pagasa philippines inc. -...

TRANSCRIPT

Pagasa Philippines Inc.

ANNUAL REPORT

Pagasa Philippines Inc. Annual Report 2016 1

About Pagasa

Pag-ASA Philippines Lending Company, Inc. (PPLCI) was registered with Securities and

Exchange Commission (SEC) on June 2007 offering financial assistance to economically poor

Filipino entrepreneurs and empowering them through better access to financial credit.

Pag-ASA ng Masang Pinoy Foundation, Inc. (PMPFI) started as the social arm of Pag-ASA

Philippines on the same year but operation started in 2009. It envisions serving more micro-

entrepreneur in the remote countryside.

Pag-ASA ng Pinoy Mutual Benefit Association, Inc. (PPMBAI) was registered on 28th Dec 2012,

in SEC and on 11th of April 2013 in Insurance Commission as part of the safety net of PPLCI and

PMPFI’s borrowers. Its overall goal is to improve the risk protection of poor households in areas

of operation by launching a sustainable micro-insurance project.

The three organizations collectively known as Pagasa seek to pursue the mission of providing

micro credit and micro insurance services to economically poor entrepreneur Filipinos and aim

to empower them by helping them access credit for their income generating activity, help

increase family income that will improve their economic condition, provide safety nets in times

of death and accidents, and become social investors in community development using the well-

known ASA Methodology. Pagasa also aims to create employment for the community and/or

locality supporting micro projects to the members and job placement in the community.

Pagasa Philippines Inc. Annual Report 2016 2

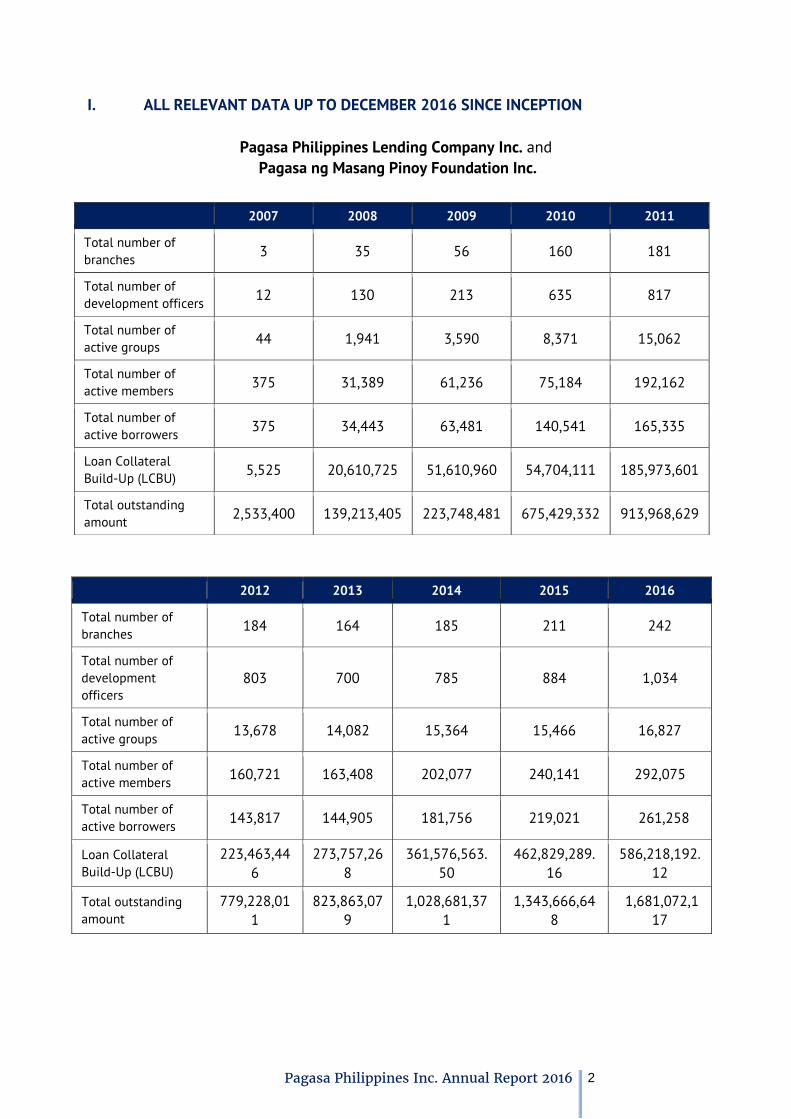

I. ALL RELEVANT DATA UP TO DECEMBER 2016 SINCE INCEPTION

Pagasa Philippines Lending Company Inc. and

Pagasa ng Masang Pinoy Foundation Inc.

2007 2008 2009 2010 2011

Total number of

branches 3 35 56 160 181

Total number of

development officers 12 130 213 635 817

Total number of

active groups 44 1,941 3,590 8,371 15,062

Total number of

active members 375 31,389 61,236 75,184 192,162

Total number of

active borrowers 375 34,443 63,481 140,541 165,335

Loan Collateral

Build-Up (LCBU) 5,525 20,610,725 51,610,960 54,704,111 185,973,601

Total outstanding

amount 2,533,400 139,213,405 223,748,481 675,429,332 913,968,629

2012 2013 2014 2015 2016

Total number of

branches 184 164 185 211 242

Total number of

development

officers

803 700 785 884 1,034

Total number of

active groups 13,678 14,082 15,364 15,466 16,827

Total number of

active members 160,721 163,408 202,077 240,141 292,075

Total number of

active borrowers 143,817 144,905 181,756 219,021 261,258

Loan Collateral

Build-Up (LCBU)

223,463,44

6

273,757,26

8

361,576,563.

50

462,829,289.

16

586,218,192.

12

Total outstanding

amount

779,228,01

1

823,863,07

9

1,028,681,37

1

1,343,666,64

8

1,681,072,1

17

Pagasa Philippines Inc. Annual Report 2016 3

Pagasa ng Pinoy Mutual Benefit Association Inc. (PPMBAI) – 2013-2016

PRODUCT /SERVICE COLLECTION

2013 2014 2015 2016

ADMISSION

FEE

Premium

Collected 14,547,206 4,855,631 9,394,010 8,728,260

Members

collected 145,472 48,556 93,940 87,283

BASIC LIFE

INSURANCE

Active

members 95,652 74,527 141,630 165,823

Premium

collection 37,304,443 42,178,017 104,528,953 124,252,598

Members

collected 95,652 108,148 268,023 314,870

CREDIT LIFE

INSURANCE

Active

members 155,490 104,981 148,687 165,821

Premium

collection 3,395,346 4,314,549 7,463,949 9,403,888

Members

collected 155,490 177,448 299,203 314,868

RETIREMENT

SAVINGS

FUND

Active

members 4,155 7,257 47,493 250,129

Premium

collection 540,151 403,200 6,753,090 24,821,558

Members

collected 4,155 3,102 44,391 188,740

CLAIMS AND BENEFIT PAYMENT

2013 2014 2015 2016

BASIC LIFE

INSURANCE

No. of claims 8 511 3,066 6,308

Claims

Payment 687,457 4,733,324 13,654,169 34,506,909

CREDIT LIFE

INSURANCE

No. of claims 7 251 835 4,592

Claims

Payment 115,794 920,108 2,124,217 3,072,739

RETIREMENT

SAVINGS FUND

No. of claims 20 55 118 4,283

Claims

Payment 2,600 7,175 17,495 1,560,301

Pagasa Philippines Inc. Annual Report 2016 4

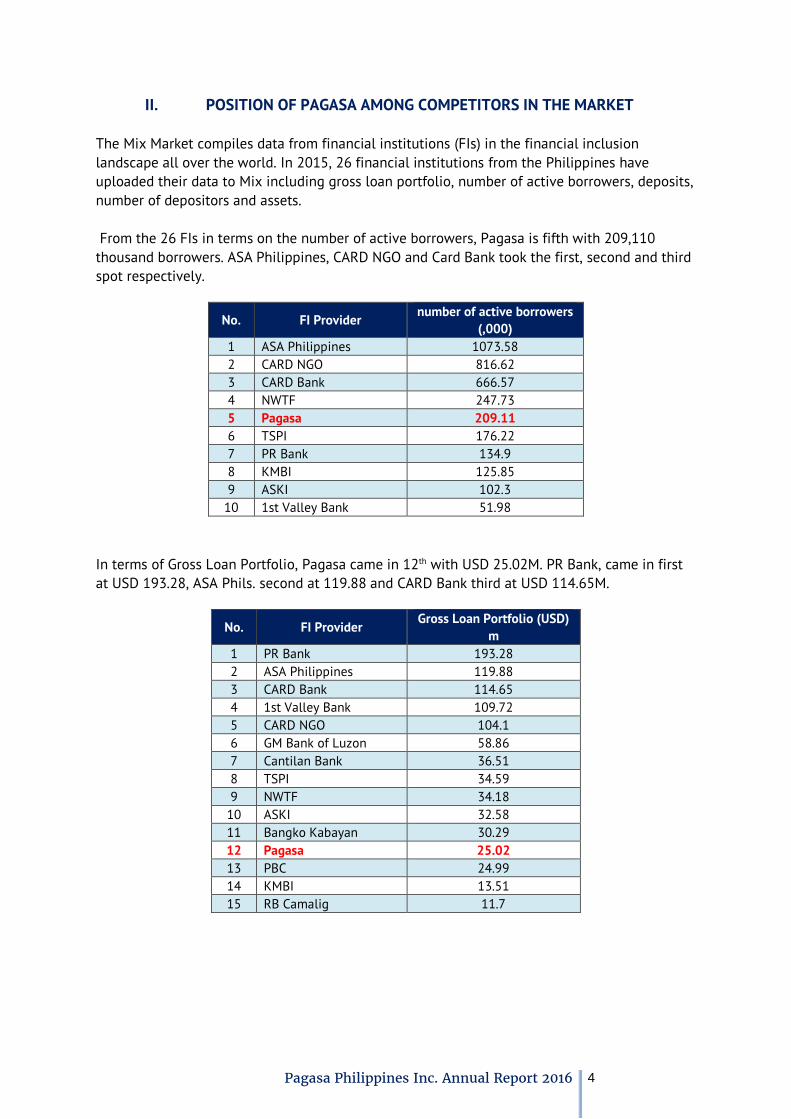

II. POSITION OF PAGASA AMONG COMPETITORS IN THE MARKET

The Mix Market compiles data from financial institutions (FIs) in the financial inclusion

landscape all over the world. In 2015, 26 financial institutions from the Philippines have

uploaded their data to Mix including gross loan portfolio, number of active borrowers, deposits,

number of depositors and assets.

From the 26 FIs in terms on the number of active borrowers, Pagasa is fifth with 209,110

thousand borrowers. ASA Philippines, CARD NGO and Card Bank took the first, second and third

spot respectively.

No. FI Provider number of active borrowers

(,000)

1 ASA Philippines 1073.58

2 CARD NGO 816.62

3 CARD Bank 666.57

4 NWTF 247.73

5 Pagasa 209.11

6 TSPI 176.22

7 PR Bank 134.9

8 KMBI 125.85

9 ASKI 102.3

10 1st Valley Bank 51.98

In terms of Gross Loan Portfolio, Pagasa came in 12th with USD 25.02M. PR Bank, came in first

at USD 193.28, ASA Phils. second at 119.88 and CARD Bank third at USD 114.65M.

No. FI Provider Gross Loan Portfolio (USD)

m

1 PR Bank 193.28

2 ASA Philippines 119.88

3 CARD Bank 114.65

4 1st Valley Bank 109.72

5 CARD NGO 104.1

6 GM Bank of Luzon 58.86

7 Cantilan Bank 36.51

8 TSPI 34.59

9 NWTF 34.18

10 ASKI 32.58

11 Bangko Kabayan 30.29

12 Pagasa 25.02

13 PBC 24.99

14 KMBI 13.51

15 RB Camalig 11.7

Pagasa Philippines Inc. Annual Report 2016 5

In terms of deposits, Pagasa placed 13th with USD 9.44M. CARD Bank, 1st Valley Bank and ASA

Philippines took the top three spots, at 90.16, 81.12 and 66.39 respectively. No. FI Provider Deposits (USD) m

1 CARD Bank 96.16

2 1st Valley Bank 81.12

3 ASA Philippines 66.39

4 PR Bank 65.11

5 CARD NGO 48.43

6 GM Bank of Luzon 42.56

7 Bangko Kabayan 40.48

8 Cantilan Bank 28.72

9 Bangko Mabuhay 23.47

10 TSPI 16.17

11 RB Camalig 15.78

12 NWTF 13.33

13 Pagasa 9.44

When it comes to number of depositors, Pagasa has a total of 228.97 making it fourth among

the FIs. CARD Bank, ASA Philippines and NWTF took the top three spots. No. FI Provider No. of Depositors '000

1 CARD Bank 1657.25

2 ASA Philippines 1073.58

3 NWTF 259.08

4 Pagasa 228.97

5 TSPI 180.8

6 KMBI 136.67

7 GM Bank of Luzon 135.76

8 1st Valley Bank 126.74

9 PR Bank 99.62

10 ASKI 96.67

On assets, Pagasa is at 12th spot with total assets of USD 41.45M. PR Bank is first with USD

248.43M, CARD Bank at second with USD 172.31M and CARD NGO is third with USD154.7M. No. FI Provider Assets

1 PR Bank 248.43

2 CARD Bank 172.31

3 CARD NGO 154.7

4 1st Valley Bank 148.44

5 ASA Philippines 121.37

6 GM Bank of Luzon 77.74

7 Bangko Kabayan 55.31

8 ASKI 54.4

9 Cantilan Bank 50.52

10 NWTF 48.38

11 TSPI 42.47

12 Pagasa 41.45

13 Bangko Mabuhay 29.46

14 PBC 26.85

15 KMBI 22.38

Pagasa Philippines Inc. Annual Report 2016 6

III. PRESENT STATE OF POVERTY, SOCIO-ECONOMIC

CONDITION OF THE PHILIPPINES

The Philippine Statistics Authority (PSA) released the 2015 data on poverty in the Philippines

last October 2016. The country has lowered its poverty incidence by 3.6% from 25.2% in 2012

down to 21.6% in 2015. That means that one out of every five Filipinos is poor or roughly 21.9

million Filipinos are living below the poverty line.

For the poverty threshold, a Filipino needs at least a monthly average income of PhP 1,813 to

meet the basic food and non-food requirements.

In 2015, the ratio of poverty incidence among families fell from 19.7% in 2012 to 16.5%;

making 3.8 million poor Filipino families. A family of 5 needs an average monthly income of at

least PhP 9,064 to meet the basic food and non-food requirements. 8.1% of the Filipino

population is classified under subsistence incidence (the proportion of families/ individuals with

per capita income less than the per capita food).

Pagasa Philippines Inc. Annual Report 2016 7

Poverty Distribution

Poverty incidence is higher than 60% in the provinces of Apayao, Eastern Samar, Lanao del Sur,

and Maguindanao. In Mindanao, apart from Lanao del Sur and Maguindanao, the rest of the

region’s provinces have indices 60% or lower. In the Visayas, the Western provinces have lower

than 30% incidence, while the eastern provinces have lower than 60% incidence. Luzon has the

least number of provinces with higher than 30% poverty incidence.

At the Regional level, ARMM remains the poorest region with the highest poverty incidence

which ranged from 40-49% in 2006, 2009, and 2012. NCR, CALABARZON, and Central Luzon

have the lowest poverty incidence in the country during 2006, 2009, and 2012.

At the provincial level, the provinces with the least poverty incidence are the 4 districts of NCR,

Bataan, Benguet, Bulacan, Cavite, Laguna, Pampanga, Rizal, and Ilocos Norte. The provinces

with the highest poverty are Eastern Samar, Lanao del Sur, Maguindanao, Masbate, Northern

Samar, Sarangani, Zamboanga del Norte, Camiguin, Lanao del Norte, North Cotabato, and

Western Samar.

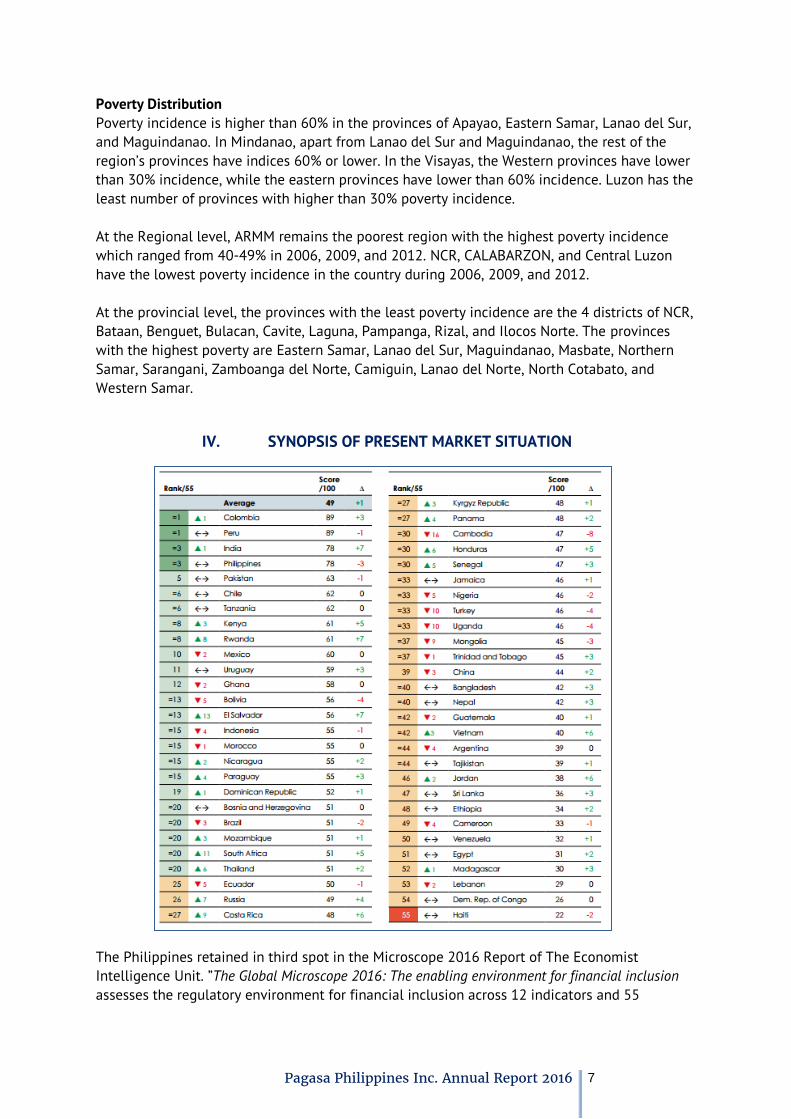

IV. SYNOPSIS OF PRESENT MARKET SITUATION

The Philippines retained in third spot in the Microscope 2016 Report of The Economist

Intelligence Unit. ”The Global Microscope 2016: The enabling environment for financial inclusion

assesses the regulatory environment for financial inclusion across 12 indicators and 55

Pagasa Philippines Inc. Annual Report 2016 8

0.7 1.1 2.4

4.4 6.1

9.9 10.1 10.5

12 61.9

0 10 20 30 40 50 60 70

Savings groups

From an employer

government entities

informal lenders

lending/ financing companies

Percent of respondents

Source of Loans

countries.” The 12 indicators include government support for financial inclusion, regulatory and

supervisory capacity for financial inclusion, prudential regulation, regulation and supervision of

credit portfolios, regulation and supervision of deposit-taking activities, regulation of insurance

for low-income populations, regulation and supervision of branches and agents, requirements

for non-regulated lenders, regulation of electronic payments, credit reporting systems, market

conduct rules, and grievance redress and operation of dispute and resolution mechanisms.

The microfinance sector is strong and continues to grow every year. The financial inclusion

advocacy and programs of the Bangko Sentral ng Pilipinas helps in democratizing access and

usage of financial services from different financial institutions.

The most recent MIX Market data reports that Philippine microfinance industry has a total of 5

million borrowers with loans outstanding US $1.3 billion and 6.9 million total depositors with

deposits of US $905.3 million (Clark, 2016).

In 2015, BSP conducted the National Baseline Survey on Financial Inclusion. The data shows

that 75.1% of respondents access loans through informal sources such as family and friends,

informal lenders, employers, and savings groups. (National Baseline

Survey on Financial Inclusion 2015, p. 32)

In terms of awareness, lending company ranked 8th (63.2%) and MFIs ranked 10th (30.5%). In

terms of actual transactions, MFIs ranked 9th (23.5%) and lending company ranked 10th

(23.2%).

4.1 18.4

23.2 23.5 26.7 29.3

43.9 48.4 49.2 51.6

58.6 71

0 20 40 60 80

NSSLA

Lending/ financing…

E-money agent

Money changer

Bank

Remittance agent

Percent of respondents

Transactions with access points

13.6 25.6 30.5

50.9 63.2 65.6 68.7 69.6

77.7 93.5 95.7 98.3

0 50 100 150

NSSLA

Microfinance NGO

Lending /…

Remittance agent

Money changer

pawnshop

Percent of respondents

Awareness of access points

Pagasa Philippines Inc. Annual Report 2016 9

With respect to socio-economic class, microfinance NGOs caters to those in Class E and D more

than those in the class ABC. Lending companies are accessed more by those in the Class D.

Also, MFIs are accessed more by those living in the rural areas (26.6%) as compared to those in

the urban areas (20.1%) while Lending companies are accessed more by those in the urban

areas (24.7%) than those in rural areas (20.7%).

Urban Rural

Lending 24.7% 20.7%

Microfinance NGOs 20.1% 26.6%

MFIs are especially accessible in Mindanao (35.7%) while Lending companies are most accessed

by those in Balance Luzon (26.5%).

NCR

Balance

Luzon Visayas Mindanao

Lending 23% 26.5% 15.7% 21.8%

Microfinance NGOs 12.7% 21.1% 19.9% 35.7%

Additionally, 20.2% of the respondents access microfinance loans through MFIs and personal

loans (53.4%) through lending companies. The main considerations in taking loan are interest

rate (57.5%), loan amount (41.7%), period of loan payment (35%), ease of loan application

(33.1%), and reputation of the institution (24.5%). 8.9% access insurance through mutual

benefit associations.

ABC D E

Lending 15% 24% 18.4%

Microfinance NGOs 20.4% 23.2% 25.2%

Pagasa Philippines Inc. Annual Report 2016 10

V. HUMAN RESOURCES

By end-December 2016, Pagasa has 1802 employees. 1423 were added in 2016 alone while 778

dropped out. Most noted addition is the appointment of a Deputy President and Chief Operation Officer.

Mr. Shamsul Hassan took over as the Deputy President while Mr. Azizur Rahman was appointed as the

COO.

As of December 2016

Sl.

No. Designation

Total no. of drop-

out staff

Total no. of

appointed staff

Total no. of

present staff

1 Division Manager 0 2 7

2 Asst. Division Manager 0 7 18

3 Regional Manager 4 28 52

4 Branch Manager 64 131 245

5 Asst. Branch Manager 23 179 172

6 Development Officer 646 934 967

7 Cook cum Peon 0 0 183

8 Group Coordinator 35 114 79

9 Division Support Staff 4 23 47

10 HO Staff/ EXECOM 2 5 32

Total 1,423 1802

DEC

Head Office Employee Information

Sl.

No. Designation

a President* 1

b Deputy President* 1

c Chief Operation Officer* 1

d Chief Financial Officer (CFO) 1

e Corporate Secretary 1

f DGM - Operations n/a

g AGM-Operations n/a

h AGM-HR n/a

i MIS Section 1

j Accounts Department 9

k HR & Admin Department 8

l Training Department 1

m Banking Section - Sr. Deputy Director

n Insurance - MBA Project Officer

o Finance Section 1

p IT Section/ ASE HO 2

q Vigilance Officer n/a

r Audit Section - Sr. Internal Auditor 1

s Front Office Executive (Executive Secretary)

t SPM OIC 1

Pagasa Philippines Inc. Annual Report 2016 11

u FMPU 1

v Messenger 1

w Driver 1

Total Head Office Staffs 32

Branch Office Staff Information

a Special Development Officer

b Loan Officer / DO 612

c Junior Development Officer 183

d Development Assistant 172

e Number of BM 245

f Senior Training Coordinator ( HO based time being) also in

charge of Logistics- Training Officer 5

g Training Executive (Currently involved in Banking work) n/a

h Number of IT Technician (Region based). 15

i Number of Audit Staff 11

Total Branch Office Staffs 1,243

Number of Regional Manager's (inclusive of RM in charge) 52

Number of District Manager (HO based time being )and Senior Regional

Managers n/a

Number of Management Trainee (Operations) AM

Other Staff

DM 7

ADM 18

Paralegal 4

HR Officer 6

HR Assistant 1

Admin 1

ABM 172

FMPU 4

Group Coordinators 79

Total Other Staff 292

Pagasa Philippines Inc. Annual Report 2016 12

ASA INTERNATIONAL

BOARD OF DIRECTORS

President

Corporate Secretary

Deputy President

Sr. Director - Finance & Accounts

Legal

Counsel Admin

Manager

Training &

Research Director

Sr. Internal

Auditor

SFA

FA

Asst. HR

Manager

HR Officer -

Benefits

HR Officer –

(Recruitment/ HRIS/ Relations)

Sr. Admin Asst. / Liaison /

Executive Driver

Maintenance

Accountant

Tax & Finance

Officer (vacant) Acctg.

Supervisor

Acctg.

Clerk

Sr. Finance Clerk / Sr. Acctg. Clerk

Sr. Acctg. Asst. / Sr. Bookkeeper /

Payroll in-charge

Jr.

Bookkeeper

Paralegal

Officers

OIC – SPM/CSR

Sr. Training

Officer

Training

Officers

IT Manager

Asst. IT

Manager

SSE

ASE

Divisional

Manager

Asst. Divisional

Manager

Regional

Manager

Branch

Manager

Asst. Branch

Manager

DA/ JDO/ DO

Division HR

Officers

FMPU

Head

FMPU

Staff

Chief Operation

Officer

HR

Manager

Field-based

Pagasa Philippines Inc. Annual Report 2016 13

VI. TRAINING AND DEVELOPMENT

Training and Development is at the core of Pagasa’s operations. In the pursuit of constantly

developing its workforce, Pagasa has conducted various training throughout the year. The

training department has also included some modules in the refresher courses for DO, ABM, BM,

RM and ADM. Already included in the training for RM and ADM are modules on mentor-mentee

relationship, aimed at cultivating mentorship between supervisors and subordinates, and

conflict management, a practical module to develop leadership not based on anger and hate

but instead fostering relations out of mutual respect.

Training Activities No. of Session Participants

1 PSO Training 213 2694

2 DO Refresher Training 22 456

3 ABM Training 8 167

4 BM Refresher Training 15 319

5 RM Training 6 78

6 Group Leaders Training 521 18438

7 Field Supports Training 1 25

TOTAL 786 22177

STAFF TRAINING

DO GATHERING

GROUP LEADERS’ GATHERING

Pagasa Philippines Inc. Annual Report 2016 14

VII. ACHIEVEMENTS AND ACCOLADES

Reaching around 300,000 client-borrowers

Having a loan outstanding of around P1.7 Billion

Operating in 45 major provinces and key cities of the country

Generating over three to five thousand job opportunities for Filipinos

99% of client are women

Digitized Borrowers’ picture- webcam integrated in the system;

Borrowers’ Account Update through SMS as part of Client Protection Principle

Intensive Group Leaders Training and Management

Regular Annual Group Leaders’ Gathering- bridging the gap between the institution and

clients

Establishment of its own MBA- microinsurance program

Pagasa Philippines endorses the Client Protection Principle of Smart Campaign for the

better practice of social commitment towards the client empowerment and protection.

VIII. SOCIAL PERFORMANCE MANAGEMENT

PPLCI hired personnel last September 1, 2016 as the Officer-in-Charge for Social Performance

Management and Corporate Social Responsibility. The SPM Unit is under the supervision of the

Training and Research Director (TRD).

The major activities undertaken for SPM are:

1. Development of the CSR Framework for the Company

2. Creation of the Client Services Committee – the committee is tasked to oversee the

implementation of the company’s CSR program including the scholarship program.

3. Conduct of the Staff Satisfaction Survey, Client Satisfaction Survey, Client Economic Yield -

Both data for the Staff Satisfaction and Client Satisfaction Surveys have been submitted to

ASAI.

Staff Satisfaction was completed in January and Client Satisfaction in February. Pagasa

staffs are generally satisfied with 68% reporting that they are satisfied, 7% extremely

satisfied and 22% slightly satisfied, with their work. Only 3% reported dissatisfaction (2%

dissatisfied, and 1% extremely dissatisfied).

The clients are generally satisfied with the services of Pagasa (53% satisfied and 37% very

satisfied). Only a combined 10% are somewhat satisfied, neither/nor, and not at all satisfied

with the services. In addition, 70% of the clients reported they will certainly recommend,

19% are very likely to and 8% will possibly recommend. A combined 2% reported

negatively: 1% unlikely and 1% impossible.

4. Training on SPM and CPP – Several orientations has been conducted on Social Performance

Management and Client Protection Principles. The orientations were conducted during

refresher courses of BM, ABM and RM and during the PSO for incoming DOs.

5. Conduct of Gap Analysis and the SPI4 for 2016 - The SPI-4 has been conducted in 2016.

The data have been submitted and reported to ASAI.

6. Conduct of Complaint Resolution Committee Meetings

Pagasa Philippines Inc. Annual Report 2016 15

Number of complain

received in 2016

Number of complain

resolved

Number of complain not resolved,

reasons?

Jan- June

7 2

5

- Complaints were forwarded/endorsed

to the concerned staff as complaint

has something to do with Branch

Operations or can be solved through

directing them to the concerned

immediate supervisor of the

complained staff

July-Dec

10

7

3

- Complaints have something to do

with policy so forwarded complaint to

management

Pagasa Philippines Inc. Annual Report 2016 16

IX. CSR ACTIVITIES AND PLAN FOR 2017

CSR Activity/

Program

Total No.

Event

Total no. of

beneficiaries

Budget 2016

USD Remarks (PHP)

Relief goods

distribution 70 74,000 Php3,478,000

Scholarship

Program 50 50 21,276 Php1,000,000

TOTAL 570 28,400 154,000 PhP 4,478,000

Number of

Beneficiaries

No of

branches Phenomenon

Average

Amount per

client

Total funds

released for

the program

Percentage of

fund utilized

495 21

Fire and

flooding due

to monsoon

rains

PhP 233.4

(4.7 USD)

PhP 115,539

(2,311 USD)

3.32% of

2016 budget

2016 marked with the monsoon rains in North Luzon and numerous fire-related incidents in

the urban areas in NCR, South Luzon, Visayas and Mindanao. Relief goods were distributed to

495 borrowers in 21 branches. Also, as per company policy, those who have been affected by

calamities are given 1 week of moratorium (minimum) from paying their loans until they get

back on their feet and engage in their business again.

Relief goods distribution in Apalit after monsoon rains caused flooding in the Pampanga and nearby provinces.

Pagasa Philippines Inc. Annual Report 2016 17

The first issue of Tanglaw Pagasa (beam of hope), Pagasa’s quarterly publication has an article

on the relief distribution. The newsletter was distributed by March 2017.

Distribution of relief goods in Mindanao

Borrowers affected by fire in Cadiz Region (Victorias, Cadiz and San Carlos) were given some relief goods.

Pagasa Philippines Inc. Annual Report 2016 18

Scholarship Program

The One Scholar per Branch program was launched in October 2016 with a target of 50

qualified scholars from the branches. Out of 30+ submissions, the program committee selected

twenty-two (22) that qualified for the scholarship. As early as November, funds were issued to

the scholars identified.

No. of scholars/

beneficiaries for

2016

No of

branches

Funds allocated

per scholar

Total funds

released for the

program

Percentage of

fund utilized

22

(out of 50 target

scholars)

20

9 scholars

received

PhP 10,000.00

(200 USD)

13 scholars

received

PhP 20,000.00

(400 USD)

PhP 350,000.00

(7,000 USD)

35% of the total

PhP 1M budget

(2016) is utilized

Scholars in their last semesters receive PhP 10,000 (200 USD). Those in their last year (2

semesters) receive PhP 20,000.00 (400 USD). They can either receive it one time or twice

(every semester).

The next steps to be taken are:

1. promote the scholarship program among the clients and members; and

2. carry over unutilized funds for 2016 to the 2017 budget

Scholar from Mabalacat and his parents

Two scholars and their borrower parents from Las Pinas 1 receive

their checks RM of Taytay issued check to Pasig Rosario 2

the borrower and her daughter.

Pagasa Philippines Inc. Annual Report 2016 19

Cabadbaran Carmen

Kidapawan 2 El Salvador

2 scholars from Novaliches 2 receive the check with their

parents (borrowers.

Silang Taytay

Paco

Pagasa Philippines Inc. Annual Report 2016 20

Tibungco Valenzuela

Padada Trento

Surallah borrower receives check during

the group meeting Arayat

Pagasa Philippines Inc. Annual Report 2016 21

2017 CSR PLAN

Sl

no.

Major CSR

Activities

Total no.

of events

Expected Total #

of Beneficiaries

Budget (local

& USD) Timefame

1 Scholarship

program 100 100

PhP2,000,000*

(40,000 USD)

Year-round

(particularly June-

Aug)

2 Relief goods

distribution 240 12000

PhP 3,000,000

(60,000 USD) Year-round

TOTAL 348 12,600

PhP 5,000,000

(10,000 USD)

X. FUTURE PLANS

PPLCI/PMPFI

1. For 2017, Pagasa management approved the plan to open 23 new branches.

Division Current no. of

branches

No. of new branches

to be opened for

2017

Total

South Luzon 44 7 51

North Luzon

PMPFI

PPLCI

11

35

3

0

14

35

South Mindanao 42 1 43

Visayas 25 12 37

Central Luzon 45 0 45

North Mindanao 40 0 40

242 23 265

2. Piloting of the use of cash card for loan releases in selected branches.

3. Piloting of the use tablets and the mobile application (AMBS) by DOs and field

personnel in recording field transactions in selected branches.

4. Online Monitoring

5. Registration of AMBS with the Bureau of Internal Revenue

PPMBAI

1. the MBA plans to increase its membership by up to 15%

2. the MBA plans to increase the CLIP premium from P2.50 / P1,000.00 to P5.00 /

P1,000.00;

3. the finalization of the MBA System;

4. the hiring of temporary encoders;

5. the introduction of new MBA products to its members; i.e. hospitalization

6. the MBA plans to increase its BLIP premium collection by 15% and its CLIP premium

collection by 100%; and

7. the allocation of the MBA’s CSR fund will be 5% of the profits

Pagasa Philippines Inc. Annual Report 2016 22

REFERENCES

Asian Development Bank (January 2017). Assessment of Microinsurance as Emerging Microfinance

for the Poor. The case of the Philippines. ADB, Manila, Philippines.

Bangko Sentral ng Pilipinas (2016). Financial Inclusion in the Philippines. Retrieved from

http://www.bsp.gov.ph/downloads/Publications/FIDashboard.pdf.

Bangko Sentral ng Pilipinas (2016). Financial Inclusion Initiatives 2016.

http://www.bsp.gov.ph/about/advocacies_micro.asp

Bangko Sentral ng Pilipinas (2016). National Baseline Survey in Financial Inclusion. Inclusive Finance

Advocacy Staff (IFAS). Retrieved from

http://www.bsp.gov.ph/downloads/publications/2015/NBSFIFullReport.pdf

Clark, Hearther (May 2016). RIF Regulation Mapping: Philippines. Social Performance Task Force.

Hailey, P., Brassel, D. & Janett, U. Micro and SME Finance Market Outlook 2017. responsAbility

Investments for Prosperity. Retrieved from:

https://www.microfinancegateway.org/library/micro-and-sme-finance-market-outlook-2017

Llanto, Gilberto M. (August 2015). Inclusion, Education, and Regulation in the Philippines. ADBI

Working Paper Series No. 541. ADB Institute. Retrieved from

https://www.adb.org/sites/default/files/publication/171786/adbi-wp541.pdf

Mix Market (2017). Philippine Market Overview. Retrieved from:

https://www.themix.org/mixmarket/countries-regions/philippines

Philippine Statistics Authority. (October 27, 2016). Poverty incidence among Filipinos registered at

21.6% in 2015 – PSA. Press Release. Retrieved from

https://psa.gov.ph/sites/default/files/Press%20Release_0.pdf

Philippine Statistics Authority (2016). 2015 Poverty in the Philippines. Infographics.

Social Sector Statistics Service (SSSS) Poverty and Human Development Statistics Division

(PHDSD). Retrieved from https://psa.gov.ph/sites/default/files/2015_povstat_FINAL.pdf

The Economist Intelligence Unit Ltd. (2016). Global Microscope 2016 The enabling environment for

financial inclusion. Retrieved from

http://www.eiu.com/Handlers/WhitepaperHandler.ashx?fi=EIU_Microscope_2016_English_web

.pdf&mode=wp&campaignid=Microscope2016

Trading Economics (2017). Philippines Economic Indicators. Retrieved from

http://www.tradingeconomics.com/philippines/indicators.