partnership for change

TRANSCRIPT

EAST ASIAN BUREAU OF ECONOMIC RESEARCH | CHINA CENTER FOR INTERNATIONAL ECONOMIC EXCHANGES

PARTNERSHIP FOR CHANGE

2016Australia–China Joint Economic Report

PAR

TNER

SHIP

FOR

CH

AN

GE A

ustralia–China Joint Economic R

eport 2016

4606487817609

ISBN 9781760460648

WHH Aus China_cover vChinese.indd 1 21/07/2016 4:02 PM

PARTNERSHIP FOR CHANGEAustralia–China Joint Economic Report

ANU Press

East Asian Bureau of Economic Research, ANU, Canberra

China Center for International Economic Exchanges, Beijing

August 2016

Published by the ANU Press, East Asian Bureau of Economic Research and the China Center for International Economic Exchanges

© East Asian Bureau of Economic Research, China Center for International Economic Exchanges 2016

ISBN 9781760460648 (print) ISBN 9781760460655 (ebook)

A CiP catalogue record of this book is available from the National Library of Australia

Creative commons licence

This report is published under a Creative Commons Attribution Non-Commercial NoDerivs 3.0 Unported Licence.

The work in this report can be copied and redistributed in any medium or format without any further permission needing to be sought, so long as: the work is copied or redistributed for non-commercial purposes; the original authors and publishers of the work are credited; and, the work is not altered, only redistributed.

The full licence terms are available at https://creativecommons.org/licenses/by-nc-nd/3.0/legalcode.

Contact

Inquiries regarding the licence and requests to use material in this document for commercial purposes are welcome at:

East Asian Bureau of Economic ResearchCrawford School of Public PolicyThe Australian National University Acton ACT 2601 Phone: +61 2 6125 6411 Email: [email protected]

This title is also available online at press.anu.edu.au

Design and artwork by Kylie Smith Printed by Prinstant, Canberra

ContentsForeword 1

Listofacronyms 5

Listoffigures 9

Listoftables 11

Listofboxes 11

Executivesummary 13

Chapter1:Strategicimportanceoftherelationship 25

Chapter2:TheeconomictransformationsinChinaandAustralia 45

Chapter3:Tradeingoodsandservices 71

Chapter4:Investment,humancapitalandlabourmovement 109

Chapter5:Financialintegration 137

Chapter6:Frameworkforcapturingopportunitiesandmanagingrisks 171

Chapter7:AustraliaandChinainregionaleconomicdiplomacy 207

Chapter8:Collaborationintheglobalsystem 233

Chapter9:Conclusions 269

References 283

iii

iv

ForewordThisReportistheproductofajointstudyundertakenbytheEastAsianBureauofEconomicResearch(EABER)intheCrawfordSchoolofPublicPolicyatTheAustralianNationalUniversity(ANU)andtheChinaCenterforInternationalEconomicExchanges(CCIEE)inBeijing.Wewereprivilegedtoguidethisworkthroughtoitscompletionoverthepastyear.

TherearefewmoreimportanteconomicrelationshipsforAustraliathantheoneithaswithChina.MerchandiseandservicestradewithChinanowaccountsformorethanaquarterofAustralia’soveralltrade.ChineseinvestmentinAustraliaisgrowingfast.FormanyAustralianbusinesses,theChinesemarketrepresentsanenormouspotentialgrowthmarket.ForChina,Australiahasbeenareliableproviderofhigh-qualityinputsfromironoretoeducation.ButasChina’sgrowthmodelandpolicyfocuschanges,therearebigadjustmentsthatwillhavetobemadeintherelationshipandnewopportunitiesthatareemergingforbothcountries.

CapturingtheeconomicpotentialoftherelationshipwilldependonhowboththepublicandprivatesectorsinAustraliaandChinaengageupcloseandshapetherelationship.Gettingthemostoutoftherelationshipforbothcountrieswillrequireafunctionalunderstandingamongpolicymakers,corporateleadersandthebroadercommunityofthechangesthatwillshapeChinaandtheregionalandglobalenvironmentinthenext10years.

Thisisacriticalmomentinaonce-in-a-generationtransition.Thisisavitalopportunityforbothcountriestothinkabouthowtoshapethefuturecourseofourrelationshipinadeliberateway,establishingsomecommonreferencepointsratherthansimplymuddlingthrough.

WhatarethedynamicforceswithinChinathataredrivingitsnewgrowthmodel?OurjointstudylookedbothbackatwhathasworkedinthepastandforwardtowhatmightyieldthebestresultsforthefutureoftheAustralia–Chinarelationship,aftertheconclusionoftheChina–AustraliaFreeTradeAgreementandinthecontextofthebigchangesthataretakingplaceintherelationship.

ThisReportseekstodefinethepotentialofourtradeandinvestmentrelationships,economiccooperationeffortsandotherinteractions,andtoproduceatangiblemacro-andmicro-levelroadmapofthefuturerelationship.Wehavealsotriedtoidentifywheretheeconomicrelationshipislikelytodevelop,lookingatthesectorsandactivitiesinwhichtradeandinvestmenttiesarelikelytoconcentrate,andwhichindustrieswillthriveandwhichwilldeclineunderChina’snewgrowthmodel.

Thekindsofeconomicinteractionsandgovernmentpoliciesthathaveunderpinnedthebilateralrelationshipthusfararethestartingpoint:whethertheseareappropriateorsufficientastheeconomicrelationshipchangesanddiversifiesisthequestiononwhichthisReporthasfocused.

TheReportidentifieskeypolicychangesinChinaandAustraliathatwillbenecessarytopromoteadeepereconomicpartnership,notonlybilaterallybutalsothroughtheirregionalandglobalcooperation.SituatingthesereformswithinthebroadercontextoftheChinesereformagenda(forexample,financialandcapitalaccountliberalisationandderegulation)andtheeconomicchallengesfacingAustralia,thisReporthassetoutdetailedconclusionsforChineseandAustralianpolicymakers,withclearprioritiesforaction.

1

FOREWORD

ThisisanindependentjointstudybyleadingthinktanksinChinaandAustralia,butithasalsohadthewarmsupportofbothgovernmentsandthecooperationofthekeyeconomicministriesandotheragenciesinbothcountries.ItalsomarshalledbroadChineseandAustralianparticipationandinputfrombusiness,fromgovernmentsatalllevels,fromleadingresearchinstitutions,andfromthewidercommunitiesofbothcountries.

TheReportalsoengagedatopteamofexpertsinbothChinaandAustraliatoguideandassistinthepreparationoftheReportanditsargument.Weareverygratefulforthesupportandadviceoftheseverybusypeopleinthecompletionofourwork.

TheAustralianGroupofExpertsincluded:DrIanWatt,formerlysecretaryoftheDepartmentofthePrimeMinisterandCabinet;ProfessorGaryBanks,ChiefExecutiveandDeanoftheAustraliaandNewZealandSchoolofGovernmentandformerlychairoftheProductivityCommission;ProfessorAllanGyngell,DirectoroftheCrawfordAustralianLeadershipForumattheANUandformerlydirector-generaloftheAustralianOfficeofNationalAssessments;DrHeatherSmith,SecretaryoftheDepartmentofCommunicationsandtheArts;andDrPhilLowe,recentlyappointedtobethenextGovernoroftheReserveBankofAustralia;andwithadvicefromProfessorRossGarnautandDrGeoffRaby,bothformerAustralianambassadorstoChina,alongwithotherexpertinputs.

TheChineseGroupofExpertsincluded:ProfessorHuangYiping,Vice-PresidentoftheNationalSchoolofDevelopmentatPekingUniversityandadvisortothePeople’sBankofChina(PBoC)MonetaryPolicyCommittee;DrHeFan,ChiefEconomistoftheChongyangInstituteofFinanceattheRenminUniversityofChina,SeniorEconomicsFellowattheInstituteforNewEconomicThinkinginNewYork,andChiefEconomicsCommentatoratCaixinMedia;ProfessorZhangYunling,DirectorofInternationalStudiesattheChineseAcademyofSocialSciencesandamemberoftheForeignAffairsCommitteeoftheChinesePeople’sPoliticalConsultativeConference;DrChenWenling,CCIEEChiefEconomist;MrLiuZuozhang,formerminister-counsellorattheChineseEmbassyinAustralia;DrZhuBaoliang,DirectoroftheEconomicForecastingDepartmentoftheStateInformationCenter;andProfessorFanGang,afacultymemberattheHSBCBusinessSchoolofPekingUniversityandSecretary-GeneraloftheChinaReformFoundation;withadviceandinputfromMrZhaoJinjun,formerpresidentoftheChinaForeignAffairsUniversityandformerChineseambassadortoFrance;MsHuXiaolian,PresidentofExport-ImportBankofChinaandformerdeputy-governorofthePBoC;andMrXuChaoyou,DirectoroftheCCIEEDepartmentofExternalAffairsandformerlyoftheMinistryofForeignAffairs(MFA).

TheReporthasbenefitedfromthevaluablesupportoftheleadersofCCIEEandtheANU—MrZengPeiyan,ChairmanoftheCCIEE,andProfessorBrianSchmidt,Vice-ChancelloroftheANU.

ThisstudywouldnothavebeenpossibleattheAustralianendwithoutthegeneroussupportofbusinesssponsorswhofirstengagedwiththeANUthroughanAustralianResearchCouncilLinkageGrantprojectonChineseoverseasdirectinvestment.OurdeepestgratitudegoestoRioTinto,andespeciallyTimLane;toMMG,andespeciallyTroyHeyandAndrewPatterson;andtoCorrsChambersWestgarth,especiallyJohnDenton.

Thesuccessofthisprojecthasbeenmadepossiblebythecommitmentandcooperationofpublicserviceleadersonbothsides.InAustralia,theReportreceivedcashandsubstantialin-kindsupportfromtheTreasury,whotookcarriageofthisReportintheAustralianpublicservice.ChrisLegg,JohnKaratsoreosandLachlanCareywereconstantlyinvolvedin

2

PartnershiP for Change

advancingtheReport,andwealsothankLeesaCroke,AdamMcKissack,JyotiRahman,JohnSwieringa,NanWang,JustinIu,VeraHolenstein,HuiYao,AdamHawkinsandAaronVanBridgesfortheirsupport.

KeyofficialsupportersoftheprojectinAustraliaalsoincludedtheReserveBankofAustralia,particularlyIvanRoberts,EdenHatzviandChrisRyan;theDepartmentofPrimeMinisterandCabinet,particularlyMartinParkinson,DavidGruen,HKYu,JasonMcDonald,HughJeffrey,AlistairMacGibbon,LukeYeaman,JayCaldwell,AndrewForrest,ErnyWahandAnnaEngwerda-Smith;theDepartmentofForeignAffairsandTrade,particularlyPeterVarghese,JanAdams,JustinBrown,BrendanBerne,GrahamFletcher,FrancesLisson,MichaelMuggliston,JamesWiblin,JasonRobertson,MichaelGrowderandKevinThomson;theDepartmentofDefence,particularlyDennisRichardson,MarcAblongandScottDewar;theOfficeofNationalAssessments,particularlyRichardMaude,RodBrazierandJonathanOlrick;Austrade,particularlyBruceGosper,DavidLanders,MarkThirlwellandKellyRalston;TourismResearchAustralia,particularlyGeorgeChenandJaniceWykes;theAustralianBureauofAgriculturalandResourceEconomicsandSciences,particularlyShengYu;andFrancesAdamsoninthePrimeMinister’sOffice.

TheChinesesidewouldliketoextendtheirdeepthankstothosewhocontributedtothesuccessoftheReportfromtheChinesegovernment.AttheChineseEmbassyinCanberra,theyincludeAmbassadorChengJingye,ChargeD’AffairesCaiWei,Minister-CounsellorHuangRengangandFirstSecretaryLiFang.InChina,theyincludeZhaoWenfeiattheMFA;LiChaoattheNationalDevelopmentandReformCommission;FangHaoattheMinistryofCommerce;QinYuexingattheMinistryofFinance;andHuangXinjuatthePBoC.

ThisReportalsobenefitedgreatlyfromconsultationsconductedwithawiderangeofinstitutionsandindividualsinAustraliaandChinaundertakenthroughoutcourseofitswriting.WewouldespeciallyliketothankformerprimeministersBobHawke,PaulKeating,JohnHoward,KevinRudd,JuliaGillardandTonyAbbottfortheiradviceandsupport.

FromAustralianstategovernmentswewouldliketoofferspecialthankstoMartinHamilton-SmithandJingLiinSouthAustralia;SimonPhemisterandDavidLatinainVictoria;andSusanCalvertandMatthewRuddinNewSouthWales.

OurprincipalsupporterswithintheAustralianbusinesscommunityweretheGlobalEngagementTaskforceoftheBusinessCouncilofAustralia(BCA).WeextendspecialthankstoJohnDenton,LisaGropp,JasonChaiandthemanyleadingcompaniesengagedwiththisprocessthroughtheBCAbothinAustraliaandinChina,includingtheChinaDevelopmentBank.

Fromthebusinesscommunitywewouldalsoliketothank:theAustraliaChinaBusinessCouncil,withspecialthankstoJohnBrumby,SeanKeenihan,CameronBrown,DanielBisignano,MoyiZheng,AaronDuffandJetteRadley;TracyColgan,VaughnBarber,GlennCampbell,NickCoyleandOliverTheobaldattheAustralianChamberofCommerceBeijing;AmyAusterandMartinFooattheAustralianCentreforFinancialStudies;StephenJoskeatAustralianSuper;PaulBloxhamatHSBC;AndrewCharltonatAlphaBeta;MickKeoghattheAustralianFarmInstitute;NickBolkusatBespokeApproach;andTimothyCoghlanattheAustraliaChinaFashionAlliance.

Fromtheacademicandresearchspherewewouldliketothank:JennyMcGregor,MukundNarayanamurti,BernardineFernandezandClioZhengatAsialink;BobCarr,JamesLaurenceson,ThomasBoakandHannahBrethertonattheUniversityofTechnologySydney;

3

FOREWORD

HansHendrischkeandWeiLiattheUniversityofSydney;ChristineWongandAnthonyGarnautattheUniversityofMelbourne;PeterCaiattheLowyInstituteforInternationalPolicy;LindaJakobsonatChinaMatters;ChrisHeathcote,BillBrummittandMarBeltranattheGlobalInfrastructureHub;JuliaEvansattheAustralianAcademyoftheHumanities;JeanDongattheAustraliaChinaOBORInitiative;andJohnLeeattheInstituteforRegionalSecurity

WeareespeciallythankfulforthesubmissionspreparedbytheAustraliaChinaBusinessCouncil;EdwardKus,EllenEganandMerricFoleyattheAustralia–ChinaYoungProfessionalsInitiative;HenrySherrellattheMigrationCouncilAustralia;SallyLoaneattheFinancialServicesCouncil;andBelindaRobinsonatUniversitiesAustralia.

TheReportwouldnothavebeencompletedwithoutthededicatedprofessionalismofthetaskforcesattheANUandCCIEEwhoassistedwithdraftingtheReport.OntheAustraliansidethisincludedShiroArmstrong,AmyKing,RyanManuel,PaulHubbard,AdamTriggs,JiaoWang,OwenFreestoneandNeilThomas.OntheChinesesidethisincludedZhangYongjun,LiuXiangdong,ChenYingchunandLinJiang.

Thereweremanyotherpeoplewithinourrespectiveinstitutionsthatprovidedimportantinputduringthedraftingprocess.AcademicsattheANU,includingDongDongZhang,PaulGretton,RichardRigby,LigangSong,HughWhite,PhilippaDee,PeterMcDonald,ZhaoZhongwei,FrankJotzo,StephenHowes,DavidVinesandAnastasiaKapetas,providedvaluablecontributionsintheirrespectivefieldsofexpertise.TheANUsecretariatincludingTomWestland,RosemaryTran,AlisonDarby,PatrickDeegan,RosaBishop,SamHardwick,MichaelWijnen,NawaazKhalfan,PatrickWilliams,HitonaruFukui,OwenHutchisonandLukeHurstprovidededitorialadvice,researchsupportandlogisticalassistance.

WewouldberemissifwedidnotextendourwarmthankstoNeilThomas,whocoordinatedtheAustralianendoftheworkontheReport,andZhangYongjun,LiuJunandotherswhocoordinatedtheprojectattheChineseend.Theirdevotiontothistaskwasessentialtoitssuccessfulcompletion.

ThisReportistheresultofasignificantandunprecedentedexerciseinbi-nationalcollaboration.Wehavesoughttoprovidecommonreferencepointsinhowwecanconductourrelationshipandprinciplestowhichwecanappealwhenfacingtheinevitableuncertaintiesthatweshallhavetomanagearoundprofoundchange.WeareconvincedthattheeffortthatthisReporthascalledforthinbothourcountriestothinkthroughthefutureofourbilateraleconomicrelationshiptogetherisinitselfanencouragingharbingerofwhatAustraliaandChinacanhopetoachievetogetheroverthecomingdecades.

Peter Drysdale Zhang Xiaoqiang

August 2016

4

PartnershiP for Change

List of acronymsAALD Australian–AmericanLeadershipDialogue

ABC AgriculturalBankofChina

ABS AustralianBureauofStatistics

ACACA Australia–ChinaAgriculturalCooperationAgreement

ACC Australia–ChinaCouncil

ACCCI Australia–ChinaChamberofCommerceandIndustry

ACJER Australia–ChinaJointEconomicReport

ACOLA AustralianCouncilofLearnedAcademies

ACRI Australia–ChinaRelationsInstitute

ACT AustralianCapitalTerritory

ACYA Australia–ChinaYouthAssociation

ACYD Australia–ChinaYouthDialogue

ACYPI Australia–ChinaYoungProfessionalsInitiative

ADB AsianDevelopmentBank

ADS ApprovedDestinationStatus

AEC ASEANEconomicCommunity

AFTA ASEANFreeTradeArea

AIIB AsianInfrastructureInvestmentBank

AJBCC Australia–JapanBusinessCooperationCommittee

AJPPPD Australia–JapanPublic-PrivatePolicyDialogue

AMPC ASEANMasterPlanforConnectivity

AMRO ASEANPlusThreeMacroeconomicResearchOffice

ANZ AustraliaandNewZealandBank

ANZSOG AustraliaandNewZealandSchoolofGovernment

ANZUS AustraliaNewZealandUnitedStatesSecurityTreaty

APEC AsiaPacificEconomicCooperation

APRA AustralianPrudentialandRegulationAuthority

ARENA AustralianRenewableEnergyAgency

ARF ASEANRegionalForum

ARFP AsiaRegionFundsPassport

ASEAN AssociationofSoutheastAsianNations

ASIC AustralianSecuritiesandInvestmentsCommission

ASX AustralianSecuritiesExchange

ATC AustralianTradeCommission

ATSE AustralianAcademyofTechnologicalSciencesandEngineering

AWIC AustraliaWeekinChina

5

List OF AcROnyms

BCA BusinessCouncilofAustralia

BCIM Bangladesh–China–India–MyanmarEconomicCorridor

BIS BankofInternationalSettlements

BIT BilateralInvestmentTreaty

BRICS BrazilRussiaIndiaChinaSouthAfrica

CBA CommonwealthBankofAustralia

CCB ChinaConstructionBank

CCIEE ChinaCenterforInternationalEconomicExchanges

CEFC CleanEnergyFinanceCorporation

ChAFTA China–AustraliaFreeTradeAgreement

CISA ChinaIronandSteelAssociation

CITIC ChinaInternationalTrustandInvestmentCorporation

CMBA ChineseMedicineBoardofAustralia

CMI ChiangMaiInitiative

CMIM ChiangMaiInitiativeMultilateralization

CNTA ChinaNationalTourismAdministration

CPEC China–PakistanEconomicCorridor

CPPCC ChinesePeople’sPoliticalConsultativeConference

CSIRO CommonwealthScientificandIndustrialResearchOrganisation

CSRC ChinaSecuritiesRegulatoryCommission

DAF DepartmentofAgricultureandFood(WesternAustralia)

DIBP DepartmentofImmigrationandBorderProtection(Australia)

DDPP DeepDecarbonisationPathwaysProject

DFAT DepartmentofForeignAffairsandTrade(Australia)

DSDBI DepartmentofStateDevelopment,BusinessandInnovation(Victoria)

DSGE DynamicStochasticGeneralEquilibrium

EABER EastAsianBureauofEconomicResearch

EAS EastAsiaSummit

EGA EnvironmentalGoodsAgreement

EIA EnergyInformationAdministration

EPG EminentPersonsGroup

ESM EuropeanStabilityMechanism

EU EuropeanUnion

FASIC FoundationforAustralianStudiesinChina

FDI ForeignDirectInvestment

FinTech FinancialTechnology

FIRB ForeignInvestmentReviewBoard(Australia)

FSC FinancialServicesCouncil

6

PartnershiP for Change

FTA FreeTradeAgreement

FTAAP FreeTradeAreaoftheAsiaPacific

GATT GeneralAgreementonTariffsandTrade

GBP PoundSterling

GCI GlobalCompetitivenessIndex

GDP GrossDomesticProduct

GNI GrossNationalIncome

GTAP GlobalTradeAnalysisProject

GVA GrossValueAdded

HELP HigherEducationLoansProgram

HKMA HongKongMonetaryAuthority

HLD High-LevelDialogue(Australia-China)

IBRD InternationalBankforReconstructionandDevelopment

ICBC IndustrialandCommercialBankofChina

ICT InformationandCommunicationsTechnology

IEA InternationalEnergyAgency

IFA InvestmentFacilitationArrangement

IMF InternationalMonetaryFund

IPCC InternationalPanelonClimateChange

IPO InitialPublicOffering

IT InformationTechnology

ITA InformationTechnologyAgreement

KBC Knowledge-BasedCapital

LED LightEmittingDiode

LNG LiquefiedNaturalGas

MFN MostFavouredNation

MoC MemorandumofCooperation

MOFCOM MinistryofCommerce(PRC)

MoU MemorandumofUnderstanding

MSR MaritimeSilkRoad

NAB NationalAustraliaBank

NAFTA NorthAmericanFreeTradeArea

NAIF NorthernAustraliaInfrastructureFacility

NDRC NationalDevelopmentandReformCommission(China)

NICM NationalInstituteforComplimentaryMedicine(Australia)

NIE NewIndustrialisedEconomy

NLA NationalLibraryofAustralia

NLC NationalLibraryofChina

7

List OF AcROnyms

OBOR OneBelt,OneRoad

OECD OrganisationforEconomicCooperationandDevelopment

PBoC People’sBankofChina

PLA People’sLiberationArmy(China)

PPP PurchasingPowerParity

PSC ProductionSharingContract

PTA PreferentialTradeAgreement

RBA ReserveBankofAustralia

RCEP RegionalComprehensiveEconomicPartnership

RFA RegionalFundingArrangement

RMB Renminbi

RQDII RenminbiQualifiedDomesticInstitutionalInvestor

RQFII RenminbiQualifiedForeignInstitutionalInvestor

SASAC State-ownedAssetsSupervisionandAdministrationCommission(China)

SBLF Australia–ChinaSeniorBusinessLeadersForum

SDR SpecialDrawingRights

SEC SecuritiesandExchangeCommission(USA)

SED StrategicEconomicDialogue(Australia–China)

SOE State-OwnedEnterprise

SSO SydneySymphonyOrchestra

STEM ScienceTechnologyEngineeringMathematics

TCM TraditionalChineseMedicine

TFA TradeFacilitationAgreement

TPP Trans-PacificPartnership

TRIM Trade-RelatedInvestmentMeasure

TTIP TransatlanticTradeandInvestmentPartnership

UKTI UnitedKingdomTradeandInvestment

UN UnitedNations

UNCTAD UnitedNationsConferenceonTradeandDevelopment

US UnitedStates

VECCI VictorianChamberofCommerceandIndustry

WA WesternAustralia

WOFE WhollyOwnedForeignEnterprise

WTO WorldTradeOrganization

8

PartnershiP for Change

List of figuresFigure1.1: Chineseandglobalsteelproduction 30

Figure1.2: SectoralvalueaddedasapercentageofChineseGDP 32

Figure1.3: China’sGDPgrowth(RHS)anditscontributiontoglobaloutput(LHS),1990–2020 33

Figure1.4: ExportstoChinaasashareoftotalexports,Australiaandothermajorexporters 34

Figure1.5: Asia’sweightintheglobaleconomy 41

Figure2.1: China’sshareoftheglobaleconomicaggregates 50

Figure2.2: InvestmentasashareofGDP 51

Figure2.3: Nationalsavingbysector 53

Figure2.4: China’sshareofglobalcommodityconsumption 53

Figure2.5: China’ssteelproduction 54

Figure2.6: MininginvestmentinAustralia 55

Figure2.7: Australia’sshareofChinesecommodityimports 55

Figure2.8: Growthinglobaltrade 56

Figure2.9: Wagesandhouseholddisposableincome 57

Figure2.10: ContributionstoChina’sGDPgrowth 58

Figure2.11: China’sexportmix1995–2015 59

Figure2.12: Domesticvalue-addedshareofChina’sgrossexports 60

Figure2.13: ContributiontoChina’sGDPgrowth 60

Figure2.14: China’ssteelproductionandironoreimports 64

Figure2.15: GrowthinAustralia’snationalincome 66

Figure2.16: Australia’sindustrialcomposition 66

Figure2.17: Australia’scompetitivenessranking 67

Figure3.1A: Exportshare

Figure3.1B: Importshare 74

Figure3.2: Ironorepriceandexportvalue 75

Figure3.3: ChineseimportsfromAustraliaandrestofworld 77

Figure3.3A: Coal(Tons) 77

Figure3.3B: LNG(Tons) 77

Figure3.4: AustralianagriculturalexportstoChina(A$million,2014–2015) 82

Figure3.5: AustraliangoodsexportstoNortheastAsianeconomies 83

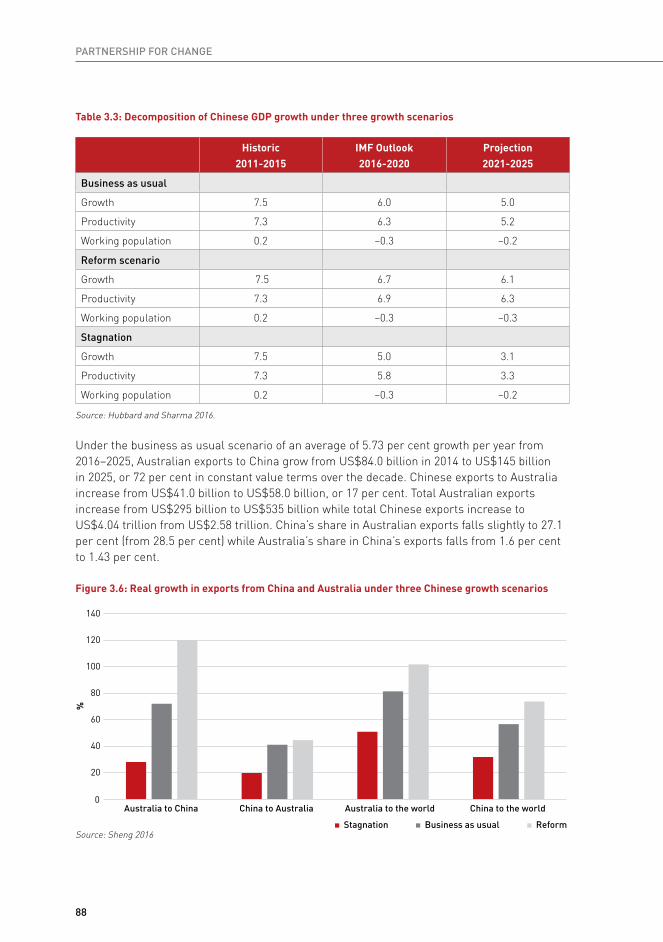

Figure3.6: RealgrowthinexportsfromChinaandAustraliaunderthreeChinesegrowthscenarios 88

9

List OF FiguREs

Figure3.7: TotalaveragespendofforeignersvisitingfriendsandrelativesinAustralia,2015 95

Figure4.1: StockofforeigndirectinvestmentinAustraliabysource(2014A$billion) 115

Figure4.2: OECDforeigndirectinvestmentregulatoryrestrictivenessindex 117

Figure4.3: RecipientsofAustraliandirectinvestment,2014(A$billion) 125

Figure4.4: Workingholidayvisasgrantedfrom1July2014to30June2015 133

Figure4.5: StudentvisaholdersinAustralia,30June2015 135

Figure5.1: Grossvalueaddedbythefinancialservicesindustryasapercentageoftotaloutput 143

Figure5.2: OECDservicestraderestrictivenessindexforcommercialbanking,2015 144

Figure5.3: OECDservicestraderestrictivenessindexforinsurance,2015 145

Figure5.4: IndexofcontrolsonChina’scapitalaccount(ka)andcurrentaccount(ca)overrecentyears 149

Figure5.5: Nominalandnominaleffectiveexchangerates—theRMBagainsttheUSdollar 153

Figure5.6: Australia’sexportsoffinancialservicestotheAsiaPacificregion 154

Figure5.7: Australia’sexportsofinsuranceandpensionservicestotheAsiaPacificregion 154

Figure5.8: TotalsalesoffinancialservicesandinsuranceandpensionservicesbyAustraliabymodeofsupply,2009–2010 155

Figure7.1: AsiaPacificeconomies’shareoftradewithEastAsia,2014 214

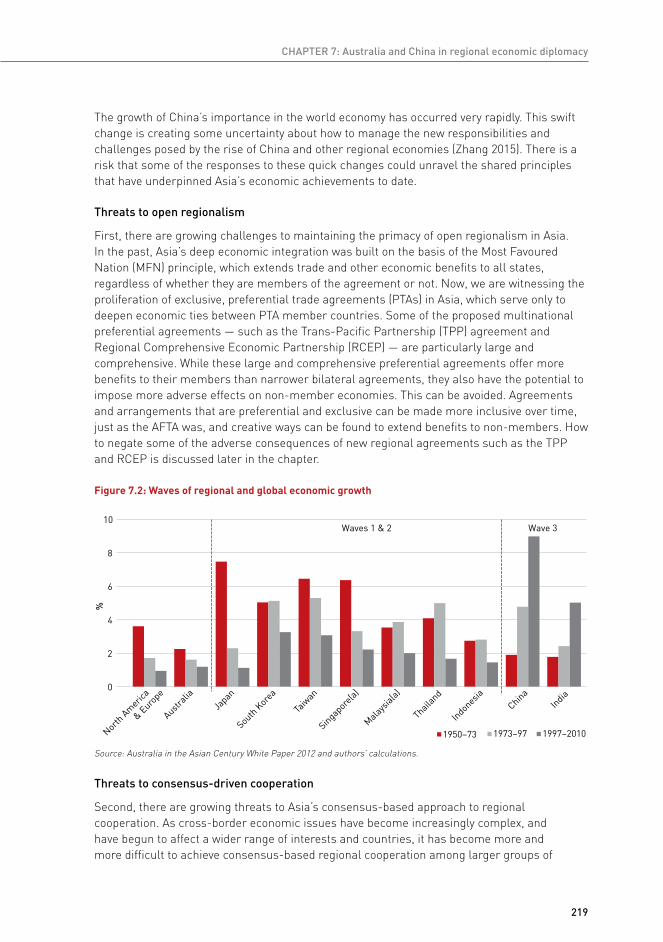

Figure7.2: Wavesofregionalandglobaleconomicgrowth 219

Figure7.3: ASEAN,APEC,EASandARFmembershipcompared 222

Figure7.4: ASEAN,RCEP,TPPandpossibleFTAAPmembership 226

Figure7.5: GDPprojectionsofRCEPandTPPgroups,1980–2050,atpurchasingpowerparity 228

Figure8.1: AustraliaandChinaintheglobalgovernancearchitecture 238

Figure8.2: ShareofglobalGDP(ppp)

Figure8.3: Globaltradevolumneofgoodsandservices(1980=100) 240

Figure8.4: Globalcapitalflowssince1980 241

Figure8.5: IMFGDPforecastsforemergingmarketanddevelopingeconomies 246

Figure8.6: Thecomponentsoftheglobalfinancialsafetynet 249

Figure8.7: Totalresourcescomparedtoavailableresources 250

Figure8.8: AustraliaandChinawithintheglobaltradingsystem 254

Figure8.9: InvestmentasapercentageofGDP 259

Figure8.10: AustraliaandChinawithintheglobalenergygovernancearchitecture 261

Figure8.11: China’sannualgrowthinGDP,CO2emissions,energyandemissionsandenergyintensity,2005–2014 264

10

PartnershiP for Change

List of tablesTable2.1: China’ssteelusagebypurpose(percentageoftotal) 63

Table3.1: ActualandprojectedexportsofcommoditiestoChina 78

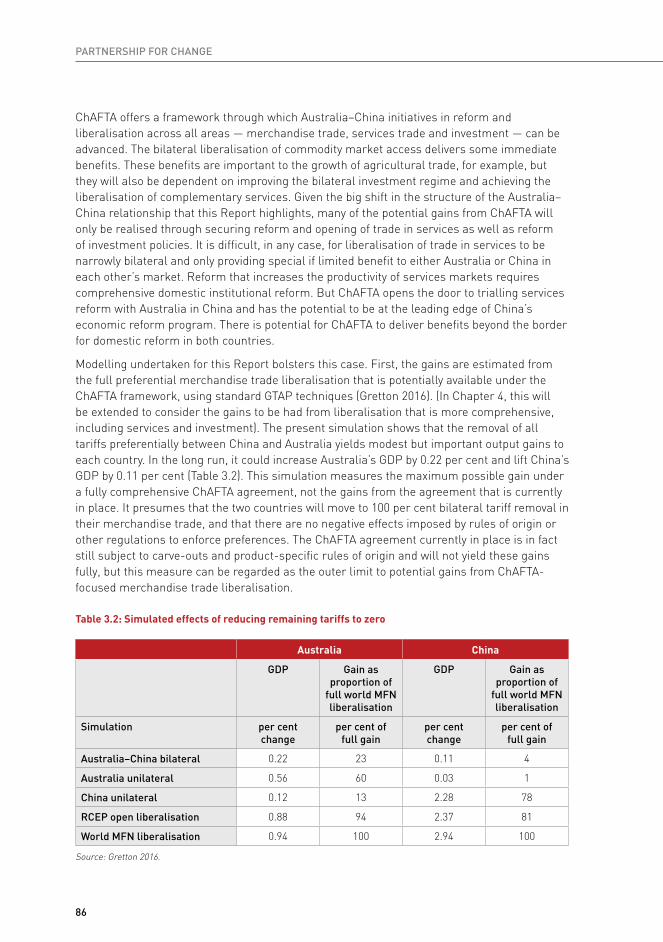

Table3.2: Simulatedeffectsofreducingremainingtariffstozero 86

Table3.3: DecompositionofChineseGDPgrowthunderthreegrowthscenarios 88

Table3.4: Actualandprojectedsharesofexportsbysector 89

Table3.5: Actualandprojectedshareofexportsbysectorinalternativescenarios 90

Table3.6: ThechangingnatureofChinesemanufacturingexportstoAustralia 92

Table3.7: Sisterstate–provincerelationshipsbetweenAustraliaandChina 102

Table4.1: Remainingbarrierstoinvestment 127

List of boxesBox2.1: Theglobalriseoftheinnovationeconomy 48

Box2.2: China’shighratesofnationalsaving 52

Box2.3: China’sprogressiontowardshigher-endandvalue-addedmanufacturing 59

Box2.4: China’seconomictransformationandthe13thFiveYearPlan 61

Box2.5: TheoutlookforChina’ssteeldemand 63

Box2.6: AnassessmentofAustralia’scompetitiveness 67

Box2.7: ReformprioritiesacrossAustralia’sservicessector 68

Box3.1: Morethanore 77

Box3.2: Resourcesecurityandglobaltrade 78

Box3.3: AlibabaGroupopensnewmarketsforAustralianexporters 84

Box3.4: Blackmores’Chinaentrystrategy 85

Box3.5: ChinesetourisminAustralia 94

Box3.6: AustraliantouristsinChina 97

Box3.7: Healthcareservices 99

Box3.8: TheAustralia-ChinaStrategicEconomicPartnership 101

Box3.9: Stateandprovincialties 103

Box3.10: CulturalconnectionsandbusinessopportunitiesfromtheChinesediaspora 106

Box3.11: BrandAustraliaandBrandChina 107

Box4.1: Thebenefitsofforeigndirectinvestment 111

Box4.2: Popularattitudestowardforeigninvestment 116

Box4.3: InfrastructureinvestmentinAustralia 119

11

List OF tABLEs, List OF BOXEs

Box4.4: ForeigninvestmentintheUnitedKingdom 120

Box4.5: UnderstandingChineseSOEs 121

Box4.6: Chineseglobalinvestmentsinironore 122

Box4.7: TheChinesediasporainAustralia 129

Box4.8: VisasforinvestorsandtourismintheUnitedKingdom 130

Box4.9: Collaborativeresearchandscientificexchange 134

Box5.1: China’sbigfourbanksinAustralia 151

Box5.2: Australia’s‘bigfour’banksinChina 155

Box5.3: AMPCapitalandChinaLife 157

Box5.4: TheAustralia–ChinaInvestmentCooperationFramework 159

Box6.1: Australia,Chinaandregionalinfrastructureinvestment 175

Box6.2: Experiencewithcommercialrisks 178

Box6.3: Australia’sreactiontoshocksfromshiftsinChinesemarketsentiment 180

Box6.4: LandbridgeGroupandthePortofDarwin 182

Box6.5: SinoGasinChina 183

Box6.6: China’saccessiontotheWTO 186

Box6.7: Deliveringprosperityandsecuritythroughthemarket 188

Box6.8: Modelsofbilateralcollaboration 195

Box6.9: RegionalsecurityandtheAustralia–Chinarelationship 201

Box6.10: Buildingpolicytrust 203

Box7.1: AsiaPacificregionalinitiativesandtheglobalsystem 216

Box7.2: ConsensusandthecreationoftheAsianDevelopmentBank 217

Box7.3: Buildingamultilateralregimeforgoverningforeigndirectinvestment 229

12

PartnershiP for Change

EXECUTIVESUMMARY

13

Executive Summary

Australia and China: forging a comprehensive strategic partnership for change

AustraliaandChina,twovastlydifferentnations,alreadyhaveahugeandjointpolitical,economicandsocialinvestmentinthesuccessoftheirbilateralrelationship.

Takentoahigherlevel,asthisReportrecommends,thisinvestmentintherelationshipcanhaveadramaticadditionalimpactonbotheconomiesandsocieties.

Thisuniquepartnershipstemsfromadeepalignmentofintereststhat,shortofhighlynegativepolicymaking,cannotbeundone.

Therelationshipisalreadylargeandwillundergoahugechange.Thescaleandcomplexityoftherelationshipisgrowingbecauseoftheincreasedroleofservicesandinvestment,aswellasitspoliticalandsecuritydimensions.

Thesecircumstanceslaidthefoundationforsupportfrombothgovernmentsforanindependentjointstudyofdevelopmentsintherelationshipinthedecadeaheadandhowtostrengthenthebilateralframeworkandthepolicysettingsformanagingit.

ThisReportistheproductofanindependentstudyjointlyledbytheChinaCentreforInternationalEconomicExchangesinBeijingandbytheEastAsianBureauofEconomicResearchatTheAustralianNationalUniversity.Itsaimistodefineaframeworkforpolicymakersandforstakeholdersinbusiness,media,researchinstitutionsandthecommunity;aframeworkthatenablesAustraliaandChinatoharnesstheopportunitiesthatarearisingfromtheprofoundtransformationsintheireconomies.

Why Australia and china are important to each other

ChinahasforsomeyearsbeenAustralia’slargesttradingpartnerandoneofitsmostimportantbilateralrelationships.ItisnowwidelyunderstoodthatAustralia’seconomicgrowthandcontinuedrisinglivingstandardsarestronglylinkedtoChina’seconomicsuccess.

IntheChinesepolicycommunity,thereiswideunderstandingandclearacknowledgementoftheeconomicandpoliticaladvantagesofopen,secureandcompetitiveaccesstoAustralianironore,coalandotherrawmaterials.

AsChina’seconomymaturesanditsmiddleclassexpands,ChinaisalsoenjoyingtheaddeddividendofaccesstoAustralianagriculture,institutionsandservices—everythingfrominfantformulatovitamins,buttertobeef,educationtotourism,aswellasadvancedscience,technologyandresearchcapabilities.Australia’sopensocietyprovidesChineseinvestmentswithsecurityinastableandwell-functioningmarketeconomythatguaranteestransparentrecoursetopolitical,legalandregulatoryinstitutions.

Thesenewavenuesofcommercialexchangeareatwo-waystreet.BothAustraliaandChinagainfromgrowinganddiversifyingtheireconomicrelationshipthroughnewflowsoftourists,students,investorsandmigrants.Formorethanadecade,Chinahasbeentheworld’smaineconomicgrowthengine.Despiterecentslowdowns,Chinawillremainakeydriverofglobalgrowthinthecomingdecade.IfChina’sreformagendasucceeds,itcanachieveannualGDPgrowthofaround6percentayearoverthenext10years.

14

PartnershiP for Change

ButitisobviousthattheimpactofChina’sgrowthonAustraliaoverthenext10yearswillbeverydifferentfrominthepast.Australiawillnolongeronlybearemotesupplierofrawmaterials.ItcanbeapalpableanddistinctivepresenceinChinesedailylife,particularlyfortheurbanmiddleclasseswhoseaspirationsandincomeswillcontinuetoexpandforseveraldecades.

ThenewlyemergingpartnershipbetweenAustraliaandChinahasasignificantandvaluableextradimension.AustraliaisnotonlyeconomicallyenmeshedwithEastAsia,givingitahighstakeinChina’ssuccess.Italsohasstrongeconomic,culturalandstrategiclinkstotheUnitedStates,andthereforeacompellinginterestinapositiverelationshipbetweentheUnitedStatesandChina.

Australia’sgeopoliticalandgeo-economicpositionanditsmulticulturalsocietyarethusuniqueassetsinshapingChina’slinkswiththeWest.

ChineseandAustralianprosperityhasdependedontheliberal,rules-basedglobalsystem.Bothcountrieshaveacompellinginterestinthesuccessfuladaptationoftheinstitutionsofglobalgovernancetotheeconomicandsecuritychallengesofthe21stcentury.AdeeperpartnershipbetweenChinaandAustraliacanbeapowerfulforceforthestrengtheninganddevelopingoftheseinstitutions.Australia’slongstandingcommitmenttoglobalinstitutions,itsdeepengagementwiththeeconomiesofAsiaanditshistoricaltieswithEuropeandNorthAmericaarecomplementarytoChina’sstatusasamajoreconomicpoweranditsdeclaredwillingnesstohelpsupplyandshapetheinternationalpublicgoodsofthe21stcenturyinthetaskofreformingandstrengtheningtheregionalandglobalframeworksofcooperationandgovernance.

ThisaddssignificantweighttoAustralia’ssupportforChina’sgrowingroleintheprovisionofinternationalpublicgoods,suchastheAsianInfrastructureInvestmentBank(AIIB).BothcountrieshaveacommoncommitmenttoChina’sparticipationinglobalinstitutionsandrules.

Benefits of closer economic partnership

Chinaisshiftingitsgrowthdriversfrominvestment,exportsandheavyindustrytoconsumption,innovationandservices.China’sgrowthslowdowndoesnotthreatenthistransformation;itisasymptomofit.

Thistransformationwill,byitself,leadtofastgrowthintradebetweenAustraliaandChinainrealterms,muchofitinservices.Eveninapessimisticscenario,inwhichaverageChinesegrowthisbelow5percentoverthenext10years,ourestimatessuggestthatAustralianexportstoChinawouldstillgrowby28percentandChineseexportstoAustraliaby20percent.A‘baseline’scenariohasAustralianexportsgrowingby72percentandChineseexportsby41percentoverthesameperiod.

Thebiggestgains,however,wouldberealisedifAustraliaandChinaworktoimplementthesupply-sidereformsrecommendedinthisReport.Ifthisreformagendaisprosecutedsuccessfully,AustralianexportstoChinawillgrowby120percentinrealterms,andChineseexportstoAustraliaby44percent.ForChina,thisisconditionalontheimplementationofareformagendathatembracesfinancialandfactorreform,state-ownedenterprise(SOE)reform,increasedopennesstoforeigninvestmentandcapitalaccountliberalisation.ForAustralia,itmeansincreasedcompetitioninshelteredindustries,opennesstoforeigninvestmentandskills,andfacilitatinginvestmentinsocialandphysicalinfrastructure.

Increasedtradeandinvestmentwillmeanhighernationalincomes,moreemploymentandmoretaxrevenueforbothChinaandAustralia.

15

EXECUTIVE SUMMARY

ThestructuralchangesintheChineseeconomypresageachangeinthestructureoftrade.TheprofoundcomplementaritystemmingfromAustralia’senergyandresourceabundanceandChina’sindustrialisationwillremainakeypillaroftherelationship,butwillbeincreasinglyaugmentedbyservicessuchaseducationandtourism,withinboundtourismfromChinasettotrebleby2025.Educationandtourismserviceswilljumpfrom8percenttoalmost20percentofAustralianexportstoChinain2025ineventhe“businessasusual”scenario.Machineryandequipmentwilljumpfromjustbelow20percentofChineseexportstoAustraliato28percent.

Chineseproductionisshiftingfromamodelbasedonadaptationandimitationofgoods,servicesandtechnologiesdevelopedelsewheretoamodelbasedondomesticinnovation.ThisisbeingdrivenbyasubstantialinvestmentinChina’sinnovationecosystem.Australia’shigh-qualitytertiaryeducationsector(alreadyamajorservicesexportertoChina)anditscommitmenttoitsownNationalInnovationandScienceAgendamakeitanaturalpartnerinthistransformation.Australia’sexperienceinbuildingahighlydevelopedfinancialsystemcanalsobeofvaluetoChina,whereasophisticatedfinancialsystemwillbecrucialforallocatingcapitaltothemostinnovativeandefficientfirms.ChinaseesspecialbenefitinthepartnershipwithAustraliafortriallingreformsininvestmentpolicyandservicesmarketsaswellasseekinggreateralignmentwithAustraliainitsgeopoliticalinterestsinAsiaandthePacific.

Inshort,thereiseveryreasontobelievethattheAustralia–Chinarelationshipwillbecomemore,notless,importanttobothcountriesastheChineseeconomycontinuestochangeandupgrade.

ForAustralia,thismeansenhancedlong-termeconomiccapacitythroughopportunitiesfornewtradeandproductivity-boostinginnovationaswellasthroughimprovingnationalinfrastructureandthedevelopmentofregionalAustralia.

ForChina,thismeansasustainablepaththroughmiddle-incomestatusonitswaytobecomingahigh-incomeeconomythrougheconomicupgradinganddiversification.

towards a new policy framework

Theneedforanupgradedpolicyframeworkisbroadlyacceptedinbothcountries.

ThatiswhybothgovernmentshavefinanciallyandinstitutionallysupportedtheproductionofthisReportandprovidedthenecessaryaccesstoallowwideconsultationswiththekeyeconomicministriesandagenciesonbothsides,aswellaswithsubnationalgovernments,keyresearchinstitutions,businessleadersandcommunityfigures.

Creatinganupgradedframeworkisacomplextask:itwillrequirebuildinganewsetofnationalcapabilitiesinbothcountries.Thesewillbestbefoundedonpastexperienceandachievements.

Inthe1980s,AustraliaandChinaestablishedwhattheycalleda‘modelrelationship’betweentwoeconomieswithdifferentpoliticalandsocialsystemsandatdifferentstagesofdevelopment.Thiswasthetwocountries’firstsignificantjointeffortatbuildingaframeworkfortheirrelations.Thisprincipleshouldcontinuetoguidethebilateralrelationshiptohigherlevels.

AustraliaembracedChina’sopennessandreformasacriticalfactorinregionalprosperityandstability.ChinaembracedthepartnershipwithAustraliaasacrucialpartofitsopeningpolicy,andAustraliaassumedakeyroleinChina’sforeigneconomicstrategy.Thispath-breakingpartnershipopenedmarket-basedresourcestrade,foreigninvestmentandregionalcooperationwithChina—leadingtopositiveengagementwithChinainAPECandworkingtogetheronChina’saccessiontotheWTO.

16

PartnershiP for Change

AustraliaandChinahavesinceworkedtostrengthenregionaleconomiccooperationthroughAPEC,theASEANPlusframeworksandtheEastAsiaSummitinordertosecuretheframeworkofpoliticalconfidenceandsecuritynecessarytoeconomicprosperity.

AustraliaandChinaalreadyhaveaComprehensiveStrategicPartnership,agreedin2014,whichguaranteeshigh-levelattentiontothebilateralrelationshipthroughanannualLeadersMeeting,StrategicEconomicDialogue,andForeignandSecurityDialogue.AustraliaandChinaalsohavetheChina–AustraliaFreeTradeAgreement(ChAFTA),whichdeliverssignificanttradeliberalisationandopensthedoorinbothcountriestonewandwideraccesstoinvestmentandtheservicessector.Indeed,ChAFTAhasthepotentialtoserveasakeyagentintransformingthecommercialrelationshipbetweenthetwocountriesinthecomingdecade.

Butthefullopportunityofthesearrangementsisfarfrombeingrealised—bothcountriesmustnowprovideforthecomprehensivesettingofstrategicbilateralobjectivesinaforwardagenda.Thiswilldependonnewframeworksforinstitutionalisingactivecollaborationonpolicydevelopmentandreform.

Chinaisnowbuildingregionalandglobalinstitutionsthatarecommensuratetoitsplaceintheinternationaleconomicsystem.China’sleadontheAIIBandtheOneBelt,OneRoad(OBOR)initiativesrepresentChinaembeddingitsinterestsjointlywithotherspartnerstobolsterinfrastructureinvestmentandregionalconnectivity.

AustraliahasworkedcloselywithChinaintheIMFandotherinternationaleconomicbodiestosupporttheseChineseinitiatives.AustraliaisafoundingmemberoftheAIIB,andparticipatesinOBORthroughprogramsincludingthedevelopmentofNorthernAustralia.TherehasbeenclosecollaborationintheG20onsharedagendasforglobalgrowthandreformingthemultilateraltradingsystem.

managing new dimensions of the relationship: policy framework and programs

HowareAustraliaandChinagoingtomanagetheirincreasinglycomplexrelationship—arelationshipinwhichChinaisbyfarthebiggesteconomyinAsia,isthesecond-largesteconomyintheworld,isdeeplyenmeshedinacomplexrelationshipwiththeUnitedStates,andisprojectinggrowingpoliticalconfidence?

ClosecooperationwithAustraliashouldbeanintegralpartofthenextphaseofChina’seconomicreformandopening.Collaborationonservicesectorreform,financialrestructuringandcapitalaccountliberalisationwillhelpChinarealiseitsgrowthpotential.Asanadvancedregionalservices-basedeconomy,AustraliaisanaturalpartnerandapromisingtestbedforChinainitsreformeffort.

ThisReportoutlinesthekeyideasandprogramsfordealingwiththisquestion.Theconclusionsthatfollowareenvisagedasalong-termagendaofcooperationforbilateralrelations,andwillrequirecarefulconsiderationbybothgovernmentsandotherstakeholdersintherelationshipoverthedecadeahead.

ThisReportshowsthat,inordertorealisetheopportunitiesandcountertheriskstobilateralgrowth,theAustralianandChinesegovernmentsshouldsensiblyelevatetheirrelationshiptotheuniquelevelofaComprehensiveStrategicPartnershipforChange.Leadershipatthehighestlevelshouldsignalthepriorityattachedtodevelopmentoftherelationship.

17

EXECUTIVE SUMMARY

Inparticular:

• ThenewComprehensiveStrategicPartnershipforChangethattheReportrecommendswouldbuildonChAFTAandthecurrentannualLeadersMeeting,andparallelministerialmeetings,throughestablishingjointpolicyworkinggroupsthatsupportthisworkandotherpolicyinitiativesstemmingfromtheleaders’dialoguesandadvanceongoingpolicydevelopmentandreform:forexample,inthenegotiationofanewAgreementonInvestmentwithintheframeworkofChAFTAoronaccesstoservicesmarketsandotherissues(seebelow).

• Jointpolicyworkinggroupscanwork,asneeded,withstateandprovincialauthorities,businesssectors,researchinstitutesandcommunity-basedinterestsonspecificinitiativestoadvancethetrade,investment,financial,regionalandglobalreformagendasofbothcountries.

– TheseworkinggroupscanassistineffectingthebilateralcommitmentstofurtherinvestmentliberalisationandexpandedaccesstoservicesmarketsmadeunderChAFTA.

– Thetwocountriesshouldalsoestablishaworkinggroupfordialogueandcooperationonthemaritimeeconomy,asthisisaparticularareaofpotentiallyproductivecollaborationbetweenAustraliaandChina.Bothcountriesaremaritimepowerswithcommoninterestsinseabornesupplyroutesandmanyothermaritimeissues.

• Bothgovernmentsshouldaim,overthedecadeahead,todrawonprecedentfromtheirotherbilateralrelationshipsandembedtheirnewpartnershipintoacomprehensivebilateralBasicTreatyofCooperation.

– Thistreatywouldlockinthepracticeandprinciplesforcooperation,and:committoregularhigh-levelgovernmentdialogues;setouttheprinciplesformanagingtherelationshipthatareenunciatedinthisReport;institutionaliseofficialbilateralexchangesandtechnicalcooperationprogramsbetweeneconomicandforeignaffairsministries,includingbranchesofthemilitary;includepolicyapproachesbetweenfederal–stategovernmentsinAustraliaandcentral–provincialgovernmentsinChina;provideforthecomprehensivesettingofstrategicbilateralobjectivesinaforwardagenda;enfoldtheagreements,mechanismsandreformsoftheChAFTAarrangement;andentrenchcooperationonimprovingeducational,culturalandpeople-to-peopleexchange.

• Bothcountriesshouldnurturethecapacitiesnecessaryfornewhigh-levelengagementthroughestablishingbytreatyagreementanewandwell-resourcedbi-nationalAustralia–China(Ao–Zhong)Commissionintheformofastatutoryentitythatoperatesindependentlyofbothgovernments.

– TheCommissionwillboostthelevelandrangeofpolicy,research,scientific,technology,education,culturalandpeople-to-peopleexchangesbetweenthetwocountries.ItsnearestparallelinAustralianexperienceisthetreatyarrangementbetweenAustraliaandtheUnitedStatesthatestablishedtheAustralian–AmericanFulbrightCommissionafterWorldWarII.

18

PartnershiP for Change

• WithintheframeworkandprovisionsofChAFTA,AustraliaandChinashouldmovetonegotiateacomprehensiveAgreementonInvestment—incorporatinga‘negativelist’approach,effectivenationaltreatmentofforeigninvestors,respectforruleoflaw,resourceaccessguarantees,andgreatermobilityofpeople—aheadofChineseagreementswiththeEuropeanUnionandtheUnitedStates.TheAgreementonInvestmentcanserveasamodelforaregionalinvestmentregimeinEastAsia.InvestmentflowsfromChinatoAustraliaandfromAustraliatoChinawillplayacriticalroleinthedevelopmentoftheneweconomicrelationshipfromexchange,toinvestment,andnowtopartnership.

– ThiswillnotbeachievedifthebroadercommunitydoesnotgraspthebenefitsofforeigninvestmentinbothAustraliaandChina.InAustralia,thismeansacceptingequaltreatmentforChineseinvestmentandreconsideringattitudestowardsstate-ownedinvestorsfromallcountries.InChina,itmeansbuildingrespectforruleoflawtomakeinvestmentssecureandpredictableforalldomesticandinternationalparties.

• ThereengineeringofthebilateralarchitecturethatisproposedshouldbealignedwiththeAustraliangovernment’sNationalInnovationandScienceAgendaandtheChinesegovernment’sinnovationpriorityinits13thFiveYearPlan.

– Thiswouldseetheprioritisationofbilateralcooperationinfutureopportunitiesinresearchanddevelopment,capitalsourcing,STEMcollaboration,researchcommercialisation,techlandingpads,thedigitaleconomy,andexchangesbetweenAustralianandChineseentrepreneursandinvestors.

• AustraliaandChinashouldattachtopprioritytotheconclusionofahigh-standardagreementontradeandinvestmentliberalisationandongoingeconomiccooperationarrangementsintheAsiaPacificundertheRegionalComprehensiveEconomicPartnership.

• Thetwocountries’sharedinterestintheG20andconstructiveparticipationinglobaleconomicgovernanceshouldfocusonChina’sroleinmutualsupportamongthemajorcurrencies;securingtheinternationalfinancialsafetynettoprotectagainstthespreadoffinancialcrises;connectingreformtoeconomicgrowth;andintensifyingeffortstoreformthemultilateraltradingsystem.

• Importantly,ChinaandAustraliashouldinstigatetop-levelregionaldialogueswithJapan,SouthKorea,India,theUnitedStatesandotherkeyplayersintheregionontheenergytransformationthatisnecessarytomitigateclimatechangeandotherenvironmentalissues.ThisisafruitfulareaforregionalcoalitionbuildingonanissueinwhichChina,asitseekstoreconcileincreasingenergyusewithitsenvironmentalambitions,andAustralia,asamajorenergysuppliertotheregion,haveamajorstake.ItisalsoanareainwhichcooperationwithotherAsiaPacificcountriescouldbeveryproductivepolitically.

Ifthesestepsaretaken,theAustralia–Chinarelationshipwillbetakentoawhollynewlevel.Whilefullyrespectfulofeachother’sexistingrelationships(suchasAustralia’sANZUSrelationshipwiththeUnitedStates),thenewpartnershipwillbeapowerfulforceforthestabilityandprosperityoftheregion,andindeedfortheglobalsystem.ItcanserveasaprincipalvectorofAustralianandChineseengagementwithinarapidlychangingworld.Nurturedcarefullyandimaginativelybygovernments,businesses,researchinstitutionsandotherstakeholdersonbothsides,thisdeeperpartnershipcouldbecomeoneofthemoststrategicallyvitalandproductivebilateralrelationshipsthateithercountryhasintheworld.

19

EXECUTIVE SUMMARY

20

PartnershiP for Change

21

EXECUTIVE SUMMARY

22

PartnershiP for Change

23

EXECUTIVE SUMMARY

24

PartnershiP for Change

CHAPTER1strategic importance of the relationship

25

Key messAges

ThereisnoeconomicorgeopoliticalfutureforChina,AustraliaortheworldthatwouldnotbeimprovedbyChina’ssustainedandbalancedeconomicgrowth.AndyetthefuturedirectionofChinesegrowthwillbeverydifferentfromthatoverthepastfourdecades.TheforcesofchangethathavealreadyunleashedawaveofconsumptiongrowthareaffectingtherelationshipwithAustraliaprofoundly.EconomicreformandliberalisationcanintensifytheongoingchangeinthestructureoftheChineseeconomyand,whilethesechangesimplyalessheavyrelianceinAustraliaontheresourcesectorforeconomicgrowth,thereareopportunitiesforgrowththatwillrequiresubstantialrepositioningofpolicyandcommercialstrategiesbybothcountriesandthedevelopmentofastillcloserrelationshipbetweenthetwocountries.

ThestructuraltransformationoftheChineseeconomyasitgrowstowardhigh-incomestatuswillbefuelledbydomesticreformsthatmaketheallocationofresourcesmoreefficientandbytheopeningofthecapitalaccount,astepthatshouldbeundertakenincrementallyandwithduecaution.Chinawillreorientitseconomytowardsdomesticconsumption.Australia’schallenge,meanwhile,istocounteractthefallinrealincomesthathasresultedfromthefallincommoditypricesasChinesedemandslows,andtoinvestinfillingtheinfrastructuregapsthatwillactasabrakeonproductivityandincomegrowthifleftunaddressed.

Therecenthistoryofthegrowingtiesbetweenthetwocountriesshowsthatthedeterminedpursuitofadeeperrelationshipyieldstangiblebenefits.TheinstitutionsandpolicyframeworksthathaveemergedtoprovidestructurefortherelationshipinrecentyearsprovideastrongstartingpointforthenextphaseoftheAustralia–Chinapartnership.

Bothcountrieshaveinvestedheavilyintheirpartnership.Thepath-breakingrecordoftheAustralia–Chinapartnershipinopeningtheresourcetrade,foreigninvestment,regionalcooperationinitiativesandChina’saccessiontotheWTOprovidesalegacyonwhichtobuildnewinternationalstandardsintotheirbilateraltrade,investmentandallotherdealings.Theirhigh-levelComprehensiveStrategicPartnershipandChAFTAaremajorinstitutionalassets(embodyingmutualtrustandpracticalcommitment)thatcanbedeployedtomanagechangeoverthedecadesahead.Stillcloserengagementandinstitutionalarrangementsareneededtocapitaliseontheopportunitiesthatthesefoundationspresent.

ChAFTAisablueprintforinitialchange,notanend-pointinthebilateralrelationship.Ajointworkplanforachievingchangewillnotonlydefineprogressinthebilateraltrade,investmentandcommercialrelationshipoverthecomingdecade;itwillalsoprovidethefoundationforAustraliaandChinapushingliberalisationandreformintheAsianregionandsettingoutthepathwaytowardsreformandstrengtheningoftheglobaltradeandeconomicsystems.Precedentexistsininstitutionalframeworkssuchasthe1976BasicTreatyofFriendshipandCooperationbetweenAustraliaandJapanforacomprehensivebilateraltreatytoprovideanoverallguidingstructurefortheAustralia–Chinarelationshipasitmatures.

26

PartnershiP for Change

Thescaleandsignificanceofdevelopmentsthatarenowtakingplace—especiallyinChinathroughitstransformationtowardsahigh-incomeeconomy—recommenddeeperbilateralinstitutionalarrangementsbetweenAustraliaandChina.Thesewouldbuildonexistingbilateralframeworkswithboldnewbi-nationalinitiatives,includingintheareasofinvestment,tourism,peoplemovement,science,andeducationalexchanges.Theywillneedtocaptureopportunitiesintherelationship,andmanagetheinevitablerisksandprocessesthatareaconsequenceoflarge-scalechange.

Bothcountriesshouldworktogethertostrengthentheestablishedregionaleconomiccooperationarrangementsandtosecuretheframeworkofpoliticalconfidenceandsecuritywithinwhicheconomicprosperitycanbeattained.ButtherearegapsinregionalpolicystrategiesthatAustraliaandChinamustnowworkmoreactivelywithregionalpartnerstofill.TheAustralia–Chinarelationshipisanchoredinglobalinstitutionalandpoliticalarrangements.Australiahasadirectandimportantstake,inpartnershipwithChina,inworkingtoensureChina’ssuccessintheassumptionofitsroleofsharedleadershipinglobaleconomicaffairs.

Inthecomingdecade,Australia’srelationshipwithChinawillbeatoppolicypriority.TradewithChinaaccountsforalmostaquarterofAustralia’soveralltrade,withChinaabsorbingalmostathirdofAustralia’stotalmerchandiseexports(DFAT2016e).Chinaisthefifth-largestsourceofforeigndirectinvestmentintoAustraliaandformanyAustralianbusinessesChinarepresentsanenormousgrowthmarket(ABS2016f).WhileAustraliaisChina’sseventh-largestsourceofimports,Australiaisalsoamajorandreliablesourceofstrategicindustrialrawmaterialsandhigh-qualityinputs,fromironoretoeducation,whichChinaneedstofuelitsindustrialisationandurbanisation.TherelationshipbetweenAustraliaandChinaisintegraltotheirotherimportantinternationalrelationships.

WithremarkablesuccessintheachievementofhigherincomesandwagesinChina,thepaceofgrowthisslowingasreadysuppliesoflowcostlabourareexhausted.TheshiftinChinafromexport-andinvestment-ledgrowthtogrowthbasedondomesticdemand,andespeciallydomesticconsumption,hascontributedtothedeclineoftheAustralianresourcesboom.

AsChina’sgrowthmodelandfocusshiftsandAustraliaseekstodefineaprosperouseconomicfuturelessreliantonitsresourcebase,bigchangesareboundtooccurintherelationship.Somebigchangeshavealreadytakenplaceandnewopportunitiesareemergingforbothcountries.Thetransformationtowardsproductivityandinnovation-ledgrowth,financialmarketreformandcapitalaccountopennesswillpropelChina’sdeeperintegrationintotheglobaleconomy.AricherChinawithamoreopenservicesindustrywillgainnewstandingamongthemajoreconomiesoftheworld.Australia’sshifttomorehumancapital-drivengrowth,togetherwiththechangesinChina,providetheopportunitytoforgenewcomplementaritiesbetweenthetwocountries,profoundlyreshapingtheirbilateralrelationshipoverthedecadeahead.

AsproductioninsomeofChina’sheavy,resourceandenergy-intensiveindustriesispeaking,thepriceofAustralia’sexportsofcommoditiessuchasironoreandcoalhasfallen.Aseconomicrebalancingtowardsconsumptionandservicesector-ledgrowthcontinues,theshareofheavyindustryintheChineseeconomywillinevitablydecline.YetChinesedemandforresourcesandenergywillremainlargeasurbanisationcontinuesinChinaandAustralia’s

27

CHAPtER 1: Strategic importance of the relationship

shareinChina’sresourceimports,whichhasrisenaspriceshavefallen,islikelytostayhigh.Asoneoftheworld’sleadingandmostcompetitivesuppliersofarangeofindustrialinputs,AustraliawillremainamajoranchorinChina’sexternalresourcesecurity.Increasingly,however,thetraderelationshipwilldiversifybeyondcommoditiesintoawiderrangeofgoodsandservices.Thetwocountries’investmentandfinancialintegrationwillbecomedeeperandmoresophisticated.Australiacanaimtobecomeamajorsupplierofknowledge,skillsandproductssupportingChina’snextstageofdevelopment,whichinvolvesanemphasisonhighvalue-addedindustries,innovationandcleanproductionprocesses.IndustrialrestructuringandupgradinginChinawillseeChina’smachineryandequipmentexportsbecomemoreimportanttoAustraliaandwilldiversifyChineseinvestmentintotourism,financeandinfrastructure.

AustraliaandChinahaveplayedakeyroleineconomiccooperationinAsiaandthePacific,regionswhichincludeeconomiesthatarethefastest-growingandmostdynamiccentresofglobaleconomicactivity.Throughregionalandmultilateralforums,bothcountrieshaveworkedcloselytopromotedevelopment,stabilityandstrongerregionalcooperation.Theyhaveadeepintersectionofinterestinstrengtheningestablishedregionalarrangements,suchasAPEC,theASEANPlusframeworksandtheEastAsiaSummit,andinglobalinstitutions,especiallytheG20.Theyalsohaveasharedinterestinsecuringtheframeworkofpoliticalconfidenceandsecuritywithinwhicheconomicprosperitycanbeattained.

ThegrowthofChina’simportanceintheworldeconomyhasoccurredveryrapidlyandhasbroughtwithitnewcapacity,responsibilities,expectationsandchallengesinmanagingitsinterdependencewiththerestoftheworld.

TheChineseeconomyaccountedforlessthan3percentofglobalGDPin1980(OECD2013a).Itisnowthesecond-largesteconomyintheworldinnominalterms,accountingfor13percentofglobalGDPincurrentUSdollars,anditsGDPislargerthanthatoftheUnitedStatesinrealpurchasingpowerparityterms(WorldBank2016).Chinabecamethesinglelargestcontributortoglobalgrowthin2007andhasmaintainedthatpositioneversince(Yueh2015).Chinaistheworld’slargestgoodstraderandisalsotheworld’ssecond-largestimporterofgoodsandservices,makingitamajorelementinglobaldemandfortradedgoodsandservices(Austrade2015a;WorldBank2016).

Untilrecently,Chinawasmainlyarule-takerintheglobaleconomicsystem.Sincethelate1970sithasbenefitedenormouslyfromopeningitseconomyandparticipatinginthepost-BrettonWoodssystem.China’sroleinglobaleconomicgovernanceremainedpassive,constrainedbythesmallsizeandlowcapacityofitseconomy.NowChinaisgrowingoutofthisstageandisthereforebecomingmoreactiveintheprovisionofglobalpublicgoods.Thetransitiontojoiningtheranksofglobalrule-makersisnotautomaticoreasyforeitherChinaortheglobalsystem.ButChinaisnowactivelyparticipatinginglobalgovernanceandactivelyassumingitsinternationalresponsibilitiesandduties.AnimportantopportunityisChina’schairingoftheG20in2016.

Australiahasadirectstakeinworking,inpartnershipwithChina,toensureChina’ssuccessintheassumptionofitsroleofsharedleadershipinglobaleconomicaffairs.ThereisspecialvalueinthedevelopmentofthispartnershipbecauseofAustralia’suniqueroleintheregionaswellasitsclosenesstotheUnitedStates.ThevalueofthepartnershipincludesthechanceofworkingwithChinainthedevelopmentofitscontributiontotheprovisionofinternationalpublicgoods,boththroughestablishedinternationalinstitutionssuchastheIMF,theWTO,theWorldBankandnewinternationalinstitutionssuchastheAIIB.ItalsoincludesAustralia’s

28

PartnershiP for Change

workingtogetherwiththeestablishedandemergingpowerstobuildnewplatformstocoordinatearangeofglobaleconomicpolicieswithintheG20andtomanagethechallengestosustainablegrowthfromclimatechangeandotherenvironmentalissues.

Thisisacriticalmomentinafar-reachingglobaleconomictransition.AustraliaandChinahaveavitalopportunitytodefinehowtheywillshapethefuturecourseoftheirrelationshipinadeliberateway,establishingsomecommonreferencepointstohelpmanageitpurposefully,astheyhavewithsomesuccessinthepast,ratherthanmuddlingthroughinthefuture.

CapturingthefullbenefitoftheeconomicrelationshipwilldependonhowboththepublicandprivatesectorsinAustraliaandChinaengageinanddeveloptherelationship.Managingtherisksanduncertaintiesthatcanimpactontheeconomicrelationshipwillbeimportant.Asastartingpoint,gettingthemostforbothcountrieswillrequireafunctionalunderstandingamongpolicymakers,corporateleadersandthebroadercommunityofthechangesthatwillshapeChinaandAustraliainthenext10years.ThisReportcanplayaroleinthis.Theunderstandingthathasbeenbuiltthroughthisworkcanbeembeddedininstitutionalformstohelpfacilitatebettermanagementoftherelationship.ChAFTArepresentsamajorstepinputtinginplacestrongerinstitutionalarrangementsforthedevelopmentoftradeandinvestmentlinks.Butarelationshipofthekindthatwillberequiredbythechangesinbotheconomies,theireconomiccooperationintheregionandtheirpartnershipinglobalaffairsincomingdecades,demandssubstantialjointpolicyinitiativeandstrengthenedinstitutionalframeworks(bothgovernmentandprivate).

In1976,AustraliasignedaBasicTreatyofFriendshipandCooperationwithJapan,anagreementwhichsetouttheprinciplesunderpinningtheirbilateralrelationship,definedkeyareasofcooperation,andpledgedtoenshrineandpreservetheprincipleofnon-discriminationineconomicrelations.Sinceitssigning,theTreaty,andthemutualconfidencethatitgavebothJapanandAustralia,hasprovidedtheframeworkwithinwhichclosertieshaveforged.TheopportunityforevolvingasimilarframeworktounderpintheAustralia–Chinarelationshipshouldnotbepassedup.ChAFTAcanprovidethebeginningsforsuchaframework.

economic transformation in China and Australia

china

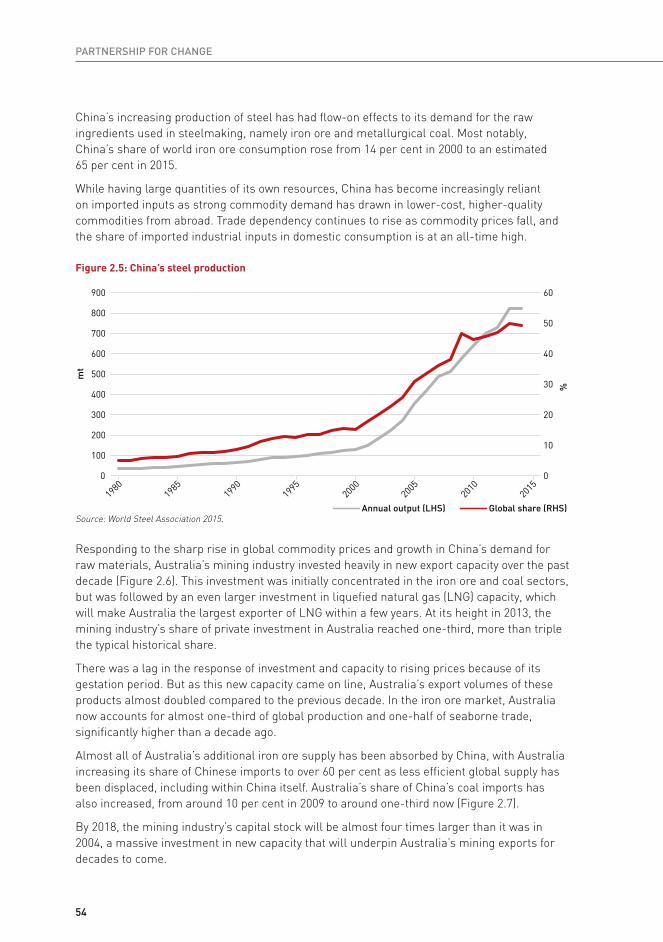

TheChineseeconomyisundergoingamajortransformationafternearly40yearsofhigh-speedeconomicgrowth.China’srapideconomicrisehasbeenfuelledbymarket-orientedreformsandeconomicliberalisationthathelpedreducethedistortionsinresourceallocationintheeconomy.Thereformwasmorethoroughinthegoodsmarketthaninfactormarketsforland,labour,capitalandenergy,whichremainedundertighterstatecontrol.Thisgrowthmodelencouragedinvestmentinmanufacturingcapacityandinfrastructure.

WithrealGDPgrowthataround10percentperannumfromthe1980s,manufacturingoutputisnowlargerthanthatinanyothereconomyintheworld.Chinaaccountedforaquarterofworldmanufacturingoutputby2015,upfromlessthan3percentin1990.Chineseconsumptionhasdominatedtheglobalmarketsforindustrialrawmaterials(WorldBank2016).Theexpansionoftheironandsteelindustry,forexample,whichproducedover800milliontonsofcrudesteelin2015,ormorethansixtimesasmuchasitdidin2000,liftedtheChineseshareinworldironoreconsumptionfrom14percentin2000toanestimated65percentin2015(Figure1.1).ThissurgeinChinesedemanddroveamorethanfive-foldriseofpricesintheyearsfrom2000–2008inthescrambleforadditionalsuppliesofironore(RBA2012).

29

CHAPtER 1: Strategic importance of the relationship

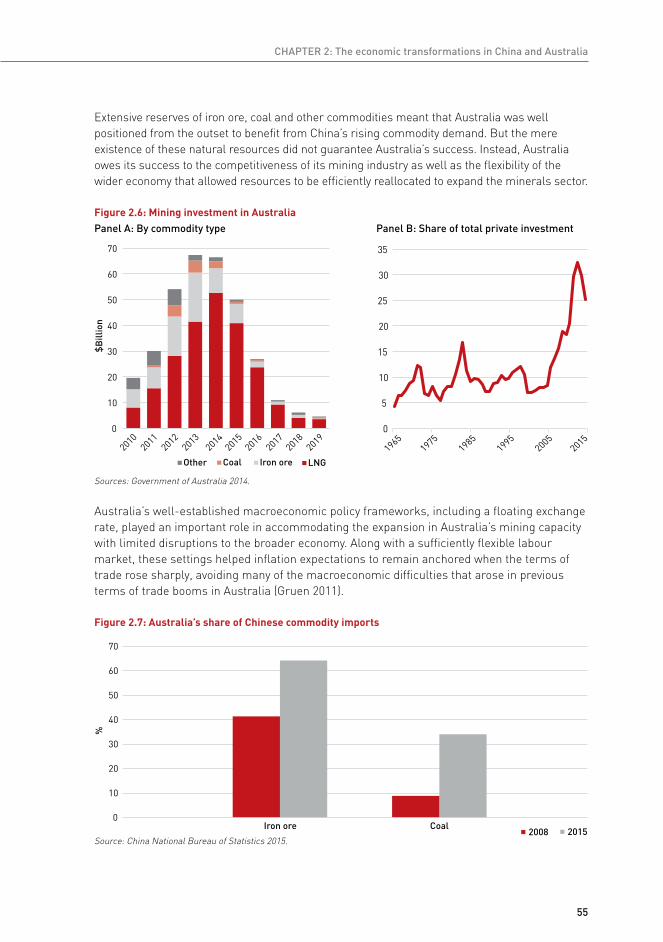

Australia’sestablishedcompetitivenessininternationalresourceandenergymarkets,relativegeographicproximityandcloseengagementsinceChina’seconomicopeninginthe1970s,madeAustraliaanaturalandcomplementarypartnerinChina’stradeandindustrialtransformation.AustraliahasbeenananchorinNortheastAsianresourcesecurityandapioneerintheexportofhighqualityresourcestoChina.AustraliabecameChina’sprincipalsupplierofimportedironore,coalandarangeofotherindustrialrawmaterialsovertheseyears.In2015,Australiasupplied64percentofChina’simportedironore,forexample,comparedwiththe43percentitsuppliedin2010(Ng2016).TherelationshipwithChinasawmassiveinvestmentintheAustralianresourcesectorinthefirstdecadeofthe21stcentury,andstronggrowthinAustraliathroughouttheglobalfinancialcrisiswhengrowthinotherindustrialeconomieslanguished.

WhileChina’sinvestment-ledgrowthdeliveredastonishingoutcomes,italsoledtostructuralimbalancesthatincreasinglythreatenedsustainablegrowthandstability.

China’sreformsnowaimtoremovethosedistortions,especiallyinthefinancialmarket,andnurtureconsumption-andservice-ledgrowth.TheChinesegovernmentisalsoimplementingmeasurestoclosedowncapacityinheavyindustries,suchasironandsteel,thatdoesnotembodybest-practiceproductiontechnologyorenvironmentalprotection.Thisentailssubstantialcostsofadjustmentandtheneedtomanageeconomicaswellassocialdislocation.Thefocusofgrowthisnowonthe‘neweconomy’.Thechangeingearfromdouble-digittosingle-digitgrowthisexpectedtoputtheeconomyonamoresustainable,butstillrelativelyhigh,long-termgrowthtrajectoryoverthecomingdecade.

Figure 1.1: Chinese and global steel production

0

200

400

600

800

1000

1200

1400

1600

1800

China World World Excluding China

Mill

ion

Tonn

es

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Source:WorldSteelAssociation2015.

AmongthenationaleconomicpolicycommitmentsthatarelikelytohavethemostprofoundeffectonChina’srelationswithAustraliaandothercountriesistheChinesegovernment’s13thFiveYearPlancommitmenttobuildanopeneconomicsystem,deepenfinancialsystemreform,liberalisefinancialmarketsandacceleratetherealisationofChinesecapitalaccountconvertibility.

30

PartnershiP for Change

CapitalaccountliberalisationisessentialtomakingChina’srenminbiatrulyglobalcurrencyandincreasingChina’sroleininternationalfinance.InclusionoftherenminbiintheIMF’sSpecialDrawingRightsbasketisafirststepinthisprocess.Fortherenminbitobecomeatrulyinternationalcurrency,however,Chinaneedstohaveanopencapitalaccount.Butthesignificanceofcapitalaccountliberalisationismuchmorewide-rangingthanrenminbiinternationalisation.

FinancialreformandcapitalaccountliberalisationarecentraltorebalancingtheChineseeconomyandfosteringinnovationandproductivitygrowth.Marketreformsandmarket-determinedinterestratesandexchangerateswillcorrectthemisallocationofcapitalthathasuntilnowfavouredparticularregions,state-ownedenterprisesandthestatebankingsector,andcrowdedoutfinancingandinvestmentfromthemoredynamicprivatesector.Healthyandwell-managedfinancialinstitutionsareattheheartoffinancialandeconomicstability.ThesechangeswillhelpChinatomovethroughtheso-called‘middle-incometrap’andtobecomeahigh-incomesociety.Capitalaccountliberalisationcouldalsoassistwithgeopoliticalstabilityintheregionthroughgreatereconomicandfinancialintegration.

ThescaleofChina’scross-bordertradeandinvestmentpaymentsandtheimportanceofusingmarketmechanisms(inparticularafullyflexibleexchangerateandarobustandmoreefficientfinancialmarket)tomanagetheinteractionbetweenthedomesticandinternationaleconomieseffectivelyrequirethemovetoanopencapitalaccount.

LiberalisingChina’scapitalaccountisanenormouschallengeanditwilltaketime.ThenervousnessininternationalmarketsaboutChinesestockmarketvolatilitiesandthemovetoanewforeignexchangerateregimewithmoreflexibilityagainstacurrencybasketoverthepastyearisaharbingerofthedifficultiesinmanagingthispolicychange.Theoverridinglessonoffinancialhistoryaroundtheworldisthattransitionsarenevereasyorsmooth.ThishasbeennolesstrueinChinathanithasbeeninothereconomiesthatareintheprocessofprofoundtransformation.Therehastobepolicytrialanderror,andtherewillinevitablybesomemissteps,butallcountrieshaveaninterestinensuringthatChina’sreformssucceed.

Theprocessofcapitalaccountliberalisationneedstobeincremental,builtonrobustinstitutionsandmarkets,andcarefullystagedandtimedtoavoidpotentiallysubstantialfinancialandforeignexchangerisks.Thisisnotjustatechnicaleconomicchallenge.IntegrationofChinaintointernationalcapitalmarketsrequiresChinatohaveamuchmoreopen,transparentandpredictablesetofinstitutionalarrangementstobuildinternationalconfidenceindealinginChinesefinancialassets,andthiswillpushattheenvelopeofpoliticalreform.

Thetrajectoryofgrowthisslowinginthistransition.Manufacturingandexportgrowthisslowing.WhileChinawillremainabigexporter,exportgrowthislikelytoslowasthestructureofexportsisupgraded.ThemassiveurbanisationthathasalreadytakenplaceinChinawillcontinueastherateofurbanisation—nowat56percentofthepopulation—stilllagsbehindthatinmanydevelopingeconomieswithsimilarincomelevels,letalonethatinadvancedeconomies(CCTV2016).Thisrequirescontinuing,albeitslower,expansionofinfrastructureinvestment.Newinvestmentwillalsobedrivenbytheneedforcleanenergyandenvironmentalprotection.

HigherChinesewagesasthelabourmarkethastightened,aswellastheremovalofsomedistortionsthatfavouredinvestmentratherthanconsumption,havemeantthatgrowthisincreasinglydrivenbyconsumerdemand.Thistrendhasbeenunderwayforsometime,with

31

CHAPtER 1: Strategic importance of the relationship

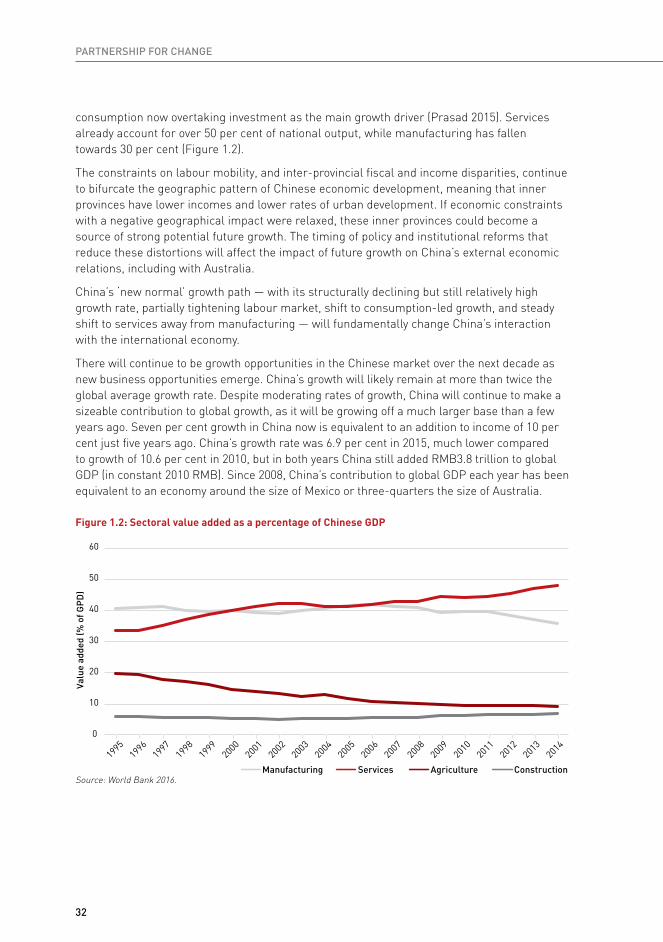

consumptionnowovertakinginvestmentasthemaingrowthdriver(Prasad2015).Servicesalreadyaccountforover50percentofnationaloutput,whilemanufacturinghasfallentowards30percent(Figure1.2).

Theconstraintsonlabourmobility,andinter-provincialfiscalandincomedisparities,continuetobifurcatethegeographicpatternofChineseeconomicdevelopment,meaningthatinnerprovinceshavelowerincomesandlowerratesofurbandevelopment.Ifeconomicconstraintswithanegativegeographicalimpactwererelaxed,theseinnerprovincescouldbecomeasourceofstrongpotentialfuturegrowth.ThetimingofpolicyandinstitutionalreformsthatreducethesedistortionswillaffecttheimpactoffuturegrowthonChina’sexternaleconomicrelations,includingwithAustralia.

China’s‘newnormal’growthpath—withitsstructurallydecliningbutstillrelativelyhighgrowthrate,partiallytighteninglabourmarket,shifttoconsumption-ledgrowth,andsteadyshifttoservicesawayfrommanufacturing—willfundamentallychangeChina’sinteractionwiththeinternationaleconomy.

TherewillcontinuetobegrowthopportunitiesintheChinesemarketoverthenextdecadeasnewbusinessopportunitiesemerge.China’sgrowthwilllikelyremainatmorethantwicetheglobalaveragegrowthrate.Despitemoderatingratesofgrowth,Chinawillcontinuetomakeasizeablecontributiontoglobalgrowth,asitwillbegrowingoffamuchlargerbasethanafewyearsago.SevenpercentgrowthinChinanowisequivalenttoanadditiontoincomeof10percentjustfiveyearsago.China’sgrowthratewas6.9percentin2015,muchlowercomparedtogrowthof10.6percentin2010,butinbothyearsChinastilladdedRMB3.8trilliontoglobalGDP(inconstant2010RMB).Since2008,China’scontributiontoglobalGDPeachyearhasbeenequivalenttoaneconomyaroundthesizeofMexicoorthree-quartersthesizeofAustralia.

Figure 1.2: sectoral value added as a percentage of Chinese gDP

0

10

20

30

40

50

60

Manufacturing Services Agriculture Construction

Valu

e ad

ded

(% o

f GP

D)

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Source:WorldBank2016.

32

PartnershiP for Change

AsFigure1.3suggests,theIMFexpectsthatChinawillcontinuetoaddmoreeachyeartoglobalGDPoverthecomingdecade(inUSdollars).ChinaislikelytoremainthebiggestcontributortoglobalGDPgrowthforthenextfiveyears,addingmoretoglobaloutputthantheUnitedStates,ormorethanIndiaandalloftheotherAsianeconomiesputtogether.

ThehugescaleofChina’seconomytoday,nonetheless,needstobeunderstoodinthecontextofitsambitionsforgrowthinthefuture.China’spercapitaincomeisstillnothigh,beingonly24percentofthatoftheUnitedStatesor34percentoftheOECDaverage(OECD2014a).Chinesepolicymakershavetomanagethetransitiontohigherincomesandkeepclosingthisgapinthecomingdecades.

Australia

China’sremarkableexpansionthroughthefirstdecadeofthecenturybroughtstronggrowthinAustralia’sminingsector.GrowthinWesternAustraliaapproachedgrowthratesinChinaduringsomeoftheseyears.Australianincomegrowthandhouseholdlivingstandardsbenefitedfromtheterms-of-trade-inducedstrengthoftheAustraliandollarasimportpricesfell.HalftheriseinAustralianincomesduringtheminingboomresultedfromtheboosttoAustralia’stermsoftrade(Downesetal2014).ItwasnotonlytheAustralianminingsectorthatbenefitedfromChinesegrowth:Australia’seducationexportsandtourismservicesgrewstrongly,accompaniedbysharprisesinChina’sshareofthesemarkets(Austrade2015b).China’sshareofAustralianexportsgrewstronglyandishigherthanthatofothermajorexportcustomers(Figure1.4).Whiletheeconomyasawholeunambiguouslybenefitedfromtheminingboom,somesectors,suchastrade-exposedmanufacturers,sawdemandfortheirproductsfallbecauseofAustralia’selevatedexchangerate.Asdramaticastheywere,thesechangeswerepartofalong-termstructuraladjustmentintheAustralianeconomythatwasalreadywellunderwayandwouldhavesubstantiallyoccurredevenwithouttheminingboom.

Figure 1.3: China’s gDP growth (RHs) and its contribution to global output (LHs), 1990–2020

0

2

4

6

8

10

12

14

16

-200

0

200

400

600

800

1000

1200

1400

1600

Bill

ion

US$

GD

P G

row

th %

GDP contribution to global output (US$) GDP growth %

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Source:IMF2015.

33

CHAPtER 1: Strategic importance of the relationship

Figure 1.4: exports to China as a share of total exports, Australia and other major exporters

40

35

30

25

20

15

10

5

0

%

Australia

Taiwan

Korea

India

Vietnam

New Zealand

Japan

Philippines

Singapore

Malaysia

Thailand

Indonesia

2007 2010 2014

Source:Gruenwald,ContiandRana2016;UNCTAD2015.

SlowergrowthinChinesedemandfor,andincreasedglobalsuppliesof,industrialrawmaterialshavesentironoreandothercommoditypricesdramaticallylower.ThedropinpriceshascausedtheshareofcommoditiesinChina’simportstocontract.ButAustraliahasincreaseditsshareinChina’simportsofindustrialrawmaterials(althoughimportvalueshavedroppedsharply)becauseAustraliacontinuestobeoneoftheworld’smostcompetitivesuppliersofcommoditieslikeironore.Newenergyprojects,inthegasanduraniumsector,willalsocomeonstreaminthenearfuture.ButgrowthinresourceexportstoChinaisunlikelytoreturntotherateseenduringthe2000s,andpricesarelikelytoremainsubdued.

Asinpastcommoditycycles,priceshavefallen(alongwiththetermsoftrade)asnewmineshavecomeonlineinAustraliaandaroundtheworld,draggingAustralianrealincomesdownatthesametime.Thistrendislikelytocontinue,althoughthereislikelytobevolatilityaroundthistrend.Australiawillovercomethisdragonincomegrowthonlythroughitsowneconomictransformationandthroughliftingproductivityacrossthewholeeconomy.

SuccessfuladjustmentandsustainedgrowthoverthecomingdecadewillrequireashiftinAustralia’seconomicstructurebacktoamorenormaltrajectory:awayfromanabnormalexpansionoftheresourcesector(evenifenergydemandcontinuestogrow)towardsresumptionofgrowthintheshareofservices,high-endmanufacturingandhighvalue-addedagriculturalproduction.Thisstructuralchange,aswellasAustralia’sstrongpopulationgrowththroughmigration,willneedlarge-scalerenovationofurbaninfrastructure,investmentininter-urbantransportandcommunications(becauseofgrowingurbancongestionandnationalconnectivitydeficiencies),newinfrastructureinvestmentandintegratedlanduseplanninginthenorthofthecountry(becauseofthelocationofnewagriculturalanddevelopmentopportunitiesthere),andinvestmentininnovation,researchandeducation.

Thesechanges,througharelativelyflexiblelabourmarketandresponsivecapitalmarket,arealreadytakingplace,butmajorchallengesremaininundertakingtoughreformsthatmaketheeconomymoreflexibleandhelptorestructureandupgradeindustry.Moreover,themarketsinwhichtheseopportunitieslieforAustraliaarefiercelycontestedinternationallyandAustraliadoesnothavethesameestablishedadvantageasithasinnaturalresources.Unless

34

PartnershiP for Change

Australia’sprivateandpublicsectorinvestmentbecomessmarter,andunlessAustraliacanmobilisecapitalathomeandfromabroadtoinvestmoreefficientlyininfrastructure,itisunlikelytoachievethe3percentGDPgrowththatithascommonlyenjoyedoverthepastfewdecades.Itwillnotbeaneasytask—totalproductivitygrowthhasbeenstagnantforsomeyears—andwhiletherearesignsofimprovement,itneedstoimprovefurther.

HoweffectivelythesechangesaremanagedwillshapethefutureoftheAustralia–Chinaeconomicrelationship.

strategic partnership for change

Inmanagingthechangeanticipatedoverthecomingdecade,boththepublicandprivatesectorscandrawuponsubstantialassetsthatalreadyexistintheestablishedbilateralrelationship.TheAustralia–Chinarelationshipisdistinguishedbyahistoryofpoliticalcommitmentatthehighestlevels,sincediplomaticrecognition,toapartnershipthathasembracedChina’sopenness,itsreformanditseconomicrise.DevelopmentoftherelationshiphasalsobeenfacilitatedbyAustralia’sopeneconomy,stronginstitutionsandrichmineralendowment,ChineseperceptionsofAustralia’sbusiness-friendlyenvironment,aswellasAustralia’sgoodstandingwithothercountries.Thoughtheyhavedifferentpoliticalandsocialsystems,bothcountriesacceptthisdifferenceandrespecteachother’sachievements,includingtheremarkableelevationoflivingstandardsandimprovementinsocialconditionsthrougheconomicreformsandliberalisationthatbothcountrieshaveputinplaceoverthepastfourdecades.

Thedeepcomplementarityoftheestablishedeconomicrelationshipandthehighpoliticalcommitmenttoitsdevelopmentbybothcountriesprovideasecurefoundationonwhichtobuildanewanddynamicpartnership.

AustralianandChinesepoliticalleadershaveinvestedheavilyintherelationshipandarenowcommittedtoitselevationasastrategicpartnershipthroughregularhigh-levelleadershipdialogues.

Maintainingtheclosenessintherelationshipatthetopleadershiplevelisapriorityforbothgovernments.Itisasignalofpoliticaltrustandgoodintentioninthepartnership.

ChAFTAisinplace—themostopenandliberalisingsucharrangementthatChinahasenteredintowithanydevelopedeconomyandonewhichgoesfurtherinitspartnercountryliberalisationthanAustralia’spreviousagreements.

Whatdothebigchangesinthestructureofbotheconomiesmeanfortheirbilateralrelationshipanditsmanagementoverthecomingdecade?

Asconsumerincomesriseandpreferencesshift,thenewpatternsofChineseconsumptionwilldrivehighergrowthinimportsofrecreationalservices(liketourism),educationalservices,healthservicesandfinancialservices.Theconsumptionandimportofhighvaluefoodstuffs,inwhichAustraliahasastrongcomparativeadvantage,areexpectedtogrowrapidlyoverthenextfewdecades.Forexample,therealvalueofbeefconsumptioninChinaisprojectedtorise236percentbetween2009and2050(ABARES2014).ChAFTAopensthedoorwidertogrowthetradeinmarketsforhighvaluegoodsandservices.ChAFTAofferstheprospectofsignificantgainsinAustralia’sshareinmarketsforimportsacrosstheboard,fromdairyproductsandhealthproductstoeducationandtourism(seeChapter3).

35

CHAPtER 1: Strategic importance of the relationship

ChAFTAopensthedoortonewopportunitiesintheservicestrade,ininvestment,intourismandinthecommoditytrade;buttherearemanyobstaclestorealisingtheseopportunitiesthatstillneedtobeovercome.Theobstacleshavetodowithhowcommercialpartiesrelatetoregulatoryinstitutionsbeyondnationalborders.Theyalsohavetodowithbuildingdeeperprivatebilateralbusinessnetworksandassociationstofacilitatebusinessbetweenthetwocountries.ThereisareviewprocessbuiltintoChAFTA—inthissense,ChAFTAisalivingagreement.Yetthenatureofthearrangementembeddedintheagreementisthatitisreactivetospecificproblemsolving—ratherthanstrategicinitspurpose,seekingopportunitiesthroughtheagreementandbeyond(seeChapters4,5and6).

AsChina’sindustrialupgradinggatherspace,Australia’simportsfromChinawillbeincreasinglydominatedbyhigher-valueappliances,equipmentandmachinery.ManyofChina’sexports,ofcourse,involvesubstantialvalue-addfromothercountriesintheregion,includingJapan,SouthKoreaandtheUnitedStates.AlargeproportionofJapanesebrandimports,fromexample,nowarriveinAustraliaviaChina.

China’scommitmenttofreeingupinvestmentabroadinthepastdecade(the‘goingout’strategy)sawAustraliaemergeasaleadingdestinationforChineseoutbounddirectinvestment.ThereformsthatarenowbeingputinplaceinthefinancialmarkethavealreadyseenChinesebanksandnon-financialenterprisesliftinvestmentinAustralianassets.Inthecomingdecade,thesereformsandwiderliberalisationofthecapitalaccountcouldfundamentallychangethestructureofeconomicrelationsbetweenthetwocountries.

FinancialmarketreformandcapitalaccountliberalisationwillalsofundamentallychangeChina’sstandingandroleintheglobaleconomy—anditsinfluenceandimportanceintheAustralianeconomy.ItwillincreasethesizeandrangeofChineseassetsheldbyAustralianinstitutionsandcorporations,aswellastheportfolioofAustralianassetsheldbyChineseinstitutionsandenterprises.ItwillseeChina’scurrencyusedmoreextensivelyininternationaltransactionsandborrowing.Chinesehouseholdsandinstitutions,notonlyenterprises,willincreasetheportfolioofassetstheyholdinAustraliaandelsewhere.

Arrangementsthatbuildconfidenceinundertakingforeigninvestmentineachcountryareapriority.DespitetheprogressmadeinChAFTA,thereremainsconfusionaboutthetreatmentofAustralianandChineseinvestorsundertheothercountry’sforeigninvestmentregimes.Policiesthatenshrinenodiscriminationagainstthesameclassofforeigninvestmentacrossforeigninvestmentsourcesandentrenchthenationaltreatmentprincipleneedtobetheanchorsofeachforeigninvestmentregime.Mechanismsfordirectcollaborationinsharinginformationanddataoninvestmentandinvestoractivitiesneedtobeputinplacebetweentherelevantagenciesineachcountry.

ThenewphasesofChineseandAustraliangrowthandtheirchangedinternationalcircumstancesrequireanewmodelofeconomiccollaborationwhichencompassesanupdateandoverhauloftheinstitutionalarrangementsthatsupportAustralia–Chinaengagement.

Aninstitutionalframeworkthatdynamicallydrivesbilateralstrategicengagement,promotingthenewopportunitiesfortradeandinvestmentintherelationshipthroughandbeyondChAFTA,willprovidesubstanceattheworkingleveltothestrategicpartnershipbetweenthetwocountriesatthetop.

Thetaskistocapitaliseonandmanagechange.ItwillrequireenergisinganddeepeningtheinstitutionalarrangementsthatarealreadyinplacebetweenAustraliaandChinato:

36

PartnershiP for Change

buildtrustaroundcommoninterestsineconomicandpoliticalrelationships;managetheuncertaintiesthatinevitablyarisethroughchange;anddeveloptheup-closecommercialandbusinessengagementneededasthestructureoftheeconomicrelationshipshiftstowardsservicesandconsumers.

Thisisanationaltaskforeachcountry.Itisalsoabi-nationaltaskthatembracesnewundertakingsandagreements.

TheframeworkofanewmodelforeconomiccollaborationwouldincludejointmechanismsandworkinggroupsthatbuilduponestablishedpartnershipsingovernmentsuchastheComprehensiveStrategicPartnership,theStrategicEconomicDialogueandtheJointMinisterialEconomicCommissionattheleaderandministeriallevels,aswellasofficialagencypartnershipssuchasthatbetweentheAustralianTreasuryandChina’sNationalDevelopmentandReformCommission(NDRC)andthetiesthataregrowingbetweentheReserveBankofAustralia(RBA)andthePeople’sBankofChina(PBoC).Thesepartnershipsshoulddrawuponbusinessandoutsideexpertise,asrequired,to:

• adviseinthedevelopmentoftheComprehensiveStrategicPartnershipdialogues;

• supportjointtaskforceorworkinggroupactivityonissuesflowingfromthedialoguesorotherbilateralinitiatives;

• workwithstateandprovincialauthoritiesindevelopinginitiativesintherelationship;

• encourageprogramsofresearchwithinandbeyondgovernmentonallaspectsoftherelationship;

• engagewiththebusinesssectorsinbothcountriesinundertakingitswork;