penwithick modelling tools comparison v2 - home … and full sap were compared across the range of...

TRANSCRIPT

Penwithick Green Deal Pilot project: Comparison of various energy modelling tools Prepared for: The BRE Trust November 2012

Report number: 283 724

1 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Prepared by

Name Caroline Weeks

Position Senior Consultant

Signature

Reviewed by

Name Colin King

Position Associate Director, Wales

Date 30th November 2012

Signature

BRE Wales & SW Ethos Kings Road Swansea Waterfront SA1 8AS T + 44 (0) 1792 630100 F + 44 (0) 1792 630101 E [email protected] www.bre.co.uk

This report is made on behalf of BRE. By receiving the report and acting on it, the client - or any third party relying on it - accepts that no individual is personally liable in contract, tort or breach of statutory duty (including negligence).

2 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Executive Summary

Cornwall Council, with their delivery partner Ocean Services, are undertaking a Green Deal retrofit pilot project in the village of Penwithick, near St Austell. BRE are acting as Technical Advisors to the project team to help achieve their objectives. During the first phase of the pilot, initial modelling was carried out by BRE using full SAP (the Government’s Standard Assessment Procedure for dwellings) on all potential measures for the dwelling types in Penwithick to prioritise which were most cost effective. The most common measures, such as loft insulation and cavity wall insulation, were demonstrated to have acceptable payback periods and would therefore inevitably be viable under the Green Deal regardless of regional and occupancy influences. This study investigates more costly measures such as External Wall Insulation (EWI) and Air Source Heat Pumps (ASHPs) in more detail to see whether different modelling tools and/ or assumptions would suggest such measures to be more or less viable under the Green Deal.

A range of modelling tools have therefore been assessed during this study, including Reduced Data SAP (RdSAP), full SAP, PVSol for the assessment of photovoltaic (PV) systems and Design Builder, which allows tailoring of occupancy patterns and behavioural impacts.

RdSAP and full SAP were compared across the range of dwellings receiving refurbishment measures to assess the impact of more accurately specifying wall U values and window areas in full SAP for equivalent properties. Overall it was determined that full SAP will generally give a more accurate representation of the dwelling and typically forecasts higher savings than RdSAP. However, overall the differences between the two tools are not likely to be great enough to influence the viability of key refurbishment measures such as EWI and ASHPs under the Green Deal.

Since both RdSAP and full SAP make the same assumptions for PV, the electricity generation forecasts for dwellings receiving PV systems were compared with estimates using PVSol software. PVSol utilises regional solar irradiation data (in this case for a location near Newquay, Cornwall) and allows specific PV panel and inverter combinations to be modelled. On average, PVSol predicted a 16% improvement in energy generation compared to SAP, which could influence the payback periods of PV under funding mechanisms such as the Green Deal and the Feed in Tariff (FIT). SAP will provide pessimistic estimates for the south of the UK but optimistic estimates for the north. Therefore, models such as PVSol that allow localised solar conditions to be considered will provide a more accurate assessment of the likely generation of a given PV system.

Design Builder modelling software was used to assess a refined selection of dwellings so that occupancy impacts could be analysed and compared with standard RdSAP results. The objective was to determine whether specifying key variables in the Design Builder models (rather than using calculated assumptions in SAP) would provide more accurate forecasts of energy usage and whether different household types would find measures such as EWI or ASHPs more viable under the Green Deal as a result.

Ultimately, the accuracy of each model will be verified against real in-use monitoring data from the Penwithick pilot study in due course. In the short term, the modelling suggests that different sized households would be likely to experience variations in fuel costs and subsequent savings, with smaller occupancy households often saving relatively more than larger households as there are assumed to be less benefit from internal gains with fewer occupants. Additionally (and perhaps unsurprisingly), significant variation can be introduced when regional climate data is utilised in Design Builder, which would certainly affect the viability of measures under the Green Deal.

3 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Overall, despite variations that emerge across the various modelling tools assessed, it still appears that in the majority of cases the capital cost of EWI and ASHPs would need to reduce or be subsidised by additional funding/ grants in order to encourage the mainstream uptake of these measures. Further financial analysis will follow in due course to see what additional economic factors may also contribute (beneficially or detrimentally) to the occupancy impacts seen here.

BRE acknowledge the ongoing support of Cornwall Council during this research and give thanks for allowing use of the Penwithick pilot project as the basis and data source for this study. The longer term monitoring programme for the dwellings that the Council has instigated will also be an asset to this ongoing research. Also, BRE wish to thank Ocean Services, who have carried out the refurbishment measures on the dwellings and provided key information on the installed measures and their costs.

4 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Contents

1 Introduction 5 1.1 Background 5 1.2 Approach to the study 5

2 Comparison of RdSAP with full SAP 2009 8 2.1 Section summary: RdSAP vs full SAP 16

3 Comparison of SAP assumptions for PV with PVSol modelling 20

4 Comparison of RdSAP with Design Builder 22 4.1 Consideration of occupancy impacts 22 4.2 Derivation of occupancy and heating patterns for modelling 22 4.3 Standardised dwelling models 25 4.4 Results of occupancy modelling 27 4.5 Section summary: RdSAP vs Design Builder occupancy assessment 35 4.6 Consideration of regional climate data 36

5 Additional influencing factors 38 5.1 Under-heated homes 38 5.2 Comfort taking 38

6 Conclusions 40 6.1 RdSAP vs full SAP 40 6.2 SAP vs PVSol 40 6.3 RdSAP vs Design Builder 40 6.4 General 42

Annexe A: Fuel cost & CO2 emissions from RdSAP and Design Builder 43

5 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

1 Introduction

Cornwall Council, with their delivery partner Ocean Services, are undertaking a Green Deal retrofit pilot project in the village of Penwithick, near St Austell. BRE are acting as Technical Advisors to the project team to help achieve their objectives. The purpose of the pilot is to determine which refurbishment measures are suitable for the various property types in the village (considered representative of Cornwall as a whole) and to investigate which offer the most benefits in terms of payback, cost savings to households and CO2 emissions reductions. A financial analysis will be completed to see how measures are likely to stack up against the Green Deal ‘golden rule’ based on energy modelling predictions. Properties receiving measures will be monitored to assess the resulting savings in fuel bills in order to provide a sensitivity analysis for the energy modelling and financial assessment.

1.1 Background

During the first phase of the pilot, initial modelling was carried out by BRE using full SAP (the Government’s Standard Assessment Procedure for dwellings) on all potential measures for dwellings in Penwithick to prioritise which were most cost effective. The findings were reported to the project team and the BRE Trust in May 2012 in the report ‘Penwithick Green Deal Pilot Project: Selection of properties for refurbishment measures’. The most common measures, such as loft insulation and cavity wall insulation, were demonstrated to have acceptable payback periods (<20 years) and would therefore inevitably be viable for the Green Deal regardless of occupancy influences.

It is likely that some households will wish to consider less conventional measures, particularly for hard to treat homes, such as solid wall and system built dwellings and/ or off-gas locations, including solid wall insulation (assumed to be externally applied in this study) and Air Source Heat Pumps. However, these are generally (currently at least) significantly more expensive measures and hence their viability under the Green Deal is less certain (or unviable within an acceptable period, as indicated from the above report). This study therefore investigates these more costly measures in more detail to see whether occupancy and behavioural factors would be likely to make such measures more or less viable.

Once completed, this data will be fed into the upcoming financial analysis in the next phase of the project to assess the impact on the potential Green Deal payback rates in more detail.

1.2 Approach to the study

1. Having established from the initial ‘Property Selection’ report the dwellings that would benefit most from receiving refurbishment measures, detailed surveys were carried out on the shortlisted properties, capturing the physical building parameters, the condition of various elements of the property and the occupancy patterns of the household.

2. Working alongside Ocean Services, the final properties and measures were selected based on their technical and practical suitability.

6 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

3. Further detailed modelling was then carried out using a range of modelling tools to establish the most accurate way of representing potential dwellings for Green Deal assessment. The intention at the end of the project is to compare the real in-use findings from the households to the various modelling tools and assumptions used to see which may offer the most realistic forecasts to households considering Green Deal loans in the future.

a. The first phase of modelling (for property selection) was carried out in full SAP in order to accurately represent U values of properties in the base case and refurbished cases. However, existing buildings are typically modelled in RdSAP (Reduced data SAP) to make various assumptions when relatively limited information about existing buildings is known. Houses receiving measures (with the exception of PV) were therefore modelled in both versions of SAP to compare what variation in forecast savings may result from these similar modelling tools. (Reported in Section 2.)

b. Since both versions of SAP make the same assumptions for PV, the estimated electricity generation for dwellings receiving a PV system was compared with a separate dedicated modelling tool – PVSol – to assess the variations that could be expected when key variables can be more accurately represented. (Reported in Section 3.)

c. It is recognised that the occupancy and behavioural impacts of households could influence the running costs and therefore savings anticipated from various refurbishment measures. BRE have developed an online Green Deal Occupancy Assessment (GD OA) tool that can be utilised by Green Deal assessors to provide households with an indication of how their circumstances may vary compared to the ‘typical’ household scenarios assumed in SAP. The tool is not yet fully capable of addressing the extent of the measures undertaken during this Penwithick pilot study; Air Source Heat Pumps (ASHPs) are not yet deemed an official Green Deal measure and so are not currently included, while in the short term it is anticipated that dwellings not of solid wall or system build construction would not consider External Wall Insulation (EWI) under the Green Deal. In any case, the output from the GD OA tool is intended to give only a summary of the variation in fuel costs that may be experienced as a result of the various occupancy and behavioural aspects, rather than presenting any level of detail regarding heating, hot water and other energy use variations.

Therefore, to investigate the influence of potential occupancy scenarios on the savings achieved by EWI and ASHPs in more detail, an alternative modelling tool has been used – Design Builder – to accurately represent the physical building parameters as well as the occupancy factors against a dynamic model (SAP is a steady state model assessed on a month-by-month basis) and compare fuel cost estimates and savings against the RdSAP ‘typical’ estimates. In order to make the Design Builder results comparable to RdSAP and focus solely on the occupancy impacts, an equivalent climate data set was selected to align with SAP’s use of the East Pennines climate. (Reported in section 4.)

d. In order to provide an indication of the range of further variability that may be experienced in the modelling when considering the Green Deal across the whole of the UK, a small number of comparative models have been run in Design Builder for North and South extremes of the UK. (Reported in section 5.)

7 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

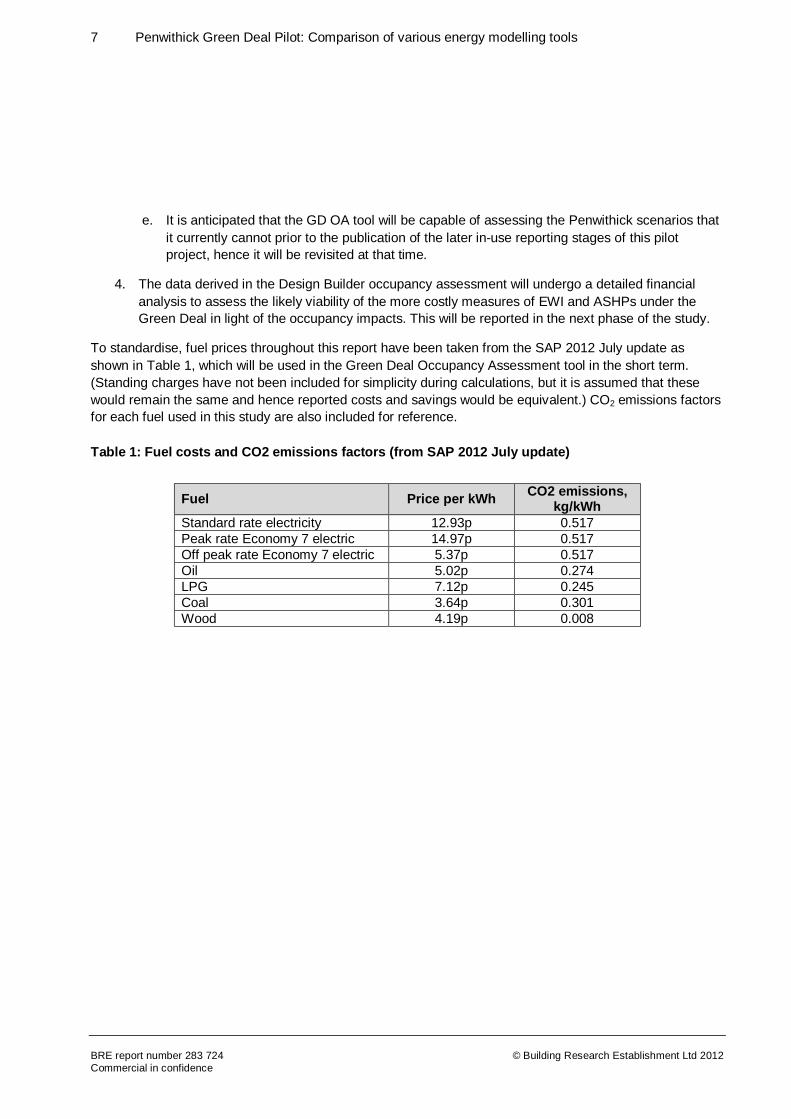

e. It is anticipated that the GD OA tool will be capable of assessing the Penwithick scenarios that it currently cannot prior to the publication of the later in-use reporting stages of this pilot project, hence it will be revisited at that time.

4. The data derived in the Design Builder occupancy assessment will undergo a detailed financial analysis to assess the likely viability of the more costly measures of EWI and ASHPs under the Green Deal in light of the occupancy impacts. This will be reported in the next phase of the study.

To standardise, fuel prices throughout this report have been taken from the SAP 2012 July update as shown in Table 1, which will be used in the Green Deal Occupancy Assessment tool in the short term. (Standing charges have not been included for simplicity during calculations, but it is assumed that these would remain the same and hence reported costs and savings would be equivalent.) CO2 emissions factors for each fuel used in this study are also included for reference.

Table 1: Fuel costs and CO2 emissions factors (from SAP 2012 July update)

Fuel Price per kWh CO2 emissions, kg/kWh

Standard rate electricity 12.93p 0.517 Peak rate Economy 7 electric 14.97p 0.517 Off peak rate Economy 7 electric 5.37p 0.517 Oil 5.02p 0.274 LPG 7.12p 0.245 Coal 3.64p 0.301 Wood 4.19p 0.008

8 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

2 Comparison of RdSAP with full SAP 2009

The majority of dwellings receiving measures have been individually modelled in RdSAP and full SAP to assess the variations predicted by each tool. In cases where properties are just receiving ventilation measures or PV, these have not been included as the influence of ventilation fans will be negligible on overall building performance and energy generation by PV is independent of the energy performance of the dwelling. (The potential FIT income will be influenced by household behaviour through the ratio of offset usage while generating and export back to the grid, but since specific export meters have not been installed with the PV, the offset usage/ export ratio will be assumed at 50%.) Data for each dwelling was gathered from detailed site surveys, covering typical information required by SAP, plus more detailed information about occupancy patterns, condition and practical building features that may influence the installation of certain measures.

The purpose of this comparison is to assess the impact of some of the more ‘rigid’ assumptions that are made in RdSAP, particularly with regard to improvement measures. For instance, the U values assumed for Cornish-type properties are classed as ‘system build’ in RdSAP, giving a wall U value of 2.0 W/m2K. However, in full SAP it is possible to input bespoke U values for the ground level walls and the mansard of 2.42 W/m2K and 2.24 W/m2K respectively.

For the timber hybrid properties, RdSAP assumes a U value of 0.8 W/m2K for all of the walls. However, more detailed knowledge of the construction allows bespoke values to be entered into full SAP of 0.89 W/m2K for the front and rear walls and 0.74 W/m2K for the gable wall. RdSAP then assumes an improvement to 0.4 W/m2K when insulating these walls, whereas in reality the U value will be improved to 0.3 W/m2K.

The most recent version of RdSAP (v9.91) actually allows improved flexibility with data entry regarding U values, as it is possible to input a specific U value for an element. However, it is likely that Green Deal assessors will not have such specific knowledge of the dwellings they will be assessing, so more generalised assumptions with regard to construction methods are likely to be made, in line with the assumptions used in this RdSAP modelling.

The sample of properties across the following tables represent the variations typical of a random cross section of dwellings, including different fuel types, the use of secondary heating systems, floor area, building extensions and the extent of measures already carried out in the pre-refurbished houses. Hence this comparison looks to identify whether any general patterns emerge across the two SAP tools, despite this range of variety. (Absolute savings per measure are relatively incomparable due to these variations, so specific savings are not a focus of this comparison exercise.)

It should be noted that although SAP scores have been quoted in the tables below, the fuel prices used to calculate the annual running costs have been updated compared to those assumed in SAP 2009, to those given in Table 1.

9 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

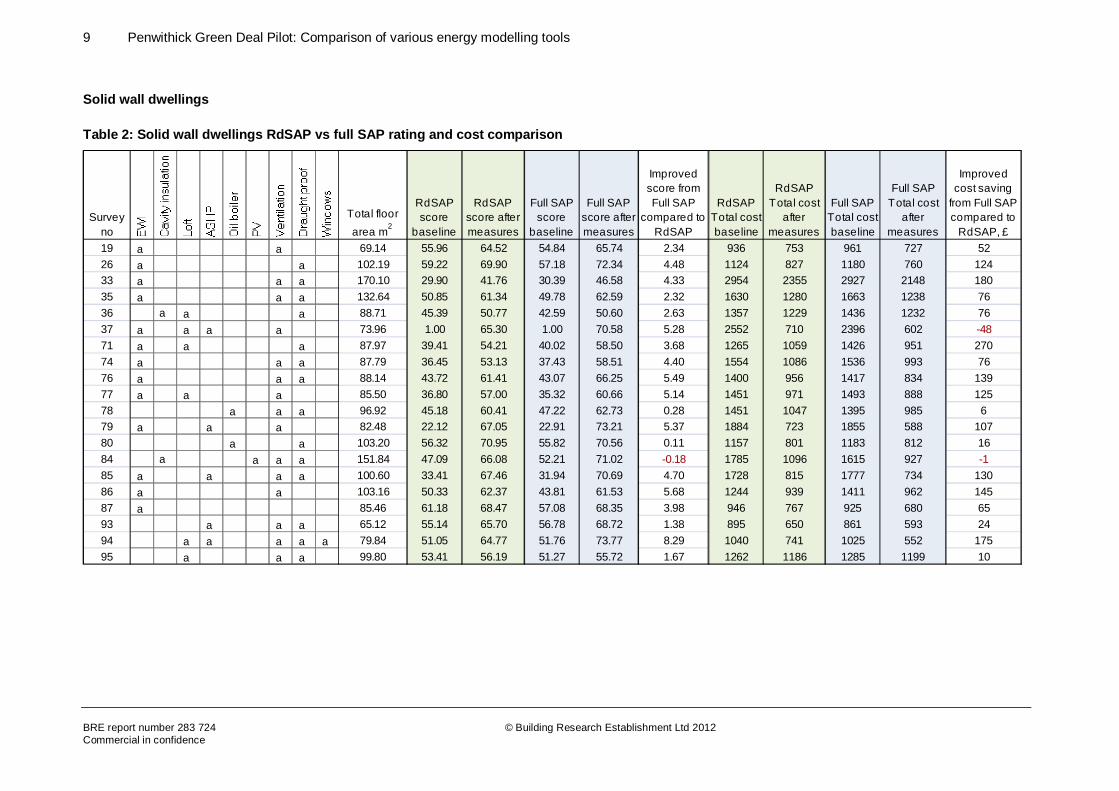

Solid wall dwellings

Table 2: Solid wall dwellings RdSAP vs full SAP rating and cost comparison

Survey no

Total floor area m2

RdSAP score

baseline

RdSAP score after measures

Full SAP score

baseline

Full SAP score after measures

Improved score from Full SAP

compared to RdSAP

RdSAP Total cost baseline

RdSAP Total cost

after measures

Full SAP Total cost baseline

Full SAP Total cost

after measures

Improved cost saving

from Full SAP compared to

RdSAP, £19 a a 69.14 55.96 64.52 54.84 65.74 2.34 936 753 961 727 5226 a a 102.19 59.22 69.90 57.18 72.34 4.48 1124 827 1180 760 12433 a a a 170.10 29.90 41.76 30.39 46.58 4.33 2954 2355 2927 2148 18035 a a a 132.64 50.85 61.34 49.78 62.59 2.32 1630 1280 1663 1238 7636 a a a 88.71 45.39 50.77 42.59 50.60 2.63 1357 1229 1436 1232 7637 a a a a 73.96 1.00 65.30 1.00 70.58 5.28 2552 710 2396 602 -4871 a a a 87.97 39.41 54.21 40.02 58.50 3.68 1265 1059 1426 951 27074 a a a 87.79 36.45 53.13 37.43 58.51 4.40 1554 1086 1536 993 7676 a a a 88.14 43.72 61.41 43.07 66.25 5.49 1400 956 1417 834 13977 a a a 85.50 36.80 57.00 35.32 60.66 5.14 1451 971 1493 888 12578 a a a 96.92 45.18 60.41 47.22 62.73 0.28 1451 1047 1395 985 679 a a a 82.48 22.12 67.05 22.91 73.21 5.37 1884 723 1855 588 10780 a a 103.20 56.32 70.95 55.82 70.56 0.11 1157 801 1183 812 1684 a a a a 151.84 47.09 66.08 52.21 71.02 -0.18 1785 1096 1615 927 -185 a a a a 100.60 33.41 67.46 31.94 70.69 4.70 1728 815 1777 734 13086 a a 103.16 50.33 62.37 43.81 61.53 5.68 1244 939 1411 962 14587 a 85.46 61.18 68.47 57.08 68.35 3.98 946 767 925 680 6593 a a a 65.12 55.14 65.70 56.78 68.72 1.38 895 650 861 593 2494 a a a a a 79.84 51.05 64.77 51.76 73.77 8.29 1040 741 1025 552 17595 a a a 99.80 53.41 56.19 51.27 55.72 1.67 1262 1186 1285 1199 10

10 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Figure 1: Forecast annual fuel savings for solid wall dwellings using RdSAP and full SAP

11 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

It is interesting to note that for some dwellings in Table 2 the baseline RdSAP score is lower than the full SAP score, whereas for other dwellings it is higher. However, regardless of the starting SAP rating, the SAP score increase is greater in full SAP in all but one case (with that case being of negligible difference).

With the exception of two dwellings assessed, full SAP forecasts higher cost savings compared to RdSAP (by £87 on average), which for the dwellings receiving EWI will be largely due to the different uplift assumptions made to the wall U values (i.e. RdSAP assuming 0.6 W/m2K by default, full SAP using 0.3 W/m2K). For dwelling number 37, RdSAP actually estimates a greater saving as a result of different efficiency assumptions made for the ASHP (despite the same heat pump being used), which itself is likely to have been a result of different overall heat loss assumptions due to window area and U value differences between RdSAP and full SAP. Dwelling number 84 received cavity insulation in an extension rather than solid wall insulation and overall the outputs from RdSAP and full SAP are virtually identical.

An additional saving of ~£87 per year over a loan period of 20 years would help fund an additional £1740 worth of measures (not taking into account interest rates or fuel cost increases), equating to approximately 15% of the average savings forecast across the solid wall properties by full SAP. In some circumstances, this could improve the viability of EWI as a Green Deal measure (depending on the actual cost, the interest rates and other factors that would need to be taken into consideration).

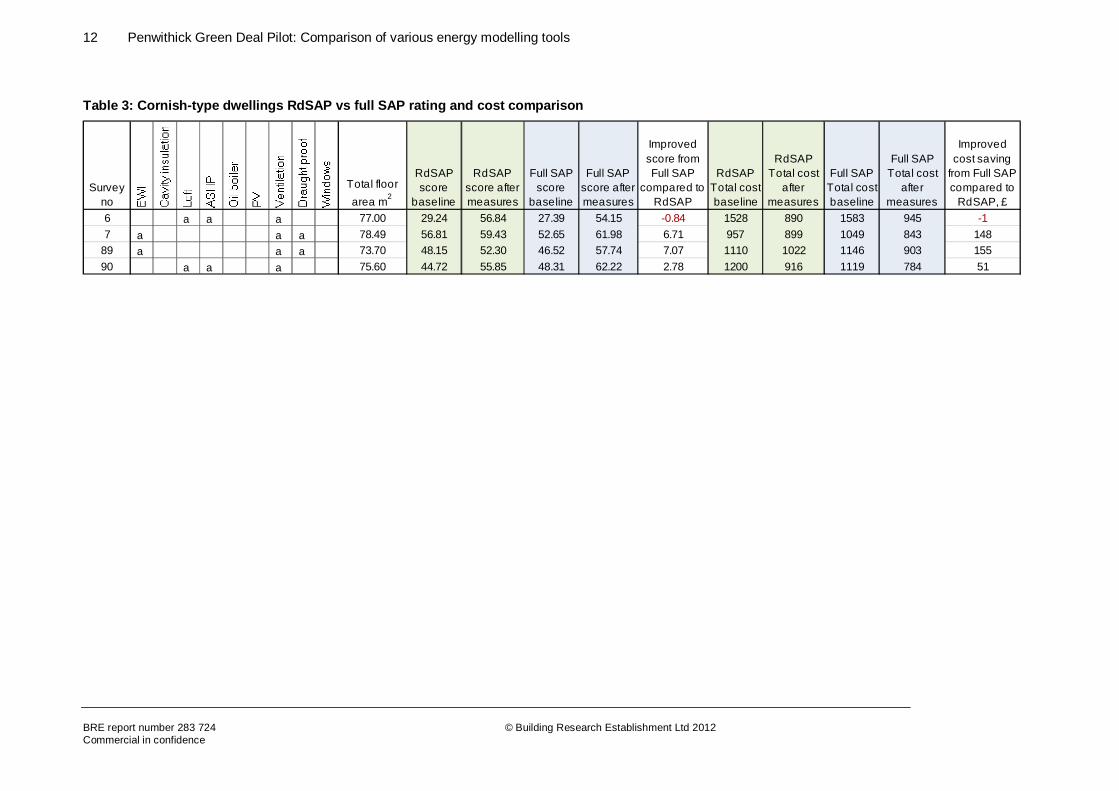

Cornish-type dwellings

The Cornish dwellings within the study are split into two key types – those that are essentially ‘as built’ (numbers 7 and 89) and those that have previously been refurbished by entirely replacing the concrete panelised walls at ground floor level with a cavity wall (numbers 6 and 90). The latter were therefore not suggested for external wall insulation but were instead offered ASHPs as they previously had no fixed heating system (relied on portable electric heaters or coal respectively).

Despite each pair of dwellings receiving comparable measures, the SAP scores in Table 3 demonstrate how other factors contribute to the potential savings, such as adjoined extensions and efficiencies in the fuel system used, which are both contributory across these four example dwellings. Overall however, full SAP forecasts higher cost savings compared to RdSAP (by ~£88 on average). This additional saving per year over a loan period of 20 years would help fund a further £1780 worth of measures (not taking into account interest rates and fuel cost increases), equating to approximately 25% of the average savings forecast across the Cornish properties by full SAP. However, this is not likely to be enough to improve the viability of more expensive measures such as ASHPs or EWI under the Green Deal for Cornish properties.

12 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Table 3: Cornish-type dwellings RdSAP vs full SAP rating and cost comparison

Survey no

Total floor area m2

RdSAP score

baseline

RdSAP score after measures

Full SAP score

baseline

Full SAP score after measures

Improved score from Full SAP

compared to RdSAP

RdSAP Total cost baseline

RdSAP Total cost

after measures

Full SAP Total cost baseline

Full SAP Total cost

after measures

Improved cost saving

from Full SAP compared to

RdSAP, £6 a a a 77.00 29.24 56.84 27.39 54.15 -0.84 1528 890 1583 945 -17 a a a 78.49 56.81 59.43 52.65 61.98 6.71 957 899 1049 843 148

89 a a a 73.70 48.15 52.30 46.52 57.74 7.07 1110 1022 1146 903 15590 a a a 75.60 44.72 55.85 48.31 62.22 2.78 1200 916 1119 784 51

13 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Figure 2: Forecast annual fuel savings for Cornish dwellings using RdSAP and full SAP

14 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

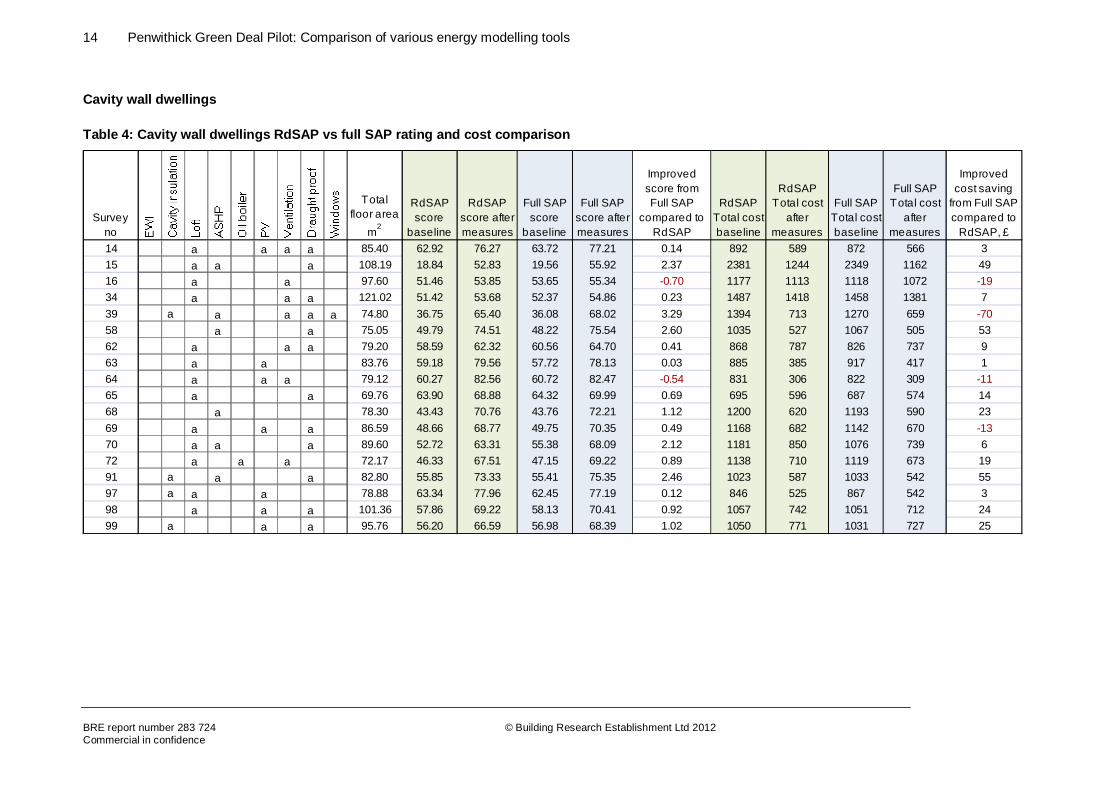

Cavity wall dwellings

Table 4: Cavity wall dwellings RdSAP vs full SAP rating and cost comparison

Survey no

Total floor area

m2

RdSAP score

baseline

RdSAP score after measures

Full SAP score

baseline

Full SAP score after measures

Improved score from Full SAP

compared to RdSAP

RdSAP Total cost baseline

RdSAP Total cost

after measures

Full SAP Total cost baseline

Full SAP Total cost

after measures

Improved cost saving

from Full SAP compared to

RdSAP, £14 a a a a 85.40 62.92 76.27 63.72 77.21 0.14 892 589 872 566 315 a a a 108.19 18.84 52.83 19.56 55.92 2.37 2381 1244 2349 1162 4916 a a 97.60 51.46 53.85 53.65 55.34 -0.70 1177 1113 1118 1072 -1934 a a a 121.02 51.42 53.68 52.37 54.86 0.23 1487 1418 1458 1381 739 a a a a a 74.80 36.75 65.40 36.08 68.02 3.29 1394 713 1270 659 -7058 a a 75.05 49.79 74.51 48.22 75.54 2.60 1035 527 1067 505 5362 a a a 79.20 58.59 62.32 60.56 64.70 0.41 868 787 826 737 963 a a 83.76 59.18 79.56 57.72 78.13 0.03 885 385 917 417 164 a a a 79.12 60.27 82.56 60.72 82.47 -0.54 831 306 822 309 -1165 a a 69.76 63.90 68.88 64.32 69.99 0.69 695 596 687 574 1468 a 78.30 43.43 70.76 43.76 72.21 1.12 1200 620 1193 590 2369 a a a 86.59 48.66 68.77 49.75 70.35 0.49 1168 682 1142 670 -1370 a a a 89.60 52.72 63.31 55.38 68.09 2.12 1181 850 1076 739 672 a a a 72.17 46.33 67.51 47.15 69.22 0.89 1138 710 1119 673 1991 a a a 82.80 55.85 73.33 55.41 75.35 2.46 1023 587 1033 542 5597 a a a 78.88 63.34 77.96 62.45 77.19 0.12 846 525 867 542 398 a a a 101.36 57.86 69.22 58.13 70.41 0.92 1057 742 1051 712 2499 a a a 95.76 56.20 66.59 56.98 68.39 1.02 1050 771 1031 727 25

15 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

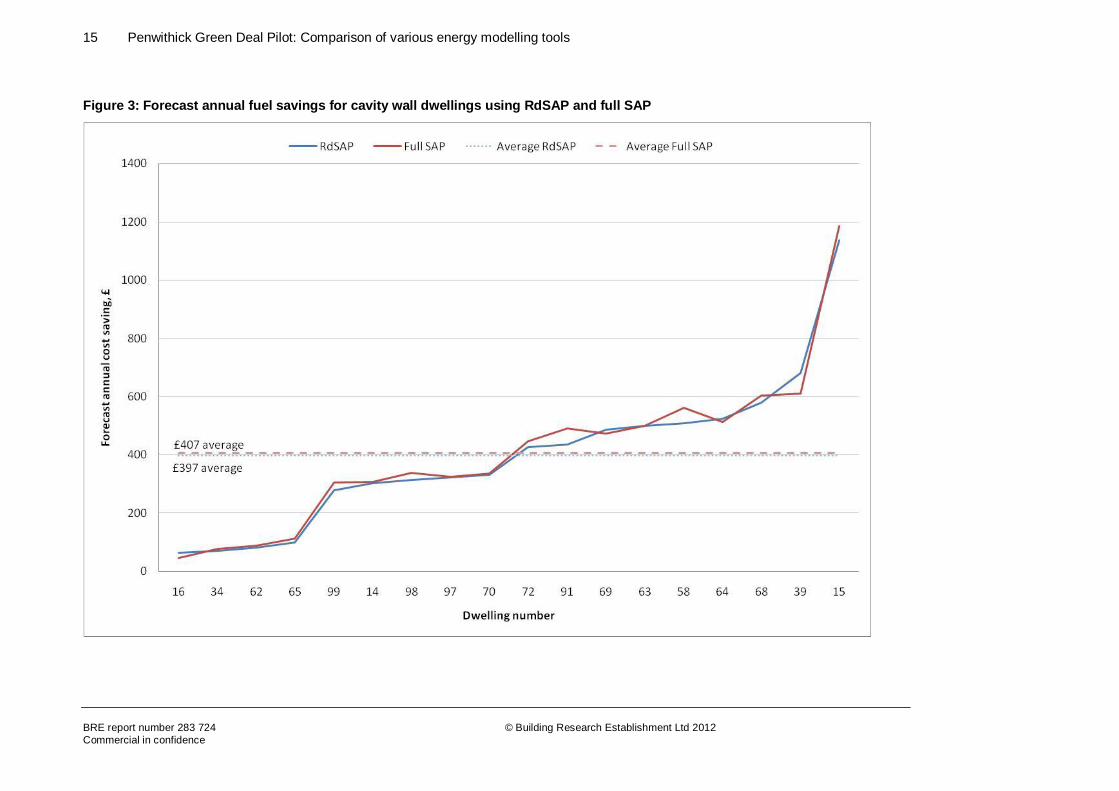

Figure 3: Forecast annual fuel savings for cavity wall dwellings using RdSAP and full SAP

16 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

As with the solid wall dwellings, in some cases the baseline RdSAP score for the cavity dwellings from Table 4 is lower than the full SAP score, whereas for other dwellings it is higher. The largest SAP improvements from full SAP compared to RdSAP arise when an ASHP is modelled, suggesting that full SAP attributes more benefit to the ASHPs than the equivalent RdSAP model does. If this is a ‘real’ effect (i.e. is realised in real life installations) it will be a useful benefit for households considering a relatively expensive measure such as an ASHP under the Green Deal. However, the savings indicated by full SAP are not very large, so it is not likely to make a significant influence on the viability of such a measure under the Green Deal. (NB: For dwelling number 39, the difference in SAP score and cost savings between RdSAP and full SAP is likely to be more influenced by the different U value assumptions for the windows between each model rather than the impact of the ASHP.)

Cavity dwellings receiving other measures (i.e. not ASHPs) do not generally bring about such differences between the RdSAP and full SAP models.

Timber hybrid dwellings

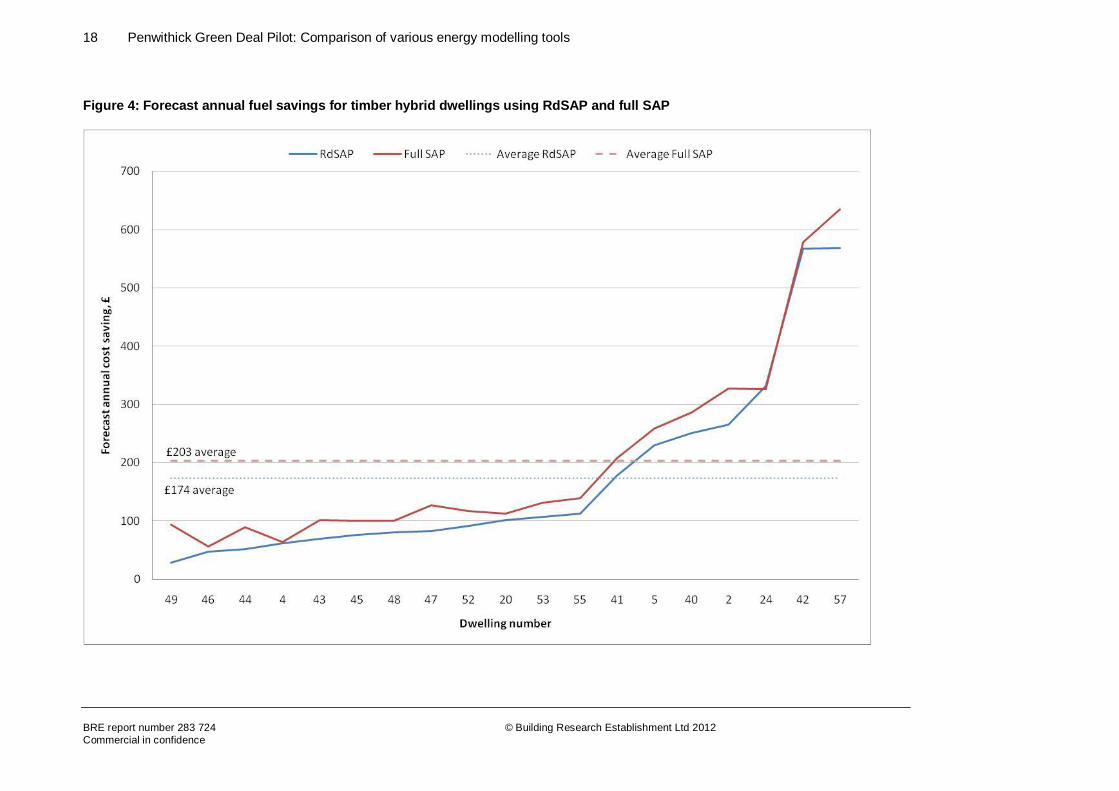

Despite the differences in U values assumed between RdSAP and full SAP for the timber hybrid dwellings, the SAP scores in Table 5 are generally relatively similar between RdSAP and full SAP, suggesting the variables counteract each other when comparing the improved scenarios with the baselines. Across the range of uplift measures assessed, full SAP generally assumes increased savings of £29 on average compared to RdSAP, but this is not likely to be a significant enough difference to make more expensive measures such as EWI or ASHPs more viable under the Green Deal. (NB: for dwelling 24, RdSAP actually forecasts a marginally higher SAP score and cost increase than full SAP, which is a result of different window areas assumed between the tools, with full SAP being more accurate.)

From the forecast cost savings witnessed from either RdSAP or full SAP, it does not appear that either tool would make the more costly measures such as ASHP or EWI appear more viable under the Green Deal.

2.1 Section summary: RdSAP vs full SAP

In all but a relatively small number of cases (7 of the 61 dwellings), the full SAP calculation estimates a larger annual fuel bill saving than the RdSAP calculations. The differences are generally caused by:

• Assumptions for the U values of the baseline scenarios, i.e. more accurate in full SAP (calculated separately in U value calculators) than RdSAP

• Differences subsequently assumed in the uplifted U values. RdSAP v9.90 offers a set improvement for solid wall insulation for instance of 50mm, while v9.91 offers the option of 50, 100 or 150mm. However, full SAP allows the specific intended U value to be input.

• Assumptions of the window areas – RdSAP assumes typical window ratios relative to the building floor area, while in full SAP the actual window sizes have been specifically input. (There is potential to do this within RdSAP but it is assumed that most Green Deal Assessors would simply use the ‘typical’ values.)

• Windows with different U values are not readily captured within RdSAP apart from whether single or double glazed – different performance double glazing is not readily accounted for, whereas in full SAP it can be input more accurately.

• The ability to specify the number of mechanical extraction fans in full SAP, which will influence the infiltration rate/ ventilation rate in the model, whereas RdSAP will make a default assumption.

17 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Table 5: Timber hybrid dwellings RdSAP vs full SAP rating and cost comparison

Survey no

Total floor area

m2

RdSAP score

baseline

RdSAP score after measures

Full SAP score

baseline

Full SAP score after measures

Improved score from Full SAP

compared to RdSAP

RdSAP Total cost baseline

RdSAP Total cost

after measures

Full SAP Total cost baseline

Full SAP Total cost

after measures

Improved cost saving

from Full SAP compared to

RdSAP, £2 a a 79.20 52.07 64.92 51.73 67.50 2.92 1015 750 1022 695 634 a a 90.42 53.27 56.55 54.84 58.21 0.09 1075 1013 1038 974 25 a a a a 80.30 51.12 62.30 52.99 65.55 1.38 1042 813 1002 743 3020 a a a a 78.10 67.69 72.07 67.15 72.02 0.49 742 640 755 642 1124 a a a 80.30 57.62 72.16 57.41 71.74 -0.21 981 650 986 660 -540 a a a a 78.84 52.07 64.37 53.13 67.11 1.68 1010 759 987 701 3641 a a a 80.30 57.66 66.55 56.40 66.65 1.36 900 721 927 719 3042 a a a a 79.20 40.54 66.77 40.38 67.11 0.50 1277 710 1281 703 1143 a a a 77.76 39.11 42.01 40.49 44.88 1.49 1298 1228 1264 1163 3244 a 96.16 58.79 60.91 58.25 61.89 1.52 987 935 1001 912 3745 a a 72.00 54.48 58.21 55.09 60.05 1.23 902 826 890 789 2546 a a 77.76 56.76 58.96 57.75 60.40 0.45 893 846 872 815 947 a a a 80.30 57.43 62.25 57.29 63.15 1.04 905 823 908 781 4548 a a a a 72.00 52.67 56.62 56.57 61.52 1.00 940 860 860 759 2049 a a 100.70 57.37 58.48 53.13 56.83 2.59 1063 1035 1170 1077 6652 a a a a 90.50 46.16 49.84 47.22 52.02 1.12 1240 1148 1213 1095 2653 a a a a 80.30 52.36 57.26 50.74 56.83 1.19 1016 910 1051 919 2555 a a a a 80.30 64.75 69.58 62.33 68.27 1.11 814 701 870 732 2657 a a a 76.32 38.93 65.61 36.25 68.23 5.30 1287 718 1354 719 66

18 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Figure 4: Forecast annual fuel savings for timber hybrid dwellings using RdSAP and full SAP

19 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Since there are such a mix of improvement measures and different baseline starting points across each of the dwellings, it is very difficult to identify trends in cost savings per measure across the properties selected. For this reason, it has been necessary to standardise the modelling in the section X in order to allow comparisons between tools and to identify the relative benefits of key improvement measures such as ASHPs and EWI.

In general, the results from the full SAP assessment of the dwellings is likely to be more accurate than those from RdSAP because the baseline U values and improved values are better represented, while RdSAP makes assumptions based on the year and construction given for the property. Some additional factors influence a small number of models, such as the window area assumed in RdSAP compared to the measured values input into full SAP, which could have a positive or negative effect on the heat loss calculation depending on whether the ratio is smaller or greater than in reality.

Typically, full SAP forecasts slightly improved cost savings compared to RdSAP, which would offer improved paybacks under the Green Deal. However, the RdSAP results are generally more conservative in their savings estimates, which may be more reassuring to householders, but may limit the uptake of some measures.

The difference between RdSAP and full SAP ultimately hinges on the knowledge that the assessor would have about a particular house while doing an assessment. RdSAP makes more generalised assumptions than full SAP, but full SAP relies on knowledge from other sources, e.g. U value calculators to input more accurate U values for the thermal elements, which a Green Deal assessor may not have to hand. Overall however, it seems there would be limited scenarios where the differences in assumptions made between RdSAP and full SAP could bring about enough variation to influence the viability of measures such as EWI and ASHPs under the Green Deal.

20 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

3 Comparison of SAP assumptions for PV with PVSol modelling

SAP models make assumptions for the electricity generation from typical performance PV panels. However, there are alternative modelling tools available dedicated to the forecast of PV electrical generation that are generally accepted to offer more accurate forecasting. For comparison, the results from SAP have been compared with models using PVSol software to assess these differences.

Within PVSol, the specific PV panel and inverter combinations being installed on the dwellings were modelled, taking into account the precise roof pitch and orientation measured on site (SAP modelling assumed approximate roof pitch and orientation from visual surveys). The software also contains a large database of solar irradiation data for various locations, allowing a location close to the installation site to be selected (St Mawgan, near Newquay, on a similar latitude to Penwithick), rather than relying on generalised assumptions for the UK as in SAP. The PV systems were designed and specified on a house-by-house basis by Ocean Services and utilised Aleo PV panels and SMA Sunnyboy inverters.

Table 6 shows the dwellings receiving PV panels under the pilot programme and the relevant panel size and general orientation. It also shows the kWh electricity generation assumed in both SAP (RdSAP and full SAP use the same estimates) and PVSol.

Table 6: PV panel sizes and forecast output from SAP and PVSol

Dwelling no

General roof

orientation

Installed kWp

SAP forecast

electricity generation,

kWh/y

PVSol forecast

electricity generation,

kWh/y

% increase

in PVSol

estimate 88 S 1.92 1648 1889 15% 96 SE 1.92 1577 1889 20% 97 SE 1.92 1577 1889 20% 98 SE 1.92 1577 1889 20%

100 SE 1.92 1577 1889 20% 27 SW 1.92 1577 1889 20% 99 SW 1.92 1577 1889 20% 3 SE 2.4 1972 2316 17%

38 SE 2.4 1972 2262 15% 14 SW 2.4 1972 2262 15% 81 SW 2.4 1972 2342 19% 25 S 2.88 2472 2876 16% 28 S 2.88 2472 2828 14% 60 SE 2.88 2366 2730 15% 69 S 3.36 2884 3310 15% 84 S 3.36 2884 3310 15% 59 SW 3.36 2761 3172 15% 63 SW 3.36 2761 3128 13% 64 SW 3.36 2761 3128 13% 22 SW 3.60 2958 3236 9%

21 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Within the PVSol modelling, some minor variation between what appear to be similar panel sizes are due to more accurate representation of roof pitch and angle of orientation from South that can be entered more specifically in PVSol (by degree, measured on site in a separate survey) compared to SAP. In general, PVSol forecasts an increase in electricity generation compared to SAP (average 16% increase) as a result of the more accurate climate data and methodology used in its calculations, which will obviously provide households with increased offset electrical usage or revenue from the Feed in Tariff.

At the current rate of Feed in Tariff (16p/kWh generation, 3.2p/kWh export to grid) and assuming that 50% of the electricity is offset at 12.93p/kWh (Table 1) and 50% exported to grid, the average increased benefit from the additional forecast electricity would be £82 per year, equivalent to £1640 over 20 years (not considering likely cost increases in electricity or index linking of the FIT rates).

Since the forecast electricity generation from SAP is more conservative than PVSol in this Southerly location, it may reassure householders that they should at least be able to achieve the paybacks forecast in the Green Deal assessment, which will be based on SAP. This may also help to account (mostly or partially) for decreases in PV panel performance over their intended lifespan typically of up to 20% as quoted by manufacturers. (Figures quoted in Table 6 assume performance for the first year of installation, i.e. panel at their most efficient.)

It should be noted however, that since SAP assumes solar irradiation on a latitude central to the UK (across the Pennines at 53.4°), locations South of this may experience greater savings as indicated above for Cornwall, but locations North of this may experience reduced savings, as solar irradiation tends to reduce further North from the equator. Hence, households in Northern parts of the UK should regard estimates from SAP as optimistic and consider seeking more accurate modelling in a tool able to utilise local solar irradiation data before considering the payback that may be achieved under a mechanism such as the Green Deal and/ or the Feed in tariff.

22 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

4 Comparison of RdSAP with Design Builder

4.1 Consideration of occupancy impacts

SAP makes standardised assumptions for occupancy patterns within dwellings. However, actual household patterns are likely to differ from these assumptions and will therefore introduce potential variations in the savings that may be achieved by households. In some instances this may make improvement measures pay back more quickly, while in others it may actually extend the potential payback periods.

For more costly measures such as solid wall insulation and air source heat pumps, the standard occupancy scenarios of SAP suggest that the savings achieved would not allow the Green Deal to be viable (see earlier report on Property Selection). An analysis has been done on a range of occupancy scenarios using the Design Builder modelling tool that allows behavioural patterns to be considered, to see if any households are likely to experience greater viability of such measures under the Green Deal. (The financial analysis that will follow will elaborate on these results further.)

Unlike SAP, Design Builder is a graphical user interface-based building energy simulation tool that uses EnergyPlus as its simulation engine. It allows more control of variables such as weather data, occupancy, heating system, etc. Each heating system can be controlled using a profile through which seasonal variations in performance can be emulated. For this study, it has been used to assess the impact of variations in occupancy profiles on the likely savings achieved by EWI and ASHPs.

4.2 Derivation of occupancy and heating patterns for modelling

During the initial surveys carried out to establish the building parameters and building condition etc, information was also collected about household occupancy and behavioural patterns, including:

• Number of people (adults and children) in household

• Hours in the day when someone is typically at home (Monday to Friday, Saturday to Sunday)

• Hours in the day when the heating is typically switched on (Monday to Friday, Saturday to Sunday)

• Typical temperature preferred by the household (if known)

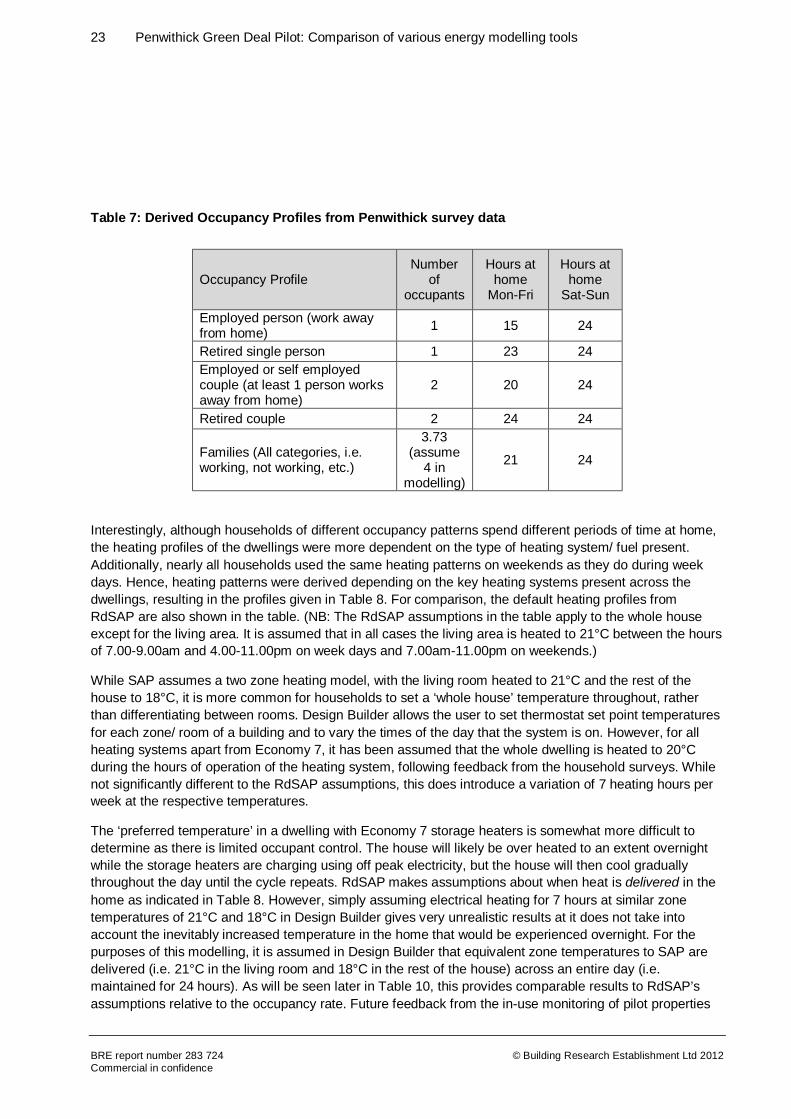

The data gathered across the participating households was then analysed and ultimately categorised into 5 occupancy groups that were then used to derive average profiles. These are shown in Table 7.

23 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Table 7: Derived Occupancy Profiles from Penwithick survey data

Occupancy Profile Number

of occupants

Hours at home

Mon-Fri

Hours at home

Sat-Sun

Employed person (work away from home) 1 15 24

Retired single person 1 23 24 Employed or self employed couple (at least 1 person works away from home)

2 20 24

Retired couple 2 24 24

Families (All categories, i.e. working, not working, etc.)

3.73 (assume

4 in modelling)

21 24

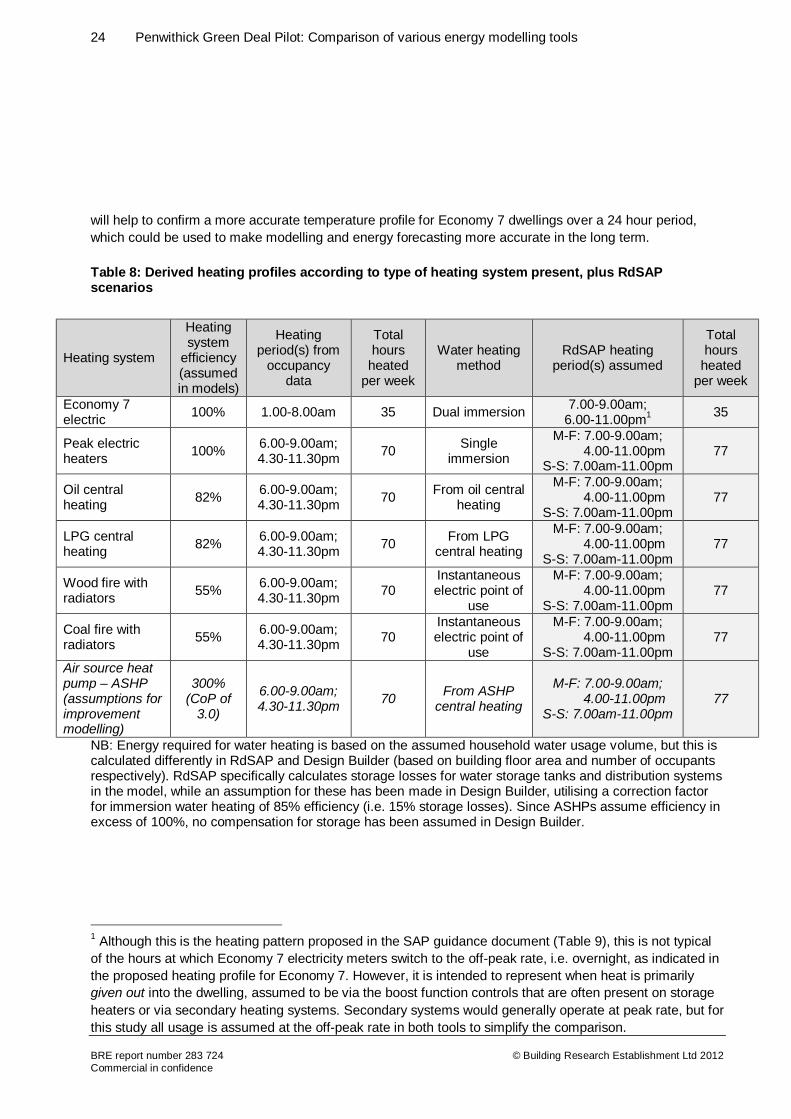

Interestingly, although households of different occupancy patterns spend different periods of time at home, the heating profiles of the dwellings were more dependent on the type of heating system/ fuel present. Additionally, nearly all households used the same heating patterns on weekends as they do during week days. Hence, heating patterns were derived depending on the key heating systems present across the dwellings, resulting in the profiles given in Table 8. For comparison, the default heating profiles from RdSAP are also shown in the table. (NB: The RdSAP assumptions in the table apply to the whole house except for the living area. It is assumed that in all cases the living area is heated to 21°C between the hours of 7.00-9.00am and 4.00-11.00pm on week days and 7.00am-11.00pm on weekends.)

While SAP assumes a two zone heating model, with the living room heated to 21°C and the rest of the house to 18°C, it is more common for households to set a ‘whole house’ temperature throughout, rather than differentiating between rooms. Design Builder allows the user to set thermostat set point temperatures for each zone/ room of a building and to vary the times of the day that the system is on. However, for all heating systems apart from Economy 7, it has been assumed that the whole dwelling is heated to 20°C during the hours of operation of the heating system, following feedback from the household surveys. While not significantly different to the RdSAP assumptions, this does introduce a variation of 7 heating hours per week at the respective temperatures.

The ‘preferred temperature’ in a dwelling with Economy 7 storage heaters is somewhat more difficult to determine as there is limited occupant control. The house will likely be over heated to an extent overnight while the storage heaters are charging using off peak electricity, but the house will then cool gradually throughout the day until the cycle repeats. RdSAP makes assumptions about when heat is delivered in the home as indicated in Table 8. However, simply assuming electrical heating for 7 hours at similar zone temperatures of 21°C and 18°C in Design Builder gives very unrealistic results at it does not take into account the inevitably increased temperature in the home that would be experienced overnight. For the purposes of this modelling, it is assumed in Design Builder that equivalent zone temperatures to SAP are delivered (i.e. 21°C in the living room and 18°C in the rest of the house) across an entire day (i.e. maintained for 24 hours). As will be seen later in Table 10, this provides comparable results to RdSAP’s assumptions relative to the occupancy rate. Future feedback from the in-use monitoring of pilot properties

24 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

will help to confirm a more accurate temperature profile for Economy 7 dwellings over a 24 hour period, which could be used to make modelling and energy forecasting more accurate in the long term.

Table 8: Derived heating profiles according to type of heating system present, plus RdSAP scenarios

Heating system

Heating system

efficiency (assumed in models)

Heating period(s) from

occupancy data

Total hours

heated per week

Water heating method

RdSAP heating period(s) assumed

Total hours

heated per week

Economy 7 electric 100% 1.00-8.00am 35 Dual immersion 7.00-9.00am;

6.00-11.00pm1 35

Peak electric heaters 100% 6.00-9.00am;

4.30-11.30pm 70 Single immersion

M-F: 7.00-9.00am; 4.00-11.00pm

S-S: 7.00am-11.00pm 77

Oil central heating 82% 6.00-9.00am;

4.30-11.30pm 70 From oil central heating

M-F: 7.00-9.00am; 4.00-11.00pm

S-S: 7.00am-11.00pm 77

LPG central heating 82% 6.00-9.00am;

4.30-11.30pm 70 From LPG central heating

M-F: 7.00-9.00am; 4.00-11.00pm

S-S: 7.00am-11.00pm 77

Wood fire with radiators 55% 6.00-9.00am;

4.30-11.30pm 70 Instantaneous electric point of

use

M-F: 7.00-9.00am; 4.00-11.00pm

S-S: 7.00am-11.00pm 77

Coal fire with radiators 55% 6.00-9.00am;

4.30-11.30pm 70 Instantaneous electric point of

use

M-F: 7.00-9.00am; 4.00-11.00pm

S-S: 7.00am-11.00pm 77

Air source heat pump – ASHP (assumptions for improvement modelling)

300% (CoP of

3.0)

6.00-9.00am; 4.30-11.30pm 70 From ASHP

central heating

M-F: 7.00-9.00am; 4.00-11.00pm

S-S: 7.00am-11.00pm 77

NB: Energy required for water heating is based on the assumed household water usage volume, but this is calculated differently in RdSAP and Design Builder (based on building floor area and number of occupants respectively). RdSAP specifically calculates storage losses for water storage tanks and distribution systems in the model, while an assumption for these has been made in Design Builder, utilising a correction factor for immersion water heating of 85% efficiency (i.e. 15% storage losses). Since ASHPs assume efficiency in excess of 100%, no compensation for storage has been assumed in Design Builder.

1 Although this is the heating pattern proposed in the SAP guidance document (Table 9), this is not typical of the hours at which Economy 7 electricity meters switch to the off-peak rate, i.e. overnight, as indicated in the proposed heating profile for Economy 7. However, it is intended to represent when heat is primarily given out into the dwelling, assumed to be via the boost function controls that are often present on storage heaters or via secondary heating systems. Secondary systems would generally operate at peak rate, but for this study all usage is assumed at the off-peak rate in both tools to simplify the comparison.

25 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

4.3 Standardised dwelling models

For each of the key dwelling construction types, an example house was selected from those within the pilot scheme to use as a generic base model. Although key parameters such as the heating system will be varied in order to run comparable scenarios, by selecting a real dwelling it will be possible to compare at least one of the scenarios per house with the real in-use monitoring data obtained later in the project. Dwellings were selected with a mid-range floor area compared to others of the same construction type that were due to receive major measures, i.e. EWI or ASHPs.

From the initial Property Selection report, it was concluded that EWI should be prioritised for solid wall properties and for Cornish properties at ground floor level. For cavity wall and timber hybrid dwellings, a fuel switch to an ASHP was deemed appropriate for properties currently served by a relatively inefficient (<80%) LPG boiler, those with wood or coal fires as the main heating system or dwellings using only portable electric heaters. A switch from Economy 7 storage heaters or oil central heating to an ASHP was not considered economical, so these have not been considered in this study. This section therefore looks at the occupancy impacts of these scenarios:

• Solid wall/ Cornish dwellings (Ground floor) à EWI

• Cavity/ Timber hybrid dwellings à ASHP

A comparison was again carried out in RdSAP, but this time fixing elemental U values to ensure they matched up with the modelling carried out in the Design Builder software, as shown in Table 9. It should be noted that despite standardising the U values across the two tools, RdSAP still makes assumptions for other aspects, such as the living room fraction and the window areas. Additionally, to allow comparison of the Design Builder results with RdSAP, climate data for the East Pennines was selected for this modelling to correspond with the default assumptions used in RdSAP. Section 4.6 discusses the implications of different climate data sets on the modelling.

It should be noted that each of these scenarios assumes that the house is fully heated during the heating periods, whereas in reality householders may not heat all rooms or at least not to the same extent, which would affect the overall heating cost assumptions and therefore the savings assumed.

26 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

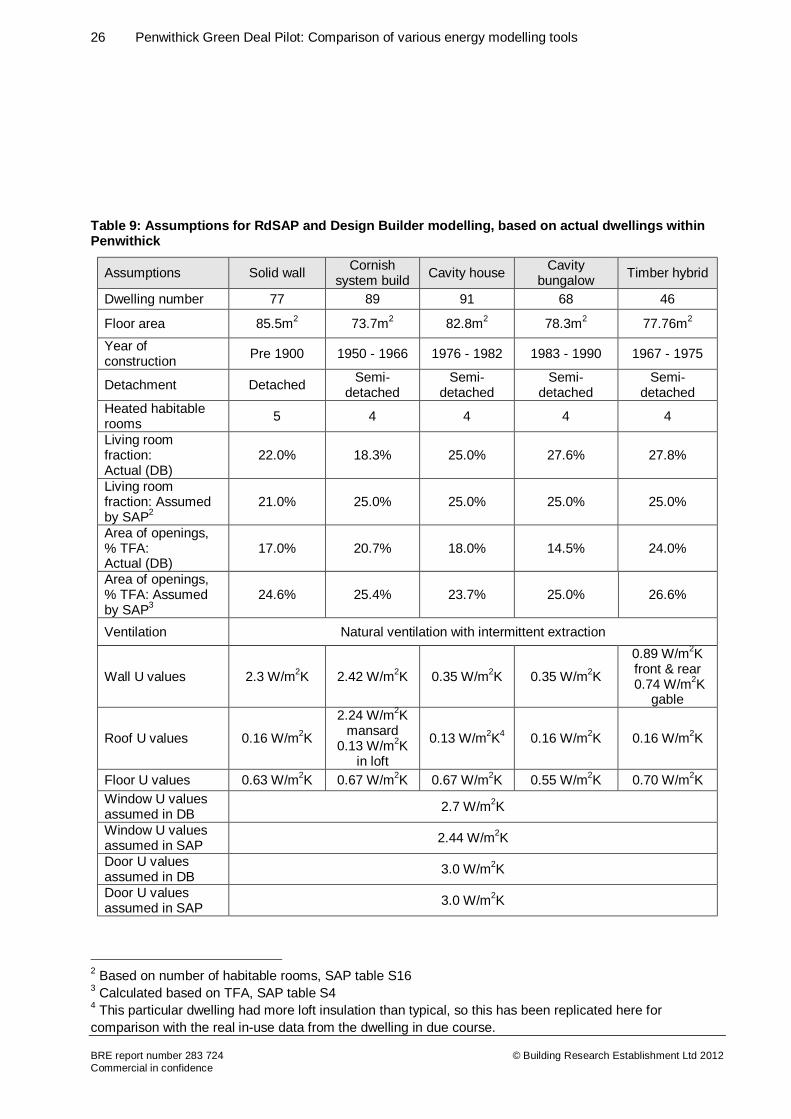

Table 9: Assumptions for RdSAP and Design Builder modelling, based on actual dwellings within Penwithick

Assumptions Solid wall Cornish system build Cavity house Cavity

bungalow Timber hybrid

Dwelling number 77 89 91 68 46

Floor area 85.5m2 73.7m2 82.8m2 78.3m2 77.76m2

Year of construction Pre 1900 1950 - 1966 1976 - 1982 1983 - 1990 1967 - 1975

Detachment Detached Semi-detached

Semi-detached

Semi-detached

Semi-detached

Heated habitable rooms 5 4 4 4 4

Living room fraction: Actual (DB)

22.0% 18.3% 25.0% 27.6% 27.8%

Living room fraction: Assumed by SAP2

21.0% 25.0% 25.0% 25.0% 25.0%

Area of openings, % TFA: Actual (DB)

17.0% 20.7% 18.0% 14.5% 24.0%

Area of openings, % TFA: Assumed by SAP3

24.6% 25.4% 23.7% 25.0% 26.6%

Ventilation Natural ventilation with intermittent extraction

Wall U values 2.3 W/m2K 2.42 W/m2K 0.35 W/m2K 0.35 W/m2K

0.89 W/m2K front & rear

0.74 W/m2K gable

Roof U values 0.16 W/m2K

2.24 W/m2K mansard

0.13 W/m2K in loft

0.13 W/m2K4 0.16 W/m2K 0.16 W/m2K

Floor U values 0.63 W/m2K 0.67 W/m2K 0.67 W/m2K 0.55 W/m2K 0.70 W/m2K Window U values assumed in DB 2.7 W/m2K

Window U values assumed in SAP 2.44 W/m2K

Door U values assumed in DB 3.0 W/m2K

Door U values assumed in SAP 3.0 W/m2K

2 Based on number of habitable rooms, SAP table S16 3 Calculated based on TFA, SAP table S4 4 This particular dwelling had more loft insulation than typical, so this has been replicated here for comparison with the real in-use data from the dwelling in due course.

27 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

4.4 Results of occupancy modelling

NB: Tables including CO2 emissions are included in Annexe A so as not to overwhelm the reader with data. The trends seen here with overall cost savings at different occupancy profiles are mirrored by the CO2 savings as they are calculated from the same kWh energy usage assumptions.

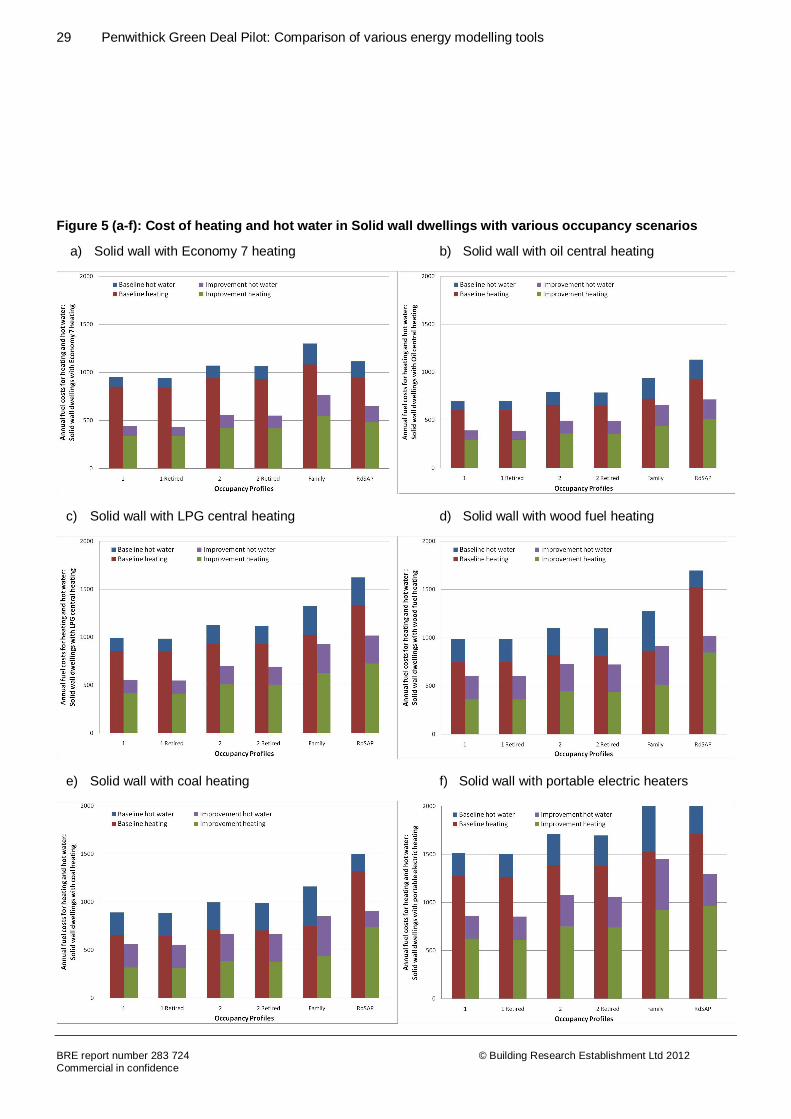

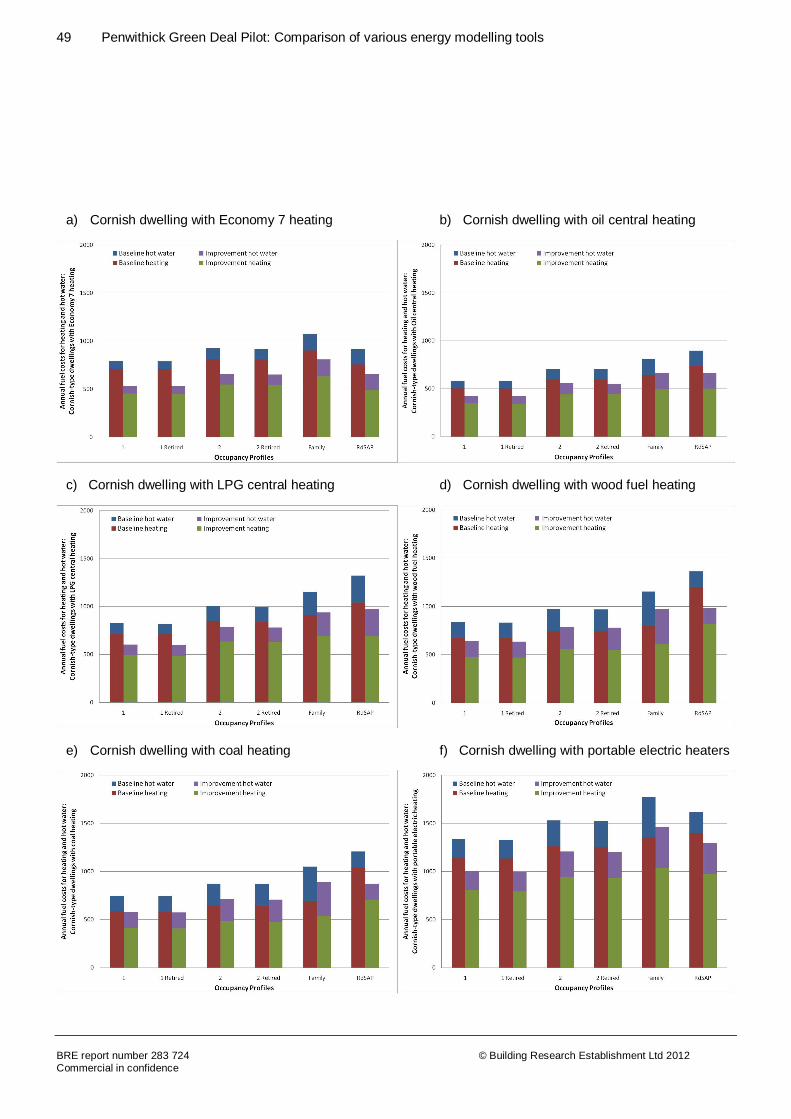

4.4.1 Solid wall dwellings The overall fuel costs for heating and hot water in solid wall properties with various assumed heating system are shown in Table 10 and displayed graphically in Figure 1.

Across all fuel types, the cost estimates from RdSAP are most closely aligned with the higher occupancy profiles in the Design Builder models. SAP calculates an assumption for the occupancy based on the floor area of the building, which in this case would be 2.7 people. It may therefore be expected that the overall energy usage for RdSAP would sit somewhere between that of the 2 person and 4 person (Family) occupancy scenarios. This is true for the Economy 7 scenario and to a less obvious extent the scenario with portable electric heaters. However, in all other cases the overall energy use in RdSAP is greater than all the Design Builder scenarios. This is likely to be mostly a result of RdSAP assuming slightly longer heating periods per week and because the proportion of windows assumed is somewhat larger in RdSAP than in the actual building. (This effect is evidently being masked due to the 24 hour heating scenario assumed in Design Builder for Economy 7. The factors influencing portable electric heaters are discussed below.)

The hot water forecasts in RdSAP form a smaller proportion of the overall energy demand compared to the Family profile scenarios in Design Builder. This is because RdSAP calculates the water usage based on the floor area of the dwelling, while Design Builder calculates the water usage based on the specified number of occupants.

The overall fuel cost forecast by Design Builder for heating and hot water generally increases as the number of occupants within the dwelling rises, even though the dwellings are assumed to be heated to the same extent. This is because the ventilation rate in the Design Builder models is determined ‘per person’ (at a rate of 10 litres/second per person) so increases with the number of occupants, which in turn increases the heating energy demand to compensate for the heat lost via ventilation. (Within SAP, the ventilation rate is calculated according to the number of chimneys, vents and fans present and so is effectively independent of the occupancy level.) Additionally, the energy required for hot water also increases per person as discussed above.

It is of note that while overall fuel costs generally increase with higher occupancy, the fuel cost savings actually decrease, since it is assumed that there are more internal gains in a larger household that will offset the need for heating to some extent, thus consequently reducing the savings that can be realised by improvement measures (assuming ventilation rates and hot water demand remain constant).

Beyond these occupant-related factors (ventilation rate, hot water usage), it should be remembered that each of the occupancy profiles, in addition to having different numbers of occupants, also assume different hours of occupancy within the dwelling. Hence, the overall fuel costs and savings also reflect the influence of internal gains per person depending on the average time spent in the dwelling.

28 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

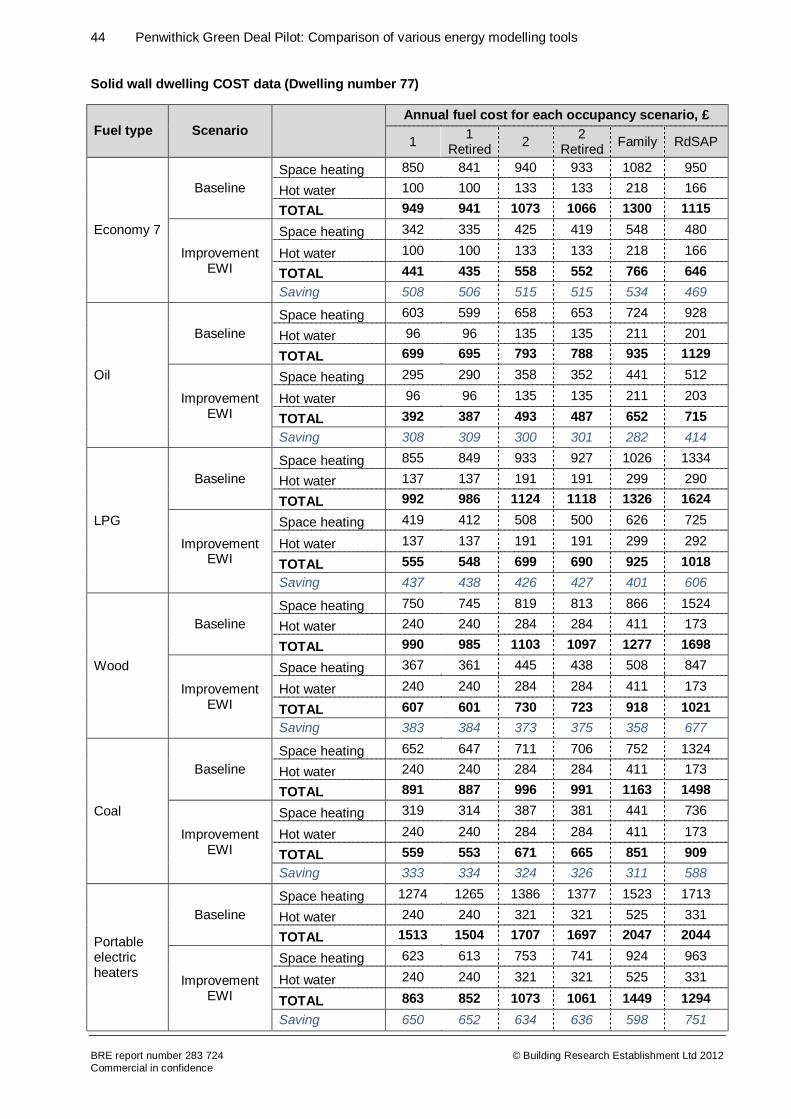

Table 10: Solid wall dwellings (Dwelling number 77)

Fuel type Scenario

Annual fuel cost for each occupancy scenario, £

1 1 Retired 2 2

Retired Family RdSAP

Economy 7

Baseline Space heating 850 841 940 933 1082 950

Hot water 100 100 133 133 218 166

TOTAL 949 941 1073 1066 1300 1115

Improvement EWI

Space heating 342 335 425 419 548 480

Hot water 100 100 133 133 218 166

TOTAL 441 435 558 552 766 646 Saving 508 506 515 515 534 469

Oil

Baseline Space heating 603 599 658 653 724 928

Hot water 96 96 135 135 211 201

TOTAL 699 695 793 788 935 1129

Improvement EWI

Space heating 295 290 358 352 441 512

Hot water 96 96 135 135 211 203

TOTAL 392 387 493 487 652 715 Saving 308 309 300 301 282 414

LPG

Baseline Space heating 855 849 933 927 1026 1334

Hot water 137 137 191 191 299 290

TOTAL 992 986 1124 1118 1326 1624

Improvement EWI

Space heating 419 412 508 500 626 725

Hot water 137 137 191 191 299 292

TOTAL 555 548 699 690 925 1018 Saving 437 438 426 427 401 606

Wood

Baseline Space heating 750 745 819 813 866 1524

Hot water 240 240 284 284 411 173

TOTAL 990 985 1103 1097 1277 1698

Improvement EWI

Space heating 367 361 445 438 508 847

Hot water 240 240 284 284 411 173

TOTAL 607 601 730 723 918 1021 Saving 383 384 373 375 358 677

Coal

Baseline Space heating 652 647 711 706 752 1324

Hot water 240 240 284 284 411 173

TOTAL 891 887 996 991 1163 1498

Improvement EWI

Space heating 319 314 387 381 441 736

Hot water 240 240 284 284 411 173

TOTAL 559 553 671 665 851 909 Saving 333 334 324 326 311 588

Portable electric heaters

Baseline Space heating 1274 1265 1386 1377 1523 1713

Hot water 240 240 321 321 525 331

TOTAL 1513 1504 1707 1697 2047 2044

Improvement EWI

Space heating 623 613 753 741 924 963

Hot water 240 240 321 321 525 331

TOTAL 863 852 1073 1061 1449 1294 Saving 650 652 634 636 598 751

29 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

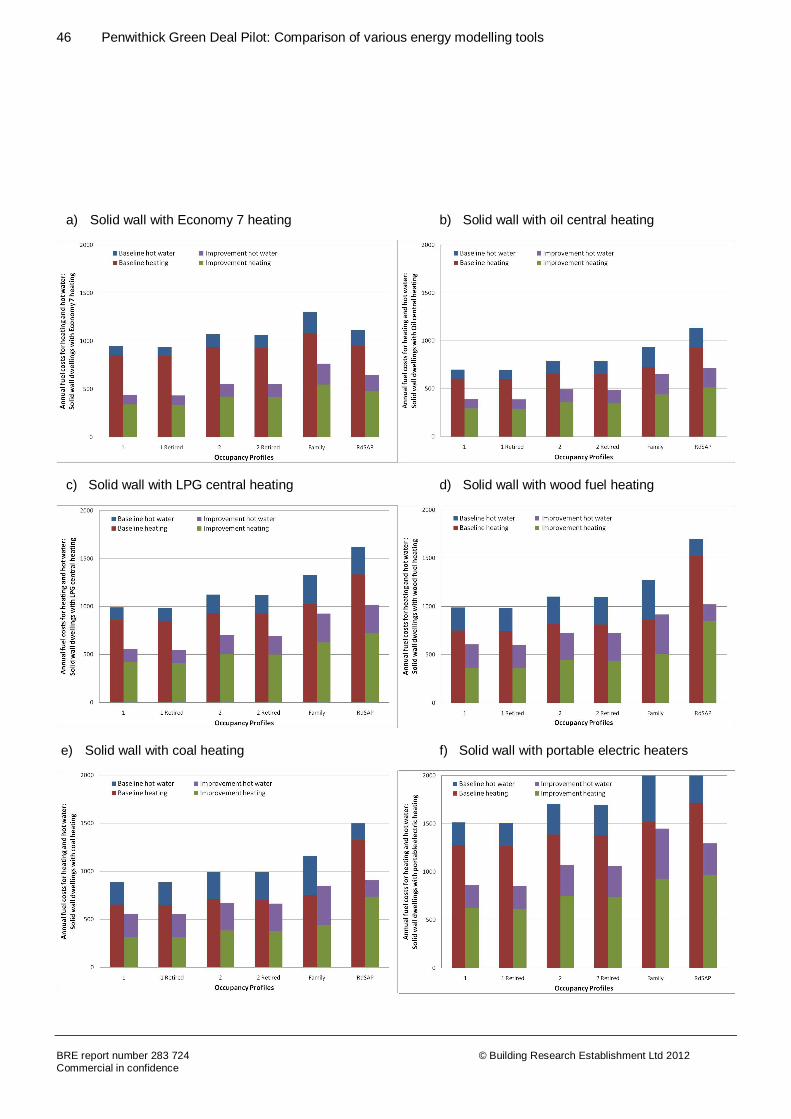

Figure 5 (a-f): Cost of heating and hot water in Solid wall dwellings with various occupancy scenarios

a) Solid wall with Economy 7 heating b) Solid wall with oil central heating

c) Solid wall with LPG central heating d) Solid wall with wood fuel heating

e) Solid wall with coal heating f) Solid wall with portable electric heaters

30 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Economy 7 heating

The solid wall dwelling model with Economy 7 heating is the only scenario for which Design Builder forecasts a higher cost saving across all occupancy profiles than RdSAP. In all other cases, RdSAP suggests a higher saving. Ocean Services’ price for EWI for this particular dwelling was £11,585, so in each case the savings with Economy 7 are likely to be just insufficient to cover the cost of External Wall Insulation within 20 years (at current prices, not taking into account interest rates on loans). However if prices for an equivalent dwelling were to drop to ~£10,000, the EWI would become more financially viable with Economy 7 heating.

Portable electric heaters

Despite the fact that portable electric heaters have been assumed to use the same heating profile as the other fuel types (with the exception of Economy 7 heating), the overall fuel cost from RdSAP falls just below that of the family Design Builder profile scenario while for other fuels RdSAP experienced a higher relative cost. Although it is accepted that RdSAP aims to heat the living area to 21°C and the rest of the dwelling to 18°C, Table 9 within the SAP guidance actually dictates that the latter temperature is calculated based on the Heat Loss Parameter (HLP) of the building with assumptions for the controllability and response time of the heating system in question. SAP Table 9 is copied here for reference.

Following through the guidance in the SAP document, portable electric heaters are assumed to have Control Type 2, while the other heating fuels (with the exception of Economy 7 heating) are assumed to have Control Type 1. The HLP in the base case RdSAP model for the solid wall properties is 4.5, hence the target temperature with Control Type 1 = 18.75°C, while the target temperature with Control Type 2 = 16.88°C. Since the dwelling with portable electric heaters is assumed to be heated to this lower

31 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

temperature, this would account for why in this case the RdSAP scenario falls lower than the family Design Builder scenario.

RdSAP estimates higher savings from the installation of EWI with portable electric heaters than all the Design Builder profile models. This may therefore mean that householders would not achieve the savings indicated by RdSAP. However, even the occupancy scenario with the lowest savings forecast by Design Builder (Family) should be sufficiently high for it to be possible to cover the cost of installing EWI within the anticipated 20 year period (in excess of £11,960 at current prices, not taking into account interest rates on loans), assuming the dwelling is fully heated to the extent assumed in this modelling.

Other fuel types

As mentioned above, in the other non-electric scenarios the baseline cost is higher than each of the Design Builder baseline occupancy scenarios. The cost savings from RdSAP are also somewhat higher than the Design Builder occupancy profile models, since theoretically there is more heating energy to be saved by the installation of new insulation measures. However, the modelled savings drop to as little as £5640 over 20 years for a family with oil central heating compared to the RdSAP scenario of £8280 over 20 years (although this would also actually be an insufficient saving to make EWI viable at current installation prices). This could be problematic for many households, since it would be likely that they would not achieve the forecast savings from RdSAP in their energy bills, which could influence the ability to pay back the cost of EWI within an acceptable time period (~20 years) without additional funds/ grants.

4.4.2 Cornish-type dwellings The overall fuel costs and CO2 emissions for heating and hot water in Cornish-type properties with various assumed heating system are presented in Annexe A.

The trends seen with the Cornish property examples are generally the same as with the solid wall dwellings, as the same factors will have affected each model. However, the savings are proportionally lower, as only the ground floor is assumed to receive EWI improving the U value to 0.3 W/m2K as was the case with the solid wall dwellings, while the first floor is assumed to be improved from a U value of 2.24 W/m2K to 1.6 W/m2K by applying insulation within the mansard structure. The capital cost of the EWI is therefore proportionally reduced to £4,367 for this particular dwelling example, suggesting the Green Deal may be viable over 20 years for Economy 7 and Portable electric heaters.

However, similar over-estimates by RdSAP are witnessed for the other fuel types considered, again most likely to be due to the different assumptions in heating periods and differences in window areas assumed between the models, so households may not achieve the forecast savings from RdSAP in their energy bills, which could influence the ability to pay back the cost of EWI within an acceptable time period (~20 years) without additional funds/ grants.

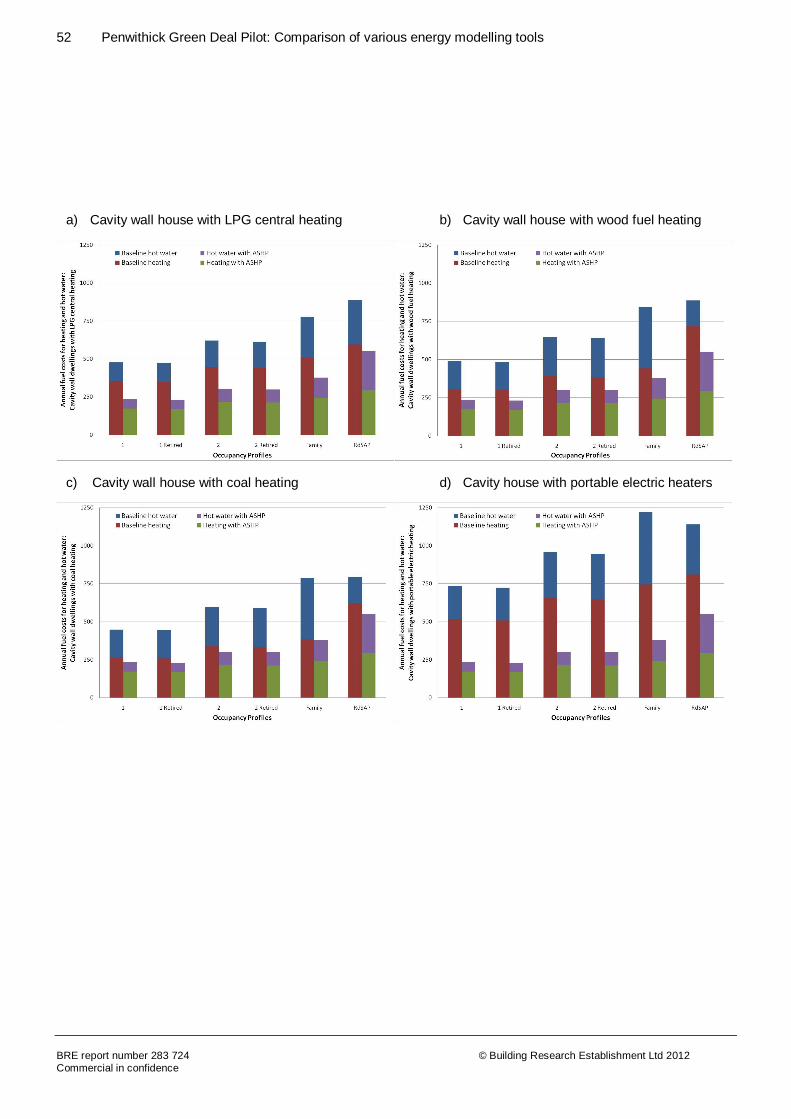

4.4.3 Cavity wall houses The overall fuel costs for heating and hot water in cavity wall properties with various assumed heating system are shown in Table 11 and displayed graphically in Figure 2.

In all cases, the RdSAP scenario is of a similar overall cost to the highest Design Builder occupancy profile (family), although in the majority of cases it assumes a higher cost, with portable electric heaters it actually drops lower than the Design Builder family scenario due to the reasons mentioned in Section 4.4.1. Also, the hot water makes a far higher contribution to the overall fuel cost than seen with the solid wall and

32 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Cornish-type properties, as the water heating requirement will be similar across both construction types but the baseline energy bills are now somewhat lower due to the improved baseline U values of the (insulated) cavity wall dwelling.

Table 11: Cavity wall houses (Dwelling number 91)

Fuel type Scenario

Annual fuel cost for each occupancy scenario, £

1 1 Retired 2 2

Retired Family RdSAP

LPG

Baseline Space heating 354 347 449 441 508 596

Hot water 124 124 172 172 270 292

TOTAL 478 471 621 614 778 888

Improvement EWI

Space heating 173 169 217 213 243 294

Hot water 61 61 86 86 134 256

TOTAL 234 231 302 298 378 549 Saving 244 240 319 315 400 338

Wood

Baseline Space heating 384 378 358 352 466 767

Hot water 174 174 243 243 381 168

TOTAL 558 552 601 595 847 934

Improvement EWI

Space heating 215 212 201 197 257 352

Hot water 58 58 81 81 127 253

TOTAL 273 270 282 278 384 604 Saving 285 282 319 316 464 330

Coal

Baseline Space heating 265 260 338 332 385 622

Hot water 184 184 257 257 403 171

TOTAL 449 444 595 589 788 793

Improvement EWI

Space heating 173 169 217 213 243 294

Hot water 61 61 86 86 134 256

TOTAL 234 231 302 298 378 549 Saving 215 213 293 291 410 244

Portable electric heaters

Baseline Space heating 518 508 657 646 746 812

Hot water 216 216 302 302 474 329

TOTAL 734 724 959 948 1220 1140

Improvement EWI

Space heating 173 169 217 213 243 294

Hot water 61 61 86 86 134 256

TOTAL 234 231 302 298 378 549 Saving 500 494 657 650 842 591

33 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

Figure 6 (a-d): Cost of heating and hot water in Cavity wall houses with various occupancy scenarios

a) Cavity wall with LPG central heating b) Cavity wall with wood fuel heating

c) Cavity wall with coal heating d) Cavity wall with portable electric heaters

For wood and coal heating systems it is assumed that the hot water is met by instantaneous electric point of use systems. Due to the relative cost per kWh of standard rate electricity compared to coal and wood, the resulting cost for this hot water heating makes a significant contribution to the overall fuel cost in the baseline cases modelled in Design Builder, as shown in Figure 6b and c. Unlike the EWI improvements, the switch to an ASHP also affects the hot water provision, hence larger savings are now seen in the family scenario than the other profiles as the energy required for hot water heating is proportionately reduced relative to the occupancy assumed in Design Builder. However, RdSAP does not share this trend in hot water cost savings, instead actually causing an increase in water heating costs for the wood and coal heating/ instant point of use electric hot water scenarios. Evidently RdSAP deems it more efficient to utilise instant point of use hot water than to maintain a storage tank of hot water with the ASHP as a result of its method of calculating the hot water consumption as a function of the building’s floor area.

34 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

The combination of these factors could make a significant impact on the potential viability of ASHPs under the Green Deal. Ocean Services’ price for the installation of an ASHP central heating system for this particular dwelling was £9,853. None of the occupancy profiles using LPG suggest that this cost could be recovered within 20 years (at current prices, not taking into account interest rates on loans), with the lowest savings only being capable of recovering approximately half of the necessary amount. Conversely, all occupancy profiles using peak electric heating could recover the up-front cost within the same period, assuming the dwelling is fully heated by this method.

Due to the relatively cheap price of coal and wood fuel, the data suggests that none of the occupancy profiles with these fuels would be likely to find an ASHP viable under the Green Deal. However, it should be emphasised that the improved user control and comfort likely to be derived from an ASHP central heating system compared to the labour intensive management of open fires is likely to carry a ‘value’ to households in itself.

Considering additional factors are likely to eat into the savings forecast here (i.e. interest rates on Green Deal loans, comfort taking, etc.), the data suggest that the capital cost of ASHPs would have to be considerably cheaper before they became a viable option under the Green Deal for the majority of modelled cavity wall dwelling scenarios.

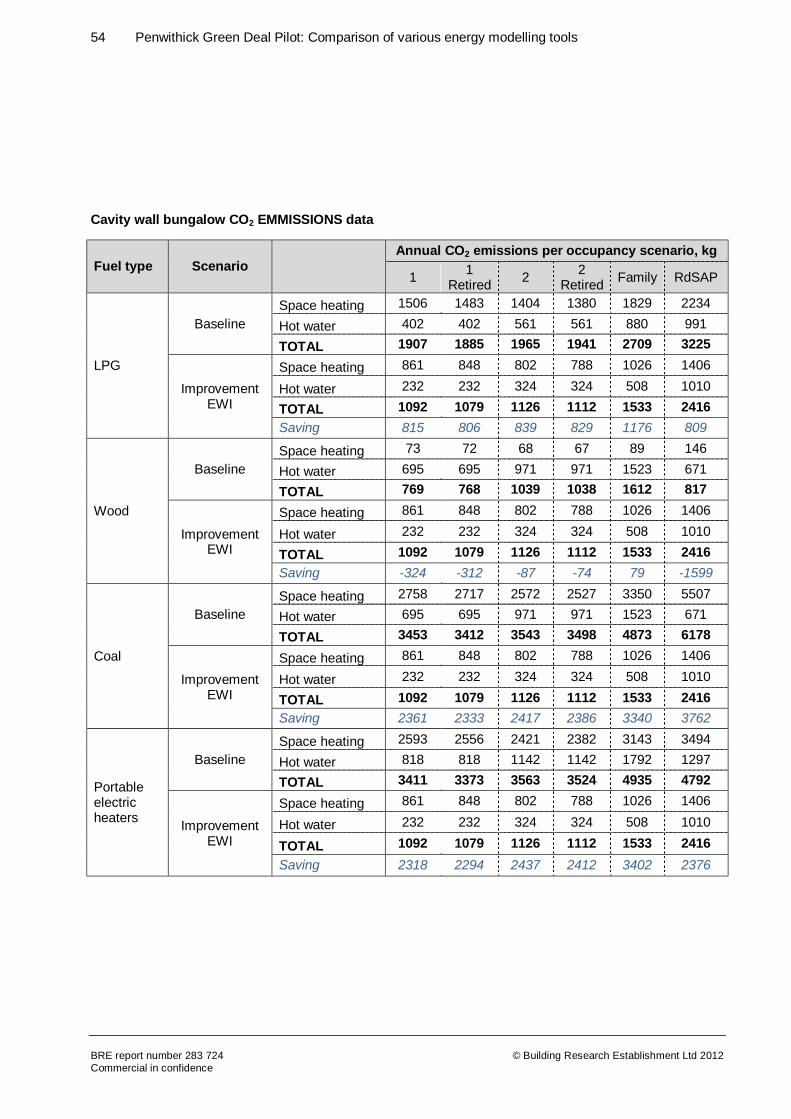

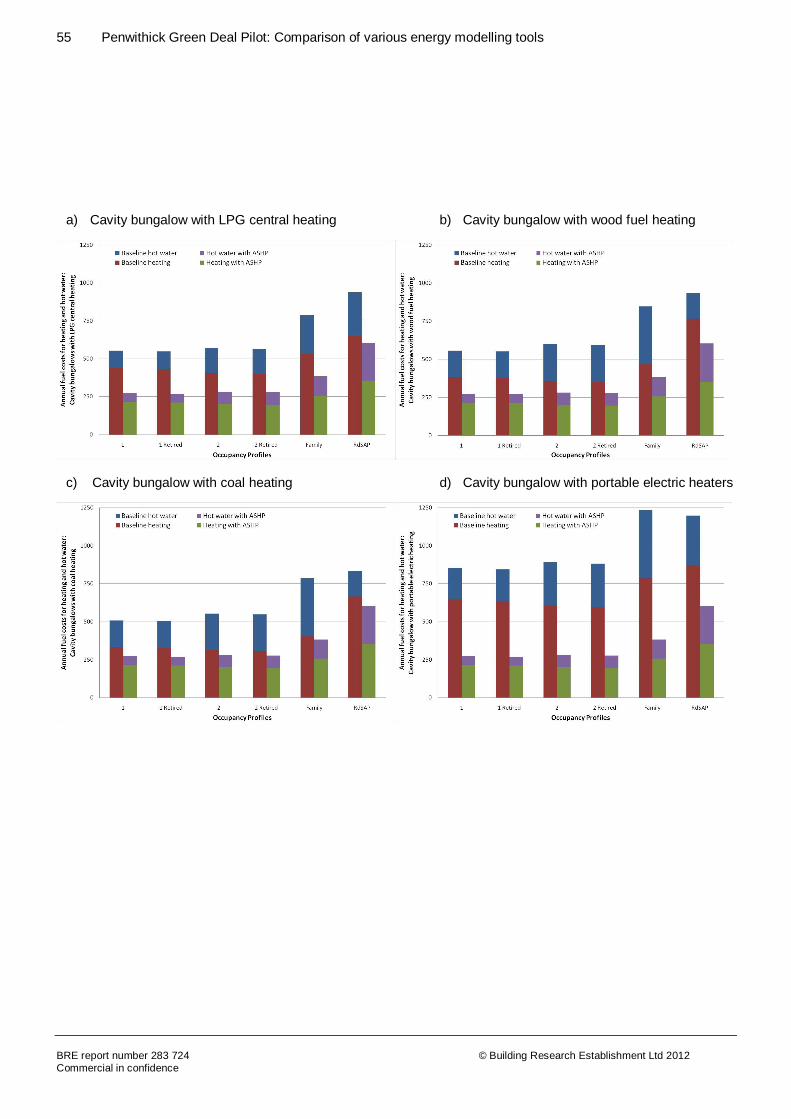

4.4.4 Cavity bungalows The overall fuel costs and CO2 emissions for heating and hot water in cavity bungalows with various assumed heating system are presented in Annexe A.

The cavity wall bungalow forecasts higher running costs across the majority of the modelled scenarios than the cavity walled house, with the exception of the 2 person occupancy profiles. In the bungalow model, the ventilation losses are only marginally higher for 2 people than they are for 1 for the given building volume, hence due to the higher occupancy gains for 2 people the overall heating demand is actually lower. This trend is not seen in any of the other house construction types assessed as the higher occupancy gains are overshadowed by the higher ventilation losses for the larger volume buildings.

Aside from this anomaly, the reason for the otherwise common increase in energy demand in the bungalow is most likely due to its more inefficient ‘form factor’. The form factor of a building is represented by the ratio of its heat loss surfaces to the floor area. The floor area of the bungalow is only slightly smaller than the overall floor area of the house, while the ratio of heat loss surfaces to floor area is higher (2.10 in the house, 2.82 in the bungalow). This means that proportionally more heat will be lost relative to the size of the building.

The general trends seen with the cavity wall house are also experienced with the bungalow, including the largest cost savings from switching to an ASHP being experienced by the family occupancy profile, largely as a result of the saving assumed in hot water provision. None of the occupancy profiles using LPG, wood or coal suggest that the capital cost of the ASHP could be recovered within 20 years (at current prices, not taking into account interest rates on loans). However, all occupancy profiles using peak electric heating could recover these costs within that period, assuming the dwelling is fully heated by this method. Overall, the data suggest that the capital cost of ASHPs would have to be considerably cheaper before they became a viable option under the Green Deal for the majority of modelled cavity wall bungalow scenarios.

35 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

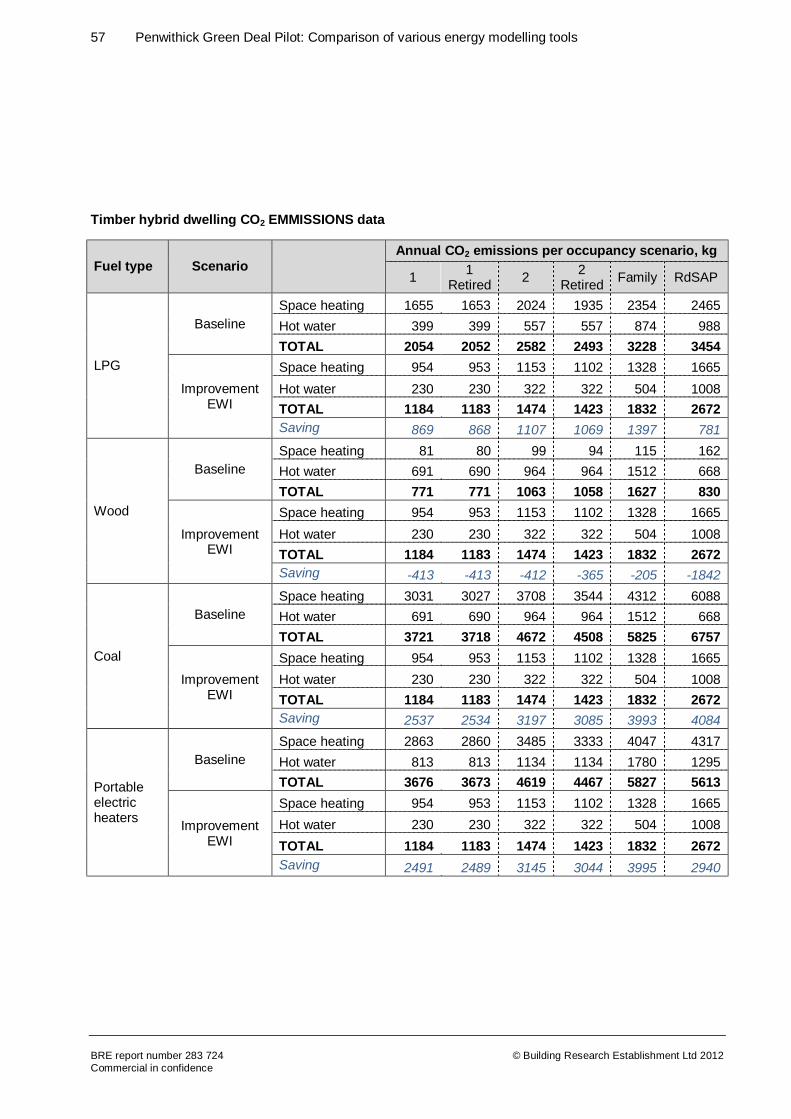

4.4.5 Timber hybrid dwellings The overall fuel costs and CO2 emissions for heating and hot water in timber hybrid properties with various assumed heating system are presented in Annexe A.

The trends seen with the Timber hybrid property examples are generally the same as with the cavity wall house, as the same factors will have affected each model. However, the overall energy costs and therefore cost savings are proportionally higher due to the U values for the timber frame dwellings being higher (0.89 W/m2K front and rear, 0.74 W/m2K gable) than the cavity dwellings (0.35 W/m2K).

The family scenarios are most likely to find the switch to an ASHP viable in timber hybrid dwellings, however with cheaper fuels such as coal it may not quite pay back within an acceptable time period (within ~20 years). All occupancy profiles using peak electric heating could recover these costs within that period, assuming the dwelling is fully heated by this method. The remaining, lower occupancy scenarios and the RdSAP forecasts suggest that the switch to an ASHP may not be financially viable in the timber hybrid dwellings without the contribution of some sort of additional grand/ funding.

4.5 Section summary: RdSAP vs Design Builder occupancy assessment

Key areas where each of the tools examined may influence the results differently will be in the calculation of the energy demand for hot water and the heat loss through ventilation, as these are calculated by different methodologies in each tool. Analysis of in-use data in due course may help to resolve which calculation method is more representative of actual performance. However, the findings reported in this section do not intend to suggest that one modelling tool is more ‘right’ than the other, as they will both be carrying out ‘correct’ calculations based on the input parameters for each model. Instead the comparison of tools serves to demonstrate that the extent to which you can influence the model and accurately align it with genuine occupancy and behavioural patterns can in some cases significantly influence the viability of the more costly potential Green Deal measures.

The occupancy scenarios derived from the surveys for this analysis are predicated on householders having a true understanding of how they use their heating system and when they are at home. But some households may actually have such varied behaviours that they would not correspond to their ‘typical profile’, which would obviously influence their payback potential. Educating householders about the potential range of scenarios (particularly once it has been verified in due course by comparing with real in-use data from pilot households) should help them make more informed decisions about their potential paybacks.

From this modelling, it would appear that typically households with electric heating (either Economy 7 or peak rate portable electric heaters), regardless of their occupancy would be most likely to find EWI viable under a Green Deal finance mechanism, whereas households with other heating fuel systems may not achieve the savings forecast by a ‘typical’ RdSAP analysis.

It would appear that ASHPs would need to be somewhat cheaper than in this study for them to be considered viable under the Green Deal, although households with only portable electric heaters at present may find it feasible if they fully heat their home by this means currently (which may be considered relatively unlikely) and/ or the occupancy necessitates a relatively high level of hot water usage.

Once the Green Deal Occupancy Assessment tool is able to provide comparisons for some of the more unusual measures considered under this pilot, it will be interesting to compare its cost estimates to those

36 Penwithick Green Deal Pilot: Comparison of various energy modelling tools

BRE report number 283 724 Commercial in confidence

© Building Research Establishment Ltd 2012

from Design Builder and then subsequently with real in-use data to see whether significant differences arise from using a steady state (SAP) versus a dynamic simulation model (Design Builder).

4.6 Consideration of regional climate data