pfe_cha

DESCRIPTION

etatTRANSCRIPT

Date29-Dec-89 42.2500 - 31-Dec-90 34.3750 3.00 -11.54% #VALUE!31-Dec-91 28.8750 1.60 -11.35% #VALUE!31-Dec-92 32.2500 1.40 16.54%31-Dec-93 54.8750 0.80 72.64%30-Dec-94 42.1250 0.80 -21.78%29-Dec-95 52.8750 1.10 28.13%31-Dec-96 55.7500 1.60 8.46%31-Dec-97 60.7500 5.59 19.00%31-Dec-98 71.5625 2.00 21.09%31-Dec-99 72.6875 14.15 21.34%

14.25% #VALUE!

0.0638 #VALUE!

25.25% #VALUE!

Ignore the material below unless you want to know how to make a backwardadjustment of prices for dividends.

Date Adjusted price29-Dec-89 42.2500 - 23.32 31-Dec-90 34.3750 3.00 37.38 20.63 31-Dec-91 28.8750 1.60 30.48 18.29 31-Dec-92 32.2500 1.40 33.65 21.31 31-Dec-93 54.8750 0.80 55.68 36.80 30-Dec-94 42.1250 0.80 42.93 28.78 29-Dec-95 52.8750 1.10 53.98 36.88 31-Dec-96 55.7500 1.60 57.35 40.00 31-Dec-97 60.7500 5.59 66.34 47.60 31-Dec-98 71.5625 2.00 73.56 57.64 31-Dec-99 72.6875 14.15 86.84 69.94 29-Dec-00 50.9375 2.00 52.94 50.94

PRICE AND DIVIDEND DATA FOR GENERAL MOTORS (GM)

Closing Price Dividend

Annual return

Average return, E(rGM)

Variance of return, s2GM

Standard deviation of return, sGM

Closing Price

Dividend Cash

Amount

Price plus

dividend

A B C D E

1

2

3456789

1011121314

15

16

17

181920212223242526

27

282930313233343536373839

Return

-11.54%-11.35%16.54%72.64%

-21.78%28.13%

#VALUE! 8.46% #VALUE!#VALUE! 19.00% #VALUE!#VALUE! 21.09% #VALUE!#VALUE! 21.34% #VALUE!#VALUE! -27.17% #VALUE!

F G H

1

2

3456789

1011121314

15

16

17

181920212223242526

27

282930313233343536373839

Date29-Dec-89 87.000031-Dec-90 75.2500 2.0 for 131-Dec-91 111.2500 1.5 for 131-Dec-92 85.3750 1.5 for 131-Dec-93 80.6250 no30-Dec-94 61.1250 2.0 for 129-Dec-95 87.7500 no31-Dec-96 82.6250 2.0 for 131-Dec-97 129.2500 no31-Dec-98 138.6875 2.0 for 131-Dec-99 116.7500 2.0 for 1

Date29-Dec-89 87.0000 1 87.00 31-Dec-90 75.2500 2.0 for 1 2 150.50 72.99%31-Dec-91 111.2500 1.5 for 1 3 333.75 121.76%31-Dec-92 85.3750 1.5 for 1 4.5 384.19 15.11%31-Dec-93 80.6250 no 4.5 362.81 -5.56%30-Dec-94 61.1250 2.0 for 1 9 550.13 51.63%29-Dec-95 87.7500 no 9 789.75 43.56%31-Dec-96 82.6250 2.0 for 1 18 1,487.25 88.32%31-Dec-97 129.2500 no 18 2,326.50 56.43%31-Dec-98 138.6875 2.0 for 1 36 4,992.75 114.60%31-Dec-99 116.7500 2.0 for 1 72 8,406.00 68.36%

62.72%

14.43%

37.99%

PRICE AND STOCK SPLIT

DATA FOR MICROSOFT (MSFT)

Closing Price

Stock split

during year?

Closing Price

Stock split

during year?

Cumulativeadjustment

factorAdjusted

priceAnnualreturn

Average return, E(rMSFT)

Variance of return, s2MSFT

Standard deviation of return, sMSFT

The cumulative adjustment factor is the product of all the splits:72 = 2*1.5*1.5*2*2*2*2

A B C D E F

1

2

3456789

101112131415

16

171819202122232425262728

29

30

31

3233

#VALUE!#VALUE!

#VALUE!

#VALUE!

#VALUE!

G

1

2

3456789

101112131415

16

171819202122232425262728

29

30

31

3233

Date29-Dec-89 1.208331-Dec-90 2.0903 73.00% #VALUE!31-Dec-91 4.6354 121.76% #VALUE!31-Dec-92 5.3359 15.11% #VALUE!31-Dec-93 5.0391 -5.56% #VALUE!30-Dec-94 7.6406 51.63% #VALUE!29-Dec-95 10.9688 43.56% #VALUE!31-Dec-96 20.6562 88.32% #VALUE!31-Dec-97 32.3125 56.43% #VALUE!31-Dec-98 69.3438 114.60% #VALUE!31-Dec-99 116.7500 68.36% #VALUE!

62.72% #VALUE!

14.43% #VALUE!

37.99% #VALUE!

DOWNLOADED GM PRICE DATA, YAHOO

Date Close29-Dec-89 21.731-Dec-90 19 -12.44% -11.54%31-Dec-91 16.47 -13.32% -11.35%31-Dec-92 19.12 16.09% 16.54%31-Dec-93 33.15 73.38% 72.64%30-Dec-94 25.86 -21.99% -21.78%29-Dec-95 33.28 28.69% 28.13%31-Dec-96 36.16 8.65% 8.46%31-Dec-97 43.17 19.39% 19.00%31-Dec-98 52.37 21.31% 21.09%31-Dec-99 66.05 26.12% 21.34%

Note: The reason the Yahoo computed returnsare different from the ones computed in the textis that the text assumes (wrongly--Yahoo is right)that dividends are paid and reinvested at the end of the year.

DOWNLOADED ADJUSTED DATA FROM YAHOOFOR MICROSOFT

MSFT adjusted

price

Average return, E(rMSFT)

Variance of return, s2MSFT

Standard deviation of return, sMSFT

return in text

A B C D

1

2

3456789

1011121314

15

16

17

1819

20

212223242526272829303132333435363738

GM AND MSFT, ANNUAL RETURN DATA

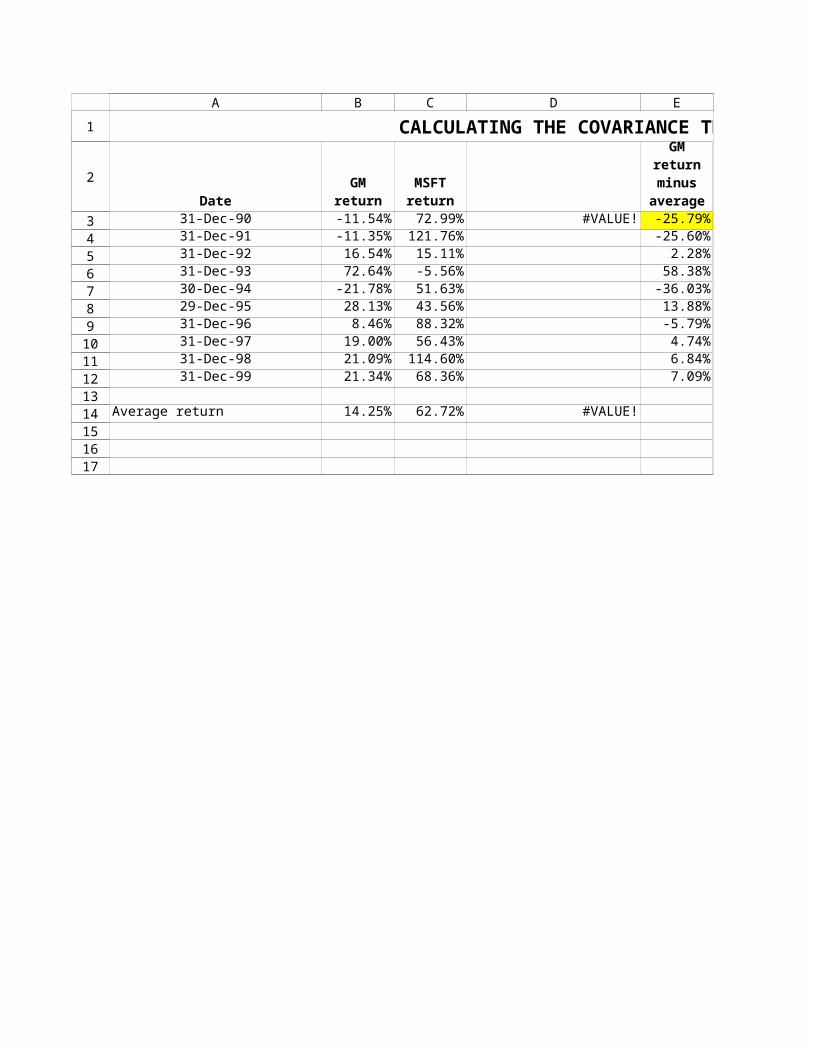

Date31-Dec-90 -11.54% 72.99%31-Dec-91 -11.35% 121.76%31-Dec-92 16.54% 15.11%31-Dec-93 72.64% -5.56%30-Dec-94 -21.78% 51.63%29-Dec-95 28.13% 43.56%31-Dec-96 8.46% 88.32%31-Dec-97 19.00% 56.43%31-Dec-98 21.09% 114.60%31-Dec-99 21.34% 68.36%

14.25% 62.72%

6.38% 14.43%

25.25% 37.99%

-0.0552

-0.5755-0.5755

GM return

MSFT return

Average return, E(rGM) and E(rMSFT)

Variance of return, s2GM and s2

MSFT

Standard deviation of return, sGM and sMSFT

Covariance of returns, Cov(rGM,rMSFT)

Correlation of returns, rGM,MSFT

A B C

1

2

3456789

10111213

14

15

16

17

18

19

GM AND MSFT, ANNUAL RETURN DATA

#VALUE!

#VALUE!#VALUE!

D

1

2

3456789

10111213

14

15

16

17

18

19

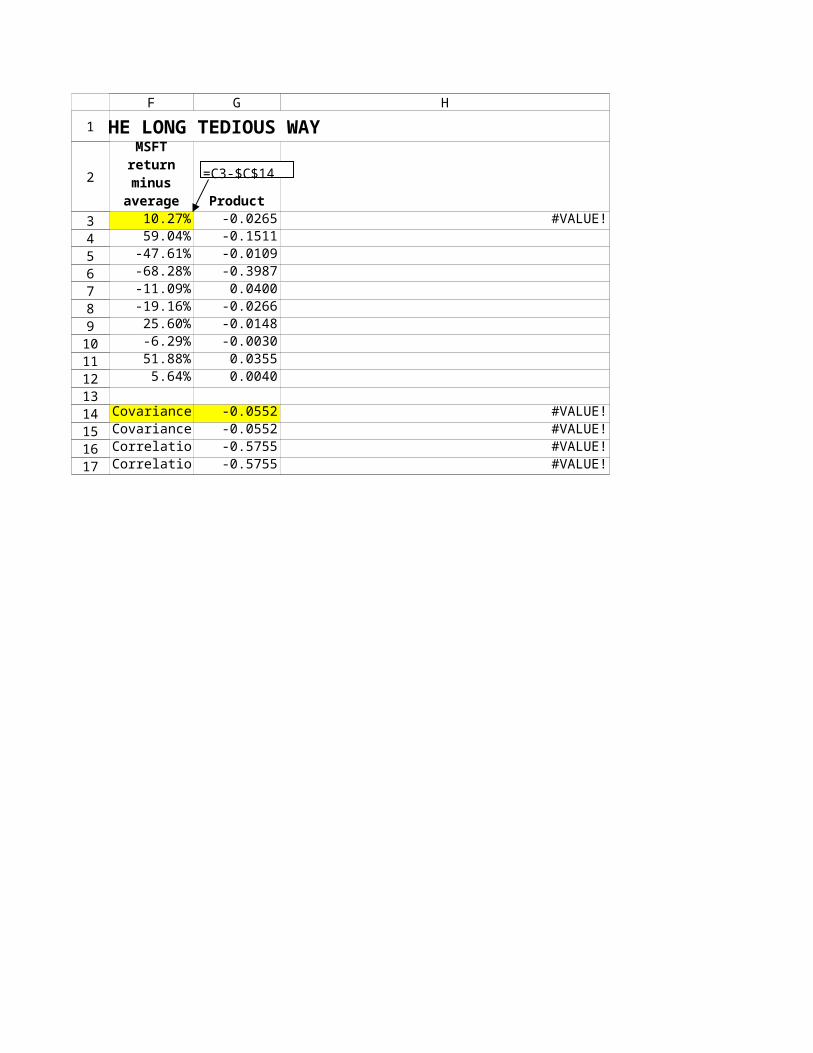

CALCULATING THE COVARIANCE THE LONG TEDIOUS WAY

Date31-Dec-90 -11.54% 72.99% #VALUE! -25.79%31-Dec-91 -11.35% 121.76% -25.60%31-Dec-92 16.54% 15.11% 2.28%31-Dec-93 72.64% -5.56% 58.38%30-Dec-94 -21.78% 51.63% -36.03%29-Dec-95 28.13% 43.56% 13.88%31-Dec-96 8.46% 88.32% -5.79%31-Dec-97 19.00% 56.43% 4.74%31-Dec-98 21.09% 114.60% 6.84%31-Dec-99 21.34% 68.36% 7.09%

Average return 14.25% 62.72% #VALUE!

GM return

MSFT return

GM returnminus

average

A B C D E

1

2

3456789

1011121314151617

CALCULATING THE COVARIANCE THE LONG TEDIOUS WAY

Product10.27% -0.0265 #VALUE!59.04% -0.1511

-47.61% -0.0109-68.28% -0.3987-11.09% 0.0400-19.16% -0.026625.60% -0.0148-6.29% -0.003051.88% 0.0355

5.64% 0.0040

Covariance -0.0552 #VALUE!Covariance -0.0552 #VALUE!Correlation -0.5755 #VALUE!Correlation -0.5755 #VALUE!

MSFT returnminus

average

=C3-$C$14

F G H

1

2

3456789

1011121314151617

Date29-Dec-8931-Dec-90 -11.54 72.9931-Dec-91 -11.35 121.7631-Dec-92 16.54 15.1131-Dec-93 72.64 -5.5630-Dec-94 -21.78 51.6329-Dec-95 28.13 43.5631-Dec-96 8.46 88.3231-Dec-97 19.00 56.4331-Dec-98 21.09 114.6031-Dec-99 21.34 68.36

14.25 62.72

637.80 1442.92

25.25 37.99

-552.10 #VALUE!

-0.5755 #VALUE!-0.5755 #VALUE!

-0.5755 #VALUE!

GM AND MSFT, ANNUAL RETURN DATAPercentages presented as whole numbers

GM annual return

MSFT annualreturn

Average return, E(rGM) and E(rMSFT)

Variance of return, s2GM and s2

MSFT

Standard deviation of return, sGM and sMSFT

Covariance of returns, Cov(rGM,rMSFT)

Correlation of returns, rGM,MSFT

Correlation is symmetric, rMSFT,GM

A B C D

1

2

3456789

1011121314

15

16

17

18

19

2021

22

Year1990 30.73% 21.44% #VALUE!1991 55.21% 36.13%1992 15.82% 12.49%1993 33.54% 23.12%1994 14.93% 11.96%1995 35.84% 24.50%1996 48.39% 32.03%1997 37.71% 25.63%1998 67.85% 43.71%1999 44.85% 29.91%

Correlation 1.00 #VALUE!

CORRELATION +1Adams Farm and Morgan Sausage Stocks

rMorgan Sausage,t = 3% + 0.6*rAdams Farm,t

AdamsFarm stock

return

MorganSausage

stockreturn

10% 20% 30% 40% 50% 60% 70%0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Annual Stock Returns, Adams Farm and Morgan Sausage

Adams Farm

Mo

rga

n S

au

sa

ge

A B C D

1

2

3456789

1011121314151617181920212223242526272829303132

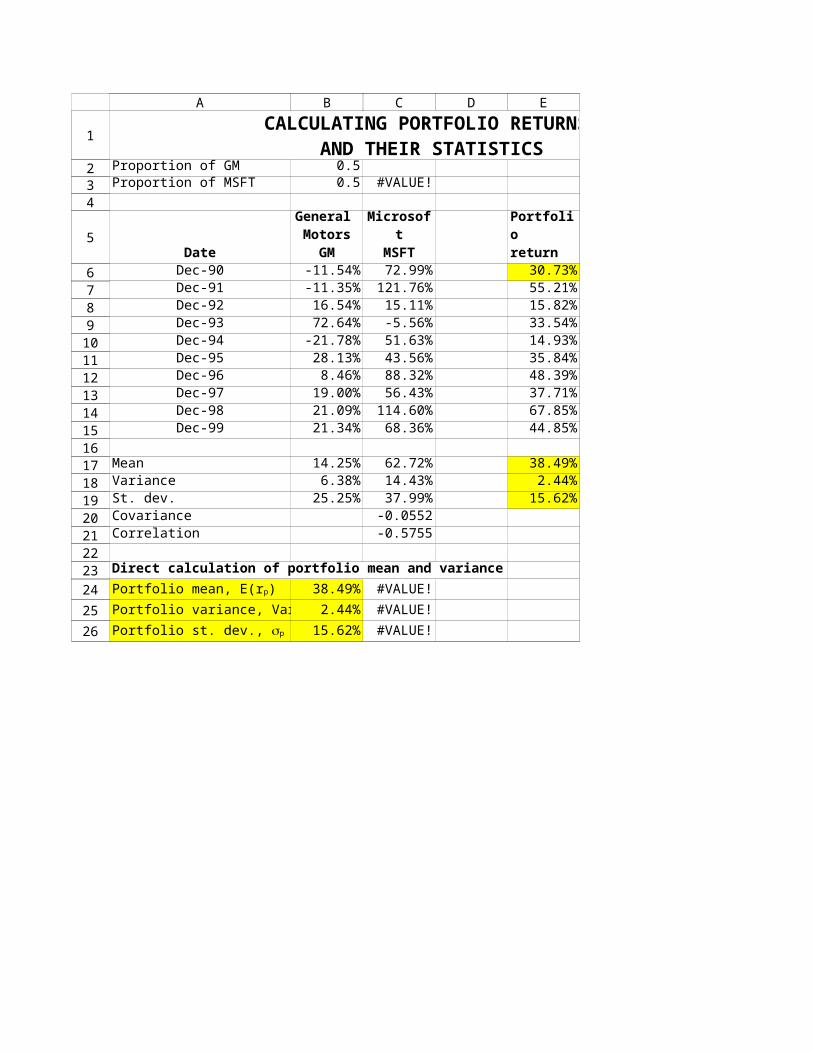

Proportion of GM 0.5Proportion of MSFT 0.5 #VALUE!

DateDec-90 -11.54% 72.99% 30.73% #VALUE!Dec-91 -11.35% 121.76% 55.21%Dec-92 16.54% 15.11% 15.82%Dec-93 72.64% -5.56% 33.54%Dec-94 -21.78% 51.63% 14.93%Dec-95 28.13% 43.56% 35.84%Dec-96 8.46% 88.32% 48.39%Dec-97 19.00% 56.43% 37.71%Dec-98 21.09% 114.60% 67.85%Dec-99 21.34% 68.36% 44.85%

Mean 14.25% 62.72% 38.49% #VALUE!Variance 6.38% 14.43% 2.44% #VALUE!St. dev. 25.25% 37.99% 15.62% #VALUE!Covariance -0.0552Correlation -0.5755

Direct calculation of portfolio mean and variance

38.49% #VALUE!

2.44% #VALUE!

15.62% #VALUE!

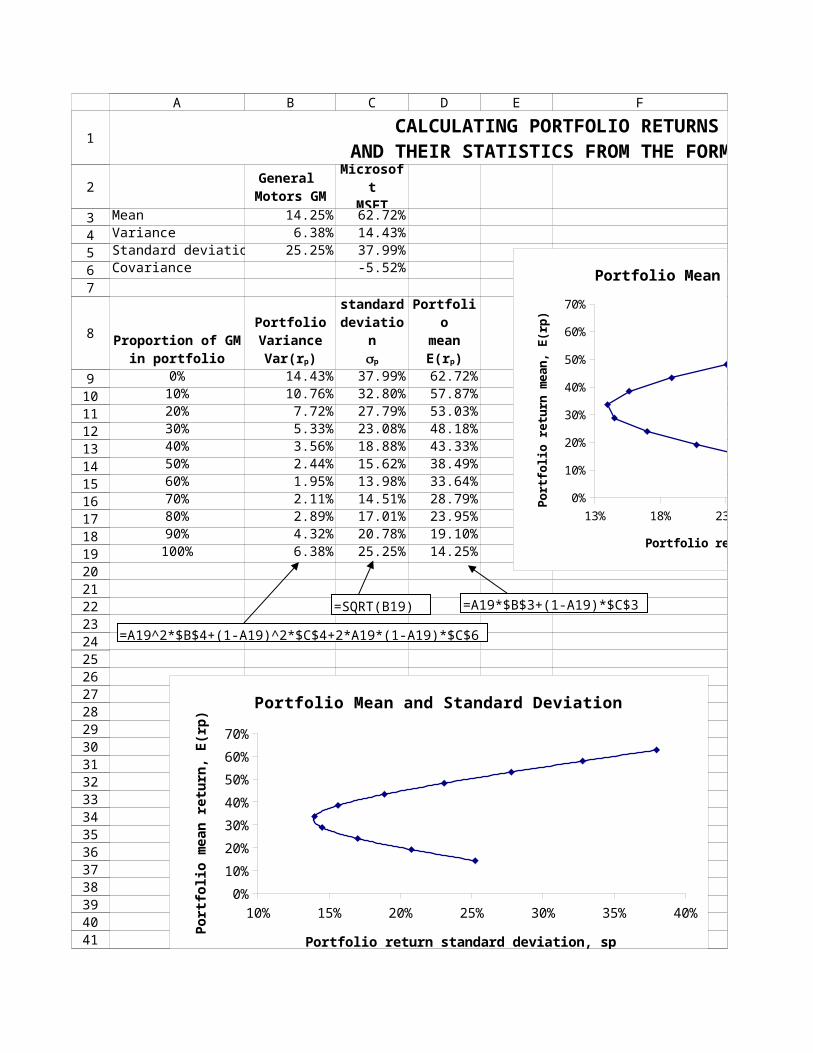

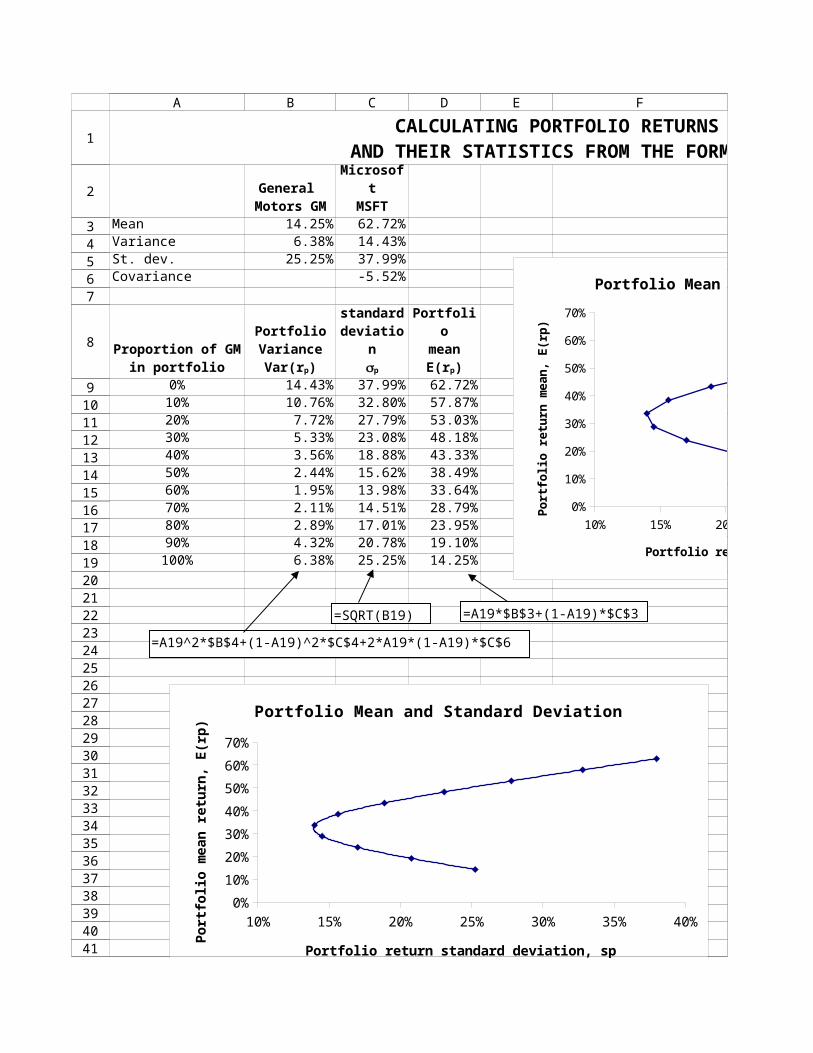

CALCULATING PORTFOLIO RETURNS AND THEIR STATISTICS

General Motors

GMMicrosoft

MSFTPortfolioreturn

Portfolio mean, E(rp)

Portfolio variance, Var(rp)

Portfolio st. dev., sp

A B C D E F

1

234

5

6789

1011121314151617181920212223

24

25

26

Mean 14.25% 62.72%Variance 6.38% 14.43%Standard deviation 25.25% 37.99%Covariance -5.52%

0% 14.43% 37.99% 62.72%10% 10.76% 32.80% 57.87%20% 7.72% 27.79% 53.03%30% 5.33% 23.08% 48.18%40% 3.56% 18.88% 43.33%50% 2.44% 15.62% 38.49%60% 1.95% 13.98% 33.64%70% 2.11% 14.51% 28.79%80% 2.89% 17.01% 23.95%90% 4.32% 20.78% 19.10%

100% 6.38% 25.25% 14.25%

CALCULATING PORTFOLIO RETURNS AND THEIR STATISTICS FROM THE FORMULAS

General Motors GM

MicrosoftMSFT

Proportion of GMin portfolio

PortfolioVariance

Var(rp)

Portfoliostandarddeviation

sp

PortfoliomeanE(rp)

10% 15% 20% 25% 30% 35% 40%0%

10%

20%

30%

40%

50%

60%

70%

Portfolio Mean and Standard Deviation

Portfolio return standard deviation, sp

Po

rtfo

lio

me

an

re

turn

, E

(rp

)

=A19*$B$3+(1-A19)*$C$3

=A19^2*$B$4+(1-A19)^2*$C$4+2*A19*(1-A19)*$C$6

=SQRT(B19)

13% 18% 23% 28% 33% 38% 43%0%

10%

20%

30%

40%

50%

60%

70%

Portfolio Mean and Standard Deviation

Portfolio return standard deviation, sp

Po

rtfo

lio r

etu

rn m

ea

n, E

(rp

)

A B C D E F

1

2

34567

8

91011121314151617181920212223242526272829303132333435363738394041

10% 15% 20% 25% 30% 35% 40%0%

10%

20%

30%

40%

50%

60%

70%

Portfolio Mean and Standard Deviation

Portfolio return standard deviation, sp

Po

rtfo

lio

me

an

re

turn

, E

(rp

)

A B C D E F4243

CALCULATING PORTFOLIO RETURNS AND THEIR STATISTICS FROM THE FORMULAS

13% 18% 23% 28% 33% 38% 43%0%

10%

20%

30%

40%

50%

60%

70%

Portfolio Mean and Standard Deviation

Portfolio return standard deviation, sp

Po

rtfo

lio r

etu

rn m

ea

n, E

(rp

)

G H I J

1

2

34567

8

91011121314151617181920212223242526272829303132333435363738394041

Mean 14.25% 62.72%Variance 6.38% 14.43%St. dev. 25.25% 37.99%Covariance -5.52%

0% 14.43% 37.99% 62.72%10% 10.76% 32.80% 57.87%20% 7.72% 27.79% 53.03%30% 5.33% 23.08% 48.18%40% 3.56% 18.88% 43.33%50% 2.44% 15.62% 38.49%60% 1.95% 13.98% 33.64%70% 2.11% 14.51% 28.79%80% 2.89% 17.01% 23.95%90% 4.32% 20.78% 19.10%

100% 6.38% 25.25% 14.25%

CALCULATING PORTFOLIO RETURNS AND THEIR STATISTICS FROM THE FORMULAS

General Motors GM

MicrosoftMSFT

Proportion of GMin portfolio

PortfolioVariance

Var(rp)

Portfoliostandarddeviation

sp

PortfoliomeanE(rp)

10% 15% 20% 25% 30% 35% 40%0%

10%

20%

30%

40%

50%

60%

70%

Portfolio Mean and Standard Deviation

Portfolio return standard deviation, sp

Po

rtfo

lio

me

an

re

turn

, E

(rp

)

=A19*$B$3+(1-A19)*$C$3

=A19^2*$B$4+(1-A19)^2*$C$4+2*A19*(1-A19)*$C$6

=SQRT(B19)

10% 15% 20% 25% 30% 35% 40%0%

10%

20%

30%

40%

50%

60%

70%

Portfolio Mean and Standard Deviation

Portfolio return standard deviation, sp

Po

rtfo

lio r

etu

rn m

ea

n, E

(rp

)

A B C D E F

1

2

34567

8

91011121314151617181920212223242526272829303132333435363738394041

10% 15% 20% 25% 30% 35% 40%0%

10%

20%

30%

40%

50%

60%

70%

Portfolio Mean and Standard Deviation

Portfolio return standard deviation, sp

Po

rtfo

lio

me

an

re

turn

, E

(rp

)

A B C D E F4243

CALCULATING PORTFOLIO RETURNS AND THEIR STATISTICS FROM THE FORMULAS

10% 15% 20% 25% 30% 35% 40%0%

10%

20%

30%

40%

50%

60%

70%

Portfolio Mean and Standard Deviation

Portfolio return standard deviation, sp

Po

rtfo

lio r

etu

rn m

ea

n, E

(rp

)

G H I J

1

2

34567

8

91011121314151617181920212223242526272829303132333435363738394041

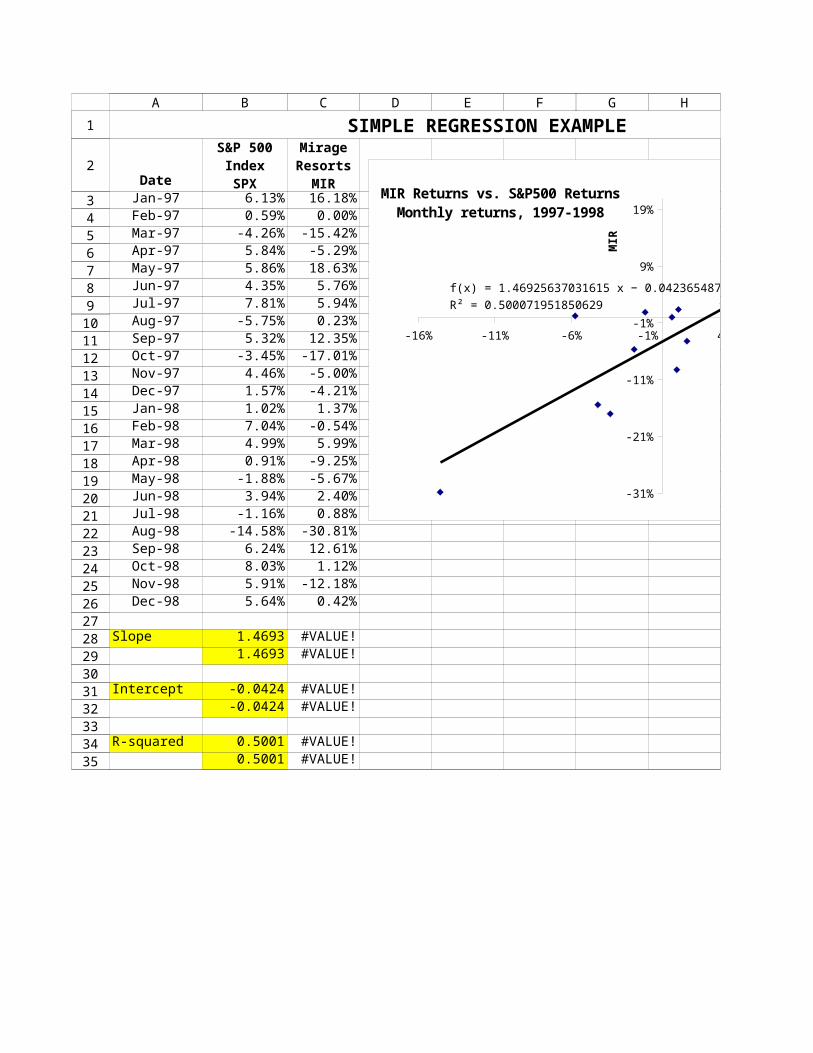

SIMPLE REGRESSION EXAMPLE

DateJan-97 6.13% 16.18%Feb-97 0.59% 0.00%Mar-97 -4.26% -15.42%Apr-97 5.84% -5.29%May-97 5.86% 18.63%Jun-97 4.35% 5.76%Jul-97 7.81% 5.94%Aug-97 -5.75% 0.23%Sep-97 5.32% 12.35%Oct-97 -3.45% -17.01%Nov-97 4.46% -5.00%Dec-97 1.57% -4.21%Jan-98 1.02% 1.37%Feb-98 7.04% -0.54%Mar-98 4.99% 5.99%Apr-98 0.91% -9.25%May-98 -1.88% -5.67%Jun-98 3.94% 2.40%Jul-98 -1.16% 0.88%Aug-98 -14.58% -30.81%Sep-98 6.24% 12.61%Oct-98 8.03% 1.12%Nov-98 5.91% -12.18%Dec-98 5.64% 0.42%

Slope 1.4693 #VALUE!1.4693 #VALUE!

Intercept -0.0424 #VALUE!-0.0424 #VALUE!

R-squared 0.5001 #VALUE!0.5001 #VALUE!

S&P 500IndexSPX

MirageResorts

MIR

-16% -11% -6% -1% 4% 9%

-31%

-21%

-11%

-1%

9%

19%

MIR Returns vs. S&P500 ReturnsMonthly returns, 1997-1998

S&P500

MIR

A B C D E F G H I

1

2

3456789

1011121314151617181920212223242526272829303132333435

SIMPLE REGRESSION EXAMPLE

-16% -11% -6% -1% 4% 9%

-31%

-21%

-11%

-1%

9%

19%

MIR Returns vs. S&P500 ReturnsMonthly returns, 1997-1998

S&P500

MIR

J

1

2

3456789

1011121314151617181920212223242526272829303132333435

SIMPLE REGRESSION EXAMPLE

DateJan-97 6.13% 16.18%Feb-97 0.59% 0.00%Mar-97 -4.26% -15.42%Apr-97 5.84% -5.29%May-97 5.86% 18.63%Jun-97 4.35% 5.76%Jul-97 7.81% 5.94%Aug-97 -5.75% 0.23%Sep-97 5.32% 12.35%Oct-97 -3.45% -17.01%Nov-97 4.46% -5.00%Dec-97 1.57% -4.21%Jan-98 1.02% 1.37%Feb-98 7.04% -0.54%Mar-98 4.99% 5.99%Apr-98 0.91% -9.25%May-98 -1.88% -5.67%Jun-98 3.94% 2.40%Jul-98 -1.16% 0.88%Aug-98 -14.58% -30.81%Sep-98 6.24% 12.61%Oct-98 8.03% 1.12%Nov-98 5.91% -12.18%Dec-98 5.64% 0.42%

Slope 1.4693 #VALUE!1.4693 #VALUE!

Intercept -0.0424 #VALUE!-0.0424 #VALUE!

R-squared 0.5001 #VALUE!0.5001 #VALUE!

S&P 500IndexSPX

MirageResorts

MIR

-16% -11% -6% -1% 4% 9%

-31%

-21%

-11%

-1%

9%

19%

f(x) = 1.46925637031615 x − 0.0423654876484542R² = 0.50007195185063

MIR Returns vs. S&P500 ReturnsMonthly returns, 1997-1998

S&P500

MIR

A B C D E F G H I

1

2

3456789

1011121314151617181920212223242526272829303132333435

SIMPLE REGRESSION EXAMPLE

-16% -11% -6% -1% 4% 9%

-31%

-21%

-11%

-1%

9%

19%

f(x) = 1.46925637031615 x − 0.0423654876484542R² = 0.50007195185063

MIR Returns vs. S&P500 ReturnsMonthly returns, 1997-1998

S&P500

MIR

J

1

2

3456789

1011121314151617181920212223242526272829303132333435

Dec-90 -11.54% 72.99% 2.46% 34.92%Dec-91 -11.35% 121.76% 14.54% 62.97%Dec-92 16.54% 15.11% 16.89% 15.93%Dec-93 72.64% -5.56% -15.95% 6.96%Dec-94 -21.78% 51.63% 6.55% 23.42%Dec-95 28.13% 43.56% 39.81% 39.35%Dec-96 8.46% 88.32% 11.56% 49.32%Dec-97 19.00% 56.43% 45.89% 45.78%Dec-98 21.09% 114.60% 14.11% 65.75%Dec-99 21.34% 68.36% -27.44% 30.22%

Average 14.25% 62.72% 10.84% #VALUE! Average 37.46%Variance 0.0638 0.1443 0.0440 #VALUE! Variance 0.0331Sigma 25.25% 37.99% 20.98% #VALUE! Sigma 18.21%

Covariances Alternative calculation of portfolio statistics

-0.0552 #VALUE! Average 37.46%

-0.0096 #VALUE! Variance 0.0331

0.0092 #VALUE! Sigma 18.21%

PORTFOLIO RETURNS FOR A THREE-STOCK PORTFOLIO

Yearending

GeneralMotors

GMMicrosoft

MSFTHeinzHNZ

Portfolioreturn

Cov(rGM,rMSFT)

Cov(rGM,rHNZ)

Cov(rMSFT,rHNZ)

A B C D E F G

1

2

3456789

101112131415161718

19

20

21

#VALUE!#VALUE!

#VALUE!#VALUE!#VALUE!

Alternative calculation of portfolio statistics

#VALUE!

#VALUE!

<-- =0.2^2*B15+0.5^2*C15+0.3^2*D15+2*0.2*0.5*B19+2*0.2*0.3*B20+2*0.5*0.3*B21

H

1

2

3456789

101112131415161718

19

20

21

WHY VARP INSTEAD OF VAR?

DateJan-97 6.13% 16.18%Feb-97 0.59% 0.00%Mar-97 -4.26% -15.42%Apr-97 5.84% -5.29%May-97 5.86% 18.63%Jun-97 4.35% 5.76%Jul-97 7.81% 5.94%Aug-97 -5.75% 0.23%Sep-97 5.32% 12.35%Oct-97 -3.45% -17.01%Nov-97 4.46% -5.00%Dec-97 1.57% -4.21%Jan-98 1.02% 1.37%Feb-98 7.04% -0.54%Mar-98 4.99% 5.99%Apr-98 0.91% -9.25%May-98 -1.88% -5.67%Jun-98 3.94% 2.40%Jul-98 -1.16% 0.88%Aug-98 -14.58% -30.81%Sep-98 6.24% 12.61%Oct-98 8.03% 1.12%Nov-98 5.91% -12.18%Dec-98 5.64% 0.42%

1.4693 #VALUE!1.4693 #VALUE!

1.4693 #VALUE!1.4080 #VALUE!

1.0000 #VALUE!1.0000 #VALUE!0.9583 #VALUE!

S&P 500IndexSPX

MirageResorts

MIR

Mirage b usingVarP

Mirage b usingVar

Market b usingVar

The S&P index represents the market returns

The beta of the market should = 1. But using Covar(rM,rMirage)/Var(rM) produces a beta < 1.

A B C D

1

2

3456789

101112131415161718192021222324252627

28

2930

31

3233

34

3536373839

The beta of the market should = 1. But using Covar(rM,rMirage)/Var(rM) produces a beta < 1.

A B C D4041

The S&P index represents the market returnsB2:

The beta of the market should = 1. But using Covar(rM,rMirage)/Var(rM) produces a beta < 1.B36: