oward improved intermodal freight transport in - fhwa operations

TRANSCRIPT

Toward Improved IntermodalFreight Transport in

Europe and the United States:Next Steps

Report of an Eno Transportation Foundation Policy Forum heldNovember 18–20, 1998

Forum Sponsors:

European CommissionDirectorate-General VII (Transport)

U.S. Department of TransportationOffice of Intermodalism and Federal Highway Administration

iii

Table of Contents

Participants and Paper Authors ................................................................................... iv

Preface ............................................................................................................................ v

Forum Proceedings ........................................................................................................ 1

Introduction ....................................................................................................... 1Interoperability and Standardization ............................................................... 2

Standardization of Loading Units ............................................................................... 2Standardization of Intermodal Information Systems ................................................ 3

Intermodal Liability Issues ................................................................................ 4Current Liability Regimes............................................................................................ 4Prospects for a New Liability Regime ......................................................................... 5Liability and the Need for Information ...................................................................... 6

Legal and Regulatory Issues in Intermodal Transport .................................... 7E.C. Regulation ............................................................................................................ 7U.S. Regulation ............................................................................................................ 7Cabotage ....................................................................................................................... 9Third-Party Logistics Providers .................................................................................. 9Open Access to Rail Facilities ..................................................................................... 9Reregulation ............................................................................................................... 11

Best Practices in Intermodal Freight Transport ............................................ 11Intermodal Rail Developments in Sweden ............................................................... 12New International Rail Corridors ............................................................................. 12Supply-Chain Management ....................................................................................... 12Airship “Cargolifter” Service .................................................................................... 13Port Investment Policies ............................................................................................ 14Electronic Commerce and Intermodal Transport .................................................... 14

Toward Improved European andU.S. Intermodal Freight Transport: Next Steps ............................................. 15

Standardization .......................................................................................................... 15European and U.S. Best Practices ............................................................................. 16Electronic Commerce and Intermodal Freight Transport ....................................... 16The Role of Governments in Infrastructure Finance .............................................. 16Liability ...................................................................................................................... 16

Article A:Interoperability in Intermodal Freight Transport ..................................................... 17

Article B:Intermodal Transportation and Carrier Liability ...................................................... 33

Article C:U.S. Intermodalism: Cargo Liability Issues ................................................................ 41

Article D:Legal and Regulatory Issues Affecting Intermodalism in the European Union.................... 59

Article E:Legal and Regulatory Barriers to Better International Intermodal Transport ........ 69

Acronyms and Abbreviations ..................................................................................... 85

iv Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

Participants and Paper Authors

Forum ChairmenDr. Wim A.G. BlonkDirector, Transport PolicyDevelopment, Research andDevelopment, EuropeanCommission, DirectorateGeneral VII

Mr. Kenneth WykleAdministrator, FederalHighway Administration,U.S. Department ofTransportation

Forum ParticipantsMr. Richard BiterDeputy Director, Office ofIntermodalism, U.S.Department ofTransportation

Mr. Thomas BrownPresident, The Riss Companies

Mr. Edward BurkhardtChairman, President andChief Executive Officer,Wisconsin Central Transpor-tation Corporation andEnglish Welsh and ScottishRailways

Mr. Franco CastagnettiDirector of Purchasing/Logistics/ProductionPlanning, Enichem/PolimeriEuropa

Prof. Ralf De WitUniversity of Brussels

Mr. Wolfgang FlickVice President Transport,United Parcel Service, Europe

Mr. Johannes FritzenPresident, VolkswagenTransport

Mr. Robert GallamoreAssistant Vice President,Communications Technolo-gies, TransportationTechnology Center, Inc.

Mr. Dirk GoedhartConsultant, PhilipsInternational

Mr. Rolf HellbergDow Chemical, Germany

Mr. Juhani KorpelaSecretary General, Ministryof Transport andCommunications, Finland

Mr. Damian J. KulashPresident and CEO, EnoTransportation Foundation

Mr. Anders LundbergSenior Vice President,Swedish Railways

Mr. Robert MartinezAssistant Vice President,Marketing, NorfolkSouthern Corporation

Ms. Mary Lou McHughAssistant Deputy UnderSecretary of Defense,U.S. Department of Defense

Mr. James MorganManaging Director, TNTAutomotive Logistics

Mr. Thomas PerdueVice President, Intermodal,C.H. Robinson Co.

Mr. Heinz SandhagerDirector General, FederalMinistry of Transport,Germany

Mr. Bert SchackniesSenior Policy Advisor,Federal Highway Administra-tion, U.S. Department ofTransportation

Mr. George SchoenerChief, Intermodal andStatewide ProgramsDivision, Federal HighwayAdministration, U.S. Depart-ment of Transportation

Mr. Otto SonefeldProgram Director for Inter-modal Activities, AmericanAssociation of State HighwayTransportation Officials

Mr. Ron Stanley, PresidentLandstar Express America

Mr. Rune SvenssonTransport Advisor, VolvoTransport

Mr. Karel VanroyeAdministrator, Unit forAnalysis and TransportPolicy Development

Mr. Riccardo VitaleProcter and GambleEuropean Supply Company

Mr. Paul WautersManaging Director, WautersTanktransport N.V.

Mr. David WinsteadSecretary of Transportation,Maryland Department ofTransportation

Mr. Peter J. ZantalThe Port Authority of NewYork and New Jersey

Paper AuthorsMs. Regina AsariotisLecturer, Institute ofMaritime Law, University ofSouthampton

Mr. John BetakPrincipal, CollaborativeSolutions, Inc.

Mr. Vincent PowerPartner, A & L Goodbody

Forum StaffMs. Jennifer ClingerLouis Berger International, Inc.

Mr. Ed RosenEno TransportationFoundation

Ms. Annemarie SchmalzFederal Ministry ofTransport, Germany

Ms. Birte Windhorst,Volkswagen Transport

Preface v

Preface

The growth of the global economy, ad-vances in information technologies, andimproved communications networks havecontributed to major changes in transportand logistics. Just-in-time inventory sys-tems, supply-chain management,outsourcing of logistics, and intermodaltransport have grown hand-in-hand withthese advances in technology and eco-nomic interaction. Further economicgrowth demands that we continue to ad-vance international intermodal transport.

Intermodal transport—door-to-door ser-vices using more than one mode, but con-tracted as a single service on a combinedbill of lading—are a key ingredient of theemerging global economy and new logisticsenvironment. Intermodal transport notonly is rapid, reliable, customer-oriented,and efficient, but also makes effective useof the existing infrastructure and can helpprovide needed transport without undueenvironmental costs. Governments aroundthe world seek to reap the benefits possiblethrough increased intermodal transport,both domestically and internationally.

The European Commission and the U.S.Federal Highway Administration recognizethe potential of intermodal transport andthe need to work together to advance it ona global scale. They convened a forum onthis potential in Washington, DC, in Octo-ber 1997, bringing together top leaders en-gaged as transport carriers, shippers, andgovernment officials from both Europe andthe United States. Participants found thisforum valuable to understanding the issuesand the perspectives of other participants.They identified a short list of specific is-sues for continued examination that formedthe basis for a second forum, which washeld in Munich, Germany, in November1998. This report summarizes the discus-sions at the 1998 event.

A variety of views is reported here: ship-pers and carriers, government and indus-try, rail and truck, logistics providers andcorporate outsourcers, and Europeans andAmericans. Sometimes the participantsshared a vision of what is needed for im-

proved international intermodal transport;often they do not. Each has a distinct andvalid interest in achieving improvements,and these improvements can only beachieved through collective understandingand action. No one fully understands theintermodal transport system, and no oneis empowered to manage its improvement:these are complex matters whose success-ful resolution hinges on many indepen-dent private and public parties. Forumslike the ones held in Washington andMunich can help to identify opportunitieswhere individuals and groups can gain theinformation and plan actions that lead tocollective improvement of the system.

We are pleased to have initiated this dis-cussion and are gratified to see that it hasdeveloped into the dynamic, productive dia-logue reported here. The discussion hasfocused attention on opportunities for im-provement, on topics where more informa-tion is critically needed, and on emergingdevelopments where all partners must worktogether to meet the needs of the future.Everyone involved in international inter-modal transport will gain by learning moreabout how these issues are viewed by dif-ferent participants. We are pleased to havebeen catalysts in this process, and we lookforward to continued efforts to improvebroad-based understanding and coopera-tion to advance international intermodaltransport capabilities.

Dr. Wim A.G. BlonkDirector for Transport PolicDevelopment: Research and DevelopmentEuropean Commission, Directorate-General VII (Transport)

Mr. Kenneth WykleFederal Highway AdministratorU.S. Department of Transportation

Forum Proceedings 1

Forum Proceedings

Introduction

In November 1998, a group of high-levelindustry and government representativesmet to discuss ways to improve intermodalfreight operations between Europe and theUnited States. The European Commissionand the U.S. Department of Transporta-tion sponsored this second such meeting.The participants’ active roles in providingand guiding intermodal transport servicesmake them uniquely qualified to identifystrategic opportunities. As individuals, asorganizational officials, and as membersof established coordination bodies theycan seize opportunities to apply the in-sights they gain through information ex-changes like this forum.

Greater reliance on intermodal transportis crucial for economic productivity and en-vironmental preservation. More than 70percent of all goods transported in the Eu-ropean Union are moved by truck, up from50 percent 35 years ago. This increase iscreating serious problems in the EuropeanUnion, including unacceptably high levelsof environmental degradation and safety-related losses, as well as productivity lossesdue to congestion. There is simply notenough space to put new roads or rails tomeet such an increase in freight. Intermodaltransport offers to rebalance the system ina way that provides needed services buteases the strain on the environment.

In Europe as in the United States, gov-ernments recognize that they cannot buildtheir way out of congestion. But the tworegions are different in important ways. Thegeography of the United States is such thatrail and road can be combined more easily.In Europe, combining modes efficiently ismore difficult due to shorter geographicdistances for shipments within Europe, dif-ficulties in operating seamless rail servicesacross national borders, and the impossi-bility (on many routes) of double-stackingcontainers. Both regions face the importantchallenge of finding ways to make more ef-ficient use of existing facilities, but underdifferent circumstances.

The discussions reported here seek toenhance the efficiency of intermodal trans-port. This goal is shared by a wide varietyof interests: firms that produce goods andfirms that ship them, government agenciesand private businesses, consumers and pro-ducers. Yet this goal cannot be reached byany one agency or organization. It requiresan exceptional amount of cooperation—be-tween modes, between countries, betweenthe public and private sectors, and acrossdifferent levels of government and differ-ent parts of the world. This cooperation isfacilitated through informal exchanges likethose discussed in the following report.

These discussions took place over twodays. Separate sessions were devotedto (1) standardization of loading units,(2) liability for damage and loss of inter-modal cargo, (3) economic regulation ofcompetition in transport, and (4) best prac-tices in intermodal transport. Backgroundpapers on these topics, which follow these

Dr. Wim Blonk,EuropeanCommission,DirectorateGeneral VII (left)and KennethWykle, FederalHighwayAdministration,U.S. Departmentof Transportation(right)

Participants inthe secondEuropean–U.S.Forum onImprovedIntermodalFreight Transporton November 18–20, 1998.

2 Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

proceedings, were prepared and distrib-uted prior to the discussions. These pa-pers were summarized briefly by theauthors at the start of each session, fol-lowed by an open roundtable discussionamong all the participants.

Interoperabilityand Standardization

Standardization of Loading Units

Standards promise many advantages. Theycan help businesses achieve greater econo-mies of scale. Using standardized units,companies can reduce the capital neededfor investment. Standards can reduce thecost of transfer facilities. Companies canmake better use of their equipment andcarrying capacity. They do not need tomaintain large stocks of duplicative equip-ment. They can improve backhaul capac-ity. They also can enhance their ability tocommunicate—to interchange business inlarger organizational or physical networksthat may involve other companies.

However, standardization can stifle in-novation and flexibility. Standards canmake a company less willing to considermodifications to accommodate specializedneeds, and services may become less re-sponsive to changing customer needs.Standards may require high front-end con-version costs, at least for some companies.Standards also can erode the competitive

edge that a firm gains from its proprietarysystems and specialized equipment. Stan-dards can create security concerns.

Introducing new standards reallocatesbenefits and costs, and such a transitionraises the difficult issues associated withhow the costs and benefits will fall on com-panies at different points along the sup-ply chain, and how companies may facedifferent competitive stakes. The shipper’sexpectations drive the process. Transportcustomers want one-stop, single-sourceshopping. But they also want flexibility astheir markets and needs change. For ex-ample, a very large shipper can developnew systems to maximize its position inthe market, and carriers must adapt.

The viability of standards in any indus-try is closely linked to the maturity of theindustry. In more mature industries,moves toward increased uniformity areless likely to conflict with other goals. Theintermodal industry, however, is far frombeing mature. Moving too quickly to stan-dardize this industry could conflict withthe healthy process of innovation that isthe essence of a dynamic industry. Forexample, intermodal transport could betransformed by the introduction ofmegaships. More than 40 of these shipsare on order and scheduled to be deliveredover the next several years. The size of thecells in these ships will drive the size ofcontainers. In turn, the size of the con-tainer will affect the prospects for stan-dardizing loading units in intermodaltransport.

European firms currently operate usinga wide variety of different container sizesand types that are not interchangeable oreasily combined. Greater standardizationoffers many benefits. Yet, the range of op-tions is limited because the physical infra-structure in Europe limits the extent towhich maximum dimensions can bechanged. Tunnel heights in many areasprevent increases in vertical size. The widthis also fixed. While the overall benefits areevident, and the range of options is nar-row, many parties have a competitive in-terest in one solution or another, and anagreement on standards cannot be reacheduntil a vast majority of affected interestssee a common gain in standardization.

Otto Sonefeld,American

Association ofState Highway and

TransportationOfficials, Anders

Lundberg, SwedishRailways, and

Robert Martinez,Norfolk Southern

Corporation (left toright)

Forum Proceedings 3

The issue of standardization is also tiedto long-run infrastructure planning: Eachneeds a vision of the other. As the meritsof increased standardization are weighed,the infrastructure implications must betaken into account. The United States, likeEurope, faces serious highway congestion,and expansion is very difficult. It takesyears to go through the planning processto add new lanes, and in the end, expan-sion may not even be possible. Even withgood planning and cooperation, it takes thepublic sector a long time to address addi-tions to capacity.

A mix of opposing forces is endemic toany consideration of standardization: Pro-ponents work toward areas where stan-dardization is a desirable end, whileindependent new developments and op-portunities unfold in ways that create fur-ther segmentation and fragmentation.Thus companies, trade groups, and govern-ments working together to achieve the so-cially desirable benefits of standardizationsometimes find, after years of effort, thatthe end-product is nonetheless more frag-mentation. In spite of this result, many inthe field recognize that greater standard-ization can be, in concept, an importantboost to efficiency. Further, most believethat private-sector interests are best ableto make judgements about where and whento increase standardization. Nevertheless,there is a need for public involvement. Thelarge public-sector role in providing infra-structure must be considered.

Standardization ofIntermodal Information Systems

A global tracking and tracing system couldbe extremely helpful to intermodal opera-tors. Such a system could bring togetherthe key elements of each transport con-tract and unite them on a common plat-form. This system, perhaps an Internetdatabase of intermodal shipments, wouldintegrate the tracking and tracing informa-tion for all parts of the movement.

Individual companies, modes, and coun-tries have successfully developed or ex-tended tracking and tracing systems.However, no standardized system is in place

that covers all modes, countries, and users.Tracking and tracing information is notcurrently uniformly available. Integrated in-formation systems are essential for im-proved efficiency. The difficulty in gettingbetter tracking and tracing information isnot fundamentally a technological problem.Some of the greatest difficulties are tied tosecurity concerns, and techniques to ad-dress these concerns are being developed.

Some road carriers have responded tocustomer needs by establishing telemetricsystems, which include mobile phones anda fax machine network, to notify shippersimmediately if any problems arise. Euro-pean shippers can also get tracking infor-mation from railroads in a member state.But they often lose sight of their shipmentsat the borders. Efficiency demands hav-ing this sort of information availablethroughout the entire trip, and integrated

Thomas Brown,The RissCompanies,FrancoCastagnetti(second from left),Enichem/PolimeriEuropa, andVincent Power,A & L Goodbody

Rune Svensson,Volvo Transport,and JuhaniKorpela, Ministryof Transport andCommunications,Finland

4 Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

intermodal information systems areneeded to provide this.

The systems that have been developedby industry on a commercial basis need tobe interconnected. The European Com-mission has taken steps in this direction.For example, the European Commissionsupports the interconnectivity and inter-operability of Port Community Systemsand is examining how seamless intermodalapplications could be developed. U.S. com-panies, through the Intelligent Transpor-tation Society of America, have establisheda program to increase domestic and inter-national in-transit visibility, for both trans-portation assets and cargo.

Intermodal Liability Issues

Ever since the beginning of for-hire haul-age, in which an independent contractortransports goods for others, liability issueshave been important. How much am I li-able for? How does this amount changedepending upon whether the cargo is lost,missing, or damaged? Who must pay?What is my exposure? What is the expo-sure of everyone else in the process?

These issues became more complexwith the development of intermodal trans-port, which, by its very nature, involvescarriage on two or more modes and en-tails transferring cargo between modes.Much of this traffic is prepackaged in con-tainers that are loaded before they begintheir sequence of modal movements andtransfers. Each mode involved in the over-

all movement has different liability re-gimes. The intermodal customer—theshipper or the beneficial owner—does notcare about how the load gets there. Thecustomer cares that it gets there on time,in good condition, and at an attractive price.The customer is not directly interested inliability. For intermodal transport as forother modes of transport, these issues mustbe negotiated as a service feature.

Current Liability Regimes

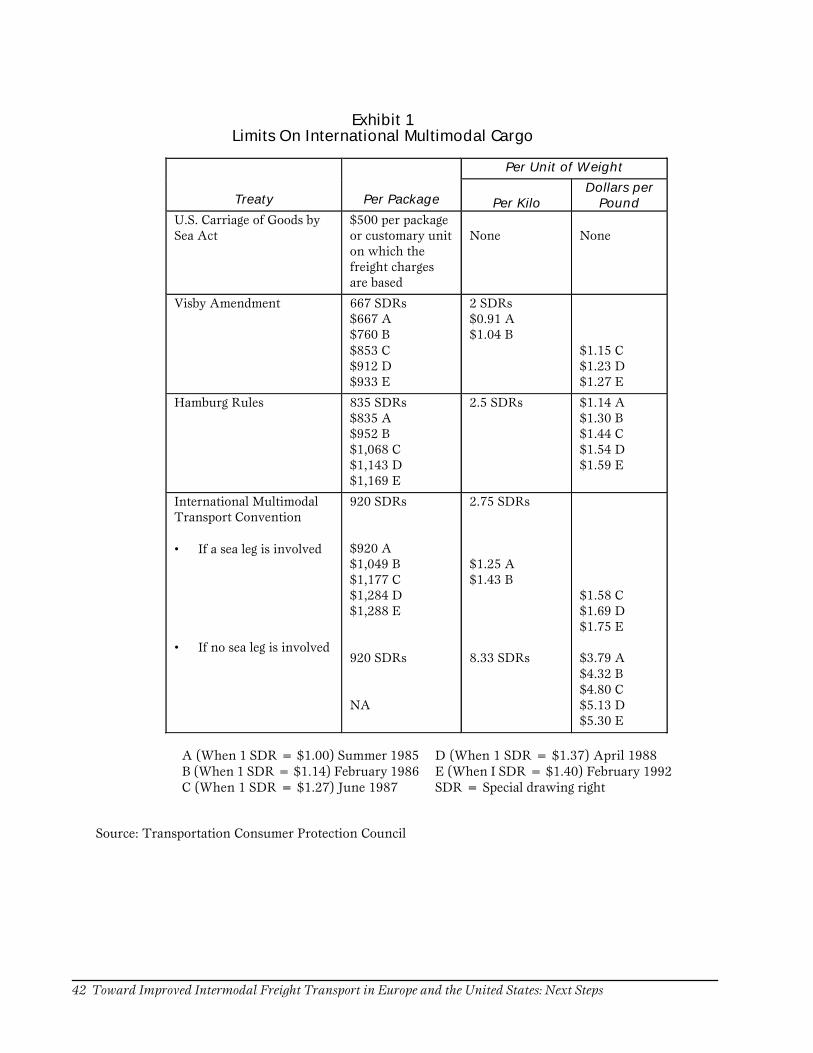

A complex maze of regulations currentlygoverns liability for international inter-modal transport. No uniform regime gov-erns liability for loss, damage, or delayduring transport in intermodal transac-tions. No uniformity exists at the interna-tional level. Nor is there uniformity in thesense of providing one standard of liabil-ity for all stages of the intermodal trans-action. The current framework consists ofa complex set of international conventionscreated primarily to regulate unimodaltransport by rail, road, air, or sea. Thesewidely accepted international conventionshave introduced mandatory minimum li-ability standards. For areas where themandatory conventions do not provide aclear determination, an array of diverse na-tional laws may apply. If damage or loss isnot covered by any international or na-tional mandatory law, then standard termcontract conditions (such as those con-tained in the International Federation ofFreight Forwarders Association (FIATA)bill of lading (FBL) or the Multidoc 95)apply.

Unfortunately, the applicable regimessometimes overlap, and more than one re-gime may apply to the same haul. Histori-cally, land, air, and sea liability regimeshave been drafted to address one or an-other particular mode of transport at atime. Liability regimes are not designed forintermodal transport. As a result, ambigu-ous intermodal situations arise.

Under unimodal regimes, every time aloss occurs, what actually happened usu-ally must be investigated. In the context ofcontainerization, investigation is extremelydifficult: How can one be sure when and

ReginaAsariotis

(right),University of

Southampton,and RalfDe Wit,

University ofBrussels

Forum Proceedings 5

where a loss occurred, that is, on whichmode the container was situated when theloss occurred? Liability varies in terms ofincidence and extent depending on the ap-plicable regime. Which regime applies, inturn, depends on whether it is possible toidentify the modal stage where the loss ordamage occurred. It also depends on thecauses of the loss, because under all theunimodal regimes, the carrier’s liabilitydepends on fault. If a carrier can establishthat other reasons were responsible for aloss, the carrier is not liable. That is, liabil-ity hinges not only on where a loss occurs,but also on how and why.

Although a shipper knows what levelof coverage is provided from the maritimebill of lading, the actual settlement ofclaims often depends on which court thematter is brought to and the court’s viewson which regime is mandatory. While gen-eral coverages may be unambiguouslyspelled out in bills of lading, if damage orloss is localized, then the liability may besubject to other limits, no matter what thegeneral contract terms say.

Shippers typically make separate ar-rangements for individual shipping con-tracts, carrying some of the liability andinsuring part of it. Third-party logisticscompanies operate like a carrier, assum-ing liability up to set standard limits. Ifshippers want higher coverage, additionalcoverage can be worked into the contract.Liability issues can thus be resolved be-tween the logistics firm and the client. Thethird-party logistics firm resolves claimson the front end with the customer andthen subrogates the matter with truck, rail,ocean, or air carriers involved. The suc-cess or failure of the final resolution istransparent to the customer. In effect,third-party logistics providers in Europehave positioned themselves as part of thesolution to complicated liability regula-tions, while in the United States they havenot generally done this yet.

Prospects for aNew Liability Regime

A key consideration at the base of any li-ability regime is the issue of whether it

would be a mandatory or a voluntary regu-latory system. A mandatory regime wouldcertainly be the most effective, but it in-creases the difficulties of reaching consen-sus. Therefore, it may be more productiveto focus efforts on a voluntary regime. Thiscould be a regime that parties must opt intoby actively incorporating it into a contract.Alternatively, a voluntary regime could beestablished that applies unless the partiesexplicitly opt out or replace it.

For any regime to be cost-effective, itshould be simple, clear, and transparent.It should cover delay as well as loss anddamage. It should operate irrespective ofthe modal stage where the loss occurs andindependent of the causes of a loss. Sucha regime would alleviate the administra-tive and legal burden of establishing therelevant regime. It would reduce the needto determine factual matters to clarify whois liable and for how much. It would in-crease efficiency, speed claims settlement,and reduce loss-recovery costs.

Concerted international actions, inconcept, appear necessary and logical.Are they possible? In principle, an in-ternational convention would be ideal.Yet, an international convention in-volves an unmanageably large numberof parties, each of which is rightly wor-ried about its own interests. As a result,such an approach may attempt to address

Rolf Hellberg,Dow Chemical,Germany

6 Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

all of the “ifs” and “buts,” leading to avery complex framework. Even if agree-ment could be reached, a conventionmay never be ratified, as experience withthe Multimodal Convention illustrates.

Similarly, an interregional conventionbetween the large European and U.S. trad-ing blocks would have obvious advantages.But the likelihood of an interregional con-vention would depend on political will.

The draft amendments to U.S. Carriageof Goods by Sea Act (COGSA), now en-tering the U.S. legislative process, havebeen written with an eye to U.S. needs.But the scope of application of this act isbroader. Any shipment of goods to or fromthe United States involving a sea leg wouldbe subject to this mandatory regime. Thesea leg does not necessarily have to betrans-Atlantic. U.S. COGSA would applyto an airfreight shipment to the UnitedStates if it included a sea leg across theMediterranean. Under this proposal, allclaims could be litigated in the same U.S.process, even if a European shipper is su-ing a European carrier. Any carrier in-volved in any leg of the shipment wouldbe governed by this mandatory regime.

The proposed changes to U.S. COGSAappear to have come about because theoriginal act, dating from 1936, is badly out-dated. It set liability at $500 per package.This number is clearly inadequate, but car-riers and shippers have been unable to agreeon an updated approach. The U.S. Mari-time Law Association formed a study groupto bring the various parties together and go

though the difficult process of develop-ing a mutually acceptable solution. In theprocess, the drafters saw the advantagesof extending the concept from more thanjust unimodal carriage by sea to the en-tire intermodal movement. What beganas a national proposal for reform to themaritime regime has grown into an inter-national, intermodal proposal that uni-laterally extends U.S. law outside itsterritory.

Liability and theNeed for Information

The lack of data on actual loss and claimexperience is universal, at least on a broad,aggregate level. Individual companies mayhave information that applies to them.Some firms, for example, regularly analyzethe premiums they pay and the claims theyexperience. From this data, they may con-clude that it is better not to take out aninsurance policy and instead self-insurethe goods. But in aggregate, data on lossesare lacking.

Arrangements that shift liability to theprimary carrier may appear to leave ship-pers satisfied, simply because they can dis-tance themselves from the underlyingvariations in conventions and nationallaws. Such practices may allow shippersto cope with or mask current liability am-biguities. Nevertheless, to manage liabil-ity efficiently, we need to know the damagehistory of actual loss experience in inter-modal transport. A common liability re-gime holds the potential for cost savings.No one can be sure of this potential, be-cause we do not know the actual exposureand claims data. But it appears plausiblethat we could manage risks more effi-ciently with better information.

These data do not exist now. In theUnited States alone, the Federal Bureau ofInvestigation estimates that more than $12billion a year is claimed for cargo theft,loss, and damage. This rough estimate sug-gests that the costs are enormous and thatmajor savings might be realized by man-aging the data better.

Faced with the lack of data, no one cansay how much these inconsistencies in the

Kenneth Wykle,Federal HighwayAdministration,

U.S. Departmentof Transportation,

and RichardBiter, U.S.

Department ofTransportation

Forum Proceedings 7

handling of liability are costing. But itappears plausible that in any system thiscomplicated, streamlining could producesavings. Particularly within the EuropeanUnion, reducing variations between modesand countries appears worthwhile. Anintermodal data standard that could beapplied to contracts for door-to-door trans-port by unspecified modes appears to bedesirable. This intermodal standard couldcoexist with other existing standards.

Legal and Regulatory Issues inIntermodal Transport

Forum participants selected the topic oflegal and regulatory impediments as a toppriority for the 1998 forum to focus oneconomic barriers, not regulations thatpromote safety, improve the environment,or preserve the infrastructure. Numerousregulations involving vehicle size andweight, labor rules, environmental protec-tion, and other aspects of transportationmay have important economic conse-quences. But these regulations are prima-rily enacted for purposes other thanregulating competition, and they are notthe focus here. This discussion is con-cerned with regulations whose explicitintent is to govern the economic competi-tiveness of new entrants in the business.

E.C. Regulation

Intermodalism in Europe is a complicatedbusiness, governed in part by the rules ofthe 15 member states, the EuropeanUnion, and international conventions. Ifthese rules are found to be in conflict, E.U.law is superior to the member states’ na-tional laws, and international law is supe-rior to E.U. law.

European law has focused on regulat-ing rather than facilitating intermodal ser-vice. Its competition and antitrust rulesseek to scrutinize and control. They im-pose high compliance costs and regulatorydelays. Further, competition law in trans-port has been formulated and is appliedseparately for air, maritime, rail, and in-

land waterways, rather than intermodally.Intermodal arrangements must win sepa-rate approvals from each of the affectedmodal regulators.

The core of E.C. regulatory policy is setout in Articles 85–94 of the E.C. Treaty,administered by Directorate-General IV.Each of these provisions applies to allmodes of transport equally. However, thedetailed regulations applied in practice areunimodal. Article 85(3) of the E.C. Treatygrants the European Commission the ex-clusive authority to permit exemptions foranticompetitive arrangements that are, onbalance, beneficial to the economy. Theseexemptions might include, for example,pricing or exclusivity arrangements tofacilitate intermodalism. Article 86 of theE.C. Treaty prohibits a dominant under-taking from abusing its dominant positionin the common market. This prohibitioncould be applied, for example, to a port, acarrier, or an intermodal operator. Articles92–94 of the E.C. Treaty stipulate thatmember states may not provide financialaid in a discriminatory manner withoutapproval from the European Commission.

The degree of E.C. intervention in themarketplace is a central issue. The com-mission’s 1994 Report on Maritime Trans-port declined to grant a block exemptionfor shipping lines to fix land rates, insteadrequiring separate review of each agree-ment. The commission also refused toadopt the so-called “rule of reason” ap-proach, which is central to U.S. antitrustlaw, again opening the door for the com-mission to intervene in such arrangements.

Robert Martinez,Norfolk SouthernCorporation, andHeinz Sandhager,Federal Ministryof Transport,Germany

8 Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

State subsidies to railroads severelylimit the prospects for intermodalism. AnyEuropean intermodal operator faces thepossibility that competitors could be re-ceiving unlawful aid. To foster sound in-termodal competition, the EuropeanCommission and multimodal operatorsmust monitor unlawful state aid. Such aidmight exist if facilities are made availableat less than commercial rates or if loansare financed beneath market rates.

U.S. Regulation

Over the decades, the United States hasdeveloped a set of mode-specific economicregulations, each with its own character.By the 1970s, this situation had resulted ina set of modal companies and modal regu-

latory agencies that had formed, in effect,alliances within each mode. Regulationscontinued to suspend antitrust laws to ac-commodate the unique features of trans-portation companies. These provisionsallowed transportation companies to oper-ate on a scale where they can achieveproduction-scale economies while stillaffording a reasonable level of consumerprotection. But regulators and carriers in-creasingly worked together to compete formodal share of the overall market and toobtain special treatment from the govern-ment. These aims were very different fromthe shipper protections that had been theimpetus for creating the regulatory struc-tures in the first place. Economic forceswithin the transport sector led to a seriesof deregulation moves during the late 1970sand early 1980s, when rail and truck trans-port were substantially deregulated.

An integrated, multimodal system hasbeen a rallying cry of every secretary whohas ever led the U.S. Department of Trans-portation. But government-led efforts toplan or coordinate a national transporta-tion system never got very far because theyhave been, and are, heavily influenced byprivate-sector decisions. In 1991, legisla-tion was passed that applied a new strat-egy. The legislation that authorized federalspending for surface transportation facili-ties included a category that could be usedfor intermodal connectors to the nationalhighway network. This authorization pro-vided a constructive vehicle around whichpublic and private interests could worktogether—a focus on strategic nodes thatpromised improved coordination withminimum shifts in public and privateroles. The Transportation Equity Actpassed in 1998 continues the focus on in-termodal connections and generally en-courages intermodalism.

The foundations that intermodal com-panies are built on are the original modesout of which the intermodal enterprisesprang. This situation has led to manybarriers that are not necessarily regulatoryin nature. The synergies promised bymultimodal companies have often provedelusive because of discrepant labor con-tracts, cultural differences, unmanageablescale, and other reasons. Still, regulatory

Heinz Sandhager,Federal Ministry

of Transport,Germany, and

Mary LouMcHugh (right),U.S. Department

of Defense

George Schoener,U.S. Federal

HighwayAdministration,

and ThomasPerdue, C.H.

Robinson Co.

Forum Proceedings 9

adjustments could compensate for someof the noneconomic barriers and make iteasier for intermodal services to thrive.

Deregulation of domestic freight transportin the United States is now virtually com-plete, inasmuch as free market entry is con-cerned. In recent years, domestic airfreightand intrastate trucking have been deregu-lated, so that few domestic barriers remain.

Cabotage

U.S. cabotage restrictions are one of theremaining barriers to intermodal trans-port. Europe previously had similar restric-tions on maritime cabotage, but theserestrictions were phased out in 1992.Greece and Spain were the most affected,and passenger operations were more af-fected than freight operations. The largestshipping line engaged in European cabo-tage is now an American shipping line.The Jones Act in the United States pre-cludes European participation in the U.S.market. While some transportation enter-prises may gain some market protectionthrough cabatoge, U.S. cabotage restric-tions are part of a strategy to maintain thenation’s ability to use U.S. commercialcapabilities to meet contingency and war-time requirements. The aim of these re-strictions is to provide incentive to U.S.carriers to provide wartime capacity byfacilitating peacetime business for them.The penalty cost to shippers has been es-timated at 14 billion U.S. dollars.

Third-Party Logistics Providers

The use of third-party logistics providersis an index of how free market competi-tion really is. Third-party logistics pro-viders have very few constraints in theUnited States, and growth in this sectorhas come hand-in-hand with expansionof intermodalism. This growth has en-hanced competition in areas where itwould otherwise be lacking. U.S. inter-ests see the rise of third-party logisticsproviders as good for competition andgood for productivity. This is also the casein Europe.

Even with the rapid rise in the use ofthird-party logistics providers in theUnited States, the market is not univer-sally open in this respect. For example,under the recently passed Ocean ShippingReform Act, nonvessel-owning commoncarriers are not granted the same abilityto enter into confidential contracts as arevessel-owning firms. This is one instancewhere third-party logistics is constrainedby regulatory barriers.

Open Access to Rail Facilities

U.S. rail operations are essentially deregu-lated, except when they are seeking ap-proval of a merger. In the case of a merger,the Surface Transportation Board reviewsthe competitive balance and may set regu-

Johannes Fritzen,VolkswagenTransport, PaulWauters, WautersTanktransportN.V., and RuneSvennson, VolvoTransport

Thomas Perdue,C.H. Robinson Co.

10 Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

latory conditions. Europe tends to bemuch more regulated, often in the nameof liberalization. The European Commis-sion has been frustrated in its attempts torealize the potential of the poorly perform-ing state railways. These railroads havebeen losing money and have often beenunable to offer the service demanded bycustomers. Solutions are necessary notonly for economic reasons, but also for en-vironmental and social reasons.

The nature of regulation in Europe isvery different from the United States. Therail problems are different, and the tworegions have very different historical pub-lic and private roles. Deregulation in theform of open access is intended to over-come the inherent limitations of the na-tional railroads. In the United States, openaccess would be difficult to impose on pri-vate companies that own their own infra-

structure and would resist such a policyas an unconstitutional taking of privateproperty. In Europe, this is not an issuebecause governments own the rail infra-structure, and governments have the au-thority to determine how their propertywill be used.

In Europe, where the rail systems havebeen monopolies within their own na-tional borders, the policy has been toseparate the operation of railroad servicesfrom the construction and maintenanceof railway infrastructure. This policy iswhat U.S. participants refer to as “openaccess” or “competitive access.” Given thegeographical boundaries and history ofpublic rail investment in Europe, theopen-access form of deregulation hasbeen Europe’s way to increase competi-tion among railroad operators, althoughnot necessarily among the railroad own-ers. The U.S. history of private rail in-vestment and the existence of realrail-to-rail competition create a funda-mentally different context.

The use of the terms “deregulation,”“privatization,” and “open access” havevery different connotations in the two re-gions. Europeans use privatization to high-light the separation of above-the-railoperations (which they hope to be openedto greater competition) from below-the-railownership (which continues to requirepublic subsidy). U.S. interests see deregu-lation as a policy for more productivealignment of market demands with pri-vately owned rail resources and new in-vestments.

As deregulation, in the form of openaccess to the European rail network, goesforward, liability will get more compli-cated. National railroads and new actorscould provide through rail service throughmultinational corridors. Traffic control,slot allocations, and multiple independentoperators using the same routes may cre-ate new factors in loss or damage claims.

The situation is fundamentally differ-ent in the United States. The railroads areprivate property, and businesses continueto invest and reinvest in these assets be-cause they own and control them. Mostmarkets are served by more than one rail-road. Average rail rates have been halved

Robert Gallamore,Trasnportation

TechnologyCenter, Inc.,

Richard Biter,U.S. Department

of Transportation,and DamianKulash, Eno

TransportationFoundation (left

to right)

Wim Blonk,European

Commission,DirectorateGeneral VII

Forum Proceedings 11

in real dollars since deregulation. Becauseof private ownership and investment inthe United States, proposals for competi-tive access raise a much larger set of issues.In Europe, where governments own the na-tional railroads, the priority given to achiev-ing market competitiveness may not be ashigh as if private-sector interests controlledthe assets. European transport interests areprepared to pay the full costs of the rail in-frastructure, but they also want to controlthe infrastructure. It would help to have thefull set of rail and road costs, payments, andsubsidies set out factually, so that policiesand decisions could be developed in a waythat maximizes competition.

The separation of infrastructure man-agement from operations is an issue forall rail operators, whether existing staterailways or other operators who may seekto enter the market. Many believe that thepolicy of seeking additional open accessfor operators who would run on the na-tional networks is a failure, because so fewoperators have emerged to purchase theaccess rights. Those that have purchasedaccess rights have tended to be tinyspecial cases. The infrastructure ownerfaces high costs and is not responsive tooperator concerns. Some operators whohave attempted to contract for the use ofrail facility report that their largest prob-lem is dealing with the infrastructureowner, who has a completely differentagenda and objectives from the operators.

Reregulation

The much-publicized service difficultiesfollowing the Union Pacific and SouthernPacific merger have stimulated some ship-pers to call for reregulation of the railroads.Carriers see this approach as unresponsiveto the real situation. Since the passage ofthe Staggers Act in 1980, the U.S. railroadindustry has 35 percent less track, 32 per-cent fewer locomotives, and 60 percentfewer employees, yet railroads in theUnited States are carrying 48 percent morefreight. Productivity has increased three-fold. The industry has reduced costs by$25 billion in constant dollars. Some 80percent of that cost reduction has been

passed on to shippers, resulting in railfreight rate declines of 1.2 percent per year.

Carriers believe it would be very dam-aging if railroads lost their ability to pricedifferentially where the market allows.Similarly, if the United States adopted anopen access system as envisioned for Eu-rope, it could have severe effects. Atpresent, system expenses and corporateoverhead benefit from the differential-pric-ing regime that supports traffic with littleor no profit margin. Railroads allocatetheir very large fixed expenses to classesof traffic based on market considerations.Intermodal rates are predicated on thesemarket considerations and could be im-paired by restricting this market freedom.

Best Practices inIntermodal Freight Transport

The intermodal share of the Europeanfreight market is currently only eightpercent. While a few intermodal operatorshave been expanding, there may be a rolefor additional providers of intermodaltransport. For economic and environmen-tal reasons, many have an interest in in-creasing the intermodal market share. Tothis end, the Freight and Logistics Lead-ers Club has been collecting actual dataon intermodal, rail, and truck services togain a better understanding of markets andopportunities. They have identified a num-ber of innovative developments, which areoutlined in the following paragraphs.

Rune Svensson,Volvo Transport

12 Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

Intermodal RailDevelopments in Sweden

The Scandinavian and Nordic railroadshave split infrastructure administrationfrom operations. Operators pay the rail fa-cilities managers a fee to use the rail plantand then run trains across these facilities.Operators can compete along the sameroute. Operators have shifted from beingclassical railroad operators, as they were10 years ago, and are offering door-to-doorsolutions to their customers. This shift hasresulted in enlarged intermodal marketshares in some cases. There have beenstrong service improvements. A directtrain and truck service to Italy that tookfive days when it began 10 years ago nowtakes only two days. In addition, reliabil-ity has improved.

Productivity has also improved signifi-cantly. For example, a very good rail networkand an ability to operate large, 60-tontrucks in Sweden has created an ideal set-ting for intermodal service. Railway costswere too high, however, and for short dis-tances, rail could not compete with directtruck. The Swedish railroad copied an ideafrom Japan and adopted a system that al-lows rail pick-ups between the hubs or railports. This approach makes intermodalrail service competitive for much shorterhauls because intermediate stops can bemade very short. No personnel are re-

quired at the intermediate terminals. Thelocomotive operator does the loading at theinterim stops using an on-board forkliftto load containers on or off. All-in-all, thismultiterminal, short-stop system is flex-ible, network-oriented, and very cost-ef-fective. Capital utilization is excellent.Unions were initially concerned aboutsafety, but the railroad has formed work-ing partnerships with the unions to resolvethis matter and to work with them to makethe railroad competitive for more classesof traffic. This type of service could be ex-panded to many other parts of Europe.

New International Rail Corridors

Rail-freight freeways must overcome manyproblems, particularly fragmentation. Eu-rope now has 43 infrastructure providers.Most of these providers are integrated withoperations, and they set timetables to op-timize their own operations. But for thefirst time this past year, the volume ofcross-border freight exceeded that of na-tional freight. To expedite this growingvolume, the European Commission intro-duced “One-Stop Shop.” It coordinates thetime tabling of all operators within a cor-ridor into a single organization.

Visionary investigations are underwayto explore Europe-India and Europe-fareast rail corridors, as well as a Berlin-War-saw-Minsk-Moscow corridor called the“Pan-European Rail-Corridor II.” WithinRussia, this concept breaks up the exist-ing system and separates different lines ofbusiness, each with its own business plan.The Trans-Siberian Railroad Council hasparticipated in these plans, and it hasadopted One-Stop Shop coordination. TheFinnish Railway now operates two directtrains per week through Russia. Using theTrans-Siberian route, shipping times canbe reduced from about 25 days via oceanshipping to about 12 days by rail. Globalrail has potential and is expanding. Thepolitical stability of the countries involvedhas been improving, and the problems ofdisparate gauges can be overcome.

However, missing links in the networkstill must be filled before it can reach far-eastern destinations. Construction is now

FrancoCastagnetti,

Enichem/PolimeriEuropa

Forum Proceedings 13

underway to fill the rail gaps in the SouthAsian corridor through India, and thiscorridor may be completely connectedwithin a year. Once this corridor is con-nected, it will allow rail freight to move toIndia from Europe. Differences in rail gaugeswill continue to exist, but these differencesmight be managed using technology that hasbeen tested for rail equipment moving be-tween Sweden and Finland, which has agauge similar to that used in Russia.

Supply-Chain Management

Up to now, mobility of cargo has beencharacterized by the management of logis-tics. But logistics within a company is nolonger enough to meet customer demands.Supply-chain management has emerged asan approach that brings all of the variablesinto perspective. Based on the rapidly ex-panding capabilities afforded by new in-formation technologies, enhanced byoutsourcing and partnering, supply-chainmanagement shows great potential for re-ducing costs and improving services.

Supply-chain management allows ex-ecutives to see and control all facets. Inresponse, firms are changing emphasisfrom distribution management to networkmanagement, from road and rail manage-ment to system management, from serviceprocurement to contract management, andfrom transport technique to technologymanagement. The emphasis is on systems.There are totally outsourced systems, andthere are new actors inside the corpora-tion. The culture needs to change from ashort-term focus to a longer-term reality.

Airship “Cargolifter” Service

Many innovations have evolved in inter-modal unit lifting technology, and an an-cient technology—the airship—may haverenewed promise today. Airship transportwould allow freight to go from everywhereto everywhere. It could reach parts of theglobe that are difficult to access becausethey have been destroyed by earthquakesor other natural disasters. It could carrycargo whose size or weight is unsuitable

for other modes of transport. It could avoidrehandling of cargo along a route.

An airship service—or “cargolifter”—might fill a niche (in time and cost) betweenocean shipping and airfreight service. Nospecial airfields are needed. Airships areable to land in an area about the size oftwo soccer fields with special tie-downequipment. The ports also need to providewater as ballast to offset the unloadedcargo. Using helium-filled balloons to liftpayloads, the cargolifters can carry 160tons (up to 3,200 cubic meters) for dis-tances of up to 10,000 kilometers. Marketstudies have estimated that 120 to 200ships of this sort could be viable.

JohannesFritzen,VolkswagenTransport

Kenneth Wykle,U.S. Departmentof Transportation,(left) with PeterZantal, The PortAuthority of NewYork and NewJersey

14 Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

Port Investment Policies

Private operators and firms make massiveinvestments to serve customer needs, butgovernment has a role as well. Govern-ments at all levels are concerned about thehealth and economic well-being of theircitizens. As major economic forces in theregion, port-related investments and poli-cies are driven by all levels of governmentas well as by private decisions.

Megaship service could further shiftthe concentration of power. These shipswill force new policy attention onintermodality and the types of intermodalsystems that are really beneficial. Becausemegaships will only be able to serve se-lected ports, they could create a vastly dif-ferent ocean-distribution system. Theirimpacts will reach far beyond the port it-self. The emergence of megaships willforce other transportation services andfacilities to respond. Megaships will alsogenerate changes in operating procedures,requiring investment in terminal and han-dling equipment.

The rise of carrier alliances in the ship-ping industry has forced ports to deal withthree or four large alliances instead of 20smaller customers. These large allianceshave approached competing U.S. portswith an open tender to establish east coasthubs. This consolidation of carriers, aswell as the introduction of megaships, willcreate a different balance of pricing power.Ports will lose pricing power, and oceancarriers will gain it. Competing in this newenvironment will require capital invest-ments—for post-panamax cranes anddock facilities to handle megaships, for

container handling and storage facilities,for expanded truck access, and for on-dockrail, because trucks alone simply cannothandle the volumes involved.

If market forces are to determine whichports move the cargoes, then the policymust be to eliminate state, regional, andlocal subsidies to ports. As a first step, weneed to know who is financing what. The1997 green paper by the European Union(Sea Ports and Maritime Infrastructure,COM (97) 678) recognizes the vital eco-nomic role of ports and the reality of com-petition between the member statesassociated with ports. The paper providesa financial overview of how ports are ac-tually financed.

European policy states that portfinance should be transparent. Any pub-lic subsidies that are made to ports aremade public. This policy would be diffi-cult to implement in the United States.Ports do not necessarily pay for ground-access and dredging costs. They benefitfrom cross-subsidies stemming from costallocation and multiple lines of busi-ness. Virtually every port in the UnitedStates receives some state or local sup-port, and some applications of federalprograms are effectively subsidies toports. U.S. ports would probably resistthe transparency in port finance beingsought by the European Commission.In matters of port finance, Europe ap-pears to be moving in a capitalistic, free-enterprise direction while the UnitedStates appears to be more socialistic.

Electronic Commerceand Intermodal Transport

Electronic commerce is the use of com-puter network technology to facilitate thebuying or selling of goods between trad-ing partners. Carriers serving this marketuse a physical network with air, ground,and ferry links in Europe. Systems are tiedtogether by electronic tracking and trac-ing capabilities, allowing customers to lo-cate their shipments at any time.

Some forecasts anticipate that elec-tronic-commerce in the United States willreach $500 billion in 2002. Companies are

Woflgang Flick,United Parcel

Service, Europe,and Dirk

Goedhart (right),Consultant to

PhilipsInternational

Forum Proceedings 15

positioning themselves to be leaders in thisfield. United Parcel Service (UPS), for ex-ample, has taken two steps into the worldof electronic commerce. The first step wasto enter into arrangements with merchan-disers to advertise jointly on the Internet.This strategy integrates UPS’s tracking ca-pability with the merchandisers’ orderingsystems, so customers know where theirorders are in the overall distribution anddelivery system. The second step was todevelop UPS Document Exchange. Thisproduct is a secure, online courier, usingthe ultimate security of 128-bit encryption,which was recently cleared for distribu-tion outside the United States.

Electronic-commerce is finding appli-cations in the rail sector. A new systemhas recently been made commerciallyavailable for electronic bills of lading, andthis system seems to be working quite well.However, nations differ in terms of whatcourts will accept as proof that a documenthas been sent, and these differences couldcomplicate international applications.

Toward ImprovedEuropean and U.S. IntermodalFreight Transport: Next Steps

Improved intermodal freight transport isimportant for transport productivity,economic growth, and environmentalprogress. Many public and private con-cerns share an interest in achieving thesegains, but they cannot make progress bythemselves. Shared understanding and co-ordinated action are essential. The ex-change of perspectives between sectors,regions, modes, and operating perspectivesoffers a fruitful way to develop shared in-sights that allow independent interests toact toward a common vision.

This useful dialogue that has been de-veloped through forums held on Europeanand United States intermodal Transportin 1997 and 1998 should be continued byholding a third session in the United Statesin the fall of 1999. The small size of theseforums, their informal style, and the par-ticipation of top-level transport leadersfrom all sectors have contributed to the

effectiveness of these forums. The 1999forum should carry forward and build onthe discussions that have been held onstandardization and best practices. Inaddition, it should begin a similar dialogueon the effects of electronic-commerce andinfrastructure investment policies. The1999 forum should also address cargo li-ability, regulations governing competition,third-party logistics providers, and othertopics of interest to participants, as out-lined in the following paragraphs.

Standardization

Greater interoperability can bring impor-tant gains to the efficiency of transport.Policies should support achieving theseproductivity improvements where appro-priate. The potential for increased stan-dardization depends on the degree ofmaturity in the industry, carrier operat-ing efficiencies, requirements for invest-ment by carriers and shippers, disparities

Karel Vanroye,Unit for Analysisand TransportPolicyDevelopment,Wim Blonk,Kenneth Wykle,and Richard Biter,(left to right)

Ron Stanley ,Landstar ExpressAmerica, BertSchacknies,Federal HighwayAdministration,U.S. Departmentof Transportation,Thomas Perdue,C.H. Robinson Co.James Morgan,TNT AutomotiveLogisitcs, andDavid Winstead,MarylandDepartment ofTransporation(left to right)

16 Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

in physical features of the surface trans-portation infrastructure, and the effects oncompetitive positions. The nuances ofthese factors are subtle, and they arebetter understood through candid discus-sions. The prospects for enhanced stan-dardization should remain on the agendain the 1999 forum.

European and U.S. Best Practices

The European working group to discussbest practices in intermodal freight hasbeen a source of many good ideas. It hasstirred great enthusiasm to work togetherfor improvement. Through this informalclub of captains of industry, public au-thorities are able to tap the private-sectorexperience, getting useful informationquickly. This working group may be an at-tractive model that may have value in theUnited States as well. U.S. participantswere impressed by the energy and enthu-siasm of the European best practices groupand will seek to establish a similar indus-try-driven, best practices group in theUnited States.

Electronic Commerce andIntermodal Freight Transport

Important, new, unfamiliar opportunitiesin intermodal transport will arise as elec-tronic commerce takes hold in the nextdecade. Further discussion should focuson how these developments might affectintermodal transport.

The Role of Governmentsin Infrastructure Finance

Public policy on both sides of the Atlanticseeks to build an economically sound in-frastructure investment framework, freefrom the distortions caused by modal orregional subsidies. In practice, this ideal isconfounded by disparities in user fees fordifferent modes, by inconsistent treatmentof external costs, by joint investments, byinconsistencies in the allocation of com-mon costs, by companion investments inaccess facilities, and by state and local sub-sidies. Major transport terminals drive theeconomies around them, making it diffi-cult to identify net public investment, letalone rationalize it across diverse local cir-cumstances. The 1999 forum should usecase materials from Europe and the UnitedStates to continue the discussion of infra-structure issues.

Liability

A proposal to reform the 1936 U.S.COGSA legislation would unilaterally ap-ply U.S. law outside its territory. This leg-islation could have a damaging effect oninternational commerce. It may also be dis-criminatory, because it could give a com-petitive advantage to U.S. carriers whenthey are in head-to-head competition withEuropean carriers to provide transport ser-vices. Such concerns need to be resolvedwith full awareness of their internationalimplications, and discussions like thesehelp to surface these concerns.

Interoperability in Intermodal Freight Transport 17

Article A:Interoperability in Intermodal Freight Transport

John BetakCollaborativeSolutions, Inc.

Ian BlackCranfieldUniversity

Edward MorlokUniversity ofPennsylvania

October 1998

Executive Summary

In October 1997, the Eno TransportationFoundation held a policy forum cospon-sored by the U.S. Department of Trans-portation and the European Commission,Directorate-General VII (Transport). Thisforum addressed issues in intermodalfreight transport in Europe and the UnitedStates. One area identified for further con-sideration was standardization, harmoni-zation, or interoperability of equipment,information, and communication tech-nologies. This paper provides a frameworkand background information reflectingobservations and data contained in the lit-erature, as well as conversations with se-nior industry representatives.

Changes in the patterns of trade andcommodity flows are leading to a rapidincrease in the amount of intermodaltransportation. This situation requires anincreased focus on system effects and theneed to modify facilities, equipment, andoperating practices to provide seamlesstransport among modes and nations. Thisnaturally raises the issue of standardiza-tion and the specific aspects of standard-ization addressed in this report—containerstandardization and interoperability in in-formation technology.

Containers and information technologyrepresent major choices that affect theform and operation of the system. Thesechoices cannot be taken lightly. They aremajor investments with relatively longlives associated with the equipment. Thus,one of the most important contributionsthat can be made by a document like thisreport is to suggest a framework withinwhich these questions and the issues asso-ciated with interoperability in containersand information flow can be considered.

Interoperability andHarmonization: A Change Process

European and North American supply-chain management and freight transpor-

tation represent a many-layered industrywith (a) interdependent and interlinkedmarkets and (b) independent and dis-jointed markets. These characteristics arewhat make harmonization of equipmentand technologies so challenging. Develop-ing a shared vision of what is to be har-monized and the resulting benefits iscrucial to success.

The harmonization task is a change pro-cess, and every change process has obstacles.Three types of barriers must be addressedto successfully achieve interoperable sys-tems, equipment, and procedures: technicalbarriers, business process barriers, and cul-tural barriers.

Technical barriers are specific to theindustry or organizations. These sorts ofbarriers can sometimes be eliminatedthrough team-based efforts to design newtechnologies or to design around the tech-nical barriers. Many of the issues associ-ated with harmonization of containers aretechnical barriers.

Business process barriers are often or-ganization or industry specific. These bar-riers are frequently the result of how anorganization or industry works.

Cultural barriers consist of existing hab-its, behaviors, and attitudes of everyonein an organization, industry, region, ornation, that is, the existing paradigms ofhow the world is “supposed” to operate.

Broadly speaking, improvements intransportation take two forms: a reductionin the cost of transport and improvementsin services that add value to the user.Clearly, many of the gains from increasedinteroperability are of the cost-reductionvariety, for example, improved containeruse resulting from investments in informa-tion technology that lead to better track-ing and control or reduced costs of terminalhandling resulting from standardization ofsizes and locking apparatus. The conse-quences of these gains can be far reaching,including improving the contribution mar-gin of intermodal services for the carriersinvolved and expanding the markets inwhich intermodal transport is competitive.

18 Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

Equally important are changes that en-hance the range of transport serviceoptions, but that may increase the directcost of transport services. Nevertheless,these changes benefit the system’s custom-ers. Actions that increase speed and reli-ability of transport often fall into thiscategory, with the increased cost of trans-port being more than offset by reducedshipper cost of inventory, reduced spoil-age, or increased shipper competitivenessresulting from more rapid and precise cus-tomer response.

An increasingly important driver inaddressing interoperability will be ensur-ing that customer expectations are an in-tegral part of the equation. In the finalanalysis, if customers receive no benefitsfrom harmonization, customers will notpay for the costs associated with achiev-ing interoperability. At the same time,customers are demanding increasing flex-ibility and visibility in managing theirsupply chains. If the intermodal freighttransport industry does not provide flex-ibility and visibility, customers will findsome other service provider who will givethem what they expect and demand.

Developing Interoperability: ASummary of ContainerStandardization

The recent history of container standardsleaves a number of unresolved issues:• Is there a need to develop a length stan-

dard longer than 40 feet (12.13meters)? Europe is moving toward 13.6meters (44.06 feet), which is not inharmony with any lengths developed inthe United States.

• Is the existence of two width stan-dards—2.438 meters (8 feet) and awider 2.55 meters (approximately 8 feet5 inches) so popular in Europe—acause for concern?

• Is there a need to reconsider the com-patibility of pallet sizes, the possibleemergence of small containers (logisticboxes), and the standard container?To answer these questions, issues of

cost and ease (or speed) of moving goodsthrough the supply chain need to be

considered. Studies that quantify the ef-fect of adopting standards on these per-formance measures of the supply areneeded.

Different stakeholders most likely canachieve consensus about the objectives ofstandardization. Where disagreement be-gins is in predicting the effect of standardson costs and use by stakeholders in differ-ent parts of the supply chain around theworld. The European standards organiza-tion developed standards that certainly re-spond to European needs but at the sametime may conflict with the wider require-ments of international trade with theUnited States and other countries.

Developing Interoperability: ASummary of Information Technology

Information systems in transportationhave become as important as the physicalmovement itself. To facilitate the smoothflow of information from one partner inthe intermodal transport chain to another,information systems must work inter-changeably and facilitate a diverse arrayof partnerships in a dynamic environment.The recent history of standards concernedwith information systems is captured inthe following quotation:

Products based on official standardshave not been widely implemented.On the contrary, they have oftenbeen displaced by so-called de factostandardized products, that is, prod-ucts successful in the market whosetechnology is based on either publicor private specifications (Bucciarelli1995, p. 423).This quotation leaves a number of un-

resolved issues regarding harmonization ofinformation systems in intermodal trans-portation:• How do we ensure that meeting shippers’

needs is an integral part of the justifica-tion of harmonization of intermodalfreight information systems?

• How do we address concerns within theintermodal transportation communityregarding data confidentiality, use ofinformation, business relationships,power, and competitive conditions?

Interoperability in Intermodal Freight Transport 19

• What role can government have in fa-cilitating the harmonization that isoccurring naturally within freight com-munities?

• How do we develop a shared vision ofwhat is to be harmonized in informa-tion systems, and what will be the ben-efits for the various members of theintermodal community?The following factors point to the need

for interoperability of hardware and soft-ware in the intermodal transport process:• Economies of scale can be generated in

producing standardized units.• Higher capital and operating costs can

be avoided by developing vehicles orvessels that can carry different loadunits or combinations of load units.

• Costs for providing specialized handlingequipment at intermodal transfer facili-ties can be reduced.

• A limited customer base for specializedunits often leads to inefficient use ofequipment or unused carrying capac-ity on vehicles.

• The ability to communicate with awider array of partners in the supplychain with reduced costs for interme-diary or translation software can beenhanced, particularly as the industrystructure changes and new intermodalalliances are developed.The main arguments against standard-

ized equipment and software are asfollows:• The flexibility to respond to unique

market challenges may be stifled.• The systems will be less responsive to

specialized product requirements, meth-ods of handling, or customer preferences.

• Standardized equipment may notnecessarily translate into lower overallsystems costs, particularly if the con-solidator function is not removed.

• The high initial capital costs of invest-ing in new equipment, facilities, or soft-ware may not be offset by future costsavings to the user.

• The “competitive edge” or stabilizationof partnerships that is provided by spe-cialized equipment and proprietary sys-tems will be lost.

• Sharing data among nonproprietarysystems raises security concerns.

• Developing standards that are compat-ible with operations and informationflows in all part of the supply chain andin different transport modes is difficult.

• The benefits and distribution of costsamong different parts of the supply chainand throughout the world are uncertain.Natural trends in production and dis-

tribution are adding complexity to supplychains and to transportation. Thus, theincentives for harmonization of informa-tion systems simply on the basis of self-interest are likely to increase. Thecomplexity of the many issues involved re-quires a more thorough understanding ofthe costs and benefits to different segmentsof industry, as well as the timing of theseeffects. The challenge for the intermodaltransport industry is to develop forumswithin which these questions can be re-solved in a voluntary manner.

The Forces Driving andConstraining Interoperability

Rationale

The need for interoperability in transpor-tation services is clear: Elements of thesystem such as vehicles, guideways, andcontrols must be able to operate togetherto provide service. Also, the geographicscope of transportation flows often leadsto individual shipments being carried bytwo or more transportation companies,often over facilities provided by yet an-other organization (frequently a govern-ment infrastructure agency).

The issue of standardization is alwayspresent in a dynamic technological envi-ronment, and the current situation ofcontinuous change in applications of newtechnologies certainly raises the issue. Ofequal importance are changes in demandfor transportation. In particular, increas-ing globalization and regionalization ofsupply chains necessitates transportationservices that transcend traditional na-tional and modal boundaries. Trends to-ward just-in-time inventory policies, masscustomization, and rapid customer re-sponse all demand more rapid and

20 Toward Improved Intermodal Freight Transport in Europe and the United States: Next Steps

reliable transportation services over in-creasingly intermodal and multicarriernetworks.

The trend toward longer supply chainsleads to longer hauls and increased like-lihood of intermodal movements. Modesthat did not exchange much traffic, andthus developed in isolation in ways thatare not readily compatible, can suddenlybe logical parts of integrated supplychains. Thus, issues of compatibilityacross different modal transportation ser-vices arise. The trend toward new pat-terns (spatial and otherwise) of industriallinkages also means that national or re-gional transportation providers who hadoverlapping or contiguous service areasbut did not exchange traffic may findthemselves called upon to provide ser-vices in an integrated way.

Elements of Interoperability

Which elements of the transportation sys-tem are reasonable targets of efforts at har-monization to enhance interoperability?Most elements of each modal system donot operate directly with one another. Inintermodal transportation, the primaryelements related to seamless functioningof the system are the containers that carrythe goods and the information flow on themovement of containers and shipments.Our focus is on these two areas.

Modal Ownership Patternsand Intermodal Transport

While the transport system is increasinglythought of as intermodal, the reality is thatmost transport is considered either(a) unimodal or (b) intermodal with onlyvery limited interconnections. This situa-tion reflects both the physical reality andthe result of institutional arrangementsthat often diminish the apparent magni-tude of intermodal connections.

The prominent role of various third par-ties or integrators in providing intermodaltransport also diminishes the apparent sig-nificance of intermodal transport to par-ticipating modal carriers. Other firms are

more heavily asset based but use comple-mentary modes and organize use so thatit is transparent to the shipper. Examplesinclude United Parcel Service (UPS), vari-ous truck lines, and national postal ser-vices. These firms also relieve modalcarriers of direct responsibility for theintermodal aspects of transportation. Be-cause so much work unique to intermodalservice is provided by these various firmsand agencies, the immediacy of intermodalthinking among modal carriers is furtherreduced.

In this environment, intermodal con-siderations are not of paramount impor-tance to all transportation carriers. Theirconcerns for efficiency, responsiveness tomarkets, and profitability are likely to bedriven largely by other portions of theirbusiness and activities. Thus, efforts atharmonization of intermodal systemsmust retain compatibility with the rest ofthe relevant modal systems.