outlook for international real estate · 29/11/2011 · outlook for international real estate ......

TRANSCRIPT

Outlook for International Real Estate

Toronto Forum

Jacques Gordon

Global Strategist

November 29, 2011

2

Agenda

Macro Outlook

Global Office Market Dynamics

Emerging Markets

Investable Universe

Capital Flows

Nightmare on which Street?

3

An Unstable Macro Environment

The G7 will be stalled in 2012

Growth also slows in Emerging Markets

Credit cycle shifts back to contraction…

Despite Central Banks easing

Governments caught in a squeeze between-Stimulating their economies-Reigning in ballooning deficits

Hiring and investment decisions in “wait and see” stance

The Eurozone debt crisis likely to drag Europe into recession

4

Source: Global Insight Forecast as of 28 November 2011

Economic Power Shifts East and SouthEmerging Markets To Account for Three Quarters of 2012 Global Growth

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

2007 2008 2009 2010 2011 2012 2013 2014

Com

pone

nts

of W

orld

GD

P G

row

th

Middle East & North Africa Latin America Rest of the WorldCEE Asia-Pacific ex-Japan North AmericaWestern Europe Japan 15 July Forecast

4.2%

Emerging Markets

DevelopedMarkets

3.8%2.9%3.0%

4.2%

-2.1%

1.7%

4.1%

5

Prime Offices – Rental Clock, Q3 2010 v Q3 2011

Q3 2011

Rental Value growth slowing

Rental Value growth

accelerating

Rental Values bottoming out

Rental Values falling

Based on rents for Grade A space in CBD or equivalent. In local currency.

Paris, StockholmMumbai, Sydney, Tokyo

Hong Kong

London, Shanghai

Milan, Johannesburg

Chicago Madrid, Seoul

Rental Value growth slowing

Rental Values falling

Rental Value

growth accelerati

ng

Rental Values bottoming out

Detroit Los Angeles

Amsterdam

San FranciscoBerlin

Moscow

Q3 2010

Mexico City

SingaporeNew York, Brussels, Frankfurt

Atlanta, Dallas, Toronto, RomeDubai

Washington DC

Sao PauloBeijing

Detroit Dubai, Seoul

San Francisco

New York

Washington DC, Toronto Milan

Dallas, Mumbai

Atlanta, Frankfurt Johannesburg

ChicagoRomeTokyo

Los Angeles AmsterdamBrussels

MadridBerlin, Sydney

Stockholm

Sao PauloParis

Beijing

London

Moscow

Mexico City

Hong Kong

Singapore

Shanghai

AmericasEMEAAsia Pacific

As of Q3 2011

The Jones Lang LaSalle Property Clocks SM

6

Completions as % of existing stock

Source: Jones Lang LaSalle, October 2011. Covers all office sub-markets in each city. Tokyo - CBD-3 kus

20122013

Office Supply Pipeline - Major Markets, 2012 -2013

% of occupied stock

Offices – Net Absorption, Year to Q3 2011

Source: Jones Lang LaSalle, October 2011. Covers all office sub-markets in each city. Tokyo - CBD-3 kus

AmericasEMEA

Asia Pacific

8

% change

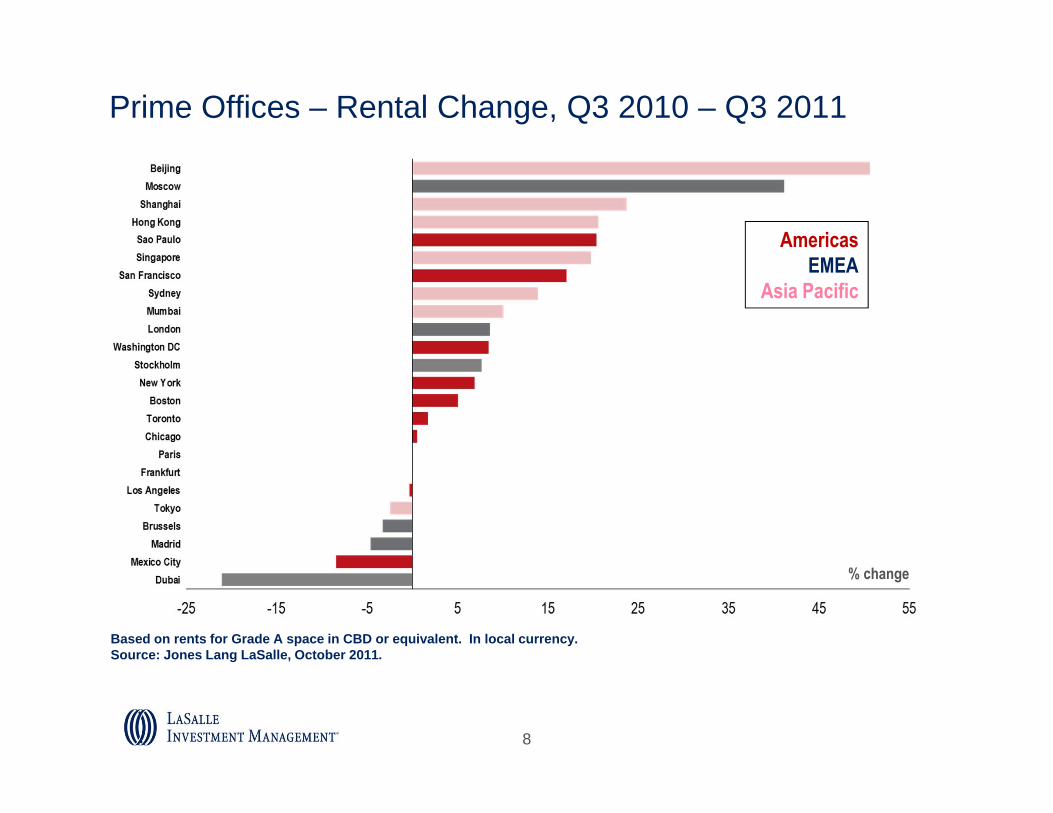

Prime Offices – Rental Change, Q3 2010 – Q3 2011

Based on rents for Grade A space in CBD or equivalent. In local currency.Source: Jones Lang LaSalle, October 2011.

AmericasEMEA

Asia Pacific

9

Emerging Markets’ Growing Share of World GDP

38% of World Output in 2010 at market exchange rates (19% in 1990)

52% of world output in 2011 on a purchasing power parity basis

GDP up 20% since 2007 (while G7 is below 2007 GDP)

75% of the world’s population

82% of mobile phone subscriptions

46% of all retail sales

70% of world steel consumption

Receives over half of world “FDI” (cross border investment)

One quarter of Global Fortune 500 companies HQ in EMs

Over half of world’s currency reserves

Sources: Economist August 2011, Fortune Magazine

10

Source: Global Insight Forecast as of 14 October 2011

China and India: A Class ApartBRICs + Turkey + Indonesia to Drive 40% of Global Growth

Bubble Size RepresentsAbsolute Forecast Change inGDP from 2010 to 2013 India

Vietnam

Indonesia

Egypt

Brazil

Poland

Malaysia

Taiwan

Thailand

Chile

South AfricaRussia

Historical vs Forecast GDP in Key Emerging Markets

11

Emerging Markets Tend to Have Younger Populations

Percent of PopulationUnder 20 65 and Over

Japan 18.1% 22.7%

Germany 18.6% 20.4%

Canada 23.1% 14.1%

US 27.1% 13.1%

Russia 20.8% 12.8%

Poland 21.3% 13.6%

Singapore 24.6% 9.0%

China 27.3% 8.2%

Brazil 33.9% 7.0%

Vietnam 33.8% 6.0%

Turkey 35.3% 6.0%

Mexico 38.7% 6.3%

India 40.4% 4.9%

Developed

Emerging

Source: United Nations Data as of 2010

12

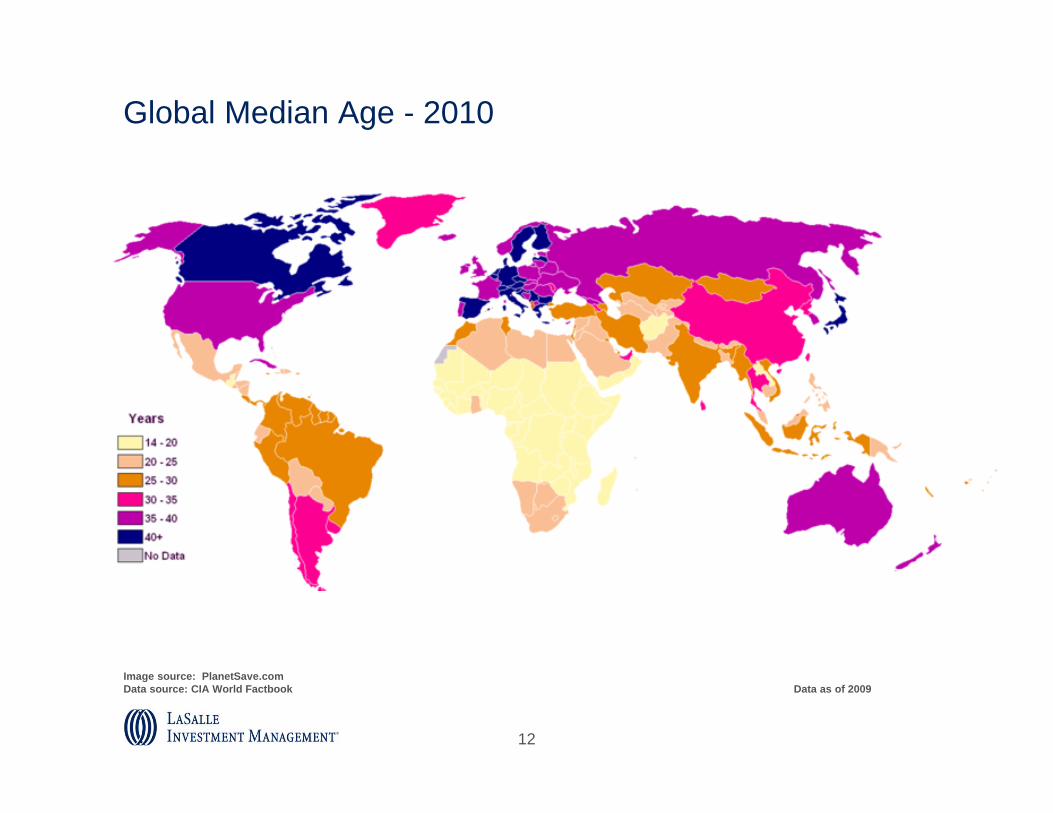

Global Median Age - 2010

Image source: PlanetSave.comData source: CIA World Factbook Data as of 2009

13

2%3%4%5%6%7%8%9%

Chi

na

Indi

a

Vie

tnam

Indo

nesi

a

Taiw

an

Chi

le

Turk

ey

Thai

land

Bra

zil

Rus

sia

Mal

aysi

a

Pol

and

Sou

th A

frica

Wor

ld

Egy

pt

2012

GDP Growth Forecast March 2011 Forecast

November 2011 Forecast

Source: Global Insight Forecast as of 15 October 2011

GDP Forecasts Have Been Revised DownBut Emerging Market Outlooks Have Been Moved Down Less

Change in 2012 GDP Forecast, March 2011 to November 2011

Largest Downward Revisions

Smallest Declines

Improved Outlook

14

Listed Real Estate (Gross Asset Value)Total = $2.0 trillion

Division of Institutional Real Estate Ownership

Source: Investment Property Databank, LaSalle Investment Management 2010 Global Investable Universe EstimateNote: The Listed Real Estate Universe includes all publicly listed property companies, primarily REITs and REOC. Diversified development companies are included in emerging markets, but homebuilders are excluded. The Institutional Real Estate Universe includes all institutional investor-owned property, public and private.

Europe18.5%

Middle East and Africa

3.3%

Asia Pacific42.9%

Americas35.3%

Public Real Estate Companies Own Greater Share of All Real Estate, Especially in Asia-Pacific

15 1

8 of Top 25 Global Public Real Estate Companies Have Large Exposure to China

16

Emerging Network of Chinese Cities

XianChengdu

ChongqingKunming

DalianBeijingTianjin

ShanghaiNingbo

NanjingSuzhou

Hangzhou

MacauDongguan

GuangzhouShenzhen

FuzhouXiamen

Pearl River Delta

Yangtze River Delta

Bohai BasinShenyang

Hong Kong

Taiwan

Wuhan

Central China

17

China: Businesses Will Continue to Head WestDelivery of infrastructure to push development

Source: CBRE

18

Pudong 1900

19

Pudong 1990

20

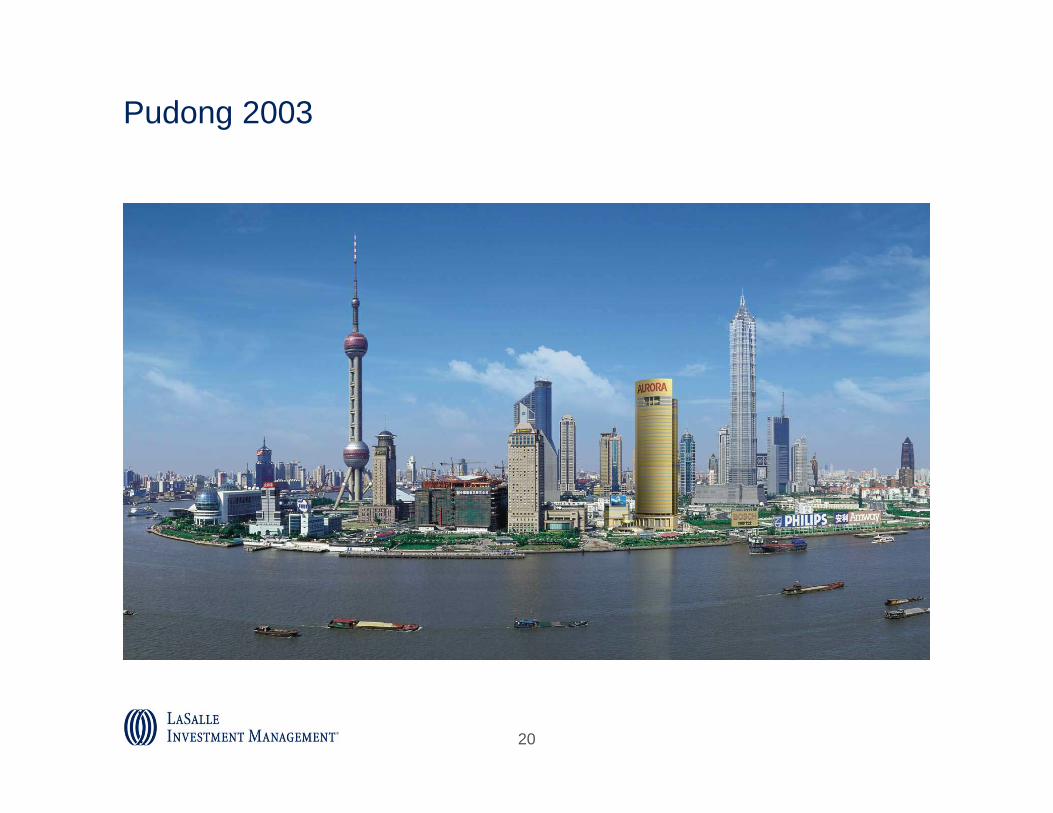

Pudong 2003

21

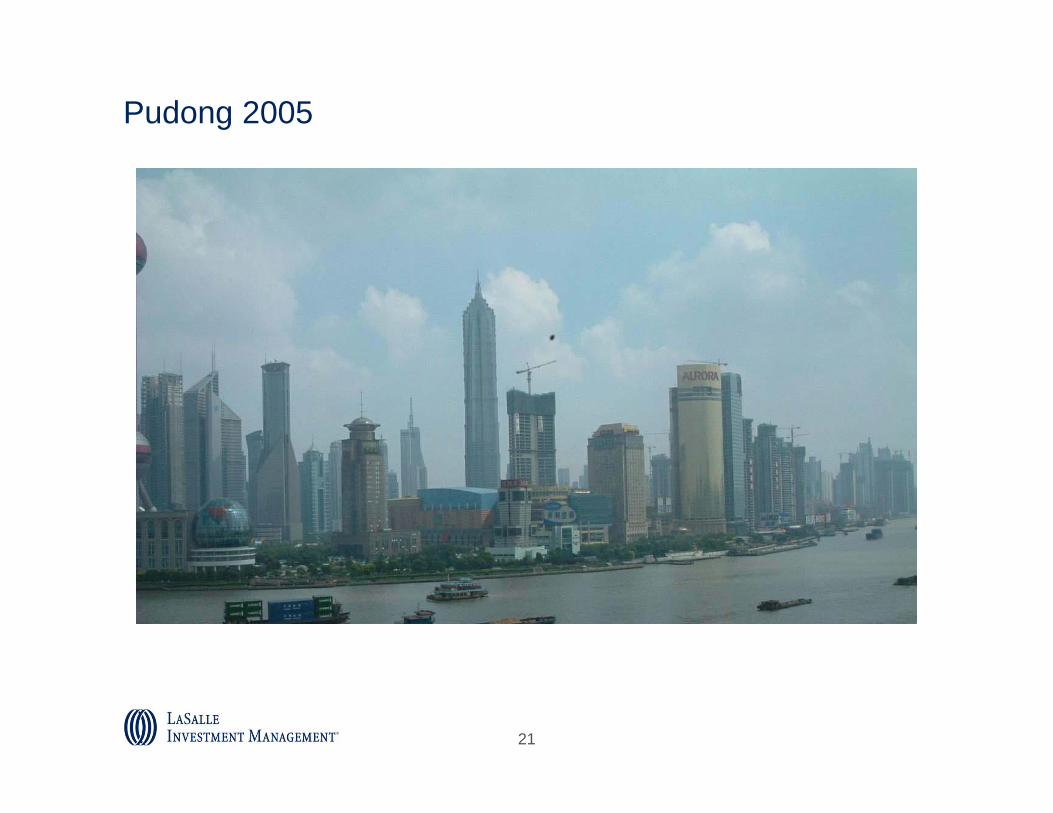

Pudong 2005

22

Pudong-Puxi 2011

23

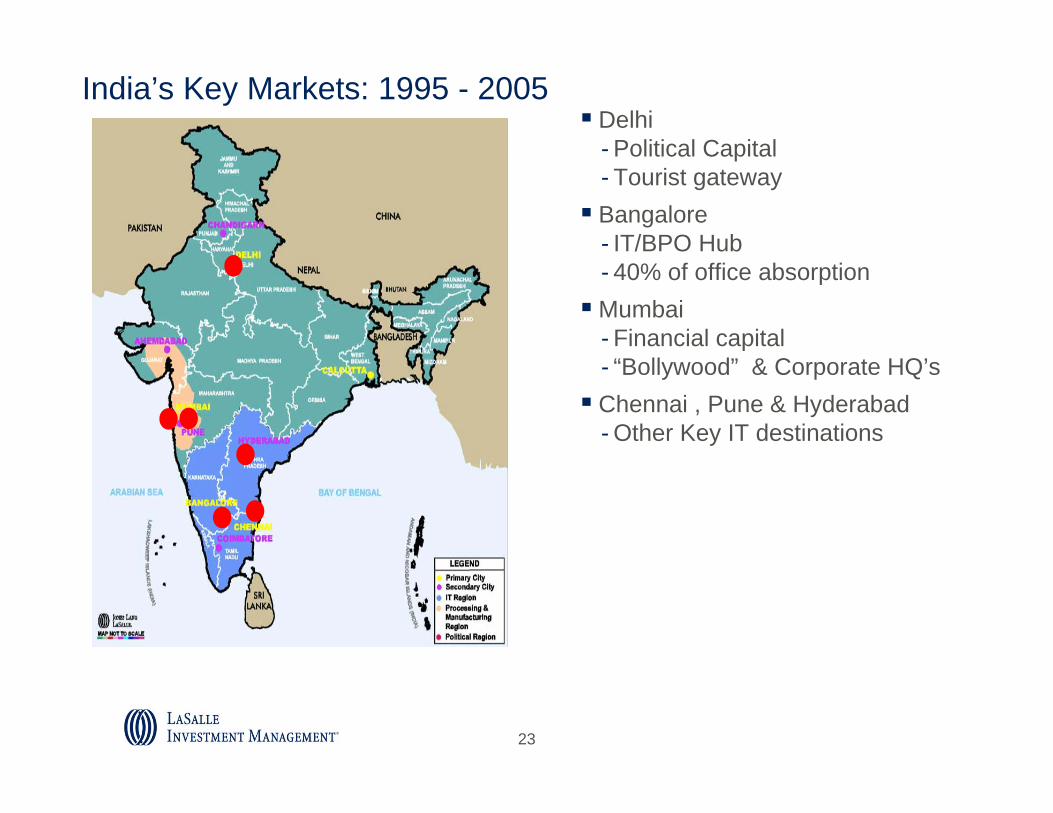

India’s Key Markets: 1995 - 2005 Delhi

- Political Capital - Tourist gateway Bangalore

- IT/BPO Hub- 40% of office absorptionMumbai

- Financial capital - “Bollywood” & Corporate HQ’s Chennai , Pune & Hyderabad

- Other Key IT destinations

24

25

Brazil Overview

186 million population (world’s 5th largest)

3.2 million sq. miles (8.5 million km2)

GDP (US$PPP): $1.8 trillion (world’s 10th largest)

GDP per capita (US$PPP): $9,695

Literacy rate: 88%

Total exports are equivalent to 14% of GDP.

Largest Trading Partner: USA (18% imports; 16% of exports).

Urban Population: 87%

Number of cities with population ≥ 1 million: 14

80% of population lives within 200 km of the Atlantic Ocean

Sao PauloRio de Janeiro

-Brazil’s total area is greater than that of the Continental USA’s.

26

Notional capital values based on rents and yields for Grade A space in CBD or equivalent. In local currency.Source: Jones Lang LaSalle, October 2011.

% change

Prime Offices – Capital Value Change, Q3 2010 – Q3 2011

AmericasEMEA

Asia Pacific

27

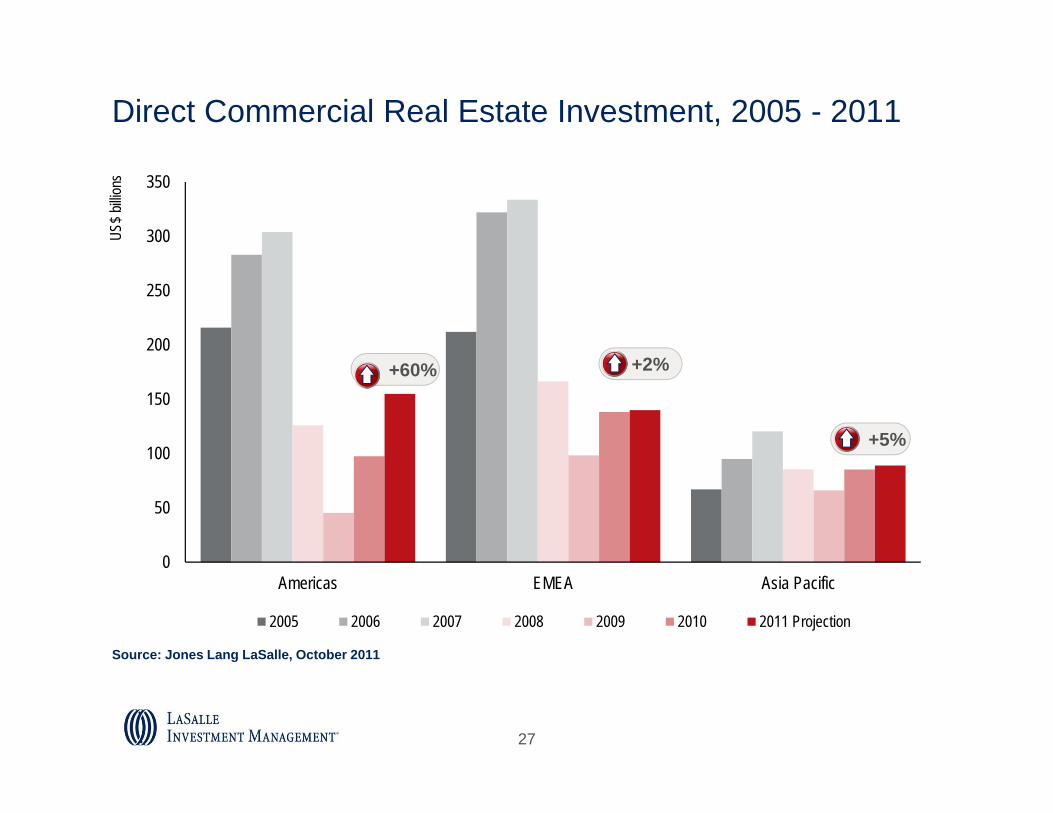

Direct Commercial Real Estate Investment, 2005 - 2011

0

50

100

150

200

250

300

350

Americas EMEA Asia Pacific

US$ b

illion

s

2005 2006 2007 2008 2009 2010 2011 Projection

Source: Jones Lang LaSalle, October 2011

+60% +2%

+5%

28

The Real Estate Investable Universe 2011

Source: Investment Property Databank, LaSalle Investment Management As of 3Q 2011

Total Investable Real Estate US$ 36.5 trillion

Institutional Public & Private US$6.9 trillion

Public Real Estate US$ 2.4 trillion

29

Global Real Estate Universe by Region 2011

Listed Real EstateTotal = $2.4 trillion

Institutional Real EstateTotal = $6.9 trillion

Source: Investment Property Databank, LaSalle Investment Management As of 3Q 2011Note: The Listed Real Estate Universe includes all publicly listed property companies, primarily REITs and REOCs. Diversified development companies are included in emerging markets, but homebuilders are excluded. The Institutional Real Estate Universe includes all institutional investor-owned property, public and private.

Europe31.8%

Middle East & North Africa3.5%

Asia Pacific30.5%

Americas34.2%

Europe16.7%

Middle East and Africa

3.1%

Asia Pacific43.2%

Americas37.0%

30

Real Estate: A Major Asset ClassBut Institutional Ownership Still Small Relative to Other Asset Classes

Source: Investment Property Databank, LaSalle Investment Management As of 3Q 2011Note: Debt data source is the Bank for International Settlements as of June 2011; Equity market capitalization source is from World Federation of Exchanges, as of August 2011; Real estate estimate source is LaSalle Investment Management

$0

$10

$20

$30

$40

$50

$60

Sovereign DebtOutstanding

Corporate andFinancial DebtOutstanding

Global EquityMarket

Capitalization

GlobalInvestable Real

Estate

Estim

ated

Val

ue, T

rillio

ns

Institutional InvestedComponent

Can Europe hold it together?

32

Eurozone Scenarios

Federate with a new treaty

Break up the Currency, Keep the Trade Pact

Devalue, Default, Deutchmark über alles

Creative Destruction… Or Muddle Through

Josef Schumpeter Belgian Surrealist

33

LaSalle Investment Management Research & Strategy

For more information please contact: Jacques Gordon +1 312 228 2760

This information is intended to assist professional investors in deciding whether they wish to consider the investment further. This publication does notconstitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in investment funds sponsored by, or the advisory servicesof, LaSalle Investment Management and is subject to correction, completion and amendment without notice. Any such offer, if made, will only be madeby means of a confidential prospectus. The prospectus will include information regarding investment risk and investors should have the financial abilityand willingness to accept these risks. All information obtained from third party sources is believed to be reliable and current, but accuracy cannot beguaranteed and we do not undertake to update any information contained in this document. All assumptions, figures and calculations contained in theinformation must be independently verified by the professional investor. This publication has been prepared without regard to the specific investmentobjectives, financial situation or particular needs of recipients. No legal or tax advice is provided. Recipients should independently evaluate specificinvestments and trading strategies. By accepting receipt of this publication, the recipient acknowledges that this publication is confidential and agreesnot to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general informationpurposes. Copyright © 2011 LaSalle Investment Management. All rights reserved. No part of this publication may be reproduced by any means,whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, orincluded in any information store and/or retrieval system without prior permission of LaSalle Investment Management.