political risk outlook investment pack - march 2015

TRANSCRIPT

www.politicalmonitor.com.au

Political risk outlook – investment pack March 2015

OUTLINE

This presentation provides a summary of Political Monitor’s monthly Political risk outlook

– investment pack. It includes Political Monitor’s proprietary risk scores and indices and

domestic, regional and global analysis of the commercial implications of political trends

and events.

To find out more about subscribing to the full monthly pack please contact:

Damian Karmelich Steve Cusworth

Partner – Sydney Partner - Melbourne

p. 0407 772 548 p. 0417 178 697

CONTENTS

• Australian Political Risk Outlook …………………………………………………………… p. 5

• State in focus: Queensland ……………………………………………………… p. 7

• Asia Political Risk Outlook ………………………………………………………………….. p. 9

• Country in focus: Indonesia …..……….…… ……..……....… ……...….……... p. 12

• Country in focus: Philippines ……………………………….…………………… p. 13

• Country in focus: Viet Nam …………….…… ……..….………..… …………... p. 14

• Global issues ………………………………..………………………….….……………..….. p. 15

• Appendix 1 – Australian Political Risk Index methodology…….……………...……..….. p. 21

• Appendix 2 – Political risk spread methodology ……………………………………..…… p. 22

• Appendix 2 - Economic & investment impact of political and social instability ……..… p. 23

Political risk outlook 3

AUSTRALIAN POLITICAL RISK OUTLOOK

AUSTRALIAN POLITICAL RISK INDEX – domestic & global

events pushed the index to its second highest level in 10 months

Political risk outlook 5

0

2

4

6

8

10

12

14

16

18

Po

litic

al U

nce

rtai

nty

Sco

re

Australian Political Risk IndexSource: Political Monitor

AUSTRALIAN POLITICAL RISK INDEX – domestic & global

events pushed the index to its second highest level in 10 months

Political risk outlook 6

• The political crisis surrounding Prime Minister Tony Abbott’s leadership has brought government business to a standstill and pushed the Australian Political Risk Index to a 10 month high.

• However, long before the prospect of a leadership challenge emerged the index was experiencing high levels of volatility as the Government’s failure to pass key legislation weighed on markets. In particular, ongoing controversy about renewable energy targets, higher education reforms and budget measures all added to concerns about Australia’s policy outlook.

• A change of government in Queensland – Australia’s third largest state – has also added to uncertainty as business tries to come to terms with the implications of Labor’s win. In addition to policy changes, the failure of the Conservative Government to remain in power despite a landslide victory just four years ago adds to the level of political uncertainty across Australia as the electorate proves to be increasingly volatile. Meanwhile, an election in Australia’s largest state of New South Wales (NSW) is due at the end of March.

• Global events are also having an influence on the index as an anti-austerity party comes to power in Greece refocusing investors attention on the challenges confronting the European Union (EU). Meanwhile, Russia continues to cast a shadow over markets as it shows no signs of easing its intrusion into the politics of its neighbours leaving the West with little choice but to consider additional economic sanctions against the Putin regime.

STATE IN FOCUS: QUEENSLAND – A NEW GOVERNMENT HIGHLIGHTS POLITICAL VOLATILITY SWEEPING THE NATION

• Queensland has entered a period of heightened

risk as markets grapple with the policy and

budgetary implications of Labor’s return to

power.

• Minority government, a relatively untested

leader and budget strains all suggest an

extended period of uncertainty for Queensland

businesses.

• Furthermore, the Labor caucus will have to deal

with the return of a number of former Ministers

swept out of office in the 2011 Newman

landslide who are likely to demand senior roles

in the new government, each with strong policy

preferences and some with leadership

aspirations. This will create tensions for the new

government.

Political risk outlook 7

0

20

40

60

80

100

120

140

Total RiskScore

Budget Risk Policy Risk Stability Risk ReputationalRisk

State Political Risk Index - February 2015

NSW Vic Qld WA SA Tas

STATE IN FOCUS: QUEENSLAND – A NEW GOVERNMENT HIGHLIGHTS POLITICAL VOLATILITY SWEEPING THE NATION

• Queensland’s Budget risk remains elevated with strained finances and a new government opposed to

raising much needed cash through asset sales. This leaves the budget in a precarious position with little

room to invest in much needed infrastructure.

• Stability risk is very high with the new government failing to command a majority in the parliament and a

crop of inexperienced MPs taking senior leadership positions. Furthermore, the return of a number of MPs

who were Ministers in the former Bligh Government is likely to create leadership tensions.

• Reputational risk is very high with the only daily newspaper having campaigned heavily against the new

government and polls showing Labor having only a small margin for error before public dissatisfaction sets

in.

• As the new government beds down its operations and direction, it can be expected that a number of

indicators will come down from their very high/extreme levels in the near future, however the range of

challenges facing the new government will result in an elevated risk profile for some time ahead.

Political risk outlook 8

ASIA POLITICAL RISK OUTLOOK

ASIA POLITICAL RISK OUTLOOK – rising food prices are fueling tensions across the region

Political risk outlook 10

• Despite recent monthly declines in its food price index the United Nations Food and Agriculture Organization has recorded a sustained rise in food prices over the last 15 years.

• The rising price of food has been accompanied by growing inequality across the region, which have been a source of tension within many countries.

• Emerging markets generally suffer more from rising food prices as a larger proportion of household budgets are committed to foodstuffs.

• Rising food prices were a critical factor in the Arab spring uprisings, which brought thousands of residents to the streets angry at the failure of largely corrupt governments to respond quickly to the stress many households were feeling.

50.0

100.0

150.0

200.0

250.0

300.0

1990199219941996199820002002200420062008201020122014

Annual Food Price IndicesUN Food & Agricultural Organisation

Food Price Index Meat Price Index

Dairy Price Index Cereals Price Index

Oils Price Index

ASIA POLITICAL RISK OUTLOOK – rising food prices are fueling tensions across the region

Political risk outlook 11

• Volatility adds to concerns as household budgets become more difficult to manage, particularly for low income earners.

• In a number of countries – including India and Indonesia – food and fuel subsidies are being removed as part of broader efforts to reduce pressure on government budgets and tackle corruption.

• While over the long term these reforms are likely to benefit the economy and allow government to better target support programs to low income households there is considerable community disquiet about the removal of subsidies threatening the electoral prospects of a number of governments.

• However, these tensions may ease if the recent decline in commodity prices continue.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Domestic food price volatility index(Food & Agriculture Organisation, United Nations)

Eastern Asia Southern Asia South-Eastern Asia

COUNTRY IN FOCUS: INDONESIA – ECONOMIC GAINS BALANCE AGAINST POLITICAL CHALLENGES

• Markets are impressed with President Joko

Widodo’s willingness to push ahead with key

reforms such as winding back fuel subsidies and

tackling corruption. These have been major factors

in the narrowing of Indonesia’s political risk spread.

However, a number of significant political

challenges remain.

• Widodo’s lack of a parliamentary majority remains a

major obstacle to his reform agenda. His

parliamentary weakness makes him more

dependent upon old-guard elements of his own

party for whom combatting corruption is not a

priority and economic reform takes a back seat to

electoral populism.

• The battle between the reform minded Widodo and

old-guard Indonesian politicians will define his

presidency throughout 2015 as both voters and

markets seek to determine whether the President

can turn his best intent into concrete political

outcomes.

Political risk outlook 12

145

155

165

175

185

195

Indonesia political risk spread

114001160011800120001220012400126001280013000

USD : IDR

COUNTRY IN FOCUS: PHILIPPINES – OUTLOOK WEAKENS AS SOCIAL COHESION FRAYS• The Philippines political risk spread has widened to its

highest level in 12 months as social and political

instability in the south continues to be a source of

national tension and President Aquino faces calls for him

to resign.

• A failed attempt by police forces to capture two terror

suspects at the beginning of the year has returned the

issue of separatism in the south to the front pages

placing doubt over the stability of the country and the

leadership of President Aquino.

• The resultant political crisis has removed any remaining

political capital held by the President limiting his

capacity to push through economic reforms. The

President will also have little ability to impact the

outcome of the presidential election in 2016 in which he

will not be a candidate.

• Hopes of a peaceful resolution to the 40 year separatist

campaign have now faded with attitudes in the north of

country hardening against a peace deal.

• High levels of youth unemployment and poverty are

adding to the social and political tensions.

Political risk outlook 13

35

40

45

50

55

60

65

Political risk spread - Philippines

42.5

43

43.5

44

44.5

45

45.5

USD : PHP

COUNTRY IN FOCUS: VIET NAM – ECONOMY REMAINS FOCUS AS POLITICAL TRANSITION BEGINS

• Viet Nam’s political risk spread has narrowed as

economic reform remains the top priority for the

country’s leadership. However, key political and

strategic challenges lie ahead.

• Viet Nam is entering a period of political transition

as it begins the process of selecting a new

leadership. This byzantine process will consume the

political elite throughout 2015 as reformist and

conservative forces wage battle for key leadership

positions to be announced in 2016.

• At the same time Viet Nam is straddling Asia’s

strategic divide as it seeks to maintain healthy

relations with the region’s two dominant powers –

China and the United States.

• However, its disputes with China over access to key

sea lanes and its interest in joining the US led Trans-

Pacific Partnership, which excludes China, will add

to tensions in the region and be a key focus of

leadership deliberations throughout 2015.

Political risk outlook 14

110

130

150

170

190

210

Political risk spread - Viet Nam

0500

100015002000250030003500

20

05

-01

-01

20

05

-11

-01

20

06

-09

-01

20

07

-07

-01

20

08

-05

-01

20

09

-03

-01

20

10

-01

-01

20

10

-11

-01

20

11

-09

-01

20

12

-07

-01

20

13

-05

-01

20

14

-03

-01

US imports / exports - Viet Nam

Exports

Imports

GLOBAL ISSUES

CRISIS IN EUROPE – Greek elections remind markets that the

Euro-crisis is yet to be resolved

Political risk outlook 16

• The election of the left-wing Syriza party in Greece and ascension of Alex Tsipras to the Prime Ministership, supported by a collection of far left and right parties, is a reminder of both the discontent still prevalent across the European electorate and that the Euro-crisis has been postponed, not resolved.

• While all parties claim to want a negotiated outcome there are growing tensions within the EU political elite with some seeking an accommodation of Greece to avoid a Grexit while others recognise that allowing Greece to escape its bailout conditions will strength the hand of similar movements across Europe. The governments of Spain, Portugal and Italy are likely to come under particular pressure if they have proved unable to negotiate an outcome for their countries similar to that of Greece.

• The current situation is a reminder that Europe can not kick its problems down the road indefinitely and that it is rapidly approaching the point at which the continent’s leaders must find an enduring political solution to what has been a political problem over a decade in the making.

• The political weakness at the heart of Europe is also evident in its continued inability to craft a decisive response to Vladimir Putin’s posturing in the east. Europe is split between those attracted to Putin’s anti-West rhetoric, those who simply don’t wish to upset a major energy supplier and those pushing for a more robust response. The resultant lackluster response from Europe lays bare the political crisis at the heart of the European project.

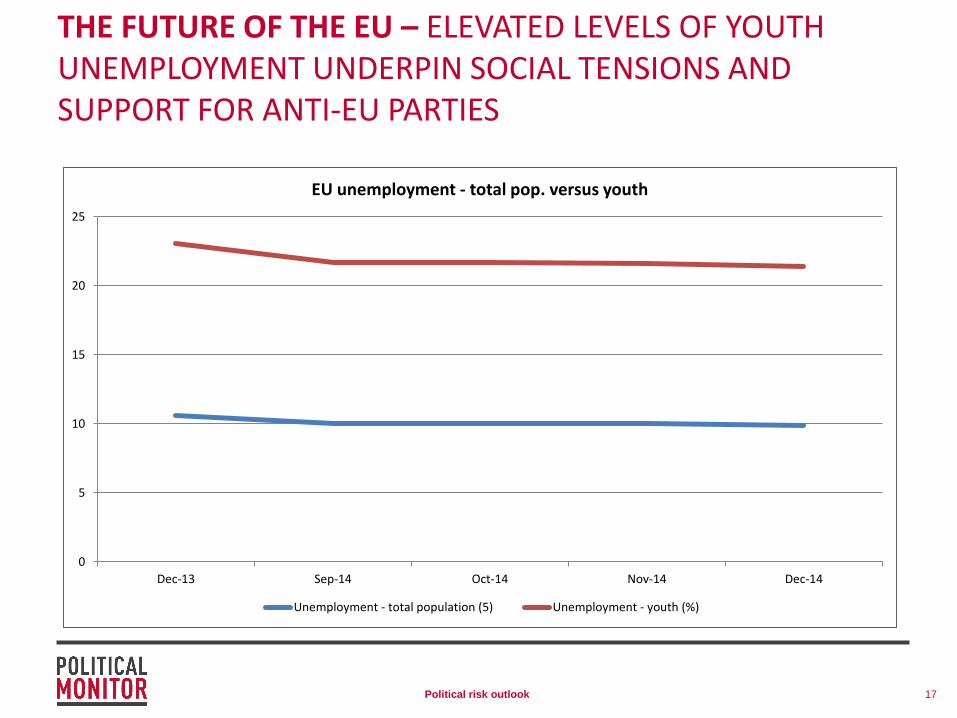

THE FUTURE OF THE EU – ELEVATED LEVELS OF YOUTH UNEMPLOYMENT UNDERPIN SOCIAL TENSIONS AND SUPPORT FOR ANTI-EU PARTIES

Political risk outlook 17

0

5

10

15

20

25

Dec-13 Sep-14 Oct-14 Nov-14 Dec-14

EU unemployment - total pop. versus youth

Unemployment - total population (5) Unemployment - youth (%)

THE WEST DOESN’T UNDERSTAND PUTIN – markets must

recognise that volatility will remain until a political solution is

found

Political risk outlook 18

• The West continues to respond to Russia’s increasing aggression with economic measures in the belief that this will give President Vladimir Putin and his network pause for thought. But this is a fundamental misreading of events in which an economic solution is being sought to a political crisis.

• To understand Putin’s behaviour take a look at a map. To the north is the Artic, which is rich in resources but provides little access for the Russian navy to the sea-lanes of the world. This makes warm water ports of vital strategic importance.

• To the south is China and Kazakhstan with the resource rich ‘Stans beyond. They were once an important buffer for the motherland but are now the subject of a global battle for influence and resources.

• To the south-west is the Black Sea and the warm water port of Sevastopol in Crimea, providing critical access to the Mediterranean and beyond. This waterway is of paramount importance for Russia as is controlling land based access routes. No amount of economic sanctions will change this reality or dissuade Putin from his pursuit of security. Such a search for security has pre-occupied Russia’s rulers since before Peter the Great.

• Investors anticipating an easing of tensions as sanctions begin to bite must understand that Putin views the world through a political prism, not an economic one. Sanctions are likely to remain and Russia’s economy likely to deteriorate for some time yet. Resolution will come from either the collapse of Putin’s regime, an easing of Western sanctions or a recognition that they have failed as Russia continues to do business with China and a host of smaller countries that continue to drift from the West’s orbit. None of these will happen quickly.

Detailed analysis on these and other political risks confronting investors can be found at

www.politicalmonitor.com.au

To find out more contact:

Damian Karmelich Steve Cusworth

Partner - Sydney Partner - Melbourne

p. 0407 772 548 p. 0417 178 697

e. [email protected],au e. [email protected]

About Political Monitor

Political Monitor is a political risk research and advisory firm. Our analysis provides

insight into the implications of political risk for commercial valuations, asset selection,

investment decisions, strategic planning and operational decisions.

Political risk outlook 19

DISCLAIMER & COPYRIGHT

Disclaimer

Information in this document is subject to change without notice and does not represent a commitment on the part of Seller.

Seller does not warrant the accuracy, completeness or timeliness of any of the data and/or programs (“Information”) available within the report.

The Information is provided “as is” without warranty of any kind, express or implied, including, but not limited to, implied warranties of

merchantability, fitness for a particular purpose, title or non-infringement.

In no event will Seller or its affiliates be liable to any party for any direct, indirect, special, consequential or other damages for any use of or

reliance upon the Information found within the report, or on any other reference documentation, including, without limitation, lost profits,

business interruption, loss of programs or other data, even if Seller is expressly advised of the possibility of such damages.

The disclaimer is in addition to the specific terms and conditions that apply to the products or services offered by Seller.

Copyright

Copyright © Political Monitor Pty Ltd 2015. This document is copyright and contains confidential information that is the property of Seller. Except

for the purposes of executing or applying this report, no part of this document may be copied, stored in a retrieval system or divulged to any

other party without written permission. Such rights are reserved in all media.

Intellectual property rights associated with the methodology applied in arriving at this document, including templates and models contained there

in, reside with Political Monitor Pty Ltd, excepting client information it contains that is demonstrably proprietary to the client or covered by an

agreement or contract defining it as such.

No part of this report may be reproduced, transmitted, stored in a retrieval system, or translated into any language in any form by any means,

without the written permission of Political Monitor Pty Ltd.

© Political Monitor Pty Ltd 2015. All Rights Reserved . ACN 166 162 572.

Political risk outlook 20

APPENDIX 1 - AUSTRALIAN POLITICAL RISK INDEX METHODOLOGY

The Political Monitor Australian Political Risk Index is a dynamic index that tracks the

level of policy uncertainty in Australia relying on a number of variables including

market volatility and the dispersion of private sector economic forecasts. The index is

refreshed daily providing an up to date gauge of political and policy uncertainty.

Political risk outlook 21

APPENDIX 2 – POLITICAL RISK SPREADS• The Political Monitor political risk spread is a proprietary score that quantifies the component of a

country’s sovereign risk spread (the difference between yields on 10 year US Treasuries and

comparable debt in respective countries) attributable to political factors such as stability of

government, judicial independence, corruption, poverty levels, food security and a range of

demographic factors such as the size of the population under the age of 30.

• The political risk spread allows investors to make a clearer distinction between the different types of

risk that influence sovereign yields. This approach means investors can distinguish between political

risks and more general economic risks when assessing country specific investments.

• The scores are refreshed daily for countries where publicly available data on bond yields are

available. They are general in nature and do not take into account the capacity of individual firms to

manage and mitigate political risk in each market.

• Political Monitor provides political risk spreads for 15 nations across Asia and 7 in which Australia’s

major mining companies have operations.

Political risk outlook 22

APPENDIX 3 - ECONOMIC & INVESTMENT IMPACT OF POLITICAL & SOCIAL INSTABILITY – DOES IT MATTER?• Political risk is the second ranked concern for publicly traded companies … "Looking ahead, investors

continue to be wary about the effects of systemic risk, politics and regulation on the world's markets and

how they'll perform.” (BNY Mellon, Global Trends in Investor Relations, 2014).

• In general political instability results in:

• (a) lower economic growth (Aisen & Veiga, 2013)

• (b) reduced private sector investment (Alesina & Perotti)

• (c) increased inflation levels & volatility (Aisen & Veiga, 2008).

• The economic effects of political & social instability remain for an observable period of 2 – 3 years. The key

determinant of whether the effect of instability ceases at that point is the speed with which countries

implement reforms & improve governance (Bernal-Verdugo, Furceri & Guillaume, IMF Working Paper,

2013).

• An increase in economic policy uncertainty foreshadows a decline in economic growth and employment in

the following months (Baker, Bloom & Davis, EPU).

• The International Monetary Fund (IMF) estimates the economic loss to Libya, Egypt, Tunisia, Syria, Yemen,

and Bahrain in 2011 at USD$20.56 billion as a result of political and social conflict.

Political risk outlook 23