policy uncertainty and the brexit shockfaculty.chicagobooth.edu/steven.davis/pdf/policy uncertainty...

TRANSCRIPT

Policy UncertaintyAnd the Brexit Shock

Steven J. DavisResearch with Scott Baker and Nick Bloom

US Treasury Department14 September 2016

Today’sRemarks1. ReviewofBBDapproachtomeasuring

EconomicPolicyUncertainty(EPU)2. OurnewestEPUindices3. AcloserlookattheBrexituncertainty

shockanditslikelynear-termeffects

Our Economic Policy Uncertainty Indices rely on computer-automated newspaper searches

• For 10 major US papers, get monthly counts of articles that contain at least one word from each of three term sets:E: {economic or economy}P: {regulation or deficit or “federal reserve” or congress or

legislation or “white house”}U: {uncertain or uncertainty}

Include “the Fed”, “regulatory” and other variants.

• Scale the EPU count for each paper and month by the count of all articles in the same paper and month

• Standardize each paper’s scaled count to unit St. Dev., then sum over the 10 papers by month to get the U.S monthly index 3

HowitworksfortheUnitedStates:

5010

015

020

025

030

0

1985 1990 1995 2000 2005 2010 2015

GulfWar I

9/11

ClintonElection

Gulf War IIBush

Election

Stimulus Debate

Lehman and TARP

Russian Crisis/LTCM

Debt Ceiling Debate

Black Monday

Fisc

al C

liff

Shu

tdow

n

Polic

y U

ncer

tain

ty In

dex

US Newspaper-Based EPU Index, 1985 to Aug. 2016

Source: “Measuring Economic Policy Uncertainty” by Scott R. Baker, Nicholas Bloom and Steven J. Davis, all data at www.policyuncertainty.com. Monthly data normalized to 100 prior to 2010. Data to August 2016

Bre

xit

Euro Crisis, and Midterm Elections

MoreNewspaper-BasedEPUIndices• U.S.category-specificEPUindices• MonthlyEPUindicesfor15countries• HistoricalEPUindicesbackto1900fortheUSandtheUK

• DailyEPUindicesfortheUSandUK• DailyEquityMarketUncertaintyindex• ImmigrationFearandPolicyUncertaintyindicesfortheUS,France,Germany,UK

Downloadableandregularlyupdatedathttp://www.policyuncertainty.com

Selected category-specific EPU Indices, Quarterly0

100

200

300

400

1985 1990 1995 2000 2005 2010 2015Year

National Security Policy UncertaintyHealthcare Policy Uncertainty

Notes: Indices reflect scaled monthly counts of articles containing the same triple as in Figure 1 and one or more terms pertaining tonational security (e.g., “war”, “terrorism”, or “department of defense”) and healthcare (e.g., “healthcare”, “hospital”, or “healthinsurance”), respectively, for the National Security and Healthcare indices. Each series is normalized to mean 100 from 1985-2009 andbased on queries run Jan 18, 2015 on Access World News Newsbank newspaper archive,which covers about1,500 US papers.

Inde

x Va

lue

Gulf War I

Gulf War II

9/11Clinton healthcare reform effort

Affordable care act

NewEPUStatisticalProducts

• Australia,monthly• Brazil,monthly• Global,monthly• UnitedKingdom,daily

EconomicPolicyUncertaintyIndexforAustralia,1998toApril20160

100

200

300

400

1998 2002 2006 2010 2014

Russian Economic Crisis, Close Australian Election FoughtOver GSTIntroduction

9/11Attacks

Invasion of Iraq

Labor Party Wins in

Landslide

Lehman Failure,Global

FinancialCrisis

Fiscal AndMiningPolicyUncertainty,EurozoneConcerns

U.S. Debt

Ceiling Dispute

Rudd Ousts Gillard as Labor Leader and PM

Greek Debt Crisis,Mining Tax &

Carbon Policy Uncertainty

Notes: Index reflects scaled monthly counts of articles in eight Australian newspapers containing “uncertain” or “uncertainty”,“economic” or “economy”, and one or more policy-relevant terms: regulation, “Reserve Bank of Australia”, RBA, deficit, tax, taxation,taxes, parliament, senate, "cash rate", legislation, tariff, war. Normalized to a mean of 100 from 1998 to 2013. Index methods follow“Measuring Economic Policy Uncertainty” by Baker, Bloom and Davis. Data available atwww.PolicyUncertainty.com.

010

020

030

040

050

0Po

licy

Unc

erta

inty

Inde

x

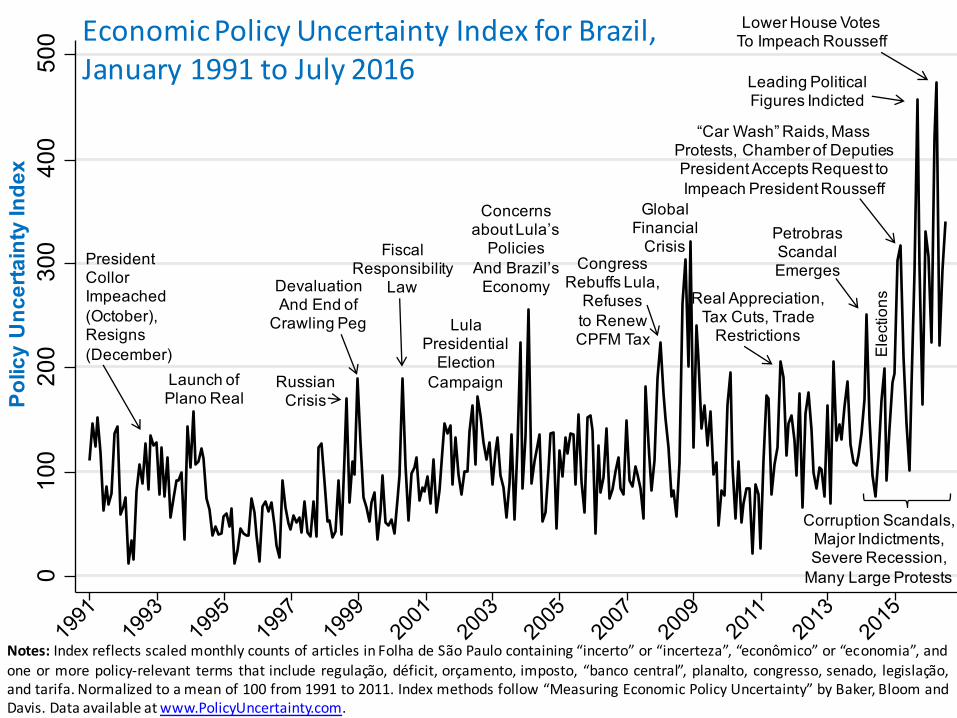

Notes: Index reflects scaled monthly counts of articles in Folha de São Paulo containing “incerto” or “incerteza”, “econômico” or “economia”, andone or more policy-relevant terms that include regulação, déficit, orçamento, imposto, “banco central”, planalto, congresso, senado, legislação,and tarifa. Normalized to amean of 100 from 1991 to 2011. Index methods follow “Measuring Economic Policy Uncertainty” by Baker, Bloom andDavis. Data available atwww.PolicyUncertainty.com.

President CollorImpeached (October), Resigns (December)

Launch ofPlano Real

Russian Crisis

DevaluationAnd End of

Crawling Peg

Fiscal Responsibility

Law

Lula Presidential

ElectionCampaign

Concerns about Lula’s

Policies And Brazil’s

EconomyCongress

Rebuffs Lula, Refuses to Renew CPFM Tax

Lower House Votes To Impeach Rousseff

“Car Wash” Raids, Mass Protests, Chamber of Deputies President Accepts Request to Impeach President Rousseff

Leading Political Figures Indicted

Corruption Scandals, Major Indictments, Severe Recession,

Many Large Protests

Elec

tions

Petrobras Scandal Emerges

Global Financial

Crisis

Real Appreciation, Tax Cuts, Trade

Restrictions

EconomicPolicyUncertaintyIndexforBrazil,January1991toJuly2016

GlobalEPUIndex,January1997toAugust2016

10

25

75

125

175

225

275

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

GlobalEPU,CurrentPricesGDP

GlobalEPU,PPP-AdjustedGDP

Notes: GlobalEPUcalculated astheGDP-weightedaverageofmonthlyEPUindexvaluesfor the US,Canada,Brazil,UK,Germany,Italy,Spain,France,Netherlands, Russia,India,China,SouthKorea,Japan andAustralia,usingGDPdatafrom theIMF’sWorldEconomicOutlookDatabase. Thecountry-levelEPUindexvaluesarefromwww.PolicyUncertainty.com and"Measuring EconomicPolicyUncertainty" byBaker,BloomandDavis. Eachcountry-levelEPUIndexisrenormalizedtoameanof100from1997to2015beforecalculating theGlobalEPUIndex.

Asian&RussianFinancialCrises

9/11GulfWarII

GlobalFinancialCrisis

EurozoneCrises,U.S.FiscalFights,ChinaLeadership

Transition

Brexit

TheBrexitUncertaintyShock

• Asurprisereferendumoutcome• IttriggeredahugespikeinUKEPU• GlobalEPUreverberations• ButconcernsaboutBrexit-relateduncertaintyhaveabatedrapidly,atleastaccordingtoourindices

TheBrexitShockandItsImmediateWake,DailyData

12

1.2

1.25

1.3

1.35

1.4

1.45

1.5

1.55

1.6

1.65

0

500

1000

1500

2000

2500

3000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31

June July

UKDailyEPUIndex(LeftScale)1+LeaveVictoryProbabilityDollar-Pound ExchangeRateNormalizedFTSE250

LeavevictoryprobabilitydatafromOddschecker; FTSE250andPound-Dollarexchangerate fromBloomberg; DailyEPUIndicesfromwww.PolicyUncertainty.com and"Measuring EconomicPolicyUncertainty"byBaker,BloomandDavis.

ABigSurprise!!

TheBrexitShockandItsImmediateWake,DailyData

13

1.2

1.25

1.3

1.35

1.4

1.45

1.5

1.55

1.6

1.65

0

500

1000

1500

2000

2500

3000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31

June July

UKDailyEPUIndex(LeftScale)1+LeaveVictoryProbabilityDollar-Pound ExchangeRateNormalizedFTSE250

LeavevictoryprobabilitydatafromOddschecker; FTSE250andPound-Dollarexchangerate fromBloomberg; DailyEPUIndicesfromwww.PolicyUncertainty.com and"Measuring EconomicPolicyUncertainty"byBaker,BloomandDavis.

MassiveSurgeInUKEPU!!

ABigSurprise!!

TheBrexitShockandItsImmediateWake,DailyData

14

1.2

1.25

1.3

1.35

1.4

1.45

1.5

1.55

1.6

1.65

0

500

1000

1500

2000

2500

3000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31

June July

LeavevictoryprobabilitydatafromOddschecker; FTSE250andPound-Dollarexchangerate fromBloomberg; DailyEPUIndicesfromwww.PolicyUncertainty.com and"Measuring EconomicPolicyUncertainty"byBaker,BloomandDavis.

ButEPUSurgeLargelyReverseswithin2Weeks

TheBrexitShockandItsImmediateWake,DailyData

15

1.2

1.25

1.3

1.35

1.4

1.45

1.5

1.55

1.6

1.65

0

500

1000

1500

2000

2500

3000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31

June July

UKDailyEPUIndex(LeftScale)1+LeaveVictoryProbabilityDollar-Pound ExchangeRateNormalizedFTSE250

LeavevictoryprobabilitydatafromOddschecker; FTSE250andPound-Dollarexchangerate fromBloomberg; DailyEPUIndicesfromwww.PolicyUncertainty.com and"Measuring EconomicPolicyUncertainty"byBaker,BloomandDavis.

FastRecoveryinEquityMarkets

TheBrexitShockandItsImmediateWake,DailyData

16

1.2

1.25

1.3

1.35

1.4

1.45

1.5

1.55

1.6

1.65

0

500

1000

1500

2000

2500

3000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31

June July

UKDailyEPUIndex(LeftScale)1+LeaveVictoryProbabilityDollar-Pound ExchangeRateNormalizedFTSE250

LeavevictoryprobabilitydatafromOddschecker; FTSE250andPound-Dollarexchangerate fromBloomberg; DailyEPUIndicesfromwww.PolicyUncertainty.com and"Measuring EconomicPolicyUncertainty"byBaker,BloomandDavis.

LargeDepreciationInPoundPersists

USDailyEPUIndexTheDailyUSEPUIndexdrawsonhundredsofnewspapersandislessnoisythantheDailyUKEPUIndex.

SmallerresponseforUSEPU,butsamepattern:Largeimpacteffectofsurprisereferendumoutcome,followedbyrapiddissipation.NoapparentEPUeffectbeyondthefirstthreeorfourweeks.

GlobalEPUIndex,January1997toAugust2016

18

25

75

125

175

225

275

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

GlobalEPU,CurrentPricesGDP

GlobalEPU,PPP-AdjustedGDP

Notes: GlobalEPUcalculated astheGDP-weightedaverageofmonthlyEPUindexvaluesfor the US,Canada,Brazil,UK,Germany,Italy,Spain,France,Netherlands, Russia,India,China,SouthKorea,Japan andAustralia,usingGDPdatafrom theIMF’sWorldEconomicOutlookDatabase. Thecountry-levelEPUindexvaluesarefromwww.PolicyUncertainty.com and"Measuring EconomicPolicyUncertainty" byBaker,BloomandDavis. Eachcountry-levelEPUIndexisrenormalizedtoameanof100from1997to2015beforecalculating theGlobalEPUIndex.

Globalindextellsthesamestory:Largeimpacteffect,rapidreturntopre-Brexitlevel

UKMonthlyEPUIndex,January2005toAugust2016

0

200

400

600

800

1000

1200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

March

June

July

August

UKMonthlyIndex:Again,thesamestory.

BBD Time-Series Approach

• Include Monthly EPU Indices in Vector Autoregressive (VAR) statistical models of the sort that macroeconomists routinely use to characterize dynamic co-movements in aggregate data.

• Fit to monthly and quarterly data for the United States and to a dozen countries in a panel VAR.

• Examine Impulse Response Functions to EPU innovations implied by Cholesky orderings.

• Main Question: What do EPU innovations portend for future movements in output growth, investment rates, employment growth, etc.?

20

-.6-.4

-.20

.2

0 6 12 18 24 30 36Months

-2-1

01

0 6 12 18 24 30 36Months

Figure 8: Industrial Production and Employment Responses to EPU Shock,VAR Fit to Monthly U.S. Data

IP R

espo

nse,

%

Notes: VAR-estimatedimpulse responsefunctions for industrialproduction andemployment to an EPUinnovation equal to theincrease in the EPUindex from its 2005-2006to its 2011-2012 averagevalue, with 90 percentconfidence bands.Identification based onthree lags and aCholesky decompositionwith the followingordering: EPU index,log(S&P 500 index),federal reserve fundsrate, log employment,log industrial production.Fit to monthly data from1985 to 2014.

Empl

oym

ent R

espo

nse,

%

-1.5

-1-.5

0.5

0 6 12 18 24 30 36Months

Figure 9: U.S. Industrial Production Response to an EPU Shock,Alternative Samples, Specifications and Identification Assumptions

Notes: The baseline case involves the same sample period, VAR specification and identification as in Figure 8. The other casesdepart from the baseline as indicated. We place EU and VIX after EPU in the ordering. For the “1920-1984” response function, weuse monthly data from 1920 to 1984 on log industrial production and EPU in a bivariate VAR with EPU ordered first.

Indu

stria

l Pro

duct

ion

Res

pons

e, %

Baseline(+ symbols)

Bivariate: EPU and logindustrial production

Six monthsof lags

1920-1984Sample

Adding EU

Adding VIX

Reverse bivariate: log industrial production, EPU

Adding a time trend

No S&P index

Figure 10: Responses to an EPU Shock in a Twelve-Country Panel VARIn

dust

rial P

rodu

ctio

n, %

Months after EPU shock

Notes: Panel-VAR estimatedimpulse response functionsfor industrial production andunemployment to an EPUinnovation equal to theincrease in the average USEPU value from 2005-2006 to2011-2012, with 90%confidence bands.Identification based on threelags and a Choleskydecomposition with thefollowing ordering: EPUindex, log(stock marketindex), unemployment rate,and log industrial production.We use own-country data anda full set of country fixed-effects in the panel VAR.Country-level data areweighted by the square rootof the number of newspapersused in the EPU index. Fit tomonthly data for Canada,China, France, Germany,India, Italy, Japan, Korea,Russia, Spain, UK and theUS from January 1985 toDecember 2014, whereavailable.

Une

mpl

oym

ent R

ate

Res

pons

e -1

.5-1

-.50

0 6 12 18 24 30 36

0.1

.2.3

.4

0 6 12 18 24 30 36

UKMonthlyEPUIndex,January

0

200

400

600

800

1000

1200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

March

June

JulyWhatsizeEPUinnovationintheVARmodelcorrespondstotheBrexituncertaintyshock?Unclear.IfUKEPUsettlesdowntoabout250fortherestof2016,theaveragevaluein2016willbeabout200pointshigherthanin2015.

That’sabouttwiceaslargeastheUSEPUincreasefrom2005-06to2011-12,whichisthesizeoftheimpulseweusedtogeneratetheresponsefunctionschartedIntheprecedingslides.

August

(Really) Crude Quantitative Assessment

- Treat the Brexit uncertainty shock as being twice as large as the EPU innovation that BBD used to generate their IRFs.

- For industrial production, they found a peak negative effect of about 1 log point after 6-12 months.

- Doubling yields a peak negative effect of about 2 log points- The large pound depreciation triggered by the Brexit

referendum outcome may mute this effect. (BBD did not account for the exchange rate channel.)

- GDP is typically less sensitive to shocks than IP, so it’s reasonable to anticipate a somewhat smaller GDP effect –perhaps with a peak effect in the range of -1 log point.

- This estimate seems high, perhaps because it does not fully reflect the aggressive BOE response to the referendum

Summary1. Brexit referendum outcome was a big surprise and a

massive shock to UK EPU, with global reverberations.2. But (concerns about) Brexit-related uncertainty dissipated

very rapidly, according to our EPU indices.3. The British Pound fell more than 10% against the US Dollar

in wake of Brexit referendum, and it remains down. 4. Equity markets, however, rebounded within a few weeks.5. Quantifying the likely near-term output effects of Brexit is

really, really hard – at least for us.6. For industrial production, our VAR models suggest a peak

negative effect of Brexit uncertainty shock of about minus 2 log points 6-12 months later.

7. Best guess for peak GDP response is about -1 log point, after considering less volatile nature of GDP, muting effect of Pound depreciation and aggressive BOE response.

Our Data Are Online at www.PolicyUncertainty.com

• MonthlyEPUindicesfor15countries,includingallG10economies,withmorecountriesintheworks.Regularupdatesinthefirstfewdaysofeachmonth.

• HistoricalEPUindicesbackto1900fortheUnitedStatesandUnitedKingdom• DailyEPUindicesfortheUSandUK,withdailyupdates• Manycategory-specificEPUindicesbackto1985fortheUnitedStates• SpecialU.S.tabulationsfor“governmentshutdown”and“debtceiling”• SpecialU.K.tabulationsforBrexit-relatedEPU.• Dailynewspaper-basedindexofequitymarketuncertaintybackto1985• Migration-relatedFearandPolicyUncertaintyIndicesforFrance,Germany,the

U.K.,andtheU.S.

ReferencesBaker, Bloom, Canes-Wrone, Davis and Rodden, 2014. “Why Has

U.S. Policy Uncertainty Risen Since 1960?” American Economic Review Papers & Proceedings, May 2014.

Baker, Bloom and Davis, 2012. “Has Economic Policy Uncertainty Hampered the Recovery?” in Government Policies and the Delayed Economic Recovery, edited by Lee Ohanian, John B. Taylor and Ian Wright, Hoover Institution Press.

Baker, Bloom and Davis, 2015. “Immigration Fears and Policy Uncertainty,” with Scott Baker and Nicholas Bloom, VoxEU, http://www.voxeu.org/article/immigration-fears-and-policy-uncertainty.

Baker, Bloom and Davis, 2016. Measuring Economic Policy Uncertainty,” NBER Working Paper No. 21633, revised in March 2016. Forthcoming in the Quarterly Journal of Economics.

Davis, 2015. “Regulatory Complexity and Policy Uncertainty: Headwinds of Our Own Making,” Hoover Institution.

Thesepapersandmoreavailableathttp://www.policyuncertainty.com/research.html.

Additional Slides –Not for Prepared Remarks

30

020

040

060

0Fi

nanc

ial R

egula

tion

Unce

rtaint

y

1985 1990 1995 2000 2005 2010 2015Year

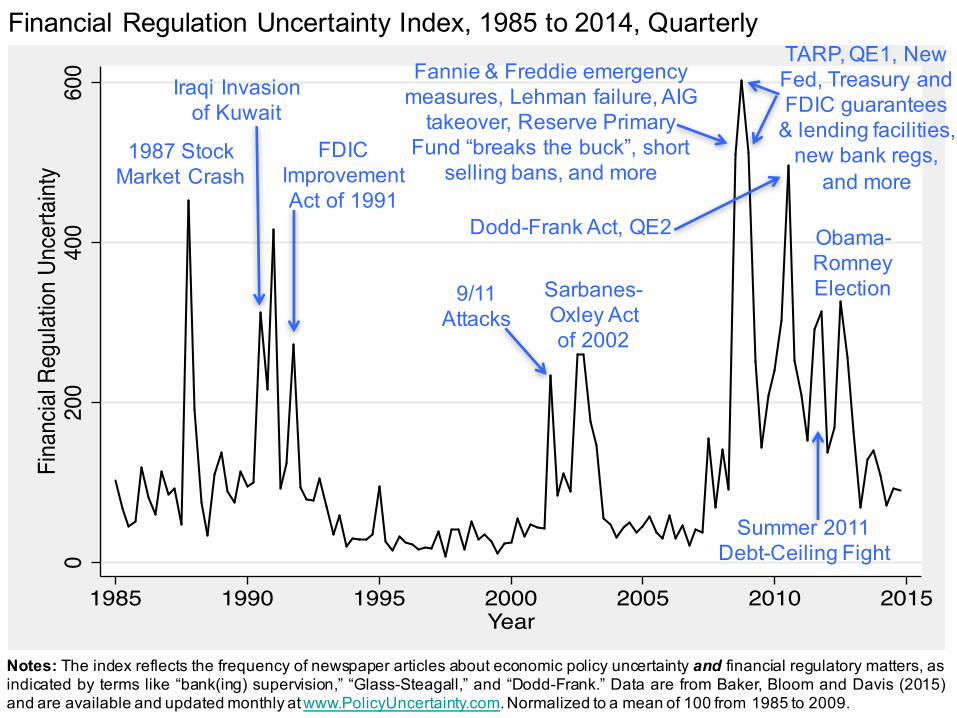

Financial Regulation Uncertainty Index, 1985 to 2014, Quarterly

Notes: The index reflects the frequency of newspaper articles about economic policy uncertainty and financial regulatory matters, asindicated by terms like “bank(ing) supervision,” “Glass-Steagall,” and “Dodd-Frank.” Data are from Baker, Bloom and Davis (2015)and are available and updated monthly atwww.PolicyUncertainty.com.Normalized to a mean of 100 from 1985 to 2009.

1987 Stock Market Crash

Iraqi Invasion of Kuwait

FDIC ImprovementAct of 1991

Sarbanes-Oxley Act of 2002

9/11Attacks

Fannie & Freddie emergency measures, Lehman failure, AIG

takeover, Reserve Primary Fund “breaks the buck”, short

selling bans, and more

TARP, QE1, New Fed, Treasury and FDIC guarantees

& lending facilities, new bank regs,

and more

Dodd-Frank Act, QE2

Summer 2011 Debt-Ceiling Fight

Obama-Romney Election

-8-6

-4-2

0

0 6 12Quarters

-2-1

.5-1

-.50

0 6 12Quarters

USVARforImpactonGDPandInvestment(quarterly)G

DP

Res

pons

e, %

Notes: VAR-estimatedimpulse responsefunctions for GDP andGross Fixedinvestment to an EPUinnovation equal to theincrease in the EPUindex from its 2005-2006 to its 2011-2012average value, with 90percent confidencebands. Identificationbased on three lagsand a Choleskydecomposition with thefollowing ordering:EPU index, log(S&P500 index), federalreserve funds rate, loggross investment, loggross domesticproduct). Fit to datafrom 195 to 2014.

Inve

stm

ent R

espo

nse,

%