origin operational review and asset visit presentations

TRANSCRIPT

Origin Energy Limited ACN 000 051 696 • Level 45 Australia Square, 264-278 George Street, Sydney NSW 2000 GPO Box 5376, Sydney NSW 2001 • Telephone (02) 8345 5000 • Facsimile (02) 9252 1566 • www.originenergy.com.au

To Company Announcements Office Facsimile 1300 135 638

Company ASX Limited Date 31 October 2013

From Helen Hardy Pages 60

Subject Origin Operational Review and Asset Visit Presentations

Please find attached a release on the above subject. Regards

Helen Hardy Company Secretary 02 8345 5023 – [email protected]

For

per

sona

l use

onl

y

Origin Operational Review and Asset Visit

31 October and 1 November 2013

For

per

sona

l use

onl

y

Important Notice The information and opinions contained in this presentation are intended solely for your personal reference and are strictly confidential. This presentation may not be used or relied upon by any other party, or for any other purpose, and may not be reproduced, disseminated or quoted without the prior written consent of Origin Energy Limited (Origin). This presentation or any materials provided in connection herewith may not be taken away by you. The contents of this presentation may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, in whole or in part, for any purpose. This presentation has been prepared by Origin. The information in this presentation is an overview and does not contain all information necessary to make an investment decision. It does not take into account the investment objectives, financial situation or particular needs of any particular investor. Origin make no recommendation to investors regarding the suitability of an investment in its or its subsidiaries’ securities, and the recipient of this presentation must make its own assessment and/or seek independent advice on financial, legal, tax and other matters, including the merits and risks involved. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in this presentation. To the maximum extent permitted by law, none of Origin, nor any of their directors, employees or agents, nor any other person accepts any liability, including, without limitation, any liability arising out of fault or negligence for any loss arising from the use of the information contained in this presentation. This presentation does not constitute an offer to sell, or a solicitation of an offer to buy, any securities in the United States or any other jurisdiction. Securities of Origin and its subsidiaries have not been, and will not be, registered under the U.S. Securities Act of 1933 (the "Securities Act") or the securities laws of any state or other jurisdiction of the United States and may not be offered or sold, directly or indirectly, in the United States absent registration except in a transaction exempt from, or not subject to, the registration requirements of the Securities Act and any other applicable U.S. state securities laws. Forward looking statements This presentation contains forward looking statements, including statements of current intention, statements of opinion and predictions as to possible future events. Such statements are not statements of fact and there can be no certainty of outcome in relation to the matters to which the statements relate. These forward looking statements involve known and unknown risks, uncertainties, assumptions and other important factors that could cause the actual outcomes to be materially different from the events or results expressed or implied by such statements. Those risks, uncertainties, assumptions and other important factors are not all within the control of Origin and cannot be predicted by Origin and include changes in circumstances or events that may cause objectives to change as well as risks, circumstances and events specific to the industry, countries and markets in which Origin and its related bodies corporate, joint ventures and associated undertakings operate. They also include general economic conditions, exchange rates, interest rates, the regulatory environment, competitive pressures, selling price, market demand, conditions in the financial markets, operating and asset risks and delays in project development and implementation and/or higher than expected costs, which may cause objectives to change or may cause outcomes not to be realised. None of Origin or any of its respective subsidiaries, affiliates and associated companies (or any of their respective officers, employees or agents) (the Relevant Persons) makes any representation, assurance or guarantee as to the accuracy or likelihood of fulfillment of any forward looking statement or any outcomes expressed or implied in any forward looking statements. The forward looking statements in this presentation reflect views held only at the date of this presentation. You are cautioned not to place undue reliance on forward-looking statements.

2 |

For

per

sona

l use

onl

y

Important Notice Statements about past performance are not necessarily indicative of future performance. Except as required by applicable law or the ASX Listing Rules, the Relevant Persons disclaim any obligation or undertaking to update any forward looking statements, whether as a result of new information or future events. This presentation contains data sourced from and the views of independent third parties. In replicating such data in this document, Origin makes no representation, whether express or implied, as to the accuracy of such data. The replication of any views in this document should not be treated as an indication that Origin agrees with or concurs with such views. Financial information All figures in this presentation relate to businesses of the Origin Energy Group (Origin, or the Company), being Origin Energy Limited and its controlled entities, for the year ended 30 June 2013 (FY2013) compared with the year ended 30 June 2012 (FY2012), except where otherwise stated. Earlier periods are referred to in a similar manner.

Origin’s Financial Statements for the year ended 30 June 2013 are presented in accordance with Australian Accounting Standards and comply with IFRS. The Segment results, which are used to measure segment performance, are disclosed in Note 2 of the Financial Statements and are disclosed on a basis consistent with the information provided internally to Origin’s Managing Director. Origin’s Statutory Profit contains a number of items that when excluded provide a different perspective on the financial and operational performance of the business. Income Statement amounts presented on an underlying basis such as Underlying Consolidated Profit, are non-IFRS financial measures, and exclude the impact of these items consistent with the manner in which the Managing Director reviews the financial and operating performance of the business. Each underlying measure disclosed has been adjusted to remove the impact of these items on a consistent basis. A reconciliation and description of the items that contribute to the difference between Statutory Profit and Underlying Consolidated Profit is provided in Note 2 of the Financial Statements.

A reference to Contact Energy is a reference to Origin’s controlled entity (53.1% ownership) Contact Energy Limited in New Zealand. In accordance with Australian Accounting Standards, Origin consolidates Contact Energy within its result.

A reference to Australia Pacific LNG or APLNG is a reference to Australia Pacific LNG Pty Ltd in which Origin had a 50% shareholding in until 9 August 2011, when completion of a share subscription agreement between Australia Pacific LNG and Sinopec resulted in a dilution in Origin’s shareholding to 42.5%. Origin’s shareholding in Australia Pacific LNG, which is equity accounted in line with Origin’s shareholding, was 42.5% as at 30 June 2012. This shareholding was subsequently diluted to 37.5% upon completion of Sinopec’s increased share subscription in Australia Pacific LNG on 12 July 2012.

A reference to $ is a reference to Australian dollars unless specifically marked otherwise. All references to debt are a reference to interest bearing debt only (which exclude Australia Pacific LNG shareholder loans). Individual items and totals are rounded to the nearest appropriate number or decimal. Some totals may not add down the page due to rounding of individual components. When calculating a percentage change, a positive or negative percentage change denotes the mathematical movement in the underlying metric, rather than a positive or a detrimental impact. Measures for which the underlying numbers change from negative to positive, or vice versa, are labelled as not applicable.

Oil and gas reserves As a company with securities listed on the ASX, Origin is required to follow the SPE/WPC/AAPG/SPEE Petroleum Resources Management System (March 2007) guidelines (PRMS Guidelines) published by the Society of Petroleum Engineers in order to comply with the ASX requirements for Australian publicly listed companies. You should note, however, that different reserves reporting systems employ different definitions and permit or require different assumptions, and that Origin’s methodologies for classifying reserves and our reserves classifications vary in certain respects from the methodologies and classifications used by oil and gas companies subject to the reporting obligations of the U.S. Securities and Exchange Commission. As a result, identical geological and engineering data can produce varying estimates of reserves. 3 |

For

per

sona

l use

onl

y

Australia Pacific LNG – CSG Production

Presented by Ross Evans

Group Manager, Exploration Appraisal & Development, QLD CSG

Origin Operational Review and Asset Visit 31 October 2013

For

per

sona

l use

onl

y

Origin is responsible for the upstream program for Australia Pacific LNG, leveraging over 16 years of CSG production experience …

2 |

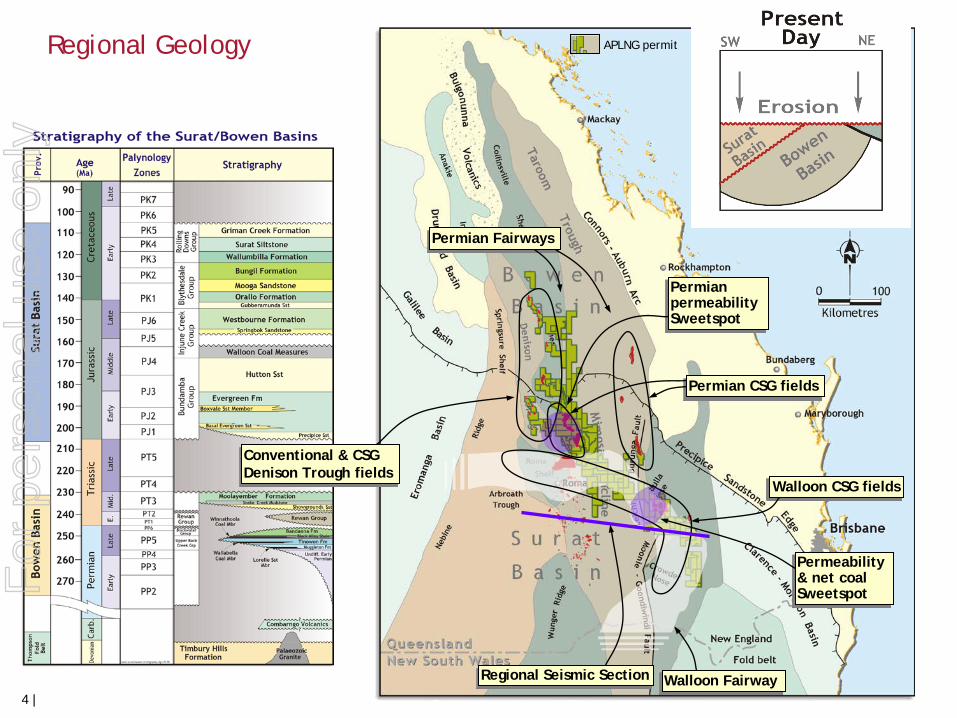

APLNG tenure in the Surat and Bowen basins at 30 June 2012

… with Australia Pacific LNG having a dominant position in Queensland's premium CSG acreage

• APLNG is the only company that has prime acreage in both of the Queensland CSG “sweet spots”

• APLNG Phase 1 targets those sweet spots for initial development and ramp up to first LNG

• APLNG has both diversity and scale of resources to better manage risks associated with CSG

For

per

sona

l use

onl

y

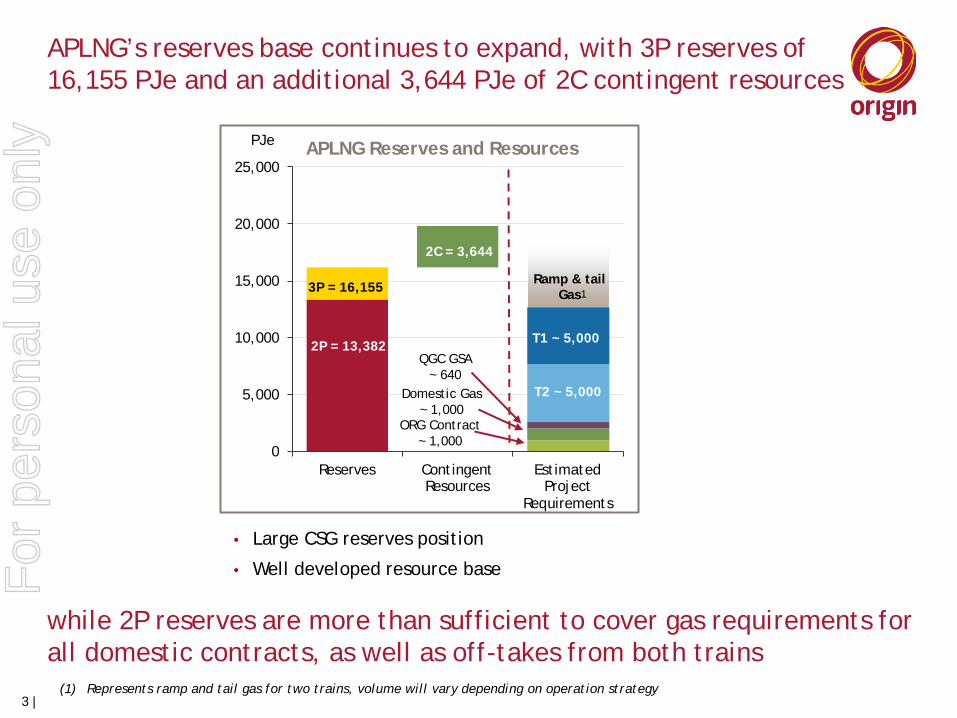

0

5,000

10,000

15,000

20,000

25,000

Reserves ContingentResources

EstimatedProject

Requirements

PJe

3P = 16,155

2P = 13,382

2C = 3,644

Ramp & tail Gas

T2 ~ 5,000

T1 ~ 5,000

APLNG’s reserves base continues to expand, with 3P reserves of 16,155 PJe and an additional 3,644 PJe of 2C contingent resources

3 |

while 2P reserves are more than sufficient to cover gas requirements for all domestic contracts, as well as off-takes from both trains

• Large CSG reserves position

• Well developed resource base

Domestic Gas ~ 1,000

ORG Contract ~ 1,000

APLNG Reserves and Resources

(1) Represents ramp and tail gas for two trains, volume will vary depending on operation strategy

QGC GSA ~ 640

1

For

per

sona

l use

onl

y

APLNG permit

Conventional & CSG Denison Trough fields

Permian CSG fields

Walloon CSG fields

Walloon Fairway

Permeability & net coal Sweetspot

Permian permeability Sweetspot

Permian Fairways

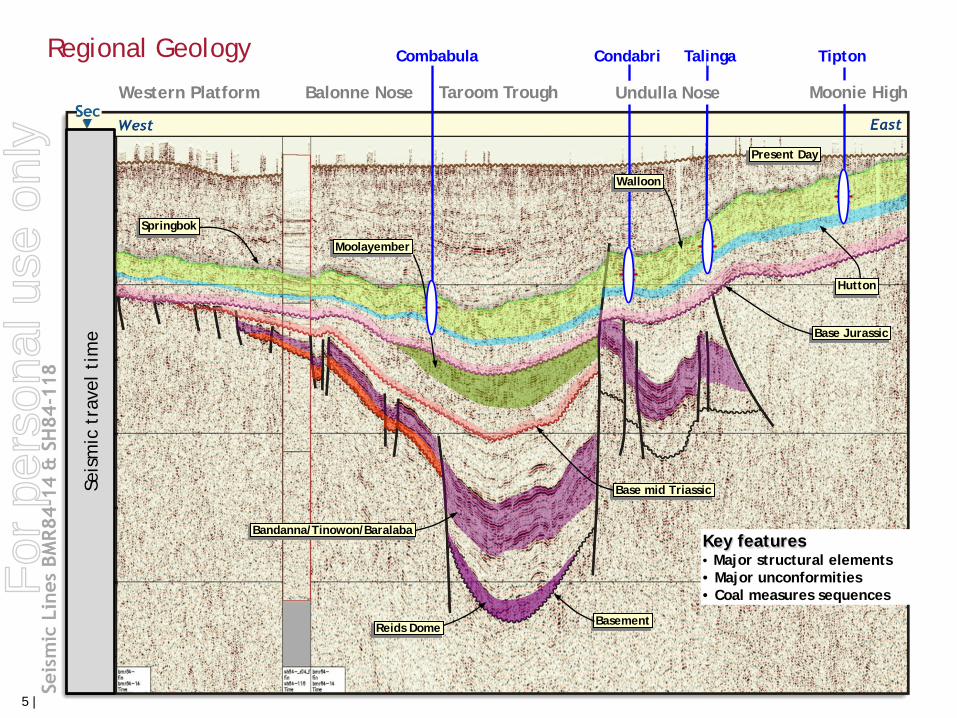

Regional Geology

Regional Seismic Section

4 |

For

per

sona

l use

onl

y

5

Basement

Base mid Triassic

Base Jurassic

Key features • Major structural elements • Major unconformities • Coal measures sequences

Western Platform Moonie High

Bandanna/Tinowon/Baralaba

Reids Dome

Springbok

Present Day

Talinga

Hutton

Seis

mic

tra

vel

tim

e

Combabula Condabri

Undulla Nose Taroom Trough Balonne Nose

Walloon

Moolayember

Regional Geology

5 |

Tipton F

or p

erso

nal u

se o

nly

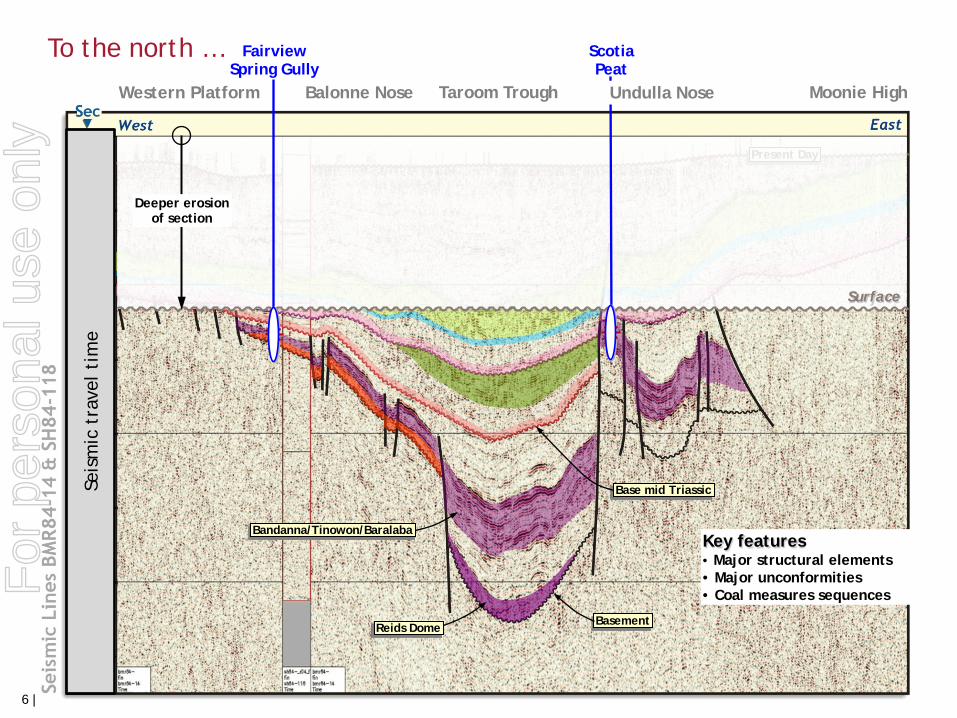

6

Basement

Key features • Major structural elements • Major unconformities • Coal measures sequences

Base mid Triassic

Taroom Trough

Present Day

Fairview Spring Gully

Scotia Peat

Moonie High Western Platform Balonne Nose

Bandanna/Tinowon/Baralaba

To the north …

Surface

Deeper erosion of section

Reids Dome

Undulla Nose Se

ism

ic t

rave

l ti

me

6 |

For

per

sona

l use

onl

y

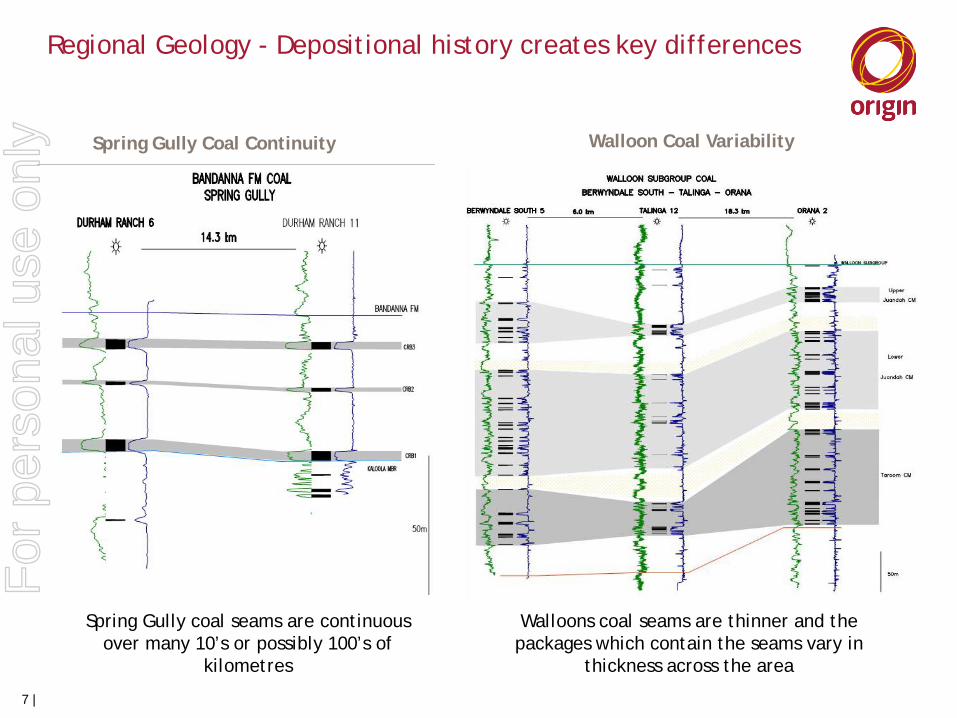

Spring Gully Coal Continuity

Spring Gully coal seams are continuous over many 10’s or possibly 100’s of

kilometres

Walloons coal seams are thinner and the packages which contain the seams vary in

thickness across the area

Walloon Coal Variability

Regional Geology - Depositional history creates key differences

7 |

For

per

sona

l use

onl

y

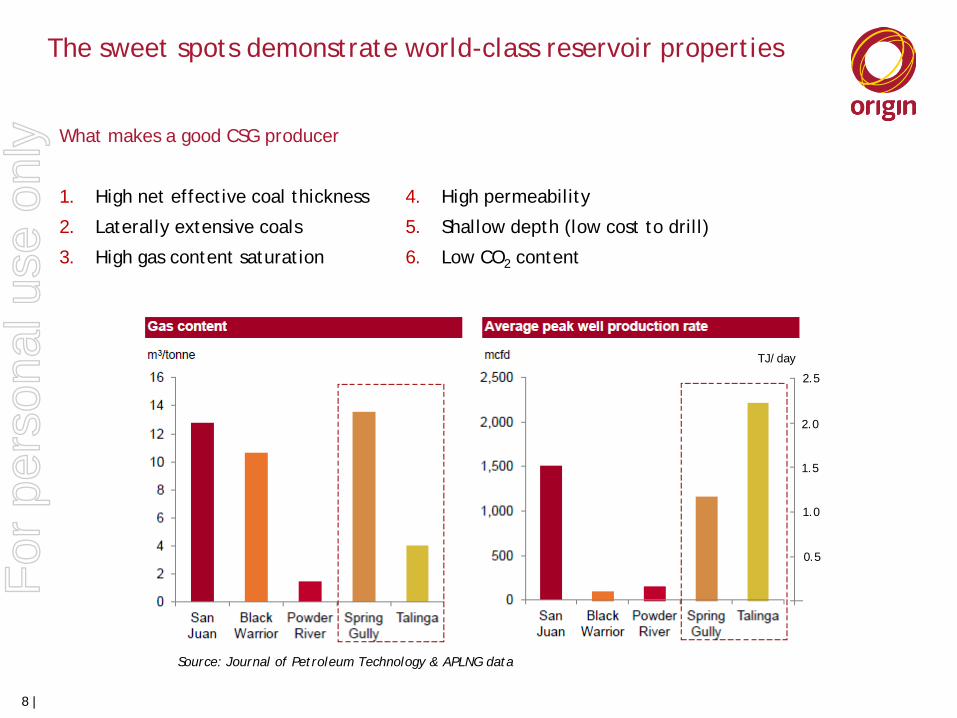

The sweet spots demonstrate world-class reservoir properties

What makes a good CSG producer

1. High net effective coal thickness

2. Laterally extensive coals

3. High gas content saturation

4. High permeability

5. Shallow depth (low cost to drill)

6. Low CO2 content

Source: Journal of Petroleum Technology & APLNG data

8 |

TJ/day

2.5

2.0

1.5

0.5

1.0

For

per

sona

l use

onl

y

APLNG has secured more prime CSG acreage...

• Successful Gazettal bid, May 2013 grant date.

• Bolt-on acreage adjacent to existing Condabri (PL265, 266, 267) development areas.

• 76km2 prime Undulla nose acreage

• High likelihood of reserves booking after initial exploration drilling.

...enabling high-value step-out development 9 |

For

per

sona

l use

onl

y

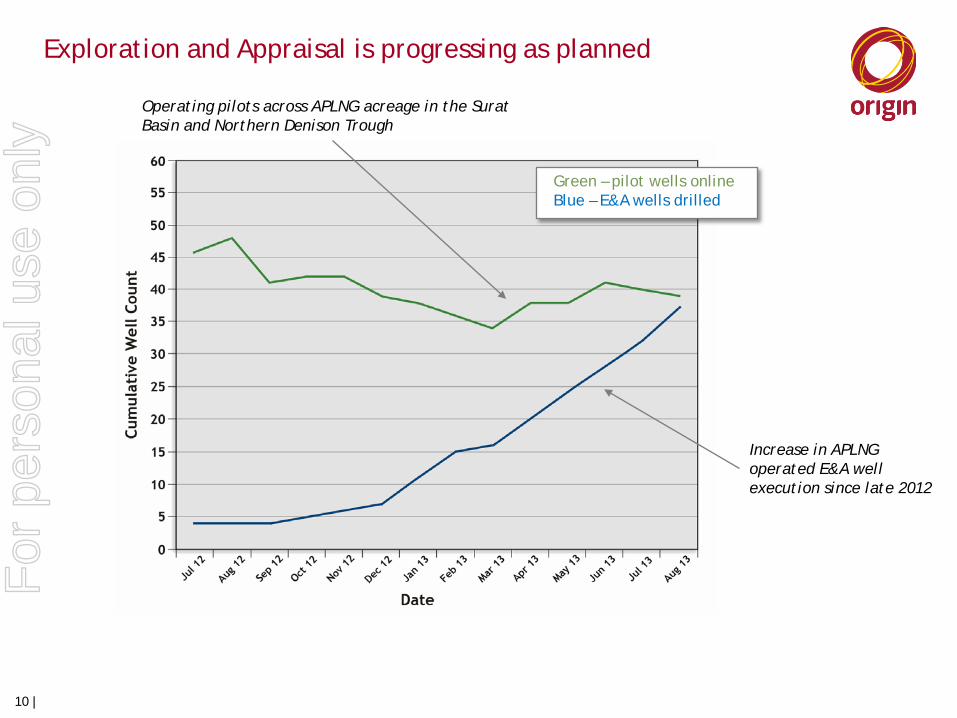

Exploration and Appraisal is progressing as planned

Green – pilot wells online Blue – E&A wells drilled

Operating pilots across APLNG acreage in the Surat Basin and Northern Denison Trough

Increase in APLNG operated E&A well execution since late 2012

10 |

For

per

sona

l use

onl

y

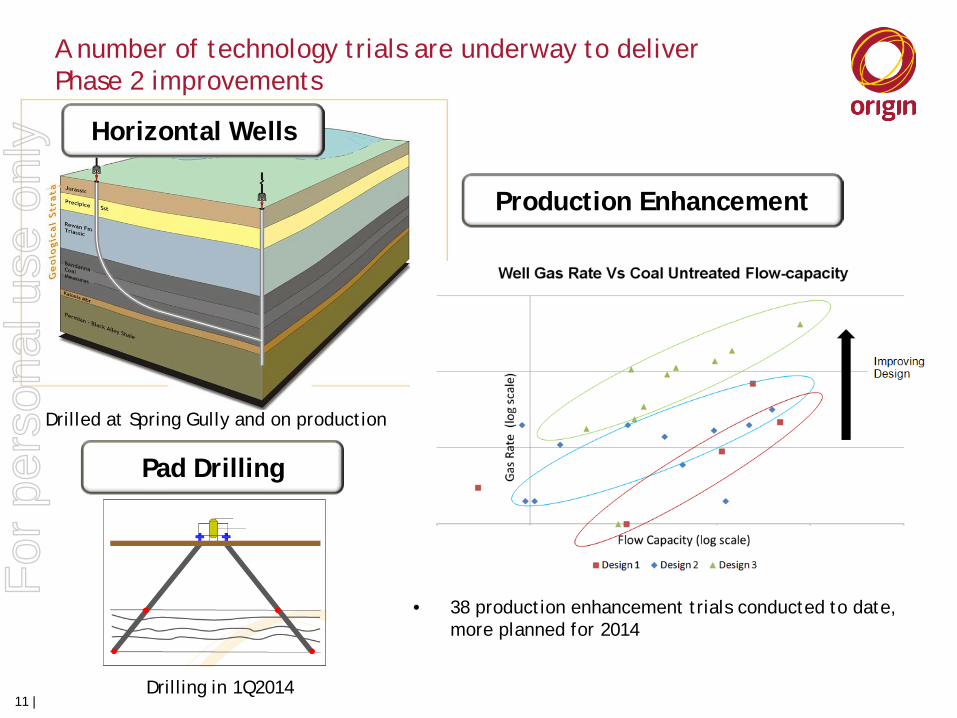

Horizontal Wells

Pad Drilling

Drilled at Spring Gully and on production

Drilling in 1Q2014

Production Enhancement

• 38 production enhancement trials conducted to date, more planned for 2014

A number of technology trials are underway to deliver Phase 2 improvements

11 |

For

per

sona

l use

onl

y

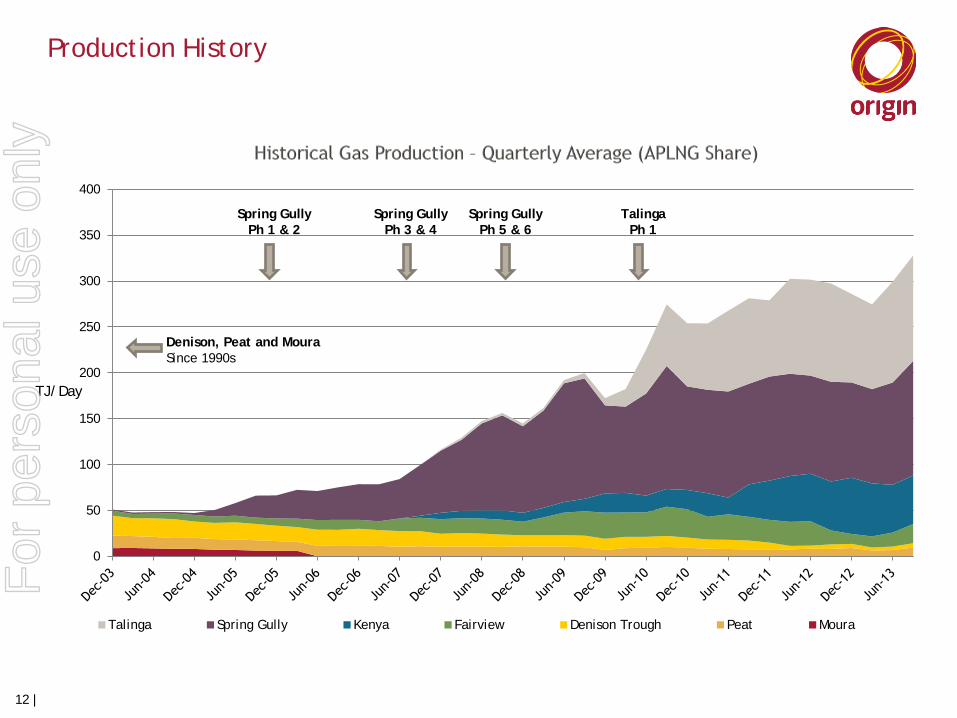

Production History

12 |

Denison, Peat and Moura Since 1990s

Spring Gully Ph 1 & 2

Spring Gully Ph 3 & 4

Spring Gully Ph 5 & 6

Talinga Ph 1

0

50

100

150

200

250

300

350

400

Talinga Spring Gully Kenya Fairview Denison Trough Peat Moura

TJ/Day

For

per

sona

l use

onl

y

13 |

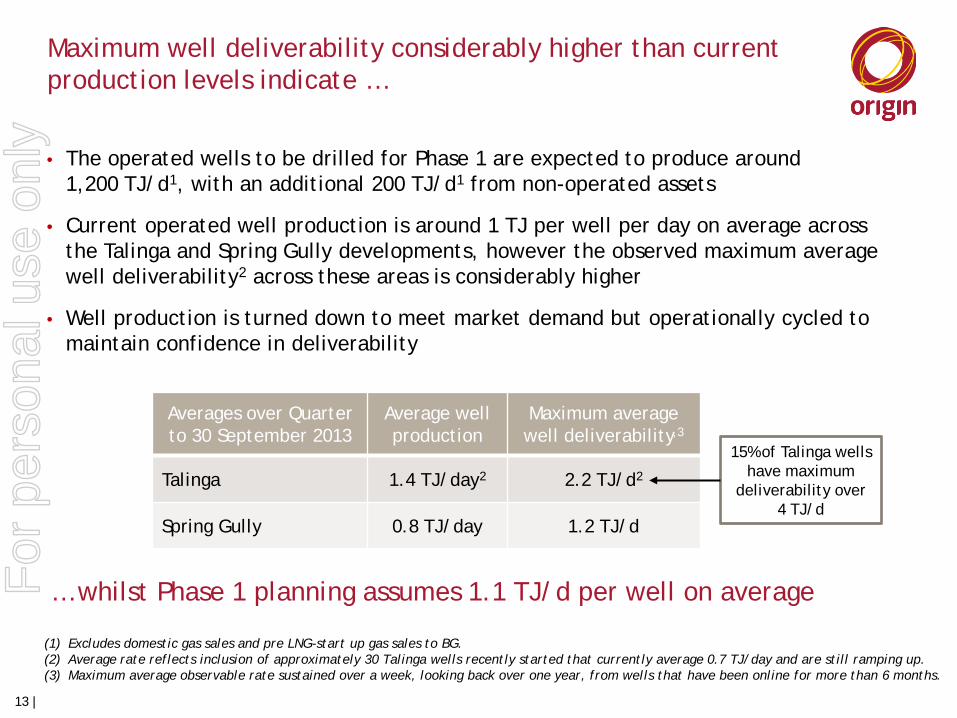

Maximum well deliverability considerably higher than current production levels indicate …

(1) Excludes domestic gas sales and pre LNG-start up gas sales to BG. (2) Average rate reflects inclusion of approximately 30 Talinga wells recently started that currently average 0.7 TJ/day and are still ramping up. (3) Maximum average observable rate sustained over a week, looking back over one year, from wells that have been online for more than 6 months.

• The operated wells to be drilled for Phase 1 are expected to produce around 1,200 TJ/d1, with an additional 200 TJ/d1 from non-operated assets

• Current operated well production is around 1 TJ per well per day on average across the Talinga and Spring Gully developments, however the observed maximum average well deliverability2 across these areas is considerably higher

• Well production is turned down to meet market demand but operationally cycled to maintain confidence in deliverability

Averages over Quarter to 30 September 2013

Average well production

Maximum average well deliverability,3

Talinga 1.4 TJ/day2 2.2 TJ/d2

Spring Gully 0.8 TJ/day 1.2 TJ/d

… whilst Phase 1 planning assumes 1.1 TJ/d per well on average

15% of Talinga wells have maximum

deliverability over 4 TJ/d

For

per

sona

l use

onl

y

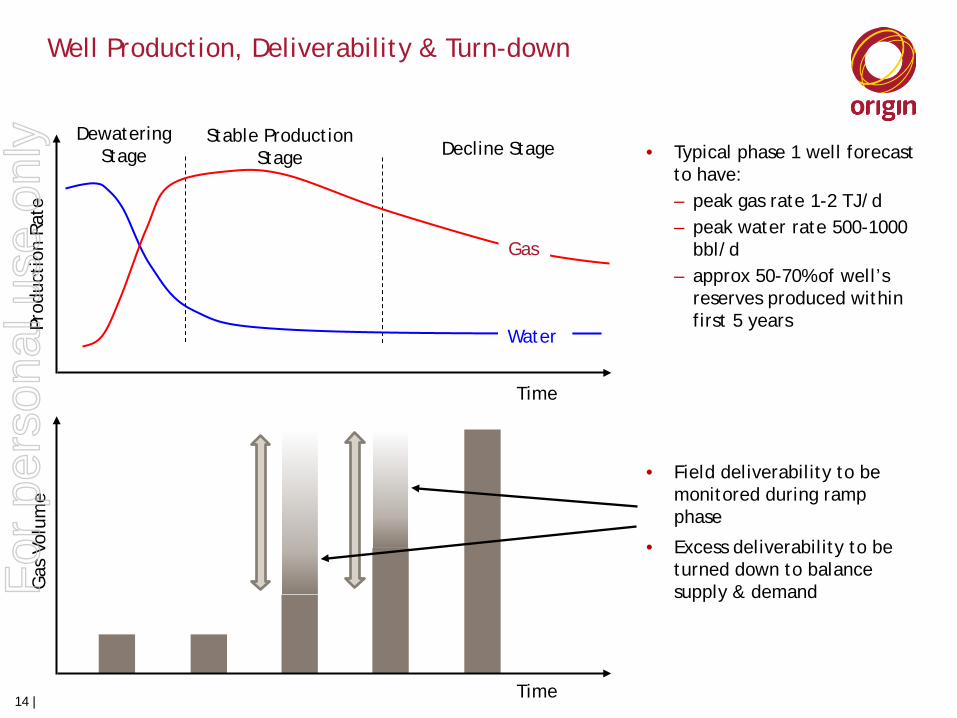

Well Production, Deliverability & Turn-down

• Typical phase 1 well forecast to have: – peak gas rate 1-2 TJ/d – peak water rate 500-1000

bbl/d – approx 50-70% of well’s

reserves produced within first 5 years

• Field deliverability to be monitored during ramp phase

• Excess deliverability to be turned down to balance supply & demand

Prod

ucti

on R

ate

Gas

Dewatering Stage

Water

Stable Production Stage Decline Stage

Time

Time

Gas

Vol

ume

14 |

For

per

sona

l use

onl

y

4 33 68

119

191 219

244 267

2 36 80 98

117

195

0

50

100

150

200

250

300

End 2011 End Q1 2012

End Q2 2012

End Q3 2012

End Q4 2012

End Q1 2013

End Q2 2013

End Q3 2013

Wells Drilled

Wells Completed

15 |

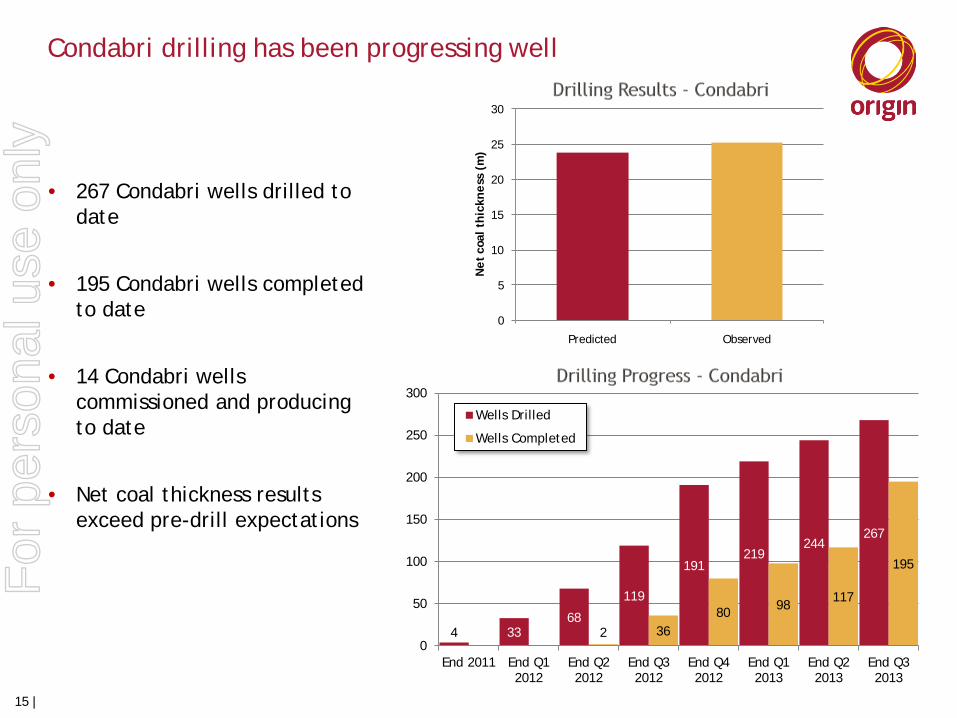

Condabri drilling has been progressing well

• 267 Condabri wells drilled to date

• 195 Condabri wells completed to date

• 14 Condabri wells commissioned and producing to date

• Net coal thickness results exceed pre-drill expectations

0

5

10

15

20

25

30

Predicted Observed

Net

coa

l thi

ckne

ss (

m)

For

per

sona

l use

onl

y

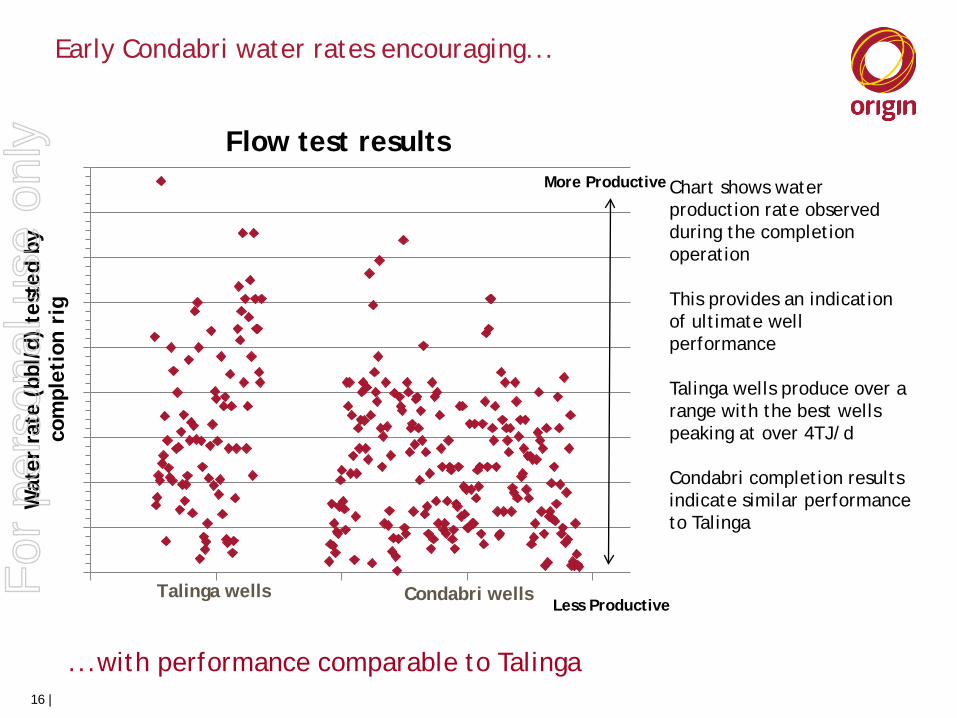

Early Condabri water rates encouraging...

16 |

...with performance comparable to Talinga

Chart shows water production rate observed during the completion operation This provides an indication of ultimate well performance Talinga wells produce over a range with the best wells peaking at over 4TJ/d Condabri completion results indicate similar performance to Talinga

More Productive

0

500

1000

1500

2000

2500

3000

3500

4000

4500

-50 50 150 250 350

Wat

er r

ate

(bbl

/d)

test

ed b

y co

mpl

etio

n ri

g

Flow test results

Talinga wells Condabri wells Less Productive

For

per

sona

l use

onl

y

Thank you

17 |

For

per

sona

l use

onl

y

APLNG Project - Upstream Delivery

Presented by Adrian Lang

Project Director

Origin Operational Review and Asset Visit 31 October 2013

For

per

sona

l use

onl

y

Upstream Project Goals

• Health and Safety •Zero Harm 1

• Environment and Land •Honour our Commitments 2

• Safe & Operable Production System •Automation from central control room 3

2 |

• Project within schedule and budget •On track to support LNG trains 4

• Team effectiveness •Operations team build underway 5

For

per

sona

l use

onl

y

Upstream Operations are like a factory

Optimise

Plan

Land Access

Drill

Complete

Connect

Operate

Produce

Scale & continuous improvement applied to

repeatable processes reduces execution risk and

drives costs lower

PJ /

yr

3 |

For

per

sona

l use

onl

y

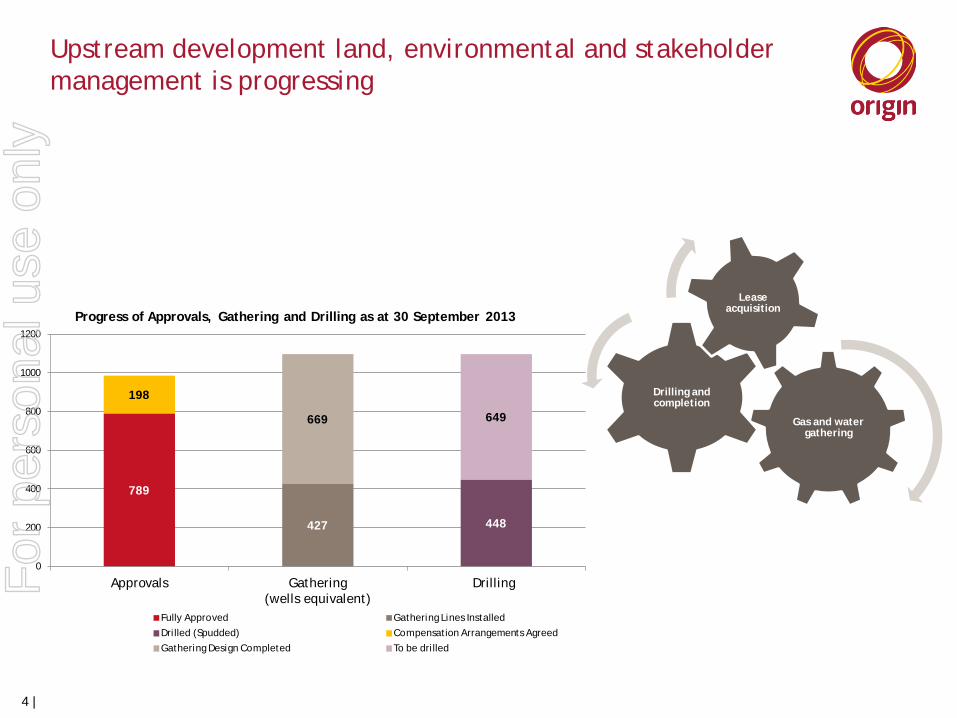

Upstream development land, environmental and stakeholder management is progressing

Gas and water gathering

Drilling and completion

Lease acquisition

4 |

789

427 448

198

669 649

0

200

400

600

800

1000

1200

Approvals Gathering (wells equivalent)

Drilling

Progress of Approvals, Gathering and Drilling as at 30 September 2013

Fully Approved Gathering Lines Installed

Drilled (Spudded) Compensation Arrangements Agreed

Gathering Design Completed To be drilled

For

per

sona

l use

onl

y

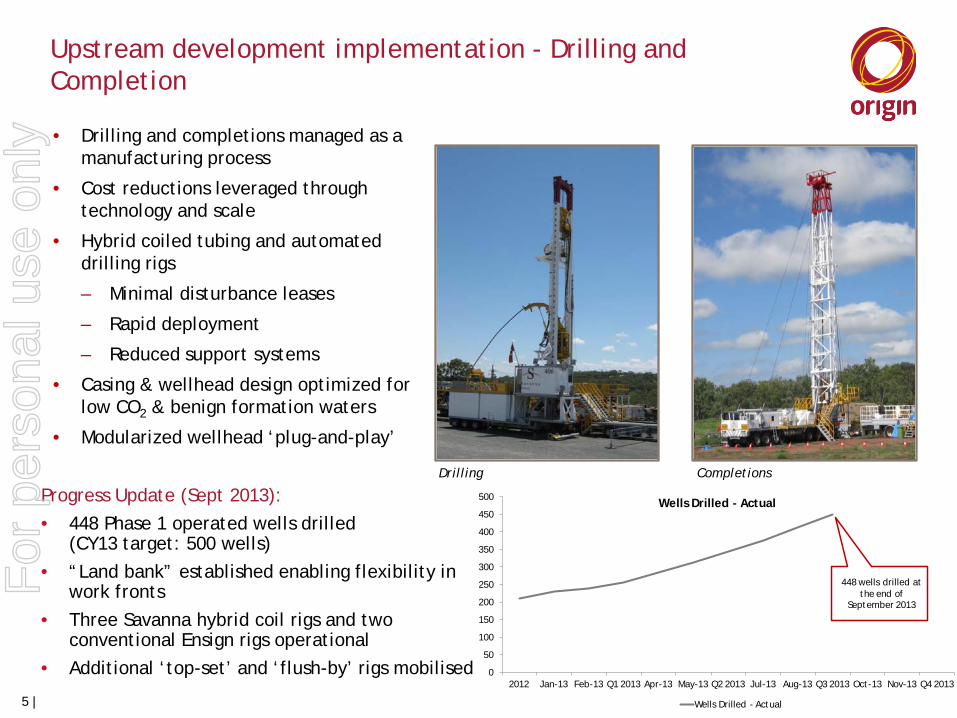

• Drilling and completions managed as a manufacturing process

• Cost reductions leveraged through technology and scale

• Hybrid coiled tubing and automated drilling rigs

– Minimal disturbance leases

– Rapid deployment

– Reduced support systems

• Casing & wellhead design optimized for low CO2 & benign formation waters

• Modularized wellhead ‘plug-and-play’

5 |

Drilling Completions

Upstream development implementation - Drilling and Completion

Progress Update (Sept 2013): • 448 Phase 1 operated wells drilled

(CY13 target: 500 wells) • “Land bank” established enabling flexibility in

work fronts • Three Savanna hybrid coil rigs and two

conventional Ensign rigs operational • Additional ‘top-set’ and ‘flush-by’ rigs mobilised 0

50

100

150

200

250

300

350

400

450

500

2012 Jan-13 Feb-13 Q1 2013 Apr-13 May-13 Q2 2013 Jul-13 Aug-13 Q3 2013 Oct-13 Nov-13 Q4 2013

Wells Drilled - Actual

Wells Drilled - Actual

448 wells drilled at the end of

September 2013

For

per

sona

l use

onl

y

Eastern Gas Fields (Condabri/Talinga) September 2013

Western Gas Fields (Spring Gully/Combabula) September 2013

Upstream development implementation – Phase 1 well progress

Miles

Condamine

Chinchilla

6 |

Combabula

Spring Gully

For

per

sona

l use

onl

y

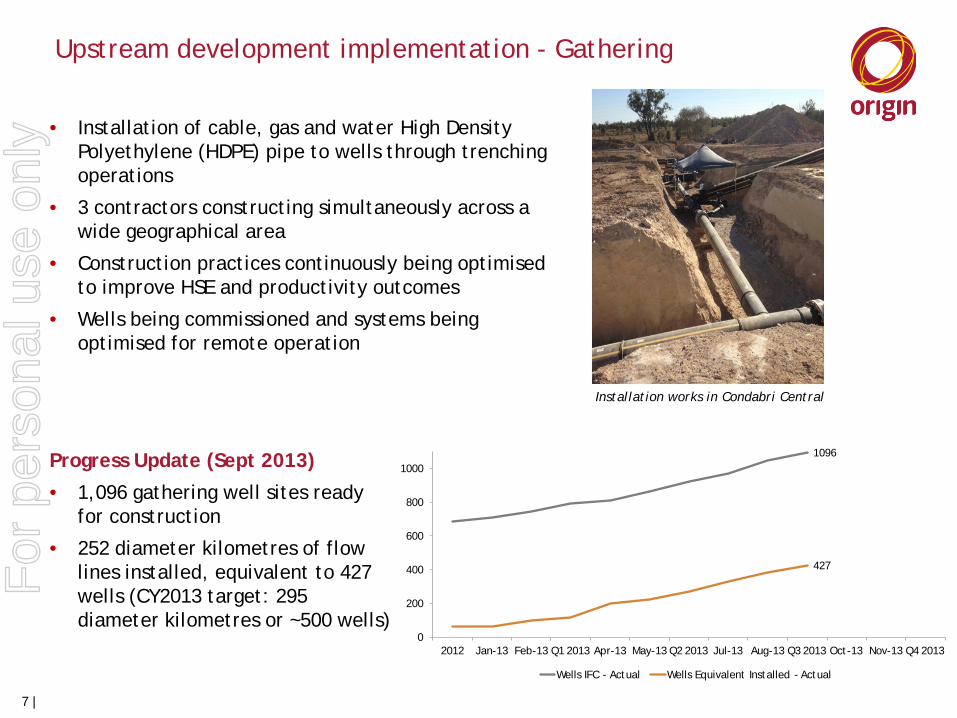

Upstream development implementation - Gathering

• Installation of cable, gas and water High Density Polyethylene (HDPE) pipe to wells through trenching operations

• 3 contractors constructing simultaneously across a wide geographical area

• Construction practices continuously being optimised to improve HSE and productivity outcomes

• Wells being commissioned and systems being optimised for remote operation

7 |

Progress Update (Sept 2013)

• 1,096 gathering well sites ready for construction

• 252 diameter kilometres of flow lines installed, equivalent to 427 wells (CY2013 target: 295 diameter kilometres or ~500 wells)

Installation works in Condabri Central

1096

427

0

200

400

600

800

1000

2012 Jan-13 Feb-13 Q1 2013 Apr-13 May-13 Q2 2013 Jul-13 Aug-13 Q3 2013 Oct-13 Nov-13 Q4 2013

Wells IFC - Actual Wells Equivalent Installed - Actual

For

per

sona

l use

onl

y

Upstream development implementation – Facilities

• 13 (out of 15 total) compressor trains arrived in Brisbane. Last 2 trains completed and ready for shipment

• First 12 gas plant pre-assembled module trains shipped from Thailand, last 3 trains due for completion end of year

• Construction under way for 5 out of 7 gas processing facilities and both water treatment facility sites

• First wells in Condabri Central brought online in August 2013, with gas flowing into gathering network and flared, and produced water flowing into ponds

• Condabri Central 1st train nearing completion, power being commissioned, capacity 90 TJ/day

8 |

TEG Module Module Unloading

For

per

sona

l use

onl

y

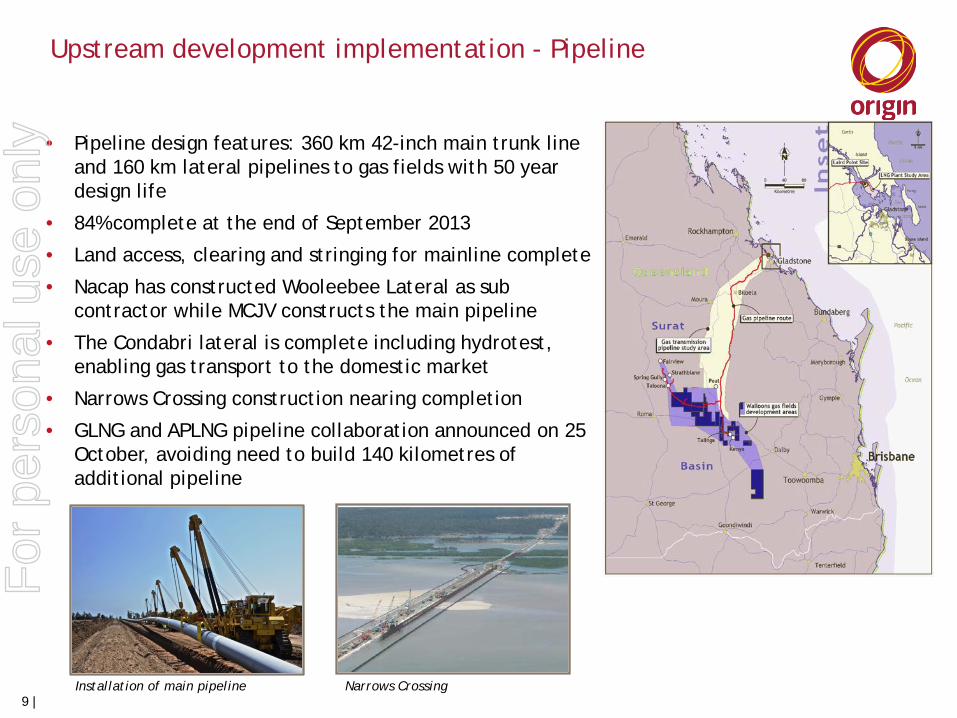

Upstream development implementation - Pipeline

• Pipeline design features: 360 km 42-inch main trunk line and 160 km lateral pipelines to gas fields with 50 year design life

• 84% complete at the end of September 2013

• Land access, clearing and stringing for mainline complete

• Nacap has constructed Wooleebee Lateral as sub contractor while MCJV constructs the main pipeline

• The Condabri lateral is complete including hydrotest, enabling gas transport to the domestic market

• Narrows Crossing construction nearing completion

• GLNG and APLNG pipeline collaboration announced on 25 October, avoiding need to build 140 kilometres of additional pipeline

Installation of main pipeline Narrows Crossing 9 |

For

per

sona

l use

onl

y

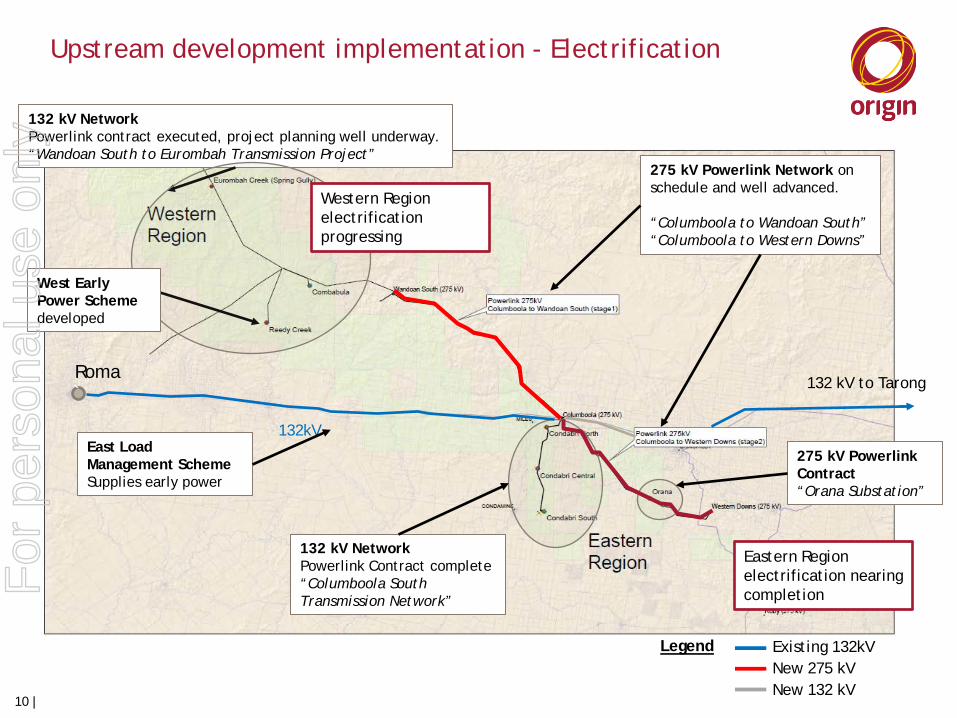

275 kV Powerlink Network on schedule and well advanced. “Columboola to Wandoan South” “Columboola to Western Downs”

132 kV Network Powerlink Contract complete “Columboola South Transmission Network”

` Roma

132kV East Load Management Scheme Supplies early power

132 kV to Tarong

275 kV Powerlink Contract “Orana Substation”

132 kV Network Powerlink contract executed, project planning well underway. “Wandoan South to Eurombah Transmission Project”

West Early Power Scheme developed

Upstream development implementation - Electrification

Existing 132kV New 275 kV New 132 kV

Legend

10 |

Western Region electrification progressing

Eastern Region electrification nearing completion F

or p

erso

nal u

se o

nly

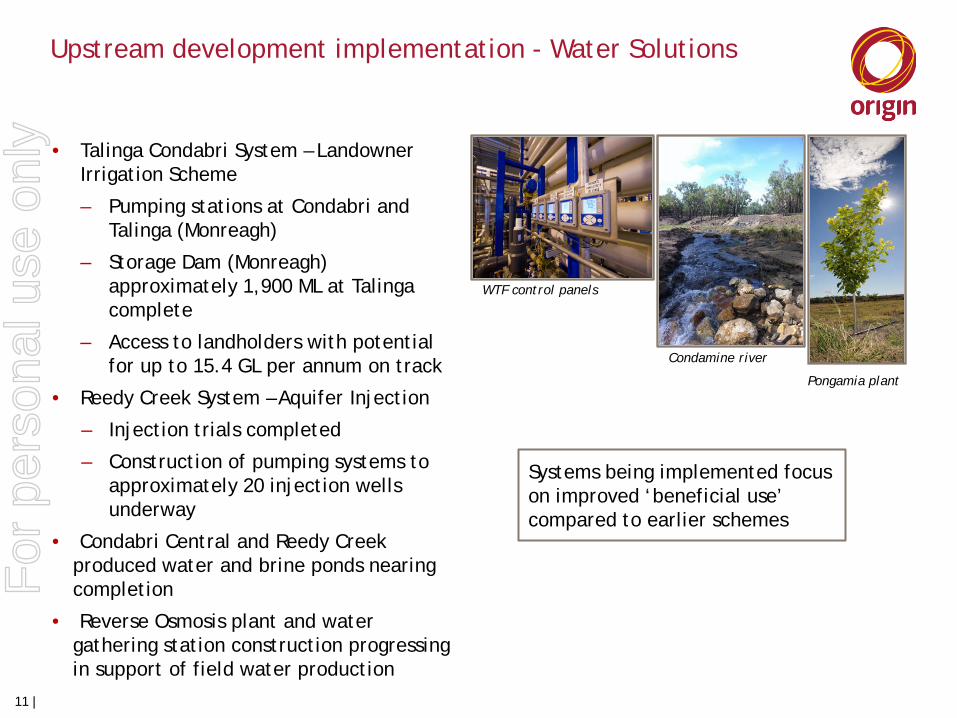

• Talinga Condabri System – Landowner Irrigation Scheme

– Pumping stations at Condabri and Talinga (Monreagh)

– Storage Dam (Monreagh) approximately 1,900 ML at Talinga complete

– Access to landholders with potential for up to 15.4 GL per annum on track

• Reedy Creek System – Aquifer Injection

– Injection trials completed

– Construction of pumping systems to approximately 20 injection wells underway

• Condabri Central and Reedy Creek produced water and brine ponds nearing completion

• Reverse Osmosis plant and water gathering station construction progressing in support of field water production

Upstream development implementation - Water Solutions

WTF control panels

Condamine river

Pongamia plant

11 |

Systems being implemented focus on improved ‘beneficial use’ compared to earlier schemes

For

per

sona

l use

onl

y

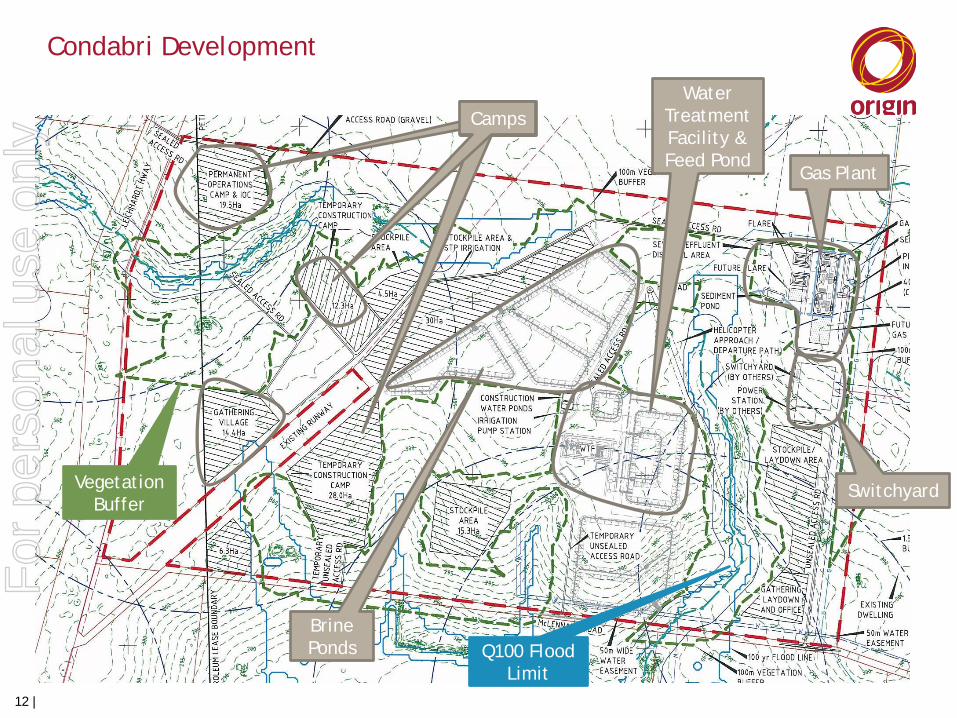

Condabri Development

Camps Camps Water

Treatment Facility & Feed Pond

Brine Ponds

Gas Plant

Vegetation Buffer

Q100 Flood Limit

Switchyard

Camps

12 |

For

per

sona

l use

onl

y

Upstream Project progress - 50% complete and on track at 30 September 2013

Spring Gully – laying of pipe

(1) Calculated by multiplying the diameter of the pipe by the length of the pipe 13 |

Upstream Operated Goals FY2014 Plan Actual Progress to 30 September

First gas and water production from Condabri Central (eastern area) Q1 Accomplished

500 wells drilled Q2 On Track: 448 wells drilled

295 diameter-kilometres1 of gathering line installed (equivalent to 500 wells) Q2 On Track: 252 diameter-kilometres installed (equivalent to

427 wells)

Condabri Central Train 1 commissioned Q3 On Track: Commissioning underway

First gas and water production from Reedy Creek (western area) Q3 On Track: Reedy Creek construction progressing

Main pipelines complete Q3 On Track: 84% complete

Gathering - Pongamia camp Reedy Creek – electrification gas engine

For

per

sona

l use

onl

y

Thank you

For

per

sona

l use

onl

y

APLNG Project – Downstream Delivery

Presented by David Hayter Deputy Project Director, Downstream Project

Origin Operational Review and Asset Visit

1 November 2013

For

per

sona

l use

onl

y

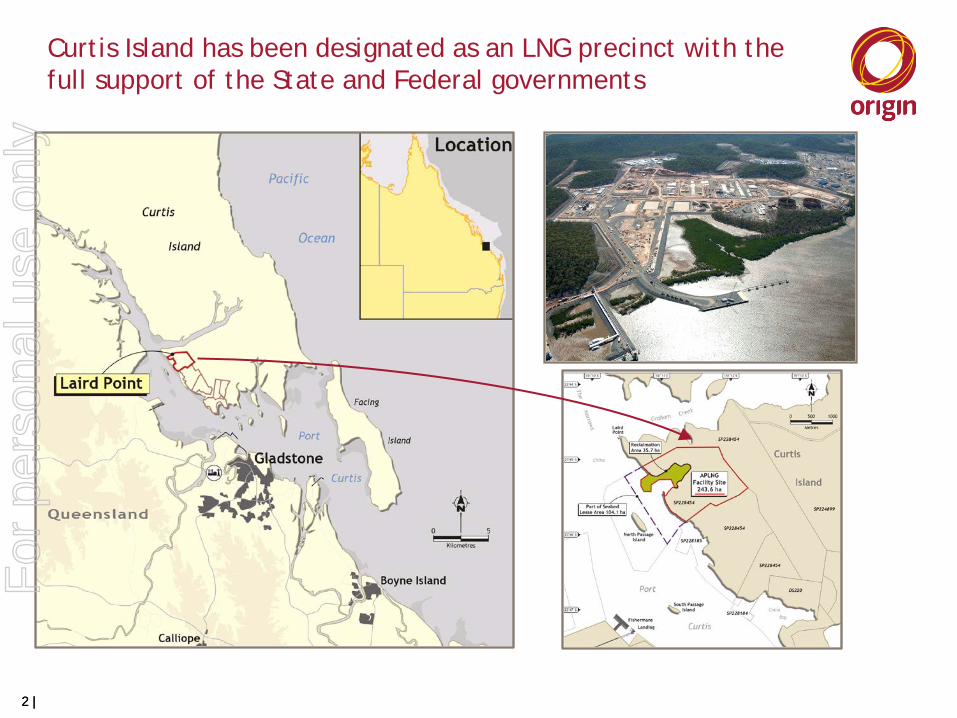

Curtis Island has been designated as an LNG precinct with the full support of the State and Federal governments

2 | 2 |

For

per

sona

l use

onl

y

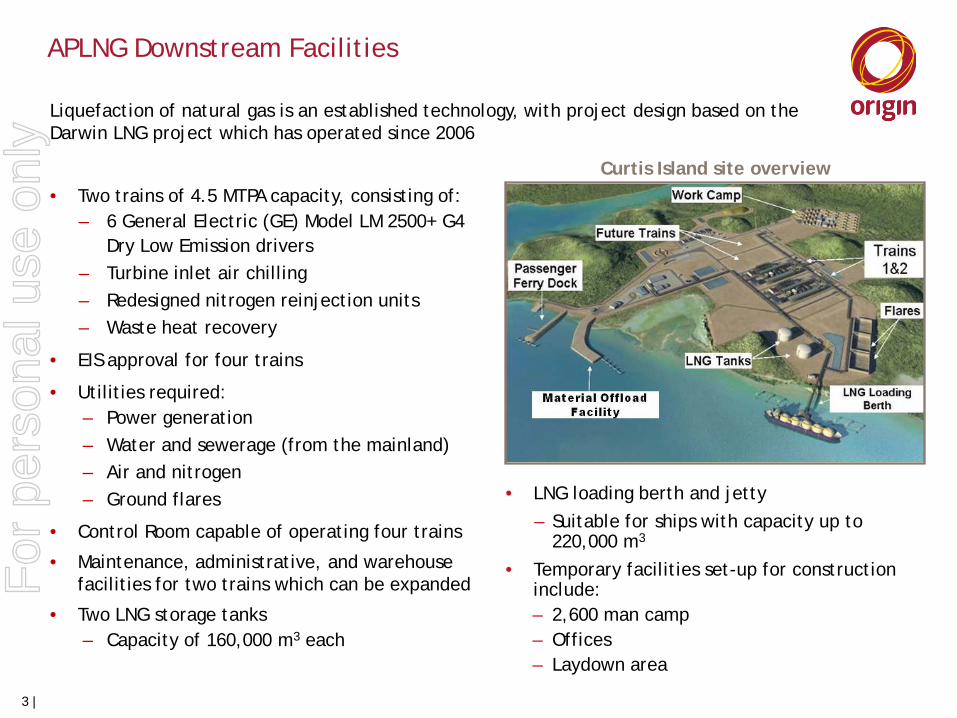

• Two trains of 4.5 MTPA capacity, consisting of: – 6 General Electric (GE) Model LM 2500+ G4

Dry Low Emission drivers – Turbine inlet air chilling – Redesigned nitrogen reinjection units – Waste heat recovery

• EIS approval for four trains

• Utilities required: – Power generation – Water and sewerage (from the mainland) – Air and nitrogen – Ground flares

• Control Room capable of operating four trains

• Maintenance, administrative, and warehouse facilities for two trains which can be expanded

• Two LNG storage tanks – Capacity of 160,000 m3 each

• LNG loading berth and jetty – Suitable for ships with capacity up to

220,000 m3

• Temporary facilities set-up for construction include: – 2,600 man camp – Offices – Laydown area

Curtis Island site overview

APLNG Downstream Facilities

3 |

Liquefaction of natural gas is an established technology, with project design based on the Darwin LNG project which has operated since 2006

For

per

sona

l use

onl

y

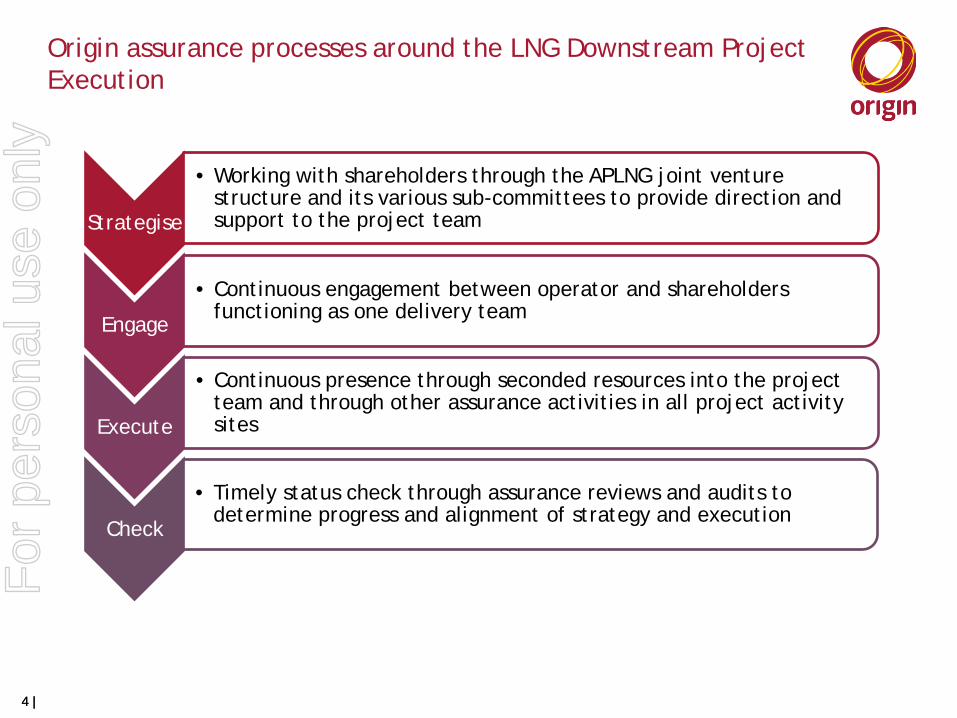

Origin assurance processes around the LNG Downstream Project Execution

Strategise

• Working with shareholders through the APLNG joint venture structure and its various sub-committees to provide direction and support to the project team

Engage

• Continuous engagement between operator and shareholders functioning as one delivery team

Execute

• Continuous presence through seconded resources into the project team and through other assurance activities in all project activity sites

Check

• Timely status check through assurance reviews and audits to determine progress and alignment of strategy and execution

4 | 4 |

For

per

sona

l use

onl

y

Downstream project current status - Engineering

• Overall engineering progress on the Downstream project is ahead of plan and nearing completion

• The final piping isometric drawings were issued in August 2013

• Monitoring of Factory Acceptance Testing remains a major activity, including:

– Remaining Train 2 GE refrigeration compressors

– Honeywell Integrated Control & Safety System (ICSS)

– Ebra cryogenic pumps

5 |

For

per

sona

l use

onl

y

• Procurement is over 80% complete, ahead of plan

• Structural steel and pipe spools continued to be delivered to the Curtis Island construction site and the Batam Module yard

• Major deliveries to Curtis Island since January 2013 have included:

– 4 main pipe rack modules

– 7 (of 7) LNG loading rack modules

– 1 (of 1) sub cooler module

– 3 (of 5) propane condenser module

– First batch of pre-fabricated generation substations

– Train 2 CO2 absorber column

– First Train 2 refrigeration compressors

– Amine storage & liquid nitrogen tanks

Power Generation Substation – Outside Battery Limits (OSBL)

Train 2 CO2 Absorber

Downstream project current status - Procurement

6 |

For

per

sona

l use

onl

y

Downstream project current status - Construction

7 |

MODULE FABRICATION, INDONESIA • 25 of 46 Train 1 & OSBL modules completed and

shipped • All remaining Train 1 & OSBL modules forecast to

be shipped before year end

DREDGING

• All dredging works complete, demobilisation in progress

• Ongoing maintenance dredging will continue, as needed

TEMPORARY WORKERS’ ACCOMMODATION FACILITY (TWAF)

• All 2,600 beds available (1,500 currently occupied)

• Additional gyms are being added due to demand

LNG TRAINS • All Train 1 refrigeration compressors are set.

Inlet and exhaust infrastructure is being erected. All large bore pipe erected under table top

• Train 2 foundations works continuing. All compressor building table tops have been poured. The CO2 absorber column has been set

LNG TANKS • Tanks A & B: each roof raised. Concrete roof

construction in progress. Outer carbon steel tank complete. Erection of inner nickel steel tank in progress

• Outer wall concrete pours continue on both tanks

MARINE FACILITIES

• Piling completed for LNG jetty, loading platform and dolphins. Headstocks installed on loading platform

For

per

sona

l use

onl

y

Resourcing

• >2,200 people at Curtis Island – 1,500 people currently staying

• >3,600 people at Batam Module Yard in Indonesia (peak will be sustained until year end, then decline)

• Curtis Island peak workforce expected to exceed 3,500 personnel (two trains) starting 1Q 2014

• Current key focus areas over the next six months are

• Special Class Welders

• Construction Superintendents and Supervisors

• More local personnel resourcing is available than planned

8 |

For

per

sona

l use

onl

y

Downstream Project progress - 54% complete and on track at 30 September 2013

LNG Tanks, September 2013 Curtis Island site, September 2013 Overview of Train 1 Inside Battery Limits (ISBL)

9 |

Downstream Operated Goals FY2014 Plan Actual Progress

Final Train 1 refrigeration compressor set Q1 Accomplished

Accommodation camp complete Q1 Accomplished

Complete Train 2 compressor table tops Q2 Accomplished

Complete loading platform for LNG jetty Q2 On Track

First Train 1 cold boxes (methane and ethylene) delivered to site and set Q2 On Track: Cold Boxes complete, due to be shipped 1st week of

November

Last Train 1 Module set Q3 On Track: All Train 1 Modules are due to be shipped early 2014

For

per

sona

l use

onl

y

Port of Gladstone Overview

Gladstone

Brisbane

FLNE

CELL 3

GOONDOON STREET

BENSTED ROAD

MARINA & RG TANNA

APLNG

10 |

QCLNG (BG)

CURTIS ISLAND

GLNG (SANTOS)

For

per

sona

l use

onl

y

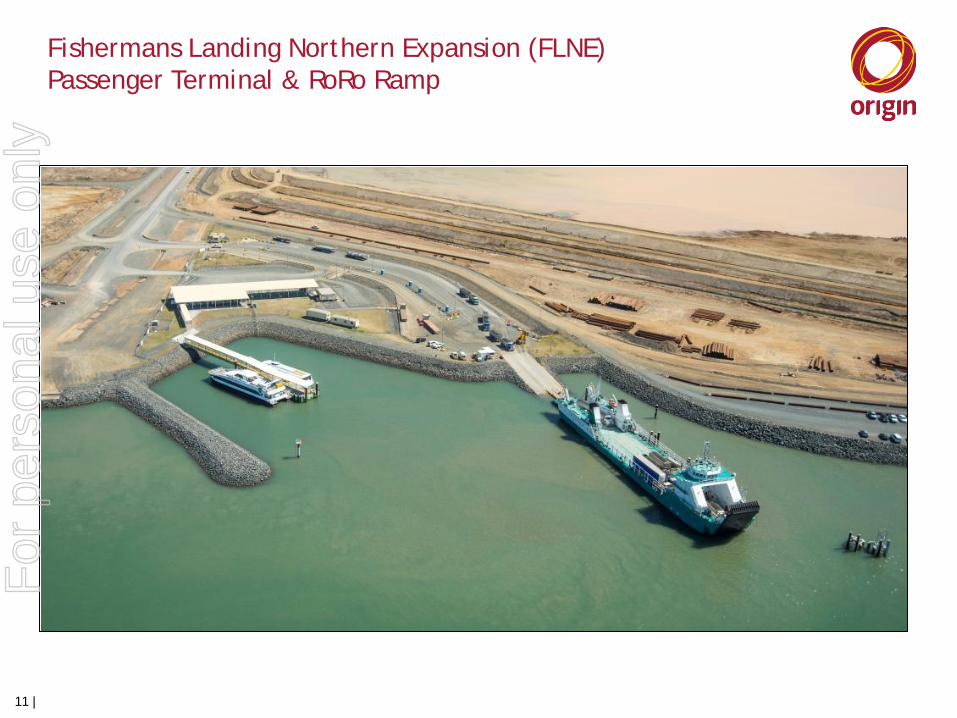

Fishermans Landing Northern Expansion (FLNE) Passenger Terminal & RoRo Ramp

11 |

For

per

sona

l use

onl

y

Fishermans Landing Northern Expansion (FLNE) Bund Wall

12 |

For

per

sona

l use

onl

y

Curtis Island Site, September 2013

13 |

For

per

sona

l use

onl

y

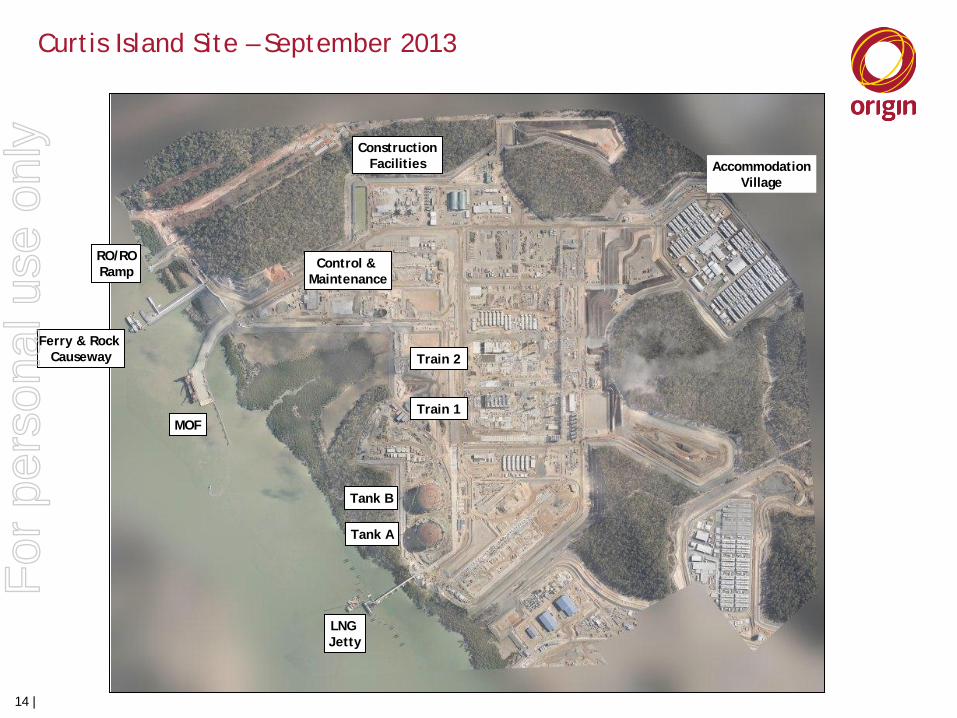

Curtis Island Site – September 2013

14 |

Utilities

Tank B

Tank A

Train 2

Train 1 MOF

Ferry & Rock Causeway

RO/RO Ramp

Construction Facilities

Control & Maintenance

Accommodation Village

LNG Jetty

For

per

sona

l use

onl

y

Trains 1 & 2 & Outside Battery Limits (OSBL) – September 2013

15 |

Train 1

Train 2

Main North-South Pipe Rack

Power Generation

For

per

sona

l use

onl

y

Trains 1 & 2 & OSBL – September 2013

16 |

For

per

sona

l use

onl

y

Trains 1 Compressor Building – September 2013

17 |

For

per

sona

l use

onl

y

Train 2 Area – September 2013

18 |

For

per

sona

l use

onl

y

LNG Tanks – September 2013

19 |

For

per

sona

l use

onl

y

Temporary Worker Accommodation Facility – September 2013

20 |

For

per

sona

l use

onl

y

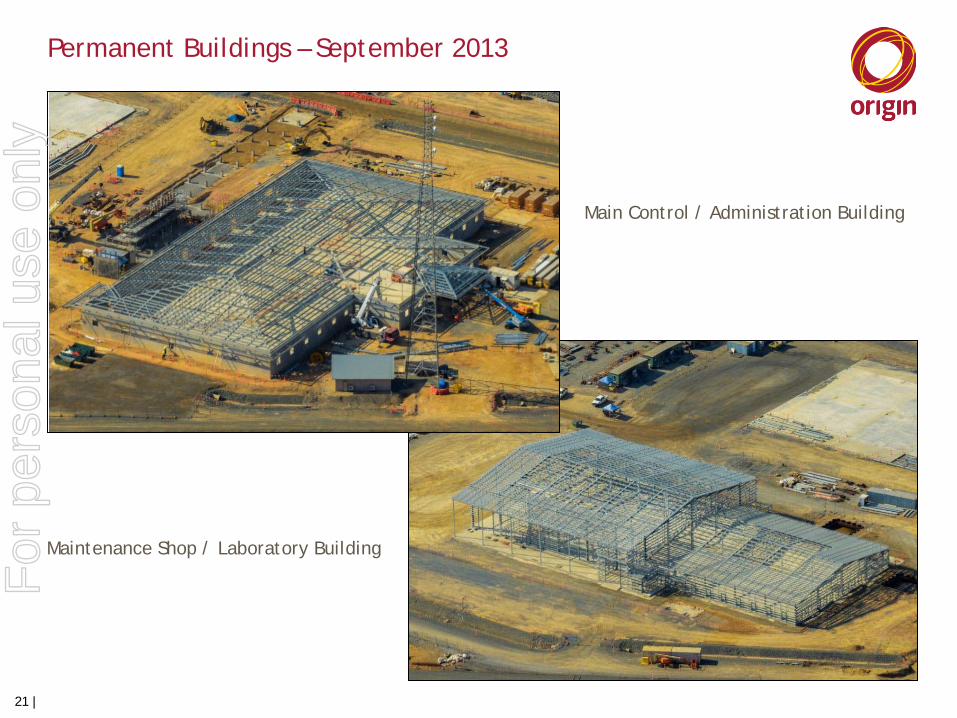

Permanent Buildings – September 2013

21 |

Main Control / Administration Building

Maintenance Shop / Laboratory Building

For

per

sona

l use

onl

y

LNG Jetty – September 2013

22 |

For

per

sona

l use

onl

y

Batam Module Yard, Indonesia – September 2013

23 |

For

per

sona

l use

onl

y

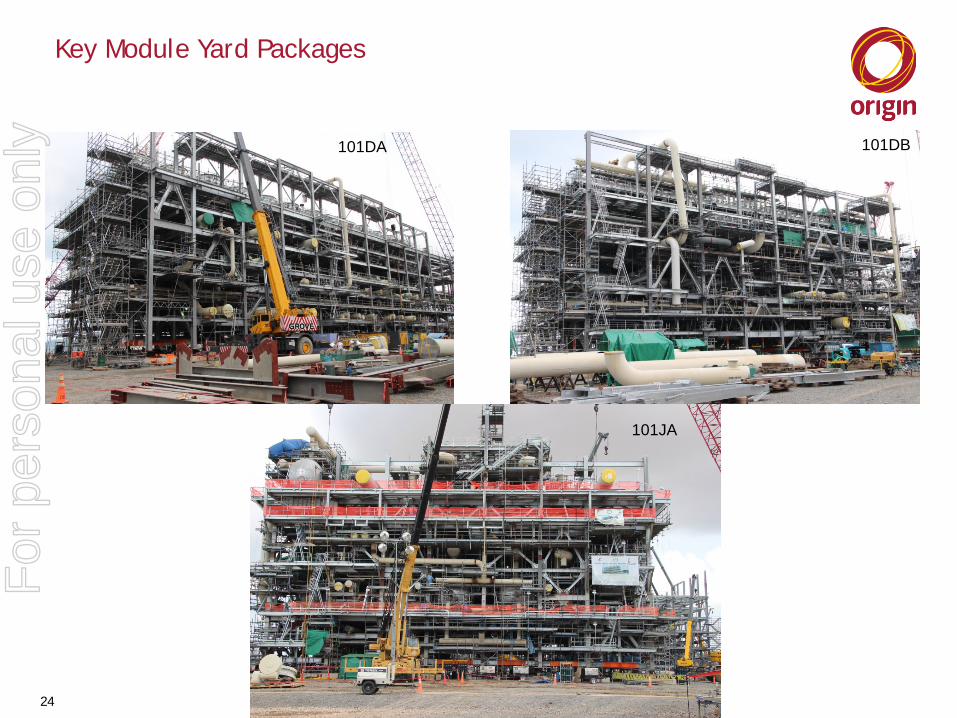

Key Module Yard Packages

24

101DB

101JA

101DA

For

per

sona

l use

onl

y

Thank you

25 |

For

per

sona

l use

onl

y