paid claims transportation services presented by: mca c - erlewine medicaid program... · medicaid...

TRANSCRIPT

Medicaid Program Integrity

Fraud, Waste & Abuse

Presented by: Kristi Erlewine

1

DAVE YOSTOhio Auditor of State

5.3% to $3.0 trillion ($9,523 per person)

Medicare 5.5% to $618.7 billion

20 % of total NHE

Medicaid 11.0% to $495.8 billion

16 % of total NHE

2014 National Health Expenditures

2

o Any payment that should not have been made or was made in an incorrect amount

o Examples:

• Duplicate payments;

• Payments to ineligible recipients;

• Incorrect amounts paid; and

• Payments for which insufficient or no documentation was found.

Improper Payment Definition

3

4

Improper Payments – Current Status

The FFY 2015 government-wide improper payment estimate totaled $136.7 billion, an increase of $12 billion from the prior year.

FFY 2015 Government-wide Improper Payment Estimates by Program

5

$21.9$19.2

$14.4$17.5

$29.1

8.1%

7.1%

5.8%6.7%

9.8%

$0

$5

$10

$15

$20

$25

$30

$35

0%

2%

4%

6%

8%

10%

12%

2011 2012 2013 2014 2015

Imp

rop

er P

aym

ent

Est

imat

e(i

n b

illi

on

s)

Err

or

Rat

e

Fiscal Year

Medicaid Improper Payments

6

CMS annually estimates the amount of improper payments in Medicaid

Payment Error Rate Measurement (PERM)

CMS randomly samples a subset of payments for review against federal and state policies

Average sample size per state : 450 Fee-for-Service & 210 managed care

Medicaid Improper Payment Overview

7

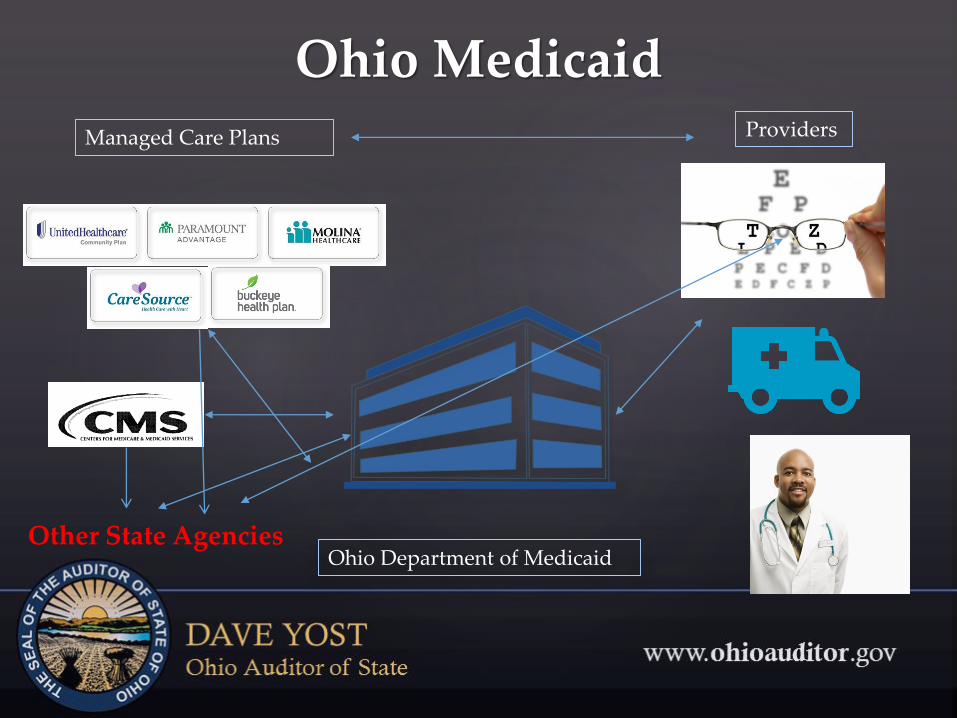

Ohio Medicaid

Ohio Department of Medicaid

Managed Care Plans Providers

Other State Agencies

Medicaid in Ohio

9

0

0.5

1

1.5

2

2.5

3

3.5

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016

Medicaid Recipients by Year

Medicaid in Ohio

10

0

2,000,000,000

4,000,000,000

6,000,000,000

8,000,000,000

10,000,000,000

12,000,000,000

14,000,000,000

16,000,000,000

18,000,000,000

20,000,000,000

FY

2002 A

FY

2003 A

FY

2004 A

FY

2005 A

FY

2006 A

FY

2007 A

FY

2008 A

FY

2009 E

FY

2010 A

FY

2011 A

FY

2012 A

FY

2013 E

FY

2014 A

FY

2015 E

FY

2016-B

FY

2017-B

Medicaid Expenditures by Year

• PIG

• MCPIG

• PIGRx

• PiggyBank

• Charlotte’s Web

• O.H.I.O.

Ohio’s Program Integrity Groups

11

• Materiality

• Change in Reimbursement

• Complexity

• Strength of Rules

• Recent Rule Changes

• Recent Industry Changes

• Control Factors

• Fraud Risk Factors

Definitions of Risk Factors

12

Medicaid Contract Audit Section

13

• A cost report payment methodology “settles” payments by calculating a final actual rate

• Advantages: provides a mechanism to report certified public expenditures and to evaluate cost trends

• Disadvantages: Time consuming

What is a Cost Report and why use one?

14

Where can things go wrong?

15

Inflating/Shifting costs to federal programs

Additional Risks With Reporting Costs

16

• Services that were never rendered

• Upcoding

• Medically unnecessary services

• Kickbacks

Common Types of Healthcare Fraud

17

• Misrepresenting non-covered treatments

• Falsifying a diagnosis

• Unbundling

Common Types of Healthcare Fraud

18

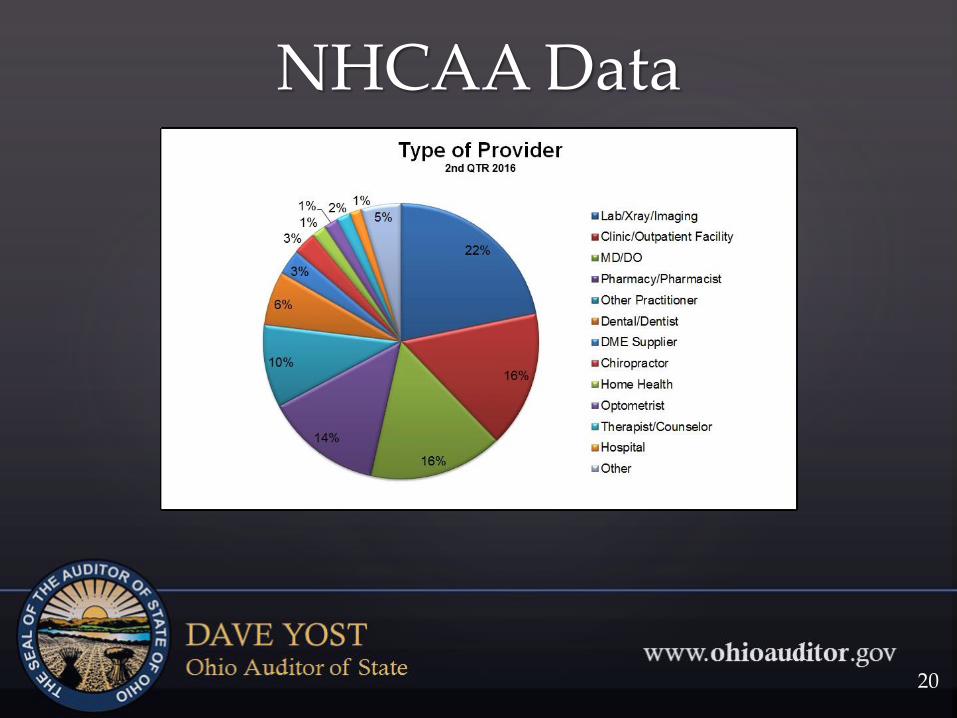

NHCAA Data

19

NHCAA Data

20

SFY 2012 through SFY 2016

• Released 98 provider examinations

• Findings of over $15.5 million

• Average of $158 K per provider

• Track ROI – average across this timespan -5:1

AOS Compliance Examinations

21

• Provider Type

• Rules/Laws/Other Applicable Criteria

• Procedure Codes

• Procedure Modifiers

• What constitutes a unit

Before Looking at Claims Data

• Reporting – Statistics, Graphing Data

• Patterns in the data –

oGap Detection

oPotential Duplicates

What Do We Do With the Data Once We Have It?

• Procedure Code/Modifier

• Date of Service

• Recipient Date of Service

oDate of Death

o Inpatient or care facility

Analyzing the Data

• Unusual modifiers

• Volume indicators

• Recipients with high number of services per date of service

• Recipients with same address receiving same type of service on the same date

Red Flags

Provider Selection Process

Provider Selection Process

# of Average %Provider Type Samples of Error

Transportation 30 77.8%Nurses 18 32.3%Home Health Agency 17 32.7%Personal Care Aide 9 50.8%School Med Program 9 50.2%Physician (& Group) 7 31.7%Psychiatric Services 6 32.0%Psychological Services 3 72.3%DME & Supplies 2 55.8%Emergency Res. Sys. 2 27.5%Podiatry 2 2.5%Dental 1 31.9%

Total: 106 50.2%

Sampling Results by Provider Type

30

Sources of Improper PaymentsDocumentation

31

Provider

Qualifications

Service

Authorization

Sources of Improper Payments

32

Sources of Improper PaymentsBilling Practices

33

Sources of Improper PaymentsNot A Covered Service

34

Contact Information

35

Ohio Auditor of StateDave Yost

88 E. Broad St.Columbus, Ohio 43215

Phone: (800) 282-0370 Fax: (614) 466-4490Email: [email protected]

www.OhioAuditor.gov