opportunity of infrastructure...

TRANSCRIPT

Darmawan JunaidiDirector

PT Bank Mandiri (Persero) Tbk

Opportunity of Infrastructure Financing

| 2

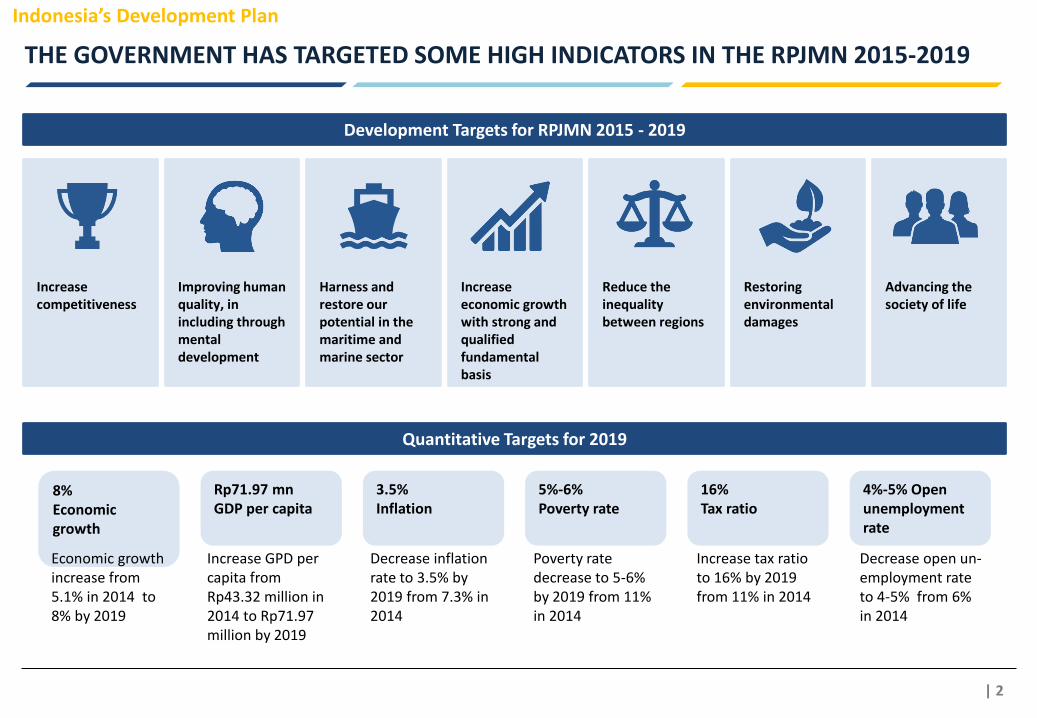

Indonesiarsquos Development Plan

THE GOVERNMENT HAS TARGETED SOME HIGH INDICATORS IN THE RPJMN 2015-2019

Increase economic growth with strong and qualified fundamental basis

8Economic growth

Rp7197 mnGDP per capita

35Inflation

5-6Poverty rate

16 Tax ratio

4-5 Open unemployment rate

Increase competitiveness

Improving human quality in including through mental development

Harness and restore our potential in the maritime and marine sector

Reduce the inequality between regions

Restoring environmental damages

Advancing the society of life

Economic growth increase from 51 in 2014 to 8 by 2019

Increase GPD per capita from Rp4332 million in 2014 to Rp7197 million by 2019

Decrease inflation rate to 35 by 2019 from 73 in 2014

Poverty rate decrease to 5-6 by 2019 from 11 in 2014

Increase tax ratio to 16 by 2019 from 11 in 2014

Decrease open un-employment rate to 4-5 from 6 in 2014

Development Targets for RPJMN 2015 - 2019

Quantitative Targets for 2019

| 3

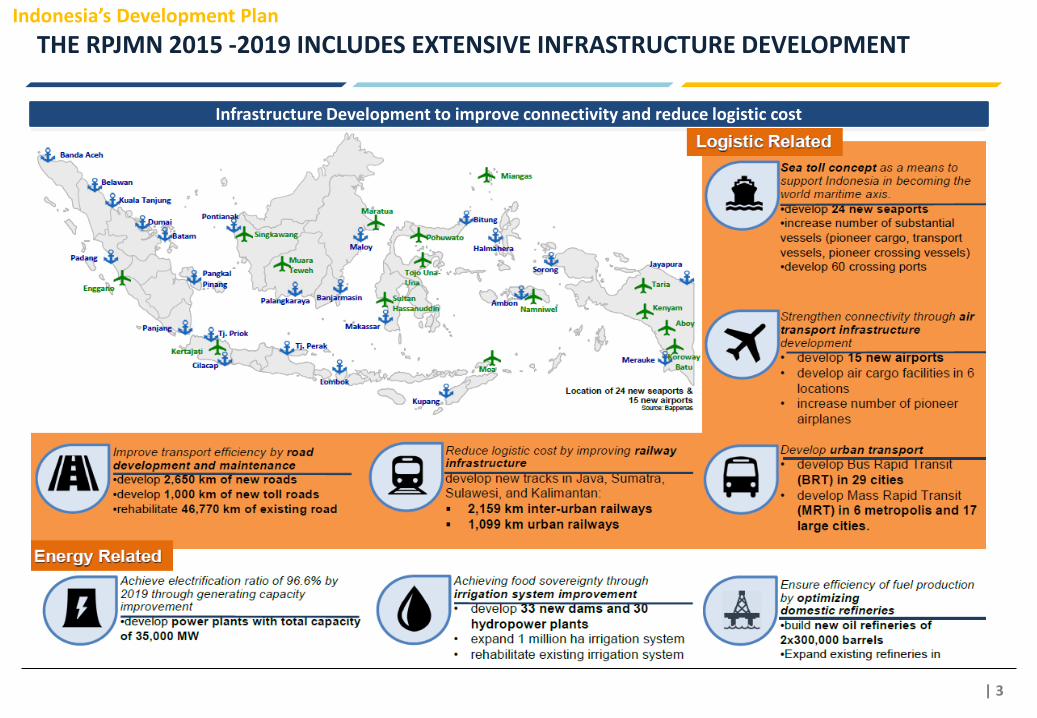

Indonesiarsquos Development Plan

THE RPJMN 2015 -2019 INCLUDES EXTENSIVE INFRASTRUCTURE DEVELOPMENT

Infrastructure Development to improve connectivity and reduce logistic cost

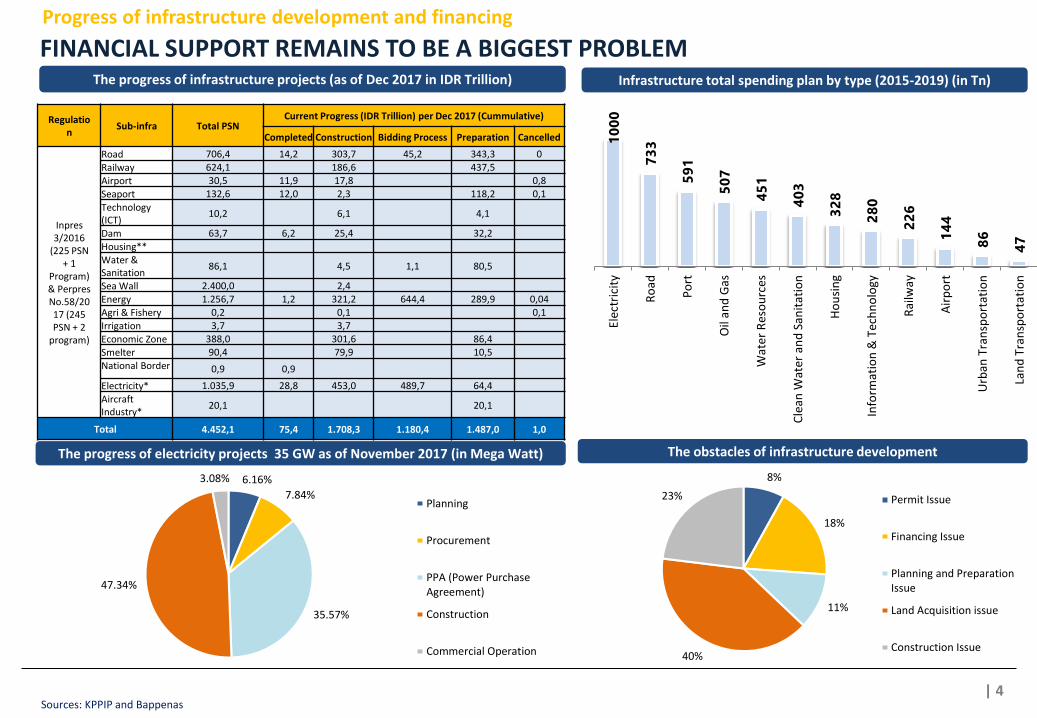

| 4

FINANCIAL SUPPORT REMAINS TO BE A BIGGEST PROBLEM

10

00

73

3

59

1

50

7

45

1

40

3

32

8

28

0

22

6

14

4

86

47

Elec

tric

ity

Ro

ad

Po

rt

Oil

and

Gas

Wat

er R

eso

urc

es

Cle

an W

ater

an

d S

anit

atio

n

Ho

usi

ng

Info

rmat

ion

amp T

ech

no

logy

Rai

lway

Air

po

rt

Urb

an T

ran

spo

rtat

ion

Lan

d T

ran

spo

rtat

ion

Sources KPPIP and Bappenas

616

784

3557

4734

308

Planning

Procurement

PPA (Power PurchaseAgreement)

Construction

Commercial Operation

8

18

11

40

23 Permit Issue

Financing Issue

Planning and PreparationIssue

Land Acquisition issue

Construction Issue

The progress of infrastructure projects (as of Dec 2017 in IDR Trillion)

Regulation

Sub-infra Total PSN Current Progress (IDR Trillion) per Dec 2017 (Cummulative)

Completed Construction Bidding Process Preparation Cancelled

Inpres 32016

(225 PSN + 1

Program) amp Perpres No582017 (245 PSN + 2

program)

Road 7064 142 3037 452 3433 0

Railway 6241 1866 4375

Airport 305 119 178 08

Seaport 1326 120 23 1182 01

Technology (ICT)

102 61 41

Dam 637 62 254 322

HousingWater amp Sanitation

861 45 11 805

Sea Wall 24000 24

Energy 12567 12 3212 6444 2899 004

Agri amp Fishery 02 01 01

Irrigation 37 37

Economic Zone 3880 3016 864

Smelter 904 799 105

National Border 09 09

Electricity 10359 288 4530 4897 644

Aircraft Industry

201 201

Total 44521 754 17083 11804 14870 10

Infrastructure total spending plan by type (2015-2019) (in Tn)

The progress of electricity projects 35 GW as of November 2017 (in Mega Watt) The obstacles of infrastructure development

Progress of infrastructure development and financing

| 5

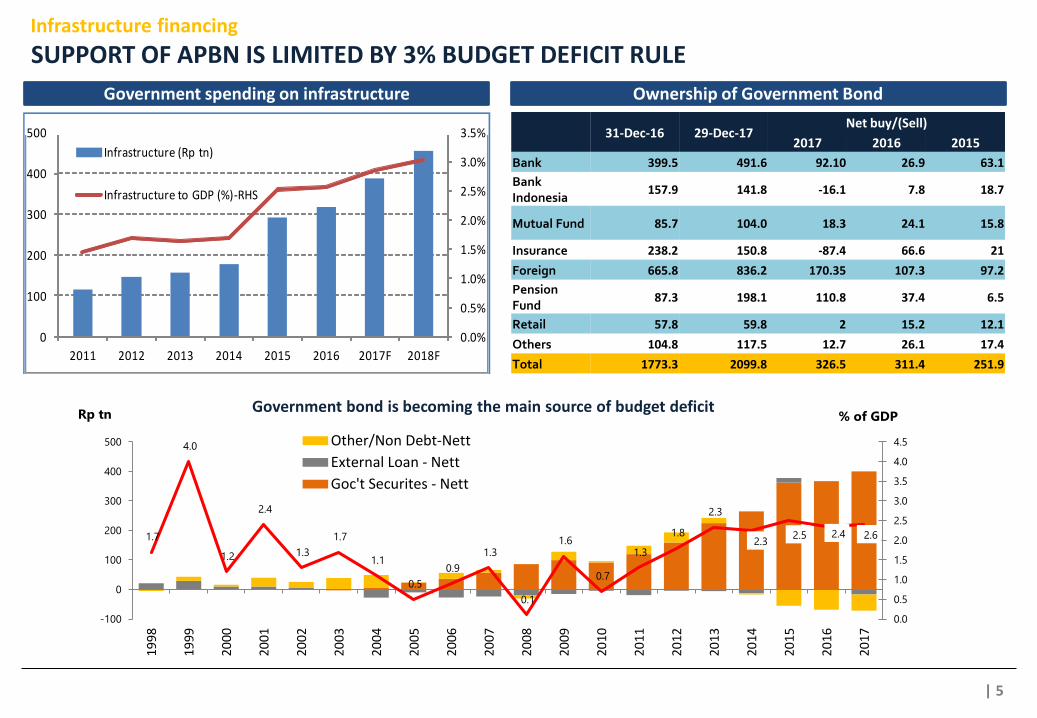

Infrastructure financing

SUPPORT OF APBN IS LIMITED BY 3 BUDGET DEFICIT RULE

Government spending on infrastructureGOVERNMENT SPENDING ON INFRASTRUTURE

Sources Nota Keuangan and our estimation

00

05

10

15

20

25

30

35

0

100

200

300

400

500

2011 2012 2013 2014 2015 2016 2017F 2018F

Infrastructure Spending

Infrastructure (Rp tn)

Infrastructure to GDP ()-RHS

31-Dec-16 29-Dec-17Net buy(Sell)

2017 2016 2015

Bank 3995 4916 9210 269 631

Bank Indonesia

1579 1418 -161 78 187

Mutual Fund 857 1040 183 241 158

Insurance 2382 1508 -874 666 21

Foreign 6658 8362 17035 1073 972

Pension Fund

873 1981 1108 374 65

Retail 578 598 2 152 121

Others 1048 1175 127 261 174

Total 17733 20998 3265 3114 2519

Ownership of Government Bond

17

40

12

24

13

17

11

05

09

13

01

16

07

13

18

23

23 25 24 26

00

05

10

15

20

25

30

35

40

45

-100

0

100

200

300

400

500

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

of GDPRp tn

OtherNon Debt-Nett

External Loan - Nett

Goct Securites - Nett

Government bond is becoming the main source of budget deficit

| 6

Infrastructure financing from bank loans

BANKS ARE STILL DEALING WITH STRUCTURAL PROBLEMS

LDR and third party fund

Sources OJK OCErsquos calculation

22 31 32 32 31

55 46 46 45 46

23 23 22 23 23

0

20

40

60

80

100

2001 2010 2015 2016 Sep-17

Saving Time Deposit Demand Deposit

6951 53 50 477

19

31 25 27 303

4 9 11 12 114

8 9 11 12 107

0

20

40

60

80

100

2001 2010 2015 2016 Sep-17

1 Month 3 Month 6 Month 12 Month

7550

9291

88185

73 96117

60

70

80

90

100

110

2010 2015 2016 Sep-17

LDR TPF

Third Party Funding Composition LDR and third party fund

Time deposit composition (IDR)

IDR

USD 2008

140

702013

118

49Sept-17

108

50

Investment Interest Rate

196

249

242

Proportion of long term loan to total loan

| 7Offsite Discussion Material | Securitization

BANK LOAN TO INFRA PROJECTS IS RAPIDLY INCREASING BUT STILL BELOW THE NEEDS

7

Sources Perpres 132010 LPI dan GCI

Sources OJK OCErsquos calculation

1142

12

17

00

20

40

60

0

20

40

60

80

100

120

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

1644

19

21

0

2

4

0

50

100

150

2002

01

0

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

398

57

79

0

2

4

6

8

10

01020304050607080

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

42 51 59 71 83 94 101 117 136 15841 57 76 93 101 118162

203255

321

3847

4360

6765

54

58

61

65

2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F

Logistics Utilities Oil amp gas

Loan Provided by Banking to Infrastructure ProjectsTypology of Infrastructure Projects

Bank loan to logistic sector Bank loan to oil and gas sectorBank loan to utilities sector

Infrastructure financing from bank loans

| 8

Bank Mandirirsquos contribution to infrastructure financing

INFRASTRUCTURE LOAN FROM BANK MANDIRI GREW 159 IN 2017

Notes) Classification is based of Perpres No38 2015 about Government Cooperation with Infrastructure Institution

1) Road and toll road2) Including ports airports and railways3) Including water waste education tourism and health

Limit 150 612 286 507 164 180 213 138 2251 159

Loan 94 364 172 274 96 103 122 97 1321 114

Road 1) Transportation 2) Oil and gas and renewable energy

Electricity Information technology

Construction Other 3) Total YoYHousing amp City Infrastructure

Data Sept-2017Rp Tn

Source Bank Mandiri

| 9

Bank Mandirirsquos contribution to infrastructure financing

BANK MANDIRI GIVES SIGNIFICANT CONTRIBUTION TO NATIONAL PRIORITY PROJECTS

Refinancing 43 port in middle IndonesiaProject Cost IDR 148 tnTenor 2016-2024 (8 years)

Solar Power Plant Kupang Len IndustryProject cost IDR 149 bnTenor sd 2022

Capex 2016-2017Angkasa Pura IProject cost IDR105 tnTenor sd 2031

438 Train Carriage RevitalizationProject cost IDR22tnTenor 2017-2018 (1 year)

Toll road Semarang ndash Solo (73 km)Project cost IDR 73 tnTenor 2009-2026 (15 years)

Source Bank Mandiri

South Natuna Blok-BProject cost USD 241 mnTenor 2016-2022 (6 years)

Steam Powerplant Lampung 2x300MWProject cost IDR 253 bn

Toll road Batang ndash Semarang(75 km)Project cost IDR 11 tnTenor 2017-2019 (2 years)

Airport TrainSoekarno HattaProject cost IDR17 tnTenor 2015-2029 (14 years)

Kuala Tanjung Port phase IProject Cost IDR 3 tnTenor 2016-2026 (10 years)

| 10

Bank Mandirirsquos contribution to infrastructure financing

MAIN CRITERIA amp PRIORITIES FOR INFRASTRUCTURE FINANCING

Included in National Priority Projects

Project Feasibility demands traffics break even point NPV IRR

Land Acquisition Percentage of land acquired (minimum 75 )

Main contractor for the project reputable contractor

Project Sponsor reputation and financial capacity

Main Criteria

No Priorities on Certain Sector as long as the Projects passed criteria above

Guarantee (if any) PT PII (PenjaminanInfrastrukturIndonesia)

Road amp Toll Road

TransportationPorts Airports amp

Railways

Oil and gas and renewable energy

Electricity Information technology

ConstructionHousing amp City Infrastructure

Other water waste tourism and health

| 11

Bank Mandirirsquos contribution to infrastructure financing

RISK MITIGATION

In-depth review on projects feasibility amp investor capacity

bull All projects should pass the criteria project feasibility land acquisition contractors Nationalpriority projects and Investee

bull Guarantee such as from PT PII is preferable

Benefits of syndicationbull Risk sharingbull Portfolio sharingbull More parties involved in analyzing the projects

bull Loan will be structured to match project financing needsbull In order to reduce loan duration loan can be repaid before matured For example after a Toll

Road is operated and generate cash flow project owner can issue bonds (bonds financing) torepay the loan (bank financing)

Syndication

Loan structuring

Benefits of syndicationbull Commitment to complete the projecbull Self-financing during construction and operational phasebull Compliance with Banks and related parties requirements in projects financing amp completion

Support from Investee

| 12

Bank Mandirirsquos contribution to infrastructure financing

ISSUES amp SUPPORT NEEDED

Limited BMPK (Legal Lending Limit) BMPK especially for BUMN Karya is almost full Current BMPK availability cannot support funding

needs for RPJMN 2015-2019BMPK

Project Turn Key

SUPPORT NEEDEDISSUES

Dana TalanganTanah (DTT)

Liquidity

Missmatch FundingShort term source of fund (3rd party funding lt 1 yr) isused to finance long term loan (gt 10 yr)

Loan to Funding Ratio (LFR) calculation have notincluded wholasale funding

DTT repayment is delayed High leveraging could cause cash flow problem

Project is paid on completion (2-3 years for TollRoad)

High leveraging could cause cash flow problem

Alternative infrastructure financing apart from BankFinancing

Encourage BPJS and Dana Haji (long term funding) tosupport infrastructre financing

Wholesale funding is included in LFR calculation

DTT repayment should be paid on schedule

Reliable source of financing

BA

NK

SD

EB

TO

R

| 13

The Next Step for Indonesiarsquos Infrastructure Financing

ALTERNATIVE FINANCING ROADMAP FOR INDONESIAS INFRASTRUCTURE

Indonesia Regional Global

Alternative methods of financing has emerged to support governments development plan via infrastructure fundingand provide the solution for corporations to fulfill their funding requirements and to expand their businesses

Domestic Securitization

Domestic IDR Bonds

Domestic Project Bonds

Cross-Border Securitization

Global IDR Bonds

Global Project Bonds

THE PASTBefore 2017

THE BREAKTHROUGH2017

THE FUTURE2018 onwards

Global IDR Bonds

Debut Issuances in 2017

1 Future Revenue Backed Securities -Domestic KIK-EBA

2 Project Bonds

3 Global IDR Bonds

Our Vision

Global Equity Offering Global Equity OfferingGlobal Equity Offering

Direct Investment

| 14

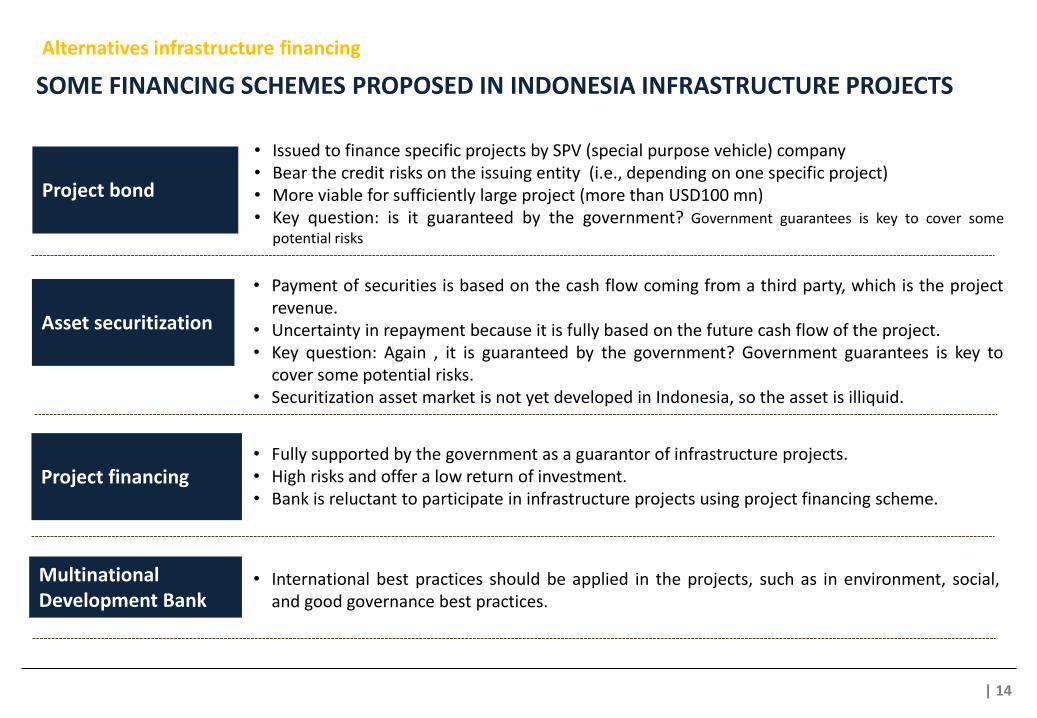

Project bond

bull Issued to finance specific projects by SPV (special purpose vehicle) companybull Bear the credit risks on the issuing entity (ie depending on one specific project)bull More viable for sufficiently large project (more than USD100 mn)bull Key question is it guaranteed by the government Government guarantees is key to cover some

potential risks

bull Fully supported by the government as a guarantor of infrastructure projectsbull High risks and offer a low return of investmentbull Bank is reluctant to participate in infrastructure projects using project financing scheme

bull Payment of securities is based on the cash flow coming from a third party which is the projectrevenue

bull Uncertainty in repayment because it is fully based on the future cash flow of the projectbull Key question Again it is guaranteed by the government Government guarantees is key to

cover some potential risksbull Securitization asset market is not yet developed in Indonesia so the asset is illiquid

Project financing

Multinational Development Bank

bull International best practices should be applied in the projects such as in environment socialand good governance best practices

Asset securitization

SOME FINANCING SCHEMES PROPOSED IN INDONESIA INFRASTRUCTURE PROJECTS

Alternatives infrastructure financing

| 15

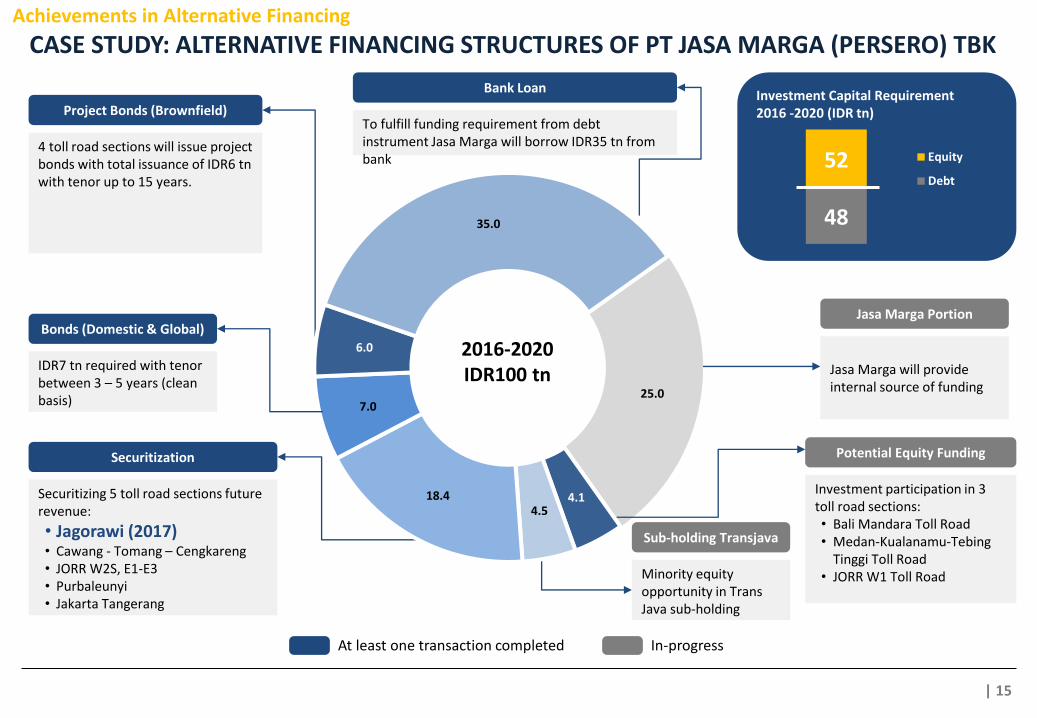

250

4145

184

70

60

350

Achievements in Alternative Financing

CASE STUDY ALTERNATIVE FINANCING STRUCTURES OF PT JASA MARGA (PERSERO) TBK

Investment Capital Requirement 2016 -2020 (IDR tn)

48

52 Equity

Debt

2016-2020IDR100 tn

Jasa Marga Portion

Jasa Marga will provide internal source of funding

Potential Equity Funding

Investment participation in 3 toll road sectionsbull Bali Mandara Toll Roadbull Medan-Kualanamu-Tebing

Tinggi Toll Roadbull JORR W1 Toll Road

Sub-holding Transjava

Minority equity opportunity in Trans Java sub-holding

Securitization

Securitizing 5 toll road sections future revenue

bull Jagorawi (2017)bull Cawang - Tomang ndash Cengkarengbull JORR W2S E1-E3bull Purbaleunyibull Jakarta Tangerang

Bonds (Domestic amp Global)

IDR7 tn required with tenor between 3 ndash 5 years (clean basis)

Project Bonds (Brownfield)

4 toll road sections will issue project bonds with total issuance of IDR6 tnwith tenor up to 15 years

Bank Loan

To fulfill funding requirement from debt instrument Jasa Marga will borrow IDR35 tn from bank

At least one transaction completed In-progress

| 16

Achievements in Alternative Financing

2017 MILESTONES FOR INNOVATIVE INFRASTRUCTURE FINANCING

InvestmentStructure

Kontrak Investasi KolektifEfek Beragun Aset (KIK EBA)

Underlying Financial Asset

Future Revenue of JagorawiToll Road

Size Rp185 tn

Tenor 5 years

Return 84

Rating idAAA

InvestmentStructure

Project Bonds

Size Rp15 tn

TenorCoupon

bull Series A 3 years 745bull Series B 5 years 775bull Series C 7 years 830bull Series D 10 years 870bull Series E 12 years 885

Rating idAAA

InvestmentStructure

Global IDR Bonds

Format 144A Reg S

Size Rp4 tn

Tenor 3 years

Coupon 75

Rating Baa3 (Moodyrsquos) BB+ (SampP)

bull IDR 4 tn issue

bull IDR 15 tn orderbook

bull 38x oversubscription

bull gt64 accounts

bull 375 bps tightening from

bull initial price guidance

bull IDR 185 tn issue

bull IDR 51 tn orderbook

bull 28x oversubscription

bull idAAA rating ndash above Jasa

Marga Consolidated (idAA)

bull IDR 15 tn issue

bull idAAA rating ndash above Jasa

Marga Consolidated (idAA)

Securitization Project Bonds Global IDR Bonds

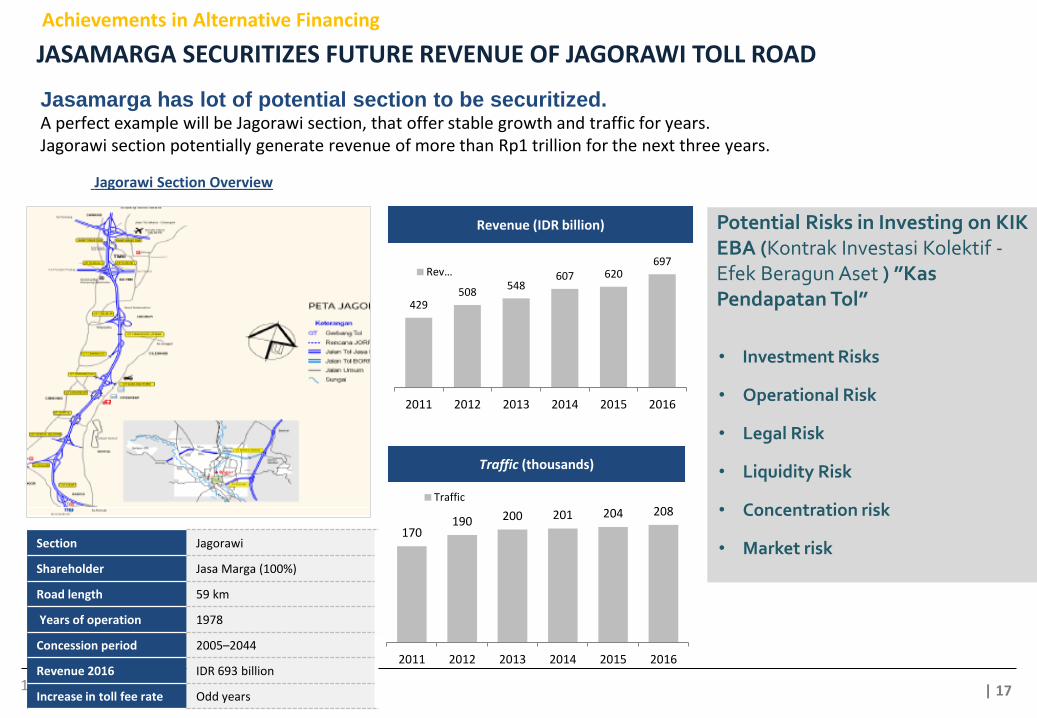

| 1717

Jagorawi Section Overview

Section Jagorawi

Shareholder Jasa Marga (100)

Road length 59 km

Years of operation 1978

Concession period 2005ndash2044

Revenue 2016 IDR 693 billion

Increase in toll fee rate Odd years

Jasamarga has lot of potential section to be securitized A perfect example will be Jagorawi section that offer stable growth and traffic for yearsJagorawi section potentially generate revenue of more than Rp1 trillion for the next three years

429508

548607 620

697

2011 2012 2013 2014 2015 2016

Revhellip

Revenue (IDR billion)

Traffic (thousands)

170190 200 201 204 208

2011 2012 2013 2014 2015 2016

Traffic

JASAMARGA SECURITIZES FUTURE REVENUE OF JAGORAWI TOLL ROAD

bull Investment Risks

bull Operational Risk

bull Legal Risk

bull Liquidity Risk

bull Concentration risk

bull Market risk

Potential Risks in Investing on KIK EBA (Kontrak Investasi Kolektif -Efek Beragun Aset ) rdquoKas Pendapatan Tolrdquo

Achievements in Alternative Financing

| 18

18

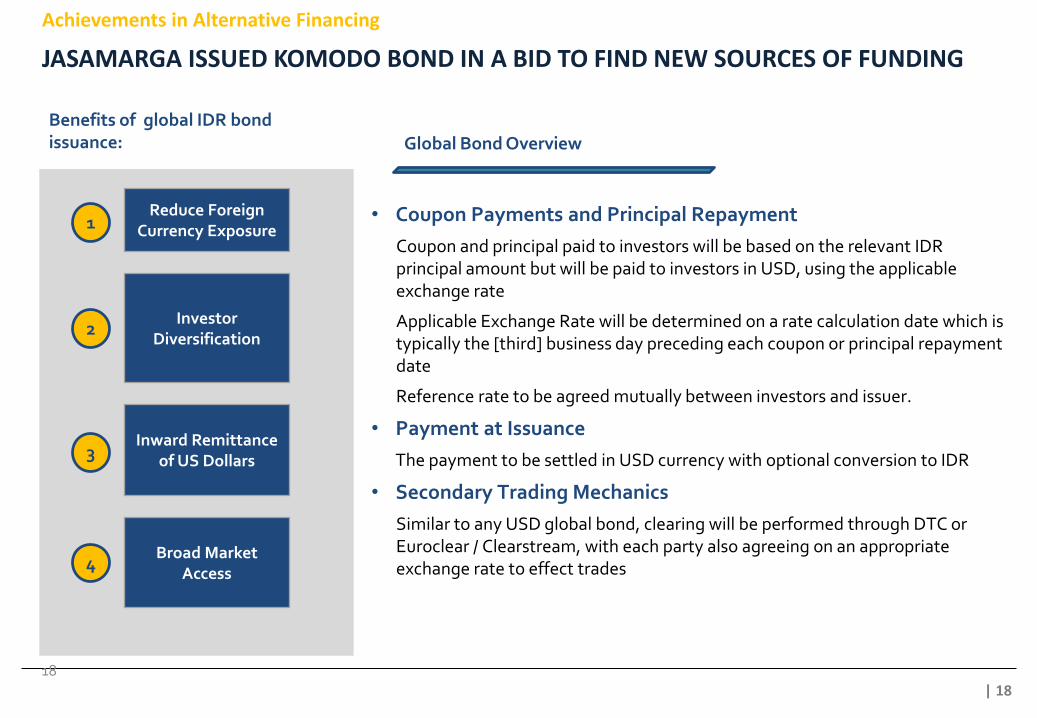

Reduce Foreign Currency Exposure

Investor Diversification

Inward Remittance of US Dollars

Broad Market Access

Benefits of global IDR bond issuance

1

2

3

4

JASAMARGA ISSUED KOMODO BOND IN A BID TO FIND NEW SOURCES OF FUNDING

bull Coupon Payments and Principal Repayment

Coupon and principal paid to investors will be based on the relevant IDR principal amount but will be paid to investors in USD using the applicable exchange rate

Applicable Exchange Rate will be determined on a rate calculation date which is typically the [third] business day preceding each coupon or principal repayment date

Reference rate to be agreed mutually between investors and issuer

bull Payment at Issuance

The payment to be settled in USD currency with optional conversion to IDR

bull Secondary Trading Mechanics

Similar to any USD global bond clearing will be performed through DTC or Euroclear Clearstream with each party also agreeing on an appropriate exchange rate to effect trades

Global Bond Overview

Achievements in Alternative Financing

| 2

Indonesiarsquos Development Plan

THE GOVERNMENT HAS TARGETED SOME HIGH INDICATORS IN THE RPJMN 2015-2019

Increase economic growth with strong and qualified fundamental basis

8Economic growth

Rp7197 mnGDP per capita

35Inflation

5-6Poverty rate

16 Tax ratio

4-5 Open unemployment rate

Increase competitiveness

Improving human quality in including through mental development

Harness and restore our potential in the maritime and marine sector

Reduce the inequality between regions

Restoring environmental damages

Advancing the society of life

Economic growth increase from 51 in 2014 to 8 by 2019

Increase GPD per capita from Rp4332 million in 2014 to Rp7197 million by 2019

Decrease inflation rate to 35 by 2019 from 73 in 2014

Poverty rate decrease to 5-6 by 2019 from 11 in 2014

Increase tax ratio to 16 by 2019 from 11 in 2014

Decrease open un-employment rate to 4-5 from 6 in 2014

Development Targets for RPJMN 2015 - 2019

Quantitative Targets for 2019

| 3

Indonesiarsquos Development Plan

THE RPJMN 2015 -2019 INCLUDES EXTENSIVE INFRASTRUCTURE DEVELOPMENT

Infrastructure Development to improve connectivity and reduce logistic cost

| 4

FINANCIAL SUPPORT REMAINS TO BE A BIGGEST PROBLEM

10

00

73

3

59

1

50

7

45

1

40

3

32

8

28

0

22

6

14

4

86

47

Elec

tric

ity

Ro

ad

Po

rt

Oil

and

Gas

Wat

er R

eso

urc

es

Cle

an W

ater

an

d S

anit

atio

n

Ho

usi

ng

Info

rmat

ion

amp T

ech

no

logy

Rai

lway

Air

po

rt

Urb

an T

ran

spo

rtat

ion

Lan

d T

ran

spo

rtat

ion

Sources KPPIP and Bappenas

616

784

3557

4734

308

Planning

Procurement

PPA (Power PurchaseAgreement)

Construction

Commercial Operation

8

18

11

40

23 Permit Issue

Financing Issue

Planning and PreparationIssue

Land Acquisition issue

Construction Issue

The progress of infrastructure projects (as of Dec 2017 in IDR Trillion)

Regulation

Sub-infra Total PSN Current Progress (IDR Trillion) per Dec 2017 (Cummulative)

Completed Construction Bidding Process Preparation Cancelled

Inpres 32016

(225 PSN + 1

Program) amp Perpres No582017 (245 PSN + 2

program)

Road 7064 142 3037 452 3433 0

Railway 6241 1866 4375

Airport 305 119 178 08

Seaport 1326 120 23 1182 01

Technology (ICT)

102 61 41

Dam 637 62 254 322

HousingWater amp Sanitation

861 45 11 805

Sea Wall 24000 24

Energy 12567 12 3212 6444 2899 004

Agri amp Fishery 02 01 01

Irrigation 37 37

Economic Zone 3880 3016 864

Smelter 904 799 105

National Border 09 09

Electricity 10359 288 4530 4897 644

Aircraft Industry

201 201

Total 44521 754 17083 11804 14870 10

Infrastructure total spending plan by type (2015-2019) (in Tn)

The progress of electricity projects 35 GW as of November 2017 (in Mega Watt) The obstacles of infrastructure development

Progress of infrastructure development and financing

| 5

Infrastructure financing

SUPPORT OF APBN IS LIMITED BY 3 BUDGET DEFICIT RULE

Government spending on infrastructureGOVERNMENT SPENDING ON INFRASTRUTURE

Sources Nota Keuangan and our estimation

00

05

10

15

20

25

30

35

0

100

200

300

400

500

2011 2012 2013 2014 2015 2016 2017F 2018F

Infrastructure Spending

Infrastructure (Rp tn)

Infrastructure to GDP ()-RHS

31-Dec-16 29-Dec-17Net buy(Sell)

2017 2016 2015

Bank 3995 4916 9210 269 631

Bank Indonesia

1579 1418 -161 78 187

Mutual Fund 857 1040 183 241 158

Insurance 2382 1508 -874 666 21

Foreign 6658 8362 17035 1073 972

Pension Fund

873 1981 1108 374 65

Retail 578 598 2 152 121

Others 1048 1175 127 261 174

Total 17733 20998 3265 3114 2519

Ownership of Government Bond

17

40

12

24

13

17

11

05

09

13

01

16

07

13

18

23

23 25 24 26

00

05

10

15

20

25

30

35

40

45

-100

0

100

200

300

400

500

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

of GDPRp tn

OtherNon Debt-Nett

External Loan - Nett

Goct Securites - Nett

Government bond is becoming the main source of budget deficit

| 6

Infrastructure financing from bank loans

BANKS ARE STILL DEALING WITH STRUCTURAL PROBLEMS

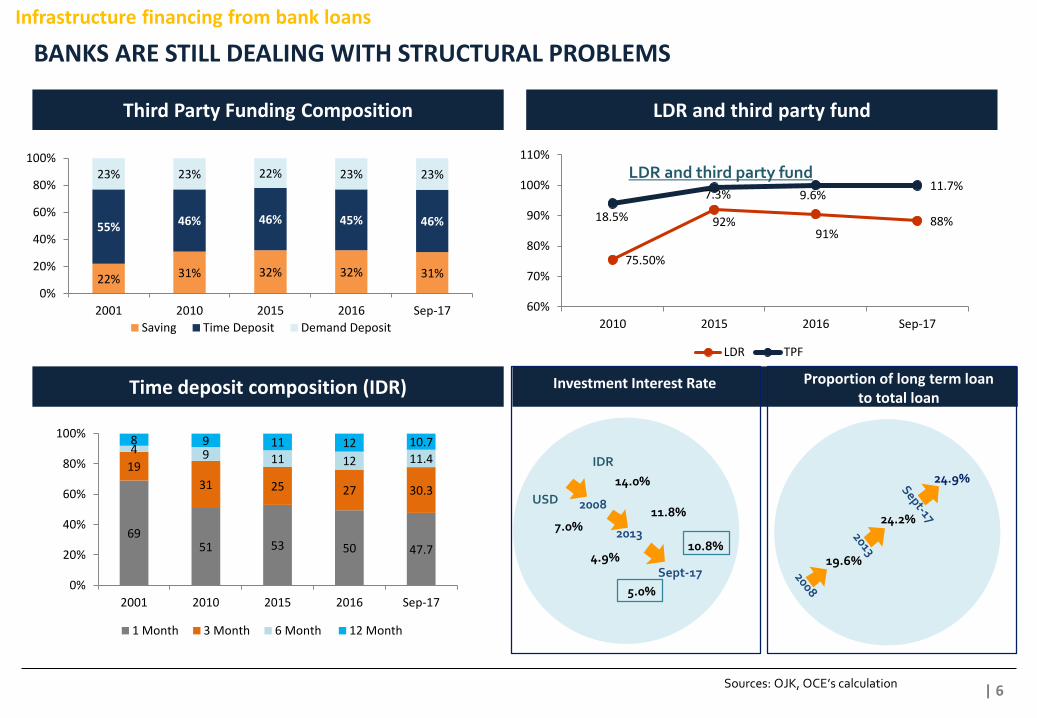

LDR and third party fund

Sources OJK OCErsquos calculation

22 31 32 32 31

55 46 46 45 46

23 23 22 23 23

0

20

40

60

80

100

2001 2010 2015 2016 Sep-17

Saving Time Deposit Demand Deposit

6951 53 50 477

19

31 25 27 303

4 9 11 12 114

8 9 11 12 107

0

20

40

60

80

100

2001 2010 2015 2016 Sep-17

1 Month 3 Month 6 Month 12 Month

7550

9291

88185

73 96117

60

70

80

90

100

110

2010 2015 2016 Sep-17

LDR TPF

Third Party Funding Composition LDR and third party fund

Time deposit composition (IDR)

IDR

USD 2008

140

702013

118

49Sept-17

108

50

Investment Interest Rate

196

249

242

Proportion of long term loan to total loan

| 7Offsite Discussion Material | Securitization

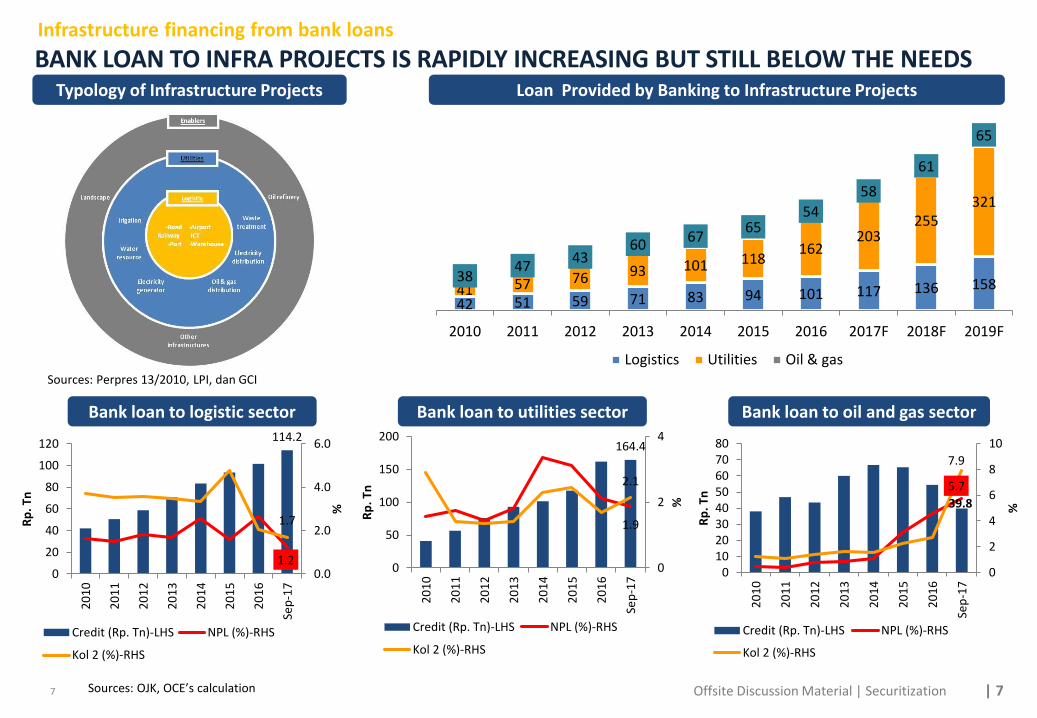

BANK LOAN TO INFRA PROJECTS IS RAPIDLY INCREASING BUT STILL BELOW THE NEEDS

7

Sources Perpres 132010 LPI dan GCI

Sources OJK OCErsquos calculation

1142

12

17

00

20

40

60

0

20

40

60

80

100

120

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

1644

19

21

0

2

4

0

50

100

150

2002

01

0

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

398

57

79

0

2

4

6

8

10

01020304050607080

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

42 51 59 71 83 94 101 117 136 15841 57 76 93 101 118162

203255

321

3847

4360

6765

54

58

61

65

2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F

Logistics Utilities Oil amp gas

Loan Provided by Banking to Infrastructure ProjectsTypology of Infrastructure Projects

Bank loan to logistic sector Bank loan to oil and gas sectorBank loan to utilities sector

Infrastructure financing from bank loans

| 8

Bank Mandirirsquos contribution to infrastructure financing

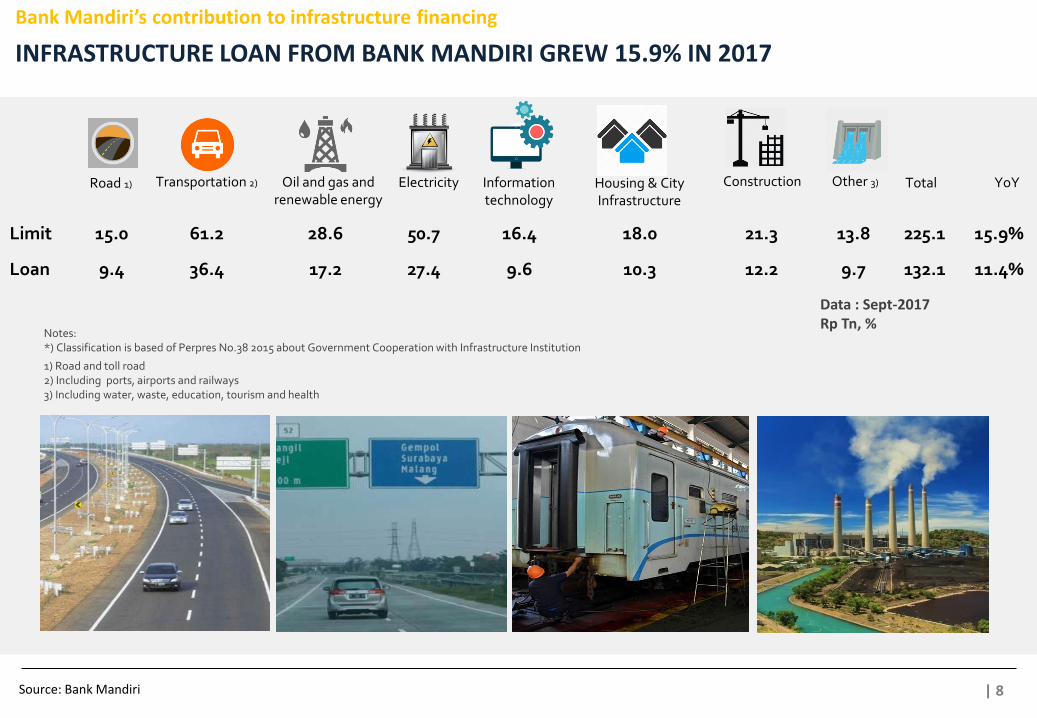

INFRASTRUCTURE LOAN FROM BANK MANDIRI GREW 159 IN 2017

Notes) Classification is based of Perpres No38 2015 about Government Cooperation with Infrastructure Institution

1) Road and toll road2) Including ports airports and railways3) Including water waste education tourism and health

Limit 150 612 286 507 164 180 213 138 2251 159

Loan 94 364 172 274 96 103 122 97 1321 114

Road 1) Transportation 2) Oil and gas and renewable energy

Electricity Information technology

Construction Other 3) Total YoYHousing amp City Infrastructure

Data Sept-2017Rp Tn

Source Bank Mandiri

| 9

Bank Mandirirsquos contribution to infrastructure financing

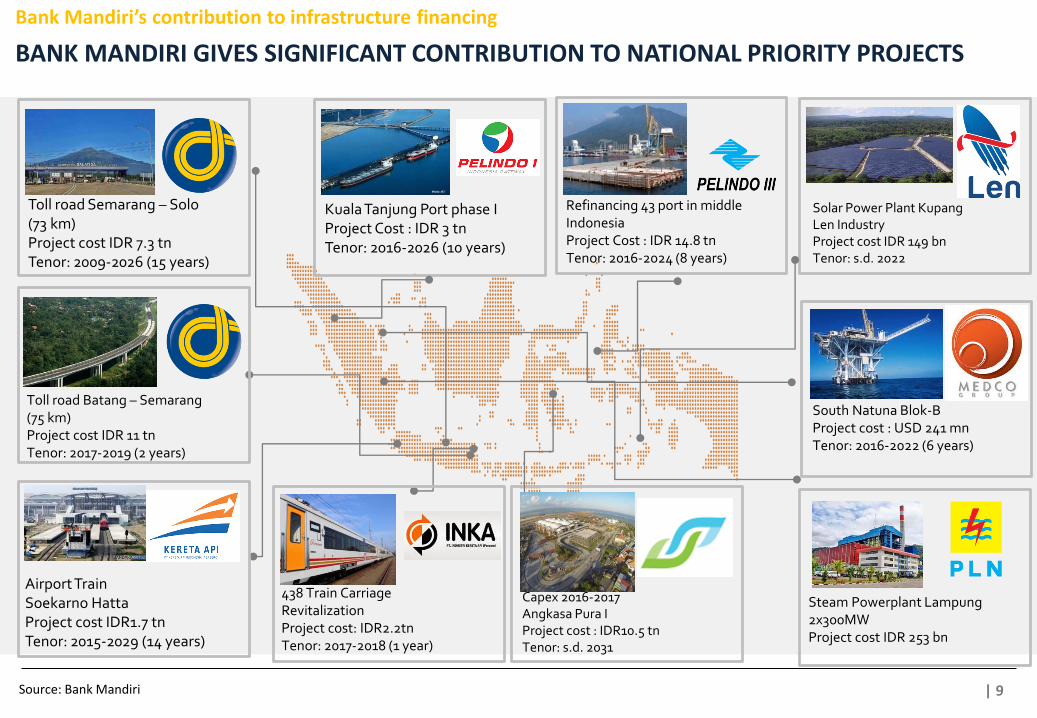

BANK MANDIRI GIVES SIGNIFICANT CONTRIBUTION TO NATIONAL PRIORITY PROJECTS

Refinancing 43 port in middle IndonesiaProject Cost IDR 148 tnTenor 2016-2024 (8 years)

Solar Power Plant Kupang Len IndustryProject cost IDR 149 bnTenor sd 2022

Capex 2016-2017Angkasa Pura IProject cost IDR105 tnTenor sd 2031

438 Train Carriage RevitalizationProject cost IDR22tnTenor 2017-2018 (1 year)

Toll road Semarang ndash Solo (73 km)Project cost IDR 73 tnTenor 2009-2026 (15 years)

Source Bank Mandiri

South Natuna Blok-BProject cost USD 241 mnTenor 2016-2022 (6 years)

Steam Powerplant Lampung 2x300MWProject cost IDR 253 bn

Toll road Batang ndash Semarang(75 km)Project cost IDR 11 tnTenor 2017-2019 (2 years)

Airport TrainSoekarno HattaProject cost IDR17 tnTenor 2015-2029 (14 years)

Kuala Tanjung Port phase IProject Cost IDR 3 tnTenor 2016-2026 (10 years)

| 10

Bank Mandirirsquos contribution to infrastructure financing

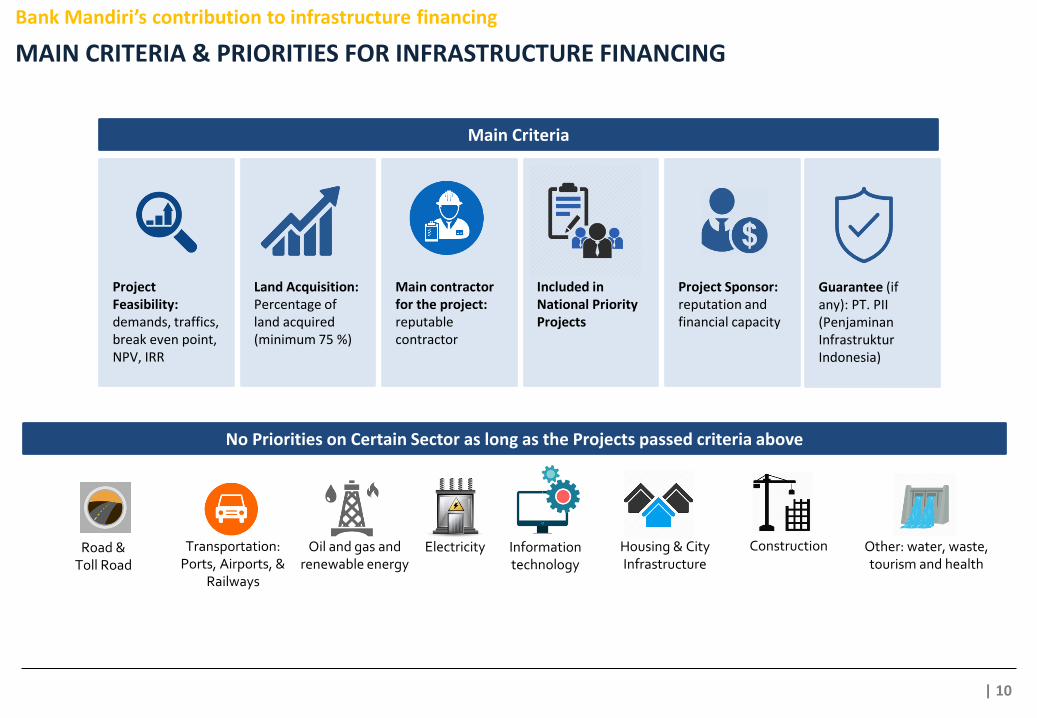

MAIN CRITERIA amp PRIORITIES FOR INFRASTRUCTURE FINANCING

Included in National Priority Projects

Project Feasibility demands traffics break even point NPV IRR

Land Acquisition Percentage of land acquired (minimum 75 )

Main contractor for the project reputable contractor

Project Sponsor reputation and financial capacity

Main Criteria

No Priorities on Certain Sector as long as the Projects passed criteria above

Guarantee (if any) PT PII (PenjaminanInfrastrukturIndonesia)

Road amp Toll Road

TransportationPorts Airports amp

Railways

Oil and gas and renewable energy

Electricity Information technology

ConstructionHousing amp City Infrastructure

Other water waste tourism and health

| 11

Bank Mandirirsquos contribution to infrastructure financing

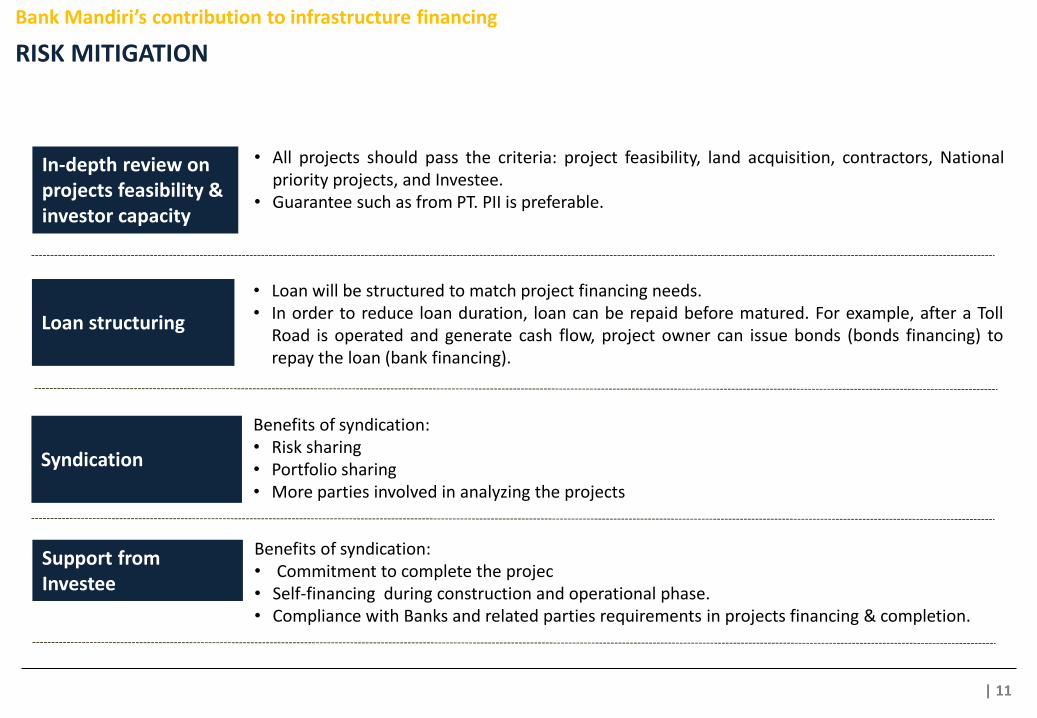

RISK MITIGATION

In-depth review on projects feasibility amp investor capacity

bull All projects should pass the criteria project feasibility land acquisition contractors Nationalpriority projects and Investee

bull Guarantee such as from PT PII is preferable

Benefits of syndicationbull Risk sharingbull Portfolio sharingbull More parties involved in analyzing the projects

bull Loan will be structured to match project financing needsbull In order to reduce loan duration loan can be repaid before matured For example after a Toll

Road is operated and generate cash flow project owner can issue bonds (bonds financing) torepay the loan (bank financing)

Syndication

Loan structuring

Benefits of syndicationbull Commitment to complete the projecbull Self-financing during construction and operational phasebull Compliance with Banks and related parties requirements in projects financing amp completion

Support from Investee

| 12

Bank Mandirirsquos contribution to infrastructure financing

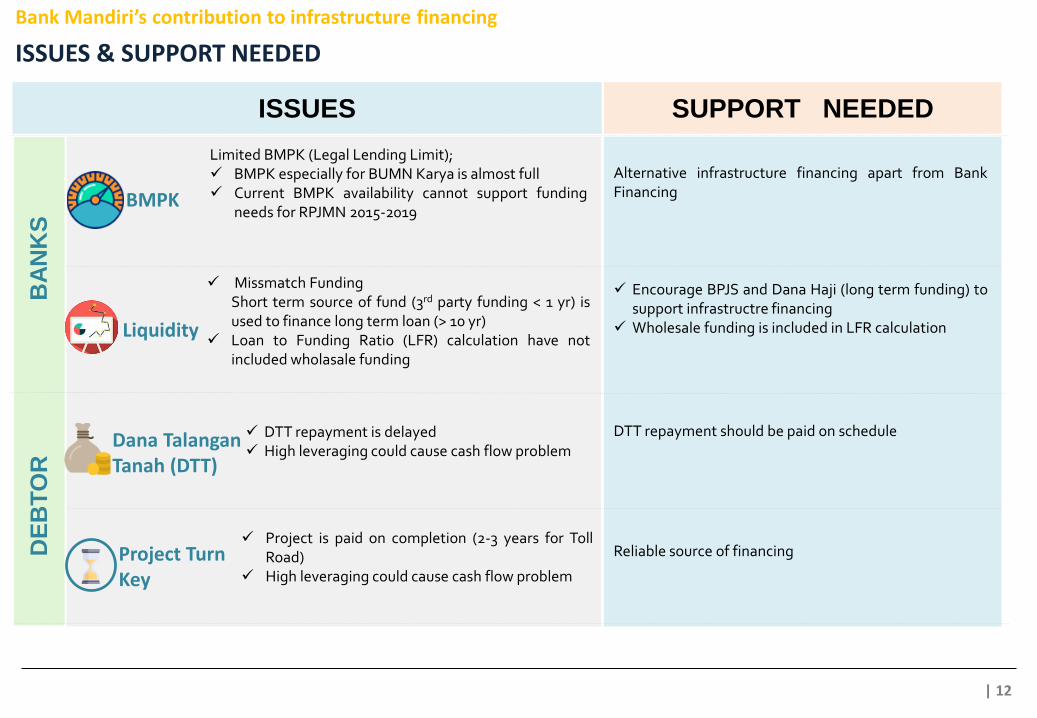

ISSUES amp SUPPORT NEEDED

Limited BMPK (Legal Lending Limit) BMPK especially for BUMN Karya is almost full Current BMPK availability cannot support funding

needs for RPJMN 2015-2019BMPK

Project Turn Key

SUPPORT NEEDEDISSUES

Dana TalanganTanah (DTT)

Liquidity

Missmatch FundingShort term source of fund (3rd party funding lt 1 yr) isused to finance long term loan (gt 10 yr)

Loan to Funding Ratio (LFR) calculation have notincluded wholasale funding

DTT repayment is delayed High leveraging could cause cash flow problem

Project is paid on completion (2-3 years for TollRoad)

High leveraging could cause cash flow problem

Alternative infrastructure financing apart from BankFinancing

Encourage BPJS and Dana Haji (long term funding) tosupport infrastructre financing

Wholesale funding is included in LFR calculation

DTT repayment should be paid on schedule

Reliable source of financing

BA

NK

SD

EB

TO

R

| 13

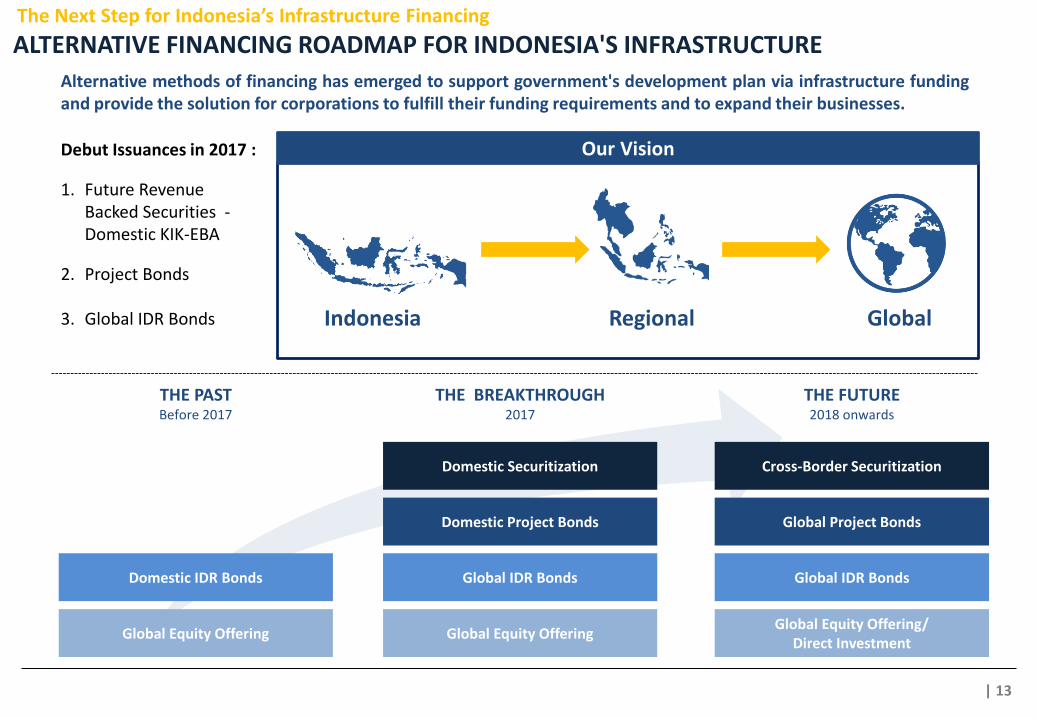

The Next Step for Indonesiarsquos Infrastructure Financing

ALTERNATIVE FINANCING ROADMAP FOR INDONESIAS INFRASTRUCTURE

Indonesia Regional Global

Alternative methods of financing has emerged to support governments development plan via infrastructure fundingand provide the solution for corporations to fulfill their funding requirements and to expand their businesses

Domestic Securitization

Domestic IDR Bonds

Domestic Project Bonds

Cross-Border Securitization

Global IDR Bonds

Global Project Bonds

THE PASTBefore 2017

THE BREAKTHROUGH2017

THE FUTURE2018 onwards

Global IDR Bonds

Debut Issuances in 2017

1 Future Revenue Backed Securities -Domestic KIK-EBA

2 Project Bonds

3 Global IDR Bonds

Our Vision

Global Equity Offering Global Equity OfferingGlobal Equity Offering

Direct Investment

| 14

Project bond

bull Issued to finance specific projects by SPV (special purpose vehicle) companybull Bear the credit risks on the issuing entity (ie depending on one specific project)bull More viable for sufficiently large project (more than USD100 mn)bull Key question is it guaranteed by the government Government guarantees is key to cover some

potential risks

bull Fully supported by the government as a guarantor of infrastructure projectsbull High risks and offer a low return of investmentbull Bank is reluctant to participate in infrastructure projects using project financing scheme

bull Payment of securities is based on the cash flow coming from a third party which is the projectrevenue

bull Uncertainty in repayment because it is fully based on the future cash flow of the projectbull Key question Again it is guaranteed by the government Government guarantees is key to

cover some potential risksbull Securitization asset market is not yet developed in Indonesia so the asset is illiquid

Project financing

Multinational Development Bank

bull International best practices should be applied in the projects such as in environment socialand good governance best practices

Asset securitization

SOME FINANCING SCHEMES PROPOSED IN INDONESIA INFRASTRUCTURE PROJECTS

Alternatives infrastructure financing

| 15

250

4145

184

70

60

350

Achievements in Alternative Financing

CASE STUDY ALTERNATIVE FINANCING STRUCTURES OF PT JASA MARGA (PERSERO) TBK

Investment Capital Requirement 2016 -2020 (IDR tn)

48

52 Equity

Debt

2016-2020IDR100 tn

Jasa Marga Portion

Jasa Marga will provide internal source of funding

Potential Equity Funding

Investment participation in 3 toll road sectionsbull Bali Mandara Toll Roadbull Medan-Kualanamu-Tebing

Tinggi Toll Roadbull JORR W1 Toll Road

Sub-holding Transjava

Minority equity opportunity in Trans Java sub-holding

Securitization

Securitizing 5 toll road sections future revenue

bull Jagorawi (2017)bull Cawang - Tomang ndash Cengkarengbull JORR W2S E1-E3bull Purbaleunyibull Jakarta Tangerang

Bonds (Domestic amp Global)

IDR7 tn required with tenor between 3 ndash 5 years (clean basis)

Project Bonds (Brownfield)

4 toll road sections will issue project bonds with total issuance of IDR6 tnwith tenor up to 15 years

Bank Loan

To fulfill funding requirement from debt instrument Jasa Marga will borrow IDR35 tn from bank

At least one transaction completed In-progress

| 16

Achievements in Alternative Financing

2017 MILESTONES FOR INNOVATIVE INFRASTRUCTURE FINANCING

InvestmentStructure

Kontrak Investasi KolektifEfek Beragun Aset (KIK EBA)

Underlying Financial Asset

Future Revenue of JagorawiToll Road

Size Rp185 tn

Tenor 5 years

Return 84

Rating idAAA

InvestmentStructure

Project Bonds

Size Rp15 tn

TenorCoupon

bull Series A 3 years 745bull Series B 5 years 775bull Series C 7 years 830bull Series D 10 years 870bull Series E 12 years 885

Rating idAAA

InvestmentStructure

Global IDR Bonds

Format 144A Reg S

Size Rp4 tn

Tenor 3 years

Coupon 75

Rating Baa3 (Moodyrsquos) BB+ (SampP)

bull IDR 4 tn issue

bull IDR 15 tn orderbook

bull 38x oversubscription

bull gt64 accounts

bull 375 bps tightening from

bull initial price guidance

bull IDR 185 tn issue

bull IDR 51 tn orderbook

bull 28x oversubscription

bull idAAA rating ndash above Jasa

Marga Consolidated (idAA)

bull IDR 15 tn issue

bull idAAA rating ndash above Jasa

Marga Consolidated (idAA)

Securitization Project Bonds Global IDR Bonds

| 1717

Jagorawi Section Overview

Section Jagorawi

Shareholder Jasa Marga (100)

Road length 59 km

Years of operation 1978

Concession period 2005ndash2044

Revenue 2016 IDR 693 billion

Increase in toll fee rate Odd years

Jasamarga has lot of potential section to be securitized A perfect example will be Jagorawi section that offer stable growth and traffic for yearsJagorawi section potentially generate revenue of more than Rp1 trillion for the next three years

429508

548607 620

697

2011 2012 2013 2014 2015 2016

Revhellip

Revenue (IDR billion)

Traffic (thousands)

170190 200 201 204 208

2011 2012 2013 2014 2015 2016

Traffic

JASAMARGA SECURITIZES FUTURE REVENUE OF JAGORAWI TOLL ROAD

bull Investment Risks

bull Operational Risk

bull Legal Risk

bull Liquidity Risk

bull Concentration risk

bull Market risk

Potential Risks in Investing on KIK EBA (Kontrak Investasi Kolektif -Efek Beragun Aset ) rdquoKas Pendapatan Tolrdquo

Achievements in Alternative Financing

| 18

18

Reduce Foreign Currency Exposure

Investor Diversification

Inward Remittance of US Dollars

Broad Market Access

Benefits of global IDR bond issuance

1

2

3

4

JASAMARGA ISSUED KOMODO BOND IN A BID TO FIND NEW SOURCES OF FUNDING

bull Coupon Payments and Principal Repayment

Coupon and principal paid to investors will be based on the relevant IDR principal amount but will be paid to investors in USD using the applicable exchange rate

Applicable Exchange Rate will be determined on a rate calculation date which is typically the [third] business day preceding each coupon or principal repayment date

Reference rate to be agreed mutually between investors and issuer

bull Payment at Issuance

The payment to be settled in USD currency with optional conversion to IDR

bull Secondary Trading Mechanics

Similar to any USD global bond clearing will be performed through DTC or Euroclear Clearstream with each party also agreeing on an appropriate exchange rate to effect trades

Global Bond Overview

Achievements in Alternative Financing

| 3

Indonesiarsquos Development Plan

THE RPJMN 2015 -2019 INCLUDES EXTENSIVE INFRASTRUCTURE DEVELOPMENT

Infrastructure Development to improve connectivity and reduce logistic cost

| 4

FINANCIAL SUPPORT REMAINS TO BE A BIGGEST PROBLEM

10

00

73

3

59

1

50

7

45

1

40

3

32

8

28

0

22

6

14

4

86

47

Elec

tric

ity

Ro

ad

Po

rt

Oil

and

Gas

Wat

er R

eso

urc

es

Cle

an W

ater

an

d S

anit

atio

n

Ho

usi

ng

Info

rmat

ion

amp T

ech

no

logy

Rai

lway

Air

po

rt

Urb

an T

ran

spo

rtat

ion

Lan

d T

ran

spo

rtat

ion

Sources KPPIP and Bappenas

616

784

3557

4734

308

Planning

Procurement

PPA (Power PurchaseAgreement)

Construction

Commercial Operation

8

18

11

40

23 Permit Issue

Financing Issue

Planning and PreparationIssue

Land Acquisition issue

Construction Issue

The progress of infrastructure projects (as of Dec 2017 in IDR Trillion)

Regulation

Sub-infra Total PSN Current Progress (IDR Trillion) per Dec 2017 (Cummulative)

Completed Construction Bidding Process Preparation Cancelled

Inpres 32016

(225 PSN + 1

Program) amp Perpres No582017 (245 PSN + 2

program)

Road 7064 142 3037 452 3433 0

Railway 6241 1866 4375

Airport 305 119 178 08

Seaport 1326 120 23 1182 01

Technology (ICT)

102 61 41

Dam 637 62 254 322

HousingWater amp Sanitation

861 45 11 805

Sea Wall 24000 24

Energy 12567 12 3212 6444 2899 004

Agri amp Fishery 02 01 01

Irrigation 37 37

Economic Zone 3880 3016 864

Smelter 904 799 105

National Border 09 09

Electricity 10359 288 4530 4897 644

Aircraft Industry

201 201

Total 44521 754 17083 11804 14870 10

Infrastructure total spending plan by type (2015-2019) (in Tn)

The progress of electricity projects 35 GW as of November 2017 (in Mega Watt) The obstacles of infrastructure development

Progress of infrastructure development and financing

| 5

Infrastructure financing

SUPPORT OF APBN IS LIMITED BY 3 BUDGET DEFICIT RULE

Government spending on infrastructureGOVERNMENT SPENDING ON INFRASTRUTURE

Sources Nota Keuangan and our estimation

00

05

10

15

20

25

30

35

0

100

200

300

400

500

2011 2012 2013 2014 2015 2016 2017F 2018F

Infrastructure Spending

Infrastructure (Rp tn)

Infrastructure to GDP ()-RHS

31-Dec-16 29-Dec-17Net buy(Sell)

2017 2016 2015

Bank 3995 4916 9210 269 631

Bank Indonesia

1579 1418 -161 78 187

Mutual Fund 857 1040 183 241 158

Insurance 2382 1508 -874 666 21

Foreign 6658 8362 17035 1073 972

Pension Fund

873 1981 1108 374 65

Retail 578 598 2 152 121

Others 1048 1175 127 261 174

Total 17733 20998 3265 3114 2519

Ownership of Government Bond

17

40

12

24

13

17

11

05

09

13

01

16

07

13

18

23

23 25 24 26

00

05

10

15

20

25

30

35

40

45

-100

0

100

200

300

400

500

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

of GDPRp tn

OtherNon Debt-Nett

External Loan - Nett

Goct Securites - Nett

Government bond is becoming the main source of budget deficit

| 6

Infrastructure financing from bank loans

BANKS ARE STILL DEALING WITH STRUCTURAL PROBLEMS

LDR and third party fund

Sources OJK OCErsquos calculation

22 31 32 32 31

55 46 46 45 46

23 23 22 23 23

0

20

40

60

80

100

2001 2010 2015 2016 Sep-17

Saving Time Deposit Demand Deposit

6951 53 50 477

19

31 25 27 303

4 9 11 12 114

8 9 11 12 107

0

20

40

60

80

100

2001 2010 2015 2016 Sep-17

1 Month 3 Month 6 Month 12 Month

7550

9291

88185

73 96117

60

70

80

90

100

110

2010 2015 2016 Sep-17

LDR TPF

Third Party Funding Composition LDR and third party fund

Time deposit composition (IDR)

IDR

USD 2008

140

702013

118

49Sept-17

108

50

Investment Interest Rate

196

249

242

Proportion of long term loan to total loan

| 7Offsite Discussion Material | Securitization

BANK LOAN TO INFRA PROJECTS IS RAPIDLY INCREASING BUT STILL BELOW THE NEEDS

7

Sources Perpres 132010 LPI dan GCI

Sources OJK OCErsquos calculation

1142

12

17

00

20

40

60

0

20

40

60

80

100

120

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

1644

19

21

0

2

4

0

50

100

150

2002

01

0

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

398

57

79

0

2

4

6

8

10

01020304050607080

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

42 51 59 71 83 94 101 117 136 15841 57 76 93 101 118162

203255

321

3847

4360

6765

54

58

61

65

2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F

Logistics Utilities Oil amp gas

Loan Provided by Banking to Infrastructure ProjectsTypology of Infrastructure Projects

Bank loan to logistic sector Bank loan to oil and gas sectorBank loan to utilities sector

Infrastructure financing from bank loans

| 8

Bank Mandirirsquos contribution to infrastructure financing

INFRASTRUCTURE LOAN FROM BANK MANDIRI GREW 159 IN 2017

Notes) Classification is based of Perpres No38 2015 about Government Cooperation with Infrastructure Institution

1) Road and toll road2) Including ports airports and railways3) Including water waste education tourism and health

Limit 150 612 286 507 164 180 213 138 2251 159

Loan 94 364 172 274 96 103 122 97 1321 114

Road 1) Transportation 2) Oil and gas and renewable energy

Electricity Information technology

Construction Other 3) Total YoYHousing amp City Infrastructure

Data Sept-2017Rp Tn

Source Bank Mandiri

| 9

Bank Mandirirsquos contribution to infrastructure financing

BANK MANDIRI GIVES SIGNIFICANT CONTRIBUTION TO NATIONAL PRIORITY PROJECTS

Refinancing 43 port in middle IndonesiaProject Cost IDR 148 tnTenor 2016-2024 (8 years)

Solar Power Plant Kupang Len IndustryProject cost IDR 149 bnTenor sd 2022

Capex 2016-2017Angkasa Pura IProject cost IDR105 tnTenor sd 2031

438 Train Carriage RevitalizationProject cost IDR22tnTenor 2017-2018 (1 year)

Toll road Semarang ndash Solo (73 km)Project cost IDR 73 tnTenor 2009-2026 (15 years)

Source Bank Mandiri

South Natuna Blok-BProject cost USD 241 mnTenor 2016-2022 (6 years)

Steam Powerplant Lampung 2x300MWProject cost IDR 253 bn

Toll road Batang ndash Semarang(75 km)Project cost IDR 11 tnTenor 2017-2019 (2 years)

Airport TrainSoekarno HattaProject cost IDR17 tnTenor 2015-2029 (14 years)

Kuala Tanjung Port phase IProject Cost IDR 3 tnTenor 2016-2026 (10 years)

| 10

Bank Mandirirsquos contribution to infrastructure financing

MAIN CRITERIA amp PRIORITIES FOR INFRASTRUCTURE FINANCING

Included in National Priority Projects

Project Feasibility demands traffics break even point NPV IRR

Land Acquisition Percentage of land acquired (minimum 75 )

Main contractor for the project reputable contractor

Project Sponsor reputation and financial capacity

Main Criteria

No Priorities on Certain Sector as long as the Projects passed criteria above

Guarantee (if any) PT PII (PenjaminanInfrastrukturIndonesia)

Road amp Toll Road

TransportationPorts Airports amp

Railways

Oil and gas and renewable energy

Electricity Information technology

ConstructionHousing amp City Infrastructure

Other water waste tourism and health

| 11

Bank Mandirirsquos contribution to infrastructure financing

RISK MITIGATION

In-depth review on projects feasibility amp investor capacity

bull All projects should pass the criteria project feasibility land acquisition contractors Nationalpriority projects and Investee

bull Guarantee such as from PT PII is preferable

Benefits of syndicationbull Risk sharingbull Portfolio sharingbull More parties involved in analyzing the projects

bull Loan will be structured to match project financing needsbull In order to reduce loan duration loan can be repaid before matured For example after a Toll

Road is operated and generate cash flow project owner can issue bonds (bonds financing) torepay the loan (bank financing)

Syndication

Loan structuring

Benefits of syndicationbull Commitment to complete the projecbull Self-financing during construction and operational phasebull Compliance with Banks and related parties requirements in projects financing amp completion

Support from Investee

| 12

Bank Mandirirsquos contribution to infrastructure financing

ISSUES amp SUPPORT NEEDED

Limited BMPK (Legal Lending Limit) BMPK especially for BUMN Karya is almost full Current BMPK availability cannot support funding

needs for RPJMN 2015-2019BMPK

Project Turn Key

SUPPORT NEEDEDISSUES

Dana TalanganTanah (DTT)

Liquidity

Missmatch FundingShort term source of fund (3rd party funding lt 1 yr) isused to finance long term loan (gt 10 yr)

Loan to Funding Ratio (LFR) calculation have notincluded wholasale funding

DTT repayment is delayed High leveraging could cause cash flow problem

Project is paid on completion (2-3 years for TollRoad)

High leveraging could cause cash flow problem

Alternative infrastructure financing apart from BankFinancing

Encourage BPJS and Dana Haji (long term funding) tosupport infrastructre financing

Wholesale funding is included in LFR calculation

DTT repayment should be paid on schedule

Reliable source of financing

BA

NK

SD

EB

TO

R

| 13

The Next Step for Indonesiarsquos Infrastructure Financing

ALTERNATIVE FINANCING ROADMAP FOR INDONESIAS INFRASTRUCTURE

Indonesia Regional Global

Alternative methods of financing has emerged to support governments development plan via infrastructure fundingand provide the solution for corporations to fulfill their funding requirements and to expand their businesses

Domestic Securitization

Domestic IDR Bonds

Domestic Project Bonds

Cross-Border Securitization

Global IDR Bonds

Global Project Bonds

THE PASTBefore 2017

THE BREAKTHROUGH2017

THE FUTURE2018 onwards

Global IDR Bonds

Debut Issuances in 2017

1 Future Revenue Backed Securities -Domestic KIK-EBA

2 Project Bonds

3 Global IDR Bonds

Our Vision

Global Equity Offering Global Equity OfferingGlobal Equity Offering

Direct Investment

| 14

Project bond

bull Issued to finance specific projects by SPV (special purpose vehicle) companybull Bear the credit risks on the issuing entity (ie depending on one specific project)bull More viable for sufficiently large project (more than USD100 mn)bull Key question is it guaranteed by the government Government guarantees is key to cover some

potential risks

bull Fully supported by the government as a guarantor of infrastructure projectsbull High risks and offer a low return of investmentbull Bank is reluctant to participate in infrastructure projects using project financing scheme

bull Payment of securities is based on the cash flow coming from a third party which is the projectrevenue

bull Uncertainty in repayment because it is fully based on the future cash flow of the projectbull Key question Again it is guaranteed by the government Government guarantees is key to

cover some potential risksbull Securitization asset market is not yet developed in Indonesia so the asset is illiquid

Project financing

Multinational Development Bank

bull International best practices should be applied in the projects such as in environment socialand good governance best practices

Asset securitization

SOME FINANCING SCHEMES PROPOSED IN INDONESIA INFRASTRUCTURE PROJECTS

Alternatives infrastructure financing

| 15

250

4145

184

70

60

350

Achievements in Alternative Financing

CASE STUDY ALTERNATIVE FINANCING STRUCTURES OF PT JASA MARGA (PERSERO) TBK

Investment Capital Requirement 2016 -2020 (IDR tn)

48

52 Equity

Debt

2016-2020IDR100 tn

Jasa Marga Portion

Jasa Marga will provide internal source of funding

Potential Equity Funding

Investment participation in 3 toll road sectionsbull Bali Mandara Toll Roadbull Medan-Kualanamu-Tebing

Tinggi Toll Roadbull JORR W1 Toll Road

Sub-holding Transjava

Minority equity opportunity in Trans Java sub-holding

Securitization

Securitizing 5 toll road sections future revenue

bull Jagorawi (2017)bull Cawang - Tomang ndash Cengkarengbull JORR W2S E1-E3bull Purbaleunyibull Jakarta Tangerang

Bonds (Domestic amp Global)

IDR7 tn required with tenor between 3 ndash 5 years (clean basis)

Project Bonds (Brownfield)

4 toll road sections will issue project bonds with total issuance of IDR6 tnwith tenor up to 15 years

Bank Loan

To fulfill funding requirement from debt instrument Jasa Marga will borrow IDR35 tn from bank

At least one transaction completed In-progress

| 16

Achievements in Alternative Financing

2017 MILESTONES FOR INNOVATIVE INFRASTRUCTURE FINANCING

InvestmentStructure

Kontrak Investasi KolektifEfek Beragun Aset (KIK EBA)

Underlying Financial Asset

Future Revenue of JagorawiToll Road

Size Rp185 tn

Tenor 5 years

Return 84

Rating idAAA

InvestmentStructure

Project Bonds

Size Rp15 tn

TenorCoupon

bull Series A 3 years 745bull Series B 5 years 775bull Series C 7 years 830bull Series D 10 years 870bull Series E 12 years 885

Rating idAAA

InvestmentStructure

Global IDR Bonds

Format 144A Reg S

Size Rp4 tn

Tenor 3 years

Coupon 75

Rating Baa3 (Moodyrsquos) BB+ (SampP)

bull IDR 4 tn issue

bull IDR 15 tn orderbook

bull 38x oversubscription

bull gt64 accounts

bull 375 bps tightening from

bull initial price guidance

bull IDR 185 tn issue

bull IDR 51 tn orderbook

bull 28x oversubscription

bull idAAA rating ndash above Jasa

Marga Consolidated (idAA)

bull IDR 15 tn issue

bull idAAA rating ndash above Jasa

Marga Consolidated (idAA)

Securitization Project Bonds Global IDR Bonds

| 1717

Jagorawi Section Overview

Section Jagorawi

Shareholder Jasa Marga (100)

Road length 59 km

Years of operation 1978

Concession period 2005ndash2044

Revenue 2016 IDR 693 billion

Increase in toll fee rate Odd years

Jasamarga has lot of potential section to be securitized A perfect example will be Jagorawi section that offer stable growth and traffic for yearsJagorawi section potentially generate revenue of more than Rp1 trillion for the next three years

429508

548607 620

697

2011 2012 2013 2014 2015 2016

Revhellip

Revenue (IDR billion)

Traffic (thousands)

170190 200 201 204 208

2011 2012 2013 2014 2015 2016

Traffic

JASAMARGA SECURITIZES FUTURE REVENUE OF JAGORAWI TOLL ROAD

bull Investment Risks

bull Operational Risk

bull Legal Risk

bull Liquidity Risk

bull Concentration risk

bull Market risk

Potential Risks in Investing on KIK EBA (Kontrak Investasi Kolektif -Efek Beragun Aset ) rdquoKas Pendapatan Tolrdquo

Achievements in Alternative Financing

| 18

18

Reduce Foreign Currency Exposure

Investor Diversification

Inward Remittance of US Dollars

Broad Market Access

Benefits of global IDR bond issuance

1

2

3

4

JASAMARGA ISSUED KOMODO BOND IN A BID TO FIND NEW SOURCES OF FUNDING

bull Coupon Payments and Principal Repayment

Coupon and principal paid to investors will be based on the relevant IDR principal amount but will be paid to investors in USD using the applicable exchange rate

Applicable Exchange Rate will be determined on a rate calculation date which is typically the [third] business day preceding each coupon or principal repayment date

Reference rate to be agreed mutually between investors and issuer

bull Payment at Issuance

The payment to be settled in USD currency with optional conversion to IDR

bull Secondary Trading Mechanics

Similar to any USD global bond clearing will be performed through DTC or Euroclear Clearstream with each party also agreeing on an appropriate exchange rate to effect trades

Global Bond Overview

Achievements in Alternative Financing

| 4

FINANCIAL SUPPORT REMAINS TO BE A BIGGEST PROBLEM

10

00

73

3

59

1

50

7

45

1

40

3

32

8

28

0

22

6

14

4

86

47

Elec

tric

ity

Ro

ad

Po

rt

Oil

and

Gas

Wat

er R

eso

urc

es

Cle

an W

ater

an

d S

anit

atio

n

Ho

usi

ng

Info

rmat

ion

amp T

ech

no

logy

Rai

lway

Air

po

rt

Urb

an T

ran

spo

rtat

ion

Lan

d T

ran

spo

rtat

ion

Sources KPPIP and Bappenas

616

784

3557

4734

308

Planning

Procurement

PPA (Power PurchaseAgreement)

Construction

Commercial Operation

8

18

11

40

23 Permit Issue

Financing Issue

Planning and PreparationIssue

Land Acquisition issue

Construction Issue

The progress of infrastructure projects (as of Dec 2017 in IDR Trillion)

Regulation

Sub-infra Total PSN Current Progress (IDR Trillion) per Dec 2017 (Cummulative)

Completed Construction Bidding Process Preparation Cancelled

Inpres 32016

(225 PSN + 1

Program) amp Perpres No582017 (245 PSN + 2

program)

Road 7064 142 3037 452 3433 0

Railway 6241 1866 4375

Airport 305 119 178 08

Seaport 1326 120 23 1182 01

Technology (ICT)

102 61 41

Dam 637 62 254 322

HousingWater amp Sanitation

861 45 11 805

Sea Wall 24000 24

Energy 12567 12 3212 6444 2899 004

Agri amp Fishery 02 01 01

Irrigation 37 37

Economic Zone 3880 3016 864

Smelter 904 799 105

National Border 09 09

Electricity 10359 288 4530 4897 644

Aircraft Industry

201 201

Total 44521 754 17083 11804 14870 10

Infrastructure total spending plan by type (2015-2019) (in Tn)

The progress of electricity projects 35 GW as of November 2017 (in Mega Watt) The obstacles of infrastructure development

Progress of infrastructure development and financing

| 5

Infrastructure financing

SUPPORT OF APBN IS LIMITED BY 3 BUDGET DEFICIT RULE

Government spending on infrastructureGOVERNMENT SPENDING ON INFRASTRUTURE

Sources Nota Keuangan and our estimation

00

05

10

15

20

25

30

35

0

100

200

300

400

500

2011 2012 2013 2014 2015 2016 2017F 2018F

Infrastructure Spending

Infrastructure (Rp tn)

Infrastructure to GDP ()-RHS

31-Dec-16 29-Dec-17Net buy(Sell)

2017 2016 2015

Bank 3995 4916 9210 269 631

Bank Indonesia

1579 1418 -161 78 187

Mutual Fund 857 1040 183 241 158

Insurance 2382 1508 -874 666 21

Foreign 6658 8362 17035 1073 972

Pension Fund

873 1981 1108 374 65

Retail 578 598 2 152 121

Others 1048 1175 127 261 174

Total 17733 20998 3265 3114 2519

Ownership of Government Bond

17

40

12

24

13

17

11

05

09

13

01

16

07

13

18

23

23 25 24 26

00

05

10

15

20

25

30

35

40

45

-100

0

100

200

300

400

500

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

of GDPRp tn

OtherNon Debt-Nett

External Loan - Nett

Goct Securites - Nett

Government bond is becoming the main source of budget deficit

| 6

Infrastructure financing from bank loans

BANKS ARE STILL DEALING WITH STRUCTURAL PROBLEMS

LDR and third party fund

Sources OJK OCErsquos calculation

22 31 32 32 31

55 46 46 45 46

23 23 22 23 23

0

20

40

60

80

100

2001 2010 2015 2016 Sep-17

Saving Time Deposit Demand Deposit

6951 53 50 477

19

31 25 27 303

4 9 11 12 114

8 9 11 12 107

0

20

40

60

80

100

2001 2010 2015 2016 Sep-17

1 Month 3 Month 6 Month 12 Month

7550

9291

88185

73 96117

60

70

80

90

100

110

2010 2015 2016 Sep-17

LDR TPF

Third Party Funding Composition LDR and third party fund

Time deposit composition (IDR)

IDR

USD 2008

140

702013

118

49Sept-17

108

50

Investment Interest Rate

196

249

242

Proportion of long term loan to total loan

| 7Offsite Discussion Material | Securitization

BANK LOAN TO INFRA PROJECTS IS RAPIDLY INCREASING BUT STILL BELOW THE NEEDS

7

Sources Perpres 132010 LPI dan GCI

Sources OJK OCErsquos calculation

1142

12

17

00

20

40

60

0

20

40

60

80

100

120

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

1644

19

21

0

2

4

0

50

100

150

2002

01

0

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

398

57

79

0

2

4

6

8

10

01020304050607080

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Sep

-17

Rp

Tn

Credit (Rp Tn)-LHS NPL ()-RHS

Kol 2 ()-RHS

42 51 59 71 83 94 101 117 136 15841 57 76 93 101 118162

203255

321

3847

4360

6765

54

58

61

65

2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F

Logistics Utilities Oil amp gas

Loan Provided by Banking to Infrastructure ProjectsTypology of Infrastructure Projects

Bank loan to logistic sector Bank loan to oil and gas sectorBank loan to utilities sector

Infrastructure financing from bank loans

| 8

Bank Mandirirsquos contribution to infrastructure financing

INFRASTRUCTURE LOAN FROM BANK MANDIRI GREW 159 IN 2017

Notes) Classification is based of Perpres No38 2015 about Government Cooperation with Infrastructure Institution

1) Road and toll road2) Including ports airports and railways3) Including water waste education tourism and health

Limit 150 612 286 507 164 180 213 138 2251 159

Loan 94 364 172 274 96 103 122 97 1321 114

Road 1) Transportation 2) Oil and gas and renewable energy

Electricity Information technology

Construction Other 3) Total YoYHousing amp City Infrastructure

Data Sept-2017Rp Tn

Source Bank Mandiri

| 9

Bank Mandirirsquos contribution to infrastructure financing

BANK MANDIRI GIVES SIGNIFICANT CONTRIBUTION TO NATIONAL PRIORITY PROJECTS

Refinancing 43 port in middle IndonesiaProject Cost IDR 148 tnTenor 2016-2024 (8 years)

Solar Power Plant Kupang Len IndustryProject cost IDR 149 bnTenor sd 2022

Capex 2016-2017Angkasa Pura IProject cost IDR105 tnTenor sd 2031

438 Train Carriage RevitalizationProject cost IDR22tnTenor 2017-2018 (1 year)

Toll road Semarang ndash Solo (73 km)Project cost IDR 73 tnTenor 2009-2026 (15 years)

Source Bank Mandiri

South Natuna Blok-BProject cost USD 241 mnTenor 2016-2022 (6 years)

Steam Powerplant Lampung 2x300MWProject cost IDR 253 bn

Toll road Batang ndash Semarang(75 km)Project cost IDR 11 tnTenor 2017-2019 (2 years)

Airport TrainSoekarno HattaProject cost IDR17 tnTenor 2015-2029 (14 years)

Kuala Tanjung Port phase IProject Cost IDR 3 tnTenor 2016-2026 (10 years)

| 10

Bank Mandirirsquos contribution to infrastructure financing

MAIN CRITERIA amp PRIORITIES FOR INFRASTRUCTURE FINANCING

Included in National Priority Projects

Project Feasibility demands traffics break even point NPV IRR

Land Acquisition Percentage of land acquired (minimum 75 )

Main contractor for the project reputable contractor

Project Sponsor reputation and financial capacity

Main Criteria

No Priorities on Certain Sector as long as the Projects passed criteria above

Guarantee (if any) PT PII (PenjaminanInfrastrukturIndonesia)

Road amp Toll Road

TransportationPorts Airports amp

Railways

Oil and gas and renewable energy

Electricity Information technology

ConstructionHousing amp City Infrastructure

Other water waste tourism and health

| 11

Bank Mandirirsquos contribution to infrastructure financing

RISK MITIGATION

In-depth review on projects feasibility amp investor capacity

bull All projects should pass the criteria project feasibility land acquisition contractors Nationalpriority projects and Investee

bull Guarantee such as from PT PII is preferable

Benefits of syndicationbull Risk sharingbull Portfolio sharingbull More parties involved in analyzing the projects

bull Loan will be structured to match project financing needsbull In order to reduce loan duration loan can be repaid before matured For example after a Toll

Road is operated and generate cash flow project owner can issue bonds (bonds financing) torepay the loan (bank financing)

Syndication

Loan structuring

Benefits of syndicationbull Commitment to complete the projecbull Self-financing during construction and operational phasebull Compliance with Banks and related parties requirements in projects financing amp completion

Support from Investee

| 12

Bank Mandirirsquos contribution to infrastructure financing

ISSUES amp SUPPORT NEEDED

Limited BMPK (Legal Lending Limit) BMPK especially for BUMN Karya is almost full Current BMPK availability cannot support funding

needs for RPJMN 2015-2019BMPK

Project Turn Key

SUPPORT NEEDEDISSUES

Dana TalanganTanah (DTT)

Liquidity

Missmatch FundingShort term source of fund (3rd party funding lt 1 yr) isused to finance long term loan (gt 10 yr)

Loan to Funding Ratio (LFR) calculation have notincluded wholasale funding

DTT repayment is delayed High leveraging could cause cash flow problem

Project is paid on completion (2-3 years for TollRoad)

High leveraging could cause cash flow problem

Alternative infrastructure financing apart from BankFinancing

Encourage BPJS and Dana Haji (long term funding) tosupport infrastructre financing

Wholesale funding is included in LFR calculation

DTT repayment should be paid on schedule

Reliable source of financing

BA

NK

SD

EB

TO

R

| 13

The Next Step for Indonesiarsquos Infrastructure Financing

ALTERNATIVE FINANCING ROADMAP FOR INDONESIAS INFRASTRUCTURE

Indonesia Regional Global

Alternative methods of financing has emerged to support governments development plan via infrastructure fundingand provide the solution for corporations to fulfill their funding requirements and to expand their businesses

Domestic Securitization

Domestic IDR Bonds

Domestic Project Bonds

Cross-Border Securitization

Global IDR Bonds

Global Project Bonds

THE PASTBefore 2017

THE BREAKTHROUGH2017

THE FUTURE2018 onwards

Global IDR Bonds

Debut Issuances in 2017

1 Future Revenue Backed Securities -Domestic KIK-EBA

2 Project Bonds

3 Global IDR Bonds

Our Vision

Global Equity Offering Global Equity OfferingGlobal Equity Offering

Direct Investment

| 14

Project bond

bull Issued to finance specific projects by SPV (special purpose vehicle) companybull Bear the credit risks on the issuing entity (ie depending on one specific project)bull More viable for sufficiently large project (more than USD100 mn)bull Key question is it guaranteed by the government Government guarantees is key to cover some

potential risks

bull Fully supported by the government as a guarantor of infrastructure projectsbull High risks and offer a low return of investmentbull Bank is reluctant to participate in infrastructure projects using project financing scheme

bull Payment of securities is based on the cash flow coming from a third party which is the projectrevenue

bull Uncertainty in repayment because it is fully based on the future cash flow of the projectbull Key question Again it is guaranteed by the government Government guarantees is key to

cover some potential risksbull Securitization asset market is not yet developed in Indonesia so the asset is illiquid

Project financing

Multinational Development Bank

bull International best practices should be applied in the projects such as in environment socialand good governance best practices

Asset securitization

SOME FINANCING SCHEMES PROPOSED IN INDONESIA INFRASTRUCTURE PROJECTS

Alternatives infrastructure financing

| 15

250

4145

184

70

60

350

Achievements in Alternative Financing

CASE STUDY ALTERNATIVE FINANCING STRUCTURES OF PT JASA MARGA (PERSERO) TBK

Investment Capital Requirement 2016 -2020 (IDR tn)

48

52 Equity

Debt

2016-2020IDR100 tn

Jasa Marga Portion

Jasa Marga will provide internal source of funding

Potential Equity Funding

Investment participation in 3 toll road sectionsbull Bali Mandara Toll Roadbull Medan-Kualanamu-Tebing

Tinggi Toll Roadbull JORR W1 Toll Road

Sub-holding Transjava

Minority equity opportunity in Trans Java sub-holding

Securitization

Securitizing 5 toll road sections future revenue

bull Jagorawi (2017)bull Cawang - Tomang ndash Cengkarengbull JORR W2S E1-E3bull Purbaleunyibull Jakarta Tangerang

Bonds (Domestic amp Global)

IDR7 tn required with tenor between 3 ndash 5 years (clean basis)

Project Bonds (Brownfield)

4 toll road sections will issue project bonds with total issuance of IDR6 tnwith tenor up to 15 years

Bank Loan

To fulfill funding requirement from debt instrument Jasa Marga will borrow IDR35 tn from bank

At least one transaction completed In-progress

| 16

Achievements in Alternative Financing

2017 MILESTONES FOR INNOVATIVE INFRASTRUCTURE FINANCING

InvestmentStructure

Kontrak Investasi KolektifEfek Beragun Aset (KIK EBA)

Underlying Financial Asset

Future Revenue of JagorawiToll Road

Size Rp185 tn

Tenor 5 years

Return 84

Rating idAAA

InvestmentStructure

Project Bonds

Size Rp15 tn

TenorCoupon

bull Series A 3 years 745bull Series B 5 years 775bull Series C 7 years 830bull Series D 10 years 870bull Series E 12 years 885

Rating idAAA

InvestmentStructure

Global IDR Bonds

Format 144A Reg S

Size Rp4 tn

Tenor 3 years

Coupon 75

Rating Baa3 (Moodyrsquos) BB+ (SampP)

bull IDR 4 tn issue

bull IDR 15 tn orderbook

bull 38x oversubscription

bull gt64 accounts

bull 375 bps tightening from

bull initial price guidance

bull IDR 185 tn issue

bull IDR 51 tn orderbook

bull 28x oversubscription

bull idAAA rating ndash above Jasa

Marga Consolidated (idAA)

bull IDR 15 tn issue

bull idAAA rating ndash above Jasa

Marga Consolidated (idAA)

Securitization Project Bonds Global IDR Bonds

| 1717

Jagorawi Section Overview

Section Jagorawi

Shareholder Jasa Marga (100)

Road length 59 km

Years of operation 1978

Concession period 2005ndash2044

Revenue 2016 IDR 693 billion

Increase in toll fee rate Odd years

Jasamarga has lot of potential section to be securitized A perfect example will be Jagorawi section that offer stable growth and traffic for yearsJagorawi section potentially generate revenue of more than Rp1 trillion for the next three years

429508

548607 620

697

2011 2012 2013 2014 2015 2016

Revhellip

Revenue (IDR billion)

Traffic (thousands)

170190 200 201 204 208

2011 2012 2013 2014 2015 2016

Traffic

JASAMARGA SECURITIZES FUTURE REVENUE OF JAGORAWI TOLL ROAD

bull Investment Risks

bull Operational Risk

bull Legal Risk

bull Liquidity Risk

bull Concentration risk

bull Market risk

Potential Risks in Investing on KIK EBA (Kontrak Investasi Kolektif -Efek Beragun Aset ) rdquoKas Pendapatan Tolrdquo

Achievements in Alternative Financing

| 18

18

Reduce Foreign Currency Exposure

Investor Diversification

Inward Remittance of US Dollars

Broad Market Access

Benefits of global IDR bond issuance

1

2

3

4

JASAMARGA ISSUED KOMODO BOND IN A BID TO FIND NEW SOURCES OF FUNDING

bull Coupon Payments and Principal Repayment

Coupon and principal paid to investors will be based on the relevant IDR principal amount but will be paid to investors in USD using the applicable exchange rate

Applicable Exchange Rate will be determined on a rate calculation date which is typically the [third] business day preceding each coupon or principal repayment date

Reference rate to be agreed mutually between investors and issuer

bull Payment at Issuance

The payment to be settled in USD currency with optional conversion to IDR

bull Secondary Trading Mechanics

Similar to any USD global bond clearing will be performed through DTC or Euroclear Clearstream with each party also agreeing on an appropriate exchange rate to effect trades

Global Bond Overview

Achievements in Alternative Financing

| 5

Infrastructure financing

SUPPORT OF APBN IS LIMITED BY 3 BUDGET DEFICIT RULE

Government spending on infrastructureGOVERNMENT SPENDING ON INFRASTRUTURE

Sources Nota Keuangan and our estimation

00

05

10

15

20

25

30

35

0

100

200

300

400

500

2011 2012 2013 2014 2015 2016 2017F 2018F

Infrastructure Spending

Infrastructure (Rp tn)

Infrastructure to GDP ()-RHS

31-Dec-16 29-Dec-17Net buy(Sell)

2017 2016 2015

Bank 3995 4916 9210 269 631

Bank Indonesia

1579 1418 -161 78 187

Mutual Fund 857 1040 183 241 158

Insurance 2382 1508 -874 666 21

Foreign 6658 8362 17035 1073 972

Pension Fund

873 1981 1108 374 65

Retail 578 598 2 152 121

Others 1048 1175 127 261 174

Total 17733 20998 3265 3114 2519

Ownership of Government Bond

17

40

12

24

13

17

11

05

09

13

01

16

07

13