pedro francke ballvé

TRANSCRIPT

Pedro Francke BallvéMinister of Economy and Finance

September 2021

COVID StatusI

2

Table of Contents

Public Finance StatusIIPublic and Private InvestmentsIIIFiscal Strategy IVBudget, Indebtedness and Finance BalanceVESG Framework VI

COVID StatusI

3

Table of Contents

Public Finance StatusIIPublic and Private InvestmentsIIIFiscal Strategy IVBudget, Indebtedness and Finance BalanceVESG Framework VI

4

Health indicators have improved in the last few months

Cumulative evolution of COVID-19 vaccine doses administered and received2

Peru: excess deaths1

(Number of people, weekly cumulative)

1/ To Sep.15, 2021. 2/ Updated to Sep. 15, 2021.Source: Minsa..

Deaths in 20190

200

400

600

800

1,000

1,200

1,400

Feb-20 Aug-20 Feb-21 Sep-21

33,134,220

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

Feb-21 Apr-21 Jun-21 Aug-21

Administered doses

Total doses received

Sep-21

5

Gradual reduction of new cases By COVID-19

World: new cases per million1

(7-day moving average)

1/ Updated to Sep. 17, 2021.Source: Our World in Data.

0

200

400

600

800

1000

Jan-20 Apr-20 Jul-20 Oct-20 Dec-20 Mar-21 Jun-21 Sep-21

FranceUnited KingdomUnited StatesIndiaJapanThailandTurkeyMexicoPeru

6

Vaccination rate versus other countries in the region and the world

1/ Updated to Sep. 17, 2021.Source: Our World in Data.

World: Population vaccinated against COVID-19¹ (Percentage of total population by country)

27.019.0

13.731.431.831.3

54.554.4

42.253.1

62.236.1

65.264.963.7

69.573.273.676.3

37.539.8

42.243.2

47.848.6

60.663.763.965.466.467.9

71.472.973.6

75.676.578.1

79.9

PeruThailand

IndiaWorld

MexicoColombiaEcuador

United StatesArgentina

JapanGermany

BrazilUnited Kingdom

ItalyFrance

CanadaChile

UruguaySpain

Fully vaccinated

Partially vaccinated

Loreto

Ucayali

Junín

Lima

Ancash

Cusco

Madre de Dios

Puno

Arequipa

Piura

Huánuco

Pasco

SanMartín

La Libertad

Tacna

Moquegua

Ica

TumbesAmazonas

CajamarcaLambayeque

ApurímacAyacucho

Huancavelica

7

Advances in the vaccination process

Vaccination progress

34% of the total target population (27.4 million people) has been vaccinated with the two doses.

To date, more than 24 million doses have been applied nationwide. 2 million doses last week

More than 12 million doses of vaccines will arrive in September, a record number of arrivals in one month.

In Metropolitan Lima and Callao we are movingforward with the vaccination of over 23-year-olds,and in other regions, we are even moving forward withthe vaccination of over 16-year-olds.

The Vacunafests made it possible to achievesignificant levels of vaccinated population.

30292523201816

Vaccination by age groups1

1/ Updated to Sep. 17, 2021.Source: Minsa.

8

Perú has implemented an important economic plan against COVID-19

Economic measures against COVID-19, 2020-2021(% of GDP)

Between March 2020 and September 2021, Economic measures' Perú are equivalent to 21.6% of GDP (up toSeptember 17th, 2021).

Tax and public spending measures are equivalent to 7.8% of GDP (up to September 17th, 2021).

21.6

0

5

10

15

20

25

30

Advancedeconomies

Perú World Similar creditrating

Emerging Low incomes1

Note: The information for country groups corresponds to the updated data as of June 5th, 2021 published by the IMF.1/ For 2020, it considers the execution of public expenditure and revenue measures. For 2021, it considers the measures approved until September 17th.Source: IMF, MEF.

9Source: MEF.

The current administration has implemented measures to face the effects of the pandemic, but under fiscal responsibility guidelines

Family grants (Yanapay Perú)

• Cash transfers of S/ 350 (USD 85) that will strengthen the national economy and support family incomes.

Trabaja Perú

• Public spending program (mainly public investment) to create temporary jobs.

• “Bono Familiar Habitacional”: subsidies for housingconstruction.

• Acceleration of public investment through resource transfers

Capital transfers

The short-term objective is to reactivate the economy and employment.

COVID StatusI

10

Table of Contents

Public Finance StatusIIPublic and Private InvestmentsIIIFiscal Strategy IVBudget, Indebtedness and Finance BalanceVESG Framework VI

Source: BCRP. 11

Strong external fundamentals

Trade balance(Accumulated last 12 months, million US$)

12,517

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Jan-19 Jun-19 Nov-19 Apr-20 Sep-20 Feb-20 Jul-21

Source: Central Bank 12

Terms of trade and export prices(Annual percent change)

5.4 5.30.7

-0.9

1.85.3 6.3

12.9 15.1 16.020.8 20.3 17.9 19.7 21.8

18.222.4

18.1

9.6

-10.2

47.6

31.9

-20

-10

0

10

20

30

40

50

60

Jan-20 Mar-20 May-20 Jul-20 Sep-20 Nov-20 Jan-21 Mar-21 May-21 Jul-21

Terms of trade

Export prices

Strong external fundamentals

Copper1

(¢US$/lb.)

131/ To Sep.16, 2021Source: Bloomberg.

Gold1

(US$/oz.tr.)Zinc1

(¢US$/lb.)

Strong Commodity Prices

4271 755

138

0

100

200

300

400

500

Jan-90 Jul-00 Feb-11 Sep-210

500

1,000

1,500

2,000

2,500

Jan-90 Jul-00 Feb-11 Sep-210

50

100

150

200

250

Jan-90 Jul-00 Feb-11 Sep-21

141/ To Sep.17, 2021Source: Central Bank

Exchange rate1

(Index, Dec-08=100)

50

100

150

200

250

300

Ene-07 Set-08 May-10 Ene-12 Set-13 May-15 Ene-17 Set-18 May-20

Brazil Chile Colombia Mexico Peru

The exchange rate was one of the most stable compared to other regional peers in the last decades

International Reserves, September 20211

(% of GDP)

1/ Considers the September advance for Mexico, Brazil, Chile and Peru, and the August result for Colombia. The percentage of GDP is calculated with information on Central Banks international reserves divided by the LatinFocus GDP projection for 2021, and in the case of Peru by the MEF GDP projection.Source: Central Banks. 15

The external position remains strong due to the accumulation of International Reserves

35.1

23.019.5

17.1 15.7

0

5

10

15

20

25

30

35

40

Peru Brazil Colombia Chile Mexico

16

Inflation(Annual percent change)

Interest rate(Percentage)

(*) Central Bank: macroeconomic expectations survey, Aug-21.Source: Central Bank

1.0

-2.07

-3

-1

1

3

5

Aug-17 Jun-18 Apr-19 Feb-20 Dec-20

Nominal interest rateReal interest rate

Sep-21

Prudent monetary policy management

Inflation target2.9

2.21.9 2.0

3.7

2.6

0.0

1.0

2.0

3.0

4.0

5.0

2010-19 2018 2019 2020 2021* 2022*

Source: Central Banks 17

Strong and fast recovery in LATAM

Mexico: IGAEColombia: ISE Chile: Imacec

85.1

104.4

80

85

90

95

100

105

110

Jan-19 Jun-19 Nov-19 Apr-20 Sep-20 Feb-21 Jul-21

86.7

101.8

85

90

95

100

105

Jan-19 Jun-19 Nov-19 Apr-20 Sep-20 Feb-21 Jul-21

77.0

102.1

75

80

85

90

95

100

105

Jan-19 Jun-19 Nov-19 Apr-20 Sep-20 Feb-21 Jul-21

74.4

97.9

70

75

80

85

90

95

100

105

110

Jan-19 Jun-19 Nov-19 Apr-20 Sep-20 Feb-21 Jun-21

78.9

97.5

75

80

85

90

95

100

105

Jan-19 Jun-19 Nov-19 Apr-20 Sep-20 Feb-21 Jun-21

59.0

99.4

50

60

70

80

90

100

110

Jan-19 Jun-19 Nov-19 Apr-20 Sep-20 Feb-21 Jul-21

Argentina: EmeaBrazil: IBCPeru: BCRP

Seasonally adjusted indices of economic activity in the region(Jan-20=100)

18

Latin America’s GDP(Annual percent change)

2021¹

1/ MEF forecast for Peru are considered. LAC: Latin America and the Caribbean.Source: IMF, Latinfocus (september 2021), MEF forecast

The Peruvian economy will continue to lead Latin America's economic growth in the next years

2022-2025¹

2.8

3.3

4.2

5.0

5.9

6.0

6.9

6.9

9.0

10.5

Uruguay

Ecuador

Paraguay

Brazil

Mexico

LAC

Colombia

Argentina

Chile

Peru

2.2

2.3

2.5

2.5

2.6

2.8

2.9

3.4

3.7

4.3

Brazil

Ecuador

Argentina

Mexico

LAC

Chile

Uruguay

Colombia

Paraguay

Peru

Peru’s GDP(Annual percent change)

Source: BCRP, INEI. 19

Economic activity continues to grow at significant rates and has already surpassed pre-COVID-19 levels

2.9 4.0

-17.7

-39.1-32.5

-18.1-11.1 -9.1 -6.0 -3.2 -2.1

1.0

-0.8 -3.5

20.0

59.4

48.3

23.412.9

2.1 0.4

-1.3 -2.9

0.1 1.1 0.4

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

Percentage change compared to 2019

20

GDP(Annual percent change)

Source: Central Reserve Bank of Peru (BCRP), MEF forecast

Peruvian economy will grow 10.5% in 2021 and will gradually converge to its potential level in the next years

5.9

2.4 3.3 4.02.5

4.02.2

-11.0

10.5

4.8 4.5 4.2 3.6

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

21

Between 2022-2025, GDP will be supported by the improved operativity of sectors most affected, mining production, and a boost to productivity

GDP contributing activities1

(Percentage point contribution to GDP)

1/ The activities most affected by COVID-19 are commerce, lodging and restaurants, transportation, and business services.Source: BCRP, INEI, MEF forecast.

Boosting competitiveness and productivity

PNIC portfolio: 52 projects (S/ 114 billion)

The PNCP has an advance of34,5%

There are ten Executive Roundtables (ER)

ER with a sector development approach.

The last ones to be created were the ER for the reactivation of

gastronomy and supply markets.

PPP portfolio 2021: 20 projects(US$ 6,3 billion)

Between public –private

Public sector

Private sector

Public sector

Private sector

Between public - public

1.1 1.1 1.00.8

1.0

0.50.4

0.2

2.1

1.61.4

1.0

2022 2023 2024 2025

MiningActivities most affected by COVID-19

COVID StatusI

22

Table of Contents

Public Finance StatusIIPublic and Private InvestmentsIIIFiscal Strategy IVBudget, Indebtedness and Finance BalanceVESG Framework VI

23

Peru: credit to private business(Annual percent change)

Credit to private business, July1

(Annual percent change)

13.6 11.7 11.0

5.6 5.12.9 2.7 2.3 2.3 1.6 0.0

-11.6

Braz

il

Rus

ia

Chi

na

Peru

Uni

ted

Stat

esN

ewZe

alan

d

Aust

ralia

Fran

ce

Chi

le

Arge

ntin

a

Col

ombi

a

Mex

ico

1/ For Mexico, June data is considered.Source: Central Banks.

6.84.3

9.2

24.6

16.8

8.27.8

5.6

0

5

10

15

20

25

30

Jan-19 Jun-19 Nov-19 Apr-20 Sep-20 Feb-21 Jul-21

Favorable credit dynamics continue

241/ Economically active population.Source: INEI

Employment(Million of people)

16.8 17.0 17.2 17.4 16.5

11.0

14.516.4 16.3 16.8

19Q1 19Q2 19Q3 19Q4 20Q1 20Q2 20Q3 20Q4 21Q1 21Q2

Unemployment(% of labor force1)

5.2

3.6 3.5 3.6

5.2

9.3 9.5

7.3 7.5

5.5

19Q1 19Q2 19Q3 19Q4 20Q1 20Q2 20Q3 20Q4 21Q1 21Q2

In 2Q2021 employment has reached 99% of the 2Q2019 level (period without pandemic shock)

The labor market has been gradually recovering

Source: Minem, Ositran, Osiptel, Proinversion, MEF forecasts. 25

Major infrastructure and mining projects will contribute to boosting private investment and sustaining economic growth

Main infrastructure projects 2021-2025 Main mining projects 2021-2025

Project Investment(US$ million)

Situation

Muelle Sur Port Terminal 627

Line 2 of the Metro ofLima and Callao 5 346 Construction

Jorge Chavez Airport 1 200 Construction

Sol Highway 493 Construction

Salaverry Port Terminal 270 Construction

Chancay Port Terminal 3 000 Construction

To start

Project Investment(US$ million)

Situation

Michiquillay 2 500

Quellaveco and theToromocho Extension 6 655 Construction

Yanacocha Sulfuros 2 100

Magistral 490

Zafranal 1 263

Los Chancas 2 600

In addition, there is a PPP portfolio to be awarded between 2021-2022 for around US$ 6 billion

Expected in 2022

Expected in 2022

Expected in 2023

Expected in 2024

Expected in 2025

We are working on an agenda to boost investment, competitiveness and productivity

Boosting investments

Mining portfolio: 46 projects(US$ 56 billion), of which 28 of

them are at different development stages and could be viable

Boosting competitiveness and productivity

26

The PNCP has an advance of34,8%

Between public –private

Public sector

Private sector

Public sector

Private sector

Between public - public

There are ten Executive Roundtables (ER)

ER with a sector development approach.

The last ones to be created were the ER for the reactivation of

gastronomy and supply markets.

PNIC portfolio: 52 projects (S/ 114 billion)

PPP portfolio 2021: 20 projects(US$ 6,3 billion)

Source: BCRP, Iproinversion, Minem, MEF.

27Source: BCRP 27

Private and public investments have recovered rapidly

Private investment(Annual percent change)

Public investment(Annual percent change)

-8.0

9.9

-0.3 -6.1

15.1

-70.7

-24.9

14.923.9

251.2

42.7

2.8

19Q1 19Q2 19Q3 19Q4 20Q1 20Q2 20Q3 20Q4 21Q1 21Q2

Percentage change compared to 2019

3.0 5.8 9.2 0.5

-14.4

-57.0

-7.5

11.336.8

162.0

17.2 12.6

19Q1 19Q2 19Q3 19Q4 20Q1 20Q2 20Q3 20Q4 21Q1 21Q2

Percentage change compared to 2019

1/ Non-mining investment is calculated as the remainder between total and mining investment. Source: BCRP, Minem, Perupetro, Ositran, Osinergmin, Osiptel, Proinversion, MEF forecast.

Non-mining investment1

(86% of the total)

28

Progressive moderation of private investment in coming years

In 1H2021, private investment had a significant dynamism, grew 80.2% annual and exceeded 1H2019 levels by 14.8%.

Private investment(Annual percent change)

Mining investment(14% of the total)

In 2021, non-mining investment: Housing market dynamism (formal and self-

construction) Execution of large infrastructure projects: Metro

Line 2, J. Chavez Airport and Chancay Port.

2022-2025: execution of PNIC projects and the PPPportfolio.

In 2021, partial recovery due to the completion of MinaJusta and the absence of new large projects.

2022-2025: start of medium-sized projects: 2022: Yanacocha Sulfuros and Magistral 2023-2025: Zafranal, Los Chancas and Michiquillay

-4.2 -5.2

0.14.1 4.5

-16.5

20.0

5.5 4.8 4.0 4.0

2015 2017 2019 2021* 2023* 2025*

Leading indicators continue to grow above pre COVID-19 levels

29

Capital goods imports (Annual percent change)

32.6

5.3

-60

-30

0

30

60

90

120

Jan-20 May-20 Sep-20 Jan-21 May-21

Percentage change compared to 2019

Aug-21

Source: COES, BCRP, Sunat

Electricity production(Annual percent change)

7.13.6

-40

-20

0

20

40

60

Jan-20 May-20 Sep-20 Jan-21 May-21 Aug-21

Percentage change compared to 2019

COVID StatusI

30

Table of Contents

Public Finance StatusIIPublic and Private InvestmentsIIIFiscal Strategy IVBudget, Indebtedness and Finance BalanceVESG Framework VI

10.811.7

9.88.8

4.6

7.6 7.3

8.99.210.4

7.7

5.7

3.4

8.87.1

4.7

0.9

3.72.8

4.93.6

2.52.0

1.0

World Advancedeconomies

Emergingmarkets

LatinAmerica

Mexico Colombia Chile Peru

2019 2020 2021 2022 2023 2024 2025 2026

31

Fiscal policy challenges around the world – Gradual Normalization

Fiscal deficit(% of GDP)

Note: Chile's fiscal deficit from 2022 onwards correspond to their structural fiscal deficit.Source: IMF, Ministries of Finance of Chile and Colombia.

In 2021, we are observing a generalized reduction in fiscal deficits. Such process of fiscal consolidation will gainstrength in 2022 and continue for the following years. Countries will gradually withdraw their fiscal impulse in order tomaintain the sustainability of its public finances.

21.619.9 19.2 19.9

23.4 23.9 24.9 25.8 26.8

34.7 35.3

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

2.1 2.3

0.9

-0.2

-1.9 -2.3-3.0

-2.3-1.6

-8.9

-4.7

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

32

Short-term fiscal strategy: fiscal policy will focus on expenditures related to the pandemic and support the process of economic recovery

Overall balance(% of GDP)

Public debt(% of GDP)

Source: BCRP, MEF forecast.

33

Medium-term fiscal strategy: execute a gradual and orderly withdrawal of fiscal impulse that strengthens the fiscal accounts without generating imbalances in the economy

Source: BCRP, MEF forecast.

For 2022, the fiscal rules for the overall balance (fiscal deficit no greater than 3.7% of GDP) and public debt (no greater than 38% ofGDP) were established through Emergency Decree No. 079-2021.

For the following years, the fiscal rules will be regulated by a Law.

Overall balance(% of GDP)

Public debt(% of GDP)

-1.6

-8.9

-4.7

-3.7

-2.7

-1.7-1.0 -1.0 -1.0 -1.0 -1.0 -1.0

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

26,8

34,7 35,336,6

37,4 36,735,8

34,934,1

33,332,5

31,7

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

54.7

73.2

55.6

72.268.4

75.8

53.3

60.8

28.2

38.5

26.8

34.9

20

30

40

50

60

70

80

2019 2020 2021 2022 2023 2024 2025 2026

Peru

Chile

Mexico

Colombia

Latin America

Emerging markets

34

Peru will maintain sound fiscal accounts: the country's public debt will continue to be one of the lowest in the emerging markets

Source: IMF, BCRP, MEF forecasts.

Public debt(% of GDP)

35

A favorable credit rating allows the Government and private companies to access financing at low interest rates to promote investments that boost the economic growth and citizens’ well-being

1/ Measured through the EMBI+, which is one of the main country risk indicators and is calculated by JP Morgan. It corresponds to the difference in the interest rate paid by the bonds denominated in dollars, issued by the emerging country and theTreasury Bonds of the United States.Source: Bloomberg, BCRP.

Country risk1

(Percentage points)

Lower levels of country risk allow the Government to obtain competitive interest rates in the capital markets. Thisreduces interest payments, providing space for productive public spending.

NFPS’s interest payments of public debt(% of GDP)

9.1

4.7

2.8 2.5 2.3 2.11.7

1.2 1.1 1.21.6

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

50

150

250

350

450

550

650

750

Jan

-16

Apr

-16

Aug

-16

Dec

-16

Apr

-17

Aug

-17

Dec

-17

Apr

-18

Aug

-18

Dec

-18

Apr

-19

Aug

-19

Dec

-19

Apr

-20

Aug

-20

Dec

-20

Apr

-21

Aug

-21

Latin America Emerging marketsColombia MexicoChile Peru

36

Amortization payments on public debt are concentrated in the medium and long term

Source: MEF.

Amortization payments on public debt(USD billion)

0,6 1,0 1,3

2,9 2,6

6,2

2,0

5,0 4,8

2,6

7,5

5,9

3,3 2,9

0,8 0,5

4,0

2,2

1,2 1,1

0,2

2,0 2,5

1,0 0,1

0,6

2,0

1,0

0

1

2

3

4

5

6

7

8

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2040

2041

2042

2046

2047

2050

2051

2054

2055

2060

2121

Peru (2020)

Peru (2014)

Chile (2017)

Colombia (2015)

Mexico (2016)

VAT CIT

38.1 49.5

29.0 44.1

20.0 31.0

16.4 19.2

20.1 34.4

37

There is scope of action to increase permanent revenues given the low levels of collection compared to other countries in the region and the OECD, and the high levels of non-compliance

Tax non-compliance by country(VAT and third category CIT non-compliance2 3 - % of

potential collection)

For this reason, it will seek to work on administration and tax policy measures that cover the following aspects:o Raise the progressivity of the tax systemo Simplification and harmonization of the tax systemo Improvement of consumption taxes

o Increase the efficiency of tax exemptionso Reduce high levels of tax evasion: cost of 8% of GDP.o Reduce informality: more than 70% of the EAP.

Latin America and OECD: relationship between revenues and non-financial expenditure of the general government1

(% of GDP)

OECD: Organization for Economic Cooperation and Development.1/ Information for the year 2019. 2/ Tax non-compliance is calculated as the difference between taxes that government could collect (potential collection) and what it collects. 3/ For Peru it corresponds to the ratio between the estimated non-complianceand the potential determined tax, net of the effect of tax expenditures, while for the rest of the countries it refers to corporate income tax non-compliance. In the case of Colombia, Chile and Peru, corporate income tax non-compliance corresponds to 2012,2009 and 2019, respectively. Source: BCRP, Cepal, Ministry of Economy and Tax Administrations of the countries, OECD, Sunat, MEF.

Peru

Chile

Colombia

Brazil

MexicoLatin America

Emerging countries

Advanced countries

OECD

15

20

25

30

35

40

45

19 24 29 34 39 44

Non

-fina

ncia

l ex

pend

iture

General government revenues

19.9

23.6 23.626.3 27.1

29.431.4

33.2 33.9

39.9

Peru CHL MEX EMDE LAC COL BRA ECU ARG OECD1 2

38

In the medium term, one of the objectives of fiscal policy will be to draw closer tax collection levels to the one of regional peers in order to reduce existing gaps in public services

General government revenue, 2019(% of GDP)

1/ Emerging markets and developing economies.2/ Represents the non-weighted average of 37 OECD member countries.Source: OECD, WEO-IMF, BCRP.

General government non-financial expenditure, 2019(% of GDP)

20.022.2

25.927.5

29.2 29.432.3 33.7 34.3

40.0

PER MEX CHL LAC EMDE COL BRA ECU ARG OECD1 2

Average ratingAAAAA+AAAA-

A+

A ChileA-

BBB+ PeruBBB Mexico UruguayBBB-

BB+ Colombia ParaguayBB

BB- BrazilB+

B BoliviaB- Ecuador

CCC+

CCC ArgentinaCCC-

CC

C

SD Venezuela

Country

Inve

stm

ent g

rade

Spec

ulat

ive g

rade

39

Sound fiscal accounts support a favorable credit rating: Peru has the second-best credit rating among LAC countries

Source: S&P, Moody’s, Fitch.

COVID StatusI

40

Table of Contents

Public Finance StatusIIPublic and Private InvestmentsIIIFiscal Strategy IVBudget, Indebtedness and Finance BalanceVESG Framework VI

41

The 2022 budget is consistent with a 3.7% fiscal deficit

Public budget1

(Billions of S/)

1/ Initial Opening Budget. Source: MEF forecast.

In 2022, public budget amounts to S/ 197 billion (USD 50 billion). The public budget is consistent with a fiscal deficit of 3.7% of GDP, allowing an expansion of public investment.

119131

138 142

157168

177183

197

27 2627 27

28

33 34

4042

20

25

30

35

40

45

50

55

60

60

80

100

120

140

160

180

200

220

2014 2015 2016 2017 2018 2019 2020 2021 2022

Public budget Public investment (right axis)

42

The 2022 budget allows the financing of 5 priorities

Health and Sanitary Emergency

attentionEducation

Strengthening agricultural

competitiveness

1 2 3

Social ProtectionPromotion of

employment and productivity

54

43

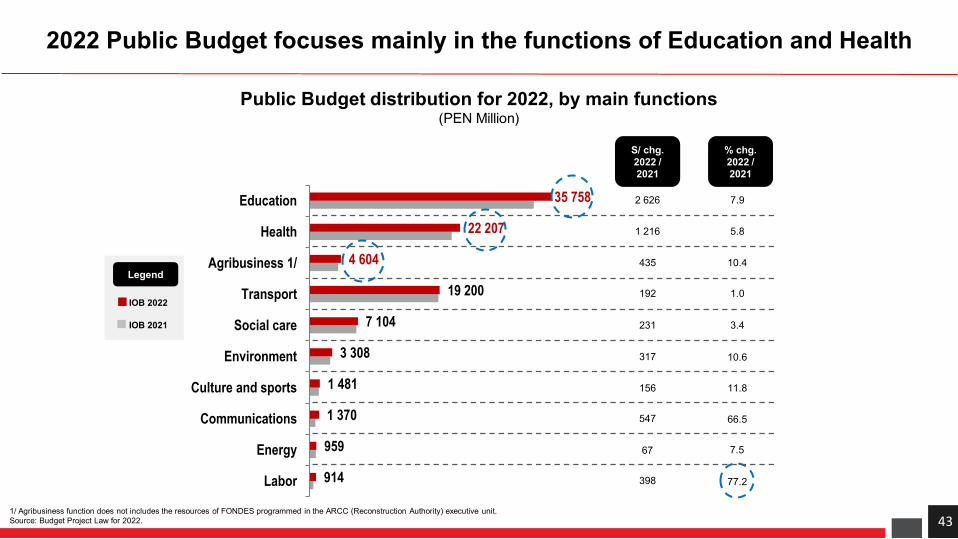

2022 Public Budget focuses mainly in the functions of Education and Health

Public Budget distribution for 2022, by main functions(PEN Million)

IOB 2022

IOB 2021

Legend

914

959

1 370

1 481

3 308

7 104

19 200

4 604

22 207

35 758

Labor

Energy

Communications

Culture and sports

Environment

Social care

Transport

Agribusiness 1/

Health

Education

S/ chg.2022 / 2021

2 626

1 216

435

192

231

156

547

317

67

398

% chg.2022 / 2021

7.9

5.8

10.4

1.0

3.4

10.6

11.8

66.5

7.5

77.2

1/ Agribusiness function does not includes the resources of FONDES programmed in the ARCC (Reconstruction Authority) executive unit.Source: Budget Project Law for 2022.

44

Composition of 2022 Indebtedness Project Law

Maximum amounts of public indebtedness for 2022(USD million and PEN Million)

This law approves the issuance of sovereign bonds up to PEN 30.6 billion (around USD 7.6 billion) for the payment of debt service andthe financing of projects in many sectors.

Additionally, approves debt management operations up to USD 6 billion (in the framework of the Asset and Liability ManagementStrategy).

Also, this law authorizes the implementation of an ETF (according to the program “Issuer-Driven ETF” with the World Bank).

1/ ONP bonds and national defense.Source: 2022 Indebtedness Project Law.

External public debt

USD million PEN million Equivalent in USD million

Economic and social sectors 1 200 15 000 3 722Public debt service 445 19 708 4 890Others¹ 409 101

Total 1 645 35 116 8 714

ItemInternal public debt

45

Composition of 2022 Indebtedness Project Law

Source: 2022 Indebtedness Project Law.

2022 public indebtedness(% of total)

2022 public indebtedness by item(% of total)

External public debt16%

Internal public debt84%

Economic and social sectors

48%Public debt service

51%

Others1%

COVID StatusI

46

Table of Contents

Public Finance StatusIIPublic and Private InvestmentsIIIFiscal Strategy IVBudget, Indebtedness and Finance BalanceVESG Framework VI

47

The Republic of Peru has made significant progress in relation to the Sustainable Development Goals (SDG)

Source: Sachs, J., Kroll, C., Lafortune, G., Fuller, G., Woelm, F. (2021) – “The Decade of Action for the Sustainable Development Goals: Sustainable Development Report 2021”.

Ranking Country Score1 Chile 77.1 2 Uruguay 74.5 3 Cuba 73.7 4 Costa Rica 73.6 5 Argentina 72.8 6 Ecuador 72.5 7 Brazil 71.3 8 Peru 71.1 9 Dominican Republic 70.8 10 Colombia 70.6 11 México 69.1 12 Jamaica 69.0 13 Barbados 68.4 14 Panama 68.0 15 El Salvador 67.9 16 Bolivia 67.6 17 Suriname 67.0 18 Paraguay 66.9 19 Nicaragua 66.3 20 Belize 64.4 21 Trinidad and Tobago 63.5 22 Honduras 62.8 23 Guatemala 59.9 24 Venezuela, RB 59.3 25 Guyana 57.9 26 Haiti 51.4

SDG Index (Score)

LAC Average: 68.5

SDG Index - LAC 2021(Score)

71,1

77,1

70,6 69,1

71,3

60

62

64

66

68

70

72

74

76

78

80

2000 2003 2006 2009 2012 2015 2018 2021

Peru

Chile

MexicoColombia

Brazil

48

Peru Sustainable Bond Framework

Public Policies

National Development and Social Inclusion Policy

National Gender Equality Policy

National Policy on Older Adults

National Environmental Policy

National Environmental Education Policy

National Financial Inclusion Policy -PNIF.

National Competitiveness and Productivity Policy

Second Party OpinionSustainalytics is of the opinion that the Peru Sustainable Bond Frameworkis credible and impactful and aligns with the Sustainability Bond Guidelines2021, Green Bond Principles 2021, and Social Bond Principles 2021. Thisassessment is based on the following: Use of proceeds Project evaluation / selection Management of proceeds Reporting

International Environmental Commitments Paris Agreement Aarhus Convention Minamata Market Convention

Agreement on Environmental Cooperation (Perú-Chile)

Marrakesh Agreement

1

Elegible Social Categories

Elegible Green Categories

Support for vulnerable groups and people in vulnerable situations

Aceess to affordable housing, education and essential health services

Support for MSMEs and social programs to

alleviate and/or prevent unemployment

Green buildings

Efficient and resilient wáter and wastewater

management

Energy efficienccy

Sustainable Agriculture

Renewable Energy

Sustainable management of natural resources, land use and marine protected areas

Low carbon

transport

Sustainable waste management

As member of the United Nations, Peru has a comprehensive visión of development that aims to achieve

the SDGs

Pedro Francke BallvéMinister of Economy and Finance

September 2021