overview of credit policy and loan characteristics chapter 15 bank management 5th edition. timothy...

TRANSCRIPT

OVERVIEW OF CREDIT POLICY AND LOAN CHARACTERISTICS

Chapter 15

Bank ManagementBank Management, 5th edition.5th edition.Timothy W. Koch and S. Scott MacDonaldTimothy W. Koch and S. Scott MacDonaldCopyright © 2003 by South-Western, a division of Thomson Learning

Recen

t tr

en

ds in

loan

gro

wth

an

d q

uality

The lending process.

A popular way to categorize banks reflects their orientation to business or individual borrowers:

1. Wholesale banks emphasize business lending

2. Retail banks emphasize lending to individuals

Obviously, most banks make loans to both types of borrowers.

Credit risk diversificationconsumer versus commercial borrowers

65.1%

34.9%

62.1%

37.9%

58.4%

41.6%

55.3%

44.7%

56.8%

43.2%

56.6%

41.7%

60.1%

39.9%

59.0%

41.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Dec-88 Dec-90 Dec-92 Dec-94 Dec-96 Dec-98 Dec-00 Dec-01

Commercial Borrowers Consumer Loans

Twin Goals of Lending

The bank does not have the luxury of being overly selective in the lending process.

There are a limited supply of quality loans. Hence the bank has two goals in formulating

their lending policy:1. Loan Volume2. Loan Quality

The bank must balance these with: Liquidity requirements Capital constraints Risk constraints Return objectives

Relative importance of loans, investment securities and cash assets

0%

10%

20%

30%

40%

50%

60%

1935 1941 1947 1953 1959 1965 1971 1977 1983 1989 1995 2001

Pe

rce

nt

of

To

tal

As

se

ts

Cash as a Percent of Total Assets

Investment Securities as a Percent of Total Assets

Total Loans as a Percent of Total Assets

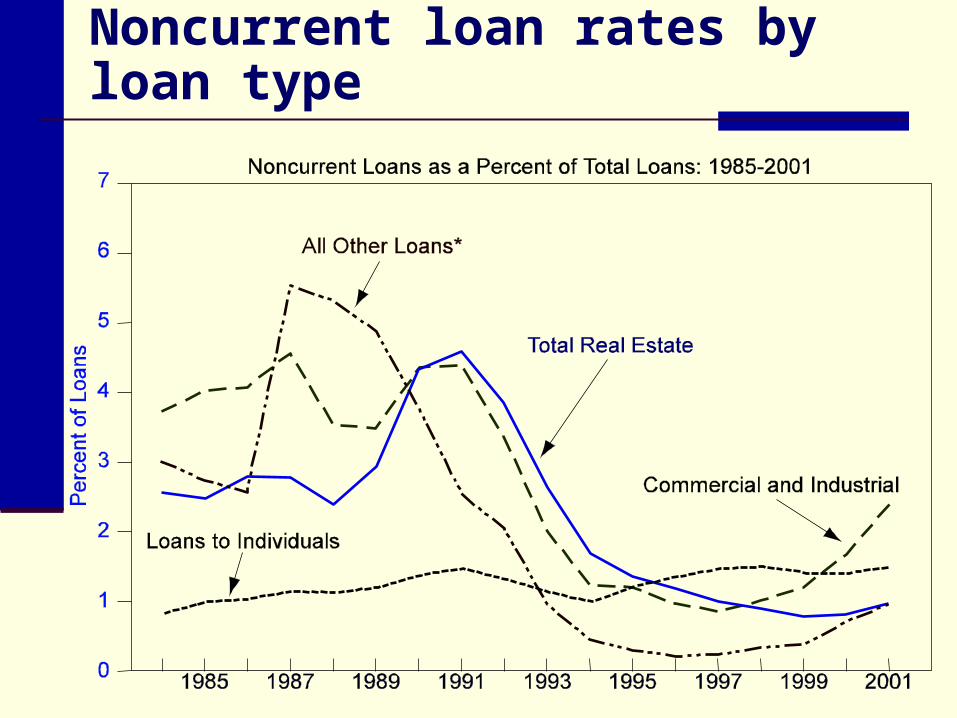

Noncurrent loans as a percent of total loans

1.74%

1.61%1.65%

2.11%

1.80%1.88%

2.31%2.22%

1.77%

1.16%

0.77%0.70%

0.64%0.57%0.57%0.58%

0.69%

0.84%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

Pe

rcen

t o

f T

ota

l Lo

ans

1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Noncurrent loan rates by loan type

Net charge-offs by loan type

Cre

dit

card

loss r

ate

an

d p

ers

on

al b

an

kru

ptc

y

filin

gs

Net Charge-off Rate (%) Number of Bankruptcy Filings (Thousands)

PersonalBankruptcy

Filings

Credit Card Charge-Off Rates

7

6

5

4

3

2

1

0

400

350

300

250

200

150

100

501984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Trends in competition for loan business

There were almost 14,500 banks by 1984 and only about 8,000 by the beginning of 2002

This reduction in the number of banks is a direct result of the relaxation of branching restrictions and increased competition

Banks today face tremendous competition for business they were previously uniquely qualified for

This has brought about a great deal of consolidation as banks have attempted to lower costs and provide a broader base of services

Increased competition for loans

Although banks have historically been the primary lenders to business, these businesses can obtain loans from many different sources today: commercial finance companies (AT&T Capital,

Commercial Credit, and GE Capital Corporation),

life insurance companies, commercial paper, and the issuance of junk bonds.

Reduced regulation, financial innovation, increased consumer awareness, and new technology have made it easier to obtain loans from a variety of sources.

The impact of technology on the bank’s lending market

Lending is not just a matter of making the loan and waiting for payment.

Loans must be monitored and closely supervised to prevent losses.

Technology advances have meant that more loans are becoming “standardized,” hence easier for market participants to offer in direct competition to banks.

Technology, loan standardization and credit scoring

Loans with standard features and uniform loan applications are more easily packaged and sold. The most commonly securitized loans are

those with the most standard features; mortgages, government-guaranteed student loans, small business loans sponsored by the Small Business Administration (SBA), credit card and auto loans.

Loans with standard features can be offered by more market participants, hence these loans often offer the smallest margins.

Many other loans are more difficult to credit score and securitize.

Not all loans can be standardized, credit scored and securitized (sold in marketable packages). Many farm and small business loans are

designed to meet a specific business need. Repayment schedules and collateral are often

customized so that they do not conform to some standard.

Medium to large businesses will have specialized needs as well.

Not surprisingly this is the area of lending that is still dominated by commercial banks and the area in which the bank is uniquely qualified for.

The credit process

Four Basic steps in the credit process:1. Business Development

2. Credit Analysis

3. Credit Execution and Administration

4. Credit Review Each of these three functions reflect the

banks loan policy.

Loan policy…formalizes lending guidelines that the employees follow to conduct bank business

It identifies and outlines: preferred loan qualities; and establishes procedures for granting,

documenting and reviewing loans Management’s credit philosophy determines

how much risk the bank will take and in what form

Credit culture…the fundamental principles that drive lending activity and how management analyzes risk.

There are three potentially different credit cultures:

1. Values-driven focus on credit quality

2. Current-profit driven and focus on short term earnings

3. Market-share driven focus on having highest market share

Business development

Market Research, Advertising, Officer call programs, and Obtaining a formal loan request

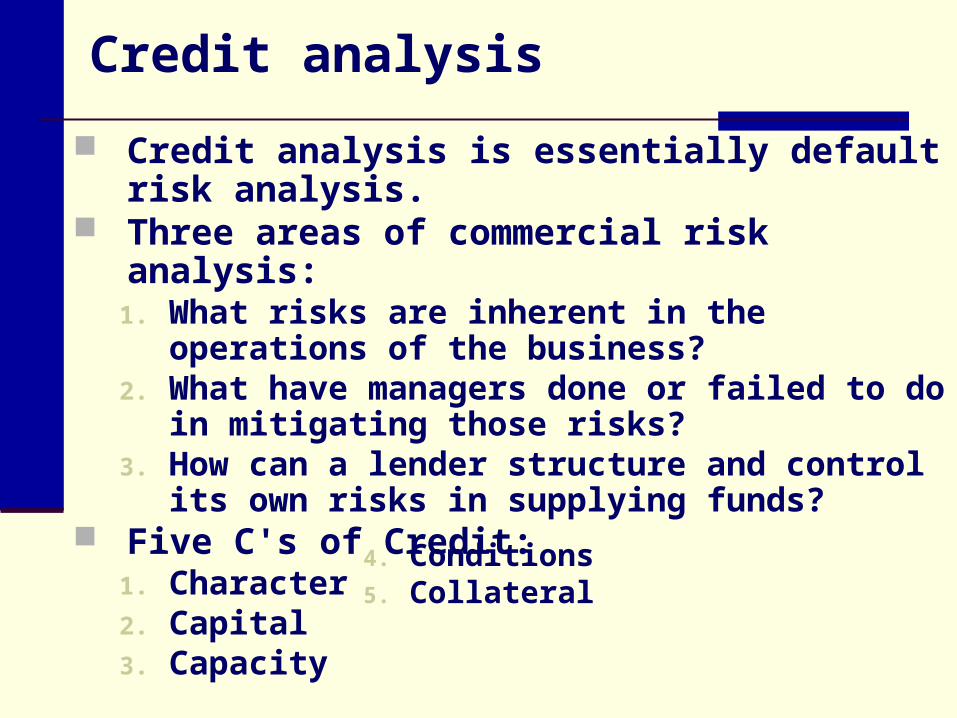

Credit analysis

Credit analysis is essentially default risk analysis.

Three areas of commercial risk analysis:1. What risks are inherent in the operations of

the business?2. What have managers done or failed to do in

mitigating those risks?3. How can a lender structure and control its own

risks in supplying funds? Five C's of Credit:

1. Character2. Capital3. Capacity

4. Conditions5. Collateral

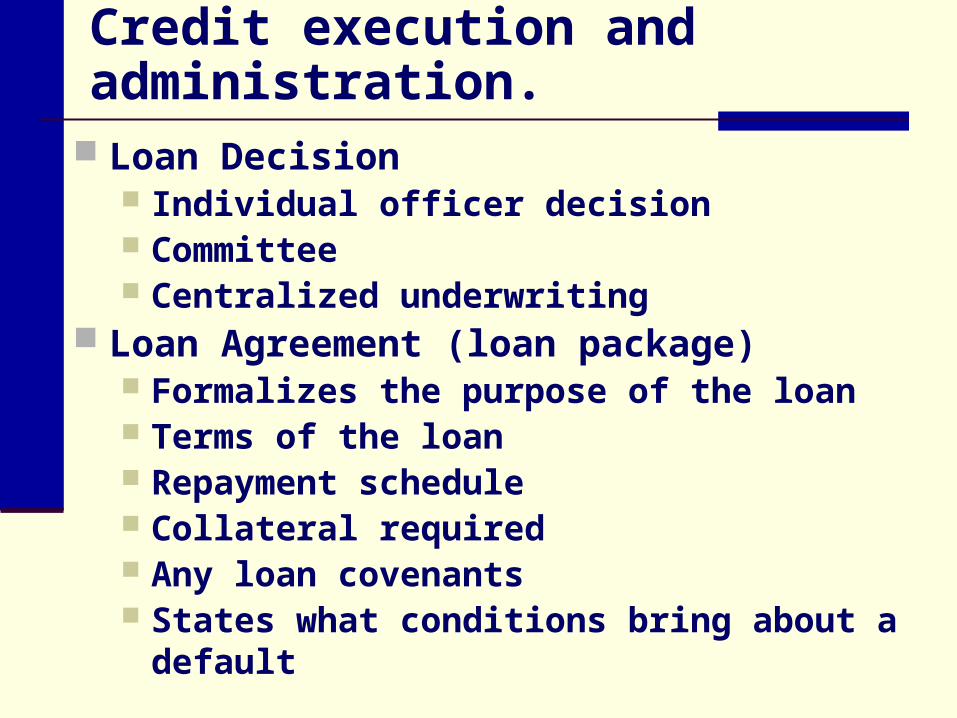

Credit execution and administration.

Loan Decision Individual officer decision Committee Centralized underwriting

Loan Agreement (loan package) Formalizes the purpose of the loan Terms of the loan Repayment schedule Collateral required Any loan covenants States what conditions bring about a default

Documentation

Perfecting the bank's security interest in collateral When the bank's claim is superior to that of

other creditors and the borrower Methods to perfect collateral interest

Require the borrower to sign a security agreement

Obtain title to equipment or vehicle Insurance (life, equipment, fire and causality)

Loan Covenants When a bank makes a loan, they in effect put

their profitability and solvency on the line

Credit review…Effective credit management separates loan review from credit analysis

The loan review process can be divided into two functions: Monitoring the performance of existing loans. Handling problem loans.

The loan review committee should act independent of loan officers and report directly to the chief executive officer.

Characteristics of different types of credits

Banks try to match credit terms with a borrower's specific needs. Long term financing needs are financed with

long term loans. Short term needs with short term loans.

Other loans

Real estate Loans Agriculture Loans Consumer Loans

Very different from commercial lending Usually much less time is required to make

consumer loans Much smaller amounts

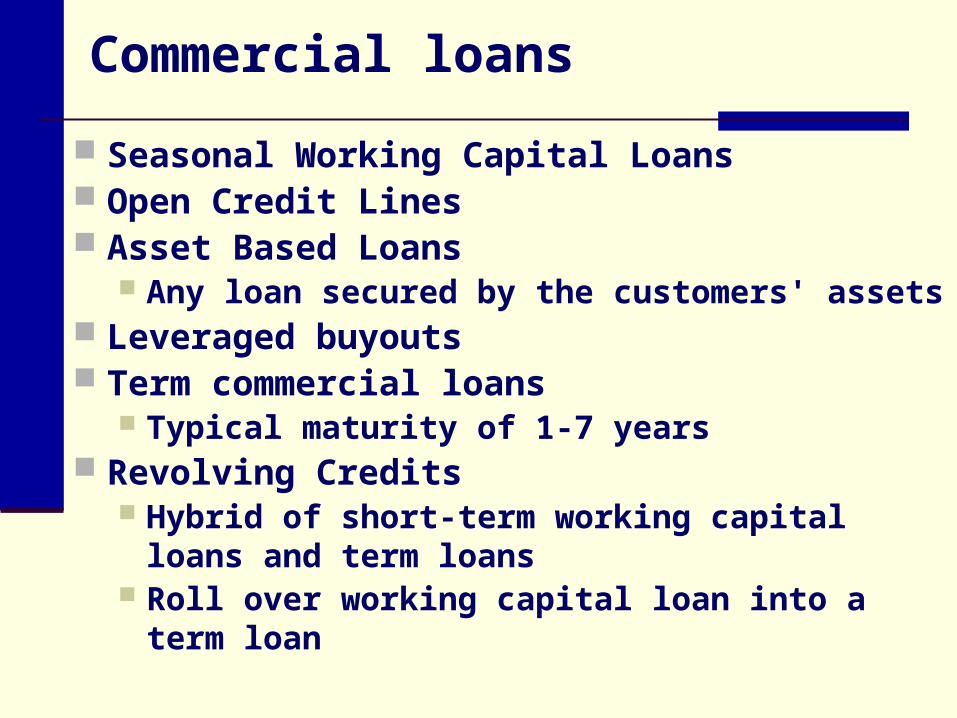

Commercial loans

Seasonal Working Capital Loans Open Credit Lines Asset Based Loans

Any loan secured by the customers' assets Leveraged buyouts Term commercial loans

Typical maturity of 1-7 years Revolving Credits

Hybrid of short-term working capital loans and term loans

Roll over working capital loan into a term loan

Working capital requirements

Net Working Capital= Current Assets - Current Liabilities

Typically, net working capital is positive Assets must be financed by:

liabilities or equity Typically, trade credit current liabilities will

finance a part of a companies current assets without the need for short term bank credit

Working capital cycle…Compares the timing differences between converting current assets to cash and making cash payments on obligations

Cash-to-cash cycle…the difference, in days, required for a company to convert its current assets and current liabilities into cash The cash-to-cash cycle essentially measures

how long a firm can receive interest free financing (trade credit)

Working capital needs = Difference in the cash-to-cash cycle times the average daily cost of goods sold

Cash to cash cycle

Days Cash

Days Payable

Days InventoryDays Acct Rec

Days Accruals

Days Financing

Working Capital Financing needs = deficit times Avg. Daily COGS

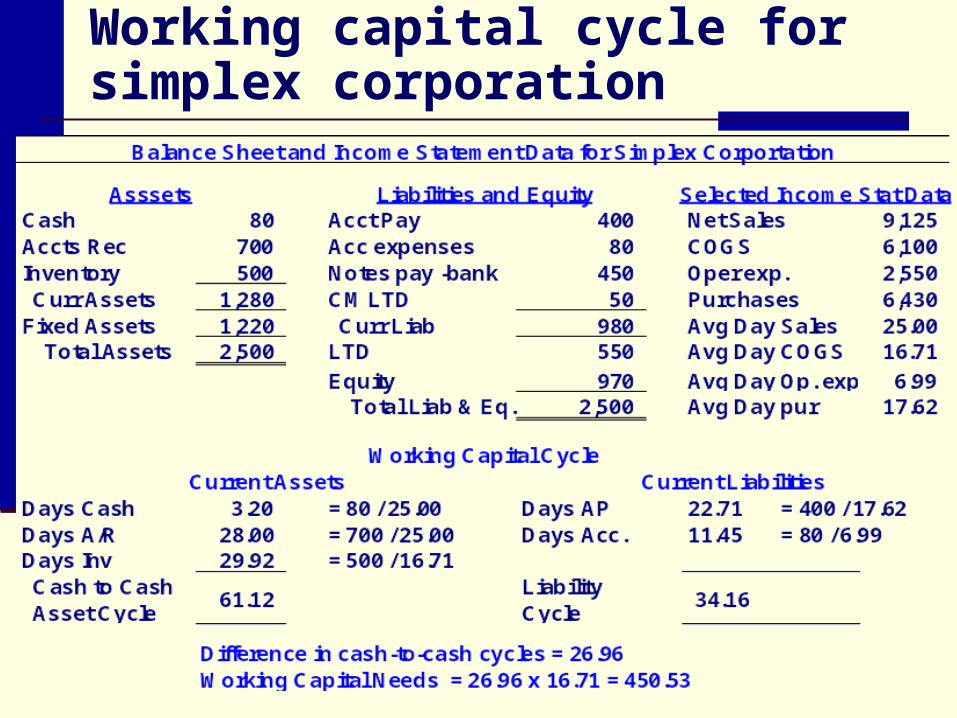

Working capital cycle for simplex corporation

Cash to cash cycle

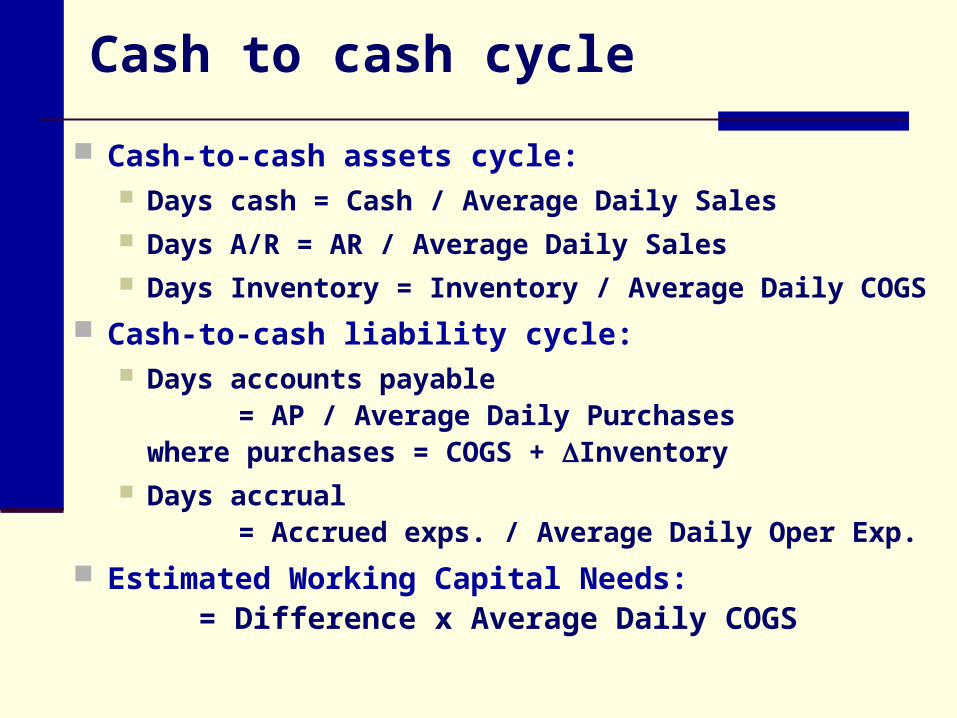

Cash-to-cash assets cycle: Days cash = Cash / Average Daily Sales Days A/R = AR / Average Daily Sales Days Inventory = Inventory / Average Daily COGS

Cash-to-cash liability cycle: Days accounts payable

= AP / Average Daily Purchaseswhere purchases = COGS + Inventory

Days accrual = Accrued exps. / Average Daily Oper Exp.

Estimated Working Capital Needs:= Difference x Average Daily COGS

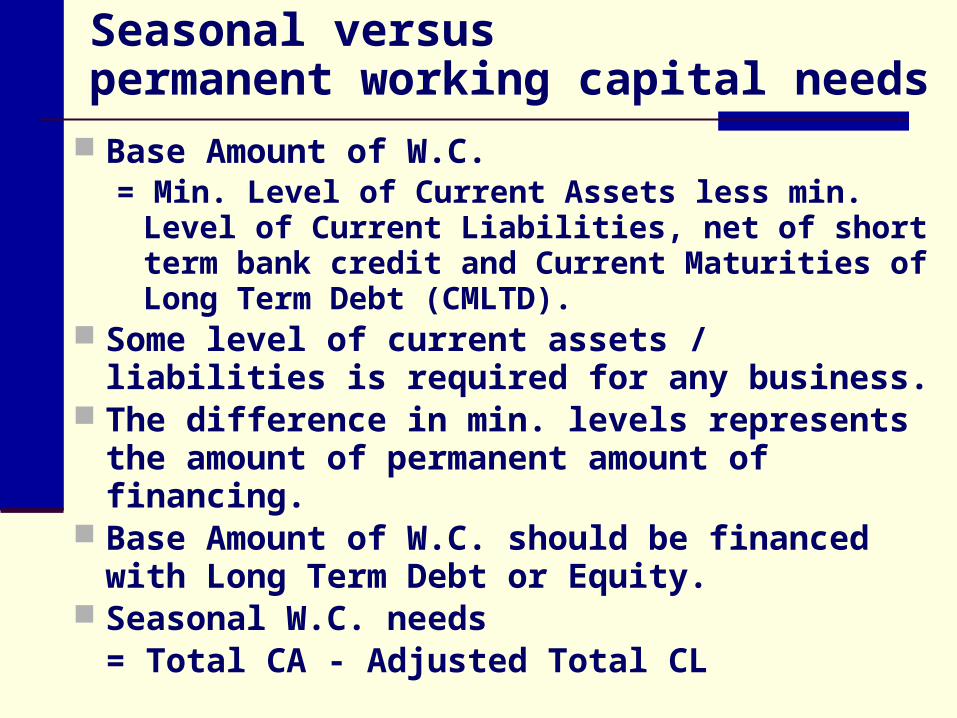

Seasonal versus permanent working capital needs

Base Amount of W.C.= Min. Level of Current Assets less min. Level of

Current Liabilities, net of short term bank credit and Current Maturities of Long Term Debt (CMLTD).

Some level of current assets / liabilities is required for any business.

The difference in min. levels represents the amount of permanent amount of financing.

Base Amount of W.C. should be financed with Long Term Debt or Equity.

Seasonal W.C. needs= Total CA - Adjusted Total CL

Tren

ds in

work

ing

cap

ital n

eed

s

Total Current Assets

Minimum Current Assets

Total Current Liabilities

Minimum Current Liabilities

Total = Permanent Working Capital Needs+ Seasonal Working Capital Needs

Permanent Working Capital Needs

qTime

Seasonal Working Capital Needs

Short-term commercial loans …Banks try to match credit terms with a borrower’s specific needs.

The loan officer estimates the purpose and amount of the proposed loan, the expected source of repayment, and the value of collateral.

The loan amount, maturity, and repayment schedule are negotiated to coincide with the projections.

Short-term funding needs are financed by short-term loans, while long-term needs are financed by term loans with longer maturities.

Seasonal working capital loans. …finance a temporary increase in net current assets above the permanent requirement

A borrower uses the proceeds to purchase raw materials and build up inventories of finished goods in anticipation of later sales.

Trade credit also increases but by a smaller amount.

Funding requirements persist as the borrower sells the inventory on credit and accounts receivables remain outstanding.

The loan declines as the borrower collects on the receivables and stops accumulating inventory.

Seasonal working capital loans. …this type of loan is seasonal if the need arises on a regular basis and if the cycle completes itself within one year

It is self-liquidating in the sense that repayment derives from sales of the finished goods that are financed.

Because the loan proceeds finance an increase in inventories and receivables, banks try to secure the loan with these assets.

Seasonal working capital loans are often unsecured because the risk to the lender is relatively low.

Open credit lines…seasonal loans often take the form of open credit lines.

Under these arrangements, the bank makes a certain amount of funds available to a borrower for a set period of time.

The customer determines the timing of actual borrowings, or “takedowns.’’

Typically, borrowing gradually increases with the inventory buildup, then declines with the collection of receivables.

The bank likes to see the loan fully repaid at least once during each year. This confirms that the needs are truly seasonal.

Asset-based loans. …In theory, any loan secured by a company’s assets is an asset-based loan.

One very popular type of asset-based short-term loan would be those secured by inventories or accounts receivable. In the case of inventory loans, the security consists of

raw materials, goods in process, and finished products. The value of the inventory depends on the marketability

of each component if the borrower goes out of business. Banks will lend from 40 to 60 percent against raw

materials that are common among businesses and finished goods that are marketable, and nothing against unfinished inventory.

With receivables, the security consists of paper assets that presumably represent sales. The quality of the collateral depends on the borrower’s

integrity in reporting actual sales and the credibility of billings.

Loans to finance leveraged buyouts are also classified in this category.

Highly leveraged transactions.

A leveraged buyout involves a group of investors, often part of the existing management team, buying a target company and taking it private with a minimum amount of equity and large amount of debt.

Target companies are generally those with undervalued hard assets.

The investors often sell off specific assets or subsidiaries to pay down much of the debt quickly.

If key assets have been undervalued, the investors may own a downsized company whose earnings prospects have improved and whose stock has increased in value.

The investors sell the company or take it public once the market perceives its greater value.

Highly leveraged transactions (HLTs) arise from three types of transactions:

1. LBOs in which debt is substituted for privately held equity

2. Leveraged recapitalizations in which borrowers use loan proceeds to pay large dividends to shareholders

3. Leveraged acquisitions in which a cash purchase of another related company produces an increase in the buyer’s debt structure

Term commercial loans

Term commercial loans, which have an original maturity of more than one year, are normally used for credit needs that persist beyond one year. Most term loans have maturities from one to

seven years and are granted to finance either the purchase of depreciable assets, start-up costs for a new venture, or a permanent increase in the level of working capital.

Because repayment comes over several years, lenders focus more on the borrower’s periodic income and cash flow rather than the balance sheet.

Term loans often require collateral, but this represents a secondary source of repayment in case the borrower defaults.

Revolving credits…Revolving credits are a hybrid of short-term working capital loans and term loans.

They often involve a commitment of funds (the borrowing base) for one to five years.

At the end of some interim period, the outstanding principal converts to a term loan. During the interim period, the borrower

determines usage much like a credit line. Mandatory principal payments begin once

the commitment converts to a term loan. The revolver has a fixed maturity and often

requires the borrower to pay a fee at the time of conversion to a term loan.

Revolvers have often substituted for commercial paper or corporate bond issues.

Consumer loans

Nonmortgage consumer loans differ substantially from commercial loans.

Their usual purpose is to finance the purchase of durable goods, although many individuals borrow to finance education, medical care, and other expenses.

The average loan to each borrower is relatively small.

Most loans have maturities from one to four years, are repaid in installments, and carry fixed interest rates.

In general, an individual borrower’s default risk is greater than a commercial customer’s. Consumer loan rates are thus higher to compensate for the greater losses.

Consumer loans are normally classified as either installment, credit card, or noninstallment credit.

Installment loans require a partial payment of principal plus interest periodically until maturity.

Other consumer loans require either a single payment of all interest plus principal or a gradual repayment at the borrower’s discretion, as with a credit line.

Banks’ share of the consumer credit market has fallen over time, but even with many competitors, commercial banks held around 38 percent of the total credit outstanding in the late 1990s and were the largest single holders of automobile loans, mobile home loans, and all other types.

Venture capital…a broad term use to describe funding acquired in the earlier stages of a firm’s economic life.

Due to the high leverage and risk involved, as well as regulatory requirements, banks generally do not participate directly in venture capital deals.

Some banks, however, do have subsidiaries that finance certain types of equity participations and venture capital deals, but their participation is limited.

This type of funding is usually acquired during the period in which the company is growing faster than its ability to generate internal financing and before the company has achieved the size needed to be efficient.

VC firms attempt to add value to the firm without taking majority control.

Often, VC firms not only provide financing but experience, expertise, contacts, and advice when required.

There are many types of venture financing. Early stages of financing come in the form seed or

start-up capital. These are highly levered transactions in which the VC

firm will lend money for a percentage stake in the firm. Rarely, if ever, do banks participate as VCs at this stage.

Later-stage development capital takes the form of expansion and replacement financing, recapitalization or turnaround financing, buy-out or buy-in financing, and even mezzanine financing.

Banks do participate in these rounds of financing, but if the company is overleveraged at the onset, the banks will be effectively excluded from these later rounds of financing.

OVERVIEW OF CREDIT POLICY AND LOAN CHARACTERISTICS

Chapter 15

Bank ManagementBank Management, 5th edition.5th edition.Timothy W. Koch and S. Scott MacDonaldTimothy W. Koch and S. Scott MacDonaldCopyright © 2003 by South-Western, a division of Thomson Learning