overview and outlook for georgia’s revenue situation and economy fiscal management council office...

TRANSCRIPT

Overview and Outlook for Georgia’s Revenue Situation and

Economy

Fiscal Management CouncilOffice of Planning and Budget

Ken HeaghneySeptember 2015

Agenda

• State of Georgia Revenues

• Georgia’s Economy – Current Trends and Outlook

State of Georgia Revenues - Overview

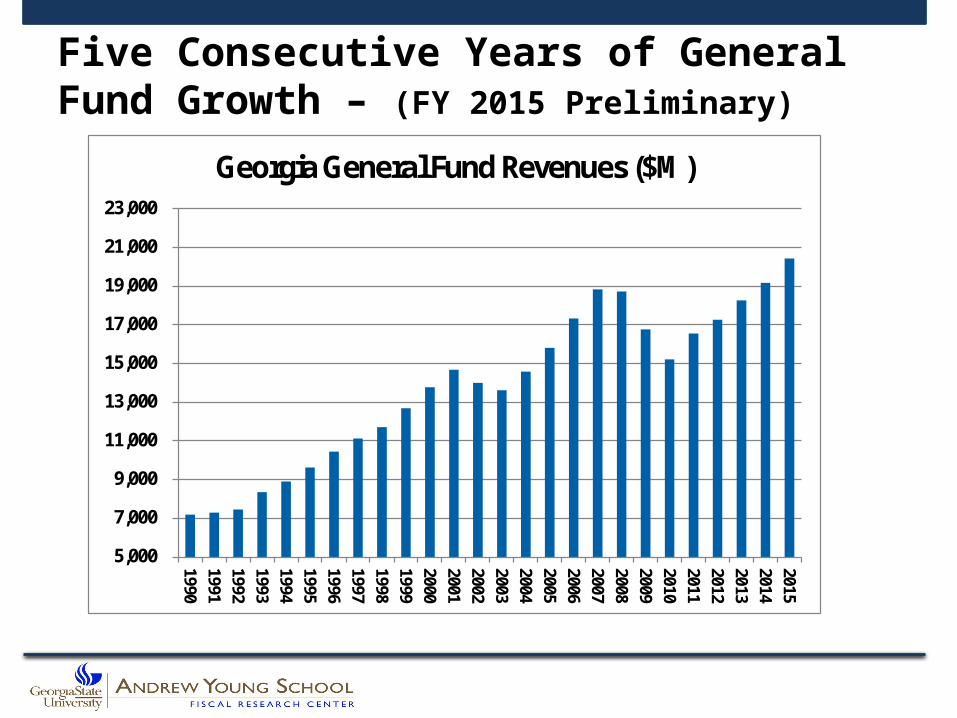

• Revenues have grown for five consecutive years after the Great Recession.

• FY 2015 revenue growth far exceeded plan. This creates some headroom for additional funding in future budget years and adds to reserves.

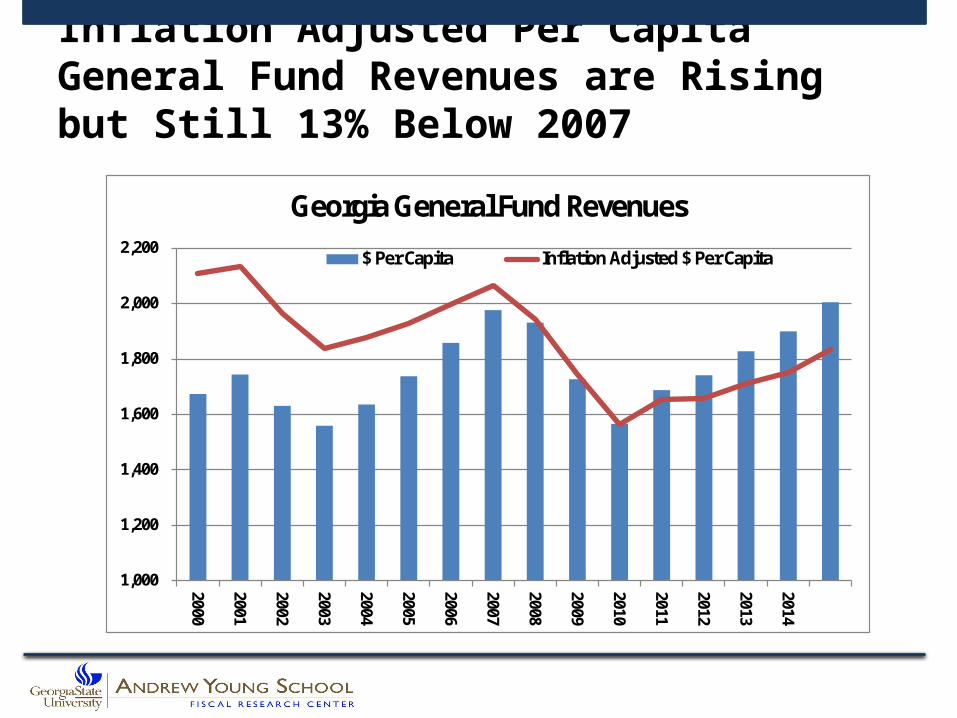

• Revenues, adjusted for inflation and population growth, are still below pre-recession peak.

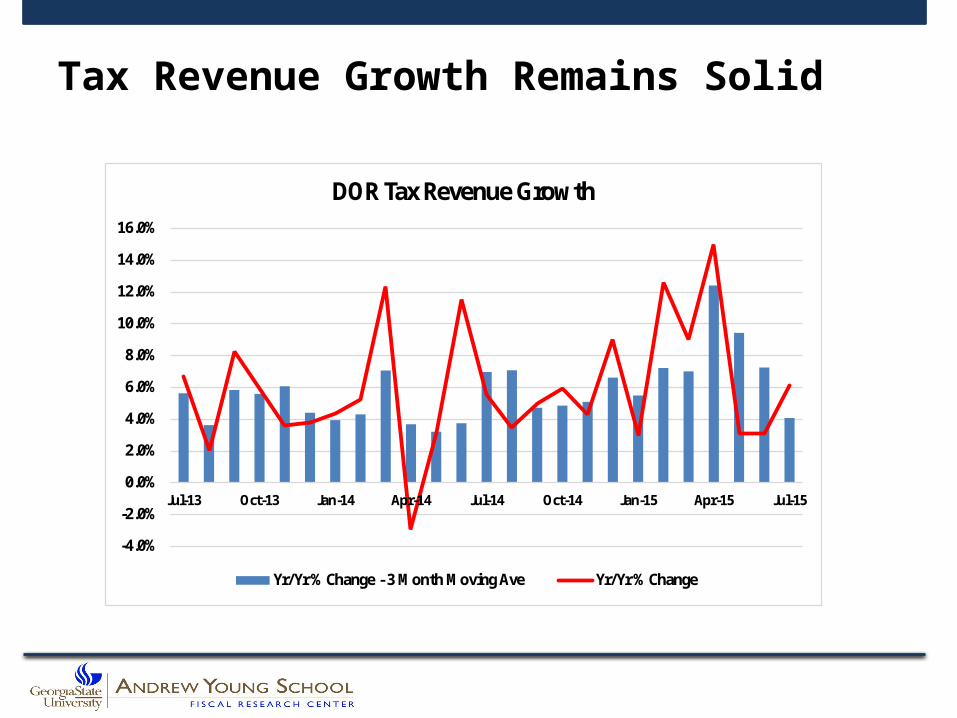

• Current revenue trends are still positive – few signs of slowdown.

Five Consecutive Years of General Fund Growth – (FY 2015 Preliminary)

5,000

7,000

9,000

11,000

13,000

15,000

17,000

19,000

21,000

23,000

19901991199219931994199519961997199819992000200120022003200420052006200720082009201020112012201320142015

Georgia General Fund Revenues ($M)

Rapid Revenue Growth in AFY 2015

3.4%

6.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Budget Plan Preliminary Actuals

Prelimunary Revenue Growth - AFY 2015

Rebuilding the Revenue Shortfall Reserve – Over $850 Million as of FY 2014

Expect RSR to Exceed $1 Billion as of FY 2015

Inflation Adjusted Per Capita General Fund Revenues are Rising but Still 13% Below 2007

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Georgia General Fund Revenues

$ Per Capita Inflation Adjusted $ Per Capita

Tax Revenue Growth Remains Solid

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15

DOR Tax Revenue Growth

Yr/Yr % Change - 3 Month Moving Ave Yr/Yr % Change

Withholding Revenue Growth is Strong

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

% C

hang

e O

ver P

iror Y

r -3

Mon

th M

ovin

g Av

g.

Individual Income Tax Withholding

Other Types of Individual Payments are Growing at Double Digit Percentages

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

July 2013

Sep. 2013

No

v. 2013

Jan. 2014

Mar 2014

May 2014

July 2014

Sep. 2014

No

v 2014

Jan 2015

Mar 2015

May 2015

Individual Payments Excluding Withholding

3 month MA % Change

One Area of Concern: Sales Tax Growth Has Weakened

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

July.2013

Sep.2013

Nov.2013

Jan.2014

Mar2014

May2014

July2014

Sept.2014

Nov.2014

Jan.2015

Mar.2015

May2015

Jul2015

Sales Tax Revenue Growth 3 Month Moving Average

Gross Net

Revenue Growth is Strong but Georgia Still Faces Budget Challenges

• Revenue trends by major tax components indicate economic conditions continue to improve – thus, revenues are expected to continue to grow at a moderate rate. Tax changes associated with transportation funding will further boost reported growth.

• However, formula growth (education, health-related) expected to continue to consume much of future revenue growth.

• Unfunded liabilities will have to be addressed over time

• RSR needs further replenishing

Georgia’s Economy – Current Conditions and Outlook

“Solid Growth Meets Increasing Market Turmoil”

Markets in Turmoil: Equity Values have Dropped Sharply

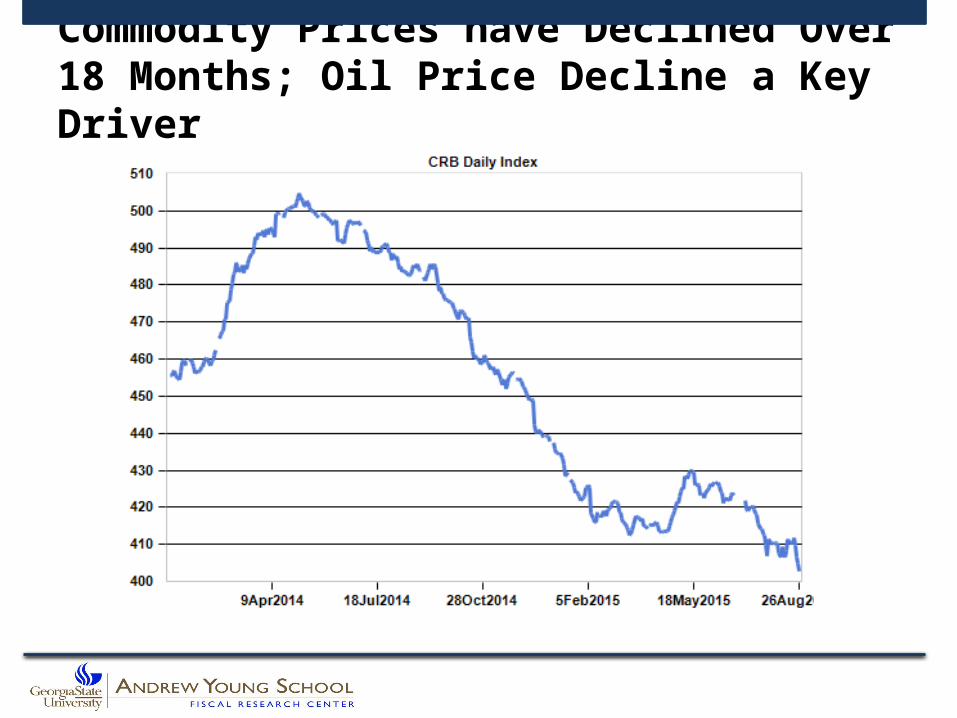

Commodity Prices have Declined Over 18 Months; Oil Price Decline a Key Driver

Market Turmoil Adds Uncertainty to an Economy Growing at Solid but Unspectacular Rate

Key Fundamentals

1. Employment growth is solid but softer than 2014

2. Consumer finances are in good shape but spending growth is modest

3. Manufacturing growth has decelerated

4. Housing recovery is on-track

5. Inflation and interest rates are very low

Will Market Turmoil Alter these Fundamentals? Will the Fed Delay Interest Rate Hikes to Begin Normalizing Monetary Policy?

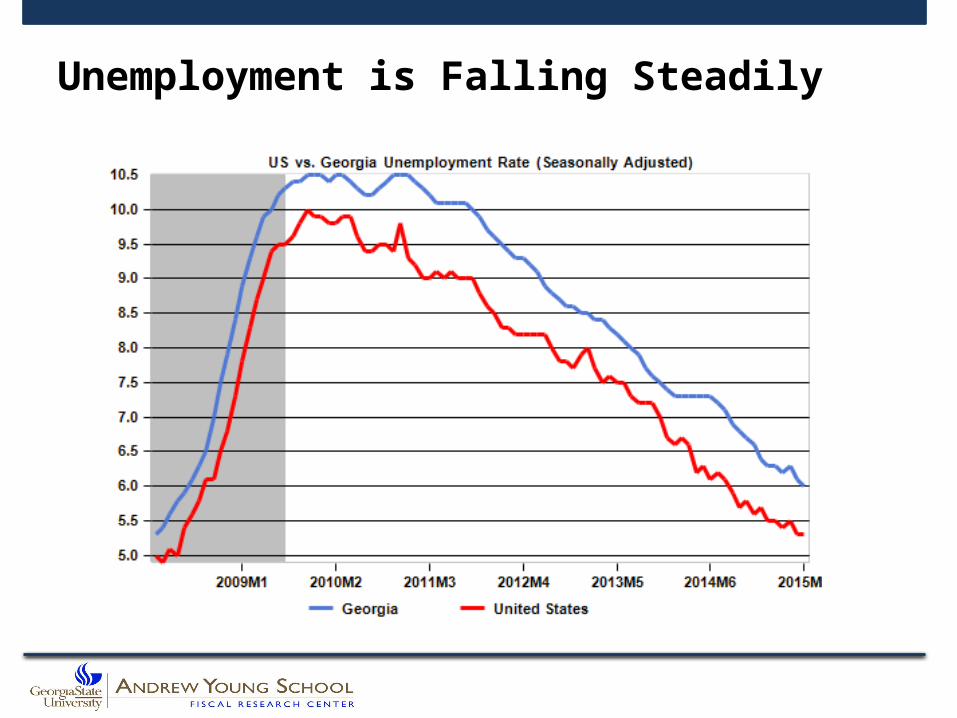

#1) Labor Market Growth is Solid but Softening – Growth in Georgia Outpacing US Growth

Net US Job Additions Over 200k Per Month – Down from Late 2014 Peak

Georgia Net Job Additions Have Eased Over the Last 3 Months

Unemployment is Falling Steadily

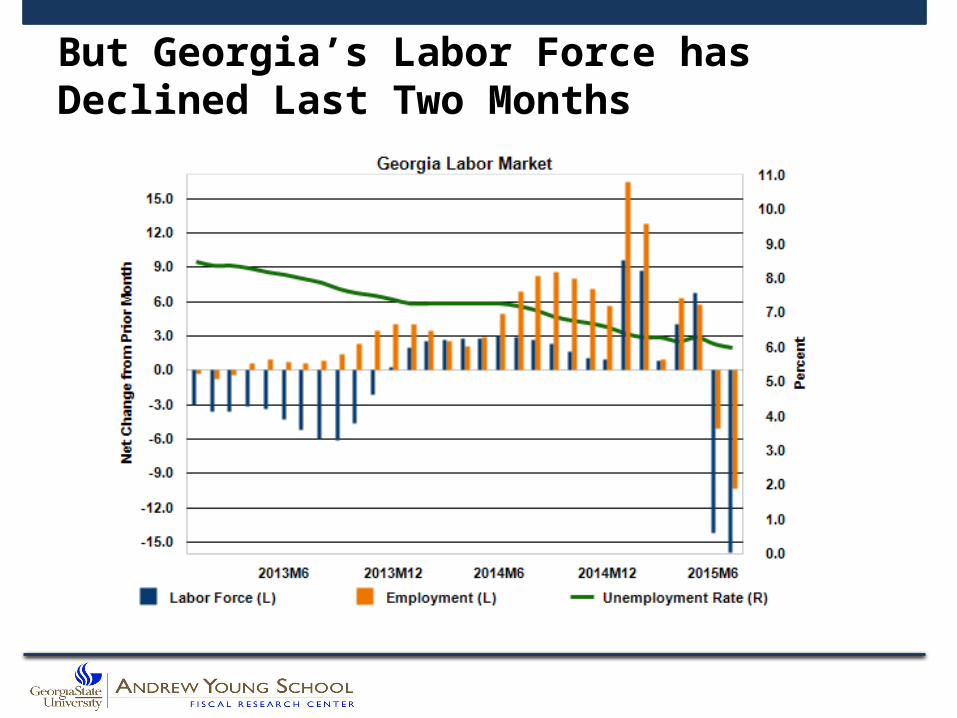

But Georgia’s Labor Force has Declined Last Two Months

Unemployment Insurance Claims are Low Indicating Low Level of Layoffs

Employment Growth is Fairly Well-Diversified Across Sectors

-1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

Other Services

Government

Information

Construction

Manufacturing

Financial

Education and Health

Trade Transportation and Utilities

Professional and Business Services

Leisure and Hospitality

GA Sector Employment Growth - Jul 2015Yr/Yr % Change - 3 Month Moving Average

And Across Metro Areas

-1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5%

ValdostaAlbanyMacon

HinesvilleRome

ColumbusAugusta

AthensSavannah

BrunswickDalton

AtlantaGainesville

Employment Growth by Metro Area - Jul 2015Yr/Yr % Change - 3 Month Moving Average

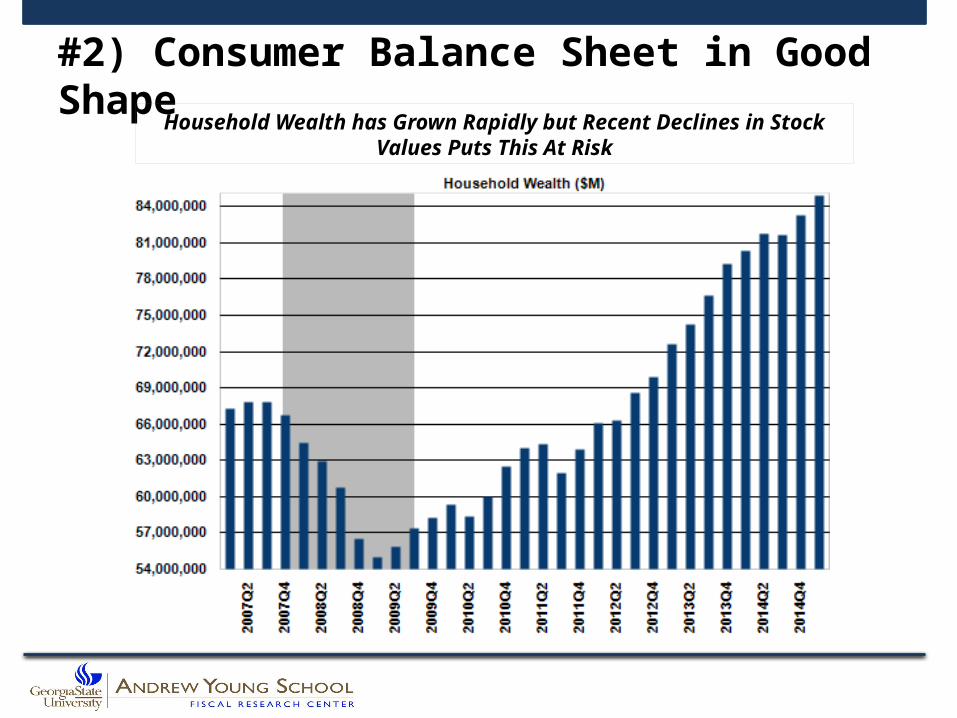

#2) Consumer Balance Sheet in Good ShapeHousehold Wealth has Grown Rapidly but Recent Declines in Stock

Values Puts This At Risk

Household Debt Obligations are Down

Real Disposable Income Growth is Solid

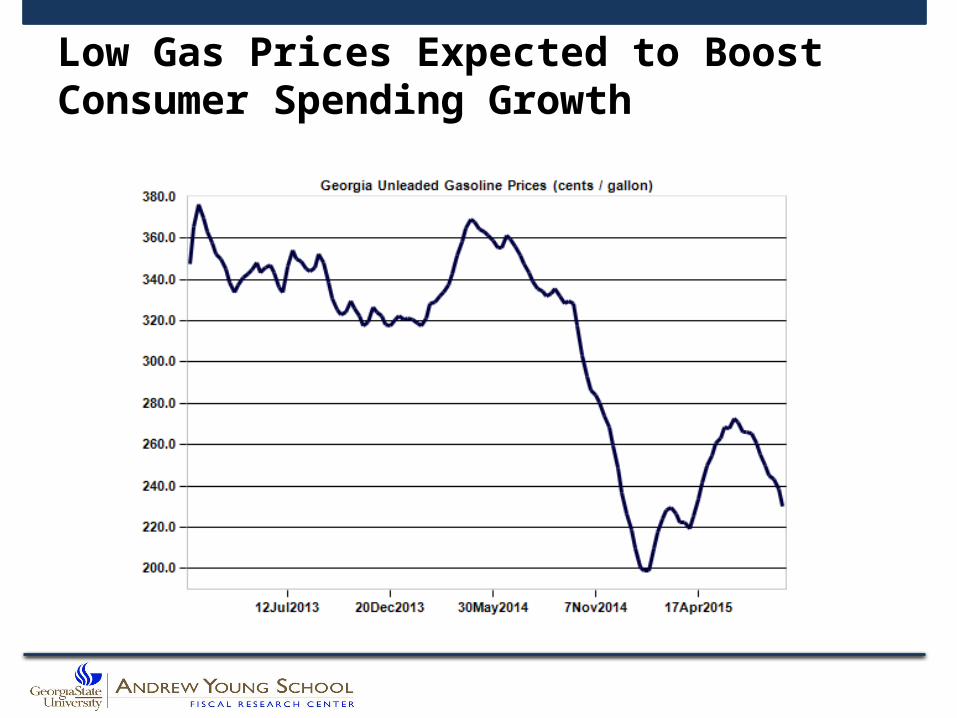

Low Gas Prices Expected to Boost Consumer Spending Growth

Expected Impact: Boost to Economy

Drilling Activity Cut – Lower

Employment & Investment

“Tax Cut” for Consumers –

Higher Spending

But consumers have been slow to spend their “windfall”

But Consumers Spending Growth is Tepid Despite Strong Fundamentals

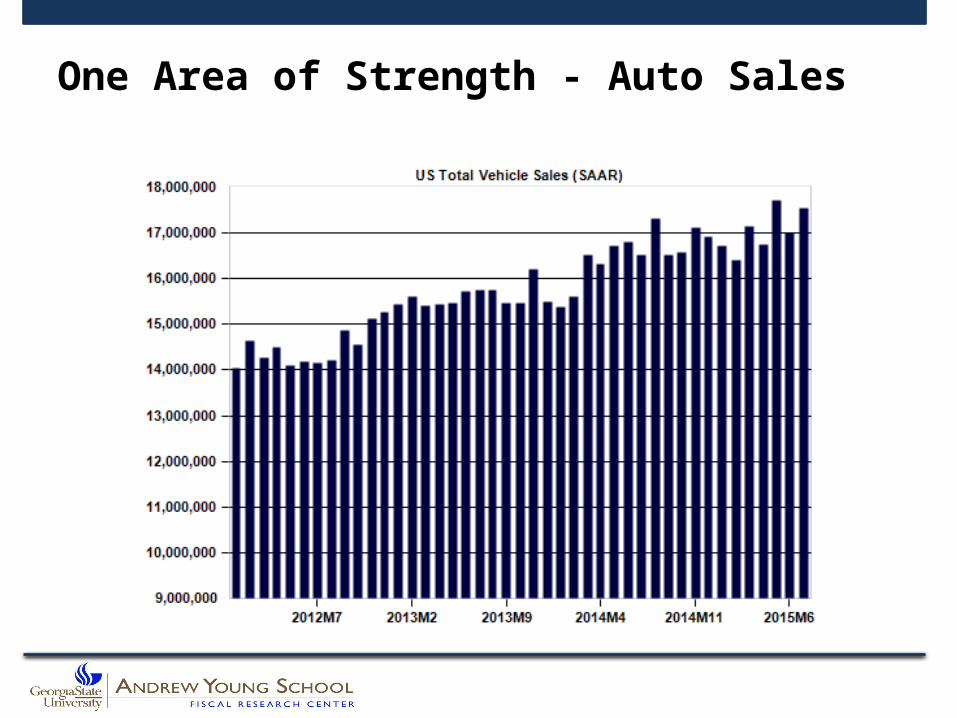

One Area of Strength - Auto Sales

#3) Manufacturing Easing as Stronger Dollar and Lower Oil Prices Create Headwinds

Manufacturing Has Lost Some Momentum

Exports Have Dropped

Key Manufacturing Activity Indicators have Softened

#4) Housing Recovery – Home Sales are Volatile But Trending Up

Housing Starts are Also Trending Up

Pace of Price Appreciation is Moderate

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

S&P Case Shiller Home Price Indices (SA)% Change over Prior Year

Atlanta Metro Composite 20 Metro Areas

#5) Inflation and Interest Rates are Low

Interest Rates

Implications for the Economy

• Broadly solid fundamentals indicate economic growth remains intact.

• Tightening labor markets are pushing the Fed to begin raising interest rates. However, low inflation gives the Fed leeway to defer a rate increase beyond September, if desired.

• Prospects for stronger growth tied to consumers beginning to spend more of the gasoline “tax cut” and a quickening in the pace of recovery in housing market.

• Market turmoil adds more uncertainty to the outlook.

• Risks to the outlook include impact of monetary policy normalization and weakness in global economy (especially China and Eurozone).