‘planetary economics’, energy transition & policy … · •introduction to “planetary...

TRANSCRIPT

• Introduction to “Planetary Economics”: Three Domains and Three Pillars of Policy

• The ‘Solow Residual’ and the innovation paradox• UK electricity market reform and transformation • Innovation pathways and the renewables revolution

• Porter’s Kick? Macroeconomics of transformation – World Bank presentation• Innovation and adaptive system Modelling – RFF presentation

‘PlanetaryEconomics’,energytransition&policyexperience

SeminartoDukeUniversity,1st December2017

Energy, Climate Change and the Three Domains of

Sustainable Development@michaelgrubb9

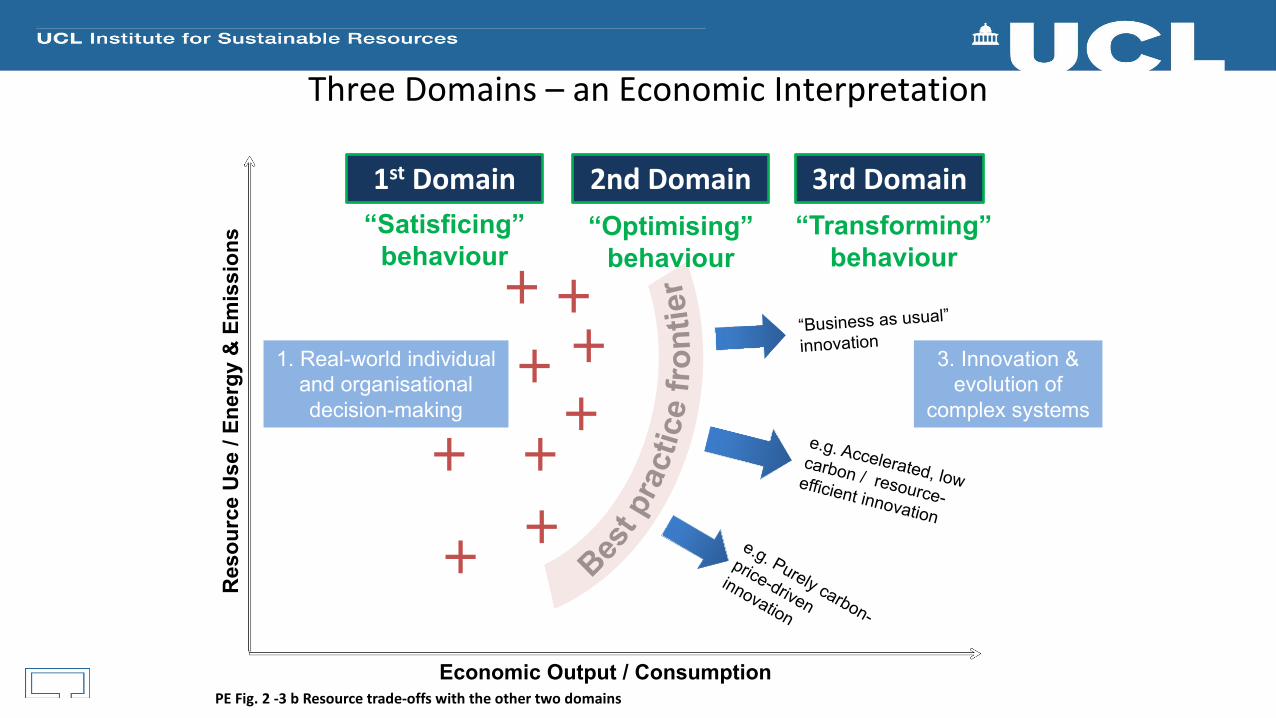

PEFig.2-3bResourcetrade-offswiththeothertwodomains

ThreeDomains– anEconomicInterpretation

Res

ourc

e U

se /

Ener

gy &

Em

issi

ons

Economic Output / Consumption

3rdDomain

1. Real-world individual and organisational decision-making

“Transforming” behaviour

“Optimising”behaviour

1st Domain“Satisficing”

behaviour

2ndDomain

3. Innovation & evolution of

complex systems

Lecture:PlanetaryEconomicsandthePoliticalEconomyofEnergy&ClimateChange,MsCinEPEE

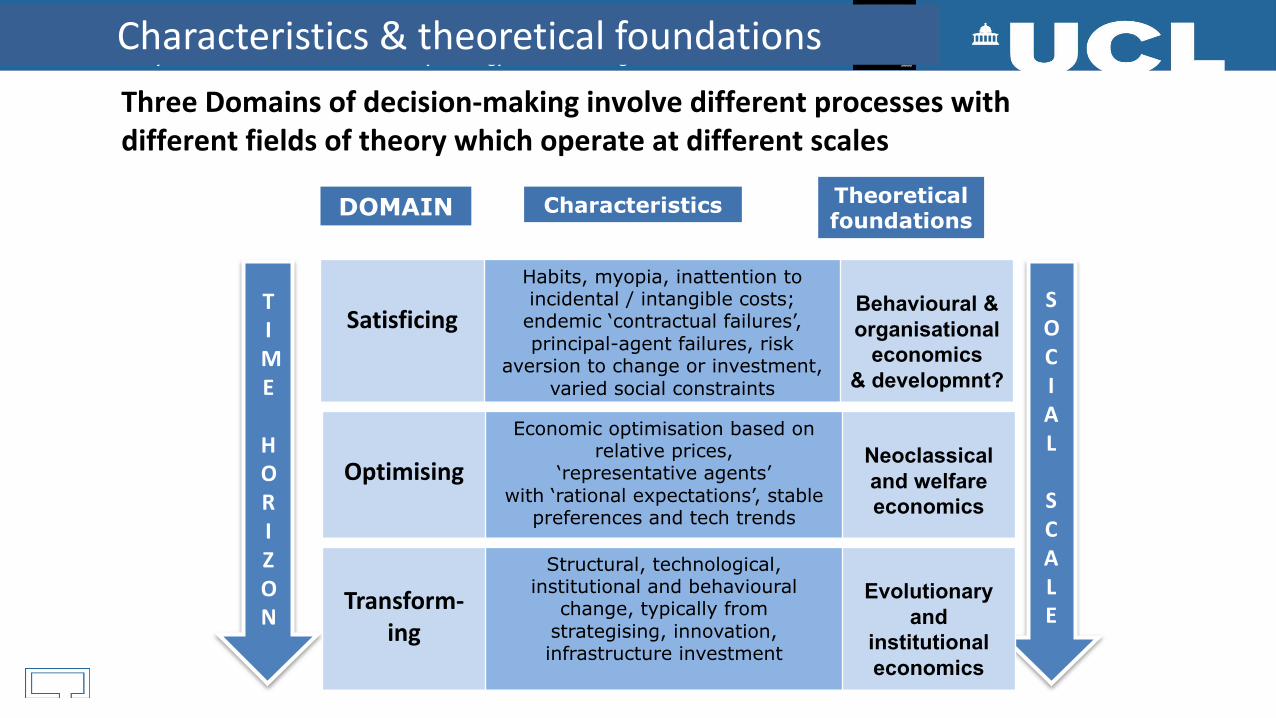

Satisficing

Habits, myopia, inattention to incidental / intangible costs; endemic ‘contractual failures’, principal-agent failures, risk

aversion to change or investment, varied social constraints

Behavioural & organisational

economics& developmnt?

DOMAIN Theoretical foundations

Characteristics

ThreeDomainsofdecision-makinginvolvedifferentprocesseswithdifferentfieldsoftheorywhichoperateatdifferentscales

SOCIAL

SCALE

TIME

HORIZON

Optimising

Economic optimisation based on relative prices,

‘representative agents’with ‘rational expectations’, stable

preferences and tech trends

Neoclassical and welfare economics

Transform-ing

Structural, technological, institutional and behavioural

change, typically from strategising, innovation, infrastructure investment

Evolutionary and

institutional economics

Characteristics&theoreticalfoundations

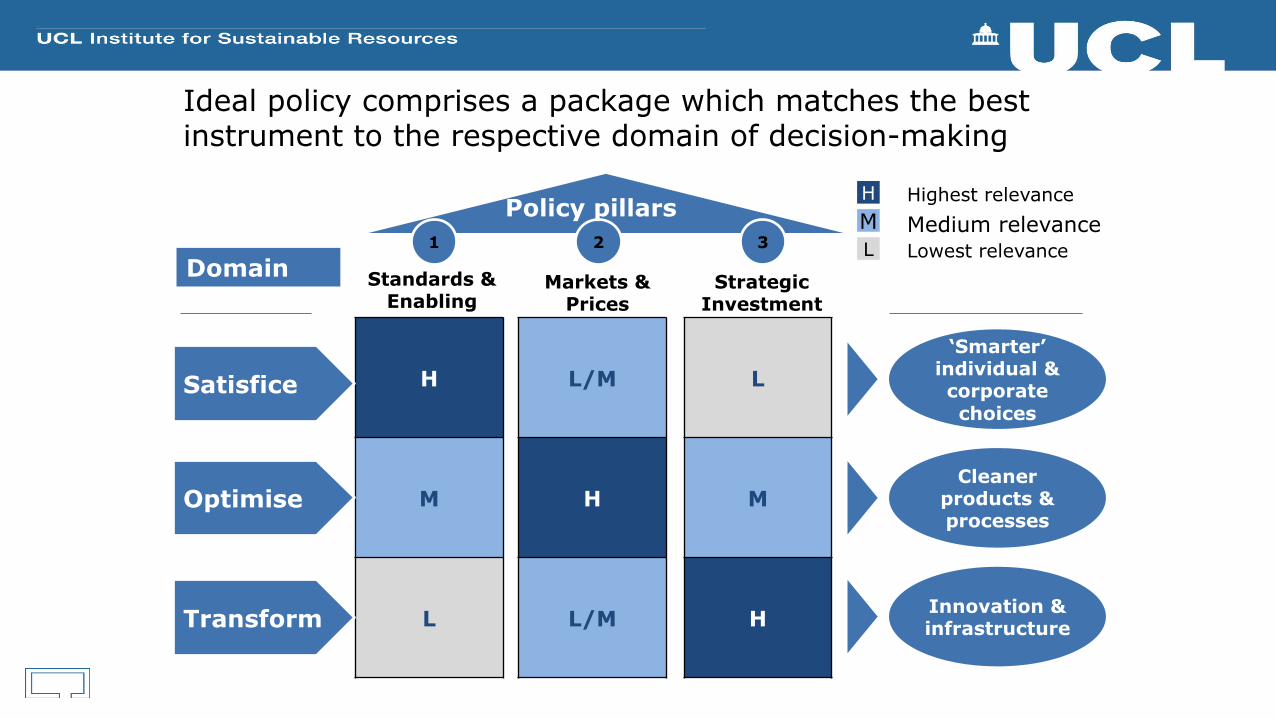

H

M

L

H Highest relevanceM Medium relevanceL Lowest relevance

Satisfice

Transform

Optimise

Domain Standards & Enabling

Markets & Prices

Strategic Investment

‘Smarter’individual & corporate choices

Cleaner products & processes

Innovation & infrastructure

1 2 3

L/M

H

L/M

L

M

H

Policy pillars

Ideal policy comprises a package which matches the best instrument to the respective domain of decision-making

• Introduction to “Planetary Economics”: Three Domains and Three Pillars of Policy

• The ‘Solow Residual’ and the innovation paradox• UK electricity market reform and transformation • Innovation pathways and the renewables revolution

• Porter’s Kick? Macroeconomics of transformation – World Bank presentation• Innovation and adaptive system Modelling – RFF presentation

‘PlanetaryEconomics’,energytransition&policyexperience

SeminartoDukeUniversity,1st December2017

Energy, Climate Change and the Three Domains of

Sustainable Development@michaelgrubb9

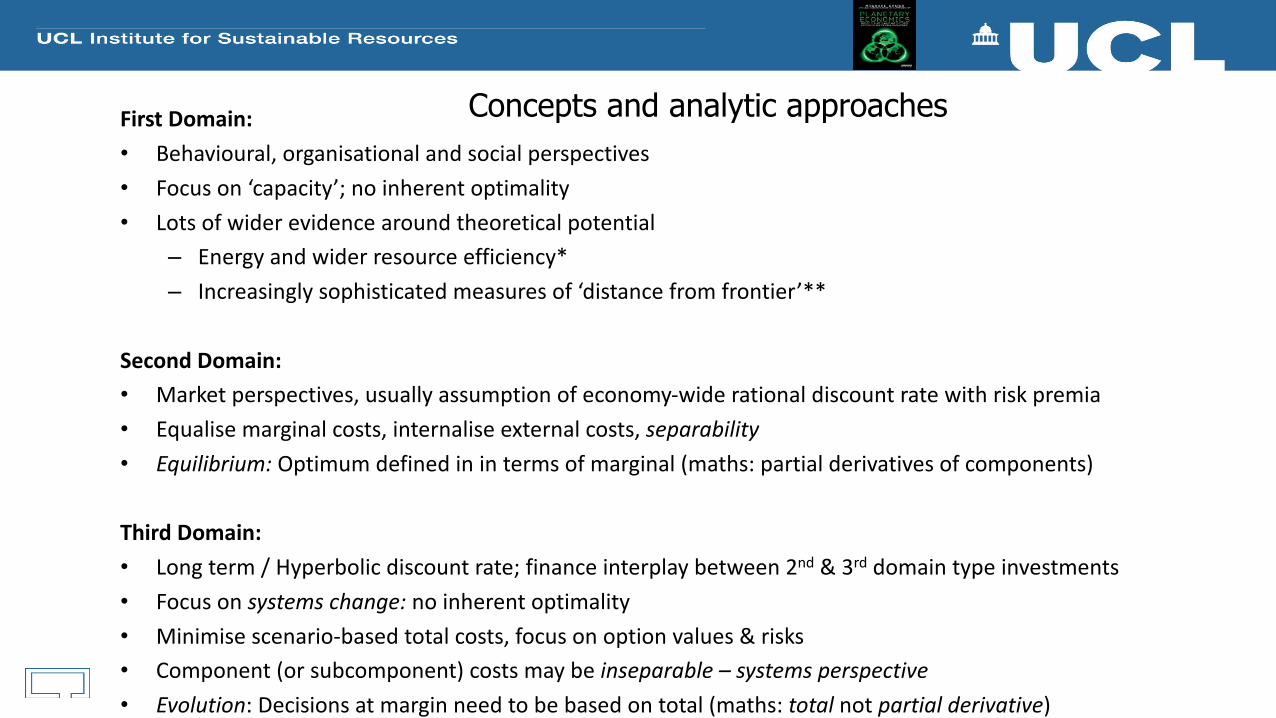

FirstDomain:• Behavioural,organisationalandsocialperspectives• Focuson‘capacity’;noinherentoptimality• Lotsofwiderevidencearoundtheoreticalpotential

– Energyandwiderresourceefficiency*– Increasinglysophisticatedmeasuresof‘distancefromfrontier’**

SecondDomain:• Marketperspectives,usuallyassumptionofeconomy-widerationaldiscountratewithriskpremia• Equalisemarginalcosts,internaliseexternalcosts,separability• Equilibrium:Optimumdefinedinintermsofmarginal(maths:partialderivativesofcomponents)

ThirdDomain:• Longterm/Hyperbolicdiscountrate;financeinterplaybetween2nd &3rd domaintypeinvestments• Focusonsystemschange:noinherentoptimality• Minimisescenario-basedtotalcosts,focusonoptionvalues&risks• Component(orsubcomponent)costsmaybeinseparable– systemsperspective• Evolution:Decisionsatmarginneedtobebasedontotal(maths:totalnotpartialderivative)

Concepts and analytic approaches

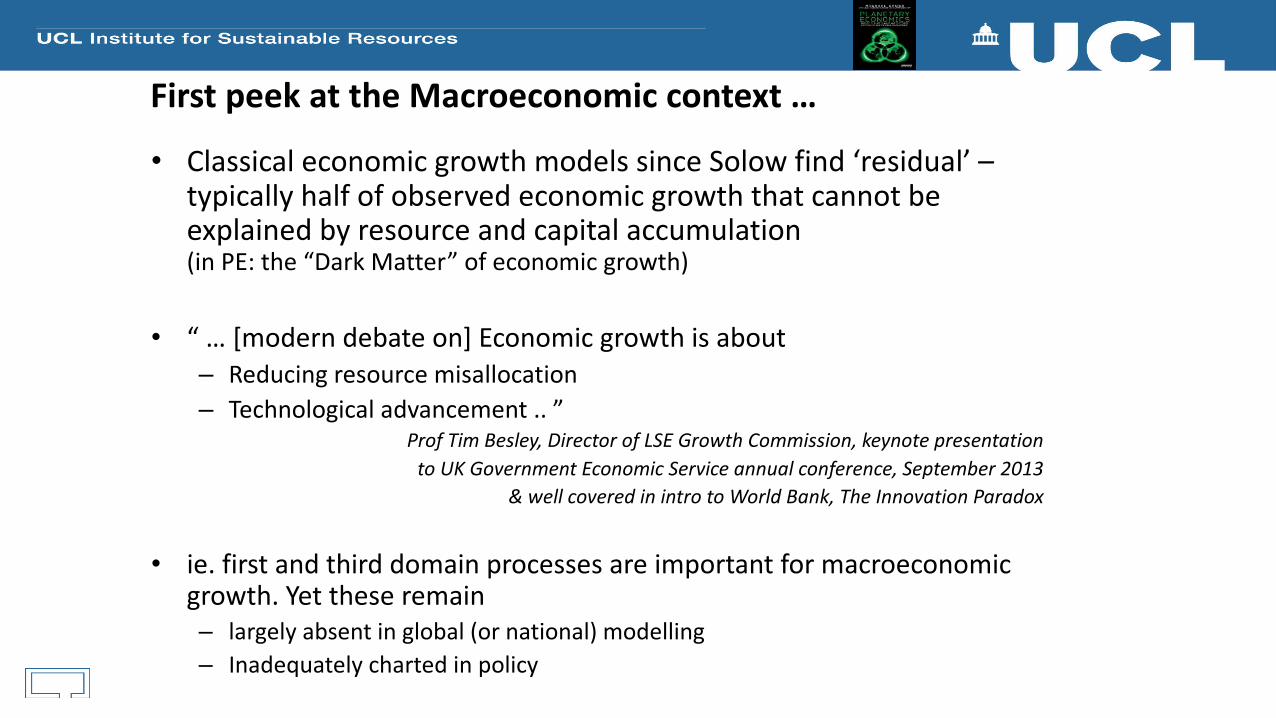

FirstpeekattheMacroeconomiccontext…

• ClassicaleconomicgrowthmodelssinceSolowfind‘residual’–typicallyhalfofobservedeconomicgrowththatcannotbeexplainedbyresourceandcapitalaccumulation(inPE:the“DarkMatter”ofeconomicgrowth)

• “…[moderndebateon]Economicgrowthisabout– Reducingresourcemisallocation– Technologicaladvancement..”

ProfTimBesley,DirectorofLSEGrowthCommission,keynotepresentationtoUKGovernmentEconomicServiceannualconference,September2013

&wellcoveredinintrotoWorldBank,TheInnovationParadox

• ie.firstandthirddomainprocessesareimportantformacroeconomicgrowth.Yettheseremain– largelyabsentinglobal(ornational)modelling– Inadequatelychartedinpolicy

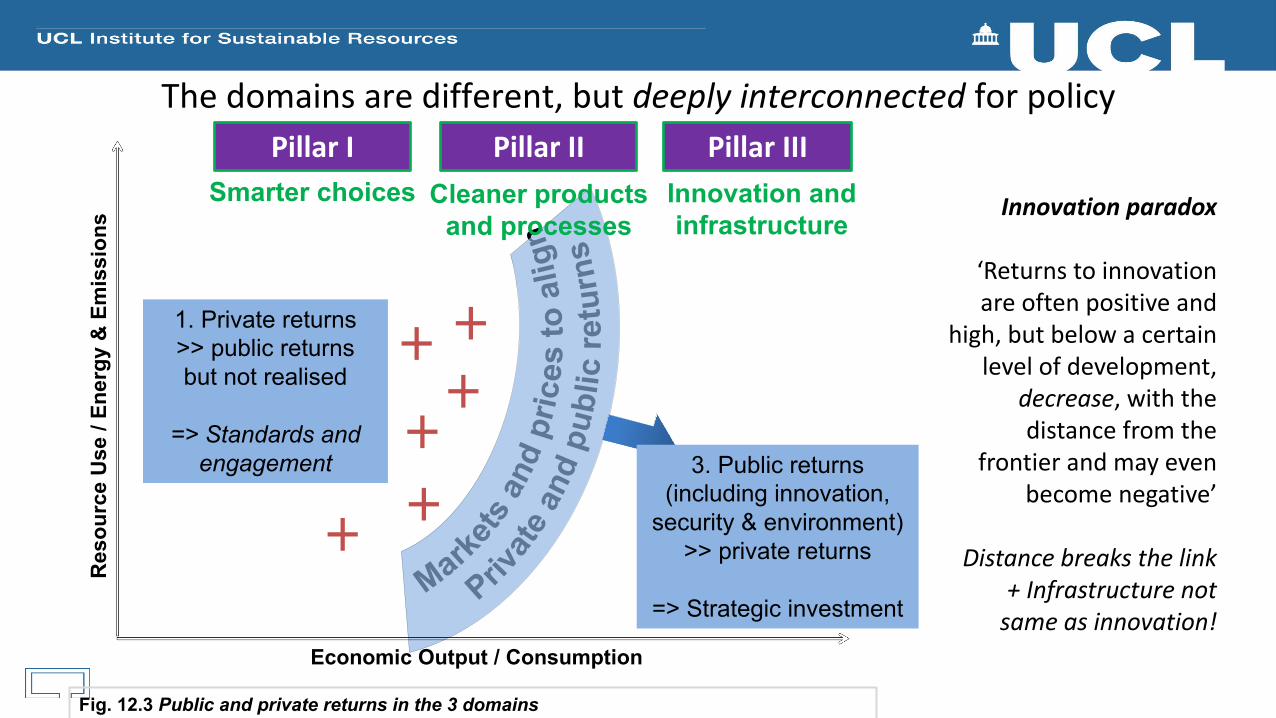

Fig. 12.3 Public and private returns in the 3 domains

Res

ourc

e U

se /

Ener

gy &

Em

issi

ons

Economic Output / Consumption

PillarIII

1. Private returns >> public returns but not realised

=> Standards and engagement

Innovation and infrastructure

Cleaner products and processes

PillarISmarter choices

PillarII

3. Public returns (including innovation,

security & environment) >> private returns

=> Strategic investment

Thedomainsaredifferent,butdeeplyinterconnectedforpolicy

Innovationparadox

‘Returnstoinnovationareoftenpositiveand

high,butbelowacertainlevelofdevelopment,

decrease,withthedistancefromthe

frontierandmayevenbecomenegative’

Distancebreaksthelink+Infrastructurenotsameasinnovation!

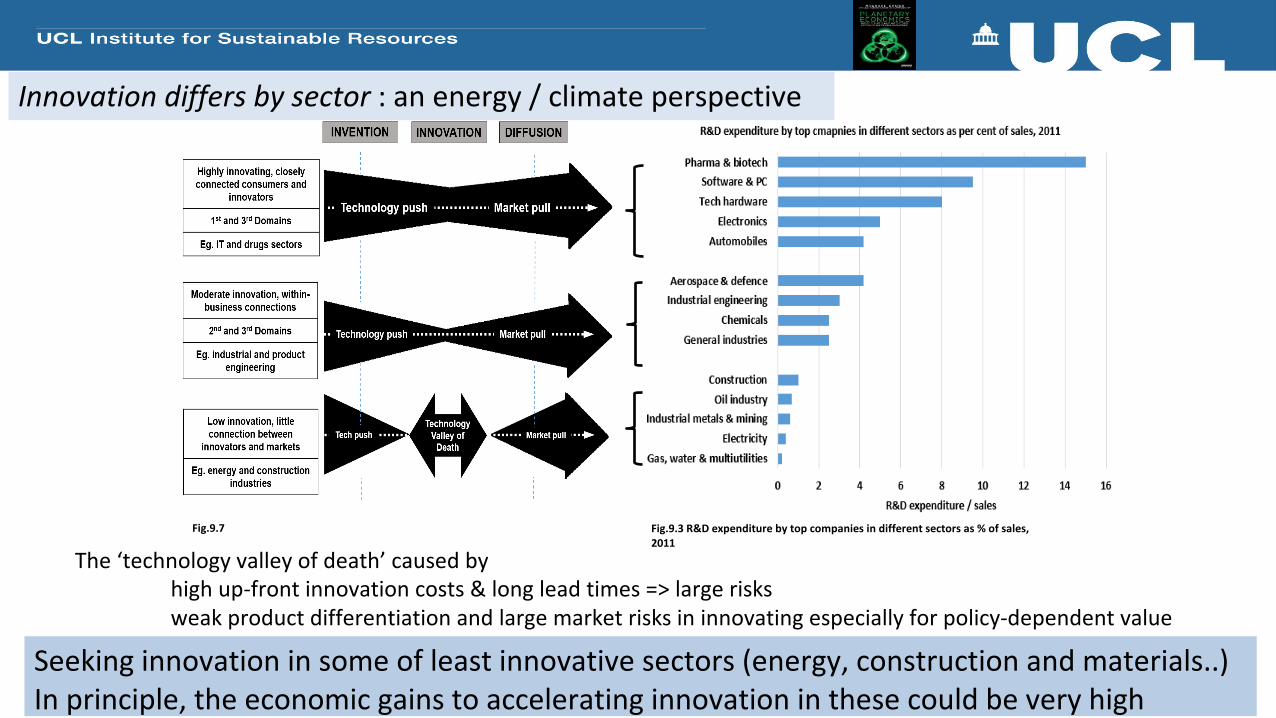

Fig.9.3R&Dexpenditurebytopcompaniesindifferentsectorsas%ofsales,2011

Fig.9.7

Seekinginnovationinsomeofleastinnovativesectors(energy,constructionandmaterials..)Inprinciple,theeconomicgainstoacceleratinginnovationin thesecouldbeveryhigh

The‘technologyvalleyofdeath’causedbyhighup-frontinnovationcosts&longleadtimes=>largerisksweakproductdifferentiationandlargemarketrisksininnovatingespeciallyforpolicy-dependentvalue

Innovationdiffersbysector:anenergy/climateperspective

• Introduction to “Planetary Economics”: Three Domains and Three Pillars of Policy

• The ‘Solow Residual’ and the innovation paradox• UK electricity market reform and transformation • Innovation pathways and the renewables revolution

• Porter’s Kick? Macroeconomics of transformation – World Bank presentation• Innovation and adaptive system Modelling – RFF presentation

‘PlanetaryEconomics’,energytransition&policyexperience

SeminartoDukeUniversity,1st December2017

Energy, Climate Change and the Three Domains of

Sustainable Development@michaelgrubb9

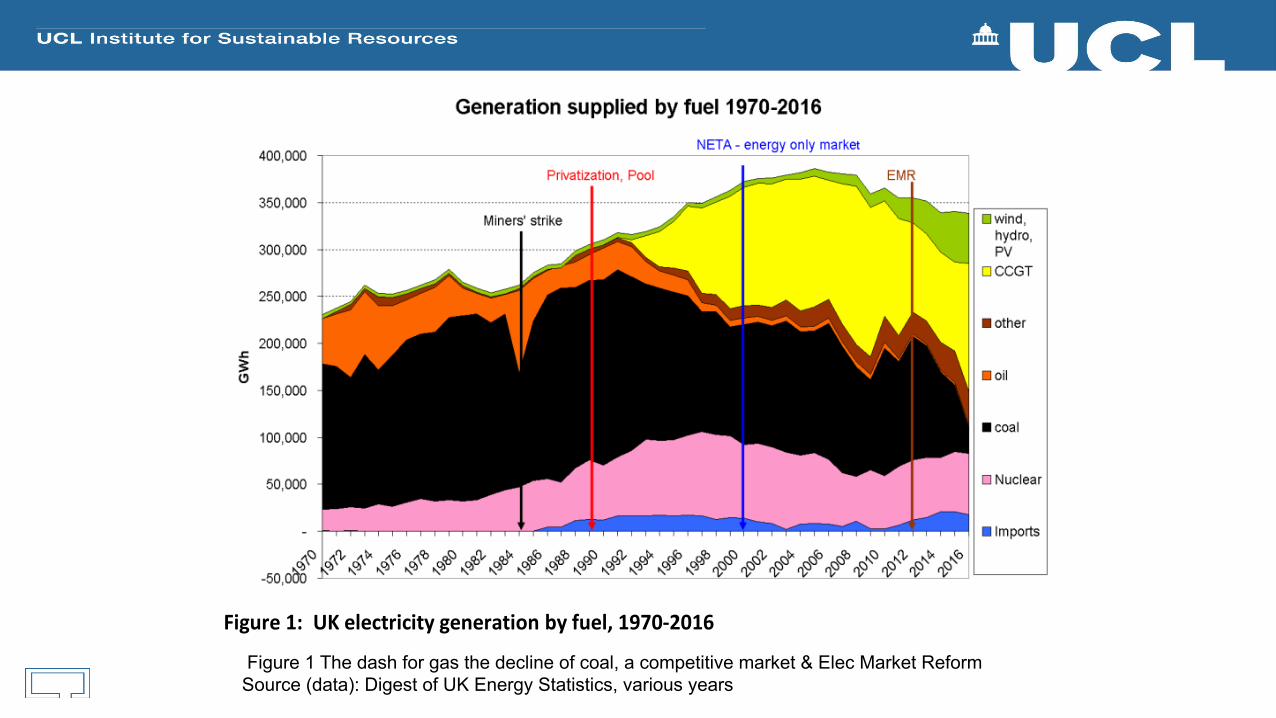

Figure 1 The dash for gas the decline of coal, a competitive market & Elec Market ReformSource (data): Digest of UK Energy Statistics, various years

Figure1:UKelectricitygenerationbyfuel,1970-2016

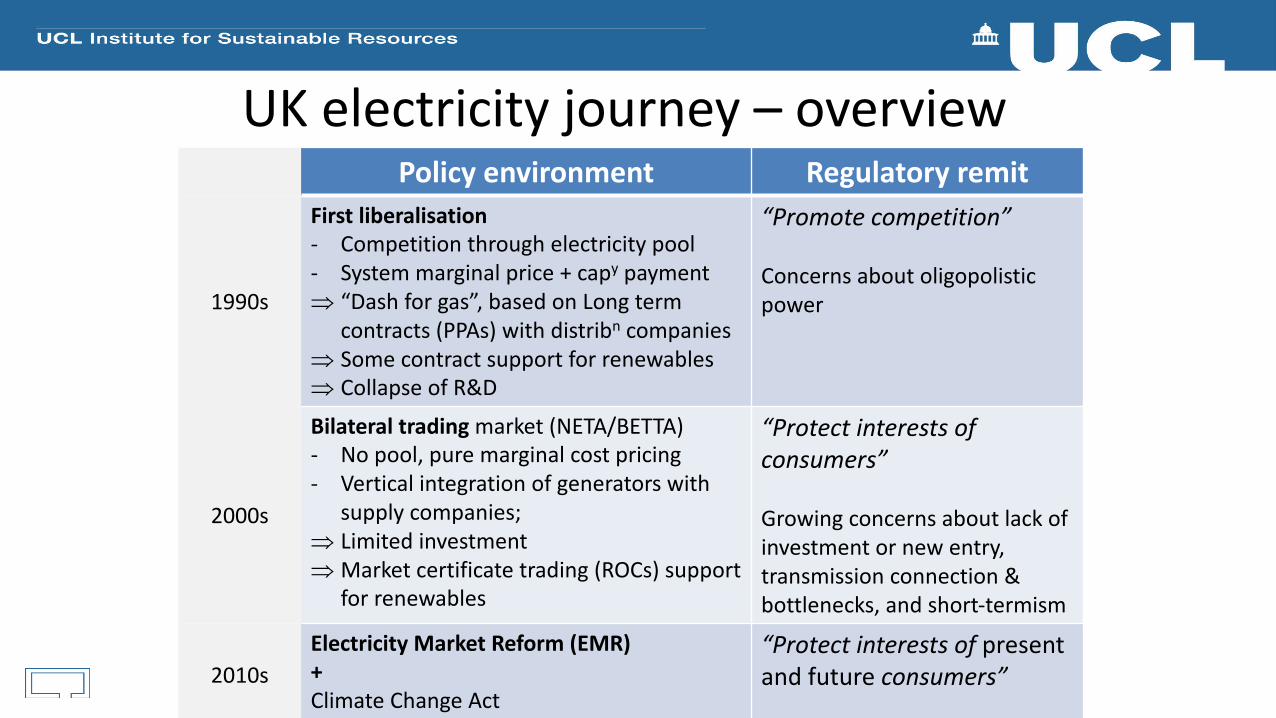

Policyenvironment Regulatoryremit

1990s

Firstliberalisation- Competitionthroughelectricitypool- Systemmarginalprice+capy paymentÞ “Dashforgas”,basedonLongterm

contracts(PPAs)withdistribn companiesÞ SomecontractsupportforrenewablesÞ CollapseofR&D

“Promote competition”

Concernsaboutoligopolisticpower

2000s

Bilateral tradingmarket(NETA/BETTA)- Nopool,puremarginalcostpricing- Vertical integrationofgeneratorswith

supplycompanies;Þ LimitedinvestmentÞ Marketcertificatetrading(ROCs)support

forrenewables

“Protect interestsofconsumers”

Growingconcernsaboutlackofinvestmentornewentry,transmissionconnection&bottlenecks,andshort-termism

2010sElectricity MarketReform(EMR)+ClimateChangeAct

“Protect interestsofpresentandfutureconsumers”

UKelectricityjourney– overview

• Academicstrugglesbetweenidealisedtheoryandemergingevidencearoundoverallinvestability

• Nuclear&renewablesseenaskeytofuture• Energytransitionestimatedtoinvolveover£100bninvestmentduring2010s– beyondthepocketsofincumbents,termsoffinancecrucial

• Political evolution:Ø RisingenergypricesØ ClimateChangeCommittee(2008)concernaroundlow

carbon/capitalintensiveinvestment,amplifiedbyinadequateCprice

Ø Ofgem (regulator)concernaroundsecurity

UKElectricityMarketReform- Background

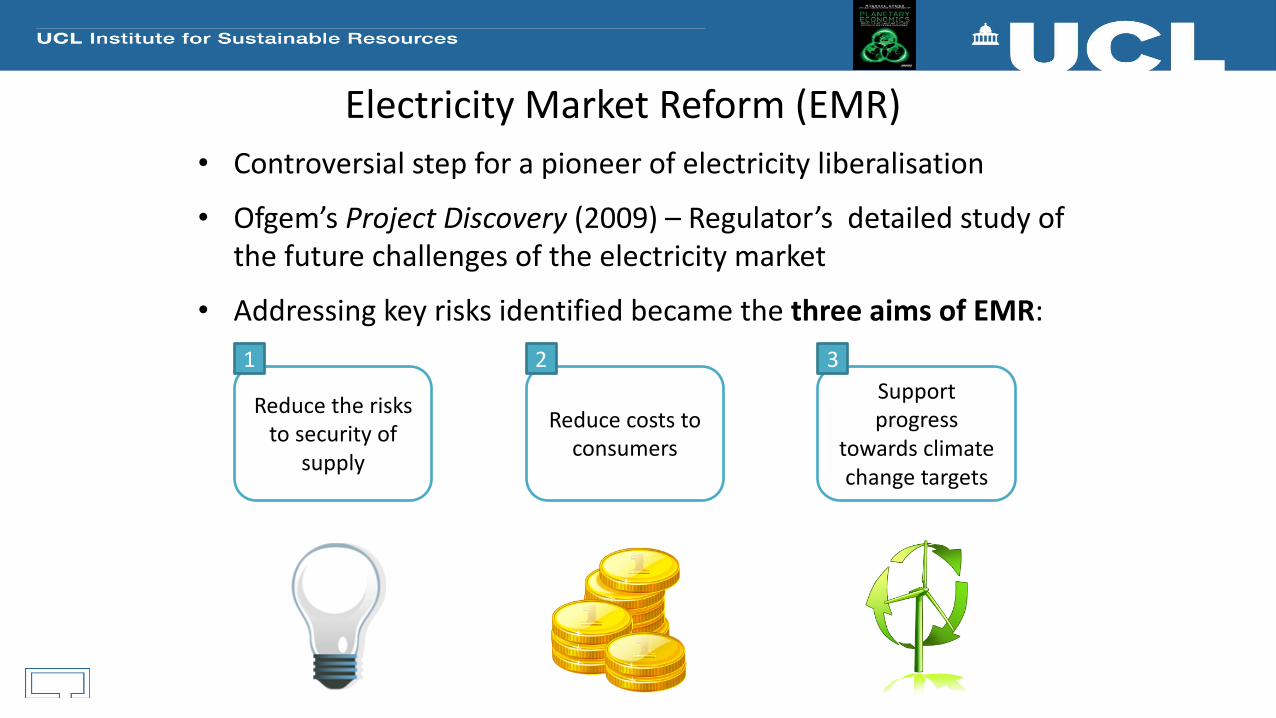

• Controversialstepforapioneerofelectricityliberalisation

• Ofgem’s ProjectDiscovery(2009)– Regulator’sdetailedstudyofthefuturechallengesoftheelectricitymarket

• AddressingkeyrisksidentifiedbecamethethreeaimsofEMR:

14

ElectricityMarketReform(EMR)

Reducetheriskstosecurityof

supply

Supportprogress

towardsclimatechangetargets

Reducecoststoconsumers

1 2 3

15

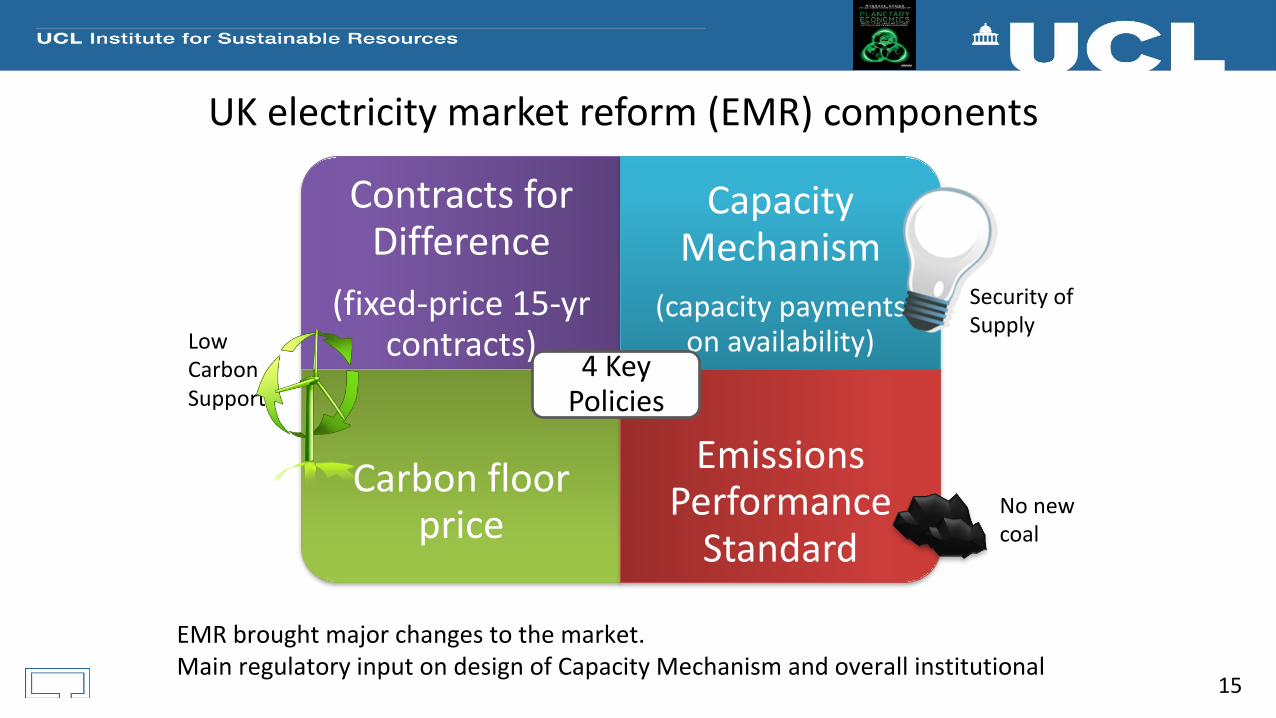

ContractsforDifference

(fixed-price15-yrcontracts)

CapacityMechanism

(capacitypaymentsonavailability)

Carbonfloorprice

EmissionsPerformanceStandard

4KeyPolicies

EMRbroughtmajorchangestothemarket.MainregulatoryinputondesignofCapacityMechanismandoverallinstitutional

SecurityofSupply

LowCarbonSupport

Nonewcoal

UKelectricitymarketreform(EMR)components

16

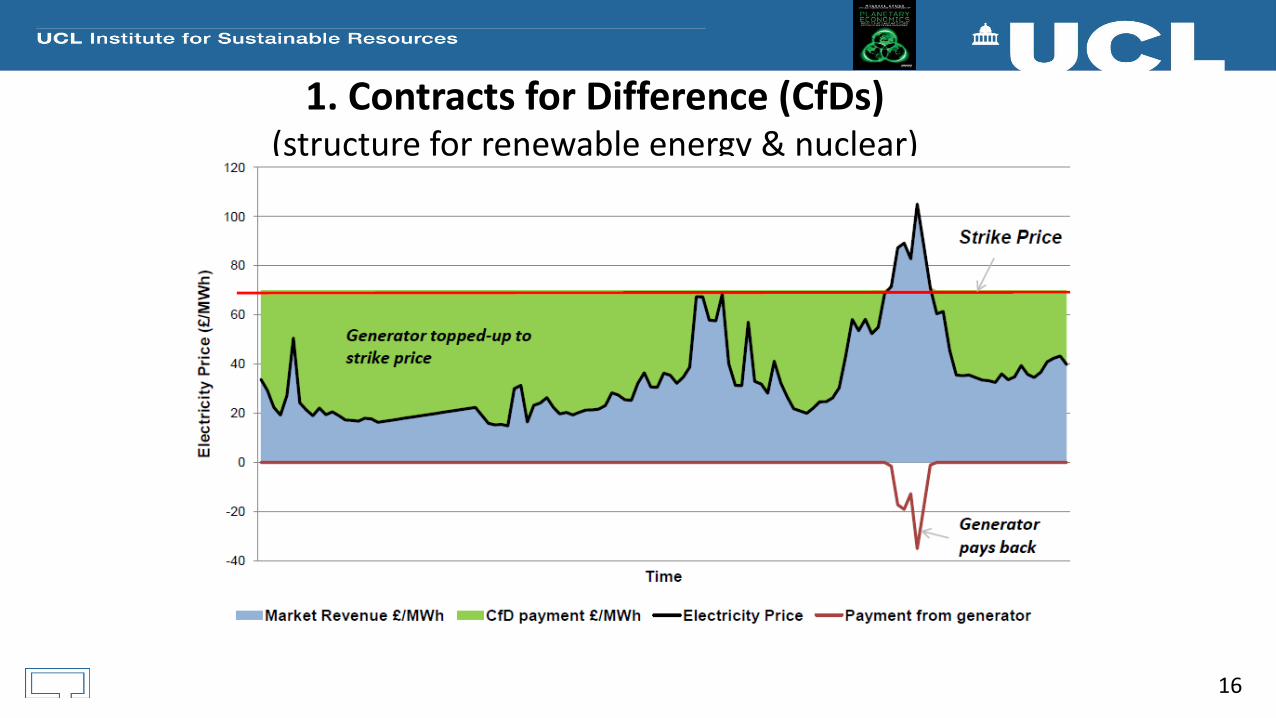

1.ContractsforDifference(CfDs)(structureforrenewableenergy&nuclear)

Initialgainfromauctionsfollowedbyhugeoffshorewindcostreduction

Source: From M.Grubb and D.Newbery (2017), ‘UK Electricity Market Reform and the Energy Transition: Emerging Lessons’, MIT working paper (submitted) * 15-yr Contract prices

£0

£20

£40

£60

£80

£100

£120

£140

£160

£180St

rike

Pric

e (£

/MW

h)

2013/14 2015/16 2017/18 2019/20 2021/22

Round 1 Admin Strike Price (Offshore Wind)Round 1 Contracts - Offshore Wind / ACTRound 2 Contracts - Offshore Wind

£155 £155£150

£140 £140

£57,50 (Hornsea II, Moray East)

£74,75 (Inc. Triton Knoll)

£114.39 (Inc. Neart Na Gaoithe)

£119,89 (Inc. East Anglia 1)

2014,administeredCfD prices,£140-£150/MWh*2015,firstauction,offshorewindprice:£114.39/MWh2017,secondauction,twoprojectsat£57.50/MWhà CompetitiveCfDs drivedowncost– hardware,

supplychain&finance(Newbery(2015)estimatesCfDs reducedWACCby3%points– saving>£2bn/yronestimatedcostofenergytransition).

à boosttoUKlow-carbonsupplychain,aspartofgovernment’semerging‘CleanGrowthPlan’

Deliveryyears(tofirstgeneration)

Allocation/auctionrounds

priceshalve

4yearsdifferenceindeliveryyears

strikepriceforfiveoffshorewindfarmsdependingoncompletiondate

Hugecostreductionsfromauctionedcontracts

Why

How

18

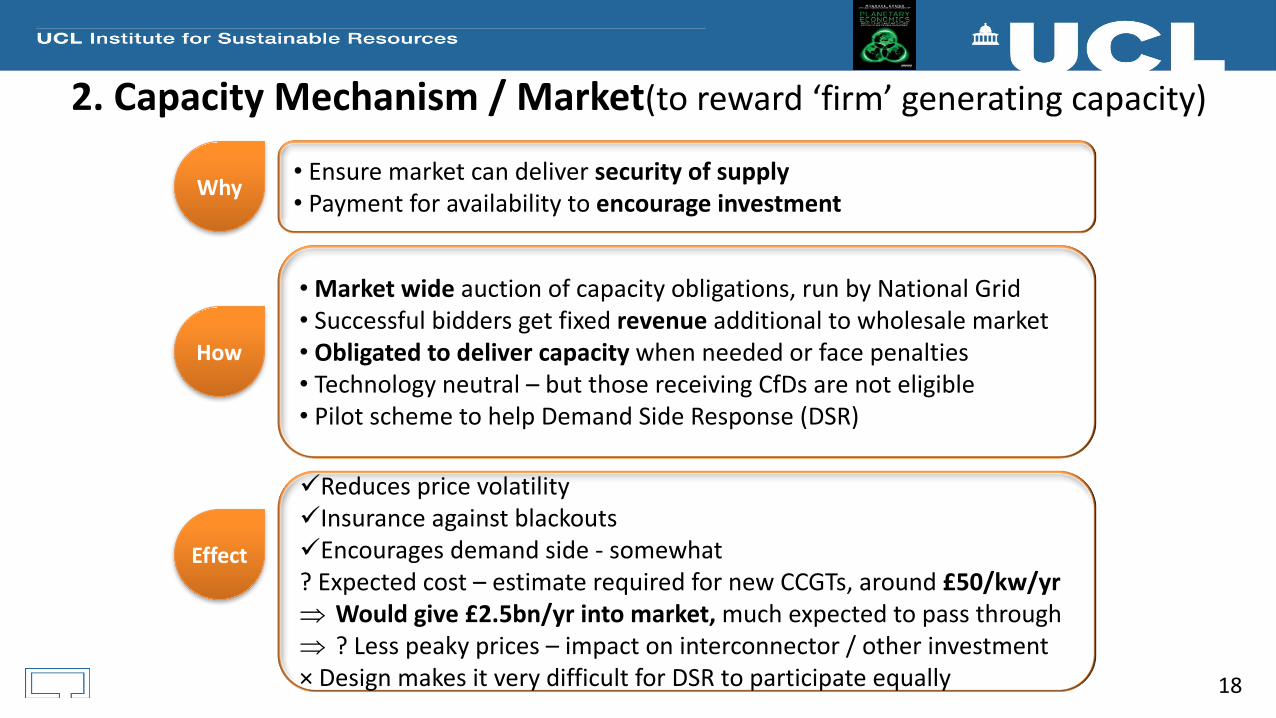

2.CapacityMechanism/Market(toreward‘firm’generatingcapacity)

• Ensuremarketcandeliversecurityofsupply• Paymentforavailabilitytoencourageinvestment

• Marketwideauctionofcapacityobligations,runbyNationalGrid• Successfulbiddersgetfixedrevenueadditionaltowholesalemarket• Obligatedtodelivercapacitywhenneededorfacepenalties• Technologyneutral– butthosereceivingCfDsarenoteligible• PilotschemetohelpDemandSideResponse(DSR)

üReducespricevolatilityüInsuranceagainstblackoutsüEncouragesdemandside- somewhat?Expectedcost– estimaterequiredfornewCCGTs,around£50/kw/yrÞ Wouldgive£2.5bn/yr intomarket,muchexpectedtopassthroughÞ ?Lesspeakyprices– impactoninterconnector/otherinvestment× DesignmakesitverydifficultforDSRtoparticipateequally

Effect

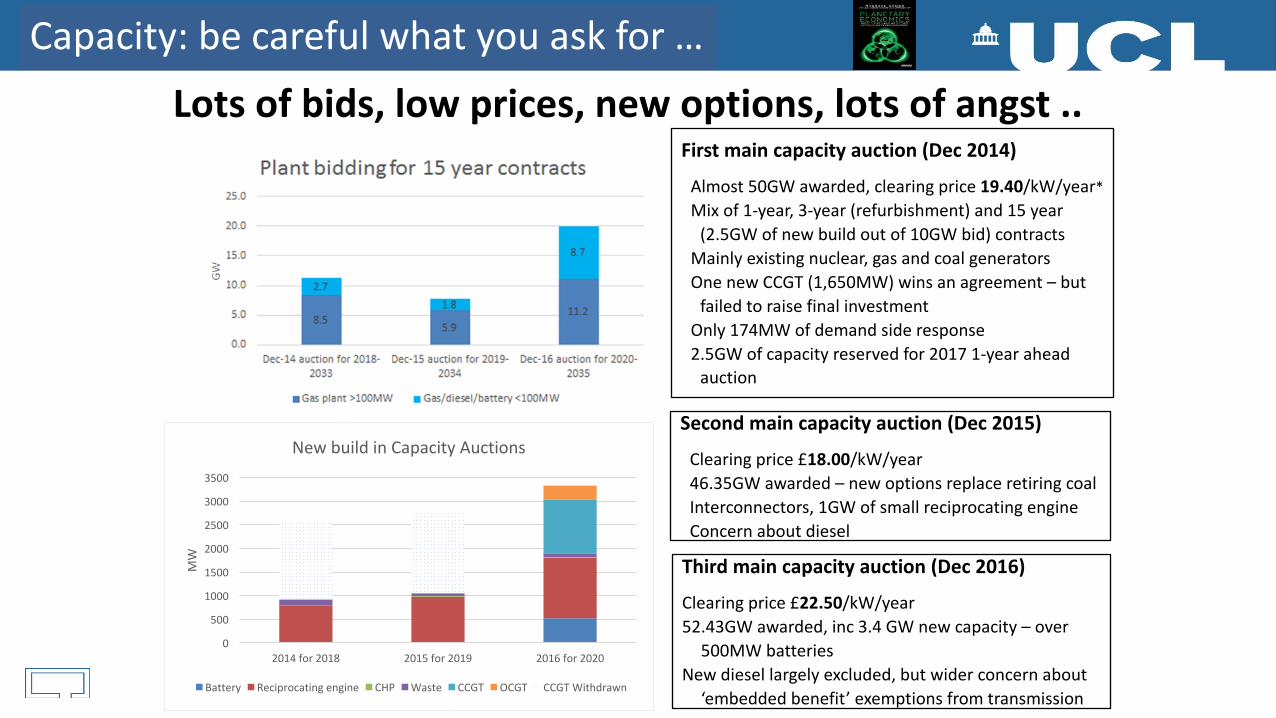

Lotsofbids,lowprices,newoptions,lotsofangst..

(b)SuccessfulNewBuildcapacitybyfuelandtechnologytypeintheT-4auctions

Firstmaincapacityauction(Dec2014)

Almost50GWawarded,clearingprice19.40/kW/year*Mixof1-year,3-year(refurbishment)and15year(2.5GWofnewbuildoutof10GWbid)contracts

Mainlyexistingnuclear,gasandcoalgeneratorsOnenewCCGT(1,650MW)winsanagreement– butfailedtoraisefinalinvestment

Only174MWofdemandsideresponse2.5GWofcapacityreservedfor20171-yearaheadauction

Secondmaincapacityauction(Dec2015)

Clearingprice£18.00/kW/year46.35GWawarded– newoptionsreplaceretiringcoalInterconnectors,1GWofsmallreciprocatingengineConcernaboutdiesel

Thirdmaincapacityauction(Dec2016)

Clearingprice£22.50/kW/year52.43GWawarded,inc 3.4GWnewcapacity– over

500MWbatteriesNewdiesellargelyexcluded,butwiderconcernabout

‘embeddedbenefit’exemptionsfromtransmission

0

500

1000

1500

2000

2500

3000

3500

2014for2018 2015for2019 2016for2020

MW

NewbuildinCapacityAuctions

Battery Reciprocatingengine CHP Waste CCGT OCGT CCGTWithdrawn

Capacity:becarefulwhatyouaskfor…

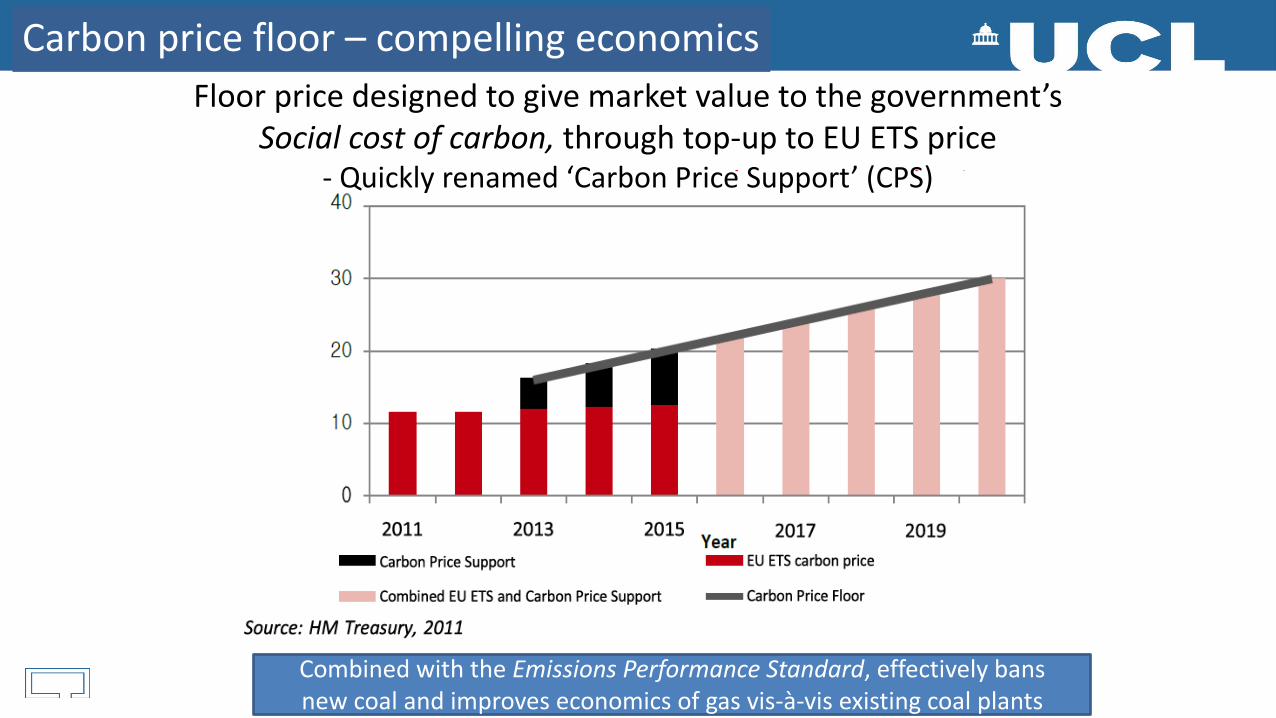

Floorpricedesignedtogivemarketvaluetothegovernment’sSocialcostofcarbon,throughtop-uptoEUETSprice

- Quicklyrenamed‘CarbonPriceSupport’(CPS)

CombinedwiththeEmissionsPerformanceStandard,effectivelybansnewcoalandimproveseconomicsofgasvis-à-visexistingcoalplants

Carbonpricefloor– compellingeconomics

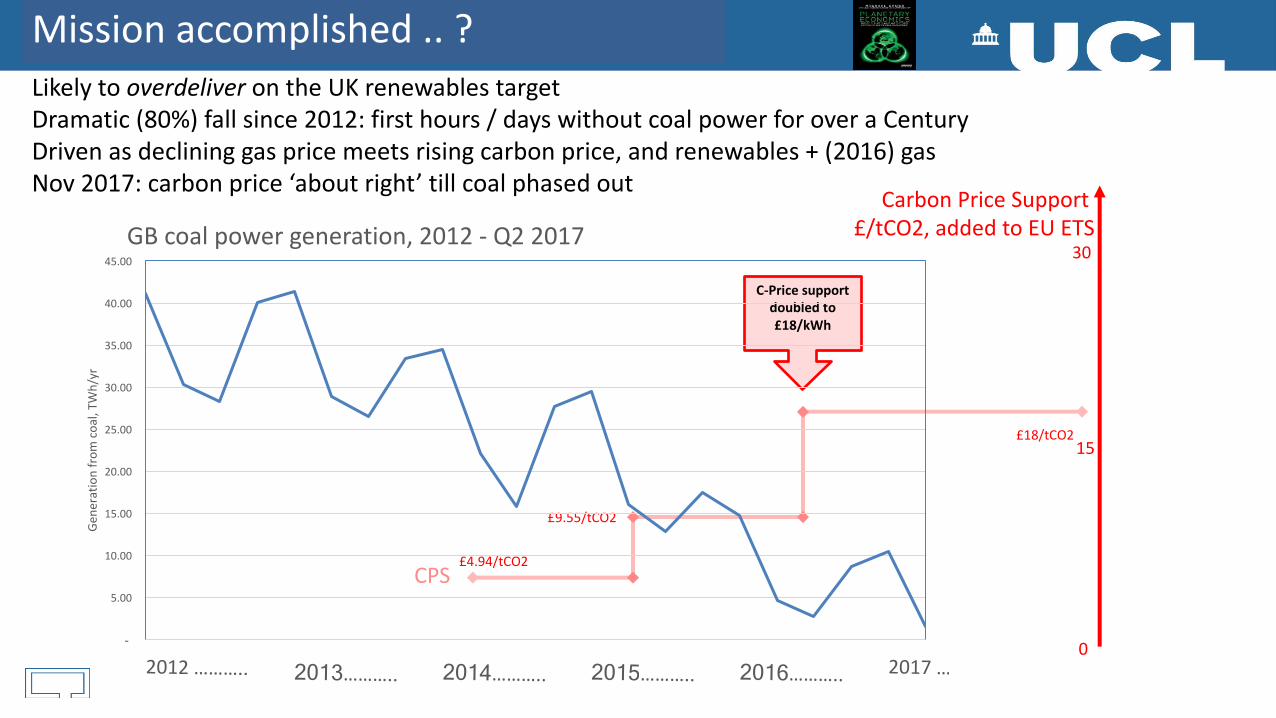

Missionaccomplished..?Likelytooverdeliver ontheUKrenewablestargetDramatic(80%)fallsince2012:firsthours/dayswithoutcoalpowerforoveraCenturyDrivenasdeclininggaspricemeetsrisingcarbonprice,andrenewables+(2016)gasNov2017:carbonprice‘aboutright’tillcoalphasedout

CarbonPriceSupport£/tCO2,addedtoEUETS

30

15

£4.94/tCO2

£9.55/tCO2

£18/tCO2

C-Pricesupportdoubledto£18/kWh

CPS

0-

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

Gene

ratio

nfrom

coal,TW

h/yr

GBcoalpowergeneration,2012- Q22017

• Introduction to “Planetary Economics”: Three Domains and Three Pillars of Policy

• The ‘Solow Residual’ and the innovation paradox• UK electricity market reform and transformation • Innovation pathways and the renewables revolution

• Porter’s Kick? Macroeconomics of transformation – World Bank presentation• Innovation and adaptive system Modelling – RFF presentation

‘PlanetaryEconomics’,energytransition&policyexperience

SeminartoDukeUniversity,1st December2017

Energy, Climate Change and the Three Domains of

Sustainable Development@michaelgrubb9

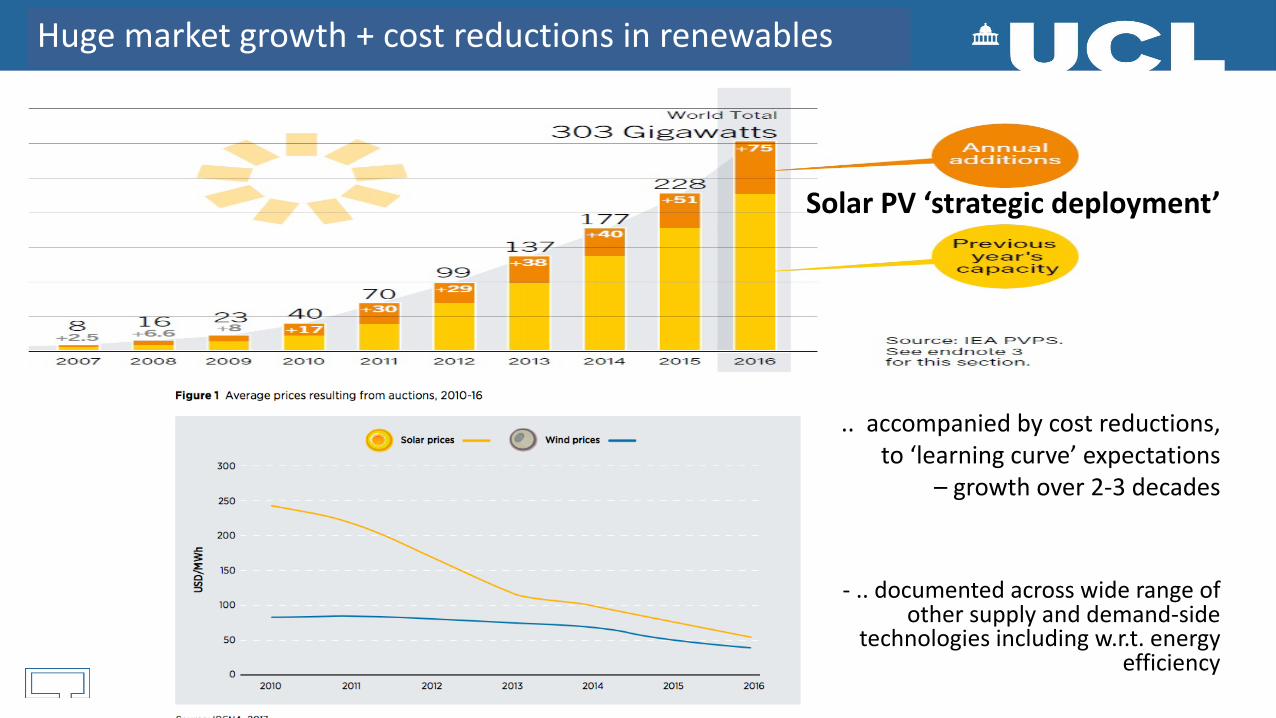

- ..documentedacrosswiderangeofothersupplyanddemand-side

technologiesincludingw.r.t.energyefficiency

..accompaniedbycostreductions,to‘learningcurve’expectations

– growthover2-3decades

SolarPV‘strategicdeployment’

Hugemarketgrowth+costreductionsinrenewables

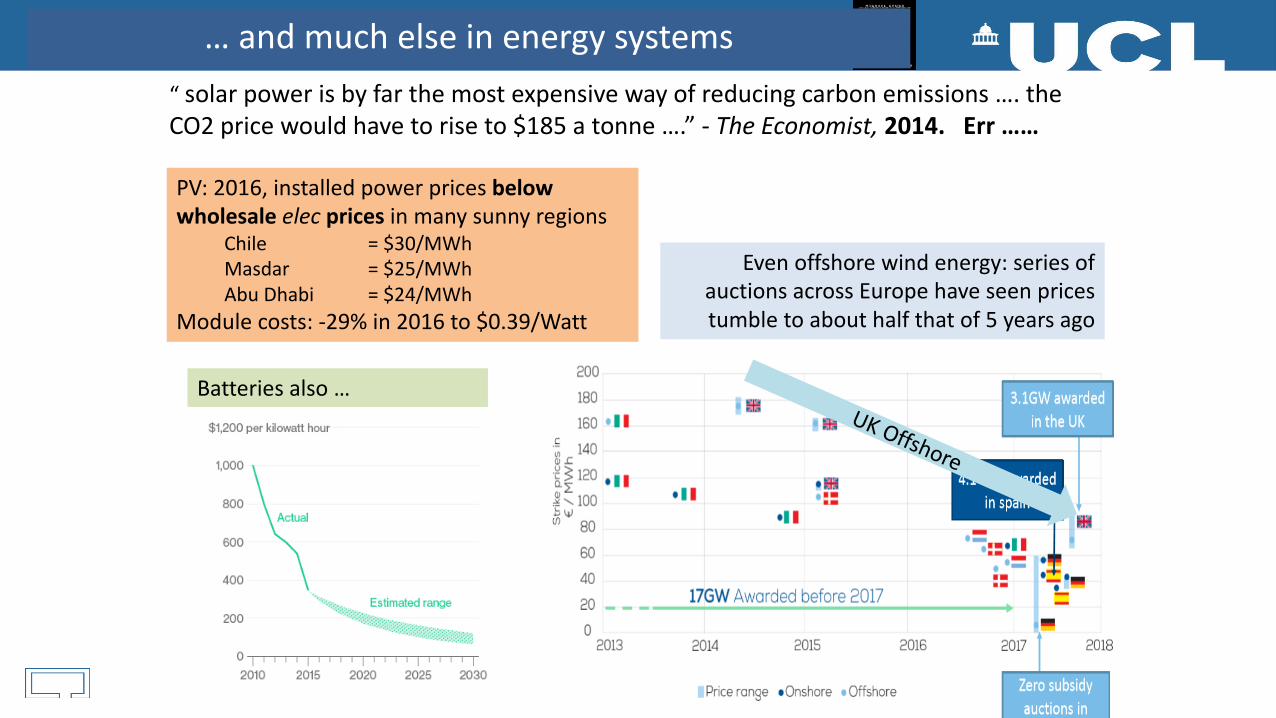

PV:2016,installedpowerpricesbelowwholesaleelec pricesinmanysunnyregions

Chile =$30/MWhMasdar =$25/MWhAbuDhabi =$24/MWh

Modulecosts:-29%in2016to$0.39/Watt

…andmuchelseinenergysystems“solarpowerisbyfarthemostexpensivewayofreducingcarbonemissions….theCO2pricewouldhavetoriseto$185atonne….”- TheEconomist,2014.Err……

Evenoffshorewindenergy:seriesofauctionsacrossEuropehaveseenpricestumbletoabouthalfthatof5yearsago

Batteriesalso…

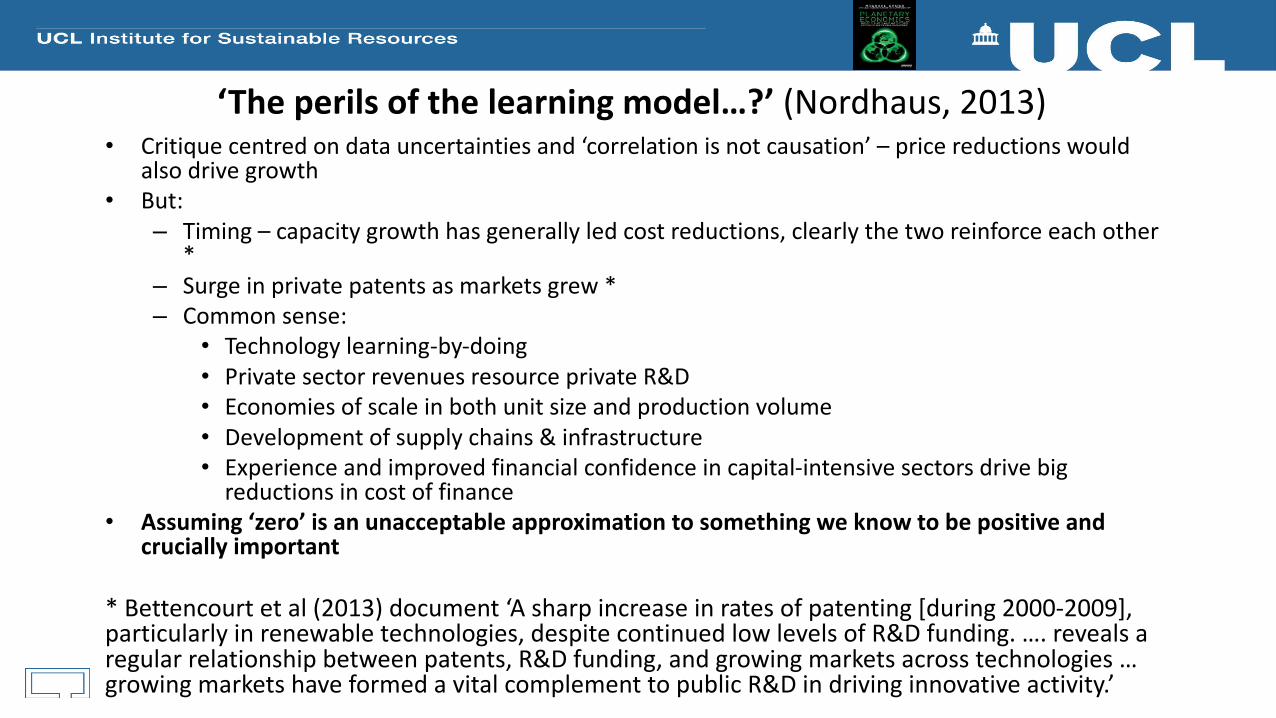

‘Theperilsofthelearningmodel…?’(Nordhaus,2013)• Critiquecentredondatauncertaintiesand‘correlationisnotcausation’– pricereductionswould

alsodrivegrowth• But:

– Timing– capacitygrowthhasgenerallyledcostreductions,clearlythetworeinforceeachother*

– Surgeinprivatepatentsasmarketsgrew*– Commonsense:

• Technologylearning-by-doing• PrivatesectorrevenuesresourceprivateR&D• Economiesofscaleinbothunitsizeandproductionvolume• Developmentofsupplychains&infrastructure• Experienceandimprovedfinancialconfidenceincapital-intensivesectorsdrivebigreductionsincostoffinance

• Assuming‘zero’isanunacceptableapproximationtosomethingweknowtobepositiveandcruciallyimportant

*Bettencourtetal(2013)document‘Asharpincreaseinratesofpatenting[during2000-2009],particularlyinrenewabletechnologies,despitecontinuedlowlevelsofR&Dfunding.….revealsaregularrelationshipbetweenpatents,R&Dfunding,andgrowingmarketsacrosstechnologies…growingmarketshaveformedavitalcomplementtopublicR&Dindrivinginnovativeactivity.’

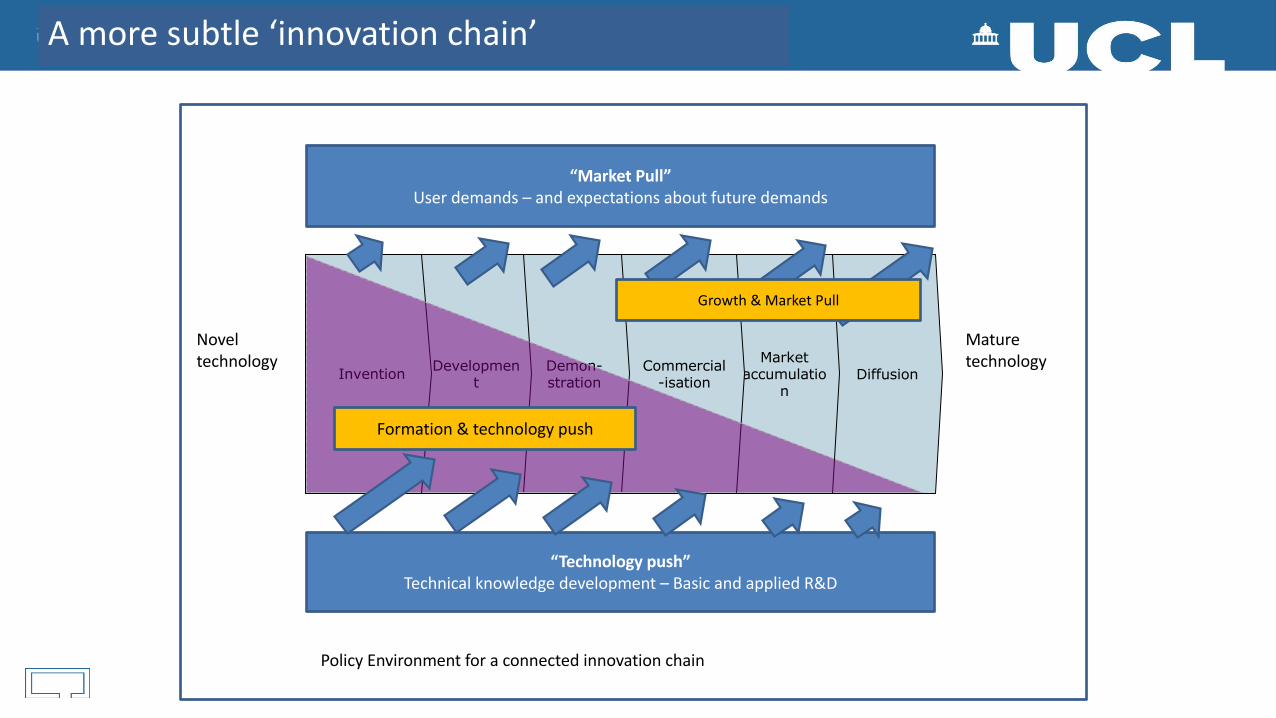

Diffusion

Supply/Research

Market accumulatio

n

Commercial-isation

Demon-stration

DevelopmentInvention

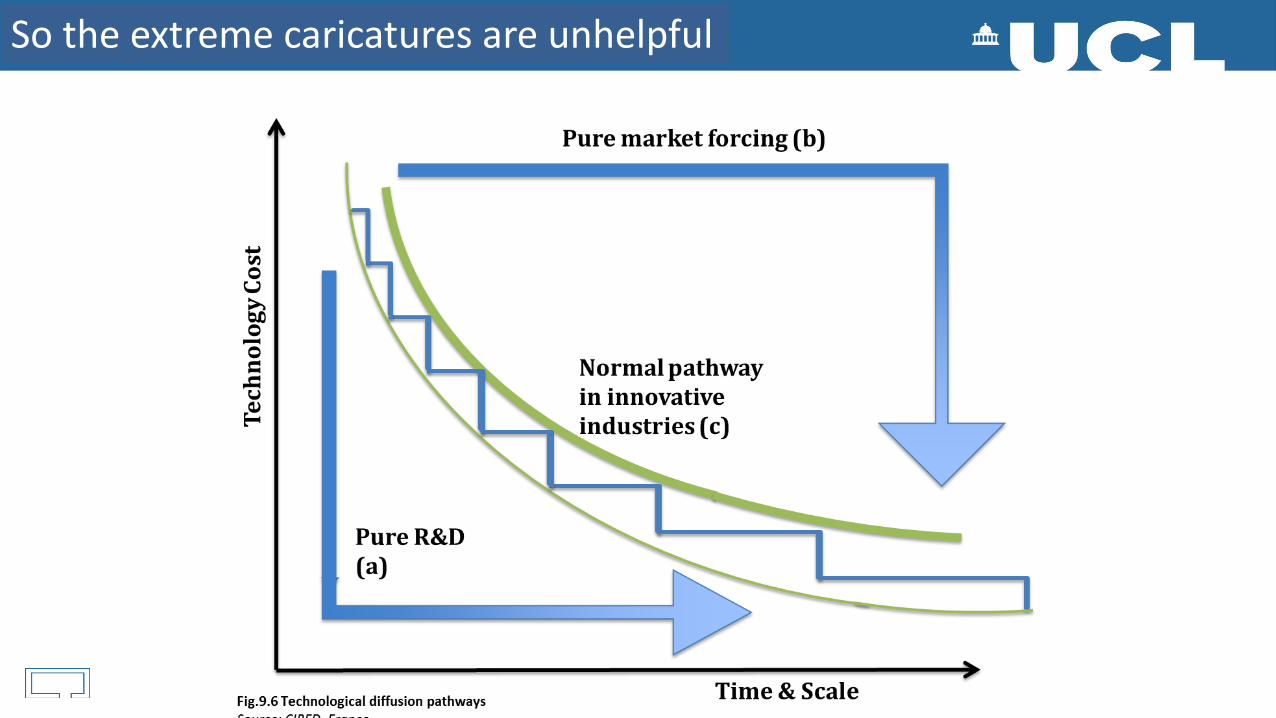

“Technologypush”Technicalknowledgedevelopment– BasicandappliedR&D

“MarketPull”Userdemands– andexpectationsaboutfuturedemands

Formation&technologypush

PolicyEnvironmentforaconnectedinnovationchain

Maturetechnology

Noveltechnology

Growth&MarketPull

Amoresubtle‘innovationchain’

Sotheextremecaricaturesareunhelpful

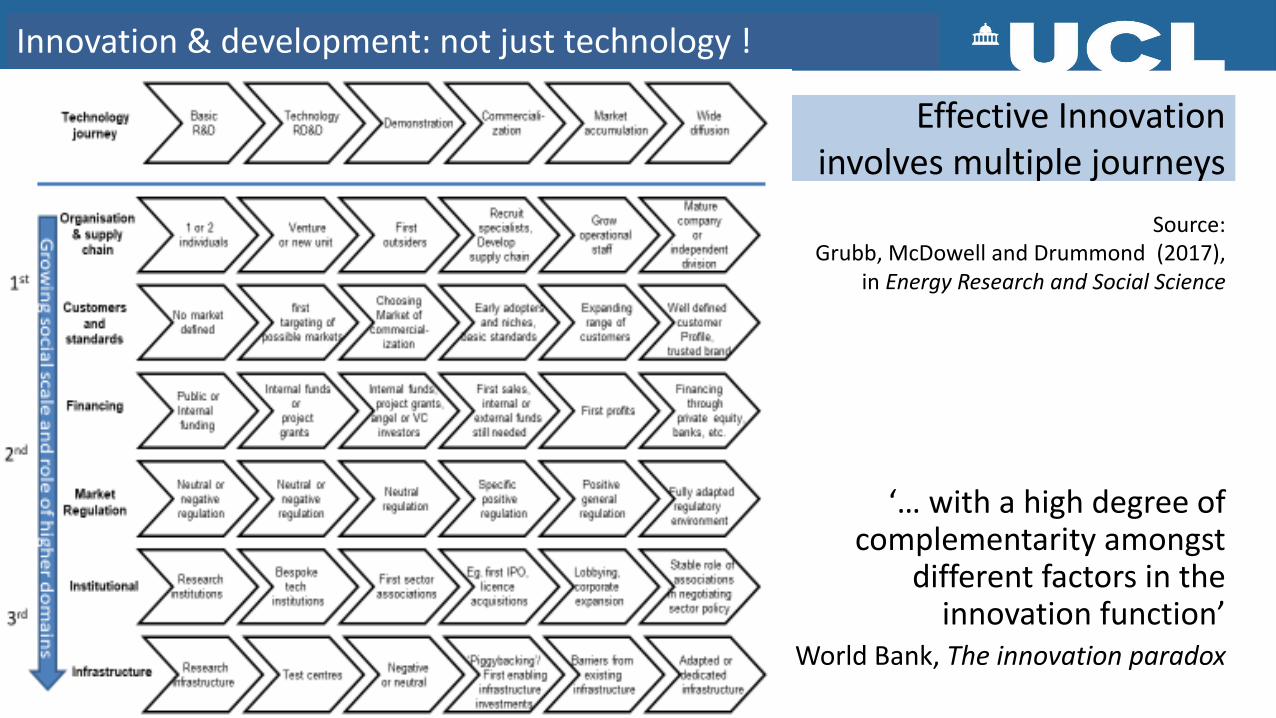

EffectiveInnovationinvolvesmultiplejourneys

‘…withahighdegreeofcomplementarityamongst

differentfactorsintheinnovationfunction’

WorldBank,Theinnovationparadox

Source:Grubb,McDowellandDrummond(2017),

inEnergyResearchandSocialScience

Innovation&development:notjusttechnology!

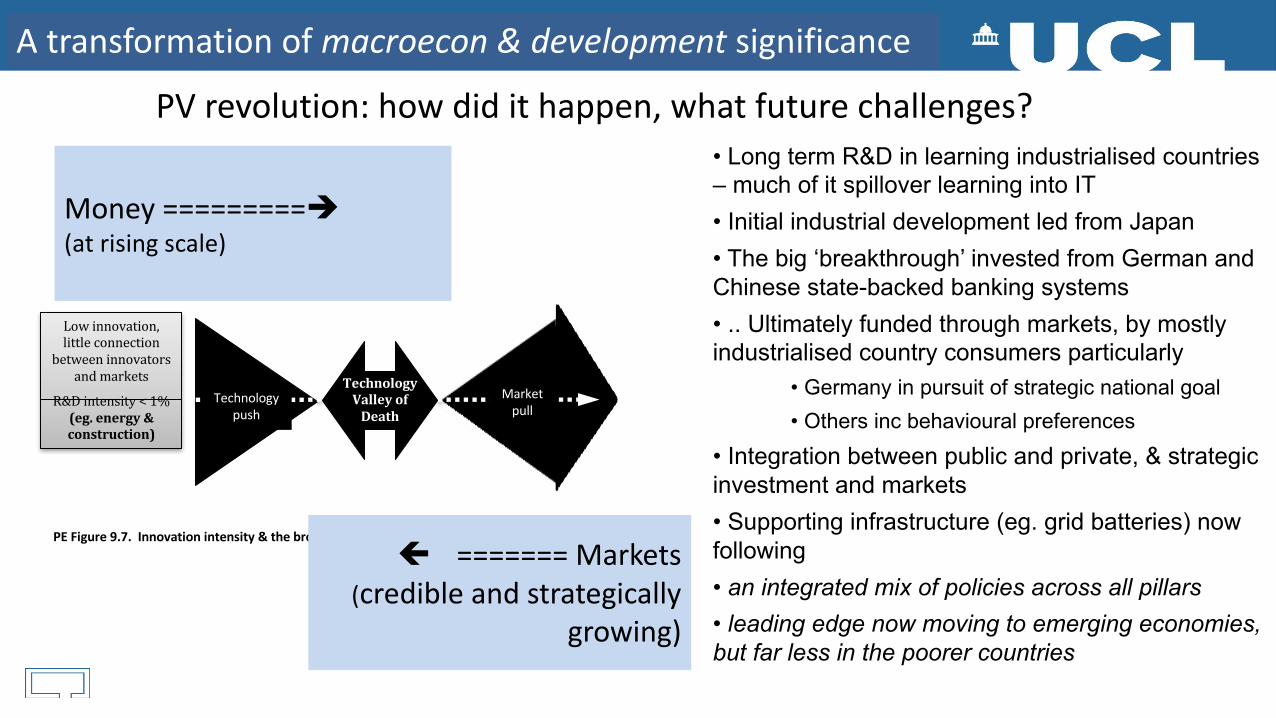

Atransformationofmacroecon &developmentsignificance

Lowinnovation,littleconnection

betweeninnovatorsandmarkets

R&Dintensity<1%(eg.energy&construction)

Marketpull

Technologypush

TechnologyValleyofDeath

PEFigure9.7.Innovationintensity&thebrokenchain

Money=========è(atrisingscale)

ç ======= Markets(credibleandstrategically

growing)

• Long term R&D in learning industrialised countries – much of it spillover learning into IT• Initial industrial development led from Japan • The big ‘breakthrough’ invested from German and Chinese state-backed banking systems• .. Ultimately funded through markets, by mostly industrialised country consumers particularly

• Germany in pursuit of strategic national goal• Others inc behavioural preferences

• Integration between public and private, & strategic investment and markets• Supporting infrastructure (eg. grid batteries) now following• an integrated mix of policies across all pillars• leading edge now moving to emerging economies, but far less in the poorer countries

PVrevolution: howdidithappen,whatfuturechallenges?

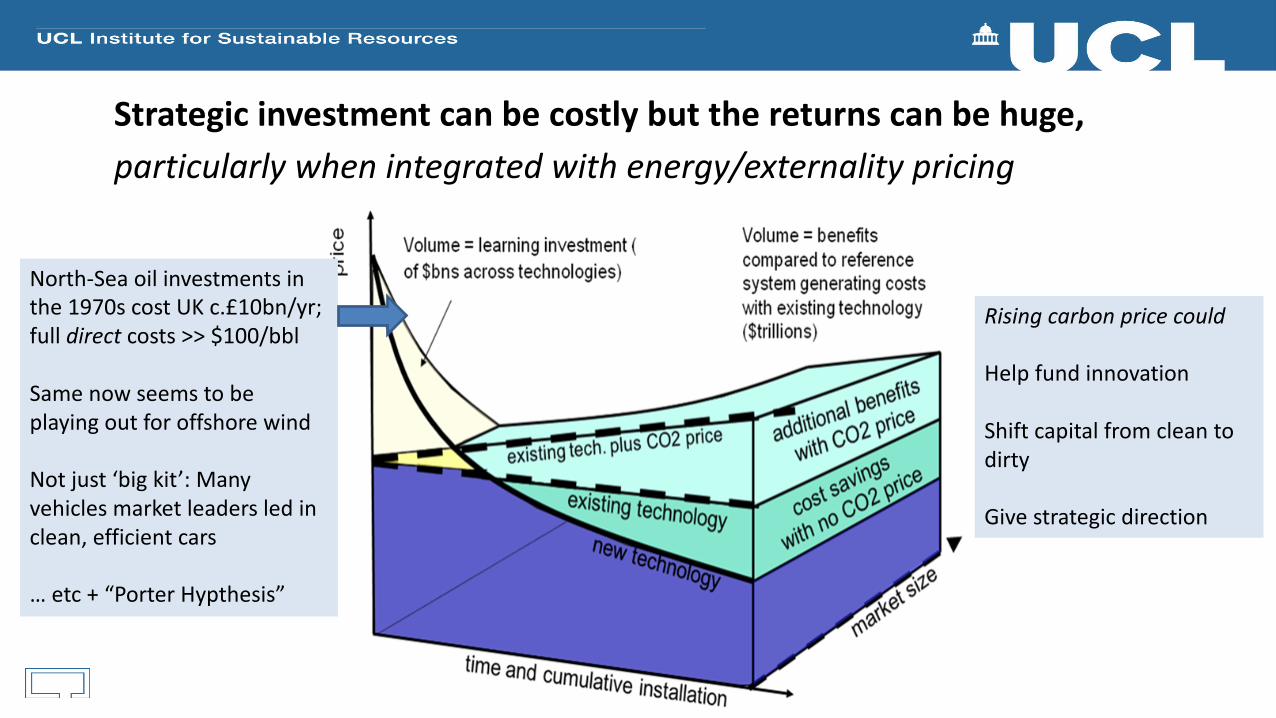

Strategicinvestmentcanbecostlybutthereturnscanbehuge,particularlywhenintegratedwithenergy/externalitypricing

North-Seaoilinvestmentsinthe1970scostUKc.£10bn/yr;fulldirectcosts>>$100/bbl

Samenowseemstobeplayingoutforoffshorewind

Notjust‘bigkit’:Manyvehiclesmarketleadersledinclean,efficientcars

…etc +“PorterHypthesis”

Risingcarbonpricecould

Helpfundinnovation

Shiftcapitalfromcleantodirty

Givestrategicdirection

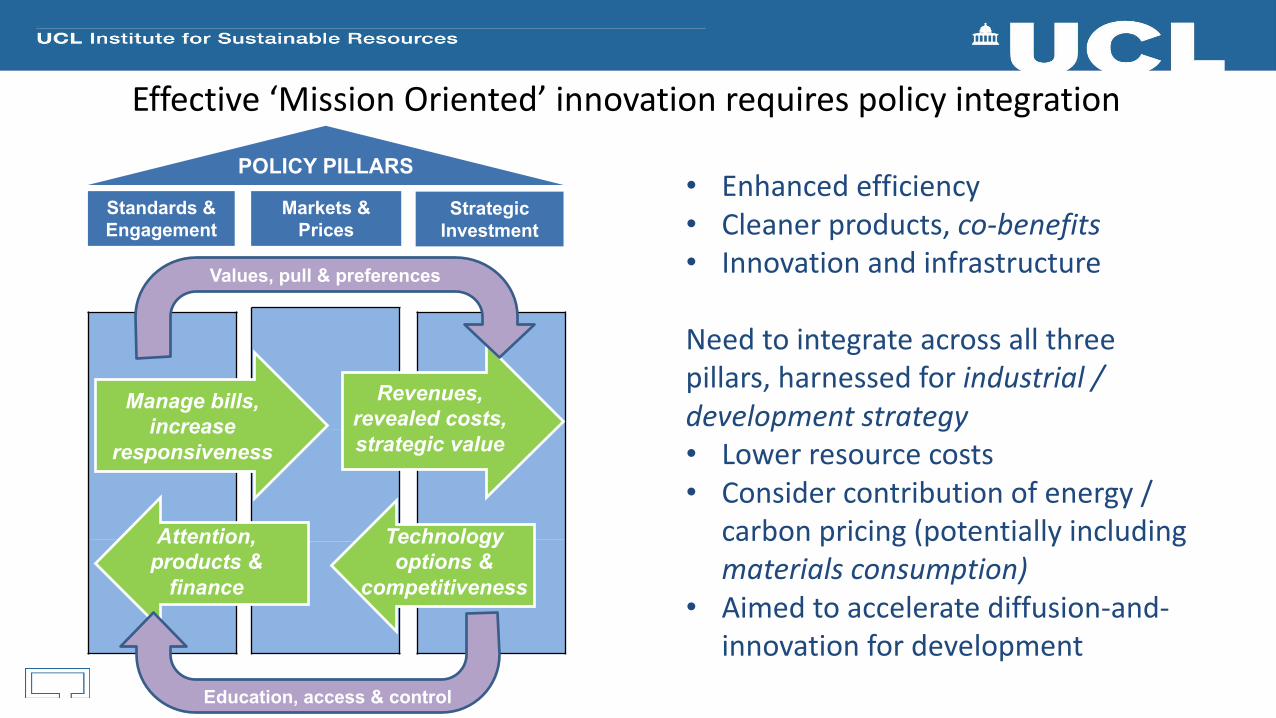

Standards & Engagement

Markets & Prices

Strategic Investment

POLICY PILLARS

Technology options &

competitiveness

• Enhancedefficiency• Cleanerproducts,co-benefits• Innovationandinfrastructure

Needtointegrateacrossallthreepillars,harnessedforindustrial/developmentstrategy• Lowerresourcecosts• Considercontributionofenergy/

carbonpricing(potentiallyincludingmaterialsconsumption)

• Aimedtoacceleratediffusion-and-innovationfordevelopment

Manage bills, increase

responsiveness

Revenues, revealed costs, strategic value

Values, pull & preferences

Attention, products &

finance

Education, access & control

Effective‘MissionOriented’innovationrequirespolicyintegration

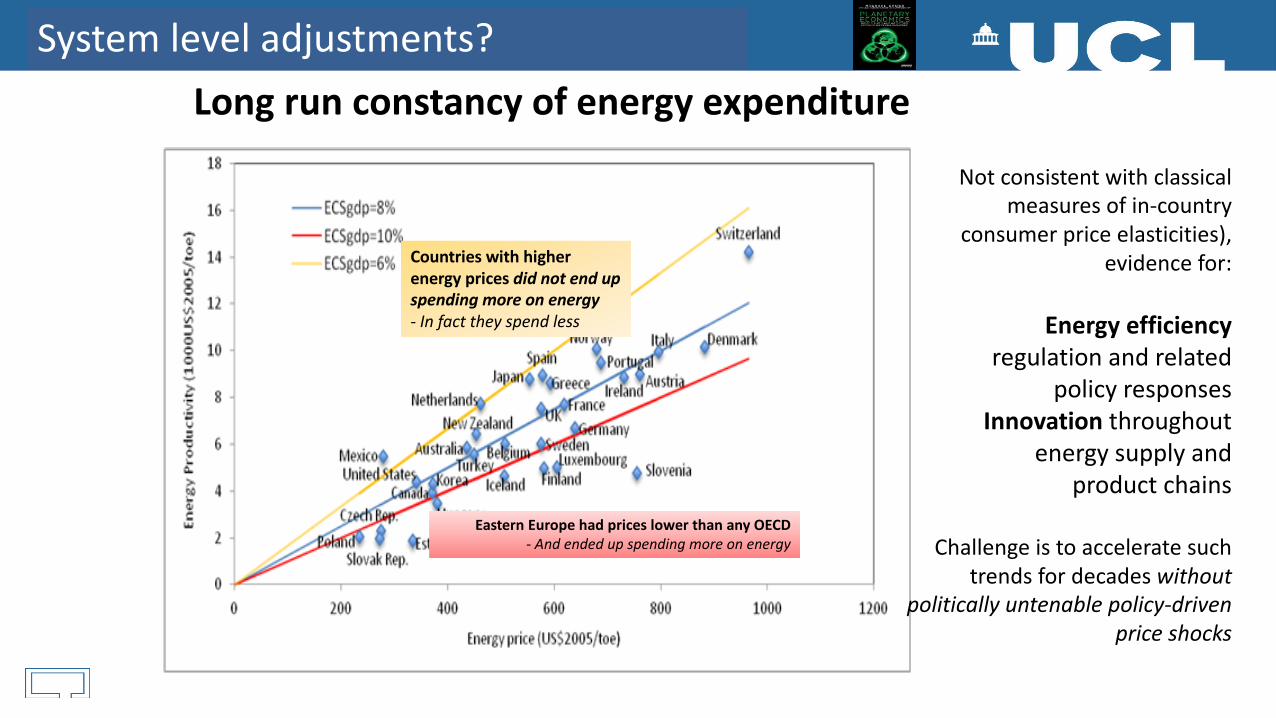

Countrieswithhigherenergypricesdidnotendupspendingmoreonenergy- Infacttheyspendless

EasternEuropehadpriceslowerthananyOECD- Andendedupspendingmoreonenergy

Notconsistentwithclassicalmeasuresofin-country

consumerpriceelasticities),evidencefor:

Energyefficiencyregulation andrelated

policyresponsesInnovation throughout

energysupplyandproductchains

Challengeistoacceleratesuchtrendsfordecadeswithout

politicallyuntenablepolicy-drivenpriceshocks

LongrunconstancyofenergyexpenditureSystemleveladjustments?

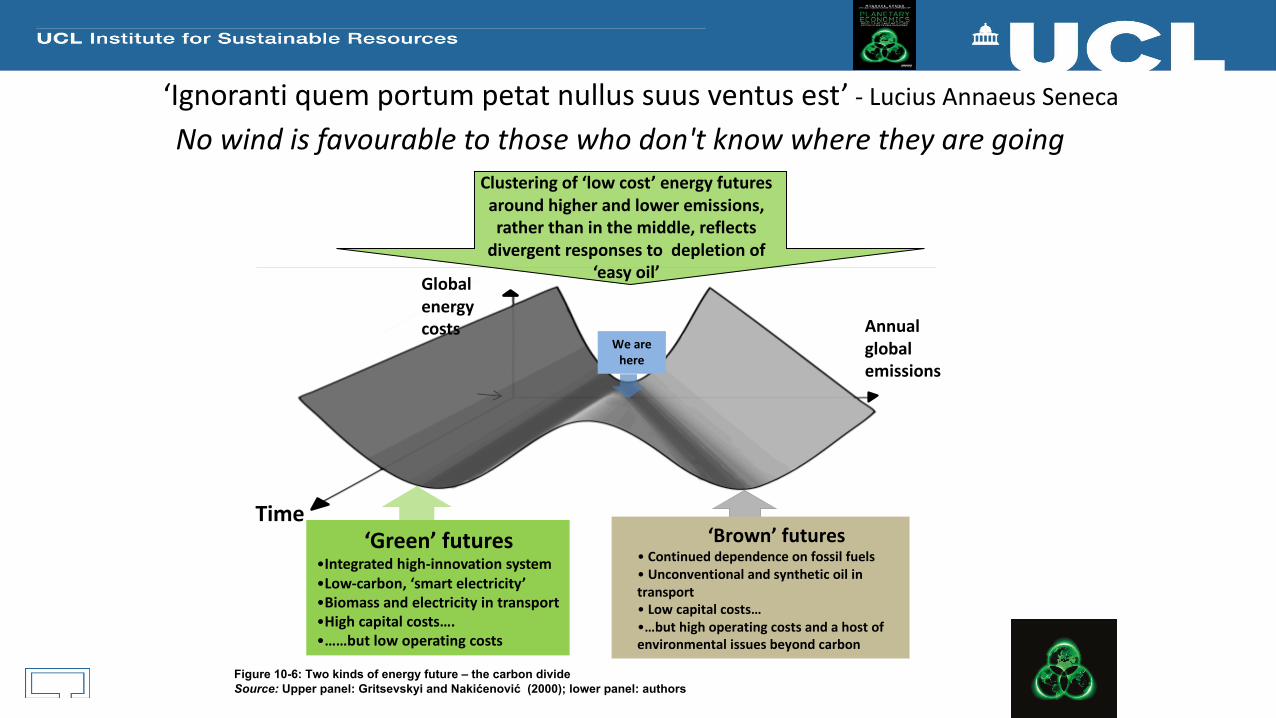

Globalenergycosts Annual

globalemissions

Time‘Green’futures

•Integratedhigh-innovationsystem•Low-carbon,‘smartelectricity’•Biomassandelectricityintransport•Highcapitalcosts….•……butlowoperatingcosts

‘Brown’futures• Continueddependenceonfossilfuels• Unconventionalandsyntheticoilintransport• Lowcapitalcosts…•…buthighoperatingcostsandahostofenvironmentalissuesbeyondcarbon

Clusteringof‘lowcost’energyfuturesaroundhigherandloweremissions,ratherthaninthemiddle,reflectsdivergentresponsestodepletionof

‘easyoil’

Wearehere

Figure 10-6: Two kinds of energy future – the carbon divideSource: Upper panel: Gritsevskyi and Nakićenović (2000); lower panel: authors

‘Ignoranti quemportum petat nullus suus ventus est’ - LuciusAnnaeus SenecaNowindisfavourabletothosewhodon'tknowwheretheyaregoing

Afinalremark:on‘interdisciplinaryeconomics’

• FullyunderstandingtheThreeDomainsinevitablymustdrawalsoonotherdisciplines– SocialandpsychologicaldimensionsofriskperceptionsandFirstDomainbehaviours

– EngineeringandphysicaldeterminantsofThirdDomaininnovationsandinfrastructure

– Theregulatory,institutionalandpolitical-economydimensionsofboth

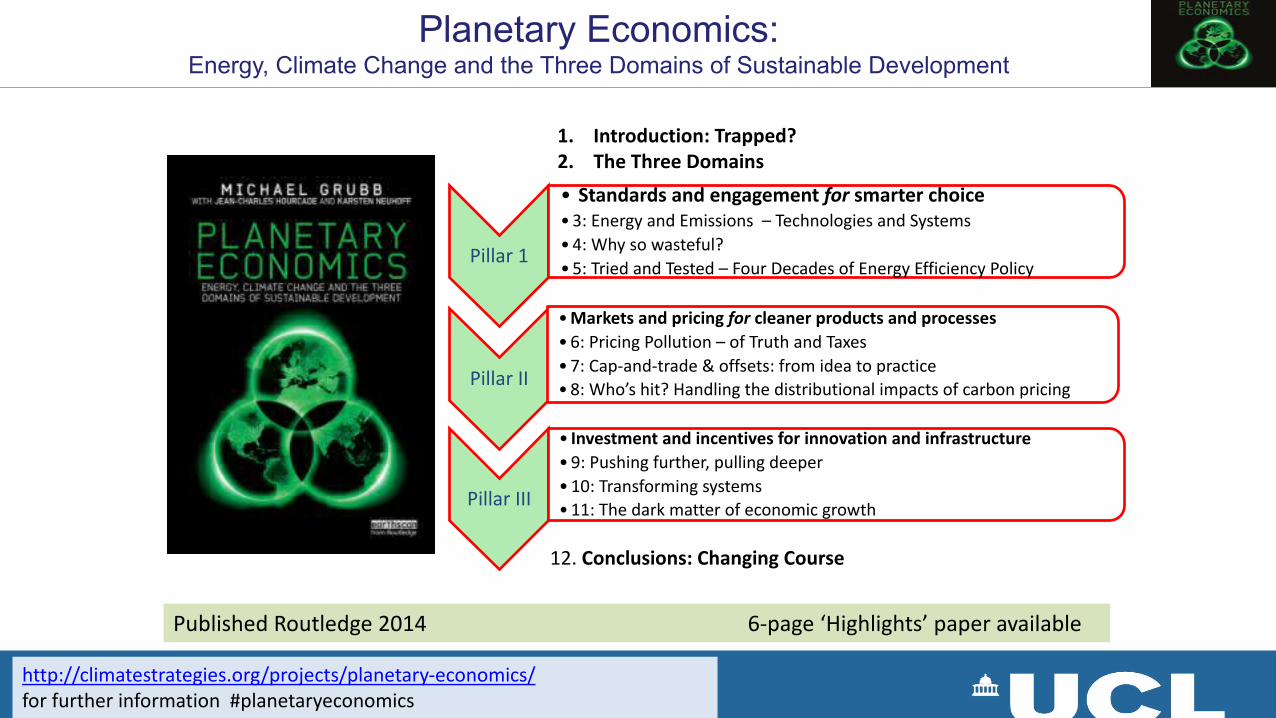

Planetary Economics: Energy, Climate Change and the Three Domains of Sustainable Development

Pillar1

• Standardsandengagementfor smarterchoice•3:EnergyandEmissions– TechnologiesandSystems• 4:Whysowasteful?• 5:TriedandTested– FourDecadesofEnergyEfficiencyPolicy

PillarII

•Marketsandpricing for cleanerproductsandprocesses•6:PricingPollution– ofTruthandTaxes•7:Cap-and-trade&offsets:fromideatopractice•8:Who’shit?Handlingthedistributionalimpactsofcarbonpricing

PillarIII

• Investmentandincentivesforinnovationandinfrastructure•9:Pushingfurther,pullingdeeper•10:Transformingsystems•11:Thedarkmatterofeconomicgrowth

1. Introduction:Trapped?2. TheThreeDomains

12.Conclusions:ChangingCourse

http://climatestrategies.org/projects/planetary-economics/forfurtherinformation#planetaryeconomics

PublishedRoutledge2014 6-page‘Highlights’paperavailable