achieved for 12 thermal projects: Total CapacityFinancial Close achieved for 12 thermal projects: Total Capacity 2400 MW, 2400 MW, Approx. Investment US$ 2.5 BillionApprox. Investment US$ 2.5 Billion

Bulk of Financing has been provided by local banksBulk of Financing has been provided by local banks

Private Power & Infrastructure Board (PPIB)Private Power & Infrastructure Board (PPIB)

10

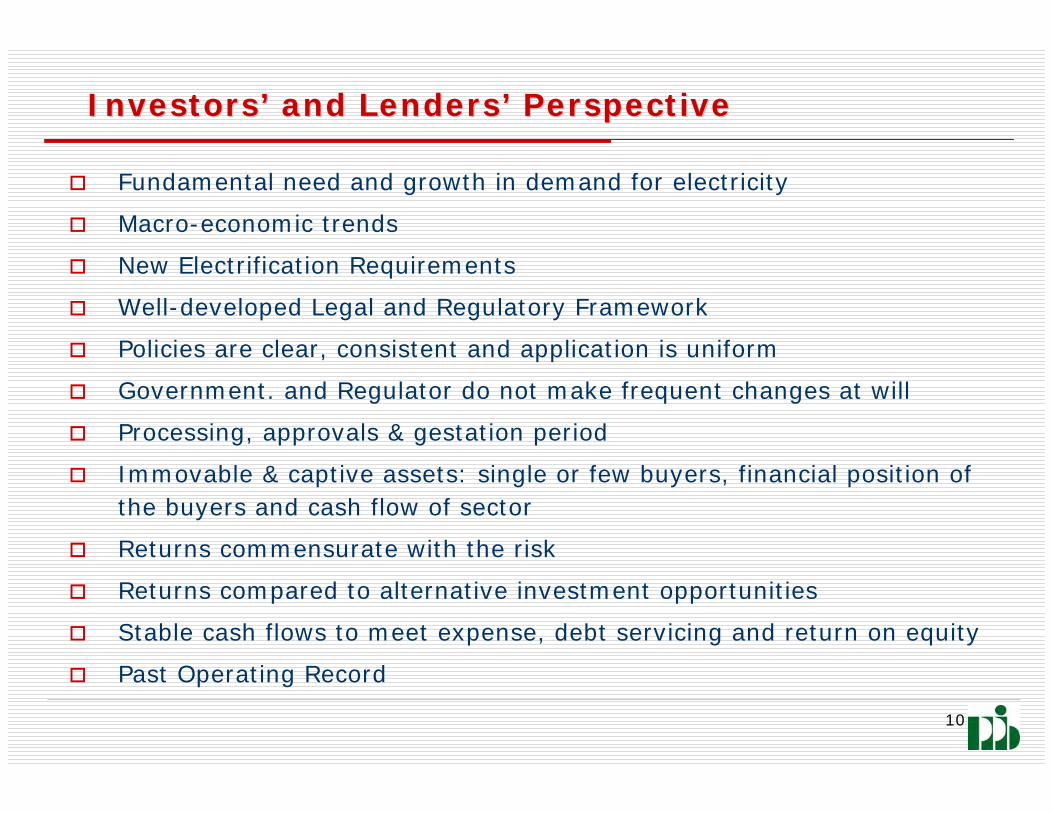

Fundamental need and growth in demand for electricity

Macro-economic trends

New Electrification Requirements

Well-developed Legal and Regulatory Framework

Policies are clear, consistent and application is uniform

Government. and Regulator do not make frequent changes at will

Processing, approvals & gestation period

Immovable & captive assets: single or few buyers, financial position of the buyers and cash flow of sector

Returns commensurate with the risk

Returns compared to alternative investment opportunities

Stable cash flows to meet expense, debt servicing and return on equity

Past Operating Record

InvestorsInvestors’’ and Lendersand Lenders’’ PerspectivePerspective

11

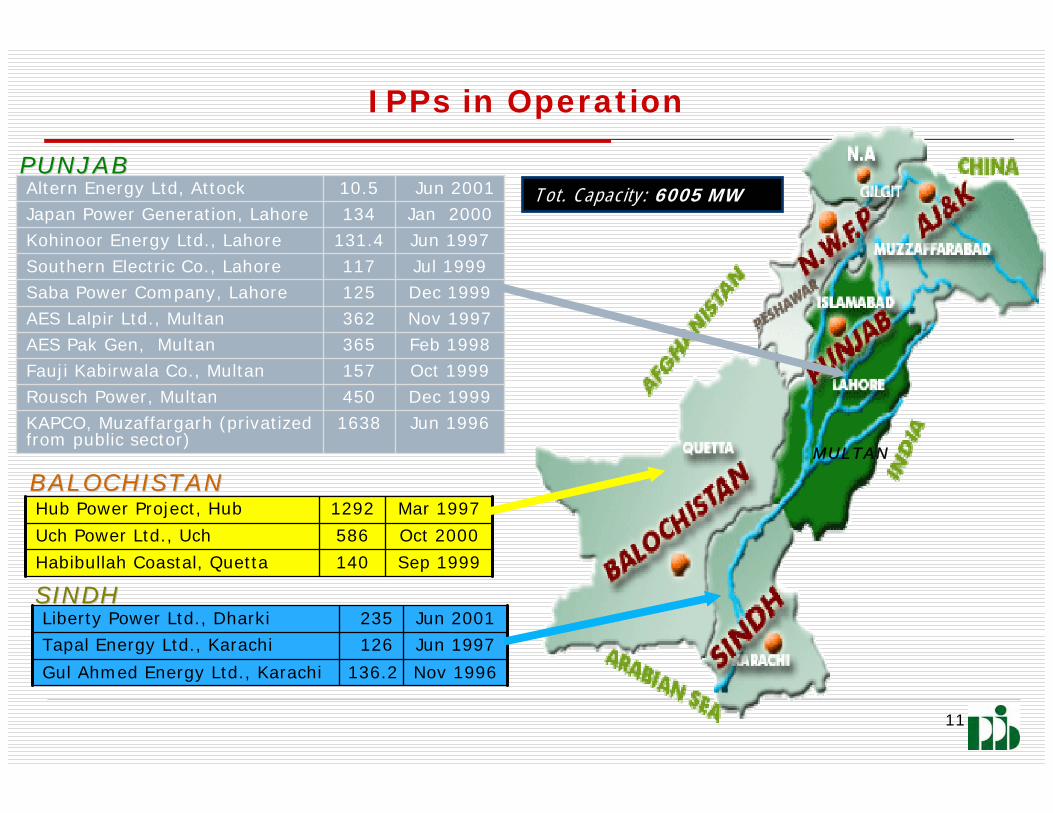

IPPs in Operation

Jun 19961638KAPCO, Muzaffargarh (privatized from public sector)

Dec 1999450Rousch Power, MultanOct 1999157Fauji Kabirwala Co., MultanFeb 1998365AES Pak Gen, MultanNov 1997362AES Lalpir Ltd., Multan

Jun 200110.5Altern Energy Ltd, Attock

Dec 1999125Saba Power Company, LahoreJul 1999117Southern Electric Co., LahoreJun 1997131.4Kohinoor Energy Ltd., LahoreJan 2000134Japan Power Generation, Lahore

Mar 19971292Hub Power Project, Hub

Sep 1999140Habibullah Coastal, Quetta

Oct 2000586Uch Power Ltd., Uch

Nov 1996136.2Gul Ahmed Energy Ltd., Karachi

Jun 1997126Tapal Energy Ltd., Karachi

Jun 2001235Liberty Power Ltd., Dharki

MULTAN

PUNJABPUNJAB

BALOCHISTANBALOCHISTAN

SINDHSINDH

Tot. Capacity: 6005 MW

12

InvestorInvestor--Friendly PolicyFriendly Policy

13

Fiscal ConcessionsFiscal Concessions

5% concessionary Import Duty on plant & equipment not manufactur5% concessionary Import Duty on plant & equipment not manufactured ed

locallylocally

No levy of sales tax on such plant, machinery and equipmentNo levy of sales tax on such plant, machinery and equipment

Inflation indexation on O&M costsInflation indexation on O&M costs

Tariff adjustments for variation in currency exchange ratesTariff adjustments for variation in currency exchange rates

Exemption from corporate income tax, turnover tax and withholdinExemption from corporate income tax, turnover tax and withholding tax g tax

Government ensures conversion of Pak Rupee & remittance of foreiGovernment ensures conversion of Pak Rupee & remittance of foreign gn

exchange for projectexchange for project--related paymentsrelated payments

14

GOP guarantees obligations of power purchaser and provincesGOP guarantees obligations of power purchaser and provinces

Capacity Payments to cover fixed costs including debt servicing Capacity Payments to cover fixed costs including debt servicing and return and return

on equity, independent of project dispatchon equity, independent of project dispatch

Power Purchaser will bear hydrological risk for hydropower projePower Purchaser will bear hydrological risk for hydropower projectscts

Continuity of Payments in case of Political Force MajeureContinuity of Payments in case of Political Force Majeure

PassPass--through of additional taxes or costs incurred due to change in lthrough of additional taxes or costs incurred due to change in lawaw

Tariff adjustment for changes in interest rates benchmarks (LIBOTariff adjustment for changes in interest rates benchmarks (LIBOR/KIBOR)R/KIBOR)

Payment of compensation in case of termination due to GOP defaulPayment of compensation in case of termination due to GOP default t

Balanced risk profile for investors, lenders & government agenciBalanced risk profile for investors, lenders & government agencieses

Payments SecurityPayments Security

15

Commercial Structure for IPPsCommercial Structure for IPPs

LongLong--Term Security Package including Implementation and Power Term Security Package including Implementation and Power Purchase Agreements and Water Usage license (for Purchase Agreements and Water Usage license (for HydelHydel Projects)Projects)

MultiMulti--year / longyear / long--term tariff term tariff –– Approved by RegulatorApproved by Regulator

Reasonable Return on Equity allowed by Regulator Reasonable Return on Equity allowed by Regulator –– 15% in US$15% in US$

Up to 50 years Concession Period for Hydel PlantsUp to 50 years Concession Period for Hydel Plants

100% foreign ownership allowed100% foreign ownership allowed

Minimum 20% equity contribution requirementsMinimum 20% equity contribution requirements

Sponsor can divest equity after six yearsSponsor can divest equity after six years

‘‘HydelHydel’’ projects on BOOT basisprojects on BOOT basis

‘‘ThermalThermal’’ projects on BOO basisprojects on BOO basis

Power Purchaser will be responsible for power transmission facilPower Purchaser will be responsible for power transmission facilitiesities

16

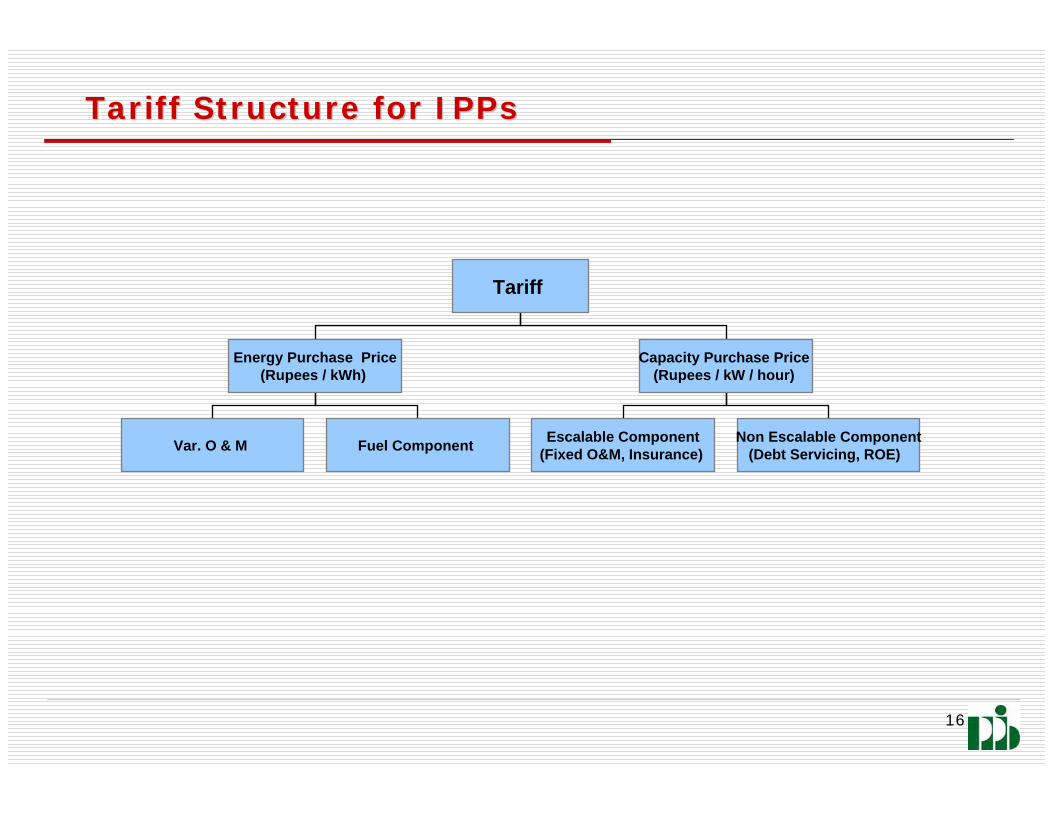

Tariff Structure for IPPs Tariff Structure for IPPs

Tariff

Energy Purchase Price(Rupees / kWh)

Capacity Purchase Price (Rupees / kW / hour)

Var. O & M Fuel Component Escalable Component(Fixed O&M, Insurance)

Non Escalable Component(Debt Servicing, ROE)

17

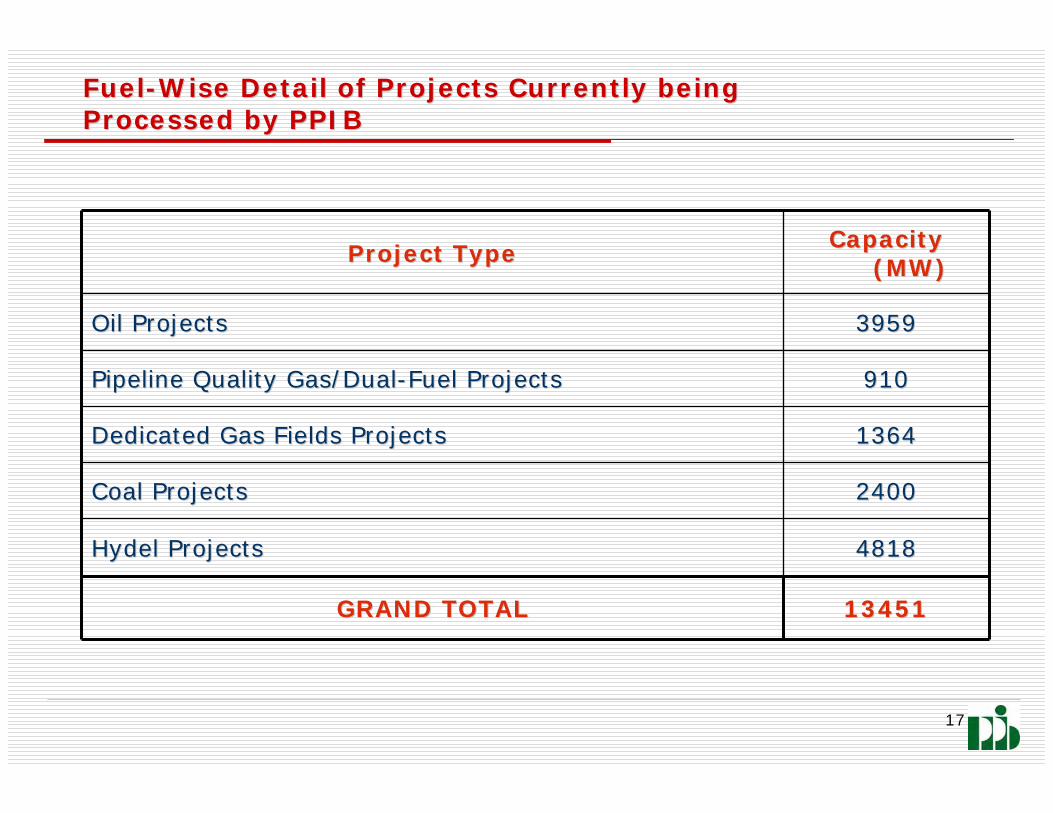

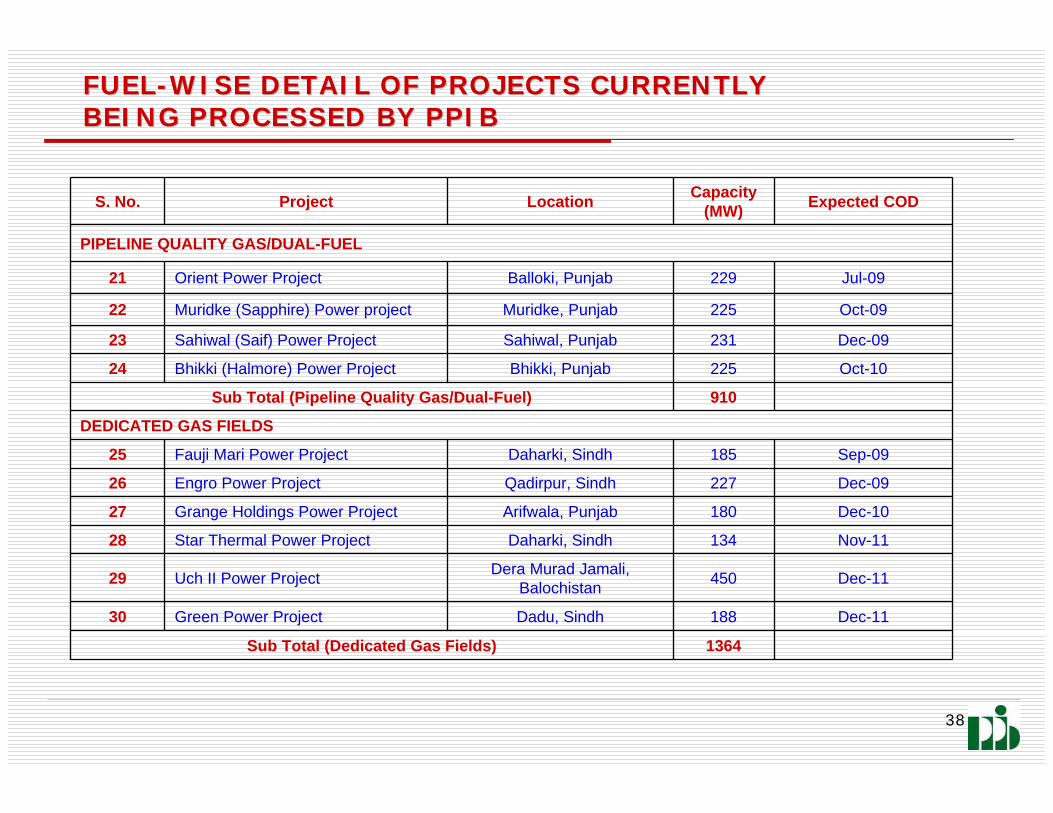

FuelFuel--Wise Detail of Projects Currently being Wise Detail of Projects Currently being Processed by PPIBProcessed by PPIB

1345113451GRAND TOTALGRAND TOTAL

48184818HydelHydel ProjectsProjects

24002400Coal ProjectsCoal Projects

13641364Dedicated Gas Fields ProjectsDedicated Gas Fields Projects

910910Pipeline Quality Gas/DualPipeline Quality Gas/Dual--Fuel ProjectsFuel Projects

39593959Oil ProjectsOil Projects

Capacity Capacity (MW)(MW)Project TypeProject Type

18

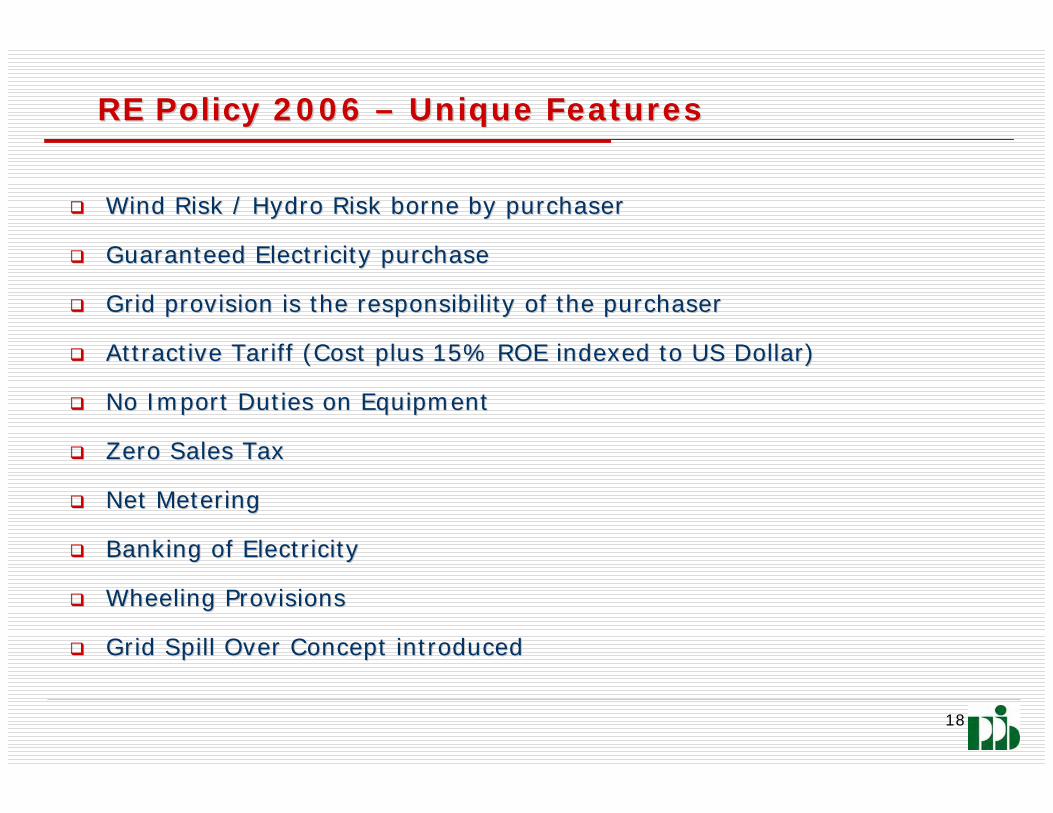

RE Policy 2006 RE Policy 2006 –– Unique FeaturesUnique Features

Wind Risk / Hydro Risk borne by purchaserWind Risk / Hydro Risk borne by purchaser

Guaranteed Electricity purchaseGuaranteed Electricity purchase

Grid provision is the responsibility of the purchaserGrid provision is the responsibility of the purchaser

Attractive Tariff (Cost plus 15% ROE indexed to US Dollar)Attractive Tariff (Cost plus 15% ROE indexed to US Dollar)

No Import Duties on EquipmentNo Import Duties on Equipment

Zero Sales TaxZero Sales Tax

Net MeteringNet Metering

Banking of ElectricityBanking of Electricity

Wheeling ProvisionsWheeling Provisions

Grid Spill Over Concept introducedGrid Spill Over Concept introduced

19

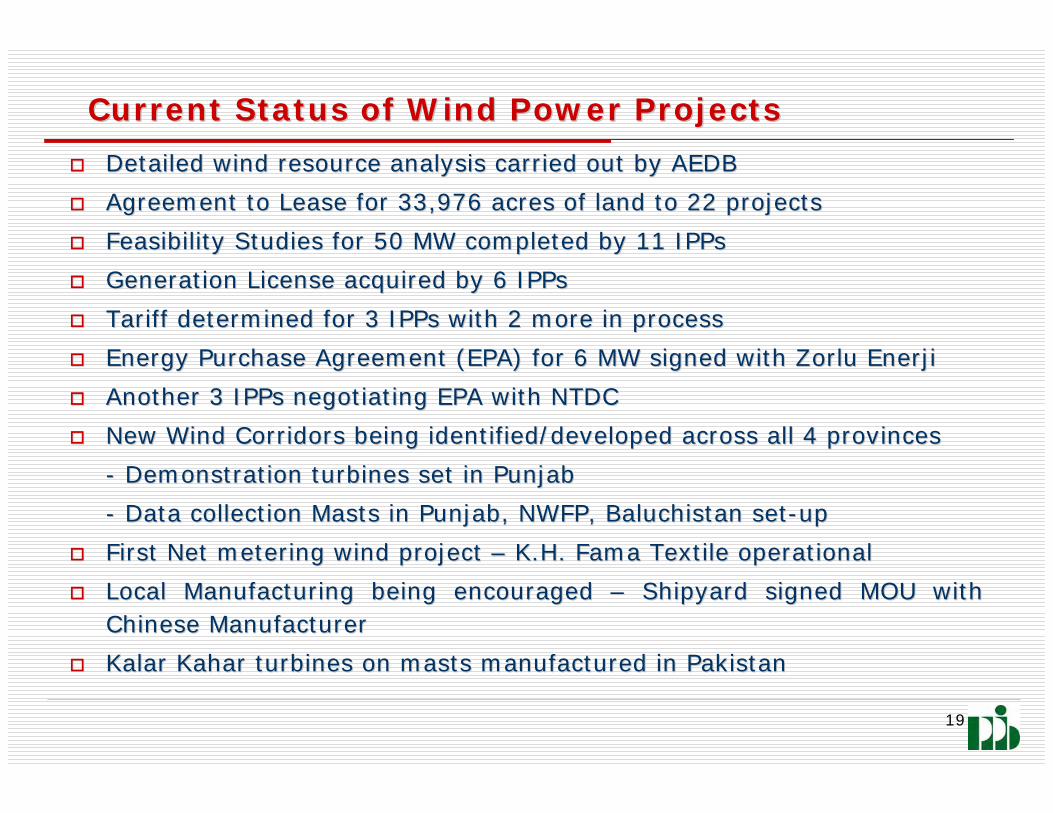

Current Status of Wind Power ProjectsCurrent Status of Wind Power Projects

Detailed wind resource analysis carried out by AEDBDetailed wind resource analysis carried out by AEDB

Agreement to Lease for 33,976 acres of land to 22 projectsAgreement to Lease for 33,976 acres of land to 22 projects

Feasibility Studies for 50 MW completed by 11 Feasibility Studies for 50 MW completed by 11 IPPsIPPs

Generation License acquired by 6 Generation License acquired by 6 IPPsIPPs

Tariff determined for 3 Tariff determined for 3 IPPsIPPs with 2 more in process with 2 more in process

Energy Purchase Agreement (EPA) for 6 MW signed with Energy Purchase Agreement (EPA) for 6 MW signed with ZorluZorlu EnerjiEnerji

Another 3 Another 3 IPPsIPPs negotiating EPA with NTDCnegotiating EPA with NTDC

New Wind Corridors being identified/developed across all 4 proviNew Wind Corridors being identified/developed across all 4 provincesnces

-- Demonstration turbines set in PunjabDemonstration turbines set in Punjab

-- Data collection Masts in Punjab, NWFP, Baluchistan setData collection Masts in Punjab, NWFP, Baluchistan set--upup

First Net metering wind project First Net metering wind project –– K.H. K.H. FamaFama Textile operational Textile operational

Local Manufacturing being encouraged Local Manufacturing being encouraged –– Shipyard signed MOU with Shipyard signed MOU with Chinese ManufacturerChinese Manufacturer

KalarKalar KaharKahar turbines on masts manufactured in Pakistanturbines on masts manufactured in Pakistan

20

Current Status of Small HydelsCurrent Status of Small Hydels

10 10 HydelHydel plants (110 MW) in public sector to become operational in 2012 plants (110 MW) in public sector to become operational in 2012 with ADB Funding (Punjabwith ADB Funding (Punjab--5, NWFP 5, NWFP --5 & NA5 & NA--2)2)

Detailed feasibility for 12 Detailed feasibility for 12 HydelHydel plants (187 MW) prepared and under plants (187 MW) prepared and under reviewreview

Tariff application for 40 MW project at C.J. Link Tail, Punjab fTariff application for 40 MW project at C.J. Link Tail, Punjab filed with iled with NEPRANEPRA

First First HydelHydel PPA (1 MW) signed between PESCO and Blue Star EnergyPPA (1 MW) signed between PESCO and Blue Star Energy

Feasibility Studies for additional 43 Small Feasibility Studies for additional 43 Small HydelHydel plants being initiated with plants being initiated with assistance from GTZ and ADBassistance from GTZ and ADB

102 micro 102 micro hydelhydel projects (15 MW) initiated in NA with AKF / UNDPprojects (15 MW) initiated in NA with AKF / UNDP--GEF GEF collaborationcollaboration

21

Regulatory FrameworkRegulatory Framework

National Electric Power Regulatory Authority (NEPRA) establishedNational Electric Power Regulatory Authority (NEPRA) established in 1997 as in 1997 as an independent an independent ““regulatory bodyregulatory body”” empowered to grant licenses, determine empowered to grant licenses, determine tariffs, prescribe rules/procedures/standards for Generation / Ttariffs, prescribe rules/procedures/standards for Generation / T&D entities&D entities

In performing its various functions, NEPRA endeavors to maintainIn performing its various functions, NEPRA endeavors to maintain a balance a balance between the interests of consumers and power companiesbetween the interests of consumers and power companies

Tariff Rules, Standard Grid Code, Generation/Distribution LicensTariff Rules, Standard Grid Code, Generation/Distribution Licensing Rules, ing Rules, Performance Standards for Generation / T&D Performance Standards for Generation / T&D –– already in placealready in place

UniformUniform Accounting StandardsAccounting Standards developed for power companiesdeveloped for power companies

NEPRA is setting tariff for power generation plants (including NEPRA is setting tariff for power generation plants (including IPPsIPPs), ), transmission and distribution companiestransmission and distribution companies

ConsumerConsumer--end tariffs are determined by NEPRA, while end tariffs are determined by NEPRA, while GoPGoP notifies these notifies these tariffs keeping provision of subsidies by the government tariffs keeping provision of subsidies by the government

Tariff Determination MechanismTariff Determination Mechanism for Hydropower projects has been developed for Hydropower projects has been developed for reducing risk and uncertainties for private investorsfor reducing risk and uncertainties for private investors

22

Sector Governance and AchievementsSector Governance and Achievements

Government commitment and consistent Policies to encourage privaGovernment commitment and consistent Policies to encourage private te

sector led growth of economy in all sectorssector led growth of economy in all sectors

Pakistan Pakistan –– today an established destination for private investments in today an established destination for private investments in

power sectorpower sector

Approximately 40% generation capacity in private sectorApproximately 40% generation capacity in private sector

Major international power companies currently operating in PakisMajor international power companies currently operating in Pakistantan

Reform of power sector through restructuring /deregulation /privReform of power sector through restructuring /deregulation /privatization atization

is well underwayis well underway

1638 MW KAPCO Power Plant privatized in 19961638 MW KAPCO Power Plant privatized in 1996

23

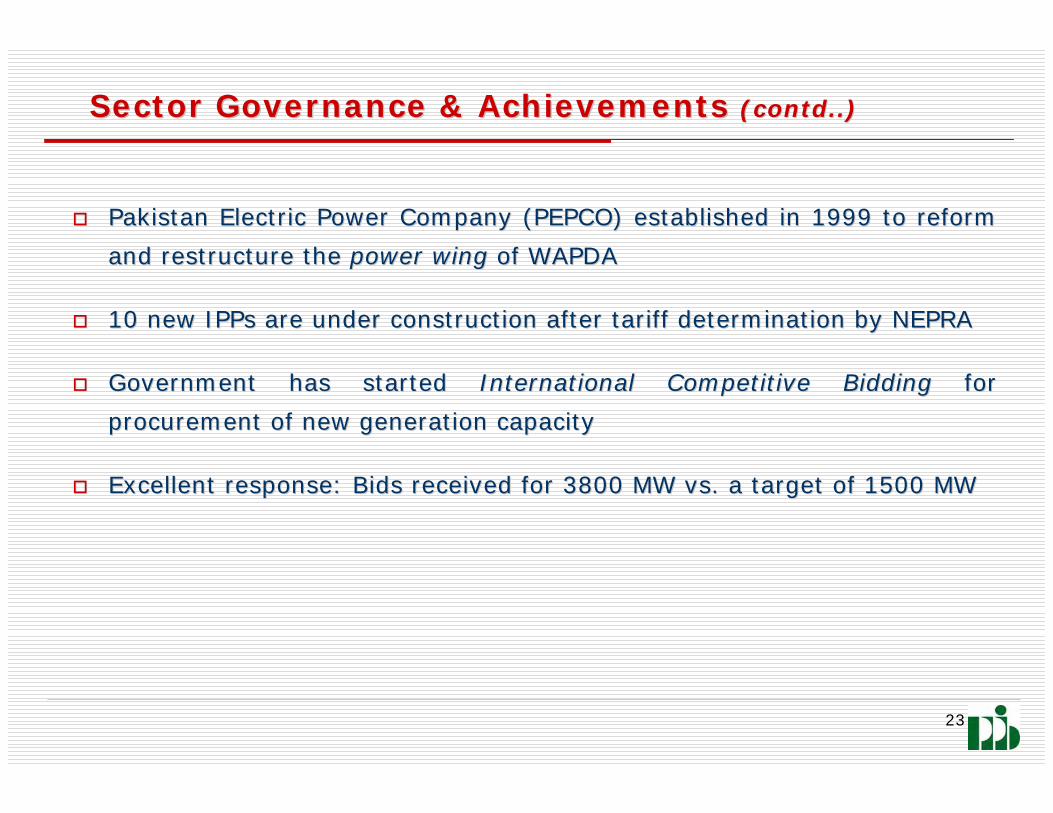

Sector Governance & Achievements Sector Governance & Achievements (contd..)(contd..)

Pakistan Electric Power Company (PEPCO) established in 1999 to rPakistan Electric Power Company (PEPCO) established in 1999 to reform eform

and restructure the and restructure the power wingpower wing of WAPDAof WAPDA

10 new 10 new IPPsIPPs are under construction after tariff determination by NEPRAare under construction after tariff determination by NEPRA

Government has started Government has started International Competitive BiddingInternational Competitive Bidding for for

procurement of new generation capacityprocurement of new generation capacity

Excellent response: Bids received for 3800 MW vs. a target of 15Excellent response: Bids received for 3800 MW vs. a target of 1500 MW00 MW

24

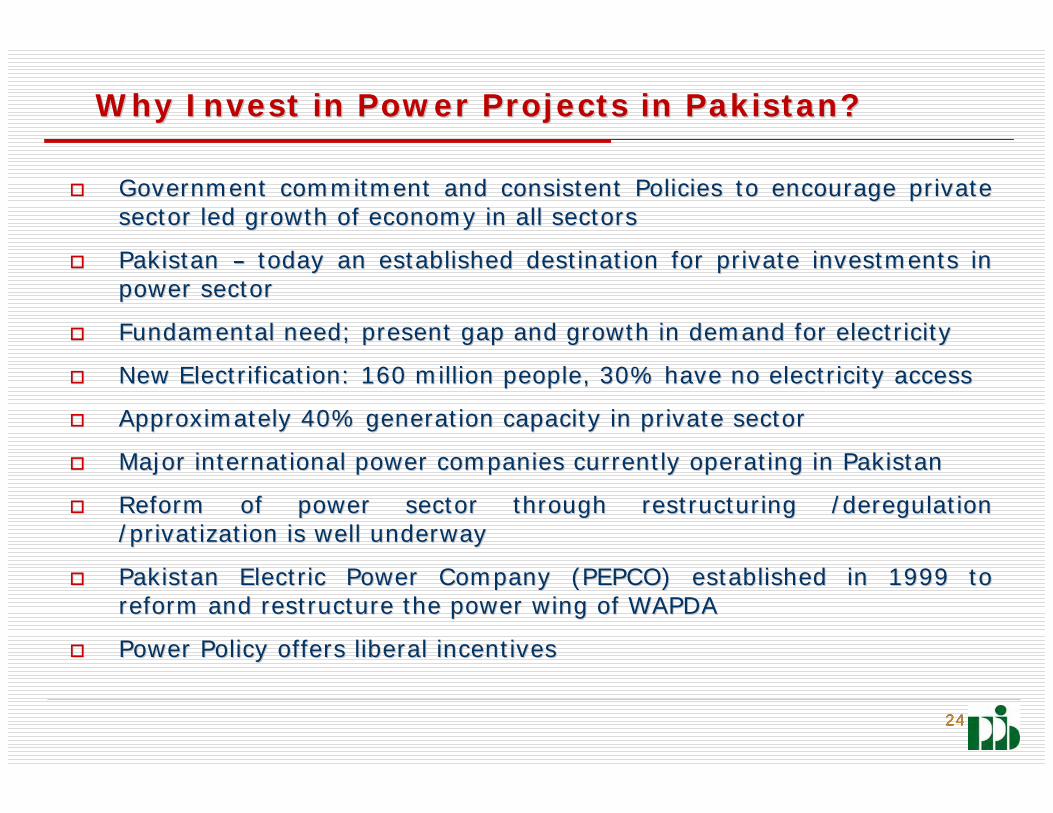

Why Invest in Power Projects in Pakistan?Why Invest in Power Projects in Pakistan?

Government commitment and consistent Policies to encourage privaGovernment commitment and consistent Policies to encourage private te sector led growth of economy in all sectorssector led growth of economy in all sectors

Pakistan Pakistan –– today an established destination for private investments in today an established destination for private investments in power sectorpower sector

Fundamental need; present gap and growth in demand for electriciFundamental need; present gap and growth in demand for electricityty

New Electrification: 160 million people, 30% have no electricityNew Electrification: 160 million people, 30% have no electricity accessaccess

Approximately 40% generation capacity in private sectorApproximately 40% generation capacity in private sector

Major international power companies currently operating in PakisMajor international power companies currently operating in Pakistantan

Reform of power sector through restructuring /deregulation Reform of power sector through restructuring /deregulation /privatization is well underway/privatization is well underway

Pakistan Electric Power Company (PEPCO) established in 1999 to Pakistan Electric Power Company (PEPCO) established in 1999 to reform and restructure the power wing of WAPDAreform and restructure the power wing of WAPDA

Power Policy offers liberal incentivesPower Policy offers liberal incentives

24

2525

OneOne--Window facility provided by PPIB for private projects.Window facility provided by PPIB for private projects.

Balanced risk profile for investors, lenders & government agenciBalanced risk profile for investors, lenders & government agencieses

Independent regulator to balance interest of consumers and powerIndependent regulator to balance interest of consumers and power sector sector companiescompanies

Attractive and competitive return on investmentAttractive and competitive return on investment

12 new 12 new IPPsIPPs are under construction after tariff determination by NEPRAare under construction after tariff determination by NEPRA

4 Rental Projects (800MW) awarded with COD of December 20094 Rental Projects (800MW) awarded with COD of December 2009

Government has started International Competitive Bidding for Government has started International Competitive Bidding for procurement of new generation capacity for both procurement of new generation capacity for both IPPsIPPs and Rentalsand Rentals

Identified Hydropower potential of over 45,000 MWIdentified Hydropower potential of over 45,000 MW

Time tested institutional and legal framework in placeTime tested institutional and legal framework in place

Track record of successful private sector participationTrack record of successful private sector participation

Government has exhibited its resolve to take bold decisions to eGovernment has exhibited its resolve to take bold decisions to ensure nsure sectorsector’’s sustainabilitys sustainability

Why Invest in Power Projects in Pakistan? Why Invest in Power Projects in Pakistan? (contd..)(contd..)

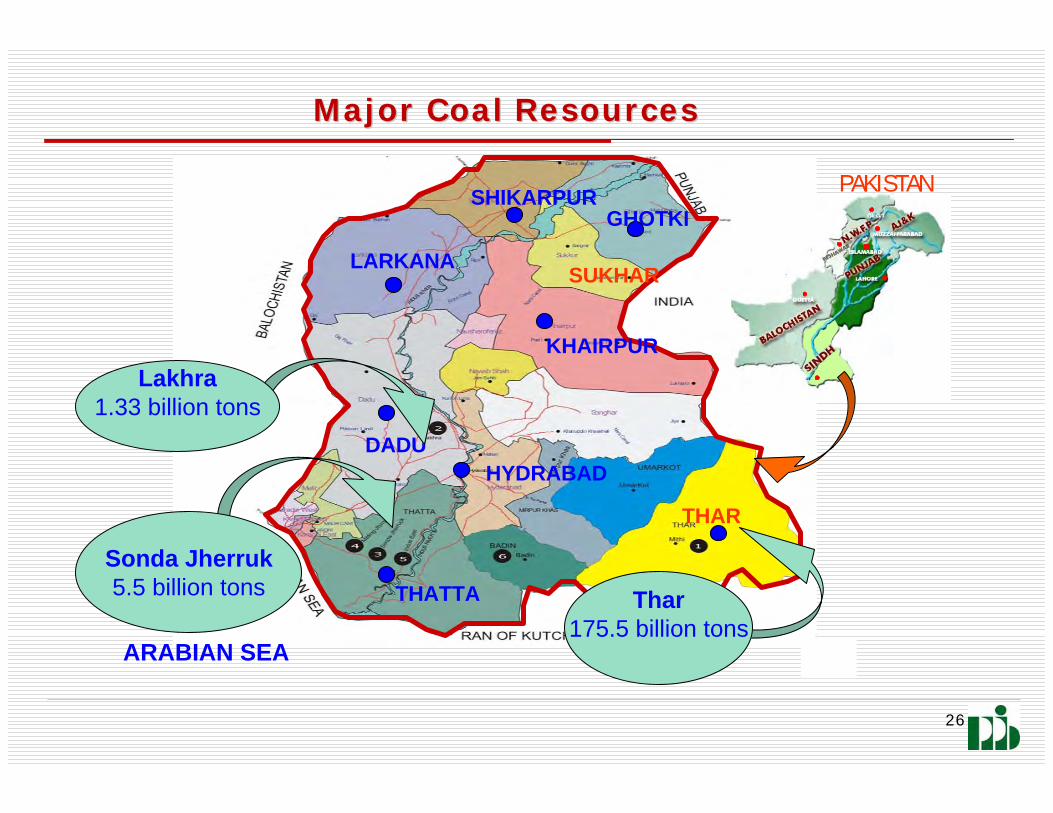

26

THATTA

LARKANA SUKHAR

KHAIRPUR

DADU

THAR

SHIKARPURGHOTKI

HYDRABAD

Major Coal ResourcesMajor Coal Resources

Lakhra1.33 billion tons

Sonda Jherruk5.5 billion tons Thar

175.5 billion tonsARABIAN SEA

PAKISTAN

27

Demand supply gap of 2,500-3,500 MW to be bridged immediately

Average generation expansion of around 2000 MW/year for next few years (growth rate 8+% p.a.) in addition to meeting the current gap

Investment of US$ 2.5-3 Billion per year for the next 8-10 years

1-2 large multipurpose Hydropower projects are needed for both irrigation and power needs with investment of over US$ 2 Billion each

1.5-2 Billion per year for transmission & distribution network expansion

Fast depleting gas resources – New generation on oil which is very expensive, Optimal fuel-mix to be worked out due to increasing oil prices

Maximum use of local hydropower resources – identified potential of 45,000 MW only 6,000 MW exploited so far

Reduction in Transmission & Distribution losses (present 23%)

Huge Government subsidies – US$ 2.2 Billion provided to utility companies to overcome gap in revenues

Current Obstacles and ChallengesCurrent Obstacles and Challenges

28

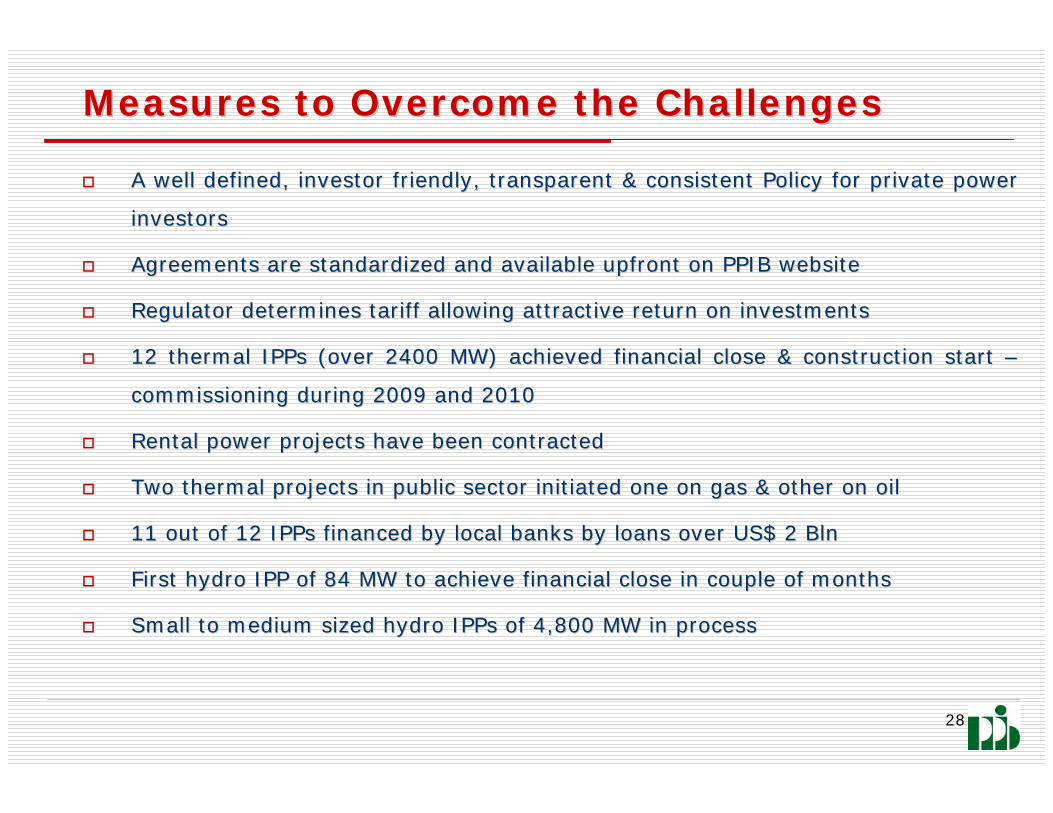

Measures to Overcome the ChallengesMeasures to Overcome the Challenges

A well defined, investor friendly, transparent & consistent PoliA well defined, investor friendly, transparent & consistent Policy for private power cy for private power

investorsinvestors

Agreements are standardized and available upfront on PPIB websitAgreements are standardized and available upfront on PPIB websitee

Regulator determines tariff allowing attractive return on investRegulator determines tariff allowing attractive return on investmentsments

12 thermal 12 thermal IPPsIPPs (over 2400 MW) achieved financial close & construction start (over 2400 MW) achieved financial close & construction start ––

commissioning during 2009 and 2010commissioning during 2009 and 2010

Rental power projects have been contractedRental power projects have been contracted

Two thermal projects in public sector initiated one on gas & othTwo thermal projects in public sector initiated one on gas & other on oiler on oil

11 out of 12 11 out of 12 IPPsIPPs financed by local banks by loans over US$ 2 financed by local banks by loans over US$ 2 BlnBln

First hydro IPP of 84 MW to achieve financial close in couple ofFirst hydro IPP of 84 MW to achieve financial close in couple of monthsmonths

Small to medium sized hydro Small to medium sized hydro IPPsIPPs of 4,800 MW in processof 4,800 MW in process

29

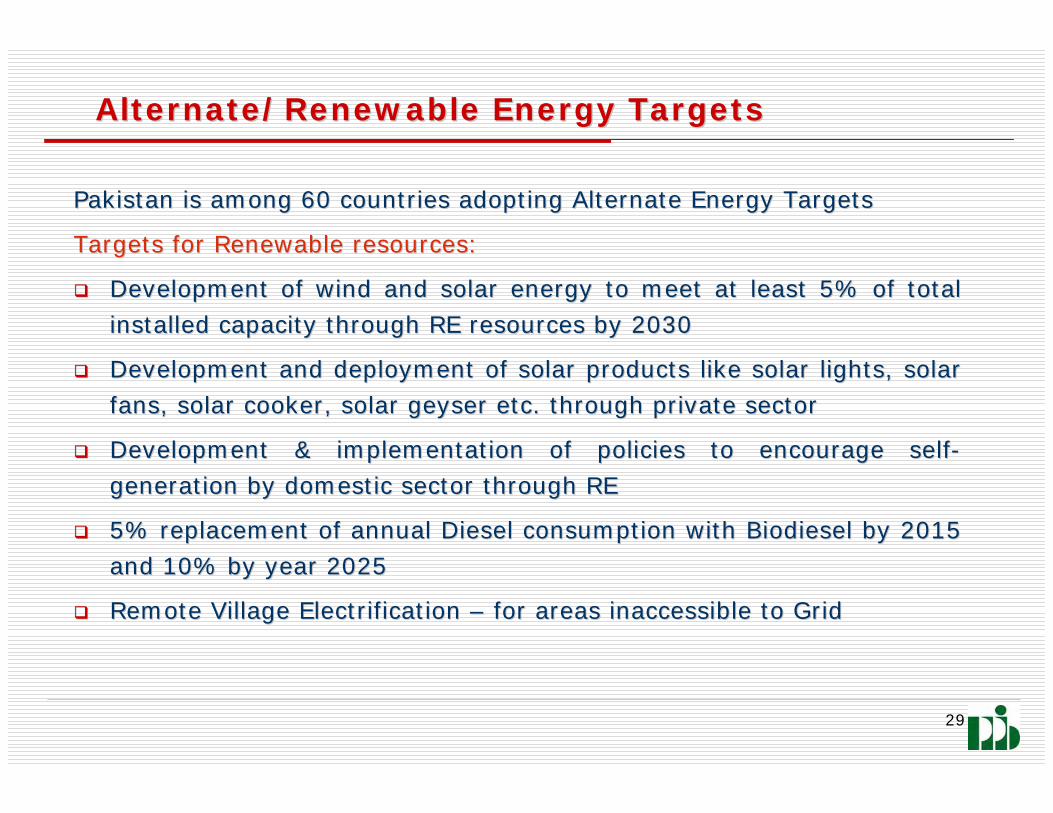

Alternate/Renewable Energy TargetsAlternate/Renewable Energy Targets

Pakistan is among 60 countries adopting Alternate Energy TargetsPakistan is among 60 countries adopting Alternate Energy Targets

Targets for Renewable resources:Targets for Renewable resources:

Development of wind and solar energy to meet at least 5% of totaDevelopment of wind and solar energy to meet at least 5% of total l

installed capacity through RE resources by 2030installed capacity through RE resources by 2030

Development and deployment of solar products like solar lights, Development and deployment of solar products like solar lights, solar solar

fans, solar cooker, solar geyser etc. through private sectorfans, solar cooker, solar geyser etc. through private sector

Development & implementation of policies to encourage selfDevelopment & implementation of policies to encourage self--

generation by domestic sector through REgeneration by domestic sector through RE

5% replacement of annual Diesel consumption with Biodiesel by 205% replacement of annual Diesel consumption with Biodiesel by 2015 15

and 10% by year 2025and 10% by year 2025

Remote Village Electrification Remote Village Electrification –– for areas inaccessible to Gridfor areas inaccessible to Grid

3030

Opportunities for Private Sector ParticipationOpportunities for Private Sector Participation

Development of small/medium/mega Hydropower projects Development of small/medium/mega Hydropower projects –– so far only so far only

around 6,000 MW tapped from an estimated potential of 45,000 MWaround 6,000 MW tapped from an estimated potential of 45,000 MW

Development of indigenous coal resources for power generation Development of indigenous coal resources for power generation –– TharThar

Coal Reserve estimated at about 175 billion ton is still untappeCoal Reserve estimated at about 175 billion ton is still untappedd

Home solar system manufacturing and supplies Privatization Home solar system manufacturing and supplies Privatization

opportunities in generation and distributionopportunities in generation and distribution

Augmentation of transmission/distribution infrastructureAugmentation of transmission/distribution infrastructure

Rental Plants for meeting short to mediumRental Plants for meeting short to medium--term demandterm demand

PublicPublic--Private Partnership for large and complex projectsPrivate Partnership for large and complex projects

O&M and EPC contractors / Consultants and AdvisorsO&M and EPC contractors / Consultants and Advisors

31

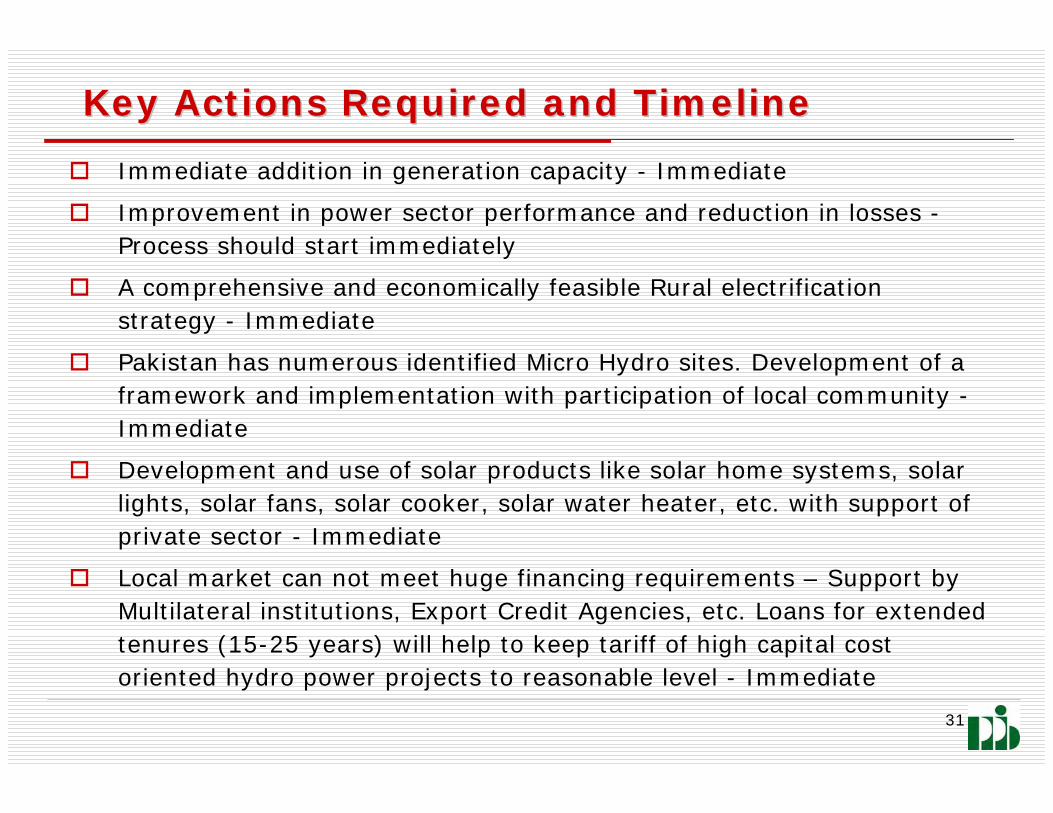

Key Actions Required and TimelineKey Actions Required and Timeline

Immediate addition in generation capacity - Immediate

Improvement in power sector performance and reduction in losses -Process should start immediately

A comprehensive and economically feasible Rural electrification strategy - Immediate

Pakistan has numerous identified Micro Hydro sites. Development of a framework and implementation with participation of local community -Immediate

Development and use of solar products like solar home systems, solar lights, solar fans, solar cooker, solar water heater, etc. with support of private sector - Immediate

Local market can not meet huge financing requirements – Support by Multilateral institutions, Export Credit Agencies, etc. Loans for extended tenures (15-25 years) will help to keep tariff of high capital cost oriented hydro power projects to reasonable level - Immediate

32

Areas where assistance is needed

Performance audit of power sector to evaluate shortcoming and suggest

improvements

Rural electrification strategy/policy for the country

Pakistan has numerous identified Micro Hydro sites. Development of a

framework and their implementation with participation of local community

Development and use of solar products like solar home systems, solar

lights, solar fans, solar cooker, solar water heater, etc. with support of

private sector

Local market can not meet huge financing requirements – Support by

Multilateral institutions, Export Credit Agencies through debt & equity

financing, Guarantees etc. Loans for extended tenures (15-25 years) will

help to keep tariff of high capital cost oriented hydro power projects to

reasonable level

33

Key Actors Involved

Ministry of Water & Power

Private Power & Infrastructure Board (PPIB)

Alternate Energy Development Board (AEDB)

Pakistan Electric Power Company (PEPCO)

34

Country Action Plan Summary

Performance AuditDevelopment of Strategy/PlanDevelopment of Strategy/PlanManufacturing / financing to share cost

Work already underwayStudy immediately

Immediate

Study Immediate

Immdiate

Ministry of Water & Power

PPIB

AEDB

Pakistan Electric Power Company

Expand Generation Capacity Implement measuresImplement Strategy

Prepare & Implement Plan

Supply on subsidisedrates to encourage

Rental Plants, IPPs

System Performance AuditRural Electrification StrategyMicro Hydro Policy & Plan

Manufacturing & Supply of systems / Products

Generation CapacityShortageHigh System LossesNo objective Rural Electrification StrategyLittle work on Micro HydrosNo use of Solar Resources

Areas of Assistance

TimelineKey Actors to be involved

Key Actions Required / Objectives

OpportunitiesCurrent Obstacles & Cahallenges

35

THANK YOU

36

FUELFUEL--WISE DETAIL OF PROJECTS CURRENTLYWISE DETAIL OF PROJECTS CURRENTLYBEING PROCESSED BY PPIBBEING PROCESSED BY PPIB

Feb-1081Eminabad, GujranwalaGulf Rental Project8

Jan-1064Lahore Sheikhupura Road, LESCOPremier Energy Rental Power Project7

Dec-09170Near Batapur Grid, LESCORuba Energy Rental Project6

Dec-09220Near Manga-Raiwind Road, LESCOReshma Power Rental Project5

Dec-09230Korangi, KarachiWalters Power Rental Project4

Nov-09249Mauripur, KarachiKarkey Rental Project3

Sep-09200Near LahoreNishat Power Project2

Jul-09225Sheikhupura, PunjabSheikhupura (Atlas) Power Project1

OILOIL

Expected CODExpected CODCapacity Capacity (MW)(MW)LocationLocationProjectProjectS. No.S. No.

37

FUELFUEL--WISE DETAIL OF PROJECTS CURRENTLYWISE DETAIL OF PROJECTS CURRENTLYBEING PROCESSED BY PPIBBEING PROCESSED BY PPIB

Dec-12150Shahpur, Near SargodhaShahpur Power Project20

Mar-12627Near Bhikki, PunjabEngro Power Generation18

Mar-12171Near Jhang, PunjabSaba Power GenerationNear Jhang, Punjab19

Dec-11200FaisalabadShahkot (Leading) Power Project17

3959Sub Total (Oil)

Expected COD

Capacity (MW)LocationProjectS. No.

Jun-11200GujranwalaGujranwala (Gulistan) Project16

Mar-11172Gujranwala-Lahore Road, PunjabReshma Power Generation15

Dec-10200FaisalabadLiberty Power Tech Project14

Mar-10200Near LahoreNishat Chunian Power Project13

Mar-10220Narowal, PunjabHUBCO-Narowal Project12

Feb-1074Kamoki, Gujranwala, GEPCOTapal Rental Power Project11

Feb-1085Sialkot, GEPCO AreaSialkot Rental Power Project10

Feb-10221Gojra, near FaisalabadIndependent Power Rental Project9

38

FUELFUEL--WISE DETAIL OF PROJECTS CURRENTLYWISE DETAIL OF PROJECTS CURRENTLYBEING PROCESSED BY PPIBBEING PROCESSED BY PPIB

Expected CODCapacity (MW)LocationProjectS. No.

PIPELINE QUALITY GAS/DUAL-FUEL

1364Sub Total (Dedicated Gas Fields)

Dec-11188Dadu, SindhGreen Power Project30

Dec-11450Dera Murad Jamali, BalochistanUch II Power Project29

Nov-11134Daharki, SindhStar Thermal Power Project28

Dec-10180Arifwala, PunjabGrange Holdings Power Project27

Dec-09227Qadirpur, SindhEngro Power Project26

Sep-09185Daharki, SindhFauji Mari Power Project25

DEDICATED GAS FIELDS

910Sub Total (Pipeline Quality Gas/Dual-Fuel)

Oct-10225Bhikki, PunjabBhikki (Halmore) Power Project24

Dec-09231Sahiwal, PunjabSahiwal (Saif) Power Project23

Oct-09225Muridke, PunjabMuridke (Sapphire) Power project22

Jul-09229Balloki, PunjabOrient Power Project21

39

FUELFUEL--WISE DETAIL OF PROJECTS CURRENTLYWISE DETAIL OF PROJECTS CURRENTLYBEING PROCESSED BY PPIBBEING PROCESSED BY PPIB

Expected CODExpected COD

Nov-14150Muzaffarabad AJKPatrind Hydropower Project4040

Jun-14101Near Kalam, NWFPGabral-Kalam Hydropower Project3838

Oct-14240Kotli, AJKKarot Hydel Project3939

Capacity Capacity (MW)(MW)LocationLocationProjectProjectS. No.S. No.

COALCOAL

Nov-14100Gulpur, AJKGulpur Hydro Power project4141

Jun-14100Kotli, AJKKotli Hydel Project3737

Dec-13157Swat, NWFPMadian Hydropower Project3636

Dec-1384Swat, NWFPMatiltan Hydro Power Project3535

Jun-13132Near Mangla, AJKRajdhani Hydro Power Project3434

Dec-1284Near Mangla, AJKNew Bong Escape Hydel Project3333

HYDELHYDEL

24002400Sub Total (Coal)Sub Total (Coal)

Jun-131200Gadani Near KarachiMitsui Imported Coal Project3232

Jun-131200Gadani Near KarachiAES Imported Coal Project3131

40

FUELFUEL--WISE DETAIL OF PROJECTS CURRENTLYWISE DETAIL OF PROJECTS CURRENTLYBEING PROCESSED BY PPIBBEING PROCESSED BY PPIB

Expected CODCapacity (MW)LocationProjectS. No.

13451GRAND TOTAL

4818Sub Total (Hydel)

Jul-161100Kohala, AJKKohala Hydropower Project52

Apr-16840Mansehra, NWFPSuki Kinari Hydropower Project51

Jan-16548Kohistan, NWFPKaigah Hydel Project50

Jun-15102Chitral, NWFPShushgai Zhendoli Hydel Project49

Jun-15127Chitral, NWFPShogosin Hyderopower Project48

Jun-15139Muzaffarabad, AJKChakothi-Hattian Project47

Jan-15197Swat, NWFPKalam-Asrit Hydel Project46

Jan-15215Near Kalam, NWFPAsrit-Kedam Hydel Project45

Dec-14222Sudhnoti, AJKAzad Patan Hydel Project44

Dec-1465Kotli, AJKSehra Hydel Project43

Dec-14115Dir, NWFPSharmai Hydropower Project42

41

Year-wise Capacity Addition by IPPS (2009 - 2016)

27732013

10932014

7802015

13451GRAND TOTAL

24882016

10322012

13442011

15502010

23912009

Capacity (MW)YEAR

Atty. Atty. RovielRoviel V. V. MasiganMasiganAttorney III, Legal Service,Attorney III, Legal Service,

Energy Regulatory Commission (ERC)Energy Regulatory Commission (ERC)

Mr. Ramon C. Mr. Ramon C. AbayaAbayaChairman, Chairman, CagayanCagayan Electric Power and Light Electric Power and Light

Company, Incorporated (CEPALCO)Company, Incorporated (CEPALCO)

Financing Sustainable Financing Sustainable Electrification in the PhilippinesElectrification in the Philippines

(Action Plan)(Action Plan)

Action Plan Outline:Action Plan Outline:

Current ChallengesOpportunitiesKey Actions RequiredKey Actors to be InvolvedTimelineAreas Where Assistance Needed

Current ChallengesCurrent Challenges

• Full implementation of the Electric Power Industry Reform Act of 2001 (EPIRA)– Open Access– Sale and Transfer of Subtransmission Assets

• Full implementation of the Renewable Energy Act of 2008– Promulgation of the Implementing Rules and

Regulations (IRR) – Creation of the National Renewable Energy Board

(NREB)– Creation of the Renewable Energy Management

Bureau (REMB)– Determination of the Feed-In Tariff System (FITS)

Opportunities Opportunities

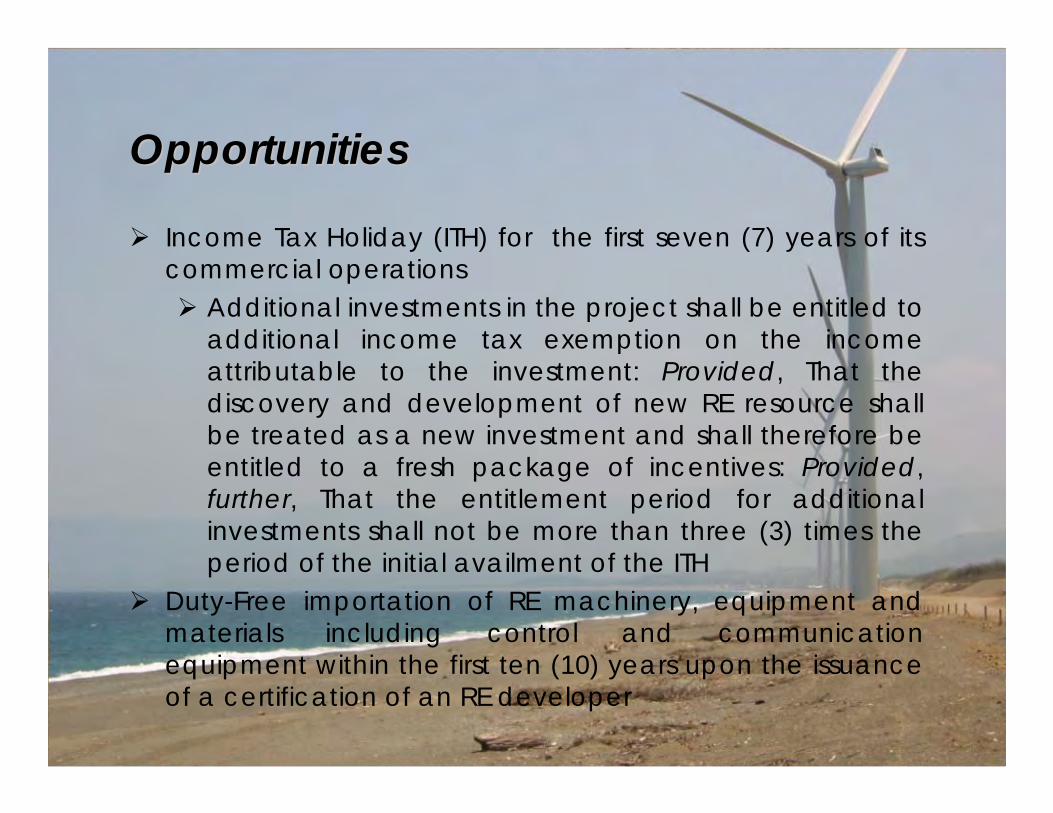

Income Tax Holiday (ITH) for the first seven (7) years of its commercial operations Additional investments in the project shall be entitled to

additional income tax exemption on the income attributable to the investment: Provided, That the discovery and development of new RE resource shall be treated as a new investment and shall therefore be entitled to a fresh package of incentives: Provided, further, That the entitlement period for additional investments shall not be more than three (3) times the period of the initial availment of the ITH

Duty-Free importation of RE machinery, equipment and materials including control and communication equipment within the first ten (10) years upon the issuance of a certification of an RE developer

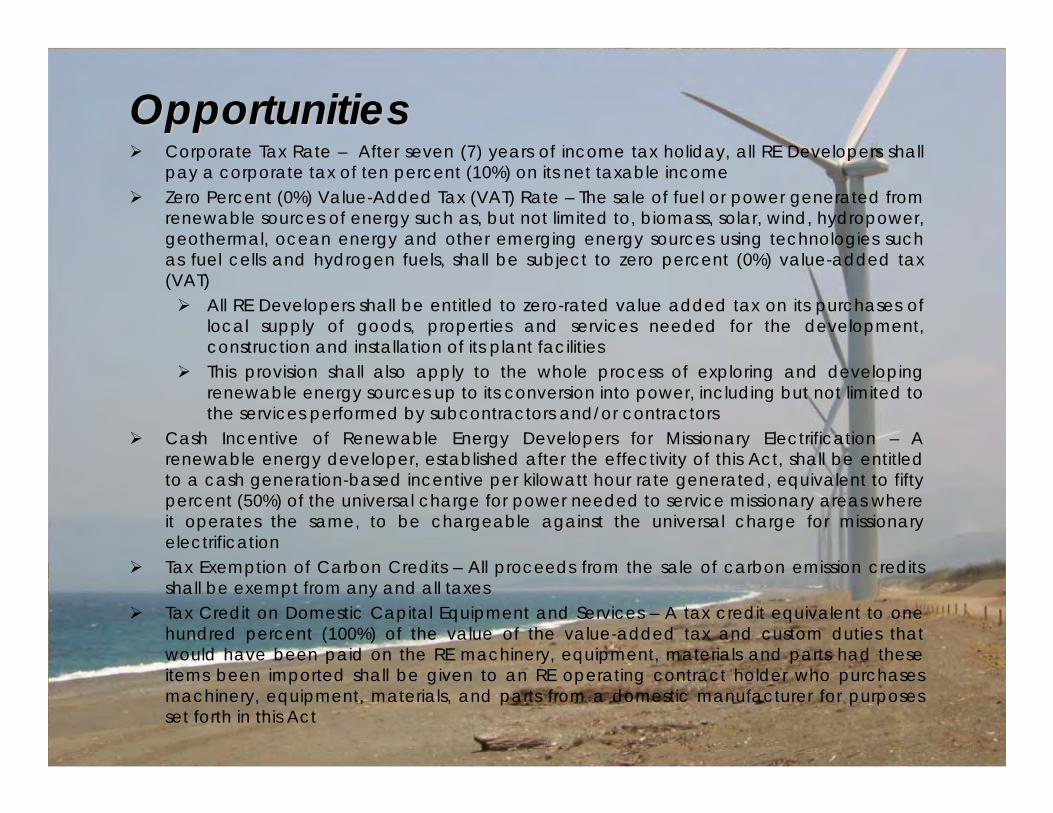

OpportunitiesOpportunities Corporate Tax Rate – After seven (7) years of income tax holiday, all RE Developers shall

pay a corporate tax of ten percent (10%) on its net taxable income Zero Percent (0%) Value-Added Tax (VAT) Rate – The sale of fuel or power generated from

renewable sources of energy such as, but not limited to, biomass, solar, wind, hydropower, geothermal, ocean energy and other emerging energy sources using technologies such as fuel cells and hydrogen fuels, shall be subject to zero percent (0%) value-added tax (VAT) All RE Developers shall be entitled to zero-rated value added tax on its purchases of

local supply of goods, properties and services needed for the development, construction and installation of its plant facilities

This provision shall also apply to the whole process of exploring and developing renewable energy sources up to its conversion into power, including but not limited to the services performed by subcontractors and/or contractors

Cash Incentive of Renewable Energy Developers for Missionary Electrification – A renewable energy developer, established after the effectivity of this Act, shall be entitled to a cash generation-based incentive per kilowatt hour rate generated, equivalent to fifty percent (50%) of the universal charge for power needed to service missionary areas where it operates the same, to be chargeable against the universal charge for missionary electrification

Tax Exemption of Carbon Credits – All proceeds from the sale of carbon emission credits shall be exempt from any and all taxes

Tax Credit on Domestic Capital Equipment and Services – A tax credit equivalent to one hundred percent (100%) of the value of the value-added tax and custom duties that would have been paid on the RE machinery, equipment, materials and parts had these items been imported shall be given to an RE operating contract holder who purchases machinery, equipment, materials, and parts from a domestic manufacturer for purposes set forth in this Act

OpportunitiesOpportunities

The government share on existing and new RE development projects shall be equal to one percent (1%) of the gross income of RE resource developers resulting from the sale of renewable energy produced and such other income incidental to and arising from the renewable energy generation, transmission, and sale of electric power except for indigenous geothermal energy, which shall be at one and a half percent (1.5%) of gross income To further promote the development of RE projects, the government

waives its share from the proceeds of micro-scale projects for communal purposes and non-commercial operations, which are not greater than one hundred (100) kilowatts

Key Actions Required Key Actions Required

Funding Development Bank of the Philippines (DBP) Land Bank of the Philippines (LBP) Philippine Export-Import Bank Other Government Financial Institutions (GFIs)

The foregoing shall, in accordance with and to the extent allowed by the enabling provisions of their respective charters or applicable laws, provide preferential financial packages for the development, utilization and commercialization of RE projects as duly recommended and endorsed by the DOE

Information dissemination for foreign investors

Key Actors to be Involved Key Actors to be Involved Board of Investments (BOI) Department of Energy (DOE) Department of Environment and Natural Resources (DENR) Department of Finance (DOF) Department of Science and Technology (DOST) Department of Trade and Industry (DTI) Distribution Utilities (DUs) Energy Regulatory Commission (ERC) Generation Companies National Power Corporation (NPC) National Transmission Corporation (TRANSCO) National Grid Corporation of the Philippines (NGCP) – concessionaire of

TRANSCO Philippine Electricity Market Corporation (PEMC) Philippine National Oil Company (PNOC) Renewable Energy Developers Investors

TEPCO KANSAI CLP Alstom GE

TimelineTimeline Creation of NREB

January 2010 Creation of REMB

January 2010 Formulation of Feed-In Tariffs System

2010 Open Access

2011 Full Implementation of the RE Act

2013

Areas Where Assistance Needed Areas Where Assistance Needed Funding from Foreign Financial Institutions

World Bank ADB

Information Dissemination Formulation of attractable Feed-In Tariffs

UNDESA

Thank You!Thank You!

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

e8-GEF-UNDESA-UNESCAP Financing Sustainable Electrification

South-East Asia DialoguesBangkok, Thailand, September 10, 2009

Country Action Plan

Sri Lanka

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

ACTION PLAN OUTLINE TO ATTRACT INVESTMENTS

1. Policy Elements 2. Obstacles 3. Challenges 4. Opportunities 5. Key Action Required 6. Key Actors to be involved7. Time Line 8. Areas where assistance needed 9. Country Action Plan Summary

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

Country Outlook

• Population 20Mn (2008)• Area 65610km2

• Installed Capacity 2656MW (2008)– Thermal 1298 MW– Hydro 1205 MW– Mini Hydro 138 MW– Bio Mass 12 MW– Wind 3 MW

• Electrification level 82% (2008)• Electricity consumers 4Mn • Total Generation 9,815 GWh• System losses 15.5%

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

1. Policy Elements

• Provide basic energy needs to all • Ensure energy security • Promote energy efficiency and conservation • Promoting indigenous resources • Adopting appropriate pricing policy • Enhancing energy sector management capacity • Consumer protection and ensuring level playing fields • Enhance quality of energy services • Protection from adverse environmental impacts of

energy facility

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

2. Current Obstacles

• Project feasibility is time taking • Extended project approval process • Some EIA Clearances-time consuming & mitigatory

actions demanded prior to project implementation• Procurement guidelines• Time consuming PPA negotiation• Sovereign Guarantees – feasible / unfeasible • Stringent bank due diligence • Lack of proposals by the IPPs• Lack of capacity for Public Private Partnerships

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

3. Challenges

• Country Risk – perception differences among investment parties

• High finance cost • Inadequate Infrastructure for most of the

potential renewable project • Micro & Macro economic issues (high inflation;

$/LKR parity, high cost of labor)• Electricity at affordable tariff• Limited hydro resources & non availability of

fossil fuel • System Losses and inefficiency

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

4. Opportunities

• Increasing power demand 7-8% annually • Low cost funding • Favorable renewable energy policy - 10% of net

generation by 2015• Huge wind, solar and biomass potential • Technology base Feed in Tariff system • Increase efficiency & rehabilitation of existing old

plants • Transforming power system into low cost power

generation methods • Well established BOI for encouraging investments • Political stability and government will

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

5. Key Actions Required

• Build low cost power plants and add renewable energy resource to the grid

• Grid enhancement & augmentation • Improvement in other infrastructure to attract investors • Ease the project approval process • Expedite EIA / Approval processes • System improvements and minimizing losses• Strengthen the capacity of PPP Unit through the BOI

by 2010

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

6. Key Actors to be Involved

• Government organizations • Utility companies • Financial institutions • Power producers • Public

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

7. Timeline

• Coal Power by 2011 • Grid enhancement by 2012 • Infrastructure development – immediately • Specific time frame for project development • Specific time frame to EIA / Approvals • Immediate action on system loss and inefficiency

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

8. Areas where Assistance Needed

• Improving regulatory framework by sharing experience among countries

• Low cost funding • Capacity building in PPP mechanism to help analysis

the proposals put forward to the government• Assistance to grid capacity enhancement • Assist in project preparatory works such as feasibility,

EIA and Detail Designs, etc

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

9. Country Action Plan Summary

•Build low cost power plants and add renewable energy resource to the grid •Grid enhancement & augmentation •Improvement in other infrastructure to attract investors •Ease the project approval process •Expedite EIA / Approval processes •System improvements and minimizing losses•Strengthen the capacity of PPP Unit through the BOI by 2010

Key Actions Required/Objectives

•Improving regulatory framework by sharing experience among countries •Low cost funding •Capacity building in PPP mechanism to help analysis the proposals put forward to the government•Assistance to grid capacity enhancement •Assist in Project preparatory works such as feasibility, EIA and Detail Design etc

•Coal Power by 2011 •Grid enhancement by 2012 •Infrastructure development –immediately •Specific time frame for project development •Specific time frame to EIA / Approvals •Immediate action on system loss

and inefficiency

Government organizations Utility companies Financial institutions Power producers

Public

•Increasing power demand 7-8% annually •Opportunities for low cost funding •Policy on renewable resources - 10% by 2015 about 450MW •Reduce system losses •Increase efficiency & rehabilitation of existing old plants •Transforming power system into low cost power generation methods •Eliminate grid constraints •Harness renewable resource •Political stability and government will

•Project feasibility is time taking •Extended project approval process •Some EIA Clearances-time consuming & demand mitigatoryactions prior to implementation•Procurement guidelines•Time consuming PPA negotiation•Sovereign Guarantees –feasible / unfeasible •Stringent bank due diligence •Lack of proposals by the IPPs•Lack of guidelines for PPP

Areas of Assistance

TimelineKey Actors to be

Involved

OpportunitiesCurrent obstacles

and challenges

e8-G

EF-U

ND

ESA

-UN

ESC

AP

Fina

ncin

g Su

stai

nabl

e El

ectr

ifica

tion

HC

B In

itiat

ive

Sout

h-Ea

st A

sia

Dia

logu

es, S

epte

mbe

r 8-

10, 2

009,

Ban

gkok

, Tha

iland

Focal Point Contact InformationName/Title:

Mr. Rajapakse PremalalChief Accountant Ministry of Power & Energy

Sri Lanka Email:

Tel: +94 112 687360Fax: +94 112 687360

1

E8-GEF-UNDSA-UNESCAPFinancing Sustainable Electrification

THAILAND Action plan-Proposes Outline

2

Enhanced Single Buyer (ESB) ModelEnhanced Single Buyer (ESB) Model

EGATGen.

EGATEGATGen.Gen.

EGAT Transmission

System Operator (SO) Single Buyer (SB)

EGAT TransmissionEGAT Transmission

System Operator (SO) Single Buyer (SB)System Operator (SO) Single Buyer (SB)

ForeignPower

Purchase

ForeignForeignPower Power

PurchasePurchaseSPPSPPSPP

PEAPEAPEA

DirectCustomer

DirectDirectCustomerCustomer

End UserEnd UserEnd User

MEAMEAMEA

Regulator

IPPIPP

VSPPVSPPVSPP

33

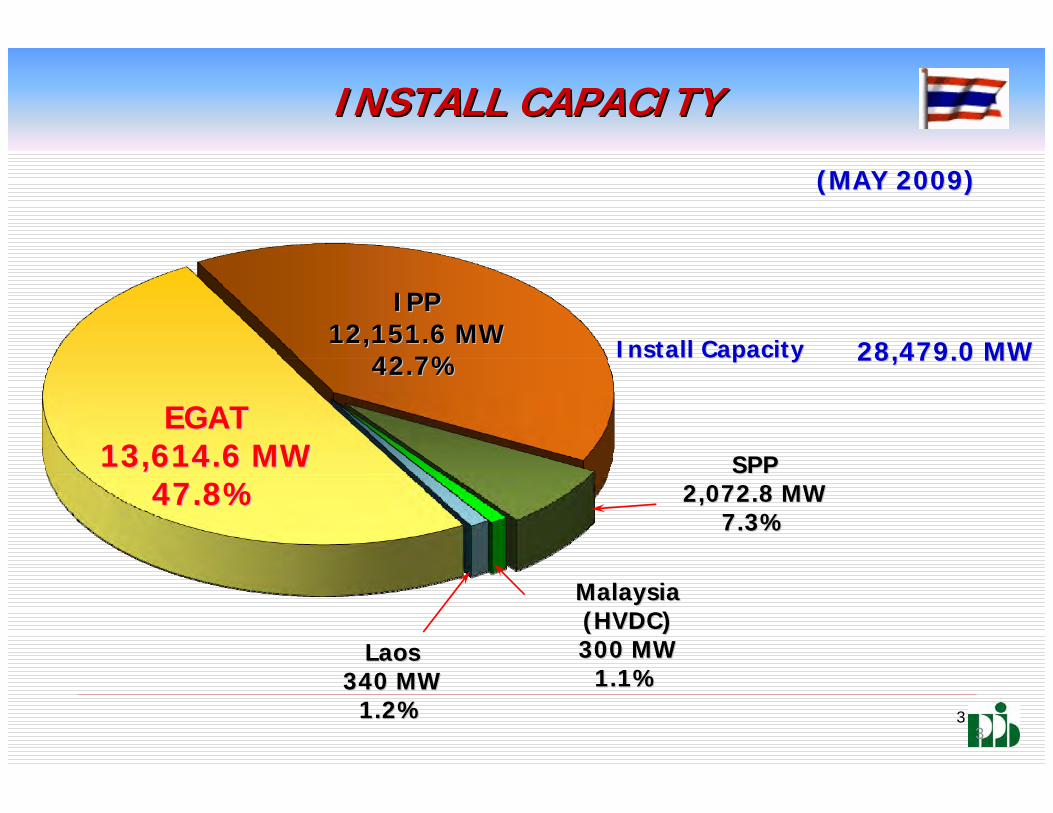

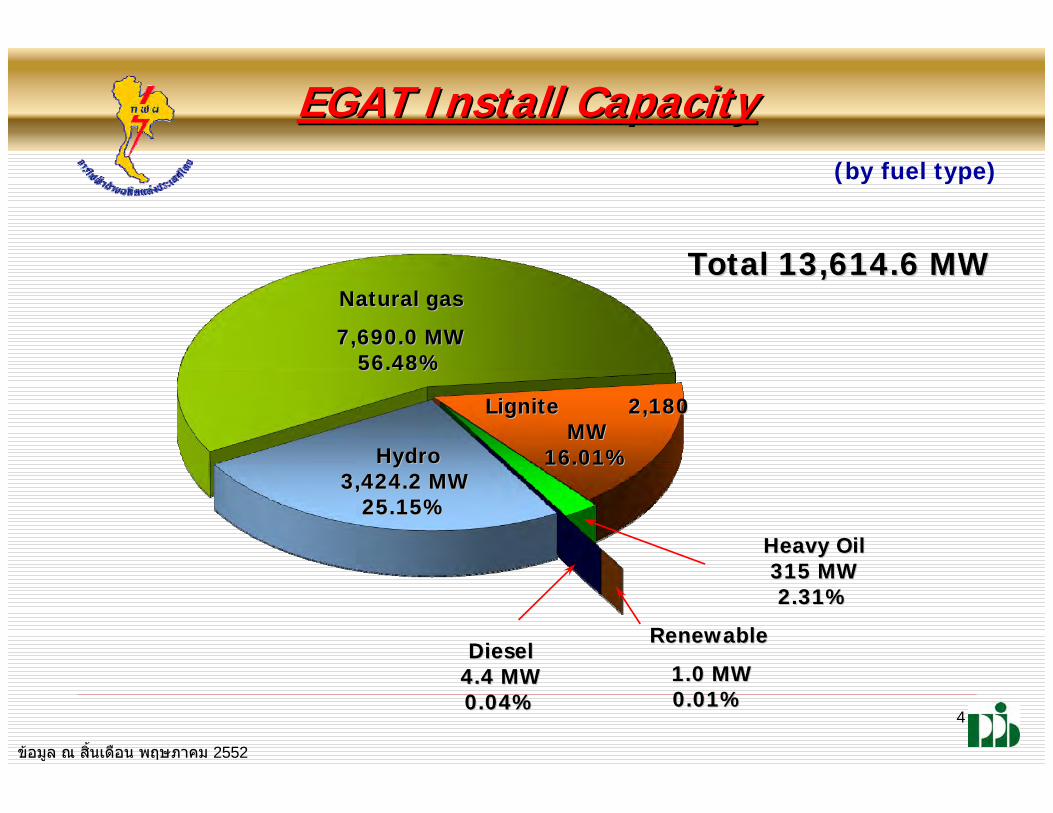

EGATEGAT13,614.6 MW13,614.6 MW

47.8%47.8%

IPPIPP12,151.6 MW12,151.6 MW

42.7%42.7%