overview, the rules, risks & rewards, 2 case studies€¦ · capital accounts will be distinct...

TRANSCRIPT

Overview, the Rules, Risks & Rewards, 2 Case Studies

1. What is Twinning?

2. Rewards of Twinning

3. Risks of Twinning

4. Rules of Twinning

Part One: What is Twinning?

Separating a Single Project with Multiple Revenue Streams into Multiple Projects with Separate Revenue Streams, Allocating Costs to Each Project, and Funding Each Project with Distinct Sources of Funding

▪ NMTC-LIHTC

▪“80-20” NYC Deals

3

Rules of Twinning

4

Post-HERA, IRC §42(i)(2) provides that

a new building is treated as "federally subsidized" if

the proceeds of a tax-exempt bond are

used (directly or indirectly) with respect to

the building or its operation. . .

The applicable percentage for these buildings is limited to the 30% applicable percentage under IRC §42(b) (1) (B) (ii).

The Risks of Twinning

The Risk

9%

▪ Total Eligible Basis: $10,000,000

▪ Allocation: $900,000

▪ Total Credits: $9M

▪ $1.00 Price

Pre-taint Equity = $9M x $1.00 = $9M

4%

▪ Total Eligible Basis: $10,000,000

▪ Annual Credit: $322,000

▪ Total Credits: $3.22M

Post-taint Equity = $3.22M x $1.00 = $3.22M

*Credit Rates 9.00%-3.22%

Adjuster of $5.78M + penalties and interest

5

The Rewards of Twinning

▪Cap on Credits or Scoring Criteria in QAP (Efficient Use of Resources)

▪Insufficient Federal, State & Local Subsidies for Gap Financing in TE/4% Project

▪“Monetizing” the Surplus Basis

▪Incentivize Behavior (use TE Bonds)

6

Virginia’s 9-4 ResultsDeal Name Final Credits per Unit (9%) # 9% Units # 4% Units Total Units Total Credits Needed if Not Split Total 9% Credits Awarded Total Savings

2015

Church Hill North Phase I $11,399 60 48 108 $1,231,094 $683,941 $547,153

Clairmont Apartments $10,952 84 68 152 $1,664,762 $920,000 $744,762

Columbia Hills East $21,582 97 132 229 $4,942,387 $2,093,500 $2,848,887

Fieldstone Senior $10,142 60 84 144 $1,460,491 $608,538 $851,953

Lexington I $14,258 48 148 196 $2,794,515 $684,371 $2,110,144

Wexford Manor $11,548 38 36 74 $854,573 $438,835 $415,738

387 516 $7,518,637

2016

Birchwood at Brambleton $15,065 56 27 83 $1,250,422 $843,658 $406,764

Gilliam Place East $23,494 83 90 173 $4,064,458 $1,950,000 $2,114,458

139 117 $2,521,222

2017

Jackson Ward Senior $10,828 72 122 194 $2,100,613 $779,609 $1,321,004

October Station $12,365 48 39 87 $1,075,721 $593,501 $482,220

Price Street Apartments $11,184 152 112 264 $2,952,632 $1,700,000 $1,252,632

Senior Residences at North Hill $9,417 63 52 115 $1,082,940 $593,263 $489,677

The Berkeley $20,000 125 131 256 $5,120,000 $2,500,000 $2,620,000

The Residences at North Hill 2 $18,912 75 89 164 $3,101,505 $1,418,371 $1,683,134

535 545 $7,848,666

1061 1178 Total Savings (2015-2017): $17,888,525

7

VHDA Summary for 9-4s

• In 2015 VHDA began offering points for 9% developments with 4% tax exempt bond funding on the same site. Government Residences was the catalyst and was funded in 2014.

• Since 2015, 14 deals that have received an allocation of 9% credits as part of this 9-4% initiative. – 14 Deals that add 2,239 total units – 1,061 funded with 9% credits; 1,178 with 4% bond financing

• VHDA’s 9-4% initiative has saved $17,888,525 in 9% credits since 2015. Savings calculated by 9% credits per unit allocated to a deal and multiplying that times the total number of units (9% and 4% combined). The difference in what was actually allocated and what would have been needed if all of the units were 9% units is considered the savings.

8

Twinning Rules—Pitfalls to Avoid

IRS Guidance (scant)

1995 Technical Advice Memorandum—IRS rules that multiple building project with TE bonds in some buildings will taint 9% in same project because:

• Cross collateralization of buildings as lender security

• Bond Indenture must specify use of bond proceeds (consistent with 95-5 tests) or bond proceeds are pro rata on all property (both 9% and 4% buildings).

[Note, NOT an issue with separate projects.]

2000 Private Letter Ruling—IRS finds that TE bonds and 4% for acquisition and 9% for rehabilitation taints 9% due to ‘single plan of financing’ (independent would be ok).

[Note, this was ONE physical building with acq “building” and rehab “building”, need to rehab is tired to acquisition.]

9

The Rules of Twinning

IRS Guidance

First Separate It, then Allocate It:

1. IRS Notice 88-91 (on BINs)—recognizes condominium units as a separate tax credit ‘building’. That is, an apartment building, single family unit, townhouse, rowhouse, duplex or condominium are each a “qualified low-income building” per the IRS. Voluminous support for this.

2. Allocation Rules

10

First, Separate It! The Real Estate

▪ Subdivide

▪ Ground Leases

▪ HUD-FHA Rider

▪ LIHTC Issues

▪ Condominium or Air Rights (A&T Lots DC)▪ Virginia versus Maryland (Doug Irvin of Ballard Spahr)

▪ Condo Documents, Voting Rights, Common Areas

▪ Time (Sequencing)—if needed

▪ Agency & Lender Concerns

▪ Security

▪ Silo versus checkerboard approach

11

First, Separate It!The Noah’s Arc of

DocumentsTWO OF EVERYTHING:

▪ Construction Contract (or alternatives)

▪ Architect Agreement

▪ Developer Agreement

▪ Corporate Documents

▪ Attorney; Accountant; Other Professionals

▪ Property Management Agreements; Consulting agreements

12

13

First, Separate It! The Costs

▪ Hard Costs

▪ Soft Costs

▪ Common Areas

▪ Parking

▪ Shared Amenities

▪ Systems and Facilities

▪ Cost Sharing

▪ Maximizing Basis in Each Project

▪ Unique Rules for TE Bonds versus 9%

▪ Lessons Learned—parking in residential, etc.

14

First, Separate It! The Costs

▪ General Rule: allocate between uses according to “any reasonable method that properly reflects the proportionate benefit to be derived [Novogradacsec 3:115 (citing Tax Reform Act of 1986 page 159).]

▪ Issues When Dividing development costs between the two entities

▪ 4% considerations

▪ Land costs

▪ 50% test

▪ Qualified costs / 95-5 test

▪ 9% considerations

▪ Impact on the application

▪ Capital accounts will be distinct

▪ NOI and local subsidy debt

▪ Bond documents must be drafted to explicitly allocate 100% of the bonds to 4% project

▪ Generally, Tax Exempt bond proceeds should not finance any portion of common areas or shared uses (“subordinate and related” test for TE Bonds and to avoid the “taint”)

▪ No cross-defaults

15

1. Many Types of Twins

2. Case Study #1 Residences at Government Center

3. Case Study #2 Gilliam Place Apartments

16

17

18

19

20

Case Study #1

Summary Project Details

Building

• 270 apartment units

• 150 units in Condo A (the 9% deal)

• 120 units in Condo B (the 4% deal)

• Structured Parking - 348 spaces

• Amenities include: community room, pool, fitness center, playground, business center, secure mail room

Property Information

• Location: Fairfax, VA

• Delivery Date: March 2017

• Construction Type: New Construction

• Occupancy Type: Family

• LIHTC Amount: $25 million

• Current Occupancy: 100%

Momentum

at Shady

Grove

Residences at Government Center

Timeline

2013 2014 2015 2016 2017

Studied Virginia QAP to structure a competitive 9% deal

Virginia revised QAP to incentivize applicants to submit using hybrid 9/4

structure

June 2014: 9% LIHTC Award was secured

Received “buy in” from all financing participants

Initial Closing

Construction

Project originally conceived as a 4% Transaction through RFP with Fairfax County

July 17, 2014 – Fed announces tapering of bond purchases. Bond markets retreat, deal becomes infeasible

SCG Development finds a creative structure to execute a tax credit transaction

100%

Leased as of

June 1st

9% LIHTC Application submitted

Sources & Uses

• 99 year ground lease with Fairfax County

• HUD 221(d)4 leasehold mortgage loan financing for each Condominium

• Cash collateralized short term bonds - Condominium B provided by Stifel*

*See next slide

Summary Project Details

Sources Total 9% LIHTC 4% LIHTC

First Mortgage Loan $30,000,000 $15,800,000 $14,200,000

Tax Credit Equity 26,000,000 18,200,000 7,800,000

Deferred Developer Fee 2,000,000 0 2,000,000

Total $58,000,000 $34,000,000 $24,000,000

Uses Total 9% LIHTC 4% LIHTC

Acquisition $0 $0 $0

Hard Construction Costs 42,000,000 24,300,000 17,700,000

Transaction Costs 7,400,000 4,600,000 2,800,000

Reserves 1,800,000 1,200,000 600,000

Interest Expense 2,000,000 1,200,000 800,000

Developer Fee 4,800,000 2,700,000 2,100,000

Total $58,000,000 $34,000,000 $24,000,000

Stifel: Bond Execution

Original Issue

■ $13,000,000 closed March 26, 2015

■ Initial Mandatory Tender – April 1, 20161

■ Initial Bond interest rate – 0.40% for 12 months2

■ A Section 221(d)(4) loan bearing interest at 3.57% provided collateral for the Bonds

■ Optional redemption on October 1, 2015

■ Negative arbitrage deposit at closing - $53,000

Remarketing

■ $13,000,000 remarketed April 1, 2016

■ Mandatory Tender – April 1, 20173

■ Remarketing interest rate – 1.00% for 12 months4

■ Money in the collateral fund was reinvested in a U.S. Treasury Note bearing interest at 0.67%

Notes:

1. Approximate construction period of 21 months – set initial tender date at 12 months then remarket for additional 12 months to capitalize on

money market eligibility.

2. 1-year MMD approximately 0.18% as of March 20, 2015

3. Money market rule change looming and interest rate advantage for eligibility has faded at time of remarketing

4. 1-year MMD approximately 0.53% as of March 21, 2016

COMBINED TAXABLE DEBT WITH SHORT TERM TAX

EXEMPT BONDS AND 4% LIHTC –

FAQ/ISSUES

27

Bond Amount to meet 50% test > Taxable Loan Amount:

Other (bankruptcy remote) sources of funds (i.e. bridge equity, subordinate loan

proceeds, etc.) are needed to cover the differential. Timing of funding is critical. Seller

Take-Back loan can often be used to collateralize bonds (see applicable slides)

Investment and other options to reduce cost:

Although short term rates have gone up, taxable investment options have gone up

also: Ex.1.25% bond rate less 1.25% investment rate = 0.00% net interest cost per

year on bonds.

Seller Take-Back Bonds can sometimes be used to help reduce costs further (see

applicable slides)

Multiple loans/projects can be pooled into a single bond issuance to spread out fixed

closing costs – all deals need to be in a position to close within the same timeframe.

Kent Neumann 703-568-0190

Despite the recent increase in short-term, tax-exempt rates, the

negative arbitrage deposit can still be significantly reduced.

28

Source: Bloomberg. Thomson Reuters

Reflects market conditions as of September 26, 2017

Thomson Reuters Municipal Market Data (MMD) AAA curve is a proprietary yield curve that provides the offer-side of AAA rated state general obligation bonds

Historical Performance for 2-Year MMD (plus credit spread) and 2-Year UST

2-Year MMD 0.87

Add: Credit Spread 0.43

Bond Rate 1.30

Less: Reinvestment Rate 1.26

Net Bond Rate 0.04

Pricing Indications

29

Publically Offered vs. Privately Placed:

Potential tax implications if Bond Purchaser is “related” to the Borrower (see §1.148

program investment regulations)

Costs of issuance are very close. Interest and investment options can vary.

Issuer considerations:

Possible limitation on Issuer Fees due to short maturity and Loan Yield limitations

Some states have very limited private activity volume cap – although this structure

does use the minimum amount of bonds to meet the 50% test

A few Issuers do not allow the structure due to limitations on fees.

Kent Neumann 703-568-0190

COMBINED TAXABLE DEBT WITH SHORT TERM TAX

EXEMPT BONDS AND 4% LIHTC –

FAQ/ISSUES

Aerial View

APAH- Mission Centered Development

Case Study #2: Gilliam Place

October 2017

Project Overview

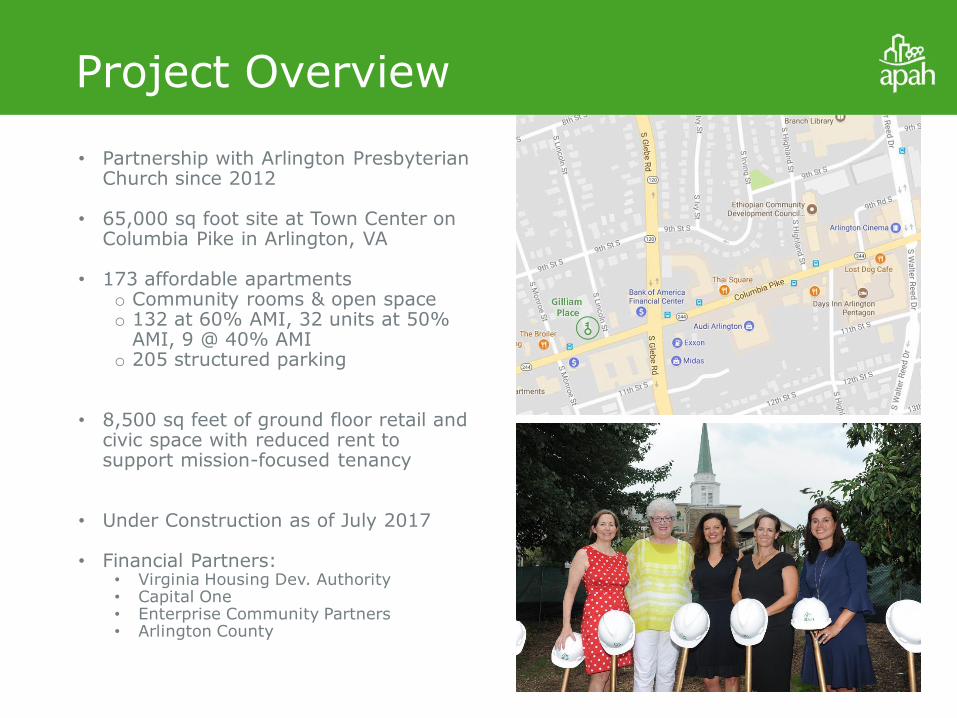

• Partnership with Arlington Presbyterian Church since 2012

• 65,000 sq foot site at Town Center on Columbia Pike in Arlington, VA

• 173 affordable apartments o Community rooms & open spaceo 132 at 60% AMI, 32 units at 50%

AMI, 9 @ 40% AMIo 205 structured parking

• 8,500 sq feet of ground floor retail and civic space with reduced rent to support mission-focused tenancy

• Under Construction as of July 2017

• Financial Partners:• Virginia Housing Dev. Authority• Capital One• Enterprise Community Partners• Arlington County

• Reflect the church’s discernment process:

o Discipleship—Church of the 21st Century

o Crossroads—outreach to community

o Affordable Housing--drives both mission and economics

• Leverage underutilized site• Declining Sunday attendance and cash • Financing and development model to:

• minimize risk,

• maximize program,

• provide good stewardship of land

Arlington Presbyterian Church – APAH Project

33

34

GARAGE

RETAIL / CIVIC

RETAIL

WEST (4% LIHTC Deal)

BUILDING LOBBY

ALLEY

GARAGE ENTRANCE

LOADING DOCK

EAST (9% LIHTC DEAL)

BUILDING LOBBY

FIRST FLOOR PLAN

9 PARALLEL PARKING

SPACES ALONG

LINCOLN ST.

6 PARALLEL PARKING

SPACES ALONG

COLUMBIA PIKE.

Gilliam Place-Hybrid- 2 buildings

Gilliam Place-Closing Budget

Total Per Unit Total Per Unit Total Per Unit

VHDA Bonds (Taxable / Tax Exempt) 4,380,000 52,771 1,500,000 16,667 - -

SPARC 1,494,000 18,000 3,240,000 36,000

REACH 2,000,000 24,096 2,000,000 22,222

AHIF 2,767,953 33,349 6,799,795 75,553 - -

Accrued Interest (AHIF Loan) 469,773 5,660 136,676 1,519 8,568,716 49,530

Tax Credit Equity 21,885,333 263,679 9,253,367 102,815 - -

FHLB AHP Funds 500,000 6,024 - - - -

VA HTF Loan 700,000 8,434 - - - -

Deferred Developer Fee - - 837,410 9,305 - -

Transit Oriented Aff. Hsg Fund and Other - - 925,298 5,349

APAH Sponsor Loan 1,120,380 13,499 1,674,007 18,600 - -

Proceeds from land sale 693,087 4,006

Total Sources 35,317,439 425,511 25,441,255 282,681 10,187,101 58,885

Acquisition 697,615 8,405 137,082 1,523 8,691,103 50,238

Construction 22,788,039 274,555 16,501,683 183,352 800,998 4,630

Soft Costs 8,247,853 99,372 4,875,433 54,171 690,000 3,988

Developer Fee & Reserves 3,583,931 43,180 3,927,057 43,634 5,000 29

Total Uses 35,317,438 425,511 25,441,255 282,681 10,187,101 58,885

Gilliam Place East/ 9%

(83 Units)

Gilliam Place West

(90 Units)Gilliam Place LLC (land)

Gilliam Place - Closing Budget

Twinning: Lessons Learned

• Cost allocation

• Consider your options for allocation method – Unit Count, Gross SF, Land Area, Detailed Construction Cost Breakdown

• A simpler method will make administration easier

• Design considerations

• How will the building operate?

• What features will be duplicated? Shared?

• Ensure commercial space is compatible with financing

• Increased documentation

• Think carefully about construction administration – how will draws be approved? Change orders?

• Good record keeping is critical

• Side-by-side underwriting

• Work closely with your investor and lender(s)

37

SCG Development

Stephen P. Wilson

President-Principal

8245 Boone Boulevard

Suite 640

Tysons Corner, Virginia 22182

Phone: (703) 942-6610 ext. 210

Cell: (703) 627-5056

www.scgdevelopment.com

Stifel, Nicolaus & Company

John B. Rucker

Managing Director

2660 Eastchase Lane

Ste. 400

Montgomery, AL 36117

Phone: (334)-834-5100

Carmen Romero

Vice-President, Real

Estate Development

Kent Neumann, Esq.

TIBER HUDSON LLC

202-973-0107 (direct)

703-568-0190 (cell)

https://tiberhudson.com/Erik T. Hoffman

Klein Hornig LLP

1325 G Street NW, Washington, DC

20005

202-842-0125 (direct)

www.kleinhornig.com