opportunities and challenges royal london · royal london 20 june 2018 tim harris: deputy group...

TRANSCRIPT

LIFE & PENSIONS: OPPORTUNITIES AND CHALLENGES

ROYAL LONDON20 June 2018

Tim Harris: Deputy Group Chief Executive & Group Finance Director

Presentation to Willis Towers Watson Life2018 Conference:“Thriving, not striving, through times of change”

2

AGENDA

1. Introduction to Royal London

2. Recent developments

3. Current strategic projects

4. The future of our industry and Royal London’s contribution

3

INTRODUCTION TO ROYAL LONDONLIFE & PENSIONS: OPPORTUNITIES AND CHALLENGES

Why am I excited about the life and pensions industry?

• Customer purpose/social need

• Economic support for our policyholders and members:

(a) Protection - to cope with the financial consequences of undesirable events

(b) Wealth – building up wealth through pensions and savings

Our purpose is to help our policyholders make financial provision for the future, and to protect their finances when the unexpected happens

4

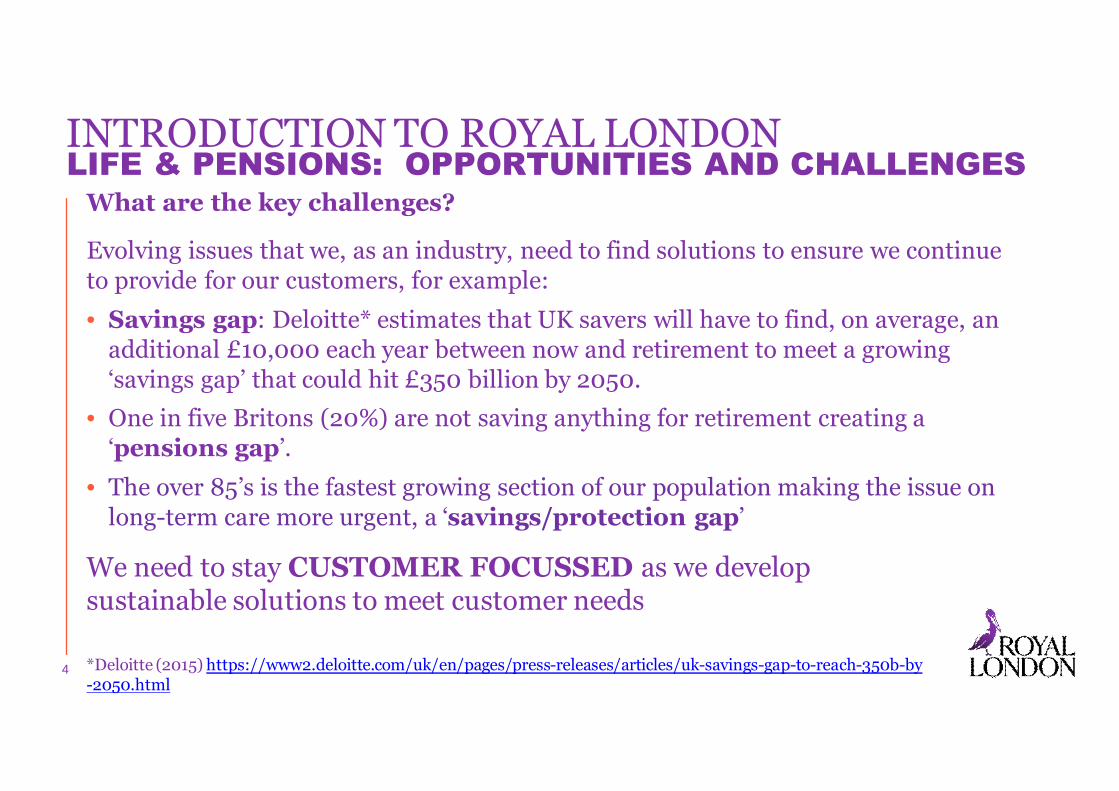

INTRODUCTION TO ROYAL LONDONLIFE & PENSIONS: OPPORTUNITIES AND CHALLENGES

What are the key challenges?

Evolving issues that we, as an industry, need to find solutions to ensure we continue to provide for our customers, for example:

• Savings gap: Deloitte* estimates that UK savers will have to find, on average, an additional £10,000 each year between now and retirement to meet a growing ‘savings gap’ that could hit £350 billion by 2050.

• One in five Britons (20%) are not saving anything for retirement creating a ‘pensions gap’.

• The over 85’s is the fastest growing section of our population making the issue on long-term care more urgent, a ‘savings/protection gap’

We need to stay CUSTOMER FOCUSSED as we develop sustainable solutions to meet customer needs

*Deloitte (2015) https://www2.deloitte.com/uk/en/pages/press-releases/articles/uk-savings-gap-to-reach-350b-by-2050.html

5

INTRODUCTION TO ROYAL LONDON

ROYAL LONDON Background

• Distinct through mutuality and number of policies we service

• Provide products to 8.8m policyholders, 1.3m of which are members

• Answerable to our members as opposed to shareholders

• Large volume of legacy business partly from past acquisitions

• Have 9 closed sub-funds and one open fund (RL Main Fund)

Royal London Vision:

We will hold uniquely positive relationships with our customers that make us the most trusted financial organisation

Be the most recommended provider in each of our chosen markets and this will tell us when we’ve been successful

ROYAL LONDON

6

INTRODUCTION TO ROYAL LONDONROYAL LONDON MARKET SHARE

Market Position

FY 2017Market Share

FY 2016 Market Share

Protection (UK Intermediary) 3rd 11.1% 11.7%

Protection (Ireland) 4th 16.1% 15.6%

Individual pensions 3rd 22.6% 19.9%

Income drawdown 1st 24.1% 23.3%

Workplace pensions 5th 10.5% 9.8%

Consumer Term 6th 2.4% 1.3%

Over 50s direct 2nd 19.5% 11.1%

Funeral plans * 46% 37%

RLPS gross flows 13th 2.2% 2.3%

*No market position quoted as industry data on volumes sold through other individual funeral providers is not publically available.

7

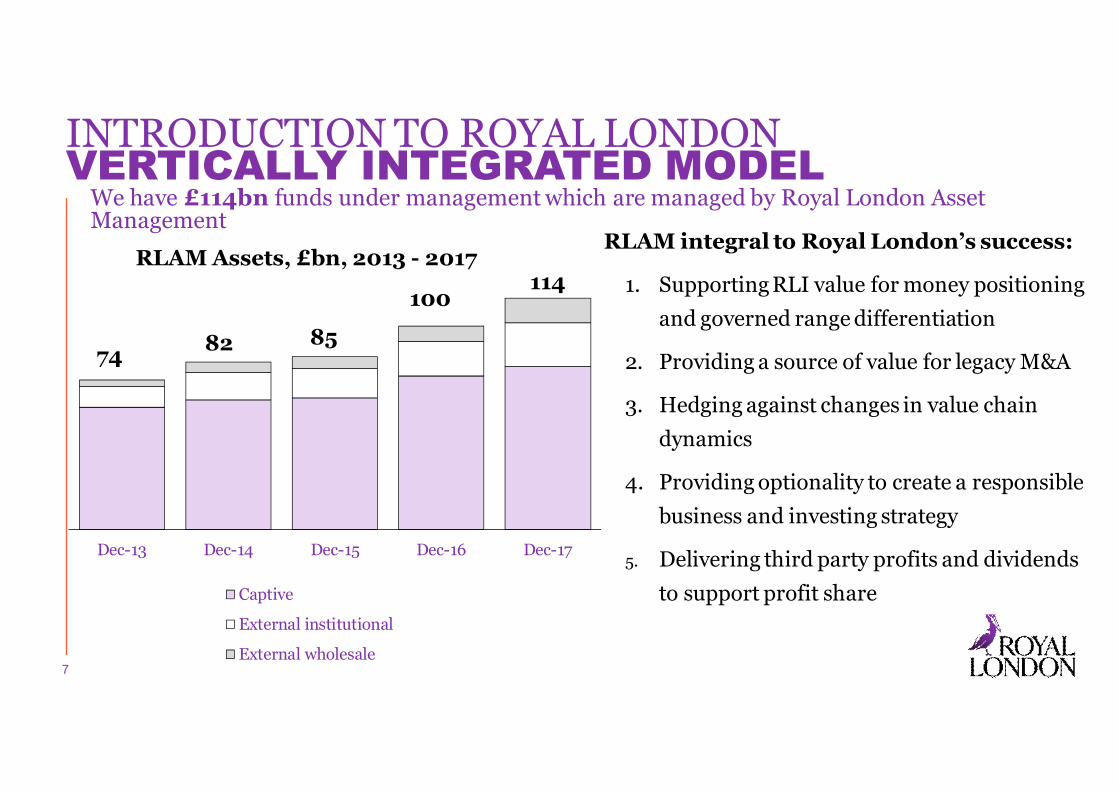

INTRODUCTION TO ROYAL LONDONVERTICALLY INTEGRATED MODEL

RLAM Assets, £bn, 2013 - 2017

74 82 85

100114

RLAM integral to Royal London’s success:

1. Supporting RLI value for money positioning and governed range differentiation

2. Providing a source of value for legacy M&A

3. Hedging against changes in value chain dynamics

4. Providing optionality to create a responsible business and investing strategy

5. Delivering third party profits and dividends to support profit share

Dec-13 Dec-14 Dec-15 Dec-16 Dec-17

Captive

External institutional

External wholesale

We have £114bn funds under management which are managed by Royal London Asset Management

8

RECENT DEVELOPMENTS AND STRATEGIC PROJECTS

Recent Developments

• Finance Transformation

• Accelerator

Current Strategic projects

• #ThinkBeyond: Pensions transformation

• Our Brexit Solution

• GAR Compromise

• ProfitShare development

9

RECENT DEVELOPMENTSFINANCE TRANSFORMATION

Like most firms we had to make changes to comply with SII but, sought to make a “virtue out of necessity” in setting the scope of our programme which included:

• New finance system (FSR)

• New actuarial model (MG-ALFA) including a strategic reporting solution (SRS)

• New risk reporting system (Archer)

Faster, more efficient, more controlled

Old Technology

New TechnologyIntegrated capital

modellingand strategic reporting

Cloud based general ledger

Old Technology

10

We can now meet SII requirements (from a standing start in 2014). However, we want it to be more than that.

NEXT FOCUS…. How can we use this technology to add value to our business and ultimately our customers? This technology will set us up for the longer term future.

ACTUARIAL FUTURE

• End reports produced automatically allowing top-down review (move from previous more bottom-up approach). Implemented for reporting and in development for other areas e.g. capital and WP management

• More controlled system for change

• Reduced time processing to allow our actuaries to add value to the businessdifferent ways e.g. strategic projects

RECENT DEVELOPMENTSFINANCE TRANSFORMATION

11

• New technology platform to support our Ascentric wrap business

• Live in April this year

• Will provide a better experience for customers through:

- More automation

- Simplified view of the client portfolio for advisors and clients

- Greater online functionality

• Provides a foundation of technology where we can thrive in a fast changing market and give us greater ability to control costs as we continue to grow as a business

• Lessons learned – but now positions us ahead of the pack

RECENT DEVELOPMENTS ACCELERATOR

12

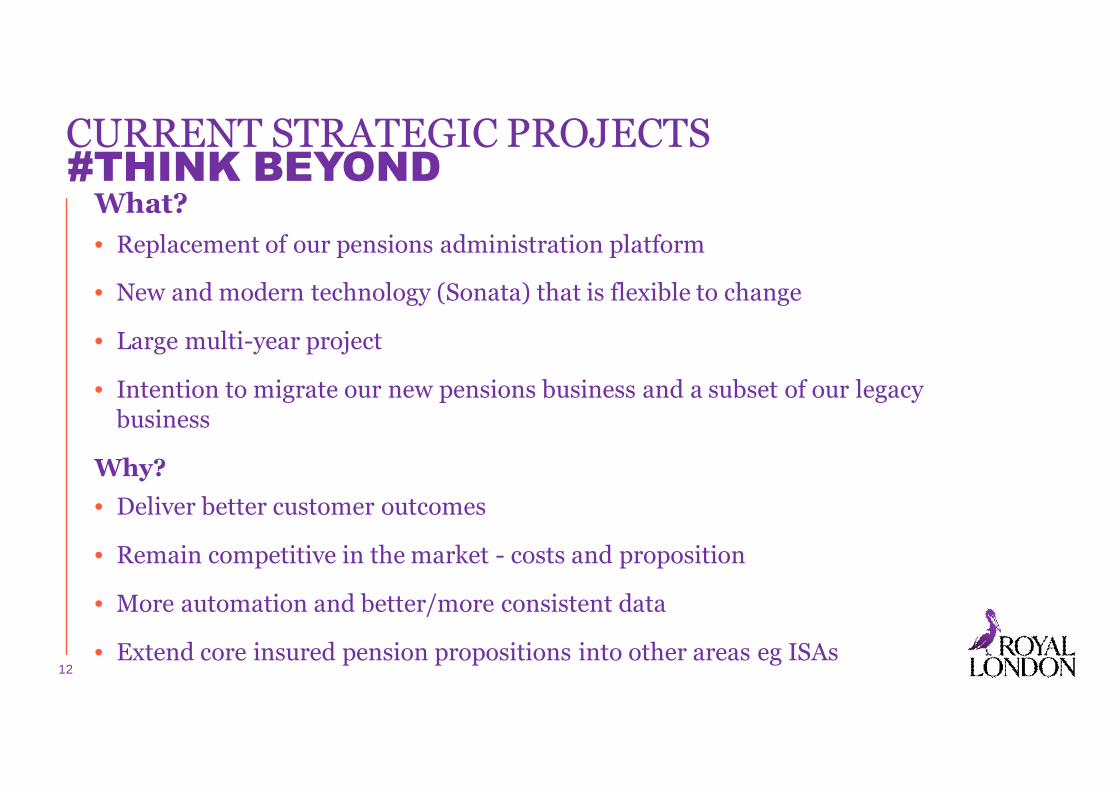

CURRENT STRATEGIC PROJECTS#THINK BEYOND

What?• Replacement of our pensions administration platform

• New and modern technology (Sonata) that is flexible to change

• Large multi-year project

• Intention to migrate our new pensions business and a subset of our legacy business

Why?• Deliver better customer outcomes

• Remain competitive in the market - costs and proposition

• More automation and better/more consistent data

• Extend core insured pension propositions into other areas eg ISAs

13

CURRENT STRATEGIC PROJECTS#THINK BEYOND

Some Key Challenges• Managing change – integrated model that will touch many areas of the business and needs a

joined up approach

• Product changes - investigating if we can remove certain legacy product features to enable customers to take advantage of the new platform

Actuarial Key Impacts• Re-specification of valuation extracts for the first time in over a decade –removal of manual work-

arounds, reduces the need for data cleaning

• Re-specification of new business reporting, Experience Analysis and the AoC – ensuring consistency

• Additional data points in the accounting and actuarial extracts to allow easier reconciliation between the two

• Reduced time for actuaries on processing

14

CURRENT STRATEGIC PROJECTSOUR BREXIT SOLUTION

• Setting up a new subsidiary in Ireland (already got a branch)

• We have 3 material blocks of non-UK business

a. Protection business sold after 2011 in RL Main Fund

b. Ireland Liver business which represents about half of the Liver Sub-Fund and includes a material amount of with-profits business

c. German Bond business in the RL Main Fund (small block)

• Part VII Transfer of all non-UK business to the subsidiary

• 100% reinsure the Liver and German Bond business back to RLMIS source funds. This will allow the Royal Liver Fund to stay economically intact.

Key challenge areas:• Timeframes ahead of Brexit

• Ensuring Scheme, amended Liver Instrument of Transfer and reinsurance arrangements all interlink correctly

• A range of other areas to consider such as WP governance , capital support and reassurance termination events

15

CURRENT STRATEGIC PROJECTSGAR COMPROMISE

Project “Talisker”:

WHAT?

• Offer to 33,000 policyholders with Guaranteed Annuity Rates

WHY?

• Can offer pensions freedoms without losing the value of GAR

• More equitable distribution of the Inherited Estate

WHERE ARE WE NOW?

• Using a Scheme of Arrangement

• 1st Court Hearing this coming Monday!

• Really positive and collaborative approach with FCA & PRA

• Positive response from policyholders so far >80% in favour

• Policyholder communications absolutely essential

• Will be more than two years from start to finish

16

• Mutuality at our core

Our journey…..

• Reducing volumes of with-profit business being sold and a divergence between membership and profit participation

• FSA (and FCA) pressure to resolve

• Considered a ‘Mutual Capital Fund’ but rejected

• Redefined the WP concept – adding profit participation to UL policies

• Large project ran like a Part VII but without Court

• Set ourselves up for the future

• Distributed £142m ProfitShare in April this year (grown from £114m in April 2017)

• Total ProfitShare distributions of £786m since 2007

THE FUTUREPROFITSHARE DEVELOPMENT

17

• Aim to continue to grow and help solve the problems of the future for our industry

This could involve…

• Developing drawdown proposition (market leader)

• Solutions to long term care problems e.g. blend of income drawdown and insurance to better enable us to meet the changing customer needs

• Growth of ProfitShare

THE FUTUREWHAT’S NEXT FOR ROYAL LONDON

18

CONCLUSIONOUR PURPOSE

As an industry we need to

remain true to our core

purpose, which is to our

customers

THANKYOU