p3 smart revision notes

DESCRIPTION

ACCA P3, Business AnalysisTRANSCRIPT

ACCA P3 - Business analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 20091

ACCA P3 – PROFESSIONAL LEVEL

Business Analysis

SMART Revision notes

Prepared by Darren Sparkes

Email: [email protected]

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 20092

Contents Page no.

A message from Darren…………………………3Paper 3 Examiners Approach…………….….... 4Extracts from the Examiners report Dec 08…...5Examination Technique……………….…..……..7Background and examination format..…..........10Syllabus Overview………………………...........11Strategic Planning………………………...….....12Mission and Objectives…………………………13Business & Professional Ethics..………….…...14Internal Analysis……………….……………..…15External Analysis……………..………………....16Strategic Options……………………….……….18Method of Growth………………………............19Portfolio Analysis…………………………….….20Strategic Choice & Change Management…....21Marketing………………………………………...22Organisational Structure…………………….….23International Market Place.…………….……....24Business Process Change…….…..…………..25Information Technology……..…….……..........26Quality………………………………….……......27Project Management………………………...…28Role of Finance………………………………...29Review and Control………………………..…..30Strategy and People……………………………31

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 20093

Thank you for requesting a copy of my ‘SMART Revision Notes’.

The notes act as a learning and memory aid for the core models, theories and academic tools included in the syllabus.However, in order to pass your examination the academic knowledge must be combined with extensive question practiceleading up to the examination.

Your examiner is not interested in the regurgitation of your knowledge but how you APPLY that knowledge to thescenarios provided in order to answer the requirement set.

I suggest that you should practice as many exam standard questions as possible before the examination. Your practiceanswers can be a mixture of answer plans and full written answers to get through as many questions as possible.

However, I would also suggest that it is essential for you to practice at least one full examination to time before enteringthe exam room. It is only by replicating the time pressure in the exam that you can appreciate the importance of timeplanning on the day.

Keep a look out for relevant articles appearing in your professional magazine or on the Institute’s website prior to theexamination, particularly if they are written by the examiner.

I would welcome feedback on the notes.

And remember….

‘Whether you believe you can or you can’t, you’re right.’ (Henry Ford)

Regards,

Darren Sparkes

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 20094

Approach Required

‘Differentiation is important to individuals seeking to pass a management and

strategy examination.

It is the ability to link strategic and financial analysis;

it is the confidence to use creative thinking in the way you answer a

particular problem…with alternative ways of viewing and solving a problem’

Ralph Bedrock (Paper 3 Assessor)

There is no absolutely correct answer – candidates who provided

coherent justification… awarded appropriate marks

Steve Skidmore (P3 Examiner)

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 20095

Extracts from the Examiners comments December 2008In general:

• Performance showed an improvement on the previous sitting

• Answers much more within the context of scenarios than previous sittings

• Financial and quantitative data figured more prominently in answers

• The three optional questions were equally popular

• Q1b was biggest problem for candidates where many answers did not address the question

• Q1a (PESTEL) so popular it lead to some candidates over-answering it, leading to time problems

• As a result, answers to the final optional question often appeared rushed

• Vast majority of papers were well written and well presented

• Hand writing still remains a problem for some – it is no use having great ideas if no-one can read them

Section A - Question 1

Q1a – there were plenty of clues in the case study, most of which featured in candidates answers, with the

exception of legal responsibilities

Some candidates strayed onto internal issues (strengths and weaknesses) which were not given marks

Q1b – The case study is rich in material to support the cultural web approach

• Asked to explain the three strategy lenses – Some candidates very well prepared – showed great

understanding and gained full marks - Others showed very little knowledge and only scored two or three

marks.

• Overall many candidates provided good answers to question 1

• Reference to the case study context was much better than on previous papers

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 20096

Section B

Many more candidates than before supporting their argument with financial analysis

Many who used financial data in part a failed to do so in part b

The model answer suggests that MMI should not acquire the company – many candidates approved the

acquisition with justification through IT synergies – credit was given for this approach

Candidates do not always have to agree with the examiner’s analysis to gain the marks on offer!

• Question combined the themes of project management, quality and the systems development life-cycle

• Part a relatively straight forward which candidates either knew or did not

• Consequently, some candidates scored very few marks whilst others gained full marks

• Part b answered relatively well – many candidates giving a wide range of options.

• Part c – often overlap with part b

• Many candidates did not clearly justify their answer

• In some cases not enough points made to get the marks on offer

• Part b – relatively difficult in the time-constrained pressurised environment of the examination

• Well answered – many scoring eight or more out of ten.

• This was very heartening!!!

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 20097

Therefore, to pass P3 learn from the examinerscomments:

• Analyse the requirements – verbs and keywords• Planning – think before you write the answer• Application, application, application• Theoretical answers score few marks• You can only apply what you know – learn it!• Use and interpret the numbers (they are usually

easy calculations so it’s the interpretation thatgets the marks)

• Time management – the marks are your guide

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 20098

Examination Technique to give the Examiner what he wants

1. USE 15 MINUTES READING TIME WISELY Examine section B questions and choose the two on which you can MAXIMISE MARKS (not necessarily

those on your ‘favourite’ topics) If you have some time left then analyse Question 1 requirements and skim read the Q1 scenario to get a feel

for the relevant issues and identify where the information is for each part of the requirements.

2. WORK OUT TIMINGS Q1 = 90 minutes. Planning = 20-25 minutes, Writing answer = 65-70 minutes Section B Questions = 45 minutes each. Planning up to 10 minutes, Writing answer 35 minutes. Break down the time required for each part of the requirements using the marks as a guide. 1.8 minutes per

mark in total, 1.4 minutes per mark after planning. I suggest you start with Question 1 as you know you have 90 minutes to complete it.

START PLANNING IN YOUR ANSWER BOOK

3. ANALYSE THE REQUIREMENTS Identify the verb, or verbs, and make it stand out. The verb tells you what the examiner wants you to do, e.g.

evaluate, recommend, analyse, calculate. Be sure to identify all the verbs in the requirement just in casethere is more than one thing to do, e.g. analyse and discuss, evaluate and recommend.

Identify key words. These tell you what to do it on or about, e.g. evaluate what?, recommend what?

4. ALLOCATE MARKS TO EACH VERB IN THE REQUIREMENT This can now determine how much to write for each verb in the requirement

5. IDENTIFY RELEVANT MODELS, TOOLS, THEORIES FROM YOUR KNOWLEDGE BANK

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 20099

6. DEVELOP HEADINGS AND NUMBERS LAYOUT Put key elements of model in plan as headings, e.g. Porters 5 Forces analysis = 5 headings. Headings will

give your answer a framework and structure. Use requirements to develop headings to show marker that you are answering the question asked

7. DISTRIBUTE MARKS ACROSS HEADINGS This can now determine how much you write under each heading

8. ANALYSE THE SCENARIO Make brief notes in your plan under relevant headings from models/tools/theories and requirement Find relevant numbers for calculations

9. WRITE UP YOUR ANSWER TO MAXIMISE MARKS Layout calculations in a logical and easy to mark format – put them in an appendix in your answer plan Add value to calculations by asking ‘SO WHAT?’ Use as many headings as possible to give the answer structure Short sentences in short paragraphs Work on 2 sentences for each mark – 1 sentence making your point/answering the question + 1 sentence for

application A third sentence giving some ‘SO WHAT?’ could get you another mark Leave a blank line between points/paragraphs to make your answer ‘easy on the eye’ Be strict with timings. When time is up on a question, or part of a question, move on. Stick to answering the requirement – use your plan to keep you on track

REMEMBER THE THREE GOLDEN RULES – 1)APPLICATION 2) APPLICATION and 3)APPLICATION

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200910

Paper Background

Candidate Requirements

Apply knowledgeand skills

Determine appropriatetechniques

Select relevantdata

Exercise professionaljudgement

Objectives of thepaper

Assess the strategic position of the organisation Evaluate strategic choices available to an organisation Discuss how an organisation might go about its strategic implementation Model and redesign business processes and structures to implement and

support the organisation’s strategy taking account of customer and othermajor stakeholder requirements

Integrate appropriate information technology solutions to support theorganisation’s strategy

Apply appropriate quality initiatives to implement and support theorganisation’s strategy

Advise on the principles of project management to enable the implementationof aspects of the organisation’s strategy with the twin objectives of managingrisk and ensuring benefits realisation

Analyse and evaluate the effectiveness of a company’s strategy and thefinancial consequences of implementing strategic decisions

The role of leadership and people management in formulating andimplementing business strategy

Format of paper

Section A 50% Compulsory Major case study Usually four parts Case will include numbers

Section B 50% Choice of two from three Each question likely to include

two parts Will include short scenario May include numbers

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200911

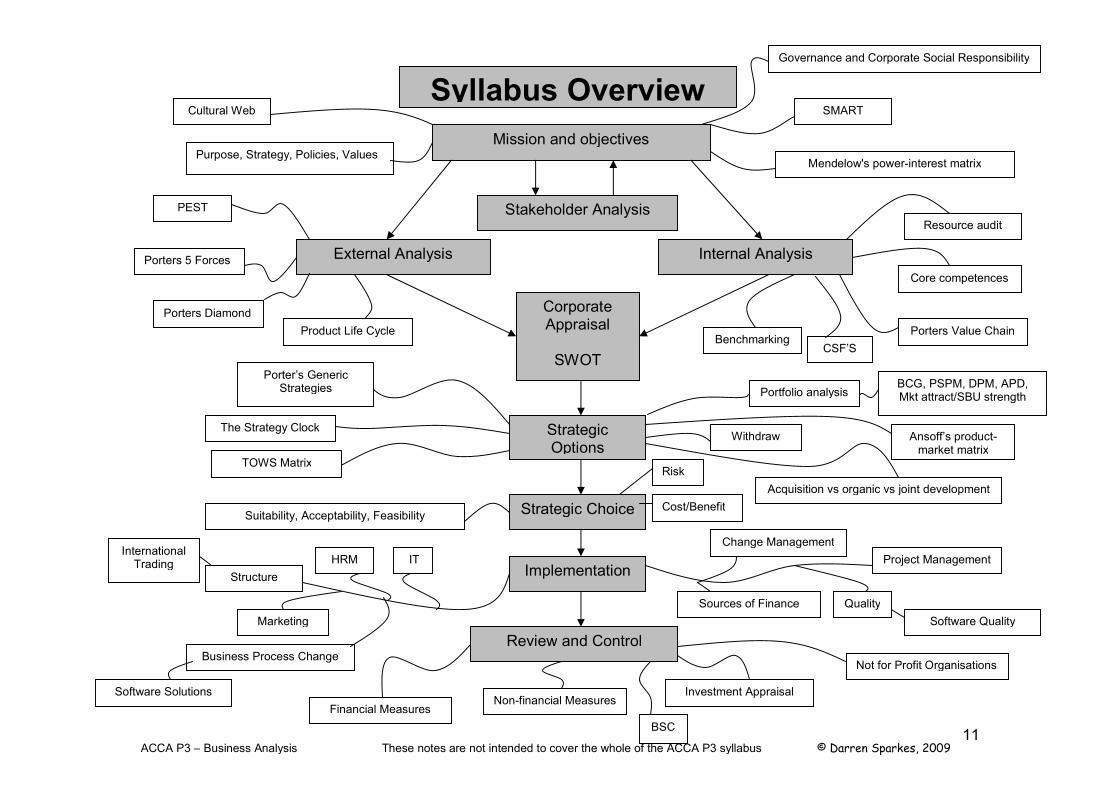

Syllabus Overview

Mission and objectives

Stakeholder Analysis

External Analysis Internal Analysis

CorporateAppraisal

SWOT

StrategicOptions

Strategic Choice

Implementation

Review and Control

Cultural Web SMART

Resource audit

Mendelow's power-interest matrix

Core competences

Porters Value ChainProduct Life CycleBenchmarking

PEST

Porters 5 Forces

Porter’s GenericStrategies

The Strategy ClockAnsoff’s product-

market matrix

Acquisition vs organic vs joint development

Suitability, Acceptability, Feasibility

Change Management

Project Management

Quality

IT

Structure

Marketing

Business Process Change

InternationalTrading

Financial Measures

Investment Appraisal

Withdraw

Purpose, Strategy, Policies, Values

Governance and Corporate Social Responsibility

Cost/Benefit

Risk

Non-financial Measures

Not for Profit Organisations

Porters Diamond

CSF’S

TOWS Matrix

Portfolio analysisBCG, PSPM, DPM, APD,Mkt attract/SBU strength

Software Solutions

HRM

Software Quality

Sources of Finance

BSC

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200912

Alternative

StrategicPlanning

Strategy‘… a course of action, includingthe specification of resources, to

achieve a specific objective

Long-term

Wholeorganisation

Integrates activities

All stakeholders

Competitive advantage

Relationship with environment

Corporate =Strategic level

Business = Tacticallevel

Functional = Operational level

Purpose

Respond and fit to environment

Utilise scarce resources Provide direction Ensure consistent objectives Monitor progress

Advantages

Identification ofstrategic issues

Consistency of goals Improve

performance/survival Pro-active Recognises

environment Optimum use of

resources

Disadvantages× Expensive (time

and money)× Bureaucracy× Stifles creativity× Less relevant in

a crisis

Rational ‘Top Down’ Approach

Mission & Objectives

Corporate appraisal

Strategic options

Strategic choice

Implementation

Review

Emergent Strategy - ‘Bottom up’ (Mintzberg)

IntendedStrategy

UnrealisedStrategy

DeliberateStrategy

RealisedStrategy

Emergentstrategy

E.G. Honda’s entry into the USA, 3M

Incrementalism (Lindblom) Building block approach Build strategy through incremental steps not radical

shifts Accepts uncertainty of future Builds commitment× May be too slow× Ideas often compromised

Freewheeling Opportunism Market Driven – reactive Hands on management Exploit complacent players Relies on leaders vision No formula for success Take advantage of market

opportunities× Stock market problems

Inter-dependant

PositionAnalysis

Choice Action

Johnson,Scholes &

WhittingtonStrategicLenses

Ideas

Design Experience

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200913

Mission andObjectives

Mission‘… the most generalised type

of objective which can bethought of as its raison d’etre.’

Purpose

Strategy

Policies andstandards

Values

Advantages Resolve stakeholder conflict Set direction Help formulate strategy Communicates values to

employees Marketing to customers

Criticisms Meaningless terms used Written retrospectively? Not communicated to

employees Ignored by managers

Objectives

S Specific

M Measurable

A Attainable

R Relevant

T Timebound

Critical SuccessFactors

"The limited number of areasin which results, if they are

satisfactory, will ensuresuccessful competitive

performance for theorganization.

They are the few key areaswhere things must go right for

the business to flourish.

If results in these areas arenot adequate, the

organization's efforts for theperiod will be less than

desired."

Stakeholders

Mendelow’s Power – Interest Matrix

InterestLow

Power

High

LowA

Minimal Effort

Give Direction

BKeep Informed

Education /Communication

CKeep Satisfied

Intervention

DKey Players

Participation – KeepClose

Not for Profit Organisations

Features of objective setting Multiple and contradictory objectives Participation in objective setting Providers of funding different to beneficiaries of service Priorities may change frequently Value for money a requirement not an objective Increased role of personal objectives

Efficiency

Effectiveness

Economy

Mission StatementPublished version of the

Mission

Culture‘The way we do things around here’

Cultural Web– cultural paradigm

Routines & Rituals Stories & Myths Symbols Power structure Organisation structure Control systems

High

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200914

Business andProfessional

Ethics

Professional Ethics‘Self control, not self interest’

C Competence

O Objectivity

P Professional due care

P Politeness

I Integrity

T Technical Standards

Corporate SocialResponsibility

Issues

Environment

Sustainability

Safety in the workplace

Consumer health and safety

Equal opportunities

Fair Trade

Honesty in Advertising

Views on Business Ethics

‘The business ofbusiness is business’(Shareholder View -

Friedman)

Management to concentrate onmaximising profits andshareholder wealth.

Businesses have no duty tosociety.

Societal benefits will arise as aresult of commercial success.

Conflict of CSR with shareholder wealth Reduced revenues Increased costs Diverts funds from shareholders Distracts management

Long-term Self-Interest /Stakeholder view

Firms should acknowledge their socialresponsibilities.Benefits to Business

Avoid future Government policy

Attract ethicalinvestor funds

Reduced risk

Competitiveadvantage

Recruitment

Innovation &ideas from

close links tocommunity

Reputationand branding Small company

advantage in thesupply chain

Potential problems

Competitive disadvantage

Deciding what is ethical Bad publicity from monitoring and enforcement

Disclosure of business information

No universal acceptance ofmorals & ethics

Johnson, Scholes & Whittington – Ethical Stances

Short-termshareholderinterest

Long-termshareholderinterest

Multiplestakeholderobligation

Shaper ofsociety

Corporate Governance Divorce of ownership and control Separate roles of CEO and Chairperson Audit Committee / Remuneration Committee Directors re-election at least every 3 years Non-exec Directors

o Independento Role on audit / remuneration

committeeso Corporate conscienceo Mentors to inexperienced execso Strategic value through expertise

Bribes

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200915

Internal Analysis(Strengths & Weaknesses)

Strategic Capability– Resource audit

9 M’s

Manpower Management Money Make-up Machinery Methods Material Markets Management Info

Core Competences‘…the activities or

processes that criticallyunderpin competitive

advantage.’

StrategicAssets

Architecture

Reputation

InnovativeAbility

Valuable Rare Can’t be copied Not substitutable Give access to wide

range of markets

…identify activities within the firm whichadd value to customers and those thatdo not

Primary Activities Inbound Logistics Operations Outbound logistics Marketing and sales Service

Support/secondary activities Procurement HRM Technology development Firm infrastructure

Uses Streamline linkages Eliminate non-value added activities Business Process Re-engineering Benchmark key processes

Basic

Benchmarking

1. Select processes to bebenchmark

2. Assign responsibilities3. Choose type of benchmarking4. Choose partner5. Interaction6. Collect data7. Implement changes

Competitive

Process/Activity

Internal

BEST IN PRACTICE

Porter’s Value Chain

Unique

CoreThreshold

Same ascompetitor / easy

to copy

Different tocompetitor /

difficult to copy

Resources

Competences

Value Networks

Knowledge Management

Explicit

Tacit

Uncover Knowledge Discover Knowledge Capture Knowledge Share Knowledge Distribute Knowledge Lever Knowledge Maintain Knowledge

Knowledge Workers Roving role Temporary roles Selection based on skill & competences Input into own development Separate & relevant incentive schemes Remote locations Flexible working

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200916

External Analysis(Opportunities and Threats)

PESTEL analysis(External, Environmental analysis)

Political Taxation Government policy Foreign trade

regulations Protectionism Globalisation

Economic Globalisation Economic cycle Interest rates Inflation Employment levels Exchange rates

Social & Demographic

Income distribution Education levels Population size Age profile Lifestyle changes Fashions and tastes Consumerism

Technological Internet Government

spending on RnD Communications Speed/rate of

change Processes and

methods ofproduction

Porter’s 5 Forces(Competitive,

Industry analysis)

Competitive RivalryGreatest where: Competitors of similar size Slow market growth rate High fixed cost industry Lack of differentiation

Threat from New Market EntrantsBarriers to Entry: Economies of Scale Other cost advantages Capital requirements Access to distribution channels Patents, Government policy Reaction of existing firms

Power of BuyersPower greatest where: Few buyers High number of suppliers available Cost is high proportion of buyers total cost Low switching costs Buyers have low profits Buyers have full information Little product differentiation

Threat from SubstituteTechnologies

Can same features be producedcheaper?

Can new features be provided for samecost?

Level of danger may be influenced bybarriers to entry and/or power of buyers

Power of SuppliersPower greatest where: Few suppliers Few substitutes High switching costs Threat from forward integration Customer not significant to supplier Supplier has differentiated product

Legal Health And Safety Employment Consumer protection Monopoly legislation Industry watch dogs

Ecological Globalisation Pollution Energy usage Disposal of waste Sustainability of

resources

External Analysis(Opportunities and Threats)

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200917

Internal + External Analysis= Corporate Appraisal = Position

Appraisal= SWOT Analysis

Strengths Weaknesses

Threats

INTERNAL

EXTERNALOpportunities

Product Life-cycleStages: Introduction: high risk, little competition, low volume, high advertising = losses + negative cash

Growth: increased competition, growing volumes, EOS, high advertising = losses to profits + negativeto positive cash

Maturity: steady repeat sales, high volumes, EOS, low level advertising = profits + positive cash

Decline: falling volumes, falling prices = profits to losses + positive to negative cash, divest

Balance the portfolio

External Analysis(Opportunities and Threats)

Porter’sDiamond

‘NationalCompetitiveAdvantage’

Firm structure, strategy, rivalry

Demandconditions

Factorconditions

Related and supporting industries

Problems: No common shape Unpredictable Self-fulfilling

prophecy Product orientated –

ignores market

External AnalysisFactors open to all in the industry

Internal AnalysisFactors specific to the organisation

Corporate Appraisal

TOWS

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200918

Strategic Options

What Basis?

Positioning view

Strategically developorganisation in linewith environment

PESTEL

Porters FiveForces

To beat the fiveforces

Porter’s Generic Strategies

Overall Cost Leadership(better margin, potential price cuts, entrybarrier, reduce supplier power)

Differentiation(Premium price, better margin, barrier,reduce buyer power)

Focus (Niche)(Cost or Differentiation, focus on marketneeds, develop core competencies)

Beware of ‘Stuck in the Middle’

Uses Analyse rivals Suggest own strategy SBU level strategy

Limitations Unclear definition of industry

Defines advantage in terms of position notresources

Lack of empirical evidence

Ignores middle ground

Restricts firm to position in presentindustry

Requires perfect information

What Direction?

Ansoff’s MatrixProducts, existing and new (PEN)Markets, existing and new (MEN)

Market Penetration (cost reductions,

price reductions, advertising, minor productmodifications)

Product Development (exploitexisting customers, RnD, buy-in and badge,JV’s, Licensing)

Market Development (new marketssuch as foreign markets, new segments suchas adult to child or industrial to consumer)

Diversification (related = vertical

integration or unrelated = conglomerate

Do nothing/ Withdraw

Risks Product Market Operations and

management Financial

Vertical IntegrationAdvantages Economies of combined

ops Economies of control and

coordination Avoiding the market Tap into technology

ConglomeratesAdvantages Flexibility Quick growth Access to capital Portfolio effect Avoidance of anti-

monopoly legislation

Disadvantages Increased operational

gearing Reduced flexibility to

change partners Capital investment needs

Disadvantages

No additional benefit toshareholders throughsynergies

No operating advantages

Horizontal diversification – competitive products,complementary products, by-products

Limitations Definition of market Ignores factors such as competitors Suggests strategies in isolation

Method of Growth? (See next page)

Low

Low High

Benefit

Price

High

Fail

Fail

FocusedDifferentiation

DifferentiationHybrid

Low Price

No Frills Fail

StrategicClock

Market Facing

Resource Based View

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200919

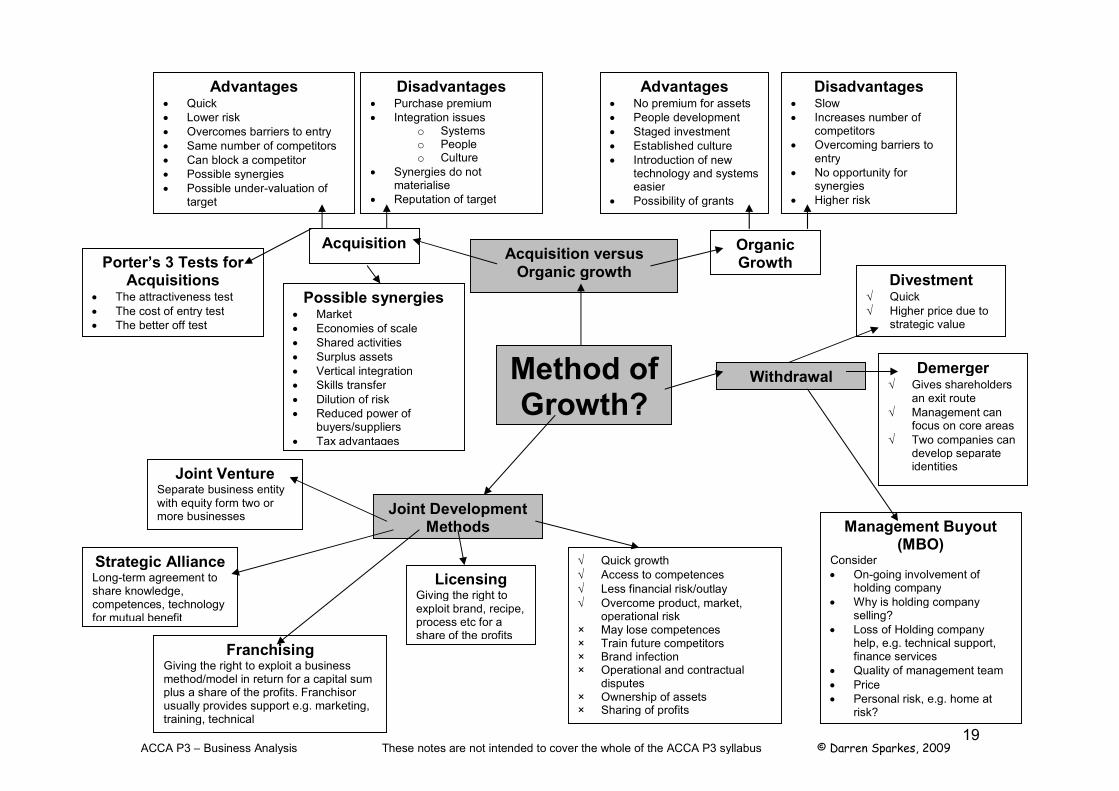

Method ofGrowth?

Acquisition versusOrganic growth

Acquisition

Advantages Quick Lower risk Overcomes barriers to entry Same number of competitors Can block a competitor Possible synergies Possible under-valuation of

target

Disadvantages Purchase premium Integration issues

o Systemso Peopleo Culture

Synergies do notmaterialise

Reputation of target

OrganicGrowth

Advantages No premium for assets People development Staged investment Established culture Introduction of new

technology and systemseasier

Possibility of grants

Disadvantages Slow Increases number of

competitors Overcoming barriers to

entry No opportunity for

synergies Higher risk

Porter’s 3 Tests forAcquisitions

The attractiveness test The cost of entry test The better off test

Possible synergies Market Economies of scale Shared activities Surplus assets Vertical integration Skills transfer Dilution of risk Reduced power of

buyers/suppliers Tax advantages

Joint DevelopmentMethods

Joint VentureSeparate business entitywith equity form two ormore businesses

Strategic AllianceLong-term agreement toshare knowledge,competences, technologyfor mutual benefit

LicensingGiving the right toexploit brand, recipe,process etc for ashare of the profits

FranchisingGiving the right to exploit a businessmethod/model in return for a capital sumplus a share of the profits. Franchisorusually provides support e.g. marketing,training, technical

Quick growth Access to competences Less financial risk/outlay Overcome product, market,

operational risk× May lose competences× Train future competitors× Brand infection× Operational and contractual

disputes× Ownership of assets× Sharing of profits

Withdrawal

Divestment Quick Higher price due to

strategic value

Demerger Gives shareholders

an exit route Management can

focus on core areas Two companies can

develop separateidentities

Management Buyout(MBO)

Consider On-going involvement of

holding company Why is holding company

selling? Loss of Holding company

help, e.g. technical support,finance services

Quality of management team Price Personal risk, e.g. home at

risk?

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200920

Business SectorProspects

High

Low

LowOpportunities to add value

BCG Matrix

High

Low

High LowRelative market

share

PROBLEM CHILDBuild or Divest

Losses, negative cash

CASH COWHold then Harvest

Profits and positive cash

DOGHarvest then Divest

Profits to losses, positiveto negative cash

Problems: Definition of axes Definition of market No account of complimentary goods Assumes high market share = advantage

PortfolioAnalysis

STARBuild then Hold

Losses to profits, negativeto positive cash

Directional Policy Matrix

Weak

Unattractive Attractive

Phasedwithdrawal

Proceed withcare

Phasedwithdrawal

Proceed withcare

Growth

Withdrawal

CashGeneration

Growth

Leader

Double or quit

Try harder

Leader

Average

Avge

Strong

Company’sCompetitivecapabilities

Public Sector Portfolio Matrix

Publicneed &Fundingeffective

ness

High

Low

High LowValue for money

Political hot box

Golden Fleece Back drawer issues –discontinue

Public sector Star

Market Attractiveness/SBU Strength matrix

High

Strong Weak

Business strength/Competitive position

Hold leadershipLeveragestrengthsUse EOS

Avoid ‘me too’Differentiate

Re-invest

Segmentbetween growth

and harvest

Enhance LeadDiversifyRe-invest

Segment focusSeek

advantage

Harvest throughsale of business

MaintainleadershipIn attractivesegments

HarvestPrice-upCut costs

Line pruning

Divest/Liquidate

Average

Med

Low

Long-termIndustry

attractiveness

Alien Territory

Ballast

Edge ofHeartland

Heartland

Ability toAdd value

High

Ashridge Portfolio Display – Corporate Parents

Marketgrowth

Value trap

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200921

`

StrategicChoice

SuitabilityIs the proposed strategy suitable for thepresent situation and circumstances of theorganisation?i.e. Is it suitable given the SWOTanalysis?

AcceptabilityWill the proposed strategy meetthe objectives of the organisationand, therefore, be acceptable tothe major stakeholders?

FeasibilityHas the organisation got, or can it get,the necessary resources to carry out thestrategy?

Strategic Drift

Risk Cost/Benefit

Strategy Environment

Types of Change

Incremental

Big Bang

Transformation RealignmentExtent of change

Adaptation

Revolution Reconstruction

Evolution

Speedof

Change

Lewin’s ForceField Analysis

Driving Forces Restraining Forces

Job Factors

PersonalFactors

OrganisationalFactors

Strengthen Weaken

Unfreeze Change Refreeze

SocialFactors

ChangeManagement

Time

Scope

PreservationDiversity Capability

Capacity

Readiness

Power

ChangeKaleidoscope

Participation Education & communication Facilitation & support Negotiation Manipulation Coercion

SupportingMechanisms

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200922

Marketing

Firm’s orientation

Productto meetneeds

ProductionSales

Marketing…identify, anticipate and satisfy

customer requirements

MarketingStrategy

Kotler’s FourPillars

Target Markets

Customer needs

Coordinated marketing

Profitability Analyse environmentand competitors – PEST

/ Porter’s five forces

Market Segmentation andTarget Market

…division of the market intohomogenous groups of potentialcustomers who may be treatedsimilarly for marketing purposes

Geographic Demographic

o Ageo Gendero Incomeo Family life-cycle

Social class Psychological Education Hobbies

Undifferentiated

Differentiated

Concentrated

Marketing Research…systematic gathering,

recording and analysing of dataabout problems relating to the

marketing of goods and services

Desk research(secondary data)

InternalAccounts, Salesreports, Customercomplaints

ExternalCSO reports,Businessmonitors, Tradejournals,newspapers

Field Research(Primary data)

Interviews, focus groups,questionnaires,

experiments, Testmarketing

Marketing Mix – 4P’s…set of controllable

marketing variables used toproduce desired response in

the target market

Product

Productmix

Product Life Cycle

Product qualitiesFeatures, options,range, warranty,branding, packaging

Place

Distributionchannels

Market coverage Outlet locations Warehousing

Promotion

Communications Mix:AdvertisingSales promotionPublic relationsPersonal selling

Price

Price levels Discounts Allowances Payment terms Delivery options

A Awareness

I Interest

D Desire

A Action Product

Implementation Issues

7 P’s

PhysicalEvidence

Processes

People

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200923

OrganisationalStructure

Centralised vs Decentralised

S Strategy

T Technology

O Objectives

P People

T Tasks

I Ideology

E Environment

S Size

Entrepreneurial Fast decisions Responsive to market Congruence× No career structure× No autonomy× Single product & market

Functional Economies of scale Specialists with some autonomy Career structures Frees up entrepreneur× Slow decisions (bureaucratic)× Functional silo’s× Few products & markets

Divisional Multiple products &

markets Autonomy for SBU

managers Training of SBU managers Frees up senior managers Focus on specific

products/markets× Loss of congruence?× Duplication of effort× Isolation of SBU

managers

Implementation Issues

Matrix Breakdown of silo’s Shared knowledge Skill development Innovation and creativity× Dual command× Dilution of functional

authority× Time consuming meetings

Mintzberg’sStructural

Strategic Apex

Middle Line

Operating core

Techno-structure

SupportStaff

Simple structure =entrepreneurial

Machine bureaucracy= functional

Professionalbureaucracy =decentralised

Divisional form

Adhocracy = matrix

Planning and control

Direct supervision

Planning processes

Performancemanagement

Internal market

Culture

Self-control

StrategicPlanning co.s

FinancialControl co.s

StrategicControl co.s

ManagingBusiness

Units

ParentalDeveloper

SynergyManager

PortfolioManager

Types of Structure

ExternalRelationships

Outsourcing

NetworkOrganisation

VirtualOrganisation

Reduced cost Skill shortages Flexibility Focus on core business× Loss of control× Supplier dependency× Confidentiality× Loss of in-house skills

Decentralisation

Advantages: Frees senior

management Better local decisions Better motivation Flexibility Training/career path

Disadvantages: Loss of control Loss of congruence Duplication of effort Extra costs of control

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200924

The InternationalMarket Place

Reasons for growth ininternational business

Convergence of Markets

Cost advantagesEconomiesof scale

Countryspecific costs

PoliticalInfluences

Trend to Globalproducts

Objectives ofinternational

growth

Expand sales

Acquireresources

Diversifysources of

sales &supply

Generalrisks

PoliticalLegal

Economic

Social/cultural

Technological

Exporting Low capital outlay Low risk Can learn about market× May not meet customer needs× Perceived lack of commitment× High distribution costs

Joint Venture &Franchising

Access to local resources Reduced national sentiment Shared capital input Access to competences and

knowledge× Shared profits× Lose competences× Train competitor× Operational disputes

Foreign Direct Investment Closer to market Retain profits More control Reduced operational conflicts× High financial risk× Staffing decision× Integration difficulties

Methods of International Expansion

Global Multi-Domestic Hybrid

Perceives foreign markets assimilar to domestic market

Products & marketing mixconstant

Standardisation to save time andmoney

Supply-driven policy

See overseas market as distinctive Customised products and

marketing mix Increased overseas sales volumesBUT Fewer EOS giving higher costs, so

volumes not turned into profits

Standardise wherever possible,e.g. RnD, Branding

Market convergence may allowstandardised product

BUT Demand-driven Customised marketing mix

where necessary = GLOCAL

STAFFING

Overcomes lack of host skills,unified culture, Transferscompetencies

× Resentment by host, singlecultural view

Multi-cultural view, inexpensive× Limits career mobility, isolates HQ

from subsidiaries

Efficient use of HR, builds strongculture and managementnetwork

× Subject to National immigrationpolicies, expensive

CompetitiveForces

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200925

Improving ProcessesHarmon’s

Process-StrategyMatrix

Planning

Redesign

Development

Analysing

BusinessProcess Change

Process Improvement

ProcessMeasures

Implementation Issues

High

Low

Low HighStrategic

Importance

Complex & dynamicHigh strategic value for

advantage- Process Improvement

Static / commodity- Outsource/Automate- Minimum resources

Static but valuable- automate for efficiency

Complex but not corecompetence- Outsource

ProcessComplexityDynamics

Process Redesign

Process Re-engineering

Transition

Feedback control systems

TARA

Input-Process-Output

Action Targets

Actuals

Review

Software Solutions –Systems Development Life

Cycle

Review

Implementation

Design

Analysis

Feasibility Technical Operational Economic Social

Interviews Questionnaires Observation Documenting tools Workshops Protocol Analysis Prototyping

Quality of Support User Friendliness Ability to meet needs Compatibility/Integration Costs Supplier factors

Staff training Installation File conversion Testing

Generic Solutions Speed Cost Risk Support× Unique needs× Supplier power× Compatibility/Integration× No advantage

Software System Project

Weighting and Scoring

Simplification –Eliminate duplicated

activities

Value -addedanalysis –

Eliminate non-valueadded activities

Gaps &disconnects –

Failures incommunication

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200926

InformationTechnology

Supply ChainManagement

Value chain

StrategicContext Web-

Presence

Generic strategies

Porters Five Forces

Support –No strategic value

Factory –See strategic valueof info system nowbut expect value to

decrease in thefuture

Turnaround –Expect info system

to becomestrategically

important in thefuture

Strategic –Depend on info

system forcompetitiveadvantage

Strategic impact of future systems

HighLow

Low

Strategicimpact ofcurrentsystems H

igh

E-commerce

IntegratedE-commerce

E-business

Barriers Technophobia Security Set-up costs Running costs Limited

opportunities Limited resource Disinterested

customers

Push vs Pull

Upstream(Suppliers)

E-procurement

E-sourcing

E-purchasing

E-payment

Risks

Downstream(Customers)

Technology Organisational No cost savings

Switching costs Disintermediation Re-intermediation Updates Communication User community Tracking

preferences Customisation

E-marketing

7P’s 4P’s People Processes Physical evidence

6 I’s Integration Industry structure Independent

locations Individualisation Intelligence Interactivity

CustomerRelationshipManagement

Acquisition

Selection

Customer LifeCycle

Retention

Extension

E-branding

-Recency-Frequency-Monetaryvalue

Implementation IssuesMcFarlan's Strategic Grid

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200927

3.4 defects in1 million

TQM‘Get it rightfirst time’

Commitment Communication

Continuousimprovement

Competence

6 C’s

Customers

Costs(PAF)

Quality

‘Fitness forUse’

Quality Control

Quality Assurance

Proactive

Reactive

Appraisal

Failure

Preventative

Internal

External

QualityStandards

QualityCertification

SixSigma

KeyRequirements

6 C’sTeam Roles

Green Belt

ImplementationLeader

Master Black belt

Black Belt

6 SigmaChampion

Problem SolvingProcess(DMAIC)

Control

Improve

Analyse

Measure

Define

QualitySoftware

The ‘V’’ Model

Acceptance testing

System testing

Integration testing

Unit testing

Coding

Unit Design

System Design

Functional spec

Requirement spec

CapabilityMaturityModel

Integration(CMMI)

Level 1Performed process

Level 2Managed process

Level 3Defined process

Level 4Quantitatively Mangd

Level 5Optimising process

Implementation Issues

99.99966%

T

I

S

A

Test Plans

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200928

ProjectManagement

(IPECC)

Initiation

ProjectInitiation

Document

ProjectAppraisalFeasibility

Stakeholders

Quality

Time

Risk

Technological Operational Economic Social

Resources

Put plan into action

Tolerate / Accept Treat / Reduce Transfer / Insure Terminate / Avoid

Purpose Scope Deliverables Costs Time Objectives Stakeholders Org structure

Sponsor Manager Team

SWOT

Project Leader

Planning

Quality Resources Evaluation Dissemination Exit Sustainability

CriticalPath

Analysis

Time

Project Evaluation & Review Technique (PERT)

WorkBreakdownStructure

CostBreakdownStructure

Execution

Motivation Planning Co-ordination Communication Problem solving Change Mgt Budgeting Meetings

MonitorAnd

Control

TARA

ProjectInitiation

Document

Frequency

Complexity Risk Cost

CorrectiveAction

Adjust Plan

Motivation

Crashing

Fast Track

Increaseresource

Completion

EnsureCompleted

Final report & audit

Smoothhandover

Tie up looseends

Compare PIDto Outcome

Formally terminateproject

Evaluate performance

Implementation Issues

Gantt Chart

Statements ofWork

ProductBreakdownStructure

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200929

Role of Finance

Strategy

FinancialStrategy

CompetitiveStrategy

InvestmentStrategy

Not for ProfitOrganisations

Objectives

Spend fundseffectively

Raisemaximum

funds

Core Costs

Management R&D Support Services

FinancingDecisions

Cost Gearing Control Security Cash flow Availability Exit routes

Considerations

Alternatives

Equity

Debt

Retained earnings Ordinary shares

Debentures Loans HP/Leasing Overdraft Trade Creditors

Pref shares

Grants

Ratios

Gearing

Liquidity

Efficiency

Profitability

ROCE Gross/Net Margin ROE

Asset turnover ROCE Receivables Payables Inventory Revenue/employee

Current ratio Quick ratio

Dividend cover Interest cover EPS PE ratio

Investor ratios

Limitations Only comparative Inflation Definitions Accounting policies Availability of info Historical

Inter-firm comparisonLimitations Accounting policies Bias by large/small firms Unrepresentative avge Industry classifications Financial periods

InvestmentAppraisal

TraditionalMethods

Discounted cashflow techniques

ROCEPayback

NPVIRR

Economy Efficiency Effectiveness

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200930

Review and Control

Profit Related Measures

Examples Gross margin Net margin Cost % sales Profit

Problem:no account taken of investedcapital used to generateprofits

Return OnInvestment

(ROI)

ResidualIncome (RI)

PBIT X 100 = %CE

Relative Measure %

PBIT(CE x imputed interest rate)

RI

Absolute Measure £’s

Problems: Sub-optimal

investmentdecisions

Deplete capitalassets too early

Problems: Absolute measure

poor forperformancecomparisons

Joint issues when used in isolation Backwards looking measures Short-termist decisions Open to easy manipulation of discretionary costs and

capital employed

ConclusionFinancial measures should not be used in

isolation to measure performance but shouldbe combined with non-financial measures.

The Balanced Scorecard

Financial Perspective

Internal BusinessPerspective

Learning & GrowthPerspective

CustomerPerspective

1. Identify CSF’s2. Identify competences required for CSF’s3. Develop KPI’s for competences4. Measure competence5. Take action – continuous improvement

Benefits Longer-term

measures More difficult to

manipulate Measures

determinants andresults

Promotes goalcongruence

Includesstakeholders

PotentialDrawbacks

× Measures conflictwith each other

× Requires culturalchange

× Overload –‘paralysis byanalysis’

× Time and cost× No obvious

relationship withshareholder wealth

ACCA P3 – Business Analysis These notes are not intended to cover the whole of the ACCA P3 syllabus © Darren Sparkes, 200931

Strategy andPeople

Strategic andcoherentapproach

HR Planning

HR Gap

Current HRposition

Current & futureHR needs

Labour supply

RewardManagement

Job design

WorkplaceLearning

CompetencyFrameworks

Assessment& Appraisal

Leadership

Classical

Purpose

Barriers

Likert'sManagement

Styles

Trait Style Contingency Situational

Charismatic Transformational Transactional

Exploitative autocratic Benevolent authoritative Participative Democratic

Communication Teamwork Delegation Motivation Trust

Performance Potential Training

Confrontation Judgement Chat Bureaucracy Event Unfinished

business

PerformanceMeasurement

Employee ranking Rating scales Checklists Critical incident method Free reporting Performance contract BARS Appraisal interviews

Categories Levels Design Issues Techniques Strategic alignment

Considerations: Fair & consistent Motivation Reward performance Recognise job factors Control salary costs

Scientific Mgt Job enrichment Japanese Mgt BPR Teamwork Succession

planning

TARA

Analyse behaviour Recruitment Training needs Manage

performance Benchmarking

Learningorganisation

KnowledgeManagement

Implementation Issues

Recruitment

Motivation