poas: dealing with the dysfunctional and non-functional

TRANSCRIPT

POAs: Dealing with the Dysfunctional and

Non-Functional By

Dawn Enoch Moore

CEO, Allegiance Title Company

And

Blair Nash

Senior Counsel, Allegiance Title Company

Texas Land Title Institute December 5-6, 2019

San Antonio, TX

Dawn Enoch Moore | Chief Executive Officer

Dawn Enoch Moore has been a leader in Dallas’ legal and business community for over

37 years. Moore is founder and Chief Executive Officer of Allegiance Title Company, one

of the largest and fastest growing independent real estate title agencies in Texas, with 22

offices and 140 employees in North Texas and Houston.

Moore has served the real estate and title industry in a variety of capacities. She was one

of six lawyers appointed by the State Bar of Texas to the Texas Real Estate Commissions’

Broker/Lawyer Committee, which is responsible for writing the residential purchase/sale

contracts used by real estate licensed holders statewide. She served in this position for

twelve years. She also served as President for the Texas Land Title Association for 2014‐

2015.

Moore had the distinct honor in 1998 of being appointed by then Governor of Texas,

George W. Bush to Chair of the Texas State Affordable Housing Corporation, which

financed thousands of units of affordable housing. Working on behalf of the homeless,

Moore has also served as Chair of the Board of Interfaith Housing Coalition and member

of the Board of Dallas Habitat for Humanity. In 2014, Moore received the Dallas Business

Journal Women in Business Award for her impact in the North Texas business community

and was recently rated the 15th largest North Texas Women-Owned Business Ranked by

2018 Local Revenue.

Moore is active in her community and served The City of University Park for six years as

a City Council member and later as Mayor Pro Tem. Prior to her election to City Council,

she served on the Planning and Zoning Commission and as Chair of the Legislative

Committee of the City. Moore is a member of the Board of the Dallas Zoological Society

and serves as this year’s Chair for the 2019 ZooToDo. She is also a member of the Alliant

National Title Insurance Company and CrossFirst Bank Advisory Board. She is a former

member of the Alumni Board of Trustees for Southern Methodist University. Additionally,

she has served in various leadership roles including Chapter Chair for the Dallas Chapter

of World Presidents’ Organization.

Moore holds a B.S. degree in Economics, graduating Magna cum Laude and a J.D.

degree from Southern Methodist University, receiving the award for the highest grade in

Real Estate Transactions. In 2005, she was awarded the Distinguished Alumni Award

for Corporate Service from the SMU Dedman School of Law.

Married to her husband, Steve, for 39 years, her proudest accomplishments are her

children, two attorneys and one Director of Strategic Marketing for HomeLight.com, and

their newest addition to the family, a granddaughter!

2019 Texas Land Title Institute –POAs: Dealing with the Dysfunctional and Non-functional 1

POAs: Dealing with the Dysfunctional and Non-Functional

A. BACKGROUND:

In a typical residential real estate transaction for a Texas property in a mandatory property owners

association (“POA”),1 the parties and/or the title company will need to be in contact with the POA. There

are both contractual and insurance obligations that necessitate this contact.

i. Contractual

The most commonly used contract form for Texas residential real estate sales is the Texas Real Estate

Commission (“TREC”) One to Four Family Residential Contract (the “TREC Contract”). If applicable, the

parties using this form usually elect to attach the TREC Addendum for Property Subject to Mandatory

Membership in a Property Owners Association (the “Addendum”). The optional Addendum indicates which

parties, if any, are responsible for ordering and paying for the “Subdivision Information” from the POA.

The “Subdivision Information” is defined to include: i) a current copy of the restrictions applying to the

subdivision and the bylaws and rules of the POA, and ii) a resale certificate. Texas Property Code § 207.003

provides that a “resale certificate” must be prepared by the POA and contain certain information, including

but not limited to: whether properties in the subdivision are subject to a right of first refusal that would

restrict the owner’s right to transfer the property; the frequency and amount of regular assessments, and the

amount and purpose of any special assessments that have been approved and will be due after the date of

the resale certificate; the total of all amounts associated with the subject property that are due and unpaid

to the POA; a description of any conditions on the property that are known to be in violation of subdivision

deed restrictions or POA bylaws and rules; POA fees charged in connection with a transfer of the property;

and information related to the status of insurance and the financial health of the POA, including pending

lawsuits, judgments, and budgets.

The Addendum calls for one of four options with regard to obtaining the Subdivision Information from the

POA, generally summarized as follows: 1) the seller is obligated to obtain and pay for it within a set number

of days; 2) the buyer is obligated to obtain and pay for it within a set number of days; 3) the buyer

acknowledges that the seller has already provided the Subdivision Information, but the buyer does or does

not elect to obtain an “updated” resale certificate; or 4) the buyer does not require the Subdivision

Information.

Even if the buyer has already received the Subdivision Information and does not elect to receive an updated

resale certificate, or if the buyer does not require the Subdivision Information at all, the Addendum still

provides for the buyer and seller to elect who will be responsible for paying for the cost of obtaining

additional information from the POA that the title company may need.

ii. Insurability

The title company is able to pull the restrictions applying to the subdivision and the POA’s rules and bylaws

(collectively, the “Dedicatory Instruments”) from the real property records, as Texas Property Code

1 Note: Condominium associations are governed by separate chapters of the Texas Property Code, and dysfunctional

and non-functional condominium associations are generally beyond the scope of this paper, which is concerned with

property in residential subdivisions.

2019 Texas Land Title Institute –POAs: Dealing with the Dysfunctional and Non-functional 2

§ 202.006 requires POAs to record such documents. However, the resale certificate contains some

information that is not found in the property records and may be relevant to title insurance.

For example, the Texas Residential Owner’s Policy of Title Insurance One-to-Four Family Residences (T-

1R) (the “Owner’s Policy”) includes the following as a covered title risk: “There is a lien on your title

because of: . . . [a] charge by a [POA].” Most Dedicatory Instruments provide for an automatic lien on each

lot to secure payment of assessments. Therefore, the title company needs to know the current status of

assessments and to collect any outstanding amounts owed from the seller at closing to prevent liability

related to an existing lien for past-due amounts. Title companies typically look to the resale certificate for

this information.

The Texas Loan Policy of Title Insurance (Form T-2) (the “Loan Policy”) lists the following as an insured

risk: “The lack of priority of the lien of the Insured Mortgage over any other lien or encumbrance.” It is

common for Dedicatory Instruments to expressly subordinate the POA’s assessment lien to purchase money

liens. Any such subordination can be found in the recorded Dedicatory Instruments. However, lenders often

request “endorsements” to their title policies, which are promulgated forms providing additional coverage

beyond that which is normally covered by the Loan Policy. Common endorsements to the Loan Policy

include the T-17, which includes specific coverage for existing violations of certain restrictive covenants

that restrict the use of the land, protections against restrictive covenant provisions that will “cause a

forfeiture or reversion of title,” and failure of title by reason of a right of first refusal that could have been

exercised on the date of the policy; and the T-19,which also includes coverage regarding existing violations

of certain restrictive covenants that affect the lien, and coverage against enforcement of a private right, such

as a right of first refusal, option to purchase, or private assessment, that affects the lien. Therefore,

examination of a resale certificate is also helpful for the title company in transactions where a T-17 and/or

a T-19 will be issued so that issues can be addressed or the lender can be informed of any deletions that the

title company may need to make to the endorsements in situations where issues cannot be adequately

addressed before closing.

iii. Contacting the POA

In order to obtain a resale certificate, the seller, buyer, their agents, or the title company will need to contact

the POA or their management company. Even though the title company can pull the Dedicatory Instruments

from the real property records, most POAs will only provide the resale certificate as part of an order for all

of the Subdivision Information, for which they can charge a “reasonable fee.” Texas Property Code

§207.003 requires a POA to provide an updated resale certificate upon request (which may be for a

reasonable fee, but without requiring the purchase of the entire Subdivision Information), but only if the

request for an updated resale certificate is made within 180 days of the date a resale certificate is issued as

part of an order for the entire Subdivision Information.

The title company can usually get the contact information for the POA directly from the seller.

Alternatively, the title company can get the contact information from the “management certificate” filed in

the real property records. Texas Property Code § 209.004 requires POAs to file a management certificate

containing contact information for the POA and the person(s) or company managing the POA.

But contacting the POA is not always so simple. Occasionally, a once-operational POA falls into

dysfunction. For example, a POA may experience financial difficulties which cause the management

company to resign. If no one steps up to manage the POA, a seller who once paid dues may no longer know

whom to pay. Other times, the subdivision’s restrictive covenants may contemplate that the subdivision

will have a POA, but it is never formally created or operational. In such a situation, there is no management

certificate, and the seller may be totally unaware of any POA in relation to his property.

What options does a title company have to proceed with a transaction when the POA is dysfunctional (the

POA has gone dormant) or non-functional (the POA has never been operational)?

2019 Texas Land Title Institute –POAs: Dealing with the Dysfunctional and Non-functional 3

B. THE DYSFUNCTIONAL POA

In the case of a dysfunctional POA, the title company can still access the Dedicatory Instruments from the

real property records, as discussed above. But with regard to the resale certificate, there are two primary

issues. The first is that, if the buyer has a contractual right to receive the complete “Subdivision

Information” (or an updated resale certificate) under the Addendum, then the buyer also has the contractual

right to terminate the contract and receive the earnest money if the complete Subdivision Information or an

updated resale certificate cannot be obtained. The second issue is how and if the title company can obtain

the information it needs to provide all required insurance coverages.

i. Assessments

With regard to coverage for past-due regular assessments, the title company may not need a resale

certificate. For example, if the Dedicatory Instruments provide for yearly assessments, and the title

company can obtain satisfactory evidence that the dues were paid for the current year, the title company

will not need the POA to provide an update as to the status of regular assessments. If the POA became

dysfunctional after yearly dues were paid and collected, the seller may have documentation of such

payment, which could satisfy the title company. However, it is more common to see monthly or quarterly

dues, in which case it may be more difficult or impossible to prove current payments if the POA has become

dysfunctional. Additionally, there may be special assessments (typically, assessments levied against the

property owners to defray one-time costs for things such as capital improvements or repairs) that are due

and payable that are not disclosed by the recorded Dedicatory Instruments, so the title company would not

know to investigate the status of such payments without information provided by the POA.

Therefore, for situations where a resale certificate or other statement of dues cannot be obtained from the

POA, the Texas legislature has devised an alternative process to protect the title company, buyer, and lender

from liability for past due assessments. Texas Property Code § 207.003(a) provides that a POA is to deliver

the Subdivision Information “not later than the 10th business day after the date a written request for

subdivision information is received . . . .”

If a POA does NOT timely deliver the Subdivision Information in accordance with that provision, Texas

Property Code § 207.004 allows for the following: the owner, owner’s agent, or title company can send a

second request for the Subdivision Information, and if the POA fails to deliver the information “before the

seventh day after the second request for the information was mailed by certified mail, return receipt

requested, or hand delivered, evidenced by receipt,” then:

a. The owner can seek one or more of the following: a court order requiring the POA to

furnish the information, a judgment against the POA for not more than $500, a judgment

for court costs and attorney’s fees, or a judgment authorizing the owner to deduct the

judgment amounts awarded from future assessments; and

b. The owner may provide a buyer under contract to purchase the property an affidavit that

states that the owner, owner’s agent, or title company made two written requests to the

POA for the Subdivision Information in accordance with the statute, and that the POA did

not timely provide the information.

The statute goes on to state that if such an affidavit is provided to the buyer, then: i) the buyer, lender and

title company are NOT liable to the POA for any money that was due and unpaid to the POA on the date

the affidavit was prepared, nor for “any debt to the [POA] or claim by the [POA] that accrued before the

date the affidavit was prepared”; and ii) “the [POA]’s lien to secure the amounts due the [POA] on the

owner’s property on the date the affidavit was prepared shall automatically terminate.”

2019 Texas Land Title Institute –POAs: Dealing with the Dysfunctional and Non-functional 4

On its face, then, it appears that the title company (or owner or owner’s agent) could send the two requests

to the dysfunctional POA and have the owner (the seller) deliver an affidavit to the buyer in accordance

with the above at closing, and then all could rely on the release of liability provided by the statute. It should

be noted that the statute cited above ties the release of liability for unpaid amounts and the termination of

the lien for unpaid amounts to the date the affidavit is prepared, not the date of closing, so it may be best to

ensure the affidavit is prepared and executed to correspond with the closing date. A sample affidavit for

this purpose is attached.

However, it is best practice to consult with the title insurance underwriter before relying on the above

method to close and insure against unpaid assessments, as the statute contains some ambiguity in its

application to dysfunctional POAs. The first step is to send a request to the POA, but no guidance is

provided as to what address may be relied on to accomplish this request. If the management certificate

reflects a management company that the title company knows has resigned from management, is that still

the appropriate address? Can another address for the POA be found? Should a request be sent to any and

all addresses connected to the POA in other records or filings?

The statute also provides that the POA must provide the Subdivision Information “not later than the 10th

business day after the date a written request for subdivision information is received.” (emphasis added).

The failure to comply with that timeline triggers the second request, but there is nothing to indicate how to

know if the request was received. Even if the letter is sent via certified mail, return receipt requested

(“CMRRR,” which is explicitly required for the second request, if not hand delivered, but not the first

request), if the POA is dysfunctional and no one is checking mail for the POA, it might not ever be

“received.”

Furthermore, while the release of liability is triggered by “providing” the affidavit to the buyer, there is no

requirement that the affidavit be recorded. But if the dysfunctional POA were to revive and attempt to assert

its lien against past-due amounts in the future, a recorded affidavit that also includes a statement about it

being provided to the buyer may be the best “proof” of compliance with the statute.

We were unable to find any case law applying the wording of the statute, so given the uncertainty with

regards to the above, all aspects of compliance with the statute should be confirmed with the title insurance

underwriter, addressing the particular facts of the dysfunctional POA situation.

ii. Rights of First Refusal and Restriction Violations

Note that the statutory process described above only protects the buyer, lender, and title company with

regard to amounts due and unpaid on the date the affidavit was prepared, and debt to the POA and claims

by the POA that accrued before the date the POA was prepared. It does not explicitly address other matters

for which a title company typically relies on the resale certificate, such as whether the POA has a right of

first refusal, or whether there are known restrictive covenant violations on the property.

A title company may be able to find in the Dedicatory Instruments whether a right of first refusal is provided

for. The resale certificate simply negates the need to look for it by answering the question for us of whether

or not the Dedicatory Instruments provide for one. However, even if such language is identified, if the POA

is dysfunctional, the owner may not be able to comply with any outlined process for overcoming the right.

For example, a Dedicatory Instrument may provide that, prior to sale, the owner shall notify the POA in

writing of the proposed sale and the terms and conditions thereof, and the POA thereafter may either

approve the sale or disapprove the sale and purchase the property itself on the same conditions. The

Dedicatory Instruments may provide that a sale is “deemed” to be approved if the POA doesn’t respond.

But if no such automatic approval language exists, or if the Dedicatory Instruments do not clearly outline

2019 Texas Land Title Institute –POAs: Dealing with the Dysfunctional and Non-functional 5

how the POA is to be notified (resulting in the same address ambiguities discussed above with regard to

requests for the Subdivision Information), then the title insurance underwriter may decide that deletions

need to be made to the endorsements, which the lender would need to approve.

Restrictive covenant violations also present a challenge if the POA is dysfunctional. The title company does

not physically inspect properties for compliance with restrictive covenants. Schedule B of the Owner’s

Policy will typically contain an exception to coverage for “restrictive covenants of record” found in the

Dedicatory Instruments, so the title company is not generally concerned with violations thereof for an

owner. However, known violations may be relevant to coverage under the T-17 and T-19 endorsements to

the Loan Policy,2 so in the case of a dysfunctional POA, the title insurance underwriter will need to

determine whether such coverages can be provided without deletions.

Please note, however, that even if the title company is able to provide all requested coverages, or if lender

agrees to any deletions required by the title company due to the inability to obtain a resale certificate, the

buyer may still wish to exercise the buyer’s contractual right to terminate for failure to receive a resale

certificate, as contemplated by the Addendum.

For example, even if the buyer is comfortable that assessments are current and that there is no right of first

refusal, the buyer may not be willing to take on the potential future problems the buyer could encounter

with a dysfunctional POA, such as not knowing how to pay dues, no certainty with regard to who will pay

for common area maintenance, and no knowledge of current liabilities of or lawsuits against the POA that

could affect the owners going forward. If the buyer is willing to proceed, that is the buyer’s choice, but in

that event, it may be in the best interest of the title company to obtain a written acknowledgement from the

buyer that the buyer did not receive the resale certificate contemplated by the Addendum, and to provide

the buyer written information from the seller with regard to the frequency and amount of dues that were

collected when the POA was last functional, if the seller has this information.

If the buyer does terminate due to the failure to receive the complete Subdivision Information or an updated

resale certificate, the owner’s recourse against the POA is limited, as discussed above: Texas Property Code

§ 207.004 allows for a judgment against the POA in an amount not more than $500, court costs, and attorney

fees. But Texas Property Code § 207.006 provides that a POA is not otherwise liable for a failure to deliver

the Subdivision Information, so a seller is not able to sue the POA for damages that may accompany the

loss of the sale.

C. THE NON-FUNCTIONAL POA

In the case of a non-functional POA, one that is contemplated by recorded documents applicable to the

subdivision but never formally activated, the challenges manifest differently.

With regard to the contractual rights of the parties, the seller may not even be aware of the purported

existence of a POA until the title company discovers it in the property records, so no Addendum is attached

to the contract. However, Para. 6E(2) of The TREC Contract does have a check box to indicate whether or

not the property is in a mandatory POA, and if this turns out to be inaccurate, the buyer may still have a

legal right to void the contract on the basis that the contract was based on a mutual mistake of fact that

materially affects the agreement.

2 While less commonly elected, the buyer also has an opportunity to purchase endorsements to the Owner’s Policy,

such as the T-19.1 endorsement, the coverage for which closely mirrors the coverage of the T-19 endorsement to the

Loan Policy. A dysfunctional POA could impact T-19.1 coverage as well.

2019 Texas Land Title Institute –POAs: Dealing with the Dysfunctional and Non-functional 6

Concerning assessments, the same statutory process regarding sending two requests to the POA could

apply, but if no management certificate was ever filed, it would be even more difficult to know where to

make the request. Fortunately, if no management certificate is found of record, Texas Property Code

§ 209.004(d) exempts the buyer, lender, and title company from amounts due on the date of the transfer and

any debts to or claims of the POA that accrued before the date of the transfer.

This statutory protection is similarly limited and does not explicitly cover the other matters, such as rights

of first refusal and violations of restrictive covenants, so these matters would need to be discussed with the

title insurance underwriter, as discussed above.

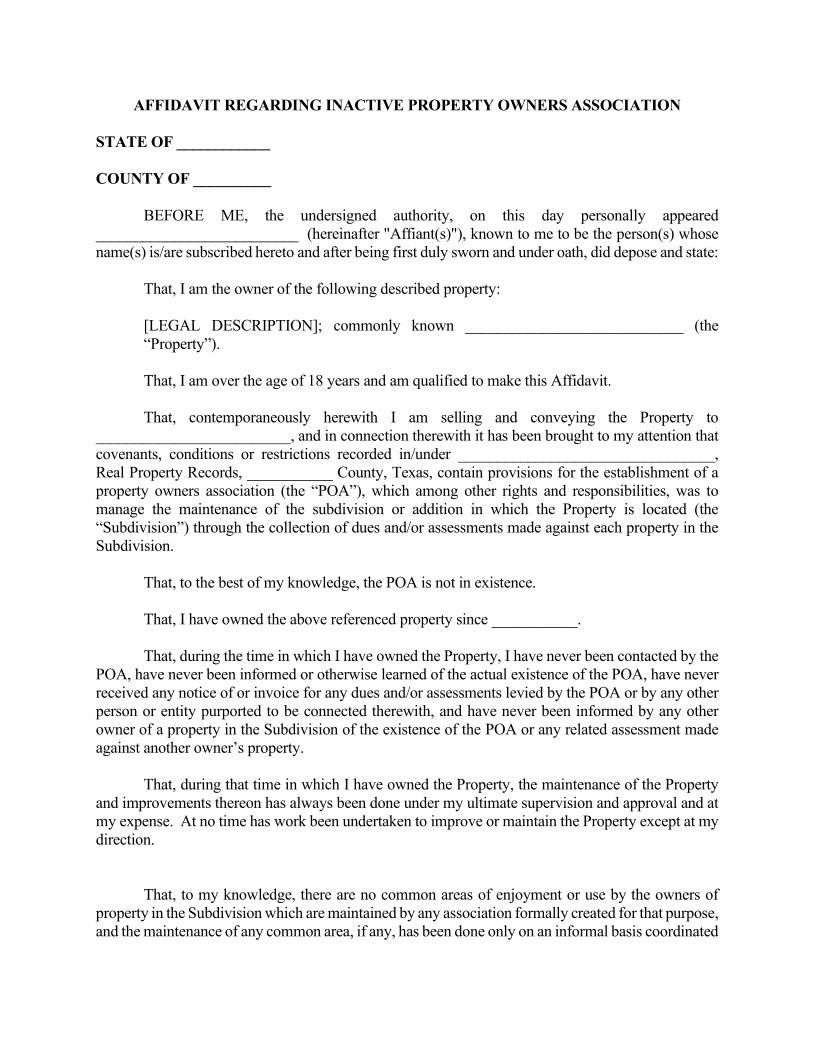

In the case of a non-functional POA, though, the underwriter may be far more willing to take a risk on

insurability than with a dysfunctional POA, as a once-functional POA may be more likely to spring up

again than one that has never operated. Such approval may include reliance on something like an “Inactive

POA Affidavit,” in which seller states that: to best of seller’s knowledge, the POA contemplated by the

Dedicatory Instruments is not in existence; since date the seller acquired the property, the seller has never

been contacted by a POA or received a notice or invoice for dues/assessments; and no common areas in the

subdivision are maintained by any formal group, and any common area maintenance has been done

informally by individual owners. A sample affidavit to this effect is attached.

Even though the title policy would still except to the Dedicatory Instruments in Schedule B, and the buyer

would not be covered for the POA’s attempts to assert its ability to collect dues in the future, to avoid future

disputes and as a customer service matter, it may still be prudent for the title company to explicitly disclose

the purported existence of the POA and have the buyer acknowledge in writing that the Dedicatory

Instruments provide for a POA, and that although the seller claims that it is non-functional, the POA may

affect the buyer going forward.

D. CONCLUSION

It may be frustrating to discover that a resale certificate cannot be obtained because a once-active POA has

gone dormant, or that a POA contemplated by the property records has never been active. But the inability

to obtain documents from such a POA is not necessarily fatal. By following statutory processes, discussing

with the insured, and consulting with the title insurance underwriter regarding acceptable risks, a closer can

successfully navigate closing a property in a dysfunctional or non-functional POA.

AFFIDAVIT REGARDING REQUESTS FOR SUBDIVISION INFORMATION

STATE OF ____________

COUNTY OF __________

BEFORE ME, the undersigned authority, on this day personally appeared

__________________________ (hereinafter "Affiant(s)"), known to me to be the person(s) whose

name(s) is/are subscribed hereto and after being first duly sworn and under oath, did depose and state:

1. I am the owner of the following described property:

[LEGAL DESCRIPTION]; commonly known as ____________________________ (the

“Property”).

2. I am over the age of 18 years and am qualified to make this Affidavit.

3. I am under contract to sell the Property to ___________________ (the “Buyer”).

4. I, my agent, or a title insurance company or its agent acting on my behalf made, in

accordance with Chapter 207 of the Texas Property Code, two written requests to the

property owners’ association for the information described in Texas Property Code

§ 207.003.

5. The first request was made on _____________, 20___, in the following manner:

____________________________________. On _______________, 20____, the second

request was made in the following manner (check one): ____ mailed by certified mail,

return receipt requested; or _____ hand delivered, evidenced by receipt.

6. The property owners’ association did not timely provide the information.

7. Contemporaneously herewith, I am delivering a copy of this affidavit to Buyer.

This affidavit is made for the purposes of: complying with Texas Property Code § 207.004,

inducing __________Title Company and its Underwriter to issue its policy(ies) of title insurance

insuring title to the property described above and/or insuring the priority and validity of liens against

said property, and inducing the insured(s) under such policy(ies) to accept and rely upon said

policy(ies).

Affiant(s) know and understand that such policy(ies) of title insurance will be issued and

accepted in reliance upon the truth and accuracy of the facts set forth and that any false statement

herein contained will render Affiant liable to criminal prosecution and/or civil liability to

_____________________Title Company and its Underwriter and the insured(s) under said

policy(ies).

Affiants further sayeth not.

_____________________________ _____________________________

SUBSCRIBED AND SWORN BEFORE ME this _______ day of __________ 20___,

by the said ___________________________.

_________________________________

Notary Public

AFFIDAVIT REGARDING INACTIVE PROPERTY OWNERS ASSOCIATION

STATE OF ____________

COUNTY OF __________

BEFORE ME, the undersigned authority, on this day personally appeared

__________________________ (hereinafter "Affiant(s)"), known to me to be the person(s) whose

name(s) is/are subscribed hereto and after being first duly sworn and under oath, did depose and state:

That, I am the owner of the following described property:

[LEGAL DESCRIPTION]; commonly known ____________________________ (the

“Property”).

That, I am over the age of 18 years and am qualified to make this Affidavit.

That, contemporaneously herewith I am selling and conveying the Property to

_________________________, and in connection therewith it has been brought to my attention that

covenants, conditions or restrictions recorded in/under _________________________________,

Real Property Records, ___________ County, Texas, contain provisions for the establishment of a

property owners association (the “POA”), which among other rights and responsibilities, was to

manage the maintenance of the subdivision or addition in which the Property is located (the

“Subdivision”) through the collection of dues and/or assessments made against each property in the

Subdivision.

That, to the best of my knowledge, the POA is not in existence.

That, I have owned the above referenced property since ___________.

That, during the time in which I have owned the Property, I have never been contacted by the

POA, have never been informed or otherwise learned of the actual existence of the POA, have never

received any notice of or invoice for any dues and/or assessments levied by the POA or by any other

person or entity purported to be connected therewith, and have never been informed by any other

owner of a property in the Subdivision of the existence of the POA or any related assessment made

against another owner’s property.

That, during that time in which I have owned the Property, the maintenance of the Property

and improvements thereon has always been done under my ultimate supervision and approval and at

my expense. At no time has work been undertaken to improve or maintain the Property except at my

direction.

That, to my knowledge, there are no common areas of enjoyment or use by the owners of

property in the Subdivision which are maintained by any association formally created for that purpose,

and the maintenance of any common area, if any, has been done only on an informal basis coordinated

through the efforts of individual owners of property in the Subdivision. In the time since I have owned

my Property, I have contributed to the maintenance of any common areas in the following manner:

______________________________________________________________

This affidavit is made for the purpose of inducing __________Title Company and its

Underwriter to issue its policy(ies) of title insurance insuring title to the property described above

and/or insuring the priority and validity of liens against said property, and to induce the insured(s)

under such policy(ies) to accept and rely upon said policy(ies).

Affiants know and understand that such policy(ies) of title insurance will be issued and

accepted in reliance upon the truth and accuracy of the facts set forth and that any false statement

herein contained will render Affiant liable to criminal prosecution and/or civil liability to

_____________________Title Company and its Underwriter and the insured(s) under said

policy(ies).

That, Affiants further sayeth not.

_____________________________ _____________________________

SUBSCRIBED AND SWORN BEFORE ME this _______ day of __________ 20___,

by the said ___________________________.

_________________________________

Notary Public