one of the two - sitka pacific · sitka pacific capital management, llc phone: 425.967.5533 •...

TRANSCRIPT

Sitka Pacific Capital Management, LLC

Phone: 425.967.5533 • Fax: 888.877.1314 • Email: [email protected] www.sitkapacific.com

January 2018

Dear Investor,

The bubble in the U.S. stock market has now grown into one of the two largest bubbles in market

history. We say one of the two largest in history, because each period always has unique facets that

make direct comparisons somewhat tricky. In fact, according to many measures, this one is the

largest, and we can unequivocally say the following: there has not been another time when,

simultaneously, stocks were so overvalued, bond and cash yields were so low, and leverage

throughout the markets and economy was so high. In summary, this is probably the single most

fragile market environment anyone active in the markets today has encountered.

Although it has carried on far longer than expected, this bubble will eventually end, and when it does

the broad U.S. equity market indexes will likely lose more than half of their value in the post-bubble

market environment that follows — as they have each time valuations have climbed as high as they

are today. If this entirely predictable outcome surprises anyone, it will be a testament to how quickly

investors forget lessons from even the recent past. In addition, it is also possible that real, inflation-

adjusted returns from bonds and cash will also be negative in the years ahead. This means that the

vast majority of financial assets in the public markets — stocks, bonds, cash and cash equivalents —

may be poised to lose real value in the years ahead. If history is any guide, a diversified portfolio of

stocks and bonds may take as long as 25 years to recover its real value from the peak.

However, judging by the muted volatility over the past year and the passive acceptance of extremely

high valuations, it appears that none of these risks are on the radar of most investors today. While

investors were scared to death to touch stocks with even a 10-foot pole when prices fell in 2009 to

their lowest valuations in more than 20 years, they are now all in with valuations at three times their

bear market lows. This “sell low, buy high” response speaks to the powerful impact of short-term

negative and positive reinforcement on decision making, and the market’s uncanny ability to push

investors into the untimeliest allocations. In our estimation, the market is doing it again today by

relentlessly encouraging investors to remain invested in stocks at one of the most unattractive

moments in market history, all because they feel there is no alternative.

That stocks, bonds and cash are poised to deliver zero or negative returns in the years ahead is a

sufficient summary of the state of the markets at the end of 2017. Sometimes, the picture really is a

simple one. We’ll fill in the details as we go along through the pages below, but even with all those

details in hand, it leaves unanswered a very important question; arguably, the most important

question: If stocks, bonds and even cash are poised to deliver a negative real return, what is an

investor to do? Our answer to this question, of what to do, and why, is the main topic of this letter.

January 2018 Page 2 of 31

How today’s investment environment feels is strongly associated with each investor’s personal

experience navigating the markets over their lifetime, and their awareness of market history. For

instance, most investors active today have had significant stakes in financial assets only in an

environment of falling interest rates, falling rates of inflation and rising valuations. This has been the

dominant market paradigm for over 35 years, and for most of the past nine years short-term interest

rates have been held near zero. Under these conditions, artificially created by the Federal Reserve,

the most recent generation of investors has had no experience of any true price discovery in the most

economically consequential of all prices: interest rates.

Whether these artificial conditions — near zero percent interest rates, and the near record-high

valuations that they have spawned — leave an investor feeling optimistic or cautious is a good

barometer of how aware they are of just how the markets have arrived at where they are today. It is

also a good barometer of how aware they are of the market chaos which inevitably follows a

monetary-fueled bubble.

We are constitutionally value-oriented, and we are also well aware of the destructive market

environments that have followed monetary bubbles of yore — perhaps too aware for our own good.

Being aware of the impact of the long-term bear markets that inevitably follow bubble valuations

leaves us severely out of step during times such as these, which represents a business risk most

investment managers simply, and sadly, are unwilling to take (even if, from a pure investment

perspective, they know it would be the right thing to do). We have naturally become more bearish

about the market’s prospects as the bubble has inflated, since long-term prospective market returns

are now strongly negative. Whether you feel this is a good or bad quality to see in your investment

manager in today’s market environment likely depends on how much you value rational decision

making, even when it is difficult, versus the excitement, flashing lights and almost certain losses in a

casino.

When the tide finally turns and begins to recede, the high-water mark of this bubble will likely stand

for a decade or longer, during which time a market environment completely different from the last

few years will be ushered in. In all likelihood, the S&P will lose around 2/3 of its real value as that

market environment unfolds, just as it did after the bubble peaks in 1929 and 2000, and after the peak

in 1966. We continue to allocate and invest in ways we think will do well during that long post-

bubble erosion of market value, because it represents a future market environment poised to settle

into the present at any moment. And for many in the baby boom generation, the long fallout from

this bubble may come to define all the years within their investment horizon.

In the pages that follow, we’ll offer our thoughts on why this bubble has inflated, and detail the post-

bubble market environment we think will eventually unfold in its wake. By the end of this letter you

should have a clear idea of where the markets are today, and a clear understanding of the allocations

we think will define our years ahead. We’ll begin this discussion with a little bit of history of why

prices rose so much in the 20th century, which offers an important foundation for an understanding

of today’s markets.

January 2018 Page 3 of 31

The Price Revolution of the 20th Century

In the year 1896, wholesale commodity prices in Britain and the United States reached their lowest level in more

than a century. Then, during the year of the Diamond Jubilee, they began to rise a little – not very much, not

enough for anyone to notice. The increase was only about 1 percent that year, smaller than the range of annual

fluctuations. But we may observe a large significance in that small advance. It marked the beginning of a price-

revolution that would continue for more than a century…

The same inflection-point simultaneously appeared in the price records of many Western nations: Austria-

Hungary (1896-97), Belgium (1895-96), Britain (1896-97), Germany (1896-97), Italy (1897-98), Norway (1897-

98), Spain (1896-97), Sweden (1895-96), and the United States (1896-97). Each of these countries had its own

monetary system. All of them began to experience the price-revolution at the same time.

- David Hackett Fischer, The Great Wave: Price Revolutions and the Rhythm of History

There are few economic concepts now as deeply rooted in our collective psyche as that of inflation.

From the ivory tower of economic academia to those who have never encountered the concept of

supply and demand, these days there is a near universal understanding and acceptance that prices

generally rise over time. We all can remember stories told by our parents and grandparents about

how little things seemed to cost way back when, and we compare those stories to our experience at

the store today and often wonder what on earth happened? The amount of money we need to buy a

new car today is the amount of money people spent on a new home fifty years ago, and the old sign

in the antique store advertising a 5-cent cup of coffee seems like from a long-bygone era. We all seem

to have a firm understanding of the fact that prices generally rise over time, and whether we realize

it or not, that assumption has permeated deep into all the decisions we make, day in and day out.

The assumptions we have about rising prices are now so taken for granted that it is often with some

degree of shock that someone realizes it hasn’t always been this way. In truth, the trend of price

increases we have now collectively accepted as the way things are, is purely an artifact of the 20th

century, as we’ll see below, and there is nothing inherently inevitable about it.

In any given bookstore, there are shelves and shelves of books about investing, but many important

concepts which are useful in navigating the financial markets are actually found in sections other

than finance. For instance, there are a great number of important investment concepts detailed in

Sun Tzu’s The Art of War, which usually sits among books about ancient China, such as the greatest

victory is that which requires no battle. Oftentimes very profitable investments can be made when no

one else is looking at them and there is no battle fought to accumulate them; or, even better is when

people are so desperate to part with some asset that they practically thank you for taking it off their

hands. This single concept from 2300 years ago is more practically useful than a lot of what is covered

in books on investing, yet it’s not even found in the same area of the bookstore.

In that same bucket, of books that aren’t explicitly about investing but which have great value to

investors, is a book entitled The Great Wave: Price Revolutions and the Rhythm of History, by David

Hackett Fischer. A copy of The Great Wave has been on our own bookshelf for more than a decade,

filled with penciled notes and underlines. It is a book that describes and explains four distinct “price

revolutions,” as the author terms them, that have occurred over the past 800 years. These periods of

January 2018 Page 4 of 31

price revolution were periods in which prices began rising for a significant amount of time, often for

a century or more, and often to the bewilderment and detriment of many of those living through

them. The book is also about the periods of relative calm between those price revolutions, which the

author terms periods of “equilibrium.” These are periods when prices generally remained stable,

often for a century or more. The alternating phases of price revolution and equilibrium have been

coincidently seen throughout the reach of modern Western culture, with only minor differences in

timing seen between regions. The chart below gives an overview of the price revolutions and

equilibriums in England from the year 1201 through 1993, shortly before the book was published.

Each of the periods identified above has its own unique story behind it, but it is the few common

threads that underlie all periods of revolution and equilibrium that are of greatest interest. In the

chart above, you can see that there are indeed four periods defined by a long-term rise in prices, and

three periods when prices generally remained the same. Yet when we zoom in we find that the there

is also tremendous short-term “noise” embedded in those broad trends. On such a long-term look at

prices as this, any price changes experienced over, say, a decade will look like one of the noisy

fluctuations on the chart above.

For example, one of the largest sources of noise in the medieval and 16th century price revolutions

came from the failure of the annual grain harvests, with some of the larger spikes in prices, such as

the one seen just after the year 1300 (just beneath “The Medieval Price Revolution” on the chart

above), occurring during periods of extended famine. Between 1314 and 1316, Europe experienced

January 2018 Page 5 of 31

its worst famine on record due to successive crop failures caused by cold and wet weather, and it’s

estimated that Europe lost nearly 10 percent of its population during this time. Food prices soared

during the famine, but the spike in prices during those years fell within the noise of a long-term trend

of rising prices that had begun a century earlier.

If the largest famine in European history can be relegated to noise within a long-term price revolution

of the past, the question immediately arises: What could possibly be a strong enough force to move

prices higher over a century or more? Although there are many factors that influence prices over

time, the strongest influence, and the underlying driver of all price revolutions, is found in changes

in population and demographics.

Famine was not the cause of the long-term rise in prices throughout the 1200s, but the famine of 1314–

1316 did mark the end of the Medieval Price Revolution because it marked the end of a long rise in

Europe’s population. Although estimates are difficult and necessarily come with large error ranges,

Europe’s population grew substantially between the 12th century and the early 14th century, and

England’s population may have doubled during its Medieval Price Revolution. This tremendous

growth in population put tremendous strain on existing resources, and the result was a long rise in

prices: for example, grain and cattle prices more than tripled, and cloth prices doubled. There were

other impacts as well: as population levels rose, a surplus in labor developed, and as a result, wages

began to lag behind rising prices.

Life in Europe became increasingly difficult during the latter decades of the 1200s, and by the early

1300s poverty and wealth inequality had increased substantially. Thus, the population of Europe in

the early 14th century was extremely fragile and susceptible to shocks, and the famine of 1314–1316

was the straw that broke the camel’s back. It’s estimated that Europe’s population didn’t rise above

its early 14th century level until 150 years later, and it’s no coincidence that during that time of

population stability a period of relative price stability unfolded — which is labeled as the Renaissance

Equilibrium on the chart above.

Population isn’t the only factor influencing prices, but it appears to be the dominant factor driving

long-term trends in prices. Long-term increases in population result in large trends higher in prices

of all kinds of consumables and assets, and they also have a dramatic impact on wages. One

conclusion which can be stated categorically is that during every price revolution over the last 800

years, real, inflation-adjusted wages have fallen each time during the revolution’s latter stages a

trend— which is, as you may have already guessed, directly relevant to our present times.

While the Medieval Price Revolution is certainly notable, you can see that it pales in comparison to

the 20th Century Price Revolution shown on the right side of the chart above. While prices of many

commodities and consumables doubled and tripled during the Medieval Price Revolution, prices

have gone up by more than an order of magnitude during the current price revolution; i.e. more than

10 times. Clearly, the 20th Century Price Revolution has been extraordinary, but in essence it has been

the result of the same factors that have driven all prior price revolutions.

January 2018 Page 6 of 31

The quote at the beginning of this passage highlights that the 20th Century Price Revolution got its

start in the 1890s, and that it began nearly everywhere in the Western world at nearly the same time.

Like the price revolutions before it, the major driver appears again to be population growth, but this

time, instead of a large rise in births, the population boom of the 20th century has been driven by a

precipitous fall in mortality and a dramatic lengthening of average life span. From the 1890s onward,

death rates from common diseases such as tuberculosis and diphtheria (among many others) began

to fall dramatically, as modern bacteriology revolutionized medicine. This ushered in a worldwide

population boom, the likes of which has never been seen before, and this boom from the falling

mortality rate exploded even as the birth rate declined.

In 1896, which is the year global commodity prices began what would prove to be the fourth price

revolution since the Middle Ages, the global population is estimated to have been around 1.5 billion.

During the prior century, the global population is estimated to have grown by about 50%, from

around 1 billion to 1.5 billion. This relatively modest rise in population during the 19th century

encompassed a period of relative price stability, termed The Victorian Equilibrium in The Great Wave.

However, in the century after 1896, the global population soared to 6 billion — a staggering 300%

rise. There has never before been a quadrupling in global population within one hundred years, and

the ripple effects from this boom have been reverberating through the global economy just as prior

population booms have — only more so.

In every price revolution over the past 800 years, there has been a clear progression as the growth in

population placed new strains on resources, and we have seen a similar progression over the past

century. It has been the case during every price revolution that returns from capital come to far

exceed the return from labor as prices continue to rise, because labor becomes relatively abundant

while capital becomes relatively scarce. As the returns from capital and labor diverge, wealth

inequality increases, and public deficits and indebtedness begin to grow alarmingly as governments

attempt to mitigate tougher times for the average citizen.

January 2018 Page 7 of 31

Toward the end of the Medieval Price Revolution, for example, Italy was the center of the financial

world, but the early 1300s witnessed the bankruptcy of many of the largest Italian banks — which

had over-lent to the monarchs of Europe, and even to the Pope. The financial crises in the early 14th

century was a symptom of public over-indebtedness, which is a symptom seen during the latter

stages of every price revolution. Centuries later, the end of the 18th Century Price Revolution

coincided with a peak in the price of bread and the peak in indebtedness of the French monarchy,

which was forced into austerity just when life for the average French citizen was at its most difficult.

The French Revolution followed soon thereafter.

In the present price revolution, public indebtedness throughout the Western world began to rise just

when real wages began to fall in the 1970s, and this has coincided with returns from assets (including

equities) remaining high, which has increased wealth inequality. These are all symptoms of labor

becoming increasingly abundant, and capital becoming increasingly scarce, and these symptoms

have been part of every price revolution.

Although the world’s population has continued to climb in the 21st century, the peak rate of

population growth was reached long before the end of the 20th century — in 1962. Since that time,

the rate of population growth has fallen from 2.1% per year to 1.2% per year, and as you can see on

the chart above, this growth rate is expected to continue falling throughout the 21st century. Setting

aside unpredictable events that can impact this trajectory, such as wars and epidemics, the growth of

The peak inflation rate of the second half of the 20th

century was an echo of the global population growth

rate, which peaked in the 1960s at 2.1%. That growth

rate has fallen by almost half over the past 50 years,

and is set to continue falling in the decades ahead back

down to its former range of 0%–0.5%.

January 2018 Page 8 of 31

the world’s population over the next century will be much lower than over the last century. In fact,

it may be similar to the growth rate during the last period of relative price stability — the Victorian

Equilibrium.

In addition, the slowing population growth of the 21st century will likely have an entirely different

impact on prices, due to demographics. While the working-age population grew substantially

relative to other age groups in the decades following World War II, the growth in the working-age

population between 2010 and 2050 is projected to be roughly matched by the growth in the numbers

of those younger than 15 and those older than 65. This demographic shift means that the population

growth of the 21st century will not only be much lower than in the 20th century, it will likely deliver

an entirely different impact on returns from assets versus returns on labor.

The main point we would like to make in this discussion is that the soaring prices of the 20th Century

Price Revolution have unfolded mainly as a response to the growth in the world’s population, but

that all price revolutions go through specific phases, and they all eventually come to an end. It

appears we are in the latter stages of the current price revolution, which necessarily means that the

future trends in prices, as well as returns from capital and labor, will likely look a lot different to what

unfolded over the past century. However, we’ve largely left out of this discussion an important

aspect of the 20th Century Price Revolution, which is especially relevant for investors — the monetary

component.

January 2018 Page 9 of 31

The Last Phase of the 20th Century Price Revolution: Deleveraging and Monetization

Central banking was meant to be about the stability of prices. But today, through its intention to stabilize, it

paradoxically has become a source of great underlying instability and risk.

- Jim Grant, 2017

The history of price revolutions and equilibriums over the past 800 years is a fascinating study of

trends which are, for the most part, hidden just underneath the surface of society’s conscious

awareness. People today are quite aware that prices are rising, but it’s rare to find someone who is

aware of why prices are rising, or aware of the fact that this has not always been the case. Stepping

outside the experience of the price revolution of the 20th century allows one to look at today’s

circumstances with a deeper understanding that the market trends of the 20th century may prove to

be as unique to the times as the general price trends were, and the population boom that fueled them.

Understanding the role of population growth is the key to understanding why prices have risen

during each of the four price revolutions over the last 800 years, and although we did not spend much

time covering it in the pages above, it is also the key to understanding why prices have remained

relatively constant for long periods as well. Yet the role of population is not the entire story — there

are many other factors have that come into play during every price revolution. And the one factor

that ranks just behind population growth in its influence on the 20th Century Price Revolution is the

role that monetary policy has played.

The last vestiges of the gold standard were

abandoned in 1971, which set global currencies

adrift without any stable anchor of value. This

accelerated population-driven price changes.

The Federal Reserve was established

in 1913, and the value of the dollar

has never been the same.

January 2018 Page 10 of 31

In every price revolution of the past, monetary debasement has played a role in the rise of prices,

typically when governments and monarchs have attempted to maintain spending even as tax

revenues begin to sag in the latter stages of a price revolution. However, the 20th Century Price

Revolution has seen the role of monetary debasement taken to an entirely new level.

In the past, countries would systematically devalue their coinage at varying rates during the latter

stages of each price revolution, as increasing poverty fueled social unrest, and monarchs struggled to

hold on to power. However, such devaluations were usually regional in their impact, and they rarely

occurred when neighboring countries were undergoing similar devaluations at the same time. Yet

during the 20th Century Price Revolution, the entire First World transitioned off gold at the same time,

opening the door to the first truly global currency devaluation.

In the decades after Nixon closed the gold window in 1971, leverage in the U.S. and global economy

soared to heights never before seen in our country’s history, and the dollar’s purchasing power

plunged by 83%. This devaluation acted as an accelerant to the population-driven rise in prices that

began at the end of the 19th century. And on the surface, it appears a lot like the devaluations seen

during price revolutions of the past, with one critical difference: the monetary inflation since 1971

fueled a buildup of debt, instead of dissolving it. This means that although the dollar has already lost

most of its value over the past 40 years, the devaluation which will result from the deleveraging of

the U.S. economy, as well as the global economy, still lies ahead of us.

Deleveraging began with the financial crisis in 2008, which

also marked the beginning of debt monetization by the Fed.

It’s likely that monetization will continue, in fits and starts,

until the economy is no longer hampered by deleveraging.

January 2018 Page 11 of 31

The financial crisis in 2008 represented far more than a typical bear market and recession — it

represented the end of the era of debt-fueled growth that unfolded in the wake of the closure of the

gold window in 1971. Although the economy has been growing since 2009, debt levels in the private

economy continue to fall, which is a trend we have not seen since the Great Depression. Without

increasing levels of indebtedness, economic growth has been weaker over the past decade that any

other time in the post-war era: real GDP growth has averaged 1.4% over the past decade, versus 3%

in the decades prior to the financial crisis. The Consumer Price Index has seen a similar slowdown,

from a 3.5% average annual rise in the decades before the financial crisis, to 1.7% over the past decade.

As slow as 1.4% is, this growth rate over the past decade was only achieved with the help of the

massive monetary expansion by the Federal Reserve, along with negative real interest rates. The

Fed’s monetary base grew from $850 billion just before the financial crisis, to $3.9 trillion at the end

of 2017. Although these numbers are a far cry from the $70 billion monetary base that forced a closure

of the gold window in 1971, you can see in the chart above that the current monetary base, while

vastly expanded since 2008, remains entirely overshadowed by public and private U.S. debt.

With aging demographics, the U.S. economy will not grow its way out of debt, but the Fed can inflate

the economy out of debt. This is what the Fed has been doing since 2008, and the impacts of this new

type of growth, powered by central bank debt monetization instead of by private credit creation, can

be seen throughout the markets. The rising value of gold versus the CRB Commodities Index, shown

below, is one such indication. The message of this trend is that the Fed is devaluing the dollar, but

that devaluation is not outweighing the heavy impact of deleveraging on economic growth.

Just as few are aware that prices have not always risen, few appear to be aware that the period since

1971 has been one large monetary experiment. So far, the result of this experiment has been an

explosion of debt, a Minsky-moment of crisis in 2008, and the beginning of deleveraging and the

Fed’s monetization. However, it’s important to realize that this monetary experiment remains

ongoing — we have not reached the end of it. In fact, we are right in the middle of it.

In 2008, gold decoupled from oil and other commodities and

began to trade more in its traditional role as sound money. By

the time the 20th century price revolution and the current

period of deleveraging have both run their course, gold will

likely be valued much higher than it is today.

January 2018 Page 12 of 31

All price revolutions in the past have ended with a series of events which push the pendulum back

the other way, correcting the imbalances that built up during the long rise in prices. The United States

came into being just as the 18th Century Price Revolution was reaching its zenith in the late 1700s,

when the governments of Europe were reeling from the pressures that had built up over 70 years of

rising prices. Between 1730 and 1790, the prices of basic commodities such as oats and firewood rose,

as did the cost of rent. During the same period, the real value of wages fell by more than half. The

pressure resulting from these trends resulted in revolution here in America and in France, and social

reorganizations of various kinds have always marked the end of price revolutions.

The last phase of the 20th Century Price Revolution will be defined by the efforts of the Fed and the

other major central banks to inflate their economies while they deleverage, and what we have seen

over the past decade is just the beginning of this effort. Although the Fed is currently trying to create

some room to maneuver by tightening monetary policy in baby steps, the other major central banks

have continued to expand; the combined balance sheets of the Fed, the Bank of England, the Bank of

Japan and the European Central Bank grew by over $1.5 trillion in 2017. That this global monetary

expansion continues nine years after the financial crisis, while the global economy is growing and

unemployment is low, is testament to just how entrenched we are on the path of monetization.

Yet, as entrenched as we are on a road of monetization, the markets have given no hint that the public

at large understands the long-term implications. The risk-free asset which has proved to be the only

durable safe-haven through all price revolutions now trades at a record low relative to the current

monetary base. By the end of this period of deleveraging, we think gold will no longer be

undervalued, but will trade as if this long monetary experiment is finally coming to an end.

1933

Today

1980

1971

January 2018 Page 13 of 31

The QE/TINA Bubble Will Be Followed by Another Long-Term Bear Market

You pay a very high price in the stock market for a cheery consensus.

- Warren Buffett, 1979

In November, Bank of America Merrill Lynch released a report summarizing the results of its latest

survey of fund managers. The report stated that a net +16% of fund managers were taking higher

than normal risk in their portfolios, which is the highest level going back to the tech bubble. Fund

managers reported they were using less downside protection, and holding less cash, even though

they worried about extremely high valuations. The author of the report, Michael Hartnett, the bank’s

chief investment strategist, summarized his feelings about the survey results: Icarus is flying ever closer

to the sun, and investors’ risk-taking has hit an all-time high. A record-high percentage of investors say equities

are overvalued yet cash levels are simultaneously falling, an indicator of irrational exuberance.

It’s remarkable that even most professional investors find themselves unable to resist the siren song

of the market during a bubble, which, in an ideal world, really should be at the top of their list of

responsibilities as investment managers. We’ll give a few reasons why this happens a little later, but

for now it’s enough to say that at the end of 2017, fund managers as a group were taking more risk

than at any other time in the last 17 years. They were doing so, not when valuations say stocks

represent a tremendous long-term value for their investors, but when valuations strongly suggest

stocks will lose the majority of their value following the peak of this bubble.

From its peak in 1929, the S&P 500 recorded a maximum loss of 81%,

and was still 67% below its peak value 20 years later. From its peak

in 2000, the S&P 500 recorded a maximum loss of 65%, and did not

rise above its peak value until 16 years later. Those holding large-cap

stocks today face the prospect of similar losses.

January 2018 Page 14 of 31

The S&P 500’s 10-year price-to-earnings ratio ended 2017 at 32, which matched the peak valuation

seen in 1929. There has only been one other period of rising prices with a higher 10-year P/E ratio

than we have today, and it was during the last 32 months of the largest speculative bubble of all time,

the tech bubble. Outside of those two and a half years, valuations have never been higher than today.

Other measures of valuation tell us that this bubble is already larger than the tech bubble, as

overvaluation is much more broadly distributed today than it was in 2000. For example, the price-

to-sales ratio of the S&P 500 matched its tech bubble peak at the end of 2017, and the median price-

to-sales ratio of the individual stocks in the S&P 500 rose to over 2.5 at the end of 2017, while it was

at 1.5 in 2000, and only 0.7 in the early 1990s. This tells us that, on a price-to-sales basis, the typical

large cap stock in the U.S. at the end of 2017 was 66% over its valuation at the tech bubble peak.

Whether we look at sales-based valuation measures or earnings-based measures, any discussion of

value should be based on measures which give us useful information about what future returns are

likely to be. Unlike earnings measures which only use the past 12 months of data, or those which

look at analysts’ estimate of the next 12 months of earnings, a price-to-earnings ratio using a long-

term average of earnings tells us what we actually want to know: are stocks expensive or cheap

relative to the highs and lows likely to be seen through the entire business cycle? During the financial

crisis, the tech bust and even the early 1990s bear market, valuation measures based on 12 months of

earnings (forward and backward) gave no hint that there were rough waters ahead. And worse,

those measures indicated the market was more expensive at the bear market lows than it was at the

highs — which is precisely the opposite advice we want from a valuation measure. A simple table

of these numbers, shown below, highlights this.

Any valuation measure that doesn’t show the market being cheaper at the end of a bear market than

it was at the beginning of the bear market isn’t worth that much — and, in fact, can be extremely

misleading. During each of the last three bear markets, a price-to earnings ratio based on the last 12

months of earnings was higher at the end of the bear market than it was at the beginning, and at the

market lows in 2009 it said the market was (literally) off-the-charts expensive, with a P/E ratio of 86.

There is simply no evidence that using valuation measures based on 12 months of earnings gives any

useful information, yet these measures continue to be the ones most often cited.

In contrast, using 10 years of earnings data along with the current price of the S&P 500 provides a

measure of valuation on which we can base practical decision making. Not only does it tell us what

we want to know at cyclical market peaks and troughs, it provides us with an accurate long-term

assessment of just how expensive or cheap the market is at those cyclical peaks and troughs. For

2007-2009

2000-2003

1989-1992

Average % Change

Recent S&P 500 Earnings Recessions

Earnings % Decline S&P 500 % Decline 10-Year P/E (Peak/Trough) 12-Month P/E (Peak/Trough)

-92% -58% 27/13 19/86

-54% -50% 44/21 34/38

Source: Robert Shiller, Sitka Pacific Capital Management, LLC

-61% -42% -39% +109%

-37% -18% 13/1517/15

January 2018 Page 15 of 31

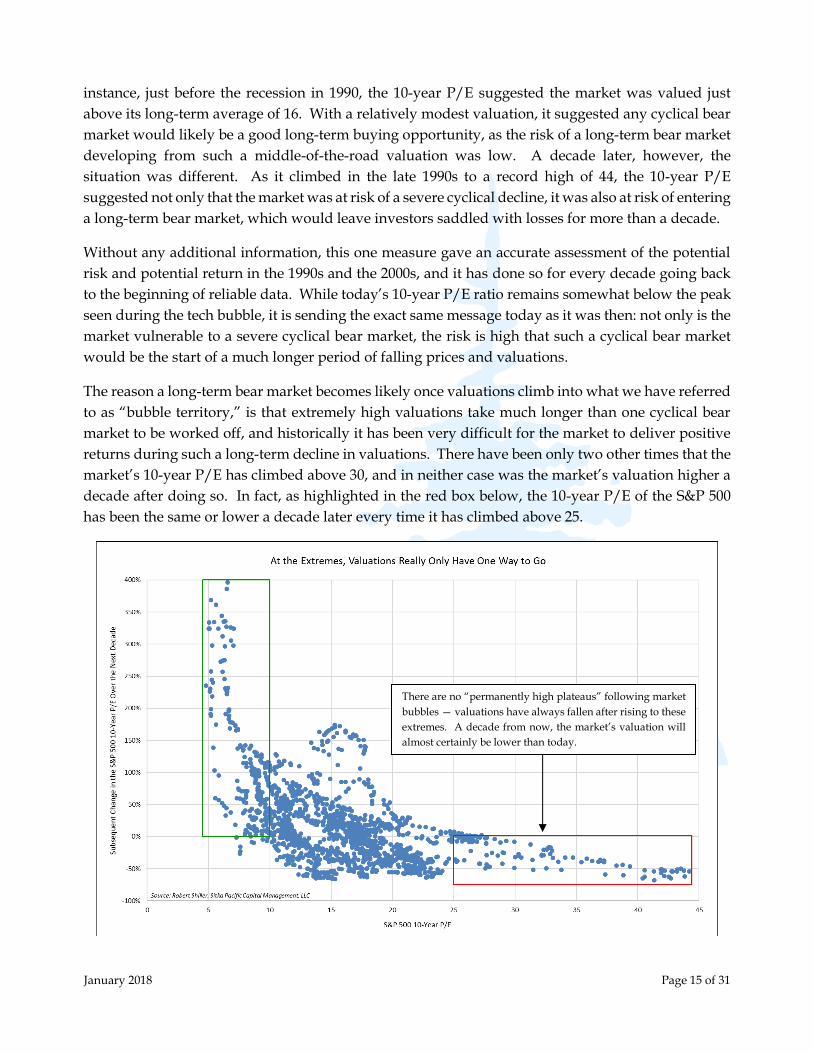

instance, just before the recession in 1990, the 10-year P/E suggested the market was valued just

above its long-term average of 16. With a relatively modest valuation, it suggested any cyclical bear

market would likely be a good long-term buying opportunity, as the risk of a long-term bear market

developing from such a middle-of-the-road valuation was low. A decade later, however, the

situation was different. As it climbed in the late 1990s to a record high of 44, the 10-year P/E

suggested not only that the market was at risk of a severe cyclical decline, it was also at risk of entering

a long-term bear market, which would leave investors saddled with losses for more than a decade.

Without any additional information, this one measure gave an accurate assessment of the potential

risk and potential return in the 1990s and the 2000s, and it has done so for every decade going back

to the beginning of reliable data. While today’s 10-year P/E ratio remains somewhat below the peak

seen during the tech bubble, it is sending the exact same message today as it was then: not only is the

market vulnerable to a severe cyclical bear market, the risk is high that such a cyclical bear market

would be the start of a much longer period of falling prices and valuations.

The reason a long-term bear market becomes likely once valuations climb into what we have referred

to as “bubble territory,” is that extremely high valuations take much longer than one cyclical bear

market to be worked off, and historically it has been very difficult for the market to deliver positive

returns during such a long-term decline in valuations. There have been only two other times that the

market’s 10-year P/E has climbed above 30, and in neither case was the market’s valuation higher a

decade after doing so. In fact, as highlighted in the red box below, the 10-year P/E of the S&P 500

has been the same or lower a decade later every time it has climbed above 25.

There are no “permanently high plateaus” following market

bubbles — valuations have always fallen after rising to these

extremes. A decade from now, the market’s valuation will

almost certainly be lower than today.

January 2018 Page 16 of 31

During a significant fall in the market’s valuation over a decade or more, its price falls faster than its

components’ underlying value rises, and this results in investor losses. This is what happened

following the tech bubble peak: while the book value of the S&P 500 rose from $325 at the end of 2000

to $579 at the end of 2010 (a respectable 78% gain, considering the turmoil of the decade), the 10-year

P/E of the S&P 500 fell 42% over that time. This fall in valuation overwhelmed the rise in the index’s

underlying value, and as a result both the nominal and the real, inflation-adjusted price of the market

was lower in 2010 than it was in 2000. In other words, returns for investors were negative even

though the index’s underlying value grew, and this was due to the long-term decline in valuations.

Once the market’s valuation climbs as high as it is today, the market’s central expected return falls

significantly below zero, and there is little investment value to be had for shareholders. This is not

necessarily a bearish assessment on the potential for large-cap stocks to create shareholder value over

the next decade, but it is a bearish assessment on what price shareholders will see on their holdings.

Based on today’s starting valuation, that market-quoted price of the S&P 500 may fall at an average

real rate of 3%–4% over the next decade, leaving a portfolio of large-cap stocks worth 30% less at the

end of 10 years. And during that time, the cumulative losses at cyclical bear market lows will almost

certainly be greater.

Profits in large-cap stocks in the U.S. have fluctuated wildly over the course of the many business

cycles, but over the course of the 20th Century Price Revolution and the reign of the Federal Reserve,

nominal profits have grown at a nominal exponential rate of 4%. There have been times when

recessions took profits below this trend rate of profit growth, and there have been boom times when

January 2018 Page 17 of 31

profits were higher for a time, but over the long haul the trend rate of nominal growth of corporate

profits has been 4%.

However, the 4% exponential profit growth rate is a nominal rate, which means that a portion of this

growth is due to inflation. Over the same period, from the beginning of the 20th century, the

Consumer Price Index has risen at a 2.6% exponential rate, which means the real, inflation-adjusted

profit growth of large public companies has been around 1.4%. If we take this 1.4% exponential

growth rate of real profits and look at market valuations, not based on a 10-year average of S&P 500

profits, but based on the trend of real earnings growth over the long term, we get the data shown in

the chart below.

As noted above, the S&P 500 was 116% above its trend median valuation at the end of 2017, and this

was higher than any other time outside the final few years of the tech bubble. The trend median

valuation (grey line in the chart) for the S&P 500 during the Fed era will reach 1365 in the year 2023,

which is 50% below its current price. Ten years later, in 2033, the trend median valuation will reach

1653, which is 40% below today’s price. If trading back down at these levels seems fantastically

outside the realm of the possible at those future dates, it’s due solely to today’s astronomically high

valuations — not what simple logic says is a reasonable value for large-cap stocks.

Looking at valuations from a trend earnings perspective is useful, because although using the average

of the past 10 years of earnings gives us a much more useful valuation tool than using a shorter

period, such as 12 months, there is no getting around the fact that there are cycles in economic growth

and inflation that can cause even decade-long periods of corporate profits to veer from their long-

96%

139%

End of 2017: 116%

56%

78%

January 2018 Page 18 of 31

term growth trend. Between 1997 and 2007, there were two large booms in the economy, and this left

a 10-year average of corporate profits unsustainably high at the end of that period; and it so happens

that the inflated 10-year average of earnings declined for the first time in its history between 2007 and

2011 to correct that boom-time deviation. When we look at market valuations based on the long-term

trend in earnings growth, we can see the market’s underlying value clearly through periods of boom

and bust that influence even a 10-year average of earnings.

A similar above-trend deviation of the 10-year average of earnings happened during the 1960s, and

the roots of that period of above-trend earnings growth, and the market over-valuation that

accompanied it (marked by the red 56% on the previous chart), are similar in some ways to the

situation today. In the two decades following World War II, corporate profit margins were high by

historic standards, and wages were still recovering from the Great Depression. As a percentage of

GDP, corporate profits averaged 10.8% between 1947 and 1969, and by the late 1960s this long era of

robust profit margins had lasted long enough to convince investors that stocks were the place to be,

regardless of high valuations. This was the era of the Nifty Fifty bubble, and also the era that spawned

modern portfolio theory, which, among other things, argued that being 100% invested at all times

made the most sense.

It is somewhat ironic, then, that the decade and a half following the late 1960s ranks as the second

worst period on record for a fully invested portfolio of stocks and bonds, as stock market valuations

fell and interest rates soared in the 1970s and early 1980s. Not coincidentally, the pivot in market

performance in the late 1960s coincided with the end of the period of high post-war profit margins.

In the first quarter of 1966, two things happened: corporate profit margins peaked at 12.2%, and the

S&P 500’s valuation also peaked. By the early 1980s, corporate profit margins had fallen by half, and

due to the fall in valuations, the S&P 500 remained at the same nominal price in 1982 as it was in 1968

— but had lost 62% of its real, inflation-adjusted value.

As much as the 1950s and 1960s were defined by high corporate profit margins, the 1970s and 1980s

were defined by lower corporate margins. Between 1970 and 1990, corporate profits averaged 8.3%

of GDP, 2.5% (of GDP) lower than in the two decades prior. Most of those lost profits found their

Corporate Profits (Blue, left scale) and Wages (Red, right scale) as a Percent of GDP

1

2

3

January 2018 Page 19 of 31

way into wages, which averaged 1.9% of GDP higher between 1970 and 1990 than in the decades

prior. This economic tug-of-war between corporate profits and wages has been part of the U.S.

economy going back as far as we have reliable data, and it has been a huge part of the story behind

the market’s high valuation over the past 20 years. This period of high market valuations began in

the mid-1990s, and, not coincidentally, the mid-1990s also marked an end to the trend of falling

corporate profit margins.

From a low of 7% of GDP in 1993, corporate profit margins have surged higher in three successive

waves (marked on the chart above with the numbers 1, 2 and 3), culminating in the rise to 12.6% of

GDP in 2012 and again in 2014. Over the very same period, wages fell dramatically — the 5.6% of

GDP rise in corporate profits over that span mirrored the 5.3% of GDP fall in wages. Although wages

briefly spiked during the tech bubble, they fell from 33% of GDP in 1993 down to a post-war low of

only 27.7% of GDP in the wake of the Great Recession.

The current era of higher corporate profits since the mid-1990s has endured as long as the preceding

era in the 1950s and 1960s, and just like in the late 1960s, a large part of today’s investor euphoria is

implicitly based on the prospect of this trend continuing indefinitely. The passage of the tax bill in

late 2017 changed the corporate tax rate from 35% to 21%, and this change has inflated investor

euphoria into the stratosphere. Although the reduction in the corporate tax rate will undoubtedly

have an impact on the taxes corporations pay, just how much of an impact is remains in the realm of

speculation.

The effective corporate tax rate has fallen steadily from over 50% in the 1950s down to 21% in recent

years, and we may eventually find that the change in the statutory rate may not even offset the impact

of the rise in wages over the past few years. The official unemployment rate hit 4.1% at the end of

2017, and since 2011 the share of GDP going to wages has been rising. This has placed a lid on

corporate profits: wages have increased by 1% of GDP, and corporate profits have fallen by 1% of

GDP. To put this into proper context, corporations only pay around 2% of GDP in taxes, so the impact

of higher wages over just a few years can swamp any impact from a change in tax rates.

For investors, however, the debate over taxes is largely academic, because corporate profits would

have to double over the next few years to justify current valuations — and that simply cannot happen

from any change in the tax code.

* * *

Here at the beginning of 2018, a traditional portfolio of stocks and bonds faces the most hostile market

environment anyone active in the markets today has likely experienced. Not only are equity market

valuations absurdly high, but late last year the Fed began shrinking the base money supply under its

pre-announced plan to begin reducing its balance sheet — which presents a clear and present danger

to equity valuations, as well as to bonds. As we discussed last summer, the Fed has intentionally

shrunk its balance sheet only twice in its history, in 1921 and 1937, and the market turmoil that

followed those episodes left a bad institutional memory in the halls of the Fed that lasted 80 years.

The Fed never again attempted to shrink the base money supply . . . until now.

January 2018 Page 20 of 31

The increase in short-term interest rates over the past few years has been quite modest, though it

represents a huge percent increase from its level near zero, and it has already been enough to have a

strong dampening effect on lending and employment growth. By this past November, the year-over-

year change in employment growth had slowed from 2.3% in 2015 to 1.4%, and the growth rate of

commercial and industrial loans had plummeted from an 11.5% year-over-year growth rate to only

0.9%. That we have seen such a dramatic slowdown in employment and lending growth from a 1%

rise in the Fed Funds rate over two years’ time shows just how fragile our over-indebted,

deleveraging economy is.

However, as the effect of the Fed’s balance sheet reduction began rippling through the markets last

fall, it became clear we had entered a new monetary environment, quite distinct from most of the past

two years — an environment of Quantitative Tightening. The two-year Treasury yield rose more in

the last four months of 2017 than it has since the onset of deleveraging a decade ago, which is a telltale

sign that monetary policy has entered new phase. By the end of 2017, the yield on the 2-year Treasury

bill had risen to 1.89%, which was the highest rate since September 2008.

The current market bubble began as a response to the massive monetary expansion during the Fed’s

quantitative easing programs in the wake of the credit crisis, but it eventually evolved into a bubble

powered by investors who felt that There Is No Alternative (TINA) to buying overvalued assets when

interest rates are near zero. However, the era that spawned this justification for buying stocks at any

valuation ended last year, as the rise in the safest short-term yields rose above the dividend yield of

the S&P 500 for the first time in almost a decade. Along with the 2-year Treasury yield at 1.89%, the

5-year Treasury yield ended 2017 at 2.2%. These yields were both above the year-end dividend yield

on the S&P 500, which had fallen to just 1.8%.

Yet while short-term yields have risen over the past two years, long-term Treasury yields have fallen,

as can be seen at the bottom of the chart above. The combination of rising short-term Treasury yields

and falling long-term Treasury yields produced a dramatic flattening of the yield curve in 2017. At

October 2017: Quantitative Tightening

begins, and short-term yields respond.

December 2015: The Fed begins increasing

the Fed Funds rate in baby steps, and the 2-

year Treasury yield begins to rise.

Long-term Treasury

yields remain lower.

January 2018 Page 21 of 31

the end of the year, the 10-year Treasury Note was yielding only 0.51% more than the 2-year Treasury,

and the 30-year Treasury bond yielded only 0.85% more than the 2-year Treasury. Not only does this

represent the flattest yield curve in a decade, it represents a dramatic disagreement between the Fed,

which influences short-term yields, and the markets, which control long-term yields. If long-term

Treasury yields were to remain where they are, it would likely take only two more 0.25% rate hikes

by the Fed to bring about the first yield curve inversion since 2006 — a traditional sign that the Fed

has already hiked the economy into a recession. (We’ve long thought that a yield curve inversion

would be near impossible in the era of zero-percent interest rates, but the Fed’s hikes in 2017 brought

such an inversion close to reality.)

If we were in a normal post-war economic and market cycle, we would likely be near the ideal time

to buy long-term Treasury bonds ahead of Fed-induced cyclical economic weakness. With the stock

market’s valuation extremely high, with the yield curve having flattened dramatically over the past

three years, and with employment and lending slowing, ordinarily we would be near the moment

when economic momentum slows enough that markets begin to price in a premium on the safest of

safe-haven financial assets.

Yet this has been no normal post-war economic cycle, and it should be clear from our discussions of

monetary policy, demographics, debt and deleveraging over these past few years that the post-war

era ended with the financial crisis in 2008. Thus, many of the cyclical inter-market relationships we

came to depend on during the post-war era may no longer unfold as expected, and a case in point is

the current technical position of long-term Treasuries.

Leading up to the summer of 2007, the trading action in long-term Treasuries, like the 30-year

Treasury bond shown above, was just as one would hope to see in a safe-haven asset during the lead-

up to the peak of a speculative bubble in risk assets: quiet and subdued. In early 2000, just when the

tech bubble was nearing its peak, long-term Treasury bonds were in an even better technical position,

with prices having sold off over the previous year and a half. For those looking for low-risk, safe-

Although long-term Treasury yields remain lower than when the

Fed began tightening, the peak in bond prices in 2016 suggests

bonds aren’t currently the place for cyclical speculation.

January 2018 Page 22 of 31

haven assets to seek shelter in to escape the inevitable fallout from the tech bubble and the housing

bubble, long-term Treasuries were not only attractive because of their yields (6% in 2000, and 5% in

2007), but they were in a state of benign neglect that carried with it the opportunity of a solid cyclical

trading opportunity.

Unfortunately, the same cannot be said today. Not only are yields extremely low, but the price action

between 2008 and 2016 carries with it a significant risk that prices for long-term Treasury notes and

bonds will fall instead of rise. The chart above of the 30-year Treasury bond price outlines the

approach to an ideal-looking speculative peak, with the initial breakdown from that speculative peak

in late 2016. Throughout 2017, the market consolidated after that breakdown, and here in early 2018

there is no indication that prices are gearing up for a cyclical bullish run. In fact, as 2017 came to an

end, it appeared long-term Treasury bond prices could be poised for another move lower.

When yields were in the 5%–6% range, and bond prices were poised to rise, the total return expected

from a cyclical investment in long-term Treasuries was significantly positive — which stood in stark

contrast to the negative outlooks for risk assets in 2000 and 2007. Yet the total return outlook today

is entirely different. With yields in the 2%–3% range, it only takes a slight decline in prices to bring

the total return below zero, which would turn this traditional, cyclical safe-haven into another source

of loss when it would be least expected.

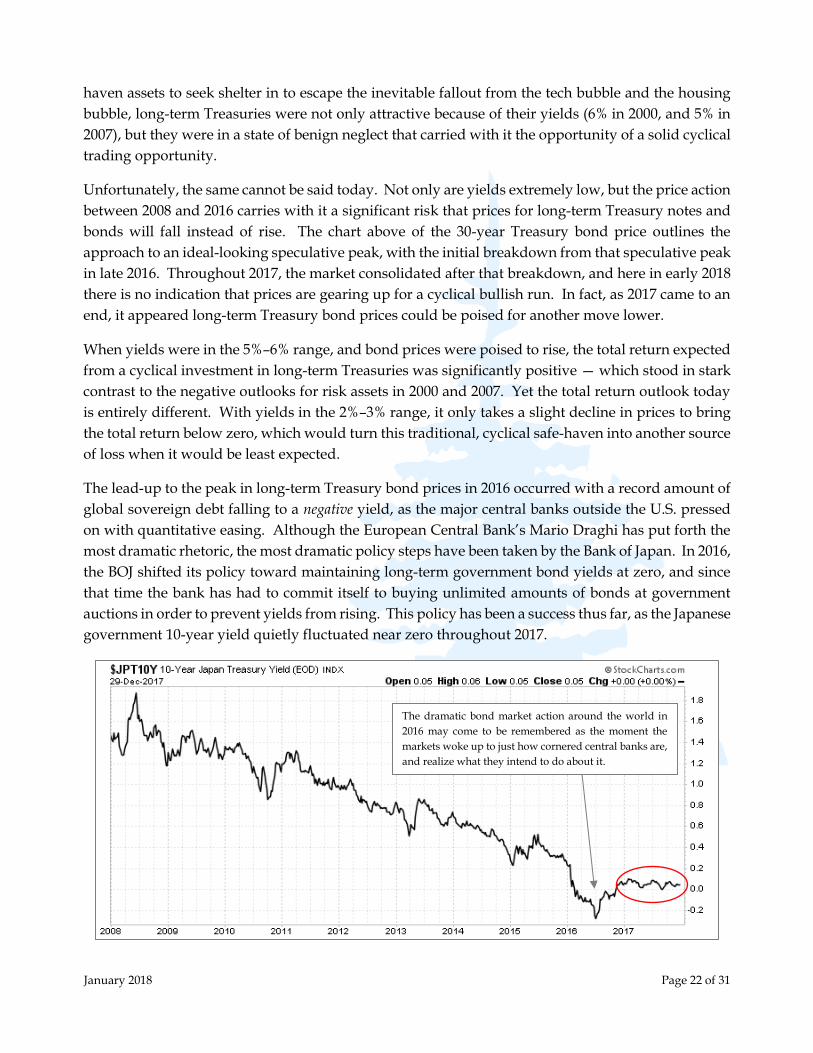

The lead-up to the peak in long-term Treasury bond prices in 2016 occurred with a record amount of

global sovereign debt falling to a negative yield, as the major central banks outside the U.S. pressed

on with quantitative easing. Although the European Central Bank’s Mario Draghi has put forth the

most dramatic rhetoric, the most dramatic policy steps have been taken by the Bank of Japan. In 2016,

the BOJ shifted its policy toward maintaining long-term government bond yields at zero, and since

that time the bank has had to commit itself to buying unlimited amounts of bonds at government

auctions in order to prevent yields from rising. This policy has been a success thus far, as the Japanese

government 10-year yield quietly fluctuated near zero throughout 2017.

The dramatic bond market action around the world in

2016 may come to be remembered as the moment the

markets woke up to just how cornered central banks are,

and realize what they intend to do about it.

January 2018 Page 23 of 31

While the Bank of Japan is now controlling the entire yield curve for Japanese government bonds, the

Fed has never intervened in the bond market with enough buying power to control the entire

Treasury yield curve, and it is now actively selling U.S. Treasury securities. This leaves Treasury

yields at the long end entirely in the hands of investors, and, in our opinion, there is no telling how

investors will react during the next downturn in risk assets. They may flood into the Treasury market

in the search for a safe-haven, as they have consistently done since the 1980s, but there are also

reasons to suspect long-term Treasury notes and bonds may eventually lose some of their safe-haven

luster (if they haven’t already). With the U.S. federal debt now above $20 trillion, and that debt

increasing by $671 billion in the past year (Q3 2016 to Q3 2017), we wonder whether investors will

seek out Treasury notes and bonds with the same enthusiasm when the deficit climbs even further

— perhaps over $1 trillion — during the next economic downturn.

It’s important to remember that the only reason for the extraordinary calm in the financial markets

over the past four years is the extraordinary policies of the largest central banks. If the Bank of Japan

were not offering to buy every single government bond issued at auction by the Japanese

government, and doing so at near zero percent interest rates, it’s possible global financial markets

would already be dealing with another debt or currency crisis emanating from Japan. And if the

European Central Bank (ECB) had not initiated its own quantitative easing program and doubled its

balance sheet between 2014 and 2017, it’s difficult to believe the Fed could have ended its own balance

sheet expansion in 2014 without more serious market repercussions.

As it stands, the global financial markets have been bombarded by continuous waves of new central

bank money since 2008, and the only difference over time has been the direction those waves have

been coming from. At times it has been the Fed which has expanded its balance sheet the most, and

at other times it has been the ECB and/or the BOJ. As was just mentioned above, since 2014 the Fed

has been holding its balance sheet relatively steady while the ECB has vastly expanded its balance

sheet, and this divergence of monetary policy was the primary reason for the dollar’s rise against the

euro and other major currencies — a trend which came to an end in 2017.

In 2017, the Dollar Index ended its 5-year bullish trend. This significantly

increases the relative attractiveness of global equity markets versus overvalued

U.S. markets, and has major implications for commodities and precious metals.

January 2018 Page 24 of 31

The end of the dollar’s bullish trend in 2017 has major implications going forward, not just for

currencies, but for stocks and bonds in the U.S. and around the world. The dollar has seen major

peaks and troughs at every major peak and trough of relative performance between U.S. and global

equity markets going back to at least the 1960s. Most recently, when the Dollar Index reached a low

in 2008, it ushered in a decade of outperformance of the S&P 500 versus global equity markets. Before

that, the peak of the Dollar Index in 2000 coincided with the peak of the tech bubble, which was

followed by seven years of global equity market outperformance versus the U.S. between 2001 and

2008.

The breakdown of the Dollar Index over the past year comes at another moment of extreme

overvaluation of U.S. markets and relative undervaluation of equity markets outside the U.S., and

the signal it sends to investors is quite clear: the decade-long period of outperformance for U.S.

financial markets is likely at an end. While it appears today that investors’ appetite for U.S. stocks

knows no limits, it is also clear from the dollar’s breakdown that money has already begun moving

out of the U.S. in search of relative value.

While equity markets outside the U.S. do indeed represent a far better value than those in the U.S., it

is also true that the effects of the end of the asset bubble in the U.S. will almost certainly reverberate

around the globe. This leaves emerging markets and other global equity markets in an attractive

relative position, but one which will most likely be made more attractive during the next global bear

market.

Few markets and asset classes benefit immediately following the peak of a large bubble — most, even

those poised to outperform over the long run, suffer during the bursting of a bubble. This will

probably prove to be the case with more reasonable valued global equity markets. Yet there are a

few exceptions, and gold is one of them. Immediately following the end of the tech bubble, gold

began a bull market that lasted a decade. It was safe to be fully invested in gold during the market’s

. . . equity markets outside the U.S. have fallen by

half relative to the S&P 500 over the past decade.

After rising 68% versus the S&P 500

between 2001 and 2008 . . .

January 2018 Page 25 of 31

last gasps in 1999 and 2000, and at no point in the years that followed did gold revisit its lows — and

we doubt those prices will ever be seen again.

The end of the bubble we are living through today will likely be a similar watershed moment for

gold, and it is possible the low at $1045, recorded in late 2015, will be another price that gold pivots

from, and never visits again. Precious metals bull markets have always begun when equity markets

are overvalued, and they have only ended when equity markets are undervalued. Although gold’s

price has risen modestly over the past two years, this rise likely represents only the very earliest

stages of another bull market; perhaps like the first two outs in the top of the 1st inning of a baseball

game. The other 8 1/3 innings lie ahead.

To summarize our market outlook:

The U.S. stock market is in a massive bubble, which, based on sentiment and valuations, could

come to an end at any time. Valuations strongly suggest the peak of this bubble will be a real,

inflation-adjusted high-water mark that lasts for 15–25 years. In the decade after the peak, a

portfolio of large-cap stocks will likely lose real value at an average rate of 3%–4% per year, with a

maximum loss of 50%–67% at cyclical lows.

The U.S. dollar is likely in the early stages of a new downtrend, and this will have profound effects

on the performance of many markets and sectors. It is a sign money has already begun moving out

of overvalued U.S. financial assets into better values abroad. The bearish trend in the dollar will

likely continue until U.S. financial assets represent a relative value versus global markets.

The outperformance of U.S. equities versus global equities over the past decade will likely come to

an end with the end of the bubble in the U.S. market, after which global equity markets will

During the decade following the tech bubble,

gold rose 560% from its lows. The decade

following the end of the QE/TINA bubble

will likely see another gold bull market.

January 2018 Page 26 of 31

outperform for an extended period of time. Equity market valuations outside the U.S. are relatively

benign, consistent with these markets being near the beginning of a new phase of outperformance.

Although equity markets outside the U.S. represent relative value, and are likely in an attractive

cyclical position with positive prospective returns for dollar-based investors, the end of the U.S.

equity market bubble will likely be a global event, which will drag down equity prices inside and

outside the U.S. More attractive buying opportunities for these markets lie ahead.

The Fed continued to increase short-term interest rates in 2017, and expectations are that there will

be additional increases in 2018. However, long-term Treasury rates remain low, indicating the

market expects the Fed’s campaign to tighten monetary policy ahead of the next economic

downturn will eventually be completely unwound.

Although long-term Treasury rates remain low, the peak in long-term Treasury bond prices in 2016

suggests prices could stagnate or decline in the years ahead. With rates on long-term Treasury

notes and bonds between 2% and 3%, the likelihood of even a modest price decline takes the

expected total return below zero for investors. This means long-term Treasuries may not provide

the safe-haven returns investors have become accustomed to.

Credit spreads beyond Treasuries have been the lowest on record in recent years, and it is possible

that the bust of the stock market bubble will be fueled, in part, by the rapid rise of corporate

indebtedness during this cycle; corporate debt now equals 31% of U.S. GDP, a record high. The

end of the current asset bubble will likely have a negative impact on corporate bonds and municipal

bonds (especially bonds from municipalities with high pension liabilities).

Commodities and other real assets are trading near their lowest inflation-adjusted prices in a

decade. Commodities will eventually benefit from the dollar’s trend change and the ongoing

monetary response to deleveraging, but the end of the current asset bubble will likely have a

negative impact on prices — though this negative impact will likely generate long-term buying

opportunities.

Gold and other precious metals are likely in the early stages of a new bull market, and market

conditions turned more supportive in 2017: the dollar no longer represents a headwind, and the

post-equity-bubble market environment will likely provide a strong tailwind for gold in the decade

following its peak.

Cash has been second only to gold in terms of its unpopularity over the past few years. Numerous

surveys show cash levels in professionally managed funds and retail brokerage accounts hit record

lows in 2017. Yet no other asset class will benefit more directly from the end of the U.S. asset bubble

than cash.

January 2018 Page 27 of 31

The Path Down from a Bubble Is Never a Smooth One, But There Is a Way Forward

Remember that history always repeats itself. Every great bubble in history has broken. There are no exceptions.

- Jeremy Grantham

One of the defining features of speculating on a bubble is that the mentality required to take

advantage of it — ignoring valuations, ignoring technical warnings, and a firm belief that this time is

different — is the very mentality that leads one to eventually give it all back in the bust. This has

happened so often throughout history that it’s amazing we are writing these words again today, but

it’s clear now that investors will have to learn the same lessons yet again.

In a recent commentary, Jeremy Grantham mentioned that one reason professional, institutional

investors were unable to avoid investing in a bubble is because most institutional clients limited

managers to a 2-year window of underperformance. In other words, if a manager failed to keep pace

with market indexes for more than two years, investment committees would vote to move on, and

the they would lose most of their institutional clients. So, if the market were to remain overvalued

for more than two years, and keep gaining during that time, most professional investment managers

would simply have “no choice” but to jump in with both feet, if they wanted to remain in business.

While we certainly understand those pressures, we feel there is a more honest way of staying in

business: instead of throwing caution to the wind and gambling by the rules which will work only

2% of the time, remain invested by the rules which will work 98% of the time — and prepare for the

inevitable fallout when markets become completely disconnected from value, as they are today.

January 2018 Page 28 of 31

The path down from a bubble is never a smooth one, but there is a way forward, and we remain

invested in ways we think will do well through the long, turbulent period that will inevitably follow

the current bubble. This bubble may last another few months, or possibly another year or two, but

the post-bubble environment that follows will likely last for a generation. By our way of thinking, at

this time there is no other prudent course, based on investment merit alone, but to invest in ways that

will generate positive returns during the upcoming 15–25-year post-bubble market environment.

The blow-off we are currently witnessing in the stock market has increased the likelihood that we’ll

see a crash immediately following the peak, to be then followed by a severe cyclical bear market with

a peak-to-trough loss of between 50% and 67% for the broader market. It doesn’t have to end in such

a violent way, but once we see such a euphoric, parabolic rise in prices, as we have over the past year,

the odds of such an end become higher than a more benign market deflation (as happened in the

years after the peak in 1966). Both the bear markets following the peaks in 2000 and 1929 saw some

areas lose more 80% of their value, and as it stands at the beginning of 2018, such an extreme reaction

following the peak of this bubble can’t be ruled out; after all, those are the only comparisons we have

to today’s high valuations.

However this bubble finally comes to an end, our expected long-term returns for major asset classes

over the next decade are outlined below. Based on the valuations and the market conditions we

observe at the beginning of 2018, we estimate the central-expected real return of U.S. large cap stocks

is near negative 4% annualized over the next decade. This negative return may not sound so harsh,

but in fact it is 10% below the long-term average real return, and it is one of only three times in history

similar valuation estimates would project a negative long-term real return.

January 2018 Page 29 of 31

There are few conventional areas in the financial markets which offer the prospect of positive real

returns from where we are today, being, as we are, on the precipice of a long-term bear market.

However, we do feel there is a clear way forward, and the allocations in your account(s) with us

largely reflect the prospective returns outlined in the chart above.

Gold is necessarily a big part of that way forward simply because no other asset has consistently

gained in value during a long-term bear market in stocks and other risk assets. In addition, as we

highlighted earlier, since the 2008 gold has decoupled from other commodities, which shows it has

begun to trade more on its value as sound, risk-free money since the onset of deleveraging. This role

of sound money will likely continue to strengthen in the years ahead, as the final stages of the 20th

Century Price Revolution — deleveraging and monetization — continue to unfold.

Yet if we restrict our view to within the 20th Century Price Revolution, gold gained in value during

the deleveraging of the Great Depression, and if we look at gold’s return just since it began trading

freely in the 1970s, we find that it has gained during every decade-long period when the 10-year P/E

of the S&P 500 has fallen. These gains range from an annualized return of 1% to an annualized return

of 34%, with a median near 15%. And during periods in which the S&P 500’s valuation fell

dramatically over a decade, i.e. more than 30%, which is what happens during a long-term bear

market in stocks, gold had a minimum annualized return of 11.5%.

Although there are many aspects of today’s market which are historically unique, we think 15%

represents a central-expected return for gold in the decade after the current bubble comes to an end,

and this return stands in stark contrast to the negative prospective return of the S&P 500.

A 50% fall in the valuation of the S&P 500 over a decade

has been associated with a 15% or higher annualized

return in gold. In addition, gold has never lost value

when the S&P 500’s valuation has fallen (green box).

January 2018 Page 30 of 31

Equity markets outside the U.S. represent a much more fertile ground for the search for positive

prospective returns, and many of those markets will likely deliver a small positive return from

today’s prices and valuations over the next decade. We remain invested in one of those markets,

Japan, and our outlook for Japanese stocks, hedged of any exposure to the Yen, remains positive in

the long-term. However, there is a high probability that markets outside the U.S. will suffer from the

fallout of today’s bubble in U.S. markets – just as they have during the last two cyclical bear markets.

As a result, the only major asset class we think is poised to deliver both short- and long-term gains is

precious metals, which is why we are invested in precious-metals-related positions in all our

portfolios. However, during the next global market downturn, our equity investing activities will

likely focus heavily on markets outside the U.S. – as we appear to be on the cusp of another extended

period of global equity market outperformance, and U.S. dollar weakness.

We have made many mistakes over the past few years, and while we will undoubtedly make more

mistakes in the future, it’s important to emphasize that most of our mistakes over the past few years

were largely tied to the rarity of the market action. The odds of the market’s valuation soaring 50%

from an already over-valued level three years ago was probably on the order of 1 in 50. Yet that event

rare happened, and many positions that lose directly during a bubble — such as hedges and short

positions — turned from reasonable allocations in an over-valued market, into mistakes. In addition,

assets like gold, which have a negative long-term correlation to stocks when they enter a bubble,

suffer greatly as well. Although we eventually bought back many of the positions we had sold and

lightened up on in 2011 and 2012 at much lower prices during the low prices in 2013-2015, the declines

in precious-metals positions during those years have weighed on our long-term returns.

After going through the South Sea bubble and bust, Isaac Newton said that “he could predict the

motions of the heavenly bodies, but not the madness of people.” Today, after seeing many examples

of bubbles and busts throughout history, we know that markets can continue on a trend for longer

than anyone thinks possible, but it is also true that valuations always eventually revert back from

extremes to more reasonable, middle-of-the-road levels (or lower). Thus, although there is no hope

in predicting just how far today’s madness will carry valuations, we do know that positions which

look like a mistake at a market extreme can quickly turn into the timeliest allocation tomorrow. As

much as any long positions were mistakes leading up to March 9, 2009, the day the market bottomed

during the financial crisis, they represented tremendous potential from their beaten down prices –

and they began realizing that potential the day after the market bottomed. It takes vision and