performance evaluation and 'good governance' in...

TRANSCRIPT

Performance Evaluation and "Good Governance" in Asia

[DRAFT]

*Koike, Osamu - Yokohama National University, Japan, [email protected] Kabashima, Hiromi - Yokohama National University, Japan, [email protected]

Paper presented at the Annual Meeting of the International Political Science Association in

Santiago, Chile, July 16th, 2008

This is a draft. Please do not quote without author’s permission.

ABSTRACT

Performance evaluation is key to “result-based management” for better efficient and

effective use of pubic money. There is an assumption that we can evaluate productivity of

public organizations by introducing appropriate measures like cost-benefit analyses,

Management by Objectives, program assessment rating tool, and so on. Political leaders

expect that performance evaluation can contribute to the enhancement or restoration of

public trust in government, transparency and can discipline public officials for seeking better

efficiency. However, there is considerable question as to the means used by public

managers for a correct evaluation of performance. Only a short-term quantitative approach

of performance evaluation should reduce a “whole-government” perspective among public

managers. Contrary to the political will, customers require more quality in public service so

as to cope with diverse social problems. In the process, human factors such as “hospitality”

and “kindness” in public service delivery are indispensable. However, they are essentially

qualitative and difficult to measure through any economic criterion. The question then is how

can we evaluate personal elements in “result-based management”? In this paper, we will

analyze various performance evaluation systems in selected Asian countries and discuss

underlying concerns and challenges in the promotion of “result-based management.”

INSTITUTIONALIZING PERFORMANCE EVALUATION IN ASIA

Performance evaluation is a tool to measure individual or organizational effort in the

achievement of public goals. It comprises of a series of actions for individuals and

organizations to improve their performance by checking their policy outputs and outcomes

internally as well as externally. Thus, evaluation of performance is recognized as a

necessary process for Results-based Management in public organizations. Since the late

1990s, performance evaluation has become popular among Asian countries. After the 1997

Asian financial crisis, political leaders welcomed “new public management” measures to

strengthen government for coping with globalized economy. Reform measures include

privatization, “agencification,” decentralization, civil service reform, and performance

management. However, as Mark Turner pointed out, enthusiasm for reforming government

is diverse among Asian countries (Turner 2002). He identified three different types of

“diners” in Asia. The first is a group of "enthusiastic diners” who have experimented with

many items off the NPM menu, consisting of countries such as Singapore and Malaysia.

The second is the “cautious diners” wary of unfamiliar dishes with countries like Philippines,

Thailand, and Indonesia. Finally, there is a group of “unfamiliar diners” who have little

knowledge of NPM like Laos and Cambodia who lack certain fundamental prerequisite

conditions to build many NPM reforms (Turner 2002).

On performance management, however, all diners taste it as shown in Table 1. In 1999,

Malaysia introduced the Integrated Results-Based Management following the

implementation of the Modified Budgeting System since 1990. Indonesia launched the

Government Agency Performance Accountability System (SAKIP) in 1999 modeled after the

Government Performance and Accountability Act of the United States. Other Asian countries,

including less developed such as Mongolia and Cambodia, have introduced similar kind of

performance management frameworks in early years of the new century. It suggests a

phenomenon of “institutional isomorphism” (DiMaggio and Powell 1983) emanating in Asian

countries after the economic crisis. However, as many scholars have already affirmed,

convergence in the mode of NPM would be an oversimplification in Asia. For the discussion,

an application of “push-pull” framework will be productive. On the “push” side, international

funding agencies such as World Bank and IMF have urged recipient countries to transform

their old public administration into more efficient ones friendly with market economy. In the

eyes of the reformists, evaluation of government performance must be a gateway for public

sector reform. In the end, development assistance has led to a coercive isomorphism on

performance management among Asian developing countries. On the “pull” side, however,

Asian political leaders have room to choose reform items from the reform menu (Turner

2002). They can choose safer items as long as the donors admit their effectiveness in

administrative reforms. As a result, only selected reform measures have been introduced as

a flagship for administrative reform in many countries.

TABLE 1 Performance Management in Asian Countries

Country Program Key Features Year

Indonesia Government Agency Performance

Accountability System (SAKIP)

Five Year Performance Plan, Annual

Performance Agreement

1999~

Japan

Policy Evaluation System Project evaluation, performance

evaluation, comprehensive evaluation

2001~

Malaysia Integrated Results-Based Management Integrating Results-Based Budgeting

system and Personnel Performance

system

1999~

Mongolia Performance Management System Three-year Strategic Business Plans,

Medium–Term Expenditure Framework

2003~

Philippines Performance Management System -

Office Performance Evaluation System

Introduction of “Point System”;

Medium–Term Expenditure Framework

2007~

Singapore

Performance-informed Budgeting

System

“Ministry Report Cards”; Focus on Outcome

2006~

South

Korea

Performance-based Budgeting Self-Assessment of the Budgetary

Program

1999~

Thailand

Results-Based Management key performance indicators; balanced

scorecard

2003~

As Anthony Cheung describes, many Asian countries retain the features of “strong

bureaucracy.” (Cheung 2005). In this rule, there is less chance to blame bureaucracy on its

“budget-maximization” behavior. It means that the backgrounds for administrative reform in

Asia are fundamentally different from those of western democracies. Most of the south-east

Asian countries are still in the process of industrialization. Political influence of labor union is

quite limited and they are interlocked with the bureaucratic authoritarian regimes. Under a

“strong state” tradition, Asian governments have established national development plans

and have mobilized societal sectors for “national interests.” In the process, political leaders

emphasize traditional values rather than democratic norms originated in the western society.

These “soft” states lack rational legal administration (Myrdal 1968). It is difficult for people to

recognize the positive role of state in providing welfare to the poor. Except in some

industrialized nations like Japan and South Korea, the middle class has not developed and

“civil society” is weak. These conditions continue to allow Asian political leaders to be

selective in applying NPM measures and performance management in their developmental

programs. It is paradoxical that authoritarian governments are eager for public management

reform. However, it would be better tactics for political leaders who face changing

governance after the financial crisis. Bidhya Bowornwathana assumes that in Thailand NPM

reform measures are preferred to governance reform. The objective of NPM is primarily to

improve efficiency of the public sector, while “good governance” contains broader reform

strategies (Bidhya 2000). In other words, “a customer-oriented government does not

threaten the power base of government agencies” (ibid:401).

Besides the above reason, we should remember that there is a traditional concern of

“management” among Asian political leaders. As mentioned above, national development

planning has been used for economic and social development strategies in many Asian

countries. In Japan, for instance, government enacted the National Land Comprehensive

Development Act in 1950. The law aims “to use the land for multiple purposes, to develop

land, to rationalize the location of industry, and to contribute to the improvement of social

welfare” (Koike 1998). For the efficient use of public resources, Japanese government

established the Administrative Management Agency in the Prime Minister’s Office in 1948 to

inspect performance of central ministries and agencies. It is in the 1980s that the managerial

reform became popular in the Southeast Asian countries. Then, the Total Quality

Management (TQM) approach was preferred to NPM measures, followed by the

“Customer’s Charter” in the 1990s. Political leaders assumed that the management reform

would not only contribute to high performance in achievement of national development plan,

but also to increase public trust in government if it improves attitude of public employees at

the same time.

ASSESSING PERFORMANCE EVALUATION IN ASIA

In an authoritarian regime, it seems relatively easy to institutionalize performance evaluation

in the government machinery. A question is how much does it contribute to the improvement

of public service delivery. In December 2005, the OECD-Asia Public Sector Performance

Symposium was held in Seoul, South Korea. It was a first Asian meeting to discuss

strategies, tools, and techniques of government performance. In the Symposium,

representatives from Cambodia, China, Indonesia, Japan, Malaysia, Philippines, South

Korea, Thailand, and Vietnam presented papers on performance management in their

countries. After the 2005 symposium, the authors have been working to up-date the

development of performance evaluation in Asia. Followings are the findings of our surveys in

2006-2008.

Indonesia: Government Agency Performance Accountability System (SAKIP) In Indonesia, a working group in the Financial and Development Supervisory Agency

(BPKP) initiated a study on performance management in 1996. According to Sobirun

Ruswadi, this initiative has been inspired by the Government Performance and Result Act

(GPRA) of 1993 of the United States (Sobirun 2005). The working group developed and

introduced a public sector performance management model named Government Agency

Performance Accountability System (SAKIP). The development of this system then was

more driven due to the monetary and economic crisis, implementation of regional autonomy,

and change of regime in the late 1990s. In 1999, the government issued the President

Instruction No.7/1999 on Government Agency Performance Accountability, in accordance

with Act No.28/999 on Good Governance of the State.

SAKIP comprises of strategic plan, performance measurement, performance reporting, and

performance evaluation. Strategic Plan is defined as a five-year time period agencies’ or

institutions’ performance plan which states vision, mission, five-year strategic goals, annual

strategic objectives, and programs. Strategic Plan then is followed by an Annual

Performance Plan. Performance measurement is done by comparing performance indicator

achievements with the targets planned, and with prior years’ achievements. Performance

achievement is reported annually in the Government Performance Accountability Report.

Table 2 shows the annual increase of performance reports submitted to the President.

Table 2 Development of Government Agency Performance Framework in Indonesia

2001 2002 2003 2004 2005

Ministry/Central Agency 37 59 62 64 68

Province 10 23 30 27 29

County/Municipal 82 273 342 291 356

TOTAL 129 319 434 382 453

Source: Sobirun Ruswadi, “The Development of Government Agency Performance Accountability System

in Indonesia,” a paper presented at the OECD-ASIAN Countries Performance Management Symposium,

Seoul, 8 December 2005; Up-dated information is provided by the Ministry of Administrative Reform.

From budget year 2005, “Annual Performance Agreement” is required between a

government official, a subordinate, and his or her superior. Along with a one page statement

of Performance Agreement, a summary of Annual Performance Plan which reveals the main

program that must be accomplished by the signing official, and strategic objectives that were

expected to be attained, and performance indicators (outputs and or outcomes), and the

budget of each program has to be attached. At the same time, the government intends to

integrate performance accountability system with budgeting system, so the state budget

becomes a performance based budget.

According to the Ministry of Administrative Reform, however, there have been significant

obstacles to the development and implementation of SAKIP (Sobirun 2005). Firstly, annual

evaluation by BPKP on Government Performance Accountability Report revealed that

commitment of the government officials to implement LAKIP was a key factor in effort of

improving both agencies’ management process and performance. Secondly, it has been a

long traditional paradigm that public servant are there to serve the government rather than

the public, and are in position of patronage rather than professionalism. Thirdly,

performance indicator is considered a key factor in performance measurement, but the

question on how to determine right performance indicators remains difficult. And fourthly,

there are still variations in the definition of performance. While some limit the meaning of

performance as output, others interpret performance as an accomplishment of the process.

SAKIP itself defines performance as “results in terms of output and or outcomes.” (Sobirun

2005). In spite of the effort taken by the Ministry of Administrative Reform, these obstacles

remain unsolved, while the use of SAKIP expanding.

.

Japan: Policy Evaluation System

Contrary to her high economic performance and stable democracy, performance

management in the Japanese public sector remains in a rudimentary stage. It is in January

2001 that the Government of Japan introduced a government-wide policy evaluation system.

It is no doubt that the political leaders of those days were caught in a fever of the New Public

Management same as in other Asian countries (Hori 2003). The Government Policy

Evaluation Bill was submitted by the Cabinet to the Diet in January 2001, enacted on June

22 and came into effect in April 2002. The newly created Ministry of Internal Affairs and

Communications (MIC) was assigned responsibility for implementing policy evaluation.

Three years later, MIC published the first Review Report on the implementation of GPEA.

The Report pointed out progress and problems that took place in three years since the

enactment of GPEA. Survey data in the report revealed that some ministries had used policy

evaluation for their result-based management and the rest had not. It is interesting to point

out that there was a spread of “evaluation fatigue” in ministries. Each year, each ministry

had to prepare a large quantity of evaluation reports for the central management agencies,

but most of the efforts were not compensated; just resulted in increased jobs!.

Japan’s policy evaluation is a decentralized structure where individual ministries plan and

implement evaluation. The roles of MIC are to conduct unified or comprehensive evaluation

of the policy of each ministry, or conduct evaluation to ensure the objective and strict

implementation of policy evaluation. In addition, MIC summarizes and publishes the results

of evaluation in the government and how these results are reflected in policy and other

administrative affairs including the holding of a meeting of a "liaison conference for policy

evaluation organizations." GPEA defines three standard evaluation methods; 1) project

evaluation, 2) performance evaluation, 3) comprehensive evaluation. MIC provides a

guideline on performance evaluation for the evaluators. For instance, the guideline

recommends use of numerical targets in performance evaluation. According to the review,

the ratio of policies that contains some numerical target has increased from 34% in 2002, to

50% in 2003, 56% in 2004, and 55% in 2004.

On the other hand, the Ministry of Finance attempts to link policy evaluation with budget

formation. However, the progress of performance management in Japan is limited. There is

no substantial discussion on the Introduction of “performance agreement,” “balance

scorecard,” “performance-based budgeting,” and “performance audit” at national level.

Malaysia: Integrated Results-Based Management: IRBM According to Koshy Thomas, the Deputy Undersecretary of the Ministry of Finance,

Malaysian government first introduced the Results-Based Management system in 1990

under the Modified Budgeting System (Thomas 2007). The original performance framework,

however, created only limited linkages between budget performance, resource usage, and

policy implementation. Based on the recognition that there were fundamental missing links,

the government introduced the “Integrated RBM (IRBM) system in 1999. The IRBM system

includes an Integrated Performance Management Framework (IPMF) that attempts to

integrate the Results-Based Budgeting (RBB) system and the Personnel Performance

System (PPS). In this system ministries and departments analyze problems at various

stages of program implementation, including efficient resources utilization (inputs), activities

completion, outputs completion, and outcome/impact achievement. It aims to establish a

government-wide results-based management system in Malaysia.

The IRBM system consists of five key components - two primary and three complementary

or support components. The primary components are the Results-Based Budgeting System

(RBB) and the Results Based Personnel Performance System (PPS). Three support

components are the Results-Based Monitoring and Evaluation (M&E) System, the

Management Information System (MIS), and an Enabling E-Government (EG) System. The

RBB measures results achieved at almost every stage of the project from input application,

activity completion, outputs delivery, and impact achievement. Measured results will be

utilized for planning, implementing, monitoring and reporting on organizational performance,

with systematic links to personnel performance, and are important for resource allocation

decisions by the Central Budget Office. The IPMF is mandated as the strategic planning

framework under IRBM. Therefore, all ministries and departments are required to prepare

their strategic plan for resource allocation using IPMF as part of the RBB system. In sum,

Malaysian IRBM seeks not only vertical integration, but also horizontal integration at

program level. Malaysian government recognizes that human capital plays a pivotal role in

organizational and personnel performance (Thomas 2007).

Mongolia: Public Sector Management and Finance Law (2003) According to the Report of ADB (Asian Development Bank) Mongolia introduced the

Government Reform Plan (GRP) in 1999 with the support of international development

partners (ADB 2008). The GRP was to help improve financial management in the public

sector by introducing institutional mechanisms modeled after New Zealand reform. At the

initial stage, GRP was introduced on a pilot basis in selected government agencies. Early

evaluation found limited progress on several key aspects of the reform process such as

strategic planning, output-based budgeting, implementing a medium-term expenditure

framework. In January 2001 the Government declared to extend the reform program to all

government ministries, six provinces, and Ulaanbaatar City.

In 2003 the Government enacted Public Sector Management and Finance Law and

introduced the Medium Term Expenditure Framework (MTEF). In MTEF, portfolio ministries

and their dependent agencies prepare rolling three-year Strategic Business Plans. The

plans show main output targets and activities by program area for the coming three-year

period. To strengthen link between budget and policy objectives at the sector level, the

Ministry of Finance (MoF) has introduced new MTEF/budget procedures that promote a

more integrated planning and budgeting process. Under the new framework, MoF has

issued budget ceilings for all portfolio ministries, within which the latter have increased

delegated authority to identify their sector priorities. In addition, to reinforce policy dialogue

between each portfolio ministry and MoF, budget expenditures should be explicitly linked to

performance indicators.

Asian Development Bank (ADB) states that New Zealand’s model of public financial

management reforms is not necessarily suitable for other countries, as its successful

implementation demands a number of prerequisites (ADB 2008). Unfortunately for the GRP,

most of the preconditions were not in place in Mongolia at the time of the program loan’s

approval, and were not achieved during the course of the loan. The evaluation offers a

number of lessons regarding Mongolia’s legal framework for reform, the need to design and

sequence reforms properly, and the importance of taking a long term approach to

development (ADB 2008).

Philippines: Performance Management System - Office Performance Evaluation System (PMS-OPES) In 2007, the Civil Service Commission (CSC) of the government of Philippines initiated a

re-assessment of the existing Performance Evaluation System (PES) and introduced a new

Performance Management System - Office Performance Evaluation System (PMS-OPES).

CSC aimed to establish a high-performance culture in the Philippine government aligning

individual objectives to the organizational objectives under the PMS-OPES. 1 PMS-OPES is

a means of getting better results from the organization, teams and individuals by

understanding and managing performance within an agreed framework of planned goals,

standards and competence requirements.

The unique component of the PMS-OPES is the use of “points system” to measure the

collective performance of individuals within an operating unit. It simplifies the performance

evaluation/measurement process and also provides an objective and user-friendly

performance management system. The PMS-OPES is primarily concerned with outputs (the

achievement of results or quantified objectives). In PMS-OPES each output is assigned a

number of points based on the length of time it takes for one person to produce an output.

The conversion of 1 hour to 1 point is used in this method. CSC explains that this makes it

simpler to compare performances of different offices by just comparing the amount of points

each office produces. Each office creates a compilation of outputs called PMS-OPES 1 Information on the Performance Management System - Office Performance Evaluation System (PMS-OPES) of Philippines is obtained from the official website of the Philippine Civil Service Commission.

Output Reference Table that contains a consolidated list of outputs of an office given its

functions which also indicate the corresponding points that an office would earn for

completing an output. It also contains operational definitions that spell out the criteria or

standards the output must meet to earn points.

The performance management system process framework consists of the following phases:

1) Performance Planning and Commitment - done at the start of the performance period

where all staff agrees on their performance expectations and the office work plan. 2)

Performance Monitoring and Coaching - the phase where checking on the progress of

achieving objectives is conducted. It is also the time where management addresses factors

that either help or hinder effective work performance. Tracking tools or monitoring strategies

are usually employed during this phase. 3) Performance Review and Feedback - this phase

aims to measure employees' commitments in the performance contract. It is during this

period that progress and achievements are assessed so that action plans can be prepared

and agreed upon. 4) Performance Evaluation and Development Planning - in this process,

improvement needs are determined and action plans are developed to address them. This

is also the phase when the rater and the one who is being rated discuss opportunities for

career planning, reward and recognition.

In Philippines, the government attempts to link performance management with budget

through the Medium Term Expenditure Framework. According to the Australian Agency for

International Development (AusAID), the 2007 Budget marked the first instance that

accurate forward estimates for all 21 departments were available, used in the budget

formulation process through the Medium Term Expenditure Framework. The 2007 Budget

was the first to be informed by a budget strategy paper. The Organizational Performance

Indicator Framework was also rolled out to all government departments for the first time

(AusAID 2007).

Singapore: Performance-informed Budgeting System Singapore is famous for its extensive use of performance and results information in the

budget process. According to the OECD report, performance management in Singapore

focuses on further developing outcome indicators (Blöndal 2006). Singapore’s objective is

not to directly link funding with performance and results indicators, rather to inform resource

allocation decisions. In fact, the very use of budget ceilings (“block budgets”) is

acknowledged to explicitly weaken any such linkages from the perspective of the Ministry of

Finance. Performance and results information, according to the OECD report, does however

form an integral part of the budgetary dialogue between the Ministry of Finance and line

ministries. The philosophy is that line ministries should take ownership in the area of

performance and results in the same manner as they do for the allocation of their budget

ceilings (“block budgets”). It is recognized that the principal uses of performance and results

information is within line ministries.

There are three principal external “venues” for performance and results information. First is

the budget documentation itself. Each ministry’s desired outcomes are listed together with

key performance indicators. Interestingly, indicators used often include the standing of

Singapore in rankings against other countries in respective areas. Secondly, individual

government organizations often publish detailed annual reports where a greater number of

performance and results indicators are published and often accompanied by a narrative

discussion. Thirdly, a flagship initiative known as the “Ministry Report Cards” is currently

being developed. Each Ministry will complete them in a standardized structure and the

Ministry of Finance will provide commentary on them. This would include commentary on

how demanding their targets were and management of resources. They are then submitted

to the Cabinet for review (Blöndal 2006).

Singapore government moves towards a focus on outcomes. Singapore recognizes that

outcomes by themselves are not sufficient to drive further improvements. For instance,

according to the OECD Report, infant mortality is a principal outcome indicator for the

Ministry of Health. Although infant mortality in Singapore is second lowest in the world,

Health Ministry reviews the indicators frequently to ensure their relevance for driving further

improvement (Blöndal 2006). Key performance indicators have been developed for each

of the outcomes, and assigned to owner ministries. This is to be submitted to cabinet each

year together with the ministry report cards. In addition, a whole-of-government strategic

planning cycle is being put in place to align the government’s strategic planning with the

budget cycle (APEC 2007). The initiatives and projects undertaken to achieve an integrated

government cover three broad areas: Framework and architecture for integration;

cross-agency collaboration projects; and supporting structures, policies and information and

communications technology (ICT). It should be noted that performance and results

information does not determine salaries. Rather, performance bonuses are determined by

performance appraisals.

South Korea: Performance-based budgeting Performance-based budgeting was introduced in Korea in three phases. The first was an

experimental pilot “Performance Budgeting” during 2000-02. It is a performance-based

system based on the model of the US Government Performance and Results Act (GPRA)

with some modifications. Then divisions in 22 ministries and agencies participated in this

project to develop annual performance plans. Building on that experience, the second

initiative titled “Performance Management System of the Budgetary Program” was

introduced as one of the four major fiscal reforms in 2003. Twenty-two ministries and

agencies were selected to submit their annual performance plans to the Ministry of Planning

and Budget (MPB) along with their annual budget requests. This second initiative was also

inspired by GPRA. In 2005, Korean government introduced a third initiative, the

“Self-Assessment of the Budgetary Program” (SABP). This system was based on the

“Program Assessment Rating Tool” (PART) of the United States, with some modifications.

Under SABP, 555 programs (about one third of all government programs) were reviewed in

2005, a pace which would allow the MPB to review every major budgetary program over a

three-year cycle. Similarly to PART, the self-assessments were done according to a

checklist developed by the MPB that lists questions on planning, management and results.

From 2006, the performance system is expanded comprehensively, requiring performance

information to be developed for every program. Performance targets, which are included in

performance plans, are set by the ministries/agencies. Following an initial self-assessment

by ministries/agencies, the MPB makes final assessment of performance. The MPB uses

annual performance reports and SABP in its negotiations with line ministries during the

annual budget process. This practice has also encouraged ministries/agencies to use

performance information in formulating their budget requests. It suggests MPB’s strategic

use of performance assessments to ensure a positive feedback between performance

information and budget allocation. To link performance information to resource allocation,

the program ratings are used by the MPB to cut ineffective programs. The budget cut

announced by the MPB was 10%. On the other, spending ministries use performance

information to reshuffle budget allocations within ministries/agencies and to justify existing

appropriations. When disagreement between the MPB and ministries/agencies occurs, MPB

has the final authority in settling the difference. In this process, past performance

information is the most frequently used rationale for performance targets as comparable

benchmark references. To encourage ministries/agencies to improve performance the MPB

provides both incentives and penalties for individuals. Incentives include promotion based

on performance evaluations and the performance-related pay scheme. In case of poor

performance, agency/ministry may be penalized with a budget cut. There is no penalty on

an organizational level, nor are there explicit penalties or incentives that affect senior civil

servants directly, despite the fact that they are required to sign performance agreements.

However, senior civil servants are quite aware that organizational performance will probably

have an impact on their own career prospects.

Korean scholars observe that not much change has taken place regarding a reduction of

input control following the introduction of performance-based budgeting, because top-down

budgeting and performance management were introduced at the same time in Korea (Kim

and Park 2007). It results in ministries/agencies’ strategic use of performance management

to protect important programs. They tend to give lower ratings to less important programs

and better ratings to those that they consider important within their program portfolio.

Notwithstanding, it is also pointed out that Korean civil servants are coming to accept

result-oriented performance management as a normal part of bureaucratic culture.

Thailand: Results-Based Management In 2003, the Office of the Public Sector Development Commission (OPDC) of Thai

Government implemented the RBM approach to measure and drive performance of

ministries, departments and all 75 provincial administrations. In fiscal year 2004, all

government agencies were required by the Cabinet to join in the system of the performance

agreement and to use a series of key performance indicators (KPIs) for achieving target

goals. To measure performance, OPDC introduced the concept of “balanced scorecard.” It

attempts to measure effectiveness of strategic plan implementation, efficiency of public

sector work, quality of service delivery, and organization development.

An assessment report compiled by the World Bank concluded that, in general, Thailand is

successfully implementing an RBM system in its early stages (World Bank 2006). 2Virtually

all public agencies show some specific efforts and some results in terms of better quality of

service delivery and reduction in administrative cost, and the government has begun to

collect data on cross-cutting issues, such as efficiency and service delivery, and to lead the

effort to increase coordination through clustering to achieve integrated results. Some

examples of improved services include the establishment of call centers for registration and

insurance, streamlining of regulatory procedures, and local service centers for social,

employment, and other services. 2 This report was prepared in partnership between the Office of the Public Sector Development Commission (OPDC)

of Thai Government and the World Bank, under the general guidance of the Country Development Partnership:

Governance and Public Sector Reform (CDP-G) Steering Committee.

However, the report also states that Thailand’s implementation of RBM has also

encountered several challenges, including uneven integration with other management

systems; difficulties in measuring outcomes; the burden of extra work to maintain current

systems while introducing additional parallel processes; and resistance to change by those

who are tasked with implementing the RBM system. More specifically, the report found that

the key institutional issues were: (i) aligning performance reforms with other management

systems, including the budget process; (ii) striking the right balance between central

leadership and agency ownership of performance management systems; (iii) harmonizing

KPIs of the line ministries/departments with those of the provinces; (iv) cascading KPIs from

ministries to departments and provincial offices of departments; (v) generating synergies

through the clustering process at both national and provincial levels; and (vi) strengthening

the role of the CEO-Governor and the provincial team in the coordination of strategy and

operations at the provincial level.

The World Bank report concludes that Thailand has an even stronger central definition of

performance targets and assessment process than many of the nations at the forefront of

performance-based management (World Bank 2006). However, these countries have

developed more advanced systems for integrating performance information and measures

into management and budgeting systems, most notably through the articulation of

performance budgeting and performance auditing. These processes are viewed as essential

to improve decision-making and ensure the sustainability of performance reforms over the

longer-term.

GOOD GOVERNANCE AND PERFORMANCE MANAGEMENT

Above findings and reports suggest that there are both commonalities and differences in the

“performance” of performance evaluations in Asia. The first is a common interest in the

results-based management and adoption of the same management tools such as “key

results area” and “performance indicators.” Also, it is getting popular among political leaders

to establish “performance agreement” between the ministers and senior bureaucrats.

Secondly, performance-related pay scheme has been introduced in many countries mostly

at the senior executive services. Thirdly, linking performance evaluation with government

budget management is adopted in many Asian nations with an exception of Japan. Japan

attempts to link policy evaluation with budget formulation, but it is less successful due to

opposition of line ministries (Koike, Hori, and Kabashima 2007). Finally, it is interesting

that “bureaucracy bashing” is not a driving force for institutionalization of performance

evaluation in Asia, except Japan and South Korea. In bureaucratic states the legislature

seems less enthusiastic in measuring bureaucratic performance.

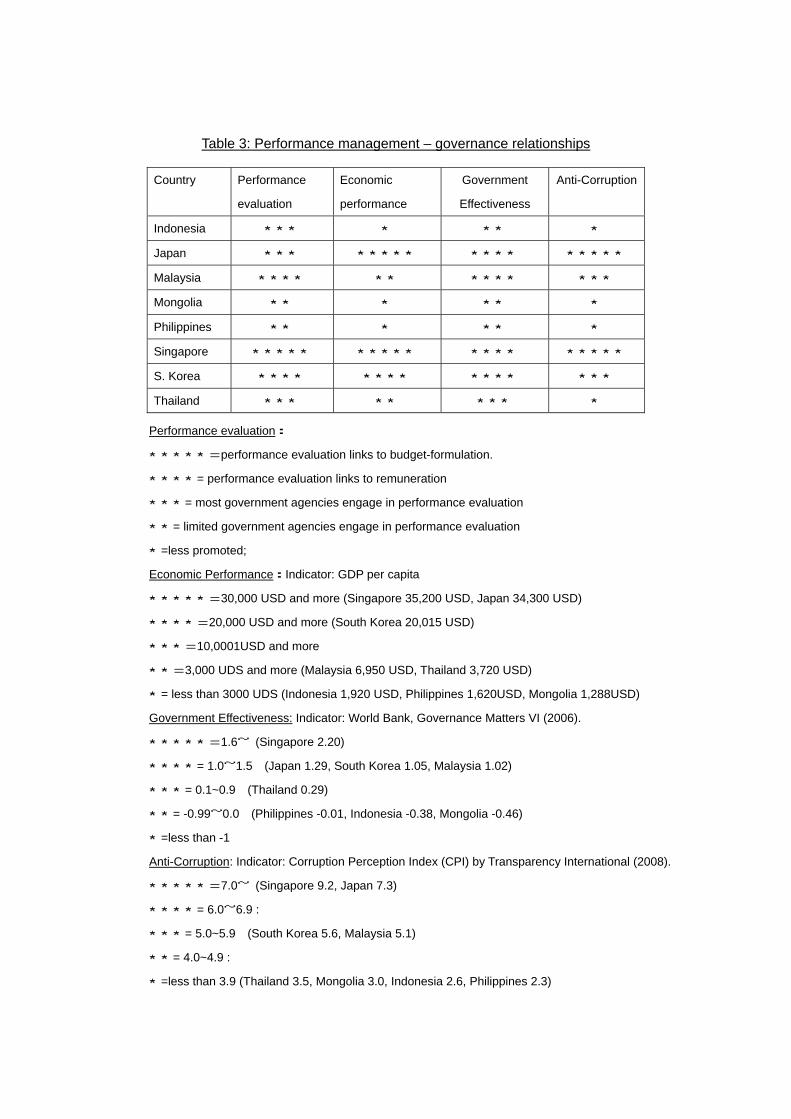

Table 3 indicates that the relation between performance management, government

effectiveness, and corruption in government is weak. In addition, it is difficult to find any link

between economic performance and corruption. Under the authoritarian regime there are

few obstacles for the introduction of performance evaluation across the government.

However, reliance on patronage weakens the merit principle and scientific management,

and it makes measurement subjective. Lack of democratic control makes political use of

performance evaluation possible to legitimatize existing regime. It is not an “iron cage” of

rationality, but a disguised rationality. Thus, the democratic background for performance

management is crucial for any country.

However, there is a pitfall in the “good governance” initiatives promoted by international

funding agencies. The donors tend to introduce their own governing model into the recipient

countries, regardless of their historical path: western countries have spent a hundred years

for establishing democratic regime. As Merilee S. Grindle argues, the “good governance”

agenda is unrealistically long and growing longer over time. It is realistic for the developing

countries to set a goal of “good enough governance” (Grindle 2004).

For the effective policy evaluation, role of civil society will be much important in Asian

countries. This is another challenge for “good enough governance” in Asia. In recent years,

reformist put more emphasis on outcome rather than input and output. Usually, the Ministry

of Finance uses performance evaluation report of line ministries for budget control. On the

other, the output-base management has been the role of the Audit Office. However, it is a

recent fashion for government to promote “results-based management” focusing more on

the evaluation of “outcome.” It requires the evaluator to study the “impact” of policy and

program on individuals and society. This warrants an important role for the civil society in

performance evaluation. However, in Asia, growth of civil society is stalled due to

authoritative governance, although the middle class is growing rapidly. Democratization is a

long and winding road for many Asian countries. But, it is necessary for the nation to make

government fair and workable. When the civil society grows up and becomes watchful of

democratization and performance management, then, performance evaluation will be a true

measure for establishment of good (enough) governance in Asia.

Table 3: Performance management – governance relationships

Country Performance

evaluation

Economic

performance

Government

Effectiveness

Anti-Corruption

Indonesia ★★★ ★ ★★ ★

Japan ★★★ ★★★★★ ★★★★ ★★★★★

Malaysia ★★★★ ★★ ★★★★ ★★★

Mongolia ★★ ★ ★★ ★

Philippines ★★ ★ ★★ ★

Singapore ★★★★★ ★★★★★ ★★★★ ★★★★★

S. Korea ★★★★ ★★★★ ★★★★ ★★★

Thailand ★★★ ★★ ★★★ ★

Performance evaluation:

★★★★★=performance evaluation links to budget-formulation.

★★★★= performance evaluation links to remuneration

★★★= most government agencies engage in performance evaluation

★★= limited government agencies engage in performance evaluation

★=less promoted;

Economic Performance:Indicator: GDP per capita

★★★★★=30,000 USD and more (Singapore 35,200 USD, Japan 34,300 USD)

★★★★=20,000 USD and more (South Korea 20,015 USD)

★★★=10,0001USD and more

★★=3,000 UDS and more (Malaysia 6,950 USD, Thailand 3,720 USD)

★= less than 3000 UDS (Indonesia 1,920 USD, Philippines 1,620USD, Mongolia 1,288USD)

Government Effectiveness: Indicator: World Bank, Governance Matters VI (2006).

★★★★★=1.6~ (Singapore 2.20)

★★★★= 1.0~1.5 (Japan 1.29, South Korea 1.05, Malaysia 1.02)

★★★= 0.1~0.9 (Thailand 0.29)

★★= -0.99~0.0 (Philippines -0.01, Indonesia -0.38, Mongolia -0.46)

★=less than -1

Anti-Corruption: Indicator: Corruption Perception Index (CPI) by Transparency International (2008).

★★★★★=7.0~ (Singapore 9.2, Japan 7.3)

★★★★= 6.0~6.9 :

★★★= 5.0~5.9 (South Korea 5.6, Malaysia 5.1)

★★= 4.0~4.9 :

★=less than 3.9 (Thailand 3.5, Mongolia 3.0, Indonesia 2.6, Philippines 2.3)

Asian governments have assumed a double mission to establish a rational-legal

bureaucracy and its modernization for the new international standard. The former is a

foundation for democratic governance (Schick 1998) and a prerequisite for the latter.

However, in challenging modernization like “Results-based Management,” Asian

government should recognize that there are questions and oppositions among the scholars

and practitioners. For instance, since the mid-1990s, the UK and other countries promote a

new vision of “a Whole of Government (WOG)” or “Joined-up Government (JOG).” They are

based on the recognition that public sector organizations are fragmented under the

“quasi-“market” structure inspired by New Public Management. Executives and public

managers become biased in seeking efficiency in a short-term under the new accountability

framework of performance agreement. As a result, it decreases the capability of government

for coping with “wicked” problems such as juvenile crime and social exclusion through

possible horizontal cooperation among organizations. It remains a riddle for government as

how to reconcile a competitive, market-type governing model with a holistic, participatory

governing model under the premise of “modernizing government.”

CONCLUSION

Since the 1980s, Asian nations have experienced a rapid economic growth. There are

“mega” shopping malls in major cities where a growing middle class enjoys consumption.

Asian governments assuming a mantle of performance management look increasingly like

modernized western bureaucracies. However, as illustrated in a variety of governance

indicators, it is hard to say that Asian governments are clean, efficient, and workable. In

democratic nations, corrupt, inefficient and unworkable governments will lose legitimacy in

governance and confidence among the citizens. Paradoxically in Asia, trust on government

has been quite high, mainly because the authoritarian governments have restrained growth

of democracy. However, as evidenced by the riots in Thailand, a growing middle class

increasingly question the government. It urges Asian “strong states” to transform their old

public administration to the more efficient, workable, and reliable. There is no doubt that

some new management tools like performance evaluation and accountability framework will

contribute to the establishment of a “good bureaucracy.” However, it must be recognized

that they must have a democratic background for public management. Building a rational

legal bureaucracy is a prerequisite for efficient government. The growth of civil society is

necessary for checking performance of public sector organization. It must be a challenge for

an authoritarian government to promote decentralization for development of participatory

governance. But, it is a good opportunity for the nation to develop a new governing model

based on cultural heritage.

Asian society puts high value on human relations, for instance. Importance of human

relations is embedded in the organizational behavior that has been acclaimed as the

“human-side of enterprises” (McGregor 1960) or “Theory Z” (Ouchi 1981). Total Quality

Management (TQM) is the best suited in Asian organizations, for it puts high value on

participation and cooperation of employees. From this standpoint, it is evident that

performance management, strategic planning, and decentralized management require a

cultural change in the bureaucracy. Human relations are crucial for horizontal cooperation

among organizations. Human factors such as “hospitality” and “kindness” are indispensable

for public organizations entrusted by the citizens. These values are already embedded in

Asian organizations in a various ways and there is no need to imitate the Western style.

Asian governments should seek Asian models of public management based on their cultural

background which is a true challenge.

Reference

ADB (Asian Development Bank) 2008. Mongolia: Governance Reform Program (First

Phase), September 2008.

<http://www.adb.org/Documents/PPERs/MON/31597-MON-PPER.pdf> (May 2009)

APEC (Asia Pacific Economic Cooperation), 2007 APEC Economic Policy Report.

Economic Committee, Asia Pacific Cooperation.

AusAID (Australian Agency for International Development) 2007. The Philippines: Annual

Program Performance Update 2006–07.

<www.ausaid.gov.au/publications/pdf/phil_appr_2007.pdf > (May 2009).

Batjargal. 2008. “Strengthening the MTEF Process in Mongolia.” IMF Public Financial

Management Blog. June 25, 2008.

<http://blog-pfm.imf.org/pfmblog/2008/06/index.html> (May 2009)

Bidhya, Bowornwathana. 2000. “Governance Reform in Thailand: Questionable

Assumptions, Uncertain Outcomes.” Governance: An International Journal of Policy,

Administration, and Institutions 13 (3): 393-408.

Blöndal, Jón R. 2006. “Budgeting in Singapore.” OECD Journal on Budgeting 6(1):44-86.

Cheung, Anthony B. 2005. “The Politics of Administrative Reforms in Asia: Paradigms and

Legacies, Path and Diversities.” Governance: An International Journal of Policy,

Administration, and Institutions 18 (2): 257-282.

DiMaggio, Paul and Walter W. Powell. 1983. “The Iron Cage Revisited: Institutional

Isomorphism and Collective Rationality in Organizational Field.” American Sociological

Review 48:147-160.

Grindle, Merilee S. 2004. “Good Enough Governance: Poverty Reductions and Reform in

Developing Countries.” Governance: An International Journal of Policy, Administration,

and Institutions 17 (4): 525-548.

Hori, Masaharu. 2003. “Japanese Public Administration and Its Adaptation on New Pubic

Management.” Ristumeikan Law Review International Edition 20.

Kim, John M. and Nowook Park. 2007. “Performance Budgeting in Korea.” OECD Journal

on Budgeting 7(4):1-11.

Koike, Osamu. 1998. “Local Government and National Development: Evolution of Local

Autonomy in Postwar Japan.” In Akira Nakamura ed. Local Governance and National

Development. Tokyo: EROPA Local Government Center.

Koike, Osamu, Masaharu Hori, and Hiromi Kabashima. 2007. “The Japanese Government

Reform of 2000 and the Self-Evaluation System: Efforts. Results and Limitations,”

Ristumeikan Law Review International Edition 24: 1-11.

McGregor, Douglas. 1960. The Human Side of Enterprise. New York: McGraw-Hill.

Myrdal, Gunner. 1968. Asian Drama: An Inquiry into the Poverty of the Nations. New York:

Pantheon.

Ouchi, William. 1981. Theory Z: How American Business Can Meet the Japanese Challenge.

Reading, Mass: Addison-Wesley.

Schick, Allen. 1998. “Why Most Developing Countries Should Not Try New Zealand

Reforms.” The World Bank Observer 13:123-131.

Sobirun, Ruswadi. 2005. “The Development of Government Agency Performance

Accountability System in Indonesia,” a paper presented at the OECD-ASIAN Countries

Performance Management Symposium. Seoul, December 8, 2005

Thomas, Koshy. 2007. “Malaysia: Integrated Results-Based Management – the Malaysia

Experience. Sourcebook on Emerging Good Practice, Second Edition, pp.95-103.

<http://www.mfdr.org/sourcebook/2ndEdition/4-2MalaysianRBM.pdf> (May 2009)

Turner, Mark. 2002. “Choosing Items from the Menu: New Public Management in Southeast

Asia.” International Journal of Public Administration 25(12): 1493-1512.

World Bank.2006. THAILAND: Country Development Partnership: Governance and Public

Sector Reform. Program Assessment and Implementation Completion Report, World

Bank. December 2006.

<http://www.siteresources.worldbank.org/INTTHAILAND/Resources/CDP-G/CDPG_Fin

al_Report_012307.pdf> (May 2009).